Embed Size (px)

Citation preview

1 / 25

Michael Reuther Member of the Board of Managing DirectorsLondon, October 4th, 2007

Commerzbank: Creating sustainable value and profitable growthMerrill Lynch Banking & Insurance CEO Conference

2 / 25

Agenda

1. Status quo: record level H1 2007 figures

2. Strategic program: stable growth and improved profitability

3. Financial outlook

4. Effects: creating sustainable value

3 / 25

Net RoE

EPS

CIR

• Strong focus on Net RoE, CIR, EPS

• Realizing growth opportunities

• High exposure to German economy

• Enhancing organic growth in core divisions

• Expanding in regions and products with competitive strengths

• Increasing profitability

• Ongoing efficiency enhancement in all divisions

• Following active portfolio management

• Ensuring efficient capital management

Commerzbank is managed along three main Group performance indicators

+3.9ppts

1.57

2.10

55.253.9

18.2

22.1

H1 2006 H1 2007

Following a balanced approach to profitability and growth

+33.8%

H1 2006 H1 2007

H1 2006 H1 2007

Note: 2006 figures based on stated results

-1.3ppts

4 / 25

Clean Net RoE*in %

Net RoE*in %

EPSin €

Commerzbank is fully in line to reach its FY 2007 targets

Clean EPSin €

H1 2006 H1 2007 H1 2006 H1 2007

Clean: excluding net result on participations, restructuring charges

CIRin %

Clean CIRin %

H1 2006 H1 2007

1.572.10

1.02

1.51

18.2

22.1

11.9

16.0

55.253.9

63.1

58.6

H1 2006 H1 2007 H1 2006 H1 2007H1 2006 H1 2007

Note: 2006 figures based on stated results

+3.9ppts +33.8%

+48.0%

-1.3ppts

+4.1ppts -4.5ppts

* Annualized

5 / 25

Operating profitin € m

192559

1,011

2,030

2,715

2002 2003 2004 2005 2006 2007p 2008-2010p

Commerzbank on track

• Restored:Corporate financial strength evenunder stress conditions

• Regained:Improved profitability in corebusinesses

• Refocused:Stable growth and furtherincrease in profitability on a risk/return optimised basis

One off gains due to sale of participations1)

146 431 326 (H1 2007)

Continuous increase in operating profit – what´s next?

Full year 2007p

39 117

1) published Afs-result (without refinancing and related items)

Note: 2005, 2006 pro forma full integration of Eurohypo

625

H1 071,983

Remaining question: What´s next?

H2 expected to beweaker than H1 due to market

conditions

6 / 25

Subprime poses no threat to Commerzbank

•CB will do whatever ittakes

•CB can affordto do whatever ittakes

•Commitments of € 10bn, nearly exclusively forCB´s own conduits

•Underlying assets are of good quality•Running of sponsored conduits or SIV’s not partof our business model

Subprime

•Stable funding concept with assets matchedthrough congruent funding

•High liquidity reserve- Liquidity ratio with 1.18 more than assured- Commerzbank acted as liquidity provider of the

German banking system- Supply of € 4.5bn term money (1-3 months) to

German banks in late August/September

Liquiditysituation

CB Effects

Conduits

•Units in New York and London with RMBS/ CDO volume of € 1.2bn

•AAA position of € 0.2bn at CB Europe which isvalued at nominal level

7 / 25

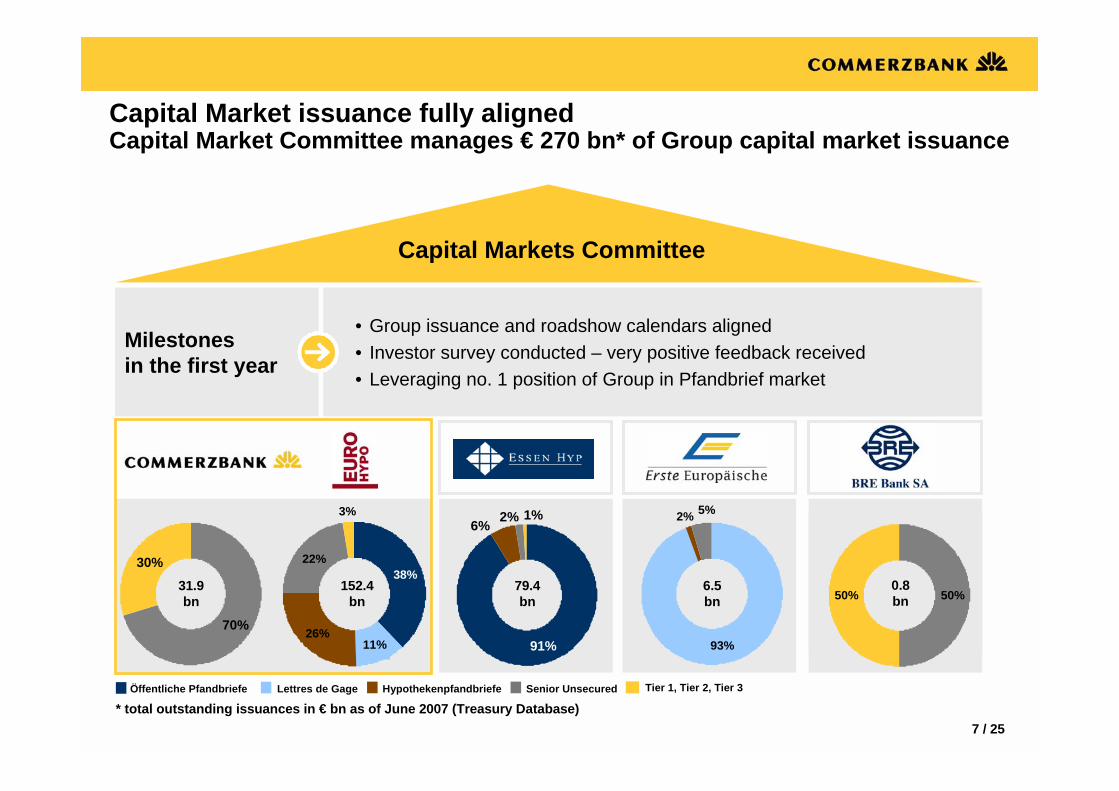

• Group issuance and roadshow calendars aligned• Investor survey conducted – very positive feedback received• Leveraging no. 1 position of Group in Pfandbrief market

Milestonesin the first year

Capital Markets CommitteeCapital Markets Committee

Tier 1, Tier 2, Tier 3Öffentliche Pfandbriefe Lettres de Gage Hypothekenpfandbriefe Senior Unsecured

6.5bn

0.8 bn

79.4 bn

152.4 bn

31.9 bn

* total outstanding issuances in € bn as of June 2007 (Treasury Database)

70%

30%

26%

22%38%

3%

11% 91%

2% 1%6%

93%

2% 5%

50%50%

Capital Market issuance fully alignedCapital Market Committee manages € 270 bn* of Group capital market issuance

8 / 25

Unsecured funding matrix

0-1Y 1-2Y 2-3Y 3-4Y 4-5Y 5-6Y 6-7Y 7-8Y 8-9Y 9-10Y > 10Y

0-1Y

1-2Y

2-3Y

3-4Y

4-5Y

5-6Y

6-7Y

7-8Y

8-9Y

9-10Y

> 10Y

Breakdown Group position “Liabilities to banks”

Liab

ilitie

s to

ban

ks

Rep

os&

col

late

ral

Ope

n m

arke

top

erat

ion

with

cen

tral

bank

Reg

iste

red

cove

red

bond

s

Pass

thro

ugh

loan

sfr

om K

fW, E

IB, e

tc.

Schu

ldsc

hein

darle

hen

plac

ed w

ith b

anks

Dep

osits

of c

entr

alba

nk c

usto

mer

s

Dep

osits

from

com

mer

cial

ban

ks

Maturing assets > liabilities

Maturing liabilities > assets

Assets

Liab

ilitie

s

Data Source: interim report & Treasury data as per 30/06/07

Maturing assets > liabilities

Maturing liabilities > assets

0

40

80

120

€bn

Sound funding structure in all maturity buckets

9 / 25

• Funding cost of commercial loan business (approx. € 210bn) only to be affected by up to 4-5 bp (increase extended over several years)

• Positive impact of widening credit margins on Group’s lending business likely to match increased funding cost

• No evidence for customer deposits to become more expensive• Issuance cost of Pfandbriefe higher than recent lows but impact limited as

more expensive Pfandbrief issues will expire• Spreads of Group’s senior unsecured capital markets funding to increase

in line with markets movements. First expectations of impact: 20-25 bp• Total outstanding unsecured debt € 60bn, to be reduced by roughly € 12

bn due to use of “refinancing register”• Funding cost to increase over several years. Effects in 2008 € 10-15m

(€ 30-35m in 2010)

What will happen?

Overall funding cost to increase moderately

Funding spreads and credit margins in general may remain at higher levels even after stressed liquidity situation of banking sector will have calmed down

Impact on assets

Outlook: Impact of increased credit spreads on Group’s P&L expected to be positive

10 / 25

Agenda

1. Status quo: record level H1 2007 figures

2. Strategic program: stable growth and improved profitability

3. Financial outlook

4. Effects: creating sustainable value

11 / 25

The leading commercial bank in Germany

Best Retail bank in Germany

Best national bank for Corporate

Customers

Europe´s leading specialist for Real Estate

Our objective: The leading commercial bank in Germany

Integrated financial platform

Equityallocation

as of 06/2007

Private & Business Customers

Mittelstand Corporates& Markets

Commercial Real Estate

PBC Private and

Business Customers

CIBCorporate Customers

and Investment Banking

Public Finance& Treasury

CREPFTCommercial Real Estate,

Public Finance and Treasury

Leading European Investment bank for

structured products and corporate customers

Europe´s leading specialist for

Public Finance

Operating RoEannualized

19%

19.8%

22% 16%31%

9%

35.4% 34.6% 15.0% 16.2%

12 / 25

Strategic program: sustainable growth and profitability

Ongoing profitability enhancementon a risk/ return optimised basis

Ongoinggrowth

Portfolio managerOriginate-and-manageloan portfolios

3.Capital managerActive equitymanagement

4.

Integrated financial platformOngoing realisation of platformsynergies

Bank of core competenciesInvestment in distinctive productlines and distribution platforms

1.Accelerating growth

and profitability

:

Internal and external initiatives

2.

CB-Growth platform

13 / 25

1. Bank of core competenciesRollout of distinctive product lines and successful distribution platforms

PBC MSB C&M CRE PFT

• Rollout derivative products (sales)

• Growth in structured finance

• Further international expansion

• Integrated public finance platform

Expansion of PBC andMSB

Accelerated growth, e.g. BRE bank, Ukraine and CB branches (esp. MSB and CRE)

Selective growth in niches with competitive advanta-ges (e.g. CRE and MSB) particularly in Asia and US

• Continued customer growth in German branches and direct banking

• Growth of assets under management in Germany

Examples

Examples • Increased market share in German SME

• International expansion of SME/ direct banking CEE

• Strengthening FI-Banking

Germany

CEE

Rest of world

• Integrated value chain

14 / 25

Active business portfolio management and further external growth• Eurohypo integration successfully completed• International Business Portfolio: active management (see below)

1. Bank of core competenciesSupported by active management of shareholdings

Examples 2007:• Jupiter, UK

- Rationale: exit from non-strategicUK asset management market;

- Transaction: sale of 100%,• PT Bank Finconesia, small bank in

Indonesia (51%), per 01/08/07 • CICM, AM Japan, ind. 100%, signed

28/08/07

Example H2 2007 : Bank Forum, Ukraine• Market: Strategic participation in fast

growing Ukrainian market• Target: Bank Forum currently

ranked number 10• Transaction: acquisition of 60% + 1

share, call option for up to 25%• Valuation: Reasonable price

Investment Divestment

15 / 25

Platform synergies, e.g.• Treasury/ Funding• Backoffice: IT, transaction banking• Strategy, accounting, financial and risk

controlling

Segment synergies, e.g.• C&M offers structured products and

services for Retail and SME-clients• MSB benefits from joint product approach

with C&M and PBC• CB-subsidiaries fully integrated

2. Integrated financial platformInterlinked business model with revenue and cost synergies

Integrated platform Effects of integration

PBC MSB C&M CRE PFT

Commerzbank platform

16 / 25

3. Portfolio manager Originate-and-manage model

Claims and securities portfolio

Outflow

•CB Origination: Loans, e.g. - German SME clients- retail customers- large customers

•Portfolio acquisition: Add-on investments in securities portfolios(high-class only)

Originate-and-manage

•Risk managementReduction bulk risks, better riskdiversification

•Margin skimmingImproved revenues

•Portfolio-sales

•Syntheticportfolio-sales

•Protection purchasevia CDS

•Securitisation(true sale, synthetic)

•Capital Efficiencycapital release, improvement RoE

17 / 25

4. Capital managerActive equity management

Development Tier I ratio and influencing factors

6.9%

+0.5- 0.7%

Mid-term

H1 2007

Basel II

Generatedearnings

?

• Business development/RWA growth

- Internal growth- External growth/divestments

• Regulatory effects- Initial Basel II release- Buffer due to increasein volatility of regulatory capital under Basel IIand IFRS influence

• Active portfoliomanagement/ contingentcapital management

• Sustainable earningsgeneration

Tier I target range: 6.5 - 7.0% adequate(based on current CB-business mix)

- RWAincrease

- Portfoliomgt.

Externalgrowth

Regula-tory:

Internalgrowth

Bank Forum

Proactive capital manage-ment to maximize value

Retain profit:• Refinance future business

activities

Capital pay-out:

• Increase of dividend • Flexible on share buy-

back

-0.2%<

18 / 25

Agenda

1. Status quo: record level H1 2007 figures

2. Strategic program: stable growth and improved profitability

3. Financial outlook

4. Effects: creating sustainable value

19 / 25

Overview main value drivers(in € m )

Outlook H2 2007H1 2006 H2 2006 H1 2007Value drivers

Net interest income (NII)(after LLPs)

Commission income

Trading profit

Operating expenses

1,7371,5271,684

1,6051,5161,449

682

454657

2,6842,6872,647

• In line with H1 2007• Franchise business well on track• LLP guidance 2007 reduced to

~ € 550m

• Strong, but seasonally weaker than H1• Dependent on equity market

development

Lower Sales & Trading in H2 due to- seasonally weaker business in equityderivatives

- difficult credit trading

• Continued cost control • Ongoing efficiency programs• Investments in growth initiatives

20 / 25

Disposal of• Germanischer Lloyd € 38m• Deutsche Börse AG € 48m• BRE’s AM-unit SAMH € 23m

Disposal of Jupiter• Proceeds from sale of Jupiter € 243m• Release of Jupiter sundry provisions € 94m• External advisory fees € -10m

Impairment of US subprime exposure € -46min Corporates & Markets

Write-downs at Commerzbank Asset € -23mManagement Asia (CAMA)

Exceptionals 2007

Positive:• Disposal of CICM Japan• Sale of real estate property in Berlin• One-off gains in Mittelstand due to judgement of

supreme tax court concerning reservemanagement above € 100m

Negative:• H2 impairment of US subprime exposure

H1 2007 effects Expected H2 2007 effects

21 / 25

Agenda

1. Status quo: record level H1 2007 figures

2. Strategic program: stable growth and improved profitability

3. Financial outlook

4. Effects: creating sustainable value

22 / 25

Revenuesincl. LLPs

Costs

Net profit1)

Averageequity

Clean netRoE2)

Value drivers (€ m)

16.0%

Outlook CB group: Further increase in growth and profitability

>12%

4,667

2,684

1,377

13,493

11.2%

8,049

5,334

1,597

12,203

Value drivers: current figures and outlook

2006 H1 20072007p (vs. 2006)

2008-2010p Outlook

• Ongoing internal and external growth

• Continued cost discipline • Investment in growth programs

• Positive profit dynamics over time

• As of 01/01/2008 Basel II conversion -projected capital release of ~10%

• Proactive capital management: investment in growth, return of potential surplus capital

• Continuous improvement in RoE above 15% to achieve standards compared to international peers

2) Clean: excluding net result on participations and restructuring charges1) 2006 figure based on stated result

23 / 25

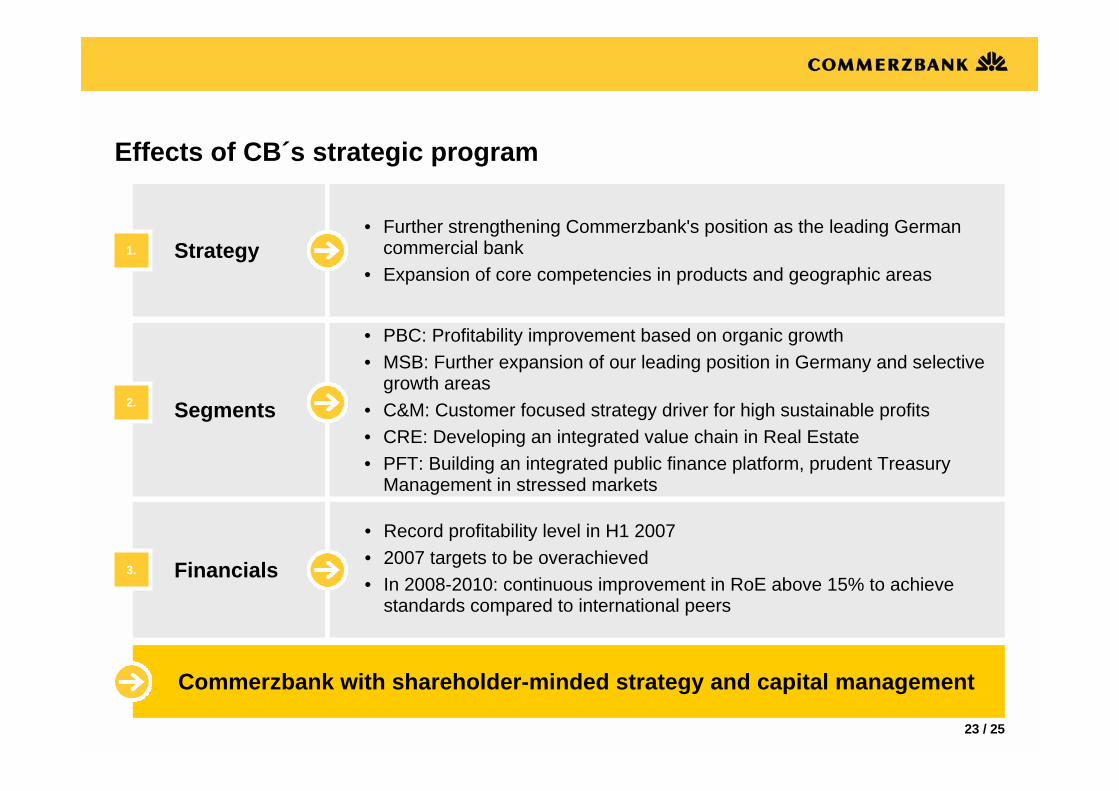

• PBC: Profitability improvement based on organic growth• MSB: Further expansion of our leading position in Germany and selective

growth areas• C&M: Customer focused strategy driver for high sustainable profits• CRE: Developing an integrated value chain in Real Estate • PFT: Building an integrated public finance platform, prudent Treasury

Management in stressed markets

Effects of CB´s strategic program

Financials

• Record profitability level in H1 2007• 2007 targets to be overachieved• In 2008-2010: continuous improvement in RoE above 15% to achieve

standards compared to international peers

Segments

Strategy• Further strengthening Commerzbank's position as the leading German

commercial bank• Expansion of core competencies in products and geographic areas

Commerzbank with shareholder-minded strategy and capital management

1.

3.

2.

24 / 25

Appendix Group equity definitions

25 / 25

Group equity definitions

Reconciliation of equity definitions

Basis for RoE on net profit

Equity basis for RoE

Basis for operating RoE and pre-tax RoE

* excluding:• Revaluation reserve• Cash flow hedges• Consolidated profit

Equity definitions in € m Jun-2007

Subscribed capital 1,708

Capital reserve 5,705

Retained earnings 5,122

Reserve from currency translation -51

Investors‘ capital excluding minorities 12,484

Minority interests (IFRS)* 1,063

Investors‘ Capital 13,547

Change in consolidated companies; goodwill; consolidated net profit minus portion of dividend; others

-7

BIS core capital excluding hybrid capital 13,540

Hybrid capital 3,096

BIS Tier I capital 16,636

Jan-Jun 2007

1,707

5,702

5,158

-133

12,434

1,059

13,493

Disclaimer

/ investor relations /

This presentation has been prepared and issued by Commerzbank AG. This publication is intended for professional and institutional customers./Any information in this presentation is based on data obtained from sources considered to be reliable, but no representations or guarantees are made by Commerzbank Group with regard to the accuracy of the data. The opinions and estimates contained herein constitute our best judgement at this date and time, and are subject to change without notice. This presentation is for information purposes, it is not intended to be and should not be construed as an offer or solicitation to acquire, or dispose of any of the securities or issues mentioned in this presentation./Commerzbank AG and/or its subsidiaries and/or affiliates (herein described as Commerzbank Group) may use the information in this presentation prior to its publication to its customers. Commerzbank Group or its employees may also own or build positions or trade in any such securities, issues, and derivatives thereon and may also sell them whenever considered appropriate. Commerzbank Group may also provide banking or other advisory services to interested parties./Commerzbank Group accepts no responsibility or liability whatsoever for any expense, loss or damages arising out of, or in any way connected with, the use of all or any part of this presentation./Copies of this document are available upon request or can be downloaded from www.ir.commerzbank.com

27 / 25

Jürgen Ackermann (Head of IR)P: +49 69 136 22338M: [email protected]

Sandra Büschken (Deputy Head of IR)P: +49 69 136 23617M: [email protected]

Wennemar von BodelschwinghP: +49 69 136 43611M: [email protected]

Ute Heiserer-JäckelP: +49 69 136 41874M: [email protected]

Simone NuxollP: +49 69 136 45660M: [email protected]

Stefan PhilippiP: +49 69 136 45231M: [email protected]

For more information, please contact Commerzbank´s IR team:

Karsten SwobodaP: +49 69 136 22339M: [email protected]

Andrea Flügel (Assistant)P: +49 69 136 22255M: [email protected]

www.ir.commerzbank.com