Embed Size (px)

Citation preview

IBM GTS Cloud Advisory Services

Cloud services for telecommunications Growth through cloud-ena bled transformation

Contents

1 Introduction: Cloud as an enabler

2 Overcoming telco industry pressures

6 Navigating a continually evolving support and engagement landscape

8 Fueling growth and innovation: The business value of cloud

10 Incorporating cloud into your business strategy

13 Conclusion

14 Recommendations

14 Enlist the right partner to plan and achieve the transformation

Introduction: Cloud as an enablerThinking of cloud solely in technology terms misses a larger point. Cloud can provide enterprises with scale and flexibility that enable more than just improved speed and savings—cloud also enables new, dynamic business models. Cloud can serve as a growth engine for organizations.

Cloud’s initial promise was based largely on its ability to reduce IT costs. More recently, enabled by its greater speed and agility, cloud has emerged as a driver of business growth and innovation. Companies use cloud to reinvent customer relationships, derive deep insights from data and collaborate more effectively.

The IBM Institute for Business Value recently conducted a global study on the challenges C-level executives face in a rapidly changing business environment. The study revealed that these executives consider technol-ogy the most important external force shaping their enterprises’ futures. The study also describes “Pacesetter” companies that are gaining competitive advantage over their rivals by deploying cloud on a broad scale. These companies are seeing high financial returns from cloud initiatives.1 Transformative cloud-enabled technologies such as social, mobile and big data/analytics are central to the equation.

IBM GTS Cloud Advisory Services

2

Cloud drives its transformative potential from:

Speed. Cloud is designed to increase the speed of innovation, enabling organizations to be more responsive. It allows for faster application development through reusing building blocks that standardize system interaction. And, it can deliver computing power on demand, allowing new services to achieve quicker market penetration and real-time improvements.

Empowerment. Cloud fosters employee empowerment. It pro-vides business users the tools they need, where and when they need them. Developers, freed up from technical challenges, can focus on new ways to engage with customers. Cloud enables IT to shift focus from maintaining the infrastructure to driving innovation.

Economics. Cloud helps improve economics by providing computing power and tools—when and in the amount needed—shifting costs from fixed to variable. Companies can realize sav-ings through automation and standardization, and can redeploy resources to strategic efforts.

Cloud is no longer simply a cost takeout play but has emerged as a strategic growth engine for business. Although cloud can provide substantial productivity and flexibility enhancements, it is not an IT cure-all. Organizations must think carefully about which cloud solutions make sense given their business needs, current IT environment and regulatory requirements.

Telecommunication (telco) C-level executives foresee major changes in their offerings, enforced by shifts in the competitive landscape. This paper introduces cloud as a business enabler in the context of current telco trends. We emphasize building new sources of revenue by introducing appealing public, private and hybrid cloud offerings to large business and growth markets. To take full advantage of cloud’s transformational potential, tel-cos should also examine how cloud can transform their internal operations, customer relationships and industry value chains.

Overcoming telco industry pressures

Revenue and subscriber growth for Communications Service Providers (CSPs) have slowed. At the same time, CSPs are forced to invest in their core networks as consumers drive demand for Over-The-Top (OTT) services and revenues shift to new competitors. For example, Google, FaceBook, Microsoft/Skype and Apple enjoy huge market valuations, while CSPs bear the costs of delivering their services.

CSPs face immense pressure to reduce their costs, increase agility and drive new sources of revenue. Cloud can play an important role in achieving these goals. Internally, cloud simpli-fies IT infrastructure and reduces costs, facilitating rapid proto-typing and innovation. This enables CSPs to easily test and integrate partner solutions into their own systems, bringing new offerings to market more quickly.

CSPs, as providers of connecting networks, hold a unique advantage over other players in the cloud marketplace. They already connect most businesses and homes in the devel-oped world, with associated billing relationships. This built-in access creates an unparalleled selling position. CSPs can harness these existing relationships to sell, refine and enhance cloud offerings. For example, telcos can improve their provisioning proficiency by using cloud’s reduced cycle time for high volume data streaming to residential and business customers.

But cloud adoption still faces challenges. Compatibility issues with legacy network infrastructure and applications, regulatory issues, security and governance all cause concern. Even as value-added cloud services come to market, the path to profitability is not always clear.

IBM GTS Cloud Advisory Services

3

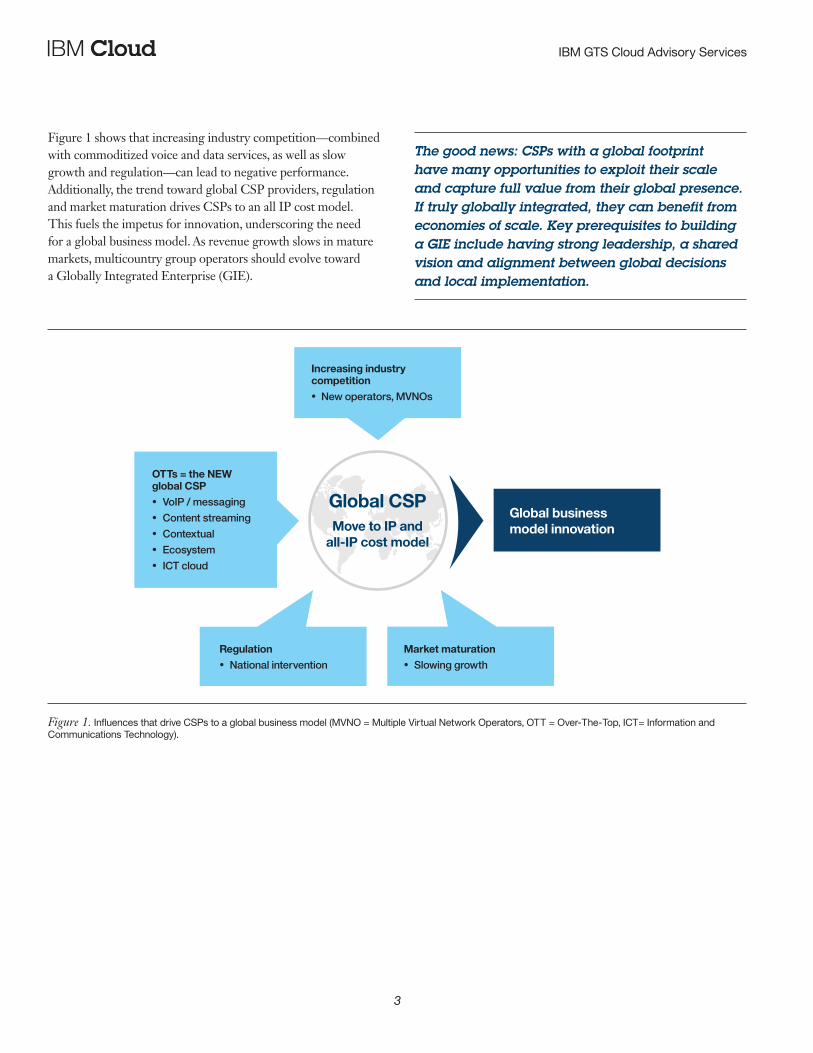

Figure 1 shows that increasing industry competition—combined with commoditized voice and data services, as well as slow growth and regulation—can lead to negative performance. Additionally, the trend toward global CSP providers, regulation and market maturation drives CSPs to an all IP cost model. This fuels the impetus for innovation, underscoring the need for a global business model. As revenue growth slows in mature markets, multicountry group operators should evolve toward a Globally Integrated Enterprise (GIE).

Global CSPMove to IP and

all-IP cost model

OTTs = the NEWglobal CSP• VoIP / messaging• Content streaming• Contextual• Ecosystem• ICT cloud

Increasing industry competition• New operators, MVNOs

Global businessmodel innovation

Market maturation• Slowing growth

Regulation• National intervention

Figure 1. Influences that drive CSPs to a global business model (MVNO = Multiple Virtual Network Operators, OTT = Over- The- Top, ICT= Information and Communications Technology).

The good news: CSPs with a global footprint have many opportunities to exploit their scale and capture full value from their global presence. If truly globally integrated, they can benefit from economies of scale. Key prerequisites to building a GIE include having strong leadership, a shared vision and alignment between global decisions and local implementation.

IBM GTS Cloud Advisory Services

4

Embracing the telco market revolutionThe telecom industry has dramatically evolved due to market saturation, support considerations, front office operations, business service strategy, consumer preferences, and regulatory requirements for the handling of personal information. To trulytransform, CSPs must embrace these market changes:

●● The communications business is quickly morphing into the Cloud Information Technology (CIT) business.– Cloud is mandatory for competitive enterprise hosting.– The creation of markets for Infrastructure as a Service

(IaaS), Platform as a Service (PaaS) and Software as a Service (SaaS) fills a critical need for new revenue sources.

●● Telcos differentiate their cloud services by bundling them with communications services.– Enterprises implement “Bring–Your-Own-Device”

programs and port applications to better secure clouds.– Telcos crowd source application development for faster

service innovation.– Companies expose their network service application

programming interfaces (APIs) to application developers, generating service demand.

●● The Internet of Things is a huge new driver for data.Optimum data monetization comes from delivering analytics for both telco-owned and subscriber-owned data streams.●● Cloud must play multiple roles in a complex telco

ecosystem, however some challenges exist.– Profitability. IaaS margins are thin, so CSPs need both

efficient IaaS delivery and consumption-based business models.

– Dynamic portfolio. Attractive marketplaces offer applications that are both “table stakes” and competitive differentiators.

– Rapid growth. Telcos rapidly scale offerings to the long tail of the global market (long tail meaning smaller, niche markets as opposed to high volume markets).

– Hybrid clouds. Telcos and their subscribers need to balance their workloads across security-rich, private clouds and commodity-priced public cloud services.

Becoming a Globally Integrated Enterprise

As the hyper growth period for mobile ends and competi-tion intensifies, many global CSPs experience reduced revenue and profit growth. Yet they also have a unique opportunity to improve their global integration to drive the synergies necessary for cost savings and growth.2

A single globally integrated technology delivery model should address public clouds for the provider, private clouds for data center and hybrid clouds to bridge the two. The goal is to optimize global hosting in strategic data cen-ters. This requires end- to- end IT service management and IT governance to standardize and consolidate IT platforms.

A GIE has:

●● Rationalized support functions to enable economies of scale

●● An optimized global footprint●● Strong governance, driving continuous improvement●● A broad approach to consolidation ●● Intelligence embedded into operations A GIE can:

●● Use global value chains●● Respond more quickly to changing markets●● Continuously transform to deliver productivity gains●● Apply greater focus on strategic initiatives3

IBM GTS Cloud Advisory Services

5

Driving toward synergies and global integrationSaturated markets increase pressure on CSPs to reduce cost and seek synergies. Arresting this decline and returning to margin growth is the critical industry call to action. Otherwise, how long will shareholders accept margin drops before they pull their funds, triggering industry upheaval?

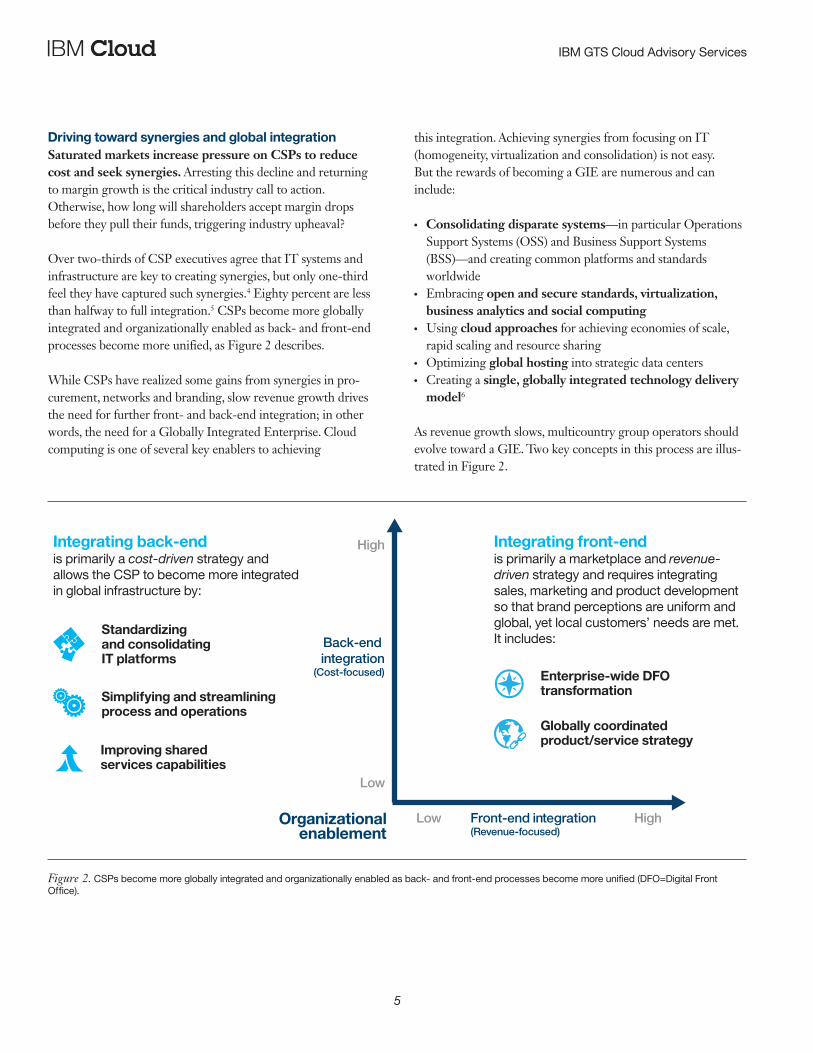

Over two-thirds of CSP executives agree that IT systems and infrastructure are key to creating synergies, but only one-third feel they have captured such synergies.4 Eighty percent are less than halfway to full integration.5 CSPs become more globally integrated and organizationally enabled as back- and front-end processes become more unified, as Figure 2 describes.

While CSPs have realized some gains from synergies in pro-curement, networks and branding, slow revenue growth drives the need for further front- and back-end integration; in other words, the need for a Globally Integrated Enterprise. Cloud computing is one of several key enablers to achieving

Figure 2. CSPs become more globally integrated and organizationally enabled as back- and front-end processes become more unified (DFO=Digital Front Office).

Integrating front-endIntegrating back-end

Enterprise-wide DFOtransformation

Standardizingand consolidating IT platforms

Simplifying and streamlining process and operations

Improving shared services capabilities

Globally coordinated product/service strategy

is primarily a marketplace and revenue-driven strategy and requires integrating sales, marketing and product development so that brand perceptions are uniform and global, yet local customers’ needs are met.It includes:

is primarily a cost-driven strategy and allows the CSP to become more integrated in global infrastructure by:

Front-end integration(Revenue-focused)

Back-end integration

(Cost-focused)

Organizationalenablement

High

High

Low

Low

this integration. Achieving synergies from focusing on IT (homogeneity, virtualization and consolidation) is not easy. But the rewards of becoming a GIE are numerous and can include:

●● Consolidating disparate systems—in particular Operations Support Systems (OSS) and Business Support Systems (BSS)—and creating common platforms and standards worldwide

●● Embracing open and secure standards, virtualization, business analytics and social computing

●● Using cloud approaches for achieving economies of scale, rapid scaling and resource sharing

●● Optimizing global hosting into strategic data centers●● Creating a single, globally integrated technology delivery

model6

As revenue growth slows, multicountry group operators should evolve toward a GIE. Two key concepts in this process are illus-trated in Figure 2.

IBM GTS Cloud Advisory Services

6

As organizations embark upon their GIE journey, they should keep the fundamentals of back-end and front-end integration in mind. The extent to which a CSP integrates both its back- and front-end service capabilities often correlates to the degree of global integration achieved:

●● Back-end integration is a cost-driven strategy that allows the CSP to integrate into the global infrastructure by standardizing and consolidating IT platforms, simplifying and streamlining processes and operations, and improving shared services capabilities.

●● Front-end integration is primarily a marketplace and revenue-driven strategy that requires integrating sales, mar-keting and product development so that brand perceptions are uniform and global, yet local customer needs are met. It includes enterprise-wide Digital Front Office (DFO) transformation and a globally coordinated product and service strategy.7

Navigating a continually evolving support and engagement landscapeCreating globally integrated support functions for centralized services such as HR, finance and payroll enables breakthrough cost savings by:

●● Decreasing incompatible or inefficient support functions●● Driving continuous improvement based on shared GIE

principles●● Reducing duplication of activities●● Facilitating best practice sharing and process

standardization●● Reducing support services spending by deploying the right

skills at the right place at the right costs

The customer support landscape is changing as well. Consumers today expect to help themselves before contacting their provider, but they will engage with providers for other reasons. For exam-ple, 84 percent of consumers said they’re willing to provide feedback to help CSPs make improvements.8

Even so, word of mouth and social media now dominate as preferred channels for CSP product and service applications. Consumers prefer to gather information about CSPs from family or friends instead of email, retail stores and shopping portals.

Transforming the Digital Front Office into a unified global experienceTransforming your enterprise-wide DFO into a streamlined, automated digital space will result in reduced IT/physical store/ care costs and one unified global experience. A CSP DFO in the cloud supports people regardless of location and provides a consistent level of customer service, self-care, shopping, customer experience, and more. CSPs should:

●● Create one global brand experience by converging marketing policies, product portfolios, care policies, and look and feel

●● Construct a DFO for customers and digital Business- to-Business (B2B) interface for partners, suppliers, and others

●● Design an integrated consumer approach by enabling multichannel management

●● Allow the addition of country-specific policies●● Align the global sales force through a common

front-office experience

IBM GTS Cloud Advisory Services

7

The emergence of mobile: Accessing new communication channels

The rapid rise of social networking, instant messaging,microblogs, Internet video, email and other OTT applica-tions has driven new communication channels. (As well, these channels provide venues for disgruntled CSP con-sumers to vent, often excluding CSPs from the dialogue.) The popularity of OTT apps like WhatsApp, WeChat,Facetime and Skype siphon conventional messaging and voice calls away from CSPs—a trend in both mature and emerging markets.9

Users often access these applications over fixed broad-band (including home WiFi). In fact, 73 percent of global Internet users are fixed broadband consumers. But mobile broadband is catching up fast. In emerging markets, 60 per-cent of people with Internet access use mobile broadband (for example, GPRS, 3G, 4G) at least once daily. Mobile broadband is the primary medium for those with Internet access in Indonesia, Nigeria and Kenya—as well as for users under age 25 in China and India.10

Stimulating consumer engagement through social media

The power of social media in the telco industry is formidable. For example, Verizon Wireless repealed its planned $2 online telephone payment fee within 24 hours of announcement in response to online petitions.11 As well, O2 offered compensation to hundreds of thousands of customers when a network failure created a more than 24- hour outage in 2012.12 Customers were unable to send or receive calls, texts, or access data, and they flocked to social media to express their anger.

Today’s consumers increasingly share negative experiences in online forums or discussion groups, and post ratings or share experiences via other social media. Unfortunately, CSPs are often excluded from these conversations. One out of five consumers will always or often post a negative comment online (21 percent) or complain on social media 20 percent).13 In fact, 38 percent of consumers do not even contact their provider when they have negative experiences.14

To better manage customer satisfaction, CSPs should exploit social networking as part of their marketing strategy and integrate digital and physical channels to better interact with their customers. Specifically, they should:

●● Become more proactive in understanding service issues●● Make call centers more consumer friendly●● Monitor social networks to understand and respond to

sources of dissatisfaction●● Offer incentives that encourage consumers to recommend

them to others●● Turn word-of- mouth and social media to their advantage by

targeting key influencers with appropriate messaging

By embracing a variety of channels, including social networking, CSPs can better connect with customers, engaging them in collaborative modes. This can drive increased customer loyalty and cultivate consumer advocates who may share positive experiences, and possibly even reverse the negative impact of antagonists.

CSPs can also negotiate with consumers about sharing their personal information with third parties. For example, CSPs can motivate customers to share such data by offering reduced pricing on higher- value products or services. In addition to com-plying with regulatory requirements for controlling personal sensitive information (PSI), CSPs should be upfront about how they gather and use this information. If handled with finesse, CSPs can use this sensitive realm to build goodwill with their customers.

IBM GTS Cloud Advisory Services

8

Fueling growth and innovation: The business value of cloudIBM’s Global C-Suite Study found business leaders are increas -ingly aware of cloud’s business value. Over the next three years, cloud’s strategic importance to business users is expected to more than double from 34 percent to 72 percent.15

Pacesetters, organizations with broad cloud deployments, realize 1.9 times higher revenue growth and 2.4 times higher gross profit than their more cautious peers. These companies are:

●● 136 percent more likely to use cloud to reinvent customer relationships

●● 170 percent more likely to use cloud extensively for analytics●● 79 percent more likely to use cloud for collaboration and

expertise16

Pacesetters are also way ahead of their peers with more robust cloud strategies. They are almost 400 percent more likely to have an enterprise-wide cloud strategy and 83 percent more likely to use hybrid cloud to capitalize on both public and private cloud strengths.17

Capitalizing on cloud’s transformative potential requires adopting differentiators to drive exponential value down the road, such as:

●● Standardized cloud builds that use automation to deliver fully functional private clouds in hours or days

●● IaaS compute and storage models to provide rapid, security- rich access to virtual environments and enable effective data storage, management and protection

●● PaaS models to dramatically speed application development and time-to-market

●● Self-service catalogs that provide modular flexibility , easy scal-ability and customization to address rapidly changing needs

●● Open cloud architectures to enable hybrid cloud interopera-bility and provide a path to collaborative innovation

●● Automated private cloud management that provides infrastructure-wide visibility across cloud and non- cloud environments

●● Fully integrated security and resiliency management, with the ability to recover from outages

●● Analytics to identify better cloud opportunities and delivery models that facilitate development of a holistic cloud strategy

Cloud- enabled businesses as a growth engine for CSPs

A major Chinese communications operator slashes time- to- market for new partner offerings from three or four months to just two or three days—creating a key competitive advantage. A leading U.S. communications operator provides its customers with cloud- based connectivity, applications and development services on both nationwide and global wireless networks.

CSPs can stop viewing cloud as the end goal and start pursuing specific cloud-enabled businesses to grow revenue and profit. For CSPs looking to improve internal operations or establish new business models, the cloud market is moving fast. Forward-looking CSPs can take full advantage of cloud strategies to:

●● Reduce cost and improve efficiencies of IT and network infrastructure

●● Innovate and deliver new service offerings on next generation networks

●● Build a cloud ecosystem to launch new service offerings

IBM GTS Cloud Advisory Services

9

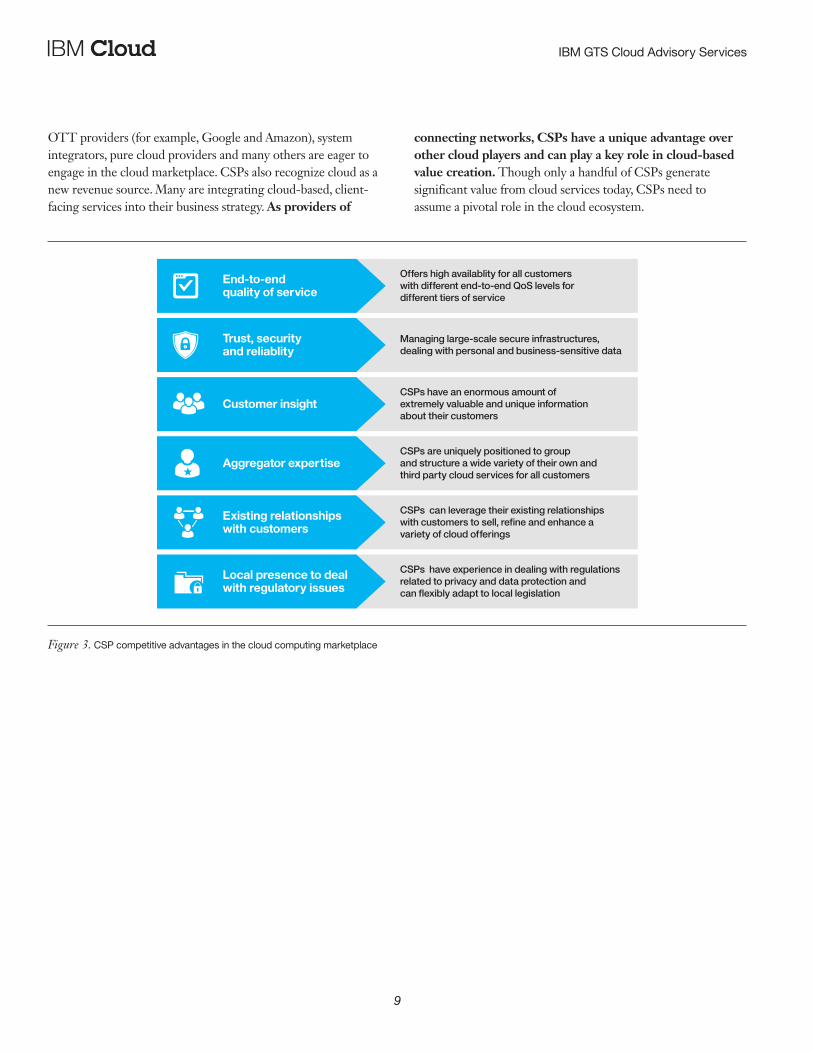

OTT providers (for example, Google and Amazon), system integrators, pure cloud providers and many others are eager to engage in the cloud marketplace. CSPs also recognize cloud as a new revenue source. Many are integrating cloud-based, client- facing services into their business strategy. As providers of

connecting networks, CSPs have a unique advantage over other cloud players and can play a key role in cloud-based value creation. Though only a handful of CSPs generate significant value from cloud services today, CSPs need to assume a pivotal role in the cloud ecosystem.

Figure 3. CSP competitive advantages in the cloud computing marketplace

Customer insight

Trust, security and reliablity

End-to-end quality of service

Aggregator expertise

Local presence to deal with regulatory issues

CSPs are uniquely positioned to group and structure a wide variety of their own and third party cloud services for all customers

CSPs can leverage their existing relationships with customers to sell, refine and enhance a variety of cloud offerings

CSPs have experience in dealing with regulations related to privacy and data protection and can flexibly adapt to local legislation

CSPs have an enormous amount of extremely valuable and unique information about their customers

Managing large-scale secure infrastructures, dealing with personal and business-sensitive data

Offers high availablity for all customers with different end-to-end QoS levels for different tiers of service

Existing relationshipswith customers

IBM GTS Cloud Advisory Services

10

CSPs have unique capabilities that enhance cloud computing, as shown in Figure 3. For example:18

●● Quality of Service (QoS). Given the control CSPs exercise over access networks, they fully control QoS at every network point. This enables CSPs to offer high availability with differ-ent end-to- end QoS levels and to price service tiers that cover both cloud and traditional network services. As an intermedi-ary between cloud users and third-party cloud providers, CSPs can also charge these third parties for service quality, resulting in a win-win situation.

●● Reliability, security and trust. Security is the top concern for cloud adoption by organizations globally. CSP brands have a strong reputation for managing large-scale security- rich infrastructures, dealing with personal and business-sensitive data in a confidential way, and flexibly adapting to local legislation and regulation. Seen as a trusted, reliable, secure partner, CSPs with cloud offerings become a natural choice for enterprises taking advantage of the technology.

●● Customer insight. What matters most in providing cloud services is an end user experience that comprises seamless cloud access from a variety of devices, from any location. CSPs possess an enormous amount of exclusive information about their customers. They can combine customer profiles with data on actual location, presence and device used. Then, they can apply analytics to produce actionable insights to enhance user experience.

●● Aggregation expertise. CSPs are uniquely positioned to group and structure a variety of their own and third-party cloud services, and to combine private and public cloud elements to suit customers’ needs. Acting as a distribution channel for third-party cloud services, CSPs can aggregate services such as data centers, managed services, application delivery and e-commerce front- ends into a single, powerful end-to- end experience. In addition, they can exploit their in-house usage- based billing capabilities to charge for clients’ cloud usage or even act as a billing aggregator.

●● Existing relationships with customers. Since cloud is network-centric, CSPs have the advantage of owning the connecting networks. Built-in direct access to large numbers of enterprise customers, small and medium business (SMB) customers and consumers—and the associated established billing relationships—offers an unparalleled selling position. No other cloud player is closer to the customer. CSPs can adopt these existing relationships to sell, refine and enhance a variety of cloud offerings.

Thinking globally and acting locallyFrom an integrated product and service strategy perspective, thinking globally and acting locally will allow global CSPs to explore and develop specific cloud-enabled features for each country, while at the same time benefiting from the strength of a global enterprise. Key opportunities include:

●● Providing shared services that can improve profitability and efficiency for services not strategic to the local operations, such as Finance, Facilities and Materials Management, HR and IT

●● Collaborating with other global vendors that can provide joint services with additional multicountry vendors (for example, Google and Facebook). VimpelCom accomplished this through its partnership with WhatsApp19

●● Optimizing roaming services—required by global custom-ers—which can enable a CSP to become a preferred roaming partner with extensive coverage—such as Vodafone’s Passport20

Incorporating cloud into your business strategyEmbracing cloud computing as a business enabler for your organization is a multi-faceted transformational continuum. As a starting point, you can use cloud to optimize economies of scale within your global organization. Cloud can also help you redefine delivery of your current service portfolio. In addition,

IBM GTS Cloud Advisory Services

11

cloud computing can serve as a catalyst that launches innovative new solutions. Finally, you can extend your newfound cloud expertise by integrating services among your partners and customers.

Realizing economies of scale through cloud- enabled synergiesIt makes sense to conduct current business more effectively by creating synergies across operating companies. Yet global telcos have not explored all opportunities. In fact, only one in four C-level executives stated that their companies have realized economies of scale to some extent.21 While global operators have progressed in some domains, cloud’s potential to facilitate synergies in these areas remains largely untapped:

●● IT/systems infrastructure(homogeneity/virtualization/consolidation)

●● Operations (operating efficiency, alignment of processes)●● Shared services (HR, Finance, and so forth)●● Resources (optimized resource allocation)

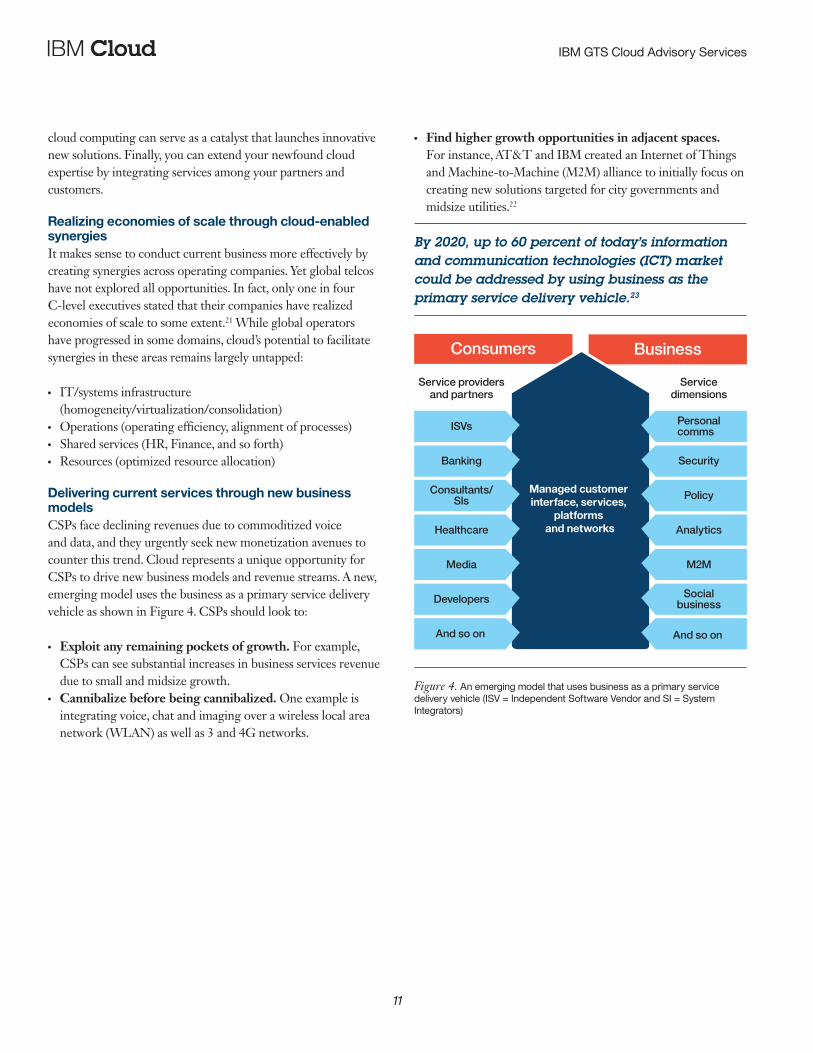

Delivering current services through new business modelsCSPs face declining revenues due to commoditized voice and data, and they urgently seek new monetization avenues to counter this trend. Cloud represents a unique opportunity for CSPs to drive new business models and revenue streams. A new, emerging model uses the business as a primary service delivery vehicle as shown in Figure 4. CSPs should look to:

●● Exploit any remaining pockets of growth. For example, CSPs can see substantial increases in business services revenue due to small and midsize growth.

●● Cannibalize before being cannibalized. One example is integrating voice, chat and imaging over a wireless local area network (WLAN) as well as 3 and 4G networks.

●● Find higher growth opportunities in adjacent spaces. For instance, AT&T and IBM created an Internet of Things and Machine-to- Machine (M2M) alliance to initially focus on creating new solutions targeted for city governments and midsize utilities.22

By 2020, up to 60 percent of today’s information and communication technologies (ICT) market could be addressed by using business as the primary service delivery vehicle.23

Figure 4. An emerging model that uses business as a primary service delivery vehicle (ISV = Independent Software Vendor and SI = System Integrators)

Service providersand partners

Servicedimensions

Consumers Business

Managed customer interface, services,

platforms and networks

Personalcomms

Security

Policy

Analytics

M2M

Socialbusiness

And so on

Banking

And so on

Consultants/Sls

ISVs

Healthcare

Media

Developers

IBM GTS Cloud Advisory Services

12

Software Defined Network technologies

Some financial and aerospace firms are using telco-der ived Software Defined Network (SDN) technologies to create software defined data centers (SDDCs), and within them, application platforms. These companies have created internal cloud ecosystems that should be more manage-able and flexible once all standards are established. SDNs also:

●● Open new markets for communications services vendors, with firms like Juniper and Cisco offering SDN-r elated products to the financial industry.

●● Allow multiple independent virtual networks to share a common physical infrastructure. This enables Business Processes as a Service (BPaaS) such as loan approval services.

●● Help Google, Verizon video and other service providers to improve the speed of implementing changes and to reduce the cost of scaling up their networks. Compa-nies use SDN technologies to create infrastructures that intimately connect to clouds—for example, a virtualized server in the data center can connect to the cloud and call up 10,000 virtual machines for testing a new application.24

●● Enable banks to retrofit technology developed for the communications industry. This illustrates the premium that businesses place on having more tools to manage the use of cloud applications and how new platforms that offer better control can enhance business agility and re-duce costs.25

Sparking innovation: Creating entirely new businesses through cloud computingTelco C-level executives see two primary trends in the coming years: 1) Increased competition from other industries, in partic-ular OTT providers, and 2) A need to develop new offerings to offset the market shifts to OTT and other competitors. New services can be based on Cloud, Big Data, Social and Mobility.26

In fact, many CSPs today are already finding new sources of revenue. For example:

●● Comcast’s Business Services revenue increased 26.4 percent to $3.2B in 2013.27 Much of this growth was from small businesses, but midsize business contribution is increasing.

●● As noted earlier, the AT&T and IBM’s Internet of Things and M2M alliance initially focuses on new solutions targeted for city governments and midsize utilities.28

●● Deutsche Telecomm (DT) established a dedicated business unit to create and implement cloud strategy. This business unit primarily focuses on SMB and consumer markets, and it manages the company’s ecosystem of cloud partnerships, primarily with ISVs. DT aims to provide intuitive, easy-to-use-cloud services, similar to the iTunes experience. Accordingly, DT’s Business Marketplace provides customers with a single point of contact, platform, interface, billing statements and privacy policy, whether sold direct or through the channel.29

CSPs intend to use cloud to improve their business capabilities in addition to enhancing internal efficiencies. In one study, 57 percent of CSPs surveyed said they plan to harness cloud for radical business model innovation within three years.30

Providing service integration among partners and customersTelco C-level executives foresee major changes in customer and partner interaction that will ultimately help telcos. These changes facilitate a growing trend toward hybrid cloud environments. Hybrid clouds require integration across on- and

IBM GTS Cloud Advisory Services

13

off-premise cloud technologies, systems, and operations span-ning multiple providers. A survey of telco C-level executives shows that:31

●● 55 percent expect to open up their enterprises—removing barriers to internal and external collaboration

●● 68 percent seek equal partners in creating business value●● 75 percent source innovation externally, increasing their

partner network●● 82 percent recognize shifts toward social and digital interac-

tion as imperative●● 67 percent expect to engage customers as individuals rather

than as a category or market segment. This means a willing-ness to pursue paths toward mutual value and including customers in key decisions

When it comes to service integration, telcos use cloud to provide end-to-end management, security and performanceoptimization of both networks and applications. Telcos regularly provide hosted services but seldom serve on-premises clouds. Many telcos create an ecosystem of ISVs that use their infrastructures and offer services to clients through a telco-owned marketplace. Typical telco customers are already heavy network users or SMBs using telco hosting services.32

ConclusionBased on current industry trends, telcos can pursue three avenues:

●● Become a consolidator●● Be consolidated●● Outperform and remain independent

Industry examples of consolidation include AT&T’s purchase of Cricket and Nextwave33 and the sale of its wireline business to Frontier.34

Swisscom provides an example of outperforming and remaining independent. According to the Financial Times: “The telco’s gains may be modest, but its share price rises have been large! What a difference the Alps make. Last year, Swisscom became the first big European telecom incumbent to show a morsel of growth after the sector’s recent doldrums.”35

To thrive in this tumultuous industry, CSPs should implement strategies designed to:

●● Deliver exceptional value to a broad target audience of internal and external clients

●● Create a uniquely attractive and easy-to-use commercial cloud services storefront for SMBs and Enterprise customers

●● Accelerate time-to-market by implementing a complete cloud services marketplace that simplifies new offering launches

●● Attract ISVs that can utilize IaaS and PaaS solutions for the creation and deployment of rich third-party SaaS offerings

●● Develop new cloud-based products and services according to local market preferences by integrating hosted and born-on-the-cloud applications

●● Retain business model flexibility and expand market reach through the ability to resell services through local channel partners

IBM GTS Cloud Advisory Services

14

RecommendationsTo optimize value from cloud-enabled business models, telcos can:

●● Formulate a clear cloud strategy, and link it to their business and marketing strategies.– Determine which cloud business enablers to adopt and

how they will be used– Develop and oversee the implementation of business

changes (such as processes and outcomes) that cloud will enable with their organization and throughout the telco industry ecosystem

– Optimize sales of cloud technologies and services for internal use. This can be done via infrastructure storage and computing, development and test environments, analytics platforms and collaboration systems such as social media

●● Look within and beyond organization borders to optimize value derived from cloud adoption– Determine how cloud strategy can impact the telco

ecosystem, and identify new partners that cloud can help incorporate. Evaluate whether cloud can or should change your own role in the ecosystem

– Use cloud to respond to customers more effectively. Explore whether – and how - cloud can help enhance your value proposition with current customers, and examine whether you can reach other customer segments through cloud

– Create strategic partnerships with selected carriers to integrate services, creating differentiated joint offers. This can be achieved through security-rich hybrid clouds or Integration Operating Teams (IOTs), and go-to-market collaboration for SaaS offerings

– Establish shared responsibility for cloud strategy and governance across business and IT

●● Enable simple, scalable sell through of cloud services by telcos (and other CSPs). This can be realized by utilizing infrastruc-ture storage and computing, managed back-up, managed security, website hosting and SaaS aggregation, and collabo-rating with partners on marketing efforts

Enlist the right partner to plan and achieve the transformationCSPs, collaborating with experienced cloud service providers, can increase their business value and industry enablement in the following areas:

1. Consult with specialists to formulate the right cloud strategy to meet your organization’s specific needs.

IBM provides a range of professional services that support the rich set of capabilities cloud technology brings to organizations everywhere, using a strategic framework as a lens, defined from our own experience. Our expertise encompasses:

Business models●● Revenue impact of cloud on business processes and

go-to-market channels●● Consultations on industry, enterprise and business unit

initiatives to drive step-change market performance

Application and delivery platforms●● Cloud-based environments for fast development and

deployment●● Competitive software delivery strategies●● Variable service models for application software to

enhance process agility and economics

IBM GTS Cloud Advisory Services

15

Data platforms●● Methods to increase business intelligence●● Deep analytics for decision making, anticipating the most

effective next action in a company’s response to the market●● Utilization of variable service models to align enterprise

capabilities in data transformation and management

Infrastructure platforms●● Cloud infrastructure strategy designed to help clients take

advantage of the transformative value of cloud for leading edge, standardized and virtualized capabilities

●● Development of a cloud infrastructure environment that enables organizations to achieve business objectives

2. Accelerate business value and enable new business opportunities

CSPs are well-positioned to deliver new services because of their local presence, communications networks and expertise in metering network traffic, billing and payment systems, and support of mobile devices. These new services could use certain IBM cloud offerings. For example, IBM’s Cloud Service Provider Platform solution is built specifically to deliver a multi-tenant robust cloud services platform.

Accelerate business value and enable new business opportunities by delivering cloud services to subscribers, using IBM offerings such as the IBM Cloud Service Provider Platform and SoftLayer. Carefully consider which cloud solutions could work as a strategic growth engine for your business. Consult with specialists to formulate the right cloud strategy to meet your organization’s specific needs.

3. Refocus on core oper ations and speed up the transformation

CSPs have a tremendous amount of customer data that is not fully utilized, especially in the social media space. A series of marketing, analytical and collaborative software solutions are available as a service (SaaS), such as Unica, SPSS, and Coremetrics. These solutions help CSPs to identify trends and usage patterns, while reducing risks and investments. CSPs can speed up transformation and reduce risks and investments by using marketing, analytical and collaborative solutions available as a service.

IBM’s Workload Transformation Analysis (WTA) for Cloud determines alignment of a client’s workload portfolio with one or more target clouds. It uses an IBM Research-developed, patent-pending tool to produce a granular and quantitative analysis of both business applications and infrastructure components to determine the cloud fit, cost and difficulty of moving to specific target cloud environment(s). WTA for Cloud gives you information to make strategic decisions on which workloads should move to the cloud.

IBM WTA for Cloud includes:

●● Validation of the target cloud environment’s ability to support client functional and nonfunctional requirements

●● Identification and prioritizion of suitable workloads for migration to the cloud to facilitate cloud migration decisions

●● Reduction of analysis time for cloud adoption by up to 66 percent in comparison with manual analysis36

IBM GTS Cloud Advisory Services

16

IBM Cloud Managed Services (CMS) is a fully managed, highly security-rich IaaS cloud offering, which is optimized for critical enterprise workloads. This cloud service delivery platform enables clients to select key characteristics of a shared, private and hybrid cloud to match workload requirements from simple Web infrastructure to complex business processes. The offering provides choices for the client, including the potential for end-to-end management of service delivery from the server through the operating system.

IBM CMS offers unique instance-level virtual machine (VM) uptime service-level agreements up to 99.95 percent. It also offers many advantages of a private cloud—such as options for dedicated servers and storage—while providing flexible scaling and the benefits of cloud economics. IBM CMS can also help organizations better manage industry-specific regulatory requirements. For example, IBM CMS can assist retailers by providing the infrastructure and virtual server image resident services necessary for placement of Payment Card Industry (PCI)-regulated applications and data. Also, healthcare clients can host business applications and transact protected health information (PHI) data subject to U.S. Department of Health & Human Services HIPAA Privacy Rules on the IBM CMS infrastructure.

4. Experiment and prototype ne w solutions to quickly deliver cloud services

Rapidly generate new revenue by capturing new customer cloud workloads. For example, the white labeling of SoftLayer, an IBM public cloud offering, enables delivery infrastructure services with reduced investment or operating costs. Use cloud-automated deployment capabilities for web-based applications, such as portals using pattern-based offerings like IBM® PureSystems®, Workload Deployer or Cloud Application Services offerings.

CSPs can provide additional investment capacity by adjusting the resource utilization to the demand. Multi-channel experience requires web technologies to be deployed on a cloud to provide operational gains and scalability—for example, IBM WebSphere® Commerce and Cognos® Enterprise. Also, Big Data solutions are gaining importance for analyzing key focus areas such as network events, customer behaviors to support personalized recommendations, promo-tional targeting and fraud detection. Such solutions are compute intensive and require flexible disposal of computing resources.

Notes

IBM GTS Cloud Advisory Services

18

1 Under Cloud Cover: How leaders are accelerating competitive differentiation. IBM Center for Applied Insights. October 2013. ibm.com/ibmcai/globalcloudstudy

2 What being global really means: Why global integration is crucial for international communications service providers. IBM Institute for Business Value. January 2014. http://www-935.ibm.com/services/us/gbs/thoughtleadership/telecom-gie/

3 Ibid.4 Ibid.5 Ibid.6 IBM Institute for Business Value internal research.7 What being global really means: Why global integration is crucial for international communications service providers. IBM Institute for Business Value.

January 2014. http://www-935.ibm.com/services/us/gbs/thoughtleadership/telecom-gie/

8 The inf luence of social: New views from the 2014 IBM Global Telecommunications Consumer Survey. IBM Institute for Business Value. May 2014. http://www-935.ibm.com/services/us/gbs/thoughtleadership/telcoconsumer/

9 Ibid.10 Ibid.11 Chen, Brian X. and Ron Lieber. “Verizon Drops Plan for $2 Fee on Some Bill Payments.” New York Times, Dec. 30, 2011.

http://bits.blogs.nytimes.com/2011/12/30/verizon-backtracks-on-plan-for-2-convenience-fee/, accessed Sept. 24, 2014.12 Stevenson, Chris. “O2 confirms compensation package to ‘make it up’ to hundreds of thousands of customers who lost service last week.”

The Independent, July 18, 2012. http://www.independent.co.uk/life-style/gadgets-and-tech/news/o2-confirms-compensation-package-to-make-it-up-to-hundreds-of-thousands-of-customers-who-lost-service-last-week-7956845.html, accessed Sept. 24, 2014.

13 The inf luence of social: New views from the 2014 IBM Global Telecommunications Consumer Survey. IBM Institute for Business Value. May 2014. http://www-935.ibm.com/services/us/gbs/thoughtleadership/telcoconsumer/

14 Ibid.15 Under Cloud Cover: How leaders are accelerating competitive differentiation. IBM Center for Applied Insights. October 2013.

ibm.com/ibmcai/globalcloudstudy

16 Ibid.17 Ibid.18 The natural fit of Cloud with Telecommunications: Winning in a new game through new business models. IBM Institute for Business Value, August 201219 Costello, Steve. “VimpelCom partners with WhatsApp,” Mobile World Live, Dec. 3, 2013. http://www.mobileworldlive.com/vimplecom-partners-whatsapp,

accessed Sept. 24, 2014.20 Make cheaper calls while abroad with Vodafone Passport, http://www.vodafone.co.uk/shop/pay-as-you-go/travelling-abroad/vodafone-passport/,

accessed Sept. 24, 2014

IBM GTS Cloud Advisory Services

19

21 What being global really means: Why global integration is crucial for international communications service providers. IBM Institute for Business Value. January 2014. http://www-935.ibm.com/services/us/gbs/thoughtleadership/telecom-gie/

22 “AT&T And IBM Join Forces To Deliver New Innovations For The Internet of Things,” IBM Newsroom, Feb. 18 2014. http://www-03.ibm.com/press/us/en/pressrelease/43223.wss, accessed Sept. 24, 2014.

23 IBM Institute for Business Value internal research.24 Cohen, Roger. Software Defined and Boundary-free: the promise of SDN and SDCCs, Saugatuck Technologies. November 8, 2013.

http://saugatucktechnology.com/research/latest-research/2855-1286mkt-software-defined-and-boundary-free-the-promise-of-sdn-and-sddcs.html

25 Ibid.26 The inf luence of social: New views from the 2014 IBM Global Telecommunications Consumer Survey. IBM Institute for Business Value. May 2014.

http://www-935.ibm.com/services/us/gbs/thoughtleadership/telcoconsumer/

27 Comcast’s CEO Discusses Q4 2013 Results - Earnings Call Transcript. http://finance.yahoo.com/news/comcasts-ceo-discusses-q4-2013-175403106.html, accessed Sept. 16, 2014.

28 “AT&T And IBM Join Forces To Deliver New Innovations For The Internet of Things,” IBM Newsroom, Feb. 18 2014. http://www-03.ibm.com/press/us/en/pressrelease/43223.wss, accessed Sept. 24, 2014.

29 IDC Link. “Deutsche Telecom Addresses Cloud Opportunity with Dedicated Cloud Business Unit.” Doc # lcUK24414813.October 2013.30 The natural fit of Cloud with Telecommunications: Winning in a new game through new business models. IBM Institute for Business Value, August 2012.31 IBM Institute for Business Value internal research.32 IDC. IDC Competitive Analysis: IT Service Providers’ Cloud Strategies in Europe 2013. Doc #QL03V, June 2013.33 “AT&T Completes Acquisition of Leap Wireless.” AT&T Newsroom, March 13, 2014. Accessed Sept. 25, 2014.

http://about.att.com/story/att_completes_acquisition_of_leap_wireless.html “AT&T Agrees to Acquire NextWave Wireless, Inc.” AT&T press release archives, Aug. 2, 2012. Accessed Sept. 25, 2014. http://www.att.com/gen/press-room?pid=23161&cdvn=news&newsarticleid=34976&mapcode=

34 McGrath, Maggie. “AT&T Selling Its Connecticut Wireline Business To Frontier For $2 Billion.” Forbes. Dec. 17, 2013. http://www.forbes.com/sites/maggiemcgrath/2013/12/17/att-selling-its-connecticut-wireline-business-to-frontier-for-2-billion/

35 “Swisscom: on the ascent.” Financial Times, February 16, 2014. Accessible by subscription only.36 Based on IBM client engagements, actual results may vary.

For more informationTo learn more about IBM Cloud Advisory Services, please contact your IBM representative or visit the following website: ibm.com/cloud computing

About the authorTeresa Hefner is a Certified IT Consultant in IBM GTS’ Cloud Advisory Services Global Center of Competency. In addition to her cloud experience, she has a background in system engineering, sales and IT strategy and design consulting.

© Copyright IBM Corporation 2014

IBM Corporation Global Technology Services Route 100 Somers, NY 10589

Produced in the United States of America October 2014

IBM, the IBM logo, ibm.com, PureSystems, WebSphere, and Cognos are trademarks of International Business Machines Corp., registered in many jurisdictions worldwide. Other product and service names might be trademarks of IBM or other companies. A current list of IBM trademarks is available on the web at “Copyright and trademark information” at ibm.com/legal/copytrade.shtml

SoftLayer is a registered trademark of SoftLayer, Inc., an IBM Company.

Microsoft, Windows and Windows NT are trademarks of Microsoft Corporation in the United States, other countries, or both.

This document is current as of the initial date of publication and may be changed by IBM at any time. Not all offerings are available in every country in which IBM operates.

The performance data discussed herein is presented as derived under specific operating conditions. Actual results may vary.

THE INFORMATION IN THIS DOCUMENT IS PROVIDED “AS IS” WITHOUT ANY WARRANTY, EXPRESS OR IMPLIED, INCLUDING WITHOUT ANY WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND ANY WARRANTY OR CONDITION OF NON-INFRINGEMENT . IBM products are warranted according to the terms and conditions of the agreements under which they are provided.

WUW12355-USEN-00

Please Recycle