Embed Size (px)

Citation preview

Clearinghouse-FiveDeterminants of voluntary clearing in European derivatives markets

Pawe l FiedorCentral Bank of Ireland

15th May 2018

Motivation Summary statistics Research Question Dataset Results Conclusions Background

MotivationWhy do I look at derivatives and clearing?

Fiedor CBI 1 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

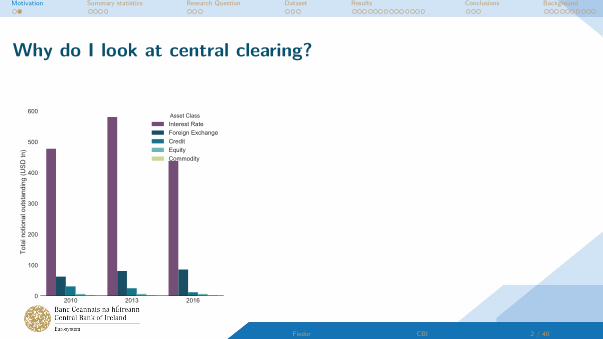

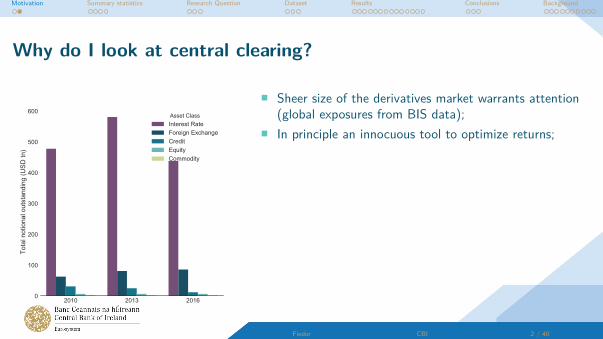

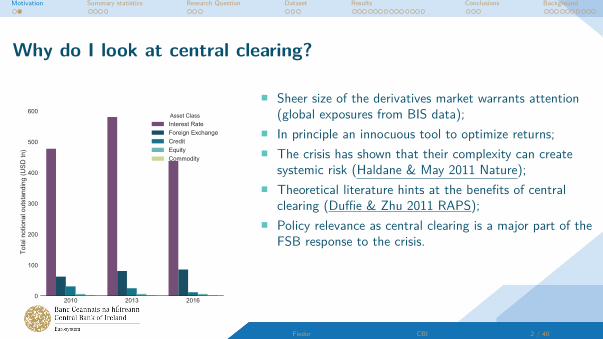

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;� The crisis has shown that their complexity can create

systemic risk (Haldane & May 2011 Nature);� Theoretical literature hints at the benefits of central

clearing (Duffie & Zhu 2011 RAPS);� Policy relevance as central clearing is a major part of the

FSB response to the crisis.

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;� The crisis has shown that their complexity can create

systemic risk (Haldane & May 2011 Nature);� Theoretical literature hints at the benefits of central

clearing (Duffie & Zhu 2011 RAPS);� Policy relevance as central clearing is a major part of the

FSB response to the crisis.

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;

� The crisis has shown that their complexity can createsystemic risk (Haldane & May 2011 Nature);

� Theoretical literature hints at the benefits of centralclearing (Duffie & Zhu 2011 RAPS);

� Policy relevance as central clearing is a major part of theFSB response to the crisis.

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;� The crisis has shown that their complexity can create

systemic risk (Haldane & May 2011 Nature);

� Theoretical literature hints at the benefits of centralclearing (Duffie & Zhu 2011 RAPS);

� Policy relevance as central clearing is a major part of theFSB response to the crisis.

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;� The crisis has shown that their complexity can create

systemic risk (Haldane & May 2011 Nature);� Theoretical literature hints at the benefits of central

clearing (Duffie & Zhu 2011 RAPS);

� Policy relevance as central clearing is a major part of theFSB response to the crisis.

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;� The crisis has shown that their complexity can create

systemic risk (Haldane & May 2011 Nature);� Theoretical literature hints at the benefits of central

clearing (Duffie & Zhu 2011 RAPS);� Policy relevance as central clearing is a major part of the

FSB response to the crisis.

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Why do I look at central clearing?

2010 2013 20160

100

200

300

400

500

600

Tota

l not

iona

l out

stan

ding

(USD

tn)

Asset ClassInterest RateForeign ExchangeCreditEquityCommodity

� Sheer size of the derivatives market warrants attention(global exposures from BIS data);

� In principle an innocuous tool to optimize returns;� The crisis has shown that their complexity can create

systemic risk (Haldane & May 2011 Nature);� Theoretical literature hints at the benefits of central

clearing (Duffie & Zhu 2011 RAPS);� Policy relevance as central clearing is a major part of the

FSB response to the crisis.

”In my view, derivatives are financial weapons ofmass destruction.” Warren Buffet, 2002

Fiedor CBI 2 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Central clearing in the European UnionSummary statistics

Fiedor CBI 3 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

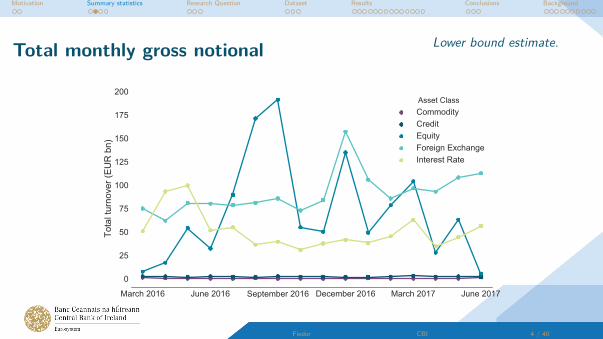

Total monthly gross notional

March 2016 June 2016 September 2016 December 2016 March 2017 June 2017

0

25

50

75

100

125

150

175

200

Tota

l tur

nove

r (EU

R b

n)Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 4 / 40

Lower bound estimate.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Total monthly gross notional

March 2016 June 2016 September 2016 December 2016 March 2017 June 2017

0.5

1.0

1.5

2.0

2.5

3.0To

tal t

urno

ver (

EUR

bn)

Asset ClassCommodityCredit

Fiedor CBI 5 / 40

Lower bound estimate.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

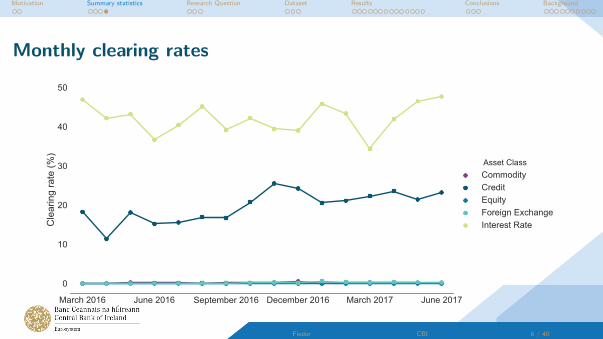

Monthly clearing rates

March 2016 June 2016 September 2016 December 2016 March 2017 June 2017

0

10

20

30

40

50

Cle

arin

g ra

te (%

)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 6 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Monthly clearing rates

March 2016 June 2016 September 2016 December 2016 March 2017 June 2017

0

10

20

30

40

50

Cle

arin

g ra

te (%

)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 6 / 40

Not all of those are clearedmandatorily!

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Research questionWhat are the determinants of voluntary clearing?

Fiedor CBI 7 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):

� H1: intragroup trades;� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,

Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):� H1: intragroup trades;

� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,

Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):� H1: intragroup trades;� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);

� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,

Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):� H1: intragroup trades;� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);

� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,

Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):� H1: intragroup trades;� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);

� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,

Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):� H1: intragroup trades;� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);

� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Hypotheses

I test various potential determinants (CCR + cost optimisation):� H1: intragroup trades;� H2: maturity (Helwege & Turner 1999 JF, Koeppl & Monet 2010 FRB, Biais et al. 2012 ECB);� H3: notional value (Duffie & Zhu 2011 RAPS, Hull 2012 JoD, Bellia et al. 2017 ESRB);� H4: non-EEA involvement (La Porta et al. 1997 JF, France & Kahn 2016 JFI);� H5: financial sophistication (Stephens & Thompson 2017 JFI, BIS 2014);� H6: effects of scale (Duffie & Zhu 2011 RAPS, Duffie et al. 2015 JFE,

Ghamani & Glasserman 2017 JFI).

Fiedor CBI 8 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WP

� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:

� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;

I H2: margins optimisation;I H3: counterparty risk.

� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;

I H3: counterparty risk.� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:

I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:I Large difference between clearing members and other entities;

I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;

I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Literature review

Bellia et al. 2017 ESRB WPStudy of Italian, German, and French sovereign CDS:� Hypotheses:

I H1: liquidity of contract and riskiness of reference entity;I H2: margins optimisation;I H3: counterparty risk.

� Results:I Large difference between clearing members and other entities;I Diverse factors play role in the three reference entities;I Net position towards a CCP and CCR matter.

Fiedor CBI 9 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

DatasetOverview and variables used

Fiedor CBI 10 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:

� reported to one Trade Repository;� not compressed;� not cancelled on the same day;� valid values in considered variables;� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;

� not compressed;� not cancelled on the same day;� valid values in considered variables;� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;� not compressed;

� not cancelled on the same day;� valid values in considered variables;� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;� not compressed;� not cancelled on the same day;

� valid values in considered variables;� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;� not compressed;� not cancelled on the same day;� valid values in considered variables;

� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;� not compressed;� not cancelled on the same day;� valid values in considered variables;� counterparty types found using Orbis;

� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;� not compressed;� not cancelled on the same day;� valid values in considered variables;� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Dataset

All new not obligatory cleared derivative contracts in the EUbetween March 2016 and June 2017:� reported to one Trade Repository;� not compressed;� not cancelled on the same day;� valid values in considered variables;� counterparty types found using Orbis;� currencies converted to EUR using ECB rates.

3terabytes

of raw data!

Fiedor CBI 11 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

� cleared. � intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:

� cleared.� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:

� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;

� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;

� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;

� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;

� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;

� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

Other independent variables:

� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

Other independent variables:� year of maturity;

� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

Other independent variables:� year of maturity;� notional in euros;

� previous months’ tradednotional;

� previous months’ clearednotional;

� previous months’ clearedratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

Other independent variables:� year of maturity;� notional in euros;� previous months’ traded

notional;

� previous months’ clearednotional;

� previous months’ clearedratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

Other independent variables:� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;

� previous months’ clearedratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Variables

Dependent variable:� cleared.

Binary independent variables:� intragroup;� clearing obligation;� non-EEA counterparty;� financial nature;� counterparty type;� trading capacity.

Other independent variables:� year of maturity;� notional in euros;� previous months’ traded

notional;� previous months’ cleared

notional;� previous months’ cleared

ratio.

Fiedor CBI 12 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

ResultsWhat are the determinants of voluntary clearing?

Fiedor CBI 13 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

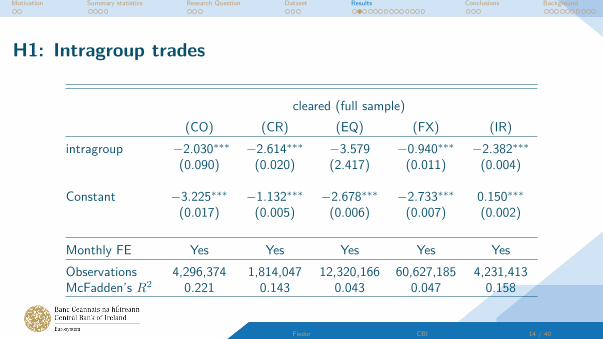

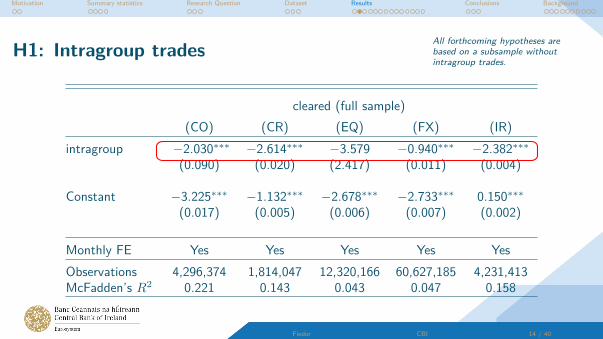

H1: Intragroup trades

cleared (full sample)(CO) (CR) (EQ) (FX) (IR)

intragroup −2.030∗∗∗ −2.614∗∗∗ −3.579 −0.940∗∗∗ −2.382∗∗∗(0.090) (0.020) (2.417) (0.011) (0.004)

Constant −3.225∗∗∗ −1.132∗∗∗ −2.678∗∗∗ −2.733∗∗∗ 0.150∗∗∗(0.017) (0.005) (0.006) (0.007) (0.002)

Monthly FE Yes Yes Yes Yes YesObservations 4,296,374 1,814,047 12,320,166 60,627,185 4,231,413McFadden’s R2 0.221 0.143 0.043 0.047 0.158

Fiedor CBI 14 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H1: Intragroup trades

cleared (full sample)(CO) (CR) (EQ) (FX) (IR)

intragroup −2.030∗∗∗ −2.614∗∗∗ −3.579 −0.940∗∗∗ −2.382∗∗∗(0.090) (0.020) (2.417) (0.011) (0.004)

Constant −3.225∗∗∗ −1.132∗∗∗ −2.678∗∗∗ −2.733∗∗∗ 0.150∗∗∗(0.017) (0.005) (0.006) (0.007) (0.002)

Monthly FE Yes Yes Yes Yes YesObservations 4,296,374 1,814,047 12,320,166 60,627,185 4,231,413McFadden’s R2 0.221 0.143 0.043 0.047 0.158

Fiedor CBI 14 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H1: Intragroup trades

cleared (full sample)(CO) (CR) (EQ) (FX) (IR)

intragroup −2.030∗∗∗ −2.614∗∗∗ −3.579 −0.940∗∗∗ −2.382∗∗∗(0.090) (0.020) (2.417) (0.011) (0.004)

Constant −3.225∗∗∗ −1.132∗∗∗ −2.678∗∗∗ −2.733∗∗∗ 0.150∗∗∗(0.017) (0.005) (0.006) (0.007) (0.002)

Monthly FE Yes Yes Yes Yes YesObservations 4,296,374 1,814,047 12,320,166 60,627,185 4,231,413McFadden’s R2 0.221 0.143 0.043 0.047 0.158

Fiedor CBI 14 / 40

All forthcoming hypotheses arebased on a subsample withoutintragroup trades.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H1: Intragroup trades

Commodity Credit Equity Foreign Exchange Interest Rate0

10

20

30

40

50

60Pr

edic

ted

clea

ring

rate

(%)

CategoryIntragroupExtragroup

Fiedor CBI 15 / 40

Assuming trades at the end of thestudied period (June 2017).

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H1: Intragroup trades

Commodity Credit Equity Foreign Exchange Interest Rate0

10

20

30

40

50

60Pr

edic

ted

clea

ring

rate

(%)

CategoryIntragroupExtragroup

Fiedor CBI 15 / 40

Assuming trades at the end of thestudied period (June 2017).

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H1: Intragroup trades

Commodity Credit Equity Foreign Exchange Interest Rate0

10

20

30

40

50

60Pr

edic

ted

clea

ring

rate

(%)

CategoryIntragroupExtragroup

Fiedor CBI 15 / 40

Assuming trades at the end of thestudied period (June 2017).

Motivation Summary statistics Research Question Dataset Results Conclusions Background

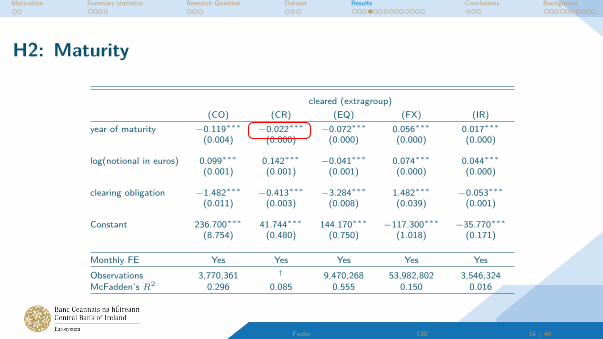

H2: Maturity

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

year of maturity −0.119∗∗∗ −0.022∗∗∗ −0.072∗∗∗ 0.056∗∗∗ 0.017∗∗∗(0.004) (0.000) (0.000) (0.000) (0.000)

log(notional in euros) 0.099∗∗∗ 0.142∗∗∗ −0.041∗∗∗ 0.074∗∗∗ 0.044∗∗∗(0.001) (0.001) (0.001) (0.000) (0.000)

clearing obligation −1.482∗∗∗ −0.413∗∗∗ −3.284∗∗∗ 1.482∗∗∗ −0.053∗∗∗(0.011) (0.003) (0.008) (0.039) (0.001)

Constant 236.700∗∗∗ 41.744∗∗∗ 144.170∗∗∗ −117.300∗∗∗ −35.770∗∗∗(8.754) (0.480) (0.750) (1.018) (0.171)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.296 0.085 0.555 0.150 0.016

Fiedor CBI 16 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H2: Maturity

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

year of maturity −0.119∗∗∗ −0.022∗∗∗ −0.072∗∗∗ 0.056∗∗∗ 0.017∗∗∗(0.004) (0.000) (0.000) (0.000) (0.000)

log(notional in euros) 0.099∗∗∗ 0.142∗∗∗ −0.041∗∗∗ 0.074∗∗∗ 0.044∗∗∗(0.001) (0.001) (0.001) (0.000) (0.000)

clearing obligation −1.482∗∗∗ −0.413∗∗∗ −3.284∗∗∗ 1.482∗∗∗ −0.053∗∗∗(0.011) (0.003) (0.008) (0.039) (0.001)

Constant 236.700∗∗∗ 41.744∗∗∗ 144.170∗∗∗ −117.300∗∗∗ −35.770∗∗∗(8.754) (0.480) (0.750) (1.018) (0.171)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.296 0.085 0.555 0.150 0.016

Fiedor CBI 16 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H2: Maturity

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

year of maturity −0.119∗∗∗ −0.022∗∗∗ −0.072∗∗∗ 0.056∗∗∗ 0.017∗∗∗(0.004) (0.000) (0.000) (0.000) (0.000)

log(notional in euros) 0.099∗∗∗ 0.142∗∗∗ −0.041∗∗∗ 0.074∗∗∗ 0.044∗∗∗(0.001) (0.001) (0.001) (0.000) (0.000)

clearing obligation −1.482∗∗∗ −0.413∗∗∗ −3.284∗∗∗ 1.482∗∗∗ −0.053∗∗∗(0.011) (0.003) (0.008) (0.039) (0.001)

Constant 236.700∗∗∗ 41.744∗∗∗ 144.170∗∗∗ −117.300∗∗∗ −35.770∗∗∗(8.754) (0.480) (0.750) (1.018) (0.171)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.296 0.085 0.555 0.150 0.016

Fiedor CBI 16 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

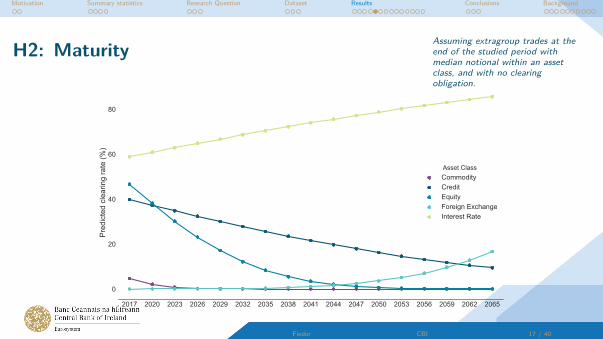

H2: Maturity

2017 2020 2023 2026 2029 2032 2035 2038 2041 2044 2047 2050 2053 2056 2059 2062 2065

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 17 / 40

Assuming extragroup trades at theend of the studied period withmedian notional within an assetclass, and with no clearingobligation.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H2: Maturity

2017 2020 2023 2026 2029 2032 2035 2038 2041 2044 2047 2050 2053 2056 2059 2062 2065

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 17 / 40

Assuming extragroup trades at theend of the studied period withmedian notional within an assetclass, and with no clearingobligation.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H2: Maturity

2017 2020 2023 2026 2029 2032 2035 2038 2041 2044 2047 2050 2053 2056 2059 2062 2065

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 17 / 40

Assuming extragroup trades at theend of the studied period withmedian notional within an assetclass, and with no clearingobligation.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H2: Maturity

2017 2020 2023 2026 2029 2032 2035 2038 2041 2044 2047 2050 2053 2056 2059 2062 2065

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 17 / 40

Assuming extragroup trades at theend of the studied period withmedian notional within an assetclass, and with no clearingobligation.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H3: Notional value

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

log(notional in euros) 0.109∗∗∗ 0.144∗∗∗ −0.029∗∗∗ 0.081∗∗∗ 0.024∗∗∗(0.001) (0.001) (0.001) (0.000) (0.000)

year of maturity −0.076∗∗∗ −0.021∗∗∗ −0.000∗ 0.041∗∗∗ 0.015∗∗∗(0.003) (0.000) (0.000) (0.000) (0.000)

non-EEA counterparty 0.145∗∗∗ 0.132∗∗∗ −1.594∗∗∗ −1.398∗∗∗ −1.216∗∗∗(0.005) (0.003) (0.008) (0.006) (0.001)

Constant 149.500∗∗∗ 38.180∗∗∗ −1.295∗∗∗ −85.870∗∗∗ −29.740∗∗∗(6.592) (0.475) (0.386) (0.261) (0.182)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.251 0.075 0.201 0.255 0.163

Fiedor CBI 18 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H3: Notional value

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

log(notional in euros) 0.109∗∗∗ 0.144∗∗∗ −0.029∗∗∗ 0.081∗∗∗ 0.024∗∗∗(0.001) (0.001) (0.001) (0.000) (0.000)

year of maturity −0.076∗∗∗ −0.021∗∗∗ −0.000∗ 0.041∗∗∗ 0.015∗∗∗(0.003) (0.000) (0.000) (0.000) (0.000)

non-EEA counterparty 0.145∗∗∗ 0.132∗∗∗ −1.594∗∗∗ −1.398∗∗∗ −1.216∗∗∗(0.005) (0.003) (0.008) (0.006) (0.001)

Constant 149.500∗∗∗ 38.180∗∗∗ −1.295∗∗∗ −85.870∗∗∗ −29.740∗∗∗(6.592) (0.475) (0.386) (0.261) (0.182)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.251 0.075 0.201 0.255 0.163

Fiedor CBI 18 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H3: Notional value

103 104 105 106 107 108 109 1010 1011

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 19 / 40

Assuming extragroup, intra-EEAtrades at the end of the studiedperiod with median (short-term)maturity within an asset class.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H3: Notional value

103 104 105 106 107 108 109 1010 1011

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 19 / 40

Assuming extragroup, intra-EEAtrades at the end of the studiedperiod with median (short-term)maturity within an asset class.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H3: Notional value

103 104 105 106 107 108 109 1010 1011

0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

Asset ClassCommodityCreditEquityForeign ExchangeInterest Rate

Fiedor CBI 19 / 40

Assuming extragroup, intra-EEAtrades at the end of the studiedperiod with median (short-term)maturity within an asset class.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

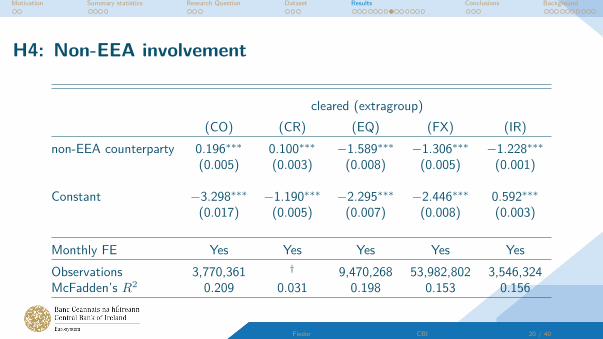

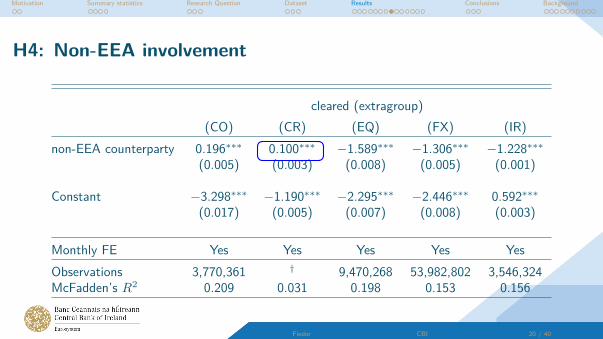

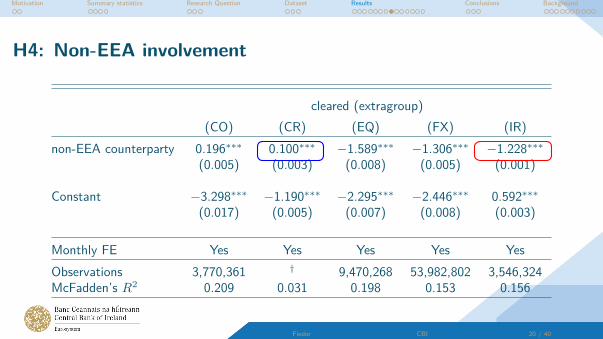

H4: Non-EEA involvement

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

non-EEA counterparty 0.196∗∗∗ 0.100∗∗∗ −1.589∗∗∗ −1.306∗∗∗ −1.228∗∗∗(0.005) (0.003) (0.008) (0.005) (0.001)

Constant −3.298∗∗∗ −1.190∗∗∗ −2.295∗∗∗ −2.446∗∗∗ 0.592∗∗∗(0.017) (0.005) (0.007) (0.008) (0.003)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.209 0.031 0.198 0.153 0.156

Fiedor CBI 20 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H4: Non-EEA involvement

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

non-EEA counterparty 0.196∗∗∗ 0.100∗∗∗ −1.589∗∗∗ −1.306∗∗∗ −1.228∗∗∗(0.005) (0.003) (0.008) (0.005) (0.001)

Constant −3.298∗∗∗ −1.190∗∗∗ −2.295∗∗∗ −2.446∗∗∗ 0.592∗∗∗(0.017) (0.005) (0.007) (0.008) (0.003)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.209 0.031 0.198 0.153 0.156

Fiedor CBI 20 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H4: Non-EEA involvement

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

non-EEA counterparty 0.196∗∗∗ 0.100∗∗∗ −1.589∗∗∗ −1.306∗∗∗ −1.228∗∗∗(0.005) (0.003) (0.008) (0.005) (0.001)

Constant −3.298∗∗∗ −1.190∗∗∗ −2.295∗∗∗ −2.446∗∗∗ 0.592∗∗∗(0.017) (0.005) (0.007) (0.008) (0.003)

Monthly FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.209 0.031 0.198 0.153 0.156

Fiedor CBI 20 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H4: Non-EEA involvement

Commodity Credit Equity Foreign Exchange Interest Rate0

10

20

30

40

50

60

70

80Pr

edic

ted

clea

ring

rate

(%)

CategoryWith non-EEA counterpartyTwo EEA counterparties

Fiedor CBI 21 / 40

Assuming extragroup trades at theend of the studied person.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H4: Non-EEA involvement

Commodity Credit Equity Foreign Exchange Interest Rate0

10

20

30

40

50

60

70

80Pr

edic

ted

clea

ring

rate

(%)

CategoryWith non-EEA counterpartyTwo EEA counterparties

Fiedor CBI 21 / 40

Assuming extragroup trades at theend of the studied person.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H4: Non-EEA involvement

Commodity Credit Equity Foreign Exchange Interest Rate0

10

20

30

40

50

60

70

80Pr

edic

ted

clea

ring

rate

(%)

CategoryWith non-EEA counterpartyTwo EEA counterparties

Fiedor CBI 21 / 40

Assuming extragroup trades at theend of the studied person.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H5: Financial sophistication

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

financial nature −0.900∗∗∗ 1.170∗∗∗ −0.891∗∗∗ 1.038∗∗∗ 0.798∗∗∗(0.019) (0.019) (0.009) (0.029) (0.008)

non-EEA counterparty 0.605∗∗∗ 0.113∗∗∗ −1.977∗∗∗ −1.411∗∗∗ −1.266∗∗∗(0.008) (0.003) (0.009) (0.006) (0.002)

Constant −4.479∗∗∗ −2.967∗∗∗ −0.014 −3.603∗∗∗ −0.429∗∗∗(0.034) (0.022) (0.013) (0.030) (0.009)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.515 0.041 0.544 0.201 0.171

Fiedor CBI 22 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H5: Financial sophistication

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

financial nature −0.900∗∗∗ 1.170∗∗∗ −0.891∗∗∗ 1.038∗∗∗ 0.798∗∗∗(0.019) (0.019) (0.009) (0.029) (0.008)

non-EEA counterparty 0.605∗∗∗ 0.113∗∗∗ −1.977∗∗∗ −1.411∗∗∗ −1.266∗∗∗(0.008) (0.003) (0.009) (0.006) (0.002)

Constant −4.479∗∗∗ −2.967∗∗∗ −0.014 −3.603∗∗∗ −0.429∗∗∗(0.034) (0.022) (0.013) (0.030) (0.009)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.515 0.041 0.544 0.201 0.171

Fiedor CBI 22 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H5: Financial sophistication

Commodity Credit Equity Foreign Exchange Interest Rate0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

CategoryNFCBankG16OFIICPF

Fiedor CBI 23 / 40

Assuming extragroup intra-EEAtrades at the end of the studiedperiod.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H5: Financial sophistication

Commodity Credit Equity Foreign Exchange Interest Rate0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

CategoryNFCBankG16OFIICPF

Fiedor CBI 23 / 40

Assuming extragroup intra-EEAtrades at the end of the studiedperiod.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H5: Financial sophistication

Commodity Credit Equity Foreign Exchange Interest Rate0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

CategoryNFCBankG16OFIICPF

Fiedor CBI 23 / 40

Assuming extragroup intra-EEAtrades at the end of the studiedperiod.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H5: Financial sophistication

Commodity Credit Equity Foreign Exchange Interest Rate0

20

40

60

80Pr

edic

ted

clea

ring

rate

(%)

CategoryNFCBankG16OFIICPF

Fiedor CBI 23 / 40

Assuming extragroup intra-EEAtrades at the end of the studiedperiod.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

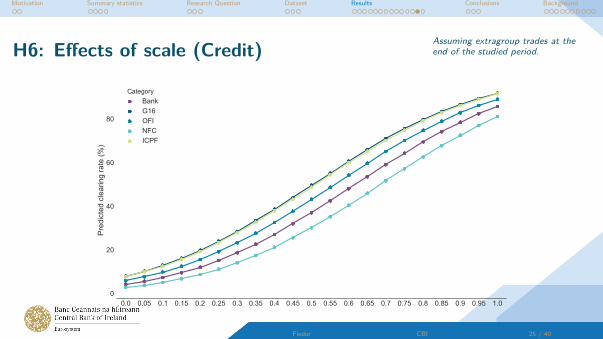

H6: Effects of scale

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

prev. cleared ratio 7.203∗∗∗ 2.798∗∗∗ 6.810∗∗∗ 1.868∗∗∗(0.048) (0.008) (0.050) (0.003)

Constant −4.265∗∗∗ −2.198∗∗∗ −4.128∗∗∗ −0.615∗∗∗(0.044) (0.011) (0.069) (0.003)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.866 0.154 0.991 0.050

Fiedor CBI 24 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6: Effects of scale

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

prev. cleared ratio 7.203∗∗∗ 2.798∗∗∗ 6.810∗∗∗ 1.868∗∗∗(0.048) (0.008) (0.050) (0.003)

Constant −4.265∗∗∗ −2.198∗∗∗ −4.128∗∗∗ −0.615∗∗∗(0.044) (0.011) (0.069) (0.003)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.866 0.154 0.991 0.050

Fiedor CBI 24 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6: Effects of scale (Credit)

0.0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.5 0.55 0.6 0.65 0.7 0.75 0.8 0.85 0.9 0.95 1.00

20

40

60

80

Pred

icte

d cl

earin

g ra

te (%

)Category

BankG16OFINFCICPF

Fiedor CBI 25 / 40

Assuming extragroup trades at theend of the studied period.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6: Effects of scale (Interest Rate)

0.0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.5 0.55 0.6 0.65 0.7 0.75 0.8 0.85 0.9 0.95 1.0

10

20

30

40

50

60

70

80

90

Pred

icte

d cl

earin

g ra

te (%

)Category

BankG16OFINFCICPF

Fiedor CBI 26 / 40

Assuming extragroup trades at theend of the studied period.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

ConclusionsWhat have we learned?

Fiedor CBI 27 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:

I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:

I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:

I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:

I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:

I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:

I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:

I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:

I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!

I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:

I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:

I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;

F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:

I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:I Other factors also have an impact dependent on their specific combination.

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Main findings

� Differences across asset classes:I Only Credit & Interest Rate are centrally cleared to a significant degree!I Some factors affect Credit & Interest Rate contracts differently.

� Effects of scale:I There are significant effects of scale connected with central clearing, both in terms of:

F previous clearing activity of the counterparty;F the notional of the specific contract;

� Other factors:I Other factors also have an impact dependent on their specific combination.

Details in the full paper (ESRB WP 72).

Fiedor CBI 28 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Policy implications

The results are timely in relation to the ongoing policy debate:

� It seems there is a scope for extending the clearing obligation given there is a significant amount ofvoluntary clearing in the markets;

� Strong effects of scale imply that future regulation may wish to take this into account in helpingovercome the fixed costs;

� In particular, three remaining asset classes may need regulatory push to kick start central clearing.

Fiedor CBI 29 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Policy implications

The results are timely in relation to the ongoing policy debate:� It seems there is a scope for extending the clearing obligation given there is a significant amount of

voluntary clearing in the markets;

� Strong effects of scale imply that future regulation may wish to take this into account in helpingovercome the fixed costs;

� In particular, three remaining asset classes may need regulatory push to kick start central clearing.

Fiedor CBI 29 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Policy implications

The results are timely in relation to the ongoing policy debate:� It seems there is a scope for extending the clearing obligation given there is a significant amount of

voluntary clearing in the markets;

� Strong effects of scale imply that future regulation may wish to take this into account in helpingovercome the fixed costs;

� In particular, three remaining asset classes may need regulatory push to kick start central clearing.

Fiedor CBI 29 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Policy implications

The results are timely in relation to the ongoing policy debate:� It seems there is a scope for extending the clearing obligation given there is a significant amount of

voluntary clearing in the markets;

� Strong effects of scale imply that future regulation may wish to take this into account in helpingovercome the fixed costs;

� In particular, three remaining asset classes may need regulatory push to kick start central clearing.

Fiedor CBI 29 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Thank [email protected]

Fiedor CBI 30 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

Background slidesSummary statistics

Fiedor CBI 31 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6a: Effects of scale (trading)

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

log(prev. months’ notional) −0.088∗∗∗ 0.041∗∗∗ −0.123∗∗∗ 0.395∗∗∗ 0.047∗∗∗(0.001) (0.001) (0.001) (0.002) (0.000)

Constant −5.098∗∗∗ −2.731∗∗∗ 0.609∗∗∗ −4.985∗∗∗ −1.046∗∗∗(0.030) (0.018) (0.014) (0.017) (0.007)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.544 0.039 0.444 0.248 0.023

Fiedor CBI 32 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6a: Effects of scale (trading)

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

log(prev. months’ notional) −0.088∗∗∗ 0.041∗∗∗ −0.123∗∗∗ 0.395∗∗∗ 0.047∗∗∗(0.001) (0.001) (0.001) (0.002) (0.000)

Constant −5.098∗∗∗ −2.731∗∗∗ 0.609∗∗∗ −4.985∗∗∗ −1.046∗∗∗(0.030) (0.018) (0.014) (0.017) (0.007)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.544 0.039 0.444 0.248 0.023

Fiedor CBI 32 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

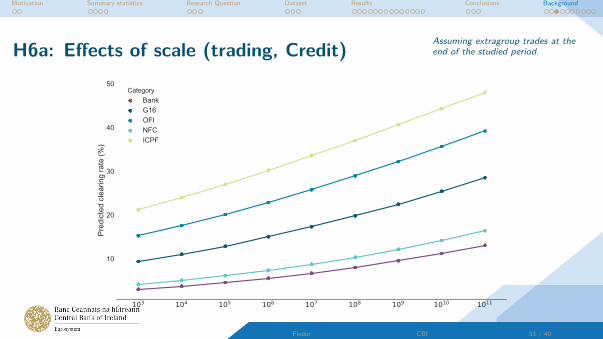

H6a: Effects of scale (trading, Credit)

103 104 105 106 107 108 109 1010 1011

10

20

30

40

50

Pred

icte

d cl

earin

g ra

te (%

)Category

BankG16OFINFCICPF

Fiedor CBI 33 / 40

Assuming extragroup trades at theend of the studied period.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

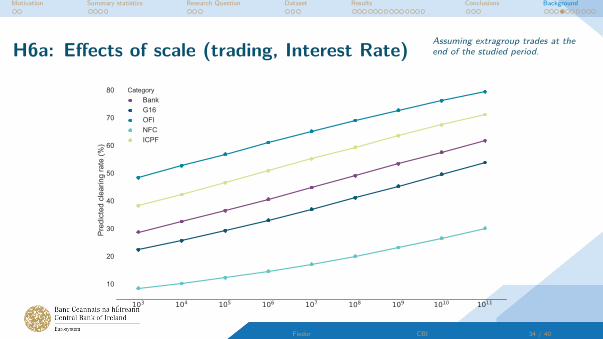

H6a: Effects of scale (trading, Interest Rate)

103 104 105 106 107 108 109 1010 1011

10

20

30

40

50

60

70

80Pr

edic

ted

clea

ring

rate

(%)

CategoryBankG16OFINFCICPF

Fiedor CBI 34 / 40

Assuming extragroup trades at theend of the studied period.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6b: Effects of scale (clearing)

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

log(prev. months’ not. cleared) 0.289∗∗∗ 0.110∗∗∗ 0.396∗∗∗ 0.071∗∗∗ 0.072∗∗∗(0.002) (0.000) (0.003) (0.000) (0.000)

Constant −3.946∗∗∗ −3.907∗∗∗ −4.652∗∗∗ −3.935∗∗∗ −1.593∗∗∗(0.035) (0.015) (0.076) (0.011) (0.006)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.885 0.119 0.990 0.177 0.049

Fiedor CBI 35 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6b: Effects of scale (clearing)

cleared (extragroup)(CO) (CR) (EQ) (FX) (IR)

log(prev. months’ not. cleared) 0.289∗∗∗ 0.110∗∗∗ 0.396∗∗∗ 0.071∗∗∗ 0.072∗∗∗(0.002) (0.000) (0.003) (0.000) (0.000)

Constant −3.946∗∗∗ −3.907∗∗∗ −4.652∗∗∗ −3.935∗∗∗ −1.593∗∗∗(0.035) (0.015) (0.076) (0.011) (0.006)

Monthly FE Yes Yes Yes Yes YesType FE Yes Yes Yes Yes YesObservations 3,770,361 † 9,470,268 53,982,802 3,546,324McFadden’s R2 0.885 0.119 0.990 0.177 0.049

Fiedor CBI 35 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6b: Effects of scale (clearing, Credit)

103 104 105 106 107 108 109 1010 1011

0

20

40

60

80

Pred

icte

d cl

earin

g ra

te (%

)Category

BankG16OFINFCICPF

Fiedor CBI 36 / 40

Assuming extragroup trades at theend of the studied period.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

H6b: Effects of scale (clearing, Interest Rate)

103 104 105 106 107 108 109 1010 1011

10

20

30

40

50

60

70

80

90Pr

edic

ted

clea

ring

rate

(%)

CategoryBankG16OFINFCICPF

Fiedor CBI 37 / 40

Assuming extragroup trades at theend of the studied period.

Motivation Summary statistics Research Question Dataset Results Conclusions Background

References

M. Bellia, R. Panzica, L. Pelizzon, T. Peltonen.The demand for central clearing: to clear or not to clear, that is the question.ESRB WP, 62, October, 2017.

B. Biais, F. Heider, M. Hoerova.Clearing, counterparty risk and aggregate risk.ECB WP, 1481, October, 2012.

Bank for International Settlements.Regulatory reform of over-the-counter derivatives: an assessment of incentives to clear centrally.October 2014.D. Duffie, M. Scheicher, G. Vuillemey.Central clearing and collateral demand.Journal of Financial Economics, 116(2):237–256, 2015.

Fiedor CBI 38 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

References

D. Duffie, H. Zhu.Does a Central Clearing Counterparty Reduce Counterparty Risk?The Review of Asset Pricing Studies, 1(1):74–95, 2011.

V. G. France, C. M. Kahn.Law as a constraint on bailouts: Emergency support for central counterparties.Journal of Financial Intermediation, 28:22–31, 2016.

S. Ghamami, P. Glasserman.Does OTC derivatives reform incentivize central clearing?Journal of Financial Intermediation, 32:76–98, 2017.

A. G. Haldane, R. M. May.Systemic risk in banking ecosystems.Nature, 469:351–355, 2011.

Fiedor CBI 39 / 40

Motivation Summary statistics Research Question Dataset Results Conclusions Background

References

J. Helwege, C. M. Turner.The Slope of the Credit Yield Curve for Speculative-Grade Issuers.Journal of Finance, 54(5):1869–1884, 1999.

J. Hull.CCPs: Their Risks, and How They Can Be Reduced.Journal of Derivatives, 20(1):26–29, 2012.

T. V. Koeppl, C. Monnet.The Emergence and future of central counterparties.FRB Philadelphia WP, 10-30, September, 2010.

R. La Porta, F. Lopez-De-Silanes, A. Shleifer, R. W. Vishny.Legal Determinants of External Finance.Journal of Finance, 52(3):1131–1150, 1997.

E. Stephens, J. R. Thompson.Information asymmetry and risk transfer markets.Journal of Financial Intermediation, 32(C):88–99, 2017.

Fiedor CBI 40 / 40

![[ ENTER CAPTIONS TEXT ] NATIONAL CLEARINGHOUSE OF ... · and voluntary separation. if a certain -- if certain elements are present. you have to prove that the parties live separate](https://img.pdfslide.net/doc/110x75/5f85c5392ddbec364d22c26d/-enter-captions-text-national-clearinghouse-of-and-voluntary-separation.jpg)