Embed Size (px)

Citation preview

COMPREHENSIVE ANNUALFINANCIAL REPORTFISCAL YEAR ENDINGJUNE 30, 2019

www.cityofandersonsc.com

CITY OF ANDERSON, SOUTH CAROLINA

COMPREHENSIVE ANNUAL FINANCIAL REPORT

YEAR ENDED JUNE 30, 2019

Prepared By: Finance Department Margot B. Martin Finance Director

CITY OF ANDERSON, SOUTH CAROLINA

TABLE OF CONTENTS

YEAR ENDED JUNE 30, 2019

Page Number

Table of Contents i

Transmittal Letter 1

List of Principal Officials and Management Team 7

City of Anderson Organizational Chart 8

Certificate of Achievement for Excellence in Financial Reporting 9

INDEPENDENT AUDITOR'S REPORT 11

Management's Discussion and Analysis 13

Basic Financial Statements

Government-Wide Financial Statements

Statement of Net Position 26

Statement of Activities 27

Fund Financial Statements:

Balance Sheet - Governmental Funds 28

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position 29

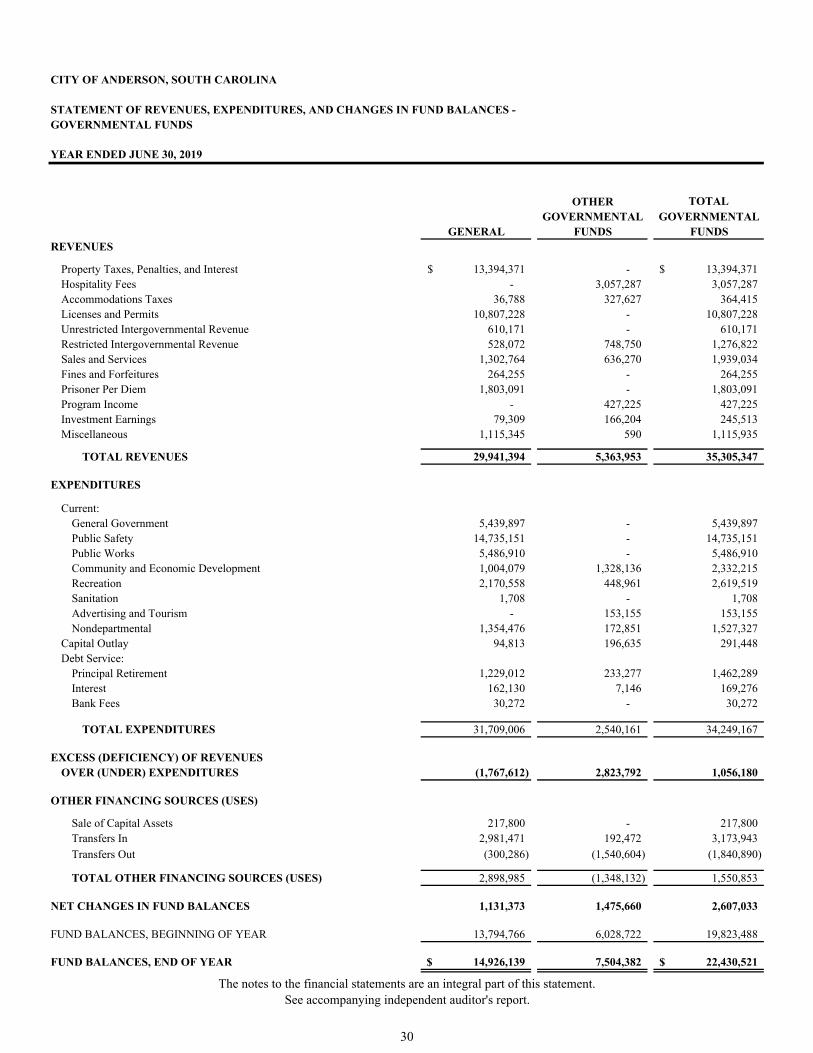

Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds 30

Reconciliation of the Governmental Funds Statement of Revenues, Expenditures,and Changes in Fund Balances to the Statement of Activities 31

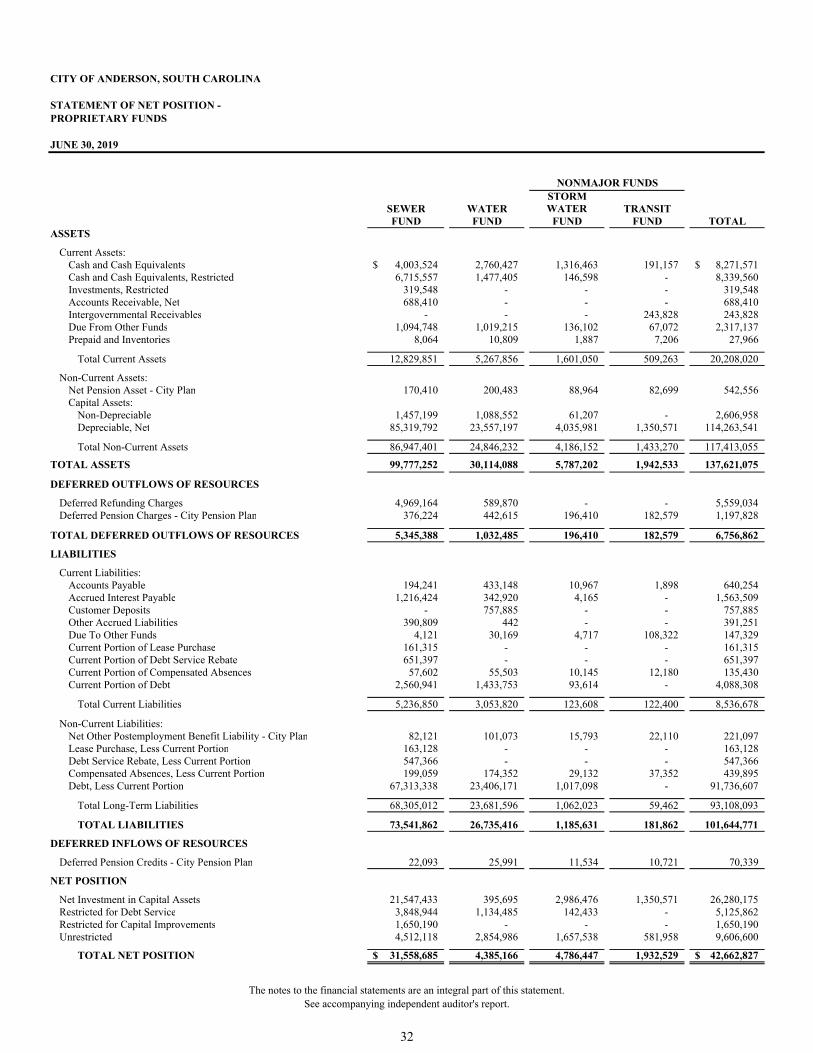

Statement of Net Position - Proprietary Funds 32

Statement of Revenues, Expenses, and Changes in Fund Net Position - Proprietary Funds 33

Statement of Cash Flows - Proprietary Funds 34

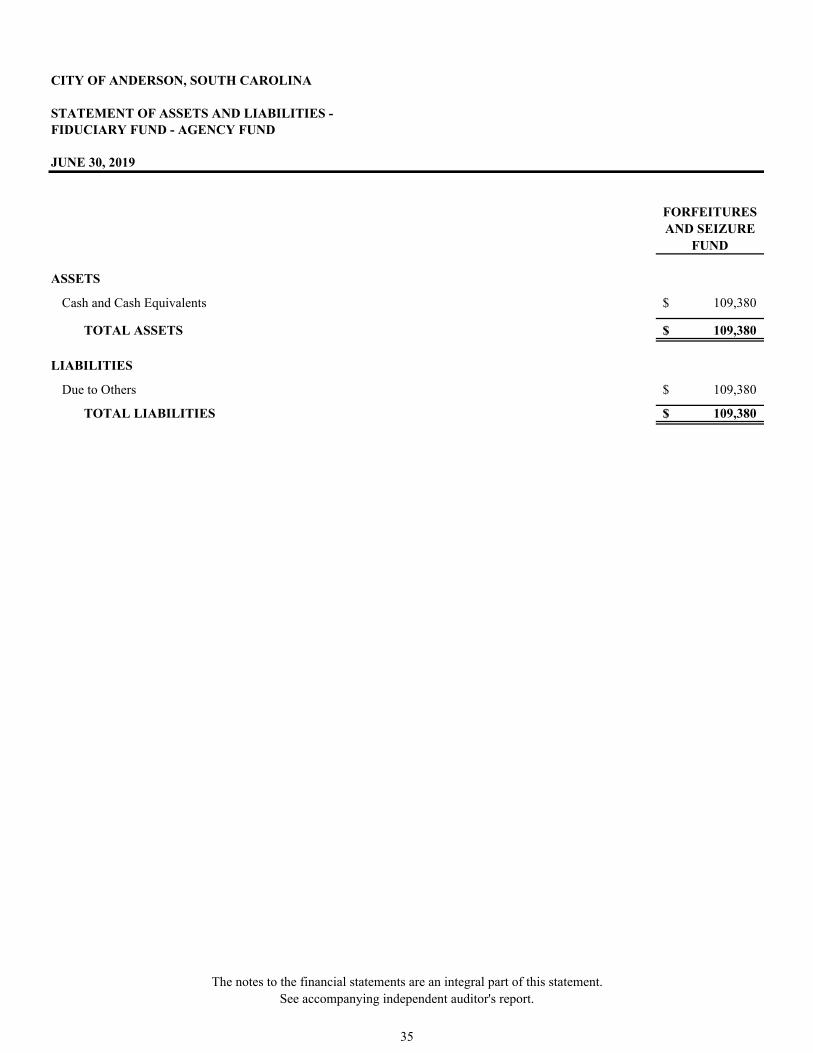

Statement of Assets and Liabilities - Fiduciary Fund - Agency Fund 35

Statement of Net Position - Fiduciary Fund - Pension Trust Fund 36

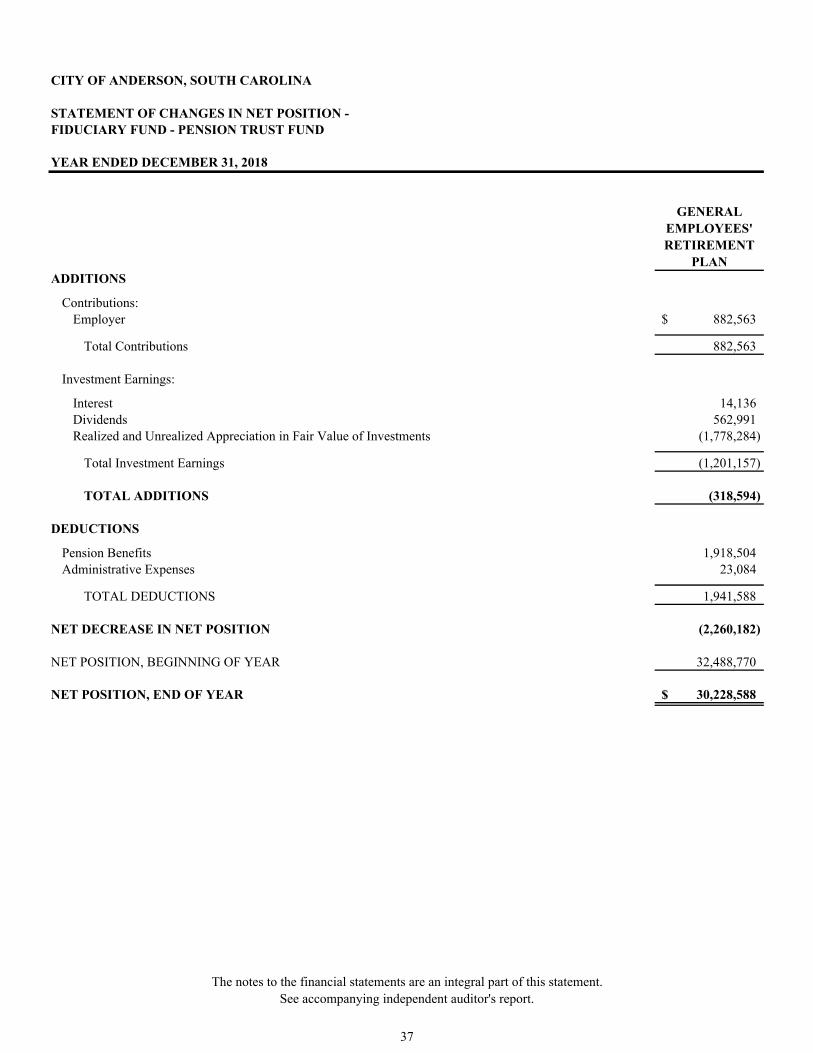

Statement of Changes in Net Position - Fiduciary Fund - Pension Trust Fund 37

Notes to the Financial Statements 38

Budgetary Comparison Schedule

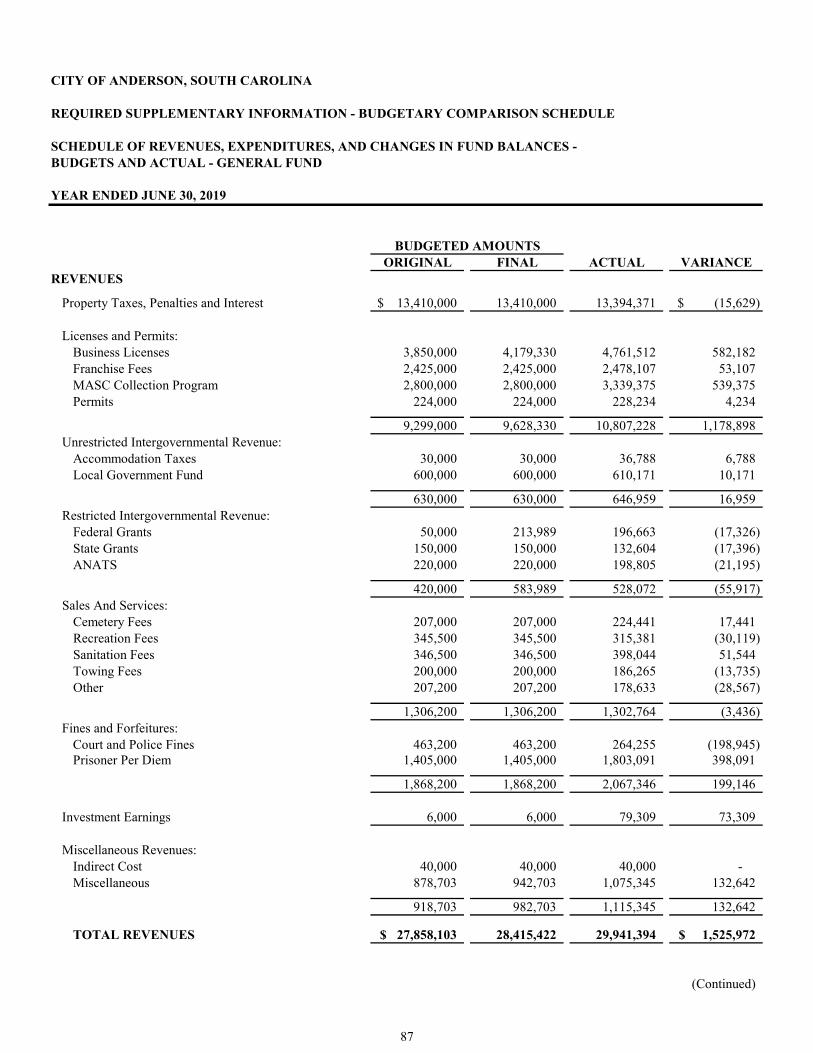

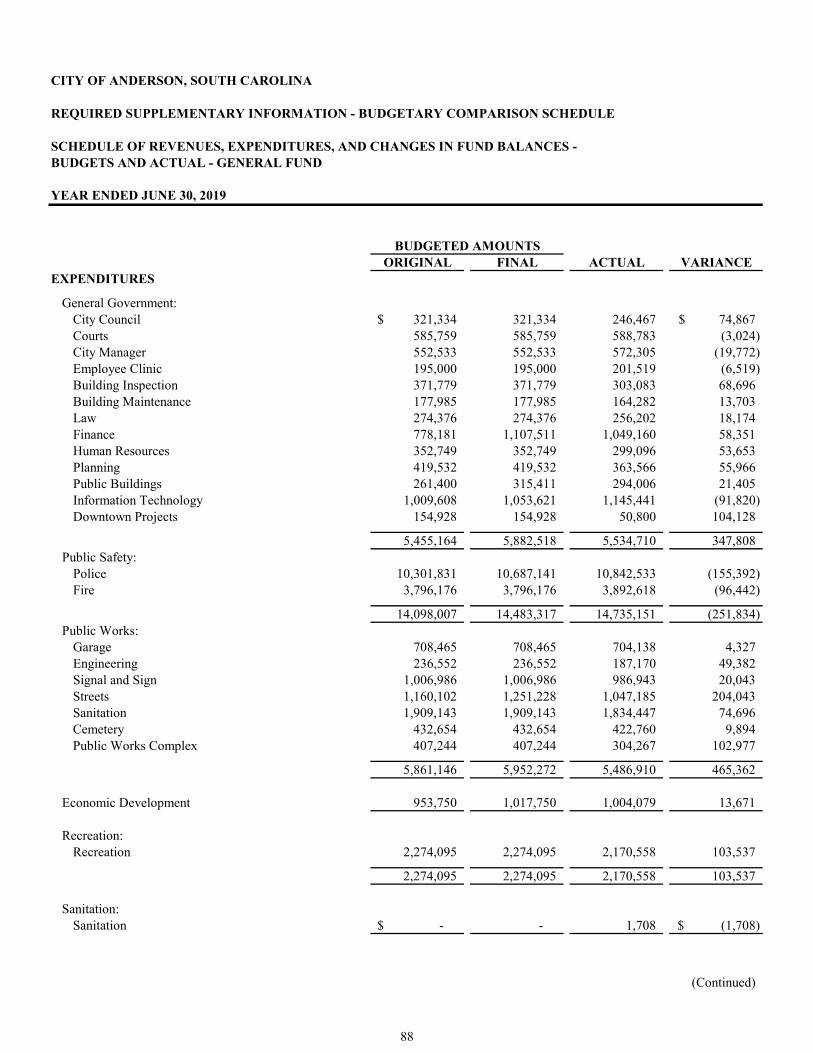

Schedule of Revenues, Expenditures, and Changes in Fund Balances - Budgets and Actual - General Fund 87

Notes to Budgetary Comparison Schedule 90

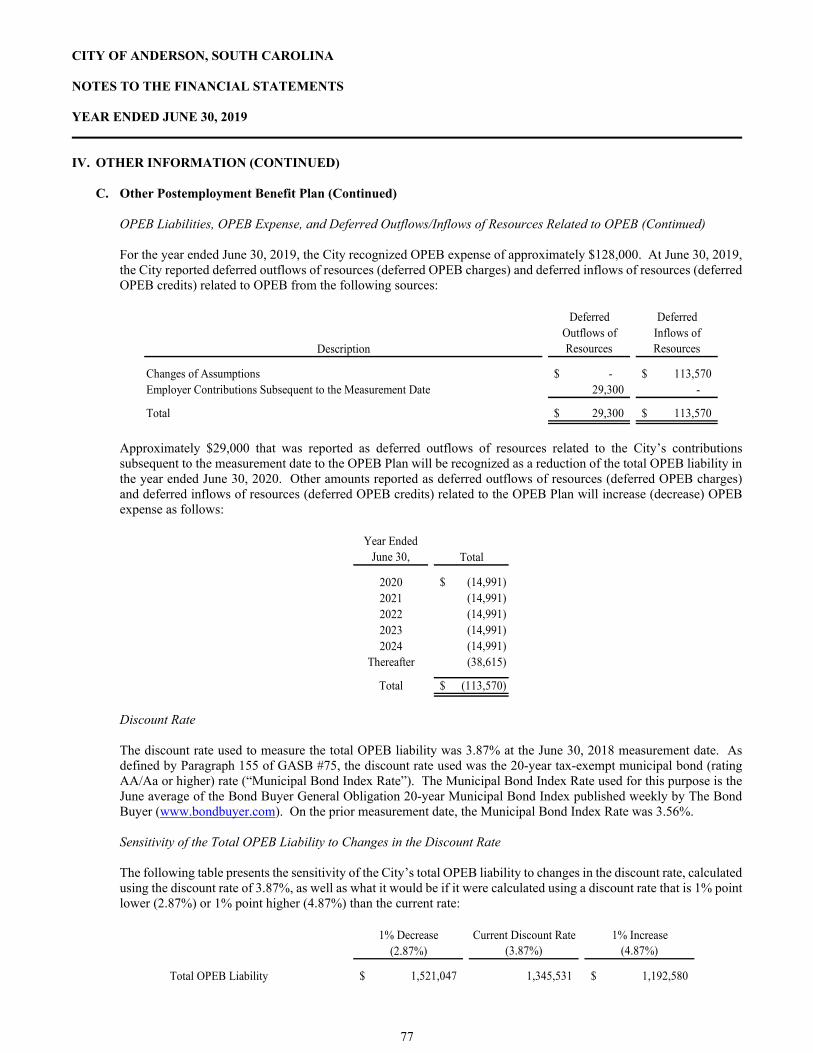

Other Postemployment Benefit Plan Schedule

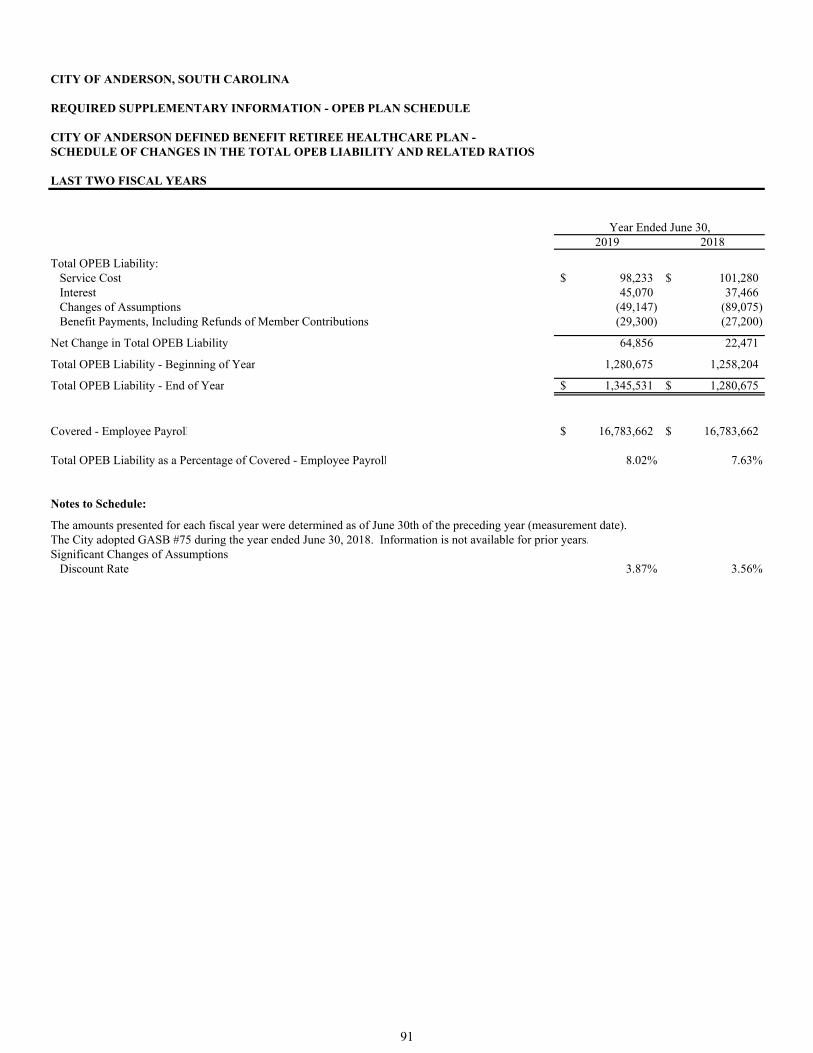

City of Anderson Defined Benefit Retiree Healthcare Plan - Schedule of Changes in theTotal OPEB Liability and Related Ratios 91

FINANCIAL SECTION

INTRODUCTORY SECTION (UNAUDITED)

Required Supplementary Information

(Continued)

i

CITY OF ANDERSON, SOUTH CAROLINA

TABLE OF CONTENTS

YEAR ENDED JUNE 30, 2019

Page Number

Pension Plan Schedules

City of Anderson General Employees' Retirement Plan Schedules

Schedule of Changes in the Net Pension Liability and Related Ratios 92

Schedule of Contributions 93

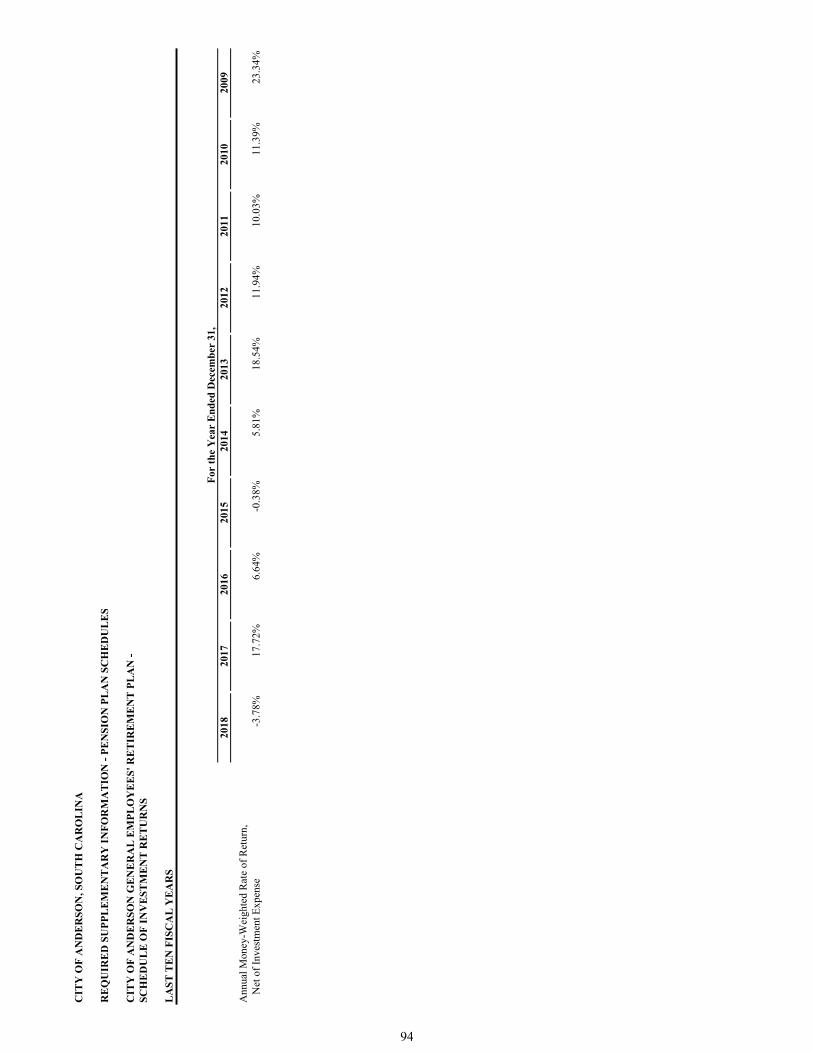

Schedule of Investment Returns 94

South Carolina Police Officers Retirement System Schedules

Schedule of the City of Anderson's Proportionate Share of the Net Pension Liability 95

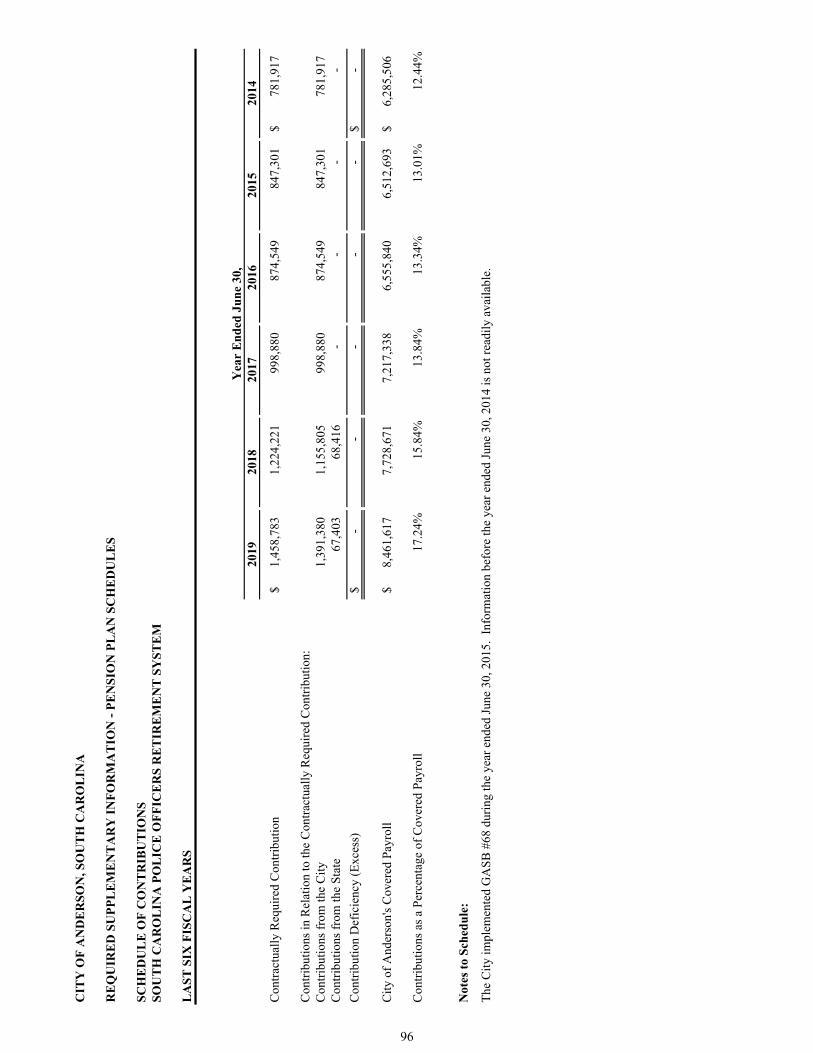

Schedule of Contributions 96

Combining and Individual Fund Financial Schedules

Combining Balance Sheet - Nonmajor Governmental Funds 98

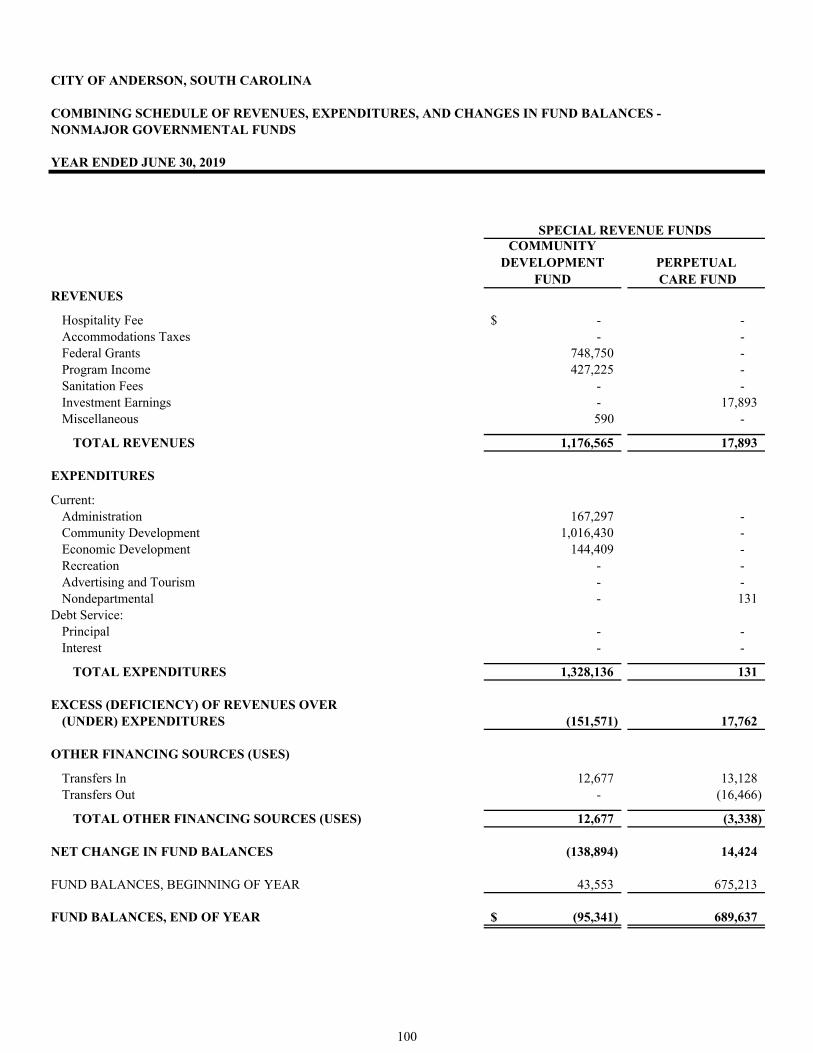

Combining Schedule of Revenues, Expenditures, and Changes in Fund Balances -Nonmajor Governmental Funds 100

Special Revenue Funds

Schedule of Revenues, Expenditures, and Changes in Fund Balances -Budgets and Actual - Community Development Fund 105

Schedule of Revenues, Expenditures, and Changes in Fund Balances -Budgets and Actual - Perpetual Care Fund 106

Schedule of Revenues, Expenditures, and Changes in Fund Balances -Budgets and Actual - Accommodations Tax Fund 107

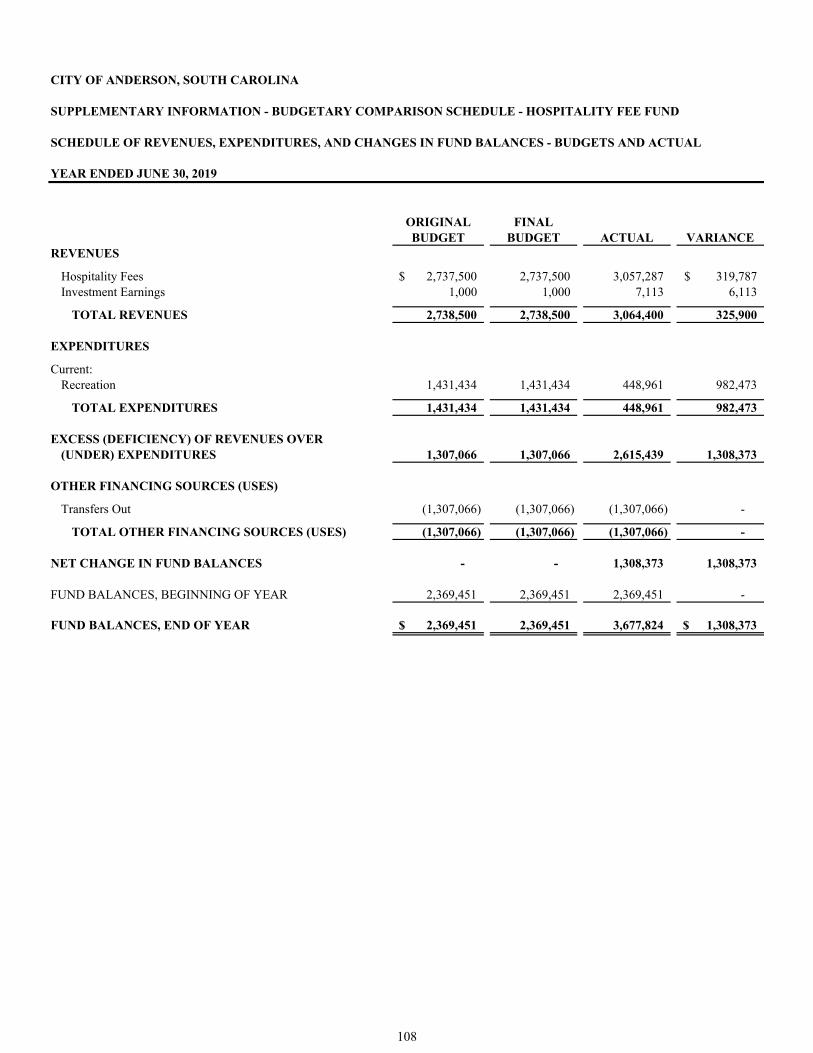

Schedule of Revenues, Expenditures, and Changes in Fund Balances -Budgets and Actual - Hospitality Fee Fund 108

Capital Projects Funds

Schedule of Revenues, Expenditures, and Changes in Fund Balances -Budgets and Actual - Capital Replacement Fund 111

Permanent Funds

Schedule of Revenues, Expenditures, and Changes in Fund Balances -Budgets and Actual - Transportation Investment Fund 115

Proprietary Funds

Schedule of Revenues, Expenses, and Changes in Fund Net PositionBudgets and Actual - Sewer Fund 119

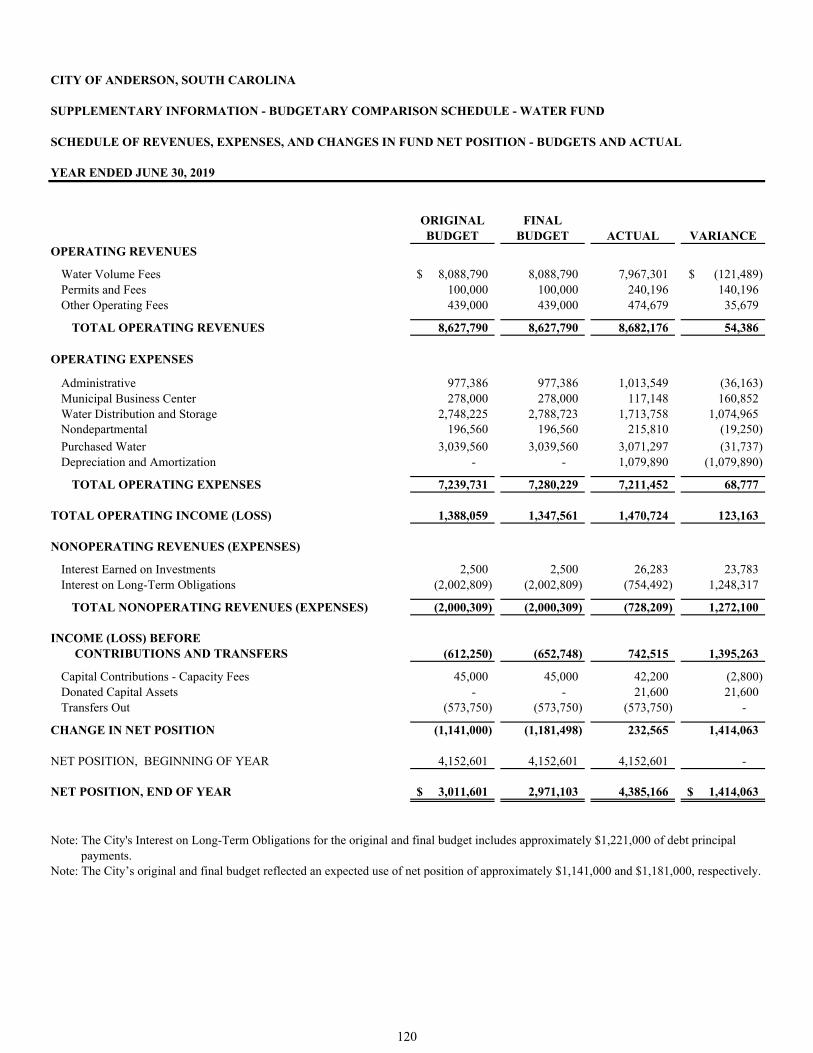

Schedule of Revenues, Expenses, and Changes in Fund Net PositionBudgets and Actual - Water Fund 120

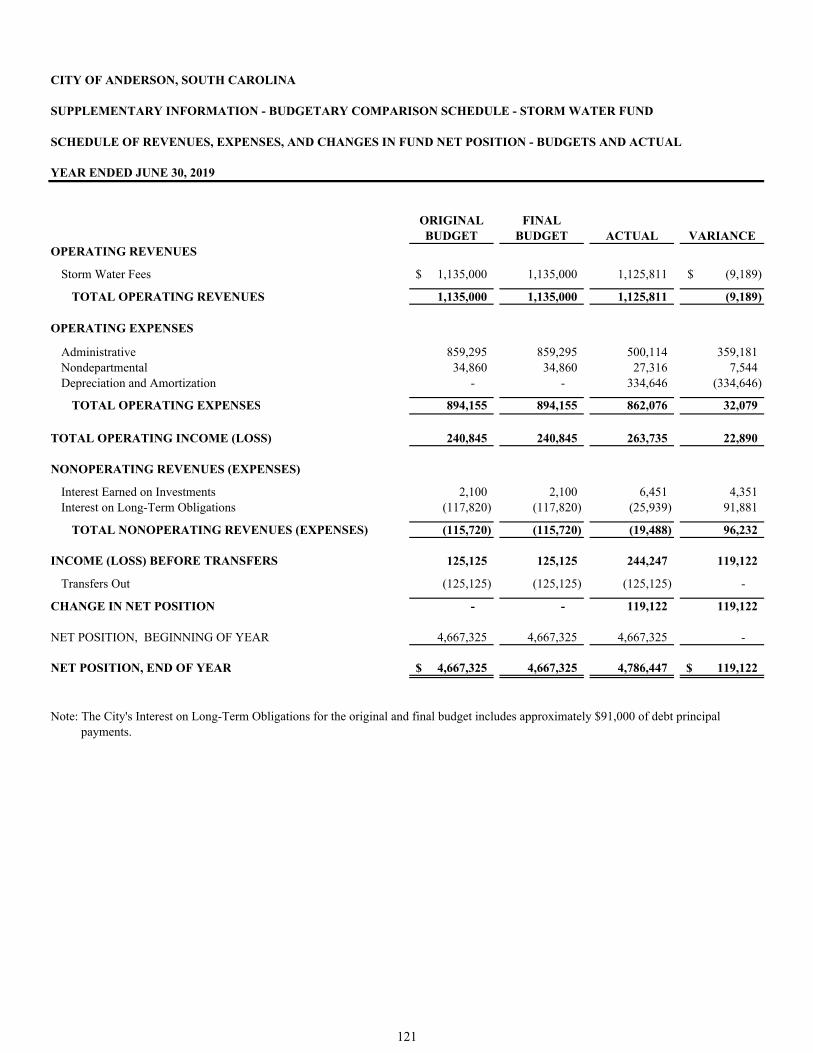

Schedule of Revenues, Expenses, and Changes in Fund Net PositionBudgets and Actual - Storm Water Fund 121

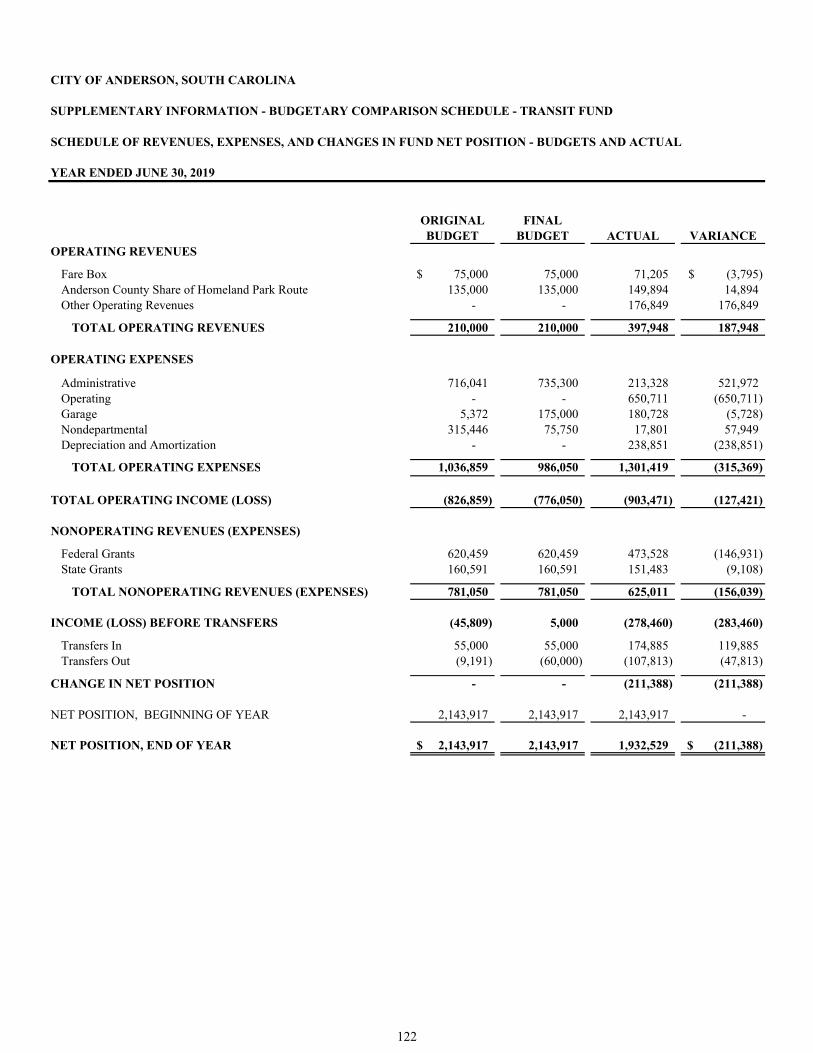

Schedule of Revenues, Expenses, and Changes in Fund Net PositionBudgets and Actual - Transit Fund 122

Required Supplementary Information (Continued)

Supplementary Information

FINANCIAL SECTION (CONTINUED)

(Continued)

ii

CITY OF ANDERSON, SOUTH CAROLINA

TABLE OF CONTENTS

YEAR ENDED JUNE 30, 2019

Page Number

Combining and Individual Fund Financial Schedules (Continued)

Fiduciary Funds

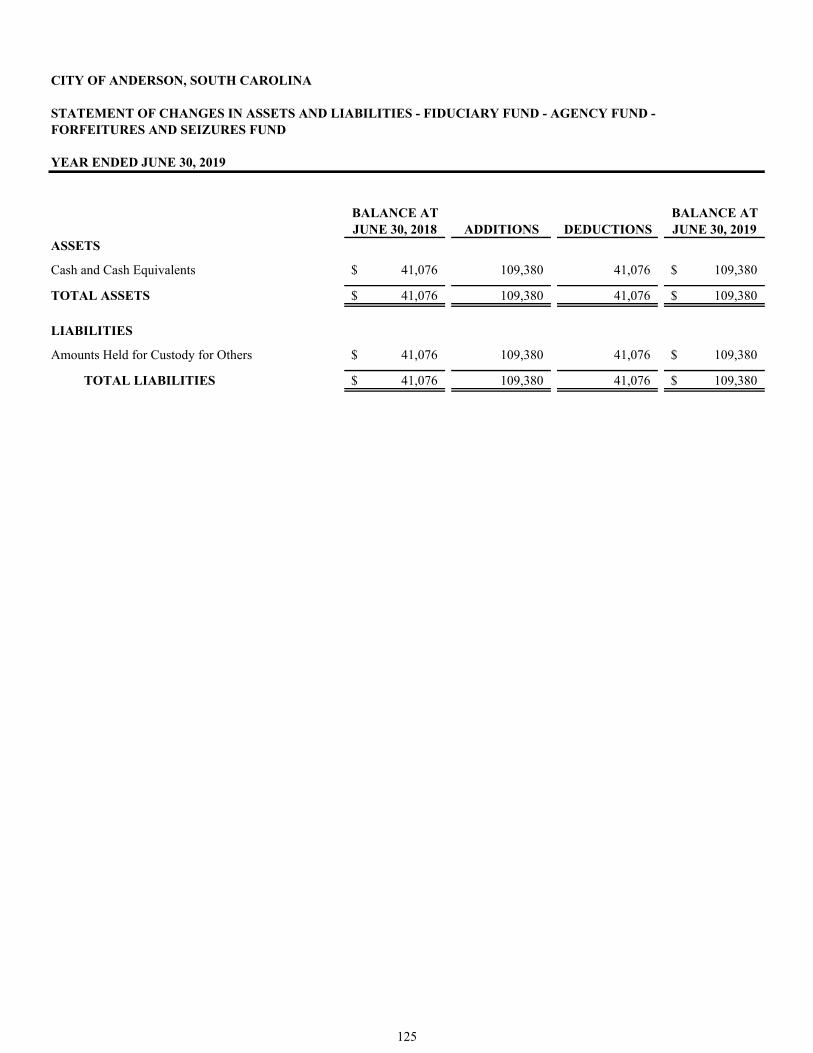

Statement of Changes in Assets and Liabilities - Fiduciary Fund - Agency Fund - Forfeitures and Seizures Fund 125

Other Schedules

Uniform Schedule of Fines, Assessments, and Surcharges (Per Act 96) 127

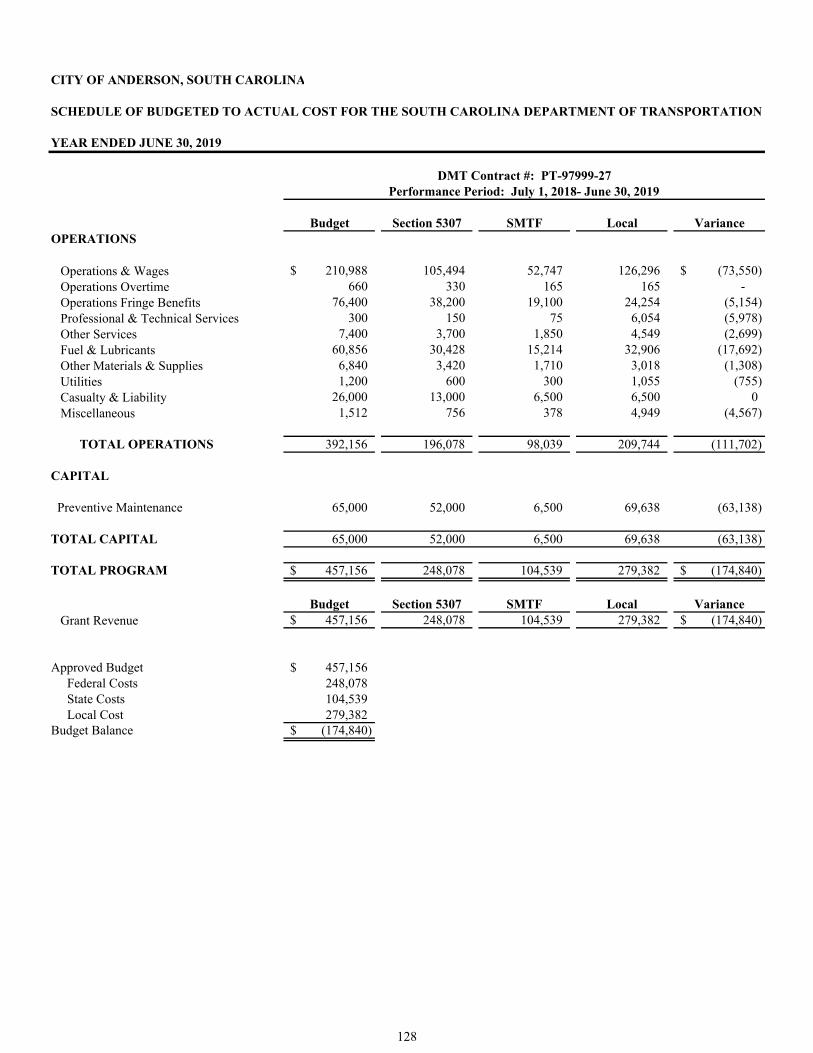

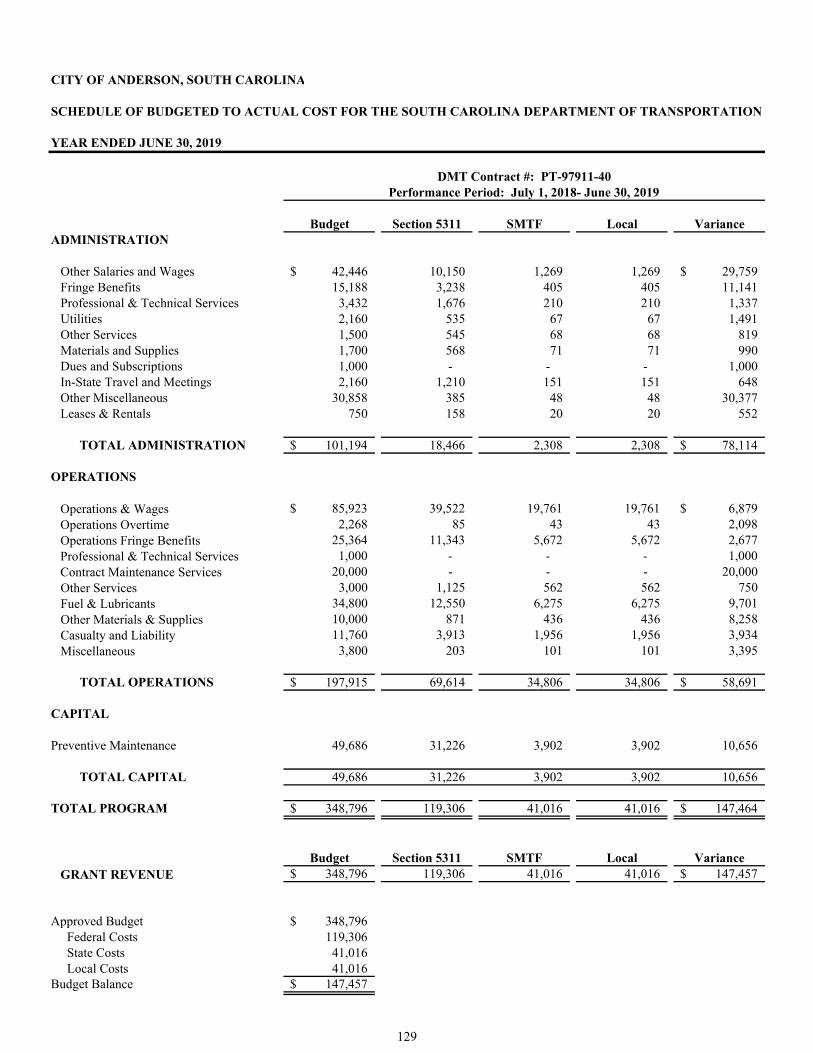

Schedule of Budgeted to Actual Cost for the South Carolina Department of Transportation 128

Financial Trends Information

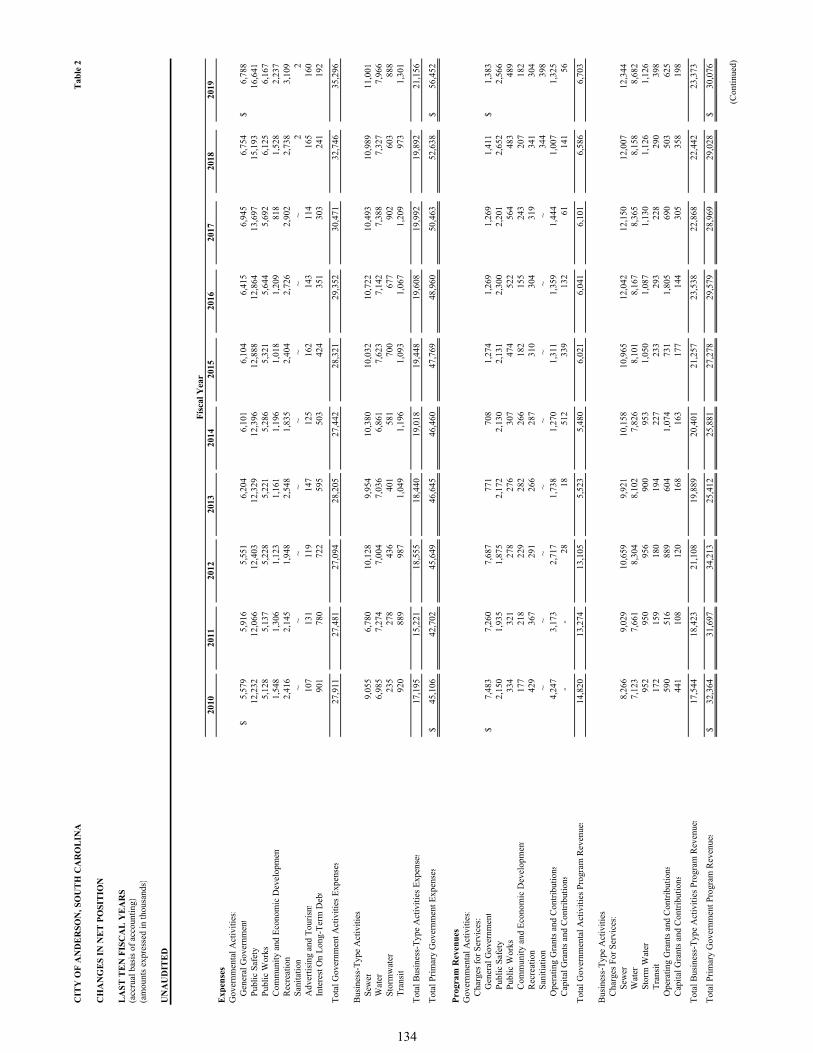

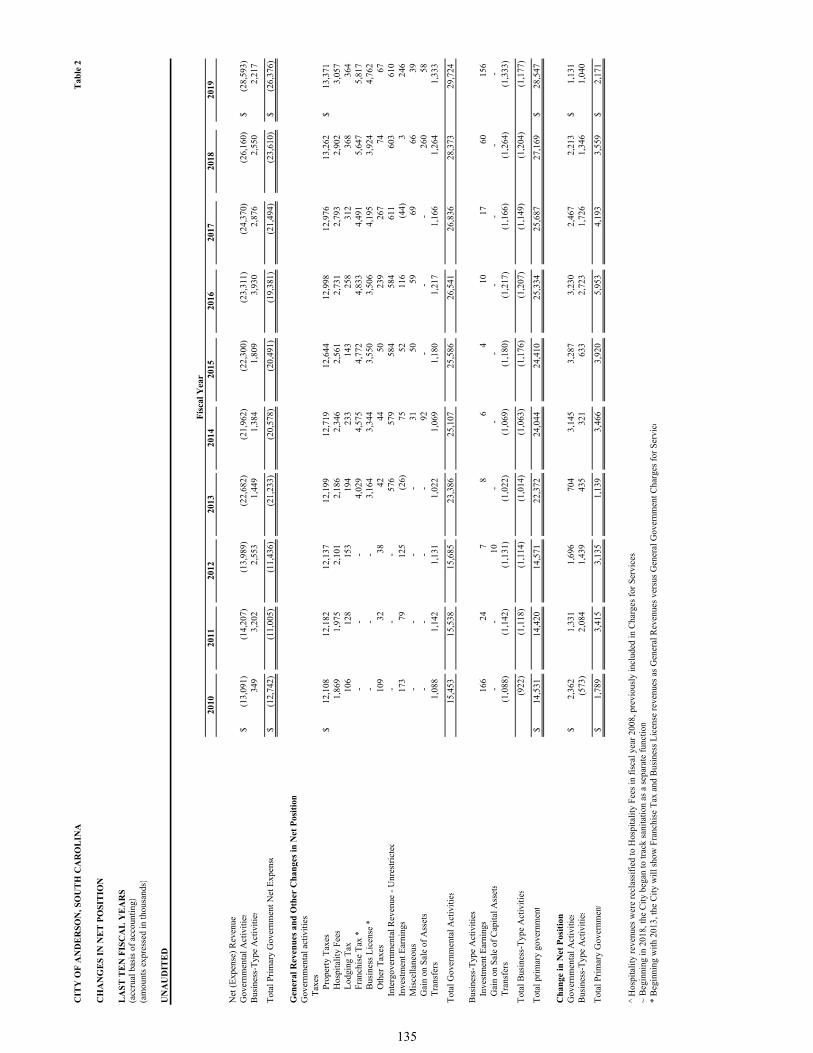

Net Position by Component - Last Ten Fiscal Years - (accrual basis of accounting) 133

Changes in Net Position - Last Ten Fiscal Years - (accrual basis of accounting) 134

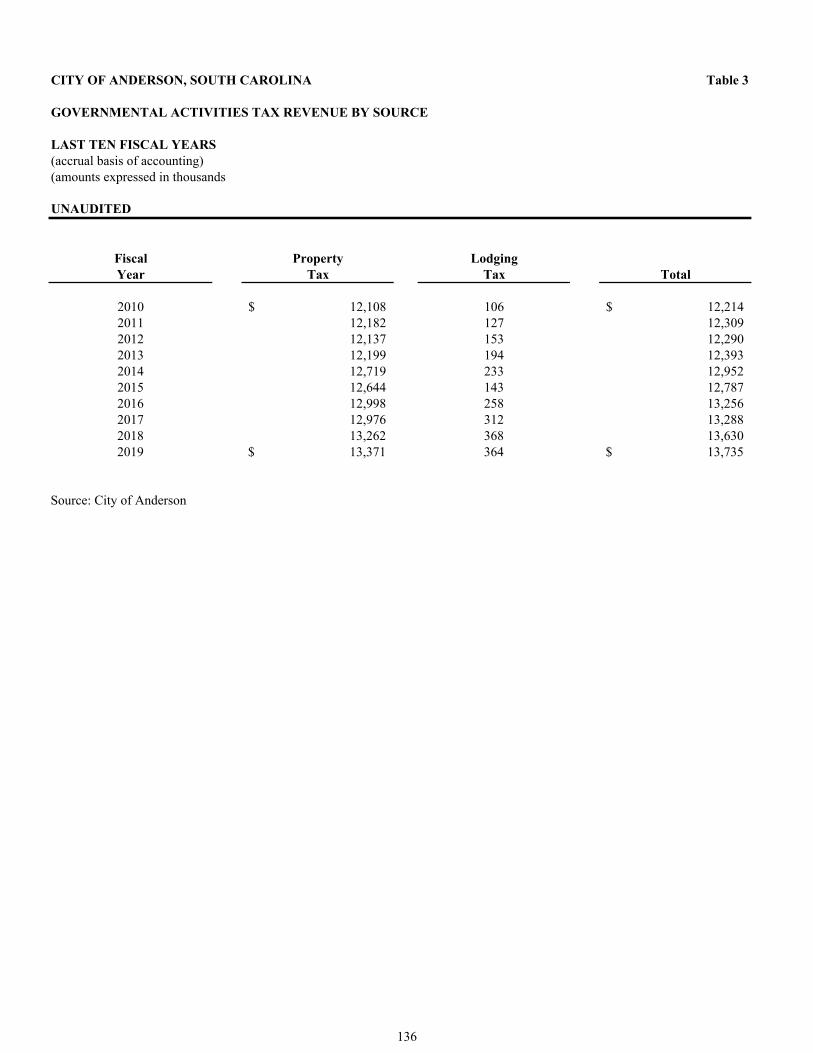

Governmental Activities Tax Revenue by Source - Last Ten Fiscal Years - (accrual basis of accounting) 136

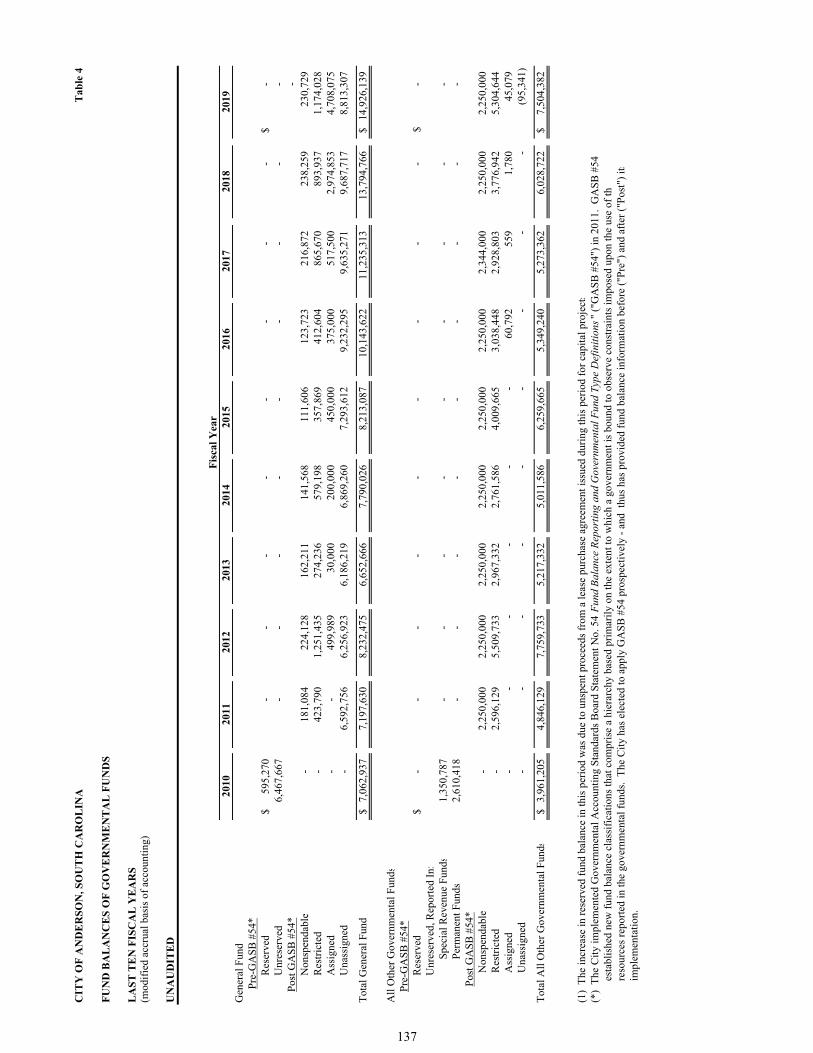

Fund Balances of Governmental Funds - Last Ten Fiscal Years - (modified accrual basis of accounting) 137

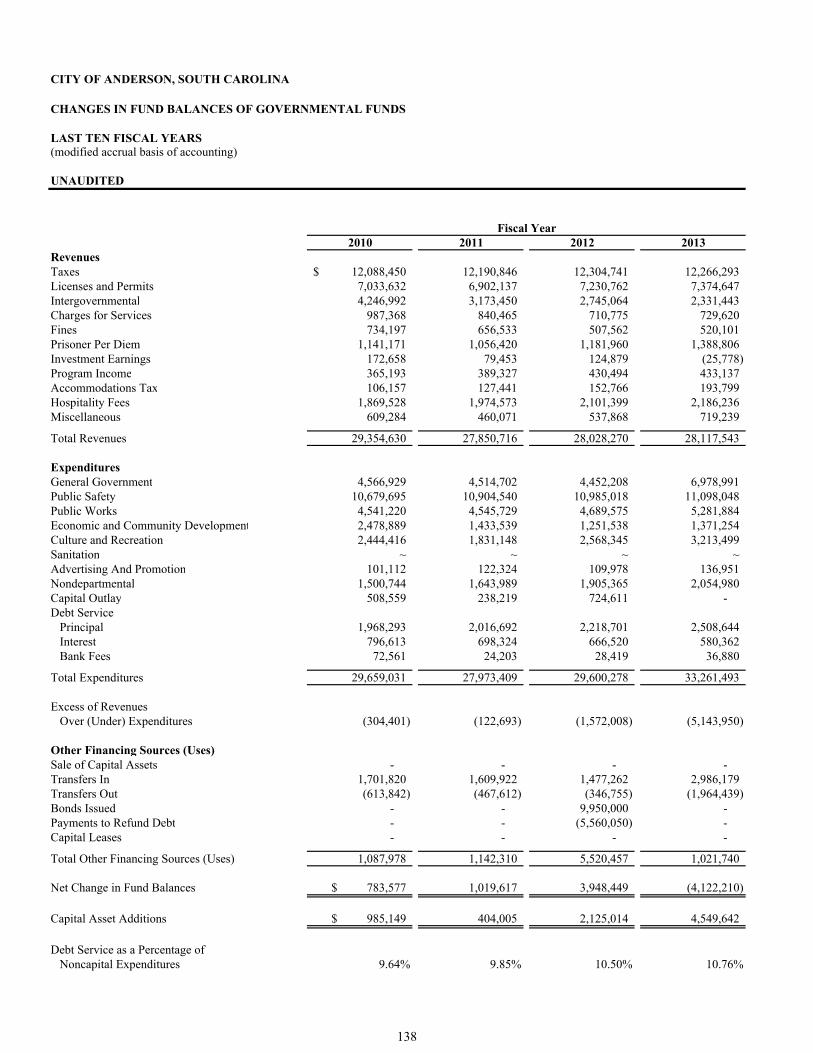

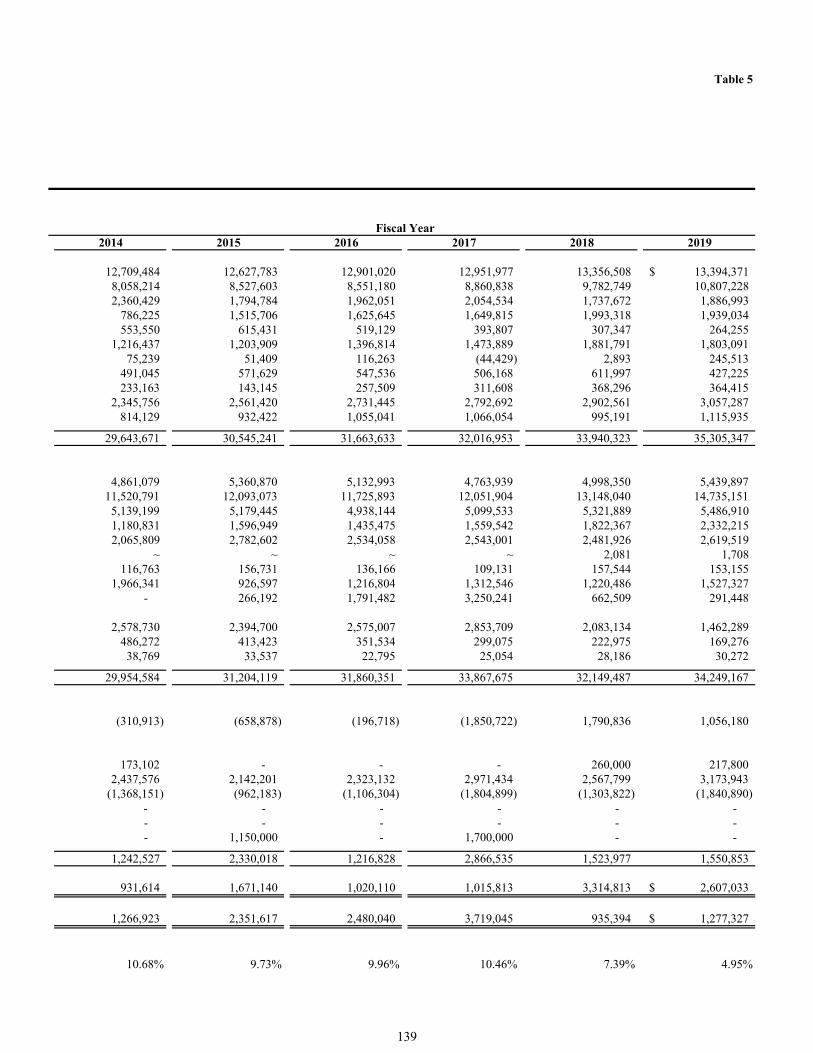

Changes in Fund Balances of Governmental Funds - Last Ten Fiscal Years - (modified accrual basis of accounting) 138

Revenue Capacity Information

Assessed Value and Estimated Actual Value of Taxable Property - Last Ten Fiscal Years 140

Property Tax Rates - Direct and Overlapping Governments - Last Ten Fiscal Years 141

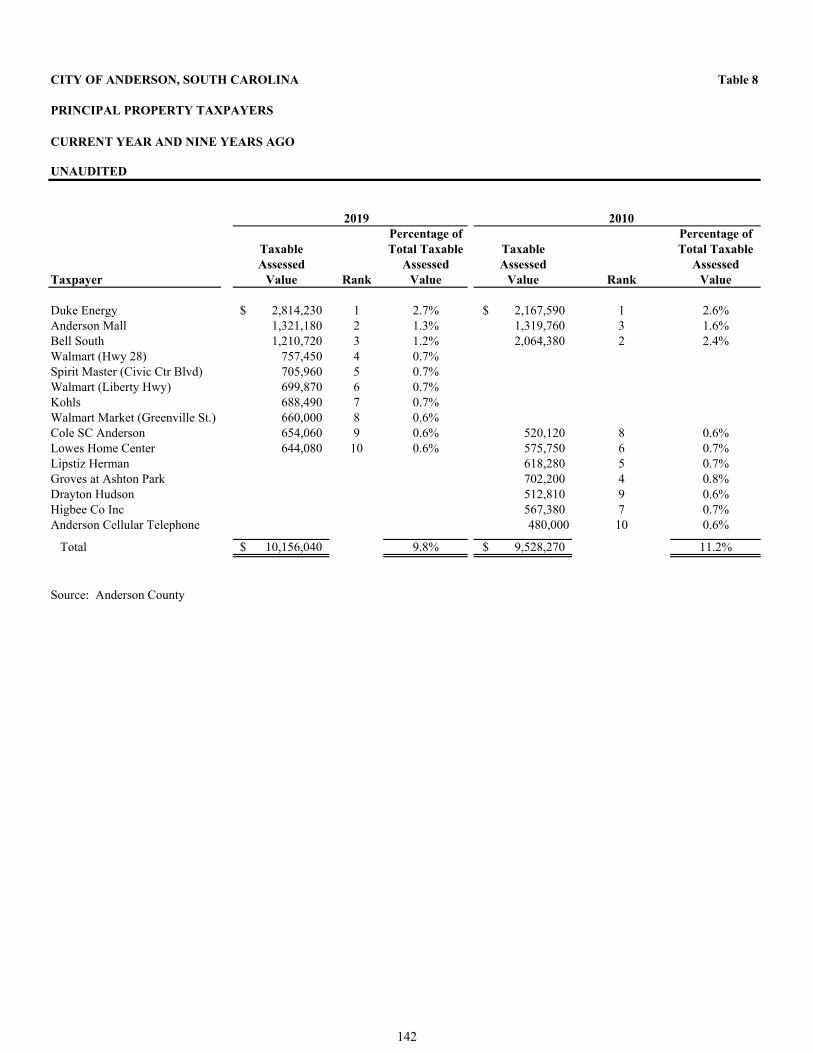

Principal Property Taxpayers - Current Year and Nine Years Ago 142

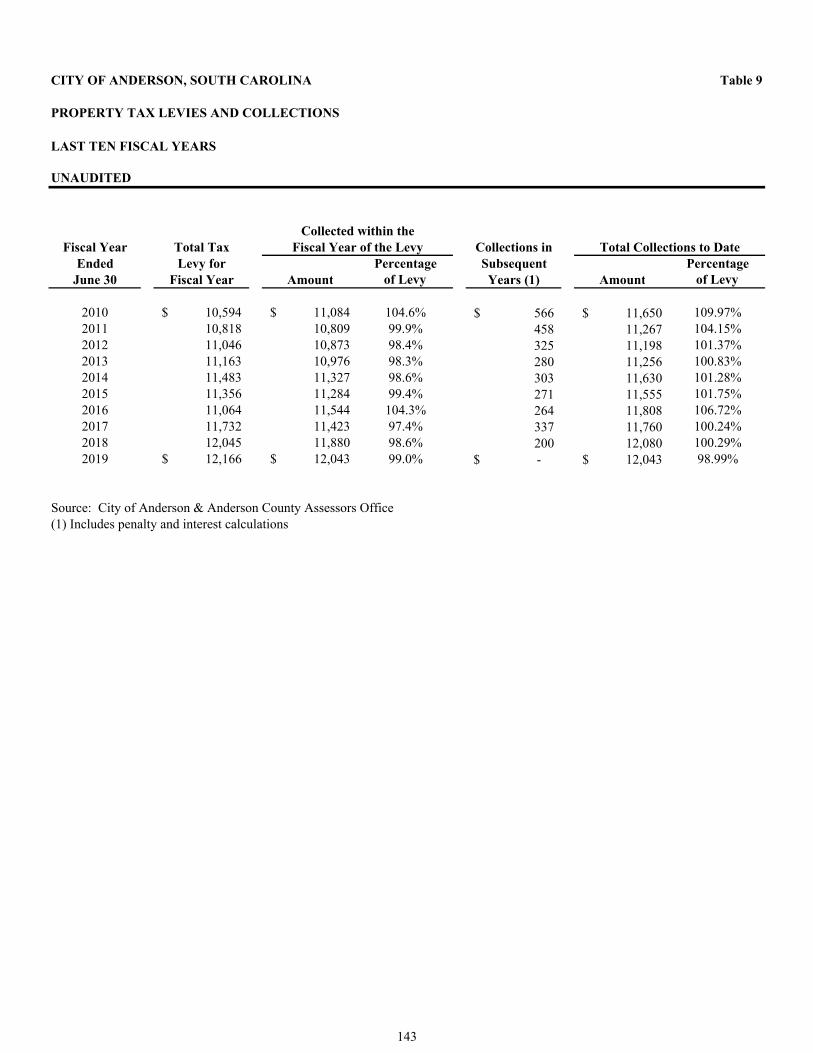

Property Tax Levies and Collections - Last Ten Fiscal Years 143

Debt Capacity Information

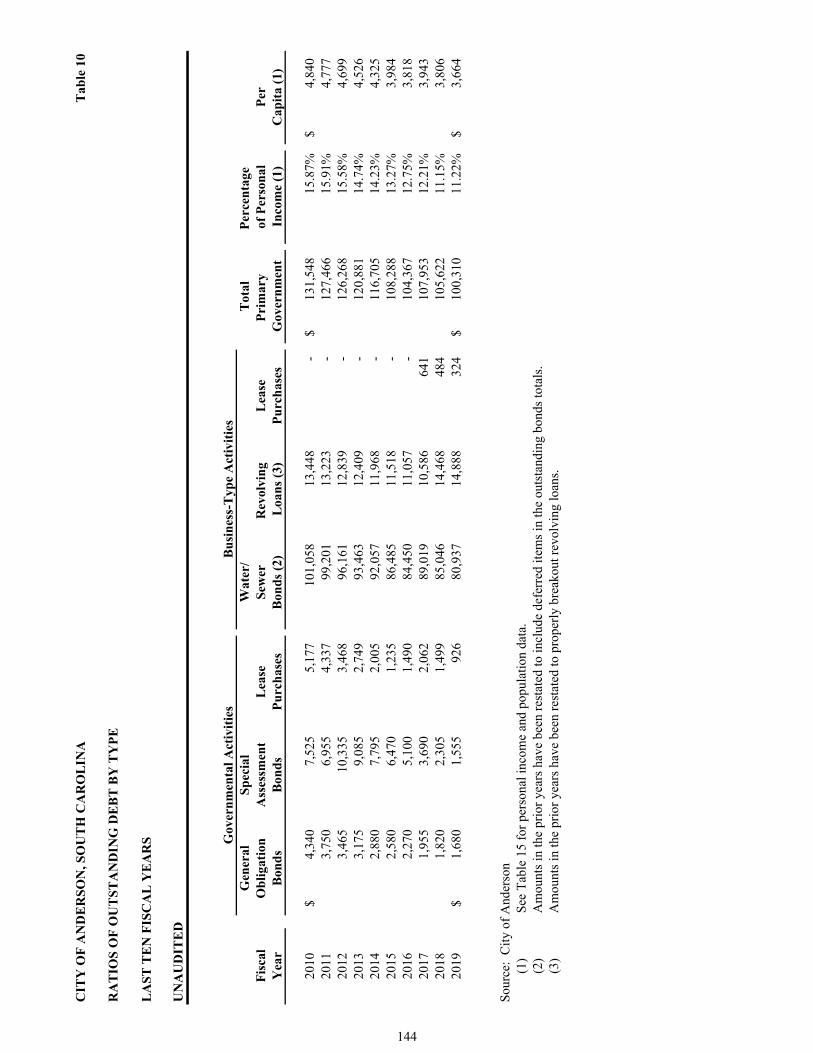

Ratios of Outstanding Debt by Type - Last Ten Fiscal Years 144

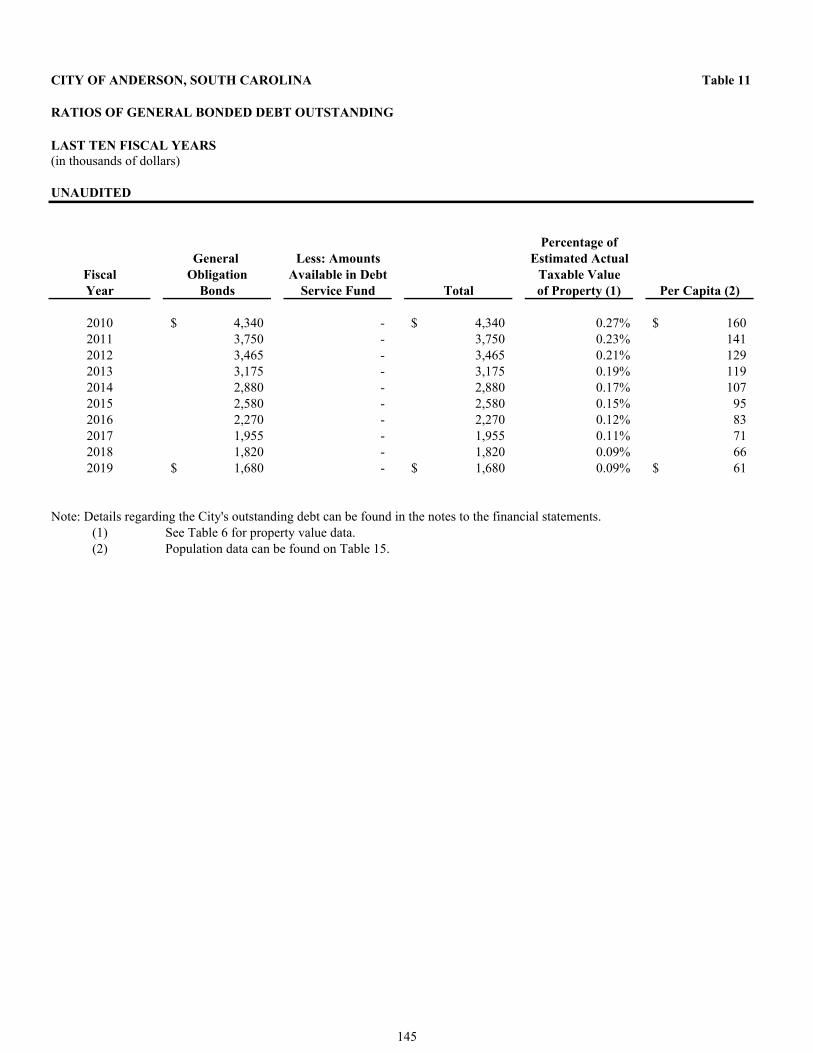

Ratios of General Bonded Debt Outstanding - Last Ten Fiscal Years 145

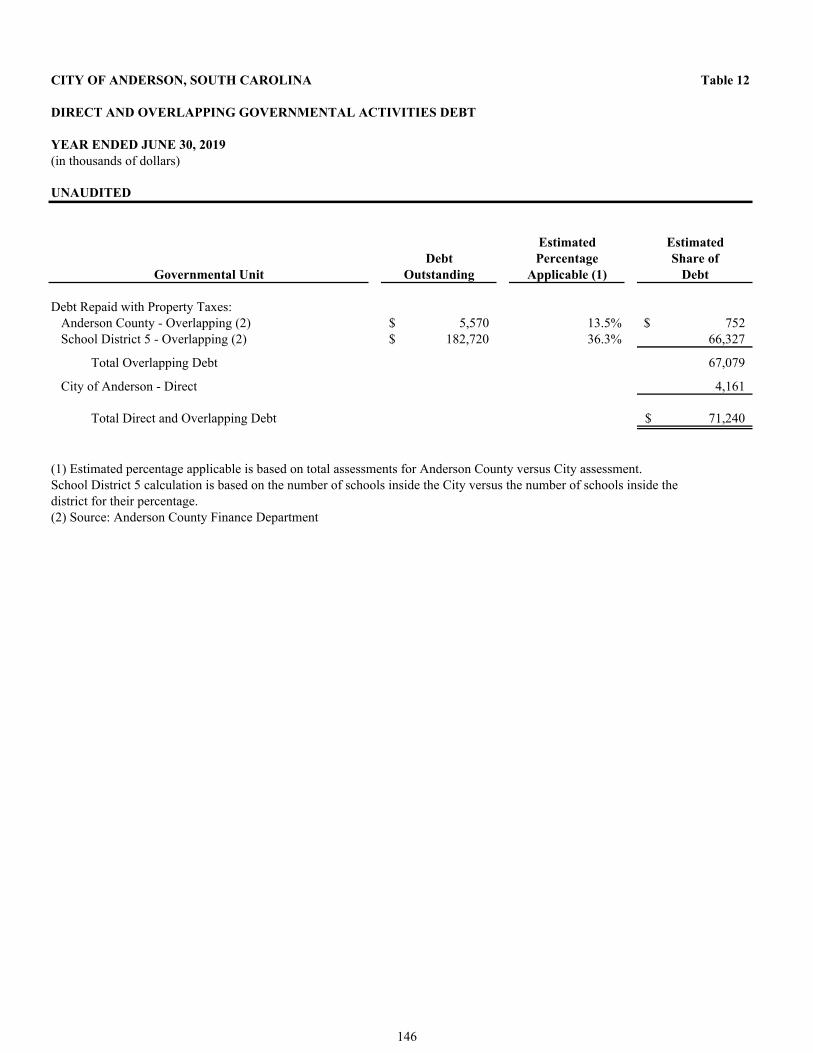

Direct and Overlapping Governmental Activities Debt - As of June 30, 2019 146

Legal Debt Margin Information - Last Ten Fiscal Years 147

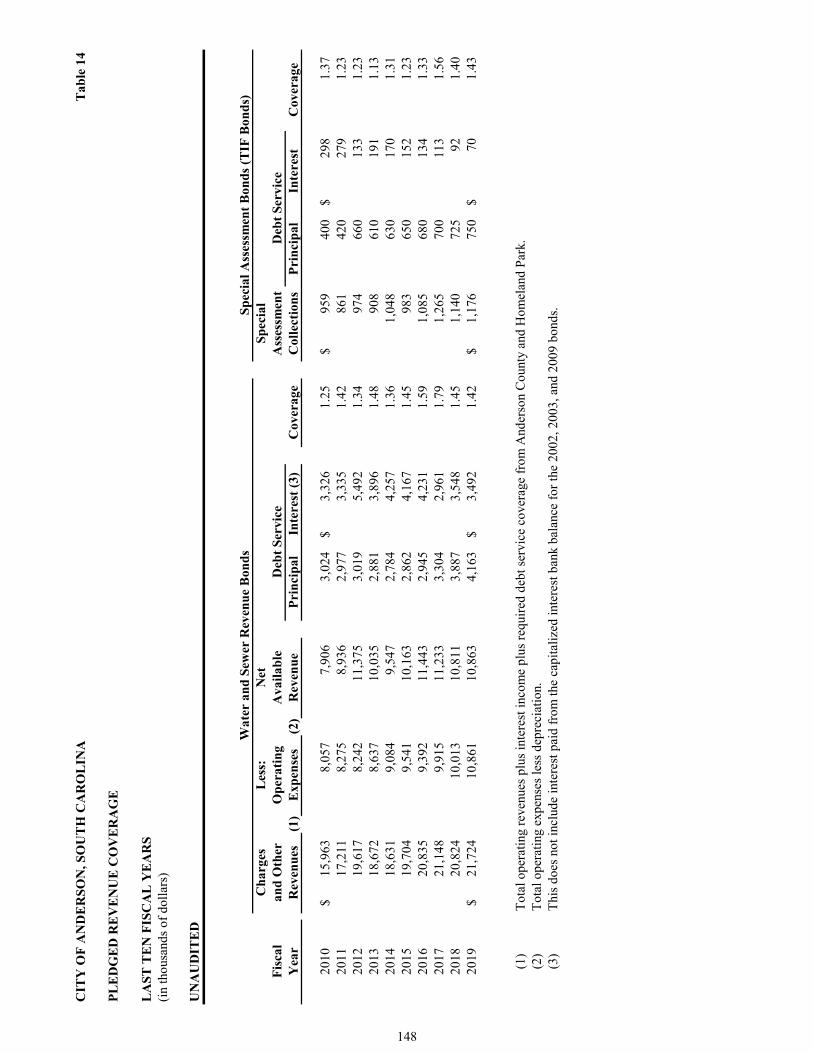

Pledged Revenue Coverage - Last Ten Fiscal Years 148

Demographic and Economic Information

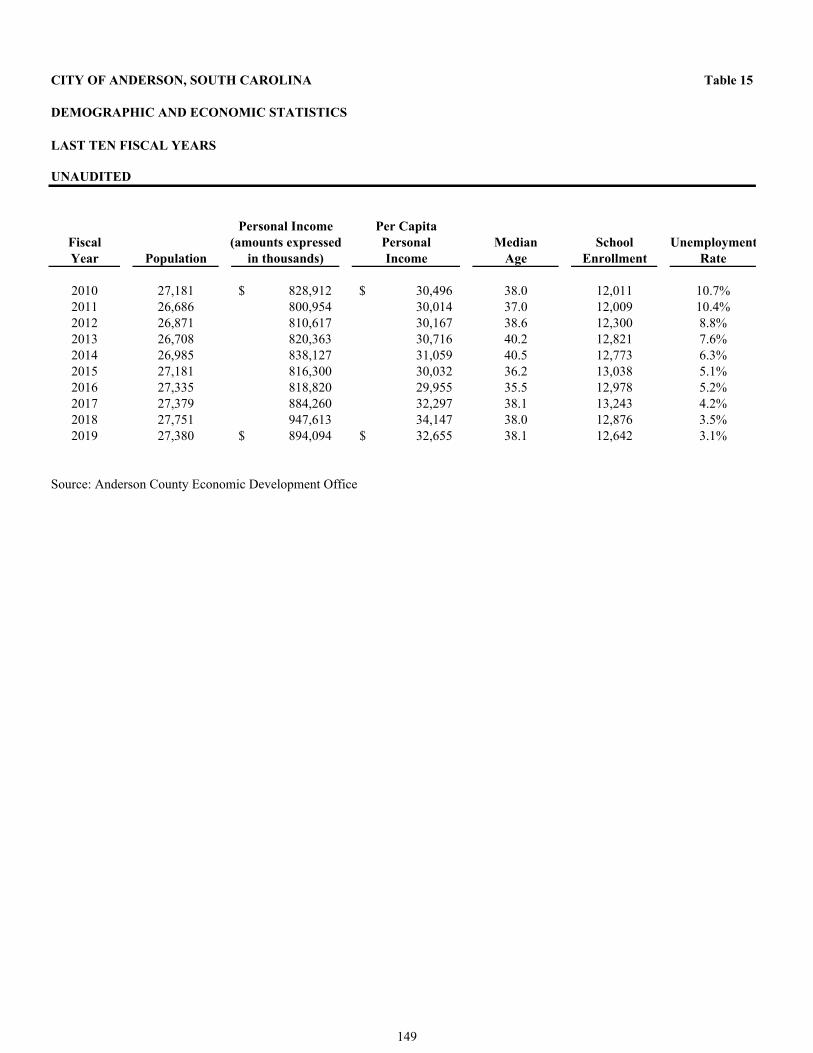

Demographic and Economic Statistics - Last Ten Fiscal Years 149

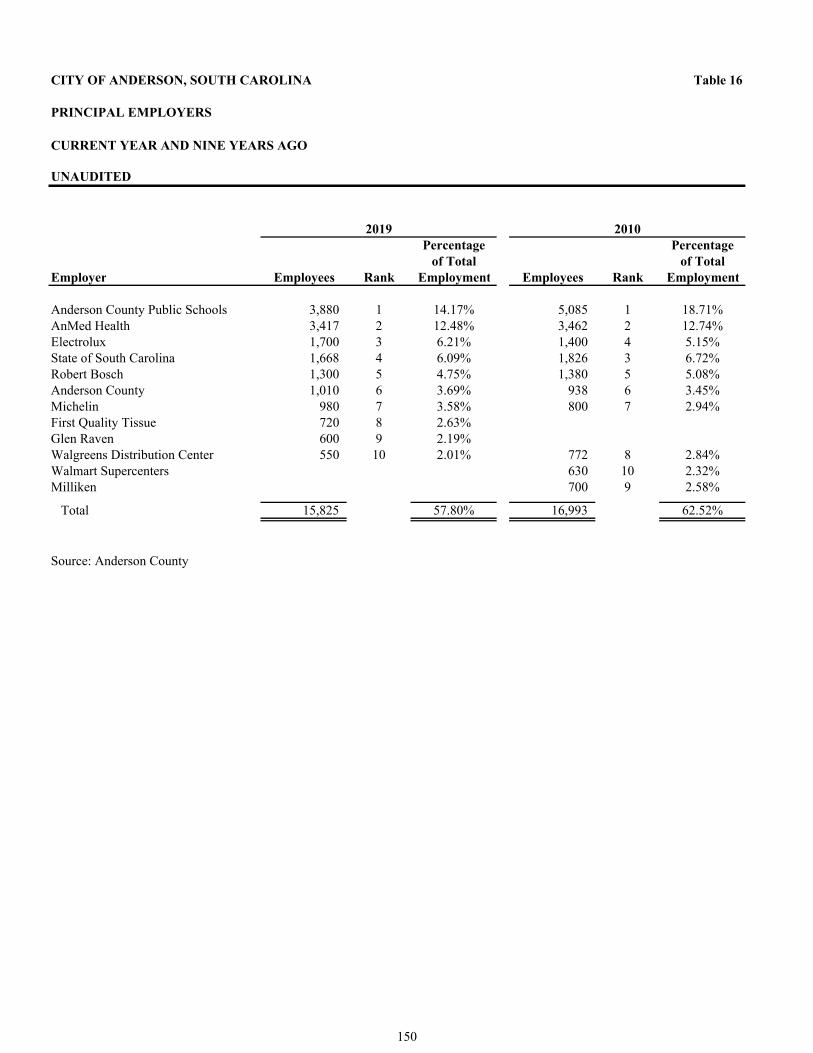

Principal Employers - Current Year and Nine Years Ago 150

Operating Information

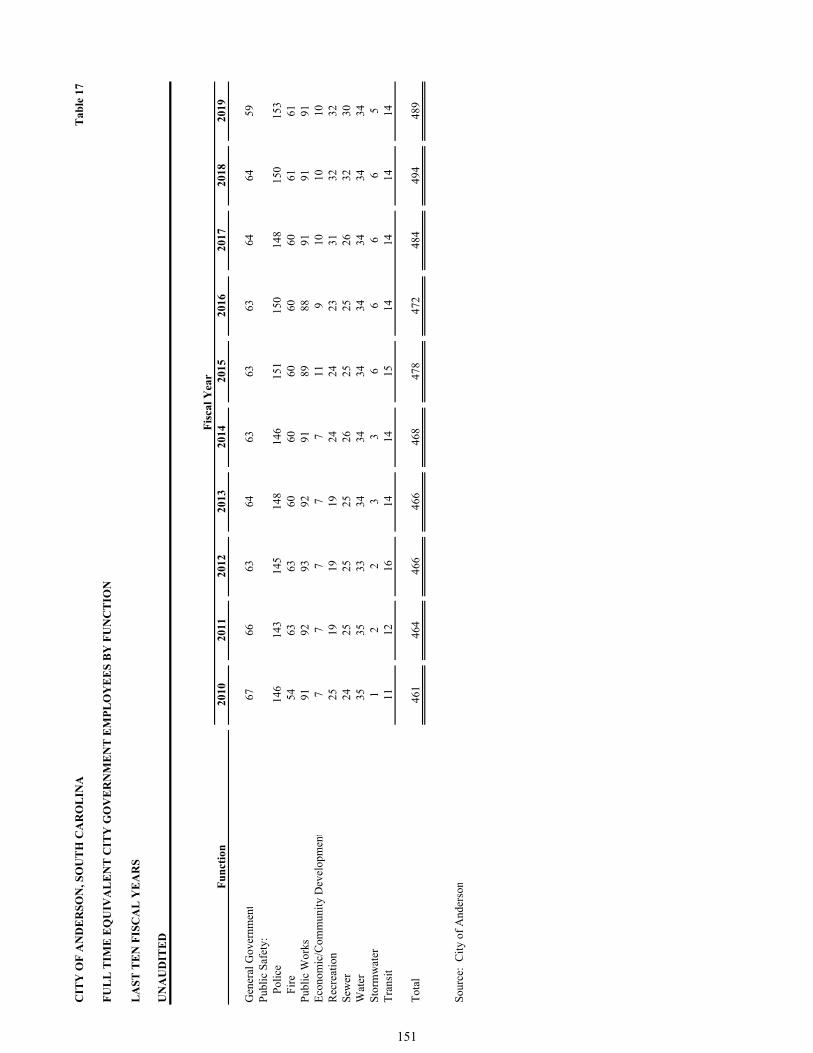

Full-Time Equivalent City Government Employees by Function - Last Ten Fiscal Years 151

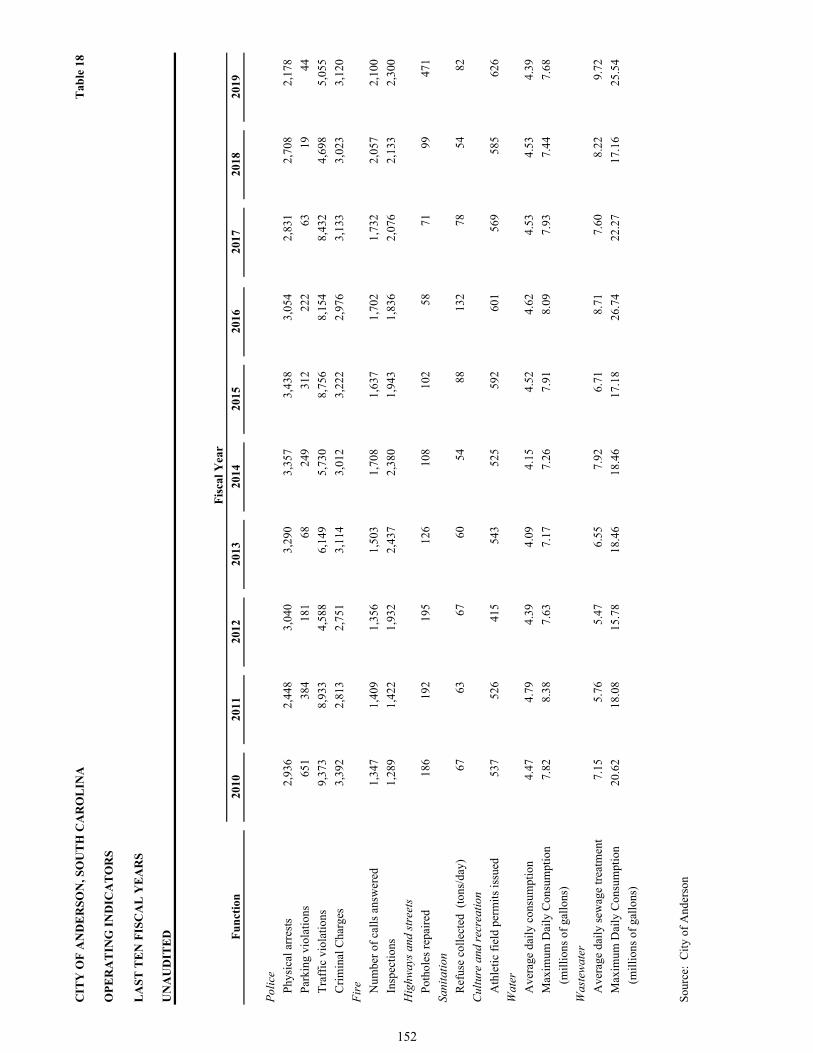

Operating Indicators - Last Ten Fiscal Years 152

Capital Asset Statistics - Last Ten Fiscal Years 153

STATISTICAL SECTION (UNAUDITED)

FINANCIAL SECTION (CONTINUED)

Supplementary Information (Continued)

(Continued)

iii

CITY OF ANDERSON, SOUTH CAROLINA

TABLE OF CONTENTS

YEAR ENDED JUNE 30, 2019

Page Number

Schedule of Expenditures of Federal Awards 155

Notes to the Schedule of Expenditures of Federal Awards 156

Independent Auditor's Report - Report on Internal Control Over Financial Reporting and on Compliance and Other MattersBased on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards 157

Independent Auditor's Report - Report on Compliance for Each Major Federal Program and Report on InternalControl Over Compliance Required by the Uniform Guidance 159

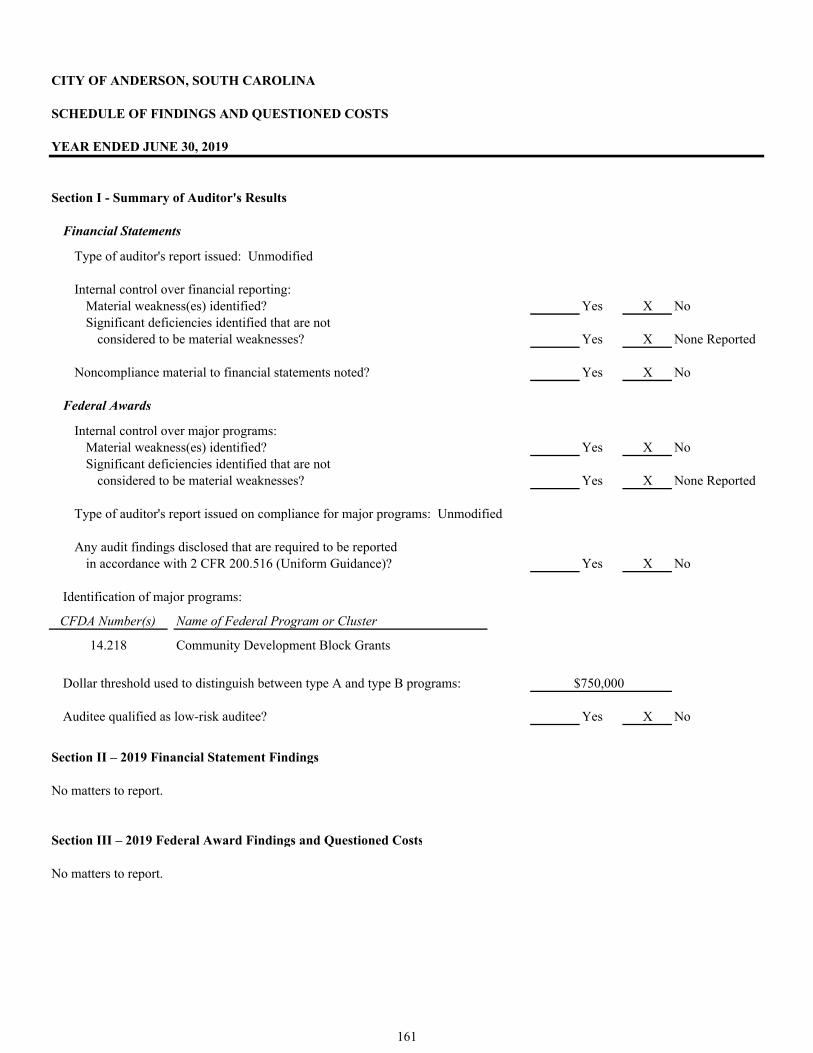

Schedule of Findings and Questioned Costs 161

Summary Schedule of Prior Audit Findings 162

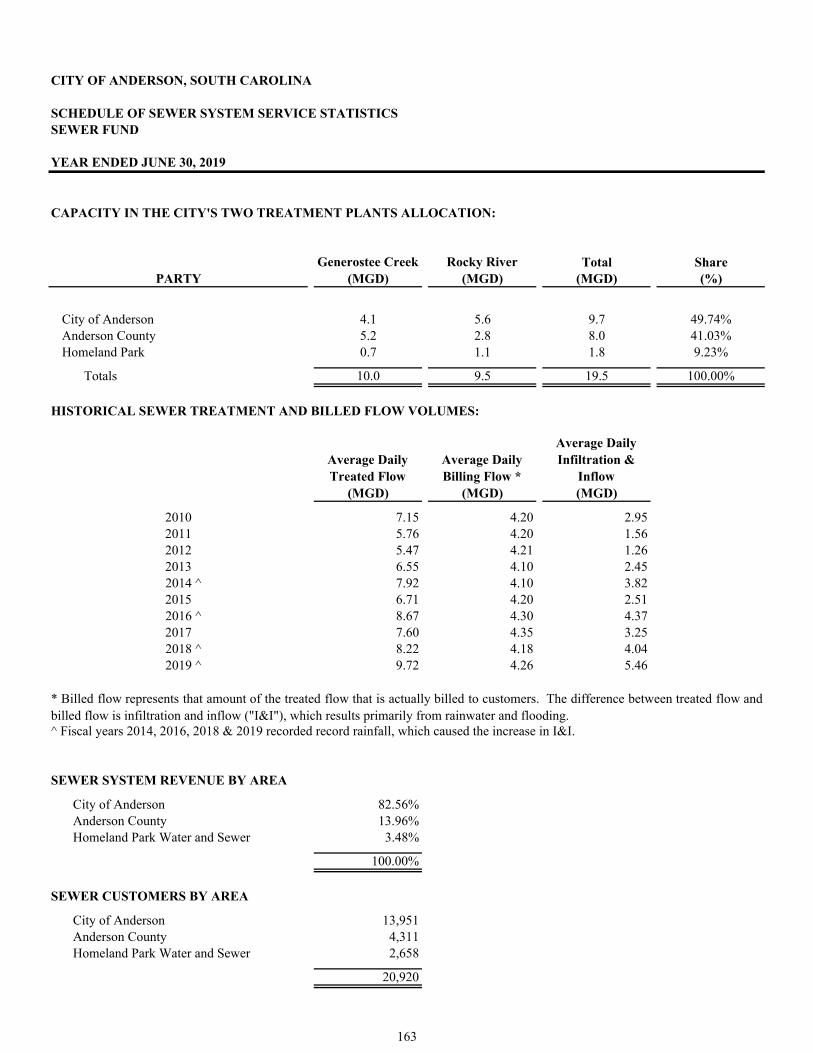

Schedule of Sewer System Service Statistics - Sewer Fund 163

Schedule of Water Meter Service - Water Fund 164

Schedule of Largest Utility Users - Water and Sewer Funds 165

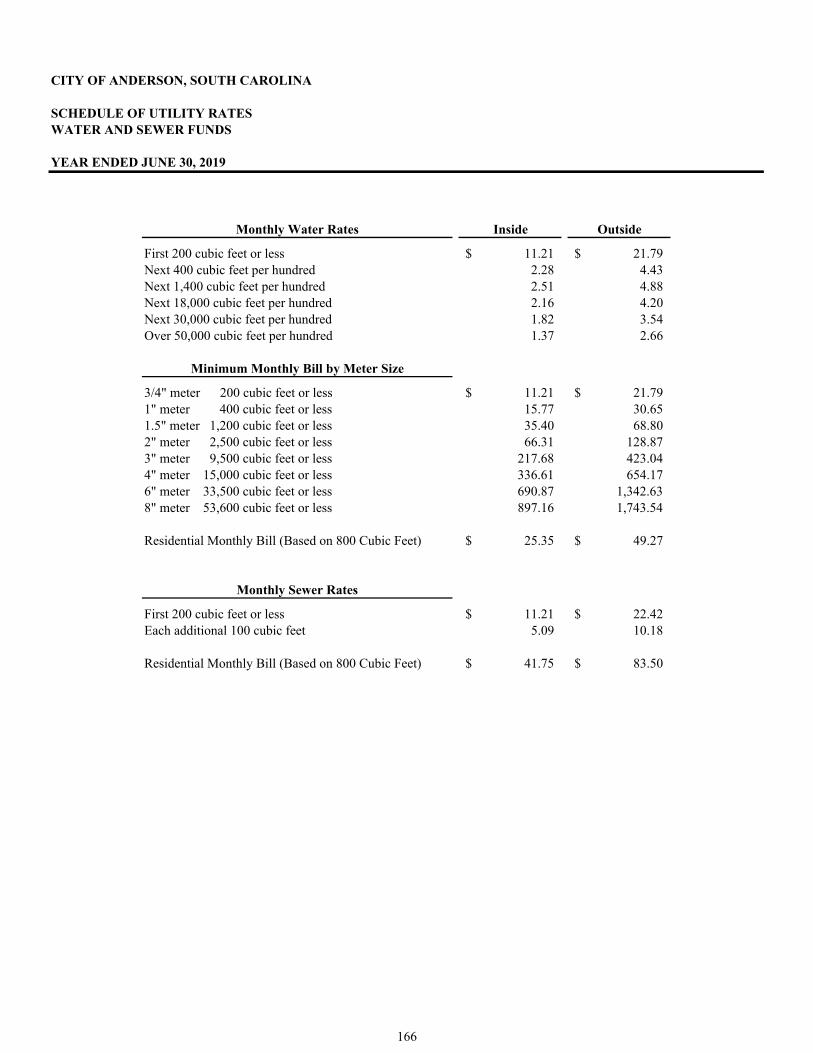

Schedule of Utility Rates - Water and Sewer Funds 166

COMPLIANCE SECTION

CONTINUING DISCLOSURE SECTION (UNAUDITED)

iv

November 22, 2019 The Honorable Mayor Members of City Council City of Anderson, South Carolina Dear Mayor Roberts and City Council Members: State law requires that all general-purpose local governments, at the close of each fiscal year, publish a complete set of financial statements presented in conformity with accounting principles generally accepted in the United States of America (“GAAP”) and audited in accordance with generally accepted auditing standards by a firm of licensed certified public accountants. Pursuant to that requirement, we hereby issue the Comprehensive Annual Financial Report (“CAFR”) of the City of Anderson, South Carolina for the fiscal year ended June 30, 2019. This report consists of management’s representations concerning the finances of the City of Anderson. Consequently, management assumes full responsibility for the completeness and reliability of all of the information presented in this report. To provide a reasonable basis for making these representations, management of the City of Anderson has established a comprehensive internal control framework that is designed both to protect the government’s assets from loss, theft, or misuse and to compile sufficient reliable information for the preparation of the City of Anderson’s financial statements in conformity with GAAP. Because the cost of internal controls should not outweigh their benefits, the City of Anderson’s comprehensive framework of internal controls has been designed to provide reasonable rather than absolute assurance that the financial statements will be free from material misstatement. As management, we assert that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects. The City of Anderson’s financial statements have been audited by Greene Finney, LLP, a firm of licensed public accountants. The goal of the independent audit was to provide reasonable assurance that the financial statements of the City for the fiscal year ending June 30, 2019 are free of material misstatement. The independent audit involved examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; assessing the accounting principles used and significant estimates made by management; and evaluating the overall financial statement presentation. The independent auditor concluded, based upon the audit, that there was a reasonable basis for rendering an unmodified opinion that the City of Anderson’s financial statements for the fiscal year ended June 30, 2019 are fairly presented in conformity with GAAP. The independent auditors’ report is presented in the Financial Section of this report. The independent audit of the financial statements of the City of Anderson was part of a broader, federally mandated “Single Audit” designed to meet the special needs of federal grantor agencies. The standards governing Single Audit engagements require the independent auditor to report not only on the fair presentation of the financial statements, but also on the audited government’s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal awards. These reports are presented in the Compliance Section of the CAFR. GAAP requires that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (“MD&A”). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The City of Anderson’s MD&A can be found in the Financial Section of the CAFR.

1

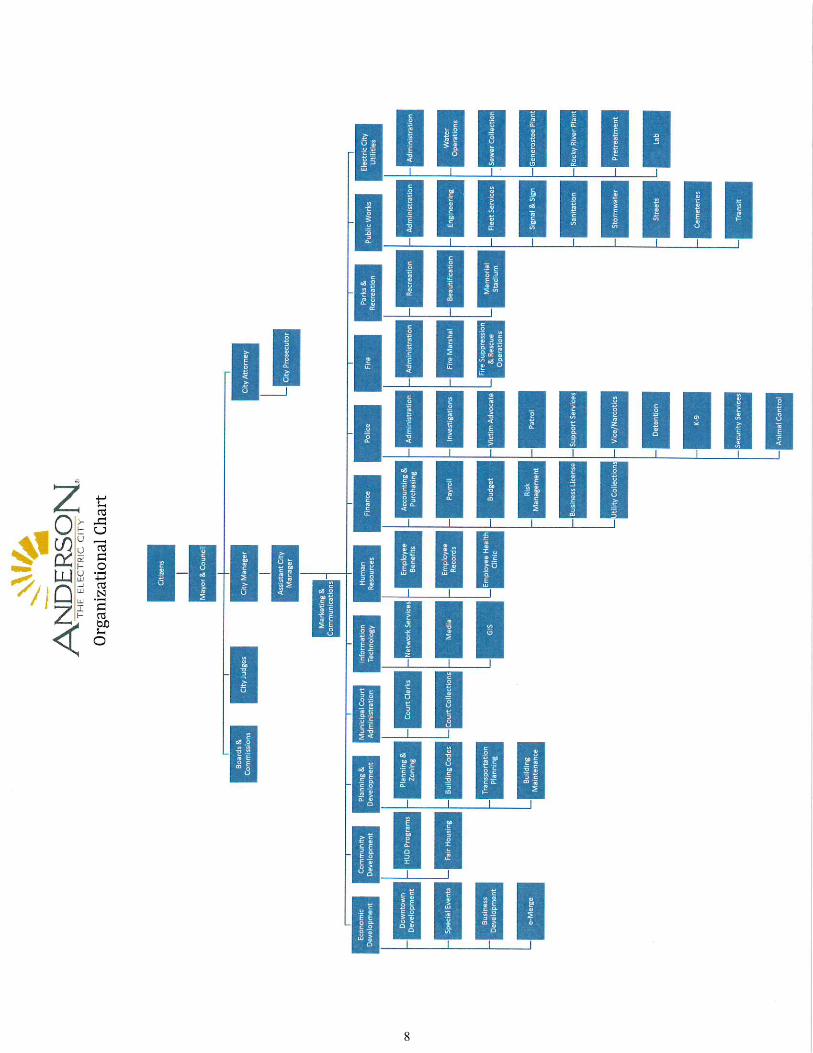

PROFILE Community Profile Anderson was named for General Robert Anderson, a Revolutionary War hero who was born in 1741 in August County, Va. As a young man, he came to South Carolina to help his good friend, Andrew Pickens, in surveying some land that had been given to the English Colony by the Indians. The City was founded in December 1826 and incorporated by an act of Legislature, December 9, 1833. Due to the innovation of engineer William Whitner, Anderson was the first city in the United States to have a continuous supply of electric power. The electricity was supplied by a water mill located in the high shoals area of the Rocky River in Anderson County. Several areas in Anderson are named in honor of William Whitner, including a downtown street. In 1897, the first cotton gin in the world to be operated by electricity was in Anderson County, earning the community the nickname “The Electric City”. City Government Section 47-26 of the 1962 Code of Laws, as amended (Home Rule Act), requires that municipalities adopt a specific form of government. The City operates under Council-Manager form of government. The Council is composed of a Mayor and eight Council members. The Mayor and two Council members are elected at-large and six Council members are elected on a single member ward basis. The Mayor and Council, elected for four-year staggered terms, are vested with the legislative and policymaking powers of the City. The Council appoints a City Manager who serves as the chief executive officer of the City and is responsible to the Council for proper administration of all affairs of the City. Thirteen division heads currently report to the City Manager and are responsible for the following functions: Police, Fire, Public Works, Electric City Utilities, Community Development, City Attorney, Courts, Finance, Human Resources, Information Technology, Economic Development, Planning & Development, and Recreation & Parks. The City operates and maintains various programs which are funded from City revenues, as reflected in its annual budget for fiscal year 2018 - 2019 and provides a full range of services contemplated by statute. These services include the public safety (police and fire) public works; utilities, recreational activities; planning; zoning and community services. Budget Process In accordance with the General Statutes of the State of South Carolina, the City Council is required to adopt an annual balanced budget prior to July 1st. The City uses the adopted budget as a management control device during the year. A balanced budget is achieved when the City is able to equate the revenues with expenditure over the business cycles. The budget process begins in February with a special, comprehensive work session in which the Finance Department and City Manager’s Office meets with all Departments to discuss current and future trends, needs, and goals of the City. During this meeting the budget calendar is reviewed and budget manuals are distributed to each department. These manuals contain a detailed description of the mechanics associated with the budget. Each department then prepares a comprehensive list of objectives and funding requests they would like to have considered for the upcoming budget year. During this time the Finance Department prepares revenue estimates for both the current and upcoming years. Appropriate departments also prepare their own revenue projections for those revenue items affecting their departments. Each department then meets individually with the City Manager’s Office and the Finance Office to review program budgets and expenditure requests. During these meetings, the goals of each department are reviewed and expenditure requests are evaluated to determine the fiscal resources necessary to accomplish these goals. Following these meetings, the City Manager’s Office and the Finance Department meet to prepare a draft budget for submission to City Council. This draft budget is submitted to Council at formal budget workshops held in May and June. The public has an opportunity to comment on the budget at a designated public hearing. A public hearing and two readings are required for formal adoption of the budget. Amendments to the budget are allowable under South Carolina law and are made throughout the year as necessary.

2

FACTORS AFFECTING ECONOMIC CONDITION Local Economy The City of Anderson is located in the northwest corner of the state of South Carolina on the Piedmont Plateau. The City of Anderson is the county seat and the largest municipality in the county with a population of approximately 27,500. The City is ideally located on the busy Interstate 85 corridor, to which much of its economic growth can be attributed. Anderson County, South Carolina lies midway between Atlanta, Georgia and Charlotte, North Carolina on the I-85 corridor, which is one of the nation’s hottest growth areas and one of the heaviest traveled highways in the southeast. Business leaders and development officials in Anderson have taken advantage of this asset, and visible progress is the result. Anderson is a major contributor to the success of the upstate. Anderson offers all of the basics upon which to build a thriving economy, including affordable land, a good transportation system, infrastructure, and a large number of recreational amenities. The Anderson community offers the feel of small-town living with the attractions and business opportunities of larger cities only a short drive away. The City encompasses approximately 15.3 square miles. Long-Term Financial Planning The City of Anderson each year presents detailed strategies for implementing annual goals. Many of these goals progress a great deal during the year, while others require more time. Both the goals and strategies are indicative of the City’s Mission Statement and our visions for the future.

Continue to improve and enhance our neighborhoods o Continue to reduce substandard housing through demolition and clearance; increase new housing

opportunities by rebuilding and partnering with residents, businesses, and other entities; boost beautification efforts through enhanced neighborhood gateways for visual appeal and safety.

o Develop sustainable programs that can be replicated throughout our neighborhoods, and encourage the engagement of neighborhood residents to work together and regroup to achieve an improved sense of livability.

o Improving the local economy by awarding business loans to small businesses and microenterprises located in a redevelopment area or Central Business District.

Continue our downtown revitalization efforts

o Increase our emphasis on assistance and incentives that encourage private investment, and increase the growth of the Tax Increment Financing district for continued public infrastructure investment.

o Expand the focus and reach of the downtown master plan by fine-tuning the elements that compliment development i.e. wayfinding, maintenance, partnerships, marketing, promotion, etc.

o Continue efforts to promote expansion of residential, retail, and other economic development as well as the amenities to compliment them.

Strengthen our recreation and parks programs and tourism opportunities

o Focus on comprehensive recreation, parks and tourism development through collaboration. o Maximize the positive impact of the Recreation Center on the community, and generate opportunities to

promote active and healthy lifestyles.

Communicate the importance and value of basic City services, with specific attention to equity - the need for all receiving services to pay their equitable portion with a plan fair to all.

Continue the City’s communications program allowing the City to tell its story through our communications tool kit

including ECTV-14, website (www.cityofandersonsc.com), focused marketing, etc. geared toward retreat issues, major projects and timely subjects.

Drive the culture change that promotes efficiency, innovation, effectiveness, and equitable value.

3

Focus and engage the management team to develop methods and actions that advance the priorities in a strategic and comprehensive manner through leadership development, cross-departmental collaboration, benchmarking, etc. Many of these goals represent multi-year tasks and strategies. Many are process-oriented rather than project-oriented. Most all of them involve the planned expenditure of budgeted funds. Others require seeking alternative resources. Because of this, the City will continue to seek new opportunities relative to funding municipal government. Financial Policies The Statement of Financial Policies presents policies that the City follows in managing its financial and budgetary affairs. Operating Budget Policies

Essential City services will receive first priority. For the purpose of this policy, these services are those that protect lives and property.

The City will avoid budgetary procedures that balance current expenditures by obligating future year funds. The City will maintain its physical assets at a level adequate to protect the City’s capital investment and to minimize

future maintenance and replacement costs. Revenue Policies

The City will try to maintain a diversified and stable revenue system. The City will follow an aggressive policy of collecting revenues. The City will consider market rates and rates charged by other municipalities of similar size for charges for services. Enterprise funds will be self-supporting.

Investment Policies

The City’s investment portfolio will be diversified to avoid incurring unreasonable risks. The City will obtain the best possible return on all investments within the limits of State law, local ordinances and

prudent investment practices. The Finance Director will receive a monthly investment report outlining the nature, value, yield, purchase price and

any other pertinent information. Accounting, Auditing and Financial Reporting Policies

An independent audit will be performed annually. The City will issue annual financial reports in accordance with generally accepted accounting principles (GAAP) as

outlined by the Governmental Accounting, Auditing, and Financial Reporting (GAAFR) book. Reserved and Unreserved Fund Balance Policies

The City seeks to maintain a prudent level of financial resources to protect against reducing levels of service because of temporary shortfalls or unpredicted one-time expenditures.

Major Initiatives For the fifteenth straight year, the Mayor, City Council and Division Heads participated in a planning retreat. This retreat helped identify the major issues facing the City. City Council and management want to ensure that the residents in the City of Anderson are provided the most efficient and effective services at the most affordable costs. AWARDS AND ACKNOWLEDGEMENTS Awards The Government Finance Officers Association of the United States and Canada (“GFOA”) awarded a Certificate of Achievement for Excellence in Financial Reporting to The City of Anderson, South Carolina for its comprehensive annual financial report for the fiscal year ended June 30, 2018. The Certificate of Achievement is a prestigious national award recognizing conformance with the highest standards for preparation of state and local government financial reports. The City of Anderson has received this award for twenty-four consecutive years.

4

In order to be awarded a Certificate of Achievement, a government unit must publish an easily readable and efficiently organized comprehensive annual financial report, whose contents conform to program standards. Such CAFR must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe our current report continues to conform to the Certificate of Achievement program requirements and we are submitting it to GFOA. The City of Anderson also received the Certificate for Excellence in Distinguished Budget Presentation from the Government Finance Officers Association of the United States and Canada for our Annual Adopted Budget for the fiscal year ended June 30, 2019. The City has received this award for thirteen years. The FY 2020 budget has been submitted for consideration of this award. Acknowledgments We appreciate the support of the Mayor and Council by encouraging excellence in financial reporting through participation in the Certificate of Achievement for Excellence in Financial Reporting Program of the Government Finance Officers Association. The preparation of the Comprehensive Annual Financial Report was made possible by the hard work of the Finance Division. Each division member has our sincere appreciation for the contributions made in the preparation of this report. Respectfully Submitted, David E. McCuen IV Margot B. Martin City Manager Finance Director

5

This page is intentionally left blank

6

CITY OF ANDERSON, SOUTH CAROLINALIST OF PRINCIPAL OFFICIALS AND MANAGEMENT TEAM

FOR FISCAL YEAR 2019-2020

MAYOR Terence V. Roberts

MAYOR PRO-TEM James A. Stewart/Seat 4

COUNCILMEMBER SEAT 1 Kyle L. Newton

COUNCILMEMBER SEAT 2 Donald G. Chapman

COUNCILMEMBER SEAT 3 Jeffrey D. Roberts

COUNCILMEMBER SEAT 5 Beatrice R. Thompson

COUNCILMEMBER SEAT 6 Richard A. Laughridge

COUNCILMEMBER AT-LARGE SEAT 8

John M. Roberts

COUNCILMEMBER AT-LARGE SEAT 7

Matthew C. Harbin

CITY MANAGER David E. McCuen, IV

ASSISTANT CITY MANAGER Andrew C. Strickland

FINANCE DIRECTOR Margot B. Martin

CITY ATTORNEY J. Franklin McClain

POLICE CHIEF James S. Stewart

FIRE CHIEF Randall K. Bratcher

PLANNING & DEVELOPMENT DIRECTOR Maurice L. McKenzie

PUBLIC WORKS DIRECTOR Kenneth M. Mullinax

UTILITIES DIRECTOR Jeffrey H. Caldwell

PARKS & RECREATION DIRECTOR Robert G. Beville

INFORMATION TECHNOLOGY DIRECTOR Mark L. Cunningham

COMMUNITY DEVELOPMENT DIRECTORErica M. Craft

HUMAN RESOURCE DIRECTORDonna M. Kazia

ECONOMIC DEVELOPMENT DIRECTORKimberly H. Spears

MUNICIPAL COURT ADMINISTRATORKimberly A. Poulin

7

8

9

This page is intentionally left blank

10

INDEPENDENT AUDITOR’S REPORT The Honorable Mayor and Members of City Council City of Anderson Anderson, South Carolina Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Anderson, South Carolina (the “City”), as of and for the year ended June 30, 2019, and the related notes to the financial statements, which collectively comprise the City’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Anderson, South Carolina, as of June 30, 2019, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

11

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that management’s discussion and analysis, the budgetary comparison schedule, the other postemployment benefit plan schedule, and the pension plan schedules, as listed in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Supplementary and Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City’s basic financial statements. The introductory section, supplementary information, statistical section, the schedule of expenditures of federal awards, as required by Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, and the continuing disclosure section, as listed in the table of contents, are presented for purposes of additional analysis and are not a required part of the basic financial statements.

The supplementary information and the schedule of expenditures of federal awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the supplementary information and the schedule of expenditures of federal awards are fairly stated, in all material respects, in relation to the basic financial statements as a whole.

The introductory section, statistical section, and the continuing disclosure section have not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated November 22, 2019 on our consideration of the City’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the City’s internal control over financial reporting and compliance.

Greene Finney, LLP Mauldin, South Carolina November 22, 2019

12

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

As management of the City of Anderson (“City”), we offer readers of the City’s financial statements this narrative overview and analysis of the financial activities of the City for the year ended June 30, 2019 (“FY 2019” or “2019”) compared to the year ended June 30, 2018 (“FY 2018” or “2018”). The intent of this management’s discussion and analysis (“MD&A”) is to look at the City’s financial performance as a whole. We would encourage readers to not only consider the information presented here, but also the information provided in the transmittal letter, the financial statements, and notes to the financial statements to enhance their understanding of the City’s overall financial performance. FINANCIAL HIGHLIGHTS

The assets and deferred outflows of resources of the City exceeded its liabilities and its deferred inflows of resources at the close of the current year by approximately $87,841,000 (net position). Of this amount, approximately $45,178,000 and $42,663,000 were related to the City’s governmental and business-type activities, respectively. In addition, the City’s unrestricted net position (which may be used to meet the government’s ongoing obligations to citizens and creditors) was approximately $801,000 for its governmental activities and approximately $10,381,000 for its business-type activities.

The government’s total net position increased by approximately $1,131,000 for governmental activities and approximately $1,039,000 for business-type activities compared to the prior year net position.

As of the close of the current fiscal year, the City’s governmental funds reported combined ending fund balances of approximately $22,431,000, an increase of approximately $2,607,000 over the prior year’s fund balance.

The City’s General Fund reported total fund balance of approximately $14,926,000. Approximately 59% of this total amount, or approximately $8,813,000, is available for spending at the government’s discretion (unassigned fund balance). The unassigned fund balance for the General Fund was approximately 28% of total General Fund expenditures for 2019.

The City’s governmental activities capital assets decreased by approximately $1,609,000 (4%) during the current fiscal year due to depreciation expense and disposals of capital assets of approximately $2,726,000 and $160,000, respectively, partially offset by capital asset additions of approximately $1,277,000. The City’s business-type activities capital assets decreased by approximately $3,300,000 (3%) during the current year primarily due to depreciation expense of approximately $5,472,000, partially offset by capital asset additions of approximately $2,172,000.

The City’s governmental activities total debt (including lease purchase obligations) decreased by approximately $1,462,000 (26%) during the current year primarily due to regularly scheduled principal payments. The City’s business-type activities total debt decreased approximately $3,849,000 (4%) during the current year primarily due to regularly scheduled principal payments of approximately $4,488,000 and amortization of premiums of approximately $454,000, partially offset by an addition to a state revolving fund loan for approximately $1,093,000.

The City currently for its 2008 general obligation bond issue has an “Aa3” rating from Moody’s Investors Service and an “AA- “from Standard and Poor’s. The City received an “Aa3” and “A+” rating from Moody’s Investors Service and Standard and Poor’s, respectively, for its 2012 and 2016 water and sewer system revenue bonds. These ratings are a reflection of the City’s strong financial stability.

OVERVIEW OF FINANCIAL STATEMENTS This annual report consists of five parts – Introductory Section, the Financial Section (which includes management’s discussion and analysis, the financial statements, required supplementary information, and supplementary information), the Statistical Section, the Compliance Section, and the Continuing Disclosure Section. Financial Statements This MD&A is intended to serve as an introduction to the City’s financial statements. The City’s financial statements are comprised of three components; 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. The financial statements present two different views of the City through the use of government-wide statements and fund financial statements. In addition to the financial statements, this report contains other supplementary information that will enhance the reader’s understanding of the financial condition of the City.

13

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

OVERVIEW OF FINANCIAL STATEMENTS (CONTINUED) Government-Wide Financial Statements. The financial statements include two kinds of statements that present different views of the City. The government-wide financial statements are designed to provide readers with a broad overview of the City’s finances in a manner similar to a private-sector business. The statement of net position presents information on all of the City’s assets and deferred outflows of resources and liabilities and deferred inflows of resources, with the differences between these items reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the City is improving or deteriorating. The statement of activities presents information showing how the government’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods. The government-wide financial statements are divided into two categories: 1) governmental activities; and 2) business-type activities. The governmental activities include general government, public safety, public works, community and economic development, recreation, and advertising and tourism. Taxes, business licenses, building permits, fines, recreational fees, and state and federal grant revenues finance most of these activities. The business-type activities are the City’s sewer, water, storm water, and transit operations for which it charges its customers a fee to provide. The government-wide financial statements can be found as listed in the table of contents. Fund Financial Statements. The fund financial statements provide a more detailed look at the City’s most significant activities. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City, like all other governmental entities in South Carolina, uses fund accounting to ensure and reflect compliance with finance-related legal requirements, such as the General Statutes or the City’s budget ordinance. All of the funds of the City can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds. Governmental Funds – Governmental funds are used to account for those functions reported as governmental activities in the government-wide financial statements. Most of the City’s basic services are accounted for in governmental funds. These funds focus on how assets can readily be converted into cash flow (in and out), and what monies are left at year-end that will be available for spending in the next year. Governmental funds are reported using an accounting method called modified accrual accounting which provides a short-term spending focus. As a result, the governmental fund financial statements give the reader a detailed short-term view that helps him or her determine if there are more or less financial resources available to finance the City’s programs. The relationship between governmental activities (reported in the statement of net position and the statement of activities) and governmental funds is described in a reconciliation that is a part of the fund financial statements. The City maintained seven (7) individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenue, expenditures, and changes in fund balances for the General Fund, Community Development Fund, Perpetual Care Fund, Accommodations Tax Fund, Hospitality Fee Fund, Capital Replacement Fund, and the Transportation Investment Fund. The governmental fund financial statements can be found as listed in the table of contents. Proprietary Funds – The City maintains one type of proprietary fund. Enterprise Funds are used to account for operations that (a) are financed and operated in a manner similar to private business enterprises — where the intent of the governing body is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis be financed or recovered primarily through user charges; or (b) where the governing body has decided that periodic determination of revenues earned, expenses incurred, and/or net income is appropriate for capital maintenance, public policy, management control, accountability, or other purposes. The City uses four enterprise funds to account for its sewer, water, storm water, and transit operations. The proprietary fund financial statements can be found as listed in the table of contents.

14

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

OVERVIEW OF FINANCIAL STATEMENTS (CONTINUED) Fiduciary Funds – Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the City’s own programs. Pension Trust funds account for resources that are required to be held in trust for the members and beneficiaries of defined benefit plans. The General Employees’ Retirement Plan Fund is used to account for the City’s single-employer defined benefit retirement plan. Agency funds are used to account for assets the City holds on behalf of others. The Forfeitures and Seizures Fund is used to account for money that was forfeited and/or seized during a law enforcement action. This money is held until completion of court proceedings. The Agency Fund is custodial in nature and does not present results of operations. The financial statement of the fiduciary funds can be found as listed in the table of contents. Notes to the Financial Statements – The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found as listed in the table of contents. Other Information – In addition to the financial statements and accompanying notes, this report includes certain required supplementary information. Regarding the City’s major governmental fund, the City adopts an annual budget for its General Fund, as required by the General Statutes. A required budgetary comparison schedule has been provided for the General Fund to demonstrate compliance with its budget. The City sponsors the General Employees’ Retirement Plan (“City Pension Plan”), a single-employer defined benefit pension plan, and a healthcare plan (“OPEB Plan”). The City has provided the required schedules for the City Pension Plan and OPEB Plan as required by GAAP. Required pension schedules have also been included which provide relevant information regarding the City’s participation in the South Carolina Police Officers Retirement System, a cost-sharing multiple-employer defined benefit plan. Required supplementary information can be found as listed in the table of contents. Supplementary information, which includes combining and individual fund financial schedules, budgetary schedules of the City’s governmental and proprietary funds, a schedule of fines, assessments, and surcharges, and schedules of budgeted to actual costs for the SC Department of Transportation are presented immediately following the required supplementary information. These schedules can be found as listed in the table of contents.

15

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

OVERVIEW OF FINANCIAL STATEMENTS (CONTINUED)

Figure A-1 Major Features of the City of Anderson’s Government-Wide and Fund Financial Statements

Fund Financial Statements Government-Wide

Financial Statements

Governmental Funds

Proprietary

Funds

Fiduciary

Funds Scope Entire City

government (except fiduciary funds).

The activities of the City that are not proprietary or fiduciary.

Activities the City operates similar to private businesses.

Instances in which the City is the trustee or agent for someone else’s resources.

Required Financial Statements

Statement of Net Position.

Statement of Activities.

Balance Sheet. Statement of Revenues,

Expenditures, and Changes in Fund Balances.

Statement of Net Position

Statement of Revenues, Expenses, and Changes in Net Position.

Statement of Cash Flows.

Statement of Assets and Liabilities and Statement of Fiduciary Net Position.

Statement of Changes in Fiduciary Net Position (not required for agency funds).

Accounting Basis and Measurement Focus

Accrual accounting and economic resources focus.

Modified accrual accounting and current financial resources focus.

Accrual accounting and economic resources focus.

Accrual accounting and economic resources focus.

Type of Balance Sheet Information

All balance sheet elements - both financial and capital, and short-term and long-term.

All balance sheet elements that come due during the year or soon, thereafter. No capital assets or long-term obligations are included.

All balance sheet elements - both financial and capital, and short-term and long-term.

All balance sheet elements - short-term and long-term.

Type of Inflow/Outflow Information

All revenues and expenses during year, regardless of when cash is received or paid.

Revenues for which cash is received during or soon after the end of the year; expenditures when goods or services have been received and payment is due during the year or soon thereafter.

All revenues and expenses during year, regardless of when cash is received or paid.

All revenues and expenses during year, regardless of when cash is received or paid.

16

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

GOVERNMENT-WIDE FINANCIAL ANALYSIS As noted earlier, net position may serve over time as a useful indicator of a government’s financial position. The following table provides a summary of the City’s net position as of June 30, 2019 compared to June 30, 2018:

2019 2018 2019 2018 2019 2018

Assets:Current and Other Assets $ 29,815,298 28,825,833 18,433,439 19,393,544 48,248,737 $ 48,219,377 Capital Assets, Net 37,922,424 39,531,186 116,870,499 120,169,922 154,792,923 159,701,108

Total Assets 67,737,722 68,357,019 135,303,938 139,563,466 203,041,660 207,920,485

Deferred Outflows of ResourcesDeferred Loss on Debt Refunding - - 5,559,034 5,867,675 5,559,034 5,867,675 Deferred OPEB Charges - City Plan 29,300 29,300 - - 29,300 29,300 Deferred Pension Charges - City Pension Plan 1,568,517 720,545 1,197,828 550,889 2,766,345 1,271,434 Deferred Pension Charges - State Retirement Plan 3,917,441 3,615,972 - - 3,917,441 3,615,972

Total Deferred Outflows of Resources 5,515,258 4,365,817 6,756,862 6,418,564 12,272,120 10,784,381

LiabilitiesLong-Term Liabilities 6,921,257 8,502,646 97,923,446 101,758,563 104,844,703 110,261,209 OPEB Liability - City Plan 1,124,434 1,070,235 221,097 210,440 1,345,531 1,280,675 Net Pension Liability - State Retirement Plan 15,453,236 14,274,263 - - 15,453,236 14,274,263 Other Liabilities 4,290,996 3,969,443 1,183,091 1,890,408 5,474,087 5,859,851

Total Liabilities 27,789,923 27,816,587 99,327,634 103,859,411 127,117,557 131,675,998

Deferred Inflows of ResourcesDeferred OPEB Credits - City Plan 113,570 79,414 - - 113,570 79,414 Deferred Pension Credits - City Plan 92,107 653,033 70,339 499,273 162,446 1,152,306 Deferred Pension Credits - State Retirement Plan 79,221 126,801 - - 79,221 126,801

Total Deferred Inflows of Resources 284,898 859,248 70,339 499,273 355,237 1,358,521

Net PositionNet Investment in Capital Assets 33,761,159 33,913,890 26,280,175 26,112,126 60,041,334 60,026,016 Restricted 10,615,667 9,010,338 6,776,052 5,575,695 17,391,719 14,586,033 Unrestricted 801,333 1,122,773 9,606,600 9,935,525 10,407,933 11,058,298

Total Net Position $ 45,178,159 44,047,001 42,662,827 41,623,346 87,840,986 $ 85,670,347

TotalGovernmental Activities Business-Type Activities

The City’s total assets and deferred outflows of resources decreased approximately $3,391,000 from the prior year to approximately $215,314,000 at June 30, 2019. Deferred outflows increased approximately $1,488,000 due to the changes in deferred pension and OPEB charges. Capital assets decreased approximately $4,908,000 from the prior year primarily due to depreciation expense exceeding capital asset additions. Total liabilities and deferred inflows of resources decreased approximately $5,562,000 from the prior year. The decrease is primarily due to scheduled principal payments on the City’s long-term obligations and decreases in the deferred pension and OPEB credits related to the City’s Pension and OPEB plans, partially offset by increases in the net pension and OPEB liabilities.

The City’s net position increased by approximately $2,171,000 during the current fiscal year due to current year revenues exceeding current year expenses. Please see discussion following the next table regarding this increase.

17

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

GOVERNMENT-WIDE FINANCIAL ANALYSIS (CONTINUED) The City’s assets and deferred outflows of resources exceeded liabilities and deferred inflows of resources (net position) by approximately $87,841,000 at June 30, 2019. The largest portion of the City’s net position of approximately $60,041,000 (approximately 68%) reflects its investment in capital assets (i.e., land, buildings, equipment, infrastructure, etc.) less any related outstanding debt/lease purchase obligations used to acquire those assets. The City uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although the City’s net investment in capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt generally must be provided from other sources, since generally the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the City’s net position of approximately $17,392,000 (approximately 20%) represents resources that are subject to external restrictions on how they may be used. This portion of net position is restricted primarily for debt service or special revenue programs which are restricted by the revenue source (i.e. hospitality fee, accommodations tax, etc.). The remaining portion of the City’s net position is unrestricted net position of approximately $10,408,000 (approximately 12%) may be used to meet the government’s ongoing obligations to citizens and creditors. The following table shows the changes in the City’s net position for 2019 compared to 2018.

2019 2018 2019 2018 2019 2018

Revenues:Program Revenues:

Charges for Services $ 5,322,220 5,438,747 22,550,311 21,581,234 27,872,531 $ 27,019,981 Operating Grants and Contributions 1,325,090 1,007,073 625,011 502,902 1,950,101 1,509,975

Capital Grants and Contributions 56,090 141,189 197,372 357,800 253,462 498,989 General Revenues:

Taxes 27,438,183 26,176,789 - - 27,438,183 26,176,789 Other 952,310 932,235 156,455 60,441 1,108,765 992,676

Total Revenues 35,093,893 33,696,033 23,529,149 22,502,377 58,623,042 56,198,410

Expenses:General Government 6,787,780 6,753,776 - - 6,787,780 6,753,776 Public Safety 16,640,973 15,192,930 - - 16,640,973 15,192,930 Public Works 6,167,425 6,125,170 - - 6,167,425 6,125,170 Community & Economic Development 2,236,466 1,528,390 - - 2,236,466 1,528,390

Recreation 3,109,423 2,738,309 - - 3,109,423 2,738,309 Sanitation 1,787 2,177 - - 1,787 2,177 Advertising and Tourism 160,248 164,801 - - 160,248 164,801 Interest 191,686 240,868 - - 191,686 240,868 Sewer - - 11,001,237 10,988,830 11,001,237 10,988,830 Water - - 7,965,944 7,327,446 7,965,944 7,327,446 Storm Water - - 888,015 602,887 888,015 602,887 Transit - - 1,301,419 973,381 1,301,419 973,381

Total Expenses 35,295,788 32,746,421 21,156,615 19,892,544 56,452,403 52,638,965

Change in Net Position Before Transfers (201,895) 949,612 2,372,534 2,609,833 2,170,639 3,559,445 Transfers In (Out) 1,333,053 1,263,977 (1,333,053) (1,263,977) - -

Change in Net Position 1,131,158 2,213,589 1,039,481 1,345,856 2,170,639 3,559,445

Net Position, Beginning of Year 44,047,001 41,833,412 41,623,346 40,277,490 85,670,347 82,110,902

Net Position - End of Year $ 45,178,159 44,047,001 42,662,827 41,623,346 87,840,986 $ 85,670,347

TotalsGovernmental Activities Business-Type Activities

18

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

GOVERNMENT-WIDE FINANCIAL ANALYSIS (CONTINUED) Governmental Activities: Governmental activities increased the City’s net position by approximately $1,131,000 in the current year. Key changes in governmental activities revenues and expenses compared to the prior year were as follows:

Total governmental activities revenues for 2019 increased approximately $1,398,000 (4%) from the prior year and were approximately $35,094,000. This increase was primarily due to increase in property taxes ($110,000), hospitality taxes ($155,000), franchise fees ($171,000), and business licenses ($838,000).

Total governmental activities expenses increased approximately $2,549,000 (8%) from the prior year primarily due

to higher salaries and benefits (2% COLA) and changes in the net pension balances related to the City Pension Plan and the State retirement plan.

Business-Type Activities: Net position for business-type activities (sewer, water, storm water, and transit) increased by approximately $1,039,000. Please see “Proprietary Funds” discussion in the following section for details. FINANCIAL ANALYSIS OF THE CITY’S FUNDS As noted earlier, the City uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental funds. The focus of the City’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the City’s financing requirements. In particular, unassigned fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. As of the end of the current fiscal year, the City's governmental funds reported combined ending fund balance of approximately $22,431,000 an increase of approximately $2,607,000 over the prior year fund balance. Please see below and discussion in the General Fund Budgetary Highlights section for more information on this increase. Approximately 39% or $8,718,000 of the total governmental fund balance of approximately $22,431,000 constitutes unassigned fund balance. The remainder of the fund balance is nonspendable, restricted, committed, or assigned to indicate that it is not available for new spending because it has already been set aside/constrained for (1) prepaids and inventory ($231,000; nonspendable), (2) victims advocate services ($37,000; restricted), (3) TIF debt service or capital projects ($1,137,000; restricted), (4) tourism related expenditures ($4,472,000; restricted), (5) perpetual care ($690,000; restricted), (6) Permanent Fund principal ($2,250,000; nonspendable), (7) appropriated for use in the FY 20 budget ($4,708,000; assigned), (8) transit expenditures ($143,000; restricted), (9) capital projects ($45,000; assigned). The General Fund is the chief operating fund of the City. At the end of the current fiscal year, the total fund balance was approximately $14,926,000. As a measure of the General Fund’s liquidity, it may be useful to compare total unassigned fund balance to total General Fund expenditures. Total unassigned fund balance of the General Fund ($8,813,000) represents approximately 28% of total General Fund expenditures for the current year. The fund balance for the General Fund increased by approximately $1,131,000, or 8%. This increase was primarily due to an increase in licenses and permits revenues and a decrease in capital outlay expenditures. In addition, the fund balances of the other governmental funds increased by approximately $1,476,000, or 24%, over the prior year ending fund balances. This increase was primarily due to lower expenditures of approximately $592,000 mainly related to a decrease in debt service payments (as the City paid off the 2011 Special Obligation Bond and Community Development Note in the prior year).

19

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

FINANCIAL ANALYSIS OF THE CITY’S FUNDS (CONTINUED) Proprietary Funds. The City’s proprietary funds provide the same type of information found in the government-wide financial statements but in more detail. Net position of the Sewer, Water, Storm Water, and Transit enterprise funds at the end of the current year amounted to approximately $42,663,000. Details on changes in the City’s proprietary funds were as follows:

Sewer Fund – total sewer operating revenues increased approximately $337,000 or 3% from the prior year. There was an incremental rate increase for the current year. Charges for services increased 5% from the prior year or approximately $471,000. Sewer operating expenses decreased approximately $10,000 or <1% from the prior year. Net position increased approximately $899,000 as a result of revenues exceeding expenses.

Water Fund – total water operating revenues increased approximately $524,000 or 6% from the prior year. There was an incremental rate increase for the current year, and water operating expenses increased $679,000 or 10% from the prior year. Net position increased approximately $233,000 from the prior year due to revenues exceeding expenses.

Storm Water Fund – total storm water operating revenues remained relatively flat with a decrease of less than $1,000 from the prior year. Total storm water operating expenses increased approximately $287,000 from the prior year, due to an increase in salaries paid due to a vacant position in the prior year and an adjustment related to the City’s Pension Plan. Net position increased approximately $119,000 from the prior year, as revenues exceeded expenses.

Transit Fund – total operating revenues increased approximately $108,000 or 37% from the prior year related to an increase in miscellaneous revenues. Operating expenses increased approximately $328,000 or 34% mainly due to increases in operating and garage expenses.

Fiduciary Funds. The City’s Pension Trust Fund is used to account for the City’s Pension Plan. During calendar year 2018, the City Pension Plan’s net position decreased approximately $2,260,000 primarily due to a decrease in investment earnings of approximately $1,201,000 and benefit and administrative payments of approximately $1,942,000, partially offset by employer contributions of approximately $883,000. The Forfeitures and Seizures Fund (“Agency Fund”) is used to account for money that was forfeited and/or seized during a law enforcement action. This money is held until completion of court proceedings. The Agency Fund is custodial in nature and does not present results of operations. The balance held by others in the Agency Fund was approximately $109,000 at June 30, 2019.

General Fund Budgetary Highlights. If budget amendments are made they generally fall into one of three categories: 1) amendments made to adjust the estimates that are used to prepare the original budget ordinance once exact information is available; 2) amendments made to recognize new funding amounts from external sources, such as federal and state grants; and 3) increases in appropriations that become necessary to maintain services. The City’s amendment to its original 2019 General Fund budget were as follows:

Use of Police Grant received (E share) during the prior year for purchase of police vehicles Increasing Police Grant revenue and expenditures (Justice Assistance Grant, Traffic Enforcement, and Law

Enforcement Victim’s Advocate) Adding Economic Development Grant and expense for the (Under the Bridge Project) Adding professional fees for the NuStrat contract Adding expenditures for special projects (Asbestos Abatement) and other equipment (Storage Area Network) Adding capital improvement (Ella Street Extension Rehabilitation Project)

The City’s actual results for the General Fund were different than the final budgeted amounts due to the following:

Business licenses and franchise fees came in higher than budget primarily due to stronger collections by an outsourced company and a recovering economy.

Expenditures came in under budget primarily in general government and public works.

20

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

CAPITAL ASSET AND DEBT ADMINISTRATION Capital Assets The City’s capital assets as of June 30, 2019 and June 30, 2018, amounted to approximately $154,793,000 and $159,701,000 (net of accumulated depreciation), respectively. This investment in capital assets includes land, construction in progress, buildings, improvements, vehicles, machinery and equipment, water and sewer lines, and other infrastructure. The City’s capital assets (net of depreciation) as of June 30, 2019 and 2018 were as follows:

2019 2018 2019 2018 2019 2018

Land $ 4,194,924 4,340,026 1,768,200 1,718,950 5,963,124 $ 6,058,976 Construction in Progress 529,192 293,252 838,758 5,089,374 1,367,950 5,382,626 Buildings and Improvements 36,604,902 36,277,345 139,308,692 133,660,319 175,913,594 169,937,664 Water Tanks and Lines - - 39,954,555 39,891,601 39,954,555 39,891,601 Infrastructure 16,268,856 16,268,856 - - 16,268,856 16,268,856 Machinery and Equipment 3,604,695 3,444,057 3,086,063 2,618,141 6,690,758 6,062,198 Furniture and Fixtures 52,566 52,566 413,737 413,737 466,303 466,303 Vehicles 11,740,580 11,638,779 5,673,022 5,607,673 17,413,602 17,246,452

Capital Assets, Gross 72,995,715 72,314,881 191,043,027 188,999,795 264,038,742 261,314,676

Accumulated Depreciation 35,073,291 32,783,695 74,172,528 68,829,873 109,245,819 101,613,568

Capital Assets, Net $ 37,922,424 39,531,186 116,870,499 120,169,922 154,792,923 $ 159,701,108

TotalGovernmental Activities Business-Type Activities

The total decrease in the City’s capital assets for the current fiscal year was approximately $4,908,000 (3%). Major capital asset events during the current year included the following:

Capital asset additions of approximately $1,277,000 for governmental activities which consisted primarily of the

following: o Additions related to construction in progress of approximately $517,000 which were primarily related to

the City Hall Roof Replacement ($167,000), the Under the Bridge project ($108,000), and other capital projects ($242,000).

o Purchase of vehicles for approximately $419,000. o Purchases of equipment for $239,000, land for $10,000, and other capital assets for $92,000

Capital asset additions of approximately $2,172,000 for business-type activities which consisted primarily of the following:

o Additions related to construction in progress of approximately $1,711,000 primarily related to the Mall Road/Wedgewood Pump Station Replacement ($864,000), the Club Drive project ($532,000), and other projects ($315,000).

o Purchase of various vehicles, equipment and other assets of approximately $461,000. Depreciation expense of approximately $2,726,000 for governmental activities and approximately $5,472,000 for

business-type activities. Additional information regarding the City’s capital assets can be found in “Note III.D” in the notes to the financial statements.

21

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

CAPITAL ASSET AND DEBT ADMINISTRATION (CONTINUED) Debt Administration As of June 30, 2019, and June 30, 2018, the City had total outstanding debt (including lease purchase obligations) of approximately $100,312,000 and $105,622,000, respectively. Of the City’s total long-term obligations at June 30, 2019, approximately $1,680,000 was general obligation debt which is backed by the full faith and credit of the City. The City’s total debt and lease purchase obligations as of June 30, 2019 and 2018 were as follows:

2019 2018 2019 2018 2019 2018

Debt:General Obligation Bonds $ 1,680,000 1,820,000 - - 1,680,000 $ 1,820,000 Revenue Bonds * - - 80,937,274 85,046,370 80,937,274 85,046,370 Tax Increment Bonds 1,555,000 2,305,000 - - 1,555,000 2,305,000 SC State Revolving Fund Loans - - 14,887,641 14,467,661 14,887,641 14,467,661 Lease Purchase Obligations 926,265 1,498,554 324,443 483,978 1,250,708 1,982,532

Total Debt $ 4,161,265 5,623,554 96,149,358 99,998,009 100,310,623 $ 105,621,563

TotalGovernmental Activities Business-Type Activities

* Including deferred items (i.e. discounts, premiums, etc.).

The total decrease in the City’s debt and lease purchase obligations for the current year was approximately $5,311,000 or 5%. Major 2019 events for the City’s governmental and business-type activities were as follows:

The City’s governmental activities total debt (including lease purchase obligations) decreased by approximately $1,462,000 (26%) during the current year primarily due to regularly scheduled principal payments.

The City’s business-type activities total debt (including lease purchase obligations) decreased approximately $3,849,000 (4%) during the current year primarily due to regularly scheduled principal payments and amortization of premiums of approximately $4,942,000, partially offset by an addition to a state revolving fund loan for approximately $1,093,000.

The State of South Carolina limits the amount of general obligation debt that a unit of government can issue to 8% of the total assessed value of taxable property located within that government’s boundaries. As of June 30, 2019, the City had approximately $1,680,000 of bonded debt subject to the 8% limit of approximately $8,534,000 resulting in an unused legal debt margin of approximately $6,854,000. Additional information regarding the City’s long-term obligations can be found in “Note III.E” in the notes to the financial statements. ECONOMIC FACTORS AND 2020 BUDGET FOR THE CITY The City’s elected officials and staff considered many factors when setting the fiscal year 2020 (“FY 20” or “2020”) budget. The state of the economy, tourism activity, anticipated building activity, future capital needs, and the best interests of the City’s residents were all taken into account. Key budget highlights were as follows:

The FY 20 budget will include an increase in revenue for the MASC Collection Program of $250,000, increase in

Business License revenue of $250,000, and an increase in Prisoner Per Diem of $395,000. The FY 20 budget will include 2.25% cost of living for employees, which will increase payroll by $388,000. The FY 20 budget for the employer contribution to the Police Officers Retirement System (PORS) will increase 1%. The FY 20 budget will include three additional Firefighters, one Building Maintenance Technician and one

Horticulturalist.

22

CITY OF ANDERSON, SOUTH CAROLINA MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2019

ECONOMIC FACTORS AND 2020 BUDGET FOR THE CITY (CONTINUED)

In FY 20 budget, the Economic Development Fund in move to the General Fund. Also, the Sanitation Department will move from the General Fund to the Sanitation Fund, as a special revenue fund.

The FY 20 capital fund budget will include monies for the City Hall and Municipal Business Center Roof Projects of $2,840,000 and Fire Station 1 Sleeping Quarters Upgrade of $300,000.

The FY 20 sewer, water, and stormwater budgets increased by approximately $1.60 million, $1.38 million, and $1.23 million, respectively. Budget increases were primarily funded using prior year funds and will be used for capital projects within the City.

Transfers from the Sewer, Water, Storm Water and Hospitality Fee Funds to the General Fund are budgeted to be approximately $1,778,596 for FY 20. This is the amount budgeted in FY 19. Hospitality monies are used to help fund the beautification department, new parks, recreation center and operations, and downtown projects. Also, the City’s administration, finance, public works and other areas provide services to all funds but are paid by the General Fund. The transfers help offset the cost born completely by the General Fund.

REQUESTS FOR CITY INFORMATION This financial report is designed to provide a general overview of the City of Anderson’s finances for all those with an interest in the government’s financing. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the Finance Director, City of Anderson, 401 S. Main Street, Anderson, South Carolina 29624 or visit our website at www.cityofandersonsc.com.

23

This page is intentionally left blank

24

Basic Financial Statements

25

CITY OF ANDERSON, SOUTH CAROLINA

STATEMENT OF NET POSITION

JUNE 30, 2019

Governmental Business-TypeActivities Activities Totals

ASSETS

Cash and Cash Equivalents 13,098,907$ 8,271,571 21,370,478$ Cash and Cash Equivalents, Restricted 6,704,547 8,339,560 15,044,107 Investments, Restricted 2,150,346 319,548 2,469,894 Receivables, Net:

Interest 4,793 - 4,793 Property Taxes 583,998 - 583,998 Accounts 443,656 688,410 1,132,066 Utilities 2,375,239 - 2,375,239 Other 168,052 - 168,052

Intergovernmental Receivables 1,254,397 243,828 1,498,225 Community and Business Development Note Receivables 1,994,285 - 1,994,285 Prepaids and Inventories 232,616 27,966 260,582 Land Held for Sale/Redevelopment 94,000 - 94,000 Net Pension Asset - City Pension Plan 710,462 542,556 1,253,018 Capital Assets:

Non-Depreciable 4,724,116 2,606,958 7,331,074 Depreciable, Net 33,198,308 114,263,541 147,461,849

TOTAL ASSETS 67,737,722 135,303,938 203,041,660

DEFERRED OUTFLOWS OF RESOURCES

Deferred Refunding Charges - 5,559,034 5,559,034 Deferred Other Postemployment Benefit Charges - City Plan 29,300 - 29,300 Deferred Pension Charges - City Pension Plan 1,568,517 1,197,828 2,766,345 Deferred Pension Charges - State Retirement Plan 3,917,441 - 3,917,441

TOTAL DEFERRED OUTFLOWS OF RESOURCES 5,515,258 6,756,862 12,272,120

LIABILITIES

Accounts Payable 1,145,712 640,254 1,785,966 Accrued Interest Payable 31,240 1,563,509 1,594,749 Accrued Salaries and Benefits 869,889 - 869,889 Customer Deposits - 757,885 757,885 Other Accrued Liabilities 42,698 391,251 433,949 Intergovernmental Payables 31,649 - 31,649 Internal Balances 2,169,808 (2,169,808) - Non-Current Liabilities:

Net Other Postemployment Benefit Liability - City Plan 1,124,434 221,097 1,345,531 Net Pension Liability - State Retirement Plan 15,453,236 - 15,453,236 Long-Term Obligations - Due Within One Year 2,838,542 5,036,450 7,874,992 Long-Term Obligations - Due in More Than One Year 4,082,715 92,886,996 96,969,711

TOTAL LIABILITIES 27,789,923 99,327,634 127,117,557

DEFERRED INFLOWS OF RESOURCES

Deferred Other Postemployment Benefit Credits - City Plan 113,570 - 113,570 Deferred Pension Credits - City Plan 92,107 70,339 162,446 Deferred Pension Credits - State Retirement Plan 79,221 - 79,221

TOTAL DEFERRED INFLOWS OF RESOURCES 284,898 70,339 355,237

NET POSITION

Net Investment in Capital Assets 33,761,159 26,280,175 60,041,334 Restricted For:

Victim's Advocate 36,896 - 36,896 TIF Debt Service or Capital Projects 1,125,183 - 1,125,183 Debt Service - 5,125,862 5,125,862 Perpetual Care 689,637 - 689,637 Transportation Investment - Nonexpendable 2,250,000 - 2,250,000 Transportation Investment - Expendable 143,212 - 143,212 Community Development 1,898,944 - 1,898,944 Tourism Related Costs 4,471,795 - 4,471,795 Capital Improvements - 1,650,190 1,650,190

Unrestricted 801,333 9,606,600 10,407,933

TOTAL NET POSITION 45,178,159$ 42,662,827 87,840,986$

PRIMARY GOVERNMENT

The notes to the financial statements are an integral part of this statement. See accompanying independent auditor's report.

26

CITY OF ANDERSON, SOUTH CAROLINA

STATEMENT OF ACTIVITIES

YEAR ENDED JUNE 30, 2019

FUNCTIONS/PROGRAMSCharges for Operating Capital Governmental Business-Type

PRIMARY GOVERNMENT: Expenses Services Activities Activities Total

Governmental Activities:General Government 6,787,780$ 1,382,755 198,806 - (5,206,219) - (5,206,219)$ Public Safety 16,640,973 2,566,396 171,234 56,090 (13,847,253) - (13,847,253) Public Works 6,167,425 489,363 101,943 - (5,576,119) - (5,576,119) Community and Economic Development 2,236,466 181,745 853,107 - (1,201,614) - (1,201,614) Recreation 3,109,423 303,917 - - (2,805,506) - (2,805,506) Sanitation 1,787 398,044 - - 396,257 - 396,257 Advertising and Tourism 160,248 - - - (160,248) - (160,248) Interest on Long-Term Obligations 191,686 - - - (191,686) - (191,686)

Total Governmental Activities 35,295,788 5,322,220 1,325,090 56,090 (28,592,388) - (28,592,388)

Business-Type Activities:Sewer 11,001,237 12,344,376 - 133,572 - 1,476,711 1,476,711 Water 7,965,944 8,682,176 - 63,800 - 780,032 780,032 Storm Water 888,015 1,125,811 - - - 237,796 237,796 Transit 1,301,419 397,948 625,011 - - (278,460) (278,460)

Total Business-Type Activities 21,156,615 22,550,311 625,011 197,372 - 2,216,079 2,216,079 .

TOTAL - PRIMARY GOVERNMENT 56,452,403$ 27,872,531 1,950,101 253,462 (28,592,388) 2,216,079 (26,376,309)

General Revenues and Transfers:

General Revenues:Taxes:

Property Taxes 12,194,437 - 12,194,437 Tax Increment 1,176,450 - 1,176,450 Hospitality Fees 3,057,287 - 3,057,287 Accommodations Taxes 364,415 - 364,415 Franchise Taxes 5,817,482 - 5,817,482 Business Licenses 4,761,512 - 4,761,512 Other Taxes 66,600 - 66,600

Intergovernmental Revenue - Unrestricted 610,171 - 610,171 Investment Income 245,513 156,455 401,968 Miscellaneous 38,526 - 38,526 Gain on Sale of Assets 58,100 - 58,100

Transfers In (Out) 1,333,053 (1,333,053) -

Total General Revenues and Transfers 29,723,546 (1,176,598) 28,546,948

CHANGE IN NET POSITION 1,131,158 1,039,481 2,170,639

NET POSITION, BEGINNING OF YEAR 44,047,001 41,623,346 85,670,347

NET POSITION, END OF YEAR 45,178,159 42,662,827 87,840,986$

NET (EXPENSE) REVENUE ANDPROGRAM REVENUES CHANGE IN NET POSITION

Grants and Contributions

Primary Government

The notes to the financial statements are an integral part of this statement. See accompanying independent auditor's report.

27

OTHER TOTALGOVERNMENTAL GOVERNMENTAL

GENERAL FUNDS FUNDSASSETS

Cash and Cash Equivalents 13,093,727$ 5,180 13,098,907$ Cash and Cash Equivalents, Restricted 1,367,883 5,336,664 6,704,547 Investments, Restricted - 2,150,346 2,150,346 Receivables, Net:

Interest - 4,793 4,793 Property Taxes 583,998 - 583,998 Accounts - 443,656 443,656 Utilities 2,375,239 - 2,375,239 Other 3,535 164,517 168,052

Intergovernmental Receivables 1,254,397 - 1,254,397 Due From Other Funds 858,294 85,131 943,425 Prepaids and Inventories 230,729 1,887 232,616 Land Held for Sale/Redevelopment - 94,000 94,000

TOTAL ASSETS 19,767,802$ 8,286,174 28,053,976$

LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND FUND BALANCES

LIABILITIES

Accounts Payable 1,021,120$ 124,592 1,145,712$ Accrued Salaries and Benefits 869,889 - 869,889 Other Accrued Liabilities 42,657 41 42,698 Intergovernmental Payables 31,649 - 31,649 Due To Other Funds 2,456,074 657,159 3,113,233

TOTAL LIABILITIES 4,421,389 781,792 5,203,181

DEFERRED INFLOWS OF RESOURCES

Unavailable Revenue - Property Taxes 420,274 - 420,274

TOTAL DEFERRED INFLOWS OF RESOURCES 420,274 - 420,274

FUND BALANCES

Nonspendable:Prepaid and Inventories 230,729 - 230,729 Permanent Fund Principal - 2,250,000 2,250,000

Restricted For:Victim's Advocate 36,896 - 36,896 TIF Debt Service or Capital Projects 1,137,132 - 1,137,132 Perpetual Care - 689,637 689,637 Tourism Related Expenditures - 4,471,795 4,471,795 Community Development - - - Transit Expenditures - 143,212 143,212

Assigned For:Capital Projects - 45,079 45,079 Appropriated for Use in FY 2020 Budget 4,708,075 - 4,708,075

Unassigned 8,813,307 (95,341) 8,717,966

TOTAL FUND BALANCES 14,926,139 7,504,382 22,430,521

TOTAL LIABILITIES, DEFERRED INFLOWS OF RESOURCES, AND FUND BALANCES 19,767,802$ 8,286,174 28,053,976$

CITY OF ANDERSON, SOUTH CAROLINA

BALANCE SHEET - GOVERNMENTAL FUNDS

JUNE 30, 2019