Embed Size (px)

Citation preview

A-1

LOCAL GOVERNMENT CODE OF ACCOUNTING PRACTICE

AND FINANCIAL REPORTING

(GUIDELINES)

Update No. 23 March 2015

Str

en

gth

en

ing

lo

cal g

ove

rnm

en

t

Str

en

gth

en

ing

lo

cal g

ove

rnm

en

t

A-2

ACKNOWLEDGEMENTS The Office of Local Government acknowledges the Australian Accounting Standards Board, CPA Australia Ltd and Chartered Accountants – Australia and New Zealand for their assistance in providing definitions from its Glossary of Terms for use in this document. © Commonwealth of Australia 2015 All legislation herein is reproduced by permission but does not purport to be the official or authorised version. It is subject to Commonwealth of Australia copyright. The Copyright Act 1968 permits certain reproduction and publication of Commonwealth legislation. In particular, s. 182A of the Act enables a complete copy to be made by or on behalf of a particular person. For reproduction or publication beyond that permitted by the Act, permission should be sought in writing from the Commonwealth available from the Australian Accounting Standards Board. Requests in the first instance should be addressed to the Administration Director, Australian Accounting Standards Board, PO Box 204, Collins Street West, Melbourne, Victoria, 8007

ACCESS TO SERVICES The Office of Local Government is located at: Levels 1 & 2 5 O’Keefe Avenue Locked Bag 3015 NOWRA NSW 2541 NOWRA NSW 2541 Phone 02 4428 4100 Fax 02 4428 4199 TTY 02 4428 4209 Level 9, 6 – 10 O’Connell Street PO Box R1772 SYDNEY NSW 2000 ROYAL EXCHANGE NSW 1225 Phone 02 9289 4000 Fax 02 9289 4099 Email [email protected] Website www.olg.nsw.gov.au

OFFICE HOURS Monday to Friday 8.30am to 5.00pm (Special arrangements may be made if these hours are unsuitable) All offices are wheelchair accessible.

ALTERNATIVE MEDIA PUBLICATIONS Special arrangements can be made for our publications to be provided in large print or an alternative media format. If you need this service, please contact our Executive Branch on 02 9289 4000.

DISCLAIMER While every effort has been made to ensure the accuracy of the information in this publication, the Office of Local Government expressly disclaims any liability to any person in respect of anything done or not done as a result of the contents of the publication or the data provided. © NSW Office of Local Government 2015 ISBN 1 920766 41 3 Produced by the Office of Local Government

www.olg.nsw.gov.au

A-3

Introduction and overview

Purpose The Local Government Code of Accounting Practice and Financial Reporting (the Code) prescribes the form of the financial statements approved by the Office of Local Government (the Office).

The Code applies to each NSW Council in respect of its general purpose financial statements, special purpose financial statements and special schedules.

The Code is intended to facilitate the practical and effective implementation of Australian Accounting Standards and aims to provide:

A basis of providing assistance in the interpretation and application of management reporting, accounting, auditing and financial reporting requirements of Chapter 13 of the Local Government Act – “How are councils made accountable for their actions?”.

A mechanism which will ensure that appropriate accounting policies and practices are implemented by all councils.

A basis for audit and review functions to be undertaken in the context of comprehensive and approved accounting standards.

Reliable, comparable and readily comprehensible financial information which will be invaluable for making and evaluating decisions about the allocation of scarce resources and which will assist in assessing the performance, financial position, finances and investments of councils.

Enhanced accountability of councils to the community.

The accounting, financial and other reporting requirements in Code Update #22 apply to all financial statements prepared by local governments for the financial period commencing 1 July 2014 and for subsequent years unless otherwise stated. The Code prescribes the minimum disclosures required – Councils can add additional disclosures at their discretion. In some cases where the standards provide options – as with the valuation of investment properties at cost or fair value – the Code will prescribe which option Councils must adopt.

Purpose of Code

The purpose of the Code is to:

(a) Establish a framework for preparation and reporting of estimates of income and expenditure. [Clause 201– Local Government (General) Regulation (LGGR)]

(b) Provide guidance on the application of professionally based accounting standards and various legislative requirements.

(c) Specify the accounting records and practices to be followed that ensure adequate systems and internal controls are in place to manage council’s resources [Clause 206 – LGGR]

(d) Establish financial reporting requirements to govern the form and content of financial statements of local governments [Clause 214 – LGGR]

(e) Specify the matters that an auditor must consider and comment on when conducting audits [Clause 227 – LGGR]

The purpose of the illustrative financial statements is to highlight disclosure requirements, provide sample disclosures and worked examples and serve as a convenient reference to source material. The fictitious circumstances of our example Council, NSW Council, have been chosen to illustrate the most common and significant accounting issues and associated disclosures under Australian Accounting Standards. These issues may not necessarily apply to all councils nor are they exhaustive.

Authority of Code

For the purpose of Section 405 of the Act, the Code issued by the Minister and published by the Office details the requirements of estimates of income and expenditure that a council must include in its draft operational plan for the year.

A-4

For the purpose of Section 412 of the Act, the Code issued by the Minister and published by the Office details the accounting records and accounting practices that a council must accord with in managing resources under its control.

For the purpose of Section 413(2b) and (3b) of the Act, the Code issued by the Minister and published by the Office details the financial reporting requirements that a council must incorporate when preparing its financial statements.

For the purpose of Section 415(3) LG Act and the LGGR the auditor, in auditing a council’s general purpose financial statements, must consider and provide comment on the following matters:

(f) Relating to the Income Statement. The gain/(loss) from continuing activities for the year including the effect of depreciation, the result for the year before capital amounts, level of grants and contributions and the level of rates increase for the year.

(g) Relating to the Statement of financial position. Consideration and comment should also be provided on the utilisation of overdraft facilities.

(h) Relating to Performance. Performance indicators and trends including current ratios, debt servicing, rates coverage, rates outstanding and the level of loan indebtedness, restricted assets and level of asset renewal.

(i) Relating to the Statement of cash flows. The effect on the statement of cash flows of material items such as borrowings or large section 94 contributions.

(j) Relating to Legislative Compliance. The meeting of all statutory reporting requirements relating to Division 2 of Chapter 13 of the LG Act and relating to the LGGR and any legislatively prescribed standards.

(k) Relating to Other Matters. The auditor should comment on other such matters which are material such as the effect of the introduction of new accounting standards, the effect of significant initiatives undertaken or future plans of council where these can be quantified and are sufficiently firm to comment on.

Foreign investment

Pursuant to Section 625 of the Local Government Act 1993, a Council may only invest money on the basis that all investments must be denominated in Australian dollars.

Legislative requirements for financial statements

A tabular and graphical illustration of the legislative requirements pertaining to financial statements is provided at Appendix D and E. The dates specified are the latest applicable for the particular legislative requirements to be satisfied. All timetable deadlines are applicable from the financial year ending 30 June 2015.

Councils are required to have access to the Australian Accounting Standards (www.aasb.gov.au).

Monitoring and review

The Office of Local Government will ensure that the Code remains current and will provide amendments by way of

publication on the Office’s internet home page, www.olg.nsw.gov.au.

Industry feedback is actively encouraged to assist the Office in the development and delivery of sound financial policies that cater for the practical needs of councils.

The Office of Local Government would like to thank CaseWare Australia and New Zealand for their assistance in the development of this Code update.

The Office of Local Government would also like to thank the Institute of Public Works Engineering Australia (IPWEA) for allowing sections of their Infrastructure Financial Management Guidelines to be used in the Code.

STEVE ORR ACTING CHIEF EXECUTIVE OFFICE OF LOCAL GOVERNMENT

A-5

Local Government Code of Accounting Practice and Financial Reporting Update 23

Contents

General purpose financial statements A6 – A141

Special purpose financial statements B1 – B16

Special schedules C1 – C27

Appendices D1 – D44

The Code prescribes the minimum disclosures required – Councils can add additional disclosures at their discretion. In some cases where the standards provide options – as with the valuation of investment properties at cost or fair value – the Code will prescribe which option Councils must adopt.

Councils must complete the five primary reports and Notes 1 to 27 in the format prescribed:

(a) The Income statement, Statement of comprehensive income, Statement of financial position and Statement of changes in equity are to be replicated with all lines from the Code even if nil value.

(b) Where there is both an expense and income line displayed then one of these can be deleted when not in use.

(c) The Statement of cashflows line items in the Code need only be included where applicable to Council.

(d) Within Notes 1 to 20 line items that are not applicable can be left out.

Notes 1 to 20 and 27 are mandatory even if of nil value. Thereafter notes need only be included if applicable and additional notes may be added as required.

For Notes 1, 13(b), 14, 17, 19 and 21 the following also apply:

Note 1 – Summary of significant accounting policies Councils are to disclose only significant accounting policies that are relevant to them. The Code provides examples of possible disclosures, but these may not be relevant to all councils.

Note 13(b) – Statement of performance measures by fund Do not complete unless Council has Water and/or Sewer Funds.

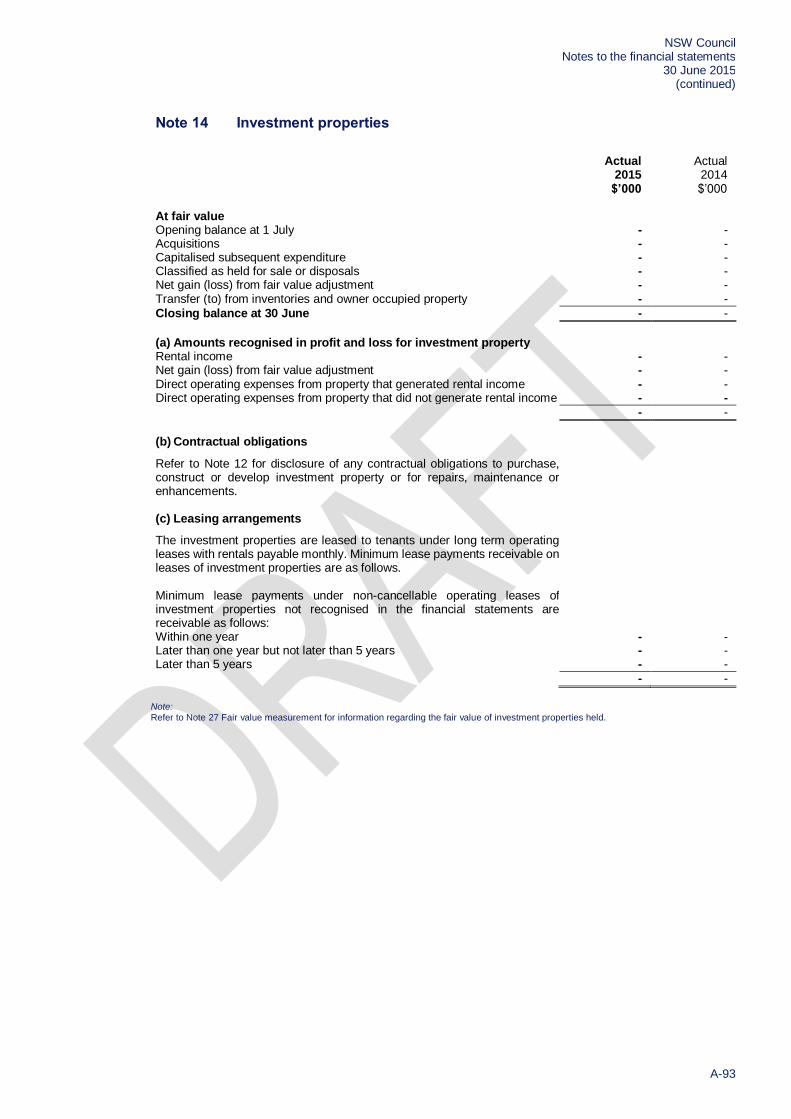

Note 14 – Investment properties If Council has no Investment properties, then a statement to this effect can replace the detail specified.

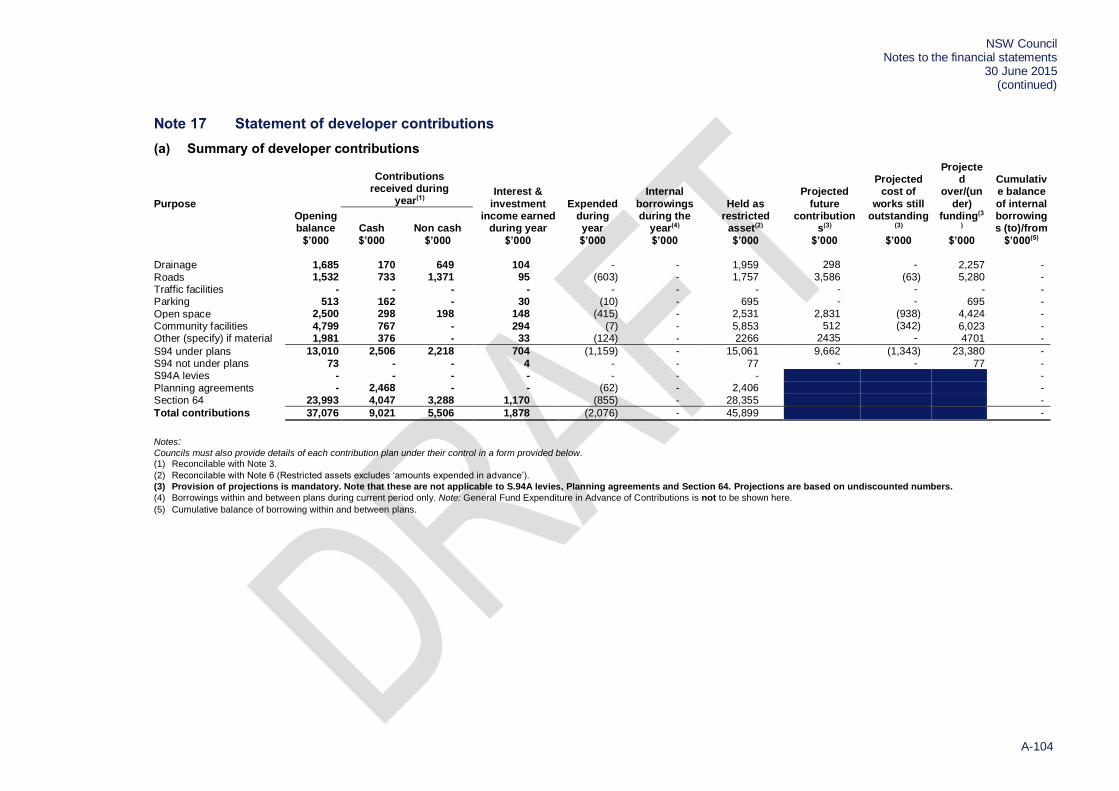

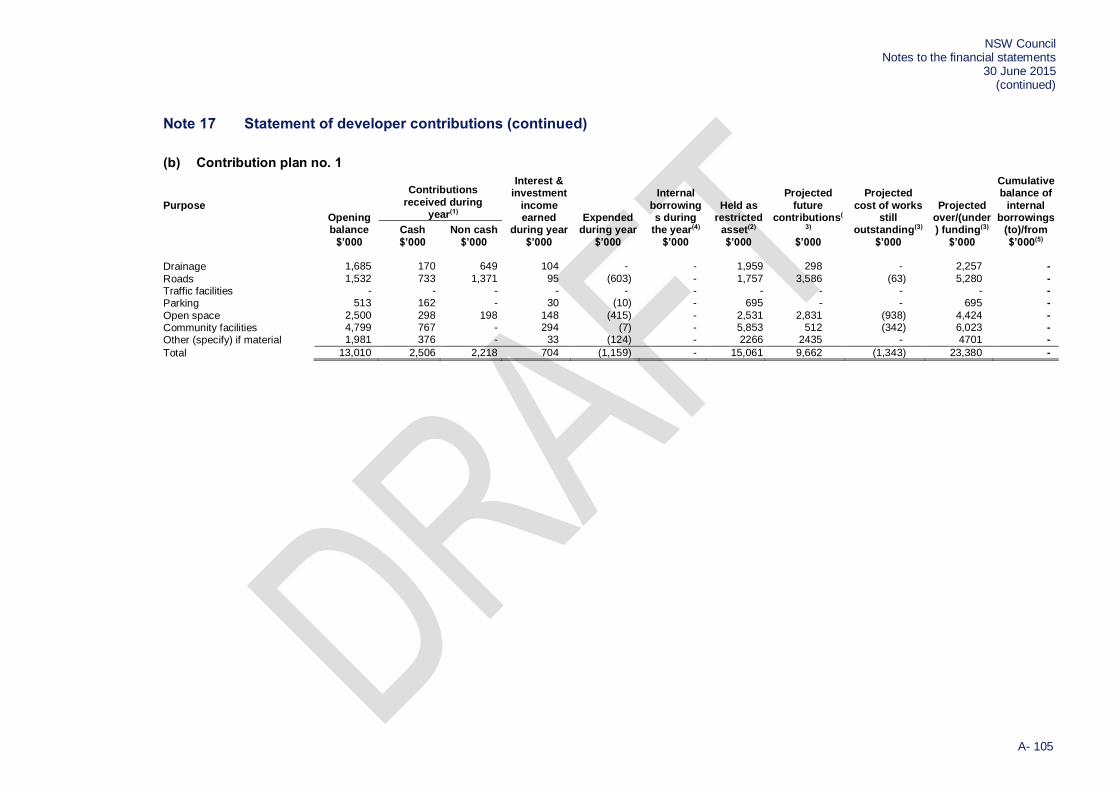

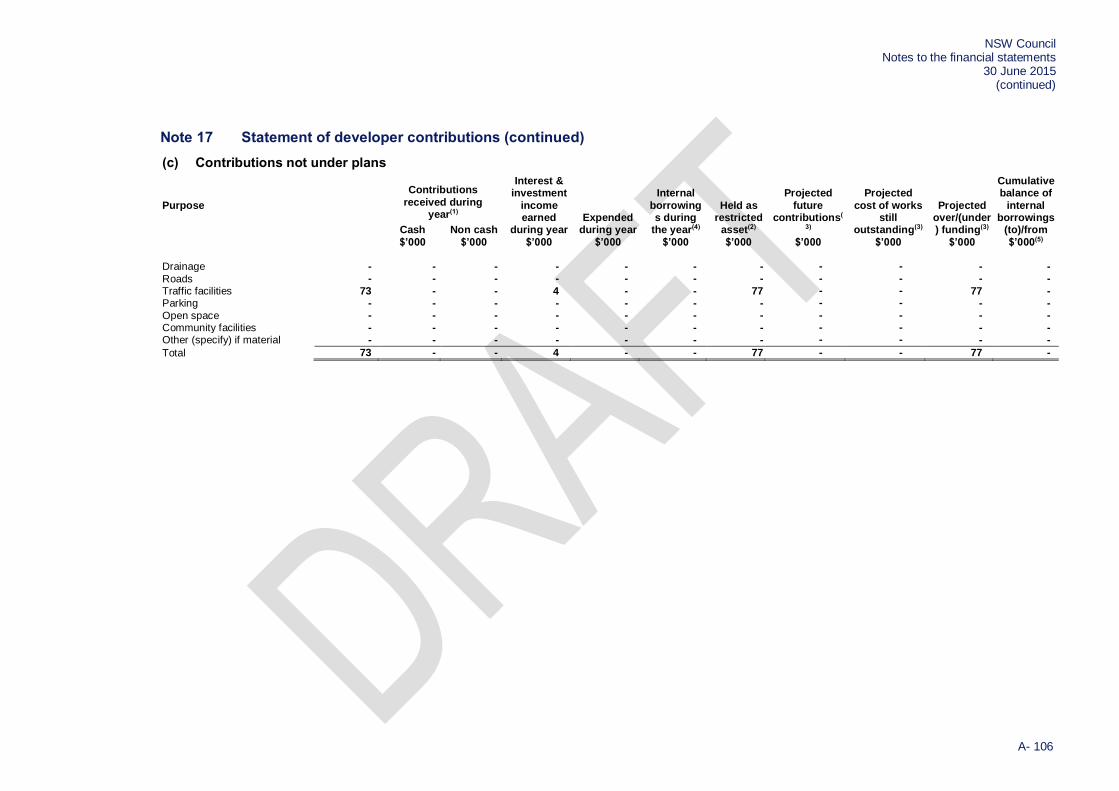

Note 17 – Developer contributions If Council has no Developer contributions, then a statement to this effect can replace the detail specified.

Note 19 – Interests in other entities Exclude sections for interests in other entity types that are not relevant to Council. Where Council has no interests in other entities a statement to this effect can replace the specified lines.

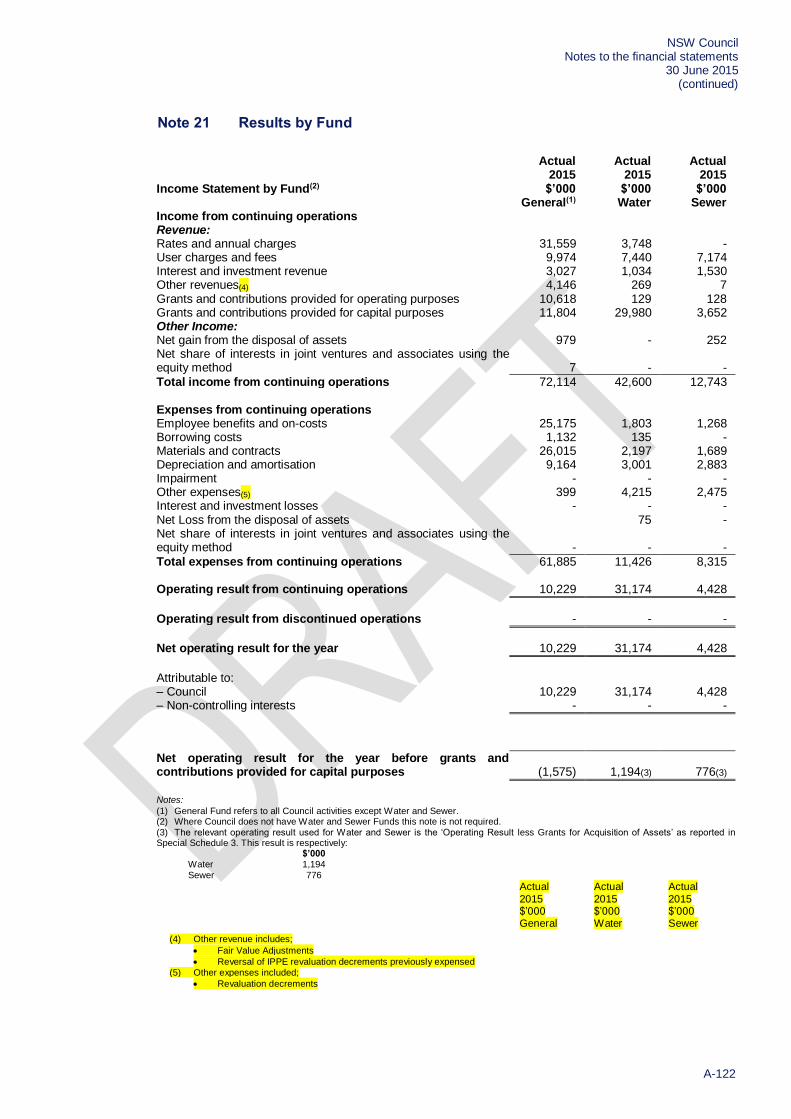

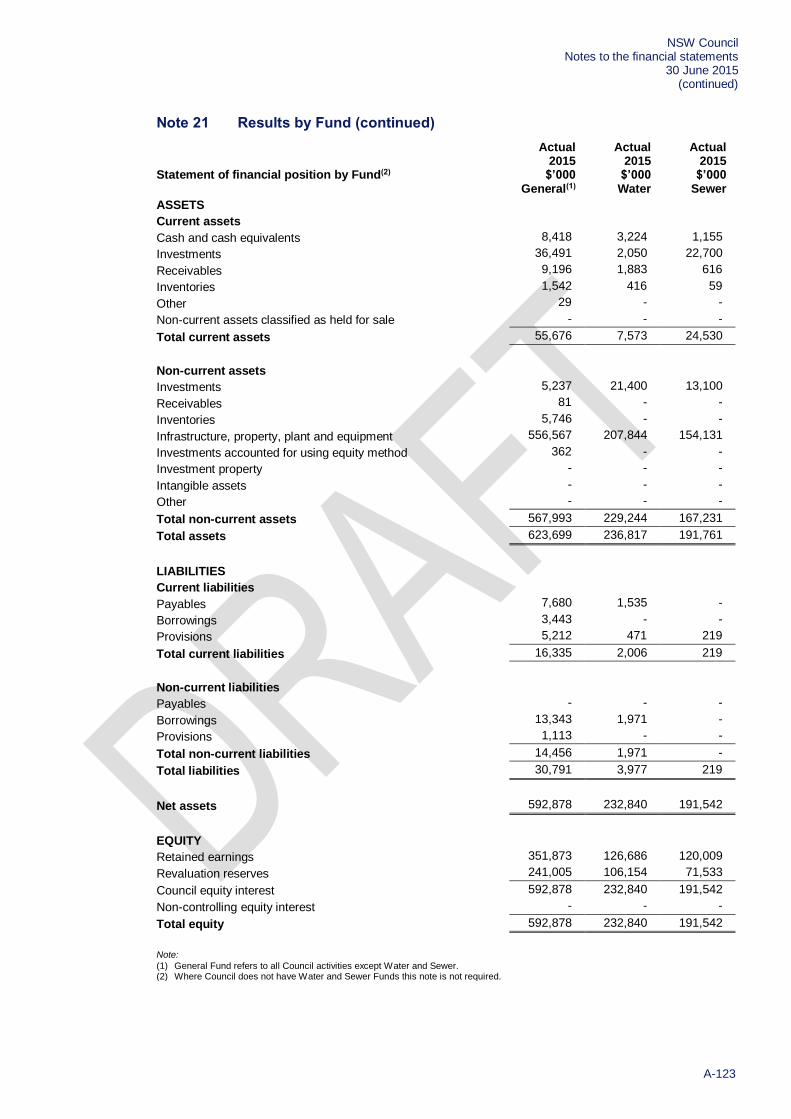

Note 21 – Results by fund Do not complete unless Council has Water and/or Sewer Funds.

A-6

NSW Council

General purpose financial statements for the year ended 30 June 2015

Contents

Page General purpose financial statements Statement by Councillors and Management A-9

Income Statement A-11

Statement of Comprehensive Income A-12

Statement of Financial Position A-16

Statement of Changes in Equity A-18

Statement of Cash Flows A-20

Notes to the Financial Statements A-23

Auditors’ reports A-143

AASB101(46)(b),(d)

These financial statements are general purpose financial statements of NSW Council and its controlled entities and are presented in the Australian currency.

AASB101(126)(a)

NSW Council is constituted under the Local Government Act (1993) and has its principal place of business at:

NSW Council XXXX Street XX NSW 2XXX. AASB110(17) The financial statements were authorised for issue by the Council on XX 2015. Council has the power to

amend and reissue the financial statements.

Through the use of the internet, we have ensured that our reporting is timely, complete, and available at minimum cost. All press releases, financial statements and other information are readily available on our website: www.council.nsw.gov.au.

NSW Council Financial statements 30 June 2015

A-7

Commentary – Financial statements

Accounting standard for financial statements presentation and disclosures AASB101(10) 1. According to AASB 101, a 'complete set of financial statements' comprises: (a) a s a statement of financial position as at the end of the period (b) a statement of comprehensive income for the period (c) a statement of changes in equity for the period (d) a statement of cash flow for the period (e) notes, comprising a summary of significant accounting policies and other explanatory notes,

and (f) if the council has applied an accounting policy retrospectively, made a retrospective

restatement of items or has reclassified items in its financial statements: a statement of financial position as at the beginning of the earliest comparative period.

AASB101(11) The statements must all be presented with equal prominence.

Consistency AASB101(45) 2. The presentation and classification of items in the financial statements shall be retained from one

period to the next unless: (a) it is apparent, following a significant change in the nature of the council’s operations or a review

of its financial statements, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, or

(b) an Australian Accounting Standard requires a change in presentation.

Materiality and aggregation AASB101(29) 3. Each material class of similar items shall be presented separately in the financial statements. Items

of a similar nature or function shall be presented separately unless they are immaterial.

Comparative information AASB101(40) 4. In some cases, narrative information provided in the financial statements for the previous period(s)

continues to be relevant in the current period. For example, details of a legal dispute, the outcome of which was uncertain at the end of the immediately preceding reporting period and that is yet to be resolved, are disclosed in the current period. Users benefit from information that the uncertainty existed at the end of the immediately preceding reporting period, and about the steps that have been taken during the period to resolve the uncertainty.

AASB101(41) 5. When the presentation or classification of items in the financial statements is amended, comparative amounts shall be reclassified unless the reclassification is impracticable. When comparative amounts are reclassified, a council shall disclose:

(a) the nature of the reclassification (b) the amount of each item or class of items that is reclassified (c) the reason for the reclassification.

AASB101(42) 6. When it is impracticable to reclassify comparative amounts, a council shall disclose: (a) the reason for not reclassifying the amounts (b) the nature of the adjustments that would have been made if the amounts had been

reclassified.

Three statements of financial position required in certain circumstances AASB101(38),(39) 7. If a council has applied an accounting policy retrospectively, restated items retrospectively or

reclassified items in its financial statements, it must present a third statement of financial position and associated notes as at the beginning of the earliest comparative period presented. However, where the retrospective change in policy or the restatement has no effect on this earliest statement of financial position, we believe that it would be sufficient for the council to merely disclose that fact.

Date of Issue of Financial Statements OLG 8. The Office of Local Government has determined that the date when the financial statements are

authorised for issue is the date on which the Council’s audit report is signed. Council should disclose that it has the power to amend and reissue the financial statements in cases where critical information is received from public submissions or where the OLG directs Council to amend the statements.

NSW Council Financial statements 30 June 2015 (continued)

A-8

Commentary – Financial statements (continued)

OLG Lodgement of Financial Statements Policy statement 9. Councils must lodge a complete set of financial statements with the Office of Local Government by

no later than the close of business on the 31st October following the financial year end. Fax copies of financial statements are not acceptable.

10. A Council’s financial statements lodged with the Office of Local Government will be deemed to be deficient if they:

(a) have missing or an incomplete statement by Council required by Section 413(2)(c) LG Act (b) have missing either of the two audit reports required by Section 417(1) LG Act (c) have incomplete statements and/or notes to the accounts (d) have material errors (e) have failed to comply with requirements of local government legislation or the Australian

Accounting Standards and have not disclosed non compliance.

11. Where financial statements are deemed to be deficient, Council will be required to re-lodge their reports and if necessary, provide public notice of any amendments made in accordance with the LG (General) Regulations.

12. Any request for extension to lodge financial statements must be in writing and lodged not later than 17 October. An application for an extension must:

(a) specify the reason(s) for which the extension is sought (b) specify the period for which the extension is being sought (c) attach a copy of the audit notification of council’s intention to seek an extension, and (d) provide the lodgement dates of financial statements and details of any extensions sought

(irrespective of approval) for the previous 3 years.

13. No extensions will be approved beyond 30 November following the financial year end. Requests for extensions to submit financial statements will not be authorised unless there are extraordinary circumstances. Requests for extension on the grounds of computer difficulties and/or lack of staff resources will not be considered extraordinary.

NSW Council Statement by Councillors and Management For the year ended 30 June 2015

A-9

NSW Council

General purpose financial statements for the year ended 30 June 2015

Statement by Councillors and Management made pursuant to Section 413(2)(c) of the Local Government Act 1993 (as amended) The attached General Purpose Financial Statements have been prepared in accordance with:

The Local Government Act 1993 (as amended) and the Regulations made thereunder.

The Australian Accounting Standards and professional pronouncements.

The Local Government Code of Accounting Practice and Financial Reporting.

To the best of our knowledge and belief, these Statements:

presents fairly the Council’s operating result and financial position for the year, and

accords with Council’s accounting and other records.

We are not aware of any matter that would render this Report false or misleading in any way.

Signed in accordance with a resolution of Council made on ……………………………………..

Councillor’s Name Mayor

Councillor’s Name Councillor

General Manager’s Name General Manager

Responsible Accounting Officer's Name Responsible Accounting Officer

NSW Council Statement by Councillors and Management For the year ended 30 June 2015 (continued)

A-10

Commentary – Statement by Councillors and Management

LGA – Sec. 413 (2) (C) Dating and signing of report 1. The Statement must be made in accordance with a resolution of the Council and specify the date on

which it was made.

NSW Council Income statements and statements of comprehensive income For the year ended 30 June 2015

A-11

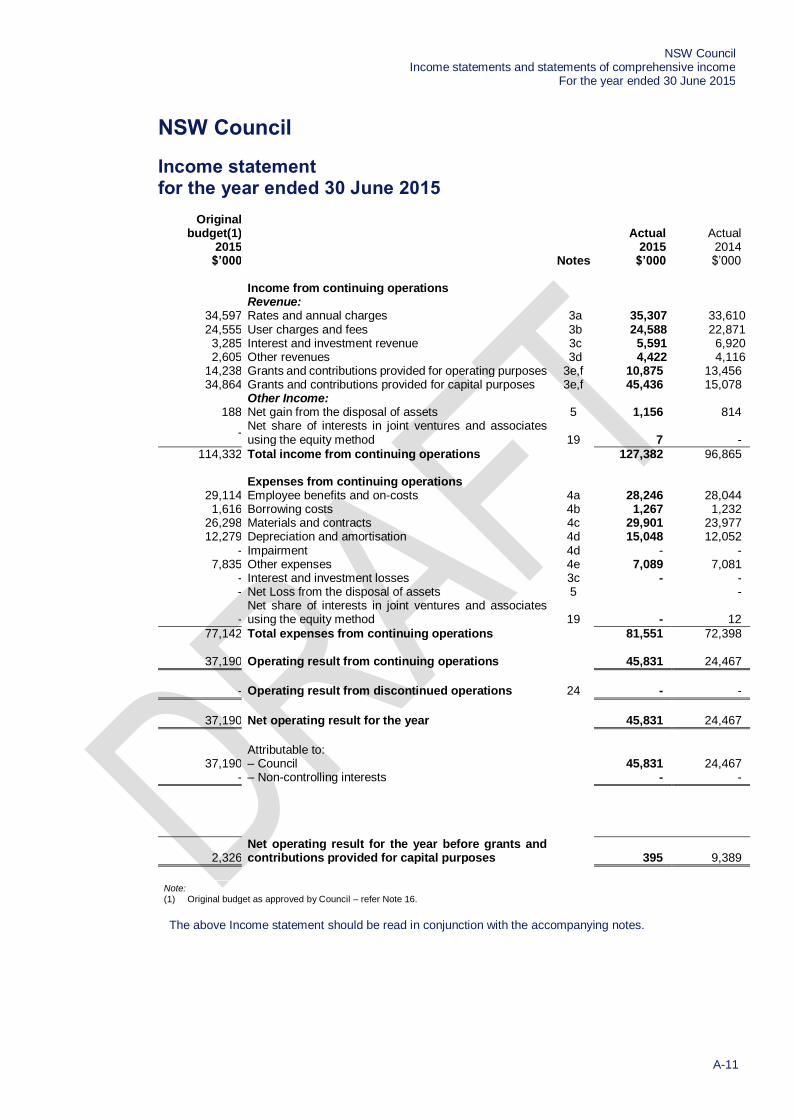

NSW Council

Income statement for the year ended 30 June 2015

Original budget(1)

2015 $’000 Notes

Actual 2015 $’000

Actual 2014 $’000

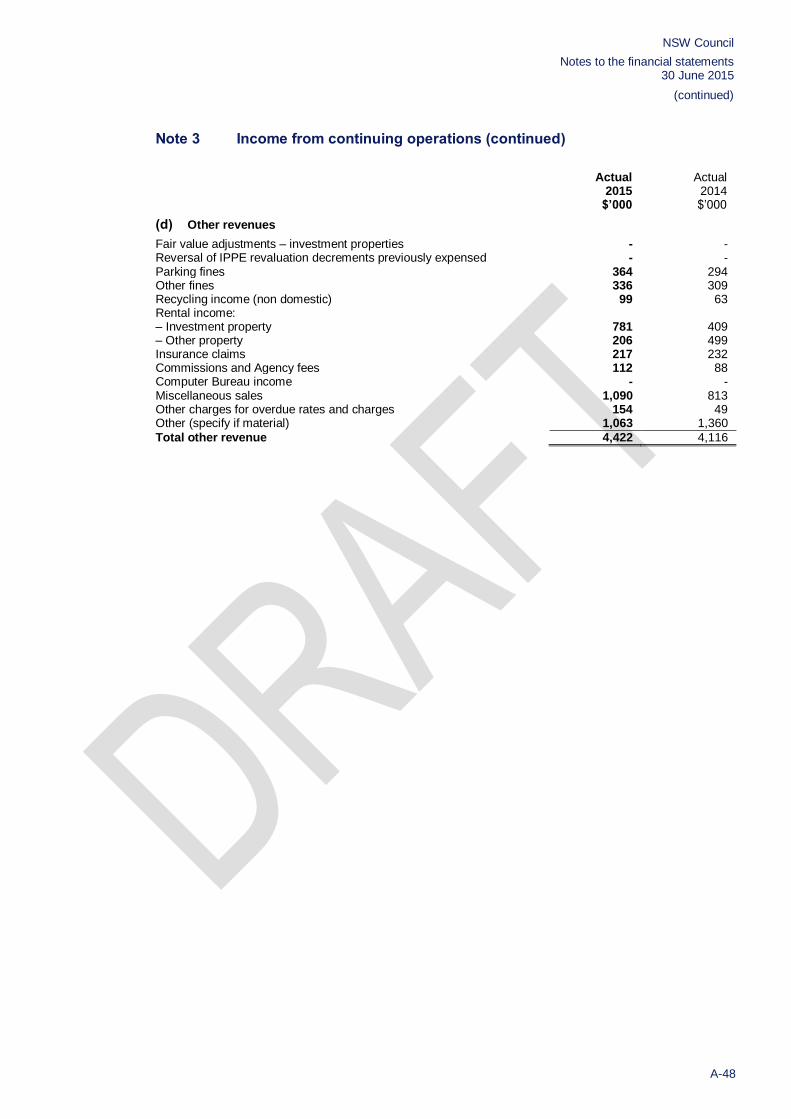

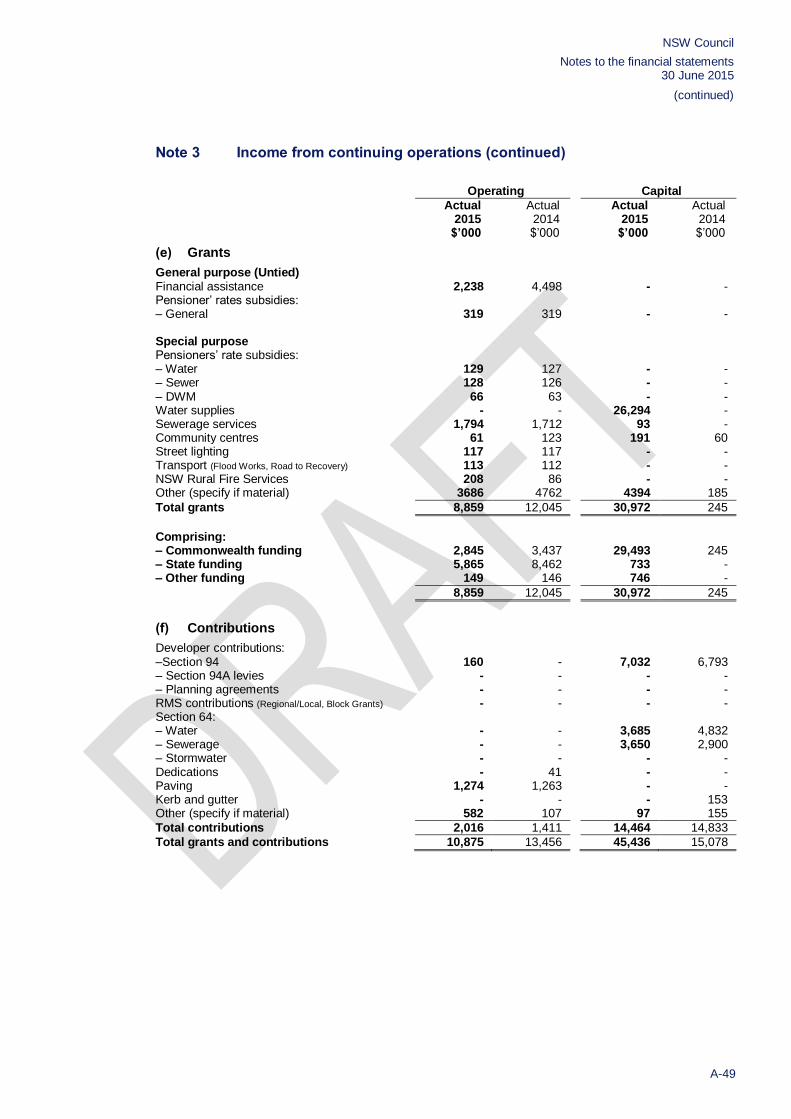

Income from continuing operations Revenue: 34,597 Rates and annual charges 3a 35,307 33,610 24,555 User charges and fees 3b 24,588 22,871 3,285 Interest and investment revenue 3c 5,591 6,920 2,605 Other revenues 3d 4,422 4,116 14,238 Grants and contributions provided for operating purposes 3e,f 10,875 13,456 34,864 Grants and contributions provided for capital purposes 3e,f 45,436 15,078 Other Income: 188 Net gain from the disposal of assets 5 1,156 814

- Net share of interests in joint ventures and associates using the equity method 19 7 -

114,332 Total income from continuing operations 127,382 96,865 Expenses from continuing operations 29,114 Employee benefits and on-costs 4a 28,246 28,044 1,616 Borrowing costs 4b 1,267 1,232 26,298 Materials and contracts 4c 29,901 23,977 12,279 Depreciation and amortisation 4d 15,048 12,052 - Impairment 4d - - 7,835 Other expenses 4e 7,089 7,081 - Interest and investment losses 3c - - - Net Loss from the disposal of assets 5 -

- Net share of interests in joint ventures and associates using the equity method 19 - 12

77,142 Total expenses from continuing operations 81,551 72,398 37,190 Operating result from continuing operations 45,831 24,467

- Operating result from discontinued operations 24 - -

37,190 Net operating result for the year 45,831 24,467

Attributable to: 37,190 – Council 45,831 24,467 - – Non-controlling interests - -

2,326

Net operating result for the year before grants and contributions provided for capital purposes 395 9,389

Note:

(1) Original budget as approved by Council – refer Note 16.

The above Income statement should be read in conjunction with the accompanying notes.

NSW Council Income statements and statements of comprehensive income For the year ended 30 June 2015 (continued)

A-12

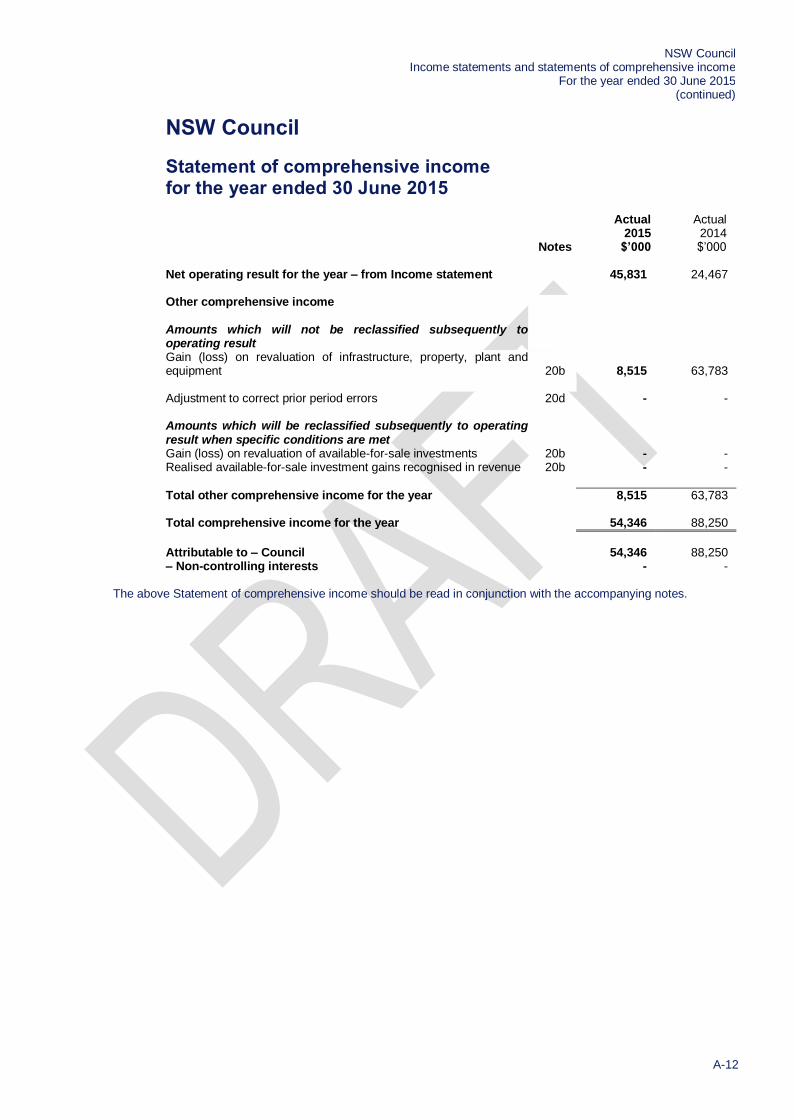

NSW Council

Statement of comprehensive income for the year ended 30 June 2015

Notes

Actual 2015 $’000

Actual 2014 $’000

Net operating result for the year – from Income statement 45,831 24,467 Other comprehensive income

Amounts which will not be reclassified subsequently to operating result

Gain (loss) on revaluation of infrastructure, property, plant and equipment

20b

8,515

63,783

Adjustment to correct prior period errors 20d - -

Amounts which will be reclassified subsequently to operating result when specific conditions are met Gain (loss) on revaluation of available-for-sale investments 20b - -

Realised available-for-sale investment gains recognised in revenue 20b - -

Total other comprehensive income for the year 8,515 63,783 Total comprehensive income for the year 54,346 88,250

Attributable to – Council

54,346 88,250

– Non-controlling interests - -

The above Statement of comprehensive income should be read in conjunction with the accompanying notes.

NSW Council Income statements and statements of comprehensive income For the year ended 30 June 2015 (continued)

A-13

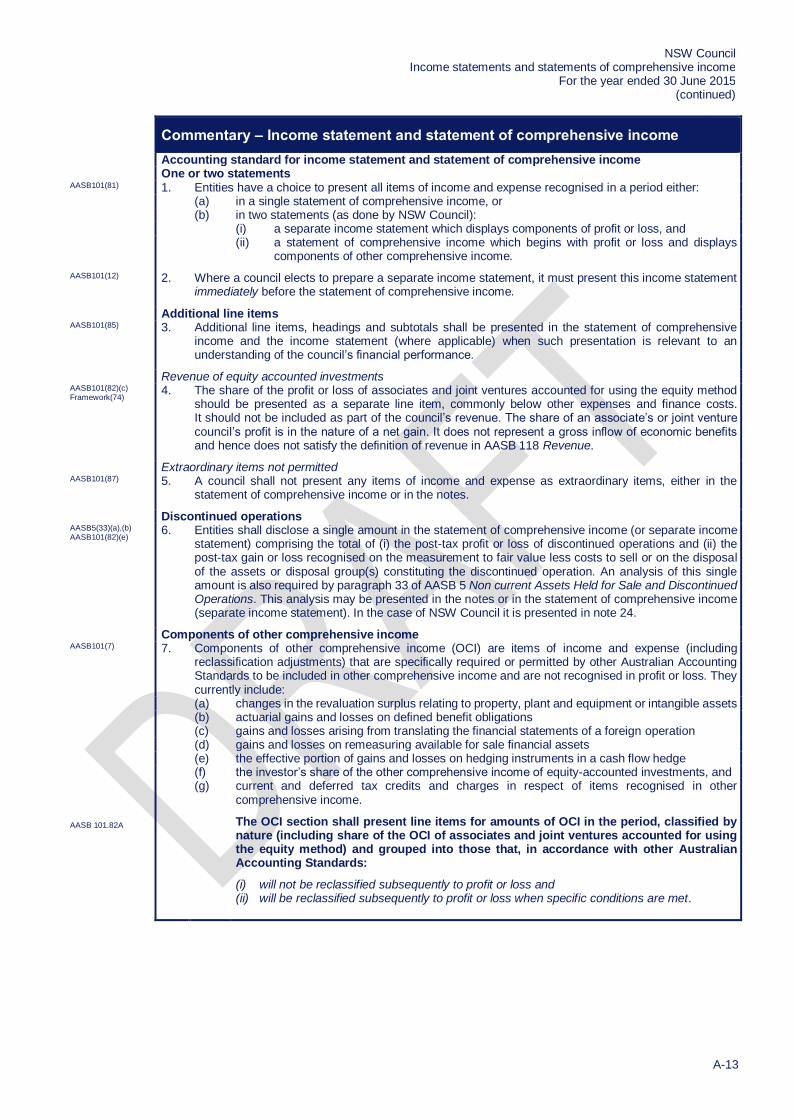

Commentary – Income statement and statement of comprehensive income

Accounting standard for income statement and statement of comprehensive income One or two statements AASB101(81) 1. Entities have a choice to present all items of income and expense recognised in a period either: (a) in a single statement of comprehensive income, or (b) in two statements (as done by NSW Council): (i) a separate income statement which displays components of profit or loss, and (ii) a statement of comprehensive income which begins with profit or loss and displays

components of other comprehensive income.

AASB101(12) 2. Where a council elects to prepare a separate income statement, it must present this income statement immediately before the statement of comprehensive income.

Additional line items AASB101(85) 3. Additional line items, headings and subtotals shall be presented in the statement of comprehensive

income and the income statement (where applicable) when such presentation is relevant to an understanding of the council’s financial performance.

Revenue of equity accounted investments AASB101(82)(c) Framework(74)

4. The share of the profit or loss of associates and joint ventures accounted for using the equity method should be presented as a separate line item, commonly below other expenses and finance costs. It should not be included as part of the council’s revenue. The share of an associate’s or joint venture council’s profit is in the nature of a net gain. It does not represent a gross inflow of economic benefits and hence does not satisfy the definition of revenue in AASB 118 Revenue.

Extraordinary items not permitted AASB101(87) 5. A council shall not present any items of income and expense as extraordinary items, either in the

statement of comprehensive income or in the notes.

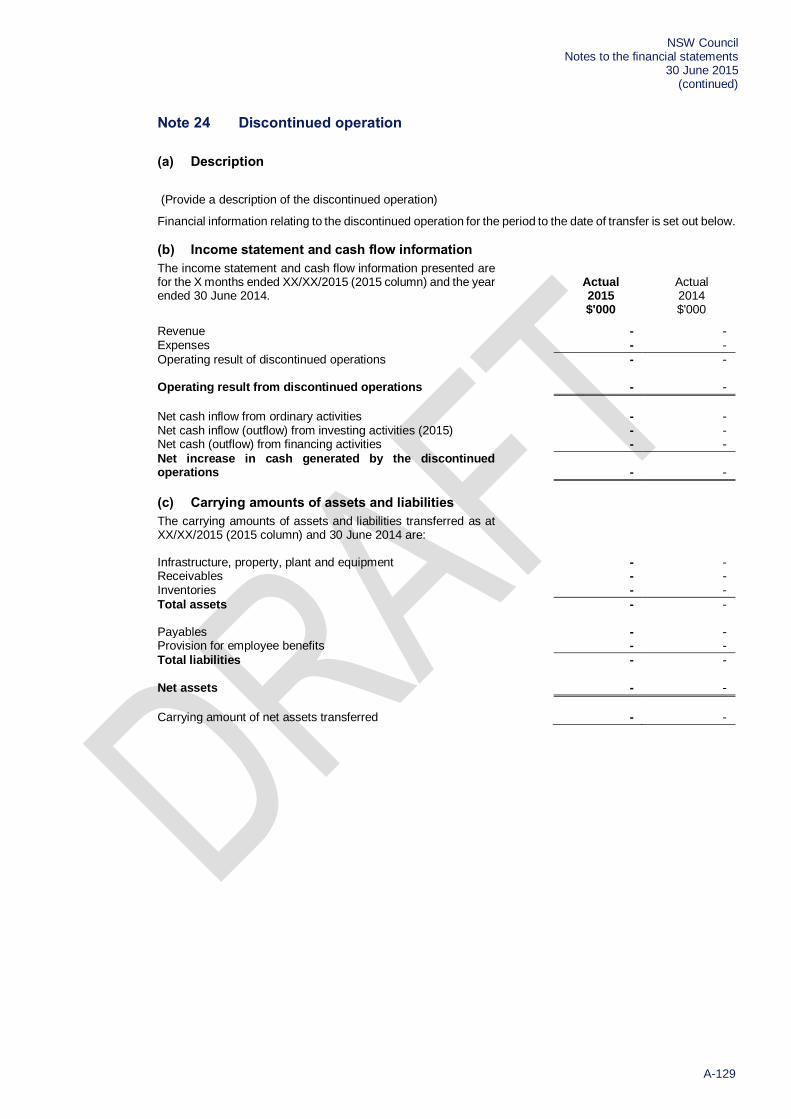

Discontinued operations AASB5(33)(a),(b) AASB101(82)(e)

6. Entities shall disclose a single amount in the statement of comprehensive income (or separate income statement) comprising the total of (i) the post-tax profit or loss of discontinued operations and (ii) the post-tax gain or loss recognised on the measurement to fair value less costs to sell or on the disposal of the assets or disposal group(s) constituting the discontinued operation. An analysis of this single amount is also required by paragraph 33 of AASB 5 Non current Assets Held for Sale and Discontinued Operations. This analysis may be presented in the notes or in the statement of comprehensive income (separate income statement). In the case of NSW Council it is presented in note 24.

Components of other comprehensive income AASB101(7) 7. Components of other comprehensive income (OCI) are items of income and expense (including

reclassification adjustments) that are specifically required or permitted by other Australian Accounting Standards to be included in other comprehensive income and are not recognised in profit or loss. They currently include:

(a) changes in the revaluation surplus relating to property, plant and equipment or intangible assets (b) actuarial gains and losses on defined benefit obligations (c) gains and losses arising from translating the financial statements of a foreign operation (d) gains and losses on remeasuring available for sale financial assets (e) the effective portion of gains and losses on hedging instruments in a cash flow hedge (f) the investor’s share of the other comprehensive income of equity-accounted investments, and (g) current and deferred tax credits and charges in respect of items recognised in other

comprehensive income.

The OCI section shall present line items for amounts of OCI in the period, classified by nature (including share of the OCI of associates and joint ventures accounted for using the equity method) and grouped into those that, in accordance with other Australian Accounting Standards:

(i) will not be reclassified subsequently to profit or loss and (ii) will be reclassified subsequently to profit or loss when specific conditions are met.

AASB 101.82A

NSW Council Income statements and statements of comprehensive income For the year ended 30 June 2015 (continued)

A-14

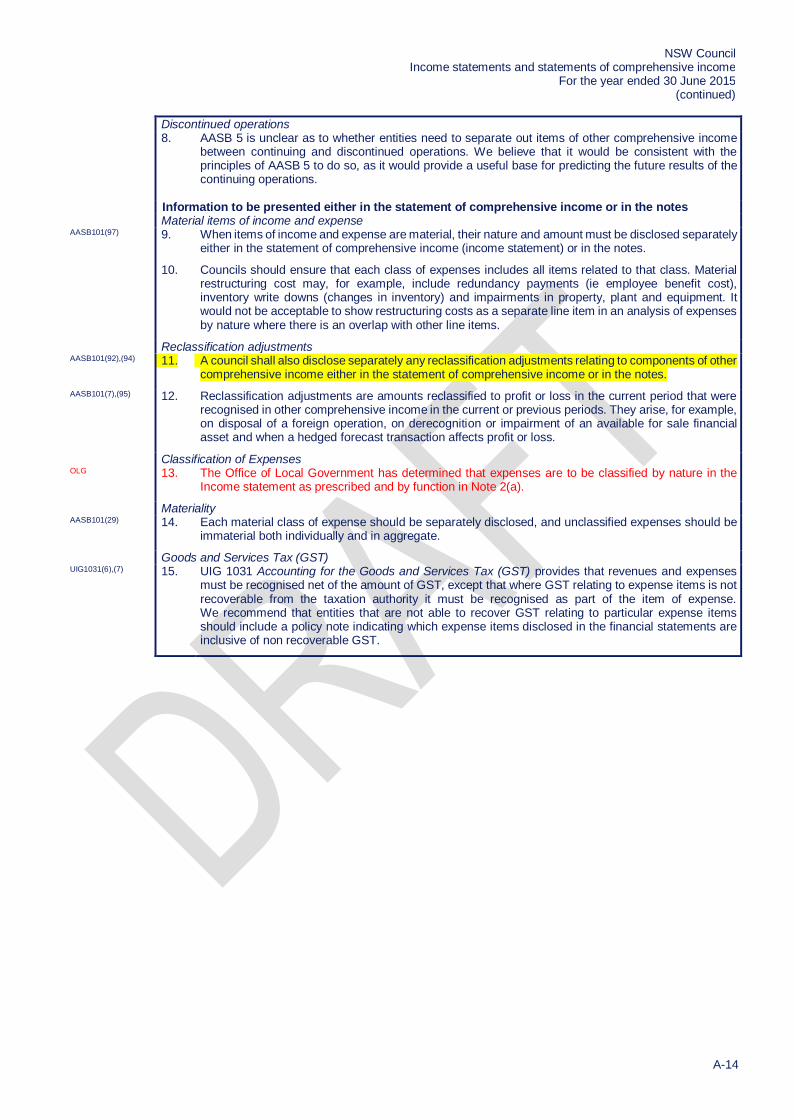

Discontinued operations 8. AASB 5 is unclear as to whether entities need to separate out items of other comprehensive income

between continuing and discontinued operations. We believe that it would be consistent with the principles of AASB 5 to do so, as it would provide a useful base for predicting the future results of the continuing operations.

Information to be presented either in the statement of comprehensive income or in the notes Material items of income and expense AASB101(97) 9. When items of income and expense are material, their nature and amount must be disclosed separately

either in the statement of comprehensive income (income statement) or in the notes.

10. Councils should ensure that each class of expenses includes all items related to that class. Material restructuring cost may, for example, include redundancy payments (ie employee benefit cost), inventory write downs (changes in inventory) and impairments in property, plant and equipment. It would not be acceptable to show restructuring costs as a separate line item in an analysis of expenses by nature where there is an overlap with other line items.

Reclassification adjustments AASB101(92),(94)

11. A council shall also disclose separately any reclassification adjustments relating to components of other comprehensive income either in the statement of comprehensive income or in the notes.

AASB101(7),(95) 12. Reclassification adjustments are amounts reclassified to profit or loss in the current period that were recognised in other comprehensive income in the current or previous periods. They arise, for example, on disposal of a foreign operation, on derecognition or impairment of an available for sale financial asset and when a hedged forecast transaction affects profit or loss.

Classification of Expenses OLG 13. The Office of Local Government has determined that expenses are to be classified by nature in the

Income statement as prescribed and by function in Note 2(a).

Materiality AASB101(29)

14. Each material class of expense should be separately disclosed, and unclassified expenses should be immaterial both individually and in aggregate.

Goods and Services Tax (GST) UIG1031(6),(7) 15. UIG 1031 Accounting for the Goods and Services Tax (GST) provides that revenues and expenses

must be recognised net of the amount of GST, except that where GST relating to expense items is not recoverable from the taxation authority it must be recognised as part of the item of expense. We recommend that entities that are not able to recover GST relating to particular expense items should include a policy note indicating which expense items disclosed in the financial statements are inclusive of non recoverable GST.

NSW Council Income statements and statements of comprehensive income For the year ended 30 June 2015 (continued)

A-15

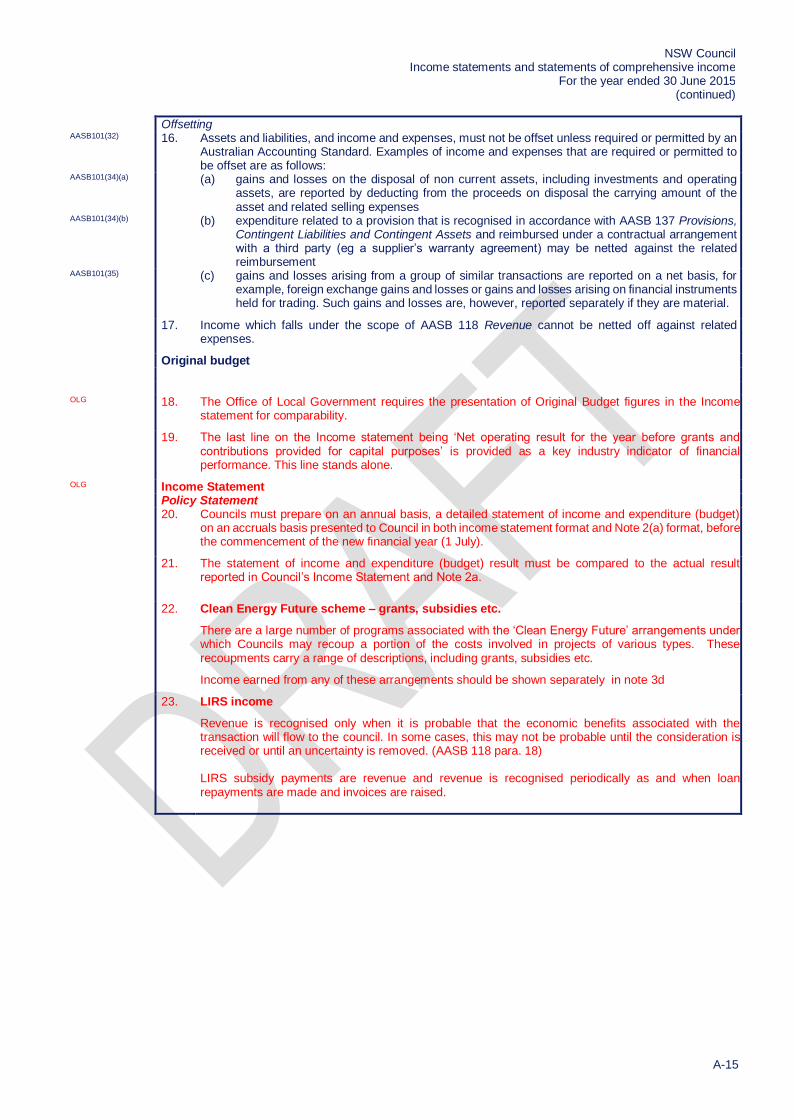

Offsetting AASB101(32) 16. Assets and liabilities, and income and expenses, must not be offset unless required or permitted by an

Australian Accounting Standard. Examples of income and expenses that are required or permitted to be offset are as follows:

AASB101(34)(a) (a) gains and losses on the disposal of non current assets, including investments and operating assets, are reported by deducting from the proceeds on disposal the carrying amount of the asset and related selling expenses

AASB101(34)(b) (b) expenditure related to a provision that is recognised in accordance with AASB 137 Provisions, Contingent Liabilities and Contingent Assets and reimbursed under a contractual arrangement with a third party (eg a supplier’s warranty agreement) may be netted against the related reimbursement

AASB101(35) (c) gains and losses arising from a group of similar transactions are reported on a net basis, for example, foreign exchange gains and losses or gains and losses arising on financial instruments held for trading. Such gains and losses are, however, reported separately if they are material.

17. Income which falls under the scope of AASB 118 Revenue cannot be netted off against related expenses.

Original budget OLG 18. The Office of Local Government requires the presentation of Original Budget figures in the Income

statement for comparability.

19. The last line on the Income statement being ‘Net operating result for the year before grants and contributions provided for capital purposes’ is provided as a key industry indicator of financial performance. This line stands alone.

OLG Income Statement Policy Statement 20. Councils must prepare on an annual basis, a detailed statement of income and expenditure (budget)

on an accruals basis presented to Council in both income statement format and Note 2(a) format, before the commencement of the new financial year (1 July).

21. The statement of income and expenditure (budget) result must be compared to the actual result reported in Council’s Income Statement and Note 2a.

22. Clean Energy Future scheme – grants, subsidies etc.

There are a large number of programs associated with the ‘Clean Energy Future’ arrangements under which Councils may recoup a portion of the costs involved in projects of various types. These recoupments carry a range of descriptions, including grants, subsidies etc.

Income earned from any of these arrangements should be shown separately in note 3d

23. LIRS income

Revenue is recognised only when it is probable that the economic benefits associated with the transaction will flow to the council. In some cases, this may not be probable until the consideration is received or until an uncertainty is removed. (AASB 118 para. 18) LIRS subsidy payments are revenue and revenue is recognised periodically as and when loan repayments are made and invoices are raised.

NSW Council Statement of financial position As at 30 June 2015

A-16

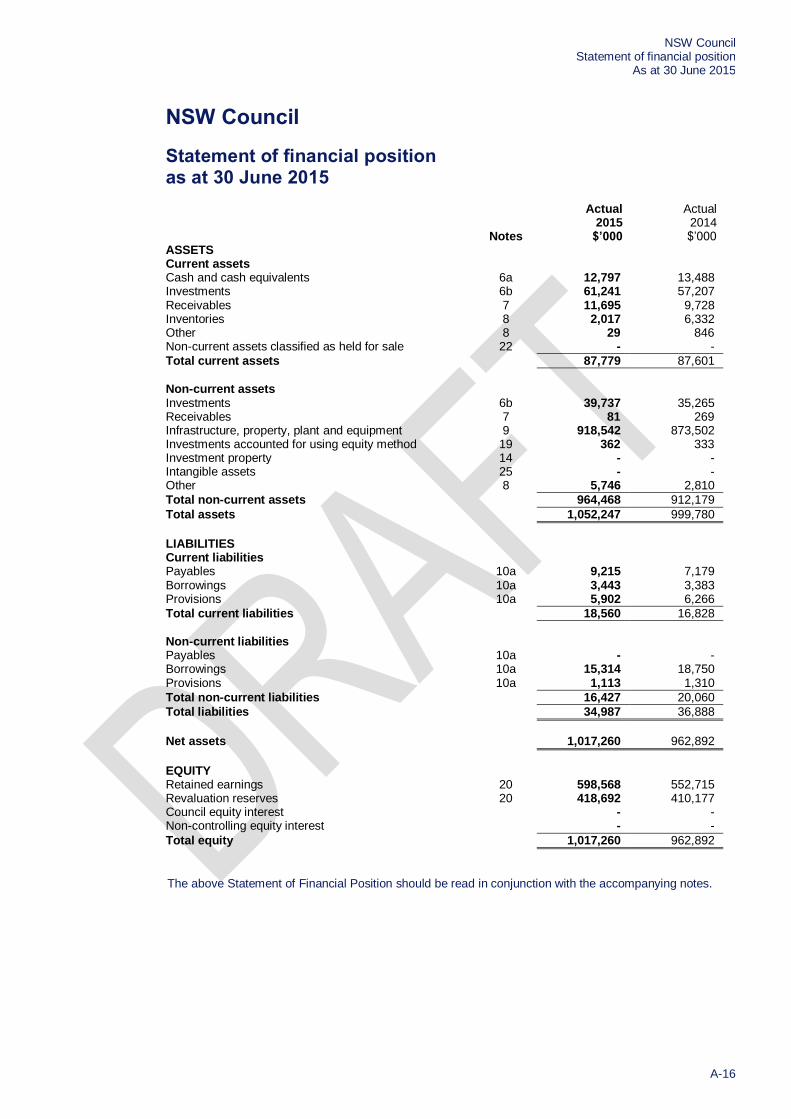

NSW Council

Statement of financial position as at 30 June 2015

Notes

Actual 2015 $’000

Actual 2014 $’000

ASSETS Current assets Cash and cash equivalents 6a 12,797 13,488 Investments 6b 61,241 57,207 Receivables 7 11,695 9,728 Inventories 8 2,017 6,332 Other 8 29 846 Non-current assets classified as held for sale 22 - -

Total current assets 87,779 87,601

Non-current assets Investments 6b 39,737 35,265 Receivables 7 81 269 Infrastructure, property, plant and equipment 9 918,542 873,502 Investments accounted for using equity method 19 362 333 Investment property 14 - - Intangible assets 25 - - Other 8 5,746 2,810

Total non-current assets 964,468 912,179

Total assets 1,052,247 999,780

LIABILITIES Current liabilities Payables 10a 9,215 7,179 Borrowings 10a 3,443 3,383 Provisions 10a 5,902 6,266

Total current liabilities 18,560 16,828

Non-current liabilities Payables 10a - - Borrowings 10a 15,314 18,750 Provisions 10a 1,113 1,310

Total non-current liabilities 16,427 20,060

Total liabilities 34,987 36,888

Net assets 1,017,260 962,892

EQUITY Retained earnings 20 598,568 552,715 Revaluation reserves 20 418,692 410,177 Council equity interest - - Non-controlling equity interest - -

Total equity 1,017,260 962,892

The above Statement of Financial Position should be read in conjunction with the accompanying notes.

NSW Council Statement of financial position As at 30 June 2015 (continued)

A-17

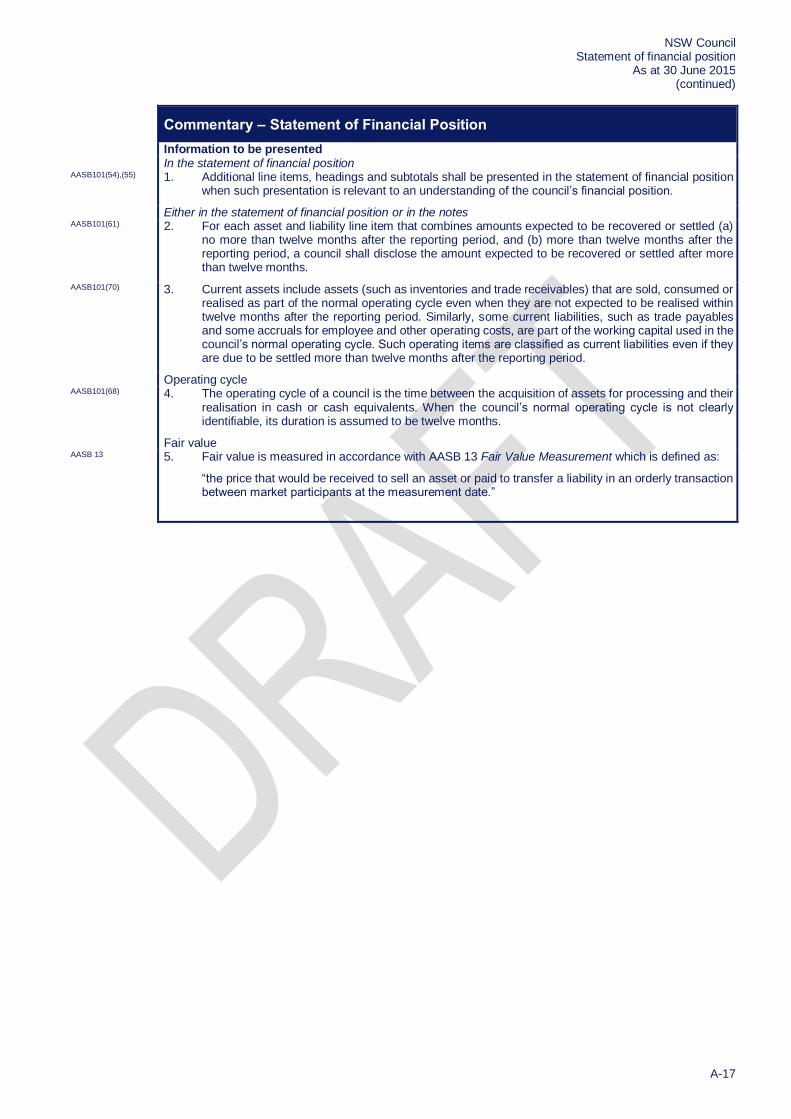

Commentary – Statement of Financial Position

Information to be presented In the statement of financial position AASB101(54),(55) 1. Additional line items, headings and subtotals shall be presented in the statement of financial position

when such presentation is relevant to an understanding of the council’s financial position.

Either in the statement of financial position or in the notes AASB101(61) 2. For each asset and liability line item that combines amounts expected to be recovered or settled (a)

no more than twelve months after the reporting period, and (b) more than twelve months after the reporting period, a council shall disclose the amount expected to be recovered or settled after more than twelve months.

AASB101(70) 3. Current assets include assets (such as inventories and trade receivables) that are sold, consumed or realised as part of the normal operating cycle even when they are not expected to be realised within twelve months after the reporting period. Similarly, some current liabilities, such as trade payables and some accruals for employee and other operating costs, are part of the working capital used in the council’s normal operating cycle. Such operating items are classified as current liabilities even if they are due to be settled more than twelve months after the reporting period.

Operating cycle AASB101(68) 4. The operating cycle of a council is the time between the acquisition of assets for processing and their

realisation in cash or cash equivalents. When the council’s normal operating cycle is not clearly identifiable, its duration is assumed to be twelve months.

Fair value AASB 13 5. Fair value is measured in accordance with AASB 13 Fair Value Measurement which is defined as:

“the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

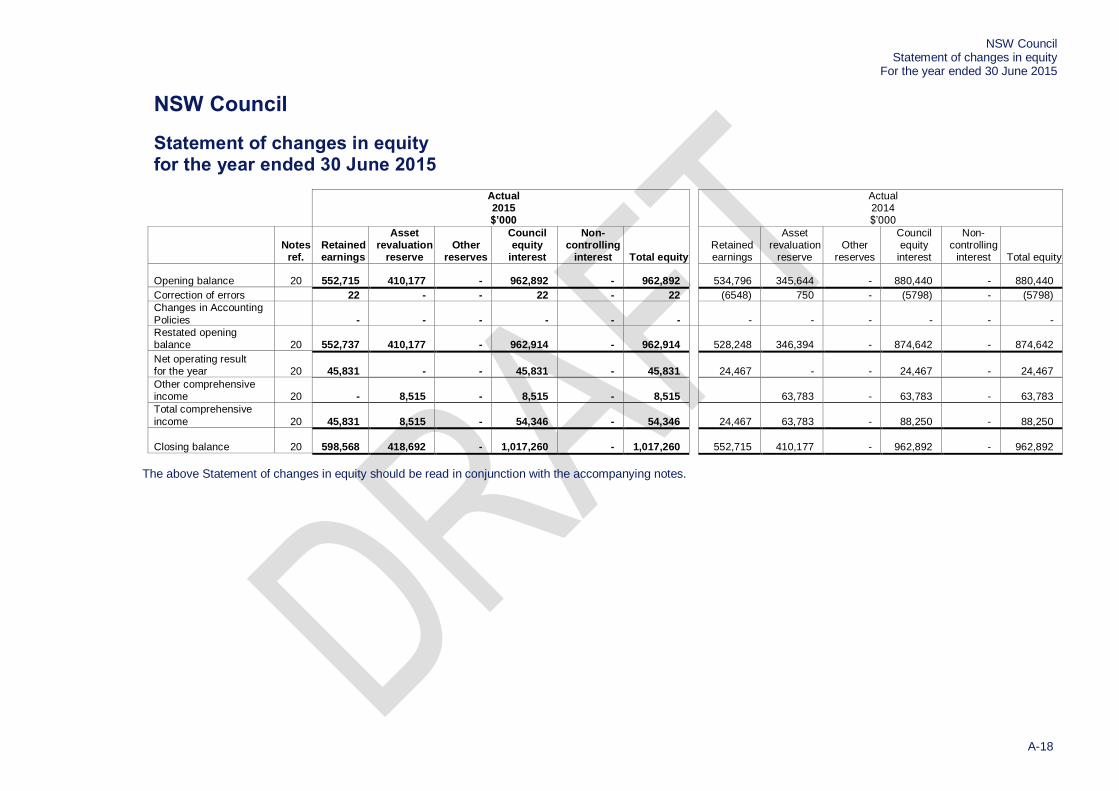

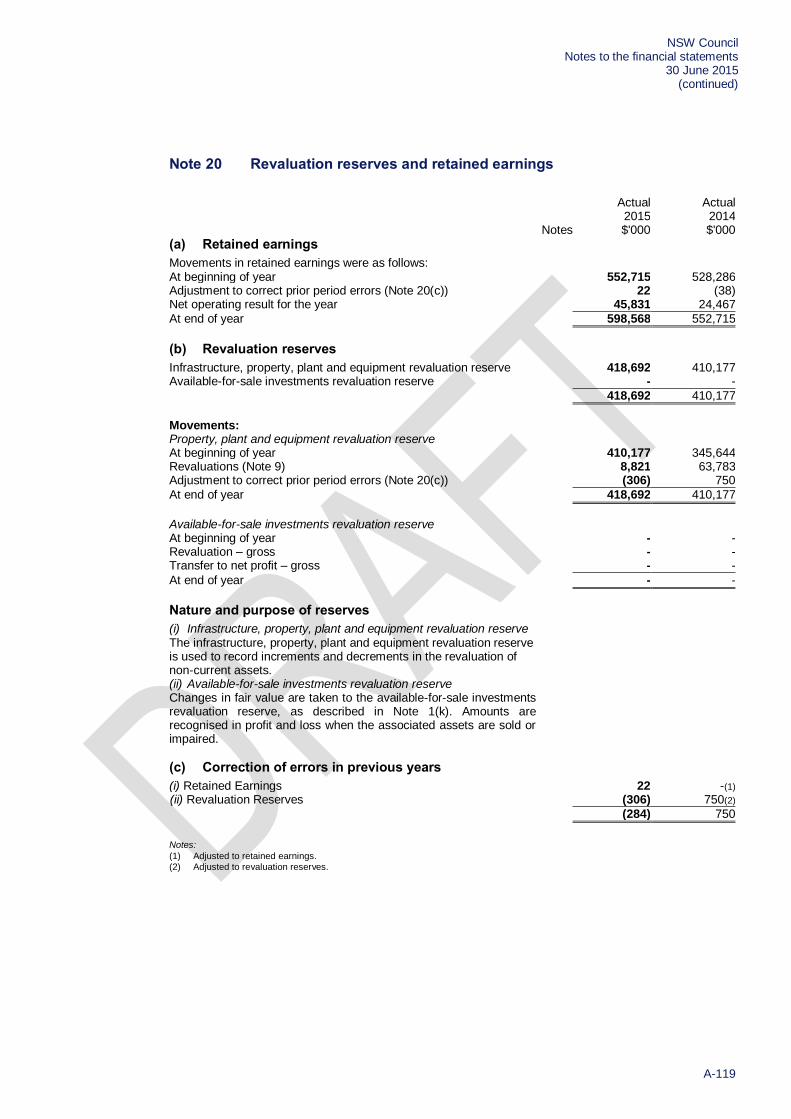

NSW Council Statement of changes in equity For the year ended 30 June 2015

A-18

NSW Council

Statement of changes in equity for the year ended 30 June 2015

Actual 2015 $’000

Actual 2014 $’000

Notes

ref. Retained earnings

Asset revaluation

reserve Other

reserves

Council equity

interest

Non-controlling

interest Total equity Retained earnings

Asset revaluation

reserve Other

reserves

Council equity

interest

Non-controlling

interest Total equity

Opening balance 20 552,715 410,177 - 962,892 - 962,892 534,796 345,644 - 880,440 - 880,440 Correction of errors 22 - - 22 - 22 (6548) 750 - (5798) - (5798) Changes in Accounting

Policies - - - - - - - - - - - - Restated opening

balance 20 552,737 410,177 - 962,914 - 962,914 528,248 346,394 - 874,642 - 874,642 Net operating result

for the year 20 45,831 - - 45,831 - 45,831 24,467 - - 24,467 - 24,467 Other comprehensive

income 20 - 8,515 - 8,515 - 8,515 63,783 - 63,783 - 63,783 Total comprehensive

income 20 45,831 8,515 - 54,346 - 54,346 24,467 63,783 - 88,250 - 88,250

Closing balance 20 598,568 418,692 - 1,017,260 - 1,017,260 552,715 410,177 - 962,892 - 962,892

The above Statement of changes in equity should be read in conjunction with the accompanying notes.

NSW Council Statement of changes in equity For the year ended 30 June 2015

(continued)

A-19

Commentary – Statements of changes in equity

AASB101(106) 1. The statement of changes in equity shall include: (a) total comprehensive income for the period, showing separately the total amounts attributable

to owners of the parent and to non controlling interests (b)

for each component of equity, the effects of retrospective application or retrospective restatement recognised in accordance with AASB 108

AASB101(106)(d) (c)

for each component of equity, a reconciliation between the carrying amount at the beginning and the end of the period, separately disclosing changes resulting from:

(i) profit or loss (ii) other comprehensive income, and (iii) transactions with owners in their capacity as owners, showing separately

contributions by and distributions to owners and changes in ownership interests in subsidiaries that do not result in loss of control.

AASB101(108) 2. Components of equity include each class of contributed equity, the accumulated balance of each class of other comprehensive income and retained earnings.

AASB101(106A) 3. The reconciliation of changes in each component of equity shall also show separately each item of comprehensive income. However, this information may be presented either in the notes or in the statement of changes in equity. NSW Council has elected to provide the detailed information in note 20.

Presentation of dividends AASB101(107) 4. The amount of dividends recognised as distributions to owners during the period must be disclosed

either in the statement of changes in equity or in the notes.

NSW Council Contents of the notes to the financial statements 30 June 2015

A-20

NSW Council

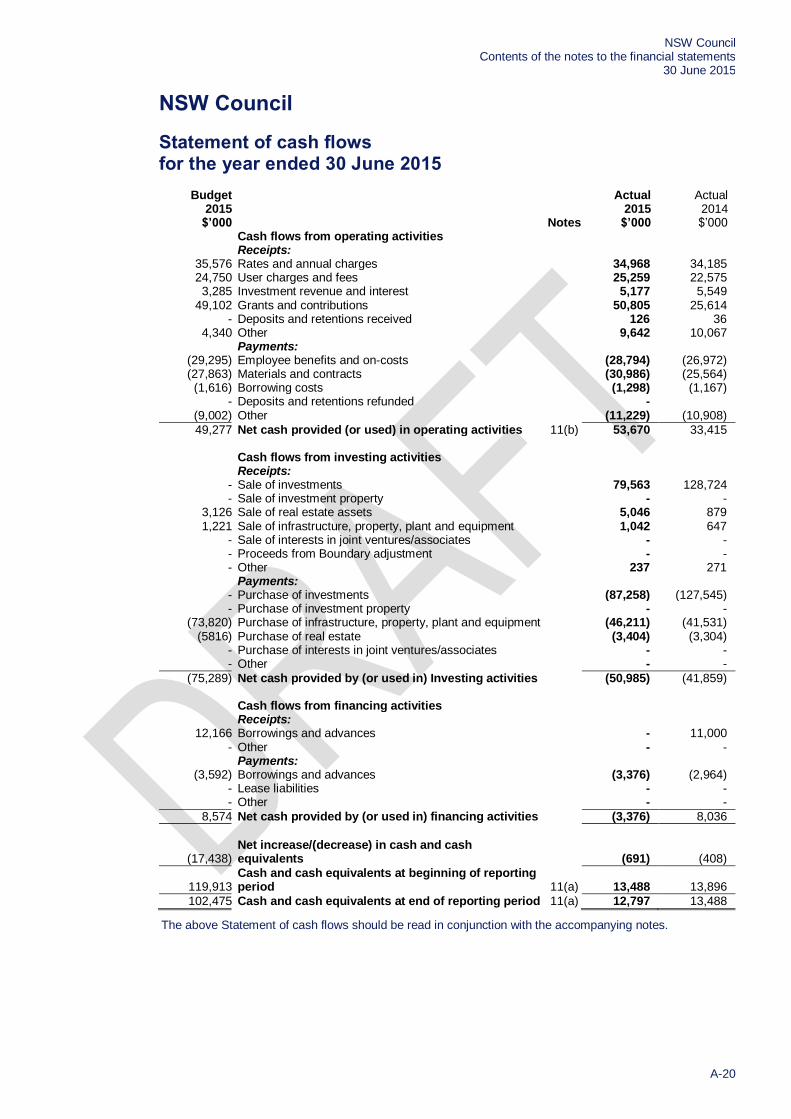

Statement of cash flows for the year ended 30 June 2015

Budget 2015 $’000 Notes

Actual 2015 $’000

Actual 2014 $’000

Cash flows from operating activities Receipts: 35,576 Rates and annual charges 34,968 34,185 24,750 User charges and fees 25,259 22,575 3,285 Investment revenue and interest 5,177 5,549 49,102 Grants and contributions 50,805 25,614 - Deposits and retentions received 126 36 4,340 Other 9,642 10,067 Payments: (29,295) Employee benefits and on-costs (28,794) (26,972) (27,863) Materials and contracts (30,986) (25,564) (1,616) Borrowing costs (1,298) (1,167) - Deposits and retentions refunded - (9,002) Other (11,229) (10,908)

49,277 Net cash provided (or used) in operating activities 11(b) 53,670 33,415 Cash flows from investing activities Receipts: - Sale of investments 79,563 128,724 - Sale of investment property - - 3,126 Sale of real estate assets 5,046 879 1,221 Sale of infrastructure, property, plant and equipment 1,042 647 - Sale of interests in joint ventures/associates - - - Proceeds from Boundary adjustment - - - Other 237 271 Payments: - Purchase of investments (87,258) (127,545) - Purchase of investment property - - (73,820) Purchase of infrastructure, property, plant and equipment (46,211) (41,531) (5816) Purchase of real estate (3,404) (3,304) - Purchase of interests in joint ventures/associates - - - Other - -

(75,289) Net cash provided by (or used in) Investing activities (50,985) (41,859) Cash flows from financing activities Receipts: 12,166 Borrowings and advances - 11,000 - Other - - Payments: (3,592) Borrowings and advances (3,376) (2,964) - Lease liabilities - - - Other - -

8,574 Net cash provided by (or used in) financing activities (3,376) 8,036

(17,438)

Net increase/(decrease) in cash and cash equivalents (691) (408)

119,913

Cash and cash equivalents at beginning of reporting period 11(a) 13,488 13,896

102,475 Cash and cash equivalents at end of reporting period 11(a) 12,797 13,488

The above Statement of cash flows should be read in conjunction with the accompanying notes.

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-21

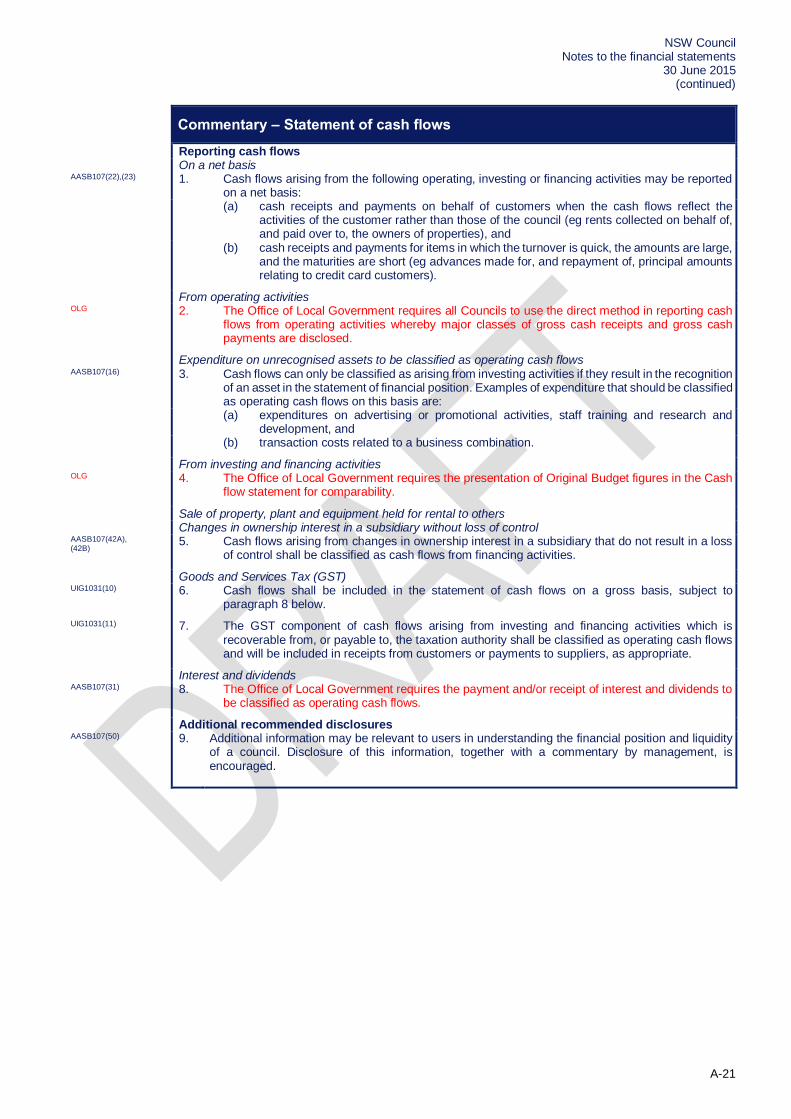

Commentary – Statement of cash flows

Reporting cash flows On a net basis AASB107(22),(23) 1. Cash flows arising from the following operating, investing or financing activities may be reported

on a net basis: (a) cash receipts and payments on behalf of customers when the cash flows reflect the

activities of the customer rather than those of the council (eg rents collected on behalf of, and paid over to, the owners of properties), and

(b) cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are short (eg advances made for, and repayment of, principal amounts relating to credit card customers).

From operating activities OLG 2. The Office of Local Government requires all Councils to use the direct method in reporting cash

flows from operating activities whereby major classes of gross cash receipts and gross cash payments are disclosed.

Expenditure on unrecognised assets to be classified as operating cash flows AASB107(16) 3. Cash flows can only be classified as arising from investing activities if they result in the recognition

of an asset in the statement of financial position. Examples of expenditure that should be classified as operating cash flows on this basis are:

(a) expenditures on advertising or promotional activities, staff training and research and development, and

(b) transaction costs related to a business combination.

From investing and financing activities OLG 4. The Office of Local Government requires the presentation of Original Budget figures in the Cash

flow statement for comparability.

Sale of property, plant and equipment held for rental to others Changes in ownership interest in a subsidiary without loss of control AASB107(42A), (42B)

5. Cash flows arising from changes in ownership interest in a subsidiary that do not result in a loss of control shall be classified as cash flows from financing activities.

Goods and Services Tax (GST) UIG1031(10) 6. Cash flows shall be included in the statement of cash flows on a gross basis, subject to

paragraph 8 below.

UIG1031(11) 7. The GST component of cash flows arising from investing and financing activities which is recoverable from, or payable to, the taxation authority shall be classified as operating cash flows and will be included in receipts from customers or payments to suppliers, as appropriate.

Interest and dividends AASB107(31) 8. The Office of Local Government requires the payment and/or receipt of interest and dividends to

be classified as operating cash flows.

Additional recommended disclosures AASB107(50) 9. Additional information may be relevant to users in understanding the financial position and liquidity

of a council. Disclosure of this information, together with a commentary by management, is encouraged.

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-22

NSW Council

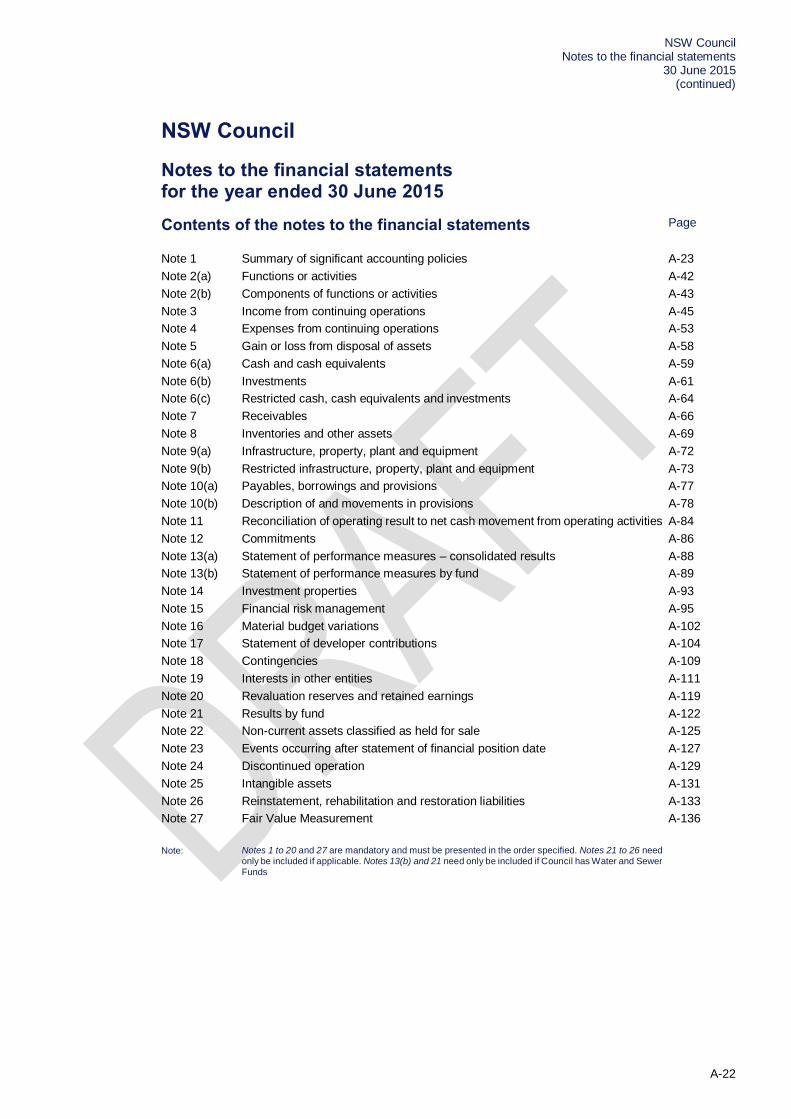

Notes to the financial statements for the year ended 30 June 2015

Contents of the notes to the financial statements Page

Note 1 Summary of significant accounting policies A-23

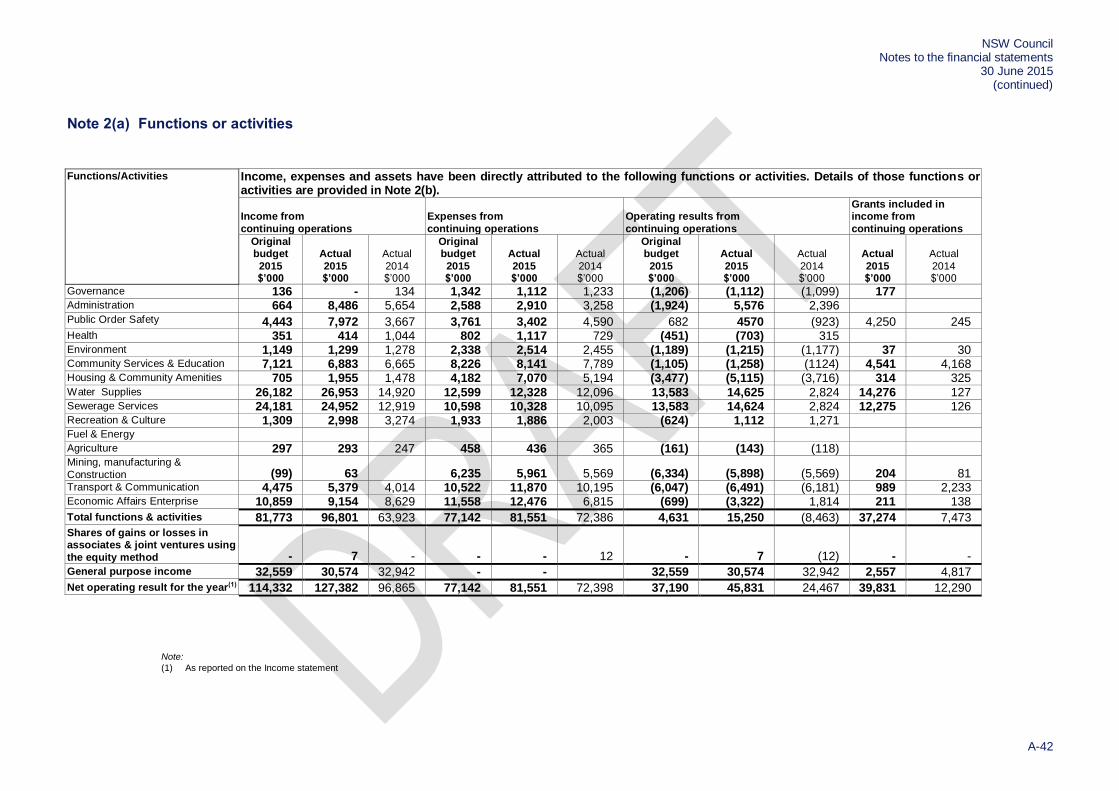

Note 2(a) Functions or activities A-42

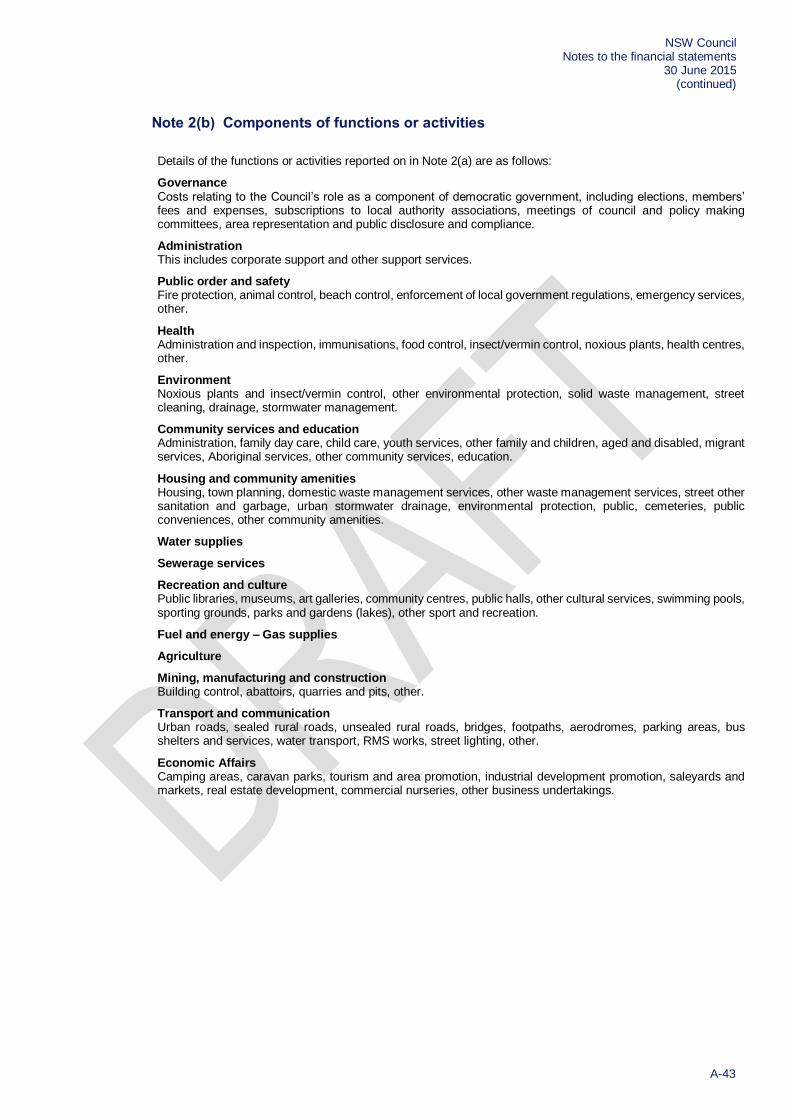

Note 2(b) Components of functions or activities A-43

Note 3 Income from continuing operations A-45

Note 4 Expenses from continuing operations A-53

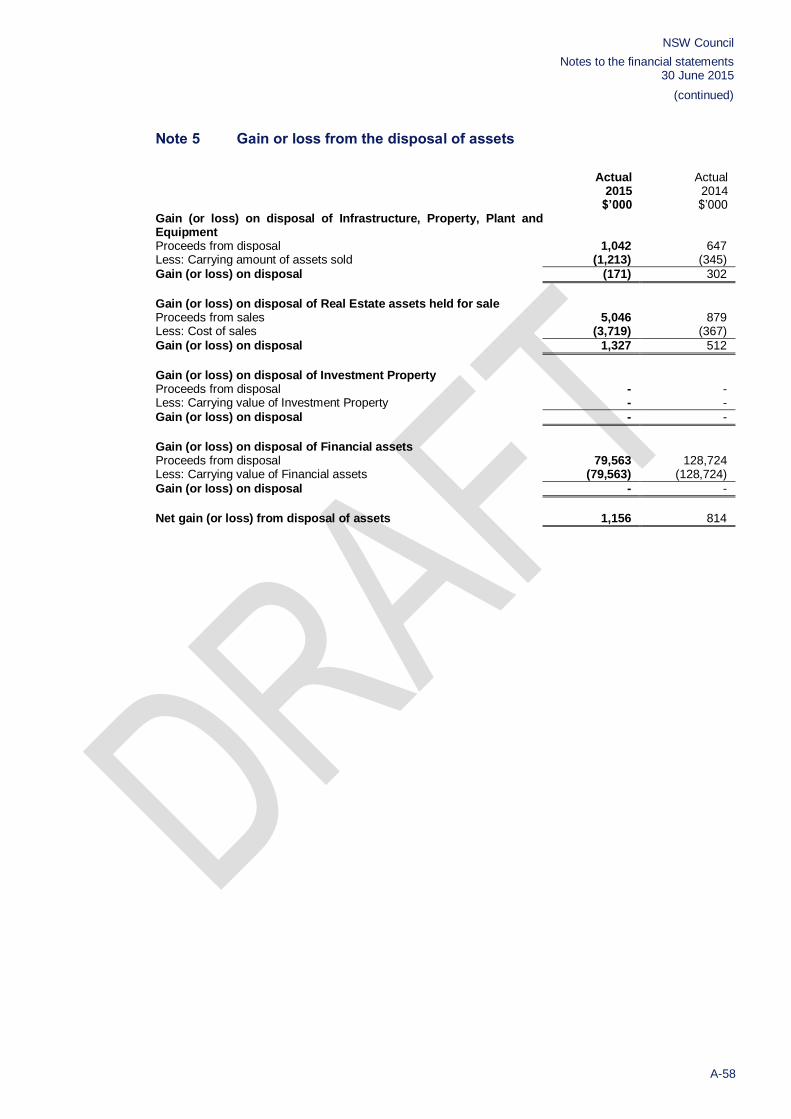

Note 5 Gain or loss from disposal of assets A-58

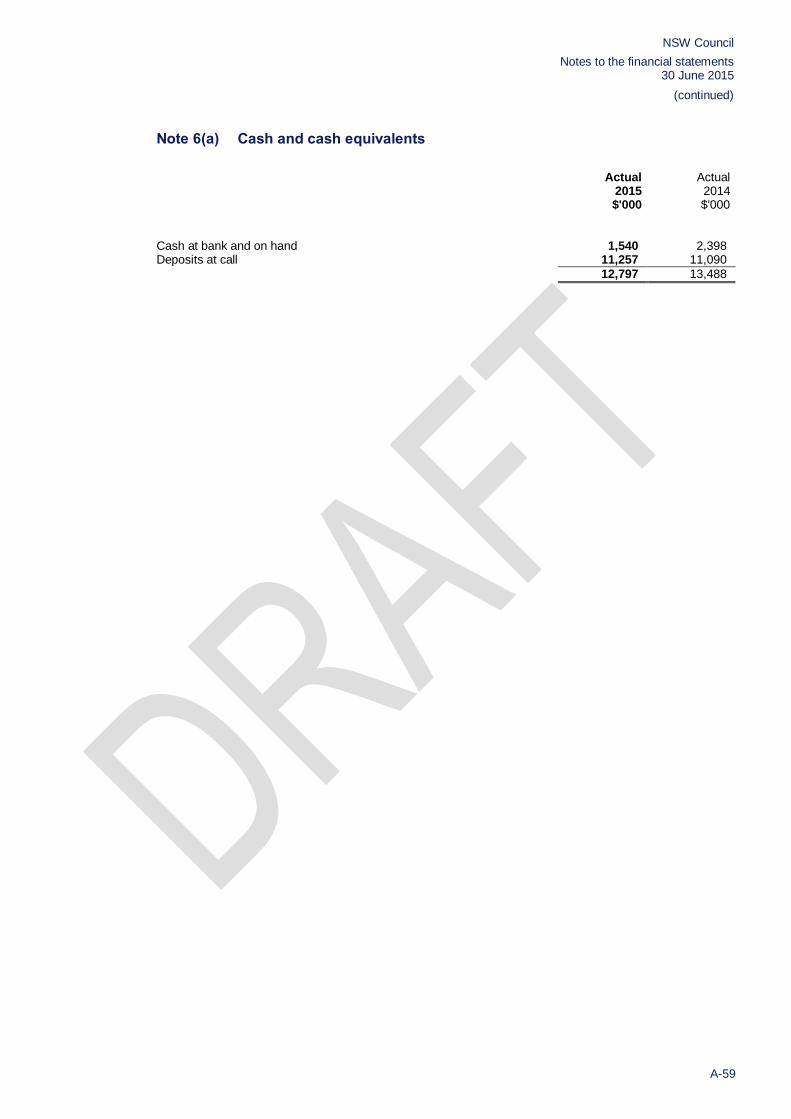

Note 6(a) Cash and cash equivalents A-59

Note 6(b) Investments A-61

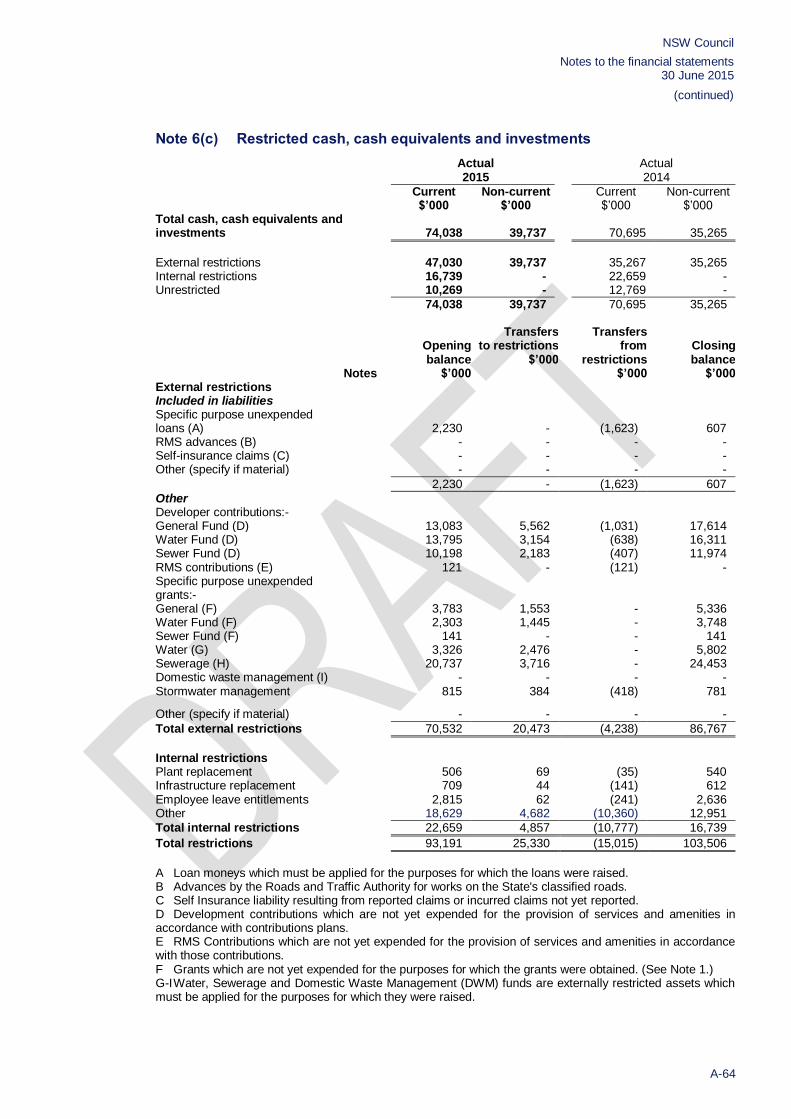

Note 6(c) Restricted cash, cash equivalents and investments A-64

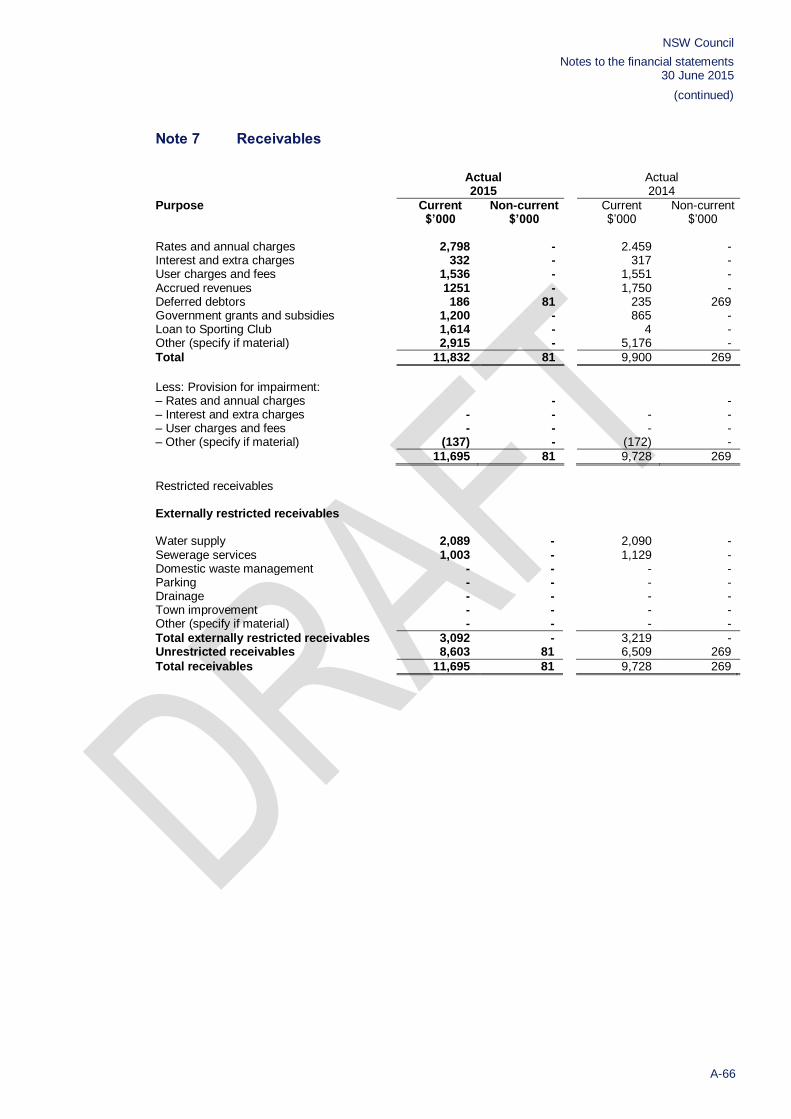

Note 7 Receivables A-66

Note 8 Inventories and other assets A-69

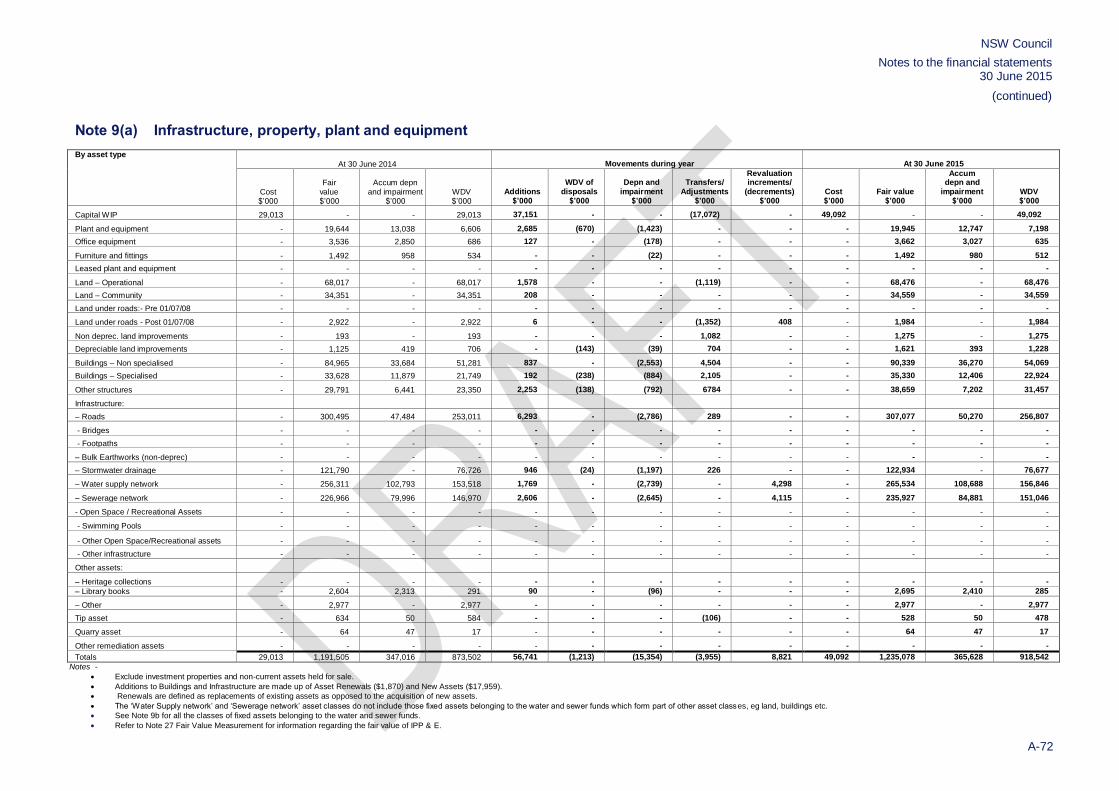

Note 9(a) Infrastructure, property, plant and equipment A-72

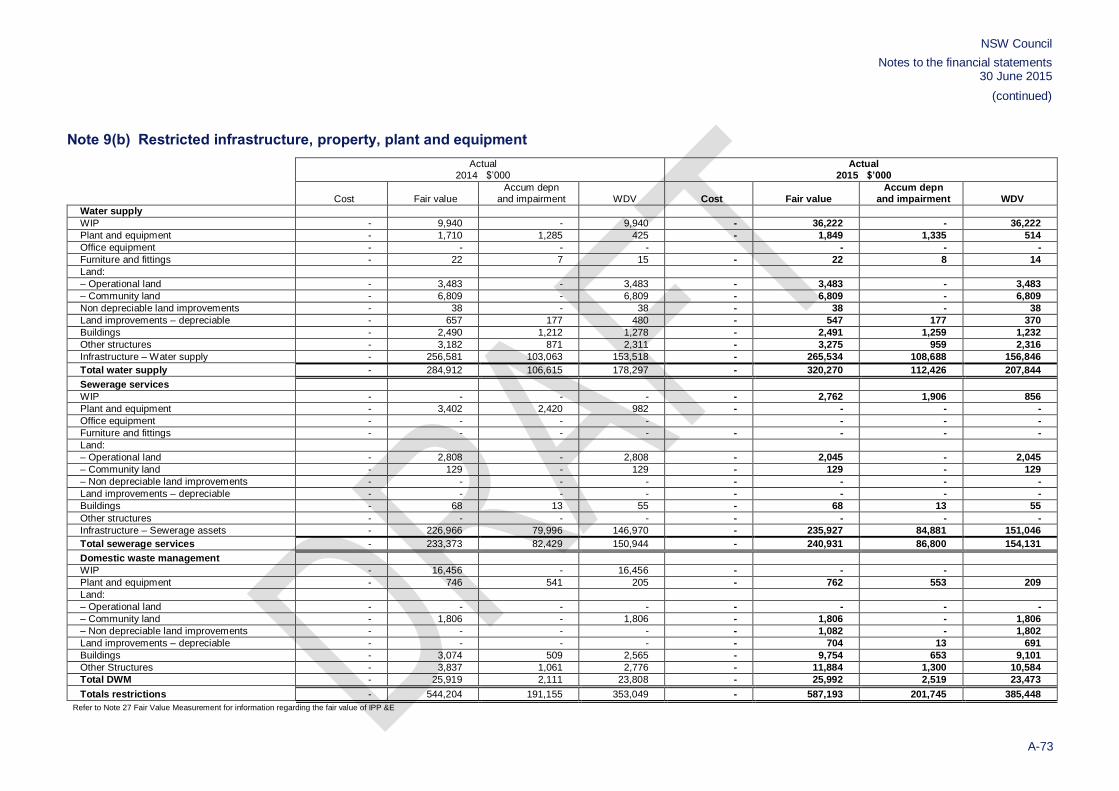

Note 9(b) Restricted infrastructure, property, plant and equipment A-73

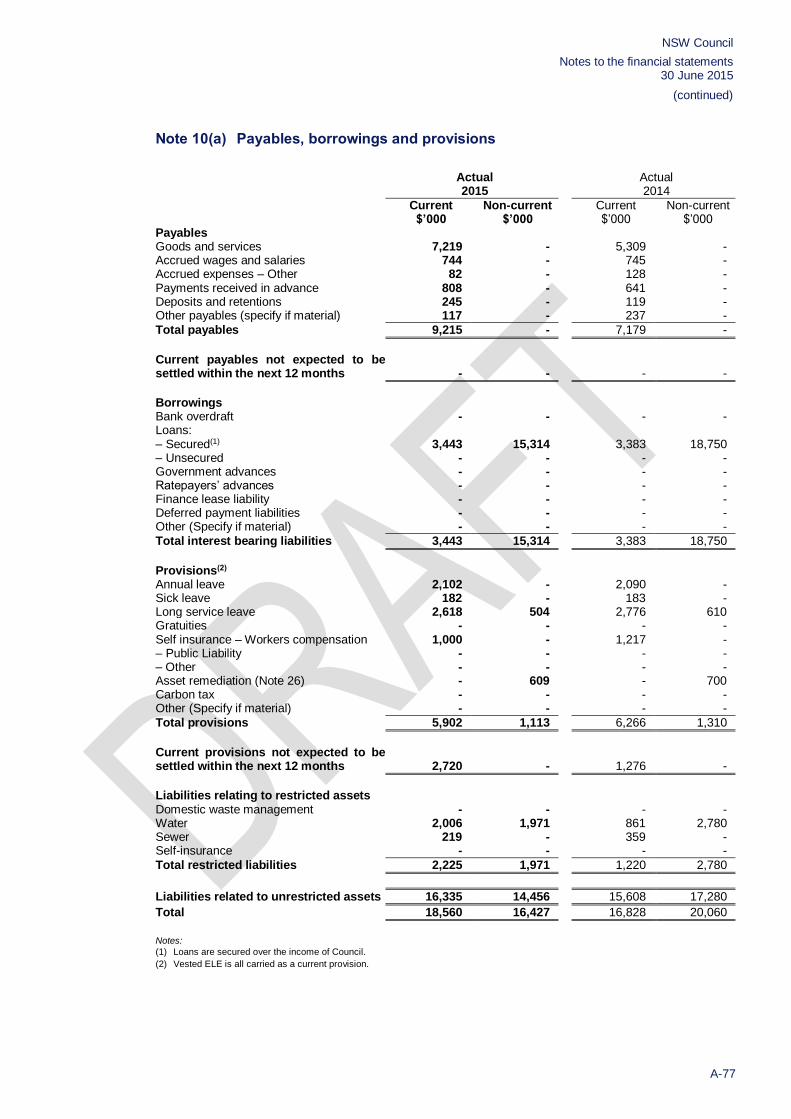

Note 10(a) Payables, borrowings and provisions A-77

Note 10(b) Description of and movements in provisions A-78

Note 11 Reconciliation of operating result to net cash movement from operating activities A-84

Note 12 Commitments A-86

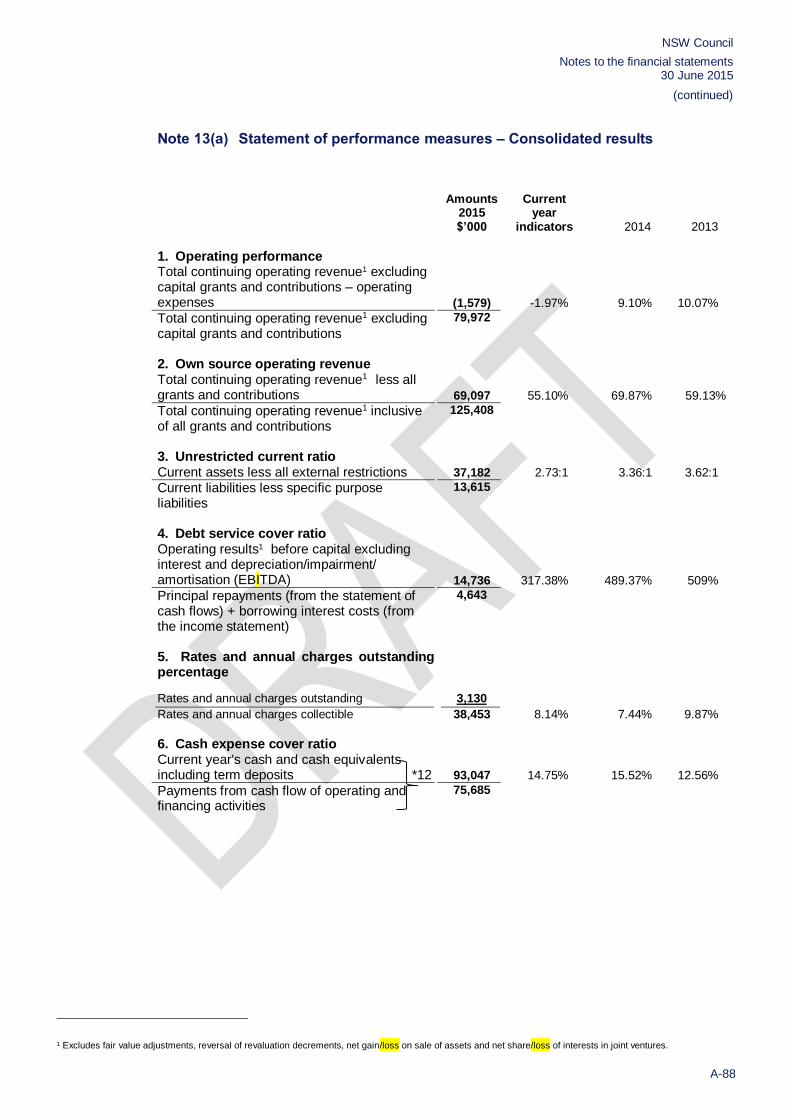

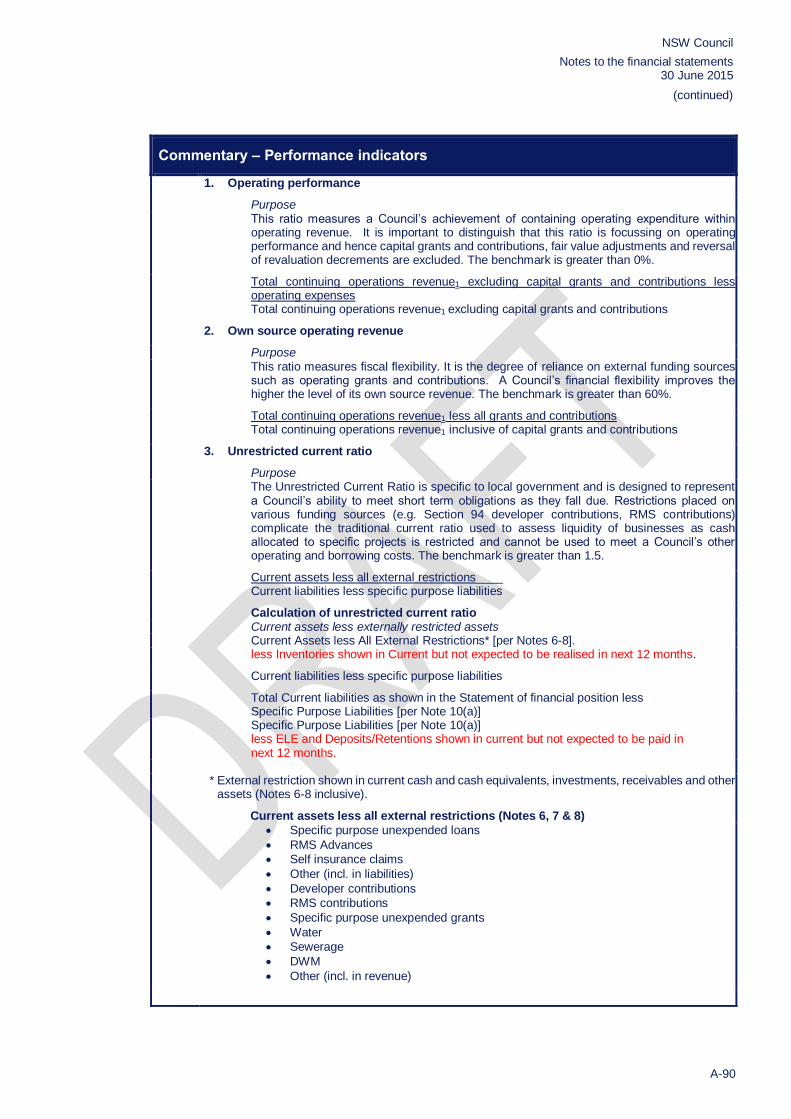

Note 13(a) Statement of performance measures – consolidated results A-88

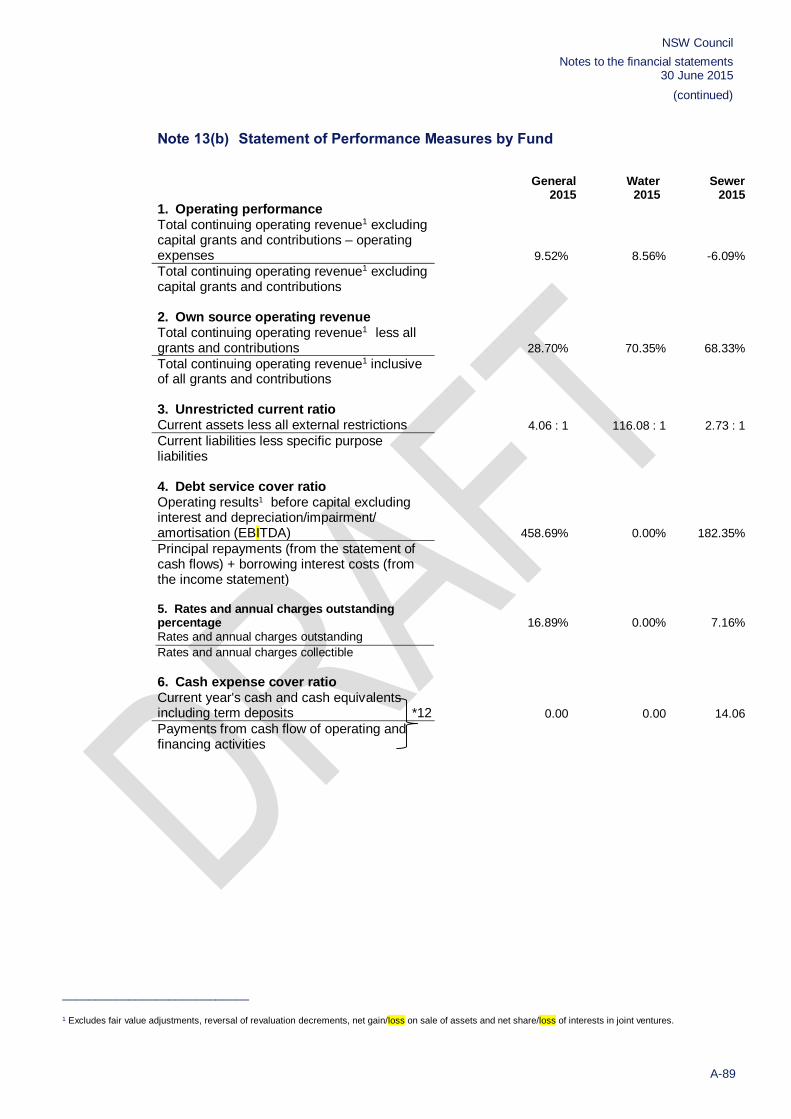

Note 13(b) Statement of performance measures by fund A-89

Note 14 Investment properties A-93

Note 15 Financial risk management A-95

Note 16 Material budget variations A-102

Note 17 Statement of developer contributions A-104

Note 18 Contingencies A-109

Note 19 Interests in other entities A-111

Note 20 Revaluation reserves and retained earnings A-119

Note 21 Results by fund A-122

Note 22 Non-current assets classified as held for sale A-125

Note 23 Events occurring after statement of financial position date A-127

Note 24 Discontinued operation A-129

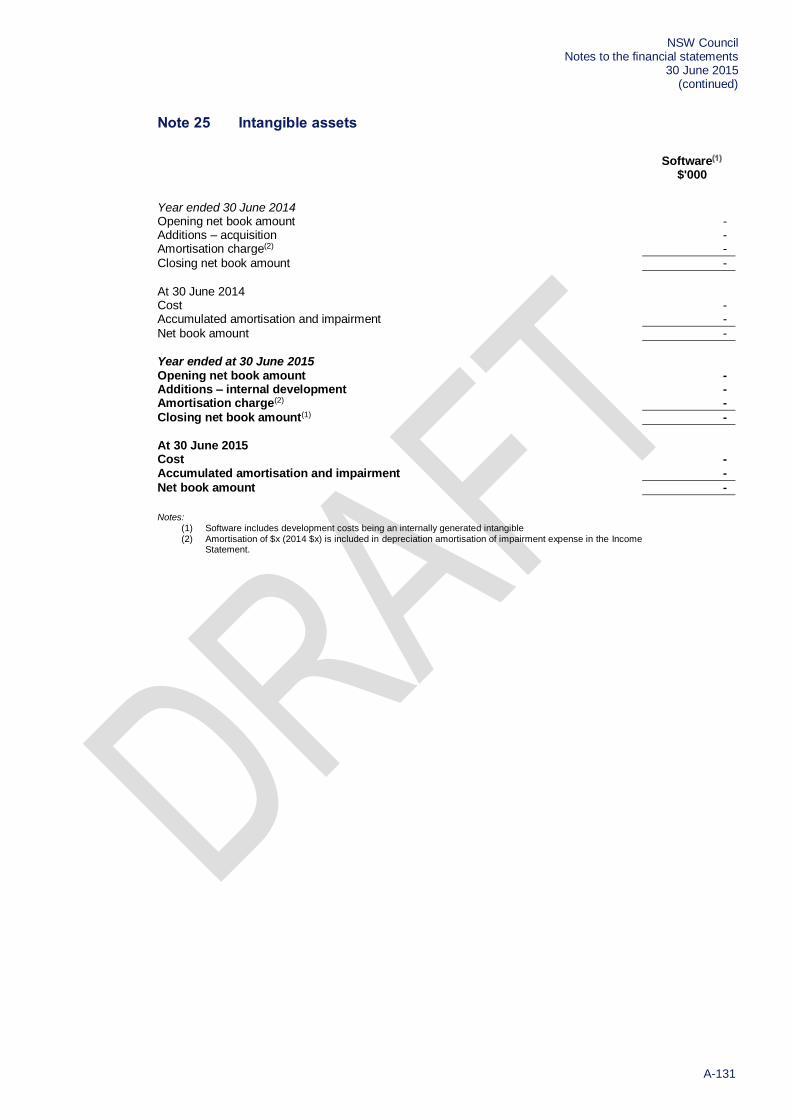

Note 25 Intangible assets A-131

Note 26 Reinstatement, rehabilitation and restoration liabilities A-133

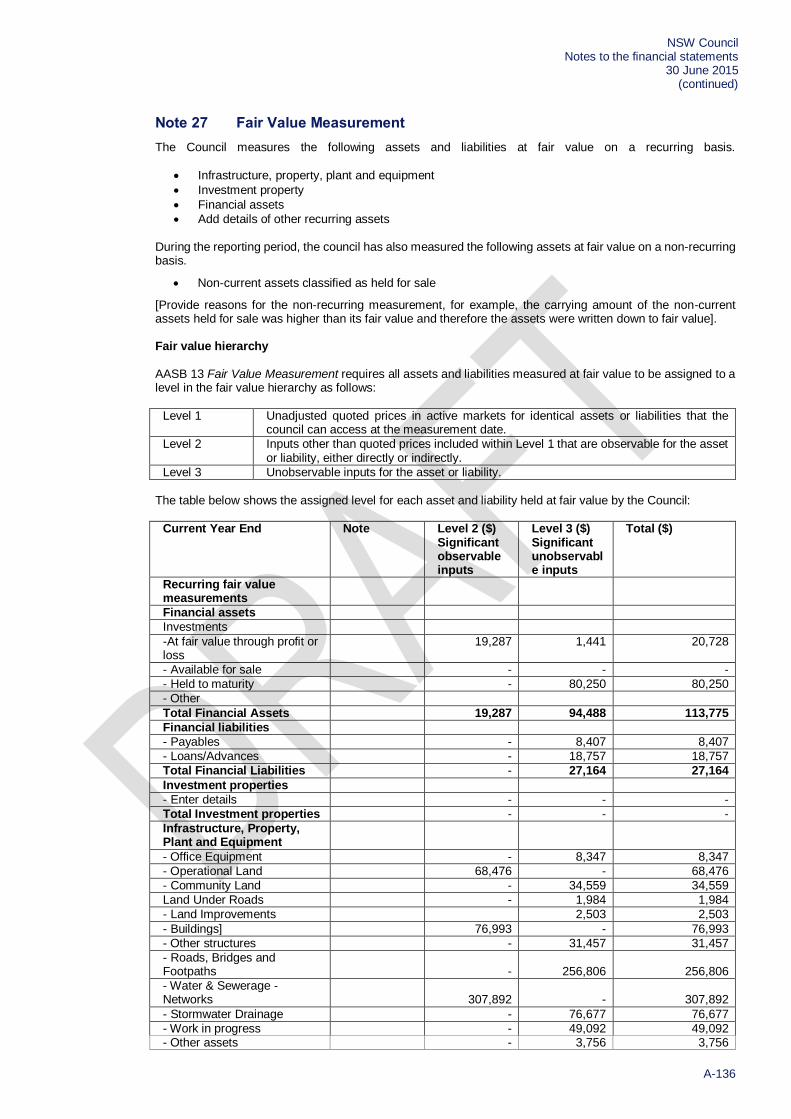

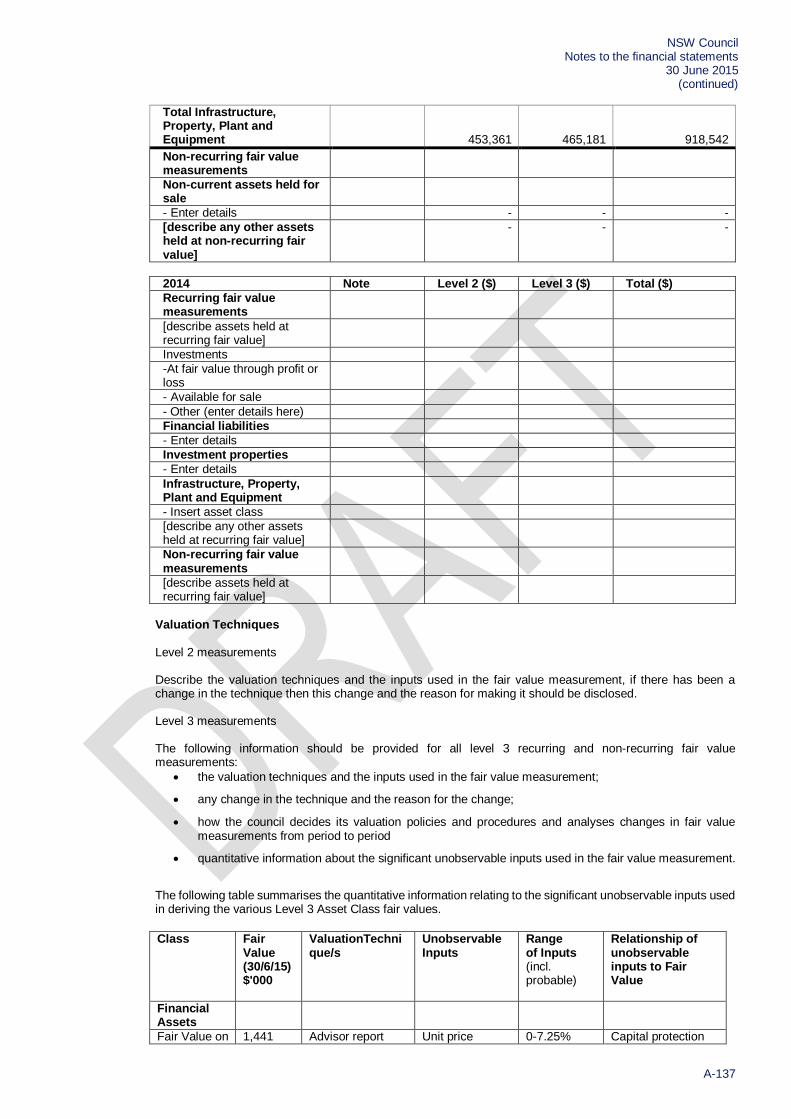

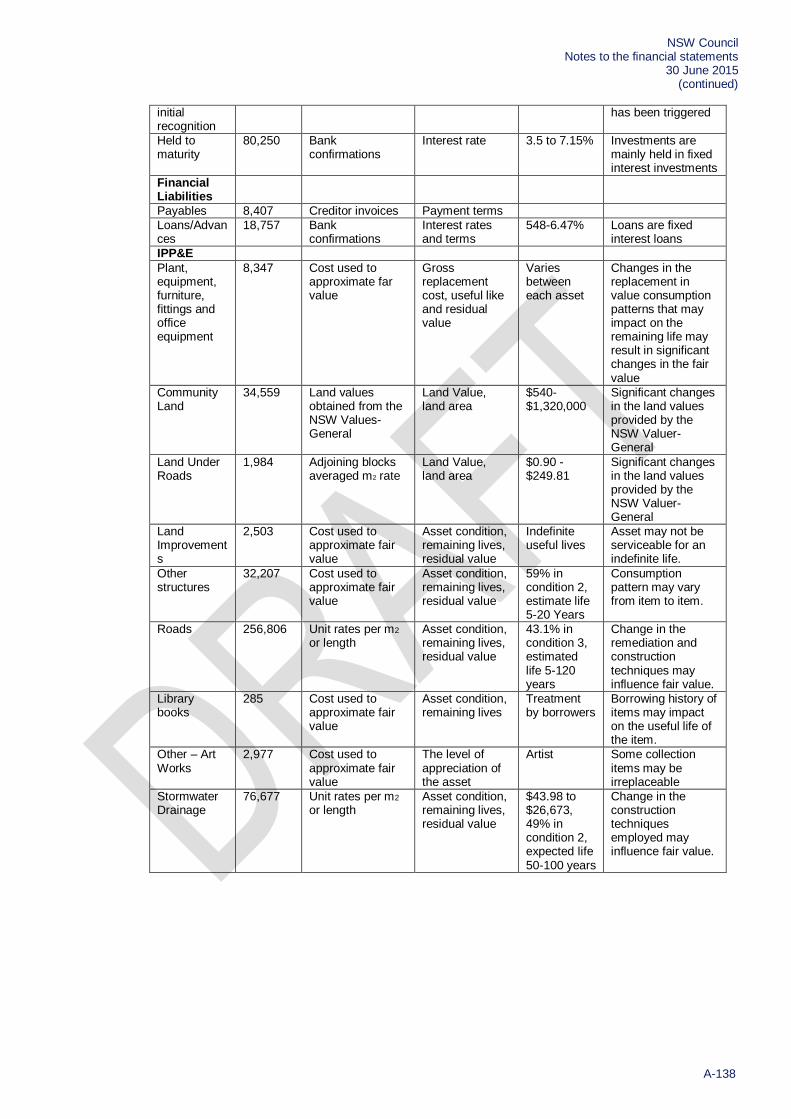

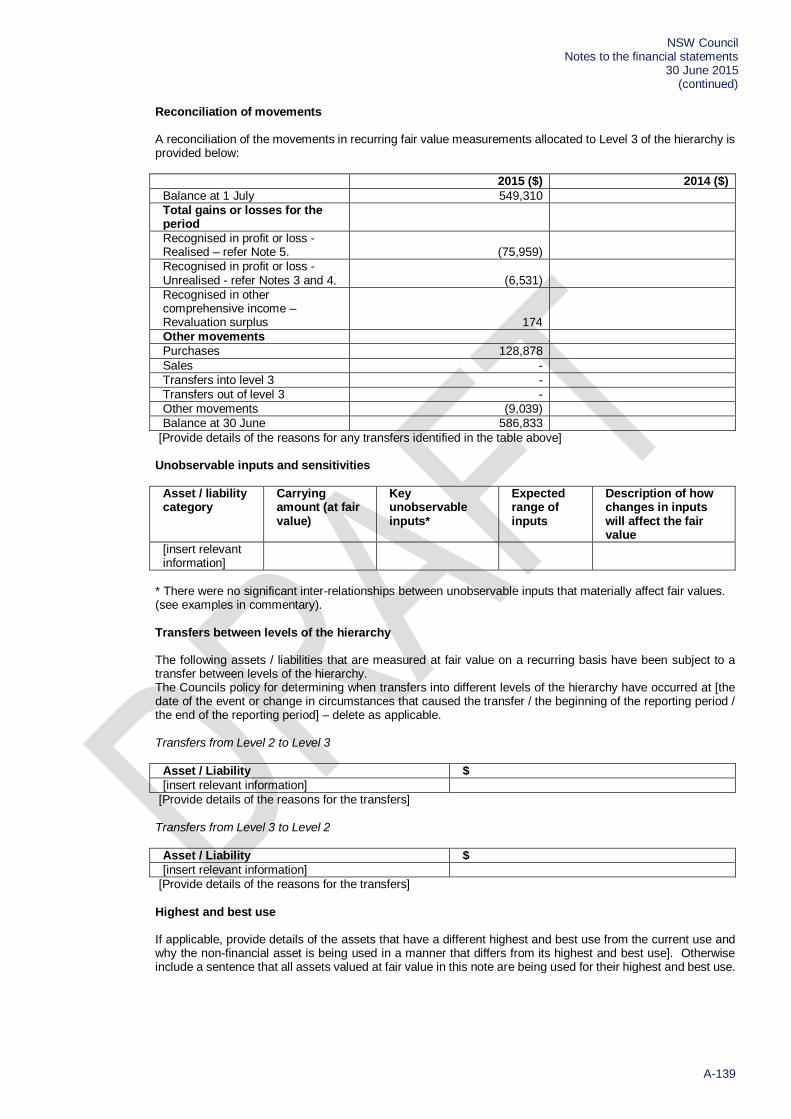

Note 27 Fair Value Measurement A-136

Note: Notes 1 to 20 and 27 are mandatory and must be presented in the order specified. Notes 21 to 26 need only be included if applicable. Notes 13(b) and 21 need only be included if Council has Water and Sewer Funds

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-23

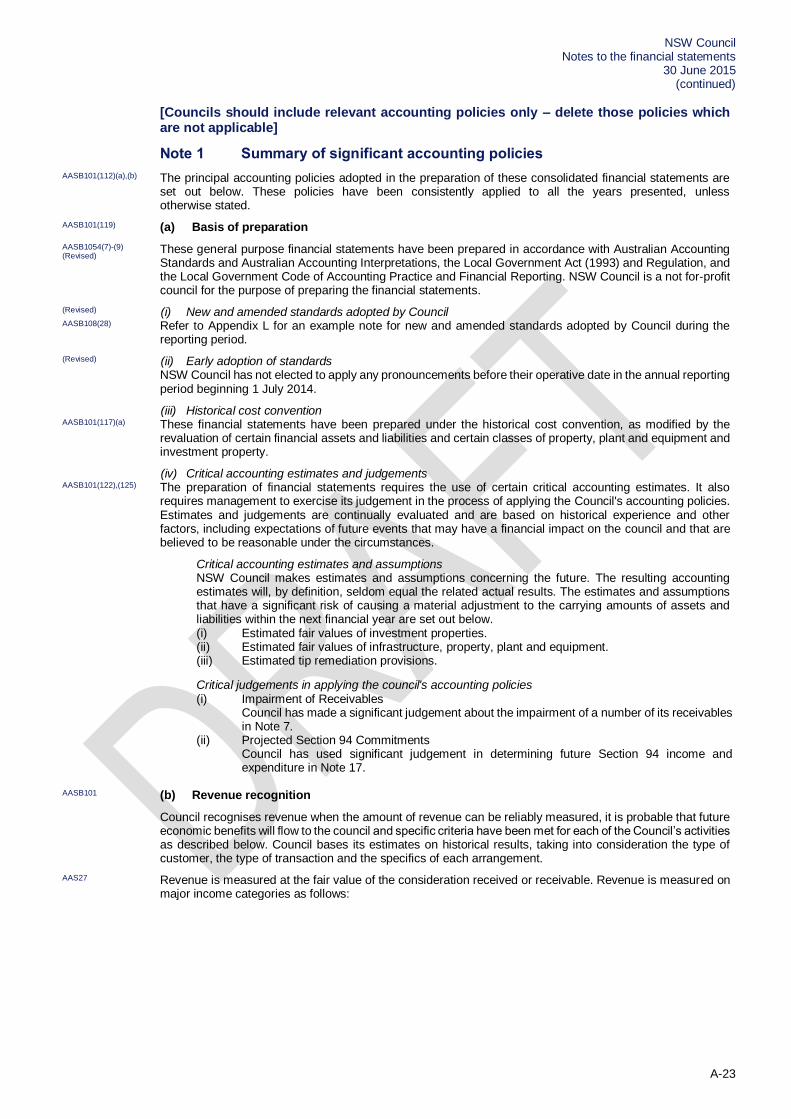

[Councils should include relevant accounting policies only – delete those policies which are not applicable]

Note 1 Summary of significant accounting policies

AASB101(112)(a),(b) The principal accounting policies adopted in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

AASB101(119) (a) Basis of preparation

AASB1054(7)-(9) (Revised)

These general purpose financial statements have been prepared in accordance with Australian Accounting Standards and Australian Accounting Interpretations, the Local Government Act (1993) and Regulation, and the Local Government Code of Accounting Practice and Financial Reporting. NSW Council is a not for-profit council for the purpose of preparing the financial statements.

(Revised) (i) New and amended standards adopted by Council AASB108(28) Refer to Appendix L for an example note for new and amended standards adopted by Council during the

reporting period.

(Revised) (ii) Early adoption of standards NSW Council has not elected to apply any pronouncements before their operative date in the annual reporting

period beginning 1 July 2014.

(iii) Historical cost convention AASB101(117)(a) These financial statements have been prepared under the historical cost convention, as modified by the

revaluation of certain financial assets and liabilities and certain classes of property, plant and equipment and investment property.

(iv) Critical accounting estimates and judgements AASB101(122),(125) The preparation of financial statements requires the use of certain critical accounting estimates. It also

requires management to exercise its judgement in the process of applying the Council's accounting policies. Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of future events that may have a financial impact on the council and that are believed to be reasonable under the circumstances.

Critical accounting estimates and assumptions NSW Council makes estimates and assumptions concerning the future. The resulting accounting

estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are set out below.

(i) Estimated fair values of investment properties. (ii) Estimated fair values of infrastructure, property, plant and equipment. (iii) Estimated tip remediation provisions. Critical judgements in applying the council's accounting policies (i) Impairment of Receivables Council has made a significant judgement about the impairment of a number of its receivables

in Note 7. (ii) Projected Section 94 Commitments Council has used significant judgement in determining future Section 94 income and

expenditure in Note 17. AASB101 (b) Revenue recognition

Council recognises revenue when the amount of revenue can be reliably measured, it is probable that future economic benefits will flow to the council and specific criteria have been met for each of the Council’s activities as described below. Council bases its estimates on historical results, taking into consideration the type of customer, the type of transaction and the specifics of each arrangement.

AAS27 Revenue is measured at the fair value of the consideration received or receivable. Revenue is measured on major income categories as follows:

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-24

Note 1 Summary of significant accounting policies (continued)

(b) Revenue recognition (continued)

(i) Rates, annual charges, grants and contributions Rates, annual charges, grants and contributions (including developer contributions) are recognised as

revenues when the Council obtains control over the assets comprising these receipts. Developer contributions may only be expended for the purposes for which the contributions were required but the Council may apply contributions according to the priorities established in work schedules.

Control over assets acquired from rates and annual charges is obtained at the commencement of the rating year as it is an enforceable debt linked to the rateable property or, where earlier, upon receipt of the rates.

Control over granted assets is normally obtained upon their receipt (or acquittal) or upon earlier notification that a grant has been secured, and is valued at their fair value at the date of transfer.

Revenue is recognised when the Council obtains control of the contribution or the right to receive the contribution, it is probable that the economic benefits comprising the contribution will flow to the Council and the amount of the contribution can be measured reliably.

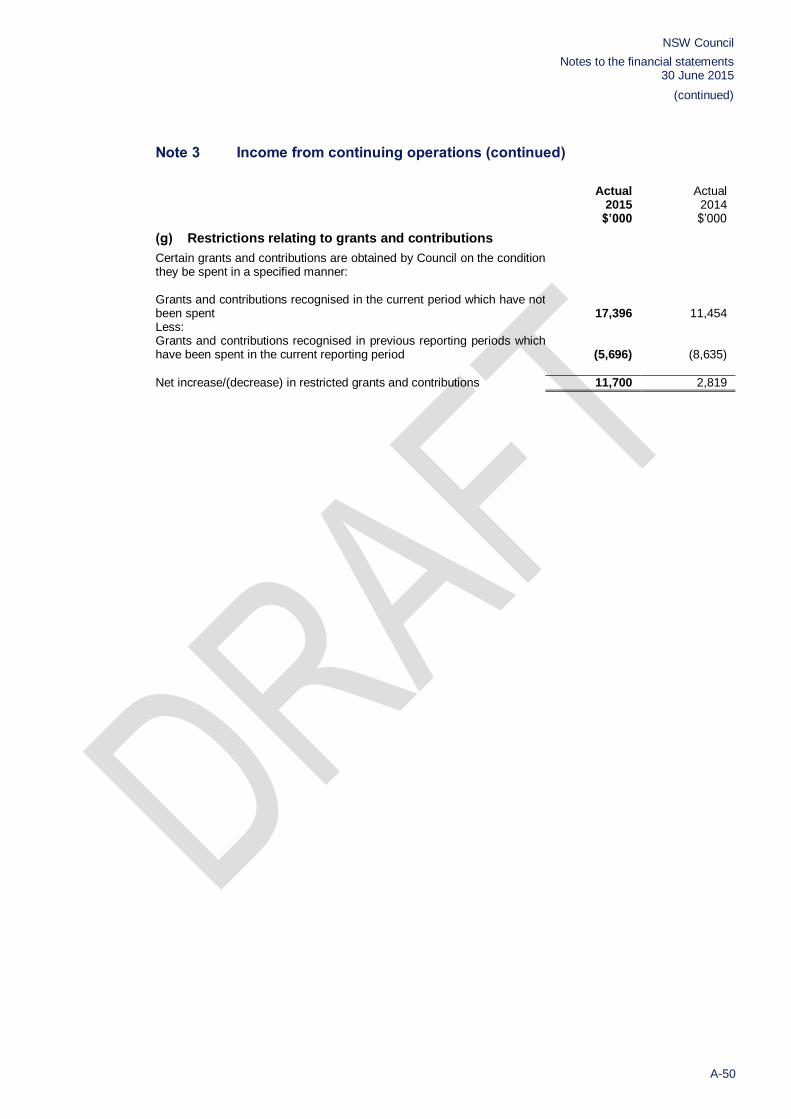

Where grants or contributions recognised as revenues during the financial year were obtained on condition that they be expended in a particular manner or used over a particular period and those conditions were undischarged at reporting date, the unused grant or contribution is disclosed in Note 3(g). The note also discloses the amount of unused grant or contribution from prior years that was expended on Council’s operations during the current year.

A liability is recognised in respect of revenue that is reciprocal in nature to the extent that the requisite service has not been provided at reporting date.

(ii) User charges and fees User charges and fees (including parking fees and fines) are recognised as revenue when the service has

been provided, the payment is received, or when the penalty has been applied, whichever first occurs.

(iii) Sale of plant, property, infrastructure and equipment The profit or loss on sale of an asset is determined when control of the asset has irrevocably passed to the

buyer.

(iv) Interest Interest income is recognised using the effective interest rate at the date that interest is earned.

(v) Rent Rental income is accounted for on a straight-line basis over the lease term.

(vi) Dividend income Revenue is recognised when the Council’s right to receive the payment is established, which is generally

when shareholders approve the dividend.

(vii) Other income Other income is recorded when the payment is due, the value of the payment is notified or the payment is

received, whichever occurs first.

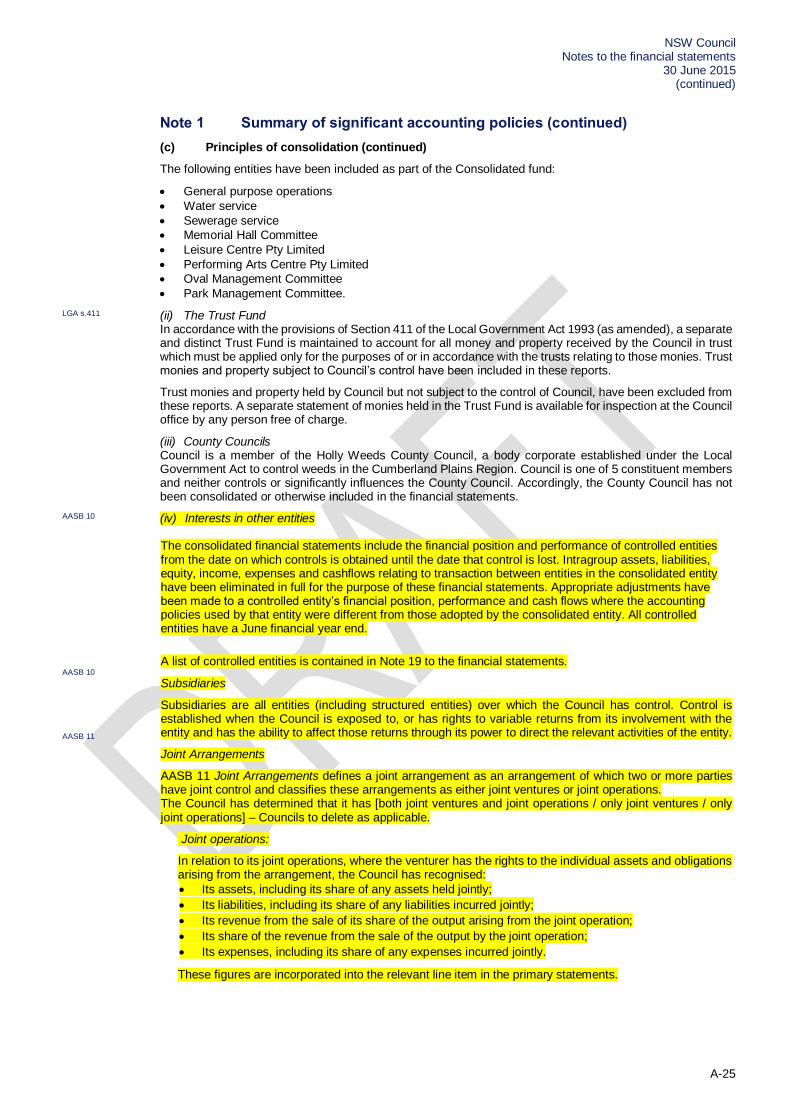

AASB101(110) (c) Principles of consolidation

(i) The Consolidated Fund LGA s.409(1) In accordance with the provisions of Section 409(1) of the LGA 1993, all money and property received by

Council is held in the Council’s Consolidated Fund unless it is required to be held in the Council’s Trust Fund.

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-25

Note 1 Summary of significant accounting policies (continued)

(c) Principles of consolidation (continued)

The following entities have been included as part of the Consolidated fund:

General purpose operations

Water service

Sewerage service

Memorial Hall Committee

Leisure Centre Pty Limited

Performing Arts Centre Pty Limited

Oval Management Committee

Park Management Committee.

LGA s.411 (ii) The Trust Fund In accordance with the provisions of Section 411 of the Local Government Act 1993 (as amended), a separate

and distinct Trust Fund is maintained to account for all money and property received by the Council in trust which must be applied only for the purposes of or in accordance with the trusts relating to those monies. Trust monies and property subject to Council’s control have been included in these reports.

Trust monies and property held by Council but not subject to the control of Council, have been excluded from these reports. A separate statement of monies held in the Trust Fund is available for inspection at the Council office by any person free of charge.

(iii) County Councils Council is a member of the Holly Weeds County Council, a body corporate established under the Local

Government Act to control weeds in the Cumberland Plains Region. Council is one of 5 constituent members and neither controls or significantly influences the County Council. Accordingly, the County Council has not been consolidated or otherwise included in the financial statements.

AASB 10

AASB 10 AASB 11

(iv) Interests in other entities The consolidated financial statements include the financial position and performance of controlled entities from the date on which controls is obtained until the date that control is lost. Intragroup assets, liabilities, equity, income, expenses and cashflows relating to transaction between entities in the consolidated entity have been eliminated in full for the purpose of these financial statements. Appropriate adjustments have been made to a controlled entity’s financial position, performance and cash flows where the accounting policies used by that entity were different from those adopted by the consolidated entity. All controlled entities have a June financial year end.

A list of controlled entities is contained in Note 19 to the financial statements.

Subsidiaries

Subsidiaries are all entities (including structured entities) over which the Council has control. Control is established when the Council is exposed to, or has rights to variable returns from its involvement with the entity and has the ability to affect those returns through its power to direct the relevant activities of the entity.

Joint Arrangements

AASB 11 Joint Arrangements defines a joint arrangement as an arrangement of which two or more parties have joint control and classifies these arrangements as either joint ventures or joint operations. The Council has determined that it has [both joint ventures and joint operations / only joint ventures / only joint operations] – Councils to delete as applicable.

Joint operations:

In relation to its joint operations, where the venturer has the rights to the individual assets and obligations arising from the arrangement, the Council has recognised:

Its assets, including its share of any assets held jointly;

Its liabilities, including its share of any liabilities incurred jointly;

Its revenue from the sale of its share of the output arising from the joint operation;

Its share of the revenue from the sale of the output by the joint operation;

Its expenses, including its share of any expenses incurred jointly.

These figures are incorporated into the relevant line item in the primary statements.

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-26

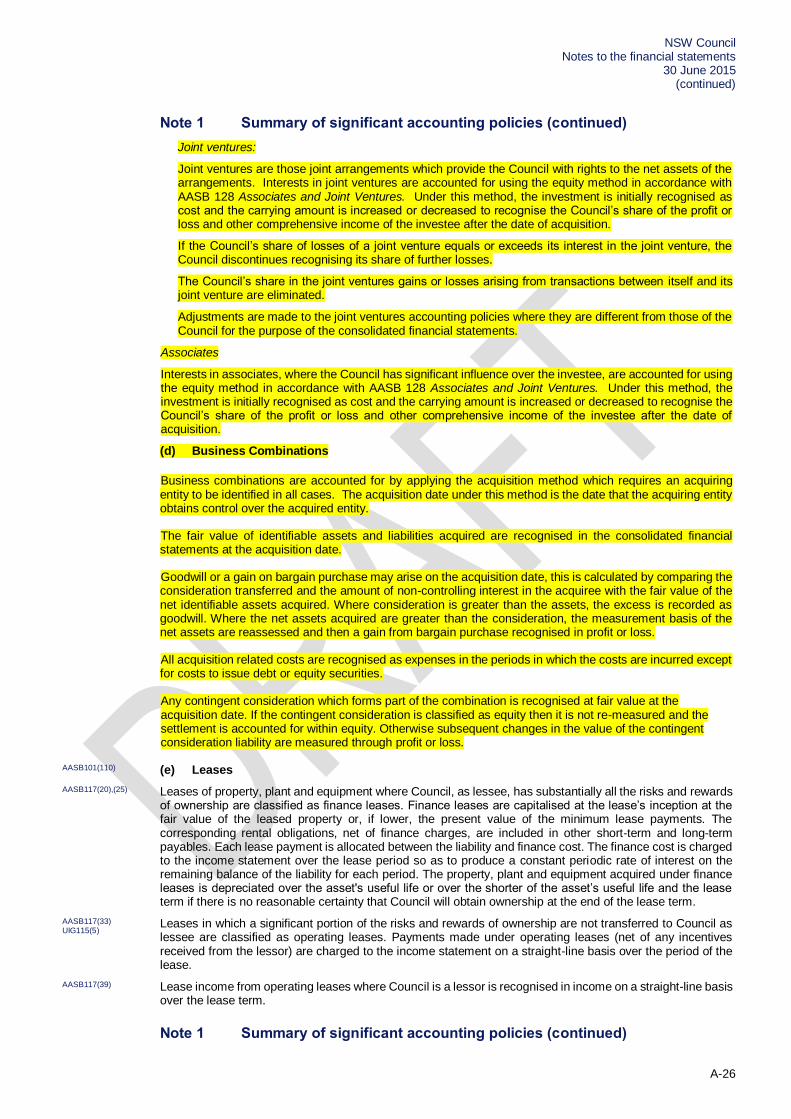

Note 1 Summary of significant accounting policies (continued)

Joint ventures:

Joint ventures are those joint arrangements which provide the Council with rights to the net assets of the arrangements. Interests in joint ventures are accounted for using the equity method in accordance with AASB 128 Associates and Joint Ventures. Under this method, the investment is initially recognised as cost and the carrying amount is increased or decreased to recognise the Council’s share of the profit or loss and other comprehensive income of the investee after the date of acquisition.

If the Council’s share of losses of a joint venture equals or exceeds its interest in the joint venture, the Council discontinues recognising its share of further losses.

The Council’s share in the joint ventures gains or losses arising from transactions between itself and its joint venture are eliminated.

Adjustments are made to the joint ventures accounting policies where they are different from those of the Council for the purpose of the consolidated financial statements.

Associates

Interests in associates, where the Council has significant influence over the investee, are accounted for using the equity method in accordance with AASB 128 Associates and Joint Ventures. Under this method, the investment is initially recognised as cost and the carrying amount is increased or decreased to recognise the Council’s share of the profit or loss and other comprehensive income of the investee after the date of acquisition.

(d) Business Combinations

Business combinations are accounted for by applying the acquisition method which requires an acquiring entity to be identified in all cases. The acquisition date under this method is the date that the acquiring entity obtains control over the acquired entity. The fair value of identifiable assets and liabilities acquired are recognised in the consolidated financial statements at the acquisition date. Goodwill or a gain on bargain purchase may arise on the acquisition date, this is calculated by comparing the consideration transferred and the amount of non-controlling interest in the acquiree with the fair value of the net identifiable assets acquired. Where consideration is greater than the assets, the excess is recorded as goodwill. Where the net assets acquired are greater than the consideration, the measurement basis of the net assets are reassessed and then a gain from bargain purchase recognised in profit or loss. All acquisition related costs are recognised as expenses in the periods in which the costs are incurred except for costs to issue debt or equity securities. Any contingent consideration which forms part of the combination is recognised at fair value at the acquisition date. If the contingent consideration is classified as equity then it is not re-measured and the settlement is accounted for within equity. Otherwise subsequent changes in the value of the contingent consideration liability are measured through profit or loss.

AASB101(110) (e) Leases

AASB117(20),(25) Leases of property, plant and equipment where Council, as lessee, has substantially all the risks and rewards of ownership are classified as finance leases. Finance leases are capitalised at the lease’s inception at the fair value of the leased property or, if lower, the present value of the minimum lease payments. The corresponding rental obligations, net of finance charges, are included in other short-term and long-term payables. Each lease payment is allocated between the liability and finance cost. The finance cost is charged to the income statement over the lease period so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period. The property, plant and equipment acquired under finance leases is depreciated over the asset's useful life or over the shorter of the asset’s useful life and the lease term if there is no reasonable certainty that Council will obtain ownership at the end of the lease term.

AASB117(33) UIG115(5)

Leases in which a significant portion of the risks and rewards of ownership are not transferred to Council as lessee are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are charged to the income statement on a straight-line basis over the period of the lease.

AASB117(39) Lease income from operating leases where Council is a lessor is recognised in income on a straight-line basis over the lease term.

Note 1 Summary of significant accounting policies (continued)

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-27

AASB101(110) (f) Impairment of assets

AASB136(9),(10) Intangible assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment, or more frequently if events or changes in circumstances indicate that they might be impaired. Other assets are tested for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use.

Where an asset is not held principally for cash generating purposes and would be replaced if the Council was deprived of it then depreciated replacement cost is used as value in use, otherwise value in use is estimated by using a discounted cash flow model.

For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash inflows which are largely independent of the cash inflows from other assets or groups of assets (cash-generating units). Non-financial assets that suffered an impairment are reviewed for possible reversal of the impairment at each reporting date.

AASB101(110) (g) Cash and cash equivalents

AASB107(6),(8),(46) For Statement of cashflow presentation purposes, cash and cash equivalents includes cash on hand, deposits held at call with financial institutions, other short-term, highly liquid investments with original maturities of three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value, and bank overdrafts. Bank overdrafts are shown within borrowings in current liabilities on the statement of financial position.

AASB101(110)

(h) Receivables

AASB7(21) AASB139(46)(a)

Receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. Receivables are generally due for settlement within 30 days.

Collectability of receivables is reviewed on an ongoing basis. Debts which are known to be uncollectible are written off by reducing the carrying amount directly. An allowance account (provision for impairment of receivables) is used when there is objective evidence that Council will not be able to collect all amounts due according to the original terms of the receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments (more than 30 days overdue) are considered indicators that the receivable is impaired. The amount of the impairment allowance is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. Cash flows relating to short-term receivables are not discounted if the effect of discounting is immaterial.

AASB7(21) AASB7(B5)(d)

The amount of the impairment loss is recognised in the income statement within other expenses. When a receivable for which an impairment allowance had been recognised becomes uncollectible in a subsequent period, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against other expenses in the income statement.

AASB101(110) (i) Inventories

AASB101(110) (i) Raw materials and stores, work in progress and finished goods AASB102(9),(10),(25), (36)(a)

Raw materials and stores, work in progress and finished goods are stated at the lower of cost and net realisable value. Cost comprises direct materials, direct labour and an appropriate proportion of variable and fixed overhead expenditure, the latter being allocated on the basis of normal operating capacity. Cost includes the transfer from equity of any gains/losses on qualifying cash flow hedges relating to purchases of raw material. Costs are assigned to individual items of inventory on basis of weighted average costs. Costs of purchased inventory are determined after deducting rebates and discounts. Net realisable value is the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale.

AASB101(110) (ii) Land held for resale/capitalisation of borrowing costs AASB102(9),(10),(23), (36)(a) AASB123(11),(25)

Land held for resale is stated at the lower of cost and net realisable value. Cost is assigned by specific identification and includes the cost of acquisition, and development and borrowing costs during development. When development is completed borrowing costs and other holding charges are expensed as incurred.

AASB123(11),(13), (23)

Borrowing costs included in the cost of land held for resale are those costs that would have been avoided if the expenditure on the acquisition and development of the land had not been made. Borrowing costs incurred while active development is interrupted for extended periods are recognised as expenses.

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-28

Note 1 Summary of significant accounting policies (continued)

AASB101(110) (j) Non-current assets (or disposal groups) held for sale and discontinued operations

AASB5(6),(15) Non-current assets (or disposal groups) are classified as held for sale if their carrying amount will be recovered principally through a sale transaction rather than through continuing use. They are measured at the lower of their carrying amount and fair value less costs to sell, except for assets such as deferred tax assets, assets arising from employee benefits, financial assets and investment property that are carried at fair value and contractual rights under insurance contracts, which are specifically exempt from this requirement.

AASB5(20)-(22) An impairment loss is recognised for any initial or subsequent write-down of the asset (or disposal group) to fair value less costs to sell. A gain is recognised for any subsequent increases in fair value less costs to sell of an asset (or disposal group), but not in excess of any cumulative impairment loss previously recognised. A gain or loss not previously recognised by the date of the sale of the non-current asset (or disposal group) is recognised at the date of de-recognition.

AASB5(25) Non-current assets (including those that are part of a disposal group) are not depreciated or amortised while they are classified as held for sale. Interest and other expenses attributable to the liabilities of a disposal group classified as held for sale continue to be recognised.

AASB5(38) Non-current assets classified as held for sale and the assets of a disposal group classified as held for sale are presented separately from the other assets in the statement of financial position. The liabilities of a disposal group classified as held for sale are presented separately from other liabilities in the statement of financial position.

AASB5(31),(32),(33)(a) A discontinued operation is a component of the entity council that has been disposed of or is classified as held for sale and that represents a separate major line of business or geographical area of operations, is part of a single co-ordinated plan to dispose of such a line of business or area of operations, or is a subsidiary acquired exclusively with a view to resale. The results of discontinued operations are presented separately on the face of the Income statement.

AASB101(110) AASB7(21)

(k) Investments and other financial assets

Classification AASB139(45),(60) Council classifies its financial assets in the following categories: financial assets at fair value through profit or

loss, loans and receivables, held-to-maturity investments and available-for-sale financial assets. The classification depends on the purpose for which the investments were acquired. Management determines the classification of its investments at initial recognition and, in the case of assets classified as held-to-maturity, re-evaluates this designation at each reporting date.

AASB101(110) (i) Financial assets at fair value through profit or loss AASB101(57),(59) AASB139(9),(45)

Financial assets at fair value through profit or loss are financial assets held for trading. A financial asset is classified in this category if acquired principally for the purpose of selling in the short term. Derivatives are classified as held for trading unless they are designated as hedges. Assets in this category are classified as current assets.

(ii) Loans and receivables AASB139(9) Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not

quoted in an active market. They are included in current assets, except for those with maturities greater than 12 months after the reporting date which are classified as non-current assets. Loans and receivables are included in other receivables (note 8) and receivables (note 7) in the statement of financial position.

(iii) Held-to-maturity investments AASB139(9) Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and

fixed maturities that Council’s management has the positive intention and ability to hold to maturity. If Council were to sell other than an insignificant amount of held-to-maturity financial assets, the whole category would be tainted and reclassified as available-for-sale. Held-to-maturity financial assets are included in non-current assets, except for those with maturities less than 12 months from the reporting date, which are classified as current assets.

(iv) Available-for-sale financial assets AASB139(9) AASB7(21),(B5)(b)

Available-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other categories. They are included in non-current assets unless management intends to dispose of the investment within 12 months of the reporting date. Investments are designated as available-for-sale if they do not have fixed maturities and fixed or determinable payments and management intends to hold them for the medium to long term.

NSW Council Notes to the financial statements 30 June 2015 (continued)

A-29

Note 1 Summary of significant accounting policies (continued)

AASB101(110) AASB7(21)

(k) Investments and other financial assets (continued)

Recognition and de-recognition AASB139(38),(43) AASB7(21),(B5)(c)

Regular purchases and sales of financial assets are recognised on trade-date - the date on which Council commits to purchase or sell the asset. Investments are initially recognised at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets carried at fair value through profit or loss are initially recognised at fair value and transaction costs are expensed in the income statement. Financial assets are derecognised when the rights to receive cash flows from the financial assets have expired or have been transferred and Council has transferred substantially all the risks and rewards of ownership.

When securities classified as available-for-sale are sold, the accumulated fair value adjustments recognised in equity are included in the income statement as gains and losses from investment securities.

Subsequent measurement AASB139(46)(a) Loans and receivables and held-to-maturity investments are carried at amortised cost using the effective

interest method.

Changes in the fair value of monetary securities denominated in a foreign currency and classified as available-for-sale are analysed between translation differences resulting from changes in amortised cost of the security and other changes in the carrying amount of the security (note Council’s obligations under Section 625 of the Local Government Act and S212 of the LG (General) Regulation 2005).. The translation differences related to changes in the amortised cost are recognised in profit or loss, and other changes in carrying amount are recognised in equity. Changes in the fair value of other monetary and non-monetary securities classified as available-for-sale are recognised in equity.

AASB7(27) Details on how the fair value of financial instruments is determined are disclosed in note 1(l).

Impairment AASB139(58),(59) Council assesses at the end of each reporting period whether there is objective evidence that a financial

asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. In the case of equity investments classified as available-for-sale, a significant or prolonged decline in the fair value of the security below its cost is considered an indicator that the assets are impaired.

(i) Assets carried at amortised cost AASB139(63) (Revised)

For loans and receivables, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced and the amount of the loss is recognised in profit or loss. If a loan or held-to-maturity investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. As a practical expedient, the group may measure impairment on the basis of an instrument’s fair value using an observable market price.

OLG Investment Policy Council has an approved investment policy complying with Section 625 of the Local Government Act and

S212 of the LG (General) Regulation 2005. Investments are placed and managed in accordance with that policy and having particular regard to authorised investments prescribed under the Ministerial Local Government Investment Order. Council maintains an investment policy that complies with the Act and ensures that it or its representatives exercise care, diligence and skill that a prudent person would exercise in investing Council funds.

Council amended its policy following revisions to the Ministerial Local Government Investment Order arising from the Cole Inquiry recommendations. Certain investments the Council holds are no longer prescribed, however they have been retained under grandfathering provisions of the Order. These will be disposed of when most financially advantageous to Council.