Embed Size (px)

Citation preview

CO-OPERATION IN CONTAINER HANDLING: WHAT ARE THE EFFECTS ON ECONOMIES OF SCALE?

Dr. Thierry Vanelslander

Department of Transport and Regional Economics - University of Antwerp Prinsstraat 13

B-2000 Antwerpen Belgium

Tel. -32-3 220 40 34 Fax -32-3 220 43 95

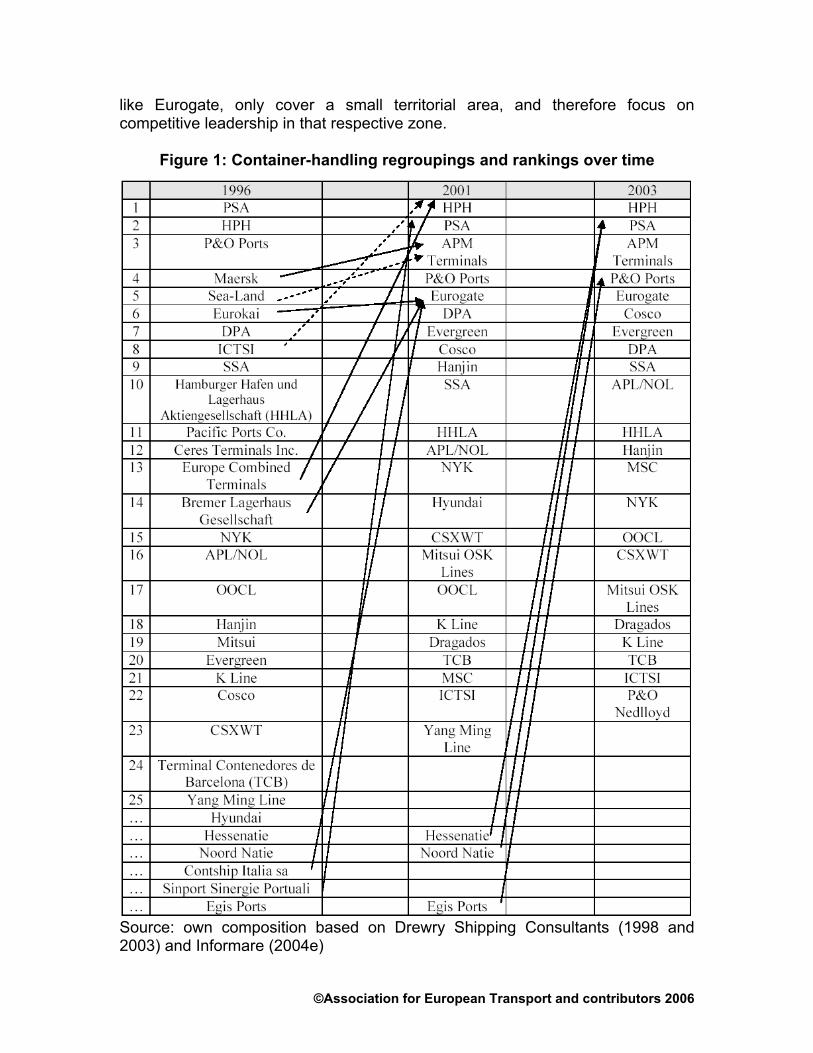

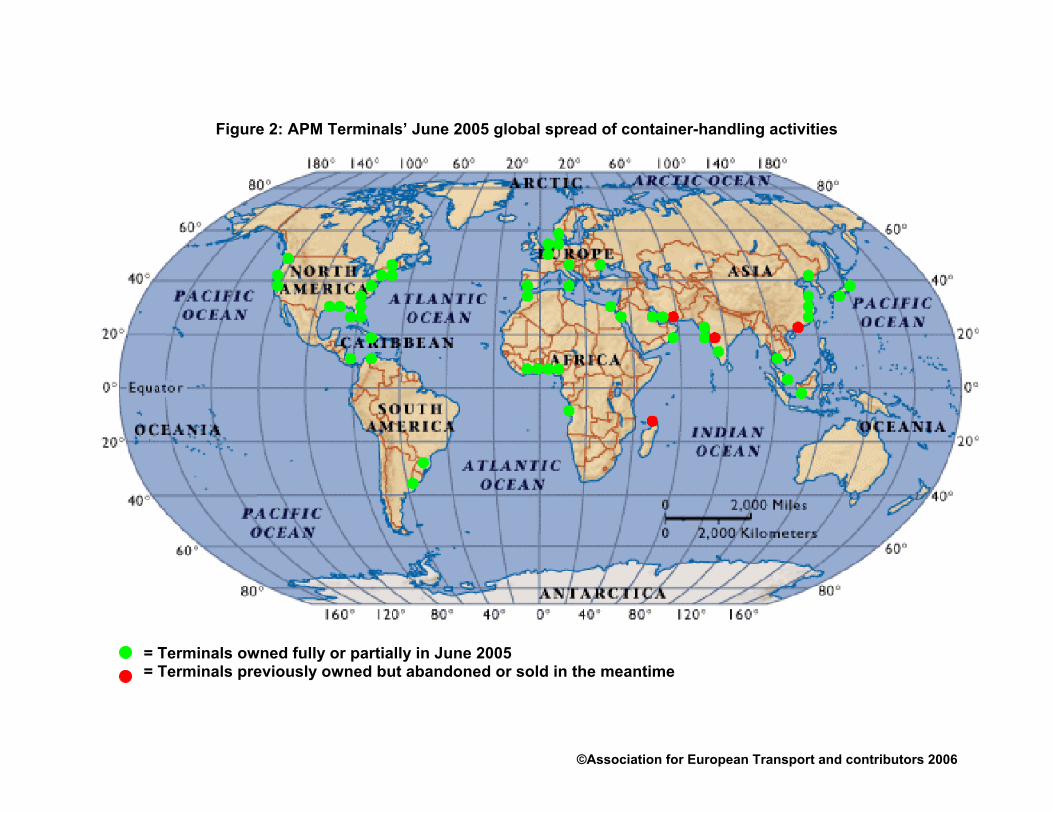

[email protected] 1. RATIONALE AND SETTING It is widely acknowledged that the competitive environment in the maritime and port sector is changing at an ever increasing pace. ‘Globalisation’ and ‘the reinforcement of the world economy’ are frequently used concepts to summarize current economic developments, also and particularly in container handling in sea ports. Container-handling companies have engaged in various forms of expansion, many of which have a co-operative character. Expansion of cargo-handling companies assumes two major forms: at own strength or through some form of co-operation. Expansion at own strength can be internal as well external. Internal expansion at own strength occurs through organic growth of a terminal. External expansion at own strength incorporates greenfield investments as well as the start-up of a subsidiary in cargo handling. Expansion through co-operation involves a wide spectrum of agreements between one or more cargo-handling companies and one or more horizontal or vertical transport chain partners or non-related investors. Common forms of horizontal co-operation aiming at expansion are mergers/acquisitions and joint ventures. Vertical expansionist co-operation occurs when upstream or downstream transport actors are involved, the most frequent types of which are joint ventures with port authorities, shipping lines and hinterland transporters. Also co-operation for expansion with non-transport partners occurs. In recent years, the previous evolution has gained momentum. This quickening pace is illustrated by Figure 1, where the integratory moves of the major container-handling operators are illustrated. The consequences this has on the world container-handling market are shown in Figure 2, where the 2005 geographical location of APM Terminals’ container-handling activities is graphed. Other major operators like Hutchison Port Holdings (HPH), Port of Singapore Authority (PSA) and Dubai Ports World (DPW), the latter of which recently acquired the bulk of P&O Ports’ terminals, have a similar geographical spread of activities. This causes the same operators to compete in various container-handling submarkets all over the globe. Other operators, even very large ones

©Association for European Transport and contributors 2006

like Eurogate, only cover a small territorial area, and therefore focus on competitive leadership in that respective zone.

Figure 1: Container-handling regroupings and rankings over time

Source: own composition based on Drewry Shipping Consultants (1998 and 2003) and Informare (2004e)

©Association for European Transport and contributors 2006

Figure 2: APM Terminals’ June 2005 global spread of container-handling activities

= Terminals owned fully or partially in June 2005 = Terminals previously owned but abandoned or sold in the meantime

©Association for European Transport and contributors 2006

A particularly striking question in this respect deals with the effect that such expansionist moves have on market functioning. It is clear that there is an effect on the individual terminals’ demand for container handling, but there is also hypothesized to be an effect on cost structures. Such effect can, on the one hand, be felt in the fixed part of the costs, leading to for instance lower prices for capital goods installed or shared overhead costs. On the other hand, variable costs can be influenced by co-operation or expansion as they lead for instance to lower prices for variable inputs. In this paper, both effects are assessed for a number of real-life terminal configurations. The results of this paper are useful from an operational as well as from a policy perspective. The absence of a framework for analyzing efficiencies in container handling is for instance felt as a shortcoming by decision makers in the business and in other, related businesses. Pricing of acquisition moves for instance should be based on the efficiencies of the terminal(s) under consideration. The efficiencies of the container-handling companies are furthermore important as they affect the cost of sea-borne trade, and therefore also impact on shipping companies, hinterland transporters and final customers. With respect to policy, it can be stated that competitive developments in container handling determine a country’s wealth through employment and value added. Section 2 delineates the research questions and the methodology to be followed. Section 3 tests whether a fixed-cost effect exists (hypothesis 1), whereas section 4 tests for economies of scale in variable inputs (hypothesis 2). Section 5 assesses the extent to which a fixed-cost effect trades off with a variable-cost effect (hypothesis 3). Section 6 finally summarizes the most important lessons to be drawn. 2. RESEARCH QUESTIONS, METHODOLOGY AND LIMITATIONS The fixed-cost and the variable-cost effect translate into two research questions that are pursued in this paper. Values for fixed capital goods are relatively well-commented in literature, although between-terminal comparisons are not always explicit. Therefore, the paper aims at assessing whether or not a fixed-cost effect occurs in container-handling companies. This effect can be termed an overall company-size effect. With respect to the economic effects of co-operation, a distinction can be made among transaction and size effects. Farrell and Shapiro (2000) denote the first type of effects as synergies, the latter as efficiencies. Efficiencies can but need not be merger-specific. In horizontal mergers or acquisitions, only the size effect occurs. The related hypothesis states that container-handling companies feature economies of company scale.

©Association for European Transport and contributors 2006

Often less clearly identified than the fixed terminal costs are the true operational costs involved in running a container terminal, and their evolution with changing output levels. It is generally accepted that a broad set of variables may impact to a larger or lesser extent on the supply and demand conditions at container terminals. However, the exact extent of such impact and of economies or diseconomies of scale has hardly been assessed in literature. Therefore, it is analyzed in this paper how co-operation and expansion determine container-handling conditions and therefore lead to different operational cost structures. This effect can be measured through the economies of scale in the variable inputs at a terminal, and is therefore termed the terminal-size effect. The corresponding hypothesis states that economies of scale differ in line with different terminal activity size. Trade-offs between fixed costs and operational costs have hardly ever been assessed in literature. Therefore, a third part of the research in this paper questions the existence of such trade-offs. The hypothesis states that there is no trade-off: shared fixed costs usually go in line with larger economies of scale. For testing the first research hypothesis, the methodology consists of comparing companies of different size, i.e. with a different amount of fixed inputs required, on the unit costs that these inputs stand for. For this assessment, companies need to have comparable types of fixed inputs. The respective companies therefore need to be carefully screened with respect to their terminal configurations. 89 variables that were characterized as influential to the level of terminal costs, and that are summarized as policy, scope, chain and terminal-specific variables, serve as a starting point for selecting terminal configurations for the analysis. The terminals of the companies selected have clearly identified values for the policy, scope and terminal-specific variables, as well as the non-size chain variables, whereas the chain-variables that determine company size are left flexible. The real-life cost values corresponding to the fixed inputs are collected by assessing the limited scientific literature available as well as the broad and diverse business-related literature. Testing the second research hypothesis involves simulating and analyzing cost functions at container terminals. In view of the data nature, the engineering technique is used: data are not always comparable or sufficiently available for allowing econometric analyses. For the simulation of the cost functions, a cost typology is elaborated which covers all operational costs. Again, the 89 variables are the basis for selecting and comparing different types of terminals. The configurations selected are tested on their economies of terminal activity scale as they are integrated in larger or smaller companies. In the configurations considered, the variables are assigned different real-life values, the corresponding variable costs of which are again collected mainly from business-related literature.

©Association for European Transport and contributors 2006

The third research hypothesis is tested by combining the analyses used when testing the first two hypotheses. A trade-off between fixed-cost and variable-cost effects is calculated by considering common terminal and container-handling company configurations. A first input in the research process was a literature review, assessing both port-economic and broad industrial-economic literature, theoretical as well as applied to comparable business sectors. The aim of the literature review was to check how previous research has approached questions similar to our research question. Translation to the cargo-handling sector requires sufficient creativity. Further on, a review of literature dealing with the operational and economic characteristics of cargo handling was used for gaining knowledge about the sector. A second research input was meetings with cargo-handling stakeholders, which include cargo-handling operators as well as shippers, shipping companies, hinterland transporters, and other related chain actors. Furthermore, a number of maritime and port experts and industry-watchers were consulted. The aim here was again to get a better understanding of the functioning of the cargo-handling sector. The perspective taken in this thesis is that of the decision maker in cargo handling. Objectives of other chain actors and of activities other than cargo handling are only dealt with in as far as they influence cargo-handling supply and / or demand. The decision maker can be the management of a cargo-handling terminal itself, as well as for instance a shipping company owning and directing a cargo-handling business unit. In that respect, the cargo-handling activity for which expansion decisions are considered needs to be a separable product. A next constraint is on the sea-port activities which compose the cargo-handling product. Paelinck (2001, p. 11) defines cargo handling as “The act of loading and discharging a cargo ship”. As a synonym, the author mentions “stevedoring”. In the course of time however, with evolving technologies and changing relationships within the transport chain, the content of the concept ‘stevedoring’ has broadened from what it originally was. Untill the mid 1900s, there used to be a distinction between the actual (un-)loading (done by stevedores) and warehousing (done by ‘naties’ in Antwerp for instance). Nowadays, both are comprised in what is called ‘stevedoring’ or ‘cargo handling’ (Devos et al., 2004), and also paid for as part of the same product. Unfortunately, there is no existing reference which defines what activities cargo handling at present exactly involves. A review of literature on sea-port activities and on which actor in the transport chain pays for what product, reveals that in most contracts and locations ‘cargo handling’ involves (un-)loading cargo, storing it and delivering it to or receiving it from a hinterland mode. In case of transhipment, inter-modal delivery / receipt as a second move is of course

©Association for European Transport and contributors 2006

replaced by a supplementary ship (un-)loading move. This way, three distinct main cargo-handling products can be distinguished. • Outbound-cargo handling. • Inbound-cargo handling. • Transhipment-cargo handling. Sea-port activities which are not part of cargo handling, but which are sold as separate products, are only considered here if they interfere with cargo-handling supply and / or demand. A third constraint is on the differentiation of the cargo-handling product over time: if different operating-cost conditions apply to cargo handling at different points in time. For instance night, weekend or holiday wages may give rise to as many products as there are different conditions. These products occur sequentially in time, which implies that setting a production quantity for one type of product, for instance cargo handling during day shifts, does not affect capacity available to any other type of product, cargo handling during night shifts for instance. If this capacity independence condition would not be met, one would end up with un-comparable cargo-handling products. A fourth constraint deals with the type of commodities: containers are the focus of this thesis. A container is defined as “a van, flat rack, open top trailer or other similar trailer body on or into which cargo is loaded and transported without chassis aboard ocean vessels; a large rectangular or square container/box of a strong structure that can withstand continuous rough handling from ship to shore and back. It opens from one side, to allow cargo to be stacked and stowed into it” (Paelinck, 2001, p. 16). Containers are usually distinguished from general cargo, dry bulk and liquid bulk (Stopford, 2002, p. 388). Motivations for focusing on containers are that it is the fastest growing cargo type, and that it is a cargo-handling sector with considerable growth and merger and acquisition activity. That some operators deal with several commodity types implies the need to analyze the existence of economies of scope with an impact on container-handling supply and demand. The fifth constraint is on the physical location which is used as a unit for cargo-handling activity: the terminal. The terminal definition used here is one adapted from Port of Miami (2004): “One or more structures comprising a terminal unit, and including, but not limited to wharves, warehouses, covered and/or open storage space, cold storage plants, landings and receiving stations, used for the transmission, care and convenience of cargo in the interchange of same between land and water carriers or between two water carriers”. Such terminal is the largest unit whose cargo-handling activities are grouped into one product, or a set of products if the terminal provides multiple or joint products. Eventually, several cargo-handling companies may run part of the same terminal, and therefore several products may be supplied at the same terminal. In the latter case, the separate companies are the terminal units under consideration in this thesis.

©Association for European Transport and contributors 2006

In relation to the fifth hypothesis, it should be added that modern industrial economics asserts that economies of scale at company level are neither a necessary nor a sufficient condition for a company to be large. Economies are not necessary: companies can be large due to an expanding market, or due to accidental factors (Gibrat’s law). Economies are not always sufficient either: sometimes, contracts may allow obtaining similar results like under a merger or acquisition. These properties of economies of scale at company level will be reflected in economies at terminal level. 3. ECONOMIES OF SCALE AT COMPANY LEVEL For testing the hypothesis on the company-size effect, use is made of a matrix of 89 variables, comprising policy, scope, chain and terminal-specific variables, as identified in Vanelslander (2005). The values for the policy, scope and terminal-specific variables, as well as for the chain variables that are not related to company size, are kept constant. Company-size chain variables that can be allowed to vary are the various relationships between terminals and cargo-handling companies, as described in paragraph one of this paper, and where the focus is on expanding activities. Depending on the operational setting used at the terminal, fixed costs are capital costs, or the intermediary lease payment in case the one-time capital investment was already made before the operator got control of the terminal, and furthermore also the maintenance costs. Lease payments may not be fixed but may vary with the use that is made of the terminal: efficient use is then stimulated. Eventually, labour may be fixed in case the labour setting is not adapted to the quantity of containers handled. In order to calculate capital costs, following specifications can be made. • A distinction should be made among new and used equipment. • Two possibilities can be considered: a situation without lease agreement,

where the total capital cost is the land and terminal cost plus the equipment cost, whereas in case of a lease agreement, the capital cost equals just the equipment cost.

• A scenario with confined dredging and one with unconstrained dredging can be in place. The second has a lower unit cost than the first.

• The container yard construction price should be split up into a container yard, a storage yard and a shed yard price.

• Dredging volume is assumed to be 32,000,000m³, like it was in for the London Gateway project.

• It can be assumed that buying used equipment is less expensive than buying new equipment.

• Superstructure settings can differ, even for terminals with equal surface. • First-generation, Panamax or Post-panamax container gantry cranes, or a

combination of them, can be installed.

©Association for European Transport and contributors 2006

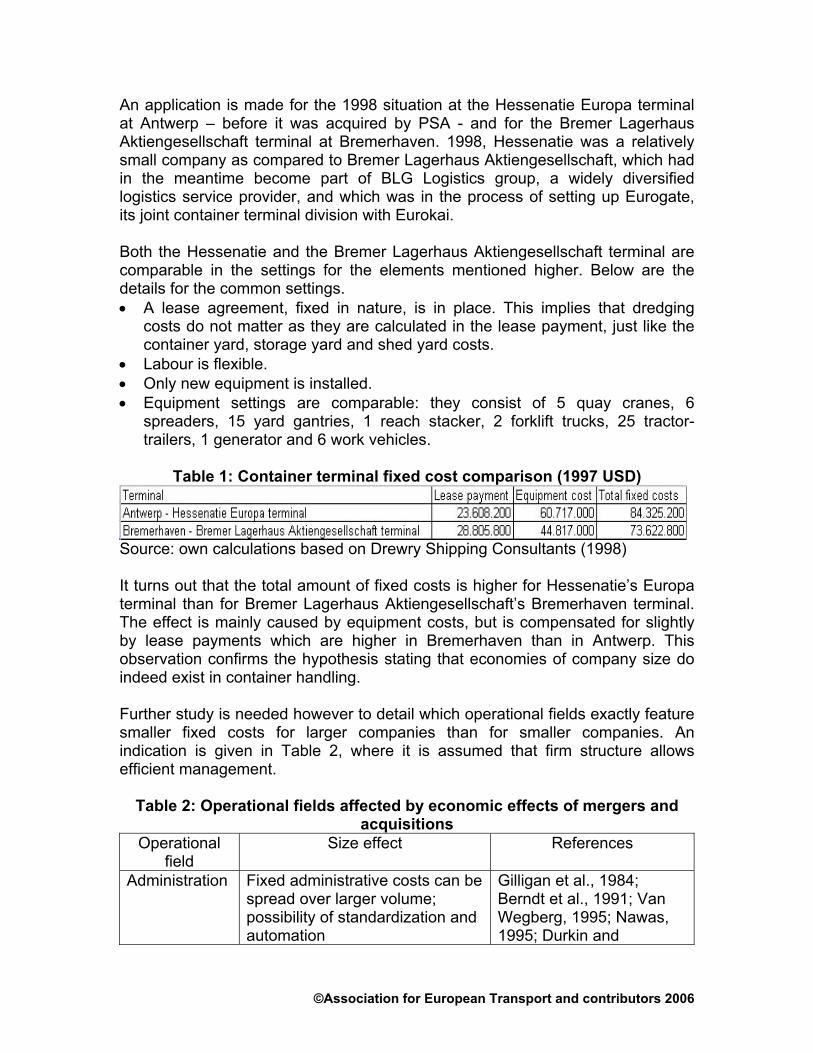

An application is made for the 1998 situation at the Hessenatie Europa terminal at Antwerp – before it was acquired by PSA - and for the Bremer Lagerhaus Aktiengesellschaft terminal at Bremerhaven. 1998, Hessenatie was a relatively small company as compared to Bremer Lagerhaus Aktiengesellschaft, which had in the meantime become part of BLG Logistics group, a widely diversified logistics service provider, and which was in the process of setting up Eurogate, its joint container terminal division with Eurokai. Both the Hessenatie and the Bremer Lagerhaus Aktiengesellschaft terminal are comparable in the settings for the elements mentioned higher. Below are the details for the common settings. • A lease agreement, fixed in nature, is in place. This implies that dredging

costs do not matter as they are calculated in the lease payment, just like the container yard, storage yard and shed yard costs.

• Labour is flexible. • Only new equipment is installed. • Equipment settings are comparable: they consist of 5 quay cranes, 6

spreaders, 15 yard gantries, 1 reach stacker, 2 forklift trucks, 25 tractor-trailers, 1 generator and 6 work vehicles.

Table 1: Container terminal fixed cost comparison (1997 USD)

Source: own calculations based on Drewry Shipping Consultants (1998) It turns out that the total amount of fixed costs is higher for Hessenatie’s Europa terminal than for Bremer Lagerhaus Aktiengesellschaft’s Bremerhaven terminal. The effect is mainly caused by equipment costs, but is compensated for slightly by lease payments which are higher in Bremerhaven than in Antwerp. This observation confirms the hypothesis stating that economies of company size do indeed exist in container handling. Further study is needed however to detail which operational fields exactly feature smaller fixed costs for larger companies than for smaller companies. An indication is given in Table 2, where it is assumed that firm structure allows efficient management.

Table 2: Operational fields affected by economic effects of mergers and acquisitions

Operational field

Size effect References

Administration Fixed administrative costs can be spread over larger volume; possibility of standardization and automation

Gilligan et al., 1984; Berndt et al., 1991; Van Wegberg, 1995; Nawas, 1995; Durkin and

©Association for European Transport and contributors 2006

Elliehausen, 1998; Van den Bossche, 2002d

Contracting Bargaining power in negotiating; avoiding intermediaries

Hagedoorn, 1993; Nooteboom, 1999

Equipment Sufficient equipment volumes to bargain input prices; equipment can be used more efficiently

Caves et al., 1984 ; Clark, 1984; Beddow, 2001; Cordts, 2001

Handling operations - technology

Possibility to standardize within constraints imposed by shipping companies; product specialization is efficient

Peltzman, 1977; Hagedoorn, 1993; Contractor and Lorange, 1988; Hennart, 1988; Encaoua, 1991; Van Wegberg, 1995; Peters, 2003

ICT ICT setup, installation and maintenance costs can be spread over larger volume; possibility of standardization; e-commerce more efficient and more attractive in larger network; sufficient volume to have in-house development, installation and maintenance of systems

Contractor and Lorange, 1988; Borys and Jemison, 1989; Hagedoorn, 1993; Van Wegberg, 1995; Nooteboom, 1999; Oum, Zhang and Zhang, 2000; Beddow, 2001; Van den Bossche, 2002d

Labour In-house training is efficient due to job specialization

Contractor and Lorange, 1988; Beddow, 2001

Marketing Fixed administrative costs can be spread over larger volume; more terminals means more attractive network; possibility of standardization; sufficient volume to do promotion with own staff

Devine et al., 1985; Hagedoorn, 1993; Van Wegberg, 1995; Cordts, 2001; Van den Bossche, 2002b

R&D Technology development costs can be spread over larger volume; sufficient volume to have knowledge in house

Nooteboom, 1999; Van den Bossche, 2002b

Security Fixed security costs to be spread over larger volume; possibility of standardization and automation; security provision can efficiently be provided in house

Van Wegberg, 1995; De Lloyd, 2003

A number of merger and acquisition effects only materialize in specific contexts due to site specificity, physical asset specificity or human operator specificity (Stewart, Harris and Carlton, 1984; Borys and Jemison, 1989, p. 77; Berger and Humphrey, 1994, p. 6; Williamson and Masten, 1999). Effects can also depend on the acquirer or merging partner: some are universal (occur with all partners),

©Association for European Transport and contributors 2006

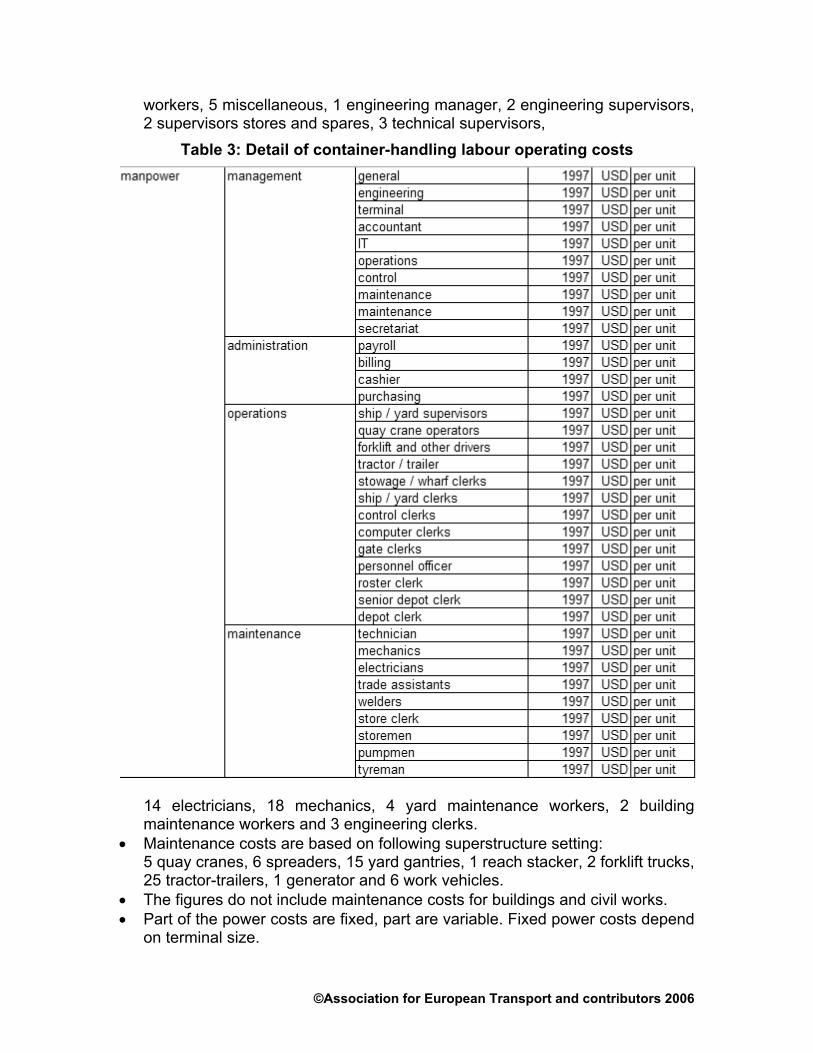

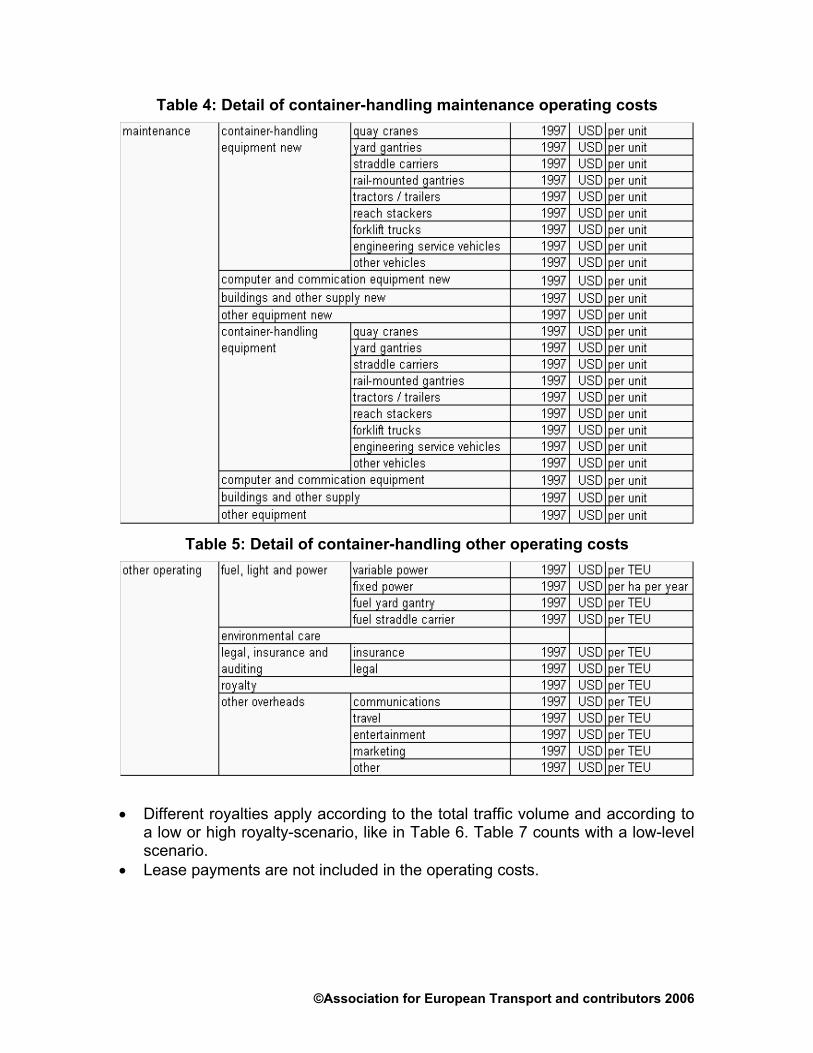

some are endemic (occur with some partners), and some are unique (to one specific partner) (Copeland et al., 2000, p. 121). 4. ECONOMIES OF SCALE AT TERMINAL LEVEL Just like for the company-size effect, testing the terminal activity-size effect requires use of the 89-variable matrix from Vanelslander (2005). Again, values for the policy, scope and terminal-specific variables are kept constant, just like all chain variables not related to company size. Testing the second hypothesis requires calculation of operational cost functions and economies of scale at the terminal level. The terminal operating cost structure is, in both cases, split up in three elements: • Labour. • Maintenance. • Other operating costs. In the labour category (Table 3), management, administration, operations as well as maintenance staff are considered. This implies all these functions are performed in-house and are not sourced in. With respect to maintenance (Table 4), there is a distinction between container-handling equipment, computer and communication equipment, buildings, and other equipment. Under other operating items are analysed fuel, light and power, environmental care, legal instruments, insurance, auditing, and other overheads. Other overheads are detailed like in Table 5. 1997 Data from Drewry Shipping Consultants (1998) are used for each of the cost items. The Drewry figures are reprocessed to calculate total labour, maintenance and other operating costs, total costs and average costs, all of them on a yearly basis. The aggregate figures are shown in Table 7. Following specifications are used. • In view of data availability, calculations are done for a 600,000 TEU capacity

container terminal featuring 16ha. This situation conforms best to the 1997 situation at both the Hessenatie Europa terminal at Antwerp and the Bremer Lagerhaus Aktiengesellschaft terminal at Bremerhaven.

• Manpower costs are based on following labour setting: 1 ceo, 1 terminal, 1 financial controller, 1 finance manager, 3 seniores accountants, 10 accounts clerks, 1 IT manager, 3 IT officer, 4 IT systems support, 1 marketing manager, 2 commercial services manager, 1 human resources manager, 1 supervisor human resources, 1 security manager, 3 securities, 4 secretaries, 6 general assistants, 1 assistant operations manager, 4 supervisors, 4 planning supervisors, 6 planning clerks, 48 general clerks, 12 gate clerks, 58 quay crane drivers, 71 yard gantry drivers, 112 tractor / trailer drivers, 55 forklift drivers, 4 foremen, 48 lashers, 10 general

©Association for European Transport and contributors 2006

workers, 5 miscellaneous, 1 engineering manager, 2 engineering supervisors, 2 supervisors stores and spares, 3 technical supervisors,

Table 3: Detail of container-handling labour operating costs

14 electricians, 18 mechanics, 4 yard maintenance workers, 2 building maintenance workers and 3 engineering clerks.

• Maintenance costs are based on following superstructure setting: 5 quay cranes, 6 spreaders, 15 yard gantries, 1 reach stacker, 2 forklift trucks, 25 tractor-trailers, 1 generator and 6 work vehicles.

• The figures do not include maintenance costs for buildings and civil works. • Part of the power costs are fixed, part are variable. Fixed power costs depend

on terminal size.

©Association for European Transport and contributors 2006

Table 4: Detail of container-handling maintenance operating costs

Table 5: Detail of container-handling other operating costs

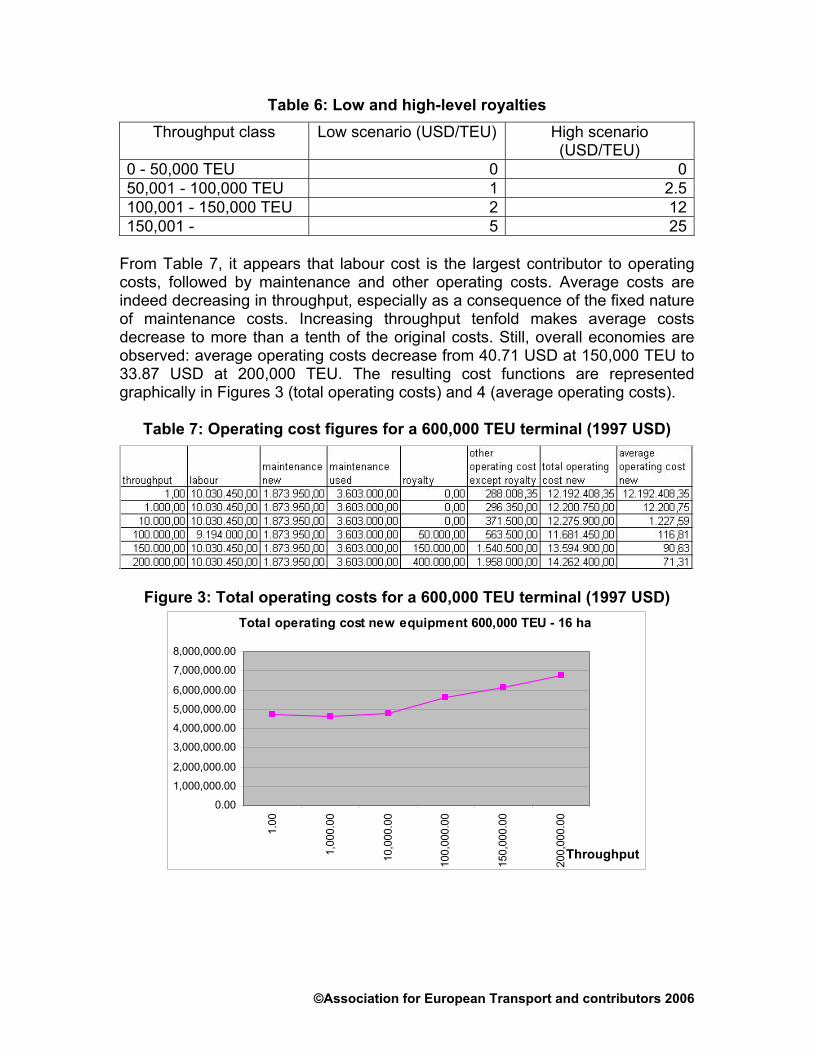

• Different royalties apply according to the total traffic volume and according to a low or high royalty-scenario, like in Table 6. Table 7 counts with a low-level scenario.

• Lease payments are not included in the operating costs.

©Association for European Transport and contributors 2006

Table 6: Low and high-level royalties Throughput class Low scenario (USD/TEU) High scenario

(USD/TEU) 0 - 50,000 TEU 0 050,001 - 100,000 TEU 1 2.5100,001 - 150,000 TEU 2 12150,001 - 5 25

From Table 7, it appears that labour cost is the largest contributor to operating costs, followed by maintenance and other operating costs. Average costs are indeed decreasing in throughput, especially as a consequence of the fixed nature of maintenance costs. Increasing throughput tenfold makes average costs decrease to more than a tenth of the original costs. Still, overall economies are observed: average operating costs decrease from 40.71 USD at 150,000 TEU to 33.87 USD at 200,000 TEU. The resulting cost functions are represented graphically in Figures 3 (total operating costs) and 4 (average operating costs).

Table 7: Operating cost figures for a 600,000 TEU terminal (1997 USD)

Figure 3: Total operating costs for a 600,000 TEU terminal (1997 USD) Total operating cost new equipment 600,000 TEU - 16 ha

0.00

1,000,000.00

2,000,000.00

3,000,000.00

4,000,000.00

5,000,000.00

6,000,000.00

7,000,000.00

8,000,000.00

1.00

1,00

0.00

10,0

00.0

0

100,

000.

00

150,

000.

00

200,

000.

00

Throughput

©Association for European Transport and contributors 2006

Figure 4: Average operating costs for a 600,000 TEU terminal (1997 USD) Average operating cost new equipment 600,000 TEU - 16 ha

0500

100015002000250030003500400045005000

1,00

0.00

10,0

00.0

0

100,

000.

00

150,

000.

00

200,

000.

00

Throughput

It is therefore found that economies of scale at the terminal level do indeed occur. It then remains to be seen whether there is a difference in the level of economies to be gained depending on the size of the company and the degree and type of co-operation agreements in place. To test this, we apply the previous calculations to the two terminals considered earlier: the Hessenatie Europa terminal and the Bremer Lagerhaus Aktiengesellschaft Bremerhaven terminal. Operational cost calculation is done for a throughput of 1,500,000 TEU. At this level, the Hessenatie terminal has an operational cost of 18,095,506 USD, whereas the Bremer Lagerhaus Aktiengesellschaft terminal has an operational cost of 17,258,183 USD. Similar calculations could be done for other throughput levels. It will in each case be observed that the cost for the Bremer Lagerhaus Aktiengesellschaft is smaller than the corresponding cost for the Hessenatie terminal. This affirms the hypothesis that terminals which are part of a larger network, and/or which have more co-operative ties, feature lower operational costs. 5. TRADE-OFFS BETWEEN FIXED AND VARIABLE COSTS In the previous paragraphs, it has on the one hand been observed that terminals which are embedded in a larger network do feature economies of company-size compared to stand-alone terminals, and that on the other hand all terminals show economies of scale in terminal size, but that the terminals embedded in a network have lower operational costs than their non-network counterparts. Therefore, it can be concluded that there is no trade-off but rather a mutual re-inforcement between the effects of fixed and variable costs. To extend the analysis, a comparison is made between fixed and operational costs of two recent terminals which are about to be built. One is 140ha terminal,

©Association for European Transport and contributors 2006

the other is a smaller terminal with a surface of 36ha. Taking into account their respective infrastructure and equipment settings, the operational costs from Table 8 are obtained. It can be observed that there too, economies of scale at the terminal level prevail. Table 8: Total and average operational costs for two recent terminal types

(1997 USD)

Table 9 puts the previous operational costs into perspective, and calculates operational costs for the designed throughput levels of both the 140ha and the 36ha terminal. First of all, it turns out that annual operational costs under an own- construction scenario are about 40 times smaller than capital costs for a 140ha terminal, and about 80 times in case of a 36ha terminal. Second, it can also be observed that for a terminal which is about four times as small as the 140ha terminal, corresponding operating costs are about four times as small too. Capital costs are only half those of the larger terminal. Therefore, there are clear economies in terminal capacity too, especially with respect to the capital cost.

Table 8: Operational costs for two recent terminal types (1997 USD)

6. CONCLUSION Three hypotheses have been tested in this paper. The first hypothesis, on the existence of economies of scale at the company level, is confirmed: the larger the network which a terminal is part of, the lower the level of fixed costs will normally be. With respect to the second hypothesis, on economies of scale at the terminal level and the specific impact of networks and co-operation agreements, the answer was affirmative again: economies of scale are observed in all situations assessed, and larger networks usually imply lower operational costs. As to the trade-off between fixed and variable costs, the answer is that there is no trade-off but rather a re-inforcement between the effect of network size and co-operation on the cost level. Capital costs usually are a multiple of the annual operating

©Association for European Transport and contributors 2006

costs, although the situation depends on the specific setting. Having a lease agreement in place for instance will usually lessen the gap between capital and operational costs. Further study needs to be done however to get a better insight in the exact determinants of the previous observations. Costs, capital as well as operational, need to be further disaggregated in order to assess what operational fields contribute most to economies of scale in container handling.

BIBLIOGRAPHY Beddow, M. (2001) All change in Antwerp, Containerisation International, edition January, 62-64 Berger, A.N., and Humphrey, D.B. (1994) Bank Scale Economies, Mergers, Concentration, and Efficiency: The U.S. Experience, Center for Financial Institutions, Wharton School, University of Pennsylvania Berndt, E.R., Friedlaender, A.F., Wang-Chiang, J.S., and Vellturo, C.A. (1991) Mergers, Deregulation and Cost Savings in the U.S. Rail Industry, Working Paper, National Bureau of Economic Research Borys, B., and Jemison, D.B. (1989) Hybrid arrangements as strategic alliances: theoretical issues in organizational combinations, Academy of Management Review, 14 (2) 234-249 Caves, D.W., Christensen, L.R., and Tretheway, M.M. (1984) Economies of density versus economies of scale: why trunk and local service airline costs differ, The RAND Journal of Economics, 15 (4) 471-489 Clark, J.A. (1984) Estimation of economies of scale in banking using a generalized functional form, Journal of Money, Credit and Banking, 16 (1) 53-68 Contractor, F.J., and Lorange, P. (1988) Why should firms co-operate? The strategy and economics basis for cooperative ventures, in Contractor, F.J., and Lorange, P. (Eds.), Cooperative Strategies in International Business – Joint Ventures and Technology Partnerships between Firms, Lexington Books, Massachusetts Copeland, T., Koller, T., and Murrin, J. (2000) Valuation – Measuring and Managing the Value of Companies, 3rd edition, John Wiley & Sons Inc., New York Cordts, M. (2001) BALTICOM - Deliverable 3.3 – The Effect of Technological and Organizational Innovation in the European Logistics Sector on Port Economic

©Association for European Transport and contributors 2006

Areas – Recommendations for Spatial and Regional Planning, http://www.balticom.org/download/reports/Deliverable_3_3.pdf De Lloyd (2003) Nog lang geen oligopolie in Europese logistiek, edition 18 March, 1-3 Devos, G., Asaert, G., and Suykens, F. (2004) De Antwerpse Naties, Lannoo, Antwerp Drewry Shipping Consultants (1998) World Container Terminals – Global Growth and Private Profit, London Drewry Shipping Consultants (2003) Annual Review of Global Container Terminal Operators, London Durkin, T.A., and Elliehausen, G.E. (1998) The cost structure of the consumer finance industry, Journal of Financial Services Research, 13 (1) 71-86 Encaoua, D. (1991) Liberalizing European airlines – cost and factor productivity evidence, International Journal of Industrial Organization, 9 (1) 109-124 Farrell, J., and Shapiro, C. (2000) Scale economies and synergies in horizontal merger analysis, Antitrust Law Journal, 68 (3) 685-710 Gilligan, T., Smirlock, M., and Marshall, W. (1984) Scale and scope economies in the multi-product banking firm, Journal of Monetary Economics, 13 (1) 393-405 Hagedoorn, J. (1993) Understanding the rationale of strategic technology partnering: interorganizational modes of cooperation and sectoral differences, Strategic Management Journal, (14) 371-385 Hennart, J.-F. (1988) A transaction costs theory of equity joint ventures”, Strategic Management Journal, 9 (1) 361-374 Informare (2004e) Studi e ricerche, http://www.informare.it/news/cisco/2004/200411duk.asp Nawas, M.E. (1995) Management van Fusie en Integratie: de Vorming van ABN-AMRO, Tilburg University Press, Tilburg Nooteboom, B. (1999) Inter-firm Alliances – Analysis and Design, New York, Routledge, 239 p. Oum, T., Zhang, A., and Zhang, Y. (2000) Socially optimal capacity and capital structure in oligopoly, Journal of Transport Economics and Policy, 34 (1) 55-68

©Association for European Transport and contributors 2006

©Association for European Transport and contributors 2006

Paelinck, H. (2001) Glossary of Terms, Antwerp Peltzman, S. (1977) The gains and losses from industrial concentration, Journal of Law and Economics, 20 (2) 229-264 Peters, C. (2003) Evaluating the Performance of Merger Simulation: Evidence from the U.S. Airline Industry, The Center for the Study of Industrial Organization at Northwestern University, Working paper n° 0032, http://www.csio.econ.northwestern.edu/Papers/2003/CSIO-WP-0033.pdf Port of Miami (2004) Port Tariff, http://www.co.miami-dade.fl.us/portofmiami/ Stewart, J.F., Harris, R.S., and Carlton, W.T. (1984) The role of market structure in merger behaviour, The Journal of Industrial Economics, 32 (3) 293-312 Stopford, M. (2002) Maritime Economics, Routledge, London Van den Bossche, B. (2002d) Burger herstructureert om beter in te spelen op toekomstige ontwikkelingen, De Lloyd, edition 10 September Vanelslander, T. (2005) The Economics behind Co-operation and Competition in Sea-port Container Handling, Ph.D thesis, University of Antwerp, Antwerp Van Wegberg, M. (1995) Mergers and Alliances in the Multimedia Market, Research Memorandum, n° 7 Williamson, O.E. and Masten, S.E. (1999) The Economics of Transaction Costs, Edward Elgar, Cheltenham