Embed Size (px)

Citation preview

clearthoughtConsumer Insights from Clearwater International Winter 2015

Gyms & FitnessThe pace of change in the sector is set to accelerate further as new players enter the market.

Fighting Fit

Key sector trends

Rapid development of the low-cost gym sector, disrupting the existing marketplace, with implications for mid-market operators through sector consolidation;

Continuing interest in premium gym facilities, including spa and other wellness facilities, offering value-added services to cash-rich, time-poor consumers;

Development of specialist fi tness concepts, refl ecting continuing consumer interest in new experiences – this has

given rise to the growth of passport type services, allowing gym goers to mix and match offerings from different fi tness facilities;

International development as players seek growth outside increasingly competitive domestic markets;

Development of strong lifestyle brands by gym and fi tness operators, with a focus on selling branded accessories, clothing and sports nutrition products.

The gym and fi tness market has seen signifi cant deal activity over the past 18 months, from the low-cost gym chains right through to top-end luxury facilities. In developed markets, increasing competition - particularly among mid-market operators - has triggered the need to consolidate.

The sector has many positive drivers, including increasing awareness of health and rising obesity levels, which are gradually raising sports participation and membership at fi tness centres.

However, like in other sectors, the mid-market is being squeezed. Cost-conscious consumers want to receive value for money and so low-cost gyms have thrived, thereby intensifying price competition and highlighting the lack of market differentiation. At the higher end, consumers have demonstrated a willingness to pay to receive exceptional service, high-quality facilities and a range of gym activities that suit their needs.

The challenge of being stuck in the mid-market has been made clear with the fortunes of Fitness First, one of the largest gym chains in the world, and, more recently, LA Fitness. Both UK-based groups have faced stiff competition from low-cost operators.

US funds Oaktree Capital Management and Marathon Asset Management bought Fitness First in 2012 in a ¤490m debt for equity swap, when the group was on the brink of administration. Post-restructuring, the company has been slimmed down.

LA Fitness came under bank ownership in 2014 after being backed since 2005 by MidOcean Partners. The majority of the

Key sector trends

group’s remaining gyms were acquired by low-cost operator Pure Gym which plans to convert them to its own format - therefore closing pools, saunas and cafés to maximise gym space.

We believe the growth in low-cost and top-end luxury facilities will continue to create investment opportunities for private equity while generating consolidation opportunities in the mid-market.

Consumer Insights from Clearwater Internationalclearthought | Winter 2015

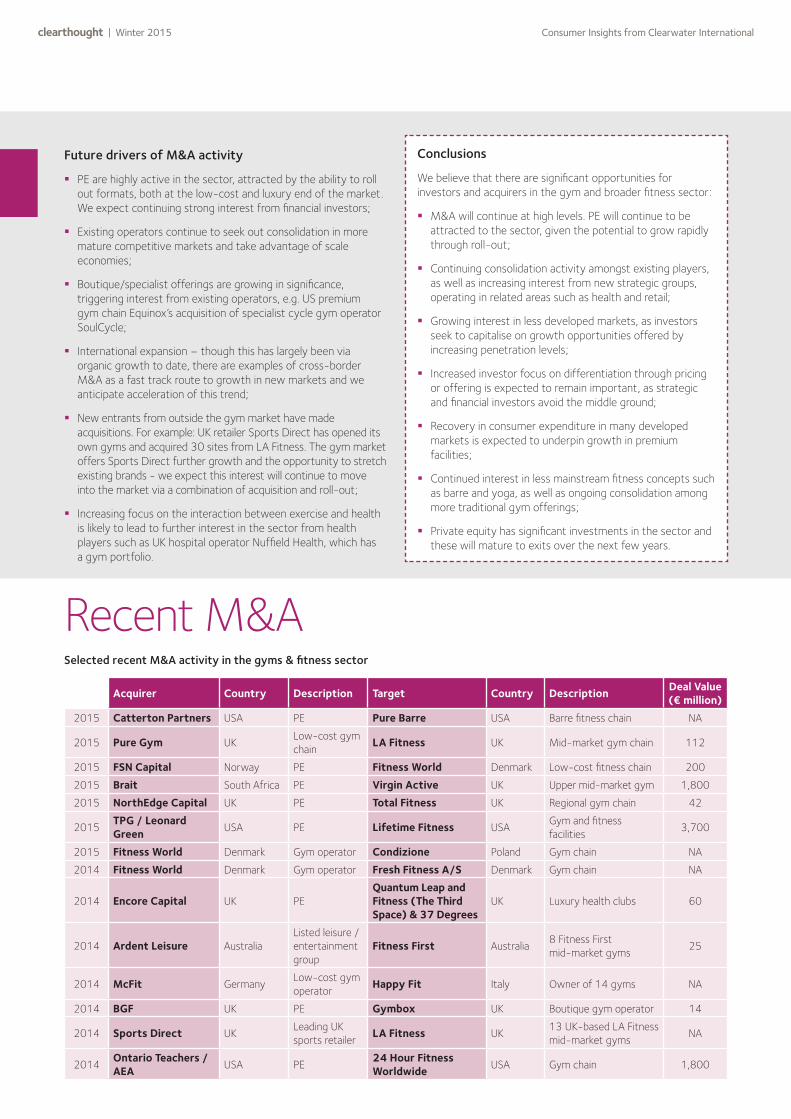

Future drivers of M&A activity

PE are highly active in the sector, attracted by the ability to roll out formats, both at the low-cost and luxury end of the market. We expect continuing strong interest from financial investors;

Existing operators continue to seek out consolidation in more mature competitive markets and take advantage of scale economies;

Boutique/specialist offerings are growing in significance, triggering interest from existing operators, e.g. US premium gym chain Equinox’s acquisition of specialist cycle gym operator SoulCycle;

International expansion – though this has largely been via organic growth to date, there are examples of cross-border M&A as a fast track route to growth in new markets and we anticipate acceleration of this trend;

New entrants from outside the gym market have made acquisitions. For example: UK retailer Sports Direct has opened its own gyms and acquired 30 sites from LA Fitness. The gym market offers Sports Direct further growth and the opportunity to stretch existing brands - we expect this interest will continue to move into the market via a combination of acquisition and roll-out;

Increasing focus on the interaction between exercise and health is likely to lead to further interest in the sector from health players such as UK hospital operator Nuffield Health, which has a gym portfolio.

Conclusions

We believe that there are significant opportunities for investors and acquirers in the gym and broader fitness sector:

• M&A will continue at high levels. PE will continue to be attracted to the sector, given the potential to grow rapidly through rollout;

• Continuing consolidation activity amongst existing players, as well as increasing interest from new strategic groups, operating in related areas such as health and retail;

• Growing interest in less developed markets, as investors seek to capitalise on growth opportunities offered by increasing penetration levels;

• Increased investor focus on differentiation through pricing or offering is expected to remain important, as strategic and financial investors avoid the middle ground;

• Recovery in consumer expenditure in many developed markets is expected to underpin growth in premium facilities;

• Continued interest in less mainstream fitness concepts such as barre and yoga as well as ongoing consolidation among more traditional gym offerings;

• Private equity has significant investments in the sector and these will mature to exits over the next few years.

Acquirer Country Description Target Country DescriptionDeal Value (¤ million)

2015 Catterton Partners USA PE Pure Barre USA Barre fitness chain NA

2015 Pure Gym UKLow-cost gym chain

LA Fitness UK Mid-market gym chain 112

2015 FSN Capital Norway PE Fitness World Denmark Low-cost fitness chain 200

2015 Brait South Africa PE Virgin Active UK Upper mid-market gym 1,800

2015 NorthEdge Capital UK PE Total Fitness UK Regional gym chain 42

2015TPG / Leonard Green

USA PE Lifetime Fitness USAGym and fitness facilities

3,700

2015 Fitness World Denmark Gym operator Condizione Poland Gym chain NA

2014 Fitness World Denmark Gym operator Fresh Fitness A/S Denmark Gym chain NA

2014 Encore Capital UK PEQuantum Leap and Fitness (The Third Space) & 37 Degrees

UK Luxury health clubs 60

2014 Ardent Leisure AustraliaListed leisure / entertainment group

Fitness First Australia 8 Fitness First mid-market gyms

25

2014 McFit GermanyLow-cost gym operator

Happy Fit Italy Owner of 14 gyms NA

2014 BGF UK PE Gymbox UK Boutique gym operator 14

2014 Sports Direct UKLeading UK sports retailer

LA Fitness UK13 UK-based LA Fitness mid-market gyms

NA

2014Ontario Teachers / AEA

USA PE24 Hour Fitness Worldwide

USA Gym chain 1,800

Selected recent M&A activity in the gyms & fitness sector

Conclusions

We believe that there are significant opportunities for investors and acquirers in the gym and broader fitness sector:

M&A will continue at high levels. PE will continue to be attracted to the sector, given the potential to grow rapidly through roll-out;

Continuing consolidation activity amongst existing players, as well as increasing interest from new strategic groups, operating in related areas such as health and retail;

Growing interest in less developed markets, as investors seek to capitalise on growth opportunities offered by increasing penetration levels;

Increased investor focus on differentiation through pricing or offering is expected to remain important, as strategic and financial investors avoid the middle ground;

Recovery in consumer expenditure in many developed markets is expected to underpin growth in premium facilities;

Continued interest in less mainstream fitness concepts such as barre and yoga, as well as ongoing consolidation among more traditional gym offerings;

Private equity has significant investments in the sector and these will mature to exits over the next few years.

Recent M&A

clearthought | Winter 2015 Consumer Insights from Clearwater International

Low-cost gyms

The sector started to take shape in the United States and has grown rapidly across many markets over the past five years, benefitting from weaker economic conditions. As in other consumer areas such as airlines, supermarkets and hotels, customers have increasingly embraced low-cost no-frills alternatives.

Key trends

Allure of luxury

While the low-cost gym sector has undoubtedly seen high growth, there is continued strong interest in the premium end of the market.

For instance: in the US, premium player Equinox Fitness (owned by real estate firm Related Cos and buyout firm Leonard Green & Partners) has continued to build its premium business by acquiring Sports Club/LA gyms in New York and four other cities as well as the Reebok Sports Club/ NY gym in Manhattan.

Equinox’s premium empire has now expanded to 73 locations worldwide. It has also been building its low-cost operations via Blink Fitness, with 50 gyms currently and a goal of opening a further 300 sites by 2020 using a franchise model.

Fitness First announced earlier this year that it was launching a new invitation-only gym brand – Gravity - targeted at CEOs looking for a private workout environment. The first Gravity health club launched this summer in Singapore.

Motivated by the possibility of cross-selling health services, Nuffield Health & Fitness acquired the London upmarket City Point Gym in 2015. Nuffield Health, a major player in the provision of private hospitals, has around 70 gyms after initially moving into the sector in 2000.

The disruptive impact of low-cost gyms on the mid-market in the UK can be seen by the loss of market share of mid-market operators such as LA Fitness.

The sector grabbed the headlines in early 2014 with a planned merger between Pure Gym, backed by CCMP Capital Advisors, and The Gym Group, backed by Phoenix Private Equity.

The merger would have created a formidable player in the low-cost sector but the Competition and Markets Authority referred the merger for detailed investigation and the companies subsequently abandoned the deal. In June 2015, Pure Gym announced that it would instead acquire LA Fitness following its restructuring. Meanwhile, in 2013, the Business Growth Fund backed low-cost gym chain Xercise4less which was founded by ex-rugby player Jon Wright. Since then, the company has opened 15 further gyms - bringing the total to 24.

In Spain, despite high levels of overall gym membership penetration, the market remains fragmented. McFit, the German discount operator, moved into the market in 2009 with a club in Mallorca and opened its first club in mainland Spain in 2010. Magenta Partners, the earlier backers of UK-based Pure Gym, has also entered the Spanish market. Having achieved a 6x return on its UK investment, Magenta replicated the same low-cost business model in Spain (under the brand Viva Gym) and South Africa.

Denmark and Sweden have some of the highest levels of gym penetration. One of the first players in the market was Fitness World, which now has a membership of around 450,000 in Denmark. In 2014, it acquired its closest competitor, Fresh Fitness, as well as making an acquisition in Poland and this year was acquired by Nordic private equity group FSN Capital. FSN had previously backed fitness chain Actic (formerly Nautilus Gym) which it divested in 2012.

Competitors from related areas are also moving into the space. Sports retailer Sports Direct has acquired a number of LA Fitness gyms and announced plans to roll out 200 low-cost gyms. JD Sports also has plans to build a national gym chain. This is not a new phenomenon, with the likes of Swiss retailer Migros being active

in the fitness space for some time. On the leisure side, Ardent of Australia - better known for operating theme parks, marinas and bowling alleys - has been building up activities in this area and now generates around 30% of revenues from gyms, following the acquisition of Fitness First’s Western Australian gyms in 2014.

1 Mintel

Low-cost German operator McFit and Basic-Fit of the Netherlands are now the leading players in Europe, in terms of membership numbers. McFit has over a million members across Germany, Austria and Spain. The group was founded in 1997 with the concept of a low-cost fitness studio, open 24 hours a day but with limited facilities and training personnel. McFit subsequently acquired Fit24, its main low-cost competitor, and the group has since consolidated its position as the leading low-cost operator with over 200 gyms.

Between 2009 and 2012, the Dutch and Belgian discount fitness markets grew at a double-digit growth rate. Basic-Fit, established in 2003, operates around 200 discount gyms across the Netherlands, Belgium, Spain and France - making it one of the largest and most international European gym operators, with half a million members. PE group 3i backed Basic-Fit in 2013, in a transaction valuing the group at ¤275m.

Despite being one of the largest European markets, the UK was relatively late to follow the low-cost gym trend, with the first one opening after 2005. It is estimated that they now account for over 20% of membership, with around 5,000 members per club compared with an industry average of about 1,9001, while budget gyms are growing faster than any other part of the sector (roughly 200% since 2011). Pure Gym has opened over 90 clubs since 2009 and has a target of 250-300 UK gyms by 2020.

Consumer Insights from Clearwater Internationalclearthought | Winter 2015

Boutique is beautiful

Premium gym operators have increasingly sought to offer niche and specialist activities. This led premium US operator Equinox Fitness to acquire a majority stake in boutique operator SoulCycle in 2011.

SoulCycle is a US indoor cycling fitness chain, with a strong lifestyle element and a cult following. The company has 42 US locations and plans to open 50 to 60 studios worldwide by next year. The company also has a retail clothing line and, according to Moody’s, is Equinox’s fastest-growing segment. It recently announced plans to float on the stock market and has inspired a number of similar concepts such as London-based Psycle.

There is growing investor interest in specialist fitness concepts such as spinning, yoga and barre. These boutique operators, which often charge per class rather than a monthly membership fee, have been taking market share from more traditional gym chains.

Private Equity has also been active in the luxury segment. Encore Capital acquired 37 Degrees - a luxury health and fitness club in London. This followed the acquisition of The Third Space chain, whose clubs in London are favoured by celebrities. Encore already owned Reebok Sports Club in London.

In 2014, the Business Growth Fund backed upmarket boutique London gym chain Gymbox with a ¤12.6m investment. Clearwater International advised the founder of the company on the transaction. Gymbox’s design-led gyms have attracted celebrity interest and include exercise classes with live DJs and an Olympic-size boxing ring. The group used the funding to expand the chain both in and outside of London.

One development fuelling the growth of smaller niche and boutique operators is the growing popularity of passport type gym memberships, an innovation which started in the US. ClassPass, a New York start-up, was valued in excess of ¤180m ($200m) in its Series B ¤37m ($40m) financing round at the start of the year.

The company launched a subscription service in 2013, for monthly fees of around ¤90 ($99) per month in most cities, where consumers can choose a variety of different workouts from different providers in their area on an unlimited basis. Each time a user attends a partner studio, ClassPass pays the studio a preset amount. The model works alongside the growth of boutique studios with more specialist classes as pioneered by operators such as SoulCycle. Following its funding round, ClassPass is now targeting the UK and Canadian markets.

Competition in these flexible passport-type arrangements is hotting up - and is not just confined to the boutique end of the market. PayasUGym, a UK start-up, is one such operator. The company was founded in 2011 and offers a one-off entry pass or short-term gym membership, allowing users to participate wherever and whenever they want. It has grown from under 300 participating gyms in early 2012 to around 1,200 today.

Given there are around 6,000 gyms and fitness centres in the UK, this represents a healthy proportion. PayasUGym has also been able to partner with outdoor operators such as British Military Fitness, which provides army-style outdoor group training at a lower cost than conventional gym classes. Mintel estimates that 32% of UK gym users prefer to pay on a per visit basis.

US consumer-focused private equity fund Catterton Partners has made a number of investments in this area. Earlier this year, the firm invested in Pure Barre - a method that combines ballet, pilates and resistance training in a low impact workout. Pure Barre now has more than 300 studios, via franchising, as well as an in-store and online retail presence selling apparel, fitness accessories and media content. Catterton’s investment will be used to support Pure Barre’s continued US and international expansion. It followed earlier investments:

A 2014 investment in Flywheel Sports, an indoor cycling brand, founded in 2010 by Ruth Zukerman, a leading name in the US indoor cycling fitness scene. Flywheel indoor cycling studios feature stadium-style seating, custom engineered bikes and performance tracking technology;

A 2013 investment in a chain of CorePower Yoga studios. CorePower is one of the largest operators, with 80 yoga studios, focused on heated power yoga. The company was founded in 2002 with a vision to create a national yoga chain focused on standards and consistency. The studios also offer lifestyle programmes such as BootCamp, to boost fitness and metabolism, and a Wellness Cleanse, to teach long-term healthy eating and living.

clearthought | Winter 2015 Consumer Insights from Clearwater International

The past five years have seen significant change in the gym and fitness landscape and the pace of change, if anything, is expected to accelerate. PE have been highly active in the sector and with so many assets still in PE ownership, we expect to see further consolidation. Consolidation amongst other existing operators will also continue, driven by the potential for scale economies in a more mature competitive market. The trend for boutique offerings looks set to stay and the more successful concepts are likely to be attractive targets for some of the more established brands, with the opportunity to develop multi-brand offerings appealing to different customer bases. There will also be increasing interest from new entrants from outside the gym market. Retailers have already moved into the sector, attracted by the opportunity to make use of vacant or under-used retail units and potentially stretch brands into new but related areas. Increasing focus on the interaction between exercise and health is also likely to lead to interest in the sector from health players. Looking further afield, there is likely to be appetite for development in some of the less developed gym and fitness markets as players seek to capitalise on the growth opportunities offered by increasing penetration rates.

The future

International development and cross-border M&A

While there has been significant domestic M&A activity across a number of markets, there has also been a reasonable amount of international development over the years - both via organic growth and M&A.

Fitness First claims to be the largest privately owned health club in the world, with almost a million members in 16 countries. Following its restructuring, the chain pulled out of all European markets except the UK and Germany to focus on markets such as Australia, Asia and the Middle East. After selling some of its Australian clubs as part of the 2012 restructuring, the group has been gradually refurbishing its remaining clubs.

In Melbourne, the group recently launched a brand new concept club - the High Performance Club - incorporating elements such as MoveLab, which uses the latest video technology to allow members to test their athletic performance, analyse their movements and perfect their technique.

Fitness First also has ambitious plans for less mature markets such as India. At the end of 2014, the group announced plans to open up 30 new clubs, reflecting expected demand from India’s growing middle class.

Virgin Active has also been developing an international presence. The group currently has 267 clubs in nine countries, with a particularly strong presence in South Africa where it acquired the assets of the Health and Racquet Club. Virgin Active remains the leading gym brand in South Africa with 114 clubs. This led to the acquisition of the group in April 2015 by South African investor Christo Wiese, in a transaction valuing the group at ¤1.8bn. The group had been considering an IPO.

Following the deal, Virgin Active has continued its international expansion by picking up Downtown Gyms based in Milan. This gave the group a total of 11 clubs in Milan and 30 clubs in Italy, where it claims to be the market leader.

It’s not just the mid-market groups that have targeted overseas expansion. Low-cost US group Anytime Fitness has grown using a franchise model and now claims to be the world’s fastest-growing health club franchise with over 3,000 clubs in 23 countries.

PE-backed Snap Fitness - also of the US and a fierce rival of Anytime Fitness - has followed a similar route, expanding internationally into countries such as India via franchising. In the face of this competition from international operators, the franchise model is also being used by low-cost Indian gym group Talwalkars Better Value Fitness as it seeks to double its gym numbers within three years.

Meanwhile, low-cost European operator McFit of Germany has also been active internationally - opening clubs in Austria and Spain, and acquiring Italy-based Happy Fit. This summer, Nordic PE group FSN Capital acquired Danish health club chain Fitness World which in turn had previously acquired Condizione, a Polish health club operator, at the start of 2015.

We expect overseas expansion, including cross-border M&A, to continue to be a feature of the gym market as players seek growth in less penetrated markets and build up regional presence. Gym membership in the US is estimated at 20%, compared to 25% in countries like Germany and Sweden and only around 13-14% in the UK. Fitness First estimates that most of its Asian markets have only a 2-3% penetration.

Consumer Insights from Clearwater Internationalclearthought | Winter 2015

www.clearwaterinternational.com

Deal highlightsSome of our recent fi tness & leisure deals Gareth Iley

Partner, UK+44 845 052 [email protected]

John JensenPartner, Denmark+45 20 33 47 [email protected]

James SinclairPartner, China+44 7704 113 [email protected]

José LemosPartner, Portugal+351 917 529 [email protected]

John SheridanPartner, Ireland+353 1 517 [email protected]

Miguel MartíSenior Advisor, Spain+34 917 812 [email protected]

Jakob Tolstrup KristensenAssociate Partner, Denmark+45 51 90 86 [email protected]

Sarah CharmanConsumer Analyst, UK+44 845 052 [email protected]

Perri BlakeyAssociate Director - Deal Origination, UK+44 845 052 [email protected]

Meet the team

Developer of fi tness and sports nutrition products

Clearwater International advised Nutramino on the cross-border sale to Glanbia plc, a leading international nutritional ingredients group

Nutramino

Leading global designer and supplier of technical marine clothing and accessories

Clearwater International advised the shareholders of Gill on the management buyout backed by YFM Equity Partners

Douglas Gill International

Boutique gym chain

Clearwater International advised the company on the ¤12.6m investment of growth capital from BGF

Gymbox

Scandinavia’s leading online football shop

Clearwater International advised Unisport on the MBI which resulted in a takeover by fi nancial investor Morten Strømsted

Unisport

Spanish group of fi tness centres

Clearwater International advised the company on the restructuring of fi nancial obligations

O2 Centro Wellness

UK holiday park owner and operator with parks famed for the quality of entertainment and leisure facilities

Clearwater International advised the shareholders of Away Resorts on the sale to LDC

Away Resorts

AARHUS • BARCELONA • BEIJING • BIRMINGHAM • COPENHAGEN • DUBLINLISBON • LONDON • MADRID • MANCHESTER • NOTTINGHAM • PORTO • SHANGHAI