Embed Size (px)

Citation preview

INDUSTRYCOMMISSION

COMPUTER HARDWARESOFTWARE AND

RELATED SERVICEINDUSTRIES

Report No. 46

30 June 1995

Australian Government Publishing Service

Canberra

© Commonwealth of Australia 1995

ISBN 0 644 45472 5

This work is copyright. Apart from any use as permitted under the Copyright Act1968, the work may be reproduced in whole or in part for study or training purposes,subject to the inclusion of an acknowledgement of the source. Reproduction forcommercial usage or sale requires prior written permission from the AustralianGovernment Publishing Service. Requests and concerning reproduction and rightsshould be addressed to the Manager, Commonwealth Information Services,AGPS, GPO Box 84, Canberra ACT 2601.

Industry CommissionLevel 3Nature Conservation HouseCornet Emu Bank & Benjamin WayPO Box 80Belconnen ACT 2616

Produced by the Australian Government Publishing Service

30 June 1995

The Honourable George Gear MPAssistant TreasurerParliament HouseCANBERRA ACT 2600

Dear Assistant Treasurer

In accordance with Section 7 of the Industry Commission Act 1989, we havepleasure in submitting to you the report on the Computer Hardware, Softwareand Related Service Industries.

Yours sincerely

Max Parker Brian JohnsPresiding Commissioner Associate Commissioner

Level 3, Nature Conservation House,

Corner Emu Bank & Benjamin Way, Belconnen ACT 2617

PO Box 80, Belconnen ACT 2616

Telephone: 06 240 3200 • Facsimile: 06 240 3399

v

TABLE OF CONTENTS

Page

Abbreviations xi

Terms of Reference xiv

OVERVIEW 1

KEY FINDINGS AND RECOMMENDATIONS 27

1 THE INQUIRY 35

1.1 Scope of the inquiry 351.2 Key inquiry issues 361.3 Relationship with other inquiries 381.4 Report structure 39

2 INDUSTRY STRUCTURE 41

2.1 Industry data 412.2 The global industries 422.3 The Australian industries 462.4 Strengths and weaknesses 512.5 Participants’ views on the industries’ potential 59

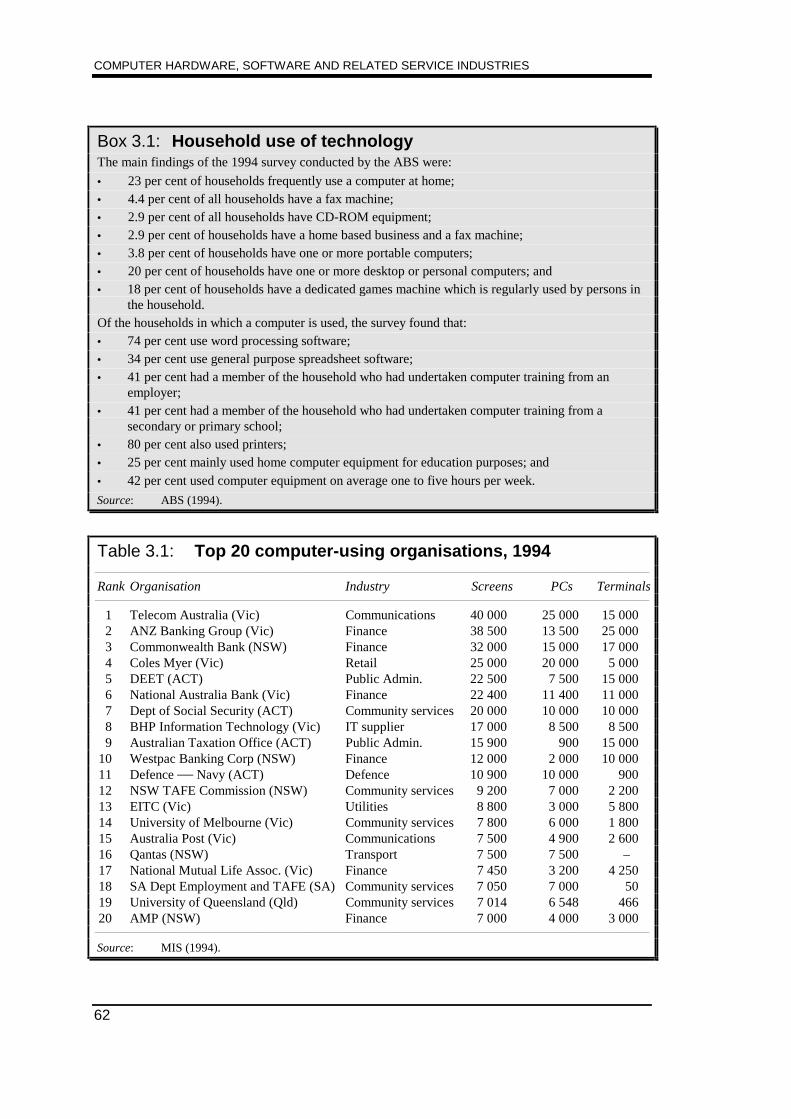

3 MARKETS 61

3.1 Information technology use in Australia 613.2 Global information technology markets 653.3 Asia-Pacific information technology markets 693.4 Australian information technology markets 733.5 Australia’s international trade in information technology 77

4 TRENDS IN TECHNOLOGY 85

4.1 From calculators to the personal computer and beyond 854.2 The plunging costs of computer power 874.3 The changing nature of computing 894.4 Convergence 904.5 Future directions in technology 93

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

vi

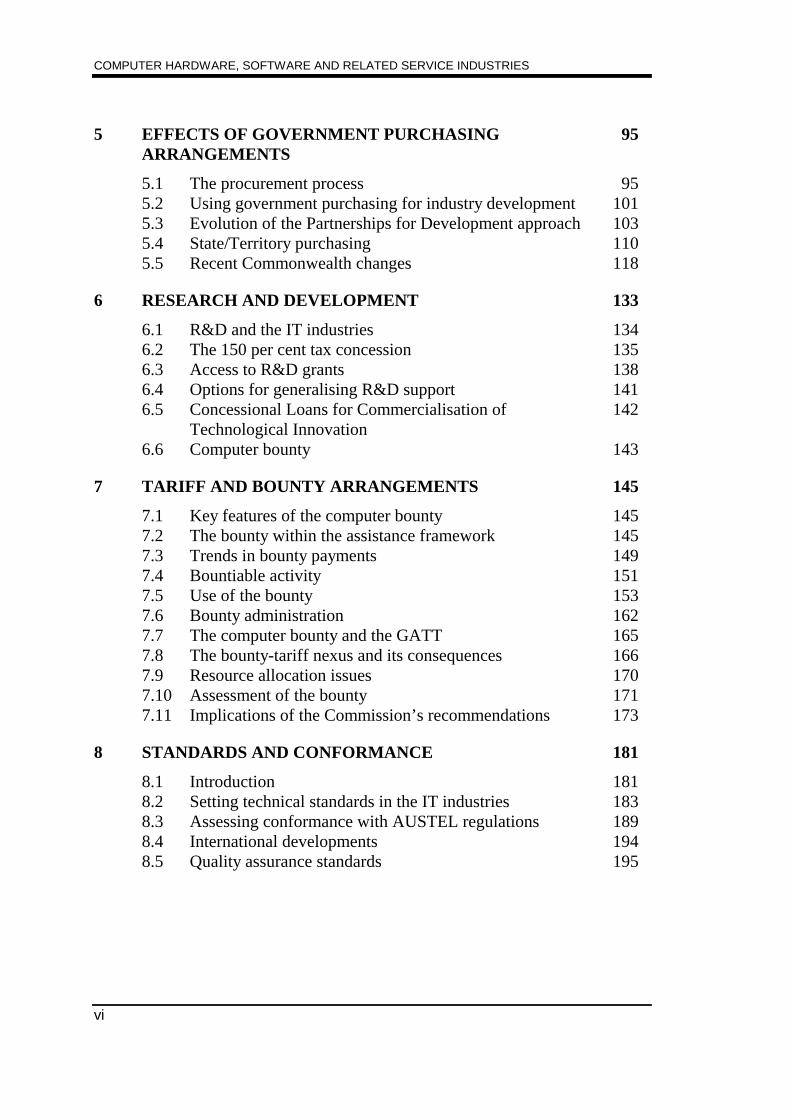

5 EFFECTS OF GOVERNMENT PURCHASING 95ARRANGEMENTS

5.1 The procurement process 955.2 Using government purchasing for industry development 1015.3 Evolution of the Partnerships for Development approach 1035.4 State/Territory purchasing 1105.5 Recent Commonwealth changes 118

6 RESEARCH AND DEVELOPMENT 133

6.1 R&D and the IT industries 1346.2 The 150 per cent tax concession 1356.3 Access to R&D grants 1386.4 Options for generalising R&D support 1416.5 Concessional Loans for Commercialisation of 142

Technological Innovation6.6 Computer bounty 143

7 TARIFF AND BOUNTY ARRANGEMENTS 145

7.1 Key features of the computer bounty 1457.2 The bounty within the assistance framework 1457.3 Trends in bounty payments 1497.4 Bountiable activity 1517.5 Use of the bounty 1537.6 Bounty administration 1627.7 The computer bounty and the GATT 1657.8 The bounty-tariff nexus and its consequences 1667.9 Resource allocation issues 1707.10 Assessment of the bounty 1717.11 Implications of the Commission’s recommendations 173

8 STANDARDS AND CONFORMANCE 181

8.1 Introduction 1818.2 Setting technical standards in the IT industries 1838.3 Assessing conformance with AUSTEL regulations 1898.4 International developments 1948.5 Quality assurance standards 195

vii

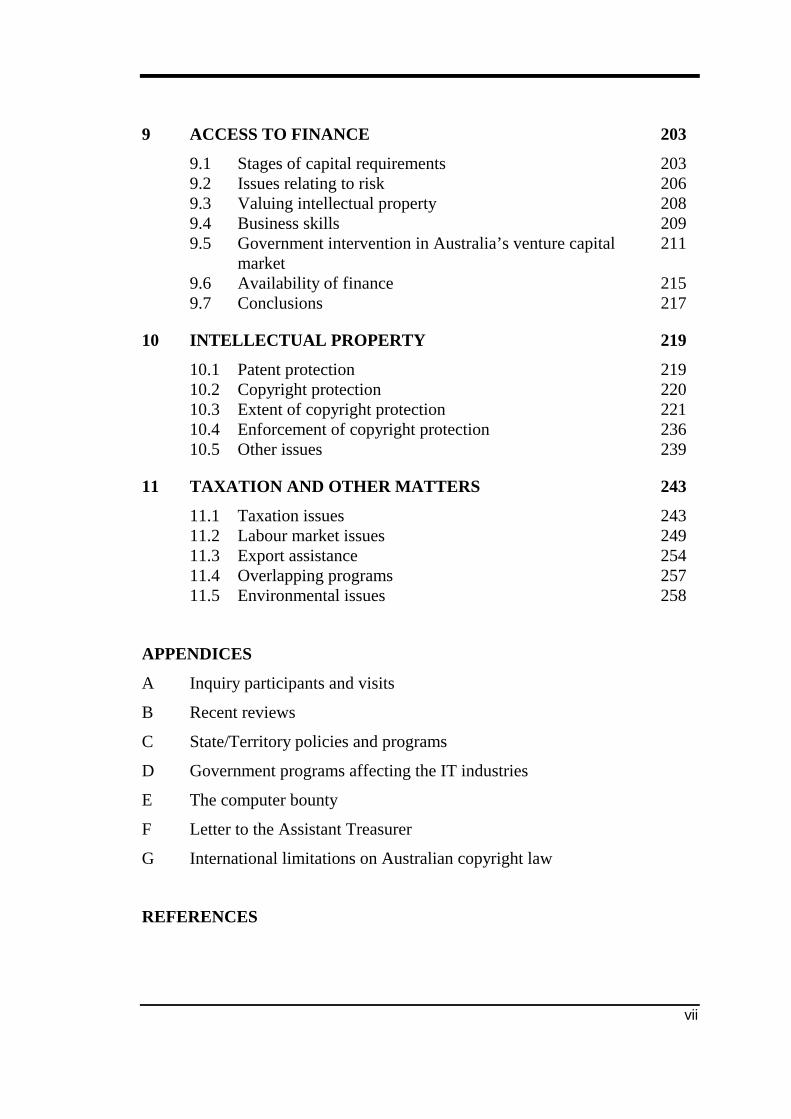

9 ACCESS TO FINANCE 203

9.1 Stages of capital requirements 2039.2 Issues relating to risk 2069.3 Valuing intellectual property 2089.4 Business skills 2099.5 Government intervention in Australia’s venture capital 211

market9.6 Availability of finance 2159.7 Conclusions 217

10 INTELLECTUAL PROPERTY 219

10.1 Patent protection 21910.2 Copyright protection 22010.3 Extent of copyright protection 22110.4 Enforcement of copyright protection 23610.5 Other issues 239

11 TAXATION AND OTHER MATTERS 243

11.1 Taxation issues 24311.2 Labour market issues 24911.3 Export assistance 25411.4 Overlapping programs 25711.5 Environmental issues 258

APPENDICES

A Inquiry participants and visits

B Recent reviews

C State/Territory policies and programs

D Government programs affecting the IT industries

E The computer bounty

F Letter to the Assistant Treasurer

G International limitations on Australian copyright law

REFERENCES

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

viii

LIST OF BOXESPage

2.1 Computer Management Centre 542.2 Intellect Australia — niche hardware and software 542.3 Computer Vision International 562.4 Email Printed Circuits 57

3.1 Household use of technology 62

4.1 The merging of computer, consumer electronics, media and 91telecommunications industries

6.1 Competitive Grants for R&D Scheme 1396.2 Concessional Loans for Commercialisation of Technological 142

Innovation

7.1 A menu of assistance schemes 1567.2 PCB manufacture and the bounty 1607.3 Working Nation initiatives to assist SMEs 161

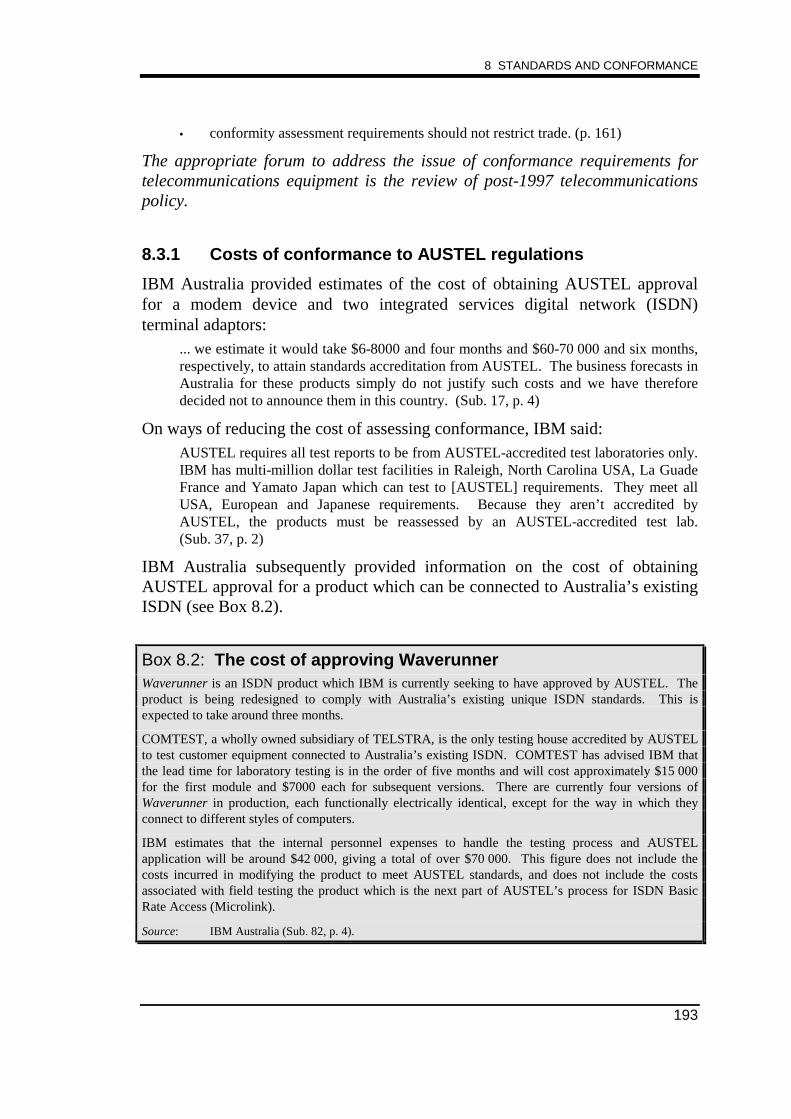

8.1 BIE evaluation of the VQS: summary of recommendations 1828.2 The cost of approving Waverunner 193

G.1 Articles of the Berne Convention which deal with copyright G2protection for computer programs

LIST OF TABLESPage

2.1 Global IT revenues, 1993 422.2 Global top 10 IT companies (by revenue), 1990 to 1993 432.3 Number of IT firms in Australia, 30 June 1993 472.4 Employment size of specialist IT firms in Australia, 30 June 1993 482.5 Revenue from Australian IT production, 1992-93 482.6 Top 10 IT companies in Australia, 1993 50

3.1 Top 20 computer-using organisations, 1994 623.2 IT expenditure by product category, 1993 643.3 IT expenditure by Commonwealth Government departments, 64

1993 and 1994

ix

3.4 Global IT sales revenues by market segment 683.5 Regional demand and supply of IT, 1987 and 1992 683.6 Asia-Pacific IT sales revenue by market segment 723.7 Country share of the Asia-Pacific IT market (excluding Japan), 72

1993 and 19973.8 Australian IT sales revenue by market segment 763.9 Share of total IT merchandise imports and exports by region and 78

country, 1993-943.10 Exports of IT commodities by region and selected countries, 80

1993-943.11 Australia’s top 10 IT export revenue earners, 1992 and 1993 783.12 Imports of IT commodities by region and selected countries, 84

1993-94

4.1 The changing nature of computing 89

7.1 Bounty and tariff assistance to the IT&T industries 1487.2 Bounty payments over $1 million, 1991-92 to 1993-94 1517.3 Bountiable research and development, 1992-93 1577.4 Assistance scenarios 177

9.1 Australian private venture capital industry (estimated base), 2121983 to 1991

9.2 ADCAL funds under management 2169.3 Investments by industry: Australia and USA, 1992-93 216

11.1 Employment in the IT industries, 1983-84 to 1992-93 25011.2 Graduates in IT-related disciplines, 1988 to 1992 25111.3 Destination of graduates, 1992 25111.4 Permanent and long-term migration of skilled labour, 253

1986-87 to 1992-9311.5 Awareness and use of export assistance programs 25511.6 Awareness, eligibility and use of export programs 255

B.1 Stages in the tender process B9

E.1 Bounty rate E4E.2 Gazette Notices pertaining to the Bounty (Computer) Act E6E.3 Materials to output ratio and nominal rate on materials, E9

1994-95 and 1996-97E.4 Computer bounty: claimants and total, average and median E11

payments, 1984-85 to 1993-94

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

x

LIST OF FIGURESPage

3.1 Top 100 computer-using organisations by industry 633.2 Global IT sales revenue: hardware, 1989 to 1998 663.3 Global IT sales revenue: software and related services, 67

1989 to 19983.4 Global IT sales revenue by region, 1993 and 1998 693.5 Asia-Pacific IT sales revenue: hardware, 1989 to 1998 703.6 Asia-Pacific IT sales revenue: software and related services, 71

1989 to 19983.7 Australian IT sales revenue: hardware, 1989 to 1998 743.8 Australian IT sales revenue: software and related service 75

industries, 1989 to 19983.9 Sales of IT hardware, packaged software and IT services in 76

Australia, 1983-84 to 1992-933.10 Production, imports and exports of IT commodities: Australia, 77

1992-933.11 Australian exports of IT hardware, packaged software and IT 79

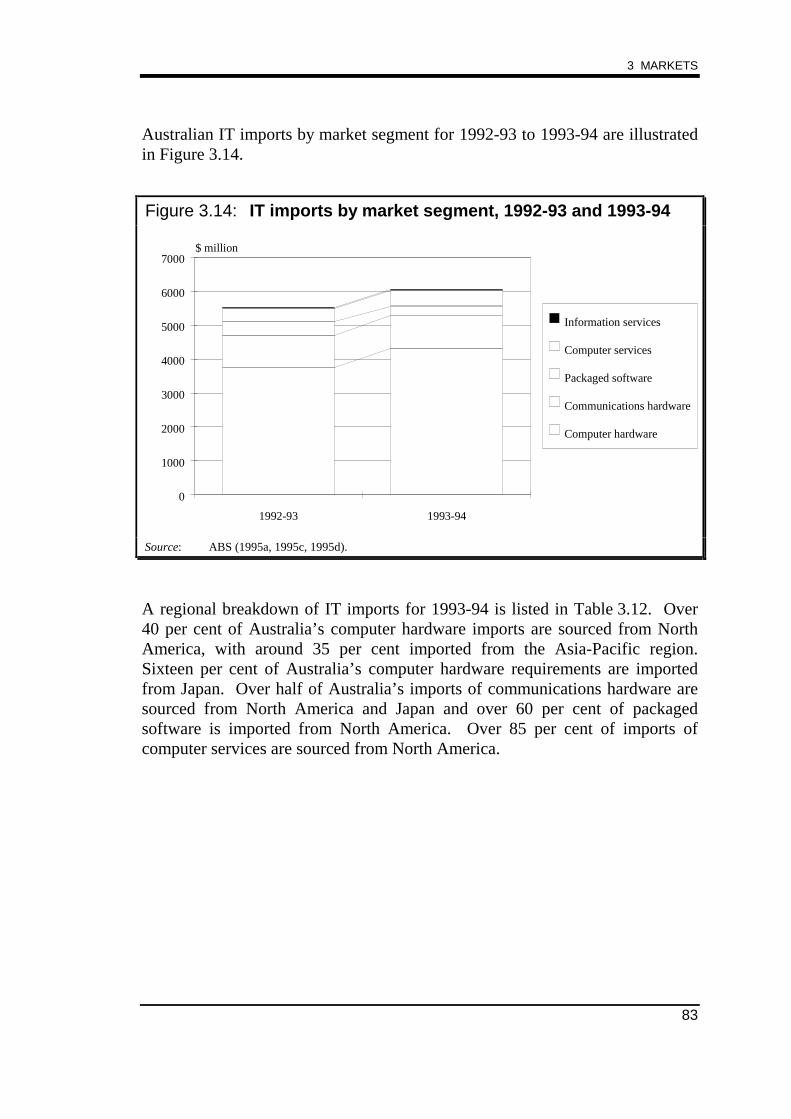

services, 1983-84 to 1992-933.12 IT exports by market segment, 1992-93 to 1994-94 813.13 Australian imports of IT hardware, packaged software and IT 82

services, 1983-84 to 1992-933.14 IT imports by market segment, 1992-93 and 1993-94 83

4.1 Chip density in Intel microprocessors, 1971 to 1993 874.2 Average selling prices for PCs, 1991 to 1995 884.3 Price of mainframe MIPS, 1974 to 1993 88

7.1 Bounty rate and effective assistance for manufacturing 1477.2 Bounty claimants and payments, 1984-85 to 1993-94 1497.3 Average and median bounty payments, 1984-85 to 1993-94 1507.4 Bountiable activity, 1992-93 152

E.1 Centile breakdown of bounty payments, 1991-92 (adjusted) E5and 1993-94

xi

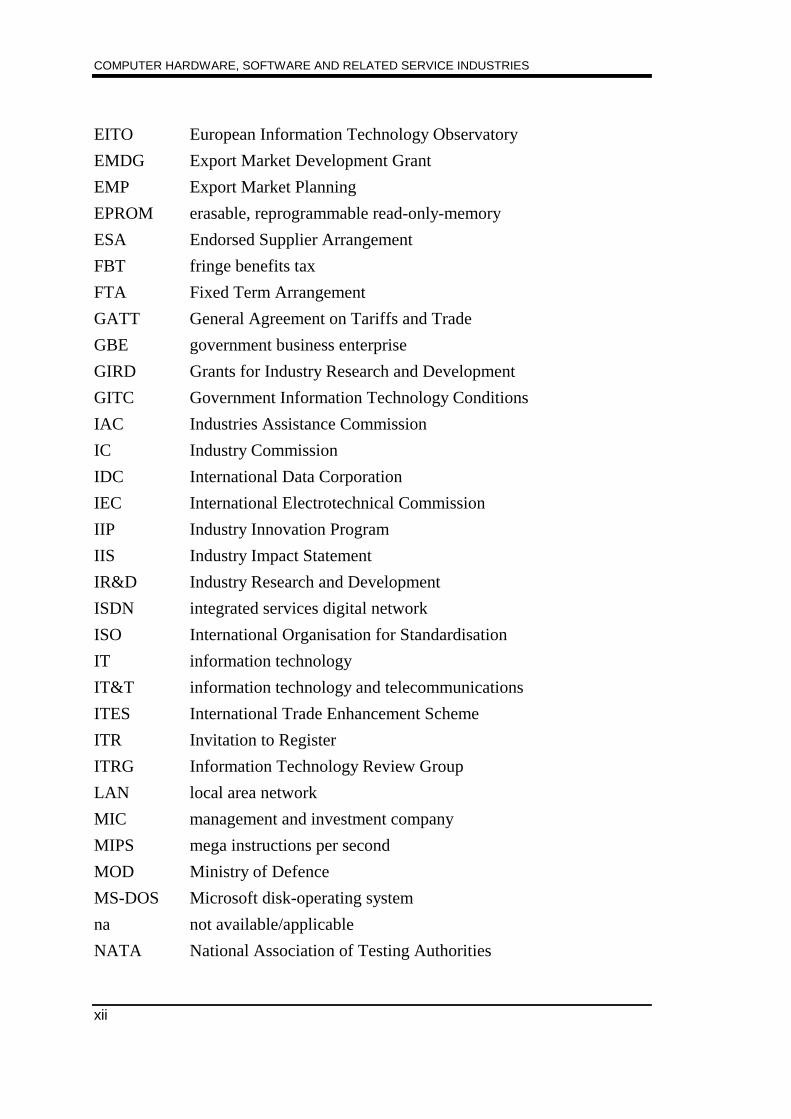

ABBREVIATIONS

ABS Australian Bureau of Statistics

ADCAL Australian Development Capital Association Limited

ADP automatic data processing

AEMS Australian Electronic Manufacturing Services

AEEMA Australian Electrical and Electronic Manufacturers’ Association

AIIA Australian Information Industry Association

ANAO Australian National Audit Office

ANZ Australia and New Zealand

APCMA Australian Printed Circuit Manufacturers’ Association

AS Australian Standard

ASIC Australian Standard Industrial Classification

ASQRI Australian Software Quality Research Institute

ATG Australian Technology Group

ATIA Australian Telecommunications Industry Association

ATO Australian Taxation Office

BIE Bureau of Industry Economics

BSAA Business Software Association of Australia

CCG Copyright Convergence Group

CD-ROM compact disk read-only-memory

CLRC Copyright Law Review Committee

COAG Council of Australian Governments

CRATMA Canberra Region Advanced Technology ManufacturingAssociation

CUC Common Use Contract

DAS Department of Administrative Services

DCTWA Western Australian Department of Commerce and Trade

DIST Department of Industry, Science and Technology

EFIC Export Finance and Insurance Corporation

EIAWA Electronic Industries Association of Western Australia

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

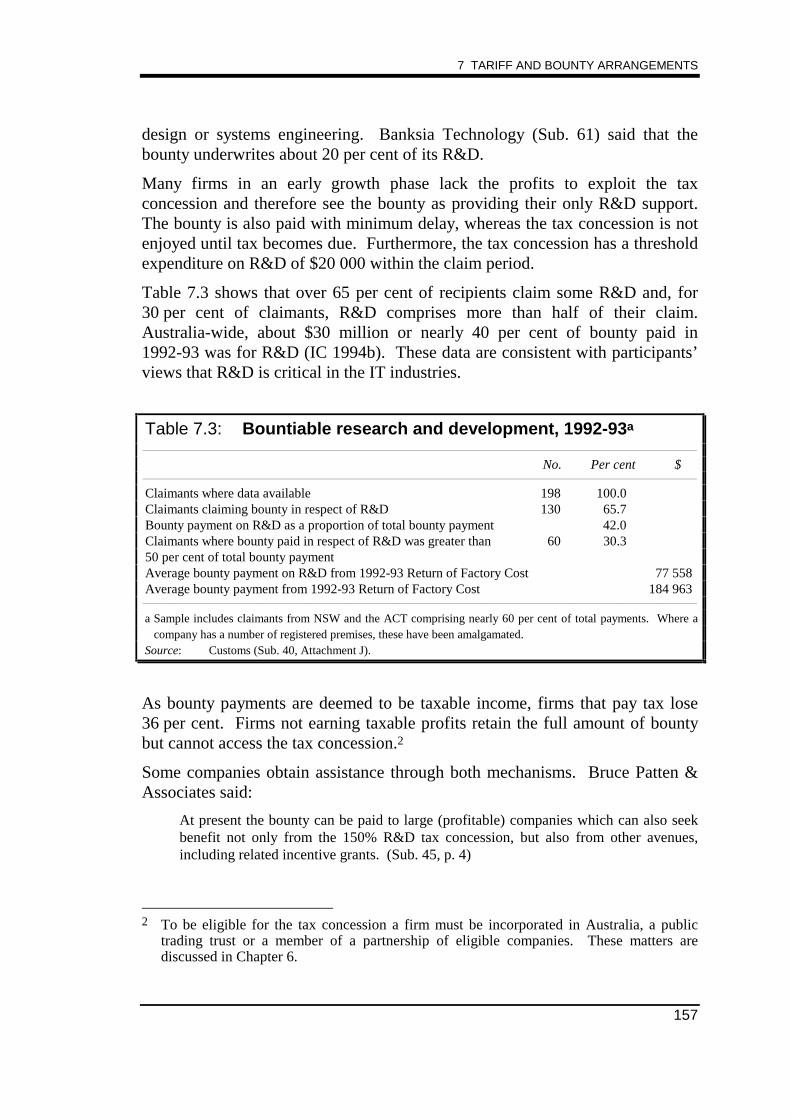

xii

EITO European Information Technology Observatory

EMDG Export Market Development Grant

EMP Export Market Planning

EPROM erasable, reprogrammable read-only-memory

ESA Endorsed Supplier Arrangement

FBT fringe benefits tax

FTA Fixed Term Arrangement

GATT General Agreement on Tariffs and Trade

GBE government business enterprise

GIRD Grants for Industry Research and Development

GITC Government Information Technology Conditions

IAC Industries Assistance Commission

IC Industry Commission

IDC International Data Corporation

IEC International Electrotechnical Commission

IIP Industry Innovation Program

IIS Industry Impact Statement

IR&D Industry Research and Development

ISDN integrated services digital network

ISO International Organisation for Standardisation

IT information technology

IT&T information technology and telecommunications

ITES International Trade Enhancement Scheme

ITR Invitation to Register

ITRG Information Technology Review Group

LAN local area network

MIC management and investment company

MIPS mega instructions per second

MOD Ministry of Defence

MS-DOS Microsoft disk-operating system

na not available/applicable

NATA National Association of Testing Authorities

xiii

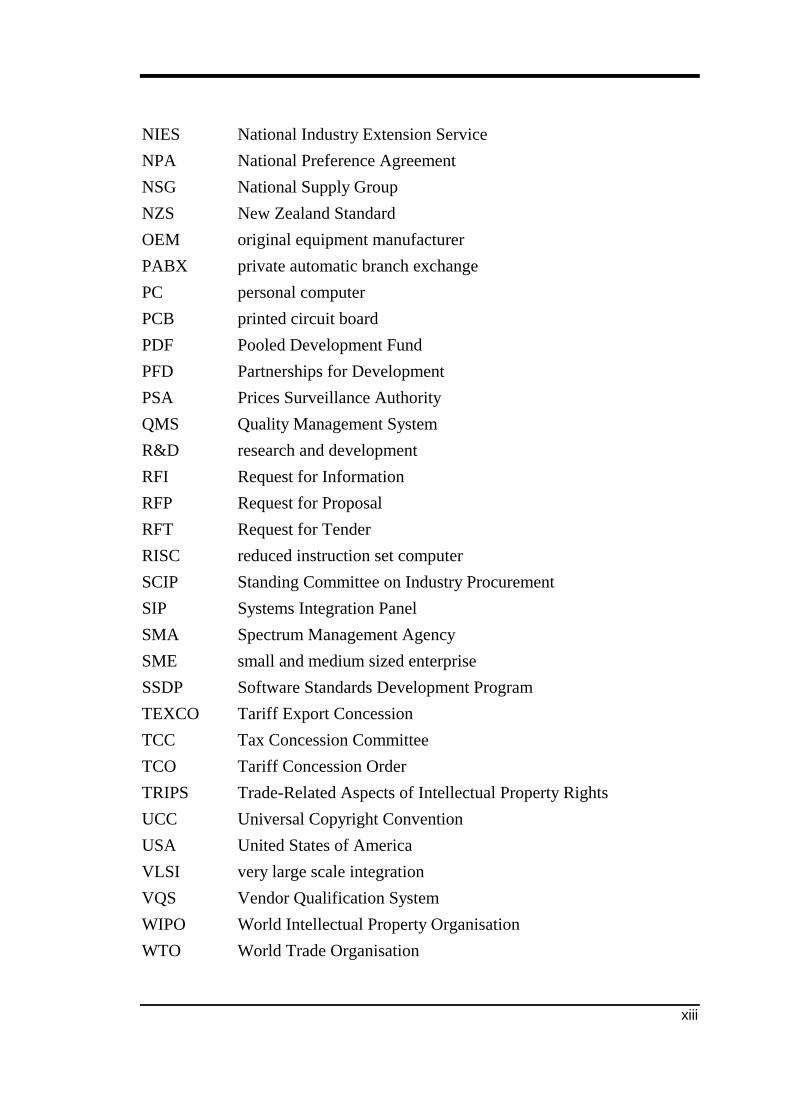

NIES National Industry Extension Service

NPA National Preference Agreement

NSG National Supply Group

NZS New Zealand Standard

OEM original equipment manufacturer

PABX private automatic branch exchange

PC personal computer

PCB printed circuit board

PDF Pooled Development Fund

PFD Partnerships for Development

PSA Prices Surveillance Authority

QMS Quality Management System

R&D research and development

RFI Request for Information

RFP Request for Proposal

RFT Request for Tender

RISC reduced instruction set computer

SCIP Standing Committee on Industry Procurement

SIP Systems Integration Panel

SMA Spectrum Management Agency

SME small and medium sized enterprise

SSDP Software Standards Development Program

TEXCO Tariff Export Concession

TCC Tax Concession Committee

TCO Tariff Concession Order

TRIPS Trade-Related Aspects of Intellectual Property Rights

UCC Universal Copyright Convention

USA United States of America

VLSI very large scale integration

VQS Vendor Qualification System

WIPO World Intellectual Property Organisation

WTO World Trade Organisation

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

xiv

TERMS OF REFERENCEI, George Gear, Assistant Treasurer, under Part 2 of the Industry Commission Act 1989:1. refer Australia’s computer hardware, software and related service industries to the

Industry Commission as an Industry Development Reference, for inquiry and report by30 June 1995;

2. specify that in making its recommendations the Commission aim to improve the overalleconomic performance of the Australian economy;

3. request that the Commission report on:(a) emerging trends in local and global markets for the computer hardware, software

and related service industries, including trends in technology convergence andprotection of intellectual property and the role of government purchasing policies;

(b) the international marketing environment, including barriers to Australianinvestment, exports and import replacement;

(c) the availability and terms under which firms in the computer hardware, softwareand related service industries can access finance, including venture capital;

(d) the current structure and competitiveness of the computer hardware, software andrelated service industries, including an identification of strengths and weaknesses,drawing international comparisons where appropriate;

(e) the taxation treatment of computer hardware, software and related service industriesand Australian standards for the production of computer hardware and software;

(f) the potential for further development of the computer hardware, software andrelated service industries, including the scope for further value adding, investment,exports and import replacement;

(g) any measures which could be undertaken to remove impediments or otherwisecontribute to the efficiency, growth and internationalisation of computer hardware,software and related service industries, in ways that are consistent with efficientresource use in the economy;

(h) the identification of groups who would benefit or be disadvantaged by 3(g) above;and

(i) the effects on the computer hardware, software and related service industries, andthe economy in general, of any measures recommended by the Commission;

4. without limiting the scope of this reference, request the report also include:(a) an evaluation of government programs aimed at improving industry performance,

including the Computer Bounty and the scope to improve the efficiency of programdelivery through better co-ordination within and between Governments;

(b) without disclosing material provided in confidence, examples of past successes andfailures in the computer hardware, software and related service industries, both inAustralia and elsewhere, by way of case studies or other means;

5. specify that the Commission report on any relevant implementation strategies;6. specify that the Commission take account of recent substantive studies undertaken

elsewhere; and7. specify that the Commission have regard to the established economic, social and

environmental objectives of governments.

GEORGE GEAR29 September 1994

COMPUTER HARDWARESOFTWARE AND

RELATED SERVICE INDUSTRIES

OVERVIEWKEY FINDINGS AND

RECOMMENDATIONS

1

OVERVIEW

Australia’s ITindustries ...

This report examines factors affecting the efficiency,growth and internationalisation of Australia’s computerhardware, software and related service industries. Theactivities covered are broadly Australia’s InformationTechnology (IT) industries.

The IT industries are important in their own right, and forthe contribution they make to improving productivity andenhancing growth elsewhere in the economy. Indeed,developments in these industries, and intelecommunications, are having a profound effect onproduction processes and the manner in which business isconducted throughout the economy. They are amongstthe fastest growing industries, globally and in Australia.

Australia’s IT industries

... are growing atmore than 10% perannum.

In 1994, revenue from IT sales in Australia was about$13 billion. In the years immediately ahead, revenue isexpected to grow at about 10 per cent per annum, thefastest growth being in services (19 per cent) andsoftware (14 per cent).

Niche marketproduction ...

Australian-based firms manufacture or assemble personalcomputers (PCs) and a wide range of other hardwareproducts, as well as some application-specificcomponents. Australia does not have a major capabilityin the manufacture of components — volume productionof standard electronic components ceased in the early1990s. However, there is significant design andmanufacture of niche market hardware.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

2

... and serviceprovision areimportant.

Much of Australia’s IT production involves the designand development of software and the provision of IT-related services. A substantial part of the output of the ITindustries is on the back of major telecommunications,banking and other commerce, and transport and miningprojects within Australia and abroad.

Australian IT production, 1992-93

Hardware18%

Packagedsoftware

8%

Services74%

Total = $5 374 million

$961m

$456m

$3 957m

Most firms aresmall ...

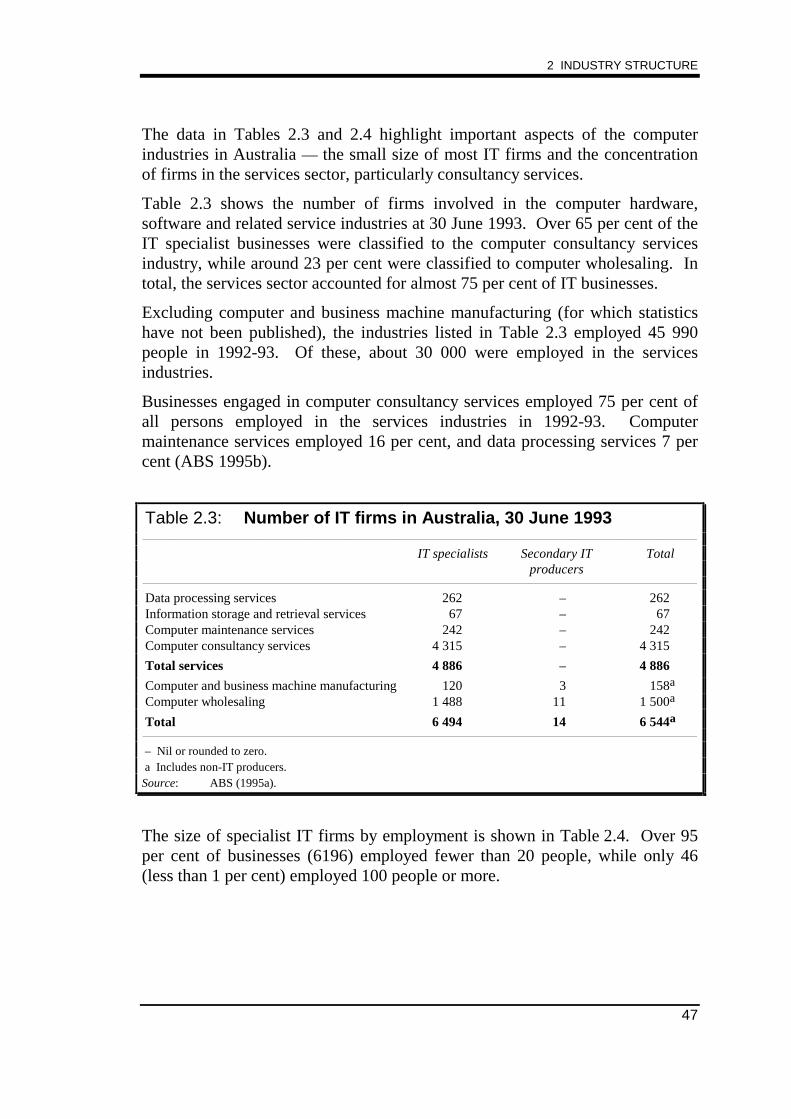

At 30 June 1993, there were 6500 Australian IT firmsemploying a total of 46 000 persons. Most firms weresmall (95 per cent employed fewer than 20 persons each)but less than 1 per cent of firms accounted for nearly halfof the industries’ employment. Sixty five per cent offirms provided computer consultancy services.

... and there issignificant trade inhardware.

In 1993-94, Australia imported $6.1 billion in IT productsand services and had exports of $2.3 billion. Of thoseexports, hardware accounted for 78 per cent and softwareand services, 22 per cent. APEC countries, whichincludes North America, provided 90 per cent ofAustralia’s IT imports and purchased 74 per cent ofexports.

OVERVIEW

3

Technological change

Rapid technologicalchange is a feature ofthese industries ...

The rapid rate of technological change which has alwaysbeen a feature of the IT industries has accelerated sincethe late 1980s. As microprocessor chip densities haveincreased, the price of computing power has plummeted.In parallel with these developments have been advancesin telecommunications technology and in softwareengineering.

Chip density in Intel microprocessors

0

500

1000

1500

2000

2500

3000

3500

1971 1974 1977 1980 1983 1986 1989 1992

4004 808880286

80386SX

80486DX

Pentium

transistors (’000)

... which areconverging with thetelecommunicationsindustries.

Although telecommunications is not under reference,developments affecting that industry are an importantbackdrop to this inquiry. The computer and tele-communications industries are rapidly converging assound, text, graphics, image, and video are digitised.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

4

Opportunities

IT&T exports were$2.6 billion in 1994and ...

The convergence of technologies has createdopportunities for innovation and the marketing of newproducts and services across the whole spectrum ofinformation technology and telecommunications (IT&T)industries. The Australian Information IndustryAssociation (AIIA), for instance, believes that revenuesof the joint industries can rise from $23.5 billion in 1993to $40 billion by 2000, with exports of $10 billion peryear by the turn of the century compared with $2.6 billionin 1994.

... there are emergingopportunities in theEast Asia region.

The East Asia region (which accounts for 19 per cent ofthe global IT&T market) is a very rapidly growing, and asyet relatively undeveloped, market for IT&T products.Our proximity to this market, with which we share acommon time zone, provides promising exportopportunities.

Inquiry participants held very positive views about thefuture of the IT industries and the ability of their ownfirms to take advantage of the emerging marketopportunities. There are sound grounds for optimism.

Australia’s IT strengths

The strengths which contribute to the favourable outlookare:

The industries havemany strengths whichprovide soundgrounds for optimism.

• A skilled and innovative workforce: There hasbeen no recent serious shortage of staff with skills inIT. The industries attract innovative personnel, andthe working environment and the cost of skilledlabour in Australia compare favourably with leadingcountries abroad.

OVERVIEW

5

• Access to technology: Despite a comparativelysmall market, Australia is regarded as a sophisticateduser of IT products and is occasionally used as a testbed for new products. Ready access to technologyputs Australia in a strong position to be competitivein world markets. Many Australian firms are at theleading edge of technological developments incomputer and telecommunications hardware andsoftware design and production.

• Development of niche markets: Australian firmshave demonstrated an aptitude for developing nichemarkets. Small scale is not necessarily animpediment to global sales of software and somehardware and peripherals. Firms producing for aniche market can be very competitive.

• Government support of R&D: Business R&Dappears to be more generously supported bygovernments in Australia than in most otherdeveloped countries — and the IT industries requirehigh levels of expenditure on R&D.

• Economic and political stability: The stableeconomic and political environment can add toinvestor confidence.

The industries’strengths can beenhanced ...

There is considerable scope to build on Australia’sstrengths in IT, notably in software, the integration ofsoftware and hardware, and the production of hardwarefor niche markets. The challenge is not only to achievegains in productivity, but to innovate and stay ahead ofoverseas competitors in the commercialisation of newproducts of high quality.

... by the firms’ owninitiatives ...

Many of the initiatives required to take advantage ofemerging opportunities can only come from the firmsthemselves. Indeed, these are industries in which thevery survival of firms depends upon their ownachievements in research and development and theircapacity to market innovative products.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

6

The search for new products is a driving force —particularly in those segments of the IT industries whereproducts have a shelf life as short as 12 months beforethey are replaced or undergo major revision.

... and bygovernments.

However, the future of the IT industries also dependsupon the actions of governments, including the ways inwhich they use their substantial presence in themarketplace as purchasers of IT products.

Government programs

Some governmentprograms need closescrutiny.

The IT industries are relatively free of regulation, andreform of the regulatory arrangements for tele-communications has contributed to the burgeoningmarket opportunities across the IT&T industries.Nevertheless, there are three areas of governmentinvolvement in the IT industries which the Commissionhas identified as requiring close scrutiny and reform.They are:

• government IT procurement;

• government support for R&D; and

• industry assistance — the computer bounty andtariffs.

Government IT procurement

Governmentsinfluence the successof the industries ...

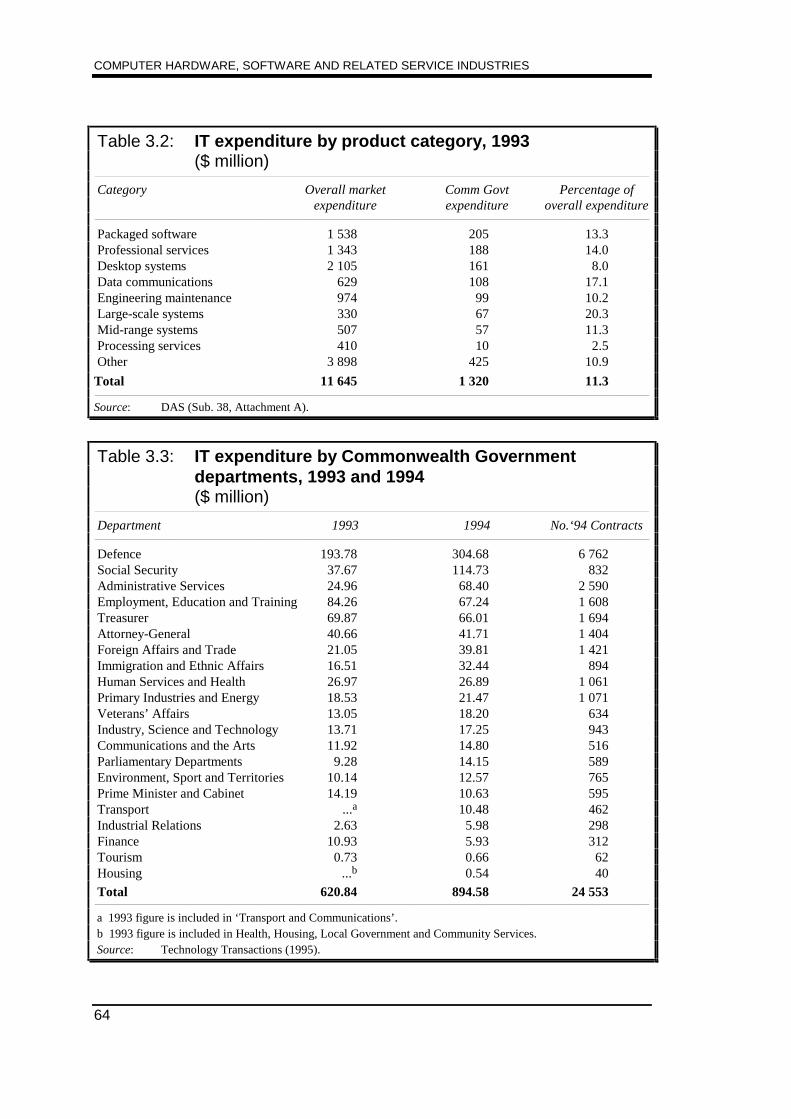

The Commonwealth Government is a major purchaser ofIT products in Australia, accounting for more than 11 percent of the total market. In 1993, CommonwealthGovernment agencies (not including government businessenterprises (GBEs)) spent $1.3 billion on purchases of IThardware, software and services.

OVERVIEW

7

... through theirprocurement of ITproducts.

Commonwealth Government IT purchases1993

IT sector $ million Percentage ofIT sector sales

Hardware 286 10 Packaged software 205 13 Data communications equipment 107 17 Services 198 11 Maintenance and other 524 11

Total 1 320 11

When State and local governments and GBEs areincluded, government purchases account for 40 to 50 percent of the Australian IT market. Consequently, theprocurement arrangements of governments can have amajor influence on the performance of the IT industries— either to their benefit, or to their detriment.

Doing business withgovernments is costly.

The inquiry found many concerns about the cost andcomplexity of doing business with governments. Theconcerns stem from both the administrative arrangementsand the ways in which governments use their buyingpower to influence the growth and location of industry.

Commonwealth purchasing programs

The PFD and FTAprograms ...

In 1987, the Commonwealth Government announced anInformation Industries Strategy, a central feature ofwhich is the Partnerships for Development (PFD)program — a program to encourage international firms,which are major suppliers to government, to undertakemore local investment and R&D, and to provideAustralian companies with greater access to internationalmarketing networks and technology. Since 1991, othergovernment IT&T suppliers have been encouraged toundertake industry development activities by enteringinto Fixed Term Arrangements (FTA) with theCommonwealth Government.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

8

... embody a nationalapproach to industrydevelopment whichcould be ...

The PFD and FTA programs avoid many of theshortcomings of earlier programs that required companiesto ‘offset’ part of the imported value of large governmentcontracts with local activities such as investments, R&Dand technology transfer. The PFD and FTA programsare not tied to specific contracts — companies have adesirable degree of flexibility in the ways in which theygo about meeting their commitments. The programs alsopreserve a national approach to industry development.

... undermined byrecent policy shifts.

Recent policy shifts are in danger of undermining thesebenefits.

Endorsed SupplierArrangements and ...

An ‘Endorsed Supplier Arrangement’ has beenintroduced ‘to further encourage world best practice anda commitment to long term value-added activities inAustralia from suppliers’. The arrangement applies to allpotential government suppliers and requires them to havemanufacturing or service provision facilities in Australiabefore access to government IT business will beconsidered.

It is sound commercial practice, which benefits bothsuppliers and purchasers, for governments to prequalifysuppliers of certain goods and services which arepurchased by government agencies. For example,prequalification avoids the need to reassess the financialviability of an enterprise each time it submits a tender forgovernment business.

The requirements which firms must meet for EndorsedSupplier status extend well beyond the obligations whichcould reasonably be expected of firms prequalifying as ITsuppliers. They act as a barrier to small firms seekingaccess to the government market, discriminate againstforeign firms and specialist distributors, and restrictgovernment purchasing opportunities.

OVERVIEW

9

... a new approach formajor acquisitionshave shortcomingsand are ...

In a new approach for major acquisitions, governmentpurchasing agencies are now required to prepare IndustryImpact Statements, which identify industry developmentopportunities arising from each contract, and to adopt a‘two-envelope approach’ to tendering. Tenderers areexpected to address these opportunities in an industrydevelopment proposal (the second envelope) whensubmitting tenders. Individual contracts will includeindustry development performance clauses.

... compromising thevalue for moneyobjective.

The Commission has examined the difficult trade-offsthat have to be considered where governments attempt tolink industry development objectives with value formoney in government procurement. Recent policy shiftsare compromising the value for money objective.

One effect of imposing industry development obligationsthrough specific contracts is to limit the flexibility offirms’ operations. This is likely to result in a lessefficient and less dynamic industry.

Industry developmentshould not be pursuedthrough individualcontracts.

The Commission has concluded that industrydevelopment undertakings should not be pursued throughindividual IT contracts.

State Government purchasing

The IT procurement policies now being developed insome States reflect a degree of disenchantment with thePFD and FTA programs. Some States and Territoriesbelieve they should have a larger share of IT industrydevelopment through those programs.

State Governmentsare reverting tooffset-likearrangements ...

They have reverted to offsets-like arrangements and areasking suppliers for industry development commitmentsover and above any that they may have under the PFDand FTA programs. There is increasing resort toincentive packages, preferential arrangements, andvarious forms of leverage to promote development at thelocal level.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

10

The South Australian Government, for instance, hasgiven priority to the nurturing of the software industryand sees the outsourcing of IT infrastructure as a meansto leverage significant investment from a multinationalfirm. The Victorian Government required a data centreto be located at Ballarat in the outsourcing of IT servicesrelated to VicRoads and the Victorian Public TransportCorporation.

... which threaten tofragment the ITindustries.

All of these arrangements carry the risk that firms andactivities within the IT industries will be fragmented.They run counter to the national approach to governmentprocurement and put at risk the development ofcompetitive Australian industries.

In 1991, a national approach was re-affirmed by theStates and the Commonwealth through the ‘GovernmentProcurement Agreement’. In the Commission’s view thebenefits of such an approach should not now be ignored.The task for governments is to ensure that the ITindustries are encouraged to develop, across Australia, inways which enhance, rather than detract from, theirinternational competitiveness.

Transparency and discretion

There is too littletransparency and ...

Transparency is important in highlighting the costs to thecommunity of requiring firms to undertake activities overand above those that are commercially justifiable. Thecost should not be disguised. At present the costs do notappear to be fully calculated, nor are they made public.

... too muchadministrativediscretion.

The Commission is concerned at the high level ofadministrative discretion inherent in specifying industrydevelopment obligations; in deciding whether penaltiesfor non-compliance will be imposed; and in setting thelevel and nature of penalties.

The IT industries in Australia are growing at a rapid paceand will do so with or without government intervention inthe procurement process. There is a danger that the highgrowth rate will mask any detrimental effects ofintervention. Indeed the pace of growth is likely to bepresented as evidence of the value of intervention.

OVERVIEW

11

Potential costs

Tender prices canincrease and othercompensation may beneeded.

Unless the industry development required to gain agovernment purchasing contract is commerciallyjustifiable in its own right, tenderers will be unwilling toproceed or they will seek offsetting benefits.Governments will either have to accept higher tenderprices or compensate firms with measures such as theprovision of infrastructure, soft loans, tax concessions ortariffs. Experience demonstrates that compensation ofthis kind tends to be perpetuated.

Governments may eventually be faced with the choice ofproviding continuous support to a fragmented industry(an unsustainable long-run strategy) or dealing with theadjustment problems of many small IT firms if the largerfirms eventually consolidate their operations withinAustralia, or offshore.

The major IT firms are aware of the costs offragmentation but have no choice at present but torespond commercially to the various investment, location,and production inducements they are offered.

Support for research and development

R&D is a majorexpense of the ITindustries.

The computer hardware, software and related serviceindustries are characterised by high levels of expenditureon R&D, and government procurement programs requirefirms to make commitments to ongoing R&Dexpenditure. Consequently, the support that governmentsprovide for R&D through the competitive grants scheme,the 150 per cent R&D tax concession, and concessionalloans for commercialisation of technological innovation,is of great benefit to these industries.

Other assistance for R&D comes through the computerbounty, collaborative schemes (including the CooperativeResearch Centres program) and government support ofresearch institutions.

Government supportof R&D has beenbeneficial, but ...

The Commission’s report on Research and Development,found that the 150 per cent tax concession has broughtnet benefits to the Australian economy.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

12

... companies notearning taxableprofits aredisadvantaged.

Participants in this inquiry are generally supportive of theR&D tax concession scheme, claiming that it is theirmajor form of assistance. However, companies that arenot earning taxable profits are unable to benefit from theconcession — a bias only partly offset by the competitivegrants scheme and by R&D syndication arrangements.This is important for firms in the IT industries whichtypically incur losses in their formative years.

In its report on Research and Development theCommission has proposed that, on equity, efficiency andadministrative grounds, the discretionary arrangementsfor assisting R&D in tax loss companies be replaced bymore generally available support.

A solution has beenproposed.

In particular, in that report, the Commission has proposedthat a generally available non-taxable grant should beintroduced in place of competitive grants for companiesnot earning taxable profits. At the current company taxrate of 36 per cent, the grant would be at the rate of18 per cent of expenditure on eligible R&D.

Such arrangements, if adopted, would remove an anomalyin the major form of assistance available to firms in theIT industries.

Industry assistance

Related andconvergingtechnologies ...

The IT&T industries are variously assisted by Customsduties on imports and the computer bounty. Theassistance regime has not kept pace with technologicalchange. At present:

• computer hardware is assisted by a bounty paid onvalue added, with imports entering free of duty;

• telecommunications equipment is assisted through atariff on imports;

... are affordeddifferent forms ...

• components, many of which are common to bothcomputers and telecommunications equipment,attract a bounty or a tariff, depending on how theyare described;

OVERVIEW

13

... and levels ofassistance and ...

• some computer software classified as systemssoftware attracts a bounty whereas applicationssoftware does not — imports of software enter dutyfree; and

• other computer services are ineligible for the bountyand can be imported free of duty.

... there is a biasagainst services.

Under this assistance regime, some software isbountiable, most is not, and the tariff treatment ofcomponents varies. There is also a bias against servicesand solutions and applications software.

The computer bounty

The computer bountyis due to expire inDecember 1995.

A bounty, paid at the rate of 8 per cent of factory cost, isavailable to domestic producers of eligible hardware andsome software. The scheme commenced in 1984 (at arate of 25 per cent of factory cost) and is scheduled toexpire in December 1995.

The rate of bounty has been reducing in tandem withgeneral reductions in assistance to Australian industry,but total payments have not fallen. There has been asteady increase in the number of firms claiming thebounty, including many firms undertaking simpleassembly.

Bounty paymentstotalled $78 million in1994 — a few firmsgot a lot, and manygot a little.

Bounty payments totalling $78 million were made to 688claimants in 1993-94. There is a wide dispersion in thevalue of payments. For instance, in 1993-94, the top 12firms (2 per cent of claimants) were each paid more than$1 million and accounted for 40 per cent of the totalvalue of payments, whereas the bottom 40 per cent ofclaimants accounted for less than 3 per cent of the valueof the bounty.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

14

Bounty claimants & payments

1984-85 to 1993-94

0

10

20

30

40

50

60

70

80

84-85 85-86 86-87 87-88 88-89 89-90 90-91 91-92 92-93 93-94

0

100

200

300

400

500

600

700

800

Payments Claimants

$ million claimants

Definition andclassificationproblems ...

Since the bounty’s inception, the arrangements referred toabove have given rise to a succession of administrativedisputes relating to the definition and classification ofproducts for bounty or tariff purposes. Firms have beenencouraged to lobby for favourable administrativedecisions.

... have beencompounded by theconvergence oftechnologies.

The convergence of technologies is compounding theseproblems and is reinforcing the need to reduce assistanceanomalies across the boundaries of computing andtelecommunications based industries. It is clear thatdemarcation problems cannot be resolved throughadministrative changes to classifications and definitions.

The rationale whichsupported thebounty’sintroduction ...

The bounty was an appropriate form of assistance in thehigh tariff environment in which it was introduced (itcompensated firms for the very high (input) tariffs at thattime and for the loss of tariff protection on their output).Yet the main benefit arose from the duty free access toimports which accompanied its introduction — thecompetitive position of using industries was greatlyenhanced.

OVERVIEW

15

... has beensubstantially eroded.

Since then, the ‘compensation’ rationale for the bountyhas been substantially eroded by general reductions intariffs. It no longer provides a compelling reason toprovide a narrowly defined group of producers withbounty assistance.

The bounty is not anappropriate industrydevelopment tool ...

Some participants attribute an industry development roleto the bounty. They see the bounty as an importantsource of finance. The Commission acknowledges thatthe bounty contributes to the upgrade of plant andequipment and supports expenditure on R&D. But thisdoes not necessarily make the bounty an appropriateindustry development tool for the IT industries. It isprovided to less than 20 per cent of Australian ITproduction, the remainder being ineligible. Furthermore,much of that ineligible activity is undertaken in areasidentified as having the most promising growth prospects— the development of software and systems integrationand other computer services.

Inquiry participants suggested various ways to fine tunethe eligibility criteria for the bounty — by the exclusionof small (or large) claims; paying only indigenouscompanies; excluding low value added assemblyoperations; including software; and restricting paymentsto computing and telecommunications applications.However reshaping the bounty to provide preferment to adifferent mix of hardware (or software) producers wouldnot overcome the problems that result from the bountyarrangements in conjunction with the existing tariffregime.

... and should beallowed to lapse.

In recommending that the bounty should lapse, theCommission has taken into account the rationale for itsintroduction, the anomalies which exist in the structure ofassistance to the IT industries, the selective assistancewhich the bounty now provides, the introduction ofgenerally available schemes to assist industrydevelopment, and the prospect that future developmentand convergence of technologies will compound thedefinitional and administrative difficulties of the bounty.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

16

Withdrawal of the bounty will contribute to a moreconsistent assistance regime across the IT industries andbe a step towards the elimination of arbitrary distinctionsat the interface between computing and telecommuni-cations. The anomaly between assistance to systemssoftware and applications software, as well as all otherservices, will be removed.

Current recipients of the bounty will be affected by itswithdrawal. But the bounty’s withdrawal should beviewed in the light of current industry policy settingswhich emphasise generally available schemes such asthose directed at R&D, rather than providing industry-specific support for firms requiring protection fromimport competition.

Removal of bountywill trigger somerestructuring ...

The Commission expects the high turnover of firms,which has been a feature of industries associated withrapid technological advances, to continue. The marketfor some of the high volume hardware products (forexample, personal computers) will become morecompetitive. The removal of the bounty will affect theviability of some of the smaller hardware assemblers. Inother areas, such as printed circuit board manufacture,rationalisation may be accelerated. Nevertheless, thegrowth of the IT industries as a whole will not besignificantly retarded.

... but the net effect onfirms will depend onfuture assistancearrangements forR&D.

If the Commission’s proposals in its Research andDevelopment report are implemented, companies notearning taxable profits will benefit from a tax credit orgrant of 18 per cent of the value of their R&Dexpenditure. For some IT firms this will more than offsetthe loss of the bounty. But where firms currently receivethe bounty and also benefit from the 150 per cent R&Dtax concession, withdrawal of the bounty will mean a netreduction in assistance.

OVERVIEW

17

While the industry has been on notice that the bountywould terminate at the end of 1995, the request for theCommission to report on the bounty in this inquiry raisedunderstandable expectations that the bounty might beextended. This contributed to some uncertainty in theseindustries, particularly in relation to the eligibility forbounty of current R&D expenditures. Consequently, atthe time of release of the draft report, the Commissionwrote to the Minister proposing that an earlyannouncement be made to extend the computer bounty forsix months to 30 June 1996. If this extension is notgranted, the bounty will lapse on 31 December 1995.

Tariffs on imports

Some tariff anomalieswill remain.

When the bounty on computer hardware comes to an end,the differential tariff treatment of telecommunicationsand computing equipment will remain. The tariff ontelecommunications equipment is to be reduced to 5 percent in July 1996 whereas computer equipment willremain on a zero tariff.

The Commission has not recommended reinstating a tariffon imports of computer hardware. To do so wouldremove one tariff anomaly but would create others. Atariff would provide assistance even more selectively thanthe bounty in that it would apply only to import-competing hardware manufacture (and not to exports) andnot to any software or services. Furthermore, a tariffwould inflate the prices of this important input to userindustries.

The option was not proposed by any participant.

Further progress in removing anomalies betweenassistance to telecommunications equipment andcomputing equipment will depend on the results of theCommission’s expected inquiry into telecommunicationsequipment, systems and services, and the CommonwealthGovernment’s response to the findings of that inquiry.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

18

Constraints on development

While government purchasing arrangements, support forR&D, and the future of the computer bounty are clearlyareas of major concern for inquiry participants, there areother issues which they see as constraints on their furtherdevelopment. These include setting of Australianstandards, access to finance, protection of intellectualproperty, and taxation issues.

Australian standards

Participants favouredinternationalstandards ...

Participants expressed two concerns relating to the settingof Australian standards which affect the IT&T industries:first, that wherever possible, Australian standards shouldmirror international standards; and second, thatAustralian standards not be mandatory unless a clearsocial benefit can be demonstrated.

Most Australian standards to which the IT&T industriesmust conform are set by Standards Australia and by theAustralian Telecommunications Authority (AUSTEL).

... and were satisfiedwith StandardsAustralia.

Standards Australia publishes and markets all forms ofAustralian standards, from design codes and technicalspecifications to quality management system standards,and adopts international standards where possible. Mostparticipants expressed satisfaction with StandardsAustralia.

Technologyconvergence iscausing problems forAUSTEL and ...

AUSTEL determines technical standards for Australia’stelecommunications networks, for customer cabling tothose networks, and for customer equipment connected tonetworks. With the convergence of technologies, anincreasing array of computer equipment is being directlyand indirectly connected to the telecommunicationsnetwork.

OVERVIEW

19

... there is concernabout AUSTEL’smandatory standardsand testing andconformancerequirements.

Some participants expressed concern that AUSTEL’smandatory standards, and testing for conformance withthose standards, will unnecessarily impede trade and denyAustralia access to equipment incorporating the mostrecent technological developments. They suggested thatAustralia should adopt international standards wherepossible and that there be more widespread recognition oftesting and certification conducted in other countries.

There is no doubt that the community will benefit whenthe costs of ensuring compliance with technical standardsare minimised. This may mean authorising suppliers toself test products where they can demonstrate that therequired standards will be enforced, and allowing thirdparty accreditation for firms that can demonstrate testingcapabilities.

The Commission notes that the CommonwealthGovernment is pursuing the issue of standards uniformitywith the members of the Asia-Pacific EconomicCooperation Group, and that negotiations havecommenced with the European Union on a mutualrecognition agreement on conformance assessment.

Access to finance

Many firms have littleaccess to finance.

The rapid growth of the IT industries has helped manyfirms to finance their activities internally and hasprovided the cash flow for others to attract debt finance.The strategic relationships which some firms havedeveloped with larger companies have assisted theiraccess to finance. However, many firms have littleaccess to external equity capital. They are typically firmsthat have been established within the past 10 years andcontinue to rely upon the IT skills, business acumen andfinancial backing of their founders.

The reluctance of investors to provide risk capital tosmall and medium sized firms is well documented. Itreflects the relatively high incidence of failure of smallbusinesses and the difficulty and costs that investors facein assessing the risks — particularly where the major assetof a business is in the form of intellectual property.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

20

Venture capital firms’lack of ITmanagement skills ...

Firms in the IT industries may be disadvantaged in theiraccess to venture capital, not because of a shortage ofventure capital funds, but because venture capital firmslack management expertise relevant to the IT industries.This has been recognised by venture capital firms andsome are employing people from the IT industries to helpevaluate and oversee suitable investments.

... may be atemporary problem.

The shortage of evaluative skills within financial marketsmay be a temporary phenomenon. As Australia’s venturecapital market continues to develop and its links with theIT industries strengthen, the problem should recede. Theprocess will be aided by access to concessional loans andother recent Commonwealth Government initiatives toimprove communication between borrowers and lendersand generally minimise financial constraints on thedevelopment of firms with high growth prospects.

Notwithstanding the new initiatives, many firms areunlikely to get all of the financial support they areseeking. However, it would not be appropriate forgovernments to underwrite the high risks faced byfledgling firms seeking to commercialise an innovation.Such an approach would not improve efficiency, wouldpenalise less risky ventures, and could impose significantcosts on the rest of the economy.

Intellectual property

The main concerns of inquiry participants relating to theprotection of intellectual property are in areas ofcomputer software protected under copyright.

Extent of protection

OVERVIEW

21

Most participants are satisfied with the extent ofprotection offered, or recognise that copyright protectionis often irrelevant because of the speed with whichsoftware is superseded. However, some raised issuesabout the parallel importing of software (imports otherthan by the licensed distributor) which is at presenttreated as an infringement of copyright. The currentarrangements are supported by the importers anddistributors of software who contend that a highproportion of illegal copies of software sold in Australiais imported.

The issue of parallelimporting of softwareis still unresolved.

The issue of parallel importing of software was recentlyreviewed by the Prices Surveillance Authority (PSA) andthe Copyright Law Review Committee (CLRC). ThePSA concluded that parallel imports of legal copies ofcomputer software should be permitted, whereas in itsfinal report the CLRC recommended that restrictions onthe parallel importation of computer programs shouldremain unchanged. The CLRC cited the threat of piracyas the principal reason to restrict parallel imports.

In the Commission’s view, the parallel importation ofsoftware and the piracy of intellectual property areseparate issues which need to be addressed with separatepolicies.

Restrictions on parallel imports of software limitcompetition in the distribution and retail markets andhave the potential to raise the price of software —provided that measures to control piracy are adequate.

Moves to allowparallel importsshould be supported.

An appropriate first step is to indicate to the WorldIntellectual Property Organisation Committee of Experts,Australia’s strong support for allowing parallel imports oflegal copies of computer software. There appear to besignificant advantages in achieving multilateralagreement, at least among the signatories to the BerneConvention, that each country would remove therestrictions currently impeding parallel imports of legalsoftware.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

22

If multilateral agreement cannot be achieved, theAustralian Government would then need to considerwhether, in the light of the costs and benefits involved, itshould take unilateral action to permit parallel importsinto Australia.

Enforcement of protection

The enforcement of copyright protection is seen as amajor issue by some participants. They drew attention to:

Small infringementpenalties ...

• relatively small penalties prescribed by theCopyright Act;

• low levels of damages and costs awarded;

• difficulties in proving ownership of copyright; and

• the lack of resources devoted to detection andprosecution for software theft.

Some participants acknowledged that it may beunrealistic to expect law enforcement agencies to policethe provisions of the Copyright Act and were resigned toundertaking that task themselves. But they advocatedsubstantially greater penalties for successful prosecutions.

This issue has been examined by the CLRC whichrecommended that criminal penalties for software theftshould be brought into line with those currently applyingto films and those proposed for sound recording. ThePSA also saw merit in bringing penalties into line acrossthe range of copyright protected material.

... should be reviewed. The Commission agrees with the CLRC and the PSA andrecommends that penalties for software theft be broughtinto line with similar breaches of the Copyright Act.

Taxation

OVERVIEW

23

Participants wereconcerned about ...

Many participants described Australia’s taxation systemas unnecessarily complex. They raised some generaltaxation issues which have broad implications extendingwell beyond the scope of this inquiry. Some said thesystem does not have regard for the unique characteristicsof the IT industries. Specific concerns include sales tax,withholding tax, and depreciation provisions.

... sales tax ... Sales tax concerns relate to the rates which apply toparticular products such as software media,CD-ROMs, and programmable memory chips, and to themost appropriate sales tax schedule for computerproducts in general.

... depreciationprovisions, and ...

Some participants argued that depreciation provisions fortax purposes have not kept pace with technologicalchange, notwithstanding provisions to claim higher thanthe scheduled depreciation rate.

A distinction must be drawn between a product’seffective life and the time a technology is regarded as‘leading edge’. Most software and hardware productshave an effective life which extends well beyond the timethe technology they contain is superseded, and it wouldbe unreasonable to expect depreciation schedules toalways reflect leading edge technology life rather thaneffective useful life.

... withholding tax. On the issue of withholding taxes applied to royalties andlicence fees, the AIIA said that these taxes have a similareffect to a tariff in that they raise the price paid byAustralian firms for access to technology. TheCommission is aware that this has the potential to denyAustralia access to some technologies but has not beenpresented with any evidence that this has occurred.

The AIIA requested that Australia adopt the provisions ofthe Model Tax Treaty of the Organisation for EconomicCooperation and Development, which recommends that azero rate of withholding tax be imposed on royaltypayments. The Commission sees merit in this proposal.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

24

The role of government

Governments canhelp.

Governments can help to improve competitiveness andgrowth opportunities in Australia’s IT industries by:

• simplifying the administrative arrangements forgovernment IT purchases;

• maintaining greater separation between ITpurchasing and industry development objectives;

• strengthening arrangements for the support of R&Din companies not earning taxable profits;

• removing anomalies in the assistance accorded toactivities within the IT industries;

• removing anomalies in the assistance accorded toactivities across the IT&T industries, and betweenIT&T and other industries;

• applying a coordinated approach to standards,regulation and industry policy generally, across theIT&T industries; and

• furthering microeconomic reform in areas stillimpeding the performance of Australian industrygenerally.

Some advocated aninterventionistapproach, but ...

Some participants expected a blueprint for the futuredevelopment of the IT industries. The Commission doesnot see this as an appropriate task for a government body.

If the expression of visions and the drawing of blueprintsis to be of value, it is a task for the industries themselves,and their industry associations. Industry associations canprovide informal guidance and market intelligence, butneither they nor governments are in a position to provideaccurate forecasts of the future direction and pace oftechnological change, the demand for products not yetdeveloped, and future supply conditions. Such a task isparticularly difficult for the IT industries, which arecharacterised by rapid rates of technological change.

OVERVIEW

25

The future development of the IT industries will bedetermined by the commercial decisions of individualfirms operating at the coal face of markets andtechnological change.

... commercialdecisions are likely toproduce the bestoutcome.

Their decisions, taken on commercial grounds, are morelikely to be of benefit to the firms and the communitythan measures that governments might take to favourparticular groups, activities, or outcomes.

IT firms have accessto many supportprograms.

In the Commission’s view, individual firms have toassess the trade-off between risk and reward and maketheir own decisions in each venture they undertake,taking into account the wide range of government supportprograms already available to firms in the IT industries.

The prime role of governments should be to removeimpediments to better performance.

The Commission’s proposed reforms — for instance, lesscomplex forms of government procurement, andgenerally available support for R&D — would simplifythe institutional and regulatory framework within whichfirms are required to operate. These are changes thathave economy-wide (not industry-specific) application.They also promote a national approach to thedevelopment of competitive Australian industries.

A national approachto industry policy iscritical.

In response to the Hilmer committee of inquiry, theAustralian States have supported a national approach tocompetition policy. As a result, utilities such as water,electricity, ports and road transport are expected to facemore open competition and come under the scrutiny ofthe Trade Practices Act 1974. A national approach toindustry policy is no less critical to the competitiveness ofAustralia’s industries. Government procurement, inparticular, should be high on the agenda ofmicroeconomic reform.

27

KEY FINDINGS AND RECOMMENDATIONS

Industry strengths

• Australia’s information technology (IT) industries demonstrate strengths in:

- innovation and development of applications software;

- systems integration, the coupling of software and hardware systems, and solutions packages incorporating hardware and software;

- innovative niche hardware; and

- undertaking small high quality runs, where larger scale plants overseas tend to be uncompetitive. [Section 2.4.1]

• Globally, IT activity is dominated by multinational firms, but there is a rolefor small and medium sized enterprises (SMEs), particularly in nichemarkets. International alliances, and/or links with multinational companiesbased in Australia, can contribute to the success of Australian SMEs.[Section 2.4.2]

• There is scope to build on Australia’s strengths in IT. Governments canhelp by removing impediments to better performance, by providing a stableinstitutional and regulatory framework, and through judicious use of theirsubstantial presence in the market as a purchaser of IT. [Section 2.5]

Government purchasing

• Government purchasing can foster development in the IT industries withoutproducing significant extra costs. Net benefits are most likely where:

- industry development obligations are not sought through specific contracts; and

- firms are given as much flexibility as possible in choosing activities that fulfil their obligations. [Section 5.2]

• The Commission endorses a consultative approach for resolving concernswith the administration of the procurement process, as embodied in theapproach of the Cost of Tendering Committee and the recent strategicreview of the government IT contract conditions. [Section 5.1]

• The benefits of the Partnerships for Development (PFD) approach andFixed Term Arrangements (FTA) programs are being undermined by policyshifts and inadequate information flows between governments. [Section 5.3]

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

28

[Section 5.3]

• The benefits of a national approach to government procurement areincreasingly at risk from State/Territory government policies. There isgreater resort to incentive packages, preferential arrangements, and variousforms of leverage to promote development at the local level. [Section 5.4]

[Section 5.4.3]

• Government requirements for prequalification as an IT supplier should beconfined to the commercial needs of purchasing agencies and should notextend to the pursuit of industry development objectives.

Recommendation 1

An independent review of the Partnerships for Development and Fixed TermArrangements programs should be undertaken in 1998. It should include anassessment of the appropriate extent of administrative discretion.

Recommendation 2

The Commonwealth, State and Territory Governments should recommit to anational approach, along the lines of the Government Procurement Agreement,in the use of government purchasing for industry development. The Council ofAustralian Governments (COAG) should seek agreement on ways to avoiddamage from industry development obligations and measures intended to attractactivity to particular locations. In so doing, COAG should be mindful that:

• adequate information flows (between the Commonwealth and the States/Territories) on opportunities for industry development are vital for the success of a national approach;

• procurement measures that discriminate against firms in other States/Territories can threaten the viability of a national approach;

• the costs and benefits of industry development commitments and incentive packages should be calculated and made as transparent as possible;

• incentives offered to attract firms can impose costs within the State, in other States and for the nation; and

• costs arising from industry development and investment attraction policies should be borne by the jurisdiction concerned.

KEY FINDINGS AND RECOMMENDATIONS

29

• The requirements that firms must meet under the Endorsed SupplierArrangement (ESA) extend well beyond the obligations which couldreasonably be expected of a firm prequalifying as a supplier to government.They are unduly onerous and act as a barrier to small firms seeking accessto the government market.

• The industry development criteria of the ESA can act as a barrier to importsof IT products.

• The ESA is administered in ways that oblige overseas firms, regardless ofsize, to enter the FTA program. [Section 5.5.1]

[Section 5.5.1]

[Section 5.5.2]

Research and development

• The Commission’s 1995 report on Research and Development proposed thatfirms not earning taxable profits should have access to a non-taxablesubsidy of 18 per cent. These firms would then receive assistance equivalentto that arising from the concessional component of the 150 per centdeduction for profitable companies. This change would remove an anomalyin the major form of assistance available to firms in the IT industries.[Section 6.4].

Recommendation 3

An independent review of the Endorsed Supplier Arrangement should beundertaken in 1996. The review should have regard to:

• the desirability of keeping prequalification as simple and inexpensive aspossible;

• the potential for the Endorsed Supplier Arrangement to act as a barrier to theentry of small firms to the government market;

• the potential for the industry development requirements to act as a barrier toimports of IT products; and

• the discriminatory treatment of overseas firms.

Recommendation 4

Governments should not seek specific industry development commitments inthe context of individual tenders.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

30

• As the computer bounty is payable in respect of R&D expenditures, somebounty recipients can receive greater support for R&D than other firms inthe IT industries or within the economy generally. [Section 7.5.1]

[Section 6.4]

Tariff and bounty issues

• The force of the argument underpinning the compensation rationale for thecomputer bounty has been substantially eroded by general reductions intariffs, changes in the focus of industry policy, and developments in the ITindustries, which now bear little resemblance to the IT industries of 1984.[Section 7.2]

• The bounty is paid predominantly on the production of hardware. Bounty isnot paid on the bulk of software development, systems design andintegration, and IT services. The latter activities, which have strengths inAustralia, account for over 80 per cent of IT production. [Section 7.4]

• Most participants’ suggestions for modifications to the computer bountywould make it even more selective. Measures that give preferment toselected industries or firms are difficult to justify and are unlikely to providenet community benefits. [Section 7.5.2]

• Related and converging technologies are variously assisted by the bountyand tariffs. Classification disputes and ad hoc adjustments to the bounty area direct result of this assistance environment. Definitional disputes andassociated administration problems will be compounded as computing,telecommunications and broadcasting technologies develop and converge.[Section 7.6, 7.8]

[Section 7.10]

Recommendation 5

Firms not earning taxable profits should have access to R&D assistance in theform of a non-taxable subsidy.

Recommendation 6

The computer bounty should lapse.

KEY FINDINGS AND RECOMMENDATIONS

31

• At the time of the release of the draft report, the Commission wrote to theMinister proposing that an early announcement be made to extend thecomputer bounty for six months to 30 June 1996. If the extension is notapproved, the bounty will lapse on 31 December 1995. [Section 7.10]

[Section 7.11.1]

Standards and conformance

• The IT industries should be represented on any advisory body established toconsider standards for equipment to be connected to Australia’stelecommunications network. [Section 8.2.2]

• Where possible, standards adopted in Australia should be aligned withrelevant international standards, and should not be mandatory unless aclear social benefit can be demonstrated. [Section 8.2.3]

• With technology convergence, an increasing number of IT products will beconnected to Australia’s telecommunications networks and the need toensure conformance with AUSTEL regulations will rise. It is important thatthe costs of compliance are kept as low as possible. [Section 8.3.1]

Access to finance

• The Commission supports recent initiatives by government and industry toimprove the channels of communication between small and medium sizedenterprises and providers of debt and equity finance. [Section 9.4]

Intellectual property

• Restrictions on parallel importing (imports other than by copyright holdersor their licensed distributors) limit competition in the distribution and retailmarkets and have the potential to raise the price of software.[Section 10.3.1]

Recommendation 7

On cessation of the bounty, the tariff rates applying to bountiable items shouldremain at zero.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

32

[Section 10.3.1]

• A licensed owner of a computer program should be able to decompile thatprogram in order to correct errors, providing that the conditions set out bythe Copyright Law Reform Committee are satisfied. [Section 10.3.2]

[Section 10.4]

[Section 10.5.2]

Recommendation 8

The Australian Government should actively support moves to allow parallelimporting of legal (non-pirated) copies of software in the forum established bythe World Intellectual Property Organisation to consider a Protocol to the BerneConvention (the Committee of Experts). If the agreed Protocol expresslyprohibits parallel importing, the Australian Government would then need toconsider whether, in the light of the costs and benefits involved, it should takeunilateral action to permit parallel imports of computer software into Australia.

Recommendation 9

Criminal penalties for software theft should be brought into line with similarbreaches of the Copyright Act.

Recommendation 10

Government departments and agencies should not seek automatically to acquireintellectual property rights associated with the goods and services they purchase.Ownership of intellectual property rights should be resolved through negotiationon a case-by-case basis.

COMPUTER HARDWARESOFTWARE AND

RELATED SERVICE INDUSTRIES

CHAPTERS

1 The inquiry

2 Industry structure

3 Markets

4 Trends in technology

5 Effects of government purchasing arrangements

6 Research and development

7 Tariff and bounty arrangements

8 Standards and conformance

9 Access to finance

10 Intellectual property

11 Taxation and other matters

35

1 THE INQUIRY

1.1 Scope of the inquiry

The Assistant Treasurer referred the computer hardware, software and relatedservice industries to the Industry Commission on 29 September 1994 for inquiryand report by 30 June 1995.

The terms of reference inter alia ask the Commission to report on any measuresthat could contribute to the efficiency, growth and internationalisation of thecomputer hardware, software and related service industries. For the purpose ofthis report, these industries will be collectively referred to as the ‘informationtechnology’ (IT) industries. This accords with common practice in theindustries concerned.

The activities directly under reference include:

• computer hardware (personal computers, mid-range and large scalesystems and other workstations);

• peripheral computer equipment (input/output devices and other peripheralcomputer equipment);

• other computer equipment, components, parts and consumables;

• certain bountiable communications and networking hardware;

• computer software (applications, systems management and utilities andtools);

• services (consulting, systems integration, outsourcing, education); and

• maintenance (hardware).

The Commission is asked to report on government programs (Commonwealthand State) and coordination within and between governments. The computerbounty, presently scheduled to terminate at the end of 1995, is under reference,along with institutional and regulatory arrangements subject to influence bygovernments that affect the performance of these industries.

The telecommunications industry is not directly under reference. This posessome difficulty for the inquiry because the synergy between computing andtelecommunications calls for a coordinated approach to standards, regulationsand industry policies. There is a danger that continuing to treat the two sectorsseparately will entrench anomalies and distortions in the use of resources.

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

36

Given this concern, some of the matters raised in this report are relevant to theCommission’s separate inquiry into the telecommunications industry, expectedto commence later in 1995.

1.2 Key inquiry issues

This report responds to an ‘industry development’ reference in which theCommission is asked to investigate growth prospects and any impediments tobetter performance in Australia’s IT industries.

The Commission has reported on emerging trends in local and global markets,on the strengths of Australia’s IT industries, and on the opportunities beingcreated for Australian firms in these and related industries. Attention is drawnto some institutional impediments — in particular, features of some State andCommonwealth Government purchasing programs — which could detract fromthe full achievement of the industries’ potential.

Some participants expected the Commission to go further and to set out ablueprint for the future development of the IT industries. The Commission doesnot see this as an appropriate task for a government body.

If the expression of visions and the drawing of blueprints is to be of value, it is atask for the industries themselves, and their industry associations. TheCommission notes that the Australian Information Industry Association (AIIA)has recently published its vision for the future of Australia’s informationtechnology and telecommunications (IT&T) industries (AIIA 1995). The AIIAdocument refers to the development of internationally competitive industrieswith a reputation for excellence, and sets targets for growth and exports to theyear 2000.

The future development of these industries will be determined by thecommercial decisions of individual firms operating at the coal face of marketsand technological change. Industry associations can provide informal guidanceand market intelligence, but neither they nor governments are in a position toprovide accurate forecasts of the future direction and pace of technologicalchange, the demand for products not yet developed, and supply conditions at theglobal, regional and country level. Such a task is particularly difficult for the ITindustries, which are characterised by rapid rates of technological change. Ifgovernments seek to influence firms’ behaviour on the basis of particularindustry plans, expectations can be raised that compensation will be provided inthe event that the planned outcomes are not achieved. In the Commission’sview, individual firms have to assess the trade-off between risk and reward andmake their own decisions in each venture they undertake.

1 THE INQUIRY

37

The task for government is to create an environment in which firms andindustries have the opportunity to develop to their full potential. This entailsremoving institutional and regulatory impediments to their operations andaddressing any ‘market failures’ (providing incentives for research anddevelopment for example).

The report draws on discussions with a wide range of organisations andindividuals with an interest in the IT industries, on the evidence presented attwo rounds of public hearings, and on the 118 written submissions received inthe course of the inquiry.

Multinational companies are well represented in these industries in Australia,but the majority of firms are small and Australian-owned. Many of these havebeen established within the last 10 years and continue to depend on the IT skills,business acumen and financial resources of their founders. Many are softwareand/or systems integration firms with innovative products but limited resourcesand skills to commercialise them. Their products may have a shelf life as shortas 12 months before they are replaced or undergo major revision. Anothergroup of firms undertakes the assembly of computer hardware from importedcomponents and, numerically, these firms comprise the majority of recipients ofthe computer bounty.

This background is reflected in the issues raised by participants during thecourse of the inquiry. Matters of concern to participants and their associationsincluded:

• access to finance;

• industry assistance (including the bounty);

• the cost of doing business with government;

• the industry development commitments that are often required of firmsselling to governments;

• industry standards;

• the protection of intellectual property; and

• certain taxation issues relating to depreciation rates and sales and with-holding taxes.

Labour market and environmental issues were seldom raised.

Cutting across these specific inquiry issues are issues associated with the highrate of technological change, which is a feature of these and other closelyrelated industries. The nature and pace of change are such that productdescriptions which form the basis of the regulatory and assistance arrangementsfor these industries have become obsolete and of little relevance to current andemerging industry circumstances. Technology convergence — the merging of

COMPUTER HARDWARE, SOFTWARE AND RELATED SERVICE INDUSTRIES

38