Embed Size (px)

Citation preview

Calin Dragan, CEOMichael Coombs, CFO

Coca-Cola East JapanQ2 & YTD 2015Earnings Presentation

August 7, 2015

www.ccej.co.jp

(Posted to CCEJ Website August 6, 2015)

The plans, performance forecasts, and strategies appearing in this material are based on the assumptions and judgment of the management of Coca-Cola East Japan Co. Ltd. (CCEJ) in view of data obtained as of the date this material was released. These forecasts may differ materially from actual performance due to risks and uncertain factors such as those listed below.

Risks and uncertain factors are not limited to the items listed below. They are also included in our annual securities report, or

“Yuka Shoken Houkokusho”.

• Intensification of price competition in the marketplace

• Change in economic trends surrounding our business

• Major fluctuations in capital markets

• Fluctuations in currency exchange rates, particularly with respect to the value of the Japanese yen and the U.S. dollar

• Increases in prices of raw materials

• Change in the tax environment

• CCEJ's ability to realize production efficiencies and to implement capital expenditures at the levels and times planned by management;

• CCEJ's ability to market and distribute effectively

• Uncertain factors other than those above

The information in this presentation is provided for informational purposes and should not be construed as a solicitation of an investment in our securities.CCEJ undertakes no duty to update any statement in light of new information or future events. You should rely on your own independent examination of us before investing in any securities issued by our company.

Forward-Looking Statements

2

Q2 & YTD 2015

Coca-Cola Zero Taste Challenge (VIDEO)

3

Q2 & YTD 2015

(TRY! #Kiki Coke – Coca-Cola Zero Taste Challenge Commercial Film)http://www.cokezero.jp/movie/#movie09

Coca-Cola Zero Taste Challenge

4

What? Is this really ZERO?• June – July promotion• Sampling ~100K cans• Nine events in CCEJ territory

Taste and then slide cover off can to discover if it was Coca-Cola or Coke Zero

Enjoy!

Q2 & YTD 2015

Introduction

• Overview and Key Messages

• Transforming our Business

Second Quarter and Year-to-Date Results

• Share, Volume and Financial Results

Rest-of-Year Outlook

• Marketing Activities and Key Milestones

Q2 & YTD 2015 Earnings Presentation

5

Q2 & YTD 2015

YTD comparable* operating income improved by 3.8 billion yen vs. prior year, including cycling the impact of the accounting policy change in Q1 2014.

Ongoing delivery of supply chain synergies, partially offset by increased expenses related to employee overtime, inventory movement & systems support for rollout of new Enterprise Resource Planning (ERP) system. Below plan YTD.

Share decline in the second quarter, cycling strong share growth in prior year and decision to decrease promotional activity at quarter-end (June)

Balanced volume and revenue performance in the quarter and year-to-date

Continued growth in tea, water & coffee led by Convenience Store channel

Acquisition of Sendai Coca-Cola bottler reflected in results from Q2

Summary of First Half Results

6* Includes Q2 2015 acquisition of Sendai bottler

Q2 & YTD 2015

Q2 & YTD 2015Results

www.ccej.co.jp

Rapid organizational transformation & integration continues; acquired Sendai Coca-Cola Bottling Company, consolidated eight subsidiaries into FV East Japan.

Two new production lines operational in Q2 (Ibaraki, Ebina)

Phase One of ERP System operational. Necessary fine-tuning and “hypercare” IT support was greater than expected. Limited customer out of stocks in spite of strong effort in Q2 to ensure stable continuity of supply during transition.

Developing capabilities and implementing programs for revenue growth management to improve price/mix.

Restructured indirect procurement into Coca-Cola Business Services Company

Transforming the Business in 2015

8

Q2 & YTD 2015

9

アプリケーションマップ(2012/11)

REDサーバ LBCクロス(溝口DC)

KBC

在庫管理

伝発名人

TCCS サーバ(コールセンター)

z

z

z

DIAS

DWH

訪問 FAX受注テレ受注

人間系の受注

弊社受信

EDI関連

Web(Infomart)

センター配送照合システム

Webクライアント

HUB I/Fシステム

MOS

ノーツ(社内コミュニケーション)

コミュニケーションメール

自販機情報

社内コミュニケーショ

ン顧客情報収集 RFA 賃貸料

管理

受注取り纏め(移行ツール)

データ取込

NetStrage260

ウィルス管理(シマンテック)

バックアップデータ

TONEAD1

ユーザー管理

ドメイン管理

TONEWSS1

ポリシー管理

Windows Updatバージョン管理

セキュリティー管理

ノーツ連携(CACHATTO)

ノーツ連携

システム監視(CAT6)

ユーザーログ監視

一往復検量

(CCJC資産) 自販機検量

CCIBS幕張サーバ

ホームページ

インターネットメール変換

プロキシ

MINIAP

HUBマスタ・トランチェック

FlashReportExcell加工

Web広報利根パックスクリエーション外部サイト

Web広報利根

アウトバウンド受注

インバウンド受注

受注KPI管理スマートフォン

EOSシステム

受注デー タ作成

ボトラー間連携

各種伝票作成

精算データ作成

ASN

受注統合管理 BISS連携 データチェック

ディスパッチ ピッキングリスト在庫引当

納品書データ作成

専用伝票出力

棚卸実差表 棚卸

配送明細配送一覧

配送ルート稼動チェック

在庫転送 破損等

PC端末

HHTアップロード補充・精算(FS)

帰

所

HHTダウンロード

納品(RS)ルートセトル

現金チェック

車上チェック

翌日積込&承認

修理受付

Web検品

入荷検品

オンライン請求

出荷伝票入力 配車

入荷伝票入力

発注書入力

送込数作成

出荷伝票出力

最終賞味期限更新

オーダー依頼 在庫実査

機器調達設置・撤去移動 修理 整備 廃棄

サニテーション

インスペクション

部品管理 部品EDI

自販機統合システム

費用管理

作業履歴管理

機器管理

修理オーダー 連携

在庫システム

機内在庫 受払 在庫実績 SAP連携

受注

J-SCALE

支店

KBC

J-SCALE

EM

J-SCALE

SM関連HHT

伝票回収チェック

銀行入金業務

FS預り金

請求データ

EOSデータ管理

共配費用処理

ボトラー間精算

z

z

z

利根移行ツールI/Fシステム

千葉LC

マテハン管理

受注・在庫連携

コード変換

D-DISデータ作成

売掛管理(一般顧客を除く)

固定資産

資金管理(一部・単独)

原価計算

部門利益管理

購買業務一般会計 買掛管理

在庫・(物流)

稟議(COA)

営業活動推進システム

スケジュール管理

顧客情報

商談進捗

活動実績

損益試算

実績紹介

各種調査

バジェット作成

TVOSS

オペレーション分析

売切分析

商品戦略

訪問計画

新商品展開

異常値検出

プレ名人

コラム戦略

KPI管理

J-SCALE

実行系

報酬管理(評価)

昇給

人事異動 賞与

退職金出向管理 福利厚生

労働者名簿

目標管理

組織管理

E-Learning

勤怠管理HCM給与(外部委託:ペイロール社)

給与計算 年末調整

共済会

保険業務 仮払い

連結決算(シナンシャル社)

FBシステム(みずほ)

SUPER COMPACT

Pathfinder

支払業務

SAP I/F(Tonekk03)

入庫登録I/F

入出庫伝票登録I/F

受注出荷I/F

営業所在庫I/Fファイル

販売リベート仕訳I/F

売上仕訳I/F

給与・賞与仕訳I/F

管理会計

費用分析

予算管理

個店損益

販売実績

各種売上管理

PowerPlay各種売上分析

定型帳票

過不足金管理(TVOSSサーバ)

個機過不足 製品過不足 現金過不足

FSコミッションJ-SCALE

BO系

未開拓顧客検索ツール

SharePointサーバ(物理的にはMOSサーバに同居)

経営層ドキュメント管理 会議室予約 帳票出力

オーダー

支店発注送り込み計算 EJP発注

J-SCALE連携

コード変換

J-SCALE:TKのレイアウト変換

トランザクションデータの管理

レガシーマスター作成

レガシートラン作成

各システム間連携

レガシーマスター作成

レガシートラン作成

統合マスター管理

顧客系 顧客契約系

レガシーマスター管理(Tonedb01)

レガシー商品マスター 業種 住所

TONEHULFT

専伝マスタ?

翌日精算業務物コン連携

修理オーダー連携

共通機能 BI/CRM/SFA関連

三井住友

支払業務

J-SCALEのSAPシステムでは直結

SAP

補完

売掛金管理システム(顧客)

計上 請求 入金 残高 与信

リベートシステム(顧客)

リベート計算リベート/未払金

レガシー

J-SCALE個別

インフラ

共配売上・在庫

健康保険組合(カシオ情報機器:健康保険総合システム)

レセプト(法研)経理・人(適用)・給付・検診

CCCJ システム全体図

=BISS(支店系)

=BISS(BO)

フルコミッション

BISS支店系/在庫管理

ロード受払

支店オーダー

(CCEJPオーダー)

BISS 実行系

在庫

会計

購買

売掛システム

売掛管理

DWH

個店損益

Visit

売上分析

在庫管理

棚卸し

受注

EOS/DIAS

端末

BISS支店系/納品準備

ディスパッチ

プレロード

自社伝票発行(端末精算)

専用伝票発行

フルプレロード

BISS支店系/納品精算

フルハンディー

レギュラーハンディー

センター納品売上インターフェイス

BISS支店系/営業所事務

過不足管理

預り金管理

釣り銭管理

入金管理

リベート

協賛計上

物流システム配送費用計算

(CJL協力会社配送費)

在庫情報検索

人事システム

給与システム

SCM

需要予測

出荷計画

LCシステム

出荷予定

入出荷実績

DCシステム

出荷

マスタ管理

受注情報 納品情報

ロード情報

DC/TC積込指示

製品移管

伝票情報

保管場所移動

製品オーダー

その他(営業所間移管)

出荷指示

入荷検収

ロード情報

売上情報

売上情報

営業仕訳

売上代入金口座管理

営業仕訳情報

センター納品クロス配送

EOS

EOS

販売

出荷予定

入荷予定

セトルメント

フルコミッション管理

賞味期限管理

CCJC

DDIS

債権管理

各種仕訳情報

一往復オペレーション

在庫情報

小払い精算

フロントプロセス

テレセルセンター

CIMMS

顧客管理

契約単価管理

顧客情報商流管理情報物流管理情報自販機情報

専伝情報管理

チェーン情報管理

CJ I/F(レガシー)

商品管理

プロモーション

出荷実績

次世代SCM対象範囲

次世代SCM

導入後廃止

EOS 個店別情報

【主なシステムの外部データセンター設置場所】[富士通FIP中原センター]・現営業所(TKシステム)サーバ・売掛金管理システムサーバ・CJ I/F(インターフェース)サーバ[富士通FIP都築センター]・需給システムサーバ・テレセルDBサーバ※BISS支店系導入が完了次第、現営業所 (TK)システムは撤去事業所サーバはFSコミ リプレイス後撤去予定

[名古屋事務所]・中京地区LCシステムサーバ・関連会社システムサーバ

【システムリプレイス時期(予定)】・売掛金、協賛金、FSコミ :2014年・テレセルセンター :2015年・DWH :2014年~2015年

CokeOne+ ERP System Deployment

Before CokeOne+ ERP System:• Non-standardized business processes• Insufficient management reporting• From 26 legal entities to four• ~200 Loosely integrated systems• Complex – 2,500 interfaces• Multiple master databases

• CokeOne+ is a full transformation of business processes and people’s daily activities, including accounting, procurement, payment, manufacturing, inventory, shipping, etc.

• Such an integrated management system is a “must-have” to manage the current business, and a foundation for further business transformation.

• We experienced a short-term impact on supply chain management in Q2, resulting in limited customer disruption, as well as increased costs.

From April 2015One System; Cloud-Based

Q2 & YTD 2015

+11%

Volume Performance in the First HalfSequential Improvement during Q2 after Tax Rise

+17%

+15%

April May

June

+3%

-1.5%

Q1

Q2Solid

performance and share

growth

Cycling prior year

decline after c-tax hike

1H volume +5.4% (+0.1%*)

Q2 Highlights• Sendai acquisition April 1• Strong volume in April

cycling C-tax last year• Less CCEJ volume

promotions in June (2L water); Heavy competitor launch and promotional activity

Outlook• Slow start to July; End of

rainy season mid-month• Competitor promotions,

new products continue• Q3 peak season for

bottling business

1H Reported Volume by Quarter

Q2 Reported Volume by Month

10* Organic volume growth, not including Q2 acquisition of Sendai bottler

Sendai Bottler acquisition effective April 1

Cycling prior year growth; Less promo

activity in SM & Discounters

+6.7%*+4.4%*

--5.6%*

-+6.7%*-+4.4%*

-+1.3%*

Q2 & YTD 2015

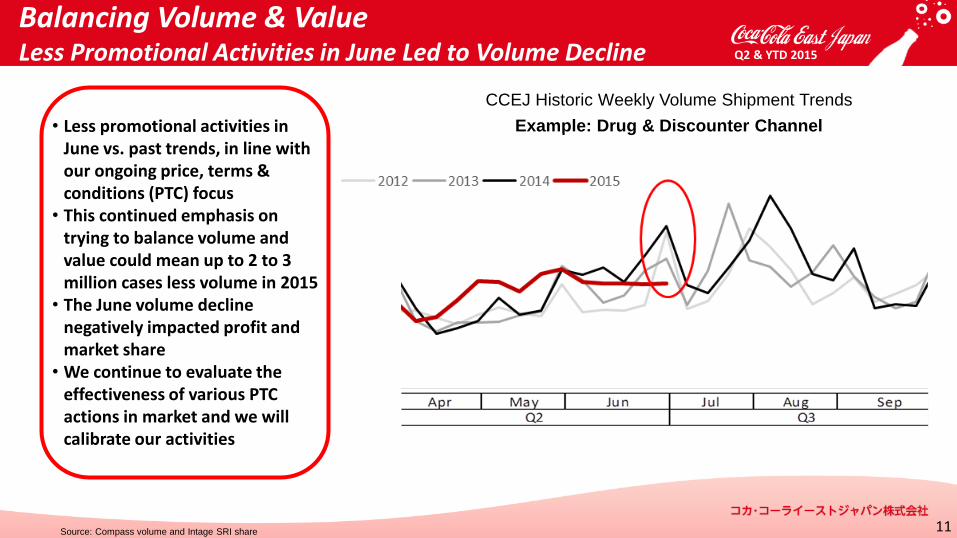

Source: Compass volume and Intage SRI share

CCEJ Historic Weekly Volume Shipment Trends

Example: Drug & Discounter Channel

Balancing Volume & ValueLess Promotional Activities in June Led to Volume Decline

• Less promotional activities in June vs. past trends, in line with our ongoing price, terms & conditions (PTC) focus

• This continued emphasis on trying to balance volume and value could mean up to 2 to 3 million cases less volume in 2015

• The June volume decline negatively impacted profit and market share

• We continue to evaluate the effectiveness of various PTC actions in market and we will calibrate our activities

11

Q2 & YTD 2015

Customer-Exclusive Branded Products Georgia European Renewal

Coca-Cola Bottle 100th Anniversary Coca-Cola Life Kiki Coke Taste Challenge

Q2

I lohas FOSHU Tea PEKO RAKU Crushable Large PET TSUMUGI Oolong Tea Toreta!Q2

Q2

KaradaSukoykacha W

1L PET

Connecting with the Consumer

Concept Cafe

Coffee House European opens in

Omotesando, Tokyo

Coca-Cola

Aluminum Contour Bottle

Share-a-Coke

I lohas

Aloe

I lohasTomato

Hajime Green Tea

Georgia Private Reserve

Using Japanese tea leaves

12

The great taste of Coca-Cola Zero

Q2 & YTD 2015

1 2 3 4 5 6 7 8 9 101112131415161718192021222324

Q3 +0.9

Q4+0.8

2014 +0.7

2014

Q2 +0.7Q1

+0.4

2013

Q2*-0.3

2015

Q1*+0.2

2015 YTD*

-0.1

Slight Share Loss Cycling Prior Year Growth

* Including Sendai Bottler (now South Tohoku Region)** Source: Intage, OTC channel, NARTD beverages

Volume Share vs. Prior Year Value Share vs. Prior Year

2015Market Share*

vs. Prior Year

Q2 YTD

Volume -0.3 -0.1Value -0.4 -0.1

Share gains in cola, teas, water;Challenges in flavored sparkling

June share reflects less promotional activity

Volume & value share growth in 6 of 7 quarters

13

1 2 3 4 5 6 7 8 9 101112131415161718192021222324

Q4+0.4

Q3 +0.6

Q2+0.9

Q1+0.2

2014 +0.5

20142013

Q2*-0.4

2015

Q1*+0.2

2015 YTD*

-0.1

Q2 & YTD 2015

vs. PriorYear

CVS D&DNat’l SM

LocalSM

VMEat & Drink

Q2 2015 +8% +1% -1% even -4% +15%

YTD 2015 +11% -1% -8% -3% -3% +10%

Total Volume, including SendaiQ2 +11.1%; YTD 2015 +5.4%

• CVS growth led by water, tea, coffee• Drug & Discounter, Supermarkets reflect less

promotional pricing and pullback in 2L water• Vending weak due to weather and channel mix.

Indoor outperforming outdoor.• Eating & Drinking growth led by outlet expansion

Channel Volume GrowthIncluding Sendai

Supermarket

(SM) 22%

Drug & Discounter

(D&D)

12%

Convenience Store (CVS)

15%

Eating & Drinking

13%

Vending (VM)27%

Others11%

Q2 Volume by Channel(% of total)

Volume Performance by Channel

14

vs. Prior Year CVS D&D Nat’l SM Local SM VM Eat & Drink

Q2 2015 +20% +13% +13% +7% +6% +23%

YTD 2015 +17% +6% even +1% +2% +14%

Organic VolumeExcluding Sendai Q2 +1.3%; YTD +0.1%

* BAPC (Bottler Actual Physical Cases)

Q2 & YTD 2015

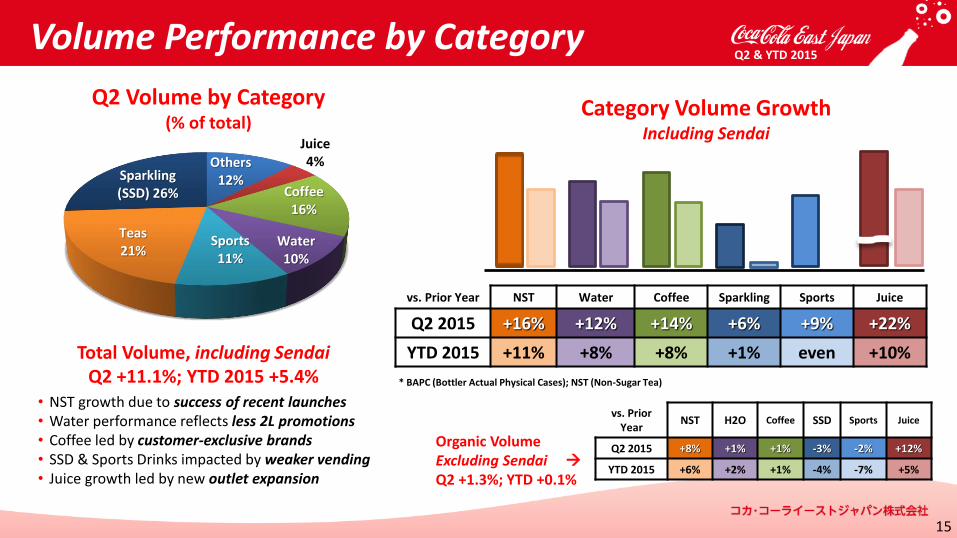

* BAPC (Bottler Actual Physical Cases); NST (Non-Sugar Tea)

vs. Prior Year NST Water Coffee Sparkling Sports Juice

Q2 2015 +16% +12% +14% +6% +9% +22%

YTD 2015 +11% +8% +8% +1% even +10%

Volume Performance by Category

Total Volume, including SendaiQ2 +11.1%; YTD 2015 +5.4%

• NST growth due to success of recent launches• Water performance reflects less 2L promotions• Coffee led by customer-exclusive brands• SSD & Sports Drinks impacted by weaker vending• Juice growth led by new outlet expansion

15

Others12%

Juice4%

Coffee16%

Water10%

Sports11%

Teas21%

Sparkling (SSD) 26%

Q2 Volume by Category(% of total)

vs. PriorYear

NST H2O Coffee SSD Sports Juice

Q2 2015 +8% +1% +1% -3% -2% +12%

YTD 2015 +6% +2% +1% -4% -7% +5%

Category Volume GrowthIncluding Sendai

Organic VolumeExcluding Sendai Q2 +1.3%; YTD +0.1%

Q2 & YTD 2015

Q2 & YTD 2015Financial Results

www.ccej.co.jp

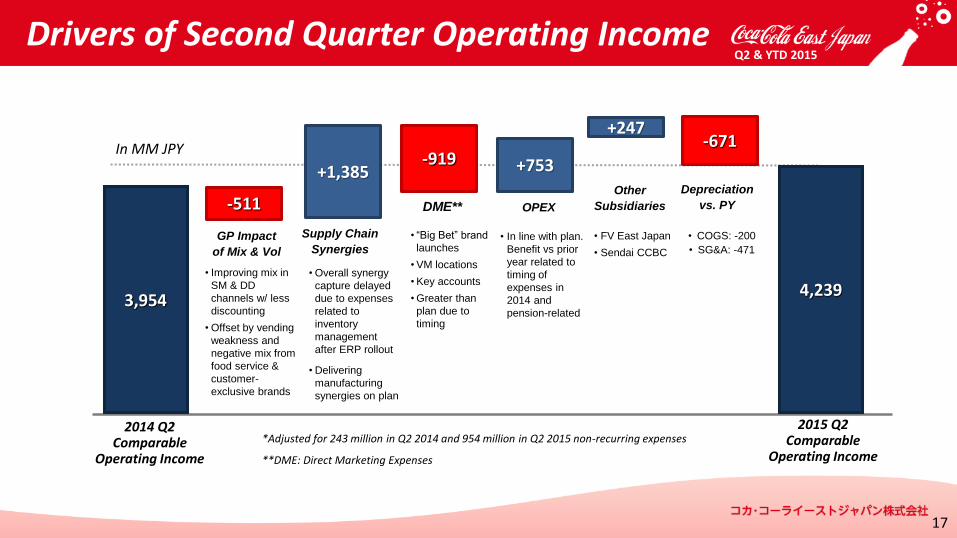

Drivers of Second Quarter Operating Income

+753

3,9544,239

-919

-511

In MM JPY

+247

+1,385

-671

17

2014 Q2Comparable

Operating Income

2015 Q2Comparable

Operating Income

GP Impact

of Mix & Vol

Supply Chain

Synergies

DME**

*Adjusted for 243 million in Q2 2014 and 954 million in Q2 2015 non-recurring expenses

**DME: Direct Marketing Expenses

OPEX

Other

Subsidiaries

• FV East Japan

• Sendai CCBC

Depreciation

vs. PY

• COGS: -200

• SG&A: -471

• Improving mix in

SM & DD

channels w/ less

discounting

• Offset by vending

weakness and

negative mix from

food service &

customer-

exclusive brands

• Overall synergy

capture delayed

due to expenses

related to

inventory

management

after ERP rollout

• Delivering

manufacturing

synergies on plan

• “Big Bet” brand

launches

• VM locations

• Key accounts

• Greater than

plan due to

timing

• In line with plan.

Benefit vs prior

year related to

timing of

expenses in

2014 and

pension-related

Q2 & YTD 2015

2015 Q2Actual

in million yen

2015 Q2One-time

items

2015 Q2Comparable

2014 Q2Comparable

Vs. PY

Diff %

Sales Volume(BAPC) (,000 cases)

80,784 - 80,784 72,725 8,059 +11.1

Net Revenue 151,828 - 151,828 136,580 15,248 +11.2

COGS 81,204 - 81,204 74,229 6,975 +9.4

Gross Profit 70,623 - 70,623 62,351 8,272 +13.3

SG&A 67,338 -954 66,384 58,397* 7,987 +13.7

Operating Income 3,285 954 4,239 3,954 285 +7.2

Profit Before Tax 2,850 1,414 4,219 4,086 133 +3.3

Net Income 2,531 910 3,441 2,437 1,005 +41.2

*Adjusted for 243 million in Q2 2014 non-recurring expensesNote: 2014 volume was revised in our Q4 2014 earnings announcement as a result of data and system standardization.

Second Quarter 2015 Results

18

• Balanced volume & revenue performance • Improving gross margin driven by manufacturing efficiency • Comparable SG&A

increase led by continued marketing investment & people costs • Q2 tax reflects deferred tax for consolidation of subs (FVEJ)

Q2 & YTD 2015

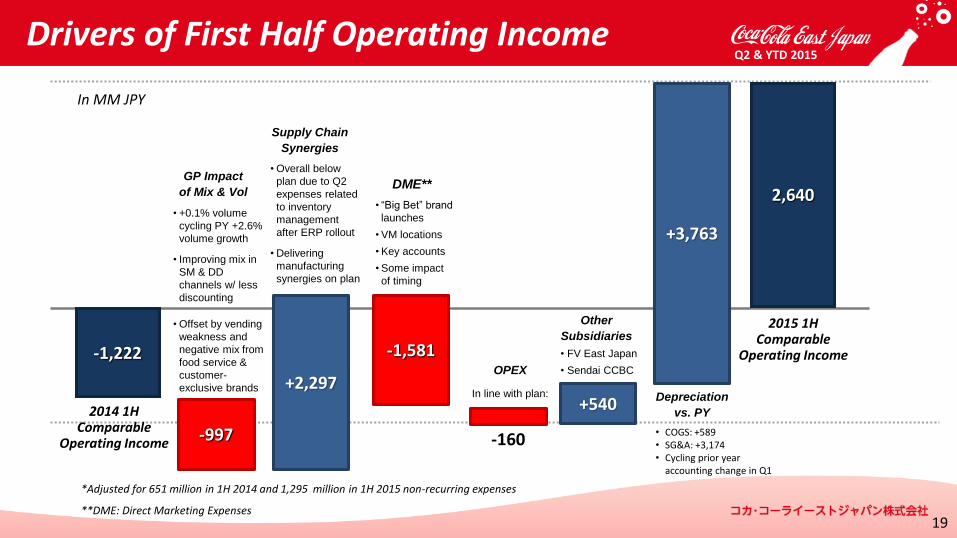

-1,222

2,640

-1,581

-997

In MM JPY

+540+2,297

+3,763

-160

19

2014 1HComparable

Operating Income

2015 1HComparable

Operating Income

GP Impact

of Mix & Vol

Supply Chain

Synergies

DME**

OPEX

Depreciation

vs. PY

• COGS: +589• SG&A: +3,174• Cycling prior year

accounting change in Q1

Drivers of First Half Operating Income

• +0.1% volume

cycling PY +2.6%

volume growth

• Improving mix in

SM & DD

channels w/ less

discounting

• Offset by vending

weakness and

negative mix from

food service &

customer-

exclusive brands

• Overall below

plan due to Q2

expenses related

to inventory

management

after ERP rollout

• Delivering

manufacturing

synergies on plan

• “Big Bet” brand

launches

• VM locations

• Key accounts

• Some impact

of timing

In line with plan:

Other

Subsidiaries

• FV East Japan

• Sendai CCBC

*Adjusted for 651 million in 1H 2014 and 1,295 million in 1H 2015 non-recurring expenses

**DME: Direct Marketing Expenses

Q2 & YTD 2015

2015 1HActual

in million yen

2015 1HOne-time

items

2015 1HComparable

2014 1HComparable

Vs. PY

Diff %

Sales Volume(BAPC) (,000 cases)

139,794 - 139,794 132,610 7,184 +5.4

Net Revenue 262,049 - 262,049 248,495 13,554 +5.5

COGS 140,051 - 140,051 135,781 4,270 +3.1

Gross Profit 121,997 - 121,997 112,714 9,283 +8.2

SG&A 120,651 -1,295 119,356 113,936* 5,420 +4.8

Operating Income 1,345 1,295 2,640 -1,222 3,862 -

Profit Before Tax 131 2,445 2,576 -1,036 3,612 -

Net Income 988 1,574 2,562 -1,540 4,102 -

*Adjusted for 651 million in 1H 2014 non-recurring expensesNote: 1H 2014 results include JPY 805 million in COGS and JPY 3,850 million in SG&A due to the write-off of residual value of existing tangible fixed assets related to a change in accounting policy Note: 2014 volume was revised in our Q4 2014 earnings announcement as a result of data and system standardization.

First Half 2015 Results

20

• Balanced volume and revenue performance • Improving gross margin driven by manufacturing efficiency • COGS and SG&A

benefit from cycling Q1 2014 accounting policy change • Q2 tax reflects additional deferred tax for consolidation of subs (FVEJ)

Q2 & YTD 2015

Second Half 2015Outlook

www.ccej.co.jp

Transform the summer

Transform yourself

22

Coca-Cola Summer CampaignQ2 & YTD 2015

23

Q2 & YTD 2015

Q3 the most important quarter of the year

We are strengthening Marketing & Execution programs in key channels

– Solid marketing calendar for second half of 2015

– Targeted promotional activities that respect PTC guidelines

Increased focus on Logistics optimization

– Increase direct shipments (plant to sales center) & reduce hub-to-hub moves

– Reduce finished goods transport distance; Improve efficiency of truck-loading

Close review of all operating expenses is underway

Second Half Outlook; “Reasons to Believe”

Continued stabilization and utilization of new ERP system in Q3; management of stable product supply as we fully shift to new system.

Two new production lines (Iwatsuki) to be commissioned in 2H

Additional Bottle Can capacity (Tokai) to be commissioned end of Q3

Operational integration of Sendai (now South Tohoku Region) and FV East Japan

Regional approach to Supply Chain optimization

Pricing, Terms & Conditions; Continued promotional optimization

Key Milestones in the Second Half

24

Q2 & YTD 2015

www.ccej.co.jp

APPENDIX

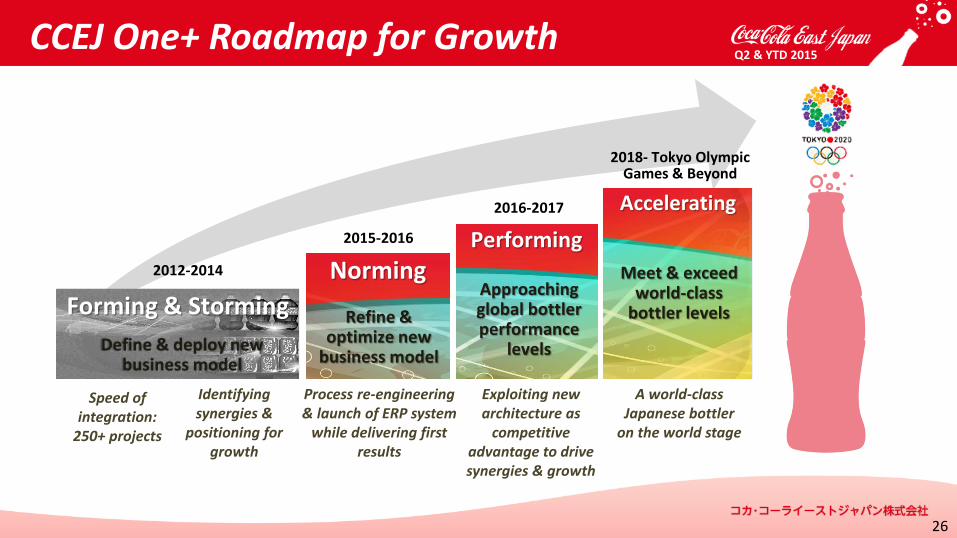

2015-2016

2016-2017

2018- Tokyo Olympic Games & Beyond

2012-2013

Forming

Accelerating

Meet & exceed world-class

bottler levels

A world-class Japanese bottler

on the world stage

Performing

Approaching global bottler performance

levels

Exploiting new architecture as

competitive advantage to drive synergies & growth

Norming

Refine & optimize new

business model

Process re-engineering& launch of ERP system

while delivering first results

26

2012-2014

Speed of integration:

250+ projects

Forming & Storming

Define & deploy new business model

Identifying synergies &

positioning for growth

CCEJ One+ Roadmap for GrowthQ2 & YTD 2015

The Coca-Cola System

The Coca-Cola system in Japan consists of the Coca-Cola (Japan) Company (CCJC), bottlers and other related companies.

CCJC, as the franchise owner, is responsible for supplying concentrate and beverage bases (coffee beans, tea leaves, juices, etc.) for allof Coca-Cola’s brands, as well as R&D, innovation, and marketing and brand development.

The bottlers, including CCEJ, as franchisees, are responsible for manufacturing, distribution and selling the finished products. We all areworking together with our system partners to grow the Coca-Cola business by optimizing our overall operations through more efficientproduction and distribution, marketplace execution that is firmly focused on the consumer, faster response to market preferences,enhanced customer service, and rigorous quality control.

Coca-Cola Tokyo Research & Development Co., Ltd. (CCTR&D)

Product development and technical support to respond to the needs of the customer in Japan. A wholly owned subsidiary of The Coca-Cola Company.

Coca-Cola Business Service Co., Ltd. (CCBSC)

Providing joint procurement of raw materials, packaging, etc. as well as business consulting services, developing and maintaining the information systems to support Coca-Cola System. Jointly owned by The Coca-Cola Company and all the

bottlers in Japan.

Coca-Cola Customer Marketing Company (CCCMC)

Business negotiations window for nationwide retail, convenience stores,supermarket and food-service chains as well as developing proposals for sales promotions and storefront activities. Jointly owned by CCJC and all the bottlers in

Japan.

FV Corporation Co., Ltd. (FVC) Sales negotiations window for national chain vending operators, and deals non-Coca-Cola products as well as Coca-Cola branded products. Jointly owned by CCJC and all the bottlers in Japan.

Other Coca-Cola System Related Companies in Japan

A powerful partnership driving growth of the Coca-Cola business

27

Q2 & YTD 2015

Glossary of Frequently Used Terms

CDE Abbreviation of Cold Drink Equipment. Vending machines, coolers and beverage dispensers, etc.

Coolers The equipment with Coca-Cola’s logos which keeps beverages at an appropriate temperature (chilled and/or hot) for immediate consumption, and ready for selling them at the storefront of retail outlets and restaurants. It serves as point-of–sales advertising, too.

DME Abbreviation of Direct Marketing Expenses. Sales promotion-related expenses reported in advertisement & sales promotion expenses and partly in sales commissions of SG&A.

FC Abbreviation of Future Consumption. Purchase or sell beverage for future consumption in home, etc. It also means the products / SKUs for FC (for example, single packages 1L or more and multi-pack of IC packages) and channels that consumers purchase the beverages for FC. (for example, supermarket, drug & discounter channels, etc.).

HORECA Abbreviation of Hotel, Restaurants and Cafeteria. Generally means sales channels of these kinds.

IC Abbreviation of Immediate Consumption. Purchase or sell beverage for consuming it immediately. It also means the products / SKUs for IC (for example, single packages less than 1L as well as fountains) and channels that consumers purchase the beverages for IC(for example, vending machine, convenience stores channels, etc.).

OBPPC Abbreviation of Occasion, Brand, Package, Price, Channel. A segmentation strategy tailored to consumption opportunities in five areas: occasion, brand, package, price and channel.

Operational Excellence (OE)

The Coca-Cola System’s way to develop people and culture around productivity which allows higher financial value achievement by driving sustainable improvement using common language and tools as well as focusing on business priorities.

RTM Abbreviation of Route-to-Market. A framework, a process, a philosophy, a proven approach for driving profitable growth.

28

Q2 & YTD 2015

www.ccej.co.jp

THANK YOUCoca-Cola East Japan

Q2 &YTD 2015 Earnings PresentationAugust 7, 2015

<Inquiries>Investor Relations

Coca-Cola East Japan

[email protected]+81-3-5575-3797

http://investor.ccej.co.jp/