Embed Size (px)

Citation preview

NOT FOR DISTRIBUTION IN THE UNITED STATES, CANADA, AUSTRALIA, NEW ZEALAND OR JAPAN

This document comprises a Prospectus relating to Coca-Cola HBC AG (the ‘‘Company’’ or ‘‘CCHBC AG’’)and has been prepared in accordance with the Prospectus Rules of the Financial Services Authority (the‘‘FSA’’) made under Section 73A of the Financial Services and Markets Act 2000 (as amended) (the‘‘FSMA’’), has been filed with the FSA and has been made available to the public as required by theProspectus Rules. The Company intends to request that the FSA provides a certificate of approval and acopy of this Prospectus to the relevant competent authorities in Greece, in connection with the admissionto trading of the Ordinary Shares on the Athens Exchange and the offering of Ordinary Shares to thepublic in connection with the Share Exchange Offer and in Austria, in connection with the offering ofOrdinary Shares to the public in connection with the Share Exchange Offer.

Application has been made to the FSA for all of the Ordinary Shares to be admitted to the premium listingsegment of the Official List of the UK Listing Authority (the ‘‘Official List’’) and to the London StockExchange plc (the ‘‘London Stock Exchange’’) for such Ordinary Shares to be admitted to trading on theLondon Stock Exchange’s main market for listed securities (together, ‘‘Admission’’). Admission constitutesadmission to trading on a regulated market. It is expected that Admission will become effective, and thatunconditional dealings will commence in the Ordinary Shares on the London Stock Exchange, at 8.00 a.m.(London time) on or around 29 April 2013. The Company has applied for a secondary listing of theOrdinary Shares on the Athens Exchange S.A. (‘‘Athens Exchange’’), subject to the receipt of necessaryapprovals. The Company will also make an application for listing of the New ADSs on the New York StockExchange (‘‘NYSE’’).

The new Ordinary Shares issued by the Company will rank pari passu in all respects with the other issuedOrdinary Shares and will carry the right to receive all dividends and distributions declared, made or paidon or in respect of the issued Ordinary Shares after Admission.

The Company, its Directors and the Proposed Directors (whose names appear on page 46 of thisProspectus) accept responsibility for the information contained in this Prospectus. To the best of theknowledge and belief of the Company, the Directors and the Proposed Directors (who have taken allreasonable care to ensure that such is the case), the information contained in this Prospectus is inaccordance with the facts and contains no omission likely to affect the import of such information.

Coca-Cola HBC AG(incorporated as a stock corporation (Aktiengesellschaft) under the laws of Switzerland

and registered in Switzerland with registered number CH-170.3.037.199-9)

Proposed issue of up to 366,553,507 Ordinary Shares in connection with the ShareExchange Offer for Coca-Cola Hellenic Bottling Company S.A. (‘‘CCH’’) and

application for admission of up to 367,553,507 Ordinary Shares to the premiumlisting segment of the Official List and to trading on the London Stock Exchange’s

main market for listed securities

Credit SuisseSponsor

You should read this Prospectus in its entirety. Your attention is specifically drawn to the discussion ofcertain risk and other factors that should be considered in connection with an investment in the OrdinaryShares, as set out in the section entitled ‘‘Risk Factors’’ on pages 25 to 45 of this Prospectus.

Prospective investors should rely only on the information contained in this Prospectus. No person has beenauthorised to give any information or to make any representations other than those contained in thisProspectus and, if given or made, such information or representations must not be relied on as having beenso authorised by the Company, the Directors, the Proposed Directors or the Sponsor. Any delivery of thisProspectus shall not, under any circumstances, create any implication that there has been no change in theaffairs of the Company or the CCH Group taken as a whole since, or that the information contained hereinis correct at any time subsequent to, the date of this Prospectus. In particular, neither the contents of theCompany’s website (www.coca-colahbcag.com) nor CCH’s website (www.coca-colahellenic.com) isincorporated into, or forms part of, this Prospectus and prospective investors should not rely on either ofthem. The contents of this document are not to be construed as legal, financial or tax advice. Eachrecipient of this document should consult his, her or its own legal adviser, independent financial adviser ortax adviser for legal, financial or tax advice.

This Prospectus does not constitute an offer of, or the solicitation of an offer to subscribe for or buy, anyOrdinary Shares to any person in any jurisdiction in which such offer or solicitation is unlawful.

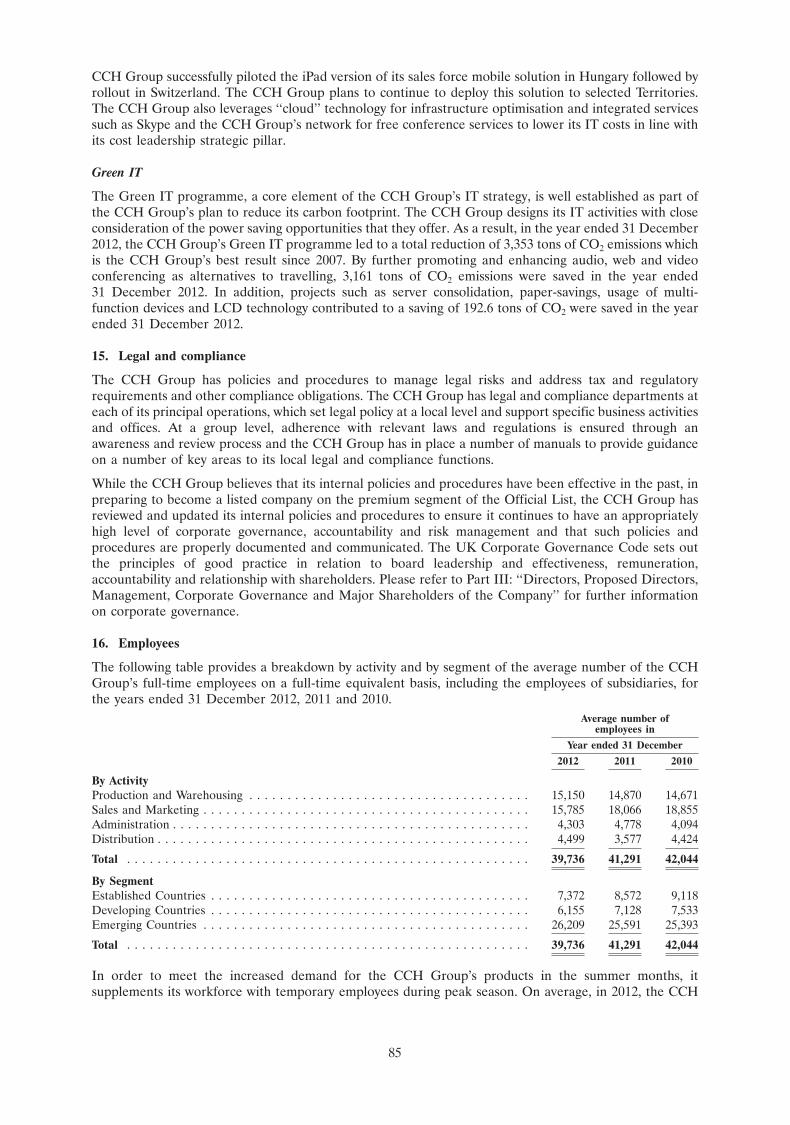

The distribution of this Prospectus and the offer of the Ordinary Shares in certain jurisdictions may berestricted by law. Other than in the United Kingdom, Greece and Austria, no action has been or will betaken by the Company to permit a public offering of the Ordinary Shares or to permit the possession ordistribution of this Prospectus (or any other offering or publicity materials relating to the Ordinary Shares)in any jurisdiction where action for that purpose may be required. Neither this Prospectus, anyadvertisement nor any other material relating to it may be distributed or published in any jurisdictionexcept under circumstances that will result in compliance with any applicable laws and regulations. Personsinto whose possession this Prospectus comes should inform themselves about and observe any suchrestrictions. Any failure to comply with these restrictions may constitute a violation of the securities laws ofany such jurisdiction.

The Sponsor is authorised and regulated in the United Kingdom by the FSA and is acting exclusively forthe Company and no-one else in connection with Admission, and it will not regard any other person(whether or not a recipient of this Prospectus) as a client in relation to Admission. Apart from theresponsibilities and liabilities, if any, imposed on the Sponsor by FSMA or the regulatory regimeestablished thereunder, the Sponsor accepts no responsibility or liability whatsoever for the contents of thisProspectus, or for any other statement made or purported to be made in it, in connection with theCompany, its Ordinary Shares or this Prospectus. The Sponsor accordingly disclaims all and anyresponsibility or liability, whether arising in tort, contract or otherwise (save as referred to above), which itmight otherwise have in respect of this Prospectus or any such statement.

THE ORDINARY SHARES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SEC,ANY OTHER FEDERAL OR STATE SECURITIES COMMISSION IN THE US OR ANY OTHERUS REGULATORY AUTHORITY, NOR HAVE ANY SUCH AUTHORITIES PASSED UPON,CONFIRMED THE ACCURACY OF OR DETERMINED THE ADEQUACY OF THISPROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENCE INTHE US.

A registration statement under the US Securities Act of 1933, as amended (the ‘‘Securities Act’’) in respectof the Ordinary Shares, including such Ordinary Shares represented by New ADSs, to be offered toExisting Shareholders located in the United States and all holders of Existing ADSs, wherever located, hasbeen filed with the US Securities and Exchange Commission (the ‘‘SEC’’). As at the date of thisProspectus, such registration statement has not yet been declared effective.

NOTICE TO HOLDERS IN THE EUROPEAN ECONOMIC AREA

In relation to each Member State of the European Economic Area which has implemented the ProspectusDirective (each, a ‘‘Relevant Member State’’), an offer to the public of any Ordinary Shares (including bymeans of a resale or other transfer) may not be made in that Relevant Member State, other than the ShareExchange Offer in the United Kingdom, Greece or Austria contemplated in this Prospectus (from the timethe Prospectus has been approved by the UK Listing Authority, in its capacity as the competent authorityin the United Kingdom, and published in accordance with the Prospectus Directive as implemented in theUnited Kingdom and in the case of Greece and Austria, passported), except that an offer to the public inthat Relevant Member State of the Ordinary Shares may be made at any time under the followingexemptions under the Prospectus Directive, if and as they have been implemented in that RelevantMember State:

• to legal entities which are qualified investors as defined in the Prospectus Directive;

• to fewer than 100, or, if the Relevant Member State has implemented the relevant provisions of the2010 PD Amending Directive, 150, natural or legal persons (other than qualified investors as definedin the Prospectus Directive), as permitted under the Prospectus Directive; or

• in any other circumstances falling within Article 3(2) of the Prospectus Directive,

provided that no such offer of Ordinary Shares shall result in a requirement for the Company to publish aprospectus pursuant to Article 3 of the Prospectus Directive or supplement a prospectus pursuant toArticle 16 of the Prospectus Directive.

For the purposes of the provisions above, the expression an ‘‘offer to the public’’ in relation to anyOrdinary Shares in any Relevant Member State means the communication in any form and by any meansof sufficient information on the terms of the Share Exchange Offer and the Ordinary Shares to be offeredso as to enable an investor to decide to accept the Share Exchange Offer, as the same may be varied in that

i

Member State by any measure implementing the Prospectus Directive in that Member State, theexpression ‘‘Prospectus Directive’’ means Directive 2003/71/EC (and amendments thereto, including the2010 PD Amending Directive, to the extent implemented in the Relevant Member State), and includes anyrelevant implementing measure in each Relevant Member State and the expression ‘‘2010 PD AmendingDirective’’ means Directive 2010/73/EU.

NOTICE TO INVESTORS IN FRANCE

This Prospectus and any other offering material relating to the Ordinary Shares has not been prepared inthe context of a public offering in France within the meaning of Article L. 411-1 of the French Codemonetaire et financier and Title I of Book II of the Reglement general of the Autorite des marches financiers(the ‘‘AMF’’) and therefore has not been submitted for clearance to the AMF or to the competentauthority of another member state of the European Economic Area and notified to the AMF.

The Ordinary Shares are not being offered or sold, directly or indirectly, to the public in France and thisProspectus and any other offering material relating to the Ordinary Shares has not been and will not bedistributed or caused to be distributed to the public in France or used in connection with any offer to thepublic in France. Such offers, sales and distributions of the Ordinary Shares in France will be made only to:(i) providers of investment services relating to portfolio management for the account of third parties(personnes fournissant le service d’investissement de gestion de portefeuille pour compte de tiers); and/or(ii) qualified investors (investisseurs qualifies), acting for their own account, in accordance with theconditions laid down by Articles L. 411-1, L. 411-2, D. 411-1, D. 411-2, D. 744-1, D. 754-1 and D. 764-1 ofthe French Code monetaire et financier.

Any direct or indirect dissemination into the public of any Ordinary Shares so acquired can only take placein accordance with the conditions of articles L. 411-1, L. 411-2, L. 412-1 and L. 621-8 -to L. 621-8-3 of theFrench Code monetaire et financier.

NOTICE TO INVESTORS IN GERMANY

No action has been or will be taken in the Federal Republic of Germany that would permit a publicoffering of the Ordinary Shares, or distribution of a prospectus or any other offering material relating tothe Ordinary Shares. In particular, no securities prospectus (Wertpapierprospekt) within the meaning of theGerman Securities Prospectus Act (Wertpapierprospektgesetz—WpPG) of 22 June 2005, as amended (the‘‘German Securities Prospectus Act’’), has been or will be published within the Federal Republic ofGermany, nor has this Prospectus been filed with, passported to or approved by the German FederalFinancial Supervisory Authority (Bundesanstalt fur Finanzdienstleistungsaufsicht) for publication within theFederal Republic of Germany. Accordingly, any offer or sale of the Ordinary Shares or any distribution ofoffering material within the Federal Republic of Germany may violate the provisions of the GermanSecurities Prospectus Act.

Dated 7 March 2013

ii

TABLE OF CONTENTS

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

DIRECTORS, SECRETARY, REGISTERED AND HEAD OFFICE AND ADVISERS . . . . . . 46

EXPECTED TIMETABLE OF PRINCIPAL EVENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

PRESENTATION OF INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

ENFORCEMENT OF JUDGMENTS IN SWITZERLAND . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

PART I: INFORMATION ON THE CCH GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

PART II: INFORMATION ON THE SHARE EXCHANGE OFFER, THE GREEKSTATUTORY SQUEEZE-OUT AND THE GREEK STATUTORY SELL-OUT . . . 90

PART III: DIRECTORS, PROPOSED DIRECTORS, MANAGEMENT, CORPORATEGOVERNANCE AND MAJOR SHAREHOLDERS OF THE COMPANY . . . . . . 98

PART IV: CCH’s RELATIONSHIP WITH TCCC, KAR-TESS HOLDING AND OTHERRELATED PARTIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

PART V: SELECTED FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

PART VI: OPERATING AND FINANCIAL REVIEW AND PROSPECTS . . . . . . . . . . . . . . 130

PART VII: CAPITALISATION AND INDEBTEDNESS STATEMENT . . . . . . . . . . . . . . . . . . 171

PART VIII: HISTORICAL FINANCIAL INFORMATION OF THE CCH GROUP . . . . . . . . . 173

SECTION A: ACCOUNTANT’s REPORT ON THE HISTORICAL FINANCIALINFORMATION OF THE CCH GROUP . . . . . . . . . . . . . . . . . . . . 173

SECTION B: HISTORICAL FINANCIAL INFORMATION OF THE CCHGROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

PART IX: TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 256

PART X: CREST AND CREST DEPOSITARY INTERESTS . . . . . . . . . . . . . . . . . . . . . . . . 270

PART XI: MANNER OF HOLDING ORDINARY SHARES . . . . . . . . . . . . . . . . . . . . . . . . 272

PART XII: COMPARISON OF SHAREHOLDER RIGHTS IN CCH AND THE COMPANY . 274

PART XIII: ADDITIONAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 300

PART XIV: DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342

iii

SUMMARY

Summaries are made up of disclosure requirements known as ‘Elements’. These elements are numbered inSections A-E (A.1-E.7).

This summary contains all the Elements required to be included in a summary for this type of security andissuer. Because some Elements are not required to be addressed there may be gaps in the numberingsequence of the Elements.

Even though an Element may be required to be inserted into the summary because of the type of securityand issuer, it is possible that no relevant information can be given regarding the Element. In this case, ashort description of the Element is included in the summary with the mention of ‘not applicable’.

Section A—Introduction and warnings

Element Disclosure requirement Disclosure

A.1 Warning This summary should be read as an introduction to theProspectus. Any decision to invest in the securities should bebased on consideration of the Prospectus as a whole by theinvestor. Where a claim relating to the informationcontained in the Prospectus is brought before a court, theplaintiff investor might, under the national legislation of themember states of the European Economic Area (the‘‘EEA’’), have to bear the costs of translating the Prospectusbefore the legal proceedings are initiated. Civil liabilityattaches only to those persons who have tabled the summaryincluding any translation thereof, but only if the summary ismisleading, inaccurate or inconsistent when read togetherwith the other parts of the Prospectus or it does not provide,when read together with the other parts of the Prospectus,key information in order to aid investors when consideringwhether to invest in the securities.

A.2 Subsequent resale of Not applicable. No consent has been given by the Companysecurities or final to the use of the Prospectus for subsequent resale or finalplacement of securities placement of securities by financial intermediaries. Thethrough financial Company is not engaging any financial intermediaries forintermediaries any resale of securities or final placement of securities in

connection with this Prospectus.

Section B—Issuer

Element Disclosure requirement Disclosure

B.1 Legal and commercial Coca-Cola HBC AGname

B.2 Domicile and legal form The Company was incorporated and registered inSwitzerland on 19 September 2012 as a stock corporation(Aktiengesellschaft/societe anonyme) under the laws ofSwitzerland with corporate registrationnumber CH-170.3.037.199-9 and its registered office and itsprincipal executive office is at Baarerstrasse 14, 6300 Zug,Switzerland. The Company is governed by its Articles. Theprincipal legislation under which the Company operates andunder which the Ordinary Shares are issued is the SwissCode of Obligations.

B.3 Operations and principal Upon completion of the Share Exchange Offer and atactivities Admission, the Company is expected to own at least 90% of

the total issued share capital of CCH and will become the

1

Section B—Issuer

Element Disclosure requirement Disclosure

parent undertaking of CCH, which is the current parentundertaking of the CCH Group. If the level of acceptance ofthe Share Exchange Offer is at least 90% of CCH’s totalissued share capital, the Company expects to be able toexercise the Greek Statutory Squeeze-out and therefore tobecome the sole shareholder in CCH and the ultimateholding company of the CCH Group.

The CCH Group is one of the largest bottlers ofnon-alcoholic ready-to-drink beverages in Europe,operating in 28 countries. It owns, controls and operates anetwork of independent bottling plants and warehousingand distribution systems. The CCH Group’s business isprincipally engaged in producing, selling and distributingnon-alcoholic ready-to-drink beverages under bottlers’agreements with TCCC. The CCH Group also produces,sells and distributes non-alcoholic ready-to-drink beveragesunder bottlers’ agreements and franchise arrangements withthird parties and under its own brand names. It alsodistributes beer and third party premium spirits in certain ofits central and eastern European operations.

The CCH Group divides its Territories in which it operatesinto three reporting segments. The Territories included ineach segment share similar socio-economic characteristics,consumer habits, per capita consumption levels, as well as,regulatory environments, growth opportunities, customersand distribution infrastructures. The CCH Group’s threereporting segments are as follows:

(i) established countries, which are Italy, Greece, Austria,the Republic of Ireland, Northern Ireland, Switzerlandand Cyprus (‘‘Established Countries’’);

(ii) developing countries, which are Poland, Hungary, theCzech Republic, Croatia, Lithuania, Latvia, Estonia,Slovakia and Slovenia (‘‘Developing Countries’’); and

(iii) emerging countries, which are the Russian Federation,Romania, Nigeria, Ukraine, Bulgaria, Serbia(including the Republic of Kosovo), Montenegro,Belarus, Bosnia and Herzegovina, Armenia, Moldovaand (through an equity investment) the FormerYugoslav Republic of Macedonia (‘‘EmergingCountries’’).

B.4a Significant recent trends Trends in Established Countries

• The Established Countries typically exhibit high levelsof disposable income per capita relative to theDeveloping and Emerging Countries.

• Macroeconomic and trading conditions havedeteriorated in some of the Established Countries inthe last two years, particularly in Greece, the Republicof Ireland and more recently Italy.

2

Section B—Issuer

Element Disclosure requirement Disclosure

• The ongoing sovereign debt crisis in the EU andparticularly in the eurozone has resulted in a slowdownand, in many cases, a contraction in the real grossdomestic product (‘‘GDP’’) of the EstablishedCountries.

• At the same time, deteriorating consumer confidenceand rising unemployment has had an adverse impact onconsumer demand.

Trends in Developing Countries

• Apart from Croatia, all of the Developing Countriesjoined the EU on 1 May 2004.

• The Developing Countries generally have lowerdisposable income per capita than the EstablishedCountries and continue to be exposed to economicvolatility from time to time.

• Macroeconomic conditions had been positive in theDeveloping Countries in the years prior to 2008, withall countries experiencing positive real GDP growth.

• However, economic growth has slowed or reversed inthe last three years as a result of the global financialand credit crisis. In 2011, GDP growth andunemployment stabilised in the Developing Countries.

• Currency fluctuations in the Developing Countriesrelative to the euro has been another significant factorcontributing to economic volatility in recent years.

Trends in Emerging Countries

• The Emerging Countries are exposed to greaterpolitical and economic volatility and have lower percapita GDP than the Developing or EstablishedCountries.

• Demographic characteristics are much more favourablein the Emerging Countries compared to the Establishedand Developing Countries, as the segment is typified byyounger and faster growing populations, particularly inNigeria.

• Consumer demand in Emerging Countries is especiallyprice sensitive, making the affordability of the CCHGroup’s products even more important.

• The Emerging Countries were the first to be affected bythe global financial and credit crisis of 2008.

• Since then the CCH Group has not experiencedconcrete and sustained evidence of recovery. Eventhough GDP appears to have stabilised in the EmergingCountries and in some cases returned to growth in2011, unemployment remained at high levels andcurrencies were very volatile, particularly in the secondhalf of 2011.

• The Emerging Countries are traditionally exposed toworld commodity prices and in this sense, have recentlyexperienced a large adverse impact from higher PETresin and world sugar prices.

3

Section B—Issuer

Element Disclosure requirement Disclosure

Anticipated trends

• The CCH Group has experienced a sustained period ofinput cost pressures, mainly attributable to EU sugarprices, but has recently observed an easing in inputcosts, primarily driven by lower PET prices, and expectsthat in the current fiscal year its revenue growthstrategy will fully recover the increase in total inputcosts in absolute terms. The CCH Group also continuesto expect a significant negative impact from currencymovements.

• The CCH Group has not yet seen signs of sustainableimprovement in consumer confidence or a resolution ofthe sovereign debt crisis. The CCH Group thereforeexpects economic volatility to be more pronouncedprimarily in the Established Countries, as well as theDeveloping Countries.

• In the Emerging Countries, Russia is expected to be akey driver and as at the date of this Prospectus, theCCH Group expects a gradual improvement ineconomic conditions.

• There is potential risk of further taxes on soft drinks, asgovernments in the regions where the CCH Groupoperates are constantly seeking for additional sourcesof revenue in order to finance their budget deficits.

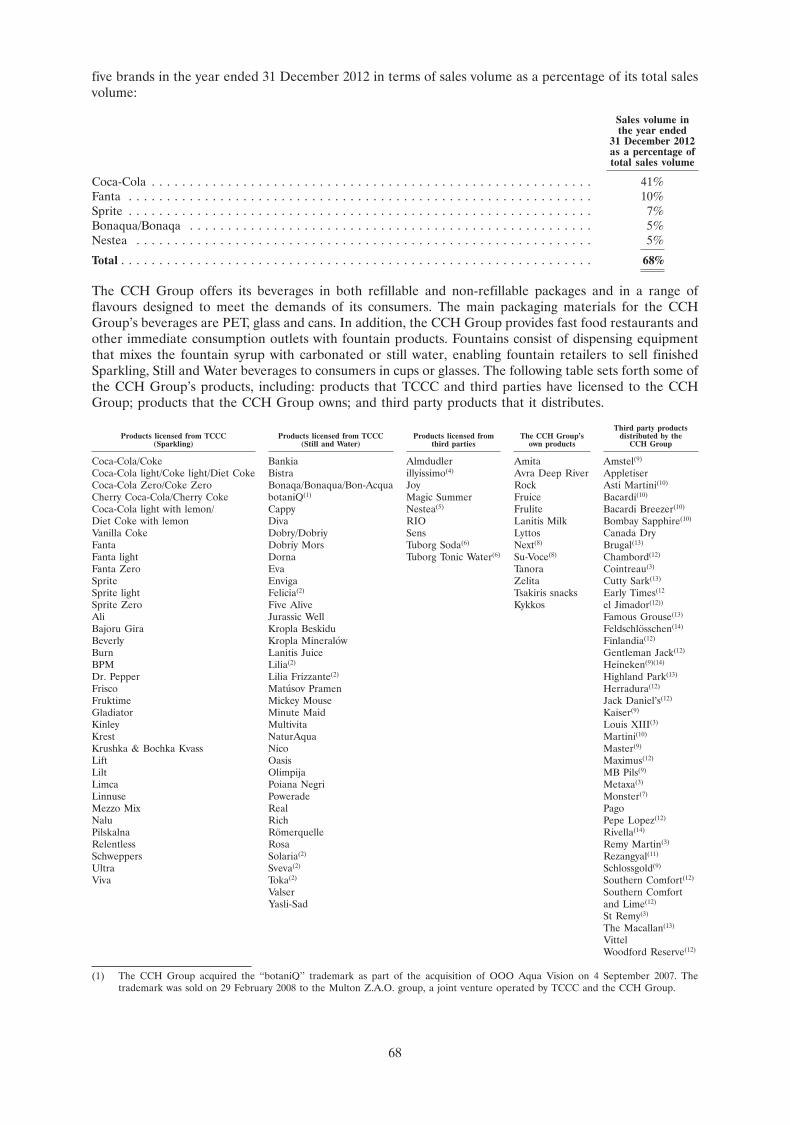

B.5 Group description The CCH Group’s business is principally engaged inproducing, selling and distributing non-alcoholicready-to-drink beverages under bottlers’ agreements withTCCC. In addition, the CCH Group bottles and distributesbeer in Bulgaria and the Former Yugoslav Republic ofMacedonia and distributes a selected number of premiumspirit brands in certain central and eastern Europeanoperations. The CCH Group is one of the largest bottlers ofnon-alcoholic ready-to-drink beverages in Europe,operating in 28 countries with a total population ofapproximately 581 million people (including the CCHGroup’s equity investments in Brewinvest S.A., a businessengaged in the bottling and distribution of beer in Bulgariaand BrewTech B.V., a business engaged in the bottling anddistribution of beer and non-alcoholic ready-to-drinkbeverages in the Former Yugoslav Republic of Macedonia).In the year ended 31 December 2012, the CCH Group soldapproximately 2.1 billion case units, generating net salesrevenue of A7.0 billion. In the year ended 31 December2011, the CCH Group sold approximately 2.1 billion unitcases, generating net sales revenue of A6.8 billion.

The CCH Group’s products include sparkling non-alcoholicready-to-drink beverages, excluding sparkling water(‘‘Sparkling’’ beverages), non-sparkling non-alcoholicready-to-drink beverages, excluding water (‘‘Still’’beverages) and various water beverages (‘‘Water’’beverages). In the year ended 31 December 2012, theSparkling beverages category accounted for 69% and the

4

Section B—Issuer

Element Disclosure requirement Disclosure

combined Still and Water beverages category accounted for31% of the CCH Group’s sales volume, as compared,respectively, to 68% and 32% in the year ended31 December 2011. The CCH Group offers its products in arange of flavours and package combinations which varyfrom country to country.

The CCH Group is one of TCCC’s key bottlers. TCCCconsiders the CCH Group to be a strategic partner, basedon factors such as size, geographic diversification andfinancial and management resources, and in which TCCChas a significant equity interest. In their day-to-day businessrelationship, TCCC and the CCH Group work closelytogether to maximise the success of TCCC’s brand-relatedbusiness. Whereas TCCC’s focus is on general consumermarketing and brand promotion of TCCC’s products(involving, for example, building TCCC brand equity,analysing consumer preferences and formulating generalstrategies and media advertising plans), the CCH Group hasprimary responsibility for, and controls, the customerrelationships and route to market in each of its relevantTerritories and develops and implements its own sales andmarketing strategy in each of its relevant Territories.

The CCH Group has entered into bottlers’ agreements withTCCC for each of the Territories under which the CCHGroup has the right to exclusively produce and, subject tocertain limitations, sell and distribute products of TCCC ineach of those Territories. Sales of products of TCCC(including trademarked beverages of joint ventures to whichTCCC is a party) represented approximately 96% of theCCH Group’s total sales volume in the year ended31 December 2012, with sales of products under theCoca-Cola brand, the world’s most recognised brand,representing approximately 41% of the CCH Group’s totalsales volume in that period. In addition to the Coca-Colabrand, the CCH Group’s other core brands include Fanta,Sprite, Coca-Cola light (which the CCH Group sells in someof its Territories, under the Diet Coke trademark) andCoca-Cola Zero. The CCH Group’s core brands togetheraccounted for approximately 63% of its total sales volume inthe year ended 31 December 2012. The CCH Group alsoproduces, sells and distributes a broad range of brands ofother Sparkling, Still and Water beverage products whichvary from country to country.

The bottlers’ agreements also require the CCH Group topurchase from TCCC and its authorised suppliers all of itsrequirements of concentrate for beverages of TCCC. Underthe bottlers’ agreements TCCC sells concentrate to theCCH Group at prices that TCCC is entitled to determine inits sole discretion, including the conditions of shipment andpayment, as well as the currency of the transaction. Inpractice, TCCC normally sets concentrate prices only afterdiscussions with the CCH Group so as to reflect tradingconditions in the relevant country and so as to ensure thatsuch prices are in line with the CCH Group’s and TCCC’s

5

Section B—Issuer

Element Disclosure requirement Disclosure

respective sales and marketing objectives for particularTCCC brand-related products and particular Territories.TCCC generally uses an incidence-based model in relationto the CCH Group to determine the price at which it sellsconcentrate to the CCH Group, which generally tracks apercentage of the CCH Group’s net sales revenue agreedfrom time to time. The CCH Group’s total purchases ofconcentrate from TCCC amounted to A123.2 million,A1,255.0 million, A1,244.8 million and A1,290.2 million in theperiod ended 25 January 2013 and in the years ended31 December 2012, 2011 and 2010, respectively. In additionto concentrate, the CCH Group purchased finished goodsand other materials from TCCC in amounts of A2.0 million,A50.4 million, A56.0 million and A78.0 million in the periodended 25 January 2013 and in the years ended 31 December2012, 2011 and 2010, respectively.

B.6 Notification interests; The Company was incorporated by Kar-Tess Holding, adifferent voting rights; significant shareholder in CCH, in order to facilitate thecontrolling interests Share Exchange Offer. As at the date of this Prospectus, the

Company has no operations and no material assets orliabilities other than in connection with the Share ExchangeOffer. With effect on and from Admission, as a result of theShare Exchange Offer, the Company will not be wholly-owned, directly or indirectly, by any person. However, witheffect on and from Admission, as a result of the ShareExchange Offer, the Company is expected to have twosignificant shareholders: Kar-Tess Holding and TCCC, whoown approximately 23.3% and 23.2% of CCH’s total issuedshare capital, respectively. The Company has receivedconfirmation from TCCC that it supports the ShareExchange Offer and intends to tender in the ShareExchange Offer and Kar-Tess Holding has stated that it willtender all of its Existing Securities in the Share ExchangeOffer. As at the date of this Prospectus, CCH is not wholly-owned, directly or indirectly, by any person but has twosignificant shareholders as aforesaid.

Ordinary Shareholders will not have different voting rightsin general meetings of the Company.

With effect on and from settlement of the Share ExchangeOffer, the existing shareholders’ agreement entered intobetween the TCCC Entities and Kar-Tess Holding inrelation to CCH (the ‘‘CCH Shareholders’ Agreement’’) willterminate and will not be renewed in relation to theCompany. Further, TCCC, the TCCC Entities and Kar-TessHolding have informed the Company that they do notconsider that they are acting in concert and that noagreement or understanding (formal or informal) existsbetween TCCC or any of the TCCC Entities on the onehand, and Kar-Tess Holding, on the other hand, in relationto the future governance or control of the Company.

Accordingly, with effect on and from settlement of theShare Exchange Offer, and in contrast to the position inrelation to CCH, there will be no formal or informal

6

Section B—Issuer

Element Disclosure requirement Disclosure

agreement or understanding between the TCCC Entitiesand Kar-Tess Holding to exercise the votes attaching to theirOrdinary Shares of the Company in relation to any matter ina pre-arranged manner and there will be no obligation onthe TCCC Entities and Kar-Tess Holding to consult witheach other on how they propose to vote in relation to anymatter considered by the Board or the shareholders of theCompany.

With effect on and from settlement of the Share ExchangeOffer, the existing relationship agreement entered intobetween the TCCC Entities, the Kar-Tess Group (of whichKar-Tess Holding is the only member holding shares inCCH) and CCH (the ‘‘CCH Relationship Agreement’’) willalso terminate and CCH has agreed to the termination ofthe CCH Relationship Agreement. The CCH RelationshipAgreement will not be renewed in relation to the Company.

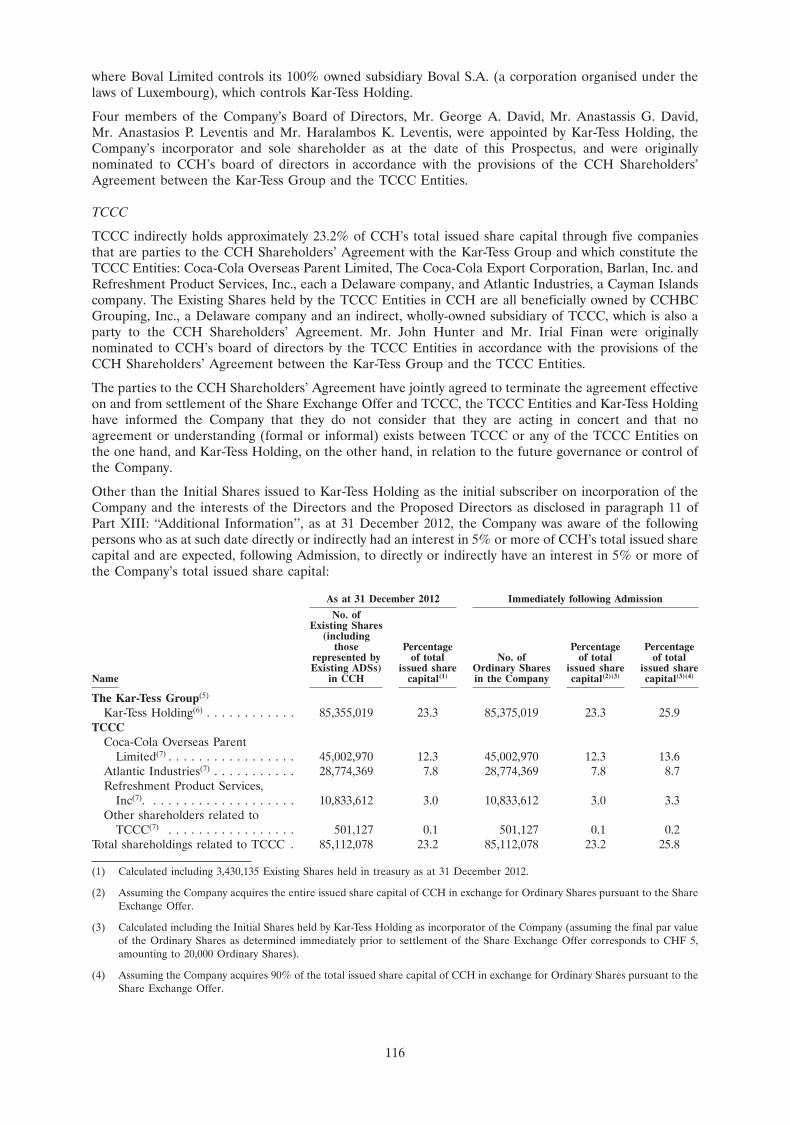

Other than the 1,000,000 fully paid-up ordinary shares ofCHF 0.10 (the ‘‘Initial Shares’’) issued to Kar-Tess Holdingas the initial subscriber on incorporation of the Company, asat 31 December 2012, the Company was aware of thefollowing persons who as at such date directly or indirectlyhad an interest in 5% or more of CCH’s total issued sharecapital and are expected, following Admission, to directly orindirectly have an interest in 5% or more of the Company’stotal issued share capital.

As at 31 December 2012 Immediately following Admission

No. of Existing Percentage Percentage PercentageShares (including of total of total of totalthose represented issued No. of Ordinary issued issuedby Existing ADSs) share Shares in the share share

Name in CCH capital(1) Company capital(2)(3) capital(3)(4)

The Kar-Tess Group(5)

Kar-Tess Holding(6) . . . . . . 85,355,019 23.3 85,375,019 23.3 25.9

TCCCCoca-Cola Overseas ParentLimited(7) . . . . . . . . . . . . 45,002,970 12.3 45,002,970 12.3 13.6Atlantic Industries(7) . . . . . 28,774,369 7.8 28,774,369 7.8 8.7Refreshment ProductServices, Inc(7). . . . . . . . . 10,833,612 3.0 10,833,612 3.0 3.3Other shareholders relatedto TCCC(7) . . . . . . . . . . . 501,127 0.1 501,127 0.1 0.2

Total shareholdings related toTCCC . . . . . . . . . . . . . . . . 85,112,078 23.2 85,112,078 23.2 25.8

(1) Calculated including 3,430,135 Existing Shares held in treasury as at 31 December 2012.

(2) Assuming the Company acquires the entire issued share capital of CCH in exchange for Ordinary Sharespursuant to the Share Exchange Offer.

(3) Calculated including the Initial Shares held by Kar-Tess Holding as incorporator of the Company(assuming the final par value of the Ordinary Shares as determined immediately prior to settlement of theShare Exchange Offer corresponds to CHF 5, amounting to 20,000 Ordinary Shares).

(4) Assuming the Company acquires 90% of the total issued share capital of CCH in exchange for OrdinaryShares pursuant to the Share Exchange Offer.

7

Section B—Issuer

Element Disclosure requirement Disclosure

(5) On 23 September 2008, Kar-Tess Holding informed CCH that on 19 September 2008 it acquired22,303,875 of CCH’s share capital from its parent, Boval S.A., in an intra-group transaction. On6 December 2010, Kar-Tess Holding transferred 22,453,254 of CCH’s shares and voting rights bytransferring nine of its 100% owned subsidiaries to entities and individuals who were either ultimatebeneficial owners of Kar-Tess Holding or have been nominated by them. None of these entities andindividuals owns individually more than 2% of CCH’s outstanding shares and voting rights.

(6) Truad Verwaltungs AG, in its capacity as trustee of a private discretionary trust established for the primarybenefit of present and future members of the family of the late Anastasios George Leventis, holds 100% ofthe share capital of Torval Investment Corp., whose 100% owned subsidiary Lavonos Limited holds 100%of the share capital of Boval Limited as nominee for Torval Investment Corp., where Boval Limitedcontrols its 100% owned subsidiary Boval S.A., which controls Kar-Tess Holding, which holds 85,355,019Existing Shares (including those represented by Existing ADSs) in CCH.

(7) These shares are all beneficially owned by CCHBC Grouping, Inc., a Delaware company and an indirect,wholly-owned subsidiary of TCCC, which is also a party to the CCH Shareholders’ Agreement.

In relation to the holdings of directors, as at the date of thisProspectus, none of the members of CCH’s board ofdirectors beneficially owns more than 1% of CCH’s totalissued share capital and following Admission, none of themembers of the Company’s Board are expected tobeneficially own more than 1% of the Company’s totalissued share capital, in each case, except through affiliationwith Kar-Tess Holding or TCCC.

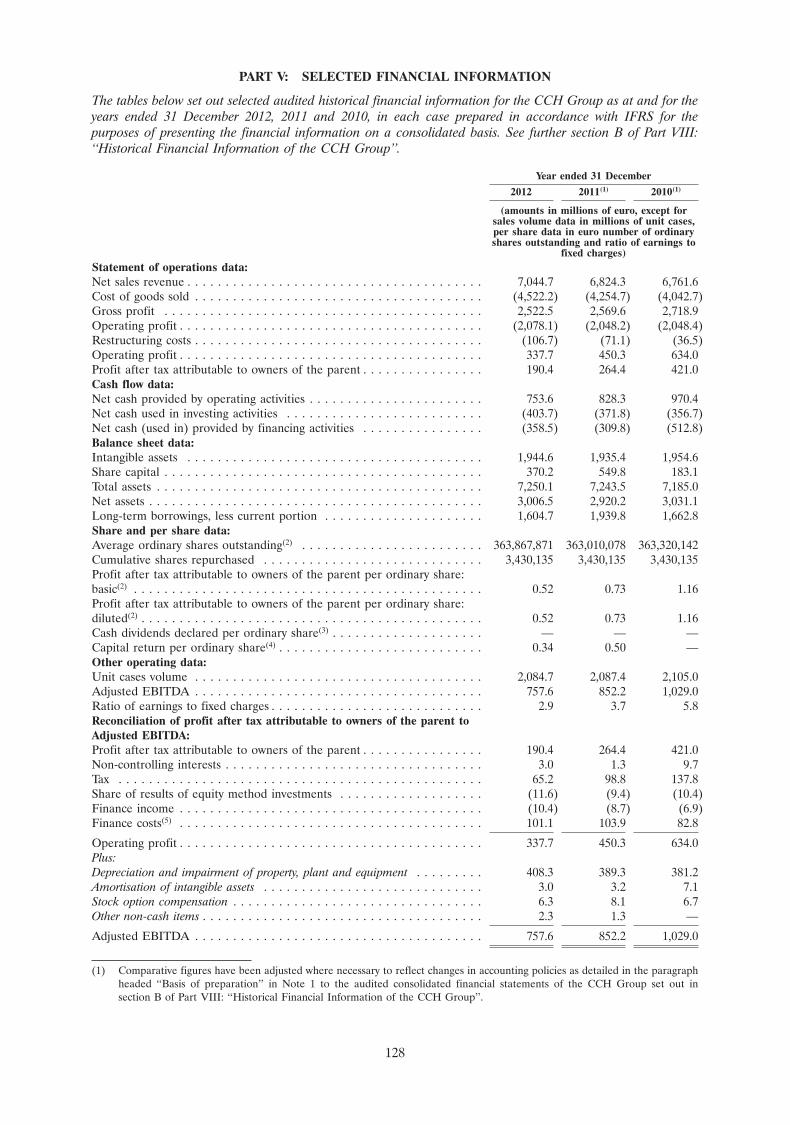

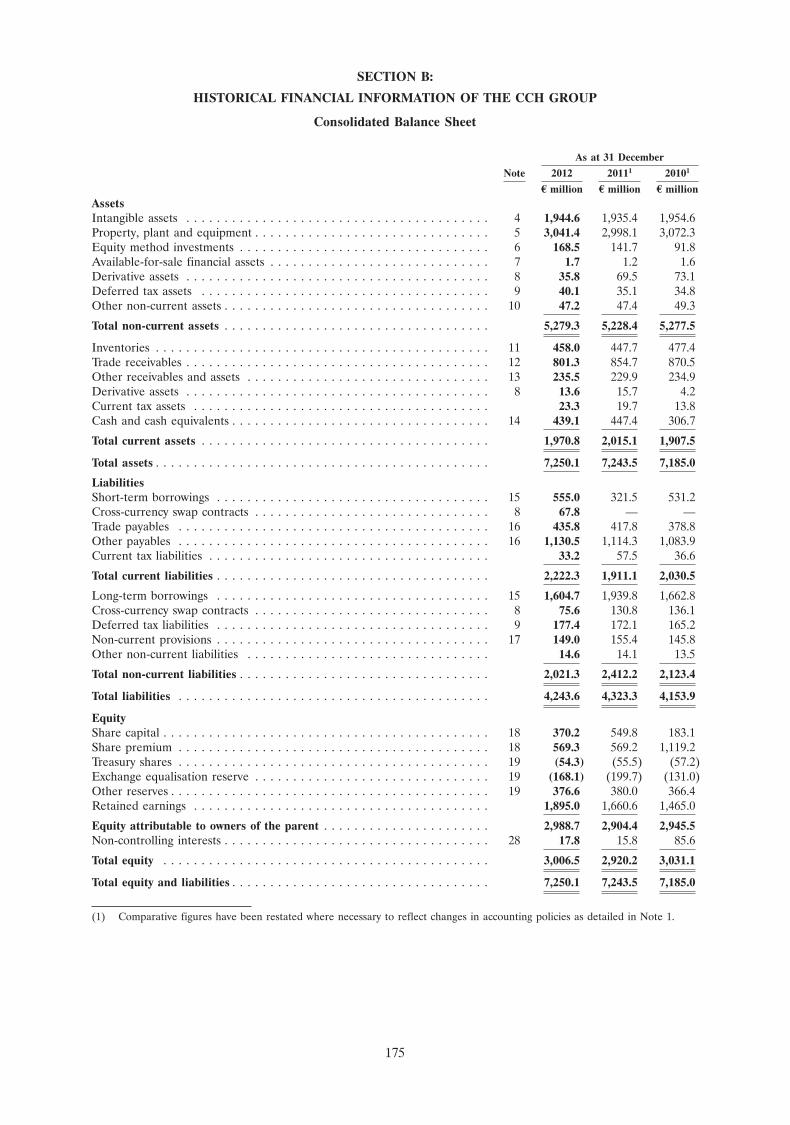

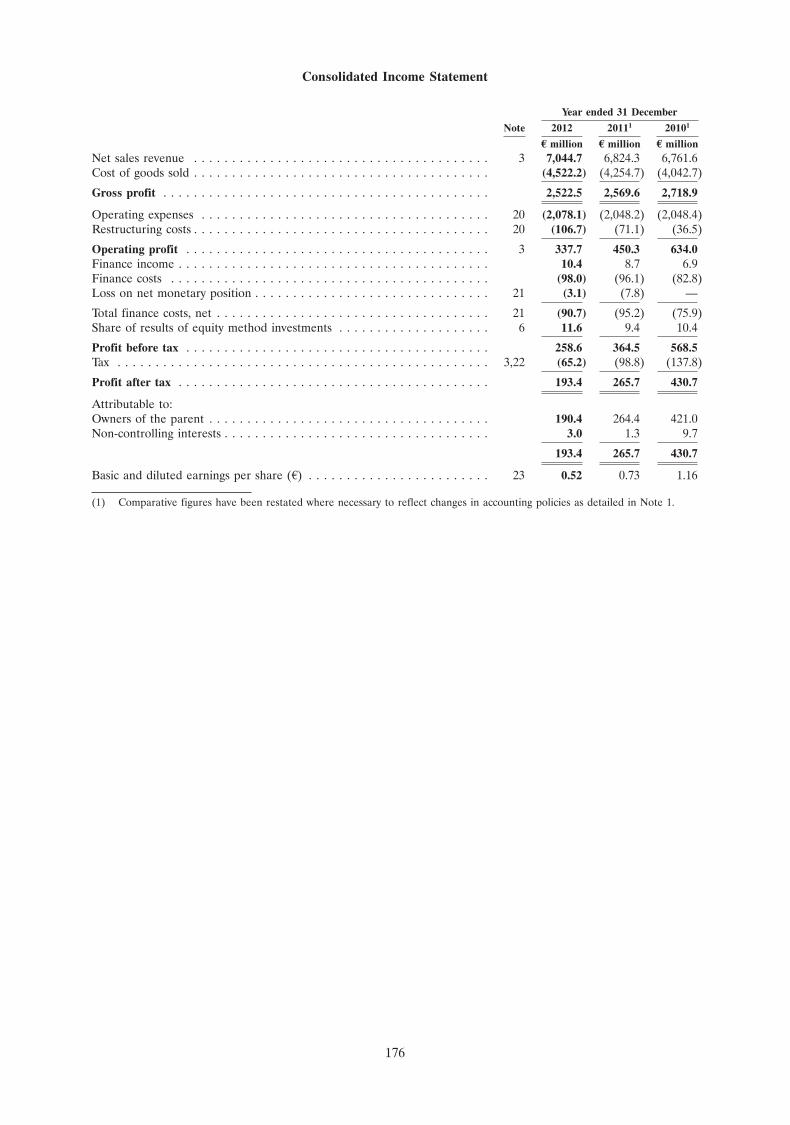

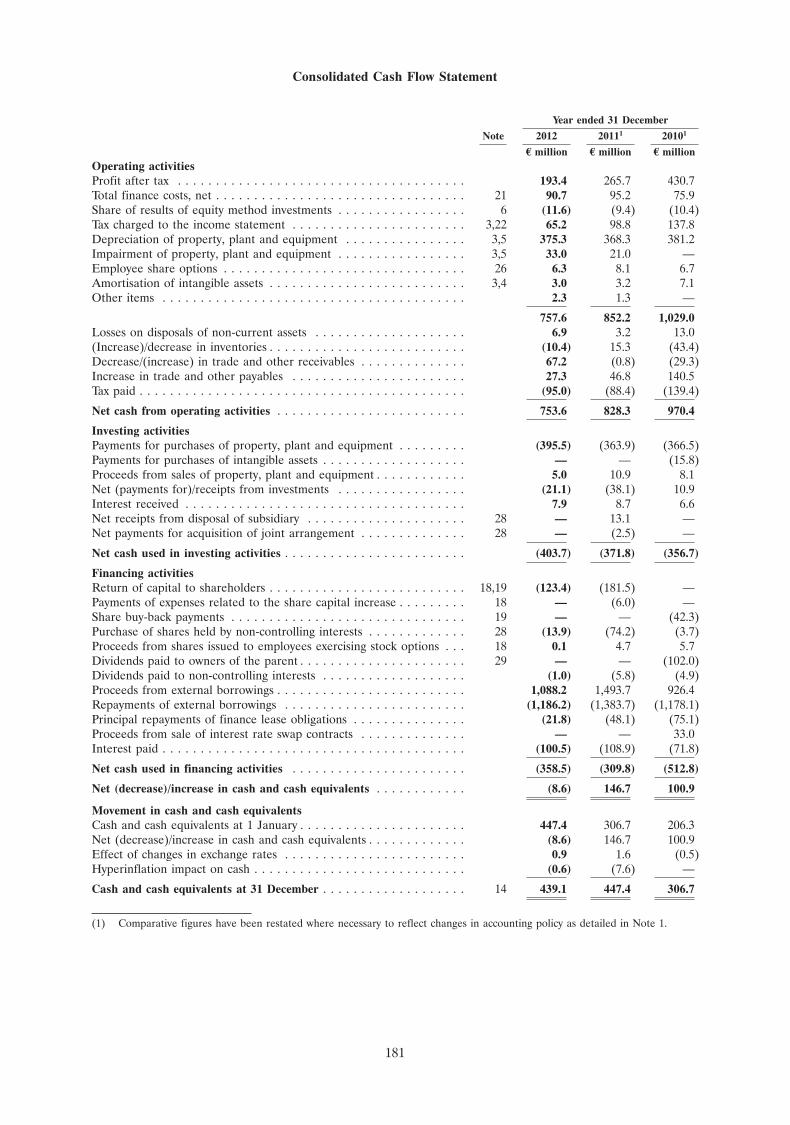

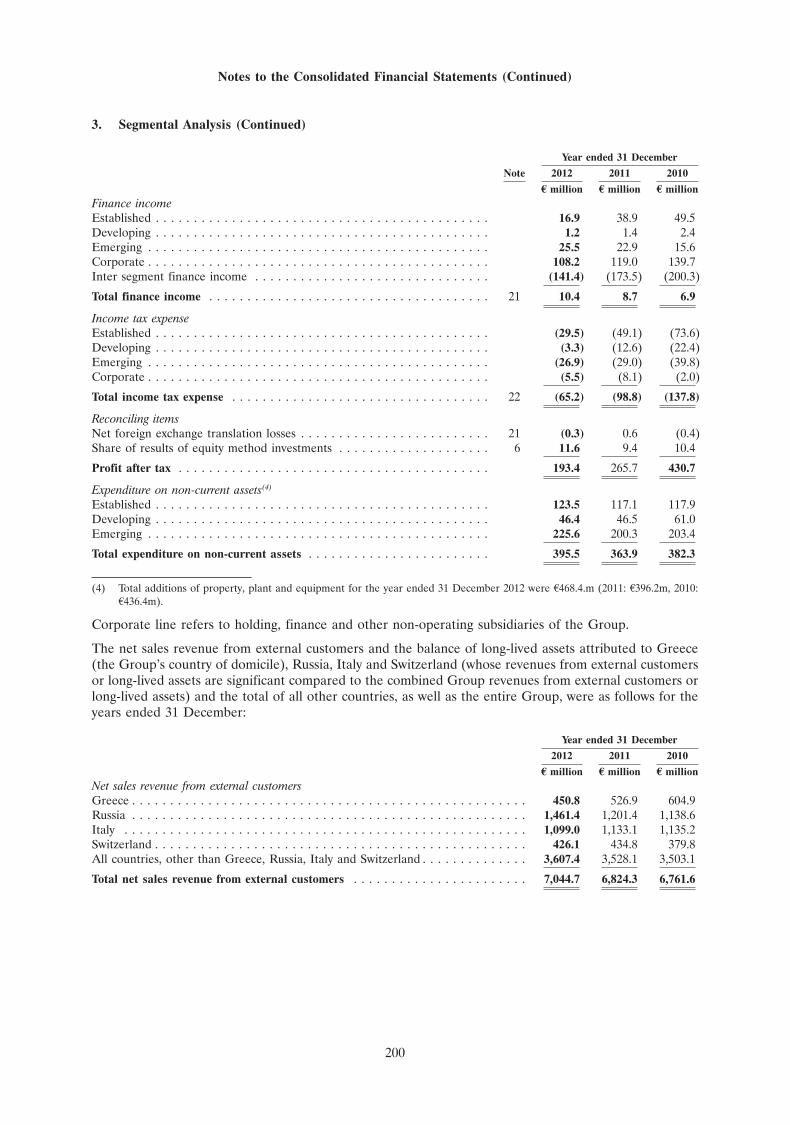

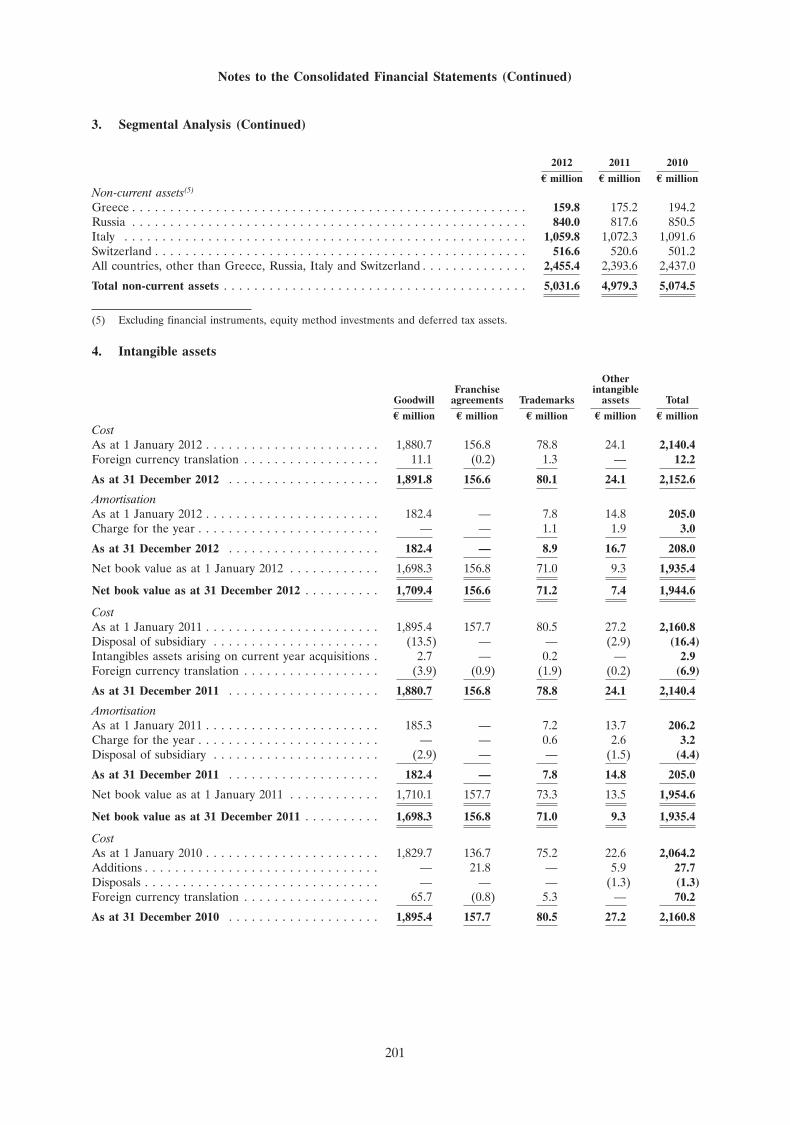

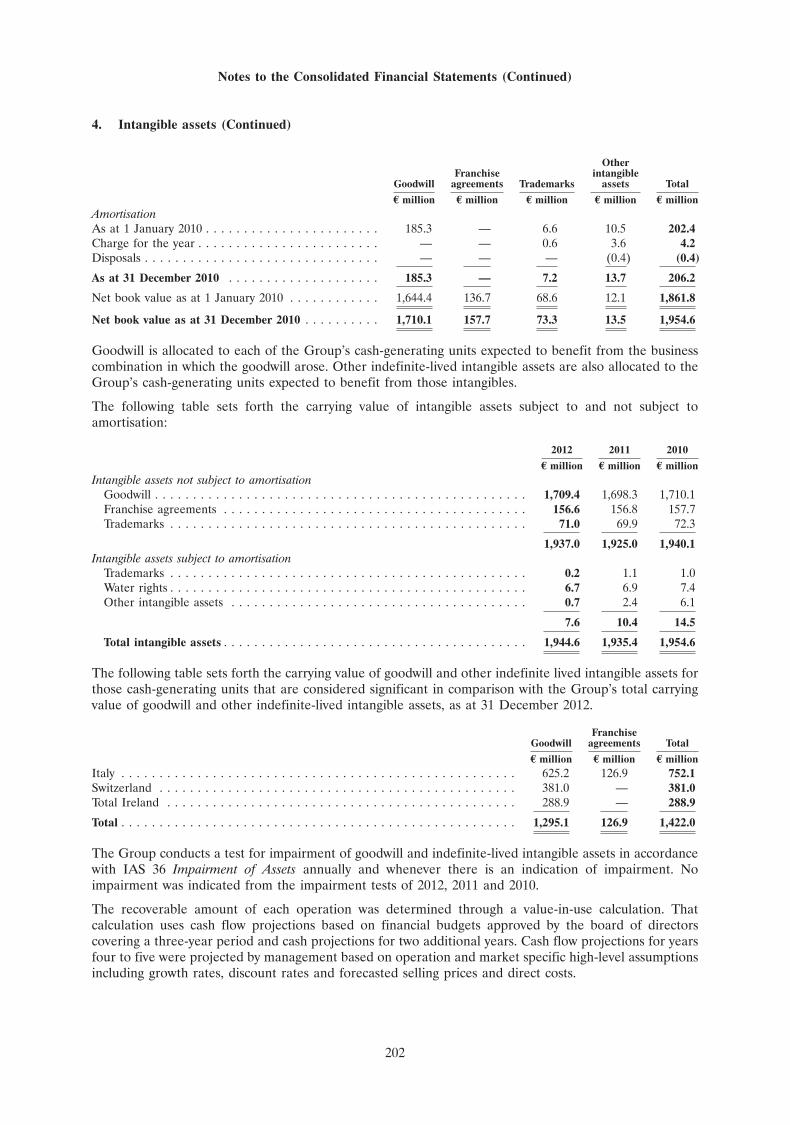

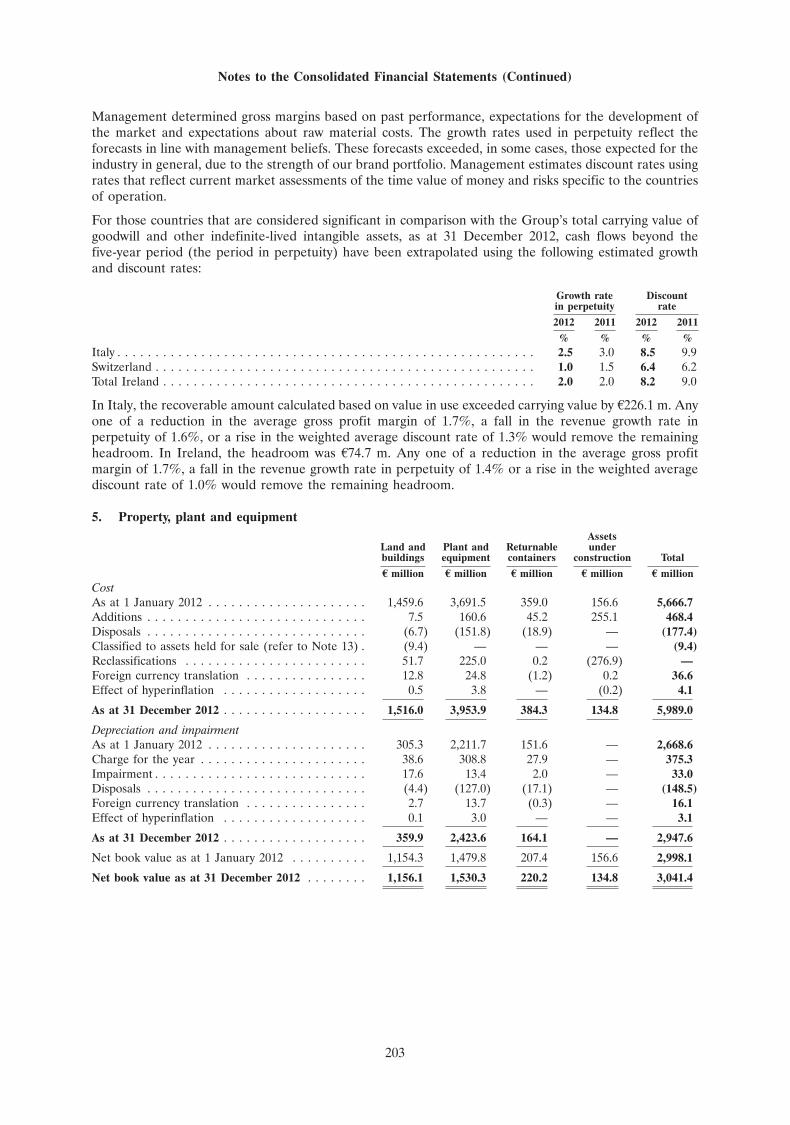

B.7 Key financial information Selected historical financial information relating to theCCH Group which summarises the financial condition ofthe CCH Group for the three financial years ended31 December 2012 is set out in the following table:

Year ended 31 December

2012 2011(1) 2010(2)

(amounts in millions of euro, except forsales volume data in millions of unit

cases, per share data in euro, number ofordinary shares outstanding and ratio of

earningsto fixed charges)

Statement of operations data:Net sales revenue . . . . . . . . . . . . . . . . . . . . . . . . . 7,044.7 6,824.3 6,761.6Cost of goods sold . . . . . . . . . . . . . . . . . . . . . . . . (4,522.2) (4,254.7) (4,042.7)Gross profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,522.5 2,569.6 2,718.9Operating expenses . . . . . . . . . . . . . . . . . . . . . . . . (2,078.1) (2,048.2) (2,048.4)Restructuring costs . . . . . . . . . . . . . . . . . . . . . . . . (106.7) (71.1) (36.5)Operating profit . . . . . . . . . . . . . . . . . . . . . . . . . . 337.7 450.3 634.0Profit after tax attributable to owners of the parent . . 190.4 264.4 421.0Cash flow data:Net cash provided by operating activities . . . . . . . . . 753.6 828.3 970.4Net cash used in investing activities . . . . . . . . . . . . . (403.7) (371.8) (356.7)Net cash (used in) provided by financing activities . . . (358.5) (309.8) (512.8)Balance sheet data: . . . . . . . . . . . . . . . . . . . . . . .Intangible assets . . . . . . . . . . . . . . . . . . . . . . . . . . 1,944.6 1,935.4 1,954.6Share capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . 370.2 549.8 183.1Total assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,250.1 7,243.5 7,185.0Net assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,006.5 2,920.2 3,031.1Long-term borrowings, less current portion . . . . . . . 1,604.7 1,939.8 1,662.8

8

Section B—Issuer

Element Disclosure requirement Disclosure

Year ended 31 December

2012 2011(1) 2010(2)

(amounts in millions of euro, except forsales volume data in millions of unit

cases, per share data in euro, number ofordinary shares outstanding and ratio of

earningsto fixed charges)

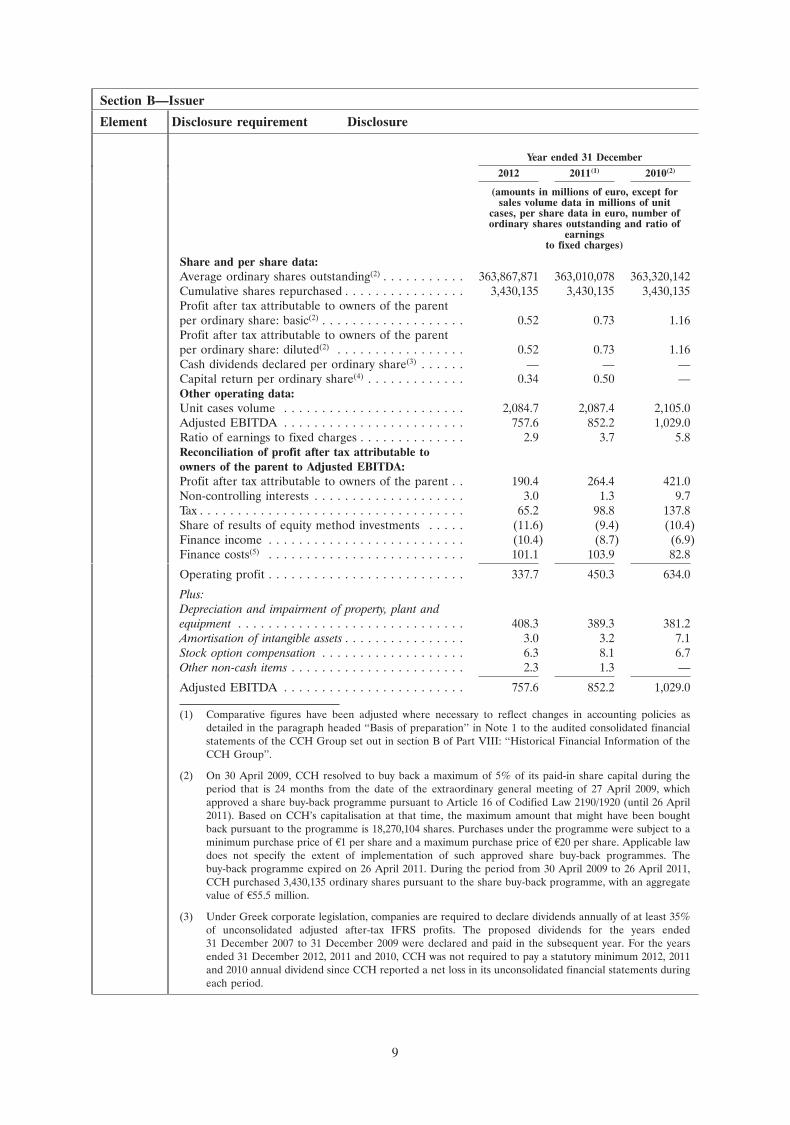

Share and per share data:Average ordinary shares outstanding(2) . . . . . . . . . . . 363,867,871 363,010,078 363,320,142Cumulative shares repurchased . . . . . . . . . . . . . . . . 3,430,135 3,430,135 3,430,135Profit after tax attributable to owners of the parentper ordinary share: basic(2) . . . . . . . . . . . . . . . . . . . 0.52 0.73 1.16Profit after tax attributable to owners of the parentper ordinary share: diluted(2) . . . . . . . . . . . . . . . . . 0.52 0.73 1.16Cash dividends declared per ordinary share(3) . . . . . . — — —Capital return per ordinary share(4) . . . . . . . . . . . . . 0.34 0.50 —Other operating data:Unit cases volume . . . . . . . . . . . . . . . . . . . . . . . . 2,084.7 2,087.4 2,105.0Adjusted EBITDA . . . . . . . . . . . . . . . . . . . . . . . . 757.6 852.2 1,029.0Ratio of earnings to fixed charges . . . . . . . . . . . . . . 2.9 3.7 5.8Reconciliation of profit after tax attributable toowners of the parent to Adjusted EBITDA:Profit after tax attributable to owners of the parent . . 190.4 264.4 421.0Non-controlling interests . . . . . . . . . . . . . . . . . . . . 3.0 1.3 9.7Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65.2 98.8 137.8Share of results of equity method investments . . . . . (11.6) (9.4) (10.4)Finance income . . . . . . . . . . . . . . . . . . . . . . . . . . (10.4) (8.7) (6.9)Finance costs(5) . . . . . . . . . . . . . . . . . . . . . . . . . . 101.1 103.9 82.8

Operating profit . . . . . . . . . . . . . . . . . . . . . . . . . . 337.7 450.3 634.0

Plus:Depreciation and impairment of property, plant andequipment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 408.3 389.3 381.2Amortisation of intangible assets . . . . . . . . . . . . . . . . 3.0 3.2 7.1Stock option compensation . . . . . . . . . . . . . . . . . . . 6.3 8.1 6.7Other non-cash items . . . . . . . . . . . . . . . . . . . . . . . 2.3 1.3 —

Adjusted EBITDA . . . . . . . . . . . . . . . . . . . . . . . . 757.6 852.2 1,029.0

(1) Comparative figures have been adjusted where necessary to reflect changes in accounting policies asdetailed in the paragraph headed ‘‘Basis of preparation’’ in Note 1 to the audited consolidated financialstatements of the CCH Group set out in section B of Part VIII: ‘‘Historical Financial Information of theCCH Group’’.

(2) On 30 April 2009, CCH resolved to buy back a maximum of 5% of its paid-in share capital during theperiod that is 24 months from the date of the extraordinary general meeting of 27 April 2009, whichapproved a share buy-back programme pursuant to Article 16 of Codified Law 2190/1920 (until 26 April2011). Based on CCH’s capitalisation at that time, the maximum amount that might have been boughtback pursuant to the programme is 18,270,104 shares. Purchases under the programme were subject to aminimum purchase price of A1 per share and a maximum purchase price of A20 per share. Applicable lawdoes not specify the extent of implementation of such approved share buy-back programmes. Thebuy-back programme expired on 26 April 2011. During the period from 30 April 2009 to 26 April 2011,CCH purchased 3,430,135 ordinary shares pursuant to the share buy-back programme, with an aggregatevalue of A55.5 million.

(3) Under Greek corporate legislation, companies are required to declare dividends annually of at least 35%of unconsolidated adjusted after-tax IFRS profits. The proposed dividends for the years ended31 December 2007 to 31 December 2009 were declared and paid in the subsequent year. For the yearsended 31 December 2012, 2011 and 2010, CCH was not required to pay a statutory minimum 2012, 2011and 2010 annual dividend since CCH reported a net loss in its unconsolidated financial statements duringeach period.

9

Section B—Issuer

Element Disclosure requirement Disclosure

(4) On 6 May 2011, CCH’s shareholders at the annual general meeting of shareholders resolved to reorganiseits share capital. CCH’s share capital increased by an amount equal to A549.7 million. The increase wasperformed by capitalising share premium reserves and increasing the nominal value of each share fromA0.5 to A2. CCH’s share capital was subsequently decreased by an amount equal to A183.2 million bydecreasing the nominal value of each share from A2 to A1.5, and distributing such A0.5 per share differenceto the shareholders in cash.

On 25 June 2012, the annual general meeting of CCH’s shareholders resolved to decrease CCH’s sharecapital by an amount equal to A124.6 million by decreasing the nominal value of each share from A1.50 toA1.16 per share, and distributing such A0.34 per share difference to shareholders in cash. On the same date,it was resolved to decrease CCH’s share capital by an amount equal to A55.0 million by decreasing thenominal value of each share by A0.15 per share, from A1.16 to A1.01 per share, in order to extinguishaccumulated losses reflected in the unconsolidated financial statements of the parent company, in an equalamount.

(5) Finance costs for the years ended 31 December 2012 and 2011 include losses on net monetary positionamounting to A3.1 million and A7.8 million, respectively, arising from the CCH Group’s Belarusianoperation. Since the fourth quarter of 2011, Belarus has been considered a hyperinflationary economy foraccounting purposes.

On 11 October 2012, the Company entered into threefinance facilities: a A550,000,000 syndicated term loanfacility (the ‘‘Statutory Squeeze-out Facility’’), aA500,000,000 syndicated term loan refinancing facility (the‘‘Bond Refinancing Facility’’) and a A500,000,000 syndicatedrevolving credit facility (the ‘‘Revolving Credit Facility’’).The Revolving Credit Facility was subsequently cancelled on29 October 2012 at the Company’s request and the terms ofthe Statutory Squeeze-out Facility and the BondRefinancing Facility were amended on 20 February 2013.

As at the date of this Prospectus, A25 million has beendrawn down under the Statutory Squeeze-out Facility tofund certain expenses of the Share Exchange Offer and noamounts have been drawn down under the BondRefinancing Facility.

On 28 December 2012, the Company received an equitycontribution from Kar-Tess Holding of A1.5 million.

Other than as set out above, there has been no significantchange in the financial or trading position of the Companysince 19 September 2012, being the date of its incorporation.

There has been no significant change in the financial ortrading position of the CCH Group since 31 December2012, being the date to which the historical financialinformation of the CCH Group has been prepared.

B.8 Key pro forma financial No selected key pro forma financial information has beeninformation included in this Prospectus. However, following completion

of the Share Exchange Offer the Company expects to own atleast 90% of the CCH Group. The consolidated financialstatements of the new CCH Group will be presented usingthe values from the consolidated financial statements of thecurrent CCH Group and will be prepared in accordancewith IFRS, as issued by the IASB. The reporting currencywill continue to be the euro.

10

Section B—Issuer

Element Disclosure requirement Disclosure

If the Share Exchange Offer had taken place at the date ofthe CCH Group’s latest balance sheet, being 31 December2012, the total assets and liabilities of the CCH Groupwould have been combined with those of the Company.

Net assets of the new CCH Group would have been reducedby a cash amount equal to the costs and expenses of theShare Exchange Offer. Any cash consideration paid toExisting Securityholders funded by the StatutorySqueeze-out Facility would have had the effect of increasingthe CCH Group’s indebtedness and reducing net assets bythe amount of such consideration.

B.9 Profit forecast Not applicable. No profit forecast or estimate is made.

B.10 Description of the nature Not applicable. The audit report on the historical financialof any qualifications in the information of the CCH Group contained within thisaudit report on the Prospectus has not been qualified.historical financialinformation

B.11 Working capital Not applicable. In the opinion of the Company, the workingcapital available to the New CCH Group is sufficient for itspresent requirements, that is, for the next 12 monthsfollowing the date of this Prospectus.

Section C—Securities

Element Disclosure requirement Disclosure

C.1 Type and class of securities The securities offered under the Share Exchange Offer andto be admitted to trading on the London Stock Exchange’smain market for listed securities are ordinary shares inregistered form with an initial par value of CHF 0.10 each inthe share capital of the Company and a final par value to bedetermined immediately prior to settlement of the ShareExchange Offer. The Ordinary Shares will trade under thesymbol ‘‘CCH’’. The ISIN of the Ordinary Shares isCH019 825 1305 and the SEDOL is B9895B7. Applicationfor the listing of New ADSs will also be made to the NYSEand, if approved, such New ADSs will trade under thesymbol ‘‘CCH’’. The Company has applied for a secondarylisting of the Ordinary Shares on the Athens Exchange,subject to the receipt of necessary approvals. If such AthensExchange listing is approved, the Ordinary Shares will tradeunder the symbol ‘‘EEEK’’.

C.2 Currency of the securities Swiss Francs.issue

C.3 Number and par value of The Company will issue up to a maximum of 366,553,507securities to be issued Ordinary Shares in aggregate under the Share Exchange

Offer. There is a minimum acceptance condition of 90% ofthe total issued share capital of CCH. If the Company hasreceived valid acceptances from Existing Securityholdersrepresenting only 90% of CCH’s total issued share capital,the Company will issue a minimum of 329,898,157 OrdinaryShares in aggregate under the Share Exchange Offer.

11

Section C—Securities

Element Disclosure requirement Disclosure

As at the date of this Prospectus, the Ordinary Shares havea par value of CHF 0.10. The final par value will bedetermined immediately prior to settlement of the ShareExchange Offer and will not exceed 30% of the issue priceof the Ordinary Shares pursuant to the Share ExchangeOffer.

C.4 Description of the rights The Ordinary Shares rank equally in all respects including inattaching to the securities relation to voting rights and the right to receive dividends or

other distributions declared, paid or made.

Each registered holder of Ordinary Shares is entitled to:

• vote in person or by proxy at every general meeting ofthe Ordinary Shareholders of the Company, subject tocompliance with registration and the notificationrequirements for beneficial ownership;

• receive dividends if, as and when declared on theOrdinary Shares of the Company; and

• participate in any distribution of the remainingproperty and assets of the Company upon thedissolution and liquidation of the Company.

Although currently only the Ordinary Shares are in issuance,the Company may by amendment of the Articles and inaccordance with Swiss law:

• create special rights or restrictions attaching to theshares of any class or series, whether or not any or all ofthose shares have been issued; and

• vary or delete any special rights or restrictions attachedto the shares of any class or series, whether or not anyor all of those shares have been issued.

Securities issued by non-UK companies, such as theCompany, cannot be held or transferred electronically in theCREST system. The Company will, prior to Admission,establish arrangements for the issue of CREST DepositaryInterests (‘‘CDIs’’) to enable investors to settle the OrdinaryShares under the CREST system.

C.5 Restrictions on the free Not applicable.transferability of thesecurities

C.6 Admission Application will be made to the UK Listing Authority forthe Ordinary Shares to be admitted to the premium listingsegment of the Official List and to the London StockExchange for the Ordinary Shares to be admitted to tradingon the London Stock Exchange’s main market for listedsecurities. It is expected that such admissions will becomeeffective, and that dealings in the Ordinary Shares willcommence, at 8.00 a.m. on or around 29 April 2013. CCHintends to cancel the listing of its Existing Shares on thestandard listing segment of the Official List, in accordancewith the Listing Rules and the Admission and DisclosureStandards and will submit an unconditional cancellationrequest to the FSA and the London Stock Exchange.

12

Section C—Securities

Element Disclosure requirement Disclosure

CCH will seek to delist the Existing Shares from thestandard listing segment of the Official List uponAdmission, irrespective of the number of Existing Securitiesacquired by the Company in the Share Exchange Offer.

The Company intends to request that the FSA provides acertificate of approval and a copy of this Prospectus to therelevant competent authorities in Greece, in connectionwith the admission to trading of the Company’s OrdinaryShares on the Athens Exchange and the offering ofOrdinary Shares to the public in connection with the ShareExchange Offer and in Austria, in connection with theoffering of Ordinary Shares to the public in connection withthe Share Exchange Offer.

The Company has applied for a secondary listing of theOrdinary Shares on the Athens Exchange, subject to thereceipt of necessary approvals. The Company will also makean application for listing of the New ADSs on the NYSE.

C.7 Dividends and Dividend The Company intends to adopt a dividend and other cashpolicy distribution policy which will take into account, and depend

upon, the profitability of the business and underlying growthin earnings of the CCH Group, as well as its ongoing capitalrequirements and cash flows, the availability of funds andother relevant factors.

Since its incorporation, the Company has not declared orpaid any dividends or other cash distributions. If the ShareExchange Offer is completed, the Company does not expectthat any dividends will be paid to shareholders of CCH orthe Company until after completion of the Greek StatutorySqueeze-out. Shortly thereafter, the Company intends tohold an extraordinary general meeting of its OrdinaryShareholders in order to declare a dividend. While suchdividend will relate to the CCH Group’s financial yearended 31 December 2012, it will be technically paid out ofthe Company’s capital contribution reserves arising from thesettlement of the Share Exchange Offer, as reflected in theaudited unconsolidated interim financial statements of theCompany prepared for the purpose of the extraordinarygeneral meeting of Ordinary Shareholders in 2013.

Dividends or other cash distributions are generally expectedto be paid in euro, although CDI Holders are expected to beable to elect through the CREST system to receive theirdividend payments or other cash distributions in poundssterling and for holders of New ADSs, dividend payments orother cash distributions will be converted into US dollars inaccordance with the terms of the ADR DepositaryAgreement.

13

Section D—Risks

Element Disclosure requirement Disclosure

D.1 Key information on the The principal risk factors relating to the Company are:risks specific to the issuer

Risks relating to the CCH Group’s relationship withor its industryTCCC and Kar-Tess Holding

• If TCCC exercises its right to terminate the bottlers’agreements with the CCH Group upon the occurrenceof certain events, or is unwilling to renew theseagreements upon expiry in 2023, the CCH Group’s netsales revenue may decline dramatically. In addition, ifTCCC is unwilling to renew the bottlers’ agreementswith the CCH Group on terms at least as favourable tothe CCH Group as the current terms, the CCH Group’snet sales revenue could also be adversely affected.

• TCCC could exercise its rights under the bottlers’agreements with the CCH Group to determineconcentrate prices and to approve only certain of theCCH Group’s suppliers, in a manner that would make itdifficult for the CCH Group to achieve its financial goals.

• If the Company does not acquire all of the ExistingShares in exchange for Ordinary Shares in the ShareExchange Offer, and subsequently acquires ExistingShares in any Greek Statutory Squeeze-out and/orGreek Statutory Sell-out in whole or in part for cashconsideration, the aggregate percentage of the OrdinaryShares beneficially owned by TCCC and Kar-TessHolding will be even greater than the percentage ofCCH’s outstanding share capital that Kar-Tess Holdingand TCCC respectively hold prior to the ShareExchange Offer. Accordingly, the influence of Kar-TessHolding and the TCCC Entities in relation to corporateactions to be approved by shareholders of the Companymay increase and their respective interests may differfrom each other and from those of other OrdinaryShareholders. In addition, save for the appointment ofMrs. Susan Kilsby, with effect upon or immediatelyfollowing settlement of the Share Exchange Offer, thecomposition of the Company’s Board of Directors willbe consistent with CCH’s board of directors. For so longas the directors originally appointed by Kar-Tess Holdingand the TCCC Entities to CCH’s board of directorspursuant to the CCH Shareholders’ Agreement remainon the Board of Directors of the Company, each ofKar-Tess Holding and the TCCC Entities are expected tobe able to exercise influence over the conduct of theCCH Group’s business through their respectiverepresentation on the Board of Directors.

Risks relating to the non-alcoholic ready-to-drinkbeverages industry

• The CCH Group’s revenues and profitability aresubstantially dependent upon sales of its core Sparklingbeverages business. Weaker consumer demand forSparkling beverages could harm the CCH Group’srevenues and profitability.

14

Section D—Risks

Element Disclosure requirement Disclosure

Risks relating to Emerging and Developing Countries

• A substantial proportion of the CCH Group’soperations is carried out in the Emerging andDeveloping Countries. Operations in these markets aresubject to various risks, including potential political andeconomic uncertainty, application of exchange controls,reliance on foreign investment, nationalisation orexpropriation, crime and lack of law enforcement,political insurrection, external interference, currencyfluctuations, changes in government policy and risk ofloss due to fraud and criminal activity, which couldaffect the CCH Group’s results by causing interruptionsto operations, by increasing the cost of operating inthose countries or by limiting the ability to repatriateprofits from those countries.

Risks relating to competition

• The CCH Group’s business is subject to thecompetition laws of the countries in which it operatesand, with respect to the CCH Group’s activitiesaffecting the EU, is also subject to EU competition law.Any change in the competition laws to which the CCHGroup activities are subject or any enforcement actiontaken by competition authorities could adversely affectthe CCH Group’s operating results.

• The increasing concentration of retailers andindependent wholesalers, on which the CCH Groupdepends to distribute its products in certain countries,could result in increasing bargaining power of suchretailers and independent wholesalers, which they coulduse in a way that could lower the CCH Group’sprofitability and harm its ability to compete.

Risks relating to prevailing economic conditions

• The Greek government debt crisis and the associatedimpact on the economic and fiscal prospects of Greeceand the other EU countries in which the CCH Groupoperates have negatively affected the disposableincome and spending of consumers and have resulted inincreased taxation on the CCH Group’s business. TheCompany has secured the funding required to refinancedebt becoming due within the 18-month periodimmediately following the date of this Prospectus andthe negative trends in the Greek economy would notimpact the availability of existing facilities, whichinclude the Statutory Squeeze-out Facility and theBond Refinancing Facility. However, such negativetrends could have severe adverse consequences for theCCH Group, including a negative impact on theCompany’s cost of funds, its ability to raise additionalfunds (should the Company so wish to undertake), itscredit rating and the ability of CCH as the Company’sdirect subsidiary to distribute funds to the Company.

15

Section D—Risks

Element Disclosure requirement Disclosure

• The global financial and credit crisis and the eurozonesovereign debt crisis may affect the CCH Group’sfinancial results and ability to obtain credit in thefuture. The CCH Group has in place sufficientcommitted, unused credit facilities to meet its fundingrequirements for the foreseeable future and thefinancial crisis would not impact on the availability ofexisting facilities. However, the continuing volatility ofthe capital and credit markets may result in the CCHGroup facing increased interest rates in the longer termand incurring other costs associated with any futuredebt financings (should the Company so wish toundertake). If the global financial crisis results indecreases in yield on, or a fall in the value of,investments held by CCH Group’s funded pensionplans, the CCH Group may have to increase its fundinglevels of such pension plans from its current fundingrequirements, which could adversely affect the CCHGroup’s results of operations and financial condition.

• Increased taxation on the CCH Group’s business mayreduce the CCH Group’s profitability. The CCH Groupis subject to multiple taxes across each of thejurisdictions in which it operates. The severe fiscalcrises currently impacting many of the CCH Group’scountries have resulted in increased taxation on theCCH Group’s business.

Risks relating to the CCH Group’s business

• The CCH Group relies on the reputation of thebranded products it produces and distributes (referredto as the ‘‘CCH Group’s brands’’). An event thatmaterially damages the reputation of the CCH Group’sbrands could have an adverse effect on the value ofthese brands and subsequent revenues from thosebrands or businesses.

• Demand for the CCH Group’s products is affected byweather conditions and tourist activity in the Territoriesin which the CCH Group operates. Adverse weatherconditions and reduced tourist activity could adverselyaffect demand for the CCH Group’s products, reducesales volumes and in turn adversely affect the result ofoperations.

• Price increases in, and shortages of, raw materials thatthe CCH Group uses to manufacture its products (inparticular, water and sugar) and packaging materialsmay affect the price and availability of ingredients thatthe CCH Group uses to manufacture its products andpackaging and could materially and adversely affect theCCH Group’s results of operations.

• Fluctuations in exchange rates between the euro andother currencies in which the CCH Group receives aportion of its income may adversely affect the results ofthe CCH Group’s operations and financial condition.

16

Section D—Risks

Element Disclosure requirement Disclosure

• The CCH Group is exposed to the impact of exchangecontrols in Nigeria, Ukraine, Belarus and Moldova,which may adversely affect its profitability or its abilityto repatriate profits. Exchange controls may also have anegative impact on the capital markets of suchcountries and the ability of companies in thoseTerritories to make dividends, distributions or loans tothe Company.

• The CCH Group’s operations are subject to extensiveregulation, including resource recovery, environmentaland health and safety standards, and are subject tomultiple taxes across the jurisdictions in which itoperates. More restrictive regulations or higher taxescould lead to increasing prices, which in turn mayadversely affect the sale and consumption of the CCHGroup’s products and reduce its revenues andprofitability.

D.3 Key information on the The principal risk factors relating to the Ordinary Sharesrisks specific to the are:securities

• Although the Company has applied for admission tothe premium listing segment of the Official List, therecan be no guarantee that the Company will be able tomaintain a premium listing if changes to the ListingRules proposed in the FSA’s consultation paperCP12/25 come into effect and the UK Listing Authoritydetermines at that time, or in the future, that suchchanges apply in respect of the Company and its twomajor shareholders, unless the Company and/or its twomajor shareholders comply with such requirements.

• Sales of substantial amounts of the Ordinary Shares byKar-Tess Holding or the TCCC Entities, or theperception that such sales could occur, could adverselyaffect the market value of the Company’s OrdinaryShares.

• If the Company is unable to make a distributionthrough a reduction in par value or out of QualifyingReserves, the Company may not be able to makedistributions without subjecting the OrdinaryShareholders to Swiss Withholding Tax.

• There is no guarantee that the Ordinary Shares will beincluded in the FTSE UK Index Series and failure toachieve such inclusion may reduce demand for theshares.

• Although the Company has received confirmationsfrom TCCC and certain other Existing Shareholdersthat they support the Share Exchange Offer and intendto tender Existing Shares in the Share Exchange Offer,and Kar-Tess Holding has stated it will tender in theShare Exchange Offer all of its Existing Shares,representing approximately 23.3% of CCH’s totalissued share capital, on the same terms and conditions

17

Section D—Risks

Element Disclosure requirement Disclosure

as the other Existing Shareholders, there can be noassurance that Existing Securityholders will accept theShare Exchange Offer. In addition, although theCompany expects to acquire at least 90% of the totalissued share capital of CCH as a result of the ShareExchange Offer, CCH may not be wholly-owned by theCompany as at settlement of the Share Exchange Offer,leaving minority shareholders in CCH who will beentitled to their pro rata share of any dividends made ordeclared by CCH until such time as the GreekStatutory Squeeze-out and/or Greek Statutory Sell-outare completed.

• Any indebtedness incurred by the Company in order topay cash consideration to Existing Securityholdersmaking such election in any Greek StatutorySqueeze-out or Greek Statutory Sell-out will increasethe Company’s leverage and the trading price of theOrdinary Shares and the New ADSs may decrease ifthe refinancing of the Statutory Squeeze-out Facility orthe Bond Refinancing Facility in the future is effectedby way of equity issuance.

• CDI holders will not be able to directly exercise anyvoting or other rights attaching to the Ordinary Sharesunderlying their CDIs. Instead, CDI Holders must relyon the CDI Depositary, or its custodian CRESTInternational Nominees Limited, to exercise rightsattaching to the underlying Ordinary Shares for thebenefit of the CDI Holders. Although, the Companyand Euroclear UK & Ireland will establish omnibusproxy arrangements, whereby CDI Holders andbeneficial owners of CDIs will, subject to certainconditions, give CDI Holders the right to vote directlyin respect of such CDI Holder’s or beneficial owner’sunderlying Ordinary Shares, there can be no assurancethat all such rights and entitlements will be duly andtimely passed on or exercised.

Section E—Offer

Element Disclosure requirement Disclosure

E.1 Net proceeds and costs of The Company is not offering any Ordinary Shares for cashthe offer and therefore the Company is not receiving any proceeds

from the Share Exchange Offer.

The estimated fees and expenses payable by the Company inconnection with Admission, the listing of the OrdinaryShares on the Athens Exchange, the listing of the NewADSs on the NYSE, and the Share Exchange Offer,including FSA and London Stock Exchange fees andprofessional fees and expenses amount to approximatelyA42 million (exclusive of recoverable VAT).

18

Section E—Offer

Element Disclosure requirement Disclosure

E.2A Reason for offer, use of On 10 October 2012, pursuant to Greek law, the Companyproceeds and net amount informed the HCMC and the board of directors of CCH ofof proceeds the initiation of the Share Exchange Offer and submitted to

them a draft of the Information Circular (the ‘‘InitiationDate’’). The Company has applied to the FSA for all theOrdinary Shares to be admitted to the premium listingsegment of the Official List and to the London StockExchange for such Ordinary Shares to be admitted totrading on the London Stock Exchange’s main market forlisted securities. As a result of the Share Exchange Offer, itis intended that the Company will become the new holdingcompany of the CCH Group.

The principal objectives of the Share Exchange Offer andAdmission are:

• to better reflect the international nature of the CCHGroup’s business and shareholder base;

• to enhance the liquidity for holders of the OrdinaryShares;

• to facilitate the potential inclusion of the OrdinaryShares in the FTSE UK Index Series; and

• to improve the CCH Group’s access to both theinternational equity and debt capital markets andincrease its flexibility in raising new funds to support itsoperations and future growth.

The objective of the Greek Statutory Squeeze-out that theCompany proposes to commence following completion ofthe Share Exchange Offer is to acquire all of theoutstanding shares in CCH held by minority shareholders atthe end of the Share Exchange Offer; the Greek StatutorySell-out is required by Greek law.

There is no use of proceeds and no net amount of proceedsas the Company is not offering Ordinary Shares for cash andtherefore will not be receiving any cash proceeds.

E.3 Terms and conditions of The Share Exchange Offer comprises two offers: the Greekthe offer Offer and a separate US Offer. Pursuant to the Share

Exchange Offer, the Company is offering all ExistingSecurityholders one Ordinary Share to be issued by theCompany for one Existing Share validly tendered (or, in thecase of Existing Shareholders located in the United States,one New ADS at the election of the holder) and one NewADS for one Existing ADS validly tendered by the ExistingSecurityholders.

The commencement of the Acceptance Period is expectedon or around 19 March 2013 and is expected to expire on oraround 19 April 2013.

The Share Exchange Offer has a minimum acceptancecondition of 90% of the total issued share capital. TheCompany has received confirmations from TCCC andcertain other Existing Shareholders, that they support theShare Exchange Offer and intend to tender Existing Sharesin the Share Exchange Offer. Kar-Tess Holding has alsostated it will tender in the Share Exchange Offer all of its

19

Section E—Offer

Element Disclosure requirement Disclosure

Existing Shares, representing approximately 23.3% ofCCH’s total issued share capital, on the same terms andconditions as the other Existing Shareholders. Suchconfirmations, together with the Existing Shares thatKar-Tess Holding has stated it will tender in the ShareExchange Offer, represent approximately 60% of CCH’stotal issued share capital. CCH has also informed theCompany that it intends to tender the Existing Shares that itholds in treasury in the Share Exchange Offer, representingan additional 0.9% of CCH’s total issued share capital.

The completion of the Share Exchange Offer is conditionalupon certain conditions being satisfied or, subject to thelimitations described below, waived by the Company on orprior to the end of the Acceptance Period of the ShareExchange Offer, including:

• no later than the end of the Acceptance Period, at least329,898,157 Existing Securities corresponding to atleast 90% of the total issued share capital of CCH shallhave been lawfully and validly tendered and notwithdrawn as at the end of the Acceptance Period. Thiscondition shall be deemed not to have been fulfilledand the Share Exchange Offer will cease to be in effectif the Registration Statement in respect of the US Offershall not have been declared effective by the SECbefore the commencement of the Acceptance Period;

• (a) the FSA, acting as the UK Listing Authority, andthe London Stock Exchange shall have acknowledgedto the Company or its agent (and such acknowledgmentshall not have been withdrawn) on or prior to the endof the Acceptance Period that the application foradmission of the Ordinary Shares to the premiumlisting segment of the Official List and to trading on theLondon Stock Exchange’s main market for listedsecurities has been or will be approved, provided thatsuch approval will become effective upon (i) thesubmission by the Company or its agent (in practice,the financial institution acting as sponsor for theadmission) to the FSA, acting as the UK ListingAuthority, of a shareholder statement in customaryform, evidencing satisfaction of the requirement underListing Rule 6.1.19 that a minimum percentage of theOrdinary Shares (currently generally 25%, however, theUK Listing Authority may accept a lower percentage incertain limited circumstances) will be in ‘‘public hands’’upon such admission (the ‘‘minimum free floatrequirement’’), and confirmation of the number andpar value of the Company’s Ordinary Shares to beissued pursuant to the Share Exchange Offer; (ii) theissuance of the Ordinary Shares to be issued pursuantto the Share Exchange Offer; and (iii) the issuance of adealing notice by the FSA, acting as the UK ListingAuthority; and (b) the minimum free float requirementshall have been met as at the end of the AcceptancePeriod; and

• the NYSE shall have approved the listing of the NewADSs, subject to official notice of issuance.

20

Section E—Offer

Element Disclosure requirement Disclosure

The conditions described above are for the Company’s solebenefit and may only be waived in whole or in part with theapproval of the HCMC. The Company does not have anyobligation to waive any conditions not satisfied on or priorto the expiration of the Share Exchange Offer and does notexpect to waive the Acceptance Condition or the AdmissionCondition described above. If the Company does not waive,or the HCMC does not consent to the waiver of, anunsatisfied condition, the Share Exchange Offer will lapseand all tendered Existing Securities will be returned to theholders thereof.

The Share Exchange Offer may also be revoked by theCompany, as contemplated by the Greek tender offer rules,following approval of the HCMC if there is an unforeseenchange of circumstances which is beyond the Company’scontrol and which renders continuation of the ShareExchange Offer particularly onerous.

The scope of this revocation right is not yet clearly definedunder the Greek tender offer rules. However, the Companydoes not intend to assert this revocation right with respect tothe Share Exchange Offer unless, prior to the end of theAcceptance Period, there is a material adverse change incircumstances that would be reasonably expected to deprivethe Company, CCH or the holders of Existing Shares(including Existing Shares represented by Existing ADSs)from the material expected benefits of the Share ExchangeOffer.

If, at the end of the Acceptance Period for the ShareExchange Offer, the Company has received tenders for, orotherwise holds, at least 329,898,157 Existing Shares,corresponding to at least 90% of the total issued sharecapital of CCH, holders of Existing Shares (includingExisting Shares represented by Existing ADSs) that werenot acquired in the Share Exchange Offer will be entitled tosell or exchange their Existing Shares to the Companypursuant to the Greek Statutory Sell-out at any time duringthe three calendar months after the publication of theresults of the Share Exchange Offer, and the Company willbe entitled to initiate a procedure to compulsorily acquireall Existing Shares held by any remaining minorityshareholders in the Greek Statutory Squeeze-out withinthree calendar months of the end of the Acceptance Periodof the Share Exchange Offer. In that case, the Companyintends to initiate the Greek Statutory Squeeze-out as soonas practicable after the announcement of the results of theShare Exchange Offer.

The consideration payable pursuant to Greek law for eachExisting Share acquired in the Greek Statutory Squeeze-outand/or the Greek Statutory Sell-out is, at the election of theholder, either one Ordinary Share, or A13.58 in cash. Thisalternative cash consideration of A13.58 per Existing Shareis mandatorily required under, and represents the minimumcash consideration permitted by, Greek law, and iscalculated as the volume weighted average market price of

21

Section E—Offer

Element Disclosure requirement Disclosure

the Existing Shares on the Athens Exchange over the sixmonths ended 9 October 2012, the last trading daypreceding the Initiation Date. The cash price is lower thanA20.48, the last reported sales price of an Existing Share onthe Athens Exchange on 5 March 2013, the last practicabledate prior to publication of this Prospectus.

The cash consideration of A13.58 per Existing Share will bereceived by Existing Shareholders after the deduction of anapplicable Greek transaction tax of 0.2%, which is expectedto be calculated based on the closing market price perExisting Share on the Athens Exchange on the daypreceding the date on which the documents required for thecorresponding transfer are submitted to HELEX. Pursuantto a ruling by the Greek Ministry of Finance with respect tothe Share Exchange Offer, this transaction tax should not bepayable by holders of Existing Shares who elect to receiveOrdinary Shares or New ADSs rather than cashconsideration in the Greek Statutory Squeeze-out or GreekStatutory Sell-out. The Company expects that, in theabsence of an alternative election by a remaining holder toreceive Ordinary Shares in the form of CDIs held throughCREST, such Existing Shareholders will receive OrdinaryShares in book-entry form held through DSS as the defaultconsideration in the Greek Statutory Squeeze-out.

Holders of Existing Shares entitled to sell or exchange theirExisting Shares in the Greek Statutory Sell-out and whowish to receive cash consideration may sell their shares inthe market following the announcement of the results oftheShare Exchange Offer and before the expiration of theGreek Statutory Sell-out period. During that period, theCompany will maintain a standing bid on the AthensExchange to purchase Existing Shares for the cashconsideration per Existing Share in the Greek StatutorySell-out as described above. Holders of Existing Shares whosell those shares to the Company in that manner will receivethe cash consideration, reduced by the Greek transaction taxas described above, in accordance with the standardsettlement cycle for trades on the Athens Exchange, which isthree Greek business days.

Holders of Existing Shares entitled to exchange theirExisting Shares in the Greek Statutory Sell-out and whowish to receive Ordinary Shares will be entitled to deliverthrough their custodians or nominees an election form toHELEX or any other agent of the Company appointed forthat purpose at any time after the announcement of theresults of the Share Exchange Offer and prior to theexpiration of the Greek Statutory Sell-out period threecalendar months following the announcement of the resultsof the Share Exchange Offer. The Company currentlyexpects the Greek Statutory Sell-out period to expire on orabout 23 July 2013.

22

Section E—Offer

Element Disclosure requirement Disclosure