Embed Size (px)

Citation preview

Company presentation

June 2007

2

DisclaimerThe present study has been prepared only for information purposes. It

does not constitute an advertisement or offer for securities in public

trading. It uses sources of information that Sygnity S.A. and Emax S.A.

have acknowledged as reliable and exact, however it is not represented

that the information is comprehensive and fully reflecting the real state.

The presentation may include forward-looking statements which

constitute an investment risk or a source of uncertainty and may

substantially differ from actual results. Sygnity S.A. and Emax S.A. bear

no responsibility for the effects of decisions taken on the basis of the

present study. The responsibility rests only on the user of the present

study. The study is subject to a protection resulting from the law on

copyright and related laws. Copying, publishing and distribution of the

study is subject to a written consent of Sygnity S.A. and Emax S.A.

2

3

Polish economy is in the good condition

• Continued economic revival commenced in 2005:– 6,4% GDP growth y-o-y in Q4 2006

– Q1 2007 GDP growth expected at historically high level and set to continue throughout whole 2007

– continued strong domestic consumption

• Improvement on the labour market: – increase of employment by 3.8% y-o-y in January 2007

• Most optimistic assessment of the economic situation by entrepreneurs since the beginning of the 1990s

3

4

Polish IT market ready for natural growth

• Annual IT spendings per capita in Poland ca. 100 EUR vs. over 700 EUR in EU 15

• EU funds availability for new EU members

• Development of outsourcing and BPO: Poland becoming the Europe’s accountant

• Domestic players outpace the international ones on the local IT services market

The expected speed of market growth in Western Europe vs. Poland

4

00,5

11,5

22,5

33,5

4

2005 2010

0

50

100

150

200

250

2005 2010

Software and IT services market growth in Poland 2005-2010E (EUR bln)

Software and IT services market growth in Western Europe 2005-2010E (EUR bln)

CAGR

12.8%

CAGR

5.8%

5

Signs of the Polish IT market revival

• Ordinance on the State Informatization Plan for the years 2007-2013

• Changes on the energy market• Medical Services Register (RUM) • Further computerization of schools by Ministry of National

Education • Border Guards projects • Projects of the Central Office of Land Surveying and Cartography• Development of local (regional) government market - EUR 2.5 mln

to be granted from EU funds• Development of banking market – increasing competition, new

products, implementation of Single European Payments Area, the development of the network of banking outlets, tendency for foreign banks to enter the Polish market

5

6

Sygnity snapshot – establishment of the Company and market capitalisation

• Sygnity has been formed as the result of the process of combining the experience and the best practicies of ComputerLand and Emax in order to bring the new quality to the Polish IT market. Sygnity SA is the second biggest Polish IT company on the market with over 3000 employees and the total turnover at the level of PLN 1.2 bln (2006)

• Proforma capitalization as of 22 May 2007: PLN 988 bln (Sygnity: PLN 660 bln; Emax: PLN 328 bln)

• Free float (after the merger): 85%

6

7

Sygnity snapshotProforma results of ComputerLand Group for 2006, including the results of Emax Group for 2006, as if the acquisition had taken place on 1 January 2006

2006 CL Group Emax Group 2006 Consolidation exclusions

CL-Emax Group

in PLN 000’s

according to Emax Group accounting principles

adjustments for

variations in accounting principles

according to CL Group

accounting

principles

the share of ComputerLand in Emax

in Q4 reached

37%

Net revenues

772 275

444 788 (4

537) 440

251 (10 701) 1 201 825

Operating profit/loss

15 076 16 426 (4

262)12 164 (88) 27 152

Net / loss profit

2 640 5 476 28 5 504 (4 439) 3 705

Employees 2 244 981 3 225

7

8

Sygnity snapshot – key references, sales structure

Key references:• Banking:

– National Bank of Poland– BPH BANK (HVB - UniCredito)– BZ WBK (AIB)– Kredyt Bank (KBC)– PKO BP SA– GE Money Bank SA– Raiffeisen Bank

• Power sector, industry and trade:– ENEA– Vattenfall– Polish Power Grid– KGHM SA– Panopa Logistic

• Telecom:– TP SA (FT)

• Healthcare:– NFZ (National Health Fund)

• Public sector:– Ministry of Labour, Ministry of Justice– Łódź City Administration– Uniform services (police, border guards)– Ministry of Education, Ministry of Finance– Police Headquarters– Polish Post

8

Computerland S.A. and Emax S.A. – 2006 proforma sales by sectors

Public sector32%

Telecomu nication

10%

Healthcare3%

General Business (energy, industry, trade)29%

Banking and Finance

26%

9

Reasons to merge

• Two of the largest domestic IT services companies with long histories of complex and successful projects

• Both companies put strong emphasis on sector expertise as a key success factor

• Significantly complementary market offer (in particular in the energy, banking and telecom)

• Both companies develop consulting and outsourcing competencies to complement their system integration services

• Track record of successful mergers and acquisitions (e.g. ComputerLand – Aram, CIE, CSBI, Elba, Polsoft; Emax – Winuel, Max Elektronik)

• Growing importance of foreign sales

• Similar organizational cultures and values: individual responsibility and business flexibility, professionalism and transparent corporate governance

9

10

The Merger History26th of May 2006 Announcement of the merger intention

27th of July 2006 Approval from antitrust regulator

11th of September 2006 ComputerLand reaches 33% of votes in Emax (12,1% in equity)

20th of September 2006 ComputerLand reaches 65% of votes in Emax (36% in equity)

24th of October 2006 ComputerLand reaches 66% of votes in Emax (37% in equity)

21th of November 2006 Announcement of the Plan of Merger

As of January 1, 2007 Implementation of the unified management

Joined organization of Departments of Marketing and Foreign Markets

5th of February 2007 Positive opinion on the Plan of Merger from auditors

February/March 2007 Consultancy with investors with respect to General Shareholders Meeting

14th and 15th of March

General Shareholders Meetings – approval of the merger and the change of the brand of the company

10th of April 2007 Registration of the new brand of the company: Sygnity SA

31st of May 2007 Registration of the desicion of Shareholders about the merger

Share exchange parity: 1 share of Emax S.A. = 1,2 share of ComputerLand S.A.

10

11

Sygnity strategy

• Sector focus accompanied by extensive industry knowledge and expertise

• Long-term client relationship based on the delivery of full scope of services – from consultancy through implementation to outsourcing

• Focus on in-house software solutions complemented by universal packages from major global players

• Revenue growth and development of services supported by mergers and acquisitions

• Marketing of tried-and-tested solutions and experience abroad

• Achieving 8% operating margin in 2008

• Maintenance of highest level of Corporate Governance

11

12

Strategy realised in particular sectors (values in PLN mln)

Banking

25%

25% 10%

Public Sector

Telecoms

Industry/Utilities

33%

300M+

400M+

120M+

300M+

– Strong client base in Poland

– Know-how in centralised systems

– Extensive product offer– Foreign sales – EU and

Eastern markets

– Sales to the FT group (KSP. NPT, Convergence)

– Growing revenues from mobile operators

– Outsourcing references

– Unquestioned leader in the power market

– Outsourcing for industry– Regional sales– ERP expertise– Growth in the

petrochemical sector

– Solutions implemented in many central institutions

– Strong position in local government

– Projects co-funded from EU funds

12

13

Achievement of operating profitability of 8%+ in 2008

by:•Maintaining revenues at stable level•Reaching a bigger share of own solutions in sales structure•Maintaining the speed of restructuring processes

Clear management goals

13

14

Market position: Banking & finance• Market drivers

– Major sources of demand: introduction of new banking products, Basel II, cost cutting

– Changes in banking law are opening the market to outsourcing initiatives

– Integration of new banking groups– New mobile technologies in banking

• Company expertise– Strong relationship with iFlex solutions, a

worldwide leader in banking software– Development of new in-house products

(MIS, ERP, Security)– Acquisition of Support, creating the basis

for offering insurance services– Partnership with SunGard Trading and

Risk Systems– Complete offer and service – dedicated

solutions eg. banking automation, security systems, loan processing systems

• Top market players– Sygnity Group– Asseco Poland

1 Market data - DiS Report 20062 Company Data without consolidation exclusions

Polish B&F IT market 2006E (PLN bln)1

2,25

14

EMAX and ComputerLand position on the Polish B&F IT market 2006 (PLN m)2

57,5

260,3

317,814,2%

2,6%

11,6%

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

EMAX ComputerLand Post mergercompany

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

Sales to the sector Market share

15

Market position: Telecoms• Market drivers

– New Generation Network (NGN, DVB)– Strong competition – the fight for new

customers

• Company expertise– Group of specialized products created on

the basis of line inventory systems, a source of stable revenues (OSS.CL)

– Partnership with Atos Origin enables CL to participate in the Oracle Financials project for TP SA and France Telecom (FT)

– Dedicated solutions implemented in TP SA (eg. mass mailing)

• Top market players– Prokom Software Group– Oracle Polska– Sygnity Group

Polish Telecom IT market 2006E (PLN bln)1

1,88

1 Market data - DiS Report 20062 Company Data without consolidation exclusions

15

EMAX and ComputerLand position on the Polish Telecom IT market 2006 (PLN mln)2

21,4

94,5

115,9

1,1%

5,3%

6,4%

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

EMAX ComputerLand Post mergercompany

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

Sales to the sector Market share

16

Market position: Utilities• Market drivers

– Deregulation, consolidation and privatization in the power electricity and gas distribution

• Company expertise– New version of in-house multimedia billing

system– Successful implementation of a Network

Inventory System (GIS) at GZE (Vattenfall)– Dedicated own solutions to power energy

trading and metering (central system for PSE – Power Energy Grid)

– Other dedicated systems– Building position on the foreign power

industry markets by offering own, proved products eg. contract with Stredoslovenska Energetika a.s. (Slovakia)

– Own ERP systems and integration of other producers’ ERP systems (SAP)

• Top market players– Sygnity Group

Polish Utilities IT market 2006E (PLN bln)1

1,27

1 Market data - DiS Report 20062 Company Data without consolidation exclusions

16

EMAX and ComputerLand position on the Polish utilities/energy IT market 2006 (PLN mln)2

177,8 178,3

356,1

28%

14%14%

-20,0

30,0

80,0

130,0

180,0

230,0

280,0

330,0

380,0

EMAX ComputerLand Post mergercompany

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

Sales to the sector Market share

17

Market position: Public• Market drivers

– Forthcoming projects financed from Schengen Funds – Border Protection (SIS II), Police, Ministry of Justice

– Continued EU funding for Poland– The development of the information society in

Poland • Company expertise

– SYRIUSZ Project – welfare support system for Ministry of Labour

– Command systems and new-generation technology for military, fire depts. and police

– e-Łódź - city administration– Space planning support systems– Local government integrated backoffice system– Complex solutions for public transport enterprises:

passenger information systems and ticket systems – e-ticket

– Smart card applications (electronic city card, electronic purse)

– Command & Control and other systems for uniform services

– Systems for document processing and workflow– Implementation of SAP in large cities (Warsaw,

Wroclaw) • Top market players

– Prokom Software Group– Sygnity Group

Polish Public IT market 2006E (PLN bln)1

3,01

1 Market data - DiS Report 20062 Company Data without consolidation exclusions

17

EMAX and ComputerLand position on the Polish public IT market 2006 (PLN mln)2

185,1207,9

39313,0%

6,9%6,1%

0,0

250,0

500,0

EMAX ComputerLand Post mergercompany

-1,0%

1,0%

3,0%

5,0%

7,0%

9,0%

11,0%

13,0%

15,0%

Sales to the sector Market share

18

Market position: Healthcare

• Company expertise – 26% of the medical IT market (NFZ + hospitals)– 100 specialists dedicated to healthcare IT

solutions– In-house built InfoMedica.CL modular software

implemented in 300 hospitals– Reference: START project (registration system)

in the Silesian Region (over PLN 20 mln) servicing 5 million patients

• Top market players– Sygnity– Spin– Kamsoft

18

• Market drivers– Annual sector IT spending ca. PLN 120 m with high growth potential– Limited competition: Spin (Prokom subsidiary), Kamsoft, Alma.– Prospective RUM (national medical service registration) system worth PLN 500-

800 mln

19

Key areas of synergies

Revenues synergies:• Intensification of sales,

and in particular exploitation of the strong position of the merged companies in selected sectors

• Application of their best experiences and practices

• Elimination of mutual competition

• Optimisation of revenue structure – among other things from expansion of the range of products and services

Cost synergies:• Rationalisation of the range of

own products offered

• Centralisation of software production

• Optimisation of service and help desk operations

• Optimisation of back office operations

• Optimisation of the holding group’s structure

19

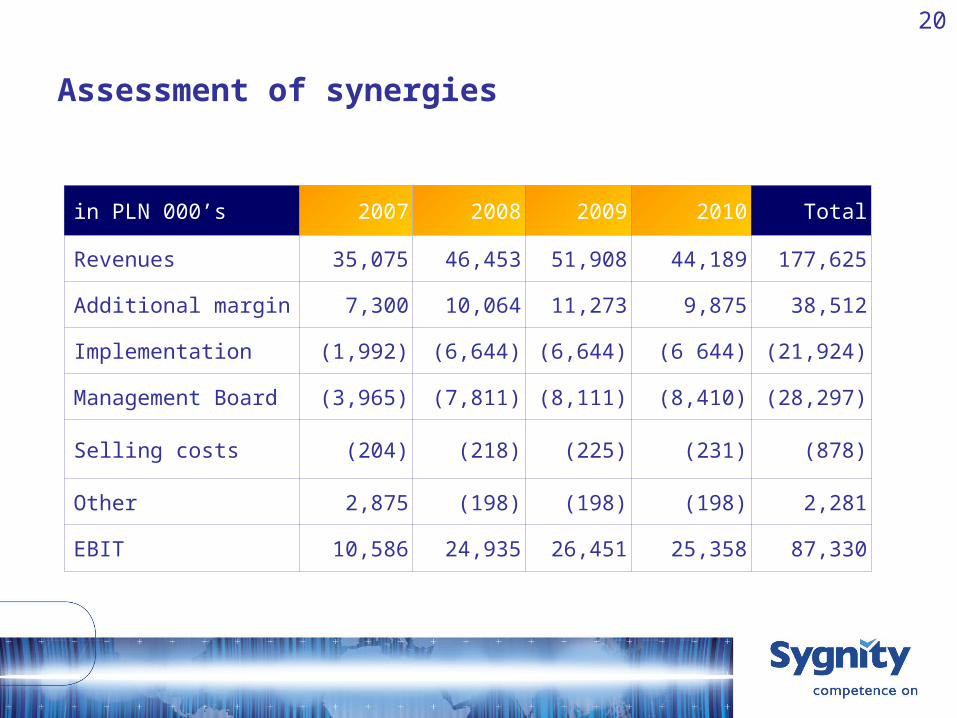

20

Assessment of synergies

in PLN 000’s 2007 2008 2009 2010 Total

Revenues 35,075 46,453 51,908 44,189 177,625

Additional margin 7,300 10,064 11,273 9,875 38,512

Implementation (1,992) (6,644) (6,644) (6 644) (21,924)

Management Board (3,965) (7,811) (8,111) (8,410) (28,297)

Selling costs (204) (218) (225) (231) (878)

Other 2,875 (198) (198) (198) 2,281

EBIT 10,586 24,935 26,451 25,358 87,330

20

21

Merger benefits

• For shareholders:– Improving the general strategic position of the Company by increasing its

critical mass and scope of activities– Strengthening the Company’s market position in certain sectors through

cross-selling – Continued improvement of the Company’s operating efficiency and the

achievement of specific cost synergies– Increased investment attractiveness of the merged Company

• For clients:– A wider range of services and products as well as increased levels of team

competence– The Company's increased creditworthiness and ability to execute large and

complex projects (including outsourcing projects)

• For employees:– Numerous large and interesting projects offer new possibilities for

professional development and careers– Achievement of a bigger market share and strategic position increases the

Company's attractiveness as an employer

21

22

Sygnity consolidated results for Q1 2007 (in PLN mln)

22

Q1 2007

THE SYGNITY GROUP EXCLUDING THE RESULTS OF THE EMAX GROUP

THE EMAX GROUP

CONSOLIDATEDEXCLUSIONS/ MORTISATION ADJUSTMENT

THE CONSOLIDATED SYGNITY GROUP

NET REVENUE 183,166 84,456 (1,320) 266,302

OPERATING PROFIT (LOSS) (9,986) (8,032) (3,106) (21,124)

NET PROFIT (LOSS) (10,732) (11,504) (2,516) (24,752)

NET PROFIT (LOSS) OF MINORITY SHAREHOLDERS

(4) (435) (6,902) (7,341)

NET PROFIT OFSHAREHOLDERS IN THE DOMINANT COMPANY

(10,728) (11,069) 4,386 (17,411)

23

Q1 2007 results - commentary• Q1 – traditionally the slowest period

of the year in IT business on the Polish market

• Stagnation on the public tenders market

• No earnings from the projects completed in 2006 (new projects has not been started yet)

• Further development of own products and costs related with the process

• The postponement of the implementation of projects in the banking, telecommunications and utilities sectors

• Additional cost of PLN 3 million in the first quarter associated with the rebranding and integration processes

23

THE COSTS REDUCTION IN Q1 BY MORE THAN PLN 3 MILLION COMPARED TO THE FIRST QUARTER OF 2006 (EXCLUDING THESE ONE-OFF EVENTS) AND BY ALMOST PLN 6 MILLION COMPARED TO AVERAGE QUARTERLY COSTS FOR LAST YEAR.

THE COSTS REDUCTION IN Q1 BY MORE THAN PLN 3 MILLION COMPARED TO THE FIRST QUARTER OF 2006 (EXCLUDING THESE ONE-OFF EVENTS) AND BY ALMOST PLN 6 MILLION COMPARED TO AVERAGE QUARTERLY COSTS FOR LAST YEAR.

24

Q1 – a period of intensive transformation

• Consent of the shareholders to the merger with Emax (14 and 15 of March)

• Implementation of the Group’s Organisational Model – ca. 100 Top Managers has their precisely defined positions.

• Commencement of the consolidation of the Group • Commencement of a product strategy review • Efects of the CoLorado project

24

25

Effects of CoLorado project in 2006 and Q1 2007

• Project - based organizational structure– Change into project – based structure (8 domains and projects bureau instead of 22

competences centers); new assignments for production and implementation employees, efficiency measures, pilot implementation of new incentive system

• Concentration of clients– Reduction of # of active accounts from 700 to 200 and reduction of selling

costs from PLN 52,5 mln in 2005 to PLN 42,3 mln in 2006, Offering Commitees

• Centralization of purchases – # of suppliers down from 1000 do 200, centralization, monitoring and

comprehensive policy of purchases

• Productivity– increase of efficiency and repeatability of projects planning, policy of

testing projects, optimization

Total 2006 savings due to implementation of CoLorado project

reached PLN 12.5 mln in 2006 and PLN 4.1 mln in Q1 2007

Total 2006 savings due to implementation of CoLorado project

reached PLN 12.5 mln in 2006 and PLN 4.1 mln in Q1 2007

25

Attachement – new name and logo

26

27

Reasons to change the name

Introducing new name

MERGERMERGER

REPOSITIONNINGREPOSITIONNING

FOREIGN MARKETSFOREIGN MARKETS

COMPLETED PROJECT OF EXPORT BRAND

COMPLETED PROJECT OF EXPORT BRAND

Introduce new name when

deciding upon merger

CURRENT SITUATION - REASONS

OPTIMAL SCENARIOCHALLENGE

27

28

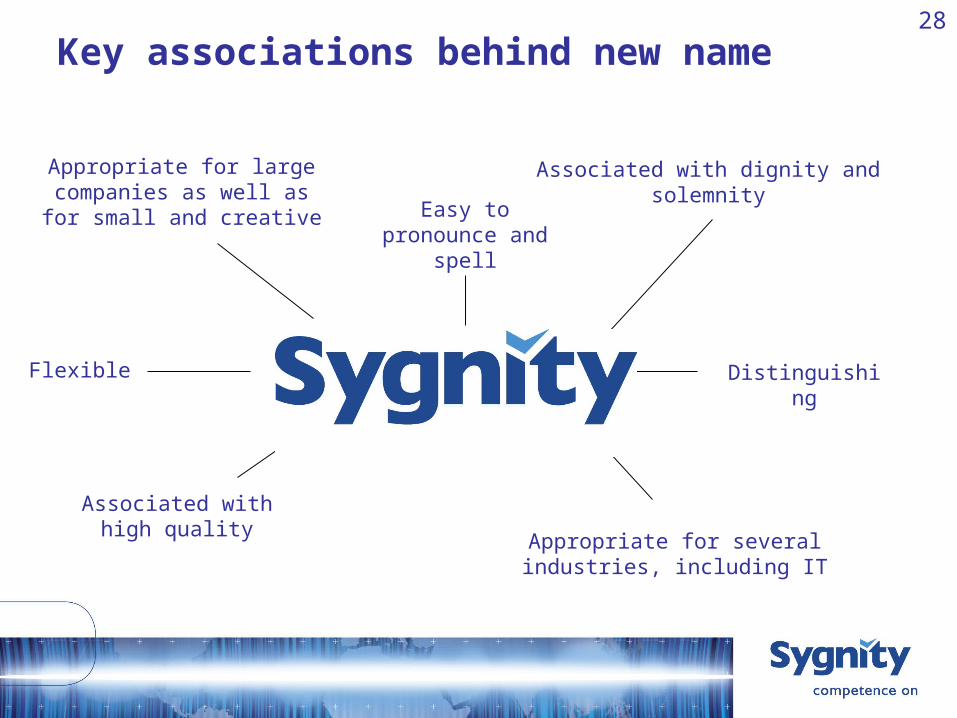

Key associations behind new name

Flexible

Easy to pronounce and spell

Appropriate for large companies as well as for

small and creative

Associated with dignity and solemnity

Appropriate for several industries, including IT

Associated with high quality

Distinguishing

28

29

29

Positioning theme: Competence on

The meaning: Efficient completion of projects thanks to full understanding of the customer’s needs

Thank you