Embed Size (px)

Citation preview

Click to edit Master subtitle style

Unit 5

Capital & Capital Budgeting

Capital forms the base for the business.

Capital, in general does not mean only money. It

may refer to money’s worth also.

Capital has different forms. Creativity,

innovation, new ideas can be considered as one

form of capital.

Some people have ideas but they may not have

money. There are some others who have only

money. The combination for business is to have

both.

INTRODUCTION TO CAPITAL

Capital is defined as wealth, which is created

over a period of time through abstinence of

spend.

Capital is the aggregate of funds used in short

run and long run.

Capital is the total amount of finances required

by the business to conduct its business

operations both in short run and long run.

An economist views capital as the total assets

available with the business.

An accountant views capital as the difference

between the assets and liabilities.

It is the capital that keeps any business going

on.

There are number of instances where the

business is closed for want of capital.

SIGNIFICANCE/ IMPORTANCE OF

CAPITAL

Capital plays crucial role in the modern

production system. It is very difficult to

imagine the production process without

the capital. Capital has a strategic role in

enhancing the productivity.

NEED FOR CAPITALThe business needs for capital are varied. They

are: To promote a business. To conduct business operations smoothly. To expand and diversify. To meet contingencies. To replace the assets. To support welfare programs. To wind up. To pay taxes. To pay dividends and interests

Capital Budgeting Capital Budgeting is the process of

evaluating the relative worth of the long term investment proposals on the basis of their respective profitability.

Long-term investment proposals require larger investment, this requires careful analysis of cash outflows & cash inflows associated with the investment proposals.

Click icon to add table

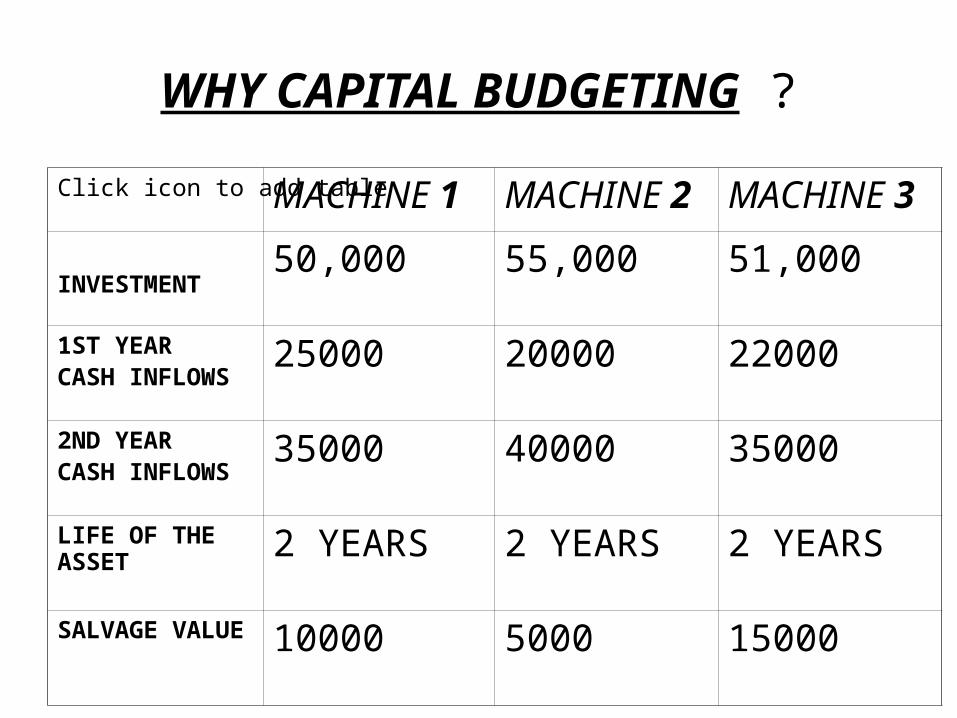

WHY CAPITAL BUDGETING ?

MACHINE 1 MACHINE 2 MACHINE 3

INVESTMENT50,000 55,000 51,000

1ST YEAR CASH INFLOWS

25000 20000 22000

2ND YEAR CASH INFLOWS

35000 40000 35000

LIFE OF THE ASSET

2 YEARS 2 YEARS 2 YEARS

SALVAGE VALUE

10000 5000 15000

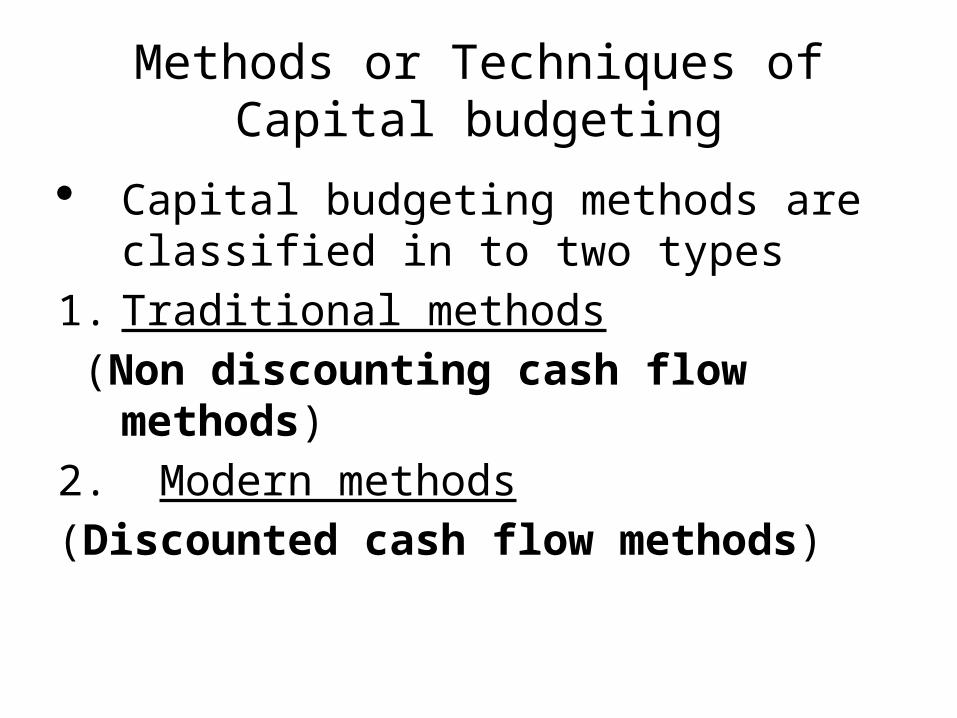

Methods or Techniques of Capital budgeting

Capital budgeting methods are classified in to two types

1. Traditional methods

(Non discounting cash flow methods)

2. Modern methods

(Discounted cash flow methods)

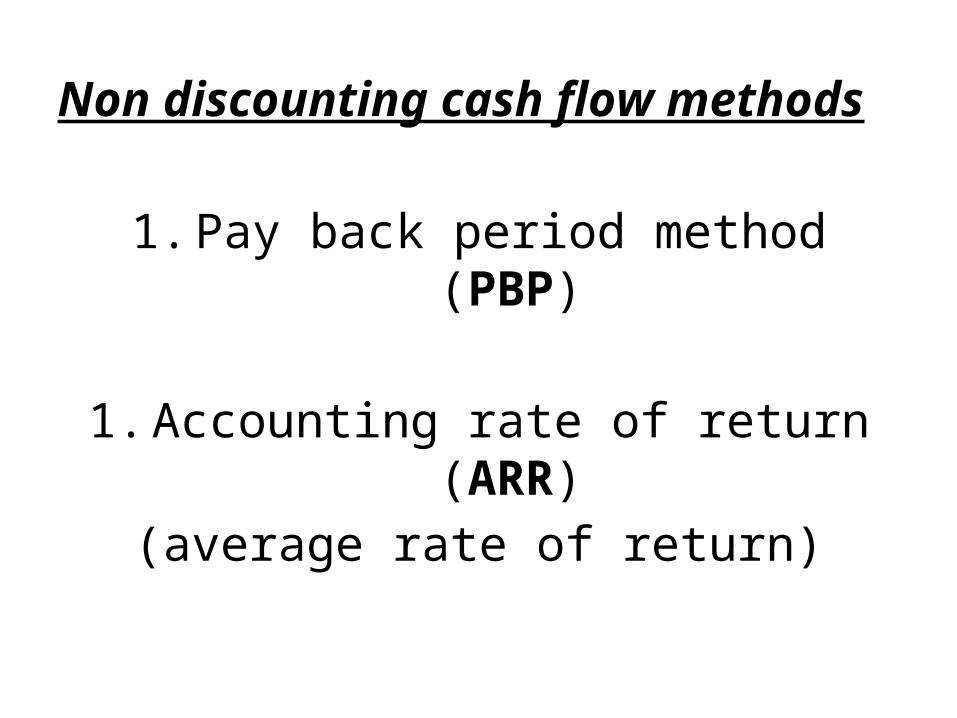

Non discounting cash flow methods

1. Pay back period method (PBP)

1. Accounting rate of return (ARR)(average rate of return)

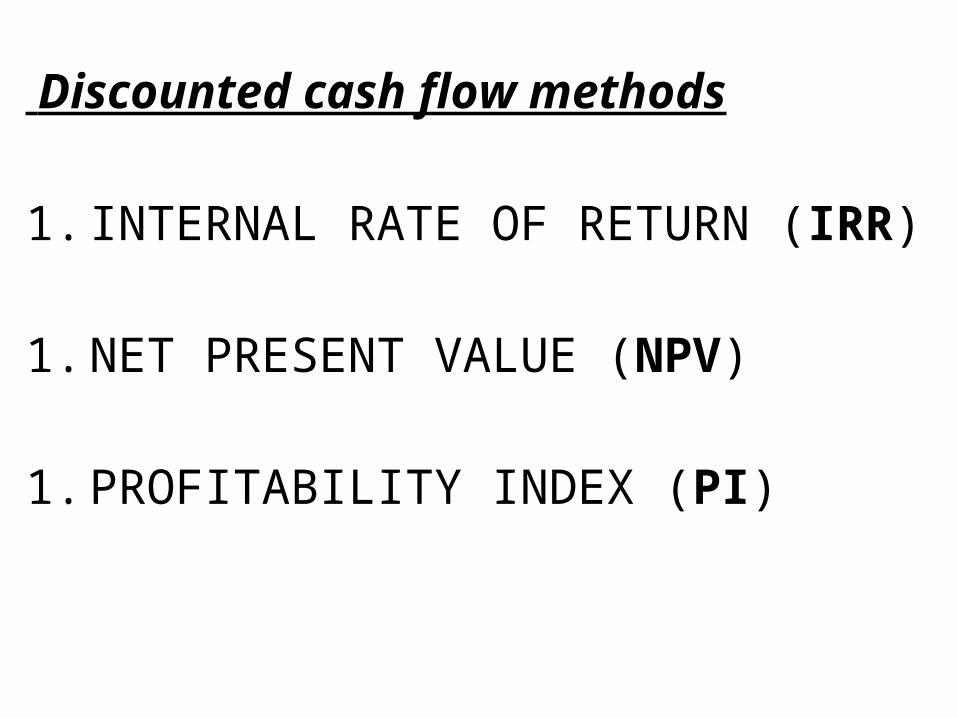

Discounted cash flow methods

1. INTERNAL RATE OF RETURN (IRR)

1. NET PRESENT VALUE (NPV)

1. PROFITABILITY INDEX (PI)

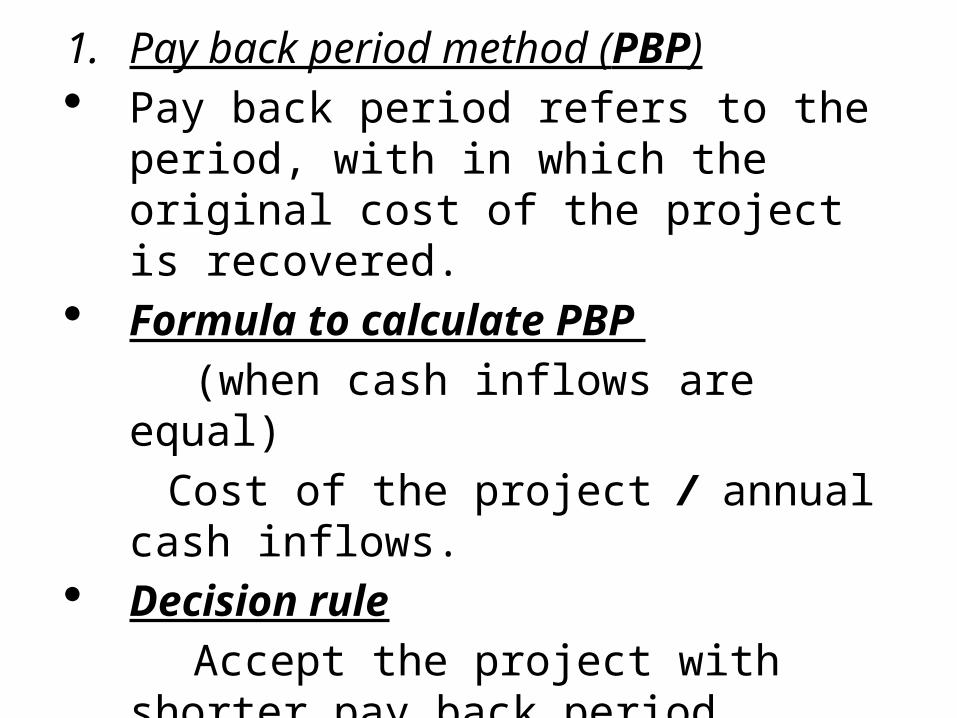

1. Pay back period method (PBP) Pay back period refers to the period,

with in which the original cost of the project is recovered.

Formula to calculate PBP

(when cash inflows are equal)

Cost of the project / annual cash inflows. Decision rule

Accept the project with shorter pay back period.

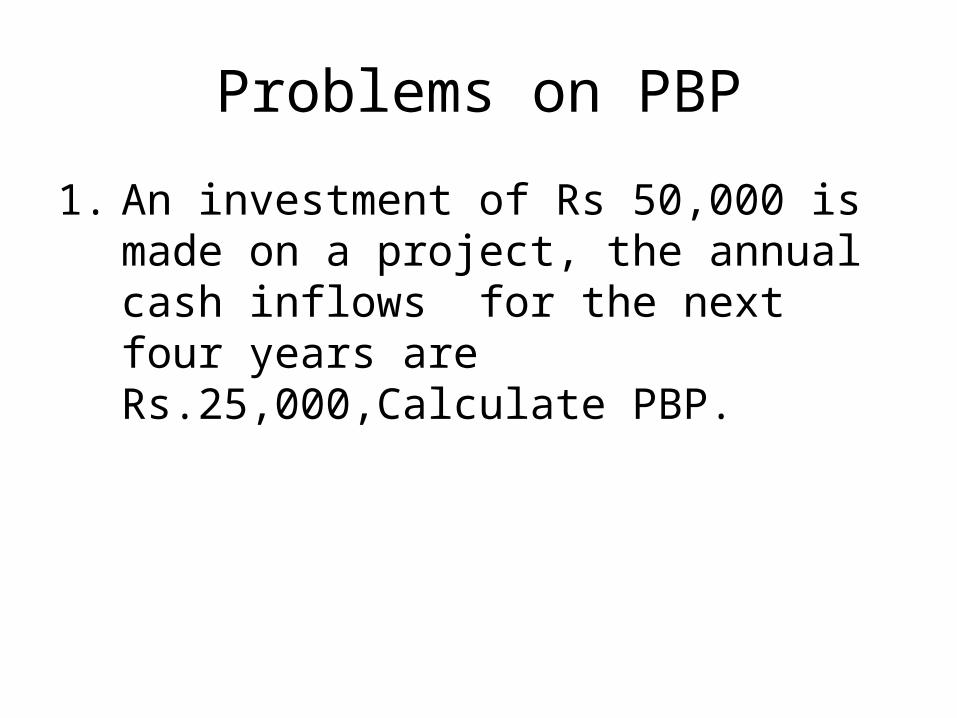

Problems on PBP

1. An investment of Rs 50,000 is made on a project, the annual cash inflows for the next four years are Rs.25,000,Calculate PBP.

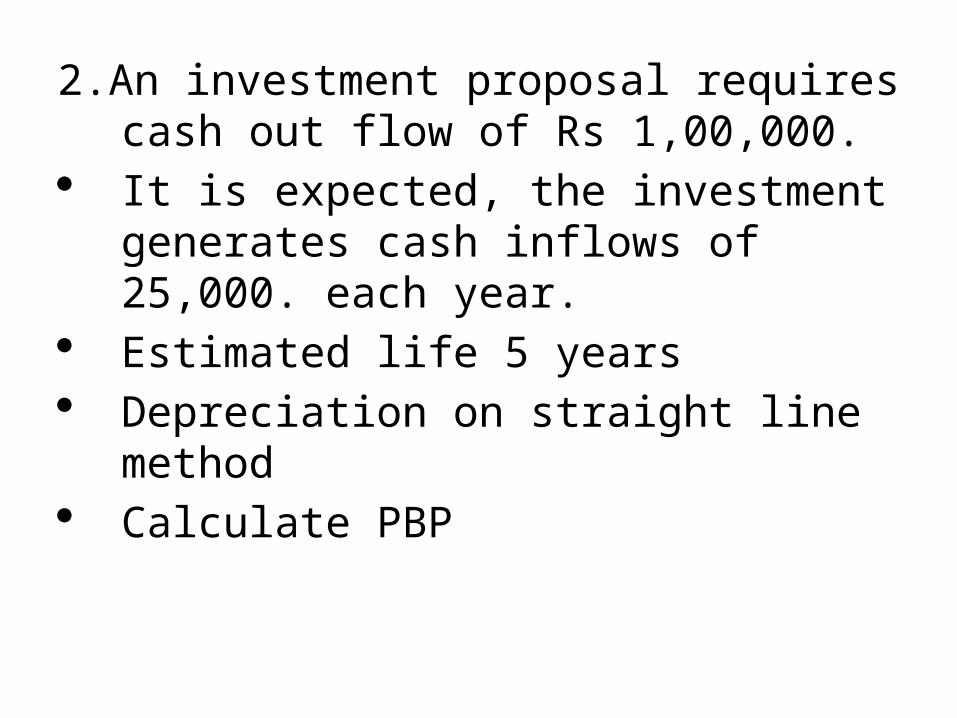

2.An investment proposal requires cash out flow of Rs 1,00,000.

It is expected, the investment generates cash inflows of 25,000. each year.

Estimated life 5 years Depreciation on straight line method Calculate PBP

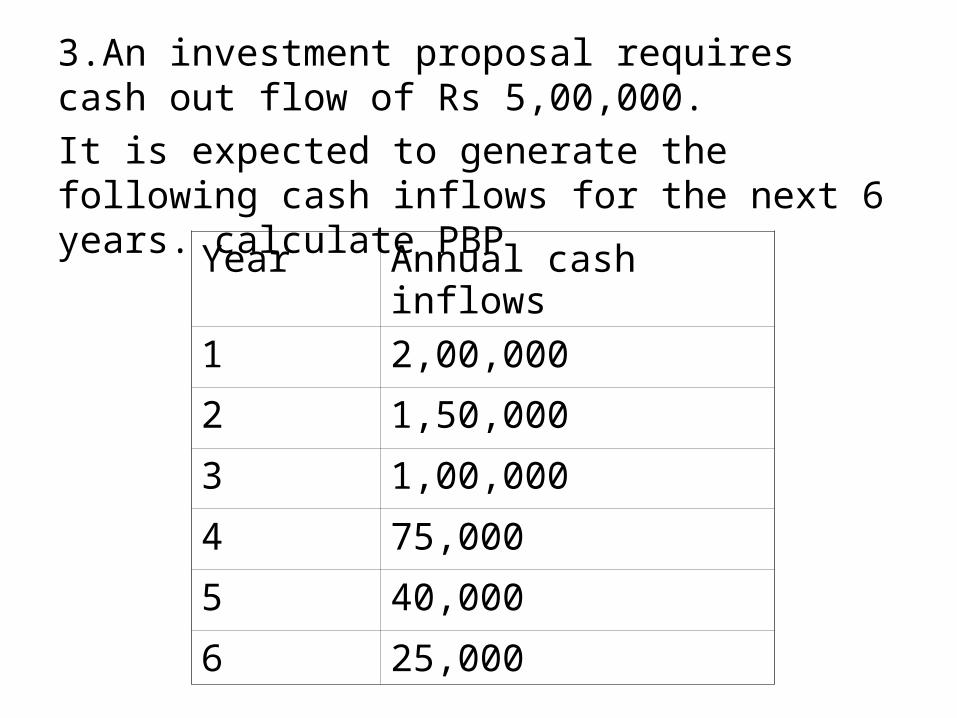

3.An investment proposal requires cash out flow of Rs 5,00,000.

It is expected to generate the following cash inflows for the next 6 years. calculate PBP

Year Annual cash inflows

1 2,00,000

2 1,50,000

3 1,00,000

4 75,000

5 40,000

6 25,000

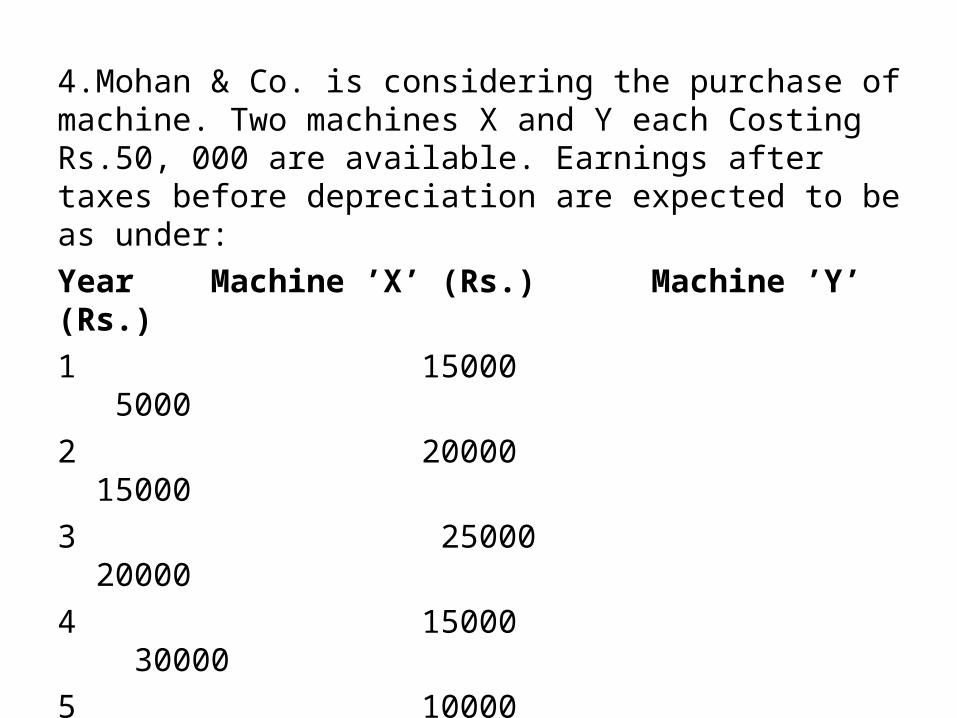

4.Mohan & Co. is considering the purchase of machine. Two machines X and Y each Costing Rs.50, 000 are available. Earnings after taxes before depreciation are expected to be as under:

Year Machine ’X’ (Rs.) Machine ’Y’ (Rs.)

1 15000 5000

2 20000 15000

3 25000 20000

4 15000 30000

5 10000 20000

Estimate the two alternatives according to:

(a) Payback method, and

(b) NPV method a discount rate of 10% is to be used.

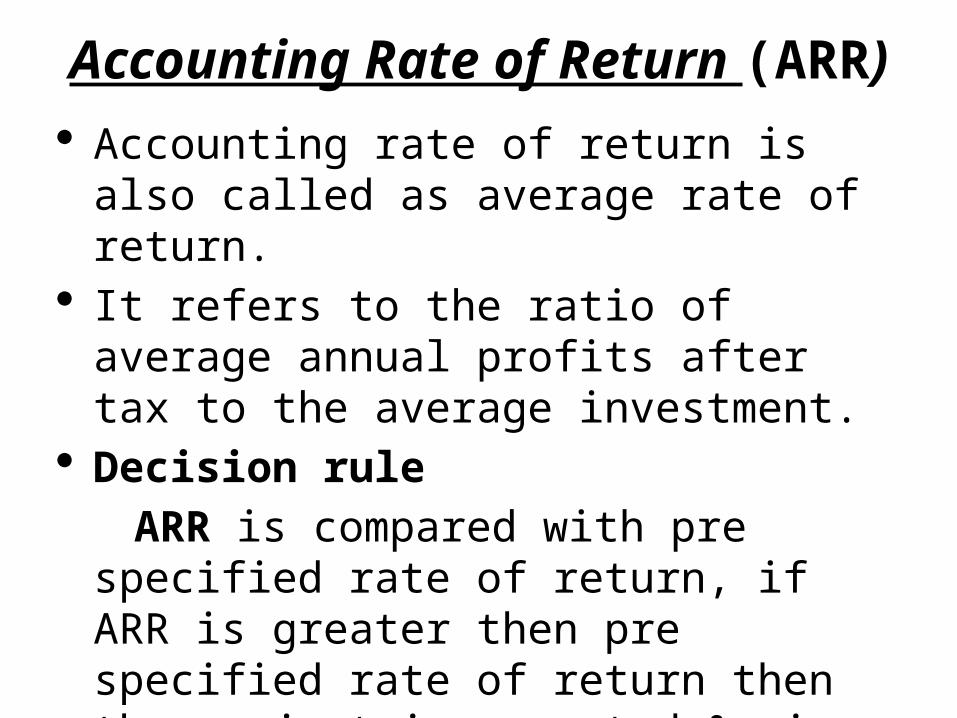

Accounting Rate of Return (ARR) Accounting rate of return is also called as

average rate of return. It refers to the ratio of average annual

profits after tax to the average investment. Decision rule

ARR is compared with pre specified rate of return, if ARR is greater then pre specified rate of return then the project is accepted & vice versa.

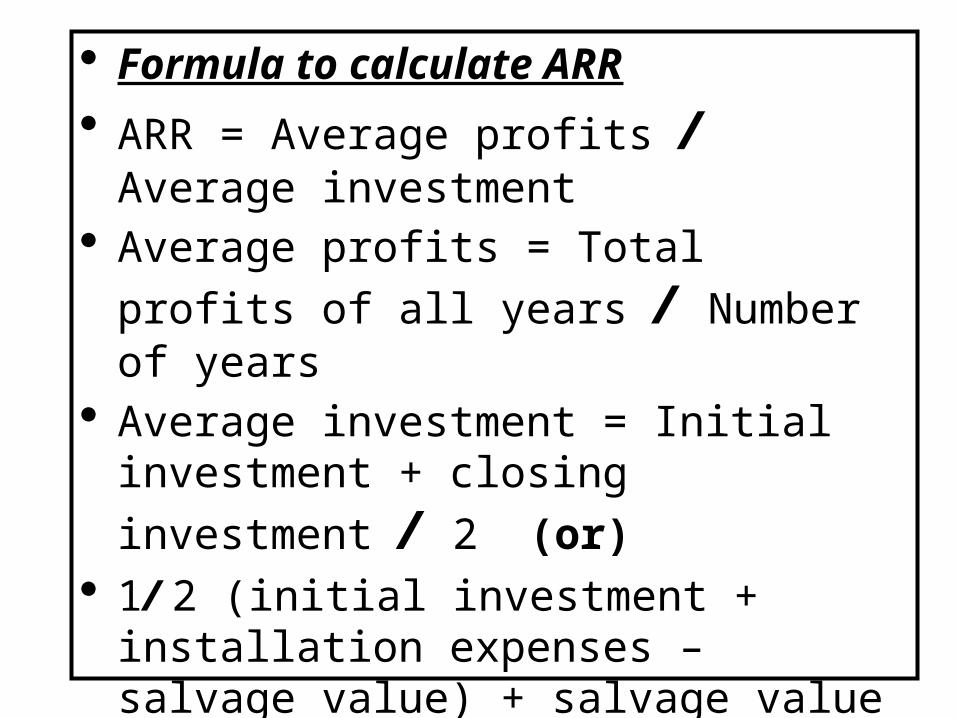

Formula to calculate ARR ARR = Average profits / Average

investment Average profits = Total profits of all

years / Number of years Average investment = Initial investment +

closing investment / 2 (or) 1/ 2 (initial investment + installation

expenses – salvage value) + salvage value

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

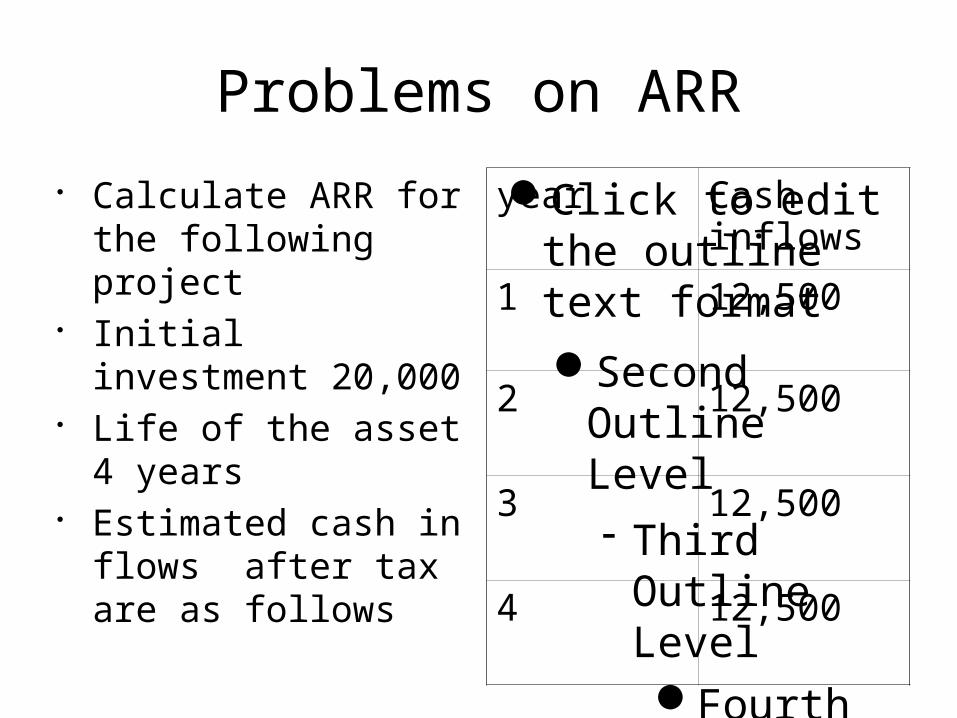

Problems on ARR

Calculate ARR for the following project

Initial investment 20,000

Life of the asset 4 years

Estimated cash in flows after tax are as follows

year Cash inflows

1 12,500

2 12,500

3 12,500

4 12,500

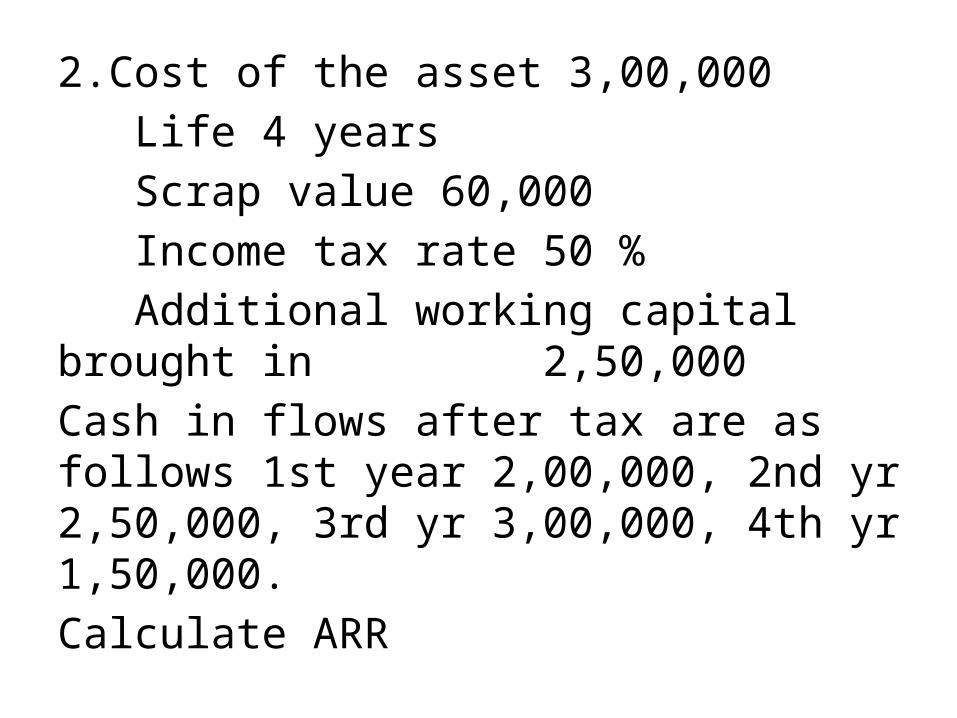

2.Cost of the asset 3,00,000

Life 4 years

Scrap value 60,000

Income tax rate 50 %

Additional working capital brought in 2,50,000

Cash in flows after tax are as follows 1st year 2,00,000, 2nd yr 2,50,000, 3rd yr 3,00,000, 4th yr 1,50,000.

Calculate ARR

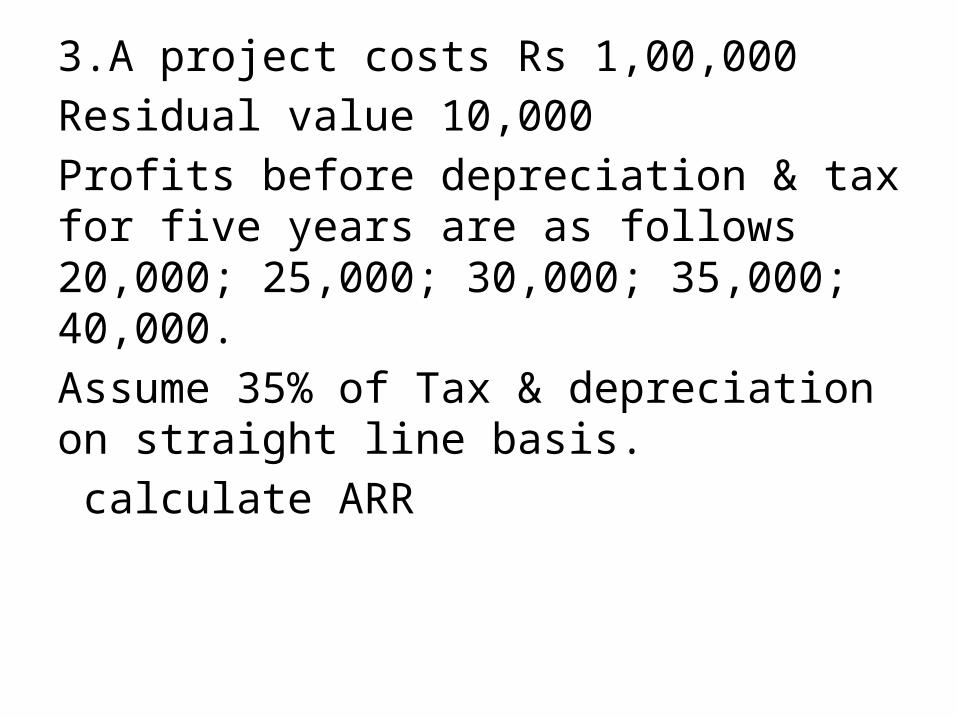

3.A project costs Rs 1,00,000

Residual value 10,000

Profits before depreciation & tax for five years are as follows 20,000; 25,000; 30,000; 35,000; 40,000.

Assume 35% of Tax & depreciation on straight line basis.

calculate ARR

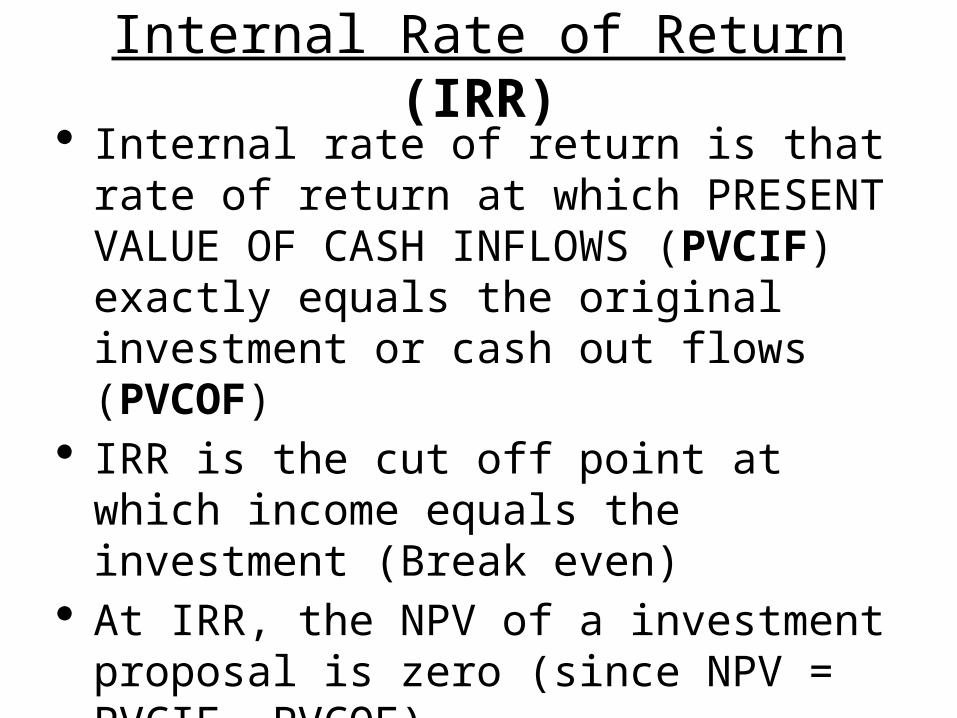

Internal Rate of Return (IRR) Internal rate of return is that rate of return

at which PRESENT VALUE OF CASH INFLOWS (PVCIF) exactly equals the original investment or cash out flows (PVCOF)

IRR is the cut off point at which income equals the investment (Break even)

At IRR, the NPV of a investment proposal is zero (since NPV = PVCIF –PVCOF)

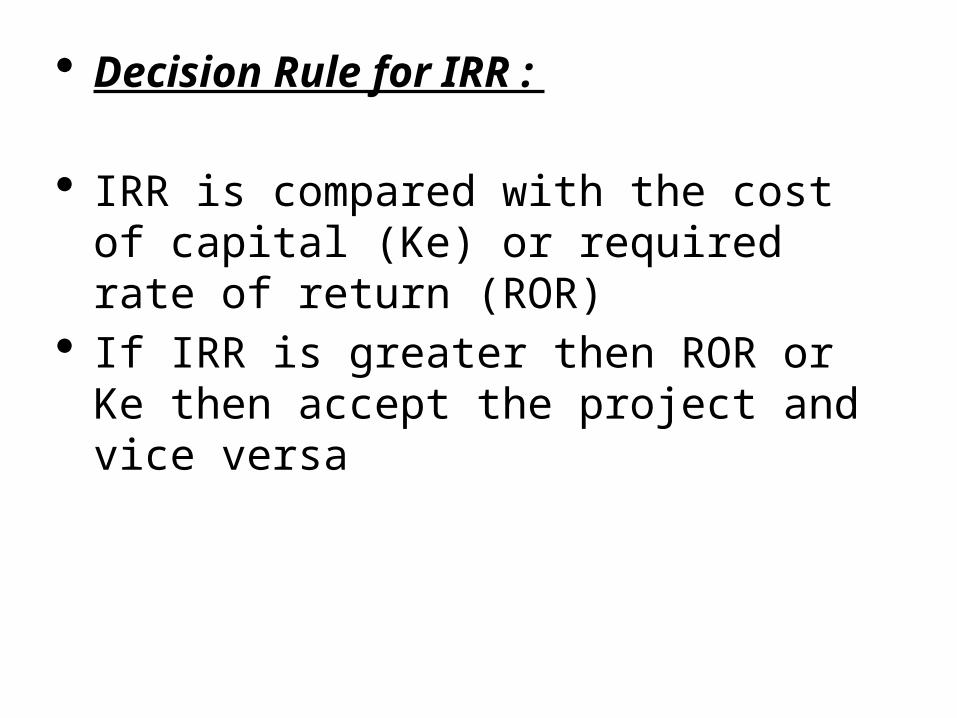

Decision Rule for IRR :

IRR is compared with the cost of capital (Ke) or required rate of return (ROR)

If IRR is greater then ROR or Ke then accept the project and vice versa

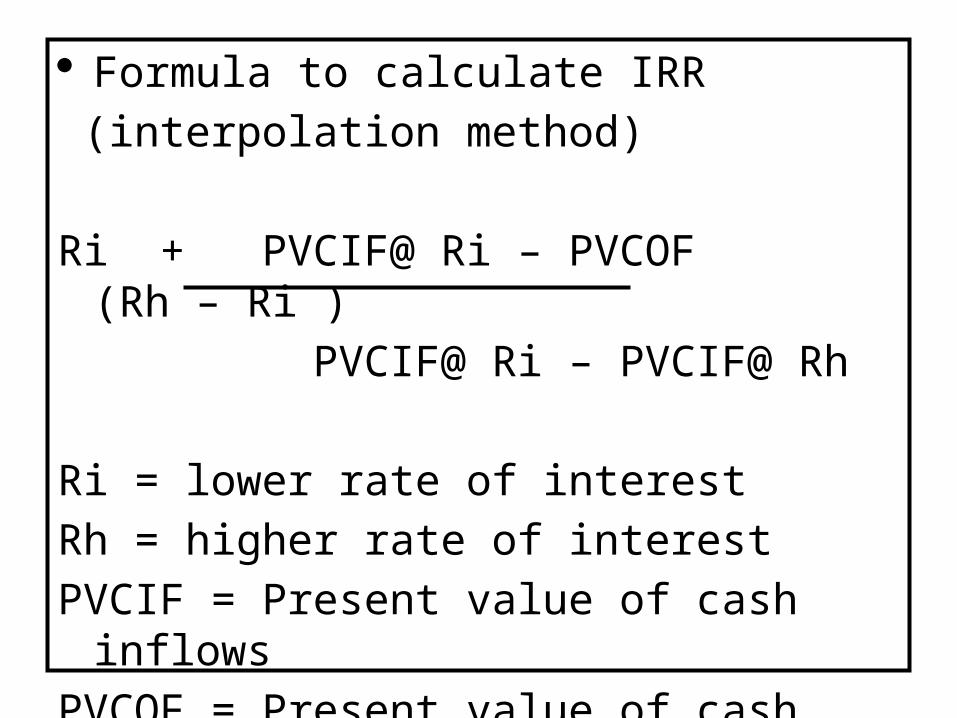

Formula to calculate IRR

(interpolation method)

Ri + PVCIF@ Ri – PVCOF (Rh – Ri )

PVCIF@ Ri – PVCIF@ Rh

Ri = lower rate of interest

Rh = higher rate of interest

PVCIF = Present value of cash inflows

PVCOF = Present value of cash outflows

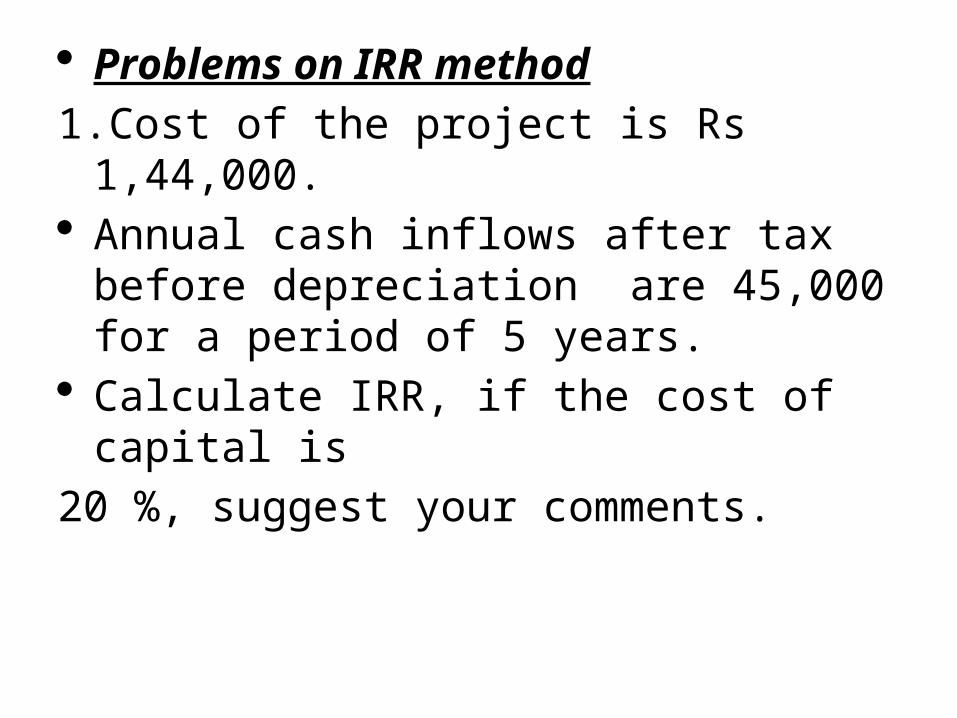

Problems on IRR method

1.Cost of the project is Rs 1,44,000. Annual cash inflows after tax before

depreciation are 45,000 for a period of 5 years.

Calculate IRR, if the cost of capital is

20 %, suggest your comments.

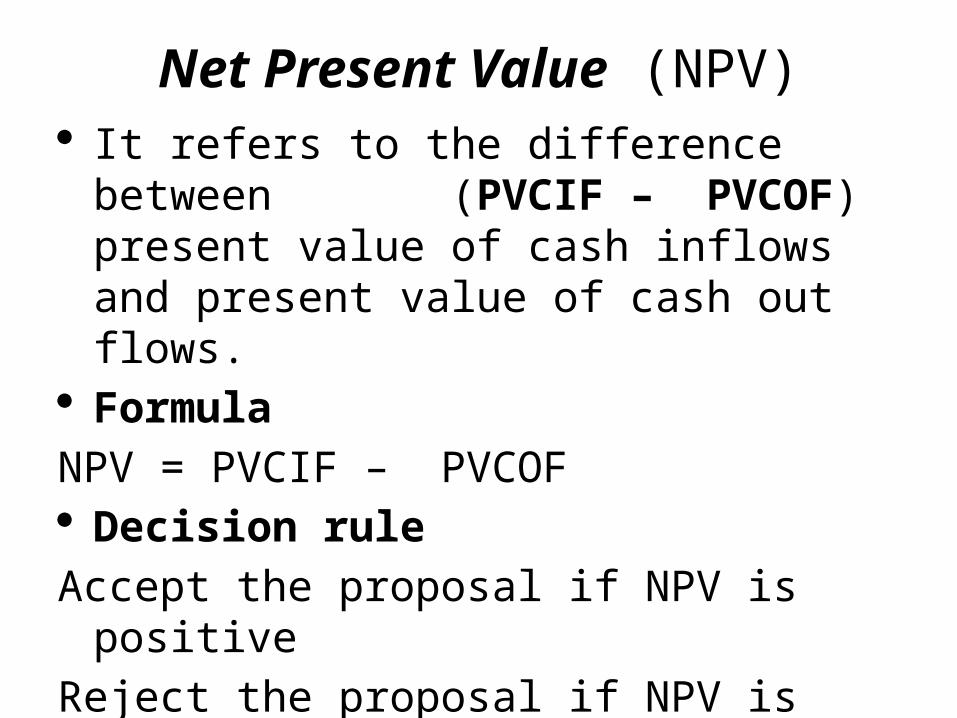

Net Present Value (NPV) It refers to the difference between

(PVCIF – PVCOF) present value of cash inflows and present value of cash out flows.

Formula

NPV = PVCIF – PVCOF Decision rule

Accept the proposal if NPV is positive

Reject the proposal if NPV is negative

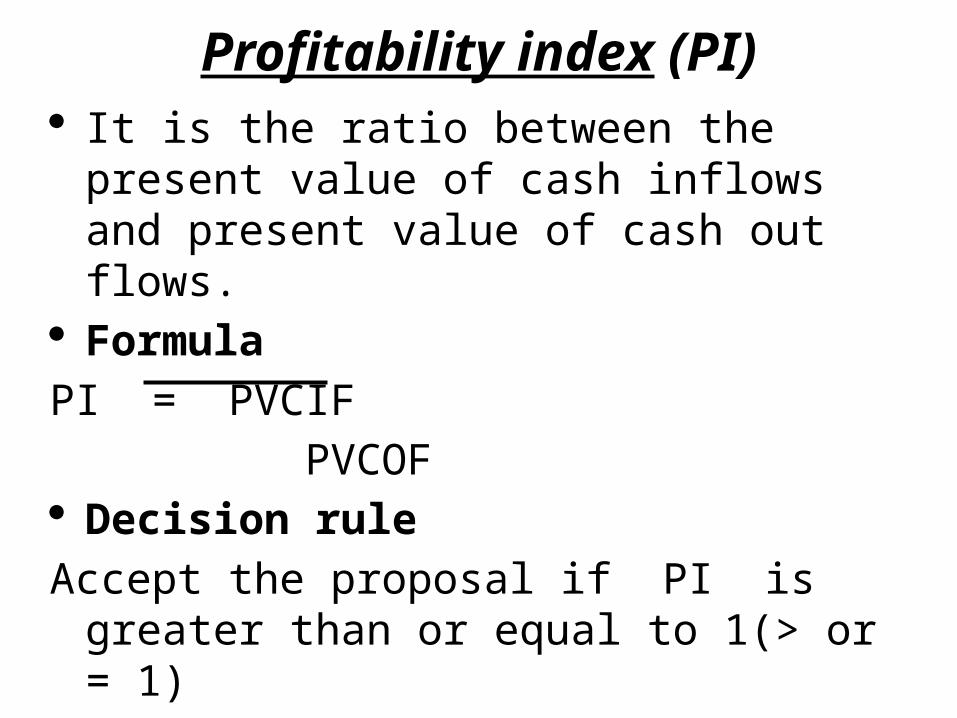

Profitability index (PI) It is the ratio between the present value of

cash inflows and present value of cash out flows.

Formula

PI = PVCIF

PVCOF Decision rule

Accept the proposal if PI is greater than or equal to 1(> or = 1)

Reject the proposal if PI is less than 1(<1)

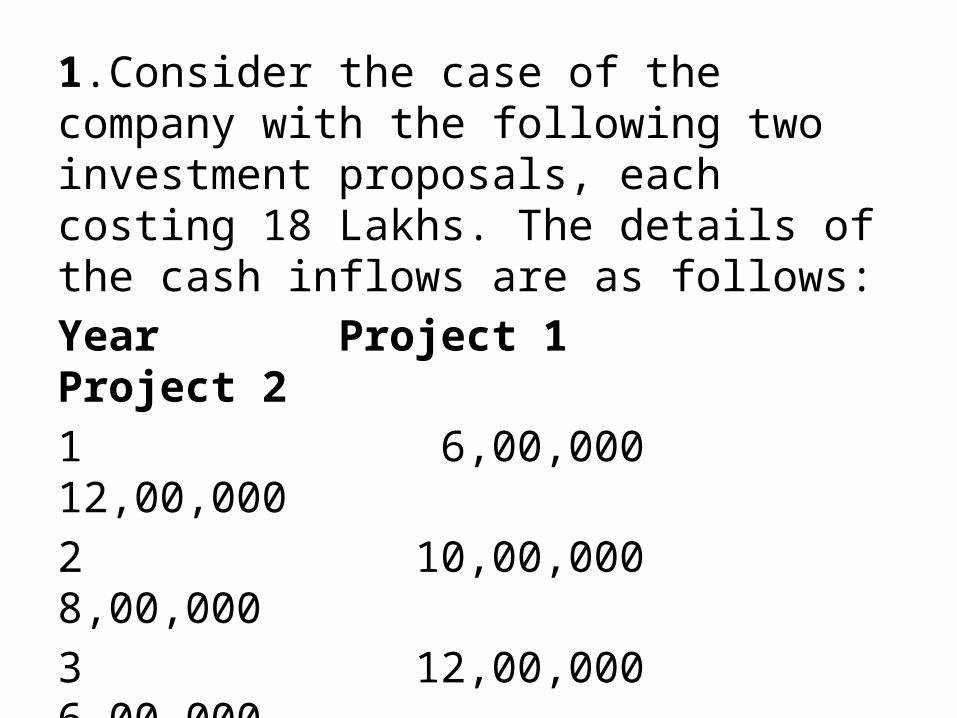

1.Consider the case of the company with the following two investment proposals, each costing 18 Lakhs. The details of the cash inflows are as follows:

Year Project 1 Project 2

1 6,00,000 12,00,000

2 10,00,000 8,00,000

3 12,00,000 6,00,000

The cost of capital is 10% per year. Which one will you choose under NPV method?

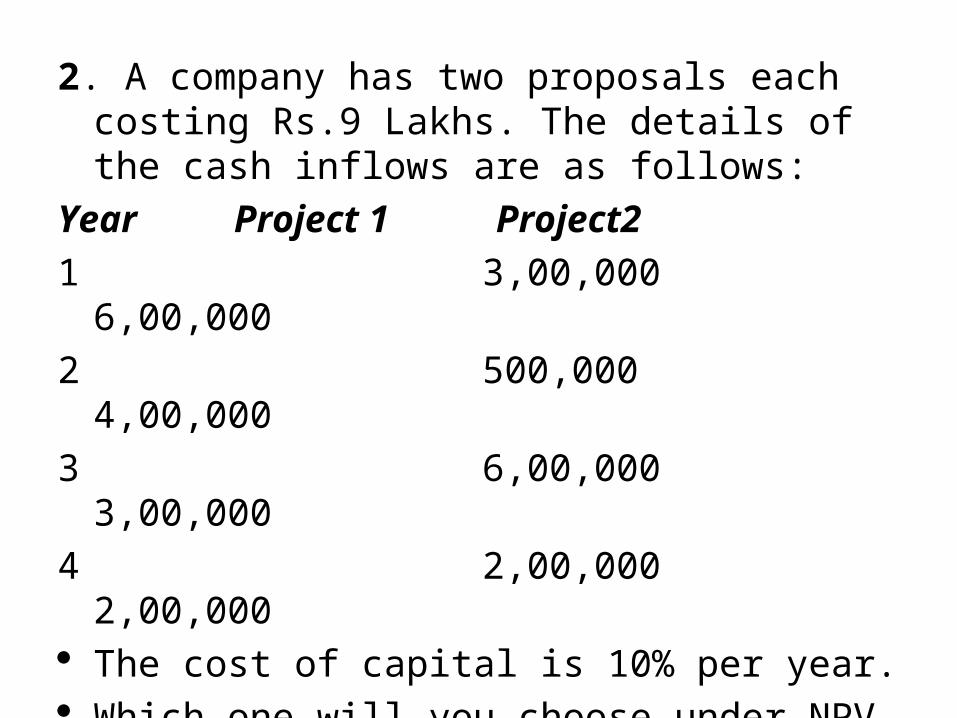

2. A company has two proposals each costing Rs.9 Lakhs. The details of the cash inflows are as follows:

Year Project 1 Project2

1 3,00,000 6,00,000

2 500,000 4,00,000

3 6,00,000 3,00,000

4 2,00,000 2,00,000 The cost of capital is 10% per year. Which one will you choose under NPV method.

Also calculate P I.

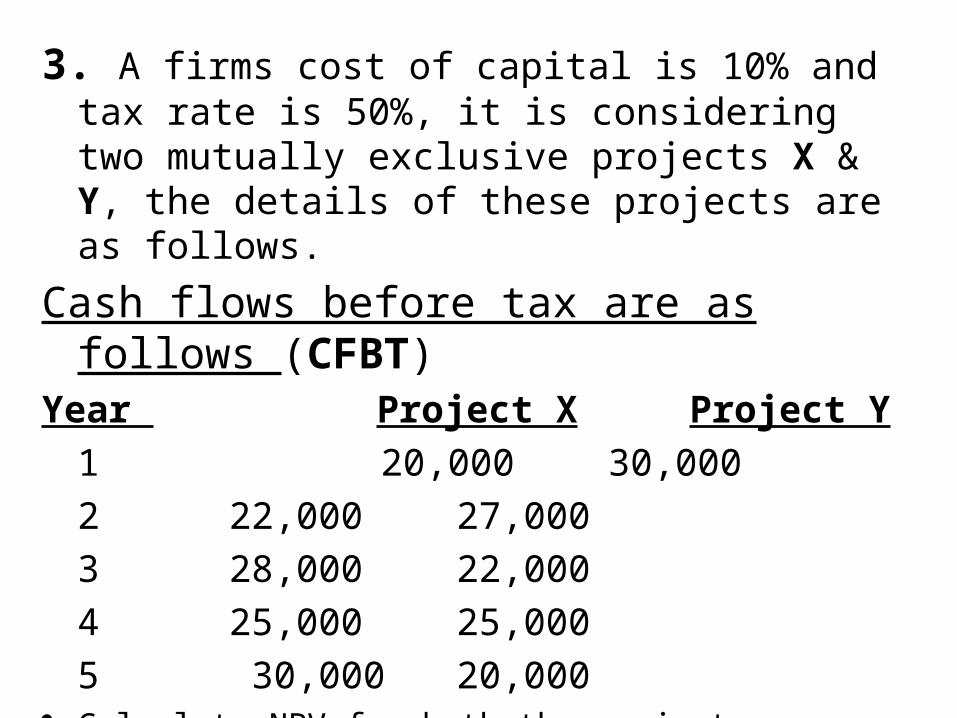

3. A firms cost of capital is 10% and tax rate is 50%, it is considering two mutually exclusive projects X & Y, the details of these projects are as follows.

Cash flows before tax are as follows (CFBT)Year Project X Project Y

1 20,000 30,000

2 22,000 27,000

3 28,000 22,000

4 25,000 25,000

5 30,000 20,000 Calculate NPV for both the projects. Which one will you choose under NPV method.

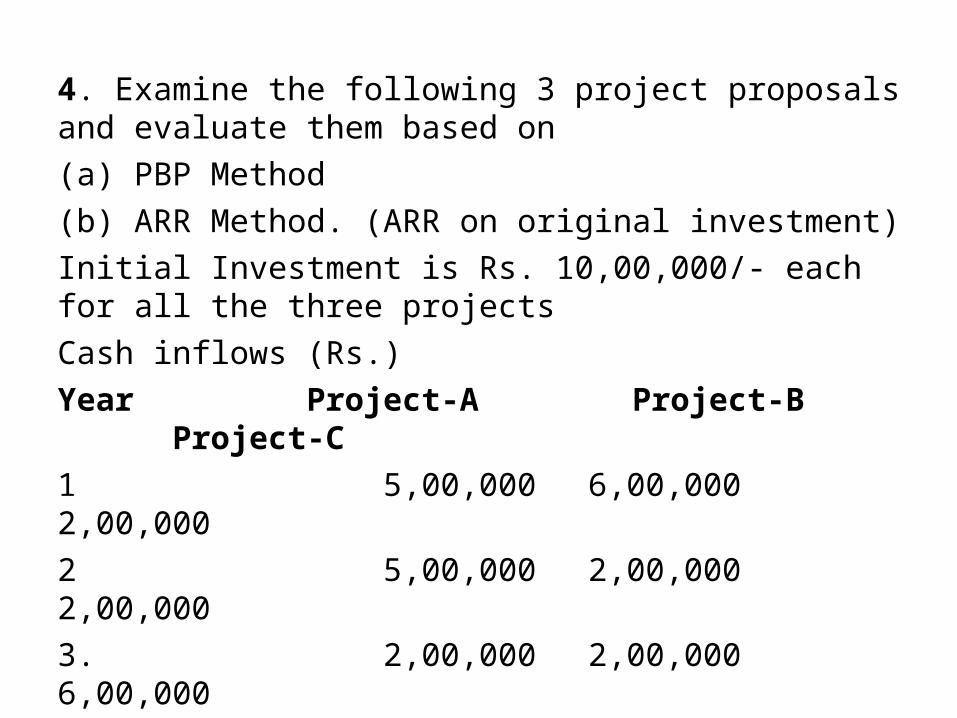

4. Examine the following 3 project proposals and evaluate them based on

(a) PBP Method

(b) ARR Method. (ARR on original investment)

Initial Investment is Rs. 10,00,000/- each for all the three projects

Cash inflows (Rs.)

Year Project-A Project-B Project-C

1 5,00,000 6,00,000 2,00,000

2 5,00,000 2,00,000 2,00,000

3. 2,00,000 2,00,000 6,00,000

4 - 3,00,000 4,00,000 ------

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

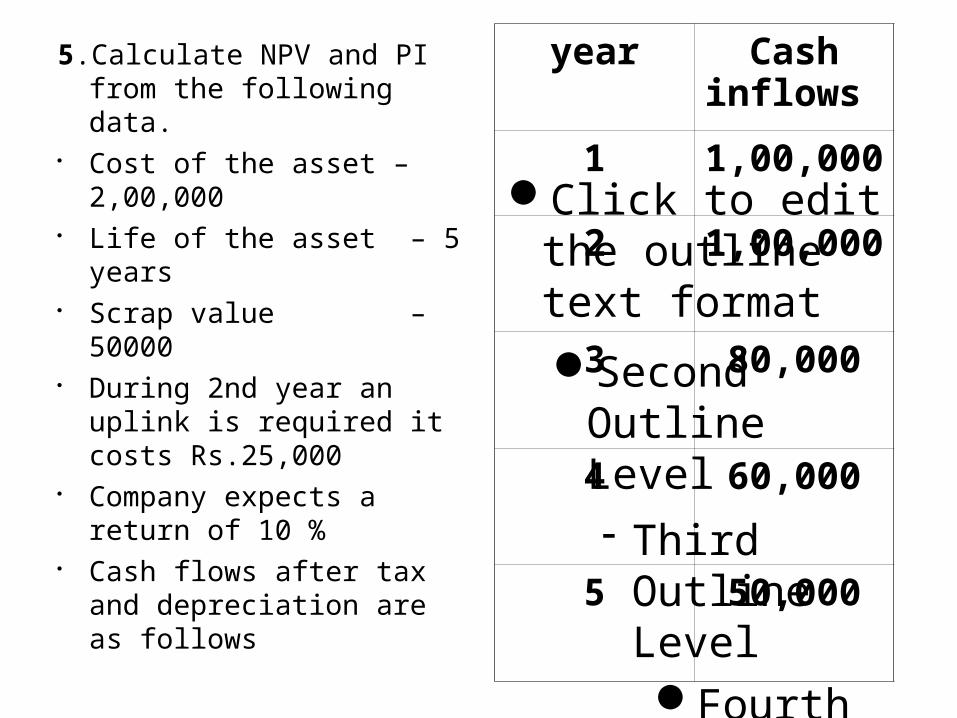

5.Calculate NPV and PI from the following data.

Cost of the asset – 2,00,000

Life of the asset – 5 years

Scrap value – 50000 During 2nd year an uplink

is required it costs Rs.25,000

Company expects a return of 10 %

Cash flows after tax and depreciation are as follows

year Cash inflows

1 1,00,000

2 1,00,000

3 80,000

4 60,000

5 50,000

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

UNIT - VI

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

CAPITAL AND CAPITAL BUDGETING

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Introduction to Capital

It’s a part of Balance Sheet Its Relating to Assets and Liabilities

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

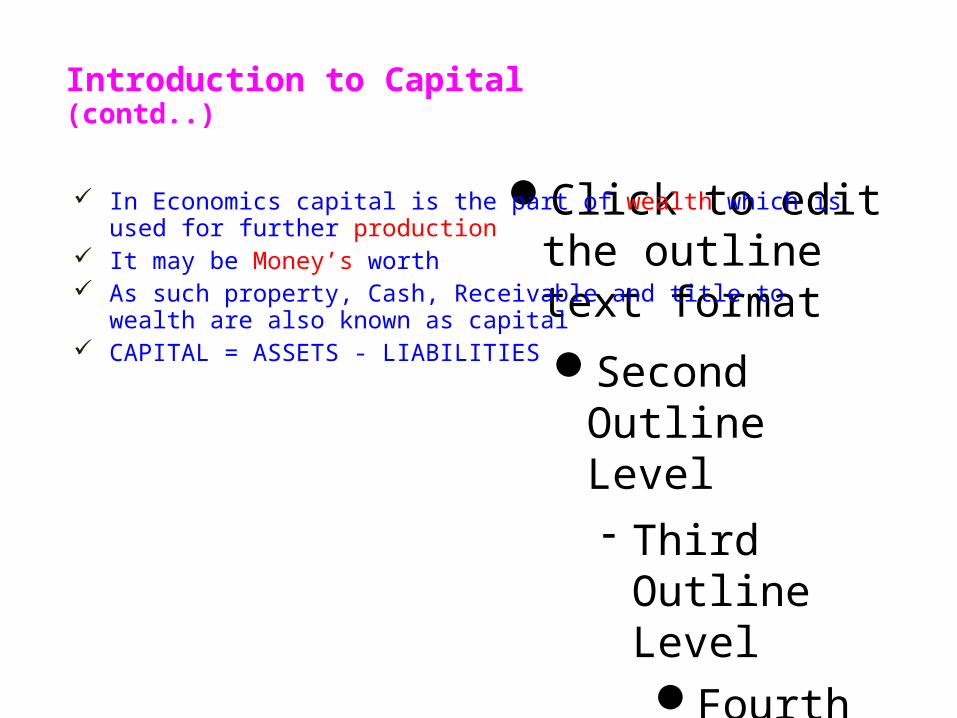

Introduction to Capital (contd..)

In Economics capital is the part of wealth which is used for further production It may be Money’s worth As such property, Cash, Receivable and title to wealth are also known as

capital CAPITAL = ASSETS - LIABILITIES

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Significance / Need of Capital

For promotion of Business For expansion growth diversification of Business For Acquisition & Replacement of Assets For conduction business operations smoothly For payment of taxes For meeting contingencies

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Types of Capital

Fixed Capital Working Capital

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Factors of Fixed Capital

Nature of commodity Size & Scale of the unit Techniques of production Methods of purchasing fixed assets

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Factors of working Capital

Nature of Business Technical & Production cycle Trade & Business cycle foliations Credit policy Profit changes

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Methods of Raising company finance

Issues of Shares Issues of Debentures Retained Earnings Public Deposits Financing through Bonds Institutional financing

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Nature of Capital Budgeting

Capital budgeting is concerned with long term funds Involves heavy expenditure Affecting cost structure High time lag b/w investment & Returns Involves considerable risk

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Scope of Capital Budgeting

Building commutative strengths Determining future destiny of the enterprise Revenue Yielding Best possible utilization of Resources Generating current assists

Click to edit the outline text format

Second Outline Level Third Outline

LevelFourth Outline Level Fifth Outline Level

Sixth Outline Level

Seventh Outline Level

Eighth Outline Level

Ninth Outline LevelClick to edit Master text styles Second level

Third level Fourth level

» Fifth level

Capital Budgeting techniques

Pay Back Period Accounting Rate of Return Net Present Value