Embed Size (px)

Citation preview

CERI Breakfast Overview

Allan Fogwill, President & CEO

Sept 19, 2018

COMPETITIVE ANALYSIS OF

CANADIAN LNG

Canadian Energy Research Institute Overview Founded in 1975, the Canadian Energy Research Institute (CERI) is an independent, registered charitable organization specializing in the analysis of energy economics and related environmental policy issues in the energy production, transportation, and consumption sectors. Our mission is to provide relevant, independent, and objective economic research of energy and environmental issues to benefit business, government, academia and the public. CERI publications include:

•Market specific studies •Geopolitical analyses •Commodity reports (crude oil, electricity and natural gas)

In addition, CERI hosts an annual Petrochemical Conference.

Core Funders:

Donors:

In-kind: Ivey Foundation

Presentation Outline Market Overview

Methodology and Assumptions

Supply Costs

Competitive Analysis

Conversion factor ------ 1 BCF/d = 7.6 MTPA

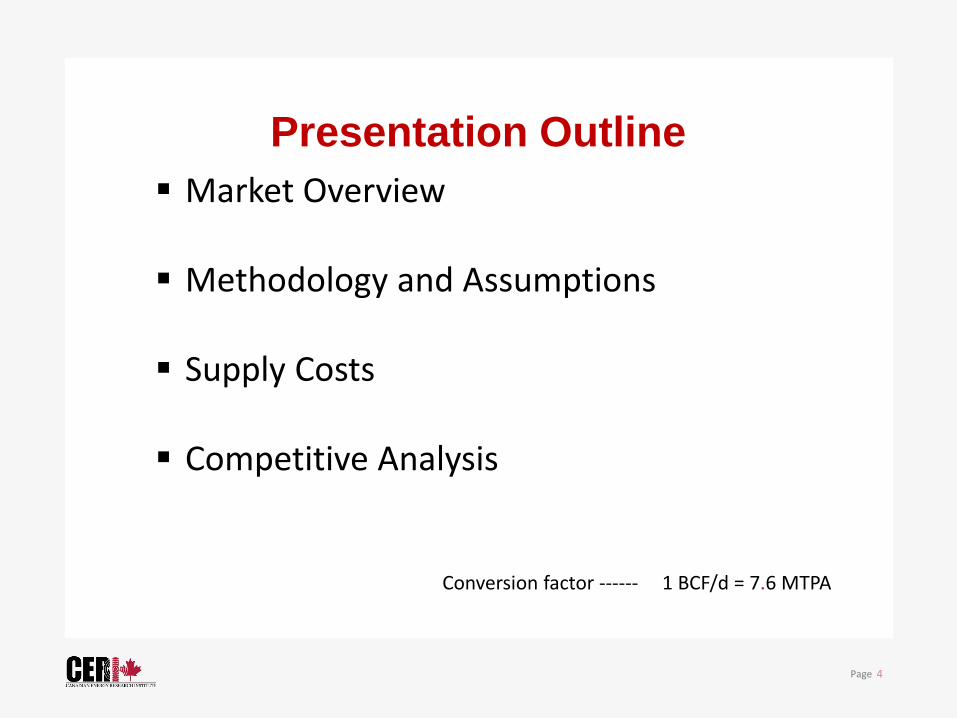

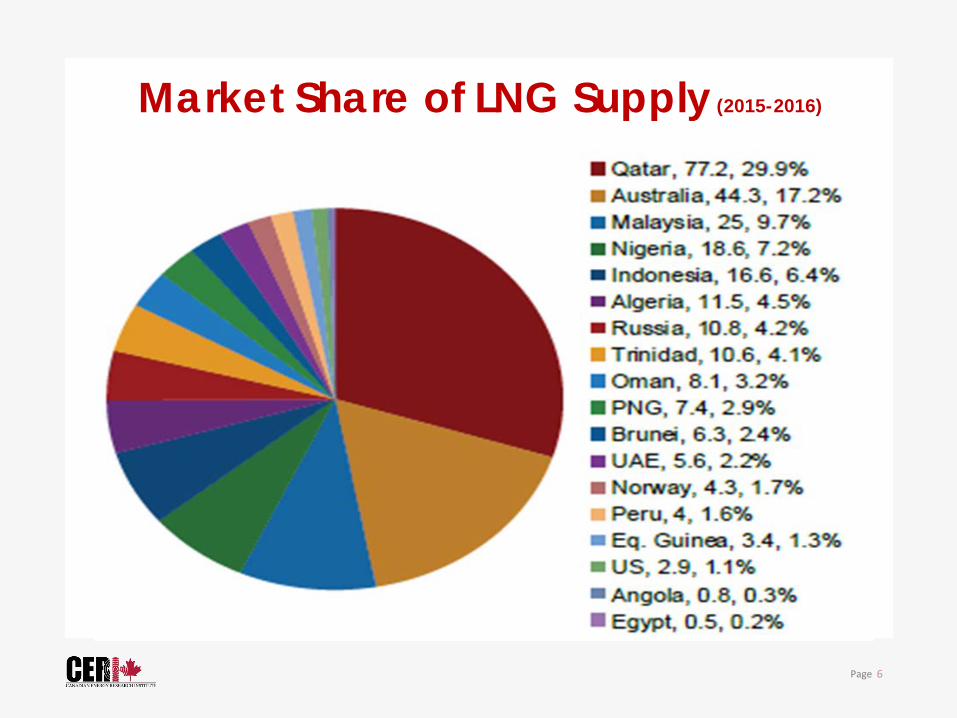

Global Market Overview • Global trade in LNG increased to 258 million tonnes per annum

(MTPA) in 2016 from 245 MTPA in 2015 and 241 MTPA in 2014

Market Share of LNG Supply (2015-2016)

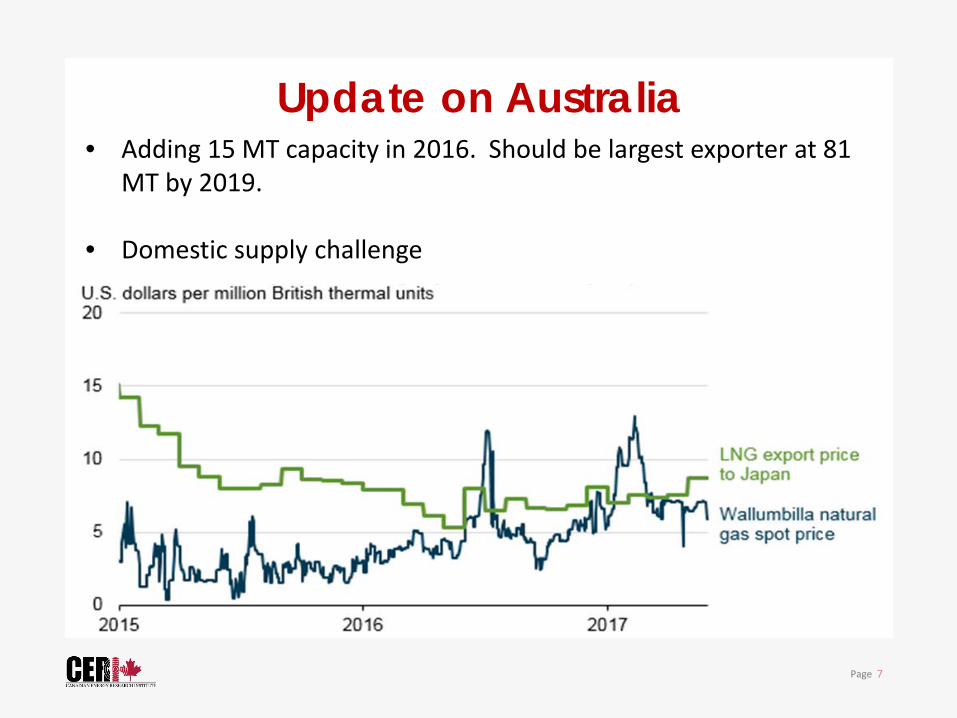

Update on Australia • Adding 15 MT capacity in 2016. Should be largest exporter at 81

MT by 2019.

• Domestic supply challenge

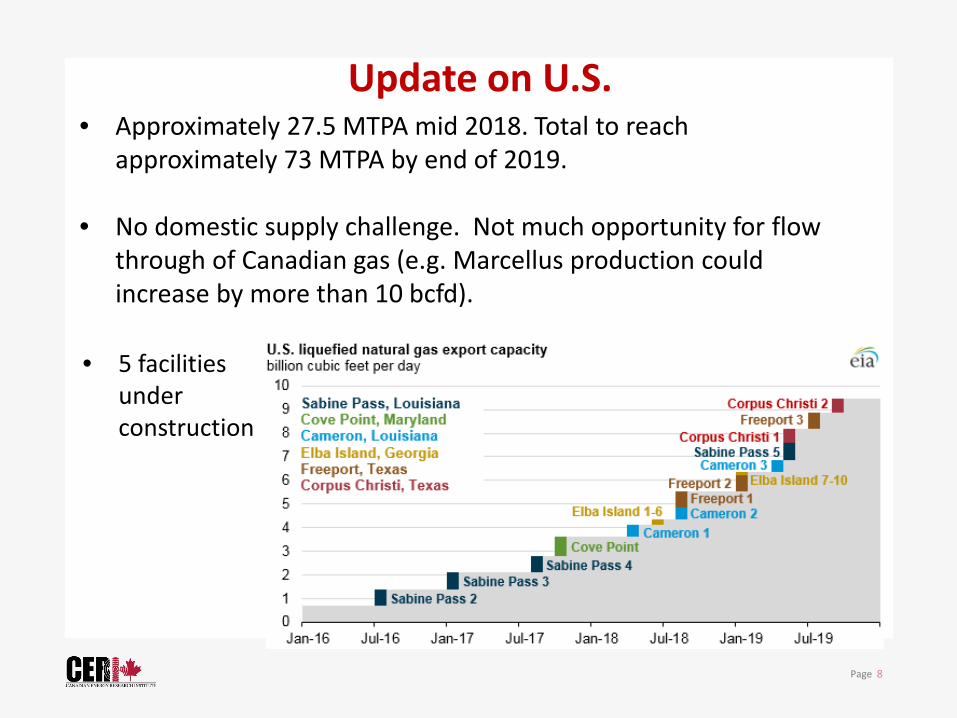

Update on U.S. • Approximately 27.5 MTPA mid 2018. Total to reach

approximately 73 MTPA by end of 2019.

• No domestic supply challenge. Not much opportunity for flow through of Canadian gas (e.g. Marcellus production could increase by more than 10 bcfd).

• 5 facilities under construction

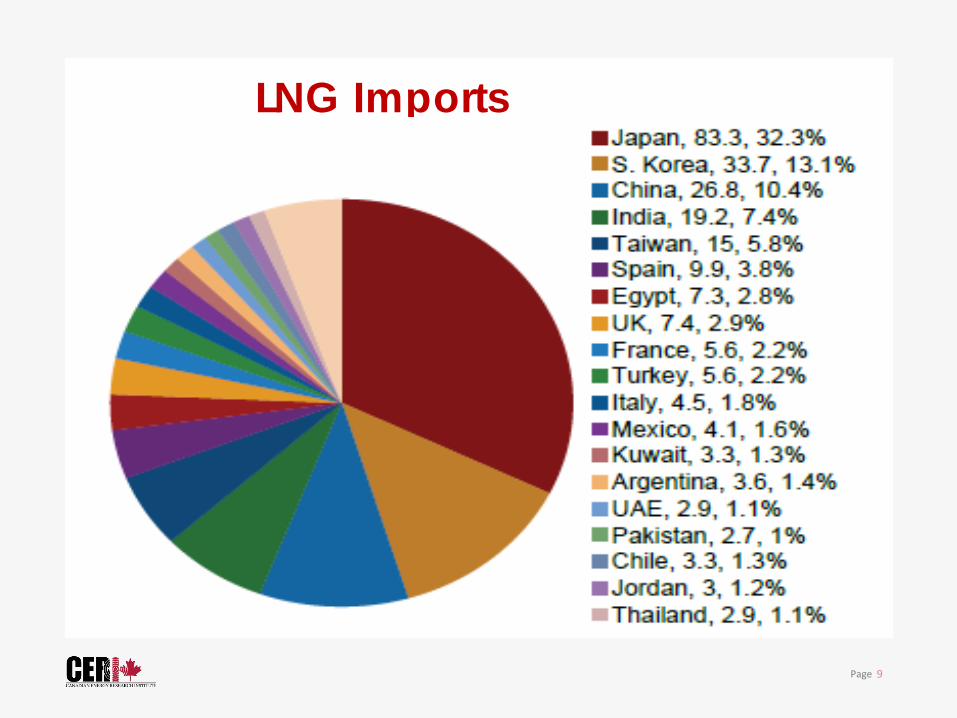

LNG Imports

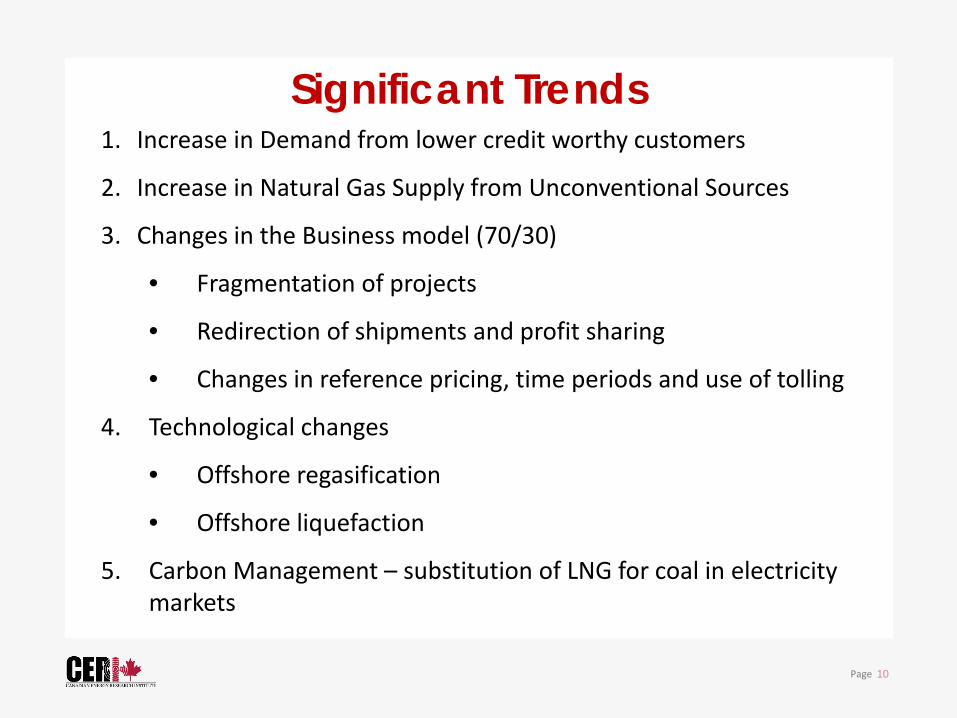

Significant Trends 1. Increase in Demand from lower credit worthy customers

2. Increase in Natural Gas Supply from Unconventional Sources

3. Changes in the Business model (70/30)

• Fragmentation of projects

• Redirection of shipments and profit sharing

• Changes in reference pricing, time periods and use of tolling

4. Technological changes

• Offshore regasification

• Offshore liquefaction

5. Carbon Management – substitution of LNG for coal in electricity markets

Canadian Projects • 35 LNG export licenses issued

• 28 in BC • 3 in QC • 3 in NS • 1 in NB

• Key projects • Goldboro LNG NS – 5-10 MTPA, integrated, 2018 FID • Bearhead LNG NS – 8-12 MTPA, tolling, 2018 FID • Woodfibre LNG BC – 2 MTPA, merchant, active • LNG Canada BC – 13 - 26 MTPA, integrated, 2018 FID • Kitimat LNG BC – 10 MTPA, integrated, n/a

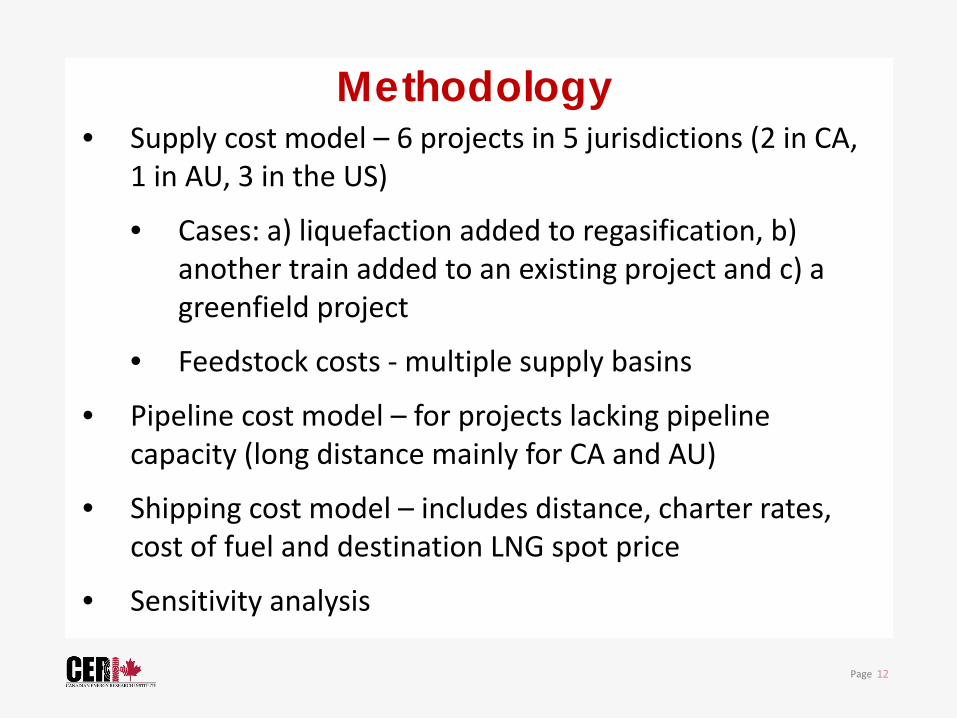

Methodology • Supply cost model – 6 projects in 5 jurisdictions (2 in CA,

1 in AU, 3 in the US)

• Cases: a) liquefaction added to regasification, b) another train added to an existing project and c) a greenfield project

• Feedstock costs - multiple supply basins

• Pipeline cost model – for projects lacking pipeline capacity (long distance mainly for CA and AU)

• Shipping cost model – includes distance, charter rates, cost of fuel and destination LNG spot price

• Sensitivity analysis

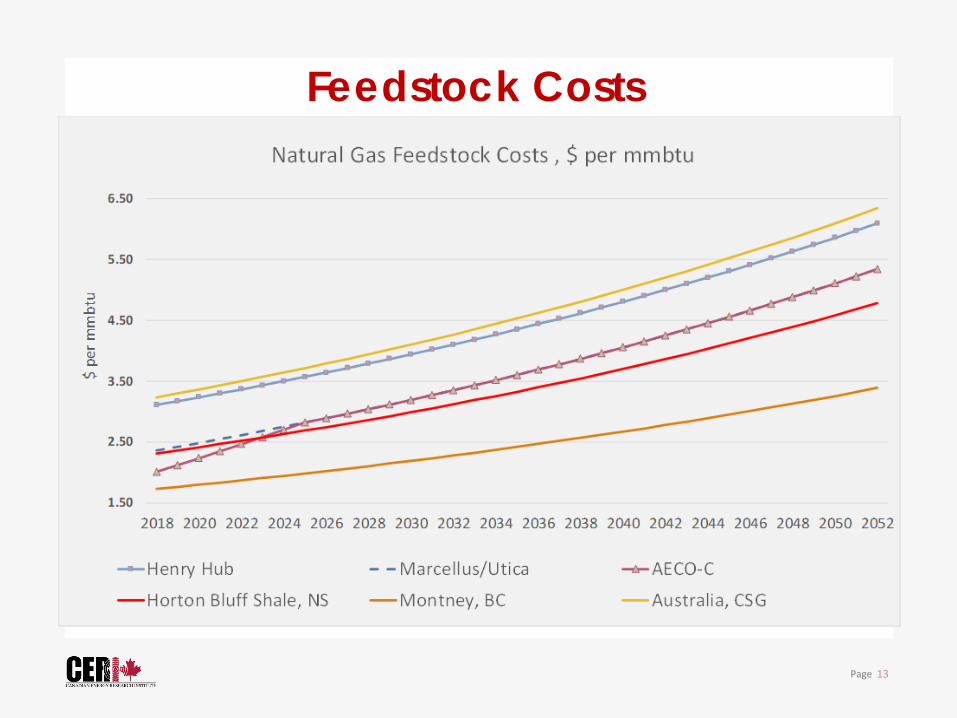

Feedstock Costs

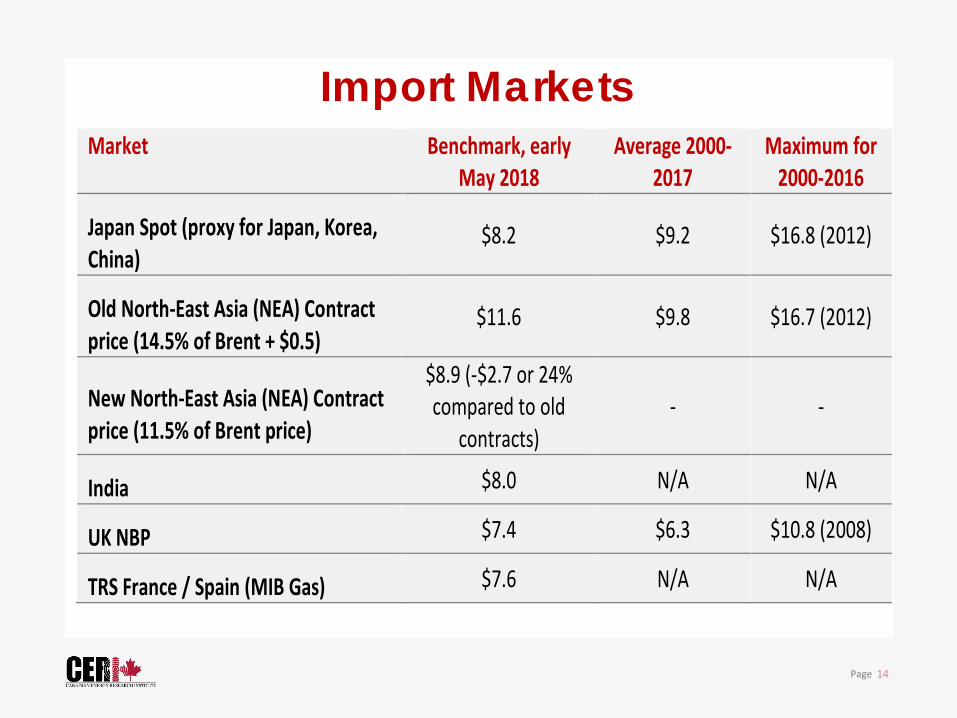

Import Markets Market Benchmark, early

May 2018 Average 2000-

2017 Maximum for

2000-2016

Japan Spot (proxy for Japan, Korea, China)

$8.2 $9.2 $16.8 (2012)

Old North-East Asia (NEA) Contract price (14.5% of Brent + $0.5)

$11.6 $9.8 $16.7 (2012)

New North-East Asia (NEA) Contract price (11.5% of Brent price)

$8.9 (-$2.7 or 24% compared to old

contracts) - -

India $8.0 N/A N/A

UK NBP $7.4 $6.3 $10.8 (2008)

TRS France / Spain (MIB Gas) $7.6 N/A N/A

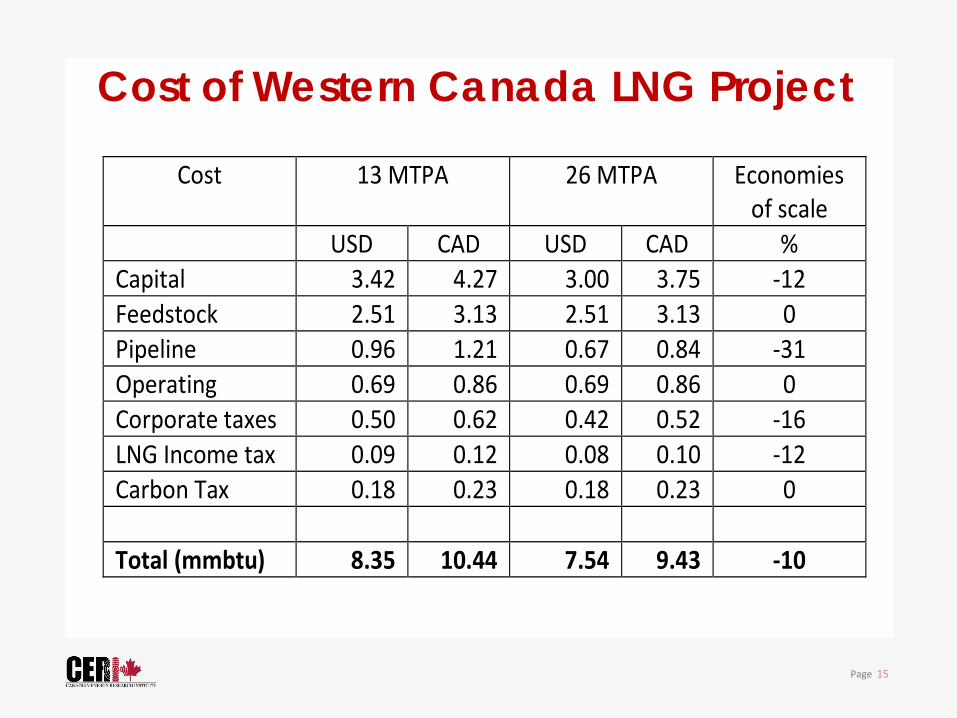

Cost of Western Canada LNG Project

Cost 13 MTPA 26 MTPA Economies of scale

USD CAD USD CAD % Capital 3.42 4.27 3.00 3.75 -12 Feedstock 2.51 3.13 2.51 3.13 0 Pipeline 0.96 1.21 0.67 0.84 -31 Operating 0.69 0.86 0.69 0.86 0 Corporate taxes 0.50 0.62 0.42 0.52 -16 LNG Income tax 0.09 0.12 0.08 0.10 -12 Carbon Tax 0.18 0.23 0.18 0.23 0 Total (mmbtu) 8.35 10.44 7.54 9.43 -10

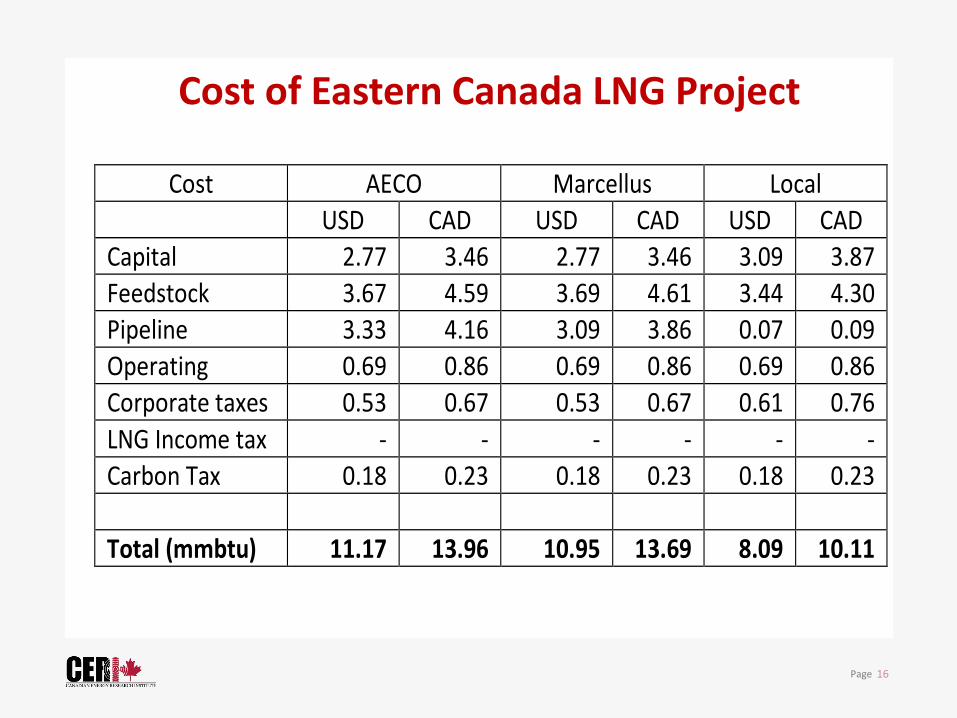

Cost of Eastern Canada LNG Project

Cost AECO Marcellus Local USD CAD USD CAD USD CAD

Capital 2.77 3.46 2.77 3.46 3.09 3.87 Feedstock 3.67 4.59 3.69 4.61 3.44 4.30 Pipeline 3.33 4.16 3.09 3.86 0.07 0.09 Operating 0.69 0.86 0.69 0.86 0.69 0.86 Corporate taxes 0.53 0.67 0.53 0.67 0.61 0.76 LNG Income tax - - - - - - Carbon Tax 0.18 0.23 0.18 0.23 0.18 0.23 Total (mmbtu) 11.17 13.96 10.95 13.69 8.09 10.11

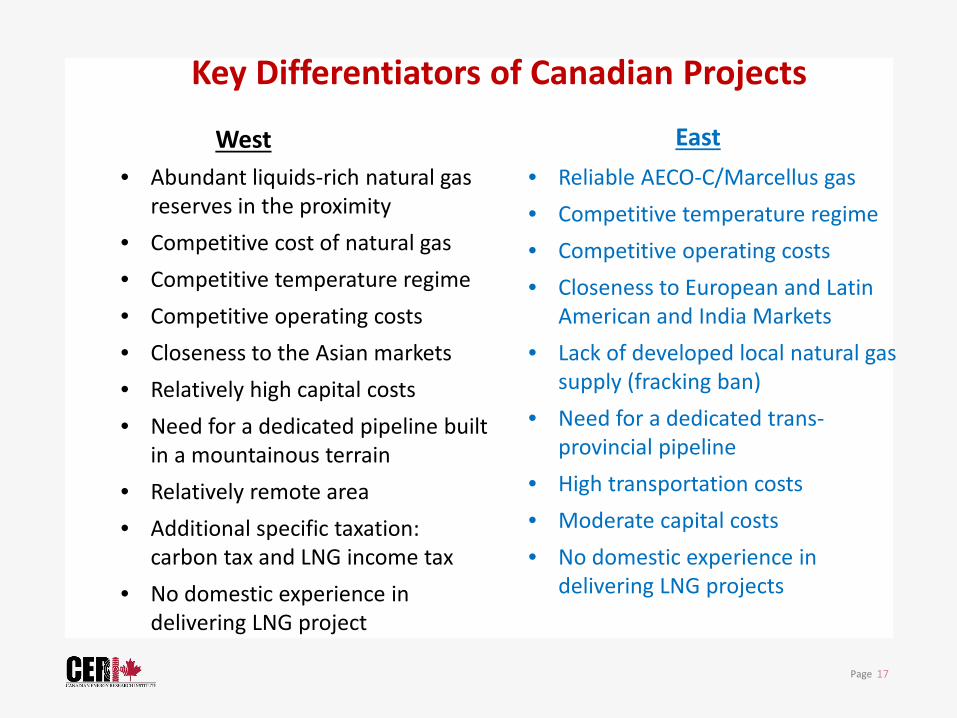

Key Differentiators of Canadian Projects

West East • Reliable AECO-C/Marcellus gas • Competitive temperature regime • Competitive operating costs • Closeness to European and Latin

American and India Markets • Lack of developed local natural gas

supply (fracking ban) • Need for a dedicated trans-

provincial pipeline • High transportation costs • Moderate capital costs • No domestic experience in

delivering LNG projects

• Abundant liquids-rich natural gas reserves in the proximity

• Competitive cost of natural gas • Competitive temperature regime • Competitive operating costs • Closeness to the Asian markets • Relatively high capital costs • Need for a dedicated pipeline built

in a mountainous terrain • Relatively remote area • Additional specific taxation:

carbon tax and LNG income tax • No domestic experience in

delivering LNG project

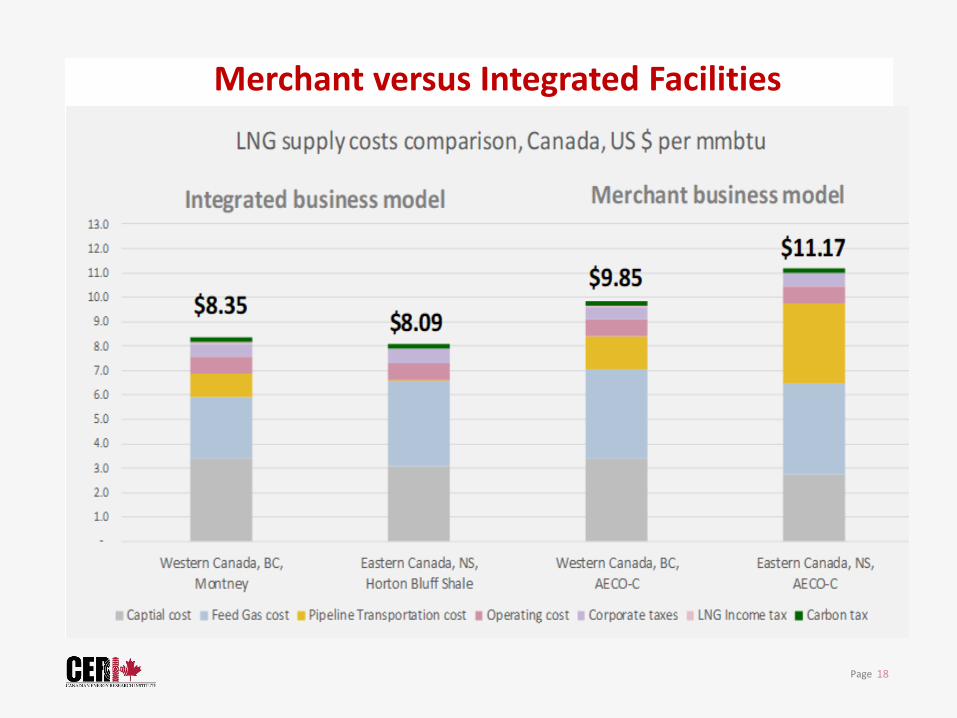

Merchant versus Integrated Facilities

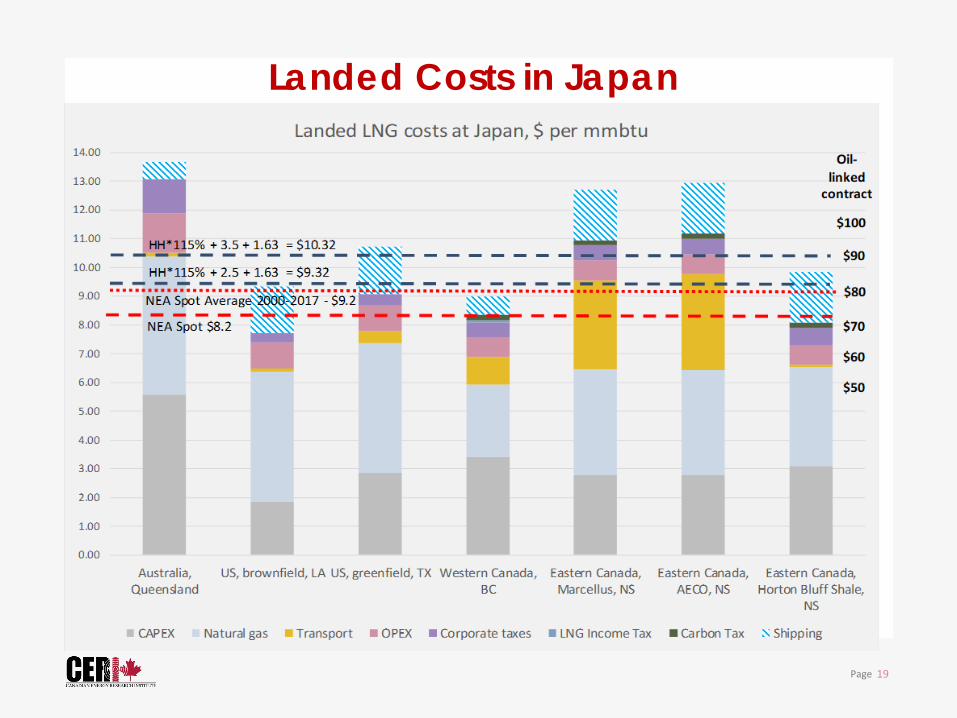

Landed Costs in Japan

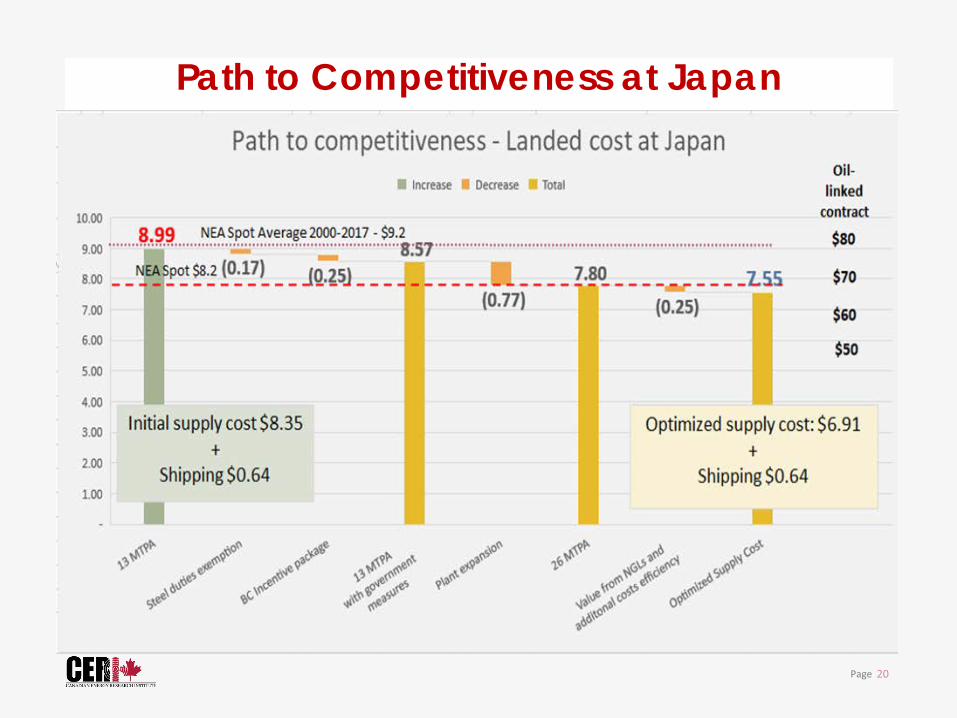

Path to Competitiveness at Japan

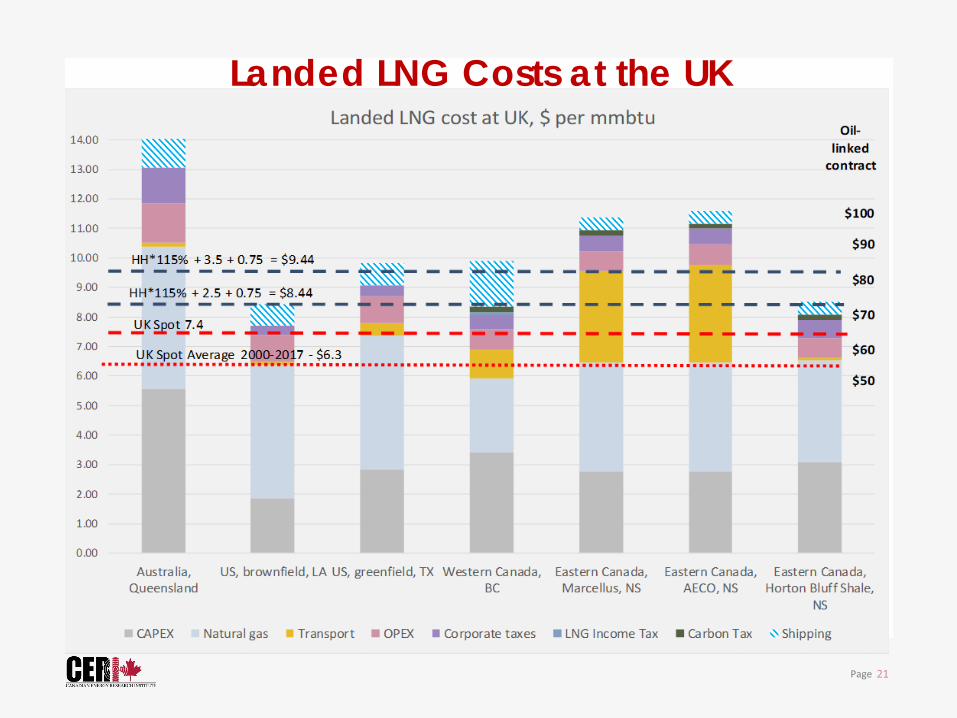

Landed LNG Costs at the UK

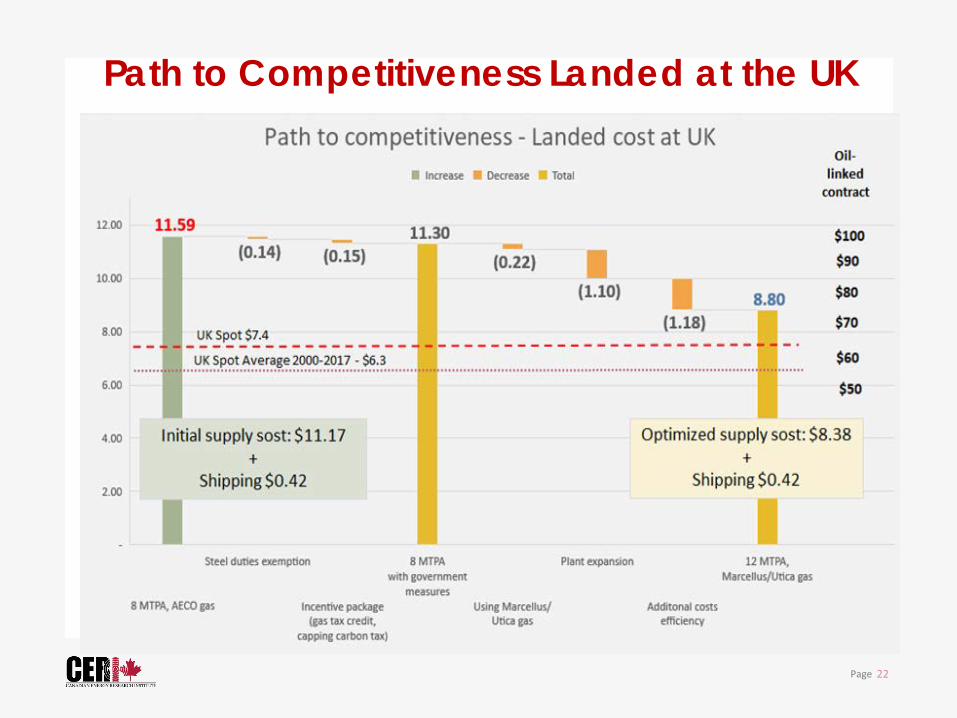

Path to Competitiveness Landed at the UK

Conclusion • Global trade is increasing faster than expectations –

mostly in Asia

• Domestic Competitiveness • Eastern integrated projects (if local gas was available)

slightly more competitive than western projects • Merchant projects in the west more competitive

mainly due to proximity to AECO • Incentives a factor in project FIDs (steel tariff

exemption, LNG tax exemption)

Conclusion - continued • Asian Markets

• CA projects more expensive than Japan spot • Western CA market more competitive than AU and US • Breakeven price is $8.99 in Japan • Oil price needed = $80

• European Markets • CA projects more expensive than UK spot • US projects more competitive than Eastern CA

projects • Breakeven price is $11.4 in the UK • Oil price needed = $100 • Market dynamic uncertainty = Gazprom

Thank You for Your Time WWW.CERI.CA

CANADIAN ENERGY RESEARCH INSTITUTE @CERI_CANADA

UPCOMING STUDIES: Natural Gas Liquids Market and Pricing Urban Energy Systems and Transportation Methane Emissions and Controls for the Natural Gas System