Embed Size (px)

Citation preview

© 2

014

Mor

rison

& F

oers

ter L

LP |

All R

ight

s R

eser

ved

| mof

o.co

m

Committee on Foreign Investmentin the United States

(CFIUS)March 27, 2014

Robert S. TownsendMorrison & Foerster LLP

2

It is the established policy of the U.S. government to “support unequivocally” international investment in the United States, “consistent with the protection of the national security.”

Source: Executive Order 13456, January 23, 2008, section 1.

3

What is CFIUS?

An executive branch interagency committeechaired by the Secretary of the U.S. Treasury Department

Authorized by statute to review transactions that could result in control of a U.S. business by non-U.S. persons in order to determine the effect of such transactions on the national security of the United States

4

Brief OverviewCFIUS reviews foreign acquisitions, mergers

and takeovers of U.S. businesses that may raise national security issues

CFIUS has the authority to approve a transactionor send it to the President for his decision

CFIUS operates on statutory deadlines consisting of an initial 30-day review, a possible further 45-day investigation, and a possible 15-dayPresidential decision

5

Origins of CFIUS Created in 1975Charged with monitoring the impact of and coordinating U.S. policy on foreign investment in the U.S.No explicit enforcement power

“Exon-Florio Amendment” passed in 1988 as part of the Defense Production Act of 1950Provided the President with express authority to review the national security effects of foreign investments and, if necessary, block such transactionsPresident delegated the new authority to CFIUS, but retained authority to ultimately block foreign investments

Following controversy caused by the Dubai Ports World acquisition of a U.S. port management business in 2006, Congress enacted the Foreign Investment and National Security Act of 2007 (FINSA)

FINSA codified and amended the CFIUS process to implement policies and procedures that CFIUS had informally applied to notified transactions

6

CFIUS Law Statute: Foreign Investment & National Security Act (FINSA),

effective as of October 24, 2007, amending Exon-Florio Amendment of 1988

Executive Order 11858: Amended as of January 23, 2008 Regulations: Final regulations published November 21, 2008 and

effective December 22, 2008, following enactment of FINSA Guidance: Published December 8, 2008, describes types of

transactions CFIUS reviews and that present national security concerns

CFIUS law references are publicly available at: http://www.treasury.gov/resource-center/international/Pages/Committee-on-Foreign-Investment-in-US.aspx

7

CFIUS MembershipDepartment of the Treasury (Chair)

8 other permanent voting members: Department of Justice Department of Homeland Security Department of Commerce Department of Defense Department of State Department of Energy Office of the U.S. Trade Representative Office of Science & Technology Policy

Treasury appoints a lead agency or agencies for each transaction notified to CFIUS

2 permanent non-voting members:• Department of Labor• Director of National Intelligence

5 observing members:• Office of Management & Budget• Council of Economic Advisers• National Security Council• National Economic Council• Homeland Security Council

8

Covered Transactions CFIUS can review any merger, acquisition, or

takeover by or with any foreign person which could result in foreign control of any person engaged in interstate commerce in the United States that may implicate national security issues

Certain transactions, such as “greenfield” investments, are exempt from the scope of FINSA

CFIUS does not provide “no action letters” or informal guidance, thus it is necessary for parties to file a full formal notification to CFIUS to confirm that a transaction is not a “covered transaction”

9

Control CFIUS broadly interprets the concept of control as “the

power, direct or indirect, whether or not exercised or exercisable through the ownership of a majority or a dominant minority of the total outstanding voting securities of an issuer, or by proxy voting, contractual arrangements or other means, to determine, direct or decide matters affecting an entity.”

Even a 10% investment in a U.S. company by a foreign entity may be deemed to convey control for purposes of FINSA

The acquisition of a U.S. company by a company in which a foreign entity has a 10% interest may also be deemed to result in foreign control of a U.S. company

10

Control CFIUS regulations provide that the acquisition of 10% or less of the voting

interests of an entity made “solely for the purpose of passive investment” is not subject to FINSA

The regulations include a list of minority shareholder protective rightsthat are not be deemed to confer control, including:power to prevent the sale of the assets of an entityprohibitions on changes to the organizational documents of an entityanti-dilution protection

However, CFIUS may view an acquisition of a 9% voting interest and a board seat as conferring control

Other factors that may indicate control include: “special shares” giving special rights the ability to appoint executive officerscontrol of budgetary mattersaccess to proprietary data

Whether “control” exists for purposes of FINSA will depend on the specific facts of a transaction

11

National Security

CFIUS review focuses solely on addressing national security issues and not other national interests

CFIUS law does not define “national security” although it does provide a list of indicative factors of consideration in evaluating the effects of a proposed transaction on national security

12

Factors CFIUS ConsidersNational security considerations include an investment’s effects on:

• domestic production needed for national defense requirements

• U.S. critical technologies and infrastructure• posing a regional military threat to U.S. interests• long-term projection of U.S. requirements for critical

resources (such as energy)• whether a covered transaction will result in foreign-

government control

13

Factors CFIUS Considers Many CFIUS reviews involve:classified defense or homeland security-related contractssole-source contracts with federal, state or local governmentscritical or emerging technologies and infrastructure technologies or products subject to export control restrictions foreign government-controlled investors making sensitive investments

Although the majority of CFIUS reviews involve defense-related acquisitions, CFIUS has reviewed transactions in the following industries, among many others: telecommunicationsaerospacesoftwareengineeringchemicals and pharmaceuticals

CFIUS does not typically review transactions in the financial servicessector, unless they involve particular national security assets or considerations, due to the existence of other robust regulatory authority in this sector

14

Notification CFIUS notification is a joint submission by the parties to a transaction and must include

information regarding: the nature of the transaction and identity of the parties the activities, assets and location of the U.S. company and any subsidiarieswhether the target is a supplier to any defense or national securities agencies (including a

list of any relevant U.S. government contracts)whether the target makes any products or has any technologies which have or could have

military applications or that are subject to export control licensing requirements the proposed intent of the acquiring partywhether the acquiring party is subject to foreign government controldetailed biographical information on the acquirer’s officers and directors

Section 721 of the CFIUS regulations prohibits disclosure to the public of information filed with CFIUS, and explicitly provides that such information is exempt from disclosure under the Freedom of Information Act (FOIA)

This confidentiality requirement applies to any information provided by the parties: in connection with a pre-notice consultation or a draft noticeas part of an initial notice in response to any follow-up questions from CFIUS

There is no filing fee for submitting a CFIUS notice

15

CFIUS Review Process

Pre-filing consultation

Initial 30-day review

Extended 45-day investigation

Mitigation agreement

Presidential determination

16

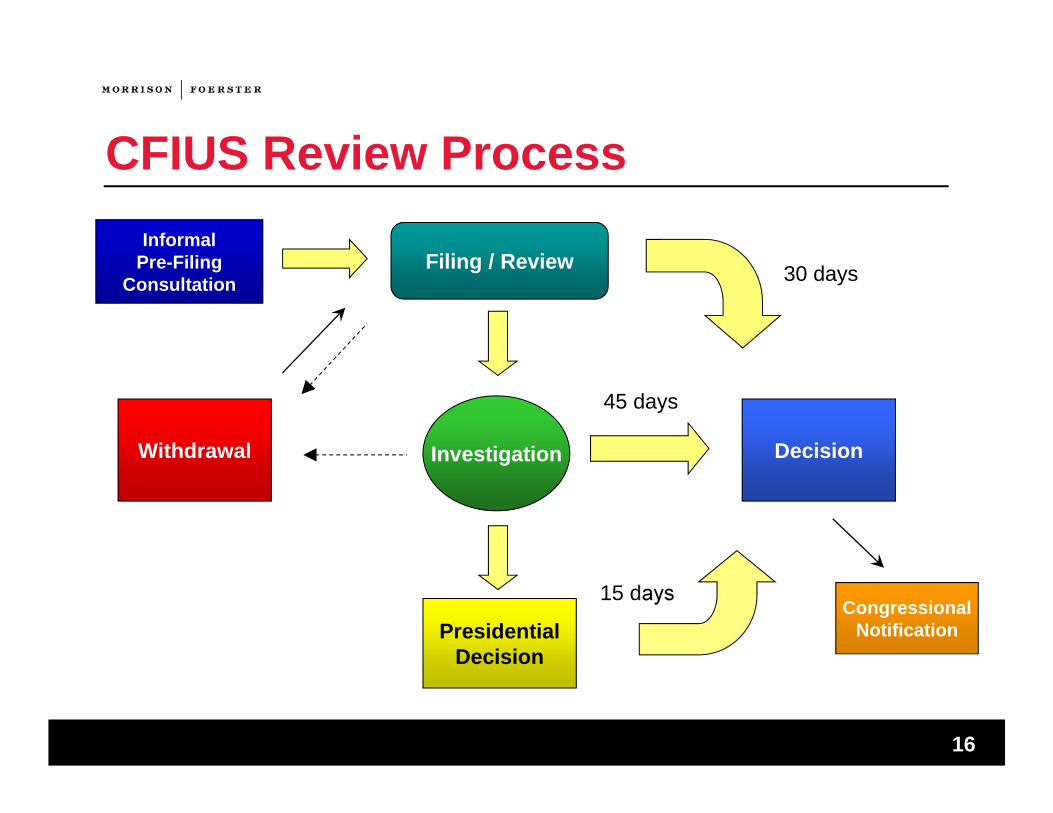

CFIUS Review Process

Filing / Review 30 days

Investigation

45 days

15 days

DecisionWithdrawal

PresidentialDecision

CongressionalNotification

InformalPre-Filing

Consultation

17

Pre-Filing Consultation The long-standing practice of engaging in pre-filing consultations

with CFIUS was formalized in the CFIUS regulations following FINSA

Parties typically engage CFIUS prior to the execution of transaction documents to identify any threshold issues, and provide CFIUS drafts of the notification prior to formal submission

The objective of pre-filing discussions is to provide CFIUS members with sufficient information about the parties and the proposed transaction to enable CFIUS to begin its assessment of the activities of the target U.S. company that may implicate national security concerns

These discussions also permit the parties to assess the likelihood that the transaction may be cleared during the initial 30-day reviewperiod, or whether an extended 45-day investigation may be required

18

Initial 30-Day Review Commencing upon receipt of a complete notification, CFIUS undertakes an initial 30-day

review of the proposed transaction

The Director of National Intelligence is required to complete a national security threat analysis within 20 days of the notification

During this period, the parties to the transaction are likely to be engaged in discussions with the lead agency or agencies, providing supplemental information and responding to specific questions

It is also common to provide CFIUS (either the full membership or interested agencies) with more detailed briefings, which may involve executives from the U.S. and foreign companies

With the consent of CFIUS, companies may withdraw and re-file a notification in order to give CFIUS additional time to review and approve their transaction without commencing an extended 45-day investigation

The vast majority of notified transactions are approved during the initial 30-day review periodHowever, the past few years have seen an increase in the number of investigations

undertaken

19

Extended 45-Day Investigation If CFIUS is unable to complete its review during the initial 30-day period,

CFIUS undertakes an extended 45-day investigation

In most cases, the parties are able to determine well in advance of the conclusion of the initial review whether an investigation may be initiated(or whether to withdraw and resubmit the notification); however, CFIUS can raise national security concerns at any time during the initial review period

There are two special circumstances under which FINSA requires a full 45-day investigation: when the transaction could result in control of a U.S. entity by a foreign government or an entity controlled by a foreign governmentwhen the transaction would result in control of any domestic criticalinfrastructure by any foreign person

Even if the transaction involves a foreign government-owned entity or critical infrastructure, an extended investigation is not required if the Secretary of the Treasury and the lead agency determine that the transaction will not impair national security

20

Mitigation Agreement CFIUS may require parties to enter into a mitigation agreement to address

national security concerns raised by the proposed transaction based on a risk analysis conducted by CFIUS

The terms of mitigation agreements are confidential and often include commitments by the foreign acquiring entity to refrain from certain actionswith respect to the operations of the U.S. company, along with restrictions on access to sensitive technologies

FINSA requires CFIUS to evaluate compliance of the parties with a mitigation agreement, although even before FINSA, CFIUS routinely monitored and audited mitigation agreement compliance as a matter of policy

If there is a material breach of a mitigation agreement, CFIUS may initiate a new 30-day review of the transaction

21

Presidential Determination If CFIUS does not clear a transaction during the 45-day investigation and

the notification is not withdrawn, CFIUS presents a report and recommendation to the President who has 15 days to approve or block the transaction

There have been only two instances where the President has used his authority to order the divestment of an acquisitionIn 1990, the President invalidated a transaction that involved the acquisition by China’s National Aero-Technology Import and Export Corporation of MAMCO Manufacturing, Inc., an aircraft component manufacturer located in Seattle, WashingtonIn September 2012, the President ordered that Ralls Corporation, ultimately owned by Chinese entities, divest certain wind farm assets held in Oregon within three months

Over the past 20 years, only five CFIUS transactions have gone to the President for a final determination

22

Possible Outcomes Transaction approved Transaction approved subject to mitigation

agreement Transaction renegotiated to address national security

concerns Transaction blocked/abandonedOccurs occasionally if the parties and CFIUS are not able to reach a mutually

acceptable mitigation agreement, or the transaction encounters significant political oppositionMany high-profile abandoned transactions involve China

Divestment

23

Congressional Notification Under FINSA, the Secretary of the Treasury and the head of the lead agency must

notify Congress of completed reviews and extended investigations Such notices include:description of actions taken by CFIUS identification of the determinative factors considered in the decisionstatement confirming there are no unresolved national security concerns related

to the transaction On a classified basis, members of Congress may request briefings on covered

transactions for which action has concluded or on compliance with a mitigation agreement

The Secretary of Treasury must also provide an annual report to Congress on covered transactions for which national security reviews or investigations were initiated

The report must include information regarding: the volume of transactions reviewed for each procedural step of the CFIUS review

process types of security arrangements entered intoperceived adverse effects of covered transactions on U.S. national security

CFIUS reports to Congress are publicly available at: http://www.treasury.gov/resource-center/international/foreign-investment/Pages/cfius-reports.aspx

24

Best Practices Political as well as legal process

Cooperation and good faith generally rewarded

Develop the political and public relations messageearly in the process

Take advantage of pre-filing consultation

Ensure adequate compliance program post-transaction

25

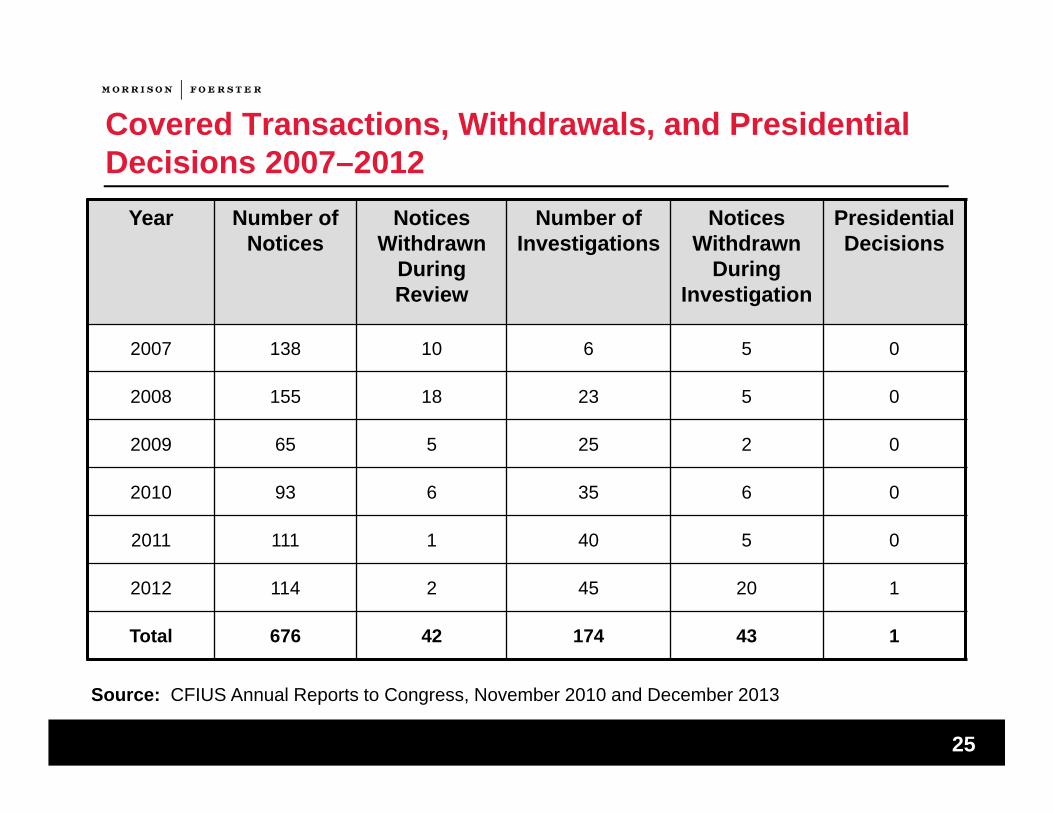

Covered Transactions, Withdrawals, and Presidential Decisions 2007–2012

Year Number of Notices

Notices Withdrawn

During Review

Number of Investigations

Notices Withdrawn

During Investigation

Presidential Decisions

2007 138 10 6 5 0

2008 155 18 23 5 0

2009 65 5 25 2 0

2010 93 6 35 6 0

2011 111 1 40 5 0

2012 114 2 45 20 1

Total 676 42 174 43 1

Source: CFIUS Annual Reports to Congress, November 2010 and December 2013

26

Importance of Filing with CFIUS Filing with CFIUS is voluntary but recommended if a

transaction may raise national security issues

CFIUS reviews less than 10% of all inbound foreign transactions

However, CFIUS actively monitors investment activity and can self-initiate a review of a transaction that is not filed voluntarily

Transactions not reviewed by CFIUS can be examined at any time in the future and can be exposed to mitigation remedies, including divestiture

27

U.S. Government Agency Regulation of Foreign Ownership, Control, and Influence

The Department of Defense (DOD), Department of Energy (DOE), and the Nuclear Regulatory Commission (NRC) regulate Foreign Ownership, Control or Influence (FOCI) with respect to companies in the national security sector

The Defense Security Service (DSS) conducts adjudication of FOCI factors of contractors performing classified contracts under the National Industrial Security Program

28

Agency Regulation of FOCI

Directive-Type Memorandum (DTM) 09-019 –Policy Guidance for Foreign Ownership, Control, or Influence (FOCI), dated September 2, 2009National Industrial Security Program Operating

Manual (NISPOM), updated February 28, 2006

FOCI Guidance:

29

Agency Regulation of FOCI FOCI issues arise when the activities of a company involve access to

classified information

Indicative personnel and information system security requirementsof such company activities may include the following:Facility Clearance, an administrative determination that, from a national security standpoint, a facility is eligible for access to classified information at the same or lower classification category as the clearance being granted

Personnel Security Clearance, an administrative determination that an industrial employee is eligible for access to classified information

Certification and accreditation of information technology systems processing classified information at contractor facilities cleared under the National Industrial Security Program

30

Agency Regulation of FOCI

Under DTM 09-019, a company is considered to beoperating under FOCI whenever a foreign interest hasthe power, direct or indirect, whether or not exercised, and whether or not exercisable, to direct or decide matters affecting the management or operations of that company in a manner which may result in unauthorizedaccess to classified information or may adversely affect the performance of classified contracts

31

Agency Regulation of FOCI NISPOM requires that a form SF 328 be submitted

during the initial facility clearance process and when significant changes occur to information provided previously

DSS requires a company with a facility security clearance to notify DSS at the commencement of entering into negotiations for a proposed merger, acquisition, or takeover by a foreign interest

32

Agency Regulation of FOCI

the type of transaction under negotiation (stock purchase, asset purchase, etc.)

the identity of the potential foreign investor

a plan to mitigate/negate the FOCI

whether the parties to the proposed transaction will be filing a notice with CFIUS

The company is required to provide DSS with the following information:

33

Agency Regulation of FOCI

DSS will only allow a company to maintain a valid Facility Clearance if an acceptable FOCI mitigation plan has been agreed upon and approved by DSS

FOCI mitigation plans must be consistent with NISPOM requirements

The elements of the plan will depend on the circumstances of the potential FOCI

34

Agency Regulation of FOCI

Board Resolutions may be appropriate when a foreign interest does not own voting interests sufficient to elect directors or is not entitled to representation on the company’s board

Security Control Agreements may be appropriate when a foreign interest does not effectively own or control a company or corporate family but is entitled to representation on the company’s board

Special Security Agreements may be appropriate when a foreign interest effectively owns or controls a company or corporate family

Voting Trust or Proxy Agreement are arrangements whereby the foreign owner relinquishes most rights associated with ownership of the company to cleared U.S. citizens approved by the U.S. Government, and may be appropriate when a foreign interest effectively owns or controls a company or corporate family

Plans may include the following types of mitigation measures: