Embed Size (px)

Citation preview

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

S.O.L.A.R. Insurance Arrangements

Self-Owned Life And Retirement (S.O.L.A.R.) Insurance Arrangements

This presentation contains information regarding insurance products for sale.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Disclosures

• ING Indexed Universal Life –Global Choice (ING IUL-Global Choice), policy form series #1186-09/12 has an

equity Indexed feature, varies by state and may not be available in every state. It is issued by Security Life of

Denver Insurance Company (Denver, CO), a member of the ING family of companies. Not available in New

York. The Index Caps and Index Participation Rates are subject to change for new Index Blocks. All

guarantees are based on the financial strength and claims paying ability of Security Life of Denver Insurance

Company which is solely responsible for the obligations under its own policies.

• ING Indexed Universal Life - Global Choice (ING IUL-Global Choice) is a flexible premium, universal life

insurance product designed to provide a death benefit and allow for surrender values. While the policy values

may be affected by external indexes, the policy does not directly participate in any index fund, stock or equity

investments. The product is not a variable product or any type of investment contract.

•The ING Life Companies and their agents and representatives do not give tax or legal advice. This

information is general in nature and not comprehensive; the applicable laws change frequently and the

strategies suggested may not be suitable for everyone. Each taxpayer should seek advice from his or her tax

and legal advisors regarding their individual situation.

•These materials are not intended to and cannot be used to avoid tax penalties; and they were prepared to

support the promotion or marketing of the matter addressed in this document. Each taxpayer should seek

advice from an independent tax advisor.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Disclosures

The Hang Seng Index (the “Index”) is published and compiled by Hang Seng Indexes Company Limited pursuant to a license from Hang Seng Data Services Limited. The mark and name “Hang Seng Index” are proprietary to Hang Seng Data Services Limited. Hang Seng Indexes Company Limited and Hang Seng Data Services Limited have agreed to the use of, and reference to, the Index by Security Life of Denver Insurance Company (“Security Life”) in connection with this indexed universal life insurance policy (the “Policy”), BUT NEITHER HANG SENG INDEXES COMPANY LIMITED NOR HANG SENG DATA SERVICES LIMITED WARRANTS OR REPRESENTS OR GUARANTEES TO ANY BROKER OR HOLDER OF THE POLICY OR ANY OTHER PERSON (i) THE ACCURACY OR COMPLETENESS OF THE INDEX AND ITS COMPUTATION OR ANY INFORMATION RELATED THERETO; OR (ii) THE FITNESS OR SUITABILITY FOR ANY PURPOSE OF THE INDEX OR ANY COMPONENT OR DATA COMPRISED IN IT; OR (iii) THE RESULTS WHICH MAY BE OBTAINED BY ANY PERSON FROM THE USE OF THE INDEX OR ANY COMPONENT OR DATA COMPRISED IN IT FOR ANY PURPOSE, AND NO WARRANTY OR REPRESENTATION OR GUARANTEE OF ANY KIND WHATSOEVER RELATING TO THE INDEX IS GIVEN OR MAY BE IMPLIED. The process and basis of computation and compilation of the Index and any of the related formula or formulae, constituent stocks and factors may at any time be changed or altered by Hang Seng Indexes Company Limited without notice. TO THE EXTENT PERMITTED BY APPLICABLE LAW, NO RESPONSIBILITY OR LIABILITY IS ACCEPTED BY HANG SENG INDEXES COMPANY LIMITED OR HANG SENG DATA SERVICES LIMITED (i) IN RESPECT OF THE USE OF AND/OR REFERENCE TO THE INDEX BY SECURITY LIFE IN CONNECTION WITH THE POLICY; OR (ii) FOR ANY INACCURACIES, OMISSIONS, MISTAKES OR ERRORS OF HANG SENG INDEXES COMPANY LIMITED IN THE COMPUTATION OF THE INDEX; OR (iii) FOR ANY INACCURACIES, OMISSIONS, MISTAKES, ERRORS OR INCOMPLETENESS OF ANY INFORMATION USED IN CONNECTION WITH THE COMPUTATION OF THE INDEX WHICH IS SUPPLIED BY ANY OTHER PERSON; OR (iv) FOR ANY ECONOMIC OR OTHER LOSS WHICH MAY BE DIRECTLY OR INDIRECTLY SUSTAINED BY ANY BROKER OR HOLDER OF THE POLICY OR ANY OTHER PERSON DEALING WITH THE POLICY AS A RESULT OF ANY OF THE AFORESAID, AND NO CLAIMS, ACTIONS OR LEGAL PROCEEDINGS MAY BE BROUGHT AGAINST HANG SENG INDEXES COMPANY LIMITED AND/OR HANG SENG DATA SERVICES LIMITED IN CONNECTION WITH THE POLICY IN ANY MANNER WHATSOEVER BY ANY BROKER, HOLDER OR OTHER PERSON DEALING WITH THE POLICY. Any broker, holder or other person dealing with the Policy does so therefore in full knowledge of this disclaimer and can place no reliance whatsoever on Hang Seng Indexes Company Limited and Hang Seng Data Services Limited. For the avoidance of doubt, this disclaimer does not create any contractual or quasi-contractual relationship between any broker, holder or other person and Hang Seng Indexes Company Limited and/or Hang Seng Data Services Limited and must not be construed to have created such relationship.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Disclosures

• A portion of the policy’s surrender value may be available as a source of supplemental retirement income through policy loans and withdrawals. Income tax free policy distributions may be achieved by policy loans or withdrawing to the cost basis (usually premiums paid). This assumes the policy qualifies as life insurance, is not a modified endowment contract and is not lapsed or surrendered with an outstanding loan. Policy loans and withdrawals may reduce or eliminate index credits, generate an income tax liability, reduce available surrender value and reduce the death benefit, or cause the policy to lapse. Select Loans have the risk that policy performance may be lower than projected if the amount credited to the account value in the Fixed Strategy and/or Indexed Strategy is less than the fixed 6% interest charged on the policy loan. Detailed additional information about policy loans is located in the policy form and any personal policy illustration.

• The S&P 500 Index is a product of S&P Dow Jones Indices LLC (“SPDJI”), and has been licensed for use by Security Life of Denver Insurance Company. Standard & Poor’s®, S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Security Life of Denver Insurance Company. Security Life of Denver Insurance Company's ING Indexed Universal Life Insurance products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

• EURO STOXX 50® Index – An index of blue-chip stocks that are represented by 50 stocks covering the largest sector leaders in the EURO STOXX 50® index. It does not reflect dividends payable on the underlying stocks. The EURO STOXX 50® index is the intellectual property (including registered trademarks) of STOXX Limited, Zurich, Switzerland and/or its licensors (“Licensors”), which is used under license. The ING Indexed Universal Life – Global Choice insurance policy is based, in part, on the Index and is in no way sponsored, endorsed, sold or promoted by STOXX and its Licensors and neither of the Licensors shall have any liability with respect thereto.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

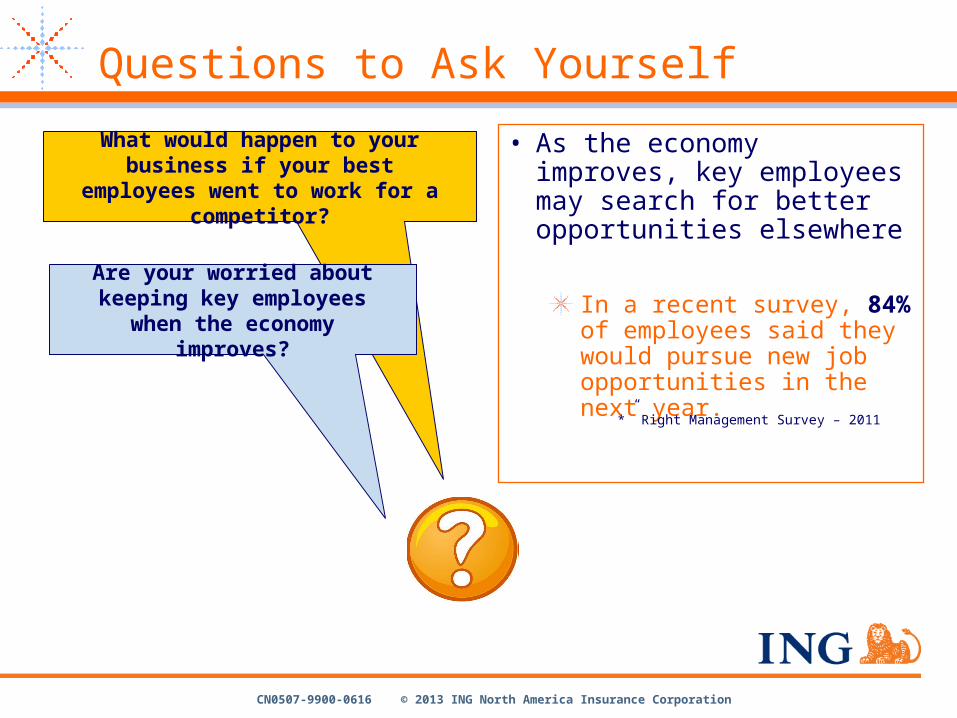

What would happen to your business if your best employees went to work for

a competitor?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

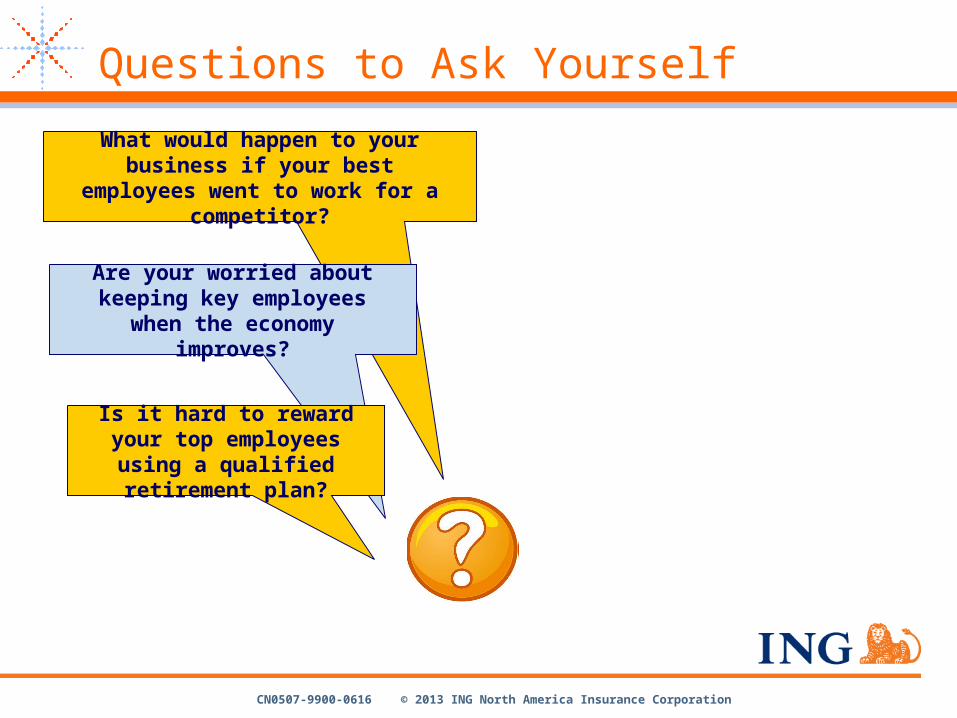

What would happen to your business if your best employees went to work for

a competitor?

Are your worried about keeping key employees when the

economy improves?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

• As the economy improves, key employees may search for better opportunities elsewhere

In a recent survey, 84% of employees said they would pursue new job opportunities in the next year.

What would happen to your business if your best employees went to work for

a competitor?

*” Right Management Survey – 2011

Are your worried about keeping key employees when the

economy improves?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

What would happen to your business if your best employees went to work for

a competitor?

Are your worried about keeping key employees when the

economy improves?

Is it hard to reward your top employees using a

qualified retirement plan?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

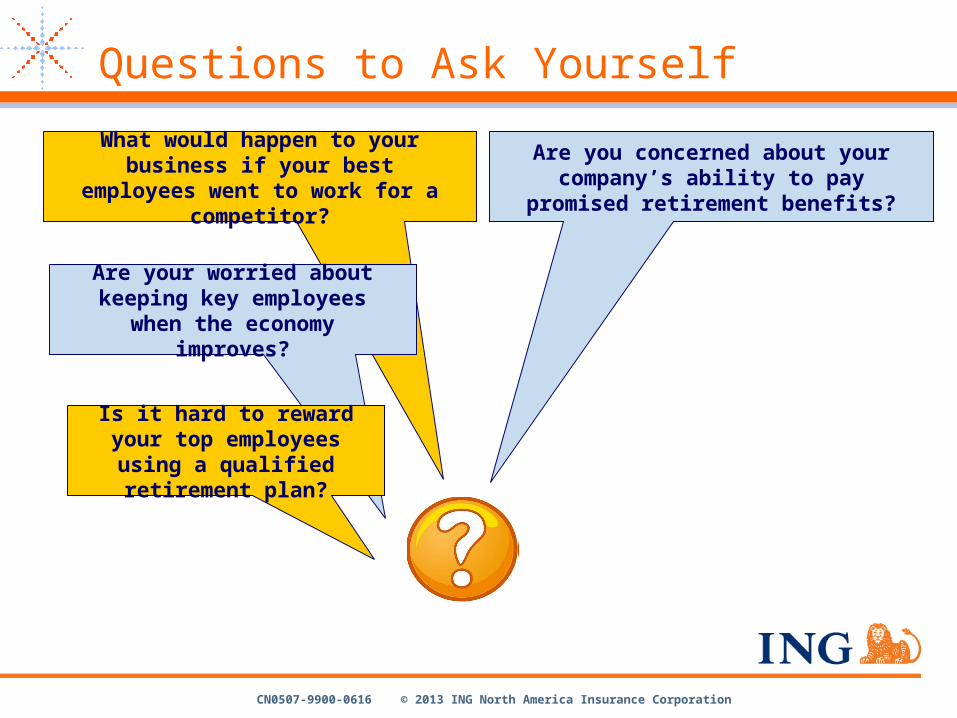

What would happen to your business if your best employees went to work for

a competitor?

Are you concerned about your company’s ability to pay promised

retirement benefits?

Are your worried about keeping key employees when the

economy improves?

Is it hard to reward your top employees using a

qualified retirement plan?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Questions to Ask Yourself

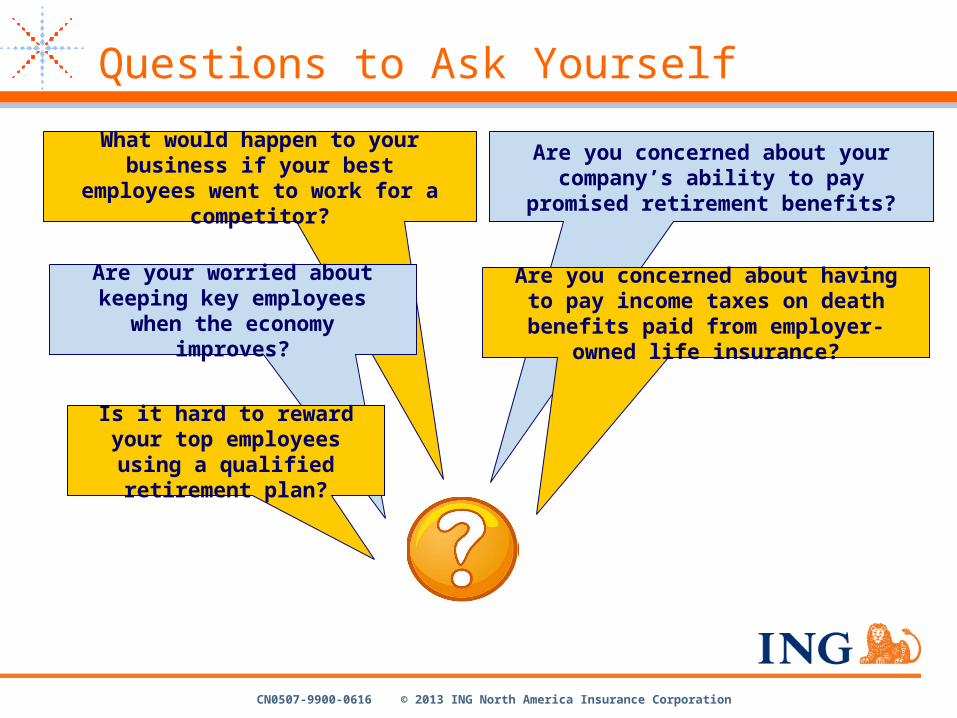

What would happen to your business if your best employees went to work for

a competitor?

Are you concerned about your company’s ability to pay promised

retirement benefits?

Are your worried about keeping key employees when the

economy improves?

Are you concerned about having to pay income taxes on death benefits paid from employer-owned life insurance?

Is it hard to reward your top employees using a

qualified retirement plan?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

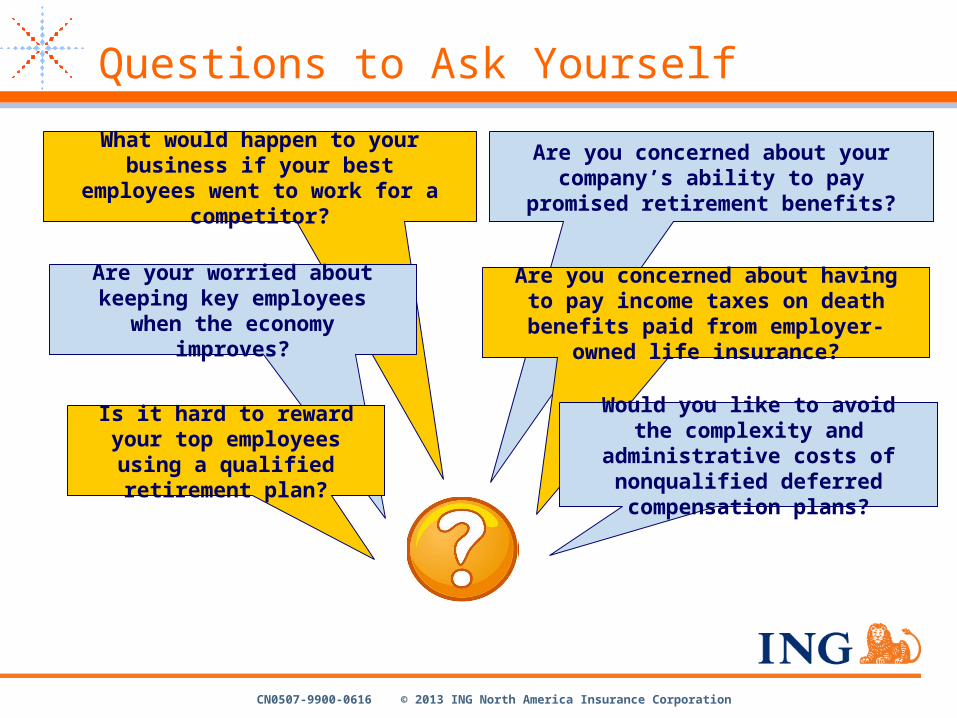

Questions to Ask Yourself

What would happen to your business if your best employees went to work for

a competitor?

Are you concerned about your company’s ability to pay promised

retirement benefits?

Are your worried about keeping key employees when the

economy improves?

Are you concerned about having to pay income taxes on death benefits paid from employer-owned life insurance?

Is it hard to reward your top employees using a

qualified retirement plan?

Would you like to avoid the complexity and administrative costs of nonqualified deferred

compensation plans?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation13

Traditional Solution – NQDC/SERP

• Employers have traditionally used Deferred Compensation Plans to recruit, retain, and reward key employees

• Many labels for the same concept

Nonqualified deferred compensation (NQDC)

Supplemental executive retirement plan (SERP)

Corporate-Owned Life Insurance (COLI)

§ 409A plan

Salary continuation

401(k) Look Alike / 401(k) Mirror

CN0507-9900-0616 © 2013 ING North America Insurance Corporation14

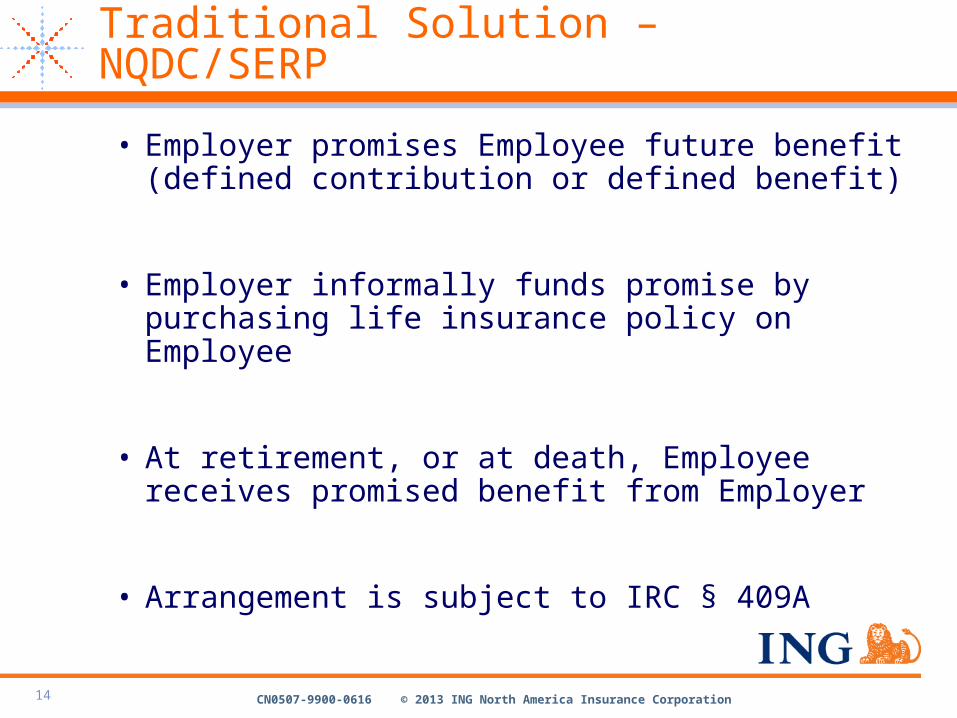

• Employer promises Employee future benefit (defined contribution or defined benefit)

• Employer informally funds promise by purchasing life insurance policy on Employee

• At retirement, or at death, Employee receives promised benefit from Employer

• Arrangement is subject to IRC § 409A

Traditional Solution – NQDC/SERP

CN0507-9900-0616 © 2013 ING North America Insurance Corporation15

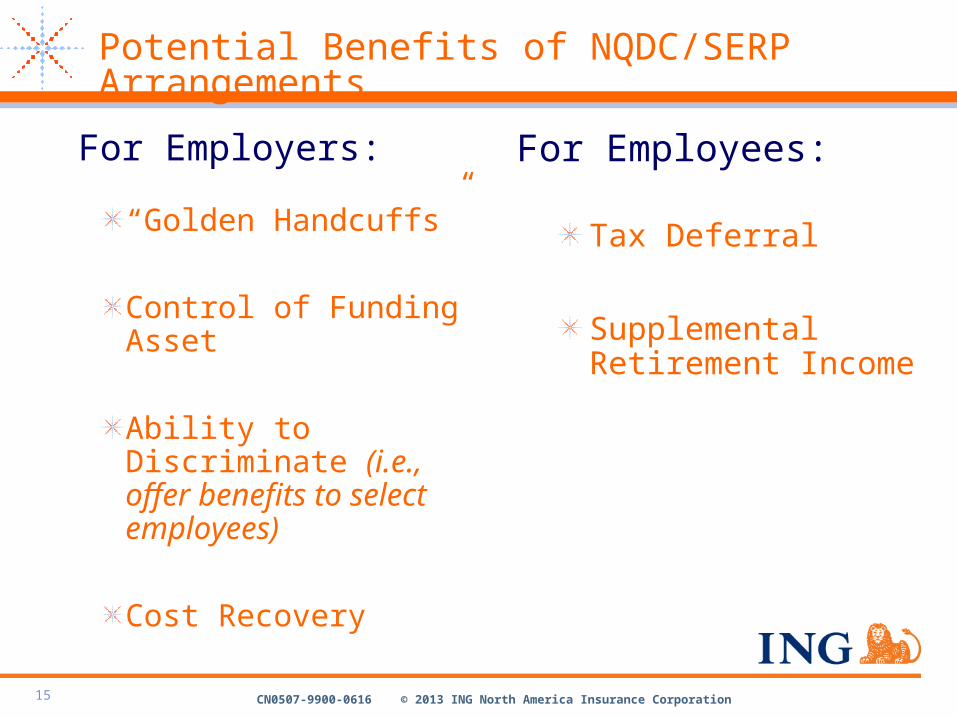

Potential Benefits of NQDC/SERP Arrangements

For Employers:

“Golden Handcuffs”

Control of Funding Asset

Ability to Discriminate (i.e., offer benefits to select employees)

Cost Recovery

For Employees:

Tax Deferral

Supplemental Retirement Income

CN0507-9900-0616 © 2013 ING North America Insurance Corporation16

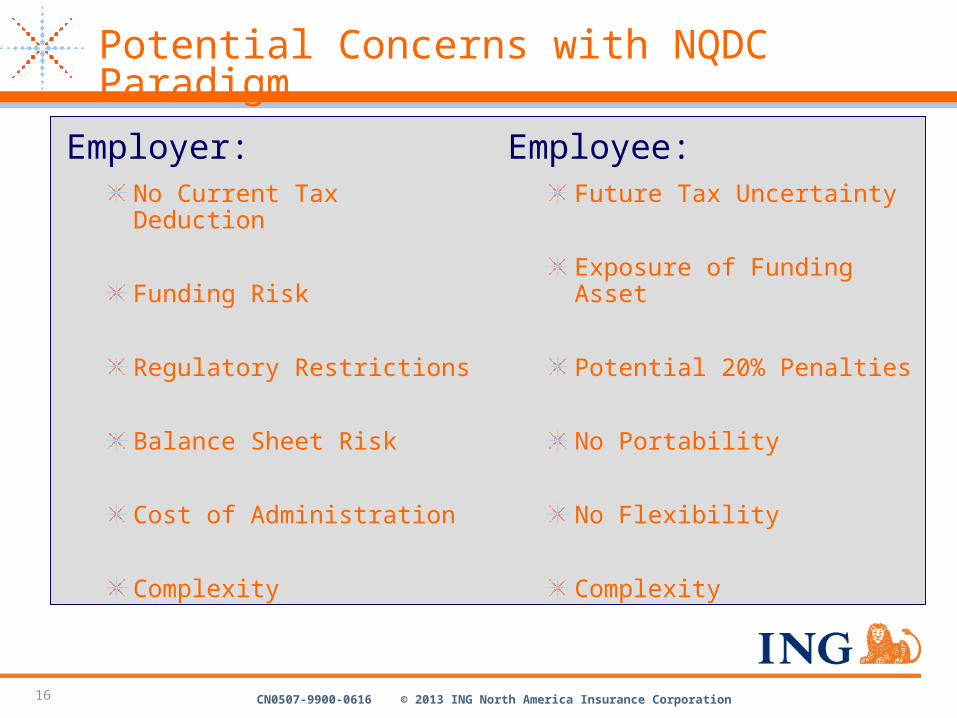

Potential Concerns with NQDC Paradigm

Employer:No Current Tax Deduction

Funding Risk

Regulatory Restrictions

Balance Sheet Risk

Cost of Administration

Complexity

Employee:Future Tax Uncertainty

Exposure of Funding Asset

Potential 20% Penalties

No Portability

No Flexibility

Complexity

CN0507-9900-0616 © 2013 ING North America Insurance Corporation17

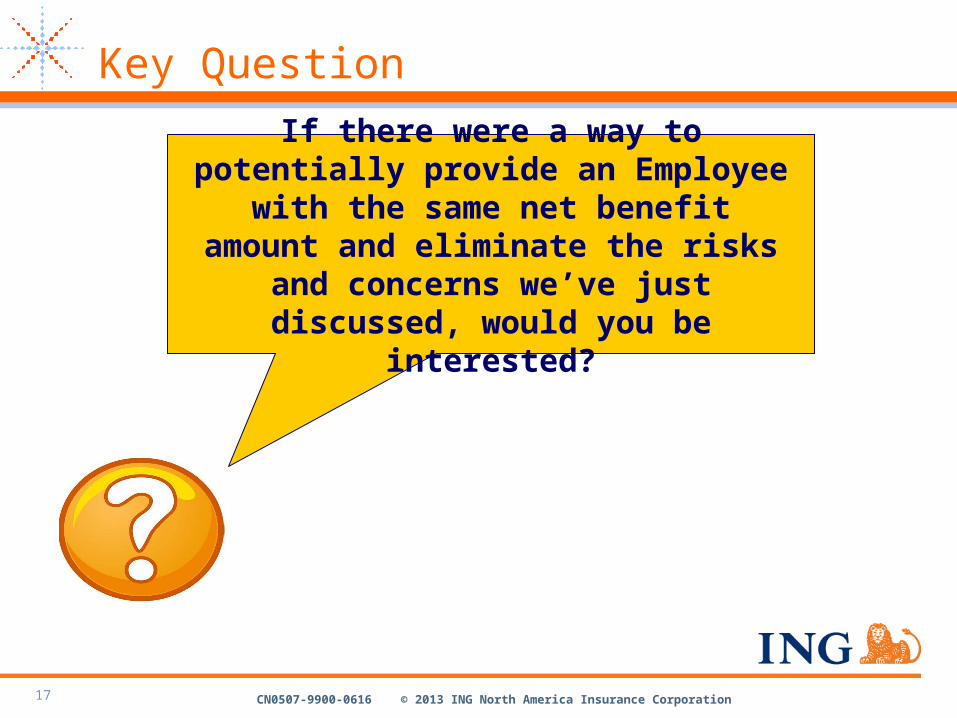

Key Question

If there were a way to potentially provide an Employee with the same net benefit amount and eliminate the risks

and concerns we’ve just discussed, would you be interested?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

S.O.L.A.R. Insurance Arrangement

CN0507-9900-0616 © 2013 ING North America Insurance Corporation19

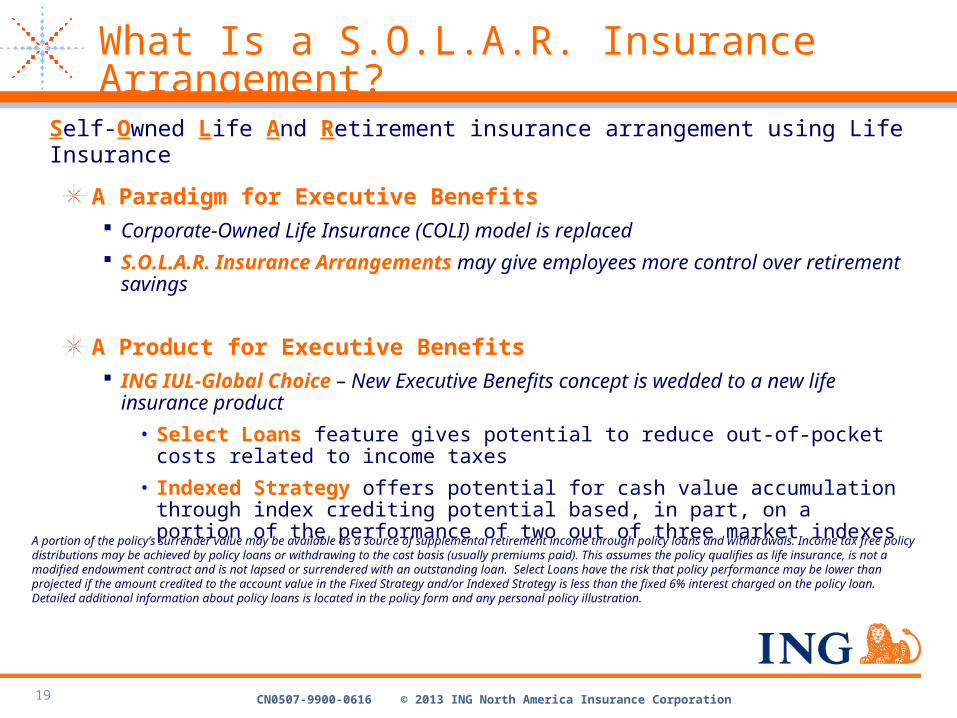

Self-Owned Life And Retirement insurance arrangement using Life Insurance

A Paradigm for Executive Benefits Corporate-Owned Life Insurance (COLI) model is replaced

S.O.L.A.R. Insurance Arrangements may give employees more control over retirement savings

A Product for Executive Benefits ING IUL-Global Choice – New Executive Benefits concept is wedded to a new life

insurance product

• Select Loans feature gives potential to reduce out-of-pocket costs related to income taxes

• Indexed Strategy offers potential for cash value accumulation through index crediting potential based, in part, on a portion of the performance of two out of three market indexes

A portion of the policy’s surrender value may be available as a source of supplemental retirement income through policy loans and withdrawals. Income tax free policy distributions may be achieved by policy loans or withdrawing to the cost basis (usually premiums paid). This assumes the policy qualifies as life insurance, is not a modified endowment contract and is not lapsed or surrendered with an outstanding loan. Select Loans have the risk that policy performance may be lower than projected if the amount credited to the account value in the Fixed Strategy and/or Indexed Strategy is less than the fixed 6% interest charged on the policy loan. Detailed additional information about policy loans is located in the policy form and any personal policy illustration.

What Is a S.O.L.A.R. Insurance Arrangement?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation2020

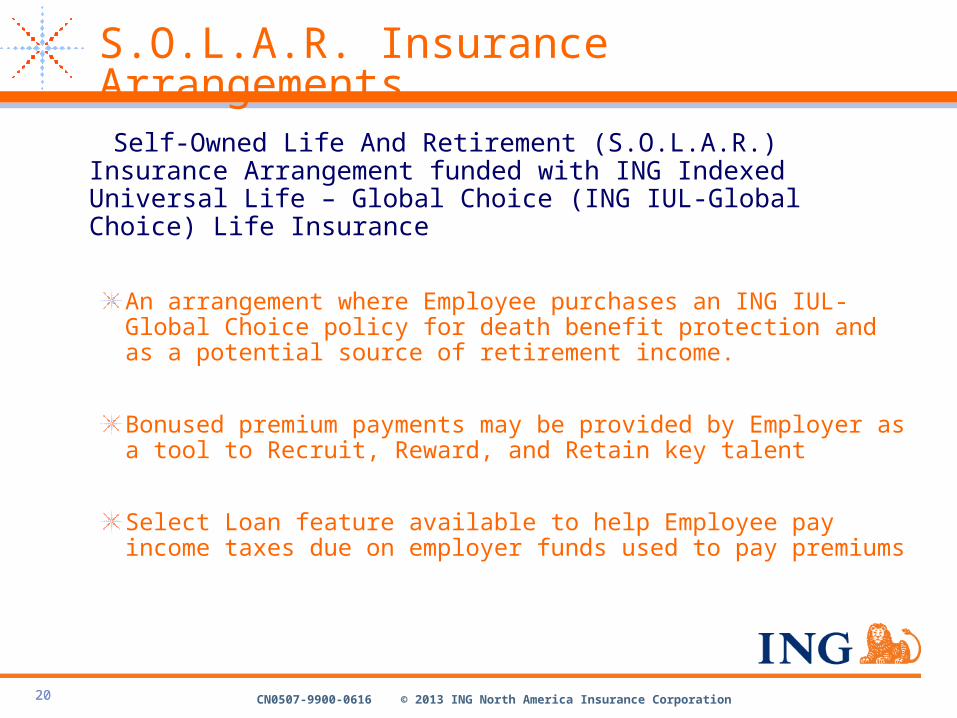

S.O.L.A.R. Insurance Arrangements

Self-Owned Life And Retirement (S.O.L.A.R.) Insurance Arrangement funded with ING Indexed Universal Life – Global Choice (ING IUL-Global Choice) Life Insurance

An arrangement where Employee purchases an ING IUL-Global Choice policy for death benefit protection and as a potential source of retirement income.

Bonused premium payments may be provided by Employer as a tool to Recruit, Reward, and Retain key talent

Select Loan feature available to help Employee pay income taxes due on employer funds used to pay premiums

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Introducing ING IUL-Global Choice

ING IUL Global Choice is an individual indexed universal life insurance policy offering valuable death benefit protection supported by policy cash values calculated under a Fixed Strategy or Indexed Strategies. The three Indexed Strategies are the S&P 500 1-Year Point to Point Indexed Strategy, the 2-year Global Indexed Strategy and the 5-year Global Indexed Strategy. While the policy values may be affected by external indexes, the policy does not directly participate in any index fund, stock or equity investments, and all policy guarantees are based solely on the financial strength and claims-paying ability of Security Life of Denver Life Insurance Company. The product is not a variable product or any type of investment contract.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Death Benefit Protection

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

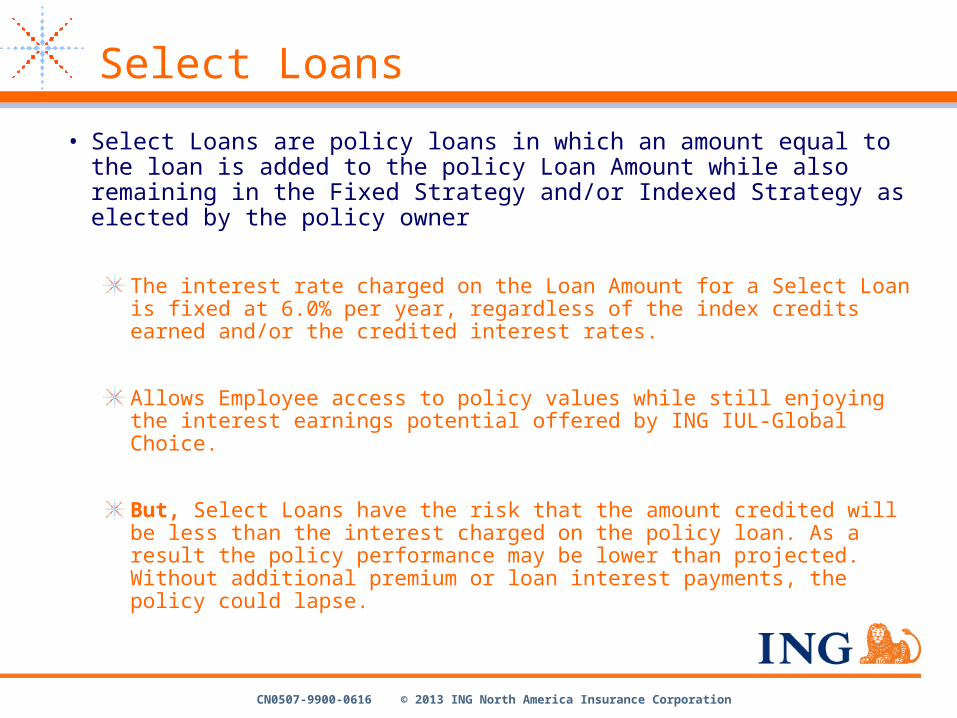

Select Loans

• Select Loans are policy loans in which an amount equal to the loan is added to the policy Loan Amount while also remaining in the Fixed Strategy and/or Indexed Strategy as elected by the policy owner

The interest rate charged on the Loan Amount for a Select Loan is fixed at 6.0% per year, regardless of the index credits earned and/or the credited interest rates.

Allows Employee access to policy values while still enjoying the interest earnings potential offered by ING IUL-Global Choice.

But, Select Loans have the risk that the amount credited will be less than the interest charged on the policy loan. As a result the policy performance may be lower than projected. Without additional premium or loan interest payments, the policy could lapse.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Select Loans

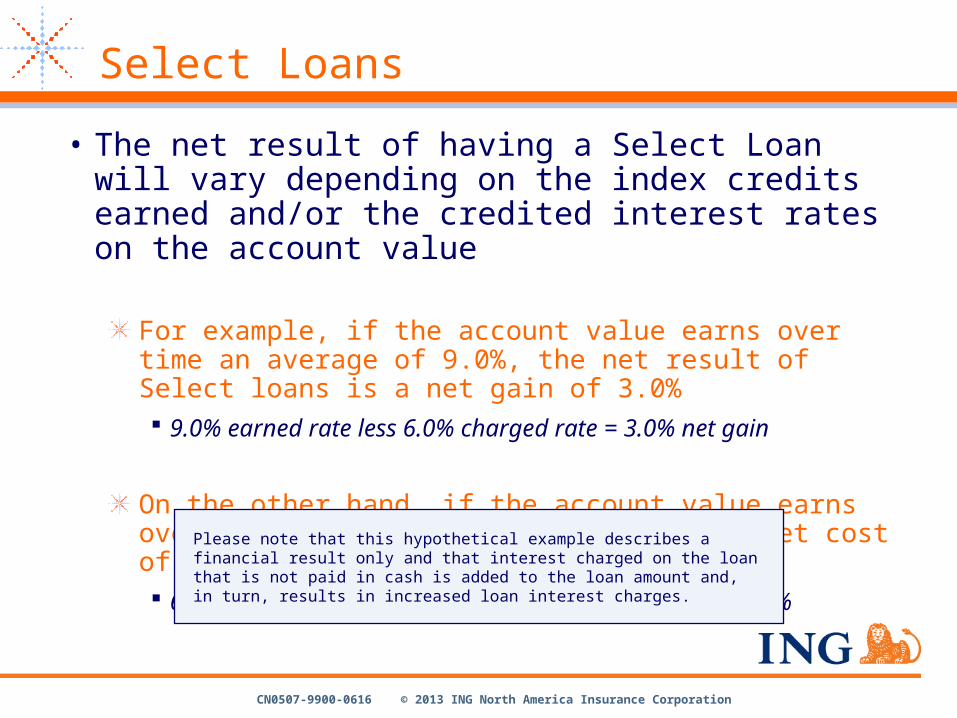

• The net result of having a Select Loan will vary depending on the index credits earned and/or the credited interest rates on the account value

For example, if the account value earns over time an average of 9.0%, the net result of Select loans is a net gain of 3.0% 9.0% earned rate less 6.0% charged rate = 3.0% net gain

On the other hand, if the account value earns over time an average of only 1.0%, the net cost of Select Loans is 5.0% 6.0% charged rate less 1.0% earned rate = net cost of 5.0%

Please note that this hypothetical example describes a financial result only and that interest charged on the loan that is not paid in cash is added to the loan amount and, in turn, results in increased loan interest charges.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

International Diversification

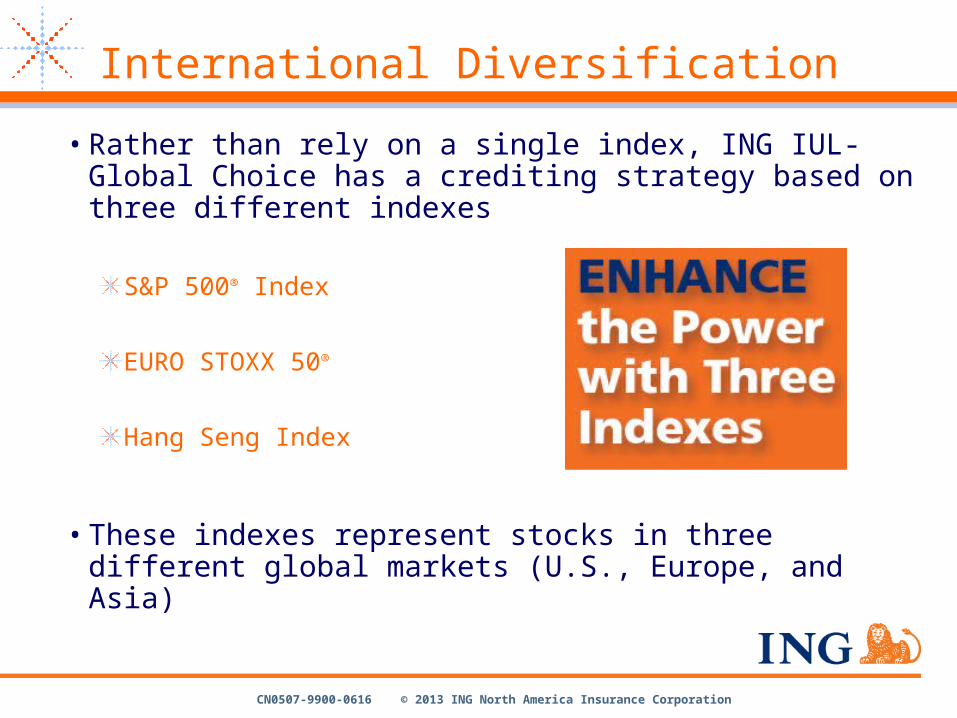

• Rather than rely on a single index, ING IUL-Global Choice has a crediting strategy based on three different indexes

S&P 500® Index

EURO STOXX 50®

Hang Seng Index

• These indexes represent stocks in three different global markets (U.S., Europe, and Asia)

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

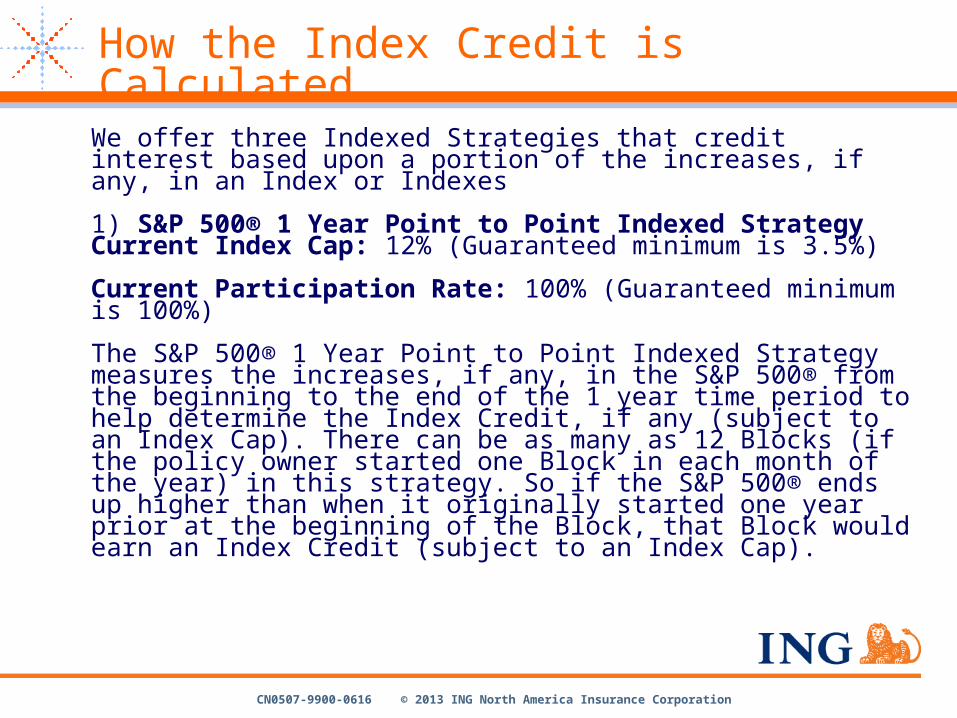

How the Index Credit is Calculated

We offer three Indexed Strategies that credit interest based upon a portion of the increases, if any, in an Index or Indexes

1) S&P 500® 1 Year Point to Point Indexed StrategyCurrent Index Cap: 12% (Guaranteed minimum is 3.5%)

Current Participation Rate: 100% (Guaranteed minimum is 100%)

The S&P 500® 1 Year Point to Point Indexed Strategy measures the increases, if any, in the S&P 500® from the beginning to the end of the 1 year time period to help determine the Index Credit, if any (subject to an Index Cap). There can be as many as 12 Blocks (if the policy owner started one Block in each month of the year) in this strategy. So if the S&P 500® ends up higher than when it originally started one year prior at the beginning of the Block, that Block would earn an Index Credit (subject to an Index Cap).

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

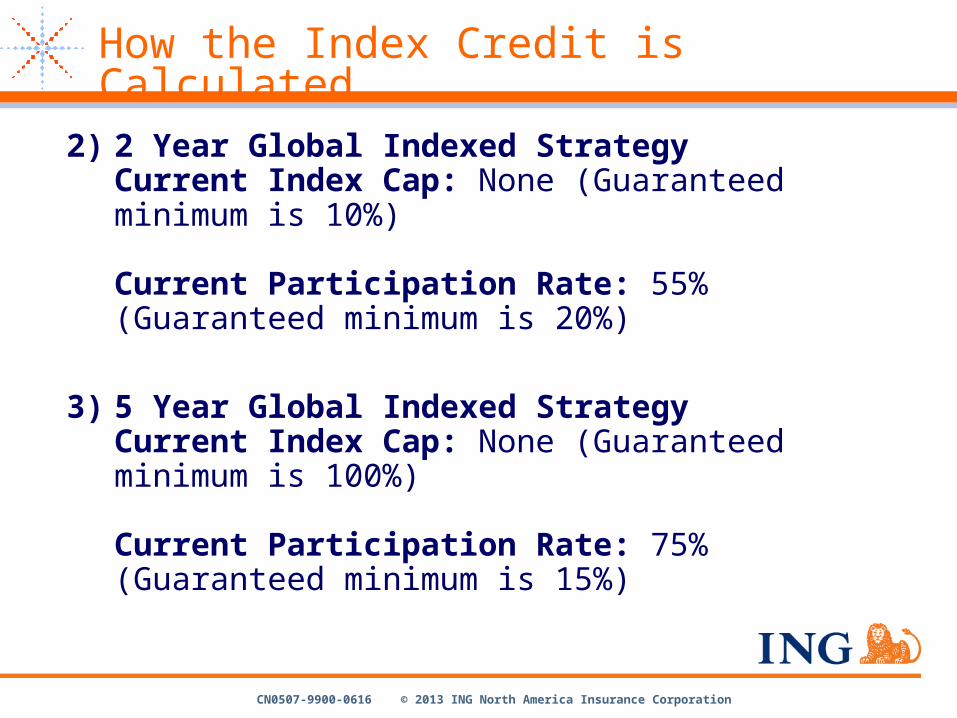

How the Index Credit is Calculated

2) 2 Year Global Indexed StrategyCurrent Index Cap: None (Guaranteed minimum is 10%)

Current Participation Rate: 55% (Guaranteed minimum is 20%)

3) 5 Year Global Indexed StrategyCurrent Index Cap: None (Guaranteed minimum is 100%)

Current Participation Rate: 75% (Guaranteed minimum is 15%)

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

How the Index Credit is Calculated

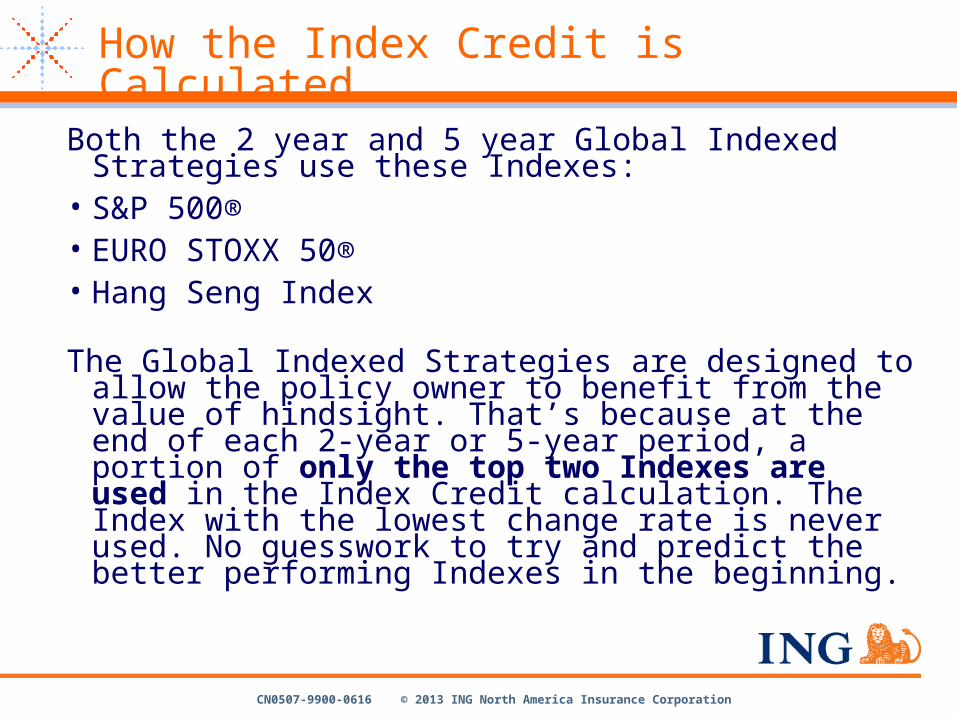

Both the 2 year and 5 year Global Indexed Strategies use these Indexes:

• S&P 500®• EURO STOXX 50®• Hang Seng Index

The Global Indexed Strategies are designed to allow the policy owner to benefit from the value of hindsight. That’s because at the end of each 2-year or 5-year period, a portion of only the top two Indexes are used in the Index Credit calculation. The Index with the lowest change rate is never used. No guesswork to try and predict the better performing Indexes in the beginning.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Guaranteed Minimum Interest Rate

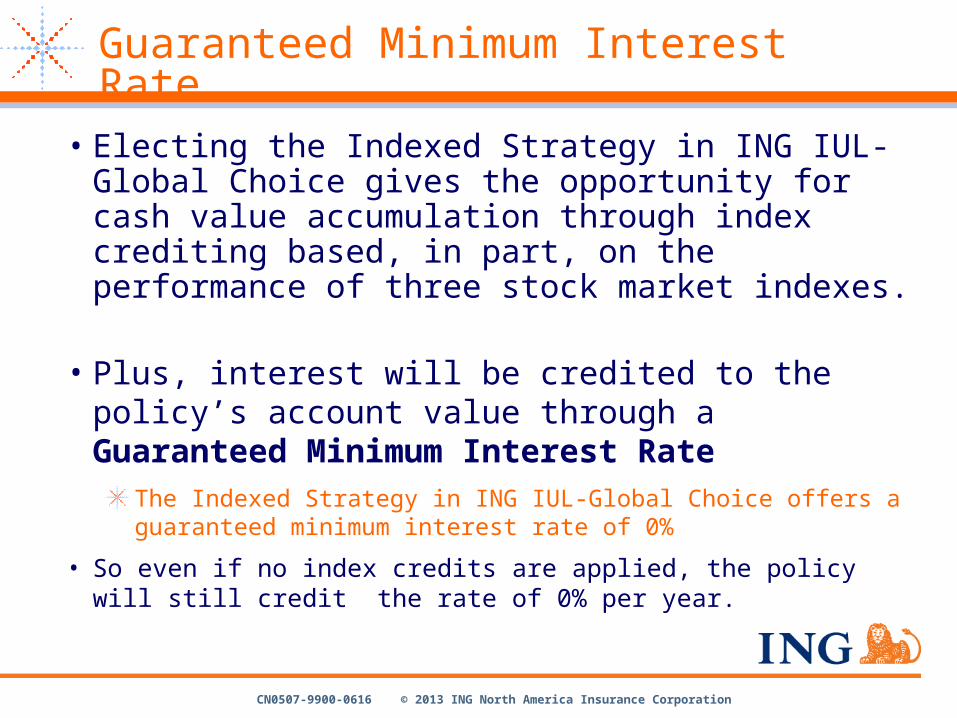

• Electing the Indexed Strategy in ING IUL-Global Choice gives the opportunity for cash value accumulation through index crediting based, in part, on the performance of three stock market indexes.

• Plus, interest will be credited to the policy’s account value through a Guaranteed Minimum Interest Rate

The Indexed Strategy in ING IUL-Global Choice offers a guaranteed minimum interest rate of 0%

• So even if no index credits are applied, the policy will still credit the rate of 0% per year.

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

How it Works

5 Steps to Implement

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

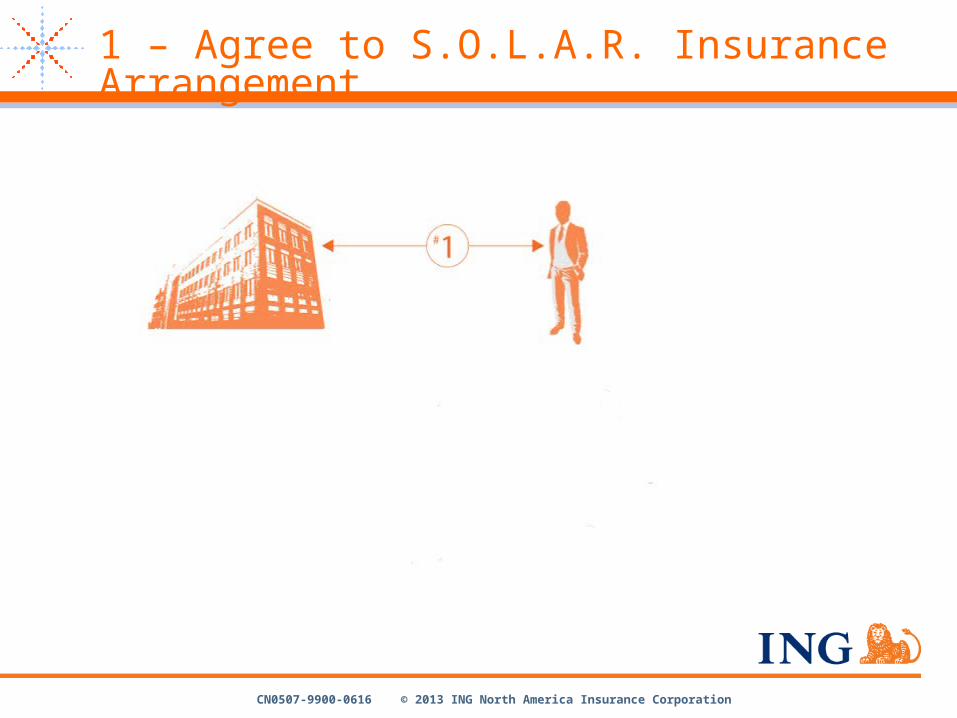

1 – Agree to S.O.L.A.R. Insurance Arrangement

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

2 – Employee Purchases ING IUL-Global Choice Policy

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

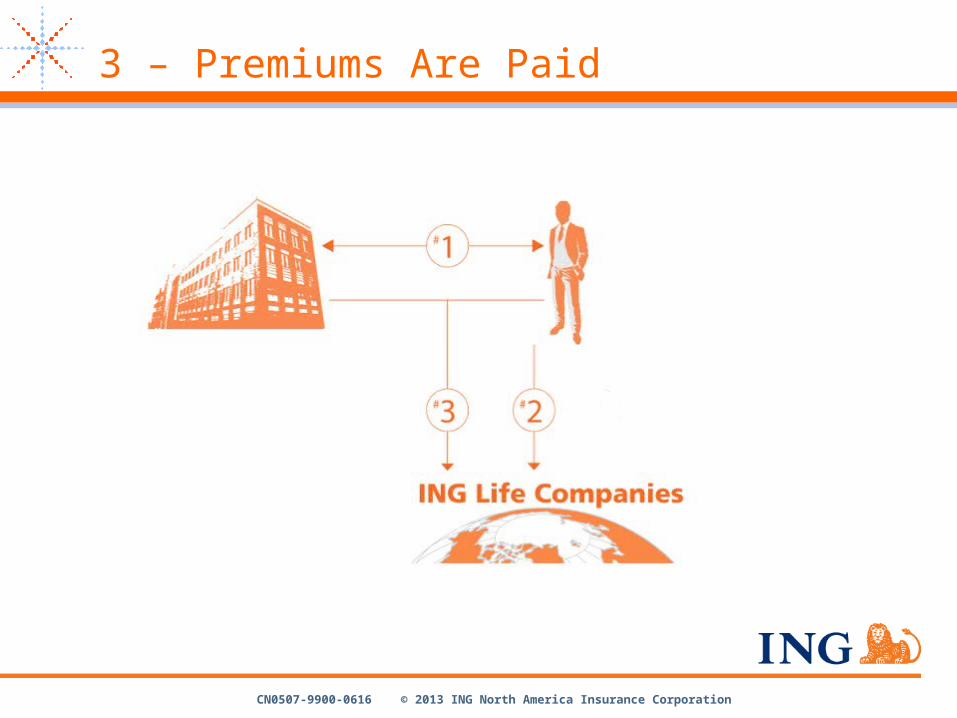

3 – Premiums Are Paid

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

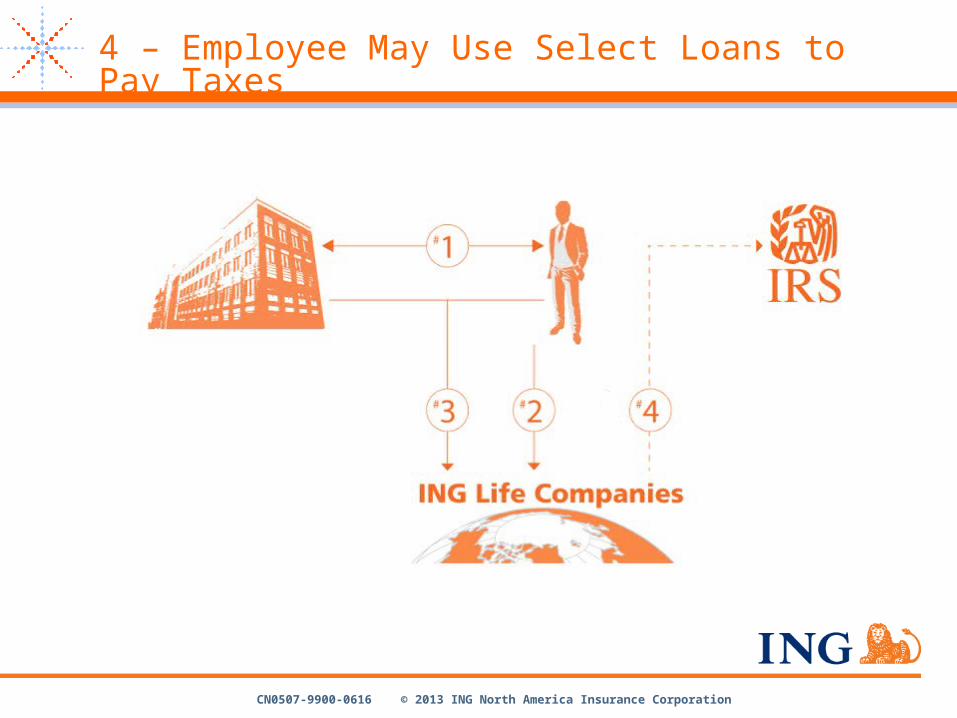

4 – Employee May Use Select Loans to Pay Taxes

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

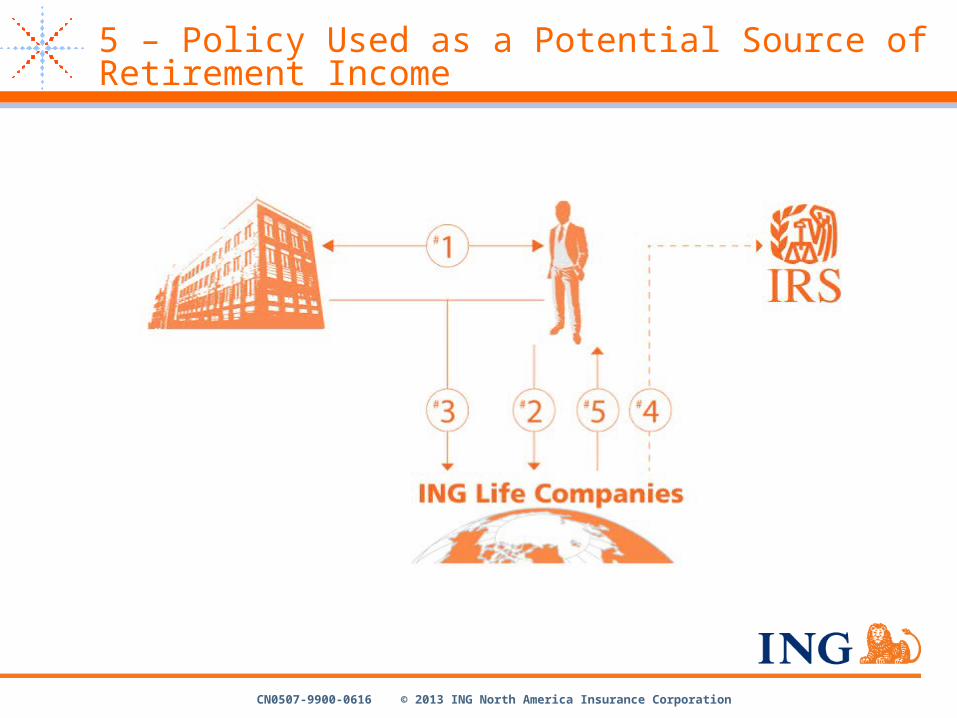

5 – Policy Used as a Potential Source of Retirement Income

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

S.O.L.A.R. Insurance Arrangementsas a Retention Tool

An Employer can fund the purchase of an ING IUL-Global Choice policy for a Key Employee through bonused premium payments Premium payments made by the employer would be treated as

taxable compensation to the employee

Employee can borrow funds from the policy to pay income taxes on premium payments made by the employer

Employer can use the “carrot” of promised future bonus payments which can be used to pay off all or a portion of the balance of Select Loans as an incentive for a Key Employee to remain with the business Incentive-S.O.L.A.R. Insurance Arrangement

Employer can use a supplemental employment agreement with the “stick” of liquidated damages (a penalty the Employee must pay to the Employer if he or she leaves early) to encourage a Key Employee to remain with the business Restricted-S.O.L.A.R. Insurance Arrangement

S.O.L.A.R. Insurance Arrangements can be structured as a Retention Tool for Key Employees:

36

CN0507-9900-0616 © 2013 ING North America Insurance Corporation3737

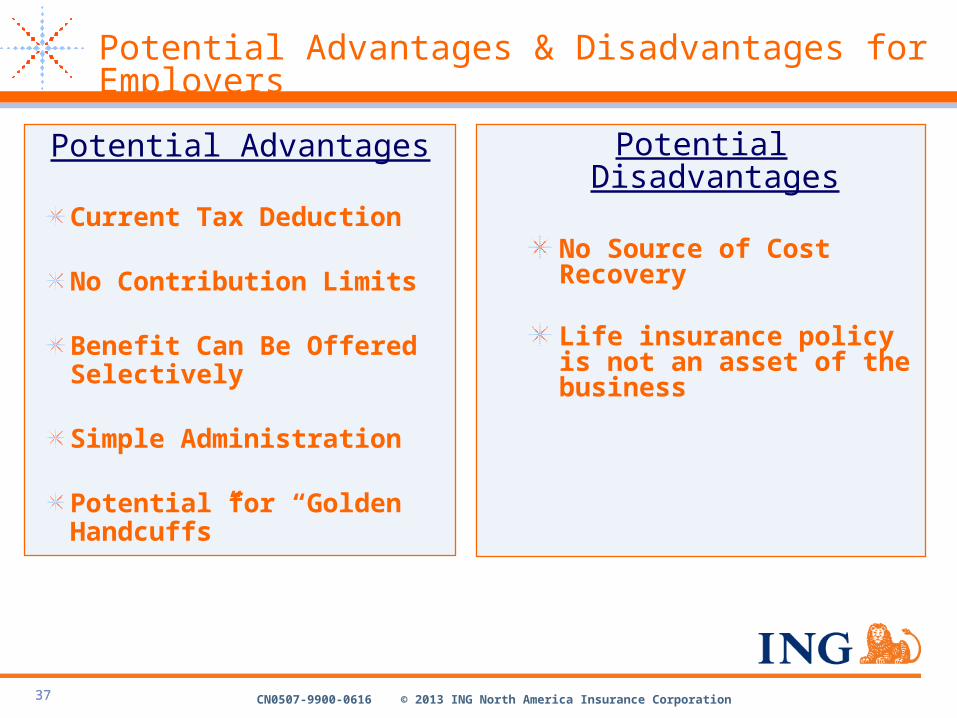

Potential Advantages & Disadvantages for Employers

Potential Advantages

Current Tax Deduction

No Contribution Limits

Benefit Can Be Offered Selectively

Simple Administration

Potential for “Golden Handcuffs”

Potential Disadvantages

No Source of Cost Recovery

Life insurance policy is not an asset of the business

CN0507-9900-0616 © 2013 ING North America Insurance Corporation3838

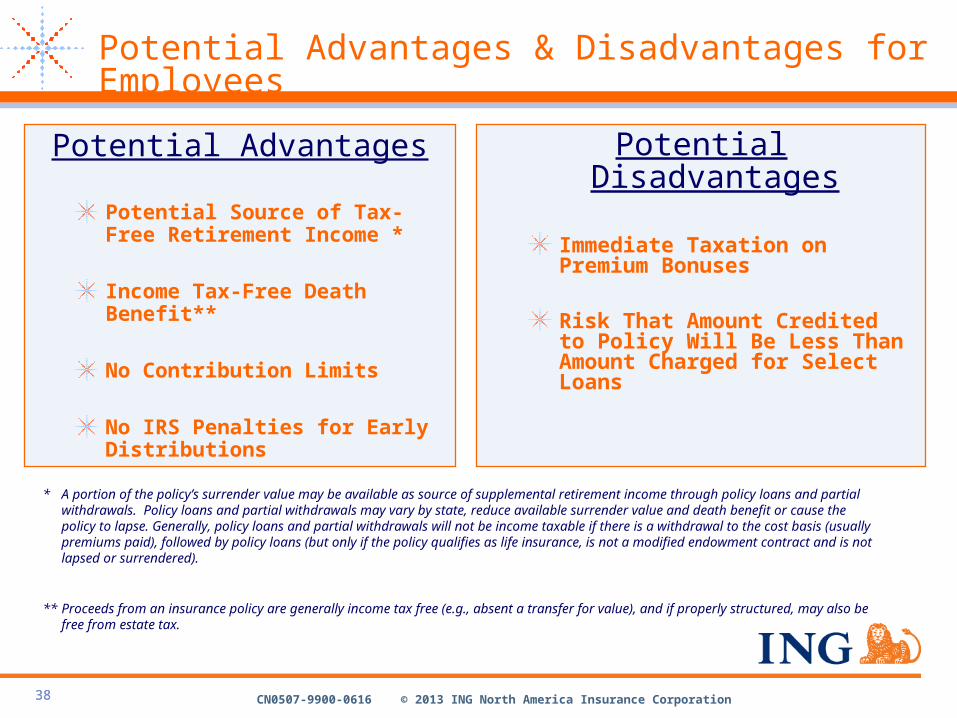

Potential Advantages

Potential Source of Tax-Free Retirement Income *

Income Tax-Free Death Benefit**

No Contribution Limits

No IRS Penalties for Early Distributions

Potential Disadvantages

Immediate Taxation on Premium Bonuses

Risk That Amount Credited to Policy Will Be Less Than Amount Charged for Select Loans

* A portion of the policy’s surrender value may be available as source of supplemental retirement income through policy loans and partial withdrawals. Policy loans and partial withdrawals may vary by state, reduce available surrender value and death benefit or cause the policy to lapse. Generally, policy loans and partial withdrawals will not be income taxable if there is a withdrawal to the cost basis (usually premiums paid), followed by policy loans (but only if the policy qualifies as life insurance, is not a modified endowment contract and is not lapsed or surrendered).

** Proceeds from an insurance policy are generally income tax free (e.g., absent a transfer for value), and if properly structured, may also be free from estate tax.

Potential Advantages & Disadvantages for Employees

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

Many Questions

What would happen to your business if your best employees went to work for

a competitor?

Are you concerned about your company’s ability to pay promised

retirement benefits?

Are your worried about keeping key employees when the

economy improves?

Are you concerned about having to pay income taxes on death benefits paid from employer-owned life insurance?

Is it hard to reward your top employees using a

qualified retirement plan?

Would you like to avoid the complexity and administrative costs of nonqualified deferred

compensation plans?

CN0507-9900-0616 © 2013 ING North America Insurance Corporation

One Potential Solution