Embed Size (px)

Citation preview

Competition in Telecom Competition in Telecom Market for Voice TelephonyMarket for Voice Telephony

Note: The views expressed in this presentation are those of the author and do not necessarily reflect the opinions of the ITU or its membership.

Saburo TANAKACouncellor,

Seminar on Economic and Market Analysis for CEEC and Baltic States

Prague, 9 – 11 September 2003

2Competition in Voice TelephonyCompetition in Voice Telephony

AgendaAgenda

l Status of competitionð Competition in Voice Telephonyð How traffic flow in the competitive market

l Role of Regulatorsl Importance of Interconnectionð Regulatory and technical issuesð Economic issues

l Importance of tariff rebalancing

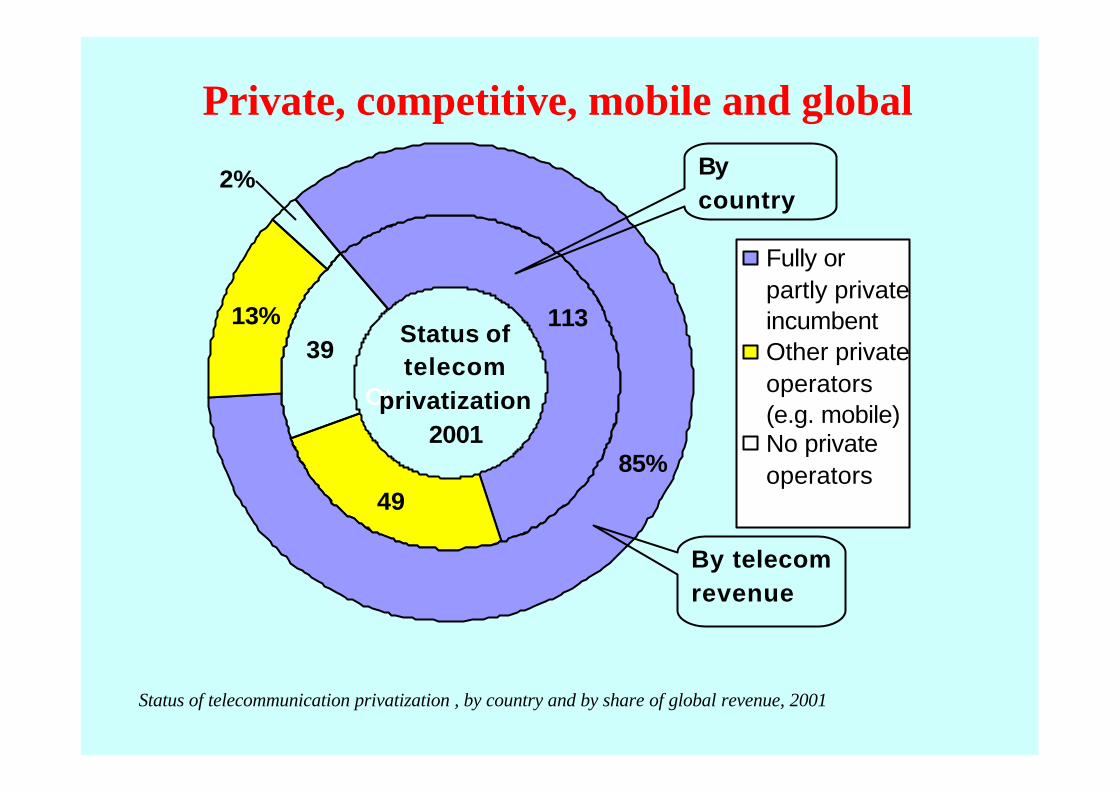

85%

13% 113

49

39

2%

Fully orpartly privateincumbentOther privateoperators(e.g. mobile)No privateoperators

Oth

By telecom revenue

By country

Status oftelecom

privatization2001

Private, competitive, mobile and global

Status of telecommunication privatization , by country and by share of global revenue, 2001

Percentage of countries with competition Percentage of countries with competition for selected services, 2001for selected services, 2001

0

10

20

30

40

50

60

70

80

90

100

Basic services Leased lines Wireless localloop

Cellular Cable TV VSAT ISPs

In %

Monopoly Competition

Source: ITU World Telecommunication Regulatory Database, 2001

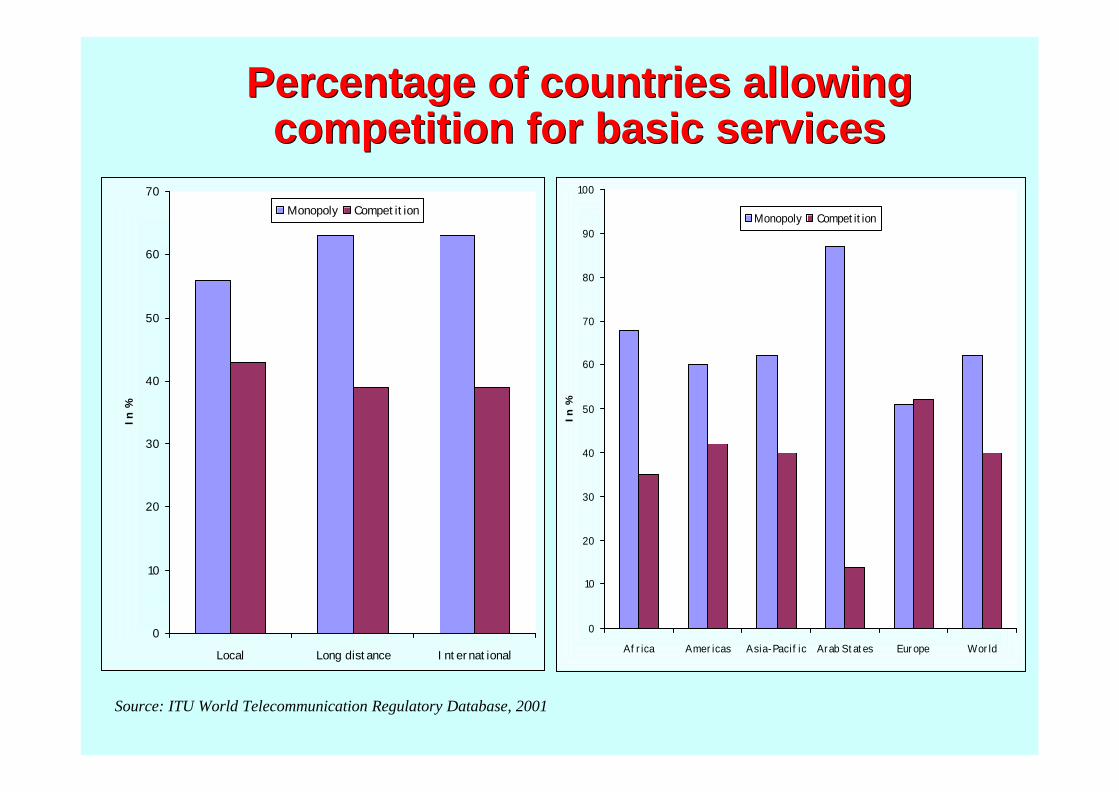

Percentage of countries allowing Percentage of countries allowing competition for basic servicescompetition for basic services

0

10

20

30

40

50

60

70

Local Long distance International

In %

Monopoly Competition

0

10

20

30

40

50

60

70

80

90

100

Africa Americas Asia-Pacific Arab States Europe World

In %

Monopoly Competition

Source: ITU World Telecommunication Regulatory Database, 2001

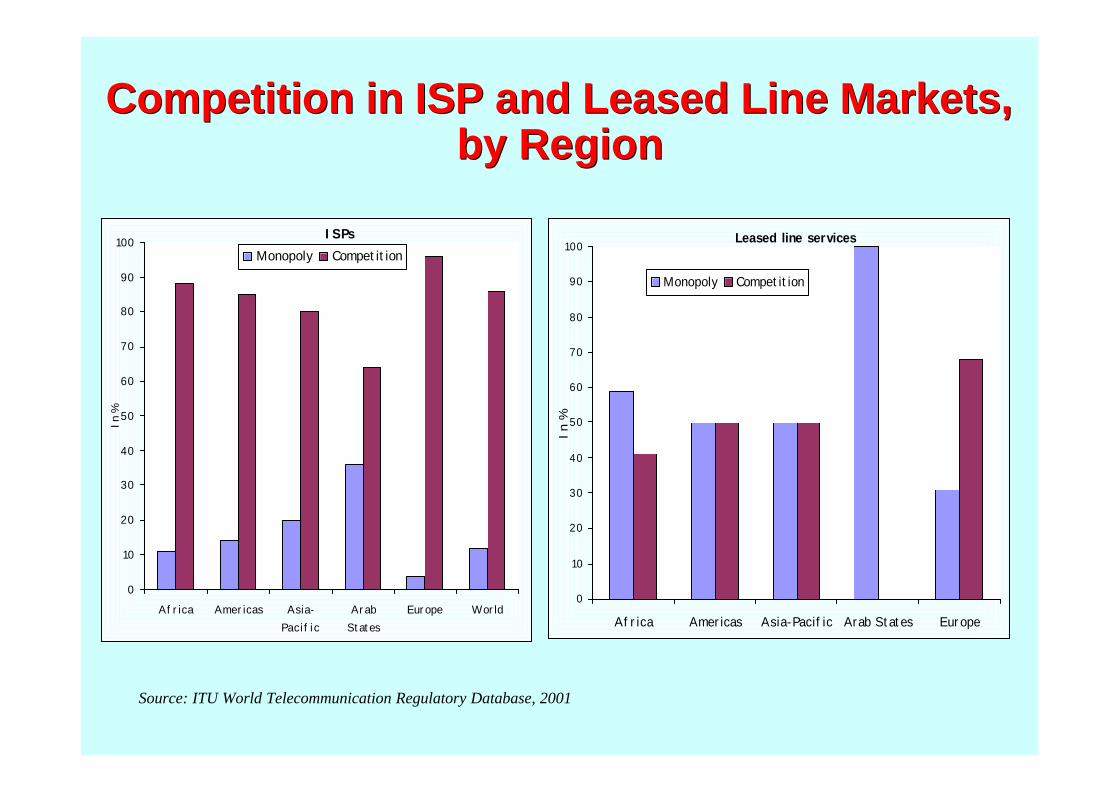

Competition in ISP and Leased Line Markets, Competition in ISP and Leased Line Markets, by Regionby Region

ISPs

0

10

20

30

40

50

60

70

80

90

100

Africa Americas Asia-Pacific

ArabStates

Europe World

In %

Monopoly CompetitionLeased line services

0

10

20

30

40

50

60

70

80

90

100

Africa Americas Asia-Pacific Arab States Europe

In %

Monopoly Competition

Source: ITU World Telecommunication Regulatory Database, 2001

Competition in Mobile Cellular ServicesCompetition in Mobile Cellular Services

Source: ITU World Telecommunication Regulatory Database, 2001

0

10

20

30

40

50

60

70

80

90

100

Africa Americas Asia-Pacific Arab States Europe

In %

Monopoly Competition

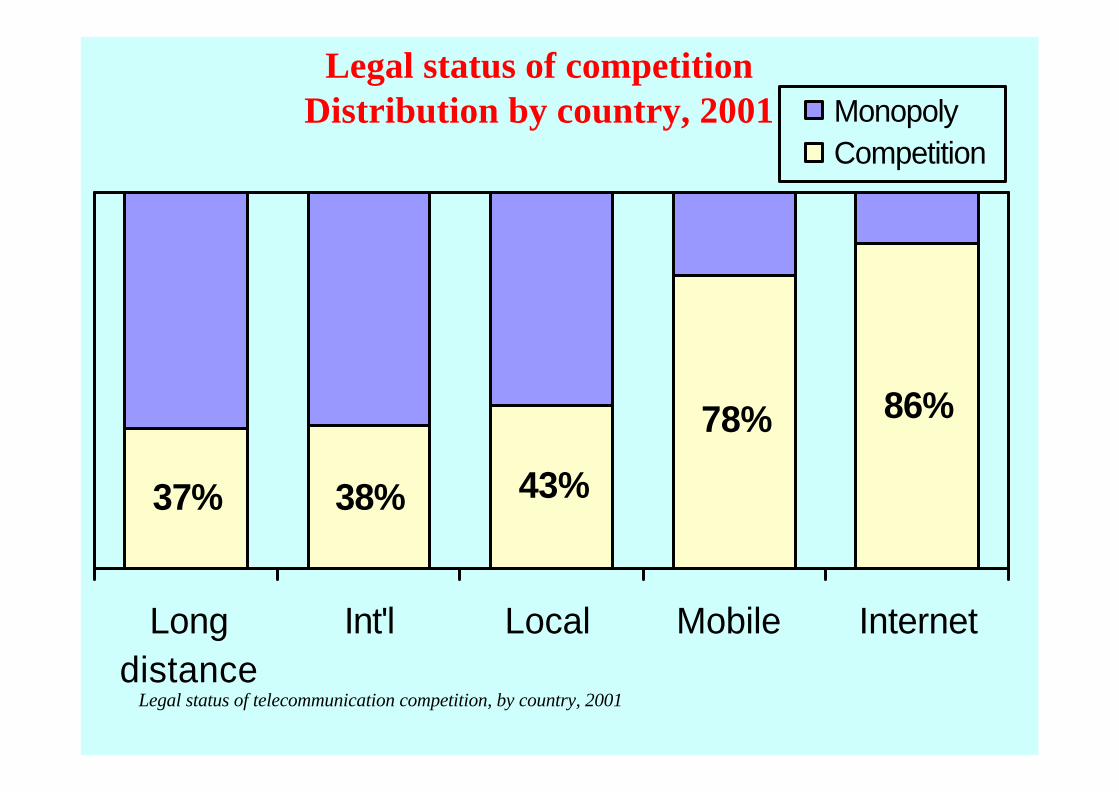

37% 38% 43%

78% 86%

Longdistance

Int'l Local Mobile Internet

MonopolyCompetition

Legal status of telecommunication competition, by country, 2001

Legal status of competitionDistribution by country, 2001

10Competition in Voice TelephonyCompetition in Voice Telephony

0

5

10

15

20

25

1986 1988 1990 1992 1994 1996 1998 2000

1988: Privatization and competition in Chile

1990: Privatization w ith 7-year exclusivity in Argentina

Exclusivity extended by 3 years in Argentina

Teledensity, in Chile and Argentina

Growth in fixed line teledensity, Chile and Argentina, 1986-2000

11Competition in Voice TelephonyCompetition in Voice Telephony

0

10

20

30

40

50

60

70

80

90

1988 1990 1992 1994 1996 1998 2000

Singapore: Mobile

competition delayed until

April 1997

Hongkong SAR: Mobile competition introduced in 1988 for analogue

Additional competition introduced w ith digital mobile in 1993

Six additional PCS licences awarded in 1996

Mobile penetration rate, per 100 inhabitants

Growth in mobile teledensity, Hong Kong SAR and Singapore, 1988-2000

Teledensity with rising rank

Country 2000 1990Rank 2000

Rank 1990 Change

China 17.8 0.6 95 159 64

V iet Nam 4.2 0.1 141 189 48

Botsw ana 21.6 2.1 91 129 38

El Salvador 21.8 2.4 90 125 35

Jamaica 34.1 4.5 71 106 35

Hungary 67.4 9.6 43 78 35

Mauritius 38.6 5.4 67 100 33

Chile 44.4 6.7 61 93 32

Philippines 12.4 1.0 112 143 31

Morocco 13.3 1.6 107 136 29

Paraguay 20.7 2.7 92 120 28

Cambodia 1.2 0.0 167 194 27

Cape Verde 17.2 2.4 98 125 27

Taiw an, China 137.0 31.4 5 31 26

Poland 45.6 8.6 60 85 25

Teledensity with falling rank

Country 2000 1990Rank 2000

Rank 1990 Change

Armenia 15.6 15.7 102 60 -42

Iraq 2.9 3.9 149 109 -40

Tajikistan 3.6 4.5 143 105 -38

Uzbekistan 6.9 6.9 128 92 -36

Kyrgyzstan 7.9 7.2 125 90 -35

Angola 0.7 0.8 177 146 -31

Liberia 0.2 0.4 190 162 -28

DPR Korea 4.6 3.8 138 111 -27

Canada 96.1 58.6 33 6 -27

Turkmenistan 8.4 6.0 123 97 -26

Cuba 4.4 3.1 140 115 -25

Moldova 16.5 10.6 99 74 -25

Kazakhstan 12.5 8.0 111 87 -24

Comoros 1.0 0.8 171 149 -22

Ukraine 22.7 13.6 87 66 -21

X X

Traditional regime:Traditional regime:Joint provision of serviceJoint provision of service

Country A Country B

14

X

Emerging regime:Emerging regime:Market entry and interconnectionMarket entry and interconnection

XXCountry A Country B

Jointly provided circuit

Circuit provided by operator B

15

Country A Country B

Operator A Operator BPSTN

IWF

Interconnect

Leased lines

International simple resale (ISR)(By-passing accounting rate)

Once a foreign carrier accepts the benchmark rate, it can negotiate ISR arrangements with US carriers

Country A Country B

Telephone service using data transmission(By-passing accounting rate)

Operator A

PSTN

Voice is packetized = data transmissionTelephone regulations do not apply

VSAT

Inter-connection

É

T 0 2 0 8 5 0 0 - 0 0( 1 0 6 1 4 7 )

I P N e t w o r k

IW F

T e r m i n a t i n gN e t w o r k

L o c a l o r d i s t r i b u t e df u n c t i o n C a l l i n i t i a t e d f r o m P S T N / I S D N / P L M N

t o P S T N / I S D N / P L M N

P S T N / I S D N/ P L M N

IW F

P S T N / I S D N/ P L M N

L o c a l o r d i s t r i b u t e df u n c t i o n

O r i g i n a t i n gN e t w o r k

Call from International Telecommunication Network (ITN) to another ITN via IP-based Network

IP Telephony (by-passing accounting rate)

7Alternative calling proceduresAlternative calling procedures

Country A

Country B Country C4.5 $

3.5$

2.0$

Call-Back

1.2$

0.8$1.0$1.5$

Interconnection of two outgoing calls in country A

Call-Back

Using ARCALL BACK using Accounting Rates

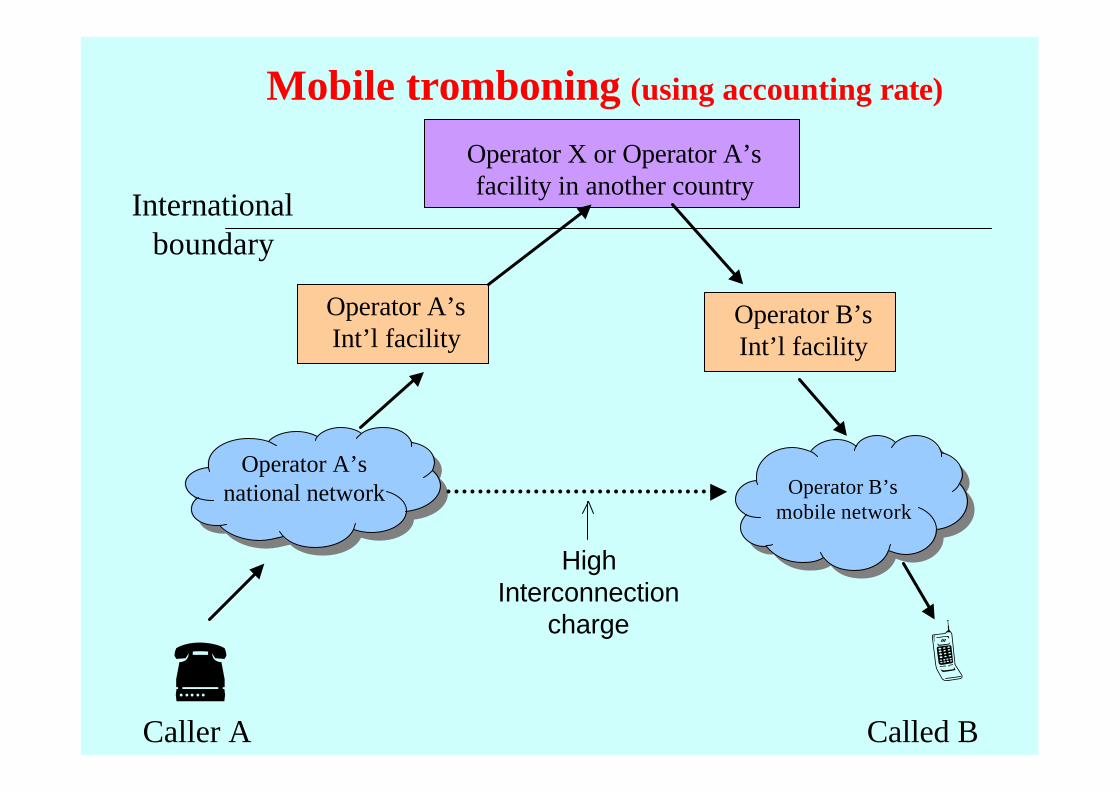

Mobile tromboning (using accounting rate)

É ÈCalled BCaller A

Operator A’s national network Operator B’s

mobile network

Operator A’s Int’l facility

Operator B’s Int’l facility

Operator X or Operator A’s facility in another country

International boundary

High Interconnection

charge

A

C

B

C

B

A

Operator in A sends traffic tooperator in C under anarrangement of exclusivity

• Operator in A is a partnerof operator in C

• Settlement rates A/B > C/B

Origin A

Destination B Origin

C

Destinati

on B

Operator in C declares traffic to B on transit through A

Operator in B receives traffic at settlement rate C/B instead of A/B

Operator in C “re-labels” the traffic as originated in C

1

2

3

4

Refile and other practices using accounting rate system

Calling opportunity in the worldCalling opportunity in the world

89.7%

5.0%5.0% 0.3%

199352.7%

19.9%

19.9%

7.5%

1998

23.4%

25.0%25.0%

26.7%

2003

Fixed-to-fixed

Fixed-to-mobile

Mobile-to-fixed

Mobile-to-mobile

Source: ITU Fixed-Mobile Interconnect website: http://www.itu.int/interconnect

More than 75% of calls involve mobile

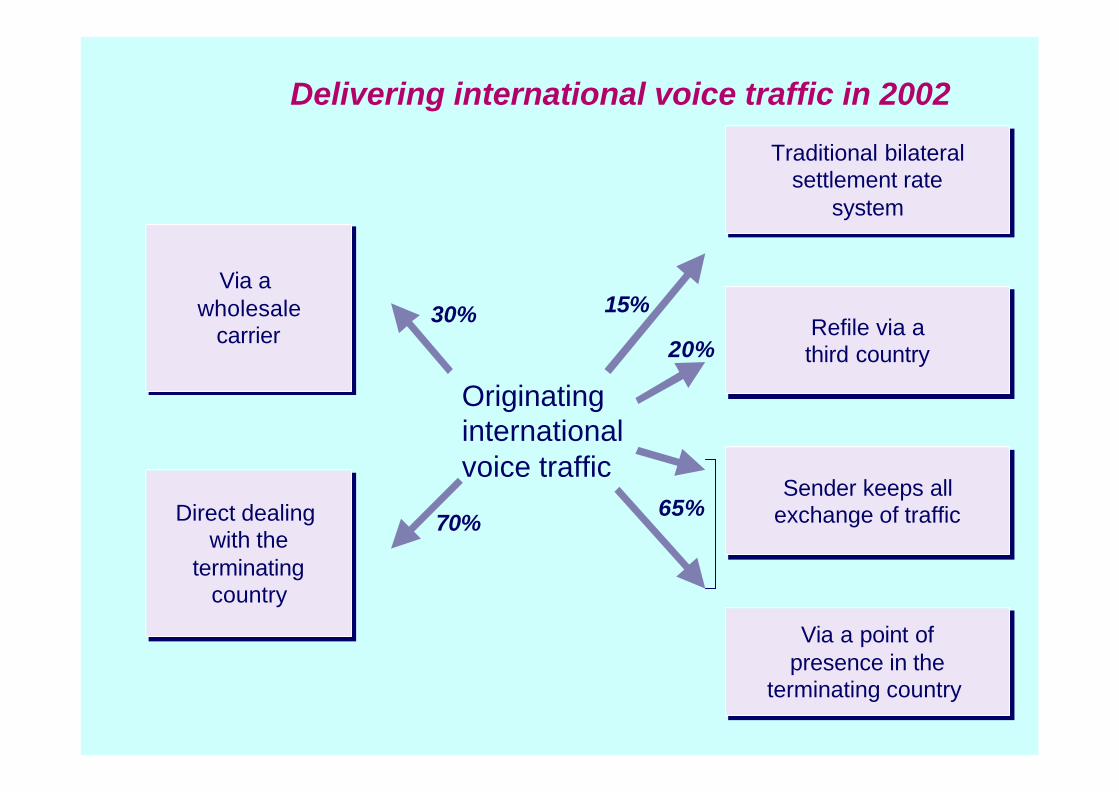

Originating internationalvoice traffic

Traditional bilateralsettlement rate

system

Traditional bilateralsettlement rate

system

Refile via athird countryRefile via athird country

Sender keeps allexchange of trafficSender keeps all

exchange of traffic

Via a point ofpresence in the

terminating country

Via a point ofpresence in the

terminating country

Via a wholesale

carrier

Via a wholesale

carrier

Direct dealing with the

terminatingcountry

Direct dealing with the

terminatingcountry

30%

20%

15%

70%65%

Delivering international voice traffic in 2002

24Competition in Voice TelephonyCompetition in Voice Telephony

So, what’s the problem?So, what’s the problem?l Competition is everywhere but..

ð Incumbents, New-comers and Regulators are not ready

l Accounting rates are the traditional way of sharing revenues from int’l servicesð BUT, creates incentives among recipient countries to

sustain rates at high levelð Accounting rate system not well-adapted to competitive

market environment

l Strong pressure to move towards a cost-oriented systemð BUT, a cost-oriented system would be asymmetricð US want cost-oriented but reject asymmetric charges for

call termination

l How to calculate cost ?ð How interconnection charge should be determined

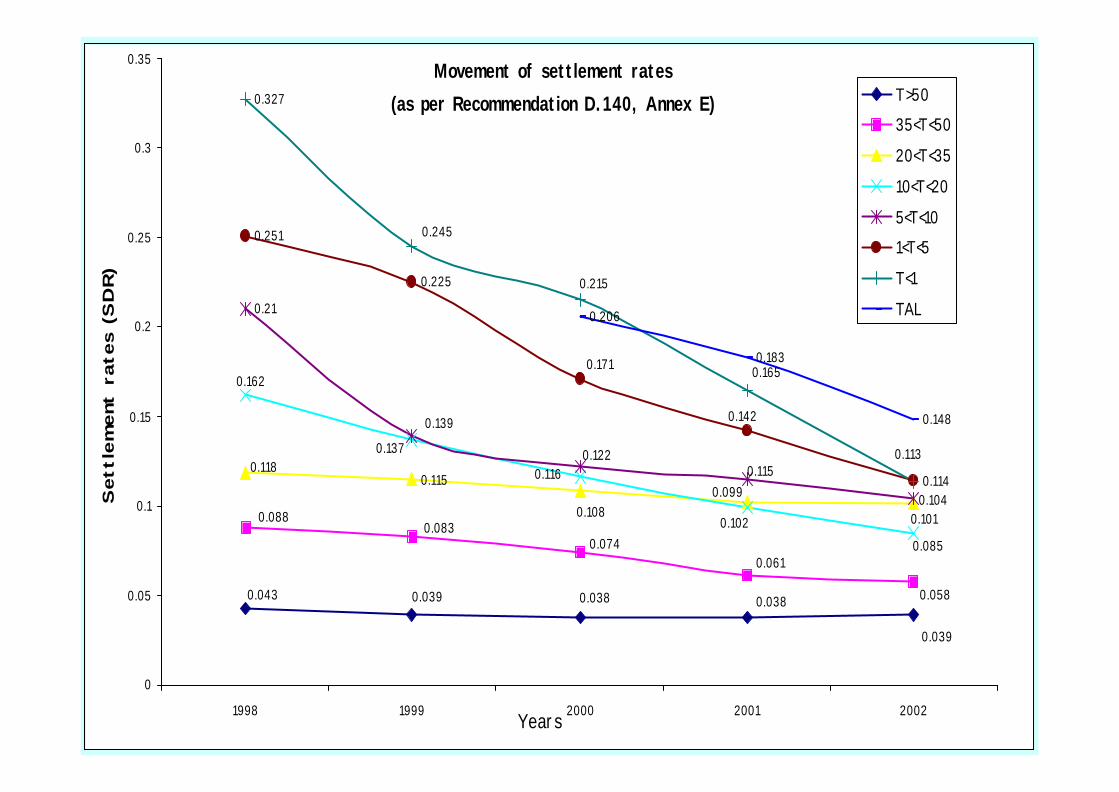

Movement of settlement rates(as per Recommendation D.140, Annex E)

0.115

0.21

0.251

0.225

0.114

0.327

0.206

0.183

0.148

0.039

0.0380.0380.0390.043 0.058

0.0880.083

0.0740.061

0.102 0.1010.108

0.1180.137

0.162

0.085

0.0990.116

0.104

0.1150.122

0.139 0.142

0.171 0.165

0.215

0.245

0.113

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

1998 1999 2000 2001 2002Years

Sett

lement

rate

s (S

DR)

T>5035<T<5020<T<3510<T<205<T<101<T<5T<1TAL

26Competition in Voice TelephonyCompetition in Voice Telephony

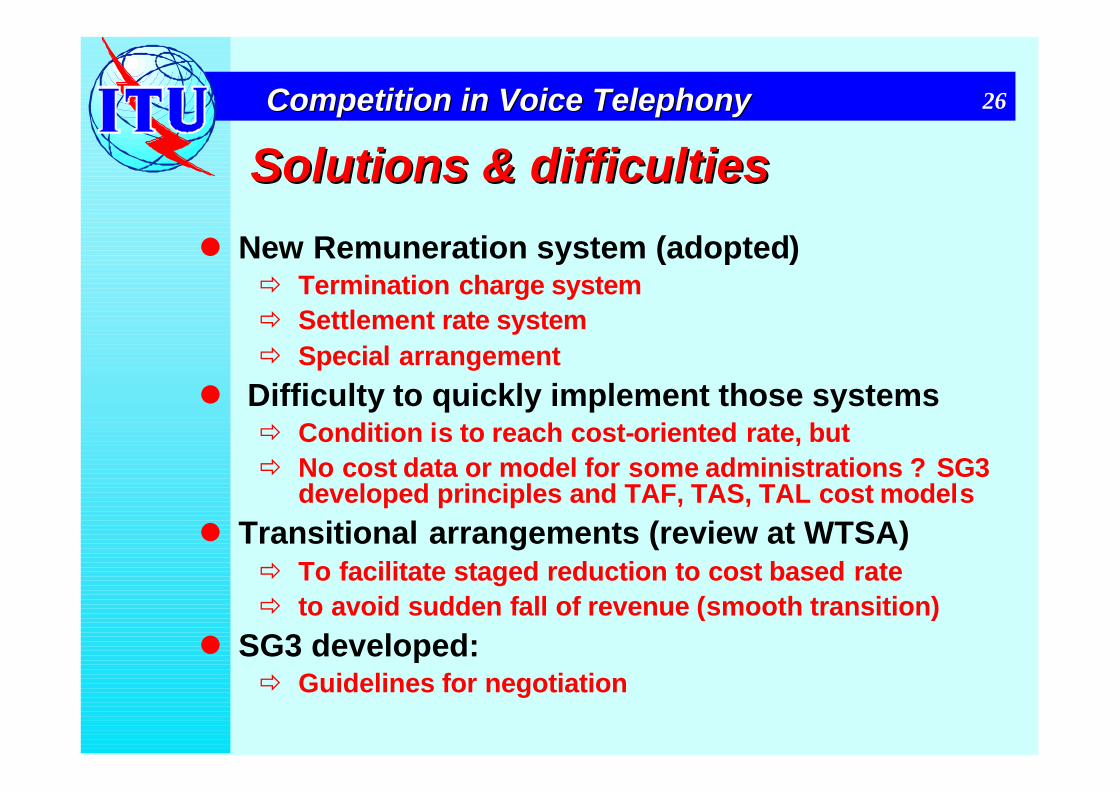

Solutions & difficulties Solutions & difficulties

l New Remuneration system (adopted)ð Termination charge systemð Settlement rate systemð Special arrangement

l Difficulty to quickly implement those systemsð Condition is to reach cost-oriented rate, butð No cost data or model for some administrations ? SG3

developed principles and TAF, TAS, TAL cost models

l Transitional arrangements (review at WTSA)ð To facilitate staged reduction to cost based rateð to avoid sudden fall of revenue (smooth transition)

l SG3 developed: ð Guidelines for negotiation

AnnexAnnex E to E to RecommendationRecommendation D.140 D.140 “indicative “indicative targettarget rates” by rates” by TeledensityTeledensity (T) (T) BandBand, in SDR (, in SDR (andand US cents) US cents) perper minute.minute.

T<1 1<T<5 5<T<10 10<T<20 20<T<35 35<T<50 T>50

0.327 SDR

0.251 SDR

0.210 SDR

0.162 SDR

0.118 SDR

0.088 SDR

0.043 SDR

43.7¢ 33.5¢ 28.0¢ 21.6¢ 15.8¢ 11.8¢ 5.7¢

Low income Lower middle Upper middle

High income

Note: The correspondence between teledensity band and income group shown in the bottom row is intended to be approximate, not precise. Source: ITU-T SG3 Report. 1 SDR = US$1.39.

27

FCC : 23 ¢(January2002/2003)

FCC : 19 ¢(January2001) 19 ¢(J.2000)

FCC : 15 ¢(January1999)

(end 2001) (end 2001) (end 2001) (end 2001)

(

end 2001) (end 2001) (end 2001)

The following non-binding guidelines could be applied when negotiating accounting rates and accounting rates share in the international service:1 Each party should ensure that; i.e., all information to be given to the other party should be credible in order to lead the negotiations into right direction.2 The parties should negotiate freely and make agreements voluntary, any kind of coercion should be avoided.Each party should act constructively, any offer, proposal, action, etc. should be directed towards reaching an agreement. Complex concepts should be simplified as much as possible.4 Each party should act time-saving, any delay should be avoided.5 Regular re-negotiations and future amendments should be possible.6 Until such time as an appropriate dispute settlement arrangement may be approved by the ITU with respect to accounting rates, both parties should have the possibility to consult a person or institution for mediation.

Guidelines to facilitate the negotiation

Addition to Recommendation D.140Addition to Recommendation D.140

1 accountingnrates for international telephone services should be cost-orientated and should take into account relevant cost trends;

2 each Administration should apply the above principle to all relations on a non-discriminatory basis; Accordingly, international calls should not be treated any less favorably than comparable national calls.

Alternative proposal from Vietnam:Accordingly, under normal circumstances (where tariff rebalancing has been effectively achieved) international calls should be treated any less….

The The importance of importance of interconnectioninterconnectionl Key to developing competitive markets

ð Interconnection is the main driver of growth and innovation in telecom market, it promote efficient infrastructure development

ð But constructing a sound interconnection framework is no easy task

l Approaches to Interconnection Policyð National approach – by 2000 101 countries had established

interconnection regulatory frameworkð Regional Approach – European Union (interconnection directive),

CITEL (Guidelines and Practices for Interconnection Regulation), APEC (Recommended Principles for interconnection), TRASA(proposed interconnection guidelines)

l WTO Reference Paper on Regulatory Issuesð Puts forward a series of interconnection commitments:

- provide interconnection at any technically feasible point- non discrimunatory terms, conditions and rates- in a sufficiently unbundled and timely fashion- calls for transparency

Key Interconnection Rules in Key Interconnection Rules in the WTO Reference Paperthe WTO Reference Paper

An independent entity (which may be the regulator) must be available to resolve interconnection dispute within a reasonable time frame

Dispute resolution

Agreements of major suppliers’ model interconnection offers must be made public

Transparency

Procedures for interconnection to major suppliers must be made public

Procedure

- At any technical feasible point in the network- In a timely fashion- At cost orientated rates- On non discriminatory and transparent terms- On an unbundled basis - At non-traditional interconnection points if requester pays charges

Interconnection with “Major Supplies”must be available

32Competition in Voice TelephonyCompetition in Voice Telephony

Regulatory and technical issuesRegulatory and technical issuesl Policy makers must resolve such basic questions as:

ð which carriers are required interconnectionð How the costs will be calculated and recovered, and ð At what points in the PSTN interconnection should occur

l Regulatory issues ð Establishing guidelines in Advance (without it, interconnection

negotiation are frequently protracted, delaying the introductionof competition)

ð Introducing competition require “dominant carriers” to interconnect with other carriers

ð Cost orientation: excessive prices deter market entry, hinder competition, end user suffer and can provide a pool of revenue

l Technical issuesð Points of interconnection: incumbent operators permit inter-

connection with their networks at any technically feasible pointð Dialling Parity and Pre-selection: Call-by-call customer

selection or Operator pre-selection by pre-subscriptionð Quality of Interconnection Service

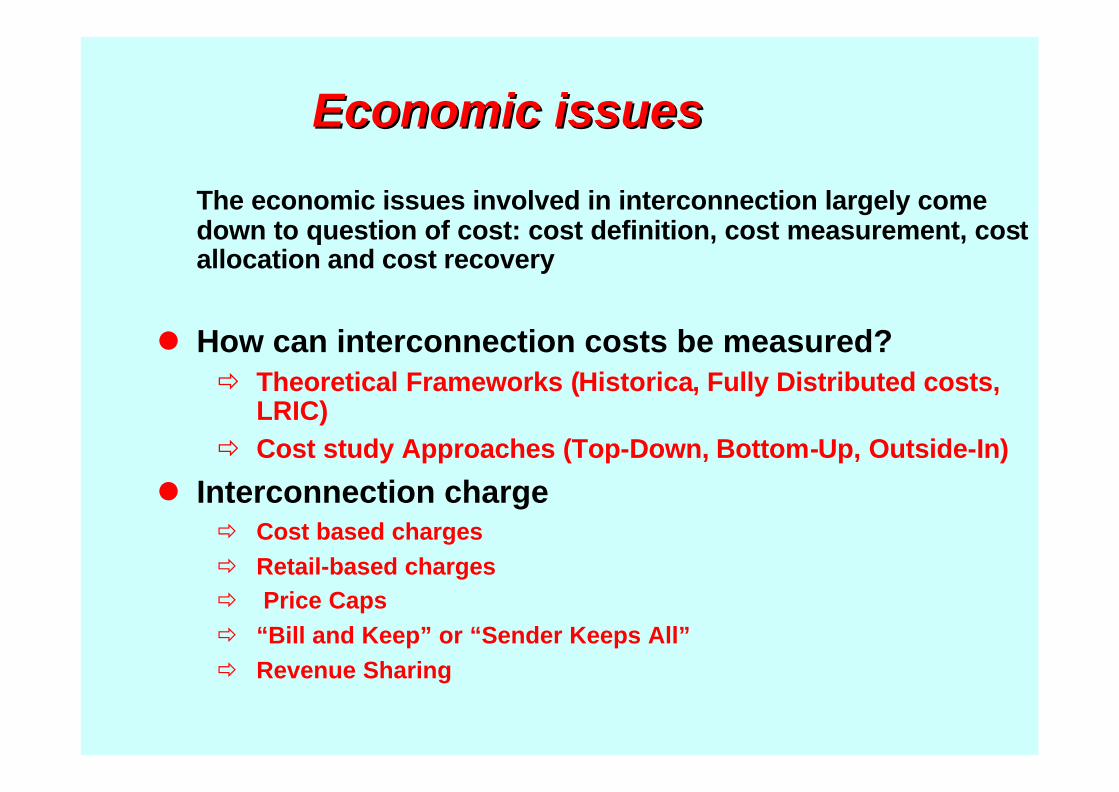

Economic issuesEconomic issues

The economic issues involved in interconnection largely come down to question of cost: cost definition, cost measurement, cost allocation and cost recovery

l How can interconnection costs be measured?ð Theoretical Frameworks (Historica, Fully Distributed costs,

LRIC)ð Cost study Approaches (Top-Down, Bottom-Up, Outside-In)

l Interconnection chargeð Cost based chargesð Retail-based chargesð Price Capsð “Bill and Keep” or “Sender Keeps All”ð Revenue Sharing

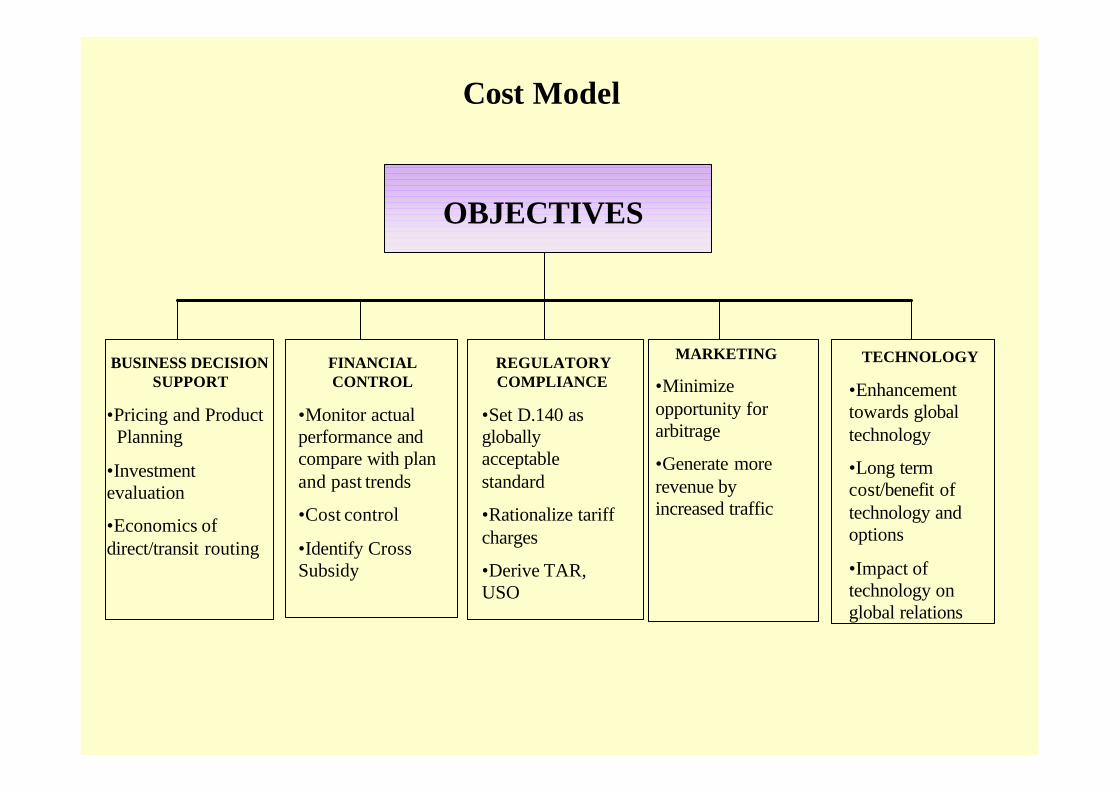

OBJECTIVES

BUSINESS DECISIONSUPPORT

•Pricing and ProductPlanning

•Investment evaluation

•Economics of direct/transit routing

FINANCIAL CONTROL

•Monitor actualperformance andcompare with plan and past trends

•Cost control

•Identify Cross Subsidy

REGULATORYCOMPLIANCE

•Set D.140 as globallyacceptable standard

•Rationalize tariffcharges

•Derive TAR, USO

MARKETING

•Minimize opportunity for arbitrage

•Generate more revenue by increased traffic

TECHNOLOGY

•Enhancement towards global technology

•Long term cost/benefit of technology andoptions

•Impact of technology on global relations

Cost Model

Costing Methodologies

METHODOLOGIES

ACCOUNTING CONVENTION COSTING APPROACH

HISTORICALCOST

ACCOUNTING

CURRENTCOST

ACCOUNTING

FULLYDISTRIBUTED

COST APPROACH

INCREMENTALCOST

APPROACH

•Actual costs incurred

•Cost of today of providing service

•Mirrors competitorspotential cost

•All costs areallocated to services

•Incremental costs only

•Often long-run incremental costs only

36Competition in Voice TelephonyCompetition in Voice Telephony

No much differences if…No much differences if…l Current cost accounting is used ð FDC=Historical Cost is no more relevant

l Costs of efficient services provision is used ð this should be the aim of all operatorsð spare capacity (legitimate if transparency)ð Disagreement on time horizon to achieve this

l Principle of cost causality is applied (ABC) ð Common cost must be attributed to the service

on the basis of the causality priniple ð However an exhaustive application of an ABC

approach may be very costlyl Need for cost recovery realised appropriatelyð IC approach should contain a markup

l Principle of transparency : The open availability of information used in the cost deviation process in order to allow comprehension of the final rate from the vantage point of an external analyst

l Principle of practicability : The ability to implement a costing methodology with reasonable demands being placed on data availability anddata processing in order to keep the costing exercise economical, yet still useful

l Principle of cost causality : The demonstration of clear cause-and-effect relationship between service delivery on the one hand and the network element and other resources used to provide it on the other hand, taking into account the relevant underlying cost determinants (cost drivers)

l Principle of reasonable contribution to common costs : Costing methodologies should provide for a reasonable contribution to common costs

l Principle of efficiency : The provision of a forecast of cost reductions that result from a more efficient combination of resources

Agreed General principles

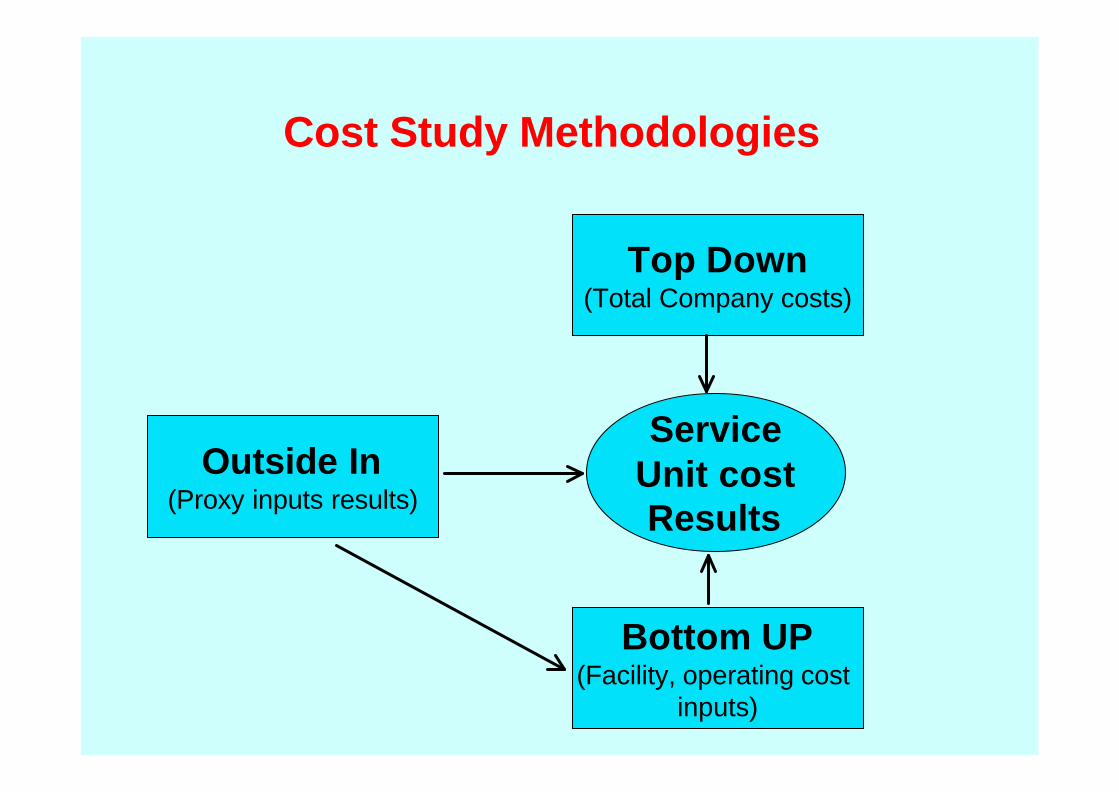

Top Down(Total Company costs)

Bottom UP(Facility, operating cost

inputs)

Outside In(Proxy inputs results)

ServiceUnit cost Results

Cost Study Methodologies

0.30

0.24

0.23

0.23

0.22

0.21

0.20

0.20

0.18

0.18

0.17

0.16

0.156

Sw itzerland

Germany

Italy

Austria

Sweden

Finland

France

Spain

Belgium

Netherlands

Denmark

UK

Norway

European fixed-to-mobile interconnect charges, (US$/min)

0 5 10 15 20 25 30

Mobile-to-fixed LOCAL

Mobile-to-fixed SINGLE

TRANSIT

Mobile-to-fixed DOUBLE

TRANSIT

Fixed-to-mobile

Lowest

Best-practice(20%) guideline

Highest

EU, range of interconnect rates, (US cents per min.)

Interconnection Rates in Selected European Countries

Calling Party Pays (CPP). In US $ per minute.

0.105

0.005

0.020

0.056

0.010

0.020

0.009

0.008

0.008

0.007

0.0012

0.000

0.000

0.008

0.000

0.0096

CPP

RPP

USA

Sri Lanka

Singapore

HK SAR

Canada

China

Mobile-to-fixedinterconnect rate

Fixed-to-mobileinterconnect rate

RPP countries

Average

0.293

0.208

0.205

0.078

0.070

0.20

0.047

0.034

0.017

0.293

0.052

0.051

0.042

0.050

0.026

0.047

0.034

0.017

Antigua

Botswana

Philippines

Dom. Rep.

Cambodia

Mexico

Guatemala

Malaysia

Costa Rica

Mobile-to-fixedinterconnect rate

Fixed-to-mobileinterconnect rate

CPP countries

Interconnection rates in selected non-European countries

Calling Party Pays (CPP) vs. Receiving Party Pays (RPP). In US$ per minute.

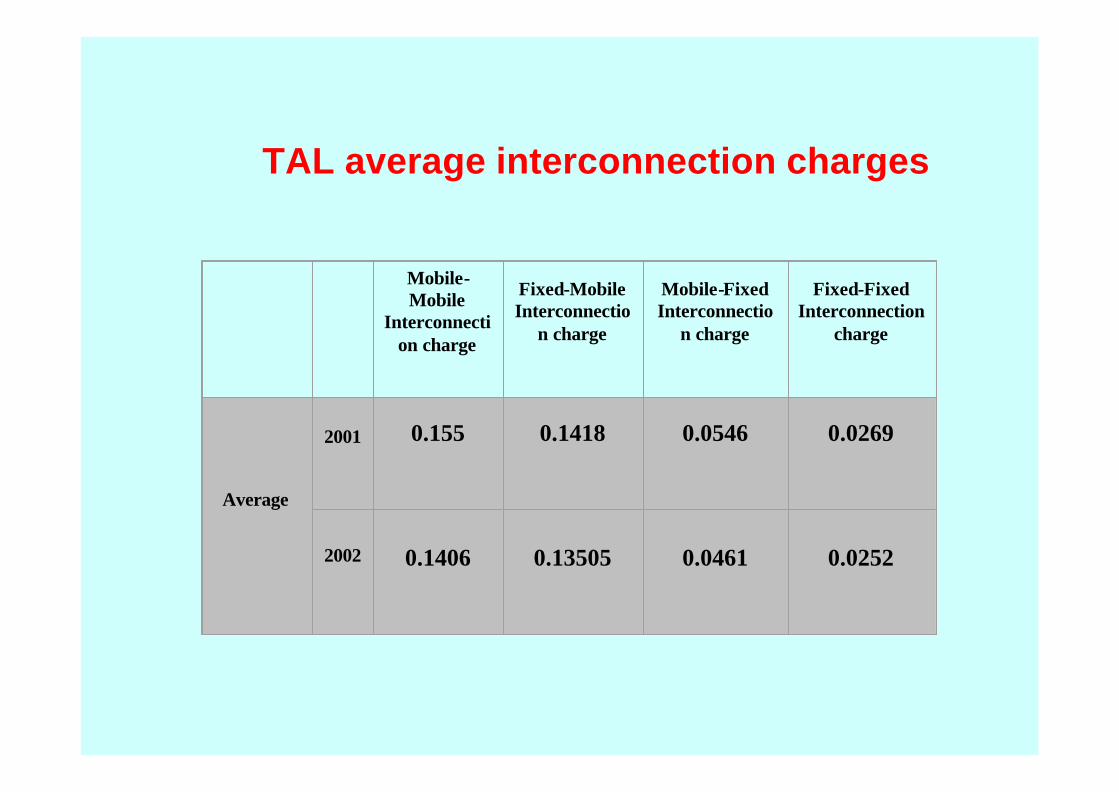

TAL average interconnection charges

Mobile-Mobile

Interconnection charge

Fixed-MobileInterconnectio

n charge

Mobile-FixedInterconnectio

n charge

Fixed-FixedInterconnection

charge

Average

2001 0.155 0.1418 0.0546 0.0269

2002 0.1406 0.13505 0.0461 0.0252

Fixed to Mobile Interconnect

charge

Mobile to fixed Interconnect

chargeLocal

Mobile to fixed Interconnect

chargeSingle transit

Mobile to Fixed Interconnect

chargeDouble transit

Average 0.167 0.078 0.096 0.150

TAF average interconnection charges

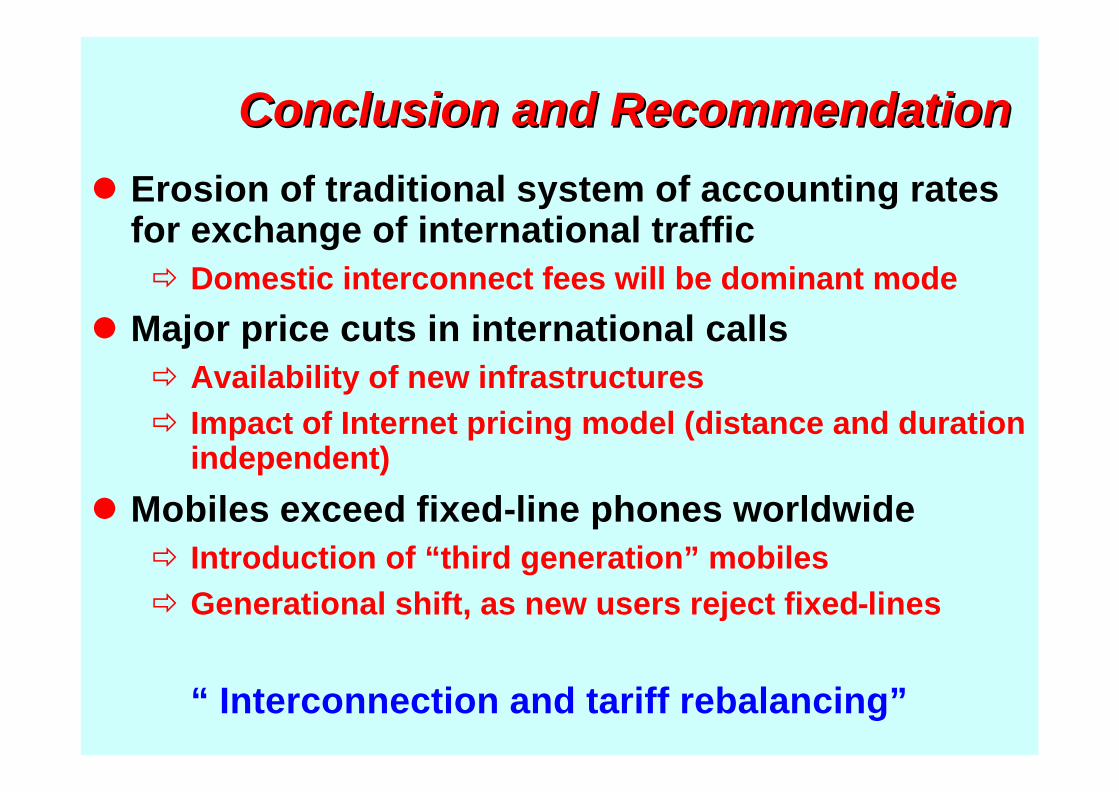

Conclusion and Recommendation Conclusion and Recommendation

l Erosion of traditional system of accounting rates for exchange of international trafficð Domestic interconnect fees will be dominant mode

l Major price cuts in international calls ð Availability of new infrastructuresð Impact of Internet pricing model (distance and duration

independent)

l Mobiles exceed fixed-line phones worldwide ð Introduction of “third generation” mobiles ð Generational shift, as new users reject fixed-lines

“ Interconnection and tariff rebalancing”