Embed Size (px)

Citation preview

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 1/ / / // / / / / / / / / / / / / / / / / / / / / / / / / / / /

CLEAN ENERGY

INVESTMENT

OUTLOOKISRAEL ENERGY AND BUSINESS CONFERENCE

28 NOVEMBER 2011

ETHAN ZINDLER

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 2/ / / /

COPYRIGHT AND DISCLAIMER

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be

photocopied, reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any

way without prior consent of Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected public sources we believe are

reasonable. We do not guarantee its accuracy or completeness and nothing in this document shall be

construed to be a representation of such a guarantee. Any opinions expressed reflect the current judgment of

the author of the relevant article or features, and does not necessarily reflect the opinion of Bloomberg New

Energy Finance. The opinions presented are subject to change without notice. Bloomberg New Energy

Finance accepts no responsibility for any liability arising from use of this document or its contents. Bloomberg

New Energy Finance does not consider itself to undertake Regulated Activities as defined in Section 22 of the

Financial Services and Markets Act 2000 and is not registered with the Financial Services Authority of the UK.

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 3/ / / /

ABOUT BLOOMBERG NEW ENERGY FINANCE

San FranciscoNew York

Washington DC

Sao Paulo

Cape TownSydney

Hong KongNew Dehli

London

BeijingTokyo

200 staff in 13 offices worldwide

Objective: serve clients with the best intelligence on finance, technology and policy developments

in clean energy, energy efficiency and carbon markets

Zurich

Singapore

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 4/ / / /

$52bn

$76bn

$113bn

$151bn

$180bn $186bn

$243bn

48%

48%

34%

19%

4%

30%

2004 2005 2006 2007 2008 2009 2010

GLOBAL TOTAL NEW INVESTMENT IN CLEAN ENERGY

2004–10 ($BN)

Source: Bloomberg New Energy Finance

Note: Includes corporate and government R&D, and small distributed capacity. Adjusted for re-

invested equity. Does not include proceeds from acquisition transactions

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 5/ / / /

Source: Bloomberg New Energy Finance

DRIVERS OF INVESTMENT GROWTH, 2009–10 ($BN)

CHINAEUROPEAN

ROOFTOP SOLAR

39.2

51.1

2009 2010

21.0

46.2

2009 2010

+120%

+30%

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 6/ / / /

0.0

0%

20.3

10%

74.5

38% 68

35%

21.4

11%

9.7

5%

2008 2009 2010 2011e 2012e 2013e

GLOBAL CLEAN ENERGY STIMULUS SPENDING BY YEAR,

2011–13 ($BN)

Source: Bloomberg New Energy FinanceNote: 2011–13 according to Bloomberg New Energy Finance expectations

Spent = $94.8bn, 49% Unspent = $99.1bn, 51%

Global total = $193.9bn

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 7/ / / /

INVESTMENT IN RENEWABLE ENERGY VS.

CONVENTIONAL CAPACITY, 2004-2010 ($BN)

Source: Bloomberg New Energy Finance; EIA, IEA

Note: Fossil Fuel investment is calculated from EIA & IEA data. Clean energy

investment includes asset finance and small scale projects, but excludes large hydro.

15

31

55

80 82

6770

4

12

21

32

5155

72

2004 2005 2006 2007 2008 2009 2010

Developed Developing

3

1510 4

14 46 2

101

18 162

61 223

VC CorpRD&D

Totalinvestment

SDC*Assetfinance

GovR&D

Publicmarkets

new equity

M&A/B-O etc.

Total transactions

Re-invested

Totalcompany

investment

PE

Technology development

Equipment manufacturing/scale-up

Projects

Asset and company mergers, acquisitions, ref inancing, buy-outs etc.

Global Trends

in Sustainable Energy

Investment

2010

Global Trends

in Renewable Energy

Investment

2011

Fossil fuel

Renewable energy

0

50

100

150

200

250

2004 2005 2006 2007 2008 2009 2010

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 8/ / / /

FINANCIAL NEW INVESTMENT IN RENEWABLE ENERGY BY

REGION, 2004-2010 ($BN)

Source: Bloomberg New Energy Finance; UNEP

Note: New investment volume adjusts for re-invested equity. Total values include

estimates for undisclosed deals. This comparison does not include small-scale

projects.

0.3 0.1 1.5 1.5 2.4 2.45.0

2004 2005 2006 2007 2008 2009 2010

Middle East & Africa

0.52.8 4.7

7.7

15.7

9.413.1

2004 2005 2006 2007 2008 2009 2010

South America

5.611.0

18.3

26.2

34.4

45.7

59.3

2004 2005 2006 2007 2008 2009 2010

Asia & Oceania3.8

10.3

24.629.4

32.3

19.7

30.1

2004 2005 2006 2007 2008 2009 2010

North America

9.0

18.4

27.3

46.6 47.6 45.0

35.2

2004 2005 2006 2007 2008 2009 2010

Europe

3

1510 4

14 46 2

101

18 162

61 223

VC CorpRD&D

Totalinvestment

SDC*Assetfinance

GovR&D

Publicmarkets

new equity

M&A/B-O etc.

Total transactions

Re-invested

Totalcompany

investment

PE

Technology development

Equipment manufacturing/scale-up

Projects

Asset and company mergers, acquisitions, ref inancing, buy-outs etc.

Global Trends

in Sustainable Energy

Investment

2010

Global Trends

in Renewable Energy

Investment

2011

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 9/ / / /

LEVELISED COST OF ENERGY Q3 2011 ($/MWH)

Source: Bloomberg New Energy Finance

Carbon forecasts from the BNEF European Carbon Model with a 2020 horizon $74/tCO2. Coal and nat gas prices

from the US Department of Energy EIA Annual Energy Outlook 2011. % change represents change in mid from

Q2 2011.

0 50 100 150 200 250 300 350 400 450 500

Natural Gas CCGT

Landfill Gas

Coal Fired

Wind - Onshore

Municipal Solid Waste

Geothermal - Flash Plant

Biomass - Incineration

Biomass - Anaerobic Digestion

PV - c-Si Tracking

Biomass - Gasification

Geothermal - Binary Plant

PV - Thin Film

STEG - Tower & Heliostat w/storage

PV - c-Si

STEG - LFR

STEG - Tower & Heliostat

Wind - Offshore

STEG - Parabolic Trough + Storage

STEG - Parabolic Trough

Marine - Wave

Marine - Tidal

LCOE BNEF 2011 EU-ETS EUA Forecast Q3 2011 Central Scenario Q2 2011 Central Scenario

+5%

+1%

+5%

+1%

-2%

+1%

-1%

+6%

+1%

-4%

-2%

-3%

-9%

+6%

+1%

-9%

-1%

-1%

-3%

799 +23%

740 +8%

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 10/ / / /

SPOT PRICES OF SOLAR-GRADE SILICON, YEAR 2000 –

NOVEMBER 2011 ($/KG)

Source: Various, Bloomberg New Energy Finance Solar

Spot Survey

Note: Annual data 2000-2007 from various industry sources. Data November 2007 – May

2009 based on a 3-point moving average of actual spot deals. Consistent monthly data

collection using the Spot Survey began in May 2009.

0

50

100

150

200

250

300

350

400

450

500

20

00

20

02

20

04

20

06

De

c 0

7

Fe

b 0

8

Ap

r 0

8

Ju

n 0

8

Au

g 0

8

Oct 0

8

De

c 0

8

Fe

b 0

9

Ap

r 0

9

Ju

n 0

9

Au

g 0

9

Oct 0

9

De

c 0

9

Fe

b 1

0

Ap

r 1

0

Ju

n 1

0

Au

g 1

0

Oct 1

0

De

c 1

0

Fe

b 1

1

Ap

r 11

Ju

n 1

1

Au

g 1

1

Oct 1

0

Spot survey results 3-point moving average Annual analyst estimates

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 11/ / / /

PRICE FOR IMMEDIATE DELIVERY OF C-SI MODULES,

NOVEMBER 2010 – 14 NOVEMBER 2011 ($/W)

Source: Bloomberg New Energy Finance

Module Spot Index

Note: From 11 July 2011 the Index is conducted on a weekly basis and the dates in chart represent first

day of the week over which the price has been averaged . ie: 8 August represents quote for period of data

collection in the week 8-14 August. Prior to the weekly updates, the Index collected price of c-Si modules

without differentiating between mono and multi crystalline silicon technology.

0.0

0.5

1.0

1.5

2.0

2.5

No

v

De

c

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

04

Ju

l

11

Ju

l

18

Ju

l

25

Ju

l

01

Au

g

08

Au

g

15

Au

g

22

Au

g

29

Au

g

05

Se

p

12

Se

p

19

Se

p

26

Se

p

03

Oct

10

Oct

17

Oct

24

Oct

31

Oct

07

No

v

14

No

v

2010 2011

Multicrystalline silicon module (c-Si) Monocrystalline silicon module (c-Si)

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 12/ / / /

CHINESE MULTICRYSTALLINE SILICON MODULE PRICE

BUILD-UP, NOVEMBER 2011 ($/W)

Source: Bloomberg New Energy Finance Solar Spot Survey

Assumes 6.0g of silicon per watt of wafer. ‘Processing cost per W’ based on SEC

filings of quoted companies, publically available reports, various discussions and

analyst estimates. SG&A represents sales, general, administration and R&D

0.1

0

0.17

0.18

0.25

0.01

0.01

0.05

0.09

0.03

0.06

0.04

0.01

0.03

0.08

$29.5/kg

$1.25/piece

$0.53/W

$0.97/W

Polysilicon

Ingot & Wafer

Cell

Module

Processing cost per W SG&A per W

Depreciation per W Best-in-class margin per W

SSSS

-0.10

Spot price

-0.05

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 13/ / / /

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

800 1,000 1,200 1,400 1,600

kWh/kW/year

2015

LCOE

Average residential power price

Japan

Spain

Germany

Denmark

France

Greece

Netherlands PortugalUKSlovakia

South KoreaUS

excl. CA

China

South Africa

10GW

50GW

Residential

power market

Hawaii

Italy

Turkey

$/kWh

RESIDENTIAL PV PRICE PARITY

Source: Bloomberg New Energy Finance

Note: LCOE based on 6% weighted average cost of capital, 0.7%/year module degradation, 1%

capex as O&M annually. CA is California.

2010

LCOE

Average residential power price

More sun

CACA

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 14/ / / /

SUPPLY AND DEMAND OF PV MODULES, 2007-2013 (GW)

Source: Bloomberg New Energy Finance

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 2013

Supply - base scenario Supply - high scenario

Demand - conservative Demand - optimistic

Historical Future

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 15/ / / /

UTILITY-SCALE PV SYSTEM PRICE FORECAST, 2010-2020

(2010 $/W)

Source: Bloomberg New Energy Finance

1.72

1.35

1.060.95 0.90

0.810.73 0.66 0.59 0.53 0.48

0.30

0.30

0.270.24 0.22

0.210.19

0.17 0.16 0.15 0.14

0.50

0.50

0.470.45

0.440.42

0.400.39

0.370.36

0.34

0.41

0.41

0.390.37

0.360.34

0.330.32

0.310.29

0.28

0.18

0.18

0.170.17

0.160.16

0.150.15

0.150.14

0.14

$3.12/W

$2.74/W

$2.36/W$2.19/W

$2.08/W$2.00/W

$1.81/W$1.68/W

$1.57/W$1.47/W

$1.38/W

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Module Inverter Balance of plant Engineering, procurement & construction Other

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 16/ / / /

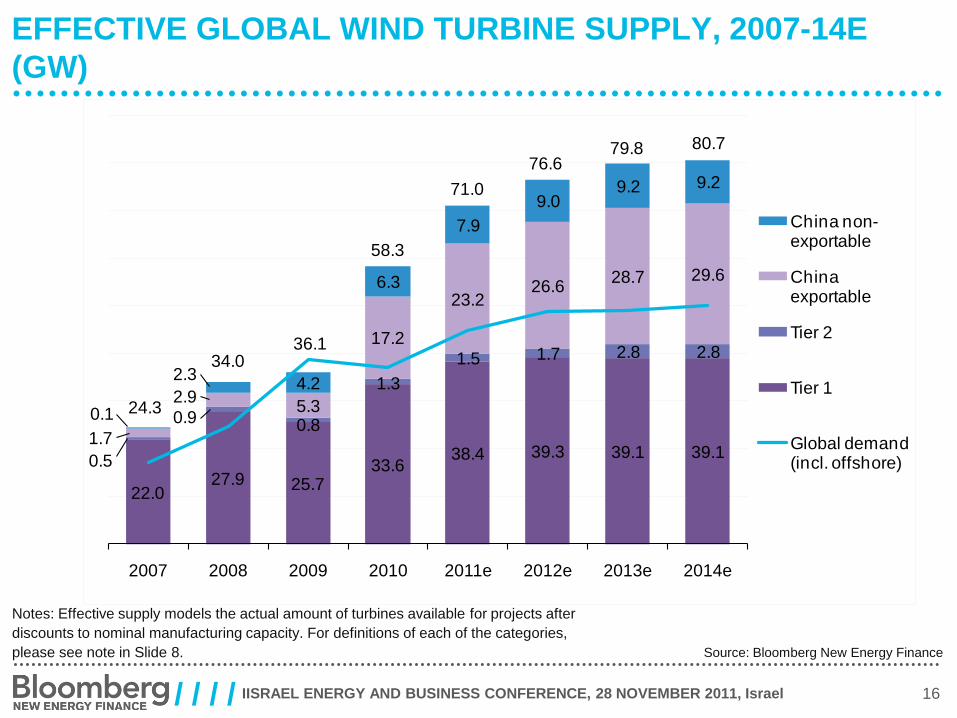

EFFECTIVE GLOBAL WIND TURBINE SUPPLY, 2007-14E

(GW)

Source: Bloomberg New Energy Finance

Notes: Effective supply models the actual amount of turbines available for projects after

discounts to nominal manufacturing capacity. For definitions of each of the categories,

please see note in Slide 8.

22.027.9 25.7

33.638.4 39.3 39.1 39.1

0.5

0.9 0.8

1.3

1.5 1.7 2.8 2.8

1.7

2.95.3

17.2

23.226.6

28.7 29.6

0.1

2.34.2

6.3

7.9

9.09.2 9.2

2007 2008 2009 2010 2011e 2012e 2013e 2014e

China non-exportable

China exportable

Tier 2

Tier 1

Global demand (incl. offshore)

71.0

76.679.8 80.7

58.3

36.134.0

24.3

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 17/ / / /

AVERAGE LCOE OF ONSHORE WIND, 1984-2011 EUR/MWH

Source: Bloomberg New Energy Finance, ExTool

Note: Learning curve (purple) is least square regression: R2=0.88 and 14% learning rate.

CAPEX, OPEX and capacity factor evolution is included in this LCOE analysis; financing

assumptions kept constant.

14%

Global

Denmark and

Germany

1984 1990 2000 2004 201110

50

100

500

1000

100 1,000 10,000 100,000 1,000,000

MW

IISRAEL ENERGY AND BUSINESS CONFERENCE, 28 NOVEMBER 2011, Israel 18/ / / /

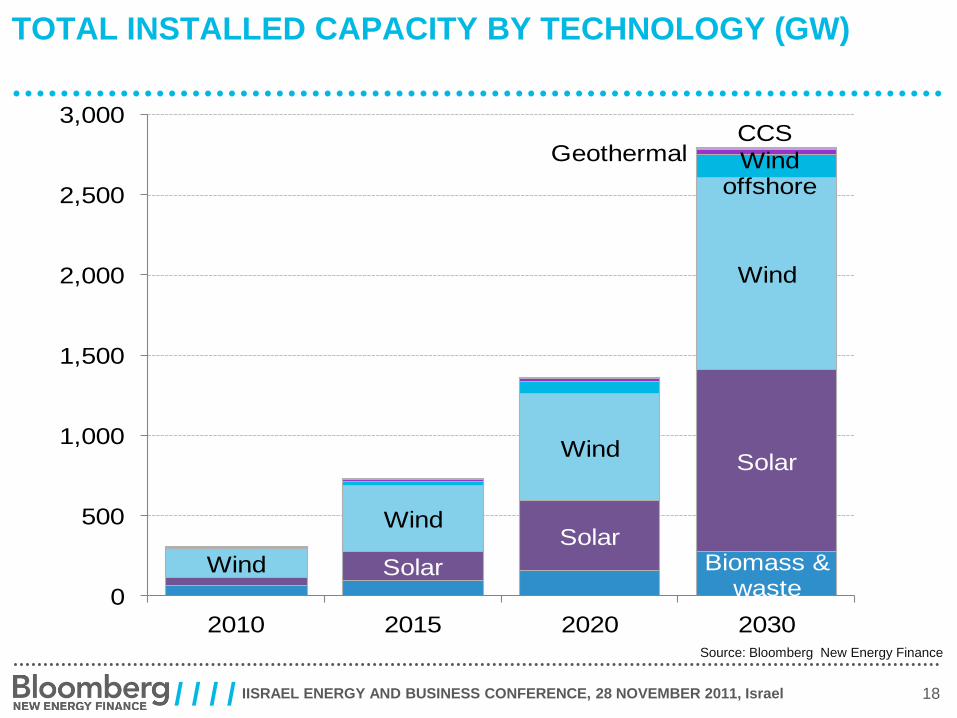

TOTAL INSTALLED CAPACITY BY TECHNOLOGY (GW)

Source: Bloomberg New Energy Finance

Biomass & waste

Solar

Solar

Solar

Wind

Wind

Wind

Wind

Wind offshore

GeothermalCCS

0

500

1,000

1,500

2,000

2,500

3,000

2010 2015 2020 2030

/ / / / / / / / / / / / / / / / / / / / / / / / / / / /

Subscription-based news, data

and analysis to support your

decisions in clean energy, power

and water and the carbon markets

MARKETS Renewable Energy

Carbon Markets

Energy Smart Technologies

Renewable Energy Certificates

Carbon Capture & Storage

Power

Water

Nuclear

SERVICESInsight: research, analysis & forecasting

Industry Intelligence: data & analytics

News & Briefing: daily, weekly & monthly

Applied Research: custom research & data mining

Knowledge Services: Summit, Leadership Forums, Executive Briefings &

workshops

THANK YOU

ETHAN ZINDLER, [email protected]

TWITTER: ETHANALL

![Accelerating Clean Innovation · 2018. 5. 22. · • Global clean tech market share = 1.4%, down 12% since 2008 [Analytica] • Canada’s performance and outlook improving – Moved](https://img.pdfslide.net/doc/110x75/5fc04014955a1216686d8b29/accelerating-clean-innovation-2018-5-22-a-global-clean-tech-market-share.jpg)