Embed Size (px)

Citation preview

1

Company Law

2

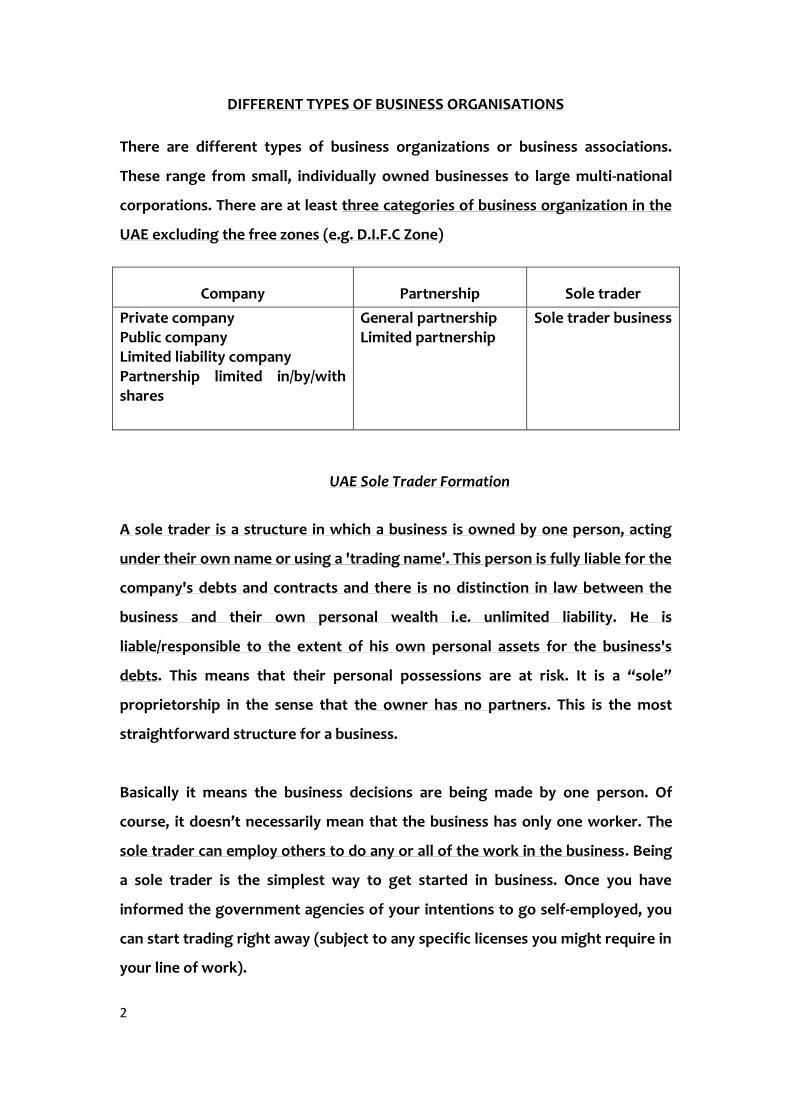

DIFFERENT TYPES OF BUSINESS ORGANISATIONS

There are different types of business organizations or business associations.

These range from small, individually owned businesses to large multi-national

corporations. There are at least three categories of business organization in the

UAE excluding the free zones (e.g. D.I.F.C Zone)

Company Partnership Sole trader

Private company Public company Limited liability company Partnership limited in/by/with shares

General partnership Limited partnership

Sole trader business

UAE Sole Trader Formation

A sole trader is a structure in which a business is owned by one person, acting

under their own name or using a 'trading name'. This person is fully liable for the

company's debts and contracts and there is no distinction in law between the

business and their own personal wealth i.e. unlimited liability. He is

liable/responsible to the extent of his own personal assets for the business's

debts. This means that their personal possessions are at risk. It is a “sole”

proprietorship in the sense that the owner has no partners. This is the most

straightforward structure for a business.

Basically it means the business decisions are being made by one person. Of

course, it doesn’t necessarily mean that the business has only one worker. The

sole trader can employ others to do any or all of the work in the business. Being

a sole trader is the simplest way to get started in business. Once you have

informed the government agencies of your intentions to go self-employed, you

can start trading right away (subject to any specific licenses you might require in

your line of work).

3

An Establishment, or Sole Proprietorship, is a simple structure whereby an

individual is issued a trade license in their own name, permitting them to trade

or conduct business activity on their own account. The sole proprietor is held

personally liable to the full extent for all assets and liabilities incurred by the

business.

Mainly, it is only UAE nationals and nationals of GCC countries (subject to certain

conditions) who are permitted to form establishments in UAE. However, in

recent years, a practice has evolved whereby a UAE national obtains a license for

an establishment and leases it to an expatriate(s) for an annual fee. These

expatriates, then, take on all management functions of the business and retain

all profits. This type of Arrangement, though common, is not recommended as it

is fundamentally unlawful and problems may arise if the business relationship

between the parties breaks down.

Certain foreigners in selected fields may form sole proprietorships if they reside

in the UAE. This is also referred to as “Professional Firm”. These include

professional consultants in:

A) medical services,

b) engineering fields,

c) the legal profession,

d) computer services,

f) artisan activities and similar services.

A professional firm of foreign sole proprietor is required to appoint a local

service agent. The local service agent must be a UAE national, but he has no

direct involvement in the business and is paid a lump sum and/or percentage of

profits or turnover. The role of the local service agent is to assist in obtaining

licenses, visas, labor cards, etc.

4

Partnership

1. General Partnership:

General partnerships are between two or more partners who are jointly or

severally liable to the extent of their personal assets for all of the liabilities of

the partnership. The name of a general partnership should consist of the names

of all of its partners or may be restricted to the name of one of its partners with

words to indicate the existence of a partnership, or it may have a special trade

name.

There is no prescribed capital requirement for general partnerships and no

negotiable shares are permitted to be issued due to the personal nature of the

company. Similarly, assignment of a partner’s share without the consent of all

partners is not permissible and any contract to the contrary is deemed to be

void. The names of the person(s) who will manage the company is required to be

set out in the company’s Memorandum of Association and decisions in a general

partnership have to be unanimous unless the memorandum provides otherwise,

in which case, the management is carried out in accordance with such

provisions. All the partners of a general partnership have to be UAE nationals.

Memorandum of Association: is a written constitution that governs or regulates

both the company’s (or firm’s) relations with the outside world and its internal

affairs.

Resolutions: this is the method by which companies or firms decide what they

are going to do. When decision has to be reached at a meeting the manger or

chairman will ask the members to vote on a resolution. In a general partnership

have to be unanimous unless the memorandum provides otherwise. For

example, memorandum of Association may allow resolutions to be passed by a

simple majority i.e. 50% + 1.

5

(Article 42) The Memorandum of Association of a general partnership shall

contain the following:

a. Name and purpose of the company.

B. The company's registered office and the branches thereof.

C. The capital and shares undertaken by each partner whether paid in cash or in

kind, the estimated value of these shares, subscription method and due dates.

D. Date of establishment, and expiry, if any.

E. Management of the company and names of authorized signatories and the

extent of their respective powers.

F. Commencement, and expiry, dates of the company's financial year.

G. Rate of distribution of the profit and loss.

(Article 45/3)

Unless the Memorandum of Association allows for a majority of votes, general

partnerships shall adopt resolutions made by unanimous voted the partners'

unanimous votes, and unless otherwise stipulated in the Memorandum of

Association, "majority" shall mean numerical majority of votes. Resolutions

pertaining to the amendment of the Memorandum of Association shall be valid

only in taken by the partners' unanimous votes.

Features of Partnerships

a. The ordinary rules of contract apply between partners, for example, the

partnership is voidable if induced by misrepresentation, and it is void if

formed for an illegal purpose.

b. Partners are known collectively as a ‘firm’. The name under which they

carry on business is the ‘firm name’.

c. The actions of one partner can bind the whole firm.

d. Partners are jointly liable for ALL the partnership’s debts - They do NOT

have limited liability.

6

e. Death, insanity, retirement or bankruptcy of any partner automatically

dissolves the entire partnership, (unless otherwise provided). For

example, a partner has the power to withdraw and dissolve the

partnership. The surviving, or remaining, partners have the right to

continue a partnership after its dissolution. When a partnership is

continued, the old partnership is continued, the old partnership is

dissolved, and a new partnership is created.

Advantages

(1) Ease of formation – no written agreement or registration required.

(2) Greater privacy - minimum of state regulation

(3) All partners have a right to participate in management of the business

Disadvantages

(1) No separate legal personality. This means that the business is the same as the

owners. Debts owed by the firm are deemed to be owed by the members. Wrongs

done by the firm are deemed to be done by the members.

(2) No limited liability. Partners fully liable for firm’s debts. This means there is no

limit to the partners’ liability. Any debt owed by the firm could be satisfied from

the personal fortunes of the partners.

(3) Difficulties of finance. More difficult to raise loans; floating charge not available

to use as security.

(4) No perpetual succession. A partnership is dissolved on

departure/bankruptcy/death of a single partner and then wound up.

7

2. Limited Partnership:

This type of entity is constituted by general or active partners and limited or

sleeping partners. General or active partners take an active part in the

management of the company and are jointly liable to third parties to the extent

of their personal assets for all of the liabilities of the partnership, while sleeping

partners do not interfere in the management of the company against third

parties and their liability is limited to the extent of their share capital in the

partnership. Limited or sleeping partners may however take part in the internal

administration of the firm to the extent permitted by the Memorandum of

Association. A limited partner’s name cannot be mentioned as part of the name

of the firm.

A limited partner may be held liable personally to third parties if he holds

himself out as a general partner and third parties are induced to believe so.

Internal decisions in a limited partnership are valid only by unanimous consent

unless otherwise provided in the Memorandum of Association. Only UAE

nationals may be active partners, however, limited partners may be non UAE

nationals. Limited partnerships are prohibited to issue negotiable shares in the

form of instruments. There is no minimum capital requirement.

COMPANIES

Companies are the most advanced form of business organisation. A company

comes into existence by a process known as incorporation.

Definition of ‘Company.’

An artificial legal person i.e. a personality created by incorporation rather than

by birth.

8

Upon incorporation, a company becomes a body corporate and assumes a separate

identity in law distinct from those of its members. Even though the company is

owned by its members, it is regarded as different from those members. The law in

a sense throws a veil between the company and its members/shareholder.

Formation of Companies

The process of formation of companies is generally referred to as incorporation.

Companies formed in accordance with the registration procedure stipulated by the

Companies Act are referred to as registered companies. Most companies now are

registered companies and we shall concentrate on such companies.

Registration of Companies

The documents needed for registration of companies are:

(a) A copy of Memorandum and Articles of Association. This is a formal document

stating the subscribers of the company and number of shares they have taken in

the company.

(b) An application for registration. The application must contain the following

particulars:

- A statement containing particulars of the first directors and secretary of the

company and their residential and service addresses. This statement must

be signed by or on behalf of the subscribers to the memorandum. It must

also contain consent by each of the persons named in it as director or

secretary to act in the relevant capacity. A private company need not have a

secretary. The shareholders have the power to appoint and remove

directors but at this stage the company does not have shareholders and this

explains why the founding members/ subscribers have the power to

appoint the first directors. However, subsequent directors will be

appointed by the shareholders.

9

- The company’s proposed name

- Statement of intended location of the company’s registered office

- The type of company

- A statement of capital and initial shareholding – This is a statement as to the

amount of share capital the company proposes to start business with. Only

companies limited by shares are required to provide this statement. The

statement should include the total amount of the share capital, its division

into smaller units, the classes of shares and number of shares in each class

and the rights attached to each class of shares, the number of shares taken

by each subscriber, and the amount paid and owed on each share.

All these documents would then be submitted to the Registrar of Companies. Once

the necessary documents have been lodged and the registrar is satisfied with

them, the registrar of issues a certificate of incorporation. The certificate will

contain the name of the company, the date of registration, type of company, and

the situation of the company’s registered office. The certificate of incorporation is

conclusive evidence that the requirements of the Companies Act have been

complied with, and that the association is a company authorised to be registered

and is duly registered under the law.

Classes of shares:

a. Ordinary shares: These are the most common. They carry no special

rights. Dividends are payable to ordinary shareholders after the

preference shareholders have been paid.

b. Preference shares: They carry special rights in relation to dividends. A

preference share confers the right to receive a specified

amount/percentage of dividends before any dividends are paid for other

ordinary shares. The right to dividends is deemed to be “cumulative”.

10

This means that if dividends are not paid in any year, they are carried

forward to the following year.

c. Redeemable shares: these are shares issued on the understanding that

they could be bought back by the company at a fixed date or when the

company desires. They give temporary membership and are used to raise

capital when needed. In other words, redeemable shares are used to raise

short-term funds without intending to make the holders permanent

member of the company.

Classification of companies as Private companies or Public companies

The main characteristics of a public company are as follows:

1. The capital is represented by negotiable shares publicly subscribed to

with provision for rights issues;

2. The minimum capital requirement is UAE Dirham 30,000,000 and a

minimum of 5 founding members are required to subscribe to a minimum

of 30% and a maximum of 70% of the share capital of the company.

3. The management vests in a Board of Directors consisting of a minimum of

three and a maximum of 11 persons, the chairman being a UAE national;

4. The liability of its members or shareholders is limited to the extent of

their respective share value.

5. There is indefinite duration and separate legal personality;

6. The shares are freely transferable provided always that 51% of the shares

are held by GCC nationals.

7. They are allowed to offer their shares for sale to the general public.

The main characteristics of a private company are as follows:

1. They are not allowed to offer their shares for sale to the general public.

11

2. The minimum capital requirement is UAE Dirham 5,000,000.

3. The management vests in a Board of Directors consisting of a minimum of

three and a maximum of 11 persons, the chairman being a UAE national;

4. The liability of its members or shareholders is limited to the extent of their

respective share value.

5. There is indefinite duration and separate legal personality;

6. This type of company is constituted by at least TWO founding members and

maximum of 200 who fully subscribe to the company’s capital between

themselves.

Advantages of incorporation

The following features/characteristics of incorporation should be noted:

(1) Incorporated companies enjoy separate legal personality different from that of

the members.

(2) Members enjoy limited liability for the company’s debts (for limited

companies). This means the members are liable to pay only the amount

outstanding on their shares, or in the case of a guarantee company, the amount

they had undertaken to pay on liquidation.

(3) Companies are easier to finance; they attract more loans and can use floating

charges

(4) Companies have unlimited capacity for growth. A small company can become a

large conglomerate

(5) A company has perpetual succession. This means the members may come and

go but the company could theoretically live forever.

12

Disadvantages of incorporation

(1) Detailed state regulation means that incorporated companies do not have as

much privacy as partnerships or sole proprietorships. Companies, especially public

ones, have to file notices of its decisions and annual returns of its activities with the

Registrar of Companies. The Companies Act provides a compulsory framework,

which all companies must comply with.

(2) Formation of companies involves some formalities and expense in comparison

to sole proprietorship or partnership.

(3) For a company to cease to exist it must be formally wound up and then

dissolved. Partnerships and sole businesses do not have to follow such formalities

before ceasing business.

(4) Owners of companies may lose control of the business to outsiders who invest

money in the company. Companies may also be taken over by other companies

against the wishes of some owners.

Limited Liability Companies (LLC):

Limited liability companies must have at one and not more than fifty partners. Each

partner is liable to the extent of his share capital. LLC must be owned 51% by the

UAE nationals or 100% by GCC nationals. In other words, should there be a foreign

(Jordanian, US, British...etc) partner, then at least 51% of the LLC must be owned by

UAE nationals. The company is prohibited from issuing negotiable share

certificates; carrying on the business of insurance, banking and investment of

funds; resorting to public subscription for raising its capital and accepting deposits

or taking loans from the public.

The shares of the company should be divided into equal shares. Partners enjoy a

right of pre-emption in respect of shares to be transferred by any partner of the

company to third parties. If any partner wishes to transfer his shares to a third

party the existing partners have the right within thirty days of receiving notice, to

13

purchase the shares offered for sale at a mutually agreed price. If no price can be

agreed, the company’s auditor must value the shares and existing partners may

purchase the shares at that price. If the existing partners do not elect to purchase

the shares offered for sale within the period of thirty days from receipt of notice,

the partner offering to sell the shares is free to sell them to third parties.

In August 2009, the UAE President, His Highness Sheikh Khalifa bin Zayed Al

Nahyan, issued a decree amending certain provisions of the UAE Commercial

Companies Law Federal Law 8 of 1984 (CCL) with respect to reducing the capital

required to form new businesses. Previously, a new limited liability company (LLC)

was required to have share capital of at least AED300,000 in Dubai and a minimum

of AED150,000 in the other Emirates. The amendment now enables partners in LLCs

to determine what they consider to be sufficient capital requirements for

establishing their company.

The LLC must have at least one manager (no maximum is prescribed by the NEW

UAE COMPANY LAW 2015) who may be appointed under the Memorandum of

Association or by a separate agreement. The manager(s) may be an expatriate and

maintain full authority to manage the affairs of the company.

If there is more than one manager the Memorandum of Association may provide

for the formation of a Board of Directors and may specify the method of operation

of the board and the majority required for passing its resolutions. If the number of

the partners in the company exceeds seven, supervision of the company must be

entrusted to a Board of Supervisors from at least three of the partners.

I explained earlier that company's constitution (memorandum and articles of

association) is a contract between all the members (shareholders) of the company.

One objective/aim of this constitution is to protect shareholders' rights (right to

vote, right to attend meetings, right to receive dividends etc...). However, some

shareholders still prefer to enter into another agreement between themselves

called "side agreements" or "shareholders' agreements" to protect their rights. A

question arises here: why would shareholder enter into another agreement? Isn't

14

the company's constitution adequate to protect shareholders' rights? One simple

answer is that some shareholders are looking for more security and that is why

they prefer to enter into side agreement (they want to get better protection). A

detailed answer as to why shareholders prefer to enter into such agreements is

shown below.

Two main reasons why shareholders in the UAE enter into a shareholders'

agreement:

1. To protect minority shareholders

A properly drafted shareholders' agreement together with a compatible

company Memorandum can be structured so as to protect the minority. The

Companies Law does provide some rights to minority shareholders most notably

the right to receive the annual audited accounts of the company and to inspect

its books and records. The shareholders' agreement can expand upon these

terms so that the minority will be able to monitor the business operations of the

company.

The law also provides that special majorities may be set for decisions of the

board of managers of a company and that special majorities in excess of

statutory requirements (being 50% for ordinary resolutions and 75% for

amendment of the company's Memorandum) can be established for shareholder

resolutions. These majorities can be set at a threshold sufficient to require

minority input, effectively giving them "negative control" over the company.

However in order to be effective these types of provisions – while they can be

embellished or expanded upon in a shareholders'' agreement – must be included

in the company's Memorandum.

15

So, minority shareholders can protect themselves by insisting upon a

shareholder's agreement (sometimes called a "minority protection agreement")1

which restricts the capacity of majority shareholders to engage in designated

"corporate actions" without the prior consent and agreement of the minority

shareholder (or the supporting vote of the minority's Board representative).

A well crafted shareholders' agreement will contain terms which make it clear

that a variety of "reserved decisions" should be taken only where there is

unanimous, 95%, or 75%, approval of the Board or the shareholders. The "usual"

list of "reserved matters" will generally extend to the following, although this

list is not exhaustive:

Changing the company's scope of business;

Selling major fixed assets;

Changing the auditors;

Altering or amending the company's constitution.

Issuing new shares;

Reducing or increasing share capital;

Entering a joint venture

Buying major fixed assets;

Entering into any major financing or leasing commitments

Hiring or changing senior executive management;

Giving guarantees;

Paying dividends;

Entering into related party transactions.

Although Article 154 of the CCL, in the absence of express provisions in the

company's articles of association, requires prior shareholder approval to the

1 Reconciliation with Memorandum: Unlike many jurisdictions, entering into a unanimous shareholders' agreement in the UAE does not bind the parties to the exclusion of the company's constating documents. Under the Companies Law, where there is a discrepancy between these constating documents and the terms of a unanimous shareholders' agreement, with few exceptions, the provisions of the Memorandum will prevail.

16

Board entering into loan agreements for a period longer than the duration of

three years; or to the Board agreeing to sell fixed real estate assets, it has

limited utility for the protection of minority shareholders, for two reasons:

The articles of association can and normally do authorise the Board to do

these things; and

The majority can usually gather 50% + 1 vote required to pass an ordinary

shareholder resolution.

Enforcement of Shareholder Agreement's Outside the Courts

Although shareholder agreements are usually enforceable through the UAE

Courts, because they are merely private contracts it can be difficult to rely on

them in dealings with government authorities and third parties. In these

situations it is better if minority shareholder rights are actually embedded and

reflected in the company's memorandum of association and articles of

association. If there is a serious shareholder dispute, unless the shareholder's

rights are "mirrored" in the memorandum and articles of association those

rights will be "invisible" to, and will likely be disregarded by, important outside

parties and authorities, e.g.:

The company's bankers;

The Department of Economic Development;

Other government departments (e.g. Ministry of Labour); and

Free zone registries.

Many shareholders are understandably reluctant to repeat and embed detailed

provisions of their shareholders' agreements in the memorandum of association

and articles of association, because these documents are, to some extent, public

documents. However, crucial terms needed to uphold minority rights (e.g. the

composition of the Board and the taking of important corporate actions) should

always be reflected in the company's constituent documents as a matter of best

17

practice. Otherwise, the onus rests with minority shareholders to enforce them

as private contracts through the Courts.

Enforcement of Shareholder Agreements in the UAE Courts

Shareholders' agreement will be enforced as binding contracts by the UAE

Courts but the remedies for a breach of contract are limited. The general

practice of the UAE Courts is to award financial damages after the loss making

event.

In general terms, the UAE courts do not make interim orders, e.g.:

Restraining orders (e.g. injunctions); or

Mandatory orders compelling a party to take specified action;

until the case before the court is tried in full. This process can take months or

years.

2. To circumvent or avoid the ownership requirement (51/49) specified in the UAE

COMPANY LAW

Shareholders' agreements are extremely common in the UAE and have been for

some time. This is due in part to a long-standing requirement under the

Commercial Companies Law of the United Arab Emirates (Federal Law No. 8 of

1984, as amended) (the "Companies Law") stipulating that every limited

incorporated within the UAE must have one or more national shareholders

whose share in the company's share capital must not be less than 51%. In other

words foreign parties are limited to 49% ownership in UAE companies, subject to

some exceptions made for ownership by nationals of the Gulf Cooperation

Council (GCC) states.

18

Accordingly into entering shareholders' agreements between foreign investors

and their UAE partners is one way protect the (minority) interests of those

foreign investors in UAE companies.

Where the company in question is owned entirely by UAE or qualified GCC

nationals there may be a less of an impetus for a shareholders' agreement to be

put in place. However these agreements are increasingly being accepted as

necessary in any event as part of good commercial practice.

Formal Requirements

There are no formal requirements for shareholders' agreements in the UAE.

Contracts concluded in written or oral form and even by telephone are given

equal recognition by the Civil Code (Federal Law No. 5 of 1985, as amended).

Commercial practice however is to have a written shareholders' agreement

signed by the parties.

It is important to note that there are important formal requirements stipulated

under the Companies Law for the Memorandum and Articles of Association

("Memorandum") of each LLC and for any subsequent Schedule of Amendments

to the Memorandum, altering its terms. These documents – which are

themselves contracts among the stakeholders - will often be drafted to conform

their terms to substantive matters provided for under a shareholders'

agreement or to include key aspects of such agreements. The Memorandum or

any amendments must follow strict the form requirements of the Companies

Law, must be executed by the parties before a notary Public and must be

properly filed with the Department of Economic Development or similar

authority in the Emirate in which the company is formed.

Limits on Term

There is no limit on the term of the shareholders' agreement itself; it is simply a

matter of contract. However the Companies Law does require the Memorandum

19

of a limited liability company to stipulate an expiry date for the company (Article

224). The Memorandum of such companies may state varying terms for the

existence of the company – ranges of between 5 to 50 years are not unusual. The

Memorandum may also stipulate rights of renewal for the stipulated terms.

Assignments of Shares and Preemption Rights

The Companies Law stipulates that:

a. No assignment of shares will be effective if:

i. It results in the shareholdings of the national shareholders of the company

being reduced to less than 51% of the total shares of the company; or

ii. Results in the increase in the number of shareholders in the company in excess

of the number prescribed for a private company (currently 50); and

b. Where a shareholders does wish to sell his shares in the company he is

entitled to do so subject to the preemptive rights of existing shareholders as set

out in the Companies Law.

These statutory preemptive rights deserve some special consideration given

their importance in the general scheme of corporate law in the UAE. Under

Article 79 of the Companies Law where a shareholder proposes to assign his

shares to a third party non-shareholder (whether for value or not) he must first

offer to sell his shares to the remaining shareholders. Each shareholder has the

right (pro-rata to their holdings if more than one take up the offer) to purchase

the shares of the departing shareholder at any agreed price or, in the absence of

agreement, at a value determined by the auditors of the company. If at the

expiry of 30 days from the date of the initial notice none of the shareholders has

exercised their right to acquire the departing shareholder's shares that

shareholder shall be free to dispose of his shares.

20

No shareholders' agreement can deprive a shareholder of this fundamental right

although many such agreements augment or flesh out the terms of the

preemptive rights – for example providing guidelines to the company's auditors

for valuation methodology or setting out basic representations and warranties

to be given by the departing shareholder on the sale of his interest. So long as

such terms do not violate the terms of the Companies Law or other applicable

law they will in all likelihood be permissible.

The parties may also seek to include other contractual restrictions into their

shareholders' agreement and potentially company Memorandum. Again to the

extent that these do not contravene the law or in particular impinge upon a

shareholder's legislated preemptive rights they will be acceptable restrictions.

Such restrictions would include "lock-ins", drag along and similar rights and buy-

sell provisions.

"Side Agreements"

Shareholders in UAE companies are motivated to enter into shareholders'

agreements as a matter of best practice for the same business reasons as in

other jurisdictions, namely to set out their respective rights and obligations and

to protect their local commercial interests.

This latter concern is of particular importance to foreign parties conducting

business through limited companies where their UAE partner has no real

involvement in the business itself. This is often the case in the UAE where the

local shareholder merely acts as a "sponsor" to the commercial activity carried

on by the foreign party. This type of arrangement is often enshrined in a form of

shareholders' agreement under which the local national is systematically

stripped of his shareholders' and management rights and proportionate share of

the company's profits while the de jure ownership is reflected in the company's

Memorandum and trade licence. The same type of arrangement may be

21

accomplished through other forms of agreements such as trust declarations in

favour of the foreign party or though loan and pledge arrangements.

While common these types of arrangements are not favoured in the UAE. On a

strict reading of the Companies Law these types of "side agreements" as they

are known are legally void. In fact in 2004 the UAE Federal National Counsel

enacted Federal Law No. 17 of 2004 - the Anti-Concealment (Fronting) Law for

the purpose of fighting the quasi-established practice of implementing side

agreements in commercial activities. The Anti Fronting Law provides that that

any arrangement designed to circumvent the ownership requirements of the

laws of the UAE would be considered unlawful, punishable by fines and possibly

imprisonment.

To date the Anti-Fronting Law has not been implemented. The UAE courts have -

pending the law's implementation - recognised the interests of foreign parties in

considering the validity of such agreements however they have also required the

companies subject to such arrangements to be dissolved subsequently. Foreign

parties entering the UAE market need to be aware of these considerations when

entering into the agreements relating to their local company.

So, in view of the Companies Law requirement to have a minimum 51% of the

shares in UAE companies owned by UAE nationals, the foreign shareholder will

often have entered into a “side agreement” with the UAE shareholder.

The side agreement probably provides for the following:

Only the foreign shareholder has contributed to the share capital of

the company and accordingly owns all the share capital of the

company.

The foreign shareholder is the sole owner of all the assets and the

trade name of the company and is the actual agent with respect to

distribution agreements and commercial agencies of the company.

22

The UAE shareholder is the custodian and trustee with regard to the

51% shares registered in his name.

The UAE shareholder will waive/give up any shares held by him in

the share capital of the company in case of liquidation of the

company (whether in the form of in kind dividends or public

auction proceedings or amicably).

The entire profits and losses in the company will be earned/borne

by the foreign shareholder except for an agreed percentage of the

net profits of the company (agreed percentage).

The UAE shareholder will not claim any right to the profits

generated by the company except for the agreed percentage.

The UAE shareholder acts only as the local sponsor for the company

to obtain and renew the licences, visas and work permits relating to

the company and its employees.

The UAE shareholder is entitled to an annual fixed fee (fixed fee) at

the beginning of each financial year for acting as the local sponsor

for the company in addition to the agreed percentage.

The UAE shareholder is entitled to 10% interest on undistributed

amounts of the agreed percentage at the end of the financial year,

to the extent that the company did not distribute profits in the

relevant financial year.

The foreign shareholder, represented by an individual, is appointed

as the manager of the company.

I explained earlier that one aim of a shareholders' agreement is to circumvent

the ownership requirement specified in the UAE Company law and that such

agreement is null and void. But what if a dispute occurs between the UAE

shareholder/partner and the foreign partner/shareholder? On one hand, the

company's constitution shows the UAE partner owns 51% of the company's share

capital. On the other hand, the side agreement either shows that the UAE

partner has not actually contributed to the company's share capital (zero

23

contribution) or that he has contributed to less than the limit specified by the

UAE Company law (e.g. 15% of the company's share capital). In such cases, we

have two contradicting documents namely the company's constitution and the

shareholder's agreement. So, which document/agreement will prevail over the

other one? In Dubai courts, judges are willing to enforce and recognize side

agreements but they will liquidate the company (bring the company's life to an

end). However, Abu Dhabi judges, as shown below, have recently declined to

enforce and recognize side agreement.

Abu Dhabi Court’s approach - Side Agreements and their enforceability

In a dispute between a UAE investor and a foreign investor, the parties disputed

over whether a side agreement or the official Memorandum of Association

(MOA) governed their relationship. The UAE investor insisted that the official

MOA is the valid document whereas the foreign investor argued that the side

agreement states that the foreign investor has a greater percentage in shares

and that the side agreement is the valid/ applicable agreement to govern the

relationship between the two parties.

As outlined in the previous article, the matter had been decided in favour of the

UAE investor at the first instance and appeal levels, however the foreign

investor appealed further to the Supreme Court.

In its judgment, the Supreme Court held that the side agreement can be

established by any means of evidence and allowed the parties to hear testimony

of witnesses.

When the Court of Appeal heard witnesses brought in by the foreign investor

and rejected the claim, the parties appealed again to the Supreme Court. The

Supreme Court considered the evidence and decided that there was enough

evidence to prove the existence of the side agreement and subsequently

directed the Court of Appeal to look into this. Upon review of the evidence, the

24

Court of Appeal issued its judgment confirming the existence of the side

agreement.

The UAE investor appealed for the third time to the Supreme Court contesting

the validity of the side agreement and it is this appeal which is the subject

matter of this update.

This recent judgment handed down by the Federal Supreme Court demonstrates

a unique position on the issue of side agreements and the removal of a partner

in a company. The judgment sheds light on the validity and enforceability of side

agreements in the context of a 49/51 UAE limited liability company. The

judgment also addressed a very important issue on whether the majority

shareholder can request the court to remove any of his partners/shareholders

and the grounds for such request. The case is discussed in detail below.

Background

A dispute arose in relation to a limited liability company in Abu Dhabi between a

UAE shareholder (owning 51 % of the shares), an Omani shareholder (owning 24 %

of the shares) and a US company (owning 25 %). An action was filed by the UAE

shareholder requesting confirmation of its entitlement to 51 % of the profits

according to the shareholder’s agreement. The UAE shareholder also requested

the court to issue judgment for the withdrawal of the Omani shareholder on the

basis that the Omani shareholder had not been cooperative and caused loss to

the company as a result of his lack of cooperation. The Omani shareholder

argued that the partners in the company signed a side agreement and entered

into an arrangement whereby the UAE partner would own 37.5 % of the shares,

the Omani partner would also have 37.5 % and 25% was owned by the US

Company.

Court of First Instance

The matter progressed before the Court of First Instance and the court issued

judgment in favour of the UAE partner on the basis of the official documents

25

(the Memorandum of Association) which confirmed that he was the owner of

51% of the shares of the company. The court however rejected the request of the

UAE partner to expel the Omani partner.

Federal Court of Appeal

Both the UAE and Omani partners appealed further against the judgment and

the Court of Appeal rejected both appeals and upheld the lower judgment.

Federal Supreme Court

Both parties appealed further to the Federal Supreme Court. The Federal

Supreme Court ruling highlighted two important issues:

Side agreements

The general principle in UAE Evidence law is that a written contract can only be

contradicted by written evidence, except where the opponent waives his right

to documentary evidence or where there is an agreement to defraud the law.

When the fraud exception to the general principle applies, the party against

whom the fraud was made can use all means of evidence including testimony of

witnesses to prove that the official agreement is not genuine vis-à-vis the side

agreement.

Withdrawal of the Omani shareholder

The UAE shareholder requested the court to dismiss the Omani shareholder as a

result of the losses he caused the company to incur. The Court of First Instance

refused to accept the UAE shareholder’s request on the basis of articles 37, 47

and 63 of the Commercial Companies Code. These articles mandate that a

numerical majority is required and in these circumstances, only one shareholder

out of three requested the dismissal. This was followed by the Court of Appeal

however this was reversed by the Federal Supreme Court (as discussed below).

Federal Supreme Court

26

The Federal Supreme Court decided that what is legally required is the majority

of shares rather than a majority of the partners and accordingly a shareholder

owning a majority of the shares could request the court to dismiss a partner

based on sufficient reasons to justify the request. As the UAE shareholder owned

51% of the shares he could request the dismissal of the Omani entity on the basis

of the following articles:

Article 677 of the civil code provides:

(1) It shall be permissible for a majority of the partners to apply for a judicial

order dismissing any partner if they adduce serious reasons justifying the

dismissal.

(2) It shall likewise be permissible for any partner to apply for a judicial order

that he cease to be a partner in the company if the company is of defined

duration, and he provides reasonable grounds for such application.

(3) In both of the foregoing events the provisions of Article 675 (2) shall apply to

the share of the dismissed or withdrawing partner, and such share shall be

assessed in accordance with its value on the date the claim was brought.

Article 675 (2) provides that ‘it shall likewise be permissible for an agreement to

be made to continue the company as between the remainder of the partners if

one of them dies or is placed under a legal restriction or becomes bankrupt or

withdraws, and in those events such partner or his heirs shall be entitled only to

his share in the assets of the company…’

In light of the above, the Federal Supreme Court overruled the Court of Appeal

judgment and remanded the case again to the Court of Appeal to look into the

appeal and consider the directions of the Supreme Court.

27

The Court of Appeal

Upon re-trial, the Court of Appeal gave the Omani shareholder the opportunity

to call witnesses to prove his side agreement. However, the case was dismissed

for lack of evidence confirming ownership of the UAE partner for 51% of the

shares. The court also dismissed the appeal filed by the UAE partner to remove

the Omani partner on the basis of lack of evidence to support such request.

Both parties appealed again to the Supreme Court. The Omani shareholder

argued that it has submitted sufficient evidence to establish the side agreement

but argued that the Court of Appeal neglected this issue. The UAE shareholder

filed its appeal insisting on its request to remove the Omani shareholder.

Federal Supreme Court

The Federal Supreme Court confirmed that the Court of Appeal neglected to

look at evidence confirming the Omani’s shareholding. The Court of Appeal did

not address the side agreement which contains a clause (Article 20 of the

contract) Article 20 of the side agreement states that “Each of the parties

acknowledges that they hold shares equally in the company.” The profits and

losses of the firm were distributed equally under Clause 20. This is in addition to

various other documents which prove that the profits and losses were

distributed equally between the two companies and not based on the official

51/49% shareholding of the UAE Company.

The Federal Supreme Court, however, rejected the appeal filed by the UAE

shareholder on the basis that there was no evidence to support its request to

remove the Omani shareholder.

The Supreme Court therefore overruled the Court of Appeal judgment for the

second time and returned the case back for retrial to look into the documents

and arguments raised by the Omani shareholder in support of the side

28

agreement.

As a result of this judgment the request of the UAE partner to expel the Omani

partner became final and the only issue that remained to be addressed by the

Court of Appeal was the issue of the side agreement as argued by the Omani

partner.

The Court of Appeal Judgment –upon retrial

As a result, the Court of Appeal heard the case again (for the third time) in order

to decide whether or not there are sufficient documents to establish the

existence of the side agreement/arrangement as argued by the Omani partner.

Upon reviewing all the documents submitted by the Omani partner, the court

concluded that there is sufficient evidence to establish the existence of the side

agreement between the parties (and that the shares have been distributed on

the basis of 37.5% to the UAE and Omani partners and 25% to the US Company).

Comment

In this case, it was clear that the shareholders of the company could continue the

company’s business on the basis of the side agreement. In the event that one of

the parties wanted to dissolve the company, a separate court judgment would

be needed to dissolve the company on the basis that the company lacked the

required legal corporate structure as the UAE partner’s shares had been

declared to be less than 51%, however the partners may need to decide whether

or not their interest are better served by living with the side agreement and

continue with the company or dissolve it.

LATEST SUPREME COURT JUDGMENT

The Supreme Court ruled on this matter for the third time and in this latest

judgment, the Supreme Court decided very differently to the last decision and

declared that the offical MOA as registered with the authorities is the valid

29

agreement that governs the relationship between the parties and not the side

agreement.

The Supreme Court relied on Articles 8, 10 and 11 of the Commercial Companies

Law (CCL) and held that it is imperative for all agreements relating to

commercial companies to be in writing, notarised and registered in the

Companies Commercial Register so as to comply with the requirements of the

CCL and that all amendments to the company documents (i.e. Memorandum of

Association) must also be duly notarised and registered in the same manner as

the MOA.

In this case, the Supreme Court concluded that as the side agreement was not

notarised or registered in the Companies Commmercial Register, it is therefore

null and void.

Reminder of the facts of the case:

A dispute arose in relation to a limited liability company in Abu Dhabi between a

UAE shareholder and an Omani shareholder over the ownership of the actual

shareholding in a limited liability company. Legal action was commenced by the

UAE shareholder requesting confirmation of its entitlement to 51% of the shares,

assets and profits of the company according to the official memorandum of

association (MOA) of the company as officially registered and declared with the

competent authorities. The Omani shareholder, however, claimed that it owned

more than it’s registered shares (as reflected in the side agreement).

COMMENTS ON THE JUDGMENT

1. It is apparent that this Union Supreme Court judgment contrasts with the

previous two judgments by the same court (in the same dispute) which

previously decided that side agreements are not null and void if they were not

notarised or registered pursuant to Articles 8,10 and 11 of the CCL. The court in

the former two rulings held that the parties can even hear witnesses to prove

30

this matter. The court also held that the side agreement can be concluded from

various documents and not necessarily from a single written agreement and that

such agreement is valid even without notarisation.

2. The new ruling is therefore a material change from the Supreme court’s

former rulings on the issue of side agreements. As side agreements are not

official agreements, they cannot be notarised or registered in the Commercial

Register.

3. The main purpose of the side agreement is that it is binding between the

two parties only and concealed from the Commercial Register. This purpose

would not be achieved if there was a requirement to notarise it or file it with the

Commercial Register. This has been confirmed by the Supreme Court itself in

former rulings. The side agreement also includes provisions that cannot be

notarised or accepted by the official authorities such as the shareholding

percentage which is usually different from the official documents.

4. It is to be noted that this latest judgment did not address the effect of

Article 395 of the Civil Code. Article 395 provides that: “If the contracting parties

conceal a true contract with an apparent contract, the true contract will be the

effective one as between the contracting parties and a special successor.” If Article

395 had been addressed by the Supreme Court, it is possible that the court would

have produced a different result.

5. It should also be highlighted here that although this judgment addressed

the issue of the validity of the nominee agreement with regard to the official

MOA, it has not however, adressed the issue of whether the rights of the parties

under the MOA should be liquidated as a result of the invalid nominee

agreement.

6. The judgment also did not address the issue of the date the invalidity

occurs i.e. whether it is from the inception of the company or from the date of

the judgment.

7. In view of the above judgment and the previous Supreme Court decisions

on the same matter, it should be noted that the courts in future cases, will not

necessarily decide that all side agreements are null and void. Each case will be

31

decided on a case by case basis and the arguments raised above (in paragraphs

3, 4, 5 and 6) may also appear in separate matters in the future.

Capitalisation of UAE companies

As a general rule, companies in the UAE must have a minimum national

shareholding of 51 per cent. Companies based in the free zones are not caught by

such ownership restrictions - although their ability to do business in the UAE

outside the free zone is restricted.

The most common forms of corporate vehicle in the UAE are limited liability

company (LLC) and joint stock company (public and private), with LLCs tending

to be the more commonly used vehicle for international investors establishing

joint venture operations.

As well as differences relating to board representation and governance

generally, the other clear distinction between the company forms is the

minimum share capital required. A Private JSC requires a minimum share capital

of AED5 million (AED 30 million for a Public JSC) and an LLC has historically

required a minimum of just AED150,000 in Abu Dhabi and AED300,000 in Dubai.

However, the minimum amount for LLCs has now been removed, although the

authorities will expect the LLC to be established with a sufficient level of capital

to conduct its proposed activities (there are no guidelines as to how this will be

assessed). Certain sectors also impose additional or higher levels of capital.

Both LLCs and JSCs must allocate 10 per cent of their net profits each year to a

statutory reserve, but this allocation can be suspended if the reserve reaches an

amount equal to 50 per cent or more of the company’s total equity share capital.

There has accordingly been a preference for shareholders of highly capitalised

UAE companies to put shareholder funds in by way of loan (as opposed to

shares), thereby avoiding the need to reserve more than necessary – an

approach assisted by the absence of any thin capitalisation rules in the UAE.

32

Partnership Limited With Shares:

A partnership limited with shares is a company formed by general partners who

are jointly liable to the extent of their personal assets and participating partners

who only participate in the capital and are jointly liable with the general partners

only to the extent of their shares in the capital of the company. All general

partners must be UAE nationals whereas participating partners may be non-UAE

nationals. The capital of a partnership limited with shares must be divided into

negotiable shares of equal value.

The names of the general partners must be part of the name of the partnership. If

the name of a participating partner is mentioned, with his knowledge, as part of

the partnership name, such a partner becomes liable towards third parties.

The capital of the company must not be less than UAE Dirhams 500,000. The

management of the partnership is entrusted to one or more general partners

under the Memorandum of Association. A participating partner may not, even with

consent of the general partners, deal with third parties. He may, however, be

actively involved in the internal management of the company within the limits laid

down in the Memorandum of Association. Every partnership limited with shares

must have a Board of Supervisors consisting of at least three members from

amongst the participating partners or others. The board of supervisors does not

take part in the day to day management of the company but performs a

supervisory function and may request managers to present reports of their

management and examine the company’s books and documents.

Free Zones in the UAE

In recent years, the UAE has become host to many free zones which offer

foreign investors numerous benefits such as 100 per cent foreign ownership (in

contrast to the 51 per cent minimum national shareholding mentioned above),

guaranteed tax free status, a one-stop-shop of support services (including

licensing and visa sponsorship procedures) and other advantages such as high

33

technology facilities and services and real estate infrastructure. In most free

zones it is possible to establish either a branch or representative office of a

foreign company or to establish a limited liability company.

There are numerous free zones in the UAE - each has its own geographic

boundaries and regulations and most have been established to accommodate

certain types of activity (such as media, education, manufacturing and financial

activities).

A free zone company is generally excluded from operating in the UAE outside of

the free zone in which it is incorporated. Despite their physical locations, free

zones are generally considered to be offshore jurisdictions and entities

operating from such zones are not permitted to carry out their activities onshore

in the UAE. Therefore, if a free zone company wants to conduct business in the

UAE outside of the free zone in which it is registered, it will in theory need to

enter into an agreement with a local agent or distributor in the UAE or establish

a formal presence, such as a branch office, onshore.

However, in a recent development, HH Sheikh Mohammed bin Rashid Al

Maktoum, Vice President and Prime Minister of the UAE and Ruler of Dubai has

issued a new licensing law which, amongst other things, provides that, in

coordination with the free zone authorities, the Dubai Department of Economic

Development may authorise free zone entities to practice their activities

onshore in Dubai. Although a welcome move, no additional clarification has been

given as to the circumstances in which such authorisation will be granted and

the conditions which must be complied with - the full effects and

implementation of the new law therefore remain to be seen.

THE NEW UAE COMMERCIAL COMPANIES LAW: A COMPARATIVE VIEW

The new Companies Law (“New Law”) as approved by the Federal National

Council introduces some incremental reforms to the existing Companies Law

34

(“Existing Law”), but mostly maintains the fundamental framework and features

of the old provisions.

Whilst the New Law introduces some new concepts and approaches, most of the

essential features of the Existing Law are maintained. Despite media

speculation, the New Law applies the same conservative approach in relation to

foreign ownership restrictions under the Existing Law, so foreign investors are

limited to 49%. Also, the New Law does not allow sell-downs in IPO deals.

By the same token, the majority of board seats, including the chairman of the

board, of public joint stock companies must be held by UAE nationals. Founders

of public joint stock companies continue to be restricted by a lockup period of

two years under the New Law, which defeats sell-down exist options in IPOs.

Also, the New Law has not reformed the governance of limited liability

companies through introducing a proper board of directors’ structure, but has

maintained the old form of governance by “managers”. However, the restriction

on the number of managers under the Existing Law (namely five managers) has

been lifted under the New Law.

On the other hand, the New Law introduces some new concepts. For example,

the New Law:

allows for sole-shareholder companies, in limited liability companies;

addresses employees’ incentive share schemes;

enables shareholders in pubic joint stock companies to sell their

preemption rights (rights issue);

facilitates strategic share placements by public joint stock companies

within pre-emptive complications;

prohibits financial assistance (in line with the international market

practice);

enables the legal pledge of quotas in limited liability companies. Some

other reforms are discussed below in details.

35

This note aims to shed some light on the main differences between the New Law

and the Existing Law, the fresh concepts enacted under the New Law, and to

highlight the practical impact of these differences.

This note follows the same sequence of the New Law.

Detailed Views

General Rules:

1. Article 5 – Free Zone Companies – Free zone companies are exempted from

the application of the New Law. However, it is to be noted that article 5 states

that there will be a Cabinet decree that will set out the conditions which should

be followed in registering free zones companies in case these companies wish to

operate onshore or outside the borders of the free zone in question.

2. Article 6 – Corporate Governance – The New Law provides that private joint

stock companies will be subject to corporate governance rules provided that

such companies are composed of more than 75 shareholders. A ministerial

decree setting out the applicable corporate governance rules will be issued in

due course. The expected corporate governance rules will include financial

penalties on board members, managers and auditors of any defaulting company.

3. Article 8 – The Concept of “sole founder” – The New law provides for the

first time the concept of having a company with a sole founder. This applies on

limited liability companies.

4. Article 10 – Local Ownership – The New Law continues to follow a

conservative approach in respect of local ownership restrictions, so companies

must be owned 51% by the UAE nationals or 100% by GCC nationals (LLC

COMPANIES).

5. Article 24 – Exclusion of Liability – The New Law introduces an explicit

clause stipulating that any provision in the articles of the company allowing the

company or any of its subsidiaries to agree to exclude any person from their

current or previous liability towards the company will be void. However, this

36

article does not address the provisions that may be agreed upon between the

shareholders in separate shareholders agreement (in particular between

nominees and beneficial owners) whereby one of the shareholders is excluded

from liability. Unexpectedly, this clause prohibits the exclusion of liability in

general without limiting the exclusion to liability arising out of gross negligence

or willful misconduct, as provided under the Civil Code.

6. Article 26 – Companies Accounting Books – New obligations are imposed

on companies to retain their accounting books for a period of not less than five

years from the end of each financial year. This is a new requirement under the

New Law that is not provided for under the old Law. This provision comes in line

with similar requirements in other Middle Eastern jurisdictions. Also, companies

may retain electronic versions of their documents provided that these

documents will be saved in compliance with a decree to be issued by the

Minister.

7. Article 28 – Financial Year – Each financial year may not exceed 18 months

and should not be less than six months. This clause will have an impact on

calculating the lockup period in public and private joint stock companies, as it

will shorten the two/one financial year(s) required with respect to the founders

of public/private joint stock companies. Likewise, it will affect the timeline

required to convert a limited liability company to a public joint stock company as

provided for under article 275 of the New Law.

8. Article 32 – offering of shares to public – This article explicitly prohibits any

company (either in one of the free zones or onshore) from making any

advertisements or marketing to invite general public to subscribe in shares

without obtaining the prior approval of SCA. Under the Existing Law, there is no

explicit provision prohibiting such practices, but rather it is a matter of practice

and unwritten rules followed by SCA.

9. Article 36 – Retention of Documents - Similar to article 26 referred to

above, article 36 provides that the Minister will issue a decree setting out the

time limit for companies to retain corporate documents.

37

Rules Governing Limited Liability Companies

1. Article 71 – Sole ownership –Article 8 provides that a limited liability company

may be established by one natural or corporate person. This approach follows

free zone regulations which allow the incorporation of a free zone

establishment (FZE), which originally is a common law concept. Under the old

Law, limited liability companies may only be established by a minimum of two

founders and a maximum of fifty. The maximum limit of fifty partners still

applies under the New Law.

2. Article 79 – Pledge of Quotas (shares) - The New Law provides that limited

liability quotas (or shareholdings) may be pledged. The old company Law is

silent in respect of pledge of quotas, and so it is questionable whether quotas

can be pledged legally. This new development will assist raising of debt finance

by owners of limited liability companies and will enhance the security package

that can be offered to the financiers. Pledge of quotas will add another level of

comfort to beneficial owners of quotas (foreign investors) in respect of their

shareholding relationship local registered owners (nominee).

3. Article 80 – Preemption Rights – preemption rights are still mandatory by

operation to law under the New Law, as is the case under the old Law.

4. Article 83 – Company’s Managers – Under the New Law, companies may

appoint one or more managers without setting out a maximum number of

managers. Under the old Law, the maximum number of mangers is five.

5. Article 86 – Competition – Under the New Law, manager(s) of a company may

not be allowed to operate any business in competition with the business of the

company in question. Defaulting manager(s) will be discharged and compensate

the company accordingly. This matter is not addressed under the Existing Law.

6. Article 93 – Invitations to General Assemblies– Invitations to general

assemblies need to be sent out 15 days before the date of the meeting or less

than 15 days if all partners agree. Under the old Law, the notice period required

is 21 days which may not be abridged.

38

7. Article 96 – Quorum for General Assemblies – Under the New Law, general

assemblies will not be valid unless attended by partners owning 75% of the

capital of the company. If the quorum is not satisfied in the first meeting, the

second meeting shall be called for within 14 days from the first meeting, which

shall not be valid unless attended by partners owning 50% of the capital of the

company. If the quorum is not satisfied in the second meeting, a third meeting

shall be called for after the lapse of 30 days from the date of the second

meeting, which shall be valid regardless the quorum attended such meeting. This

means that the existing difficulties in achieving quorum general assemblies for

public joint stock companies at the first attempt have been magnified by the

New Law. Resolutions of general assemblies shall only be valid if approved by

partners owning at least 50% of the capital of the company. Under the old Law,

general assemblies may only be valid unless attended by partners owning 50% of

the capital of the company. If the quorum is not satisfied in the first meeting, a

second meeting shall be called for within 21 days from the first meeting, which

shall be valid regardless of the quorum attended such meeting. Also under the

old law, any amendment to the articles of the company requires the approval of

partners owning at least 75% of the capital of the company. However, under the

new law, amendment to the articles of the company requires the approval of

partners holding at least 75% of the votes represented at the general assembly

meeting.

8. Article 103 – reference to joint stock companies rules – Article 103 of the New

Law refers to the rules governing joint stock companies with respect to any

matter which is not addressed under the rules of limited liability companies.

Such reference is not provided for under the old Law.

Rules Governing Public Joint Stock Companies (“PJSC”)

1. Article 107 – Number of founders - PJSC may be established by a minimum of

five founders. Under the Existing Law, PJSC requires a minimum of 10 founders.

This article will facilitate the constitution of PJSC, in particular in the set up

phase before offering the company’s shares to public.

39

2. Article 112 - Founders’ committee – The New Law provides that founders

committee shall be composed of three members without setting out a maximum

limit. Under the old Law, founders committee should be between three to five

members.

3. Article 117 – Founders’ ownership – The New Law provides that founders may

own a minimum of 30% and a maximum of 70% of the capital of the

company. Under the Existing Law, founder may own a minimum of 20% and a

maximum of 45% of the capital of the company. This article will have an impact

in relation to encouraging investors to promote an IPO without facing the risk of

losing their control of their business, as they are allowed to own up to 70% of the

company and offer 30% to public. This will also promote IPOs for companies that

have good financial standing and do not require additional capital inflows which

are high compared to their pre-existing issued capital. Unfortunately, the New

Law does not facilitate or permit sell-downs by existing shareholders, an avenue

already available in most developed markets. Such a reform would have greatly

encouraged new IPO transactions.

4. Article 123 – Underwriters – For the first time in the UAE the New Law

recognizes the role of underwriters. Under the old Law, underwriting activity is

not addressed. There will be a ministerial decree regulating the underwriting

activities to subscribe for unsubscribed shares and resell them again in the stock

market. The facilitators of underwriting could enable the IPO market to flourish

and attract leading global financial institutions to act as underwriters and

develop the UAE capital market.

5. Article 124 - Subscription period – Subscription period opens for a period of a

minimum of 10 days and a maximum of 30 days. Under the old Law, the

subscription period opens for a period of a minimum of 10 days and a maximum

of 90 days.

6. Article 129 – Book Building - The New Law refers explicitly to a book

building mechanism in relation to the pricing of newly issued IPO shares. The

detailed regulations governing and regulating book building will be issued later.

Pricing is to be determined at the discretion of the issuer and the banks at a

40

valuation that is acceptable to investors, the issuer and the selling

shareholder(s).

7. Article 131 – Constitutional General Assembly – Under the old Law,

constitutional general assembly requires the attendance of shareholders owning

at least 75% of the capital. However, the New Law provides that the

constitutional general assembly shall be valid if attended by shareholders

representing 50% of the capital of the company. This article comes as an attempt

to facilitate and expedite the process for incorporation.

8. Article 143 – The Composition of the Board of Directors – Board of directors

under the New Law should be composed of a minimum of three members and a

maximum of 11. Under the old Law, board of directors should be composed of a

minimum of three members and a maximum of 15.

9. Article 144 – Election of Board Members/Expert board members – The New

Law provides for cumulative voting at any election of board members.

Cumulative voting is not provided for under the old Law, but rather it was under

the applicable Corporate Governance rules. The voting mechanics will allow each

shareholder to distribute voting powers amongst various board candidates. This

should increase the chances of minority shareholders achieving board

representations. The Existing Law also allows the general assembly to appoint

“expert” board members who are not shareholders provided that the total

number of “expert” board members may not exceed one third of the total

number of the board of directors.

10. Article 151 – Nationality of Board Members – The requirement under the

Existing Law that the majority of board members and the chairman should be

UAE local nationals continues to apply under the New Law.

11. Article 156 – Board Meetings - Under the New Law, the board of directors

shall meet at least four times a year. Such requirement is not provided under the

Existing Law. This is something that has been dealt with separately under the

Corporate Governance rules.

12. Article 170 – Voidance of resolutions - Any resolution not in compliance with

the provisions of the New Law, or adopted without consideration to the

41

company’s interests in favor of a particular group of shareholders, causing

damage to them or providing a private benefit to the members of the board of

directors or to third parties may be revoked. Proceedings for annulment are

time barred on the expiry of 60 days from the date of adopting the resolution

contested. Under the old Law, the applicable prescription period is one year.

13. Article 172 - Invitations General Assemblies– General assembly invitations

need to be sent out 15 days before the date of the meeting or less than 15 days if

95% of the shareholders agree. Under the old Law, the notice period required is

21 days and cannot be abridged.

14. Article 193 – Issued and Authorized capital – The New Law provides that the

issued capital of PJSC shall be not less than AED 30 million. In addition, the

company may decide to have an authorized capital which may not exceed twice

the value of the issued capital. Authorized capital is defined as the maximum

number of shares that the company is authorized by the constitution

(memorandum and articles of association) to issue. More specifically, under the

old Law, the concept of “authorized” capital is not addressed. A new set of rules

have be issued to allow companies to increase its issued capital within its

authorized capital. By way of explanation, the authorized capital is not more

than a notional concept which has no financial implications or effect. In other

jurisdictions, it only allows the board of directors of joint stock companies to

increase the issued capital within the limits of the authorized capital by a board

resolution instead of having an extraordinary general assembly resolution

(shareholders' consent is not required). So the difference between authorised

capital and issued capital is analogous to the difference between an approved

loan facility and a partially drawn approved loan facility. For example, if the

authorized capital of a company is AED 120 million and its issued capital is AED 50

million. The board members of such company can increase the issued capital

with any amounts until they reach the ceiling of AED 120 million with a board of

directors resolution only instead of holding an extraordinary general assembly

(shareholders' consent is not required). Any increase of capital in excess of the

120 million (authorized capital) should be pursuant to a resolution from the

42

extraordinary general assembly of the company; shareholders' consent is

required. So, if the AED 120 million authorized capital has been fully exhausted

by the company's directors, they will not be able to issue a single share/stoke

above the AED 120 million authorized capital without seeking the permission of

shareholders. Therefore, the authorized capital is merely to facilitate procedural

matters associated with capital increases. In the UAE, there will be a ministerial

decree that will set out the procedures by which the issued capital can be

increased within the authorized capital. As for the issued capital, the Companies

law allows the shareholders to pay 25% only of the issued capital of a company

upon its incorporation and the remaining 75% should be completed within 5

years. For example, if the issued capital of a company is AED 40 million, the