Embed Size (px)

Citation preview

Commodity Prices, Government Policies and Competition

Steve McCorristonUniversity of Exeter, UK

WTO/CUTS Symposium on “Trade in Primary Product Markets and Competition Policy”

WTO, Geneva, 22nd September, 2011

Structure of the Presentation

• Recent events (quickly!)

• Characteristics of world commodity markets and commodity price behaviour

• Government policies

• Overview of sources of competition concerns

• Why does competition matter?

• Issues that still need to be addressed

Three broad observations

• Competition issues in commodity and food markets, and how they impact on the behaviour of prices, has received comparatively little (but not no) attention

• Need to make the distinction between commodity and food markets-this is important in identifying where competition issues may arise

• Why do departures from competition matter in the context of commodity and food markets?

Brief Overview of Recent Events

• Recent commodity price spikes• ….coming against the background of relatively

previously low prices

• ‘Spike’ less significant than the 1972-74 commodity crisis in real terms

• Widespread commentary on the potential causes of the recent events

Figure 1: Monthly Food Price Index, 1990-2010

Source: FAO

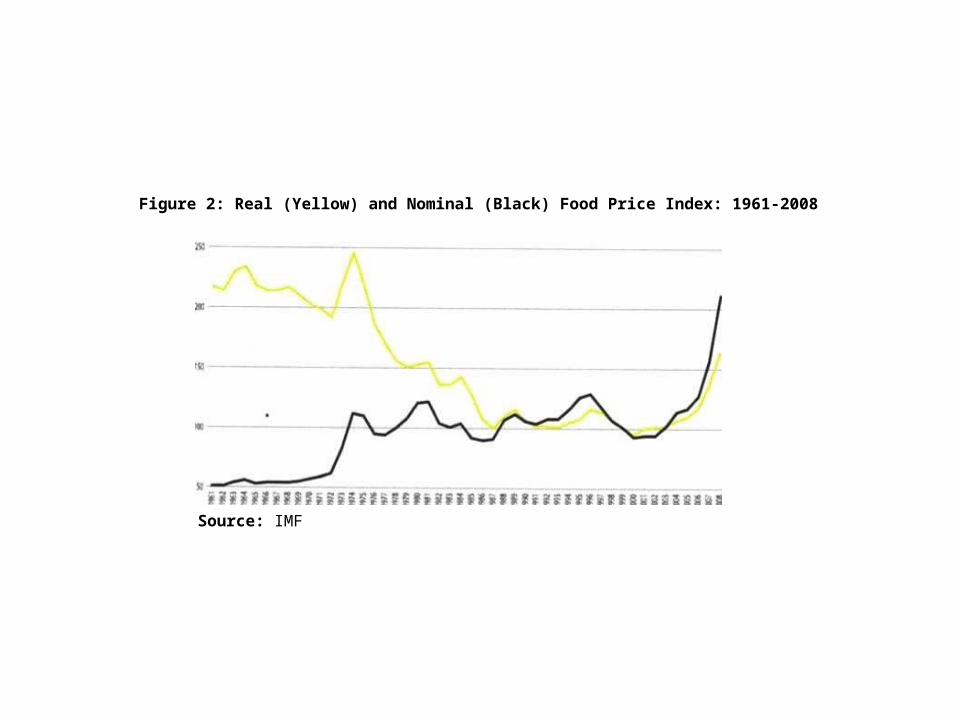

Figure 2: Real (Yellow) and Nominal (Black) Food Price Index: 1961-2008

Source: IMF

What do we know about the behaviour of commodity prices?

• Long term: Prebisch-Singer hypothesis.

Taken over the long-run, there will be a secular tendency for the relative prices of primary commodity prices to decline

• Differences in income elasticities and market structure

• Evidence? Mixed with the challenge of allowing for structural breaks.

Volatility

• Prices change (a lot) but the issue here is to do with the amplitude and frequency of price changes that causes problems for producers and consumers

• Why? Low demand and supply elasticities

• Commodity prices may be more volatile than other prices but there is no evidence that over the medium to long-run that commodity price volatility has increased.

Commodity price ‘spikes’

• Related to but distinct from volatility

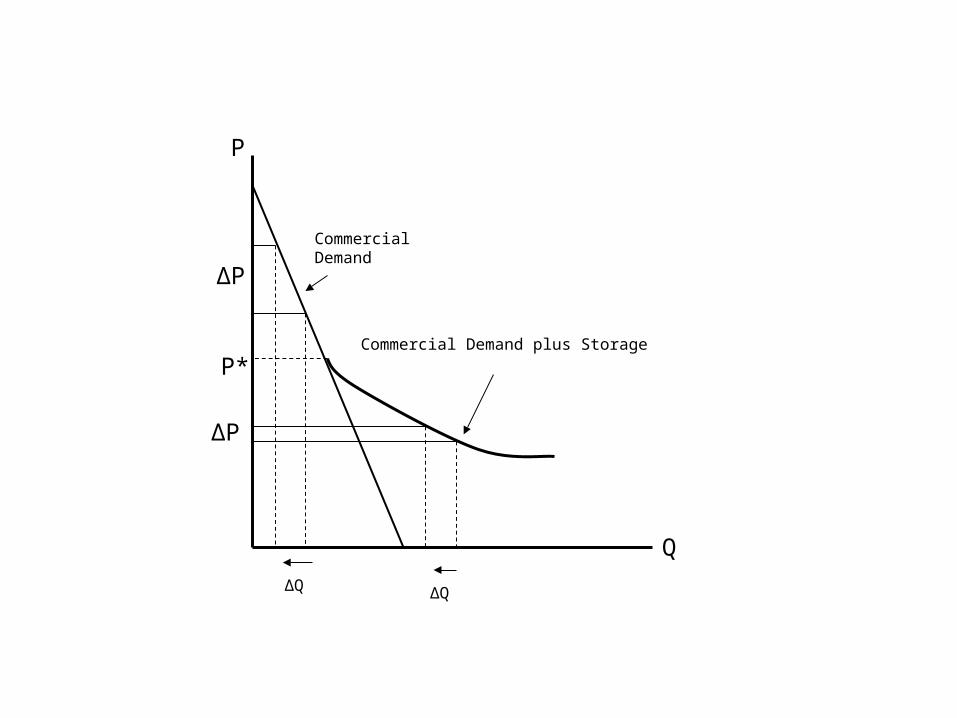

• Underlying characteristic of many commodities is that they are storable-there is an inter-temporal aspect to commodity markets.

• The demand curve is non-linear

• This changes the way in which we think about the impact of shocks depending where we are on the demand curve i.e. if stocks are high or low

Commercial Demand

Commercial Demand plus Storage

P*

P

Q

ΔQΔQ

ΔP

ΔP

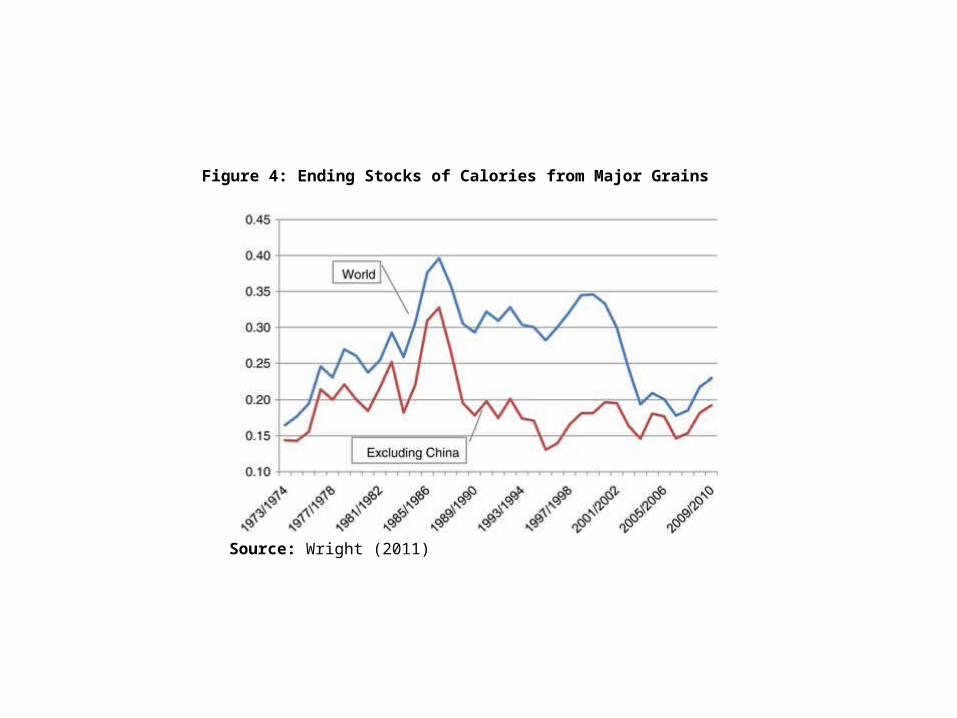

Figure 4: Ending Stocks of Calories from Major Grains

Source: Wright (2011)

Implications of this for understanding commodity price behaviour

• Possibility of stock outs• Commodity prices characterised by:….asymmetry (long periods of low prices

punctuated with short lived high prices)….changing variance….positive skewness….excess kurtosis

• Evidence: not overwhelming!

Government Policies

• Agriculture is one of the sectors where markets have and are highly distorted by government policies.

• Wide range of policy interventions (domestic and trade) that have impacted on the progress of trade negotiations

• Cuts the link between what happens domestically and what happens on world markets

• But national policies also impose an externality on world markets

…low (high) domestic prices raises (lowers) world market prices

…as government policies seek domestic security, world markets become more volatile

…the export supply/import supply schedules become more inelastic.

World commodity and domestic food prices

• Behaviour can be very different

• The impact of world commodity market shocks not fully transmitted to changes in domestic market food prices

• Horizontal and vertical price transmission

• Domestic food prices can be more stable than world market commodity prices

Figure 5: World and Domestic Prices for Selected Developing Countries

Source: IMF

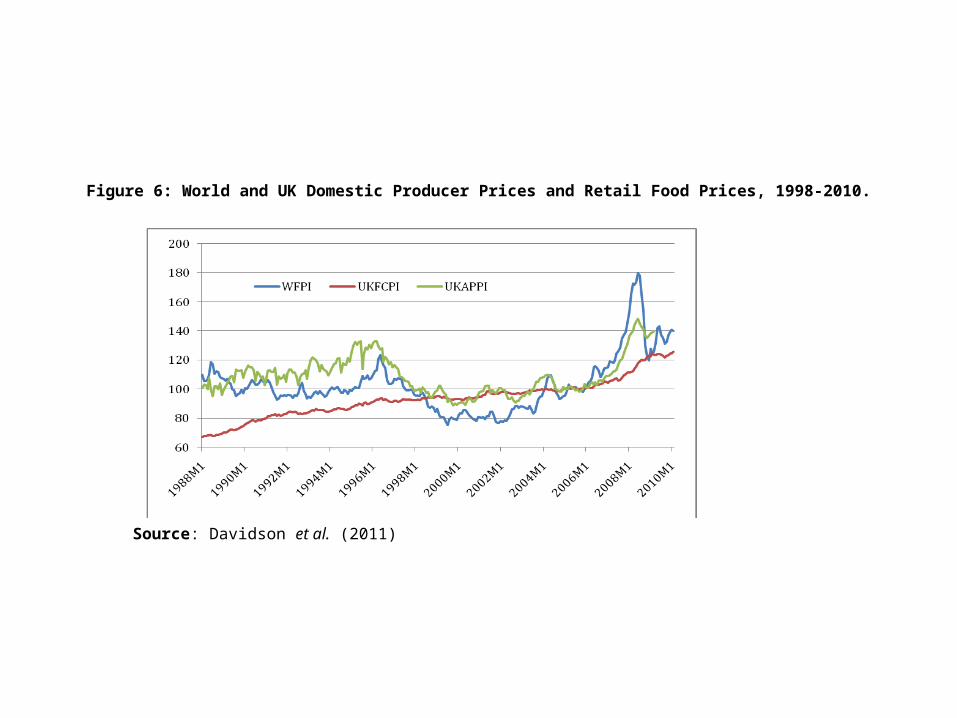

Figure 6: World and UK Domestic Producer Prices and Retail Food Prices, 1998-2010.

Source: Davidson et al. (2011)

Competition Issues

• Largely ignored: concerns about competition in commodity and food markets can arise locally, nationally and internationally

• Can involve the state or private firms and can impact within or across borders

State Manipulation of Market Structure

• International commodity agreements (?)

• State sanctioned cartels

• State trading enterprises…not per se associated with state ownership but direct manipulation of markets both domestic and with respect to trade

Competition concerns relating to private firms

• Cartels, domestic and across borders

• Downstream markets (i) Export supply chains (Porto et al. (2011) on

coffee, cotton and cocoa sectors)(ii) vertically-related and imperfectly-competitive

domestic food markets…successive oligopoly(iii) Market power concerns (buyer and selling)

within and between stages

Domestic ag.

comms

World Markets

ProcessingSector

Retailing Sector

Consumers

Competition and Regulation throughout Food Chain

Input sector

Competition issues related to commodity markets

Competition issues in the upstream input sector

Characteristics of Food Markets

• High levels of concentration at all stages (processing and retailing)…successive oligopoly

• Tendency towards increasing concentration• Consolidation and M&As both domestically and

nationally• Between (not just within) stage issues also

matter• But note, other inputs will matter too for the final

price of food products at the retail sector

Why does it matter?

• Potential abuse of market power

• Selling and buyer power may matter

• Price transmission effects

• Behaviour of prices for downstream products differs from upstream commodity markets

• Net welfare and distributional effects associated with price shocks

Figure 6: Change in Exporters’ Producer Surplus from Trade Liberalization

0.00

0.02

0.04

0.06

0 0.2 0.4 0.6 0.8 1

Market Power Index

Pro

du

cer

Su

rplu

s C

han

ge

Oligopsony Oligopoly

Oligopsony & Oligopoly Successive Oligopsony with Oligopoly

Successive Oligopoly with Oligopsony

Figure 7: Change in Producer Surplus, Consumer Surplus

and Marketers' Profits from Trade Liberalization for the case

of Successive Oligopoly with Processor Oligopsony

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0 0.2 0.4 0.6 0.8 1

Market Power Index

Pro

du

cer

Su

rplu

s, C

on

sum

er S

urp

lus,

M

arke

ters

' Pro

fits

Producer surplus Consumer surplus Marketers' profits

Observations

• Competition will matter in a variety of contexts

• Commodities are only one part of the food chain and may represent a small share of the final food product

• So, other issues matter too.

• But small deviations in competition can have large effects particularly on the distribution of welfare following shocks

Further issues

• How does competition impact on the volatility of prices?

• How do departures from the competitive benchmark impact on risk exposure for farmers and consumers?

• How do departures from competition in domestic markets impact on world markets?

• How do departures from competition and its impact on volatility impact on investment?