Embed Size (px)

Citation preview

Coal distribution and transportation –Bottlenecks & plausible remedies

B K SAXENADIRECTOR(Marketing), CIL

New Delhi20th November, 2012

Distribution of coal – perspectives and policies

• Distribution and Pricing of coal deregulated in the year 2000 • A policy for distribution of coal introduced by CIL including

internet based e-auction of coal in 2004.• The Policy was challenged in the Court of Law• A direction was given by the Hon’ble supreme Court to

introduce a New Coal distribution Policy involving all the stake holders.

• A committee under the Chairmanship of Secy(Coal) deliberated the issues and recommended a policy which was introduced by Govt on 18-Oct-2007

Genesis

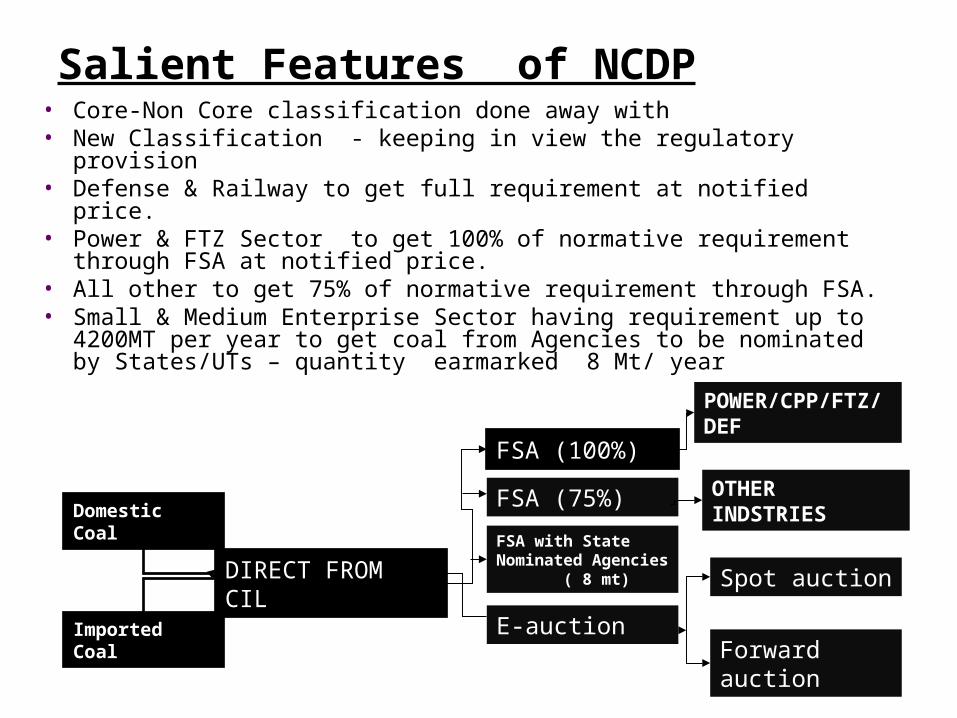

Salient Features of NCDP

3

• Core-Non Core classification done away with • New Classification - keeping in view the regulatory provision• Defense & Railway to get full requirement at notified price.• Power & FTZ Sector to get 100% of normative requirement through FSA at

notified price.• All other to get 75% of normative requirement through FSA.• Small & Medium Enterprise Sector having requirement up to 4200MT per

year to get coal from Agencies to be nominated by States/UTs – quantity earmarked 8 Mt/ year

Domestic Coal

Imported Coal

FSA with State Nominated Agencies ( 8 mt)

DIRECT FROM CIL

FSA (100%)

FSA (75%)

E-auction

Spot auction

Forward auction

POWER/CPP/FTZ/ DEF

OTHER INDSTRIES

Salient Features (NCDP) …….(cont)

4

• All existing linkage holders including SMEs required to execute FSA for continuation of coal supply.

• For new consumers– Power , Cement and Sponge Iron sectors LOAs to

be issued on the recommendation of SLC(LT)– For other sectors CIL to be responsible for

clearance of applications for issuance of LOA by supplying coal companies

– LoA to have validity of 24/12 months for Power/other consumers for conversion into FSAs.

Salient Features (NCDP) …………(Cont)

5

• CIL, to meet full domestic requirement of coal under FSA, even by resorting to import, if feasible

• Coal being scarce commodity- discipline in its economic use suggested

• Around 10% of production earmarked for e-auction as an additional option for sourcing coal.

• Forward e-auction scheme for actual consumer to be introduced for ensuring longer term requirement

Implementation• NCDP mandated CIL to meet the entire demand under the FSA

even by import of coal if feasible.• FSA, a legally enforceable document, contains provisions for

penalty and incentives for failure in meeting the commitment• CIL in one hand has to accept all consumers approaching for

FSA and on the other to protect its interest against the contractual failure in supply commitments.

• CIL had to make built-in provisions in the FSA for regulating the committed supply level which triggers penalty for supply failure.

• Different trigger level is set for different model of FSAs applicable to different category of consumers considering the sectoral importance and the status as to whether new or existing units

6

Coal Balance Position

7

#Production projection is at optimistic level subject to getting all clearances in time

*The requirement for up-coming power stations would be on the basis of actual commissioning, the figure indicates commitment given by CIL . As per the indication available from CEA the likely demand as per commissioning schedule is as under:

Particular 2012--13

2013-14 2014-15 2015--16

2016--17

ProductionProjection #

464 487 530 574 615

Committed Demand a/c on-going supplies and LOAs for new units for Power Utilities*

727 727 727 727 727

Committed Demand a/c on-going supplies and LOAs for new units for non-power sectors

136 136 136 136 136

E-auction 46 49 53 57 61

Total demand/requirement 909 912 916 920 924

Gap (-) 445 (-) 425 (-) 386 (-) 346 (-) 309

Figs. In Mt

2012-13 2013-14 2014-15 2015-16 2016-17

Demand 467 511 560 584 586

Bottlenecks in the distribution arrangement

• The negative coal balance position in excess of 400 Mt to continue till the end of XII Plan based on LOAs issued so far

• Issuance of further coal clearances by SLC (LT) is withheld for the widening gap between commitment vis-à-vis availability – more than 1500 applications for about 3000Mt of coal are reported to be in pipeline (as per MOC website)

• The FSA model offered by CIL not acceptable to new power utilities• CIL would be depending on supply of imported coal for fulfilling its

FSA commitment, now amended as per the Presidential Directive• Implementing policy for issuance of LOA to new consumers in the

Non SLC/LT segment is also pending• Supply-mix for new consumers under FSA limited up to 50% of

indigenous coal for other than designated power utilities

8

Bottlenecks (continued)

• No level playing field for new consumers.• Future consumers have no avenue to procure coal

other than e-auction with limited quantity of around 10% of the production

• Price difference between the market driven and notified price increasing with the growth in demand

• The coal supplied through FSAs finding the grey market more profitable

• No effective means available to control diversion of coal sold under FSAs

9

Plausible remedies

• Prevent diversion of coal -- all buyers, excepting those in regulated sectors, to get coal through a single price mechanism

• E-auction already established its acceptance across all coal consuming sectors

• All consumers other than those in regulated sector may, therefore, be brought under e-auction – commensurate increase in quantity – level playing field for all

• Consumers have the scope to exercise their options in respect of quality, quantity and logistics issues – the most flexible system

• Termination of FSA possible in the event Government notified any material changes in the distribution policy

10

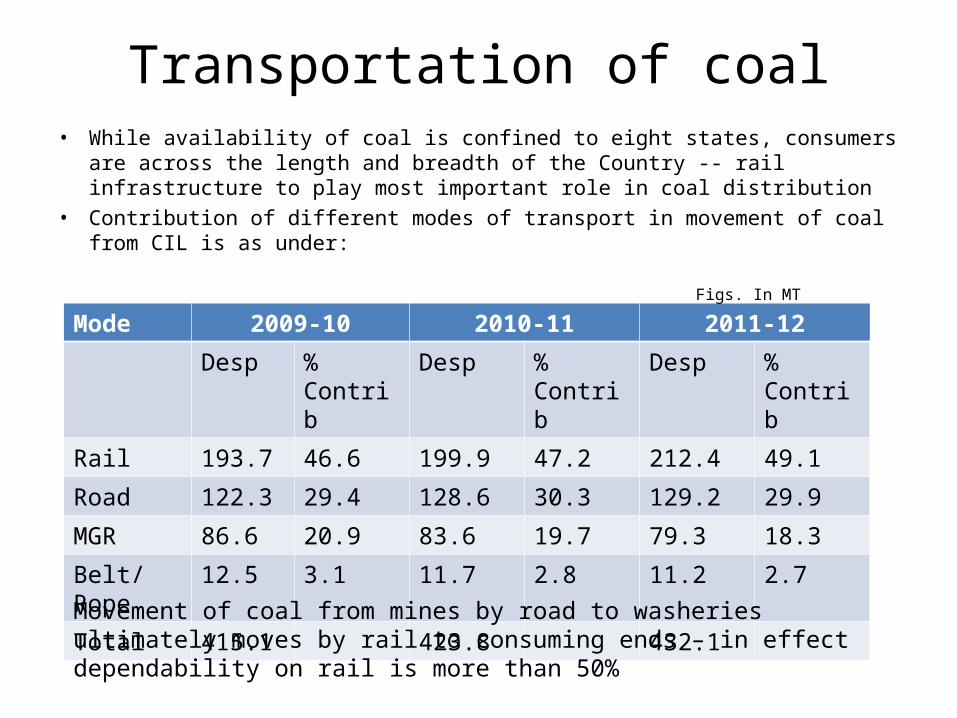

Transportation of coal• While availability of coal is confined to eight states, consumers are across the

length and breadth of the Country -- rail infrastructure to play most important role in coal distribution

• Contribution of different modes of transport in movement of coal from CIL is as under:

Mode 2009-10 2010-11 2011-12

Desp % Contrib Desp % Contrib Desp % Contrib

Rail 193.7 46.6 199.9 47.2 212.4 49.1

Road 122.3 29.4 128.6 30.3 129.2 29.9

MGR 86.6 20.9 83.6 19.7 79.3 18.3

Belt/Rope 12.5 3.1 11.7 2.8 11.2 2.7

Total 415.1 423.8 432.1

Figs. In MT

Movement of coal from mines by road to washeries ultimately moves by rail to consuming ends – in effect dependability on rail is more than 50%

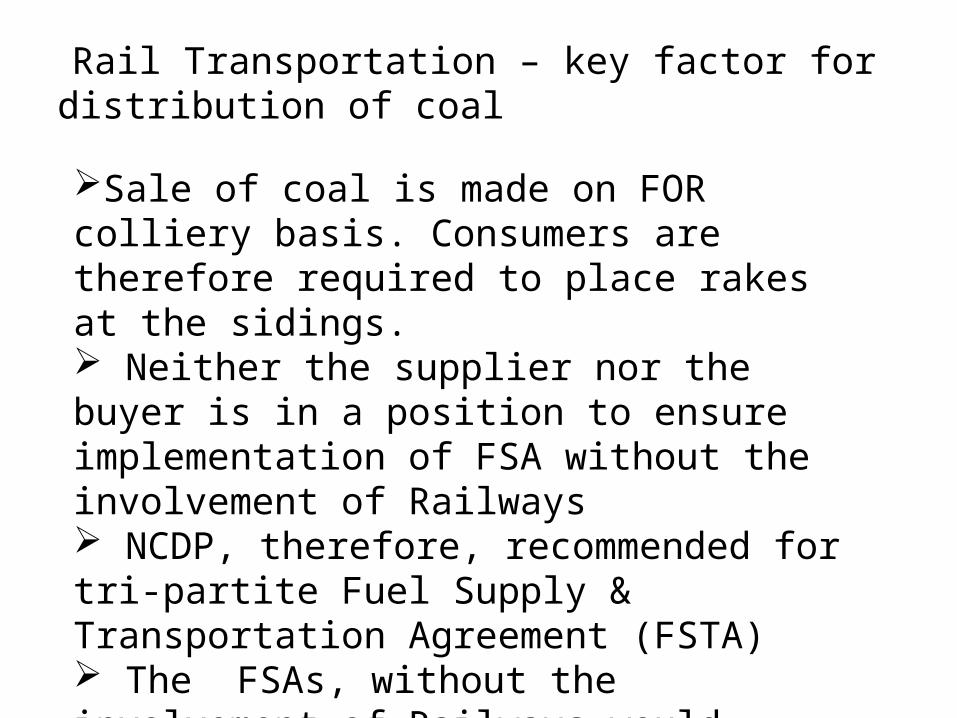

Sale of coal is made on FOR colliery basis. Consumers are therefore required to place rakes at the sidings. Neither the supplier nor the buyer is in a position to ensure implementation of FSA without the involvement of Railways NCDP, therefore, recommended for tri-partite Fuel Supply & Transportation Agreement (FSTA) The FSAs, without the involvement of Railways would continue to be commercially not tenable

Rail Transportation – key factor for distribution of coal

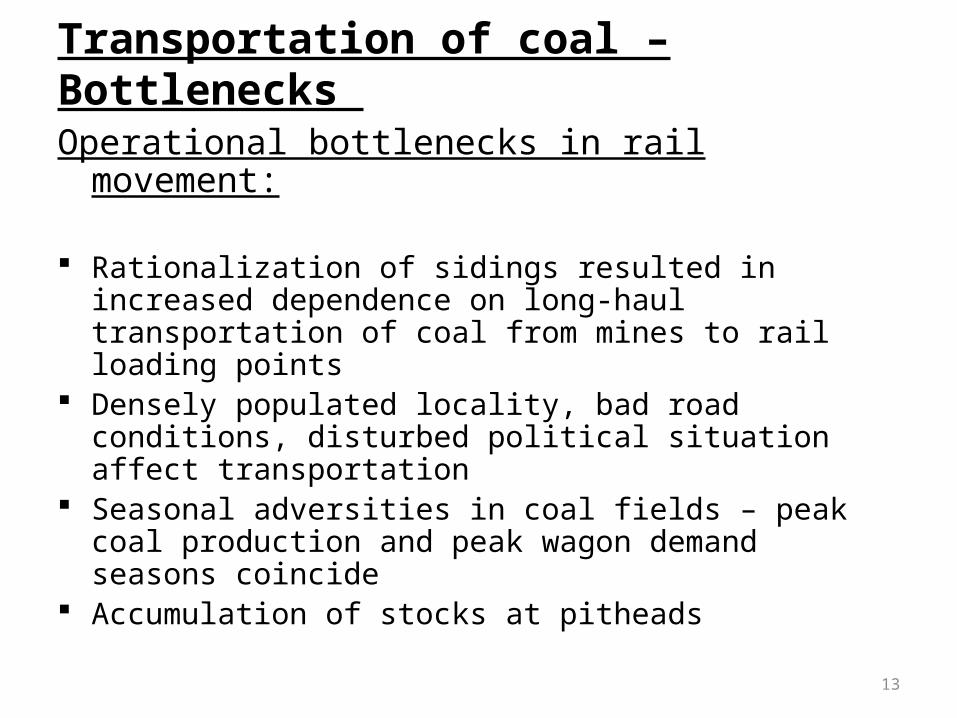

Transportation of coal –Bottlenecks

Operational bottlenecks in rail movement:

Rationalization of sidings resulted in increased dependence on long-haul transportation of coal from mines to rail loading points

Densely populated locality, bad road conditions, disturbed political situation affect transportation

Seasonal adversities in coal fields – peak coal production and peak wagon demand seasons coincide

Accumulation of stocks at pitheads

13

Transportation bottlenecks (continues)

Bottlenecks arising out of skewed distribution of production growth Major incremental growth of CIL to come mainly from CCL, SECL and MCL New demands were, therefore, linked to these coalfields Transport links not developed attuned to projected growth in production Perpetual shortfall in availability of rolling stocks resulted in accretion of stock at pitheads – These three fields account for 67% of the total stock of CIL Railways, to achieve better tonnage, often prefer for short-haul destinations for improving turn round of rakes A few power stations are served better than their requirement at the cost of others.

Transportation bottlenecks (continued)

Imported coal additional burden on movement infrastructure Major part of the import in the country arrives during the peak indigenous production months Constraints at ports in handling different types of vessels constricts the choice Rail connectivity issue narrows down the choice of Port further Movement of coal from port and from indigenous mines – clash of priority and interest; Most of the time indigenous mines are casualties The coal available in the country accumulates at the pitheads instead of being consumed at plants

Transportation bottlenecks (continued)

Gap between requirement and availability in rail infrastructure:

Procurement of wagons around 70% of the target – acute shortage leading to continuance of use of defective/condemned wagons – safety and operational hazards Shortage of locomotive Track capacity – delay in project delivery Mismatch between load-bearing capacity of tracks and wagons –leading to inefficient movement matrix

Plausible remedies While Railways need to augment capacity both in term of track and rolling stocks, comprehensive steps to be taken by producers and users of coal for bringing efficiency in terminal operations to optimize use of the transport infrastructure Working Group on Coal & Lignite projected transportation requirement of more than 1,00,000 truck trips/day for shifting coal at the sidings by the end of XII Plan to cater to projected rail movement. Considering the impact of such movement on the road condition, atmosphere, and the society in general alternative modes – particularly use of cross-country conveyor for transportation of coal to railway siding needs to be ensured.

Plausible remedies …. continued

The conveyor system needs to be considered an integral part of the mining project and no stop-gap road transport arrangement should be promoted in lieu All the requisite logistics infrastructure identified in the DPR of the mining projects -- coal crushing/sizing arrangements, railway sidings, weighbridges etc. require synchronization with production Power stations and other bulk consumers need to develop infrastructure for handling all types of wagonsCoal handling capacity at power stations needs to be attuned to projected coal requirement

Plausible remedies …. continued

Reducing dispersion in requirement of wagons between lean and peak season -- lean season freight discount could be one of the way Source rationalization for indigenous coal Implementation of FSTA to make all the stakeholders accountable Like availability of coal, transport capacity should be equally taken into account before promoting a project Consider evacuation issues from new coalfields before according linkages CIL investing on development of railway track in the upcoming coalfields at North Karanpura (Tori-Shivpur-Hazaribagh), Basundhara-Garjanbahal Area of MCL (Gopalpur-Manoharpur ) and Korba-Raigarh. Railways to ensure timely execution of these projects

Conclusion

Planned production of coal requires matching development of transport logisticsRailways would continue to be mainstay for evacuation of coalUnless steps are taken to develop Railway infrastructure production potential likely to face severe jolt Equally important is to synchronize development of loading infrastructure at collieries, including crushing and coal conveying arrangement

ConclusionEven with growth in production coal scarcity in different consuming ends likely to persist without corresponding improvement in terminal management at loading and unloading endsOperational and commercial bottlenecks in transportation logistics to be addressed at planning levelScopes of optimum utilization of available infrastructure with proper attention to cost – could be a key issue to reduce dispersion in demand of wagonsWithout FSTA, effective implementation of the NCDP is not possible Rationalization of source of supply in line with transport capacity should be a priority area