Embed Size (px)

Citation preview

Comprehensive Annual Financial Report

For the Fiscal Year Ended June 30, 2014

ARLINGTON INDEPENDENT SCHOOL DISTRICT

1203 W. Pioneer Pkwy, Arlington, TX 76013

Prepared By The Finance Department:

Cindy Powell, CPA Chief Financial Officer

ARLINGTON INDEPENDENT SCHOOL DISTRICT TABLE OF CONTENTS

Page

Exhibit/ Table

Introductory Section

Board of Trustees and Administration i Certificate of the Board viii Transmittal Letter ix GFOA Certificate of Achievement xvi ASBO Certificate of Excellence xvii Organizational Chart xviii

Financial Section

Report of Independent Auditors

1

Management’s Discussion and Analysis

7

Basic Financial Statements: Government-Wide Financial Statements

Statement of Net Position 27 A-1 Statement of Activities 28 B-1

Governmental Fund Financial Statements Balance Sheet 30 C-1 Reconciliation of Balance Sheet for Governmental Funds to the

Statement of Net Position

33

C-2 Statement of Revenues, Expenditures, and Changes in Fund Balance 34 C-3 Reconciliation of the Statement of Revenues, Expenditures, and

Changes in Fund Balance of Governmental Funds to the Statement of Activities

36

C-4 Statement of Revenues, Expenditures, and Changes in Fund Balances -

Original Budget, Amended Final (GAAP Basis) and Actual - General Fund

37

C-5 Proprietary Fund Financial Statements

Statement of Net Position 38 D-1 Statement of Revenues, Expenses and Changes in Fund Net Position 39 D-2 Statement of Cash Flows 40 D-3

Fiduciary Fund Financial Statements Statement of Fiduciary Assets and Liabilities 41 E-1

Notes to the Financial Statements

42 F-1

Other Supplementary Information: Combining Fund Statements:

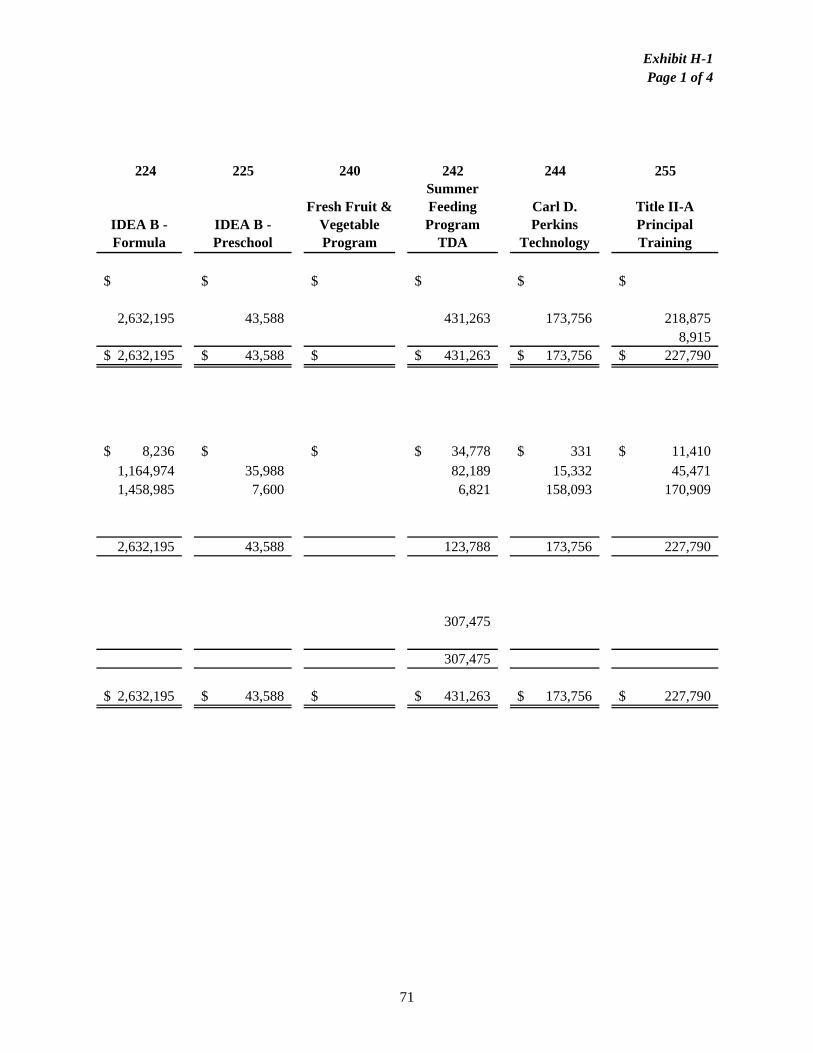

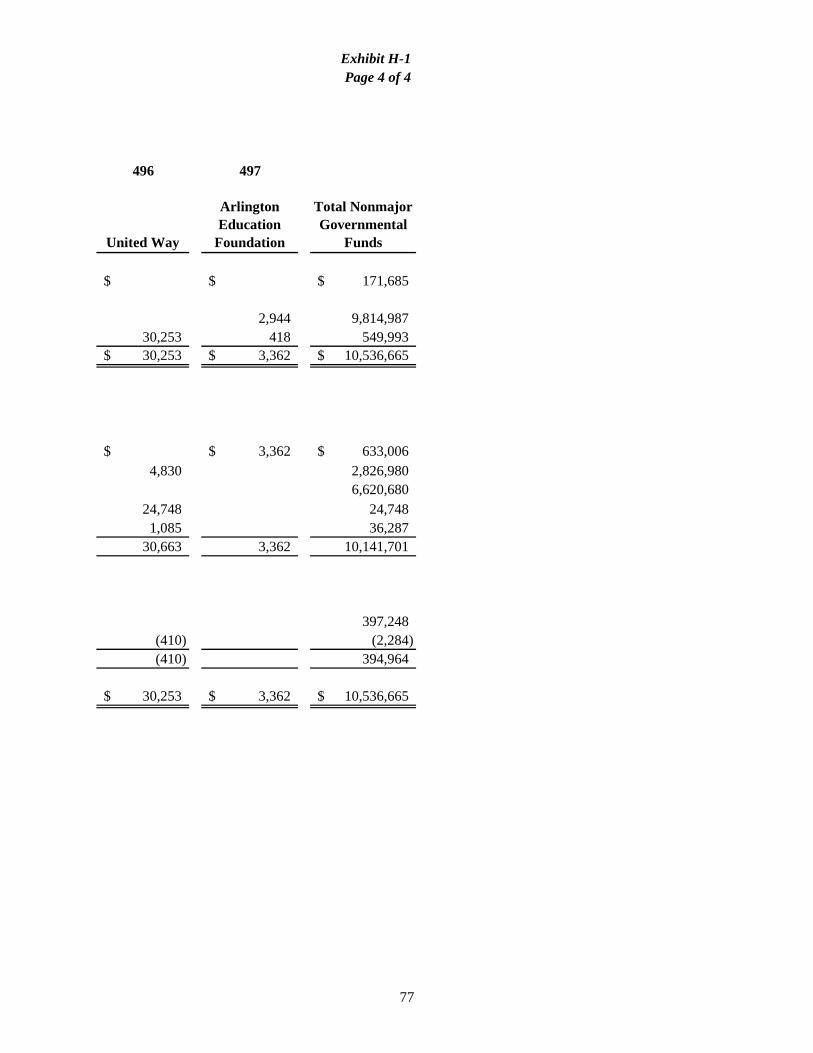

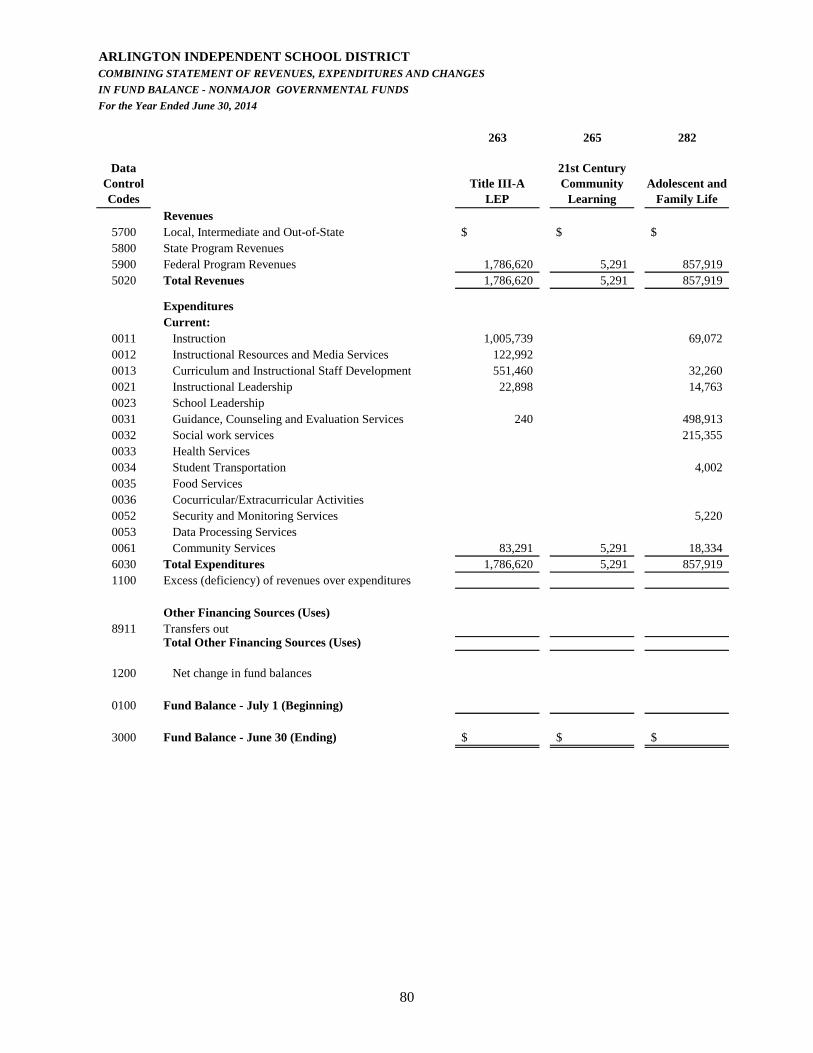

Combining Balance Sheet - Nonmajor Governmental Funds 70 H-1 Combining Statement of Revenues, Expenditures, and Changes in

Fund Balance - Nonmajor Governmental Funds

78

H-2

ARLINGTON INDEPENDENT SCHOOL DISTRICT TABLE OF CONTENTS (continued)

Page

Exhibit/ Table

Financial Section (continued)

Other Supplementary Information (continued): Combining Fund Statements (cont.):

Combining Statement of Net Position - Internal Service Funds 86 H-3 Combining Statement of Revenues, Expenses, and Changes in Net

Position - Internal Service Funds

87

H-4 Combining Statement of Cash Flows - Internal Service Funds 88 H-5 Statement of Changes in Assets and Liabilities - Agency Funds 91 H-6

Required TEA Schedules

Schedule of Delinquent Taxes Receivable 94 J-1 Schedule of Revenues, Expenditures, and Changes in Net Position -

Original Budget, Amended Final and Actual - Child Nutrition

96

J-4 Schedule of Revenues, Expenditures, and Changes in Fund Balance -

Original Budget, Amended Final and Actual - Debt Service Fund

97

J-5 Schedule of Revenues, Expenditures, and Changes in Fund Balance -

Original Budget, Amended Final and Actual - Capital Projects Fund

98

J-6 Statistical Section (Unaudited)

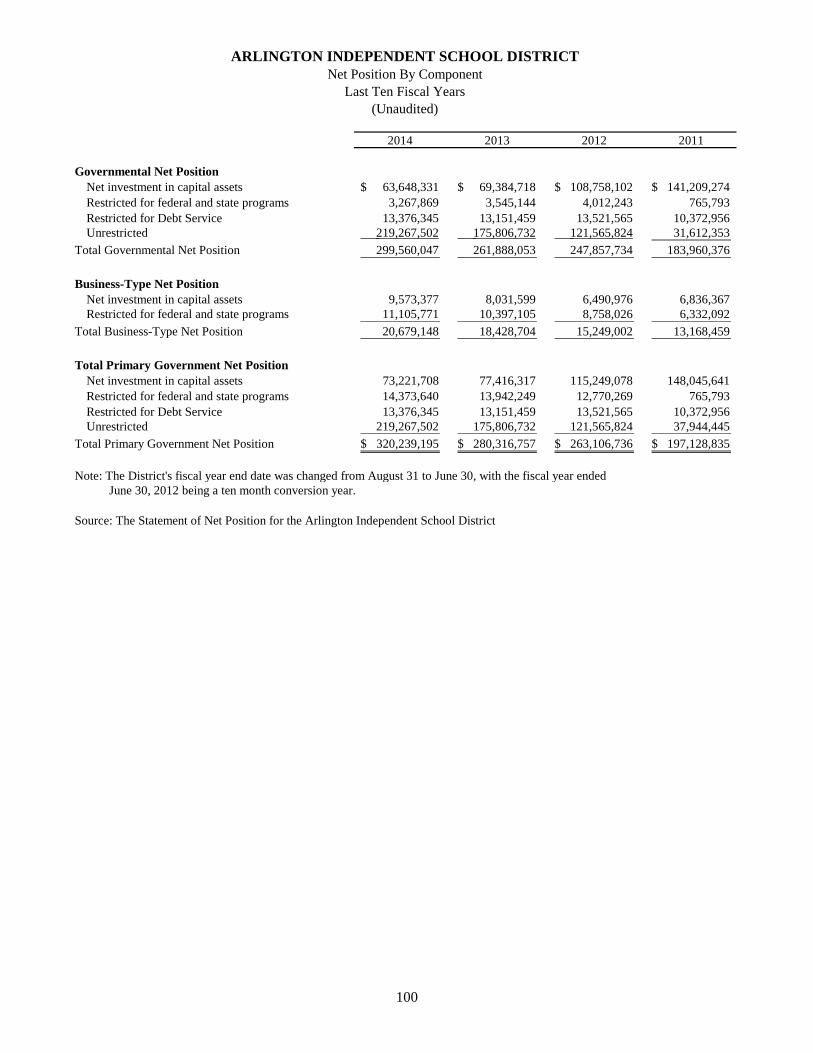

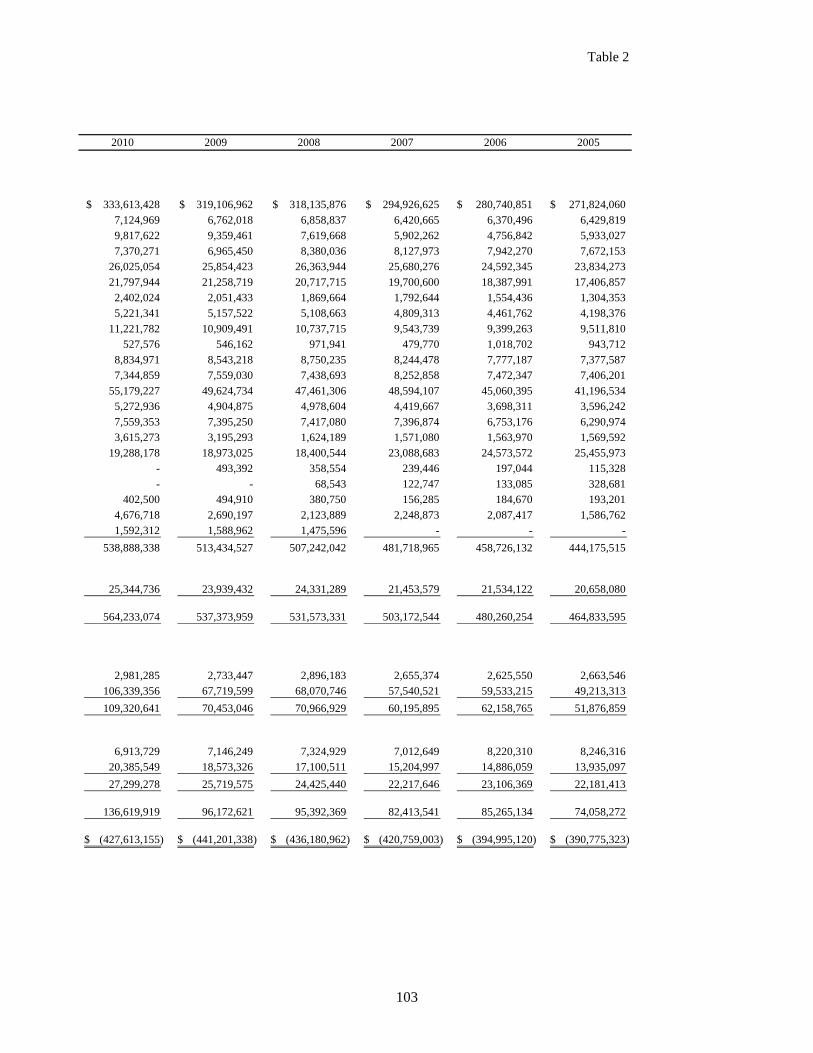

Net Position by Component 100 1 Expenses, Program Revenues, and Net Expenses 102 2 General Revenues and Total Change in Net Position 104 3 Fund Balances, Governmental Funds 106 4 Governmental Funds Expenditures and Debt Service Ratio 108 5 Governmental Funds Revenues 110 6 Other Financing Sources and Uses and Net Change in Fund Balances 112 7 Appraised Value and Actual Value of Taxable Property 114 8 Direct and Overlapping Property Tax Rates 115 9 Direct and Overlapping Property Tax Levies 116 10 Principal Property Taxpayers 117 11 Property Tax Levies and Collections 118 12 Outstanding Debt by Type 119 13 Ratio of Net Bonded Debt to Assessed Value and Net Bonded Debt Per Capita

120 14

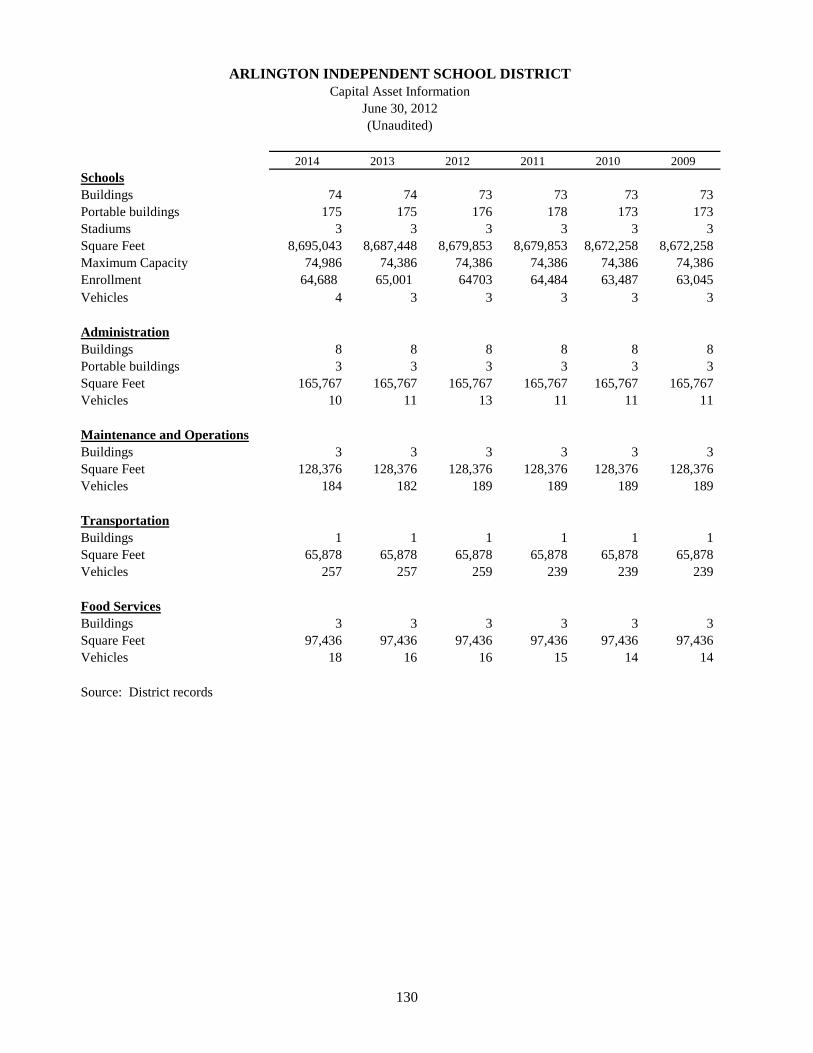

Statement of Direct and Overlapping Debt 121 15 Legal Debt Margin Information 122 16 Demographic and Economic Statistics 123 17 Principal Employers 124 18 Full-Time Equivalent District Campus Employees 126 19 Operating Statistics 129 20 Capital Asset Information 130 21

ARLINGTON INDEPENDENT SCHOOL DISTRICT TABLE OF CONTENTS (continued)

Page

Exhibit/ Table

Federal Awards Section

Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

135

Independent Auditors’ Report on Compliance for Each Major Program and on Internal Control over Compliance Required by OMB Circular A-133

137

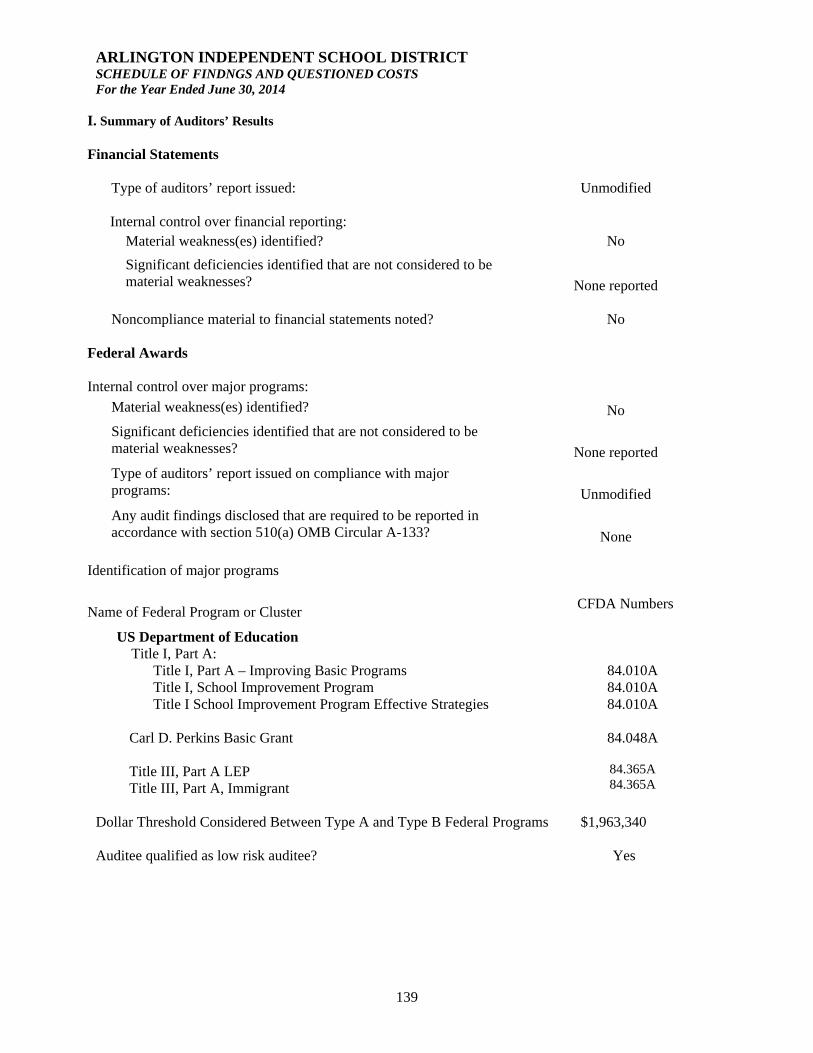

Schedule of Findings and Questioned Costs 139

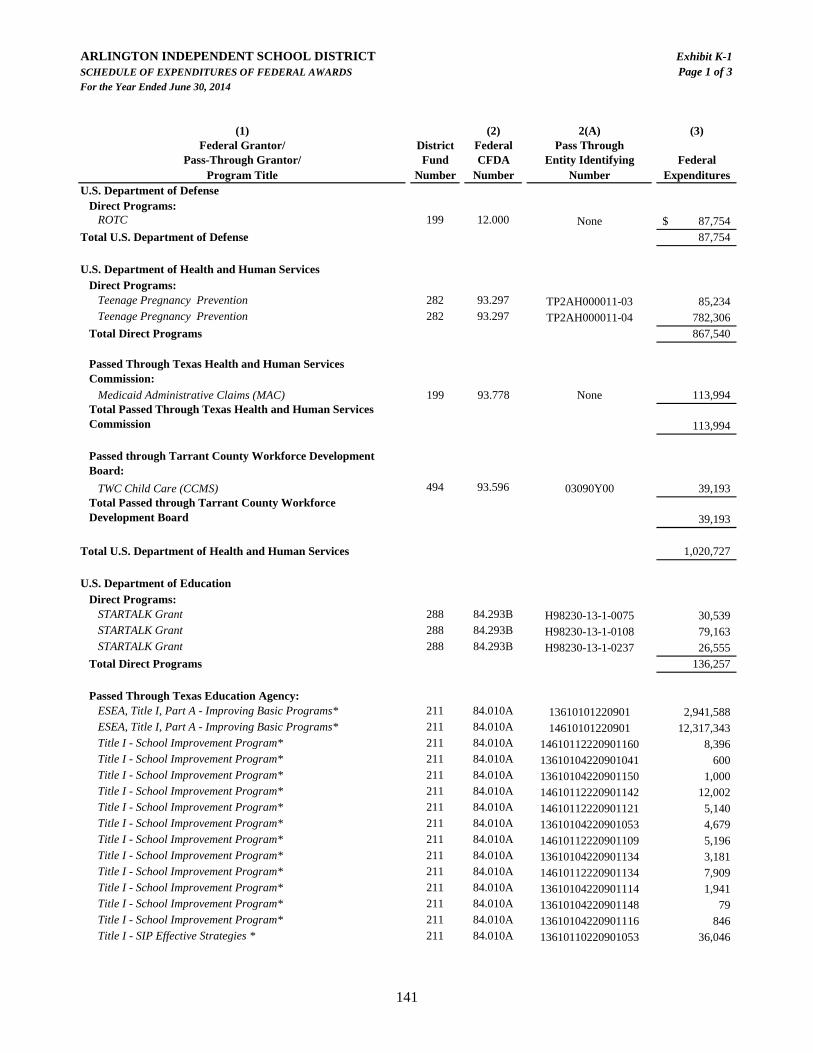

Schedule of Expenditures of Federal Awards 141 K-1

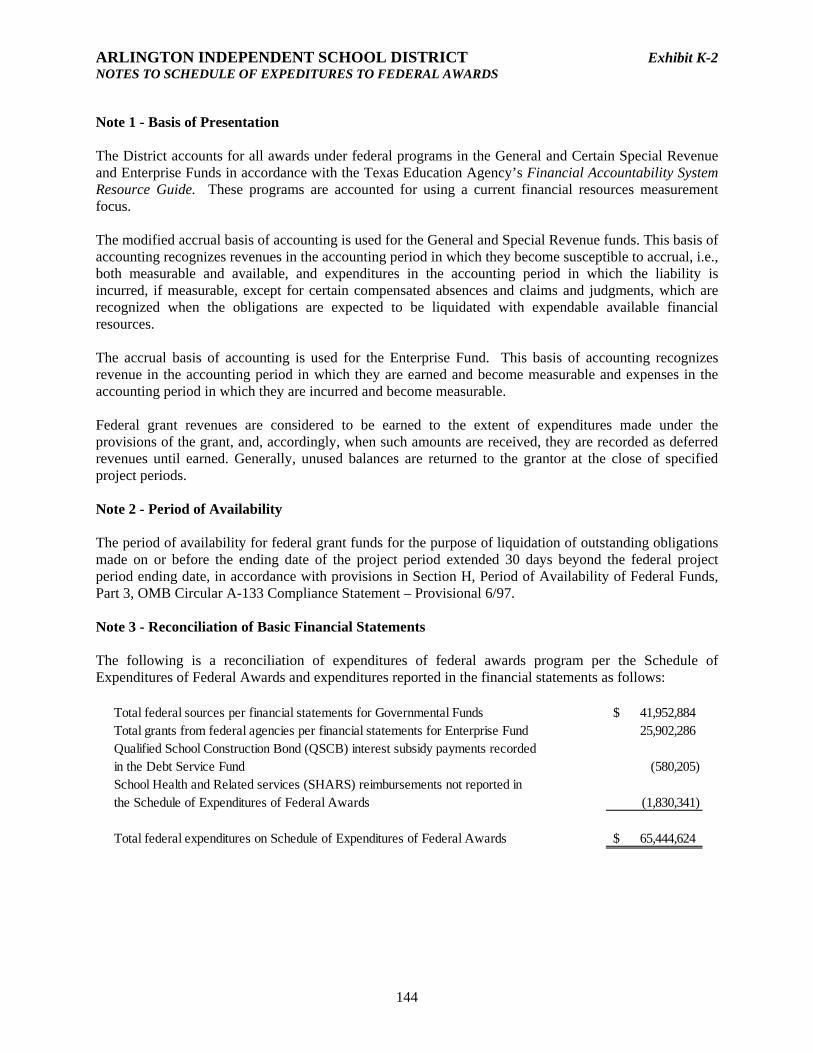

Notes to Schedule of Expenditures of Federal Awards 144 K-2

INTRODUCTORY SECTION

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration

i

Mr. Bowie Hogg PresidentMs. Jamie Sullins Vice PresidentDr. Aaron Reich SecretaryMs. Gloria Peña Assistant SecretaryMr. Peter BaronMr. John HibbsMs. Kecia Mays

Cindy Powell, CPA

ASSISTANT SUPERINTENDENT OF TECHNOLOGY

Chad Branum

Vacant

AREA SUPERINTENDENT - SECONDARY

AREA SUPERINTENDENT - ELEMENTARY

AREA SUPERINTENDENT - ELEMENTARY

ASSISTANT SUPERINTENDENT OF ADMINISTRATION

Michael Hill

BOARD OF TRUSTEES

SUPERINTENDENT

Marcelo Cavazos, Ph.D.

CHIEF FINANCIAL OFFICER

CHIEF ACADEMIC OFFICER

Steven Wurtz, Ed.D.

Michelle Wilmoth-Senato

EXECUTIVE DIRECTOR OF FINANCE

Melissa Haubrich, Ed.D.

Timothy Edwards, CIA, CFE

Tony Drollinger

DIRECTOR OF BUDGET/CASH MANAGEMENT

Mandy Mew

DIRECTOR OF ACCOUNTING

Natasha Whetstone

CHIEF INTERNAL AUDITOR

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration (continued)

ii

BOARD OF TRUSTEES Bowie Hogg – President

Bowie Hogg was elected to the board in May of 2008 and is a product of the Arlington schools from kindergarten through high school graduation. Mr. Hogg graduated from The Mays Business School at Texas A&M University with a Bachelors of Business Administration degree. Mr. Hogg also represented Arlington and the Dallas-Fort Worth metroplex by being chosen out of 216,000 applicants to appear on the original edition of the Emmy nominated television show, The Apprentice. Mr. Hogg is a healthcare executive with Aon Corp., while also serving his community as a Board member for the United Way of Tarrant County, Leadership Arlington and the Advisory Board for the Arlington Life Shelter and Junior League Arlington. Mr. Hogg’s passions are education, healthcare and community service, with his wife who is also a 5th grade teacher.

Jamie Sullins – Vice President

Mrs. Sullins was elected in May 2010. She has a Bachelors of Business Administration in Finance from Texas Tech University. She worked at Lockheed Martin Missiles and Advanced Programs Division in financial planning and analysis evaluating the feasibility and cost effectiveness of capital improvement projects. She also worked for Interturbine Group of Companies, as the corporate Manager of Financial Planning and Analysis for international operations. Mrs. Sullins is a life-long community volunteer. She has served as a full-time volunteer in Arlington schools for 16 years serving on four PTA Executive boards. She is founder and past president of the North Arlington Education Alliance, a non-profit organization working in close parallel with the District to connect people and to mobilize ideas that promote educational excellence. Mrs. Sullins and her husband, Gerald, have lived in Arlington for over 26 years. They have two children; one graduated from AISD in 2007 and the other in 2011.

Aaron Reich – Secretary

Dr. Reich was re-elected to the Board in May of 2012. He has lived in Arlington for 22 years and is married with two children currently enrolled in the AISD. He and his wife of 21 years have two businesses in Arlington; a CPA practice (his wife, Debra J. Freiheit, CPA, MS) and TRINU Healthcare (a professional development, education and consulting firm for healthcare). Dr. Reich has been an invited lecturer on a local, state and national level. He received his Doctor of Pharmacy degree from Creighton University, Omaha, Nebraska and came to Texas via his post graduate residency at UT MD Anderson Cancer Center in Houston. Dr. Reich has served on many non-profit Boards of Directors and committees, mostly related to his professional practice and healthcare education. Specific to education and the local community, he is a very active parent, President and co-founder of Positive Influence, which is a non-profit organization dedicated to parental and father figure involvement programs for primary and secondary education. He also serves on the Board of Directors for Theatre Arlington. Along with being a proud member of the First United Methodist Church, Ft. Worth, Aaron enjoys his family, community advocacy, the outdoors, and traveling.

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration (continued)

iii

BOARD OF TRUSTEES (continued)

Gloria Peña - Assistant Secretary

Mrs. Peña was elected to the Board in May 2005, and has served as Secretary, Assistant Secretary, Vice-President and President. She also serves on the State Board of Directors of the Texas Association of School Boards and the Mexican American School Board Association. She graduated Magna Cum Laude from Northwood University with a Bachelor’s degree in Business Administration in management. Prior to her election she was involved in and continues to be involved in various AISD committees. She serves on multiple boards in the community and is an active member of St. Vincent de Paul Church as well as other community involvement. She and her husband of 31 years, Richard, have one daughter who graduated from Martin High School and Tarrant County College. Mrs. Peña enjoys spending time with her family, working with children of all ages, sewing, ceramics, learning and traveling. She recently retired from the US Army Corps of Engineers after 37 years of service.

Peter Baron

Mr. Baron was re-elected in May 2012. He is a Lieutenant Colonel, retired, in the United States Marine Corps. He served 23 years on active duty, retiring in 1991 as a Naval Aviator, with 5000 flight hours in helicopters and jets, and over 200 carrier arrested landings. A decorated Vietnam veteran, he moved to NAS Beeville, Texas, in 1988 to become the first Marine to command a US Navy Strike Training squadron. Mr. Baron has a BS from Auburn University and a master’s degree in Aeronautics from Embry Riddle University. A Master Technology Teacher, he taught mathematics and computer classes at Arlington High School for thirteen years. After being elected to the board in 2008, he resigned his teaching position in Arlington and subsequently taught high school mathematics in a neighboring school district until retiring this year after 20 years in the classroom. Peter Baron is a Life Member of the USMC Combat Helicopter Association, the Military Officers Association of America, and the Glock Sport Shooting Federation. He rides with the Lone Star Cyclists bicycle club and is a member of the Knights of Columbus at St. Maria Goretti Church. He has represented AISD on numerous occasions as a presenter at TASA/TASB conventions, Texas Computer Educators Association conventions and at ESC Region XI workshops. Additionally, he has served on the AISD Financial Futures Committee, the Textbook Selection Committee, the Mathematics Benchmark Test Committee, and numerous Board committees. He and his wife, Carole, have resided in Arlington since 1991. They have three grown children and five grandchildren.

John Hibbs

Mr. Hibbs was elected to the Board in May 2010. He is the Western Regional Lab Manager for Bausch & Lomb, a leader in the eye care industry. He has been employed with Bausch & Lomb for 23 years. He also is a licensed Contact Lens Examiner. Mr. Hibbs is a 1985 graduate of Texas Christian University where he received a BA degree. John Hibbs and his wife, Mary, have been married for 29 years. They have one son and two daughters, all of whom have attended the Arlington Independent School District. Prior to being elected to the School Board, John received both the PTSA Life Membership and PTSA Extended Life Membership awards for his volunteerism within the AISD. He currently serves as a director for the Arlington Children’s Toy Charities, and serves in a leadership role in the Children’s Ministry at Lake Arlington Baptist Church. His passion is his family and the community he serves.

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration (continued)

iv

BOARD OF TRUSTEES (continued) Kecia Mays

Mrs. Mays is an auditor for the State Comptroller’s Office. She serves as a Field Service Rep for the Texas PTA Board of Directors and Serves on the Executive Board for the Black Former Students Network of Texas A&M University along with volunteering in multiple capacities in her children’s schools.

ADMINISTRATION

Dr. Marcelo Cavazos –Superintendent

Dr. Marcelo Cavazos started his teaching career as an English teacher in the Mission Consolidated ISD in 1990. In 1992, he moved to McAllen ISD where he taught English and government. He was named the secondary language arts supervisor for Mercedes ISD in 1993 and became associate adviser for San Benito Consolidated ISD in 1995. Cavazos went to work for the Texas Education Agency Department of School Finance and Support in 1998. He joined the AISD in 1999 as associate superintendent for instruction and served as interim deputy superintendent for seven months before being named deputy superintendent in February 2009. He has previously served as a lecturer for the University of Texas at Arlington’s Department of Educational Leadership and Policy Studies. Cavazos served as interim superintendent for six months before being named superintendent Dec. 6, 2012. He holds a bachelor’s and a master’s degree from the University of Texas – Pan American and a doctorate from the University of Texas at Austin. In addition to his professional accomplishments, Cavazos is active in the community. He serves on the Texas School Alliance Board, United Way of Tarrant County Board Executive Committee, , the Workforce Solutions for Tarrant County Board, the River Legacy Foundation Board, the Salvation Army Youth Education Town North Texas Advisory Council and the Arlington ISD Education Foundation Board. He’s an ex-officio member of the Arlington Chamber of Commerce Board. Cavazos is an associate member of the Rotary Club of Arlington, an associate member of the Greater Arlington Lions Club, a Lifetime Supporting member of the Texas Lions Camp, a member of the Knights of Columbus and active at St. Matthew Catholic Church. He received the 2009 Arlington MLK Celebration Sharing the Dream Award for Asian- American Chamber of Commerce and the 2013-2014 Elks Distinguished Citizenship Award from the Arlington Elks Lodge No. 2114. He has been married to Nora for 14 years; his children Theresa and Diego attend school at Key Elementary.

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration (continued)

v

ADMINISTRATION (continued)

Steven Wurtz – Chief Academic Officer

Wurtz has served as an area superintendent of elementary schools for Arlington ISD since June 2013. Prior to that, he was the division director of elementary schools in the Irving ISD since 2011, following his position as principal at Schulze Elementary. Prior to that, he was principal at Austin Elementary in the Grand Prairie ISD from 2007 to 2009 and assistant principal at Keyes Elementary in the Irving ISD from 2003 to 2007. He was a bilingual elementary teacher in the Irving ISD before that. He has a bachelor’s degree from Brigham Young University, a master’s degree from the University of Texas at Arlington, and a doctorate from Dallas Baptist University. Wurtz was formerly a member of the state board of directors for the Texas Elementary Principals and Supervisors Association and he is currently the second vice president elect for the TEPSA District 11 board. Wurtz serves on the TEPSA state advocacy committee, and he has been a member of TEPSA for 11 years. Wurtz is also a member of the Texas Association of School Administrators.

Cindy Powell – Chief Financial Officer

Cindy Powell has been AISD's Chief Financial Officer (previously titled Associate Superintendent of Finance) since October 2008. Mrs. Powell was originally hired in September 1993 as the District’s first Internal Auditor. She served in that capacity for three years. Mrs. Powell then was named Director of Accounting in 1996 and held that position for three years before being named Executive Director of Finance in 1999. She has 28 years total experience in public accounting, private sector auditing, and governmental accounting. She graduated from Texas Tech University with a BBA in Accounting and is a Certified Public Accountant.

Michael Hill – Assistant Superintendent of Administration

Michael Hill was named Assistant Superintendent of Administration in February of 2013. He started his teaching career in 1996 as an Economics/Government teacher in the Union Parish School System in Louisiana. In 1997 he moved to Fort Worth ISD where he taught and coached at Paschal High School. In 2002 he moved to Arlington ISD and taught and coached at Bowie High School. Later he moved into administration at Bowie High School as an assistant principal, serving in that capacity for 3 years. Mr. Hill then became the Academic Associate Principal at Timberview High School in the Mansfield ISD. He served in that capacity for a little less than two years before returning to Arlington ISD as the principal at Juan Seguin High School. He served in that capacity from January 2011 until February 2013. Mr. Hill holds a master’s degree in Educational Leadership and Policy Studies and a superintendent certification from the University of Texas at Arlington and a bachelor’s degree from Grambling State University in Louisiana.

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration (continued)

vi

ADMINISTRATION (continued)

Chad Branum – Assistant Superintendent of Technology

Chad Branum was named Assistant Superintendent of Technology for Arlington ISD in May 2013. He started his career in the business sector and transitioned to education in 1999 with Coppell ISD. He served in several roles for Coppell ISD with the most recent being the Executive Director of Technology for 12 years. He is involved with Educational Technology organizations from around the country and is an active officer for the Texas K-12 CTO Council organization. He holds a bachelor’s degree from Texas A&M University and a master’s degree from Western Michigan University. Additionally, Chad obtained the Certified Education Technology Leader (CETL) certification in the summer of 2014 from the Consortium for School Networking (CoSN). The CETL certification is based upon the Framework of Essential Skills of K-12 CTO and demonstrates the knowledge and skills necessary to be an effective and visionary technology leader.

Vacant – Area Superintendent - Elementary

Melissa Haubrich – Area Superintendent - Elementary

Haubrich has served as an Area Superintendent since January 2013. Prior to that, she was the director of elementary personnel for Arlington ISD, principal at Ferguson Junior High and Pearcy Elementary in Arlington and Southwest Elementary in the Belton ISD. Haubrich was also an elementary school teacher in the Belton ISD and the Killeen ISD. She has a bachelor’s degree from the University of Texas at San Antonio, a master’s degree from the University of Mary Hardin-Baylor, and a doctorate from Tarleton State University. Haubrich has published articles in several psychology journals and presented at the National Council of Professors of Educational Administration. She is a member of the Texas Elementary Principals and Supervisors Association, the National Association of Bilingual Education, and the Association for Supervision and Curriculum and Development.

Michelle Wilmoth-Senato – Area Superintendent - Secondary

Michelle Wilmoth-Senato was appointed Area Superintendent of Secondary Schools in January 2013. She began her teaching career in Arlington ISD in 1980. For 19 years, she taught a variety of courses, including English, Humanities, Debate, and Psychology at both Arlington High School and Bowie High School. In 2000, she became assistant principal at Bowie High School. In 2006 she was appointed principal of Boles Junior High. In 2008, she returned to Bowie High School as principal, a position she held until her appointment as area superintendent. From 1997-1999, while teaching for AISD, she also served as adjunct instructor at the University of Texas at Arlington in the College of Education, teaching classes at both the undergraduate and graduate levels. She holds a bachelor's in Education and a master's in Humanities from the University of Dallas. She holds a master's in Educational Administration and Policy Studies from the University of Texas at Arlington. Ms Wilmoth-Senato is a member of TASA and TASSP.

ARLINGTON INDEPENDENT SCHOOL DISTRICT Board of Trustees and Administration (continued)

vii

ADMINISTRATION (continued) Tony Drollinger – Executive Director of Finance

Tony Drollinger originally came to the District in October 1996 as the District’s Internal Auditor. After serving in that capacity for three years, he was named Director of Accounting in 1999, and then was named Executive Director of Finance in November of 2008. Prior to coming to the District, Mr. Drollinger worked four years as a financial consultant and software trainer for Texas Educational Consultative Services (TECS) in Austin. Before that time Mr. Drollinger spent five years working for the Texas Education Agency in the areas of School Audits and PEIMS. He is a graduate of Southwest Texas State University with a BBA in Accounting, and is a member of the Texas Association of School Business Officials and the Government Finance Officers Association.

Natasha Whetstone – Director of Accounting

Natasha Whetstone was named Director of Accounting in February 2013. Prior to joining the District she worked at Cleburne ISD for three years as the senior accountant and served six months as the Director of Federal Grants. Before that time Natasha spent three years working as an auditor for a local CPA firm. She is a graduate of the University of Texas at Arlington with a BS in Accounting and is a member of the Government Finance Officers Association.

Mandy Mew – Director of Budget and Cash Management

Mandy Mew has worked with Public School Finance since 1988. She was the Chief of School Finance for the North Carolina Department of Public Instruction until moving to Texas in 2000. After moving to Texas she worked for the Fort Worth ISD and the Hurst-Euless-Bedford ISD. In July, 2010 she moved to Arlington ISD as the Director of Budget and Cash Management. Ms. Mew graduated from Wake Forest University. She is also a graduate of the Education Policy Fellowship Program, sponsored by the Institute for Educational Leadership.

Tim Edwards – Chief Internal Auditor

Tim Edwards was appointed as the Chief Internal Auditor for AISD in December 2010. Previously, he served as the Chief Internal Auditor for a university system, was the Senior Manager of Corporate Audit for a Fortune 500 corporation, and led the start-up of an Internal Audit function for the largest real estate association management company in the country. Mr. Edwards has a BBA degree in Corporate Finance and is a Certified Internal Auditor and Certified Fraud Examiner.

ix

1203 W. Pioneer Pkwy Arlington, Texas 76013 682-867-7250

November 20, 2014 To the Board of Trustees and Citizens of the Arlington Independent School District: The Texas Education Code requires that all independent school districts file a complete set of financial statements within 150 days of the close of each fiscal year with the Texas Education Agency (“TEA”). The financial statements must be presented in conformity with generally accepted accounting principles (“GAAP”), and must be audited by a firm of licensed certified public accountants in accordance with generally accepted auditing standards. Pursuant to that requirement we hereby issue the comprehensive annual financial report of the Arlington Independent School District (“District” or “AISD”) for the fiscal year ended June 30, 2014. This report consists of management’s representations concerning the finances of the District. Consequently, management assumes full responsibility for the completeness and reliability of all of the information presented in this report. To the best of our knowledge and belief, we assert that this financial report is complete and reliable in all material respects. The District’s financial statements have been audited by Whitley Penn, LLP, a firm of licensed certified public accountants. The goal of the independent audit is to provide reasonable assurance that the financial statements of the District for the fiscal year ended June 30, 2014, are free of material misstatement. The independent audit involves examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; assessing the accounting principles used and significant estimates made by management; and evaluating the overall financial statement presentation. The independent auditors concluded, based upon the audit, that there was a reasonable basis for rendering an unqualified opinion that the District’s financial statements for the fiscal year ended June 30, 2014, are fairly presented in conformity with GAAP. The independent auditors’ report is presented as the first component of the financial section of this report. GAAP also requires that management provide a narrative introduction, overview and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (“MD&A”). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The District’s MD&A can be found immediately following the report of the independent auditors. The independent audit of the financial statements is part of a broader, federally-mandated “Single Audit” designed to meet the special needs of federal grantor agencies. The standards governing Single Audit engagements require the independent auditor to report not only on the fair presentation of the financial statements, but also on the audited government’s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal awards. These reports may be found in the Federal Awards section of this report.

x

District Profile The Arlington Independent School District was established as a political subdivision of the State of Texas and incorporated in 1902. It lies halfway between Dallas and Fort Worth and serves students in four cities - the City of Arlington, the Tarrant County portion of the City of Grand Prairie, the Town of Pantego, and the City of Dalworthington Gardens. It is fully accredited by the TEA and is regulated by the Texas Education Code as established by the Texas State Legislature. The District is not a component unit of any other entity, nor does it have any component units within its overall structure. The Arlington Independent School District is the 11th largest school district in Texas. The District currently operates six traditional high schools, one early college high school, 12 junior high schools, 51 elementary schools, a pre-kindergarten campus and four alternative campuses (one is housed at one of the junior high school buildings). During the 2013-14 school year the District employed 8,055 full-time equivalent staff members of which 4,113 were classroom teachers. Enrollment for the 2013-14 year was 64,688 as reported to the State through the Public Education Information Management System (“PEIMS”). This enrollment figure represents a decrease of approximately 0.48% from the enrollment figure reported through PEIMS the previous year. Enrollment for 2014-15 is expected to be 64,757 at the fall PEIMS snapshot date which is 2% less than the 2013-14 official enrollment. All academic and extracurricular programs are supported by a highly qualified, culturally-diverse teaching staff. The average pupil-teacher ratio was 16 to 1 throughout the District. Texas law mandates that no more than 22 students be assigned to one classroom teacher in kindergarten through grade four. The mission of the Arlington Independent School District is to empower and engage all students to be contributing, responsible citizens reaching their maximum potential through relevant, innovative and rigorous learning experiences. To this end, the District provides regular, special education, career/technology, gifted/talented, and bilingual/ESL curricula in order to meet the needs of the diverse student population. Additionally, a broad range of electives, extra-curricular, and concentrated advanced academic programs are also offered to enhance learning opportunities beyond core curriculum. AISD currently offers the International Baccalaureate World School Program at four of its high schools. The District also offers an Advanced Placement program that gives students the opportunity to graduate with 30 or more college credits and also offers dual-credit choices so that students at each high school can take advantage of earning on-site AISD and Tarrant County College credits. Governance The District is under the control and management of a board of seven trustees, each of whom is elected by the District’s registered voters to serve a three year term. All of the trustees are elected at-large and serve without compensation. The elections are staggered so that not all positions are voted on during the same year. In general, the Board adopts policies, sets direction for curriculum, employs the Superintendent and oversees the operations of the District and its schools. Besides general Board business, Trustees are charged with numerous statutory regulations including appointing the tax assessor/collector, calling trustee and other school elections and canvassing the results, organizing the Board and electing its officers. The Board is also charged with setting the tax rate, acting on real property matters, setting salary schedules, acting as a board of appeals in personnel and student matters, confirming recommendations for textbook adoptions, and adopting and amending the annual budget.

Local Economy Arlington’s diverse economy and unique location within the D/FW Metroplex drive the city’s growth. Arlington hosts employers from a variety of industries, including defense contractors, an automobile manufacturer, high tech companies, higher education institutions, major finance companies, medical facilities and entertainment companies. The area’s major transportation systems afford area businesses easy access to cities throughout the world. Arlington is only fifteen minutes from D/FW International Airport, one of the

xi

busiest airports in the world. Interstate Highways 20 and 30 are the major east/west arteries through the city. Access to Interstate Highway 35, traversing the United States from Mexico to Canada, is also convenient. Rail transportation is available for both public transportation and freight. Arlington is known as the “Entertainment Capital of Texas.” Each year approximately 6.8 million people visit Arlington. The four main entertainment attractions are: Six Flags Over Texas amusement park; Globe Life Park, home of the Texas Rangers baseball team; Six Flags Hurricane Harbor water park; and AT&T Stadium, home of the Dallas Cowboys. AT&T Stadium has only been in operation for five years, but has already hosted numerous NFL and college games, major concerts, the 2010 NBA All Star game, the Cotton Bowl, Super Bowl XLV, and the 2014 NCAA Final Four. The 2015 NCAA football championship game will be played at AT&T Stadium in January 2015.

Relevant Financial Policies Factors affecting financial control Management of the District has established a comprehensive internal control framework that is designed both to protect the District’s assets from loss, misuse or theft, and to compile sufficient reliable information for the preparation of the District’s financial statements in conformity with GAAP. Because the cost of internal controls should not outweigh their benefits, the District’s comprehensive framework of internal controls has been designed to provide reasonable assurance rather than absolute assurance that the financial statements will be free from material misstatement. Budgetary Control The annual budget serves as the foundation for the District’s financial planning and control. Texas State law requires the Board president to call a Board meeting for the purpose of discussing and adopting the budget and the tax rate. A notice of this meeting must be published at least 10 days but not more than 30 days before the public meeting. The budget must be adopted prior to June 30. The District maintains budgetary controls throughout all of its financial systems. The objective of budgetary controls is to ensure compliance with legal provisions embodied in the official budget adopted by the Board. The Board adopts an official budget for the General Fund, Natural Gas Special Revenue Fund, Debt Service Fund, Capital Projects Fund and Food Service Fund (which is accounted for as an Enterprise Fund). In accordance with procedures prescribed by the State Board of Education, budget amendments that affect the total amount in a fund or functional spending category must be approved by the Board prior to expenditure of funds. The functional level is specified by Board policy as the legal level of budgetary control. Budgetary control is maintained at the organizational level by the encumbrance of estimated purchase amounts prior to the release of purchase orders to vendors. Outstanding encumbrances at the end of the fiscal year are an assignment of fund balance and are treated as expenditures in the subsequent year upon receipt of goods and services.

Major Initiatives Achieve Today. Excel Tomorrow. Strategic Plan Achieve Today. Excel Tomorrow. is a three-year strategic plan adopted by the Board in August 2012. The plan encompasses eleven goals grouped into a framework for success that includes Inspired Learners, Effective Leadership, and an Engaged Community. Strategies to achieve our goals include the following:

• Implement a Managed Performance Empowerment model of school administration to give specific autonomies to high-performing principals;

• Select an instructional model that promotes engagement, critical thinking and student achievement; • Implement workforce development and higher education partnerships to enhance student

opportunities to excel after graduation;

xii

• Create and implement a facilities vision to provide world-class facilities that support the educational process;

• Implement a competitive compensation plan and develop a measurement tool for teacher effectiveness that positively impacts student learning;

• Develop internal teacher, student and administrator leadership training and opportunities; and • Implement a plan to increase engagement with faith-based organizations, businesses, non-profits,

governmental entitites, higher education institutions, and volunteers. Achieve Today. Excel Tomorrow. is a detailed roadmap for students, staff and community that defines where we want to be and how we will get there. The plan does this while maintaining the district’s commitment to utilize our resources in the most efficient way possible. To Achieve Texas Education Agency 2014 Satisfactory or Advanced Performance Status AISD was rated “Met Standard” for 2014 by the Texas Education Agency, and 34 schools received distinction designations. To help our students and schools perform at high levels, resources have been committed to develop and implement a system of academic interventions, to reduce course and subject failure rates, to develop subject area vertical alignment, to more fully engage families and the community in the education process, to prevent campus violence, to reduce the annual dropout rate and improve the student completion rate, and to maintain compliance with State and Federal programs. 2014 Bond Program On May 10, 2014, AISD voters approved a $663.1 million bond proposition with an approval rate of almost 70 percent. This five-year program will transform the District and our community. Proceeds of the bond issue will be used to build new facilities, upgrade and renovate existing facilities, address safety and security district-wide, upgrade technology infrastructure and equipment, expand access to technology, provide fine arts equipment and address transportation needs. A 38-member Capital Needs Steering Committee recommended the bond package based on a comprehensive facilities assessment, enrollment forecasts and program priorities identified through community questionnaires and surveys. Construction projects will begin during the 2014-2015 school year and are scheduled to be completed in 2019. Twelve architecture firms have been selected to design the 21 construction and renovation projects in phases 1 and 2 of the bond program, and stakeholder committees are currently developing educational specifications for three of those projects. Educational specifications illustrate the goals and outcomes, activities to be conducted, persons to be served, spatial relationships of program areas, equipment needs, technology needs, and any special considerations for an instructional facility. Teachers, parents, students, administrators and industry specialists make up the stakeholder committees. New construction projects currently in design include two dual language/fine arts academies, a districtwide Career and Technical Center, multi-purpose activity centers for our six high schools, a classroom addition at one junior high school and two new elementary schools. Other purchases made this fall as part of the 2014 bond program include 36 buses, 39 white fleet vehicles and 43 copiers. Planning is underway for network infrastructure upgrades and fine arts purchases scheduled for phase 1 of the program. Instructional Model AISD is implementing an instructional model that promotes engagement, creativity, critical thinking and student achievement as part of our Achieve Today. Excel Tomorrow. strategic plan. An instructional model is designed to maximize student success by providing a common framework for research-based instructional planning, instructional delivery and assessment. A 41-member Instructional Model Committee consisting of teachers, campus administrators, parents, curriculum and instructional staff, and community members underwent the instructional model selection process and recommended the Seven Strategies of Assessment for Learning model based on the research of Dr. Rick Stiggins with the goal to engage students in thinking about themselves as learners. The model is based on three questions from the students’ point of view:

xiii

• Where am I going?

o Strategy 1: Provide students with a clear and understandable vision of the learning target. o Strategy 2: Use examples and models of strong and weak work.

• Where am I now? o Strategy 3: Offer regular descriptive feedback. o Strategy 4: Teach students to self-assess and set goals.

• How can I close the gap? o Strategy 5: Design lessons to focus on one learning target or aspect of quality at a time. o Strategy 6: Teach students focused revision. o Strategy 7: Engage students in self-reflection, and let them keep track and stare their learning.

Initial implementation of the instructional model began in January 2014 with school pilot groups. Phase I of system-wide implementation began in the fall of 2014. 2009 Bond Program Work is wrapping up on a $197.5 million bond package approved in November 2009. Bond proceeds were used to fund new construction, two new science labs at each high school, fine arts equipment and uniforms, technology and new propane-fueled buses. Construction projects will help relieve overcrowding at a number of locations by providing one new elementary school, classroom additions at two elementaries and Lamar High School, and expansion of the Arlington High School cafeteria and kitchen. The remaining $17.6 million of bonds authorized in the 2009 bond package were sold during the 2013-14 fiscal year. All work is scheduled to be completed during the 2014-2015 school year, and the overall bond program is expected to have a budget surplus. A citizens bond oversight committee meets quarterly to review bond program activities and reports its findings and recommendations to the Board semi-annually. Other Major Initiatives Other major initiatives include the development of programming to support transformational learning opportunities for students and implementation of recommendations for a curriculum audit completed in 2013. Also, in alignment with the district’s strategic plan, initial implementation of Positive Behavioral Interventions and Supports (PBIS) has begun with the goal to improve student academic and behavior outcomes. PBIS emphasizes systems development guided by six important principles:

• Develop a continuum of scientifically based behavior and academic interventions and supports • Use data to make decisions and solve problems • Arrange the environment to prevent the development and occurrence of problem behavior • Teach and encourage pro-social skills and behaviors • Implement evidence-based behavioral practices with fidelity and accountability • Screen universally and monitor student performance and progress continuously

PBIS focuses on the establishment of the behavioral supports and social culture for students to achieve academic success through learning environments that are engaging and responsive.

Long-term Financial Planning The Board recognizes the significance of adopting balanced budgets, sustaining a healthy fund balance, and long-range financial planning. To these ends, the Board has adopted a policy that sets forth parameters for annual budget development and targets the unassigned General Fund fund balance at two-months of operating expenditures. The parameters include prioritizing resources into programs that promote student achievement growth, maintaining competitive compensation to attract and retain a highly qualified workforce, board approval of staffing ratios, balancing the budget with limited use of surplus fund balance for one-time expenditures, and

xiv

prioritizing any necessary reductions in areas that have the least impact on instruction. Multi-year budget forecasts are presented to the Board each summer and are considered by the Board when evaluating the impact of potential new initiatives. Strategies included in the Achieve Today. Excel Tomorrow. Strategic Plan focus resources and long-range planning on District priorities in a manner that will help protect the District’s financial well-being. On August 28, 2014, State District Court Judge John Dietz ruled the Texas school finance system unconstitutional. The ruling was issued in a case brought by five plaintiff groups and one intervener. Arlington ISD is a member of the Texas Taxpayer and Student Fairness Coalition (“Coalition”), a coalition of more than 400 school districts that is one of the plaintiff groups suing the State. Judge Dietz ruled that the system is inadequate, arbitrary, inequitable and has created a de facto statewide ad valorem tax in violation of the state constitution. He further ruled that the system is unsuitable for the provision of the constitutionally-required general diffusion of knowledge. Judge Dietz issued an initial verbal ruling that the school finance system was unconstitutional in February 2013. He reopened the case in January 2014 to consider whether changes made to the funding system by the 83rd Texas Legislature in spring 2013 were sufficient to alter his initial ruling. The 83rd Texas Legislature restored $3.4 billion of the $5.4 billion it cut from public education during the 2011 legislative session. While most districts benefited from the additional appropriation, Judge Dietz ruled that the legislature made no changes to the formula structure to correct equity and adequacy claims set forth in the Coalition’s lawsuit. The State will appeal the case directly to the Texas Supreme Court, and a final ruling expected by early 2016. A special session could be called in spring/summer of 2016, if necessary, to address the Supreme Court’s ruling. While no overhaul of the state school finance formulas is expected prior to the Texas Supreme Court ruling in the school finance lawsuit, it is reasonably expected that the 84th Texas Legislature will increase the appropriation of funds for public education when it convenes in spring 2015. State revenue is trending higher than budgeted in the 2014-15 state budget biennium, and indications are that sufficient revenues will be available to increase appropriations to public education for the 2016-17 biennium.

Awards and Acknowledgements Innovative programs, teachers and volunteers are all key to the success of AISD students. TEA currently rates each district and campus as “Met Standard” or “Improvement Required.” AISD has a district rating of “Met Standard,” and 70 AISD campuses are rated Met Standard. Four campuses are rated “Improvement Required.” This year the District is continuing its efforts to improve and is working toward a goal of having the District and all schools achieving the Met Standard rating for 2015 Accountability. The Government Finance Officers Association (“GFOA”) awarded a Certificate of Achievement for Excellence in Financial Reporting to the Arlington Independent School District for its comprehensive annual financial report for the year ended June 30, 2013. This was the 35th consecutive year that the Arlington Independent School District has received this prestigious award. In order to be awarded a Certificate of Achievement, the District published a comprehensive annual financial report that was easy to read and was efficiently organized. This report satisfied both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program's requirements, and we are submitting it to the GFOA to determine its eligibility for another certificate. Additionally, the Association of School Business Officials International (“ASBO”) awarded a Certificate of Excellence in Financial Reporting by School Systems to the Arlington Independent School District for the 25th consecutive year. The Certificate of Excellence in Financial Reporting for School Systems Program is a voluntary program sponsored by ASBO to foster excellence in the preparation and issuance of school system financial reports. A Certificate of Excellence is awarded to those school systems that have voluntarily submitted

xv

their comprehensive annual financial report (“CAFR”) for review by an ASBO Panel of Review. Upon completion of a vigorous technical review, the panel of review members concluded that the Arlington Independent School District’s financial report met the criteria for excellence in financial reporting. We believe that our current CAFR continues to meet the requirements of the Certificate of Excellence in Financial Reporting by School Systems program, and we are submitting it to ASBO to determine its eligibility for another certificate. The preparation of this report on a timely basis could not be accomplished without the efficient and dedicated services of the entire staff of the finance department. We would like to express our appreciation to all members of the department who assisted and contributed to the preparation of this report. We would also like to thank the members of the Board of Trustees for their interest and support in planning and conducting the financial operations of the District in a responsible and progressive manner.

xvi

xvii

xviii

FINANCIAL SECTION

Houston Offi ce 3411 Richmond AvenueSuite 500Houston, Texas 77046713.621.1515 Main

whitleypenn.com

An IndependentMember of

Dallas Fort Worth Houston

1

REPORT OF INDEPENDENT AUDITORS To the Board of Trustees Arlington Independent School District Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund and the aggregate remaining fund information of Arlington Independent School District (the “District”) as of and for the year ended June 30, 2014, and the related notes to financial statements, which collectively comprise the District’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due fraud or error. Auditor’s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall financial statement presentation. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

To the Board of Trustees Arlington Independent School District

2

Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the District as of June 30, 2014, and the respective changes in financial position, the respective budgetary comparison schedule for the general fund and, where applicable, cash flows thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 7 through 23 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of the financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the District’s basic financial statements. The combining and individual nonmajor fund financial statements, TEA required schedules and other supplementary information, as listed in the table of contents, and schedule of expenditures of federal awards, as required by Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and the other information, such as the introductory and statistical section are presented for the purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual nonmajor fund financial statements, TEA required schedules and other supplementary information, as listed in the table of contents, and the schedule of federal awards is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual nonmajor fund financial statements, TEA required schedules and other supplementary information, as listed in the table of contents, and the schedule of federal awards is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

To the Board of Trustees Arlington Independent School District

3

The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on it. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated November 20, 2014, on our consideration of the District’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the District’s internal control over financial reporting and compliance.

Houston, Texas November 20, 2014

4

5

MANAGEMENT’S DISCUSSION AND ANALYSIS

6

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

7

In this section of the Comprehensive Annual Financial Report, we, the managers of Arlington Independent School District (“District”), discuss and analyze the District’s financial performance for the fiscal year ended June 30, 2014. We encourage readers to consider the information presented here in conjunction with additional information furnished in our letter of transmittal on pages ix - xv, the independent auditors’ report on pages 1 through 3, and the District’s basic financial statements which begin on page 27. FINANCIAL HIGHLIGHTS The assets and deferred outflows of the District exceeded its liabilities at the close of the fiscal

year by $320,239,195 (net position). Of this amount $219,267,502 (unrestricted net position), or 68%, may be used to meet the District’s ongoing obligations.

The District’s total net position increased by $39,922,434. The factors that substantially contributed to increases in revenue included the net effect of changes in property tax collections due to higher property values, increased state revenue due to state funding cuts being restored by the 83rd Texas Legislature, and the recognition of prior year state aid in the current year because funds were received beyond the allowable 60-day year-end accrual period, netted against lower student enrollment. The factors that substantially contributed to net increases in expenditures included increases in payroll costs for pay increases and new positions, contracted services for a state backed energy conservation retrofit project, library books and summer book backpacks funded through grants, and capital purchases.

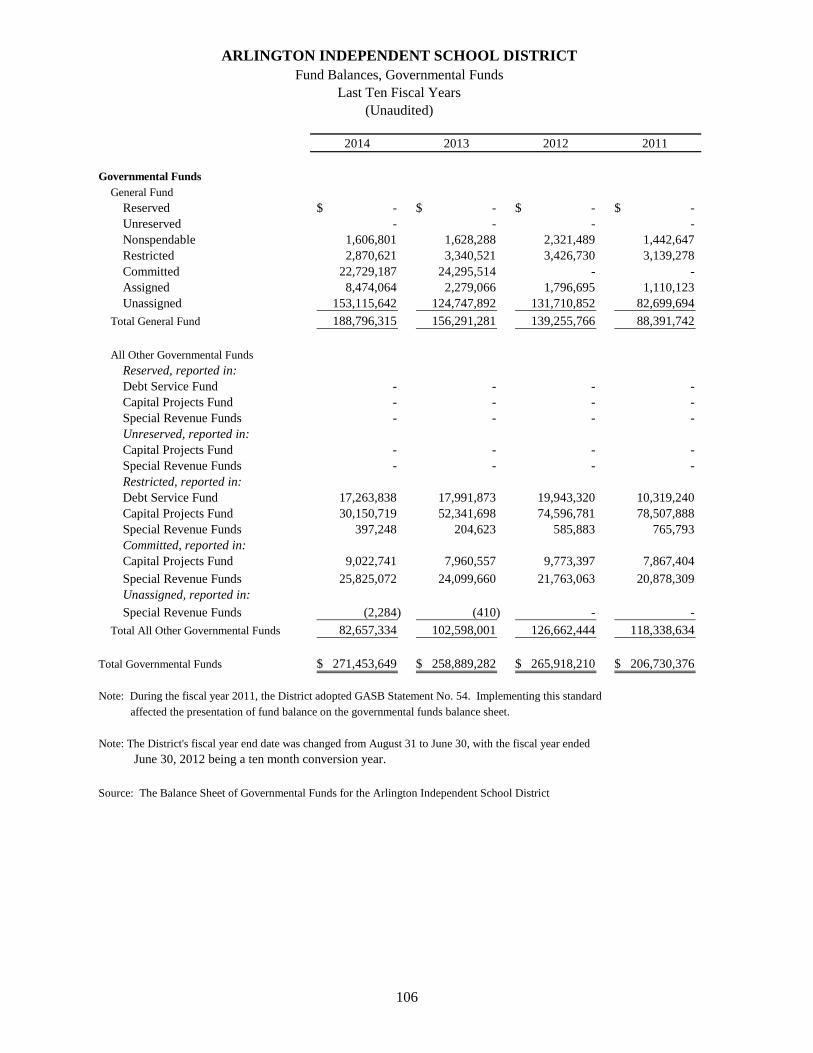

As of the close of the fiscal year, the District’s governmental funds reported combined ending fund balances of $271,453,649, which is $12,564,364 more than the previous year. 56% of the combined fund balance, $153,113,358, is available for spending at the District’s discretion (unassigned balance).

USING THIS ANNUAL REPORT The annual report consists of a series of financial statements, notes to those statements, and other supplementary information. The basic financial statements include two types of statements that present different views of the District:

1) Government-wide financial statements provide information about the activities of the District as a whole and present both a long-term and short-term view of the District’s finances. The government-wide financial statements include the Statement of Net Position and the Statement of Activities (on pages 27 through 29).

2) Fund financial statements (starting on page 30) report the District’s operations in more detail

than the government-wide statements by providing information about the District’s most significant funds. For general governmental activities, these statements tell how services were financed in the short term as well as what resources remain for future spending. For proprietary activities, fund financial statements tell how goods or services of the District were sold to external customers and how funds were accumulated and costs were allocated internally among various functions. The remaining fund financial statement, the fiduciary statement, provides financial information about activities for which the District acts solely as a trustee or agent for the benefit of parties outside of the District. The fiduciary statement can be found on page 41.

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

8

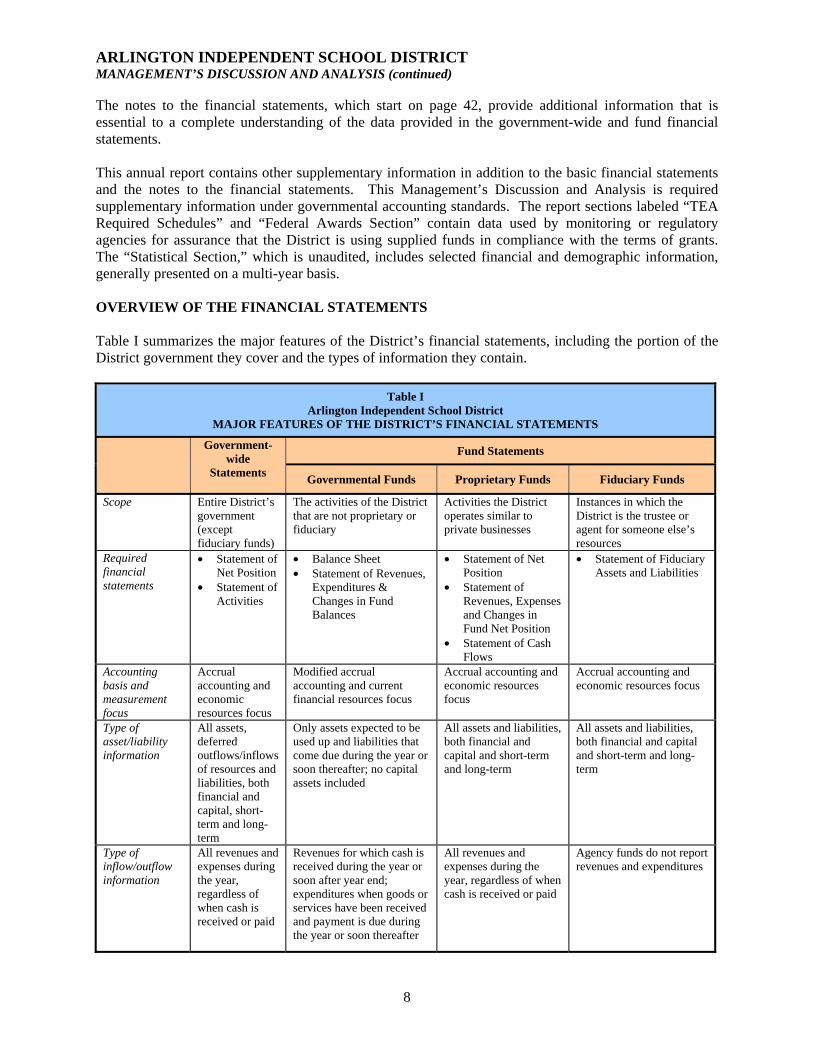

The notes to the financial statements, which start on page 42, provide additional information that is essential to a complete understanding of the data provided in the government-wide and fund financial statements. This annual report contains other supplementary information in addition to the basic financial statements and the notes to the financial statements. This Management’s Discussion and Analysis is required supplementary information under governmental accounting standards. The report sections labeled “TEA Required Schedules” and “Federal Awards Section” contain data used by monitoring or regulatory agencies for assurance that the District is using supplied funds in compliance with the terms of grants. The “Statistical Section,” which is unaudited, includes selected financial and demographic information, generally presented on a multi-year basis. OVERVIEW OF THE FINANCIAL STATEMENTS Table I summarizes the major features of the District’s financial statements, including the portion of the District government they cover and the types of information they contain.

Table I Arlington Independent School District

MAJOR FEATURES OF THE DISTRICT’S FINANCIAL STATEMENTS

Government-wide

Statements

Fund Statements

Governmental Funds Proprietary Funds Fiduciary Funds

Scope Entire District’s government (except fiduciary funds)

The activities of the District that are not proprietary or fiduciary

Activities the District operates similar to private businesses

Instances in which the District is the trustee or agent for someone else’s resources

Required financial statements

• Statement of Net Position

• Statement of Activities

• Balance Sheet • Statement of Revenues,

Expenditures & Changes in Fund Balances

• Statement of Net Position

• Statement of Revenues, Expenses and Changes in Fund Net Position

• Statement of Cash Flows

• Statement of Fiduciary Assets and Liabilities

Accounting basis and measurement focus

Accrual accounting and economic resources focus

Modified accrual accounting and current financial resources focus

Accrual accounting and economic resources focus

Accrual accounting and economic resources focus

Type of asset/liability information

All assets, deferred outflows/inflows of resources and liabilities, both financial and capital, short-term and long-term

Only assets expected to be used up and liabilities that come due during the year or soon thereafter; no capital assets included

All assets and liabilities, both financial and capital and short-term and long-term

All assets and liabilities, both financial and capital and short-term and long-term

Type of inflow/outflow information

All revenues and expenses during the year, regardless of when cash is received or paid

Revenues for which cash is received during the year or soon after year end; expenditures when goods or services have been received and payment is due during the year or soon thereafter

All revenues and expenses during the year, regardless of when cash is received or paid

Agency funds do not report revenues and expenditures

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

9

Government-wide Financial Statements The government-wide financial statements – consisting of the Statement of Net Position and the Statement of Activities – report information about the District as a whole. These statements are designed to provide readers with a broad overview of the District’s finances. The government-wide statements apply the accrual basis of accounting, which is similar to the accounting basis used by most private-sector companies. The Statement of Net Position includes all of the District’s assets, liabilities, and deferred inflows/outflows of resources, with the difference reported as net position. The Statement of Activities presents information showing how the District’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. The two government-wide financial statements report the District’s net position and changes in them. Net position (the difference between assets, deferred inflows/outflows and liabilities) provide one measure of the District’s financial health, or financial position. Over time, increases or decreases in the District’s net position are one indicator of whether its financial health is improving or deteriorating. To fully assess the overall health of the District, however, you should consider additional factors as well, such as changes in the District’s property tax base, state funding, or its average daily attendance and the condition of the District’s facilities. In the Statement of Net Position and the Statement of Activities, we divide the District into two kinds of activities: Governmental activities – Most of the District’s basic services are reported here, including

instruction, student support services, transportation, maintenance, and general administration. Property taxes, state aid, and state and federal grants finance most of these activities.

Business-type activities – The District’s food service operation is reported here. The District

charges a fee to “customers” to help it cover the cost of services it provides in the food and nutrition program.

Fund Financial Statements The fund financial statements provide detailed information about the District’s most significant funds, as opposed to the District as a whole. Laws and bond covenants require the District to establish some funds, such as grants received under the No Child Left Behind Act from the U.S. Department of Education. The District’s administration establishes other funds to help it control and manage money for particular purposes. The three kinds of funds used by the District – governmental, proprietary and fiduciary – use different accounting approaches:

Governmental funds – Most of the District’s basic services are reported in governmental funds. These funds use modified accrual accounting (an accounting method that measures the receipt and disbursement of cash and all other financial assets that can be readily converted to cash) and report balances that are available for future spending. The governmental fund statements provide a detailed short-term view of the District’s general operations and the basic services it provides. Governmental fund information helps users determine the availability of financial resources to finance the District’s programs. We describe the differences between governmental activities (reported in the Statement of Net Position and the Statement of Activities) and governmental funds in reconciliation schedules following each of the fund financial statements.

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

10

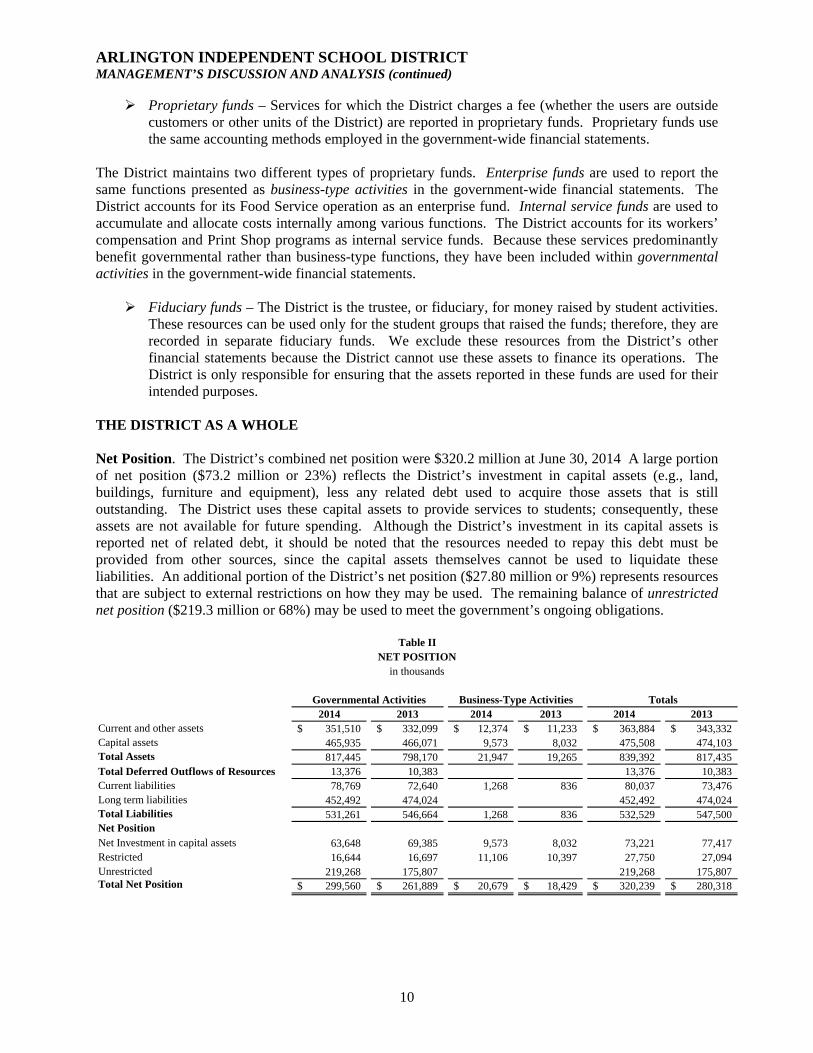

Proprietary funds – Services for which the District charges a fee (whether the users are outside customers or other units of the District) are reported in proprietary funds. Proprietary funds use the same accounting methods employed in the government-wide financial statements.

The District maintains two different types of proprietary funds. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The District accounts for its Food Service operation as an enterprise fund. Internal service funds are used to accumulate and allocate costs internally among various functions. The District accounts for its workers’ compensation and Print Shop programs as internal service funds. Because these services predominantly benefit governmental rather than business-type functions, they have been included within governmental activities in the government-wide financial statements.

Fiduciary funds – The District is the trustee, or fiduciary, for money raised by student activities. These resources can be used only for the student groups that raised the funds; therefore, they are recorded in separate fiduciary funds. We exclude these resources from the District’s other financial statements because the District cannot use these assets to finance its operations. The District is only responsible for ensuring that the assets reported in these funds are used for their intended purposes.

THE DISTRICT AS A WHOLE Net Position. The District’s combined net position were $320.2 million at June 30, 2014 A large portion of net position ($73.2 million or 23%) reflects the District’s investment in capital assets (e.g., land, buildings, furniture and equipment), less any related debt used to acquire those assets that is still outstanding. The District uses these capital assets to provide services to students; consequently, these assets are not available for future spending. Although the District’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the District’s net position ($27.80 million or 9%) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net position ($219.3 million or 68%) may be used to meet the government’s ongoing obligations.

Governmental Activities Business-Type Activities Totals2014 2013 2014 2013 2014 2013

Current and other assets 351,510$ 332,099$ 12,374$ 11,233$ 363,884$ 343,332$ Capital assets 465,935 466,071 9,573 8,032 475,508 474,103 Total Assets 817,445 798,170 21,947 19,265 839,392 817,435 Total Deferred Outflows of Resources 13,376 10,383 13,376 10,383 Current liabilities 78,769 72,640 1,268 836 80,037 73,476 Long term liabilities 452,492 474,024 452,492 474,024 Total Liabilities 531,261 546,664 1,268 836 532,529 547,500 Net PositionNet Investment in capital assets 63,648 69,385 9,573 8,032 73,221 77,417 Restricted 16,644 16,697 11,106 10,397 27,750 27,094 Unrestricted 219,268 175,807 219,268 175,807 Total Net Position 299,560$ 261,889$ 20,679$ 18,429$ 320,239$ 280,318$

NET POSITIONin thousands

Table II

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

11

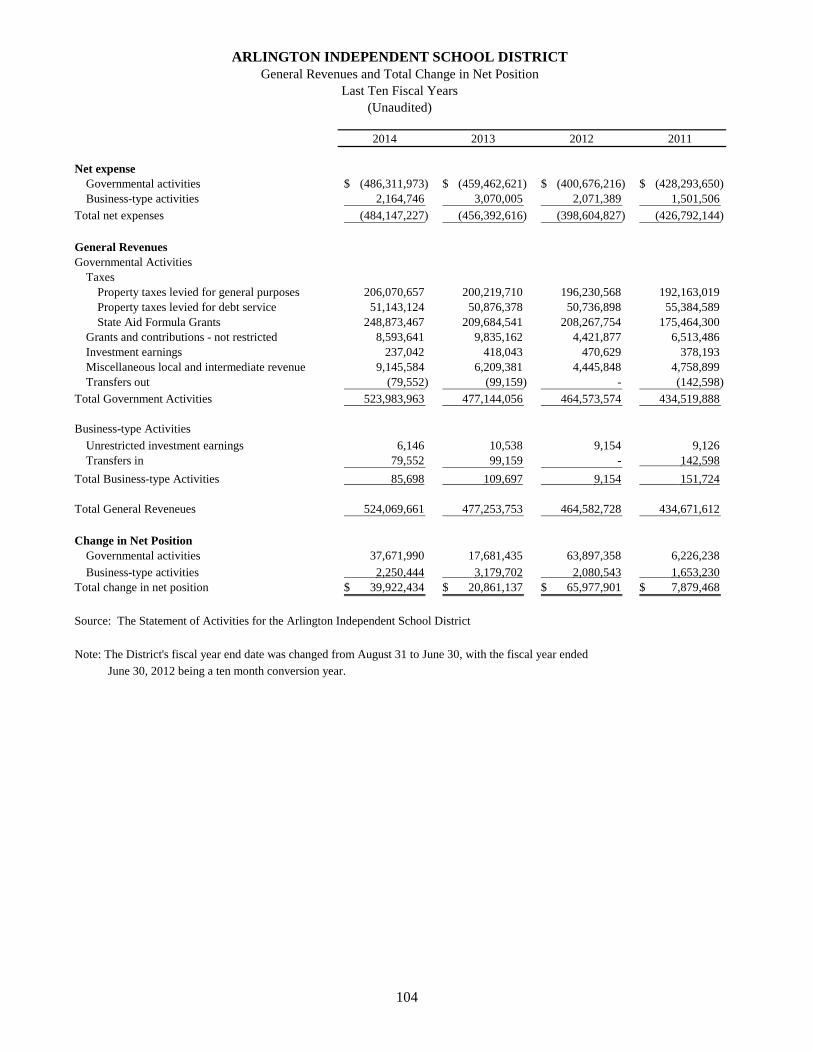

Changes in Net Position. Total net position of the District increased by $39.9 million over last year (see Table III). Governmental activities increased net position by $37.7 million. Business-type activities increased net position by $2.3 million. Following are separate discussions of changes in revenues and expenses for governmental activities and business-type activities. Governmental activities. Revenues from governmental activities were $592.5 million. The cost of all governmental programs and services were $554.8 million. Governmental activities increased net position by $37.7 million

Governmental Activities Business-Type Activities Totals2014 2013 2014 2013 2014 2013

RevenuesProgram Revenues:

Charges for services 2,865$ 2,956$ 6,197$ 6,234$ 9,062$ 9,190$ Operating grants 65,603 62,110 25,902 24,725 91,505 86,835 Capital grants 273 684 273 684

General Revenues:Property taxes 257,214 251,096 257,214 251,096 State Aid - Formula Grants 248,873 209,685 248,873 209,685 Grants and contributions not restricted 8,594 9,835 8,594 9,835 Investment earnings 237 418 6 11 243 429 Other 9,146 6,210 9,146 6,210

Total Revenues 592,532 542,310 32,378 31,654 624,910 573,964

ExpensesInstruction, curriculum and media 365,037 342,749 365,037 342,749 Instructional and school leadership 34,378 32,412 34,378 32,412 Student support services 44,260 41,133 44,260 41,133 Food services 389 432 30,208 28,573 30,597 29,005 Cocurricular activities 9,413 8,833 9,413 8,833 General administration 7,034 6,540 7,034 6,540 Plant maintenance, security and data processing 64,788 63,450 64,788 63,450 Community services 3,180 3,115 3,180 3,115 Debt service 15,486 19,368 15,486 19,368 Facilities repairs and maintenance 1,413 971 1,413 971 Intergovernmental charges 9,402 5,527 9,402 5,527

Total Expenses 554,780 524,530 30,208 28,573 584,988 553,103 Excess (deficiency) before transfers 37,752 17,780 2,170 3,081 39,922 20,861 Transfers (80) (99) 80 99 Increase (Decrease) in Net Position 37,672 17,681 2,250 3,180 39,922 20,861 Net Position - Beginning 261,888 244,207 18,429 15,249 280,317 259,456 Net Position - Ending 299,560$ 261,888$ 20,679$ 18,429$ 320,239$ 280,317$

CHANGES IN NET POSITIONin thousands

Table III

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

12

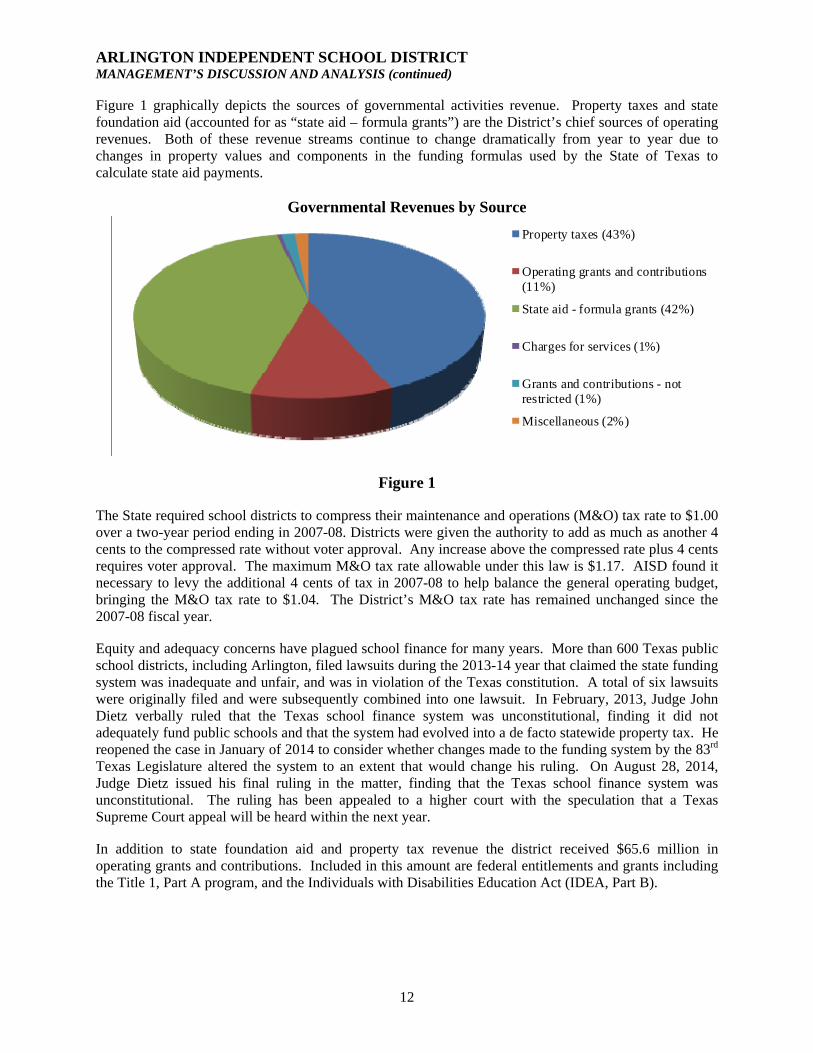

Figure 1 graphically depicts the sources of governmental activities revenue. Property taxes and state foundation aid (accounted for as “state aid – formula grants”) are the District’s chief sources of operating revenues. Both of these revenue streams continue to change dramatically from year to year due to changes in property values and components in the funding formulas used by the State of Texas to calculate state aid payments.

Governmental Revenues by Source

Property taxes (43%)

Operating grants and contributions(11%)

State aid - formula grants (42%)

Charges for services (1%)

Grants and contributions - notrestricted (1%)

Miscellaneous (2%)

Figure 1

The State required school districts to compress their maintenance and operations (M&O) tax rate to $1.00 over a two-year period ending in 2007-08. Districts were given the authority to add as much as another 4 cents to the compressed rate without voter approval. Any increase above the compressed rate plus 4 cents requires voter approval. The maximum M&O tax rate allowable under this law is $1.17. AISD found it necessary to levy the additional 4 cents of tax in 2007-08 to help balance the general operating budget, bringing the M&O tax rate to $1.04. The District’s M&O tax rate has remained unchanged since the 2007-08 fiscal year. Equity and adequacy concerns have plagued school finance for many years. More than 600 Texas public school districts, including Arlington, filed lawsuits during the 2013-14 year that claimed the state funding system was inadequate and unfair, and was in violation of the Texas constitution. A total of six lawsuits were originally filed and were subsequently combined into one lawsuit. In February, 2013, Judge John Dietz verbally ruled that the Texas school finance system was unconstitutional, finding it did not adequately fund public schools and that the system had evolved into a de facto statewide property tax. He reopened the case in January of 2014 to consider whether changes made to the funding system by the 83rd Texas Legislature altered the system to an extent that would change his ruling. On August 28, 2014, Judge Dietz issued his final ruling in the matter, finding that the Texas school finance system was unconstitutional. The ruling has been appealed to a higher court with the speculation that a Texas Supreme Court appeal will be heard within the next year. In addition to state foundation aid and property tax revenue the district received $65.6 million in operating grants and contributions. Included in this amount are federal entitlements and grants including the Title 1, Part A program, and the Individuals with Disabilities Education Act (IDEA, Part B).

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

13

Revenues for governmental activities increased by $50.2 million in 2013-14. The bulk of this increase is due to changes in state aid, property taxes and operating grants. These revenue items are examined in more detail, below: State aid increased by $39.2 million due to the net difference between legislative funding cuts for the

2012-2013 biennium being restored for the 2014-2015 biennium, lower student enrollment, changes in property values, and prior year state aid recognized in the current year because funds were received beyond the allowable 60 day year-end accrual period. The 82nd state legislature reduced the Regular Program Allotment component of the state funding formula to account for a $4 billion shortfall in the state education budget in the 2012-13 biennium. As previously mentioned, these reductions were restored by the 83rd state legislature for the 2014-15 biennium. This increase, netted against the prior year state aid, the effects on state funding formulas of a decrease in student enrollment of 325 students and changes in property values, resulted in the net increase to state aid.

In 2013-14 the District’s M&O taxes increased $6.2 million due to a 4.42% increase in certified property values, and due to increased collection trends.

The District received $3.5 million (or 5.6%) more for operating grants and contributions in 2014 compared to the prior year.

Expenses are summarized by functional categories that reflect the purpose of the transaction. Various operating expenses are recorded within each functional category. Total expenses increased $30.3 million (or 5.8%) over 2013. Increases in the 2014 fiscal year budget are primarily due to increased expenditures for salaries and related benefits, contracted services for energy retrofit projects, reading materials and library books, and capital asset purchases.

Governmental Expenses by Function

Instruction and student-related(80%)

Plant maintenance, security, anddata processing (12%)

Debt service (3%)

Cocurricular activities (1%)

Administration and other (3%)

Community services (1%)

Figure 2

Payroll, accounting for approximately 84% of total expenses, is the most significant operating expense incurred by the District and is recorded in the majority of functional categories. Payroll expenses were $19.4 million (or 4.8%) higher than last year primarily due to: 72.7 new positions added during the staffing process and to staff the new Adams Elementary school campus; additional stipends for academic enrichment, expanded academic offerings, leadership academies and expansion of athletic programs at the junior high schools; a 3.0% across the board pay increases for all employees; increasing beginning teacher salaries to $50,000; equity adjustments for steps 1-20 of the teacher salary schedule; and salary adjustments as a result of a contracted salary market study related to the District’s strategic plan.

ARLINGTON INDEPENDENT SCHOOL DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS (continued)

14