Embed Size (px)

Citation preview

1

Columbus Gold – Two Gold Stocks In One

Columbus Gold (CGT.TO; CBGDF.OTCQX) is a rare two-for-one opportunity, with a big, advanced gold project ready for a takeover and a portfolio of prime Nevada exploration projects.

That portfolio is about to get the attention it deserves by getting spun out into a new company called Allegiant Gold, led by Nevada legend Andy Wallace.

Invest in Columbus Gold today, before the imminent spinout, and get both Columbus and Allegiant in your portfolio!

There are two moments in the lifespan of a discovery that give investors the most upside.

The first is at the very start. New discoveries send share prices soaring.

The second is when the discovery gets close to becoming a mine. Share prices ramp up as a project reaches production – or when news breaks that a major miner is buying a project to build it.

It’s rare to get exposure to both in the same deal. Deposits have to get well down the development path to attract a takeover bid; all the required drilling, engineering, permitting, metallurgy, and financing work leave no time for a company to also explore for new discoveries.

So stocks offering the two best aspects of exploration investing – an advanced, takeout-ready project and an exciting exploration program – are rare.

But not impossible. In fact right now one company – Columbus Gold (CGT.TO; CBGDF.OTCQX) – offers exactly that.

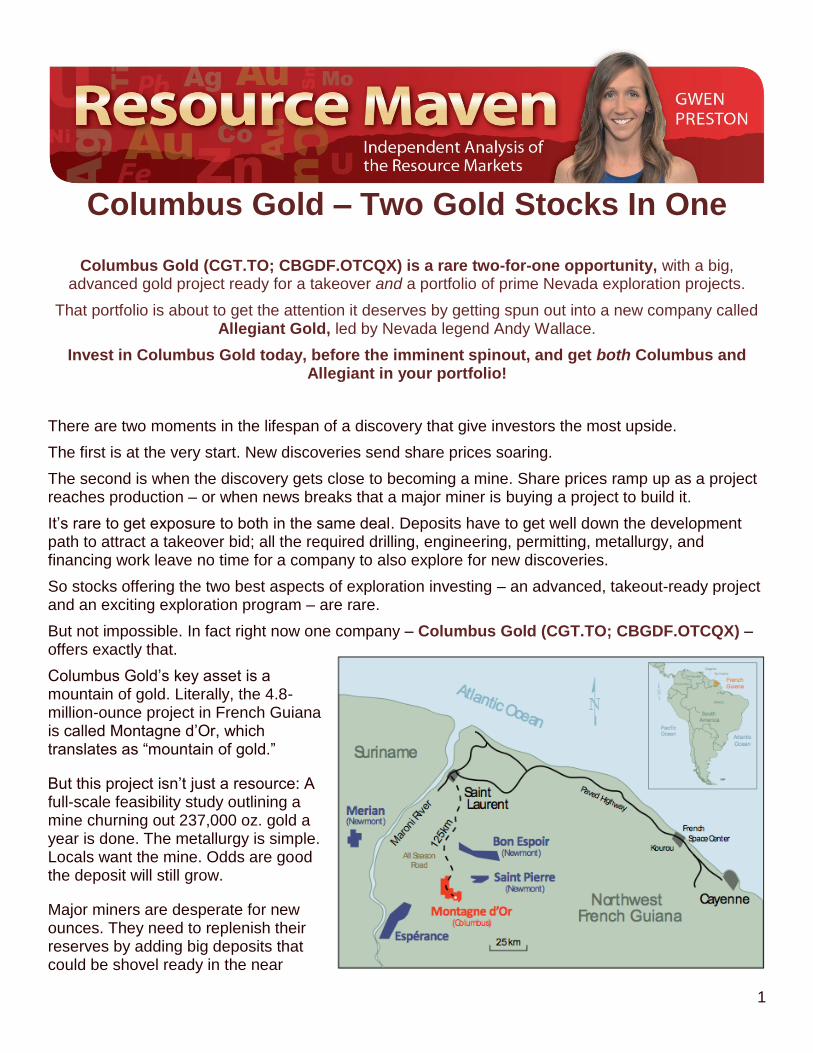

Columbus Gold’s key asset is a mountain of gold. Literally, the 4.8-million-ounce project in French Guiana is called Montagne d’Or, which translates as “mountain of gold.”

But this project isn’t just a resource: A full-scale feasibility study outlining a mine churning out 237,000 oz. gold a year is done. The metallurgy is simple. Locals want the mine. Odds are good the deposit will still grow.

Major miners are desperate for new ounces. They need to replenish their reserves by adding big deposits that could be shovel ready in the near

2

term. But after a five-year bear market stopped most projects in their tracks, there are very few gold projects that fit the bill.

As a feasibility-level project able to produce 237,000 ounces of gold annually – enough to move the needle for even the largest of the world’s gold miners – Montagne d’Or is a clear M&A target.

A major miner is going to build this project. It’s just a question of who – and that question will get answered over the next year or two, as the project moves through permitting and likely attracts a takeout.

So with Montagne d’Or, Columbus Gold gives shareholders exposure to whatever miner ends up buying this big, advanced gold project.

That alone makes Columbus Gold attractive. But here’s the kicker...

If you invest in Columbus before December 11th, you also get in early with a brand-new company about to start exploring a prime portfolio of 14 US exploration targets.

December 11th is when Columbus Gold will spin out Allegiant Gold. Anyone who owns CGT shares on that Monday will get one Allegiant share for every five Columbus shares held.

Montagne d’Or is reason enough to own Columbus, but buy in ahead of December 11th and you’ll also get exposure to dynamic new explorer headed by a Nevada legend with plans to drill no fewer than 10 projects in the next 12 months.

They already have one gold deposit that could get bigger and just finished drilling another project that could produce a new discovery. These two projects alone backstop Allegiant’s valuation.

And then there are the 12 other projects, in Nevada, Utah, and Arizona, all handpicked by exploration legend Andy Wallace.

Gwen Preston is the Resource Maven.

Maven means ‘a trusted expert in a particular field who seeks to pass

knowledge on to others.’ Gwen is the maven of the exploration and mining

markets.

After a decade of research and investing, Gwen has a deep base of knowledge and

a broad network of contacts in the resource sector. She understands which projects and pieces of news matter. She understands what it takes for a project to

advance along the exploration-development-production path and what

opportunities each stage offers. She knows how the metals markets work,

alone and within the global economy, and how to profit from commodity cycles.

Gwen chronicles her thoughts, buys, and sells each week in The Maven Letter, a

subscriber-supported newsletter.

Sign up now for a free trial

subscription!

3

No one knows Nevada gold better than Wallace. Wallace discovered a number of multi-million-ounce gold deposits that later became gold mines, some of which are still producing today. And over the last ten years Wallace has been quietly acquiring his favorite Nevada exploration properties and putting them into Columbus Gold.

Wallace has prospected, mapped, and sampled these properties. He ran geophysics, generated geologic models, and delineated drill targets.

All he needed was a corporate directive to get going – and now he’s getting exactly that – and with it a chance to make another big gold discovery.

Columbus gets zero value for its Nevada portfolio because the Mountain of Gold overshadows it completely. By spinning it out, the market is going to see the value and potential in this incredible portfolio.

And Wallace is going to get the money and focus to explore his hidden cache of prime gold targets.

That’s the short version of the story. And the conclusion – that you should buy into Columbus Gold right now to take advantage of this rare two-for-one deal.

There is, of course, much more to say. Read on for more about Montagne d’Or, the US exploration portfolio, and the potential for value sitting inside Columbus Gold.

Immediate Value

Allegiant Gold really represents the unlocking of a cache of hidden value.

The portfolio of projects is home grown. It grew slowly over the last ten years, as Wallace used the bear market to pick up one prime target after another.

So Columbus investors have owned these projects for years…but the market gives Columbus zero value for them. That’s just how it goes when a company’s flagship is a 4.8-million-oz. gold project being driven towards production by an aggressive Russian partner – the exploration portfolio gets completely overshadowed.

A focused management team sees when assets are getting ignored and finds a way to bring them to light. Especially when the assets deserve attention.

The projects in Wallace’s portfolio are deserving.

When metal prices move, explorers hit new discoveries, or deals go down – Gwen explains

what it all means.

Check out her website for free articles and

videos

4

The most advanced project, Eastside, already hosts 721,000 oz. inferred gold plus 272,150 oz. historic gold, all in near surface deposits, and odds are good the resource can grow with a bit of effort.

The second-in-line project, Bolo, is a Carlin-style target that hasn’t seen real work since the 1980s. The drill holes from those days rarely went deeper than 45 metres and explorers assumed only certain rock types were prospective for gold, but it turns out gold at Bolo spreads farther and deeper than they thought.

With just those two advanced assets plus millions in the bank, it’s easy to argue Allegiant will carry a market cap in the tens of millions. Clear comparables like NuLegacy Gold, Contact Gold, and TriMetals Mining have market caps ranging from $34 million to $65 million.

All for a portfolio that is getting zero value in Columbus. That’s unlocking value.

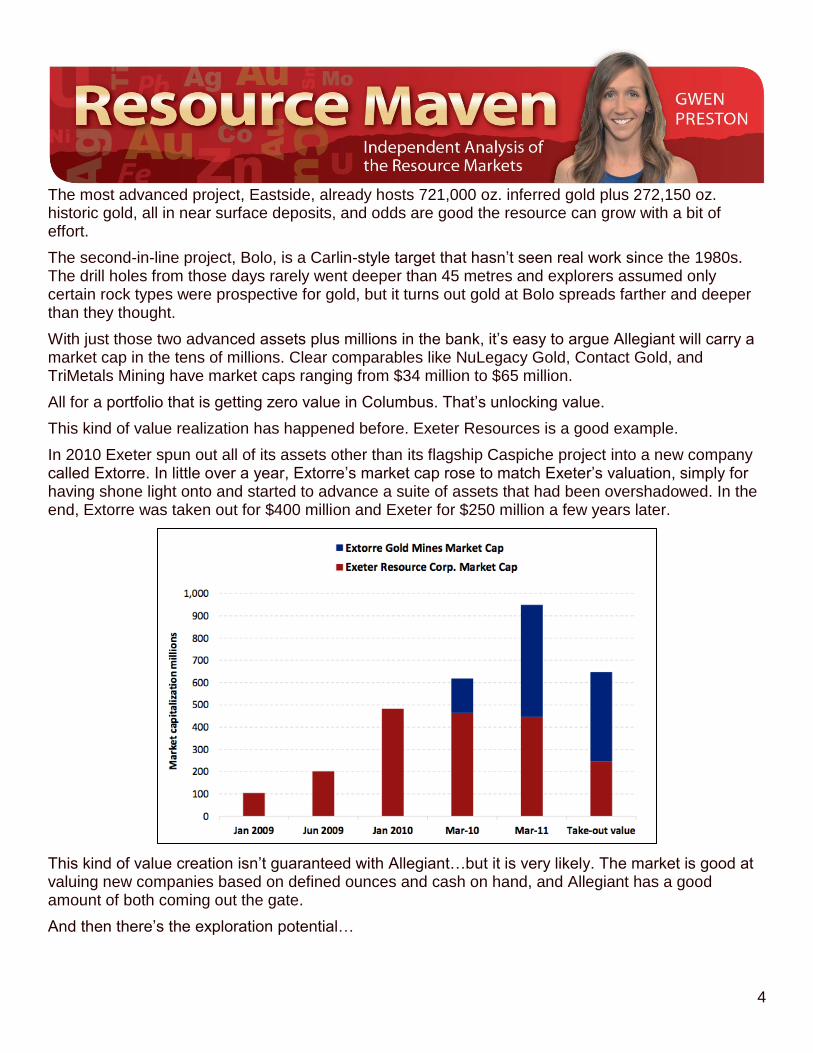

This kind of value realization has happened before. Exeter Resources is a good example.

In 2010 Exeter spun out all of its assets other than its flagship Caspiche project into a new company called Extorre. In little over a year, Extorre’s market cap rose to match Exeter’s valuation, simply for having shone light onto and started to advance a suite of assets that had been overshadowed. In the end, Extorre was taken out for $400 million and Exeter for $250 million a few years later.

This kind of value creation isn’t guaranteed with Allegiant…but it is very likely. The market is good at valuing new companies based on defined ounces and cash on hand, and Allegiant has a good amount of both coming out the gate.

And then there’s the exploration potential…

5

Exploration Upside

Before jumping into the projects, let me set the stage.

There’s one force that unifies this portfolio: Andy Wallace.

Wallace joined Cordex Exploration in 1974, at the height of the Nevada gold rush. Within ten years he was Manager of Exploration – and this for a group credited with an unprecedented eight gold mine discoveries in Nevada.

A number of those came under Wallace’s management, including the 5-million oz. Marigold mine, the 12-million oz. Stonehouse/Lone Tree mine, and the Daisy mine. As part of Cordex Wallace was also involved in discovering the Sterling, Dee, and Pinson mines.

Wallace knows Nevada. He knows how to find gold in Nevada. And over the last ten years, every time he came across a property that he thought prospective he grabbed it and put it into Columbus Gold.

Wallace did more than fill the portfolio. He also advanced each project to drill ready. He mapped, prospected, and in some cases ran geophysical surveys. He dropped properties that failed to return promising results and replaced them with new ideas, over and over again.

The result is 14 projects with clear geologic concepts that are ready to be drill tested.

And Allegiant will drill ten of them in the next 12 months.

Eastside

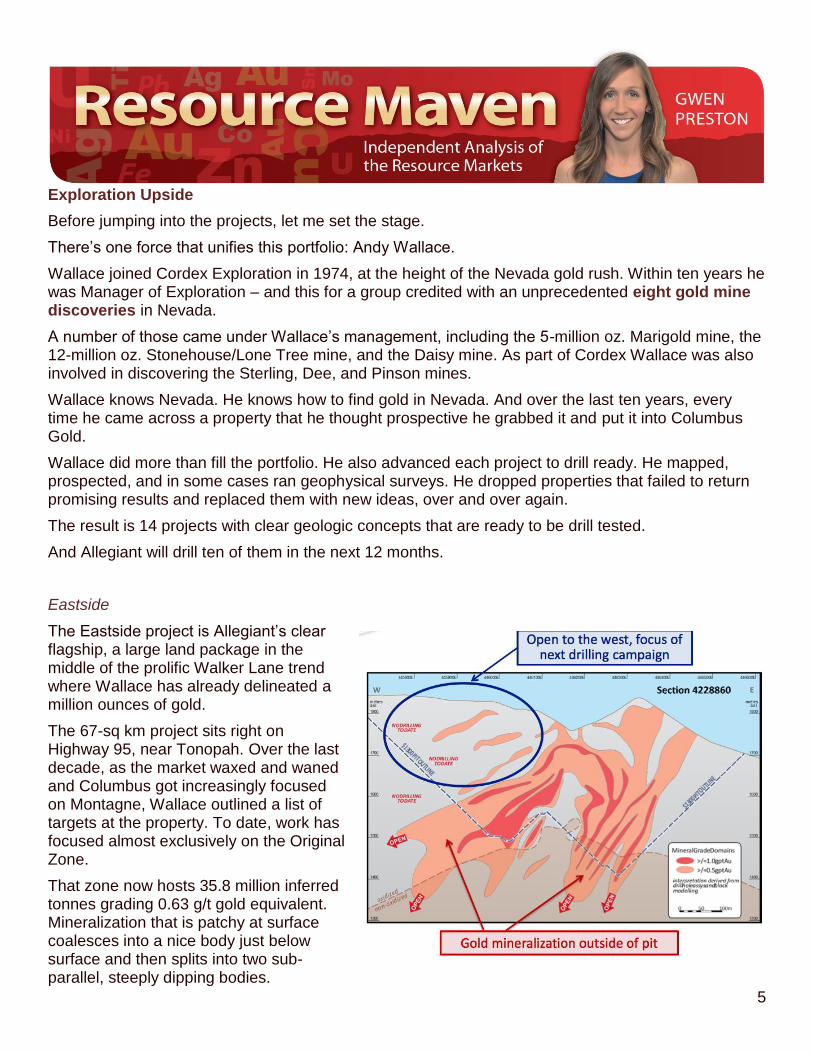

The Eastside project is Allegiant’s clear flagship, a large land package in the middle of the prolific Walker Lane trend where Wallace has already delineated a million ounces of gold.

The 67-sq km project sits right on Highway 95, near Tonopah. Over the last decade, as the market waxed and waned and Columbus got increasingly focused on Montagne, Wallace outlined a list of targets at the property. To date, work has focused almost exclusively on the Original Zone.

That zone now hosts 35.8 million inferred tonnes grading 0.63 g/t gold equivalent. Mineralization that is patchy at surface coalesces into a nice body just below surface and then splits into two sub-parallel, steeply dipping bodies.

6

Several faults cut through the deposit and where they do the gold and silver grades increase.

The deposit is clearly open to the south and west, areas that haven’t been drilled, and at depth. Those areas are obvious targets, as success would grow a deposit that is already defined, carries a good grade, and looks to make sense as an open pit.

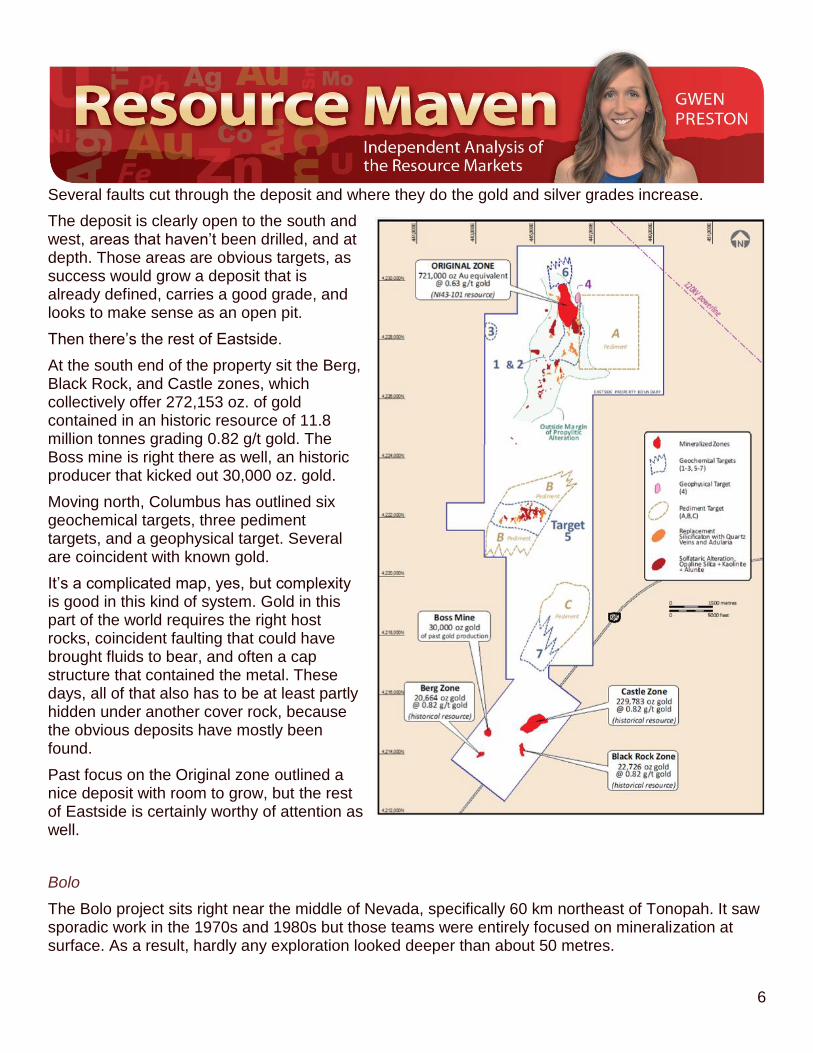

Then there’s the rest of Eastside.

At the south end of the property sit the Berg, Black Rock, and Castle zones, which collectively offer 272,153 oz. of gold contained in an historic resource of 11.8 million tonnes grading 0.82 g/t gold. The Boss mine is right there as well, an historic producer that kicked out 30,000 oz. gold.

Moving north, Columbus has outlined six geochemical targets, three pediment targets, and a geophysical target. Several are coincident with known gold.

It’s a complicated map, yes, but complexity is good in this kind of system. Gold in this part of the world requires the right host rocks, coincident faulting that could have brought fluids to bear, and often a cap structure that contained the metal. These days, all of that also has to be at least partly hidden under another cover rock, because the obvious deposits have mostly been found.

Past focus on the Original zone outlined a nice deposit with room to grow, but the rest of Eastside is certainly worthy of attention as well.

Bolo

The Bolo project sits right near the middle of Nevada, specifically 60 km northeast of Tonopah. It saw sporadic work in the 1970s and 1980s but those teams were entirely focused on mineralization at surface. As a result, hardly any exploration looked deeper than about 50 metres.

7

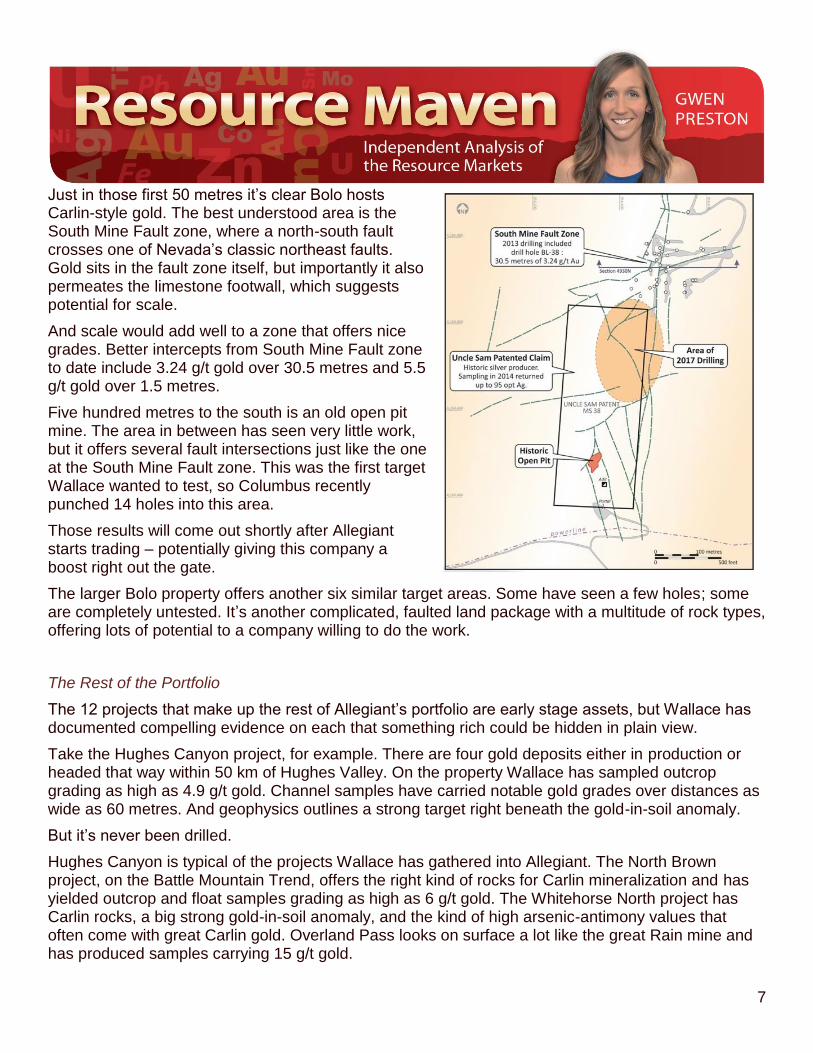

Just in those first 50 metres it’s clear Bolo hosts Carlin-style gold. The best understood area is the South Mine Fault zone, where a north-south fault crosses one of Nevada’s classic northeast faults. Gold sits in the fault zone itself, but importantly it also permeates the limestone footwall, which suggests potential for scale.

And scale would add well to a zone that offers nice grades. Better intercepts from South Mine Fault zone to date include 3.24 g/t gold over 30.5 metres and 5.5 g/t gold over 1.5 metres.

Five hundred metres to the south is an old open pit mine. The area in between has seen very little work, but it offers several fault intersections just like the one at the South Mine Fault zone. This was the first target Wallace wanted to test, so Columbus recently punched 14 holes into this area.

Those results will come out shortly after Allegiant starts trading – potentially giving this company a boost right out the gate.

The larger Bolo property offers another six similar target areas. Some have seen a few holes; some are completely untested. It’s another complicated, faulted land package with a multitude of rock types, offering lots of potential to a company willing to do the work.

The Rest of the Portfolio

The 12 projects that make up the rest of Allegiant’s portfolio are early stage assets, but Wallace has documented compelling evidence on each that something rich could be hidden in plain view.

Take the Hughes Canyon project, for example. There are four gold deposits either in production or headed that way within 50 km of Hughes Valley. On the property Wallace has sampled outcrop grading as high as 4.9 g/t gold. Channel samples have carried notable gold grades over distances as wide as 60 metres. And geophysics outlines a strong target right beneath the gold-in-soil anomaly.

But it’s never been drilled.

Hughes Canyon is typical of the projects Wallace has gathered into Allegiant. The North Brown project, on the Battle Mountain Trend, offers the right kind of rocks for Carlin mineralization and has yielded outcrop and float samples grading as high as 6 g/t gold. The Whitehorse North project has Carlin rocks, a big strong gold-in-soil anomaly, and the kind of high arsenic-antimony values that often come with great Carlin gold. Overland Pass looks on surface a lot like the great Rain mine and has produced samples carrying 15 g/t gold.

8

On it goes. Twelve projects, chosen by Wallace, with groundwork done and drill targets defined, all getting zero value in Columbus, are about to step out from the shadow of the Montagne.

Good Targets and Lots of Them

Exploration is a risky venture, but one good way to lower risk is to spread your bets and place some of them on known entities. Allegiant is doing exactly that.

In its first year, the company plans to:

Drill 20,000 metres at Eastside to expand the known resource there (including bringing an historic resource into compliance – shooting fish in a barrel)

Drill 4,000 metres at Bolo to update the historic resource there (again, low risk)

Drill 16,000 metres across 8 untested projects.

Some of the eight new projects will be dusters, for sure. That’s the nature of exploration. But drilling that many projects means Allegiant is likely to hit into something good on at least one of them, if not several.

These are, after all, Andy Wallace targets. Lots of companies have exploration projects or ideas in Nevada, but none of them have Wallace. His experience means Allegiant’s odds of success are simply better than almost anyone else’s.

Investors love a new discovery, especially one in a proven jurisdiction. Nevada couldn’t be more proven and no one is better suited than Andy Wallace and Allegiant to make a new Nevada discovery.

Don’t Forget the Mountain of Gold

While Allegiant gets to work to create value in the new company, the core investment – Columbus Gold – will be maneuvering for position.

To start, let me outline what Montagne d’Or has to offer. The resource totals almost 5 million ounces. It’s a road accessible project near the coast in northwest French Guiana. This is gold region; the area right around Montagne has already produced more than 2 million oz. gold from small-scale workings.

If you enjoy the style and content of this special report, you would enjoy the metals commentary and stock analysis in The Maven Letter. Sign up here for a free trial subscription.

9

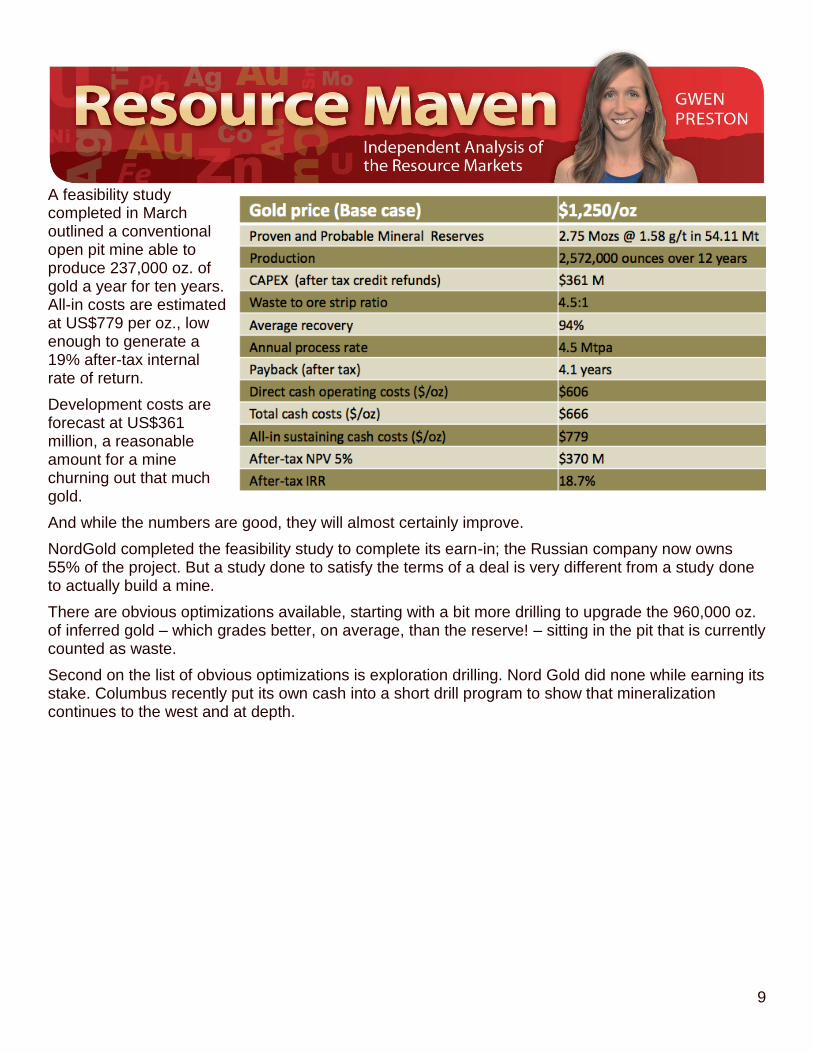

A feasibility study completed in March outlined a conventional open pit mine able to produce 237,000 oz. of gold a year for ten years. All-in costs are estimated at US$779 per oz., low enough to generate a 19% after-tax internal rate of return.

Development costs are forecast at US$361 million, a reasonable amount for a mine churning out that much gold.

And while the numbers are good, they will almost certainly improve.

NordGold completed the feasibility study to complete its earn-in; the Russian company now owns 55% of the project. But a study done to satisfy the terms of a deal is very different from a study done to actually build a mine.

There are obvious optimizations available, starting with a bit more drilling to upgrade the 960,000 oz. of inferred gold – which grades better, on average, than the reserve! – sitting in the pit that is currently counted as waste.

Second on the list of obvious optimizations is exploration drilling. Nord Gold did none while earning its stake. Columbus recently put its own cash into a short drill program to show that mineralization continues to the west and at depth.

10

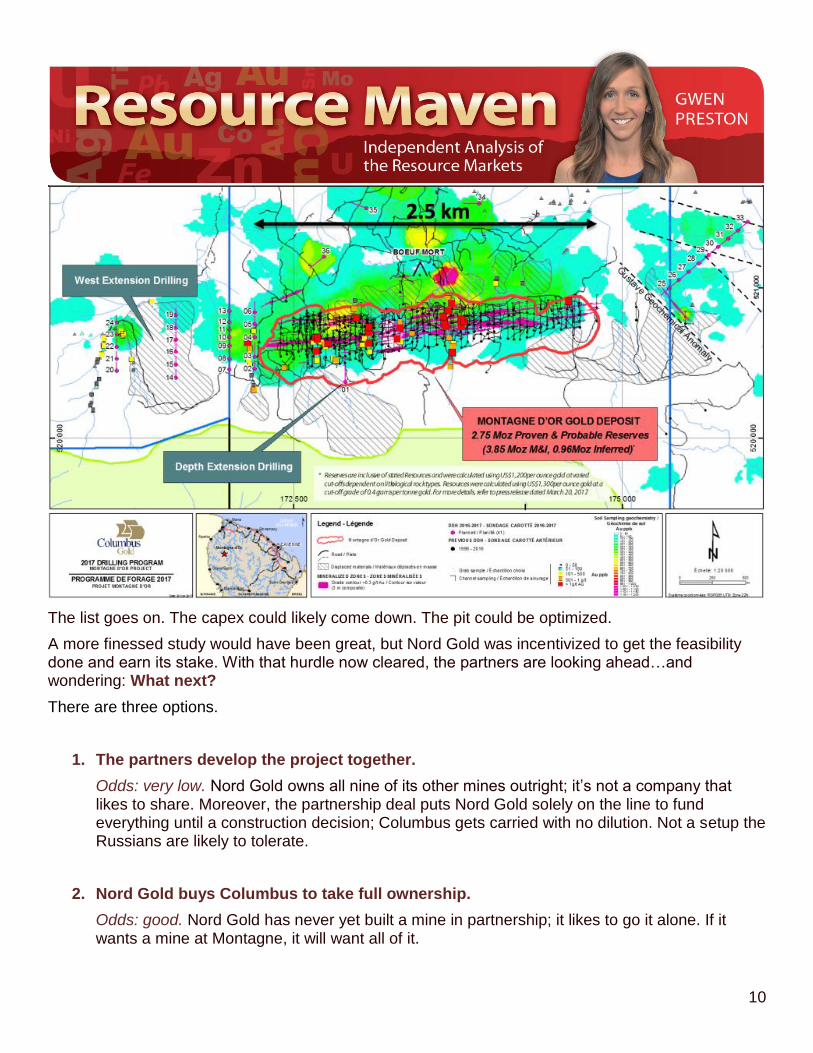

The list goes on. The capex could likely come down. The pit could be optimized.

A more finessed study would have been great, but Nord Gold was incentivized to get the feasibility done and earn its stake. With that hurdle now cleared, the partners are looking ahead…and wondering: What next?

There are three options.

1. The partners develop the project together.

Odds: very low. Nord Gold owns all nine of its other mines outright; it’s not a company that likes to share. Moreover, the partnership deal puts Nord Gold solely on the line to fund everything until a construction decision; Columbus gets carried with no dilution. Not a setup the Russians are likely to tolerate.

2. Nord Gold buys Columbus to take full ownership.

Odds: good. Nord Gold has never yet built a mine in partnership; it likes to go it alone. If it wants a mine at Montagne, it will want all of it.

11

3. Another miner buys some or all of Montagne.

Odds: also good. As mentioned, Montagne is one of only a few advanced gold projects in the world that looks able to produce 237,000 oz. gold annually for less than US$800 per oz. all in, and it is in a jurisdiction that is actively supporting the mine. This asset would fit nicely with many mid-tier and major miners.

It’s impossible to know which will happen or when. In the meantime, though, one thing is clear: Montagne d’Or needs to keep moving down the permitting track.

That’s where things get interesting.

Columbus was very clever when crafting the JV deal. Nord Gold and Columbus are 55-45% partners but Nord Gold is responsible for all costs until a construction decision is made.

Yup, Columbus gets carried without dilution until the decision to build.

Nord Gold isn’t going to want to pay for everything while only owning 55% of the project. No one would! So that one contractual clause suggests Nord Gold might make a move sooner rather than later.

And Columbus isn’t sitting still. There are two key reasons Allegiant Gold is being spun out right now: to unlock the value in the overshadowed Nevada portfolio and to turn Columbus into a clean vehicle that simply owns 45% of Montagne.

With complications removed, deals are easier and more likely.

Columbus management, led by Robert Giustra, is out making sure all interested parties understand the opportunity at Montagne.

A deal will come. It’s just a question of when.

It could happen tomorrow or it could take a year or two. If the latter, a rising gold price will make the asset more and more valuable, supporting the share price amidst the uncertainty.

The Take Home

This is a rare two-for-one deal: Buy one stock and get two companies.

One company gets you exposure to early-stage discovery and resource growth in one of the best gold jurisdictions in the world. The other is likely to be acquired by a mid-tier or senior at a premium to market.

But you have to act now. You have to be a Columbus shareholder of record as of December 11th. I urge you to act without delay.

12

--------------------------------------------------------------------------------------

EDITORIAL POLICY AND COPYRIGHT: Companies are selected based solely on merit; fees are not paid. This document is protected by copyright laws and may not be reproduced in any form for other than personal use without prior written consent from the publisher.

DISCLAIMER: The information in this publication is not intended to be, nor shall constitute, an offer to sell or solicit any offer to buy any security. The information presented on this website is subject to change without notice, and neither Resource Maven (Maven) nor its affiliates assume any responsibility to update this information. Maven is not registered as a securities broker-dealer or an investment adviser in any jurisdiction. Additionally, it is not intended to be a complete description of the securities, markets, or developments referred to in the material. Maven cannot and does not assess, verify or guarantee the adequacy, accuracy or completeness of any information, the suitability or profitability of any particular investment, or the potential value of any investment or informational source. Additionally, Maven in no way warrants the solvency, financial condition, or investment advisability of any of the securities mentioned. Furthermore, Maven accepts no liability whatsoever for any direct or consequential loss arising from any use of our product, website, or other content. The reader bears responsibility for his/her own investment research and decisions and should seek the advice of a qualified investment advisor and investigate and fully understand any and all risks before investing. Information and statistical data contained in this website were obtained or derived from sources believed to be reliable. However, Maven does not represent that any such information, opinion or statistical data is accurate or complete and should not be relied upon as such. This publication may provide addresses of, or contain hyperlinks to, Internet websites. Maven has not reviewed the Internet website of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the convenience and information of this website's users, and the content of linked third-party websites is not in any way incorporated into this website. Those who choose to access such third-party websites or follow such hyperlinks do so at their own risk. The publisher, owner, writer or their affiliates may own securities of or may have participated in the financings of some or all of the companies mentioned in this publication.

In the weekly Maven Letter, Gwen assesses news from the metals and mining spaces, explains trends and seasonal trading opportunities, and outlines what explorers, developers, and miners

she is buying – and selling – and why. Sign up today for a free three-week trial subscription!