Embed Size (px)

Citation preview

Companies Bill 2012Companies Bill 2012

CS. Asish MohanDirector

WWW.ARTISMC.COM

Senior PartnerSenior PartnerABP & AssociatesCompany SecretariesKochi, Trivandrum, Bangalore, Mumbai,Delhi

(C) Artis Management Consultants 1

Why new Companies Bill ?Why new Companies Bill ?

� This presentation is based on Companies Bill 2012.

� In view of the changes happening at the National /International economic environment and expansion andgrowth of the country , the Central Government afterdue deliberations decided to repeal the present act andbring in a new legislation to meet these requirements.bring in a new legislation to meet these requirements.

� Various attempts were made by various governments ofthe day to bring in a new legislation, the last being theCompanies Bill 2012.

(C) Artis Management Consultants 2

Status of the Present BillStatus of the Present Bill

� The Companies Bill 2012 has been passed by LOK SABHA on 18.12.2012.

� Once the same goes through the RAJYA SABHA and technical formalities being SABHA and technical formalities being completed , the same will be become an Act soon.

(C) Artis Management Consultants 3

Presentation StructurePresentation Structure

� This presentation is based on what's newin the bill.

� Will be focusing on the new and� Will be focusing on the new andimportant provisions of the bill

� Will be taking in a chapter wise manner.

(C) Artis Management Consultants 4

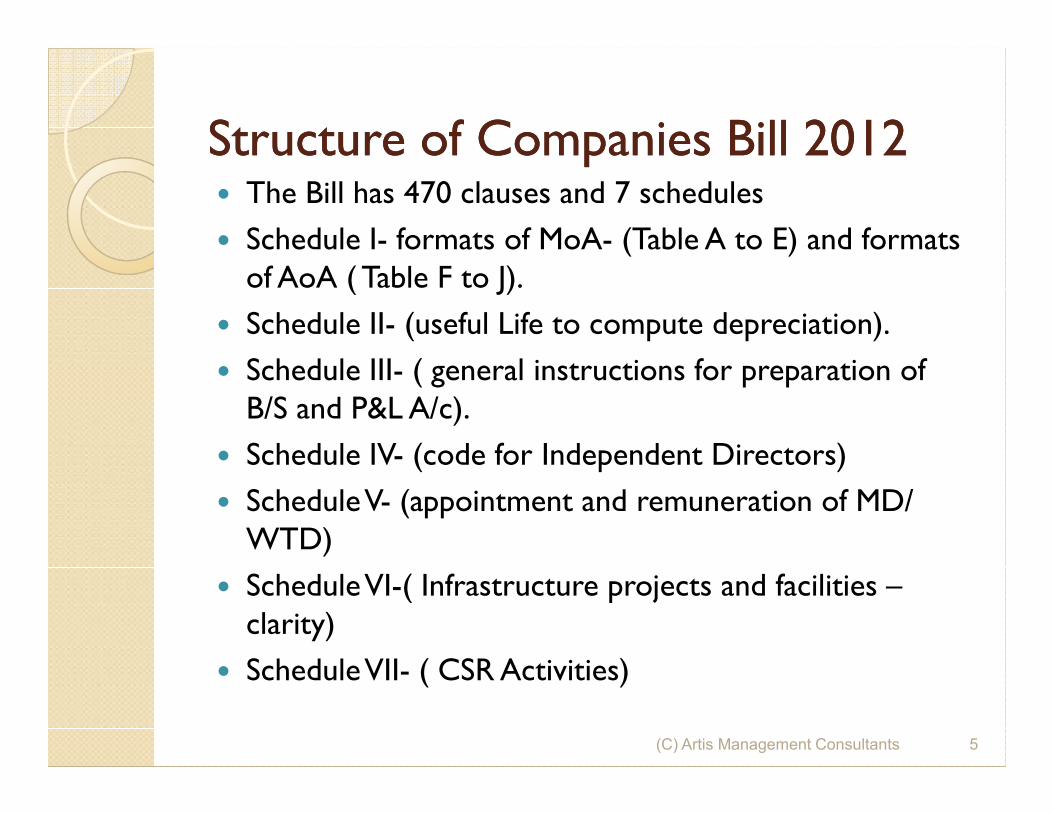

Structure of Companies Bill 2012Structure of Companies Bill 2012� The Bill has 470 clauses and 7 schedules

� Schedule I- formats of MoA- (Table A to E) and formats of AoA ( Table F to J).

� Schedule II- (useful Life to compute depreciation).

� Schedule III- ( general instructions for preparation of B/S and P&L A/c).B/S and P&L A/c).

� Schedule IV- (code for Independent Directors)

� Schedule V- (appointment and remuneration of MD/ WTD)

� Schedule VI-( Infrastructure projects and facilities –clarity)

� Schedule VII- ( CSR Activities)

(C) Artis Management Consultants 5

Part Part --11

�APPLICABILITY OF BILLBILL

(C) Artis Management Consultants 6

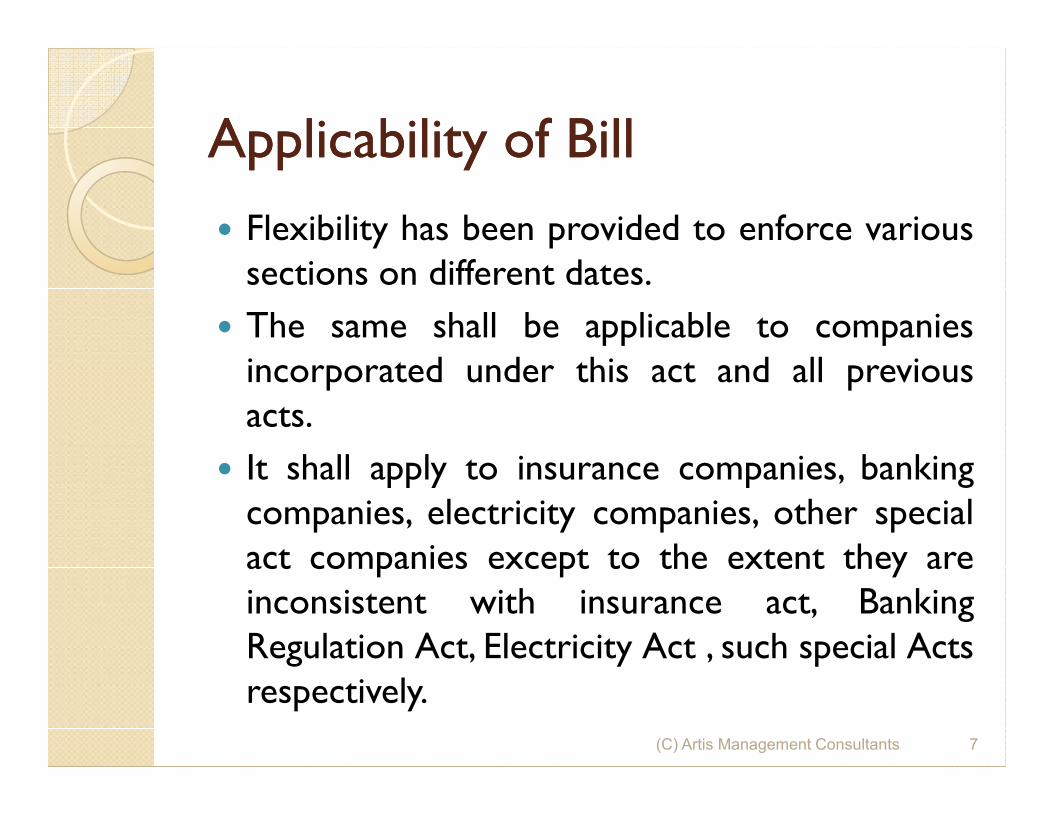

Applicability of BillApplicability of Bill

� Flexibility has been provided to enforce varioussections on different dates.

� The same shall be applicable to companiesincorporated under this act and all previousacts.acts.

� It shall apply to insurance companies, bankingcompanies, electricity companies, other specialact companies except to the extent they areinconsistent with insurance act, BankingRegulation Act, Electricity Act , such special Actsrespectively.

(C) Artis Management Consultants 7

Some new important definitions Some new important definitions addedadded--clause 2 (95 definitions in total)clause 2 (95 definitions in total)� Auditing standards

� Associate Company

� CEO

� CFO

� ESOP

� Financial Statement� Financial Statement

� Financial Year

� GDR

� Independent Director

� KMP

� One Person Company

� Promoter

� Small Company

� Turnover

(C) Artis Management Consultants 8

Part Part --22

INCORPORATION RELATED RELATED MATTERS

(C) Artis Management Consultants 9

Incorporation Related MattersIncorporation Related Matters--NEW ENTITYNEW ENTITY� The Bill provides for a new form of entity –ONE PERSON

COMPANY (OPC), along with the Public and normal PrivateLimited Companies.

� The Memorandum of the OPC shall indicate the name of the otherperson, with his prior consent in the prescribed form withROC, who shall in the event of the subscribers death become themember.member.

� The person can withdraw his consent in such manner as may beprescribed.

� The member of the OPC can change the name of such otherperson by giving notice in the prescribed manner.

(C) Artis Management Consultants 10

Incorporation Related MattersIncorporation Related Matters--Membership of a Private CompanyMembership of a Private Company

�The maximum number of Members has been increased Members has been increased

from 50 to 200.

(C) Artis Management Consultants 11

Incorporation Related MattersIncorporation Related Matters

� Memorandum Contents

The bill does not require the object clause to be classified as main objects, incidental objects and other objects.and other objects.

It seems that the provisions of section 149(2A) of the present Act would not apply and Special Resolution for carrying on other objects would not be required. ( rules may be brought in)

(C) Artis Management Consultants 12

Incorporation Related MattersIncorporation Related Matters

� Alteration of Object clause-new changesIf the company has unutilized amounts of public issue, in addition to passing a Special Resolution for alteration of object clause, publish notice of such resolution in newspapers (English and vernacular) and place it on the newspapers (English and vernacular) and place it on the website of the company if any indicating and justifying the variation.

The dissenting shareholders shall be given an opportunity to exit by the promoters in accordance with the SEBI Regulations.

(C) Artis Management Consultants 13

Incorporation Related MattersIncorporation Related Matters

� Commencement of Business

If one goes through the bill , its almost similar with the existing lines , but with the variation that it applies to all companies

That means even a Private Company needs to get the Commencement of Business.

(C) Artis Management Consultants 14

Incorporation Related MattersIncorporation Related Matters

� Companies with charitable objects.Clause 8 of the bill is similar to Section 25 of the present Act, but in addition to the objects of promotion of commerce, art, science , religion, charity –the clause also states sports, education, research, social welfare and environment protection

The Bill extends this facility to a person also, so it looks like OPC can also form such type of companies.

(C) Artis Management Consultants 15

Incorporation Related MattersIncorporation Related Matters

� Name RelatedAs in the earlier law, once the name is applied (fresh and for change) and approved the same will be reserved for a period of 60 days ( procedural aspect brought in the Bill itself)

Further, the Bill provides, where the name is reserved and later its found that the name was applied by furnishing wrong / incorrect found that the name was applied by furnishing wrong / incorrect information then

� If the Company is not incorporated –the reserved name shall be cancelled and the person making the application shall be liable to a penalty not exceeding Rs. 1,00,000/-

� If the Company is incorporated – the ROC after giving the Company a hearing direct the company to change its name within 3 months or make a petition for winding up of the Company.

(C) Artis Management Consultants 16

Incorporation Related MattersIncorporation Related Matters

� Change of Name during Last 2 Years.

If the company has changed name during the last 2 years, it shall affix, outside every the last 2 years, it shall affix, outside every office, place of business and print in all letter heads, bill heads etc along with its name the former name or names changed during the said period.

(C) Artis Management Consultants 17

Incorporation Related MattersIncorporation Related Matters

� Articles

The Articles of the Company can contain entrenchment provisions,

these may be more restrictive than passing a Special Resolution for altering certain provisions.

The respective forms of Articles have been specified in Table F, G, H, I and J under Schedule I

(C) Artis Management Consultants 18

Part Part --33

�ALLOTMENT OF SECURITIESSECURITIES

(C) Artis Management Consultants 19

ALLOTMENT OF SECURITIESALLOTMENT OF SECURITIES

� Mode of IssueA Public Company may issue securities

-through prospectus by complying with the provisions of Part I of Chapter III, or

-through private placement by complying with the provisions of -through private placement by complying with the provisions of Part II of Chapter III ,or

-through rights/ bonus issue as per bill and in case of listed companies by also complying with SEBI Act and Regulations.

A Private Company can only issue securities

-through private placement by complying Part II of Chapter III

-through rights/ bonus issue

(C) Artis Management Consultants 20

ALLOTMENT OF SECURITIESALLOTMENT OF SECURITIES

� Offer for SaleIn a public company if certain members propose in consultation with the Board to offer part of their holdings to public, they may do so in accordance with the prescribed procedure.

The offer document will be deemed to be the prospectus and the people offering the shares shall collectively authorize the Company people offering the shares shall collectively authorize the Company for all actions and shall reimburse the company of all expenses incurred in this connection

(one will have to see SEBI takeover code if the company is a listed company)

(C) Artis Management Consultants 21

ALLOTMENT OF SECURITIESALLOTMENT OF SECURITIES

� GDR

The bill provides for issuing depository receipts to be dealt in depository mode in any foreign country subject to such in any foreign country subject to such conditions as may be prescribed-

provided the company approves the same by way of a Special Resolution passed in General Meeting.

(C) Artis Management Consultants 22

Part Part --44

�SHARES AND DEBENTURESDEBENTURES

(C) Artis Management Consultants 23

Shares and DebenturesShares and Debentures

� Voting Rights of Preference Shares

There seems to be no difference in terms of thedistinction between cumulative and non cumulativepreference shares in terms of the voting rights as in thepreference shares in terms of the voting rights as in thepresent Act.

The Bill says that where the dividends payable in respectof a class of preference shares are in arrears for aperiod of two years or more, such class of preferenceshareholders shall have the right to vote on allresolutions placed before a meeting of the Company.

(C) Artis Management Consultants 24

Shares and DebenturesShares and Debentures

� Preference Shares for a period exceeding 20 years

The bill provides for issue of preference shares redeemable after a period of 20 years from the date of issue by Infrastructure Companies, date of issue by Infrastructure Companies, subject to redemption of such percentages on an annual basis at the option of such preference

shareholders.

The present Act bars issue of the preference shares beyond 20 years

(C) Artis Management Consultants 25

Shares and DebenturesShares and Debentures

� Shares at Discount

� The Bill prohibits issue of shares at discount and further states that any issue of shares at discounted price shall be voidof shares at discounted price shall be void

� The only one exception that seems to be on issue sweat equity shares provided in the Bill.

(C) Artis Management Consultants 26

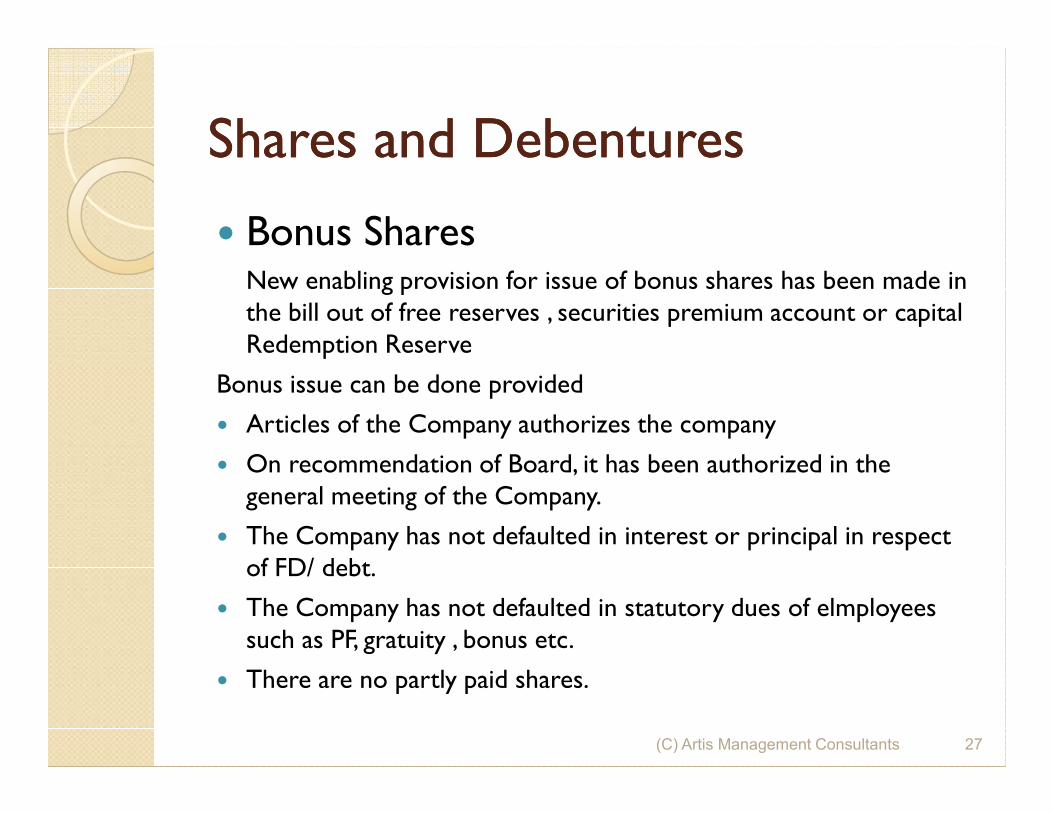

Shares and DebenturesShares and Debentures

� Bonus SharesNew enabling provision for issue of bonus shares has been made in the bill out of free reserves , securities premium account or capital Redemption Reserve

Bonus issue can be done provided

� Articles of the Company authorizes the company

� On recommendation of Board, it has been authorized in the general meeting of the Company.

� The Company has not defaulted in interest or principal in respect of FD/ debt.

� The Company has not defaulted in statutory dues of elmployees such as PF, gratuity , bonus etc.

� There are no partly paid shares.

(C) Artis Management Consultants 27

Shares and DebenturesShares and Debentures

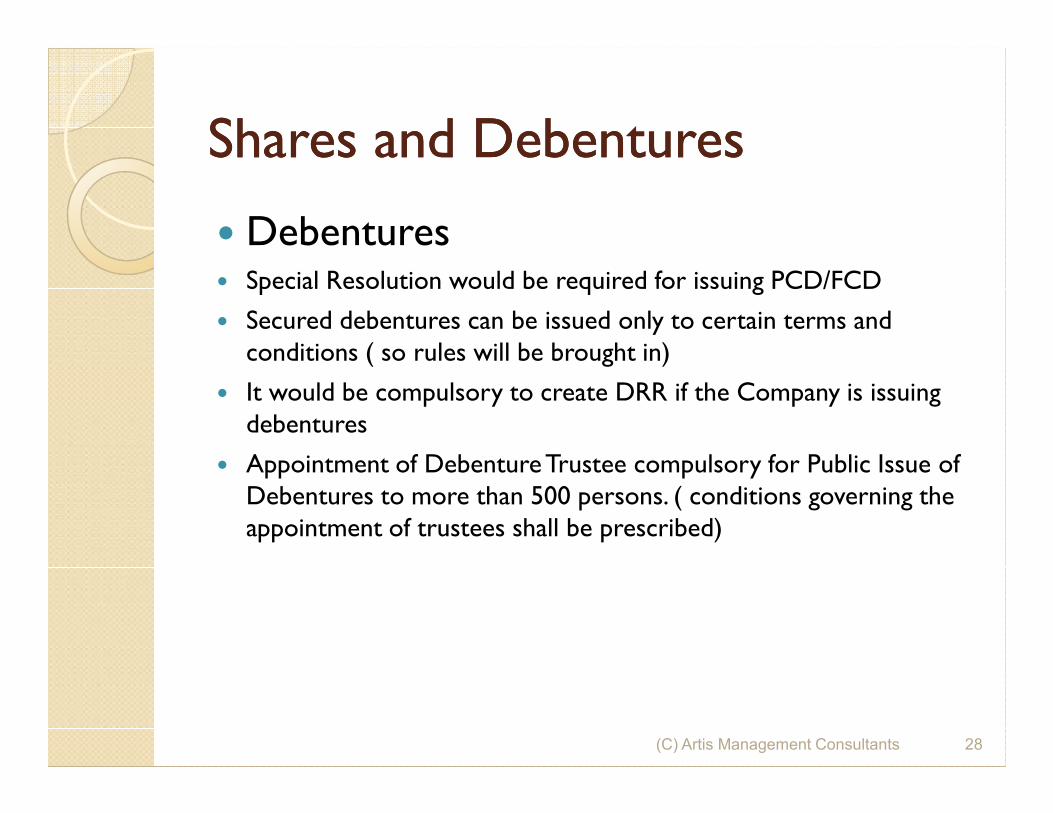

� Debentures� Special Resolution would be required for issuing PCD/FCD

� Secured debentures can be issued only to certain terms and conditions ( so rules will be brought in)

� It would be compulsory to create DRR if the Company is issuing It would be compulsory to create DRR if the Company is issuing debentures

� Appointment of Debenture Trustee compulsory for Public Issue of Debentures to more than 500 persons. ( conditions governing the appointment of trustees shall be prescribed)

(C) Artis Management Consultants 28

Part Part --55

�DEPOSITS

(C) Artis Management Consultants 29

DepositsDeposits

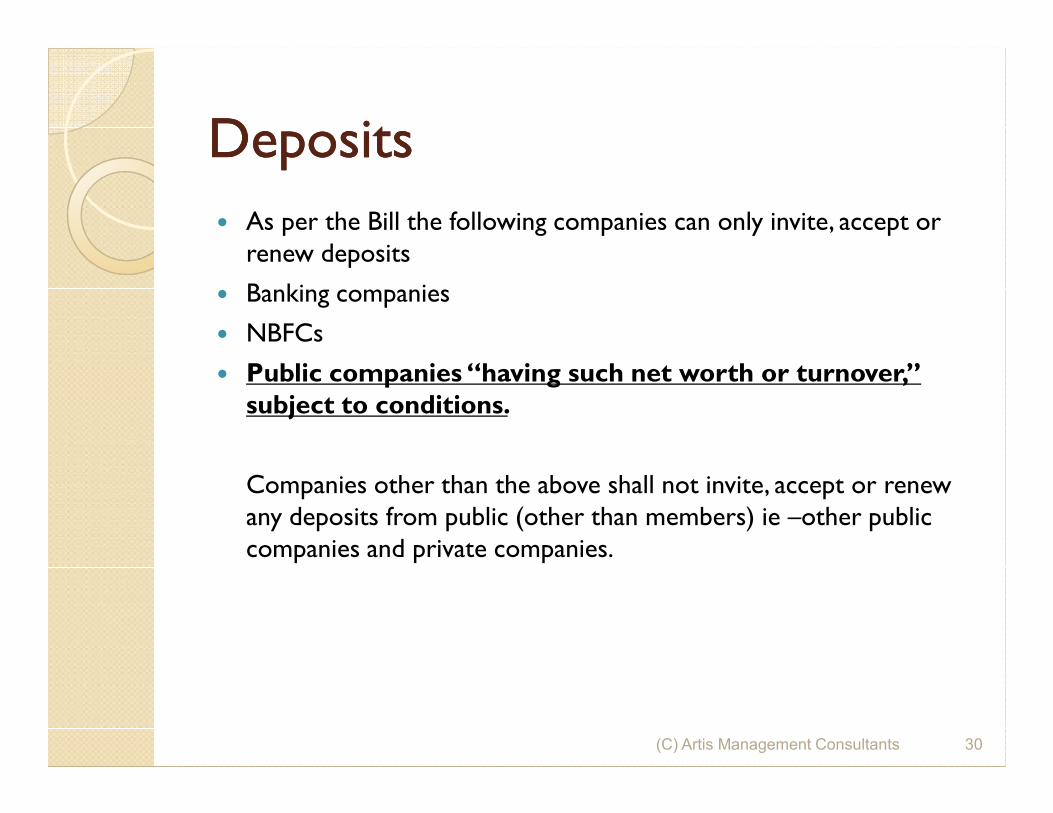

� As per the Bill the following companies can only invite, accept or renew deposits

� Banking companies

� NBFCs

� Public companies “having such net worth or turnover,” subject to conditions. subject to conditions.

Companies other than the above shall not invite, accept or renew any deposits from public (other than members) ie –other public companies and private companies.

(C) Artis Management Consultants 30

DepositsDeposits

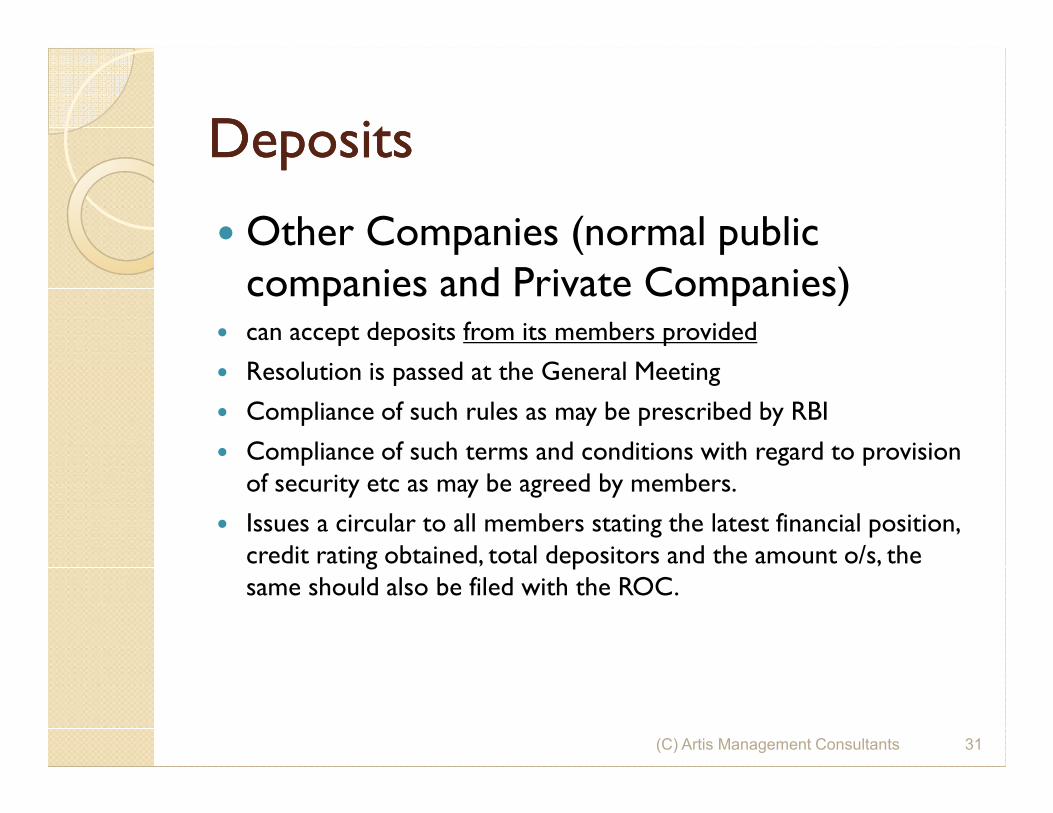

� Other Companies (normal public companies and Private Companies)

� can accept deposits from its members provided

� Resolution is passed at the General Meeting

� Compliance of such rules as may be prescribed by RBI� Compliance of such rules as may be prescribed by RBI

� Compliance of such terms and conditions with regard to provision of security etc as may be agreed by members.

� Issues a circular to all members stating the latest financial position, credit rating obtained, total depositors and the amount o/s, the same should also be filed with the ROC.

(C) Artis Management Consultants 31

DepositsDeposits

� Depositing a sum of not less than 15% of the amount of deposits maturing during a FY in a Deposit Repayment Reserve Account (DRRA).

� Providing such Deposit Insurance as may be prescribed.

� Providing such security for repayment and charge be created on assets , if no security provided then state the same as unsecured assets , if no security provided then state the same as unsecured deposits in every circular and advertisements.

� To obtain a certification that the company has not defaulted in repayment of deposits.

(C) Artis Management Consultants 32

DepositsDeposits

� Deposits by Public Companies from others than members

� The Company has to comply all the conditions as applicable to other companies as stated before.

� The Company shall obtain a rating , from a recognized Credit rating � The Company shall obtain a rating , from a recognized Credit rating agency , the rating shall ensure the adequate safety. It shall be obtained each year.

� The company shall within 30 days of acceptance of deposits create a charge on the property of the Company.

(C) Artis Management Consultants 33

Part Part --66

�CHARGES

(C) Artis Management Consultants 34

ChargesCharges

� Clause 2(16) defines charge with a wider coverage as under:

� It included any interest or lien created on the assets of thecompany or its undertakings and it includes mortgage

� ALL CHARGES-to be Registered

� Presently nine type of charges specified in Section 125 needs to be� Presently nine type of charges specified in Section 125 needs to befiled, the bill provides that the Company is bound to register theparticulars of every charge created on its assets with ROC within30 days of its creation

(C) Artis Management Consultants 35

ChargesCharges� Every charge to be registered with ROC with the particulars of charge within 30 days of its creation (existing sec 125 states within 30 days after its creation).

� ROC may allow the registration within a � ROC may allow the registration within a period of 300 days of its creation, with such additional fees.

� Company can also seek extension with Central Government if the same could not be done in 300 days.

(C) Artis Management Consultants 36

ChargesCharges

� Company to give notice of satisfaction of chargewithin 30 days from the date of satisfaction/payment.

� ROC shall send a notice to the charge holderto explain within 14 days – as to why the chargeto explain within 14 days – as to why the chargeshould not be registered and if no causementioned , ROC to register the satisfaction.

� Provided such notice shall not be required if theform for satisfaction of charge is also signed bythe charge holder.

(C) Artis Management Consultants 37

Part Part --77

�AGM/ GM RELATED RELATED MATTERS

(C) Artis Management Consultants 38

AGM / GM Related MattersAGM / GM Related Matters

� Period

� As in the present Act not more than 15 months shall elapse between two AGM of a Company

� First AGM shall be held within 9 months from the date of closing the first FY. If it is so held the Company shall not be required to hold its AGM in the year of incorporation or following year.hold its AGM in the year of incorporation or following year.

� AGM,s other than the first one shall be held within 6 months from the date of closing of the FY.

� Time

� The business hours for conduct of AGM has been defined between 9.00 AM and 6.00 PM, further the AGM can be called on a public holiday but not a National Holiday.

� National Holiday are holidays declared as such by Government.

(C) Artis Management Consultants 39

AGM/ GM Related MattersAGM/ GM Related Matters

� Explanatory Statement(ES)� It states that where ES needs to be given- all material facts

concerning each item of special business needs to be annexed to the notice, further it states

� Material Facts should contain

� The nature and concern of interest , financial or otherwise , if any in respect of each item of every director, manager, KMP, relatives of all of them and

� All other information and facts that may enable the members to understand the implications of items of business.

(C) Artis Management Consultants 40

AGM Related MattersAGM Related Matters

� OPC � An OPC is not required to hold AGM compulsorily

� If any business is to be transacted by OPC in AGM or other general meeting, the same will be done as under

� The sole member shall communicate the resolution to the The sole member shall communicate the resolution to the Company.

� The resolution shall be entered in the minute book and signed and dated by the Sole Member, such date shall be deemed to be the day of the meeting (GM)

� In case of Board Meeting of OPC, if there is only one Director, it shall be sufficient if resolution is entered in the minute book and signed and dated by such Director and said date shall be deemed to be the day of the meeting (BM)

(C) Artis Management Consultants 41

AGM Related MattersAGM Related Matters

� QUORUM for Public Companies

� As per the bill the quorum for public companies for general meeting shall be

� 5 members personally present if as on date of meeting the number of members are not more than 1000

� 15 if more than 1000 but not more than 5000

� 30 if members more than 5000

(C) Artis Management Consultants 42

AGM Related MattersAGM Related Matters

� Report on AGM by Listed Companies

Every listed company is required to file a report in the prescribed manner with the ROC

-The report shall contain the details of the meeting held

-The same should be filed within 30 days from the AGM

(C) Artis Management Consultants 43

Part Part --88

�ANNUAL RETURN AND AND

CONNECTED MATTERS

(C) Artis Management Consultants 44

Annual Return (AR) and connected Annual Return (AR) and connected mattersmatters� Every Company is required to file an AR containing the

following.

� Registered Office, principal business activities, details of holding/subsidiary companies.

� Shares, debentures, other securities and shareholding pattern.

� Its indebtedness.� Its indebtedness.

� Members, debenture holders, along with changes since the close of last FY.

� Promoters, directors, KMPs, along with changes since the close of last FY.

� Details of Meetings of members, board, committee along with attendance details.

� Remuneration of Directors and KMP

(C) Artis Management Consultants 45

Annual Return (AR) and connected Annual Return (AR) and connected mattersmatters� Penalties and punishments imposed on company, its directors and

officers, details of compounding of offences.

� Matters related to certification of compliances, disclosures as may be prescribed.

� Details of Foreign Institutional Investors indicating their name , address, countries of incorporation, % age of Shareholding etc.address, countries of incorporation, % age of Shareholding etc.

� Such other matters as may be prescribed.

Time Limit for Filing with ROC.

The AR should be filed within 30 days from the date of AGM

and if AGM not held ,

should be filed within 30 days from the date the AGM should have been held along with the statement specifying the reason for not holding the AGM

(C) Artis Management Consultants 46

Annual Return (AR) and connected Annual Return (AR) and connected mattersmatters� Certification of AR� In case of OPC & Small Companies –AR should be signed by

CS and if there is no CS then by director.

� In case of Listed Companies and Prescribed Companies with such paid up capital and turnover (to be prescribed) in addition it has to be Certified by a PCS stating that AR discloses the facts has to be Certified by a PCS stating that AR discloses the facts correctly and that the Company has complied with the provisions of the Act. The Right to give qualified report has also been provided.

� For all Other Companies it should be signed by director and CS and if there is no CS then by a PCS.

� An extract of the return forms part of the Directors Report.

(C) Artis Management Consultants 47

Annual Return (AR) and connected Annual Return (AR) and connected mattersmatters� Small Company means a company other than PublicLimited Company.

� (i) paid-up share capital of which does not exceed fifty lakhrupees or such higher amount as may be prescribedwhich shall not be more than five crore rupees;

or

� (ii) turnover of which as per its last profit and loss accountdoes not exceed two crore rupees or such higheramount as may be prescribed which shall not be morethan twenty crore rupees:

(C) Artis Management Consultants 48

Annual Return (AR) and connected Annual Return (AR) and connected mattersmatters� New Return

� Every listed company is required to file with ROC with respect to any shareholding change in promoters and top ten shareholders.

� The same should be filed within 15 days.

(C) Artis Management Consultants 49

Part Part --99

�DIVIDEND

(C) Artis Management Consultants 50

DividendDividend

� No requirement to transfer % of profits to reserve.

� The present Act requires such % of profits not exceeding 10% to be transferred to reserves while Dividend is declared.while Dividend is declared.

� The Bill leaves this provision and leaves it at the option of the company to decide.

(C) Artis Management Consultants 51

DividendDividend

� Interim Dividend-restrictions� The bill states that the interim dividend if any shall be only out of the surplus in the P&L account as well as the profits for the FY in which interim divided is declared.

� In case the Company has incurred loss during the � In case the Company has incurred loss during the current FY up to the end of the quarter immediately preceding the declaration of interim dividend , such dividend shall not be declared at a rate higher than the average dividends declared by the Company during the immediately preceding three Fys.

(C) Artis Management Consultants 52

DividendDividend

� Violation of Acceptance of Deposits provisions.

A company shall not declare any dividend on A company shall not declare any dividend on equity shares as long as the company fails to comply with the provisions of deposits rules.

(C) Artis Management Consultants 53

DividendDividend

� Investor Education and Protection Fund� As in the present Act the unclaimed / unpaid dividend for a period of seven years shall be transferred to IEPF

� The Bill further states that all shares in respect of which the unclaimed/ unpaid dividend are transferred ; those the unclaimed/ unpaid dividend are transferred ; those shares shall also be transferred in the name of IEPF along with the prescribed statement.

� Any claimant can claim his shares to be transferred from IEPF name to his name on following the procedure and submission of required documents.

(C) Artis Management Consultants 54

Part Part --1010

�ACCOUNTS AND DIRECTORS DIRECTORS REPORT

(C) Artis Management Consultants 55

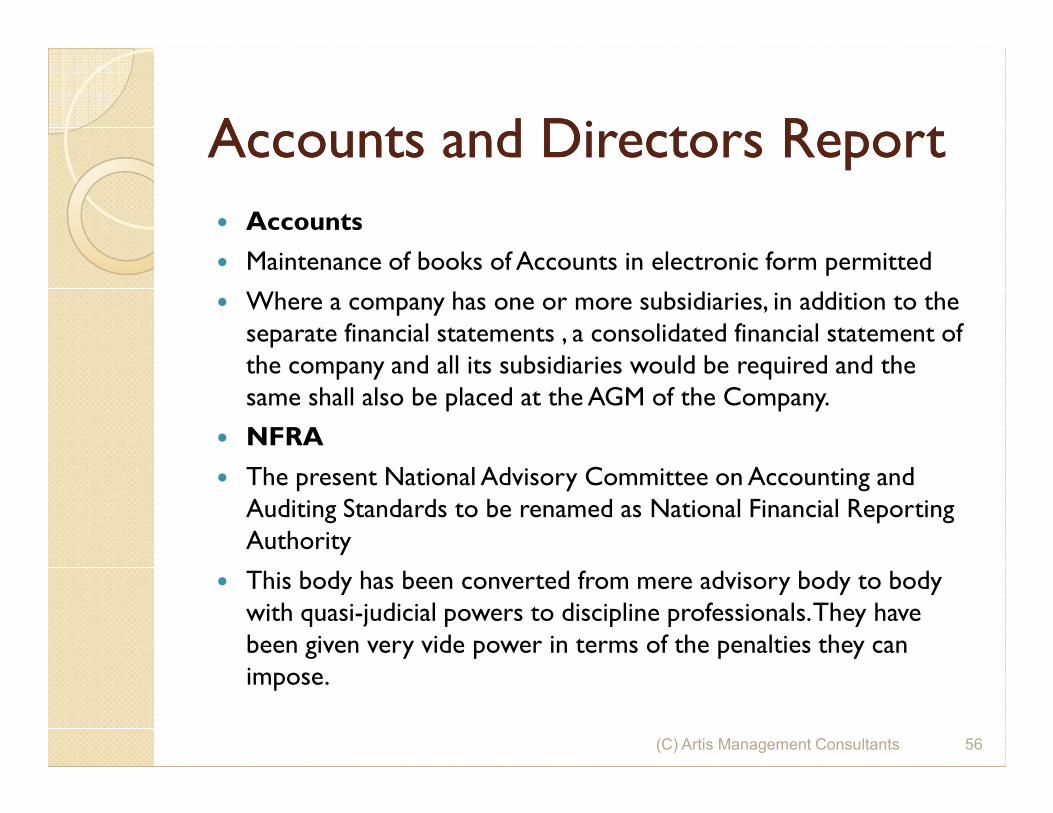

Accounts and Directors ReportAccounts and Directors Report

� Accounts

� Maintenance of books of Accounts in electronic form permitted

� Where a company has one or more subsidiaries, in addition to the separate financial statements , a consolidated financial statement of the company and all its subsidiaries would be required and the same shall also be placed at the AGM of the Company.same shall also be placed at the AGM of the Company.

� NFRA

� The present National Advisory Committee on Accounting and Auditing Standards to be renamed as National Financial Reporting Authority

� This body has been converted from mere advisory body to body with quasi-judicial powers to discipline professionals. They have been given very vide power in terms of the penalties they can impose.

(C) Artis Management Consultants 56

Accounts and Directors ReportAccounts and Directors Report

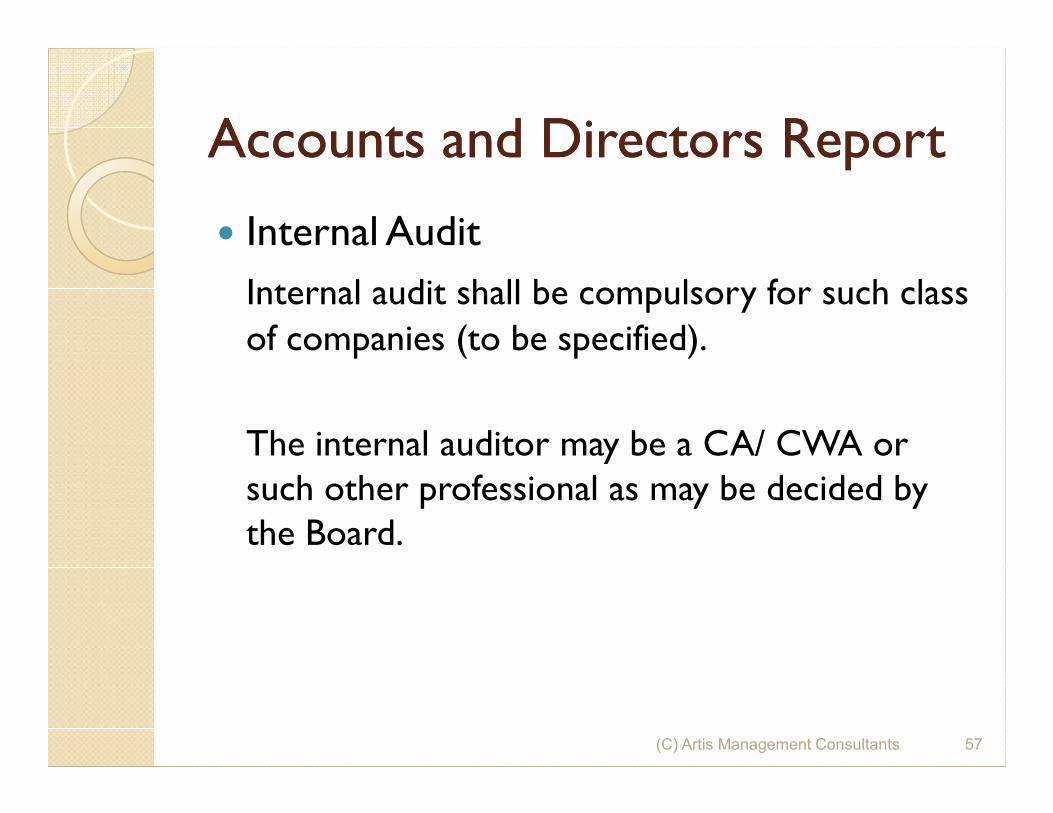

� Internal Audit

Internal audit shall be compulsory for such class

of companies (to be specified).

The internal auditor may be a CA/ CWA or such other professional as may be decided by the Board.

(C) Artis Management Consultants 57

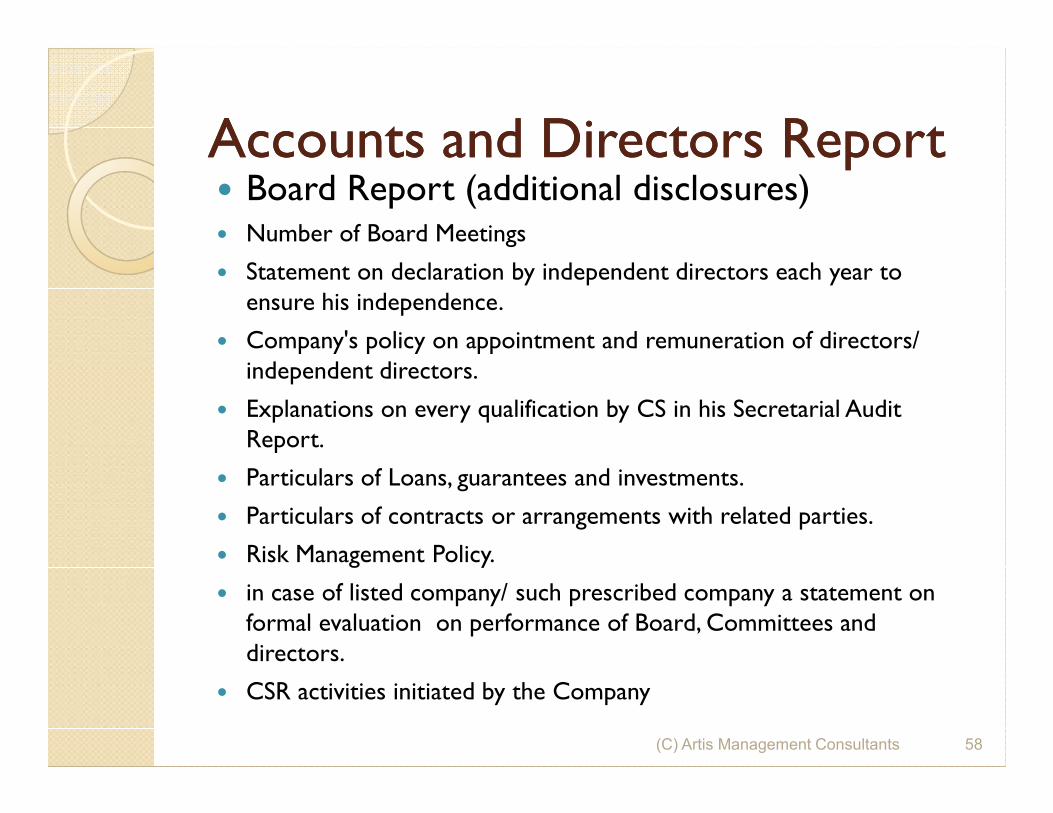

Accounts and Directors ReportAccounts and Directors Report� Board Report (additional disclosures)� Number of Board Meetings

� Statement on declaration by independent directors each year to ensure his independence.

� Company's policy on appointment and remuneration of directors/ independent directors.

� Explanations on every qualification by CS in his Secretarial Audit � Explanations on every qualification by CS in his Secretarial Audit Report.

� Particulars of Loans, guarantees and investments.

� Particulars of contracts or arrangements with related parties.

� Risk Management Policy.

� in case of listed company/ such prescribed company a statement on formal evaluation on performance of Board, Committees and directors.

� CSR activities initiated by the Company

(C) Artis Management Consultants 58

Accounts and Directors ReportAccounts and Directors Report

� Corporate Social Responsibility (CSR)� As per the bill every company having, a net worth of Rs. 500

Crores or turnover of Rs.1000 Crore or a net profit of Rs. 5 Crore or more shall constitute a CSR committee of the Board consisting of three or more directors with at least one independent director.

� The Board Report shall disclose the composition.

� The CSR committee shall formulate and recommend to the Board , a CSR policy indicating the activities to be undertaken as specified in schedule VII

� The Board of every company shall ensure that the company spends,in every financial year, at least two per cent. of the average netprofits of the company made during the three immediatelypreceding financial years, in pursuance of its Corporate SocialResponsibility Policy.

(C) Artis Management Consultants 59

Accounts and Directors ReportAccounts and Directors Report

� Directors Responsibility Statement

� Further to the existing provisions in DRS, the following additions have been made.

� In case of a Listed Company-the directors had laid down the Internal Financial Controls.laid down the Internal Financial Controls.

� The directors have devised proper systems to ensure compliance with the provisions of this Act and that they are operating adequately.

(C) Artis Management Consultants 60

Part Part --1111

�AUDIT RELATED

(C) Artis Management Consultants 61

Audit relatedAudit related� 5 years tenure for auditors/ instead of retiring at each AGM

� The bill states that every company (other than Govt Companies) shall at the first AGM , appoint an individual, firm or LLP as auditor who shall hold office from the conclusion of the that meeting till the conclusion of the 6thAGM and thereafter till conclusion of the conclusion of the 6 AGM and thereafter till conclusion of every 6th meeting.

� Automatic Reappointment of existing auditor –where no auditor is reappointed at AGM.

� In case of Govt Companies, C&AG will appoint the first auditor within a period of 60 days from incorporation of the Company. Subsequent years C&AG will appoint the auditors within 180 days from the commencement of FY, the auditor so appointed shall hold office till the conclusion of AGM.

(C) Artis Management Consultants 62

Audit relatedAudit related

� Rotation of Auditors� A listed company and such prescribed companies shall not appoint

/ reappoint an individual as auditor for a term of more than 5 consecutive years or an audit firm for a period of two terms of 5 consecutive years.

� Further the auditor/ firm who have completed their term of 5 � Further the auditor/ firm who have completed their term of 5 years shall not be eligible to be appointed as auditors in same company for 5 years further. The same shall be applicable to firms having common partners.

� The bill provides that the members can also resolve that the partner conducting the audit can be rotated every year or that the audit can be conducted by more than one auditor.

(C) Artis Management Consultants 63

Part Part --1212

�DIRECTORS

(C) Artis Management Consultants 64

DirectorsDirectors

� No Government Approval for increase inDirectors.

� The maximum number of directors a company can haveis increased to 15 , any further increase can be doneby passing a Special Resolution and CentralGovernmentApproval no more required.GovernmentApproval no more required.

� Woman Director

� Its proposed that such class of companies as may beprescribed shall have at least one woman director.

(C) Artis Management Consultants 65

DirectorsDirectors

� A person can be a Director in Maximum twentycompanies (including any alternate directorship)

� Provided that the maximum number of publiccompanies in which a person can be appointed as adirector shall not exceed ten. Directorship in holding orsubsidiary company of a Public Company will besubsidiary company of a Public Company will beincluded in the 10.

� the members of a company may, by special resolution,specify any lesser number of companies in which adirector of the company may act as directors.

(C) Artis Management Consultants 66

DirectorsDirectors--Duties Duties � shall act in accordance with the articles of the company.

� act in good faith in order to promote the objects of the company for thebenefit and interest of its members,company, its employees, theshareholders, the community and for the protection ofenvironment.

� exercise his duties with due and reasonable care, skill and diligence andshall exercise independent judgment.

� shall not involve in a situation in which he may have a direct or indirectinterest that conflicts, or possibly may conflict, with the interest ofthe company.

� shall not achieve or attempt to achieve any undue gain or advantageeither to himself or to his relatives, partners, or associates and ifsuch director is found guilty of making any undue gain, he shall beliable to pay an amount equal to that gain to the company.

� shall not assign his office and any assignment so made shall be void.

.

(C) Artis Management Consultants 67

DirectorsDirectors� Independent Directors

� Every Public Listed Company shall have at least1/3rd of the total number of directors asindependent directors.

� The Central Government will prescribe the� The Central Government will prescribe thenumber of independent directors for othercompanies.

� The independent directors will not be entitledto any remuneration other than sitting fee/profit related commission if any approved bymembers

(C) Artis Management Consultants 68

DirectorsDirectors

� Clause 49-listing agreement-comparison.

� The Board of directors of the company shall have an optimum combination of executive and non-executive directors with not less than fifty percent of the board of directors comprising of non-executive directors.

� Where the Chairman of the Board is a non-executive director, at least one-third of the Board should comprise of independent directors and in case he is an executive director, at least half of the Board should comprise of independent directors.

(C) Artis Management Consultants 69

DirectorsDirectors� Tenure of Independent Directors.� No independent directors shall have a tenure exceedingin aggregate a period of 5 consecutive years.

� He shall though be eligible for reappointment by SpecialResolution and required disclosure but shall not holdoffice for more than two consecutive terms.office for more than two consecutive terms.

� He can be further reappointed only after the expirationof three years of ceasing the office.

� During these three years he shall not be a director inany of the associated companies also.

� The independent directors shall not be coming underretirement of directors by rotation clause

(C) Artis Management Consultants 70

DirectorsDirectors

� Resignation of Director� The bill provides that a director may resign from his office by giving

a notice in writing.

� The Board will have to take note of the same and intimate theROC in the prescribed manner and also the fact of resignation willbe placed before the next general meeting.be placed before the next general meeting.

� The director shall also forward a copy of his resignation to ROCwith detailed reasons within 30 days of resignation.

� The resignation shall be effective from the date on which notice isreceived by the company or any date specified by the director inthe notice, whichever is later.

(C) Artis Management Consultants 71

DirectorsDirectors--Vacation of Office due to Vacation of Office due to absence from meetingsabsence from meetings

� The Office of Director shall becomevacant if he absents himself from all themeetings of the Board of Directors heldmeetings of the Board of Directors heldduring a period of twelve months withor without seeking leave of absence.

(C) Artis Management Consultants 72

Part Part --1313

�BOARD MEETING AND AND

CONNECTED MATTERS

(C) Artis Management Consultants 73

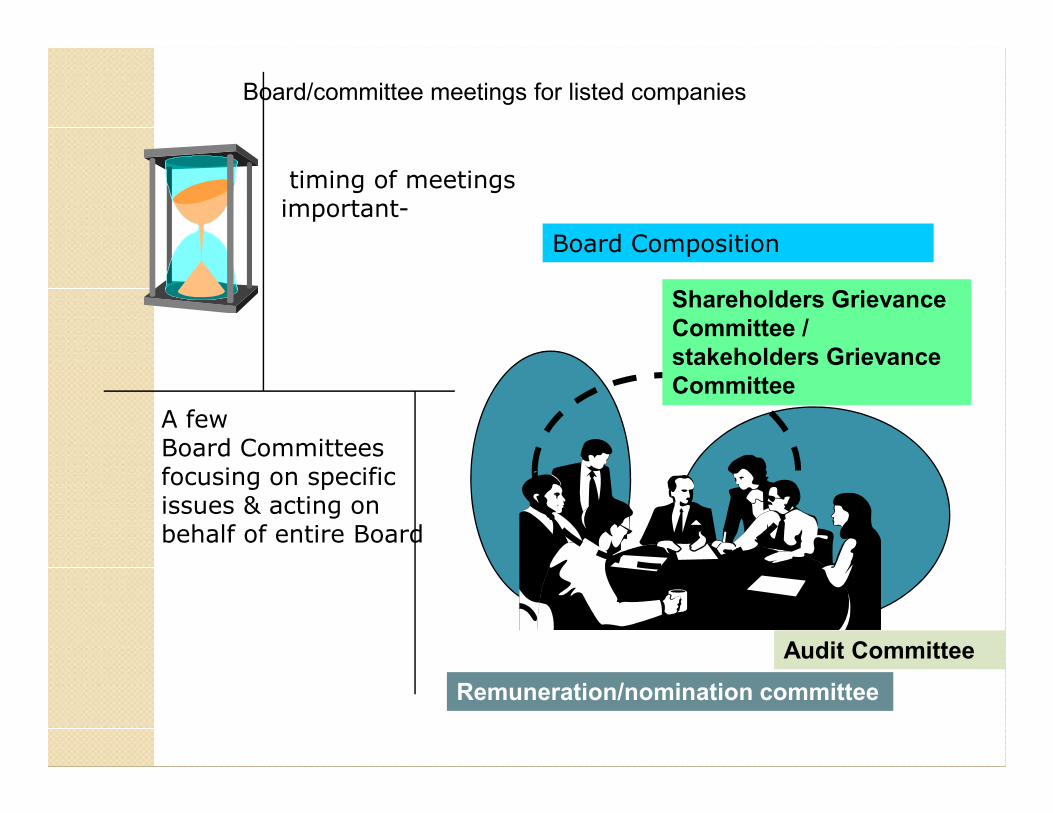

Board Meeting and connected Board Meeting and connected mattersmatters� First meeting of the Board should be held within 30 days of its incorporation. Thereafter company should hold minimum 4 meetings in an year and there should not be more than 120 days gap between two consecutive meetings.

With regard to OPC and Small Company, at least one � With regard to OPC and Small Company, at least one meeting should be held in each half of the calendar year and that the gap between two such meetings is not less than 90 days.

� Bill enables board meeting by video conferencing and such participation shall be counted for the purposes of quorum.

(C) Artis Management Consultants 74

Board Meeting and connected Board Meeting and connected mattersmatters� Board Meeting Notice.� 7 days notice to given for Board Meeting, it should be inwriting and given to every director at his addressregistered with the company.

� Notice may be given by hand delivery/ electronic means� Notice may be given by hand delivery/ electronic means

� Shorter notice may be given for urgent business, but atleast one independent director should be present insuch a meeting and if they are absent the decisionstaken will be circulated to all directors and approvedonly if ratified by at least one-independent director.

(C) Artis Management Consultants 75

Board Meeting and connected Board Meeting and connected mattersmatters� Audit Committee

� The Board of Directors of every listed company and such other class or classes of companies, as may be prescribed, shall constitute an Audit Committee.

� The Audit Committee shall consist of a minimum of three � The Audit Committee shall consist of a minimum of three directors with independent directors forming a majority:

� Provided that majority of members of Audit Committee including its Chairperson shall be persons with ability to read and understand, the financial statement.

(C) Artis Management Consultants 76

Board Meeting and connected Board Meeting and connected mattersmatters� New Committees� Every Listed and such other company as may be prescribed shall

form a Nomination and Remuneration committee. TheCommittee will have three or more non-executive directors out ofwhich at least 50% shall be independent. The Committee shallidentify and formulate the criteria for selecting directors, senioridentify and formulate the criteria for selecting directors, seniormanagement personnel and such policy will be disclosed in theBoard's report.

� A company having combined membership of shareholders,debenture holders and other security holders of more than 1000at any time during a FY shall form a Stakeholders RelationshipCommittee under the chairmanship of a non executive director.The Committee shall consider and resolve the grievances ofstakeholders.

(C) Artis Management Consultants 77

Board Composition

timing of meetings important-

A few

Shareholders Grievance

Committee /

stakeholders Grievance

Committee

Board/committee meetings for listed companies

A fewBoard Committeesfocusing on specificissues & acting on behalf of entire Board

Audit Committee

Remuneration/nomination committee

Board Meeting and connected Board Meeting and connected mattersmatters� Political Contribution

� Limit on political contribution has beenincreased from 5% to 7.5% of the average netprofits of the preceding three Fys.

� Further it defines a Political party as any partyregistered so under Section 29A ofRepresentation of the People Act 1951.

(C) Artis Management Consultants 79

Board Meeting and connected Board Meeting and connected mattersmatters� Related party transactions� Except with the approval of the Board, no company shall enter into a

contract or arrangement with related party for

� Sale, purchase, supply of goods and materials.

� Selling or disposing of any property.

� Leasing of property.Leasing of property.

� Rendering of services.

� Appointment of relative to Place of Profit.

� Appointment as agent for purchase and sale of goods, materials ,services or properties.

� Underwriting the subscription of any securities or derivatives.

� Provided a company with such paid up capital has to take prior approval of shareholders by Special Resolution.

� Central Govt Approval (prior) has been taken away.

(C) Artis Management Consultants 80

Board Meeting and connected Board Meeting and connected mattersmatters� Related Party� Related party with reference to a company means

� Director or his relative (relative almost same as in the present Act).

� KMP or his relative .

� Firm in which a director, or relative is a partner.� Firm in which a director, or relative is a partner.

� A Private Company of which such director is a member or director.

� A Public Company in which a director or relative or together holds 2% of paid up capital.

� A Body Corporate whose BOD are accustomed to act in accordance of the directions of the director.

(C) Artis Management Consultants 81

Board Meeting and connected Board Meeting and connected mattersmatters� Non –cash transactions by directors� Bill provides that a company, subsidiary, or associate shall not enter

into specified non cash transactions with director, director of holding company, or person connected with them unless

� Prior approval has been obtained in general meeting by resolution, where in the details of the transaction or arrangement along with where in the details of the transaction or arrangement along with value of the assets have been given to shareholders.

� Non-cash Transactions are any arrangements by which a director of the company or its holding company, subsidiary, associate or connected person with him acquires assets for consideration other than cash from the company or vice versa.

(C) Artis Management Consultants 82

Part Part --1414

�KMP RELATED

(C) Artis Management Consultants 83

KMP RelatedKMP Related

� The bill provides that every company belonging to such class or description shall have the following as KMP

� MD or CEO or Manager and in their absence WTD and

� Company Secretary.

� If the office of the KMP is vacated, the resulting vacancy � If the office of the KMP is vacated, the resulting vacancy shall be filled by Board within a period of 6 months from the date of such vacancy.

� Though CFO is also mentioned in the definitions of KMP , the mode of appointment / or qualification levels seems not to have been captured.

(C) Artis Management Consultants 84

KMP RelatedKMP Related

� Prohibition on forward dealings/ Insider Trading

� The Directors and KMP,s may be barred from doing a forward deal in securities of the company at certain periods.company at certain periods.

� They will be barred from doing insider trading in usual course or while there is window closure period on the basis of unpublished price sensitive information

(C) Artis Management Consultants 85

Part Part --1515

�MANAGERIAL REMUNERATIONREMUNERATION

(C) Artis Management Consultants 86

Managerial RemunerationManagerial Remuneration

� The bill provides for remuneration as per thepresent Act (11% of net profits).

� The Company having no adequate profits/ noprofits can go as per new ScheduleV.

For Companies not being able to comply the� For Companies not being able to comply theScheduleV – central Govt approval required.

� One needs to understand that with the presentnotifications already in place –there is bound to besome changes.

(C) Artis Management Consultants 87

Part Part --1616

�COMPANY SECRETARYSECRETARY

(C) Artis Management Consultants 88

Company SecretaryCompany Secretary

� CS once appointed is a KMP and functions defined for first time

� To report to board about compliance with theprovisions of the Act, rules and other applicable laws tothe company.the company.

� To ensure compliance with SS issued by ICSI.

� To discharge such other duties as may be prescribed.

(C) Artis Management Consultants 89

Company SecretaryCompany Secretary

� Secretarial Audit

� Every listed company and company belonging tosuch class shall annex with Boards Report aSecretarial Audit Report given by PCS.

� The Company has to provide all assistance tothe PCS.

� The Board has to explain in Boards Report, thequalifications made by PCS.

(C) Artis Management Consultants 90

Part Part --1717

�SERIOUS FRAUD INVESTIGATION INVESTIGATION

OFFICE

(C) Artis Management Consultants 91

Serious Fraud Investigation OfficeSerious Fraud Investigation Office

� Investigation Report of SFIO filed withcourt for framing charges shall be treatedequivalent to report filed by a PoliceOfficer.Officer.

� SFIO shall have powers to arrest inrespect of certain offences of the billwhich attract punishment for fraud.

(C) Artis Management Consultants 92

Part Part --1818

�MERGERS / AMALGAMATIONS AMALGAMATIONS / ARRANGEMENTS

(C) Artis Management Consultants 93

Mergers/ Amalgamations/ Mergers/ Amalgamations/ ArrangementsArrangements

� Simplified procedure for compromise and arrangements between two or more small companies or between holding and subsidiary company/ companies is being subsidiary company/ companies is being brought in.

� The details will be prescribed.

(C) Artis Management Consultants 94

Mergers/ Amalgamations/ Mergers/ Amalgamations/ ArrangementsArrangements� Cross Border Mergers

� The bill provides enabling provisions for merger ofcompanies incorporated in jurisdictions of suchcountries as may be notified with companies registeredunder this Act

� The Central Government may make rules inconsultation with RBI with regard to the same.

(C) Artis Management Consultants 95

Mergers/ Amalgamations/ Mergers/ Amalgamations/ ArrangementsArrangements� Power to Buy Out

� where the acquirer or person acting in concert (PAC)

holds 90% of shares or when a group of personsbecome holders of 90% shares by virtue of any schemeof amalgamation , conversion etc.of amalgamation , conversion etc.

� The bill provides for a detailed process by which theminority share holders can dispose of their shareholdingto the majority group.

� One has to also take into account the provisions ofSEBITakeover code if theTC is a Listed Company.

(C) Artis Management Consultants 96

Part Part --1919

�OPPRESSION AND MISMANAGEMENTMISMANAGEMENT

(C) Artis Management Consultants 97

Oppression and MismanagementOppression and Mismanagement

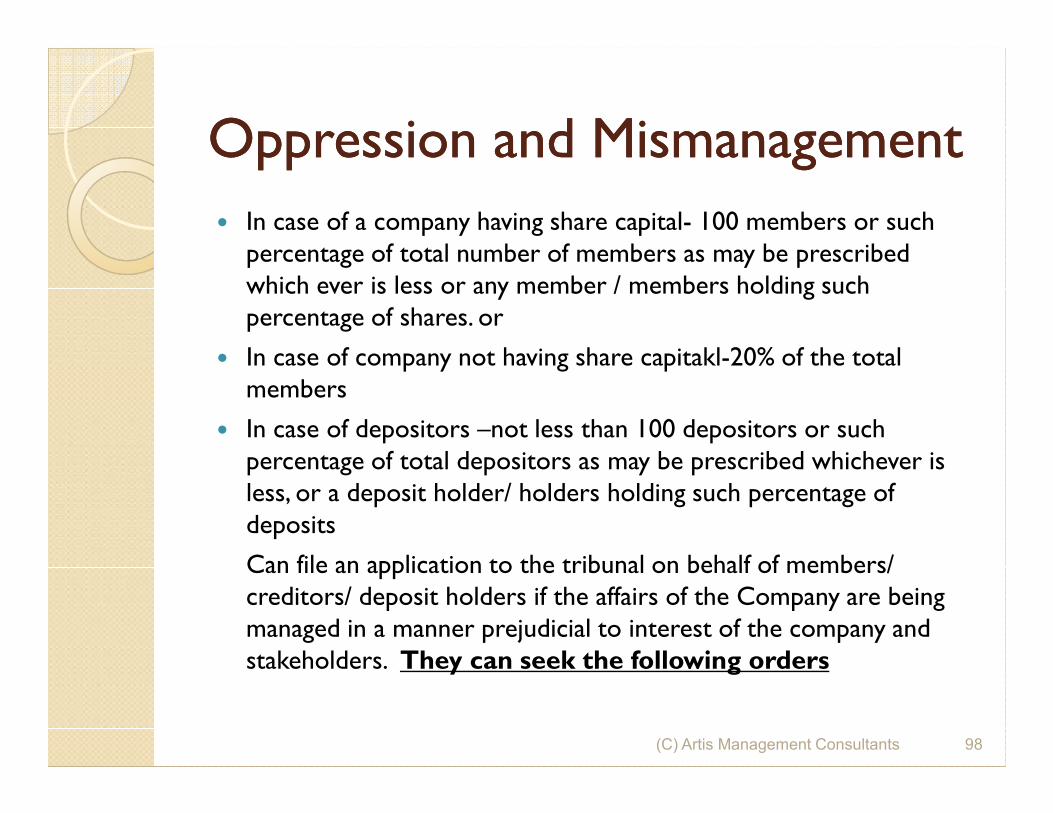

� In case of a company having share capital- 100 members or such percentage of total number of members as may be prescribed which ever is less or any member / members holding such percentage of shares. or

� In case of company not having share capitakl-20% of the total members

� In case of depositors –not less than 100 depositors or such percentage of total depositors as may be prescribed whichever is less, or a deposit holder/ holders holding such percentage of deposits

Can file an application to the tribunal on behalf of members/ creditors/ deposit holders if the affairs of the Company are being managed in a manner prejudicial to interest of the company and stakeholders. They can seek the following orders

(C) Artis Management Consultants 98

Oppression and MismanagementOppression and Mismanagement� Restrain company from acting ultra vires

� Restrain breach of company's M&AoA

� To declare resolution altering M&AoA as void, if thesame was done by suppressing the facts

� Restrain company and directors from acting on suchresolution.resolution.

� Restrain company from acting contrary to resolutionpassed by members.

� To claim damages from directors for fraudulent acts,from auditors/ consultants for wrongful act oromission in their report/ advise.

� Such other matters as tribunal may deem fit

(C) Artis Management Consultants 99

Part Part --2020

�REGISTERED VALUERSVALUERS

(C) Artis Management Consultants 100

Registered ValuersRegistered Valuers

� The bill requires that wherever there is a requirement of valuation of property, stocks, shares , debentures, goodwill, net worth, such valuation shall be done byworth, such valuation shall be done by

� A registered valuer under the Act.

� So framework for a new set of professionals has been made.

(C) Artis Management Consultants 101

Part Part --2121

�SICK COMPANIES

(C) Artis Management Consultants 102

Sick CompaniesSick Companies

� Sick industrial Companies Act 1985, limits its scope to industrial companies predominantly , while the present bill covers these provisions for all the covers these provisions for all the Companies

� Further sickness is just not determined on the negative net worth criterion but on the basis of whether a Company can pay its debts.

(C) Artis Management Consultants 103

Part Part --2222

�WINDING UP

(C) Artis Management Consultants 104

Winding UpWinding Up

� New grounds for winding up� Company acts against the sovereignty and integrity of India, security

of india, foreign relations and foreign states, public order, decency or morality.

� If tribunal has ordered winding up ( as per the revival of sick companies)companies)

� If tribunal has on an application by Registrar is of the opinon that the company be wound up as company’s affairs are done fraudulently or there is mismanagement of affairs.

� The Company has defaulted in filing of Financial Statements/ Annual Return for immediately 5 consecutive previous Fys.

(C) Artis Management Consultants 105

Part Part --2323

�NCLT AND SPECIAL COURTSSPECIAL COURTS

(C) Artis Management Consultants 106

NCLTNCLT

� The National Company Law Tribunalprovisions have been made in detail, theComposition of judicial/ technicalmembers are as per the Supreme Courtmembers are as per the Supreme CourtJudgment.

� Appeals from NCLT shall lie withNational Company LawAppellateTribunal.

(C) Artis Management Consultants 107

Special CourtsSpecial Courts

� The Bill intends to bring in an mechanism of Special Courts for trying out offences under the Act.

(C) Artis Management Consultants 108

Question TimeQuestion Time

(C) Artis Management Consultants 109

THANK YOUTHANK YOU

CS.Asish Mohan

110(C) Artis Management Consultants

![Companies Bill 2013 [Carocks.wordpress.com]](https://img.pdfslide.net/doc/110x75/577cd9bc1a28ab9e78a40e55/companies-bill-2013-carockswordpresscom.jpg)