Embed Size (px)

Citation preview

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

CO2e Accounting and Forest: Principles, Methods, and Challenges for

Accounting Professional with reference to India

Dr. Prashant Kumar

Professor Faculty of Commerce, Banaras Hindu University, Varanasi, India

Tara Prasad Upadhyaya

Research Scholar, Faculty of Commerce, Banaras Hindu University, Varanasi, India

Abstract

Global awareness about climate changes brought countries on a round table known as Kyoto

Protocol. Because of the interest and responsibilities towards planet parties involved are trying to

estimate and manage the CO2e, the total amount of carbon emitted during the production, processing,

and distribution of a product as well as forest change. The final outcome of this exercise is called the

product‟s „carbon footprint‟ and the exercise itself is known as „carbon accounting‟. Carbon

footprints are expressed in units of CO2 equivalents (CO2e). Though there is a cacophony concerned

to universally accepted principles of carbon accounting and standards but it is an accounting practice

of making scientifically robust and verifiable measurements of GHG emissions. The Kyoto protocol

has paves the way for its principles, methods, and practices in the field of GHGs emission field.

There are three types of forest carbon accounting methods as developed: stock accounting, emissions

accounting and project emission reductions accounting. Fuzzy accounting environment, question

about asset type and accounting value (cost or fair market value of CERs) are still in question for

carbon accounting in India. Besides this, the various other challenges of forest carbon accounting

could be pointed out as its versatile definition, lack of measurement of direct human induced impact

on forest and changing pattern of harvested wood product.

Key words: Carbon accounting, CO2e, Forest carbon accounting and Kyoto Protocol

Introduction

Forest cover 31% of the total land area, primary forest account for 36% of forest area, 30% of forest

are used for production of wood and non-wood products, the livelihoods of over 1.6 billion people

depend on forest, forest are home to 80% of our terrestrial biodiversity, trade in forest products

estimated at $327 billion in 2004, forest are home to 300 million of people around the world (UNDP,

2010). Sequestering and emitting carbon dioxide (CO2) is a natural phenomenon of Forests and is

leading reasons of climate change due to GHGs. There is no single definition globally, and countries

have tended to define their forests according to (i) legal, administrative, or cultural requirements; (ii)

land use; (iii) canopy cover; or (iv) carbon density (biomass) (Neef et al., 2006). The majority of

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

definitions are based on a single variable canopy1 cover exceeding a given minimum threshold.

Canopy cover in this context is defined as „the percentage of the ground covered by a vertical

projection of the outermost perimeter of the natural spread of the foliage of plants‟ (IPCC, 2003).

Generally, „forest‟ means an area having trees and other vegetation, while ecologically the areas

without tree cover not put to human use, like grassy blanks in a wildlife sanctuary or the rocky areas

in the forests constitute an integral part of the forested eco-system (FSI, 2009). In an important study

(Brenton, Jones, & Jensen, 2009) stated that concern about climate change has stimulated interest in

estimating the total amount of carbon emitted during the production, processing and distribution of a

product. The final outcome of this exercise is called the product‟s „carbon footprint‟ and the exercise

itself is known as „carbon accounting‟. Carbon footprints are expressed in units of CO2 equivalents

(CO2e). This is because different GHGs have different impacts on the atmosphere so-called

radioactive forcing. The GHG data reported by Parties contain estimates for direct greenhouse gases,

such as: CO2 - Carbon dioxide, CH4 - Methane, N2O - Nitrous oxide, PFCs – Per fluorocarbons,

HFCs – Hydro fluorocarbons, SF6 - Sulphur hexafluoride, as well as for the indirect greenhouse

gases such as SO2, NOx, CO and NMVOC (UNFCC, 1992). A net release of CO2 from forests emits

CO2 into the atmosphere (source), while a net CO2 uptake in forests removes CO2 from the

atmosphere (sink) (Kurz, Apps, Benfield, & Stinson, 2002). Required information to analyze forest

CO2 stocks and stock changes must be based on the best available science and compliant with

evolving international CO2 accounting rules (Kurz, Apps, Benfield, & Stinson, 2002). The Green

House Gases are changing the earth‟s energy balance and are already resulting in observed impacts

on the global climate system (Houghton, J.T.,Y.Ding, D.J.Griggs et al, 2001). Terrestrial ecosystems

play an important role in the global carbon cycle. Counteracting deforestation by paying for the

stored carbon is being regarded as a cost-efficient approach to reduce the global greenhouse gas

emissions (IPCC, 2007) and (IUFRO, 2009). The net flux of CO2 from changes in land use is

important in the global carbon cycle for a number of reasons. First, changes in land use have caused

a net release of carbon to the atmosphere over the last centuries and decades. Estimates vary,

however, and the annual net release is more uncertain than other terms in the global carbon budget

(Le Qu er e et al., 2009) and (Canadell et al., 2007); Le Qu er e et al., 2009). If the net flux of carbon

from land-use change were well enough known, it would help constrain both the residual terrestrial

flux and trends in the air borne fraction (Knorr, 2009). Ideally, changes in land use would be defined

broadly to include not only changes in land cover (e.g. conversion of forest to cropland), but all

forms of land management (Houghtan, 2010). During the first Kyoto commitment period (2008-

1 The uppermost layer in a forest, formed by the crowns of the trees is called crown canopy.

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

2012), tree plantation projects were considered eligible for carbon credits under the Clean

Development Mechanism (CDM), whereas sustainable forest management was excluded from the

CDM for a number of political, practical and ethical reasons (Griffiths, 2007). Since carbon

emissions from deforestation represent close to one fifth of all anthropogenic greenhouse gases, an

initiative was created at the Climate Conference in Montreal in 2006 to “Reduce Emissions from

Deforestation and Degradation” (REDD)2. REDD carbon credits are at the moment included only on

the voluntary market. The process of respiration and decaying of organic matter or burning of

biomass caused forests to release carbon (UNEP, 2009).

Methodology and objective

Carbon accounting with contemporary to Forest carbon accounting in the world with special

reference to India is the subject matter of this study. The following is the main objective has been

considered under the study:

To assess the present status of carbon accounting as well as forest carbon accounting around the

world with reference to Indian present context of carbon accounting and forest carbon

accounting. While studying the carbon accounting concept and practices qualitative aspect plays

a dominating role in this study.

Methodology:

Descriptive study has been adopted to become familiar with the carbon accounting terminology,

methodology, and side by side the forest carbon accounting through different and available literature.

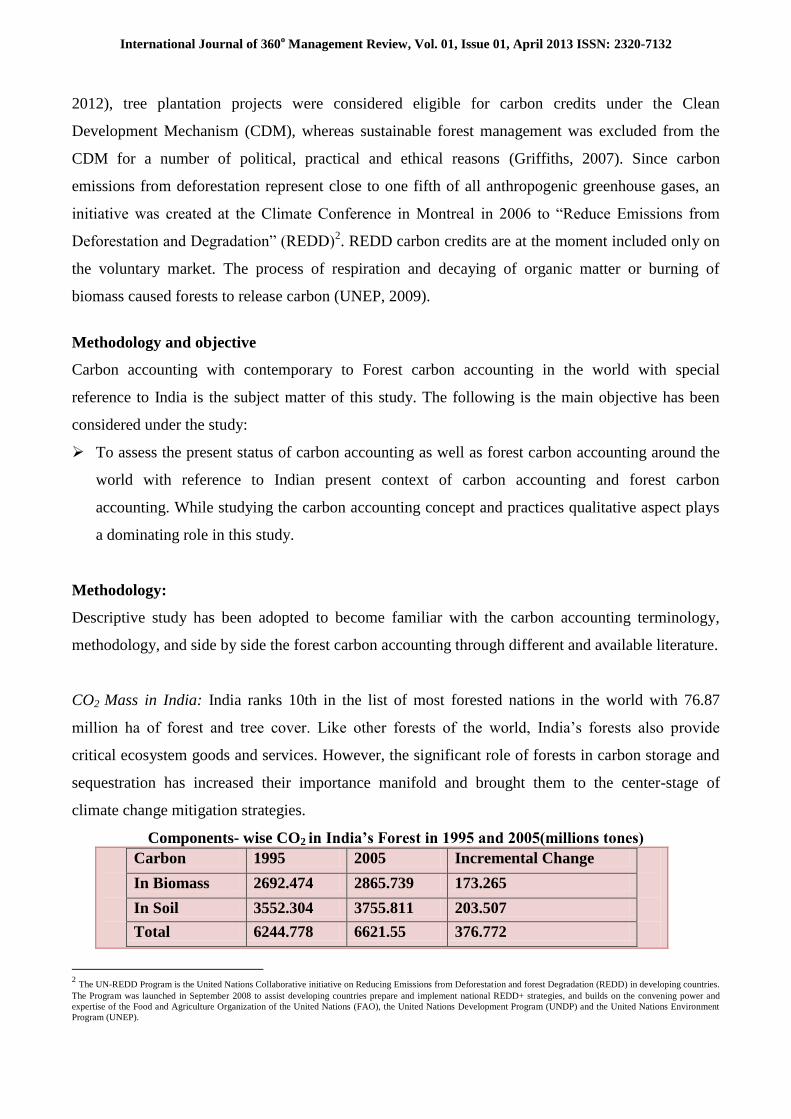

CO2 Mass in India: India ranks 10th in the list of most forested nations in the world with 76.87

million ha of forest and tree cover. Like other forests of the world, India‟s forests also provide

critical ecosystem goods and services. However, the significant role of forests in carbon storage and

sequestration has increased their importance manifold and brought them to the center-stage of

climate change mitigation strategies.

Components- wise CO2 in India’s Forest in 1995 and 2005(millions tones)

Carbon 1995 2005 Incremental Change

In Biomass 2692.474 2865.739 173.265

In Soil 3552.304 3755.811 203.507

Total 6244.778 6621.55 376.772

2 The UN-REDD Program is the United Nations Collaborative initiative on Reducing Emissions from Deforestation and forest Degradation (REDD) in developing countries.

The Program was launched in September 2008 to assist developing countries prepare and implement national REDD+ strategies, and builds on the convening power and

expertise of the Food and Agriculture Organization of the United Nations (FAO), the United Nations Development Program (UNDP) and the United Nations Environment

Program (UNEP).

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

The analysis showed that there is improvement in forest carbon stocks on temporal basis from 1995

to 2005. The difference of 376.772 mt between figures of 1995 and 2005 shows the incremental

carbon accumulation in India‟s forests during the period. On yearly basis, the addition of carbon was

37.677 mt ≈ 37.68 mt (say), which means an annual removal of 138.15 mt CO2 eq (Kishwan,

Pandey, & Dadhwal, 2009).

Kyoto protocol and Carbon Accounting: Kyoto Protocol is an agreement made under the United

Nations Framework Convention on Climate Change (UNFCCC). The treaty was negotiated in Kyoto,

Japan in December 1997, opened for signature on March 16, 1998, and closed on March 15, 1999.

The agreement came into force on February 16, 2005, under which the industrialized countries will

reduce their collective emissions of greenhouse gases by 5.2% compared to the year 1990 (but note

that, compared to the emissions levels that would be expected by 2010 without the Protocol, this

target represents a 29% cut).

CDM: The Clean Development Mechanism (CDM) is an arrangement under the Kyoto Protocol

allowing industrialized countries with a greenhouse gas reduction commitment to invest in emission

reducing projects in developing countries as an alternative to what is generally considered more

costly emission reductions in their own countries. The developed country would be given credits

(Carbon Credits) for meeting its emission reduction targets, while the developing country would

receive the capital and clean technology to implement the project (KYOTO MECHANISM Article

12).

Carbon Credits: Carbon credits are certificates issued to countries that reduce their emission of GHG

(greenhouse gases) which causes global warming. Carbon credits are measured in units of certified

emission reductions (CERs). Each CER is equivalent to one tone of carbon dioxide reduction

(KYOTO MECHANISM Article 17).

IET: Under IET (International Emissions Trading) mechanism, countries can trade in the

international carbon credit market. Countries with surplus credits can sell the same to countries with

quantified emission limitation and reduction commitments under the Kyoto Protocol. Developed

countries that have exceeded the levels can either cut down emissions, or borrow or buy carbon

credits from developing countries (KYOTO MECHANISM Article 6).

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

Indian scenario: As a third category of signatories to UNFCCC, India signed and ratified the

Protocol in August, 2002 and has emerged as a world leader in reduction of greenhouse gases by

adopting Clean Development Mechanisms (CDMs) in the past few years.

Carbon accounting Methods: Though there is a cacophony concerned to universally accepted

principles and standards but it is an accounting practice of making scientifically robust and verifiable

measurements of GHG emissions. The Kyoto protocol has paves the way for its principles, methods,

and practices in the field of GHGs emission field. Since Carbon accounting is concerned to all the

GHG but this study of accounting is directly concerned to Forest Carbon accounting in the world.

Although characteristics of forests have been recorded for numerous historical purposes, accounting

for carbon is a more recent addition to forest inventories. This follows the growing need to quantify

the stocks, sources, and sinks of carbon and other GHGs in the context of anthropogenic impacts on

the global climate (Watson, 2009 ).

Stock accounting: The starting point of forest carbon accounting is begun with the forest carbon

stock accounting for emissions and project-level accounting. Establishing the terrestrial carbon stock

of a territory and average carbon stocks for particular land uses, stock accounting allows carbon-

dense areas to be prioritized in regional land use planning. An early form of forest carbon

accounting, emissions, and emission reductions accounting has evolved from the principles

established for stock accounting (Watson, 2009).

Emissions accounting: Forest Emission accounting assesses the volume of CO2 emissions from the

forestry sector relative to other sectors. It helps the different nations for setting their goals of

emissions targets. Under the United Nations Framework Convention on Climate Change (UNFCCC)

and the Kyoto Protocol, countries are mandated to undertake some land use, land use change, and

forestry (LULUCF) carbon accounting which are stated below.

Project emission reductions accounting: Project emission reduction accounting for forest is a

challenge for both projects undertaken under the flexible mechanisms of the Kyoto Protocol and the

voluntary carbon markets. Both necessitate good carbon accounting to ensure that emissions

reductions are real, permanent, and verifiable. For projects to generate tradable emission reductions,

accounting methods between countries, regions, and projects must be standardized in both developed

and developing countries (Watson, 2009).

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

Obligations for forest Carbon accounting under the UNFCCC and Kyoto Protocol: Parties to the

UNFCCC are required to submit national reports on the implementation of the Convention to the

conference of the parties (COP). Emissions and removals of GHGs are central in these National

Communications, although reporting requirements differ between Annex I3 and non-Annex I

countries. All Parties (Annex I and non-Annex I countries) have to submit national inventories of

anthropogenic emissions by source and removals by sinks of GHGs to the COP. However, while

Annex I countries must do this annually, there are no fixed dates for submission of the National

Communications of non-Annex I Parties (Kyoto Protocol UNFCCC, article 4). Annex I countries are

required to account for emissions from direct human-induced activities of a-forestation, reforestation

and deforestation in forest areas not existing before 1990. The Marrakech4 Accords allow net

emissions from a-forestation, reforestation and deforestation within the commitment period (2008-

2012) to be offset through forest management up to a limit of 33 mega tons (Mt) of CO2 per year

(Kyoto Protocol UNFCCC, article 3.3). Annex I countries can voluntarily account for direct human-

induced activities associated with forest management, cropland management, grazing land

management and re-vegetation that have occurred after 1990. This voluntary accounting is likely to

be conducted where countries believe that emissions in the commitment period will be lower than

those in the base period (1990) and so the net impact of these activities is negative, a carbon sink.

When this occurs, Removal Units (RMUs) of carbon can be issued up to a specified cap, helping

countries to meet emission targets (Kyoto Protocol UNFCCC, article 3.4).

Annex I countries with more emissions than removals from the land use change and forestry sector in

1990 are required to include the Land Use, Land-Use Change and Forestry (LULUCF)5 sector in

their 1990 baseline. This means LULUCF emissions are then included in the calculation of Assigned

Amount Units which represent the emissions cap for a country in the commitment period (Kyoto

Protocol UNFCCC, article 3.7). Although non-Annex I countries are not obliged to annually account

and present GHG emissions to the COP, they are not without forest carbon accounting experience. A

small number of forest carbon projects have necessitated accounting for tradable emission

reductions, either via the Clean Development Mechanism of the KP or through voluntary carbon

markets.

3 The UNFCCC divides countries into two main groups: A total of 41 industrialized countries are currently listed in the Convention’s Annex-I , including the relatively wealthy industrialized countries that were members of the Organization for Economic Co-operation and Development (OECD) in 1992, plus countries with economies in transition (EITs), including the Russian Federation, the Baltic States, and several Central and Eastern European States. The OECD members of Annex-I (not the EITs) are also listed in the Convention’s Annex-II . There are currently 24 such Annex-II Parties. All other countries not listed in the Convention’s Annexes, mostly the developing countries, are known as non-Annex-I countries. They currently number 145. 4 The MA is a set of agreements reached at the 7th Conference of the Parties (COP7) to the UNFCC, held in 2001on the rules of meeting the targets set out in the

Kyoto Protocol. 5 According to UN climate change secretariat LULUCF is “A greenhouse inventory sector that covers emissions and remova ls of GHGs resulting from direct human-induced

and land use, land use change and forestry activities.

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

Principles of forest carbon accounting: Good practice for forest carbon accounting

(1) Accurate and precise: Two statistical concepts. Accuracy is how close estimates are to the true

value; accurate measurements lack bias and systematic error. Precision is the level of agreement

between repeated measurements; precise measurements have lower random error.

(2) Comparable: The data, methods, and assumptions applied in the accounting process must be

those with widespread consensus and which allow valid meaningful comparisons between areas.

(3) Complete: Accounting should be inclusive of all relevant categories of sources and sinks and

gases, as limited accounting may lead to misleading results. If carbon pools or gases are excluded,

documentation and justification for their omission must be presented (for example, for purposes of

conservative estimates).

(4) Conservative: Where accounting relies on assumptions, values and procedures with high

uncertainty, the most conservative option in the biological range should be chosen so as not

overestimate sinks or underestimate sources of GHGs. Conservative carbon estimates can also be

achieved through the omission of carbon pools.

(5) Consistent: Recognizing that trade-offs must be made in accounting as a result of time and

resource constraints, the data, methods and assumptions must be appropriate to the intended use of

the information.

(6) Relevance: Recognizing that trade-offs must be made in accounting as a result of time and

resource constraints, the data, methods and assumptions must be appropriate to the intended use of

the information.

(7) Transparent: The integrity of the reported results should be able to be confirmed by a third party

or external actor. This requires sufficient and clear documentation of the accounting process to be

available so that credibility and reliability of estimates can be assessed (Greenhalgh et al., 2006a);

(Pearson et al., 2005 a); (IPCC, 2000).

Biomass, carbon pools, and stock accounting: In an important FAO forestry paper (Brown, S., 1997)

has stated that Forest biomass is organic matter resulting from primary production through

photosynthesis minus consumption through respiration and harvest. In a similar type study of

(Westlake, D. F., 1966) has stated that with approximately 50% of dry forest biomass comprised of

carbon. Biomass assessments also illustrate the amount of carbon that may lose or sequestered under

different forest management regimes. Carbon is lost to the atmosphere as CO2. To convert carbon in

biomass to CO2, the tons of carbon are multiplied by the ratio of the molecular weight of carbon

dioxide to the atomic weight of carbon (44/12). Estimating the biomass density of forest components

is, therefore, the first step in forest carbon accounting.

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

Approaches to emissions accounting: The purpose of emissions accounting is to quantify the

exchange of GHGs between the atmosphere, terrestrial vegetation, and soils through photosynthesis,

respiration, decomposition, and combustion. There are two main approaches to emissions

accounting: the inventory approach and the activity-based approach, which are outlined below and

mathematically represented. Both approaches are supported under IPCC guidance (IPCC, 2003) and

are based on the underlying assumption that the flows of GHGs to or from the atmosphere are equal

to changes in carbon stocks in the biomass and soils.

Equation 1: Inventory/Periodic

Accounting

Equation 2: Activity-based/Flux

Accounting

▲C = ∑ (Ct2 – Ct1) / (t2 – t1)

▲C = carbon stock change, tones C per

year

Ct1 = carbon stock at time t1, tones C

Ct2 = carbon stock at time t2, tones C

▲C = ∑ [A ٭ (CI – CL)]

A = area of land, ha

CI = rate of gain of carbon, tones C per

ha per year

CL = rate of loss of carbon, tones C per ha

per year

Accounting for emission reductions: The World Resource Institute (Greenhalgh et al., 2006 b),

World Bank and Winrock (Pearson et al., 2005 b), and The Voluntary Carbon Standard (VCS, 2008)

has tried best to familiarize the standards of accounting for emission reduction in a number of ways.

Accounting for emission reductions is most commonly required at the project level, where forestry

carbon projects generate emission reductions; these can be traded as offsets either under the Kyoto

Protocol or on the voluntary carbon markets. The supplementary principles can be listed as the

complexities of baseline establishment, demonstration of additionality, issues of leakage, and the

permanence of emissions reductions.

Base line: In a study (Bond et al., 2009) has emphasized that In order to set emission reduction

targets, a baseline scenario must be developed. Also called a counterfactual, this baseline scenario

estimates what would have happened in the absence of a policy or project. It is required so that the

mitigation impact of a project or policy can be quantified. In the forestry sector, the baseline is

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

particularly important in attempts to reduce emissions from deforestation and degradation, and raises

both technical and political considerations.

Additionality: The term additionality meant that a project to be an additional, it must be proven that

emission reductions would not have occurred in the absence of this project. This is an important

principle when emissions reductions at a project location are used to offset GHG emissions at

another location. If there is no additionality, overall GHG emissions will increase as a result of the

project activity.

Leakage: In an important study in Bolivia (Sohngen & Brown, 2004) expressed that a leakage is the

process by which emissions are reduced in one area but are also impacted outside of the area in

question. Although positive leakage is a possibility, concern is

directed to negative leakage, where emissions are merely shifted to another geographical area and

fewer, or no, actual reductions are generated by the project activities.

Permanence: Permanence refers to the persistence of emission reductions over time. Unlike other

sectors, such as industry, energy, waste management and transport, there is a risk that forest carbon

sinks, having delivered emissions reductions, may deteriorate or be depleted over the long term

(Watson, 2009 ).

Carbon Accounting in India: Indian business houses are becoming more responsible towards their

corporate social responsibilities and started seeing value in undertaking carbon accounting and

reporting it in public forums. Such forums include Carbon Disclosure Project (CDP) and company's

Sustainable Development Reports. The Carbon Disclosure Project (CDP) 2010 - India 200 Report

presents the strategies adopted by Indian businesses in response to climate change. These strategies

have been disclosed, as part of their response to the CDP 2010 questionnaire6 (WWF, 2010).

ICAI and Carbon Accounting: Accounting Standards Board, The institute of Chartered Accountants

of India has issued an Exposure Draft: Guidance Note on Accounting for Self-Generated Certified

Emissions Reductions (CERs). Besides this there is not any accounting standards approved and in

practice.

6 The CDP 2010 questionnaire is available on the CDP website www.cdproject.net

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

Whether CER is an ‘asset: „Framework for the Preparation and Presentation of Financial

Statements‟, issued by the Institute of Chartered Accountants of India, defines an „asset‟ as follows:

“An asset is a resource controlled by the enterprise as a result of past events from which future

economic benefits are expected to flow to the enterprise.” From the above-mentioned definition of

„asset‟ it follows that for a CER to be considered as an asset of the generating entity, it should be a

resource controlled by the generating entity arising as a result of past event/s, and from which future

economic benefits are expected to flow to the generating entity (ICAI, 2010 ).

Recognition of CERs: According to the „Framework for the Preparation and Presentation of Financial

Statements‟ “An asset is recognized in the balance sheet when it is probable that the future economic

benefits associated with it will flow to the enterprise and the asset has a cost or value that can be

measured reliably.” accordingly CERs come into existence when these are credited by UNFCCC in a

manner to be unconditionally available to the generating entity. Therefore, CERs should not be

recognized before that stage (ICAI, 2010).

Type of asset: CERs are non-monetary assets without a physical form; they do not strictly fall within

the meaning of „intangible asset‟ as per AS 26. Instead, CERs generated by the generating entity are

held for the purpose of sale (ICAI, 2010).

Measurement of CERs: CERs are inventories for an entity which generates the CERs. Therefore, the

valuation principles as prescribed in AS 2 should be followed for CERs. As per AS 2, inventories

should be valued at the lower of cost and net realizable value. Accordingly, CERs should be

measured at cost or net realizable value, whichever is lower.

Cost of CERs Inventories: CERs are inventories for an entity which generates the CERs. Therefore,

the valuation principles as prescribed in AS 2 should be followed for CERs. As per AS 2, inventories

should be valued at the lower of cost and net realizable value. Accordingly, CERs should be

measured at cost or net realizable value, whichever is lower (ICAI, 2010 ).

Net Realizable Value of CERs: In the determination of the net realizable value of CERs, paragraph

22 of AS 2 reproduced below should be used as guidance: “22. Estimates of net realizable value are

based on the most reliable evidence available at the time the estimates are made as to the amount the

inventories are expected to realize. These estimates take into consideration fluctuations of price or

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

cost directly relating to events occurring after the balance sheet date to the extent that such events

confirm the conditions existing at the balance sheet date”(ICAI, 2010 ).

Challenges of Carbon Accounting

Fuzzy accounting Environment: In spite of growing awareness about the climate change and carbon

emission none of the nations of the world has developed clear cut accounting principles and

methodology for carbon accounting. There is currently no authoritative accounting literature from

either the Financial Accounting Standards Board (FASB) or the International Accounting Standard

Board (IASB) on accounting for emission allowances (Rohrig & Davis, 2011 ).

Question about the asset type: Emission allowances, expressed as carbon credits, entitle the holder of

such credits to emit one ton of carbon per credit. Emission allowances, as intangible assets, have a

number of unique characteristics that challenge the accurate measuring and reporting of their value.

Intangible assets are identifiable nonfinancial assets that lack physical substance (Rohrig & Davis,

2011). From a definitional perspective, emission allowances appear to align more closely to

intangibles than inventory, although some traditional intangible accounting practices may not be a

precise fit for the allowances. For one, intangibles with a finite life are typically amortized over the

period based on a unit-of-production approach (or straight line if the previous method is difficult to

identify). The two possible accounting value models for initial recognition are “cost” and “fair

value.” Under both the intangible and inventory models, assets acquired through purchase are

commonly recorded at cost (Rohrig & Davis, 2011).

Forest carbon accounting challenges

Definition of Forest: There is a wide range heterogeneous definition of forest around the world

therefore what is to be included in the forest and what should be excluded from is a burning question

for carbon forest accounting in the world. The substantial variation in forest definition leaves many

ambiguities. By utilizing canopy cover as a key characteristic of the forest, the carbon density of a

forest is effectively ignored.

Direct human induced impact: Forest carbon accounting aims to capture the direct result of

anthropogenic activities and not merely natural variation or indirect human-induced effects. But the

factor affecting the forest carbon stocks for example climate variability (heat waves, oscillation);

indirect human impact (CO2 fertilization, Nitrogen disposition, air pollutant effects, length of

growing season, fire and insect attack); direct human impact (afforestration, reforestation,

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

deforestation, cropland management, grazing land management) has a lot of saying on the CO2 e

therefore a matrix form of carbon accounting specially for forest carbon accounting is a need of 21st

century.

Harvested wood product: The IPCC (2006) presents four approaches to accounting for HWPs but

also offers the option of reporting zero impact in inventories. This default approach has considerable

implications for accounting in countries where changes in the stocks of forest products can be more

important that standing biomass, for example net importers of HWPs with constant forest areas.

Conclusion

The evolvement of carbon market has knocked the financial door of the world. The accounting world

is also in dilemma and trying its best to develop and adopt universally accepted accounting principles

for the carbon world. Europe most experienced in carbon trading having it‟ s involvement for last

four years still reeling on the matter how about the carbon accounting be finalized with greater

consensus in the world. Carbon traders in the United States have only begun to grapple with the

accounting issues of an already complex and unfamiliar market. Moreover, as carbon markets evolve

and incorporate new elements, additional accounting challenges will continue to emerge. There is

currently no authoritative accounting literature from the International Accounting Standards Board

(IASB) on accounting for emission allowances. Forest carbon accounting is just not a Childs play

because it is a multi-disciplinary task. It is interlocked and interwoven with expertise from forestry

science, ecological modeling, statistics, remote sensing, and at the field measurement level and

hereafter the accounting science followed by financial theories is must be in practice. For carbon

accounting good and complete information on the sources and sinks of carbon is a pre-requisite for

appropriate emission targets and goals. Therefore it is felt that without greater investment in forest

carbon accounting neither accounting method could be developed which could be universally

accepted under conditions nor the quality of data could be improved. These investments should aim

to reduce the complexity of accounting and limit the trade-offs that must be made between costs and

accuracy. The carbon accounting in India is in an infant stage therefore it is a need of time that The

Institute of Chartered Accountants of India must adopt a concrete policy for the further development

of carbon accounting standards as soon as possible. The exposure draft of ICAI is silent about the

methodological part of forest carbon accounting for India and it is just based on CERs but what

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

about carbon offset credits7, banking and borrowing mechanism in the national and international

arena. Fuzzy accounting environment, question about asset type and accounting value (cost or fair

market value of CERs) are still in question for carbon accounting in India besides this the challenges

of forest carbon accounting could be pointed out as versatile definition of forest, measurement of

direct human induced impact on forest and harvested wood product assessment for forest carbon

accounting are standing as a barrier for forest carbon accounting in India.

References

1. Brenton, p., jones, g. E., & jensen, m. F. (2009 ). Carbon labelling and low income-country

exports: a review of development issues. Development policy review , 27 (3), 243-267.

2. Buendia, l., hoppaus, r., martinsen, t., meijer, j., miwa, k. And tanabe, k. (eds).

Intergovernmental panel on climate change (ipcc), ipcc/oecd/iea/iges, hayama, japan

3. Canadell, J. G., Le Qu er e, C., Raupach, M. R., Field, C. B., Buitenhuis, et al. (2007).

Contributions to accelerating atmospheric CO2 growth from economic activity, carbon intensity,

and efficiency of natural sinks. Proc. Natl. Acad. Sci. 104, 18866–18870

4. Deloitte China Research and Insight Centre. (2010 a). Deloitte. Retrieved August 14, 2011,

from New challenges in carbon accounting: an overview energysolutions:

www.deloitte.com/energysolutions

5. FSI (2009). India State of Forest report. Dehradun: Forest Survey of India(Ministry of

environment & forest, Government of India)

6. Greenhalgh, S., Daviet, F. and Weninger, E.,( 2006 ). The Land Use, Land-Use Change, and

Forestry Guidance for GHG Project Accounting. The Greenhouse Gas Protocol, World

Resources Institute

7. Houghtan, R. A. (2010). How well do we know the flux of CO2 from land-use change? Tellus ,

62 (B), 337 - 351.

8. Houghton, J.T., Y. Ding, D.J. Griggs, M. Noguer, P.J. van der Linden and D. Xiaosu (eds.).

(2001). Climate Change 2001: The Scientific Basis. Contribution of Working Group I to the

Third Assessment Report of the Intergovernmental Panel on Climate Change (IPCC).

Cambridge University Press, UK. 944 p

9. ICAI. (2010 ). The Institute of Chartered Accountants of India. Retrieved August 15, 2011,

from Whats New: http://icai.org/backindex.html

10. IPCC .(2003). Good Practice Guidance for Land Use, land-Use Change and Forestry. Penman,

J., Gytarsky, M., Hiraishi, T., Kruger, D., Pipatti, R., Buendia, L., Miwa, K., Ngara, T., Tanabe,

K. and Wagner, F. (Eds). Intergovernmental Panel on Climate Change (IPCC), IPCC/IGES,

Hayama, Japan

11. IPCC (2000). Good Practice Guidance and Uncertainty Management in National Greenhouse

Gas Inventories. Penman, J., Kruger, D., Galbally, I., Hiraishi, T., Nyenzi, B., Enmanuel, S.,

7 Entities participating in the funding of projects that reduce carbon emissions such as various types of renewable energy may receive offsets that can be used in place of allowances. Some regulators have caps on total offsets allowed and/or a ratio of offsets to allowances that can be used.

International Journal of 360o Management Review, Vol. 01, Issue 01, April 2013 ISSN: 2320-7132

12. IPCC ( 2007). ipcc fourth assessment report. climate change 2007. the physical science basis.

contribution of working group i to the fourth assessment report of the intergovernmental panel

on climate change edited by solomon, s., d. qin, m. manning, z. chen, m. marquis, k.b. averyt,

m. tignor and h.l. miller. cambridge university press, cambridge, united kingdom and new york,

ny, usa, 996 pp

13. INSWA. (2007, February). National Solid Waste association of India. Retrieved August 12,

2011, from Library Newsletters: http://www.nswai.com/library-newsletters.php

14. IUFRO( 2009). Adaptation of Forests and People to Climate Change. A Global Assessment

Report. IUFRO, International Union of Forest Research Organizations, World Series Volume

22. Helsinki. 224 Kishwan, J., Pandey, R., & Dadhwal, V. K. (2009). India's Forest and Tree

Cover: Contribution as a Carbon Sink. Indian Council of Forest Research and Education

15. Kurz, W. A., Apps, M., Benfield, E., & Stinson, G. (2002, Sept-Oct). Forest carbon accounting

at the operational scale. The Forestry Cronicle , 78 (5), pp. 672 - 679

16. Knorr, W. (2009). Is the airborne fraction of anthropogenic CO2 emissions increasing?

Geophysics. Res. Lett. 36, L21710, doi:10.1029/2009GL040613

17. Le Qu er e, C., Raupach,M. R., Canadell, J. G., Marland, G., Bopp, L. et al.( 2009). Trends in

the sources and sinks of carbon dioxide. Nat. GeoSci. 2, 831–836

18. Neef, T., von Luepke, H., Schoene, D.( 2006). Choosing a forest definition for the Clean

Development Mechanism. Forests and Climate Change Working Paper 4, FAO

19. Planning Commission . (2003). Report of the Working Group on National Action Plan for

operationalising Clean Development Mechanism(CDM) in India. Govt. of India.

20. Pearson, T., Walker, S. and Brown, S.(2005 ). Sourcebook for Land Use, Land-Use Change and

Forestry Projects. Winrock International and the Bio Carbon Fund of the World Bank

21. Rohrig, M., & Davis, M. (2011 , April). Deloitte China Research and Insight Centre. Retrieved

August 14, 2011, from Deloitte energy solution: www.deloitte.com/energysolutions

22. UNDP. (2010). UN. Retrieved August 11, 2011, from International year of Forest 2011:

http://www.un.org/en/events/iyof2011/index.shtml

23. UNFCC. (1997, December 11). United Nations Frame Convention on Climate Change.

Retrieved August 15, 2011, from Kyoto Protocal:

http://unfccc.int/kyoto_protocol/items/2830.php

24. UNFCC. (1992). United Nations Framework Convention on Climate Change. Retrieved August

16, 2011, from GHG Data from UNFCC:

http://unfccc.int/ghg_data/ghg_data_unfccc/items/4146.php

25. UNEP. (2009). United Nations Environmental Programme. Retrieved August 17, 2011, from

Historical Forest Carbon Balance: http://maps.grida.no/go/graphic/historical-forest-carbon-

balance-1855-1995

26. Watson, C. (2009 , August 12). UNDP. Retrieved August 13, 2011, from Home Forest Carbon

Accounting: Overview and Principles: http://www.undp.org/climatechange/carbon-

finance/Docs/Forest%20Carbon%20Accounting%20-%20Overview%20%26%20Principles.pdf

27. WWF. (2010, February 1). Carbon Disclosure Projects 2010 India 200 Report. Retrieved

August 14, 2011, from WWF: http://www.wwfindia.org/wwf_publications/cdp_india/