Embed Size (px)

Citation preview

COMPARATIVE COSTS OF IA SYSTEMS

by

Estelle Jamesprepared for delivery at World Bank Institute Pension Reform Seminar,

Budapest, 2001

Comparative costs of IA systems

• Prefunding desirable--financial sustainability and long term saving

• Danger of political manipulation and low returns to publicly managed funds

• But decentralized individual accounts (IA’s) may have high administrative costs

• What is the most cost-effective way to organize IA systems?

– Key choice: retail or institutional market?

We compare:1) IA’s in retail market

• Direct relation between individual & fund

• Open entry, free choice, unrestricted fee

• Retail funds incur high marketing costs

• Administrative costs are 15-30% of new contributions, equivalent to .75-1.5% of assets per year for lifetime worker

• Examples: Latin America, Poland, Hungary, Kazakhstan, UK, US mutual funds

2) IA’s in institutional market• Intermediary aggregates IA contributions; main

competition is for market access: – competitive bidding over fees narrows eligible

pension funds to small number – winners compete for workers’ money but are likely to

get large money blocs

• Best if R&C and investment are separated • Costs are half as much as in retail market <

10% of new contributions, < .5% of assets, even less with passive investing

• Bolivia, industry funds in Australia, US TSP, US pension funds, Sweden

We found: Large cost saving possible in institutional market

• Scale economies: Less excess capacity, especially at start-up and in small countries

• Save on marketing expenses

• More bargaining power, less oligopoly profit

• Change product mix: Investment choices constrained to low cost strategies (passive)

• If institutional market isn’t used market will eventually concentrate industry--but start-up and marketing costs, therefore fees, higher

• But many caveats--will be discussed at end

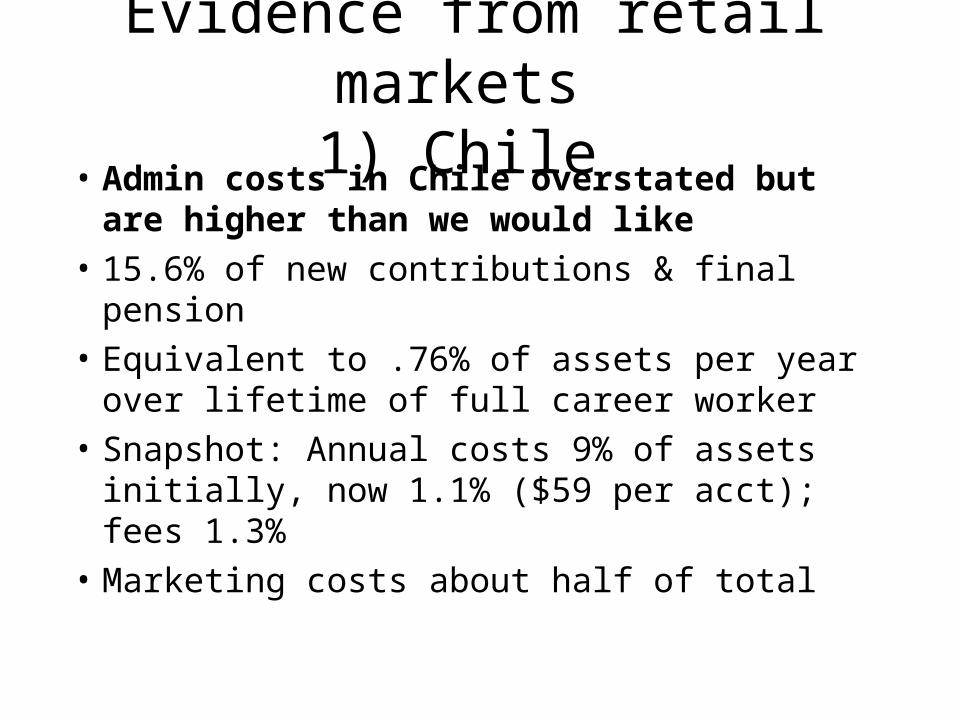

Evidence from retail markets 1) Chile

• Admin costs in Chile overstated but are higher than we would like

• 15.6% of new contributions & final pension

• Equivalent to .76% of assets per year over lifetime of full career worker

• Snapshot: Annual costs 9% of assets initially, now 1.1% ($59 per acct); fees 1.3%

• Marketing costs about half of total

Costs of Chilean AFP System, 1982-1998

Relation Between Fee as % of Assets andAverage Account Size

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6

Assets per Affiliate (1998 thousands US$)

Fee

per

Uni

t of A

sset

s (%

)

Economies of scale• My analysis shows scale economies continue

until 3 million affiliates, $15 billion per AFP--half total industry in Chile

• Concentration is being achieved through market (previously 20, now 7-8 AFP’s)

• Will probably fall to 5 AFP’s--scale economies but marketing costs continue

• Institutional approach would get us there faster, and with lower equilibrium costs, but raises other problems

2) Latin America

• Cost and fee is 15-25% of contributions

• Per unit of assets 4-9% ($21-98 per acct)

• Scale: Costs lower for larger AFP’s

• Expenses smaller in Bolivia (institutional approach) and Chile (size, experience, concentration)

C osts o f L atin A m erican A F P S ystem s, 1998

R ela tion B etw een C ost as % of A sse ts an dA verage A ccou n t S ize

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6

Assets per Aff ilia te (U S $ 000 's )

Expe

nses

per

Uni

t of A

sset

s (%

)

C hile

B o livia

M e xico

3) U.S. Mutual funds

• Many years of operation, very large, service

• Costs & fees more dispersed but similar to Chile: average = 1.4% of assets

• Costs are lower for: larger funds, no-loads (no commissions), passive investments

• Marketing expenses about 50% of total cost

• Higher costs don’t lead to higher returns

U.S. Mutual Fund Costs, 1997

As % of Assets

Actively Managed Passively Managed

Asset Management 0.64 0.11

Marketing 0.65 0.03

R&C Costs 0.12 0.05

Other 0.08 0.13

Total 1.50 0.32

In $’s per Account

Actively Managed Passively Managed

Asset Management 160 28

Marketing 163 8

R&C Costs 30 13

Other 20 33

Total 375 80

Institutional market--1) U.S.• Large investors pay .04-.08% of assets for

passive mgt, .35-.65% for active mgt. + .1-.15% for other expenses. Half retail costs, lower for large institutions.

• Reasons for lower fees:– Large money blocs--scale economies– Low marketing costs– Low R&C costs– Heavy use of passive investment– Better information, bargaining power

Long Run Costs of Retail and

Institutional Markets in US

(in basis points)

Retail 1 Institutional 2

Passive Active Passive Active

Asset management 3 11 64 4-8 35-65

Marketing 3 65 1 5

R & C 5 12 9 9

Other 13 8 6 6

Total cost 32 150 14 – 18 49 - 79

$ cost per $25,000 account 80 375 35 - 45 122 - 197

1. Average for mutual fund2. Range for institutional investors3. Includes brokerage fees for trading

2) Bolivia

• International bidding process, 2 winners, no switching (greater entry & switching later)

• Fee structure: 5% contributions+.43% assets

• Equivalent to: .56% for full career worker

• Snapshot today: 3% of assets, $16 per account

• Much cheaper than Chile at start-up

Bolivia: caveats

• Is saving due to competitive bidding & no marketing or to lumping IA’s with large privatization assets & cross-subsidization?

• Potential problems: service, performance incentives, regulation, unexpected contingencies, rebidding problems

3) U.S. thrift savings plan

• Voluntary IA plan for federal government employees with matching contributions

• Competitive bidding with 3 portfolios, all passive management, 1 company

• Costs: .11% of assets or $30 per account

• Is saving due to competitive bidding, limited choice (index funds) or hidden costs?

Cost of U.S. Thrift Savings Plan, 1988-1998

Relation Between Cost as % of Assets andAverage Account Size

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0 5 10 15 20 25 30

Assets per Account (in thousands U.S. $'s)

Exp

ense

Rat

io a

s %

of A

sset

s

4) Sweden

• Centralized R&C: 2.5% IA contributions go to public agency, then reallocated (blind) to mutual funds selected by workers

• Mutual funds must accept agency’s fees--sliding scale, depending on funds attracted

• Estimated expected fee=.8% (.5% in lg run)

– lower than Chilean AFP’s, US or Swedish mutual funds because less marketing

– higher than TSP because greater choice

What does the evidence tell us?• Economies of scale: Cost per account falls as #

affiliates grow, cost per asset unit falls as assets grow; industry consolidates. This happens in retail and institutional markets

• Institutional costs lower than retail--competitive bidding limits number of funds, gains from scale economies early, low marketing costs, constrain choice to low cost products, bargaining power

• Costs <.5% of assets annually; would reduce pensions<10%, half as much as retail market, even less with passive investing

Average Annual Fees as % of Assets for Alternative IA Systems

Retail Institutional

Latin America Chile Bolivia – Competitive Bidding

Start up 9.39 3.00Current 1.36 3.00Lifetime simulation 0.76 0.54

Sweden Mutual Funds IA Systems – Price Ceilings

Current 1.50 0.80Long run - 0.50

United States Mutual Funds Hypothetical IA Systems

Active 1.50 0.64Passive 0.32 0.16

TSP - Competitive bidding, passive

0.11

Trade-offs and caveats• May choose wrong number of funds

• Performance incentives hard to specify

• Slow to innovate, adapt to new conditions

• Difficult to handle unforeseen contingencies

• Possible corruption, collusion, regulatory capture

• Credible rebidding strategy needed with fixed costs staying in system; or first entrants have long run monopolistic advantage

• But low cost IA system is feasible; especially useful at start-up and for small countries or contribution base

What is the relevance to ECA/FSU?

• As you choose your new systems, don’t automatically choose the retail model just because many other countries have done so

• Reforming countries, especially small countries, should consider pros and cons of the institutional approach, to attract foreign expertise and cut administrative costs