Embed Size (px)

Citation preview

CONFERENCE

Fights and Friction in Global Trusts and Estates ON Thursday 5 December 2013, 9.10am – 12.45pm AT Park Plaza Hotel London Victoria, 239-251 Vauxhall Bridge Road, London SW1V 1LJ, United Kingdom SPONSORS

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 ________________________________________________________________________________

These Notes are intended to do no more than refresh the memories of those attending the conference of the salient points made. Whilst every care has been taken in preparing the Notes to ensure their accuracy, they cannot be exhaustive and are no substitute for detailed examination of the relevant statutes, cases and other materials when advising clients on particular matters. No responsibility can be accepted by the Society of Trust and Estate Practitioners or the speakers for any loss occasioned to any person acting or refraining from action in reliance on anything contained in these Notes. No part of the Notes may be reproduced in any form without the prior permission of the speakers.

© STEP Conferences 2013

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 ______________________________________________________________________________

Notes for delegates claiming points under CPD/CPE schemes

Attendance at today’s conference will assist delegates in meeting their structured training commitments as follows:

Society of Trust and Estate Practitioners

The event qualifies for 3 hours towards meeting STEP members’ structured training commitment under the Society’s own Continuing Professional Development Scheme.

The Solicitors Regulation Authority (formerly the Law Society)

The event is accredited with 3 hours under the Solicitors Regulation Authority continuing professional development scheme. Please note, however, that to claim the hours, solicitors must sign the attendance register on the conference registration desk at the end of the conference (in order to confirm their attendance for the whole of the event under the Solicitor Regulation Authorities guidelines). Please quote your roll number, as well as your name and firm. The reference allocated by the Solicitors Regulation Authority to courses run by STEP, which must be quoted on your claim form, is AKZ/STCL.

NB In all cases, points/credits are subject to the appropriate claim being made

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 ______________________________________________________________________________

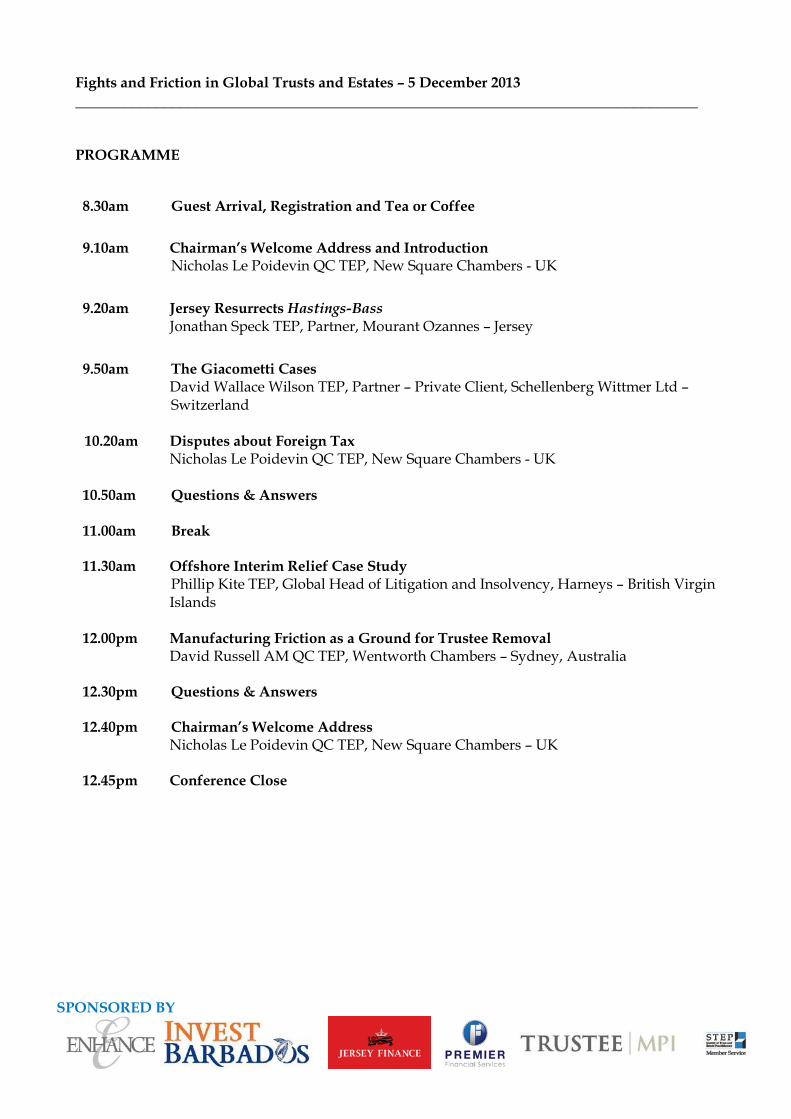

PROGRAMME

8.30am Guest Arrival, Registration and Tea or Coffee

9.10am Chairman’s Welcome Address and Introduction Nicholas Le Poidevin QC TEP, New Square Chambers - UK

9.20am Jersey Resurrects Hastings-Bass Jonathan Speck TEP, Partner, Mourant Ozannes – Jersey

9.50am The Giacometti Cases David Wallace Wilson TEP, Partner – Private Client, Schellenberg Wittmer Ltd – Switzerland

10.20am Disputes about Foreign Tax Nicholas Le Poidevin QC TEP, New Square Chambers - UK

10.50am Questions & Answers

11.00am Break 11.30am Offshore Interim Relief Case Study

Phillip Kite TEP, Global Head of Litigation and Insolvency, Harneys – British Virgin Islands

12.00pm Manufacturing Friction as a Ground for Trustee Removal

David Russell AM QC TEP, Wentworth Chambers – Sydney, Australia 12.30pm Questions & Answers

12.40pm Chairman’s Welcome Address

Nicholas Le Poidevin QC TEP, New Square Chambers – UK

12.45pm Conference Close

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 ______________________________________________________________________________

DELEGATE LIST

Alistair Abbott Forbes Hare LLP

Muhammad Assad Yussuf Abdullatiff Axis Fiduciary Ltd

Natalie Augustin Financial & Corp. Services LTD (FINCOS)

Catharine Bell Lawrence Graham LLP

Ashton Davies Thomas Eggar

Richard Dew Ten Old Square

Sibauste Enrique Xperta Corporate Services/ Patton Moreno & Asvat

Lesley Fogden Rosemont Monaco SAM

Lucy Gill Foot Anstey LLP

Dawn Goodman Withers LLP

Victoria Grogan Carey Olsen

Linnane Haley Landmark Management

Mark Haranzo Withers LLP

John Heaps RBC Services (Channel Islands) Limited

Philip Hesketh Hesketh Mediation Services

Anna Heywood Michelmores LLP

Michael Heyworth Trust Corporation of the Channel Islands Limited

Sian Hodgson Penningtons Solicitors LLP

Belinda Hornsby Cox Belmont & Lowe

Lorraine Jeffery Bircham Dyson Bell

Rachel Jones Druces LLP

Graham Journeaux Ohad Trust BSC(c)

Felicity Keller Private Client Advisory Service

SPONSORED BY

DELEGATE LIST CONTINUED

Sharon Kenchington Boodle Hatfield LLP

Charlotte Knight Lawrence Graham LLP

John Lawrence Windermere Corp Mgt

Daniel Lehmann Baker Tilly Roelfs

Mark Lindley Boodle Hatfield LLP

Neil Long Howard Kennedy FSI

Paraic Madigan Matheson

Sue Medder Withers LLP

Patrick Murrin

Amanda Noyce Withy King

David Ostle Landtax LLP

Nigel Porteous Maples and Calder

James Price Farrer & Co

Tim Prudhoe Kobre Kim LLP

Gowtam Ramsurrun Kleinwort Benson Bank

Lisa Shaw Royal Bank of Canada Trust Corporation Limited

Pedley Simon Pannone LLP

Arshoo Singh Russell-Cooke LLP

Mark Studer Wilberforce Chambers

Sangeet Tatem Prettys

Alexandra Taylor Botvyle Consultants

Paul Tracey Grosvenor Law LLP

Christine Van Cauwenberghe Investors Group Financial Services Inc.

Angelo Venardos Heritage Trust Group

Christine Webber Thrings Solicitors LLP

SPONSORED BY

DELEGATE LIST CONTINUED

Warren Whitaker Day Pitney

Ian Worland Legacy Tax & Trust Lawyers

SPONSOR LIST

Gordon Bennie Enhance Group

William Byrne Jersey Finance Limited

Hannah Carolan Jersey Finance Limited

Jean-Paul Cumberbatch Invest Barbados

Vimal Damry Premier Financial Services Limited

Françoise Hendy Invest Barbados

Juliette Holder Invest Barbados

Bakul Kothari Premier Financial Services Limited

Oliver Mourant Enhance Group

James Painter Enhance Group

Lee Quemard Enhance Group

STAFF LIST

Nicola Fletcher Society of Trust and Estate Practitioners (STEP)

Kerri Roffey Society of Trust and Estate Practitioners (STEP)

Emma Yeats Society of Trust and Estate Practitioners (STEP)

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 _____________________________________________________________________________

Jonathan Speck TEP, Partner, Mourant Ozannes - Jersey

Jonathan is joint head of the International Trusts & Private Client Team in Jersey. He was called to the English Bar in 1990 and, after returning to Jersey, was sworn in as an advocate in 1994. Although, he undertakes a wide range of commercial litigation, the substantial majority of Jonathan's practice comprises contentious and non-contentious trust cases, about which he has written and lectured around the world.

Over the past ten years, Jonathan has been centrally involved in virtually all of the most high-profile, high-value and complex trust disputes in Jersey, including the AlhAmrAni litigation. He is

Chambers & Partners' only star-rated litigator in Jersey, top-ranked by Legal 500 and recommended, with honours, for both contentious and non-contentious trusts by Citywealth, who comment that he is 'the leading trusts litigator on Jersey'.

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 _____________________________________________________________________________

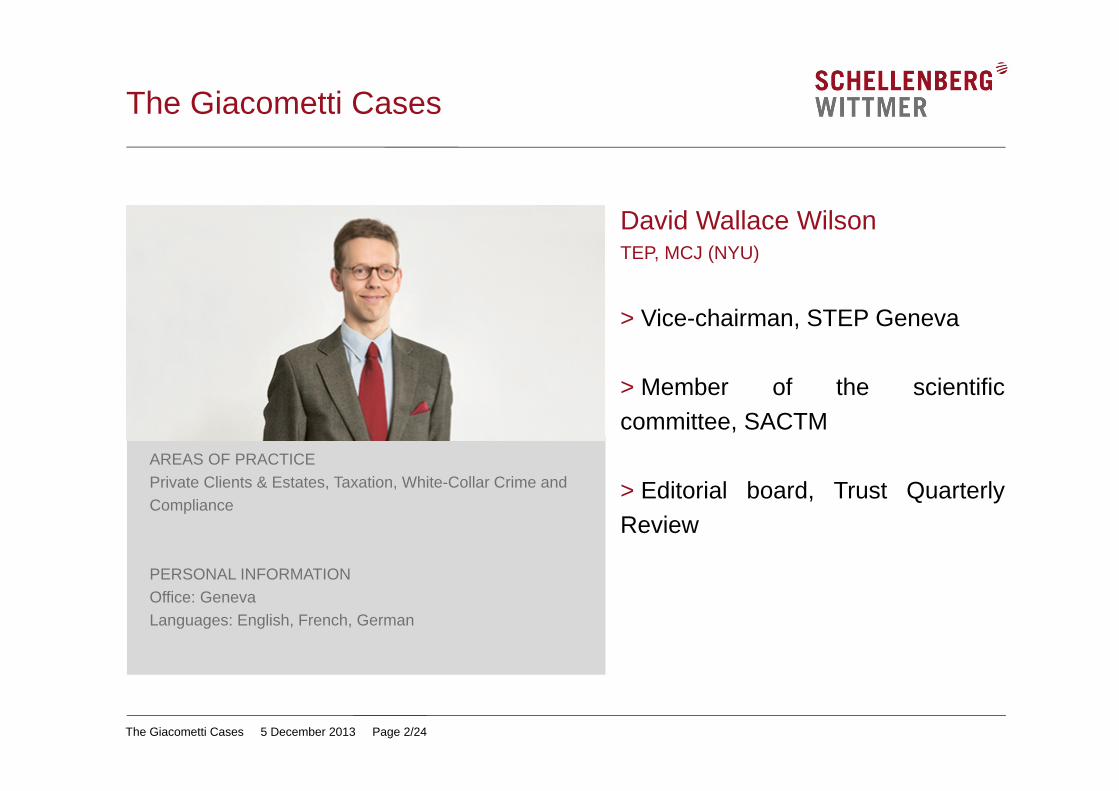

David Wallace-Wilson TEP, Partner – Private Client, Schellenberg Wittmer Ltd - Switzerland

David Wallace Wilson is a partner in Schellenberg Wittmer’s Private Client practice in Switzerland. He advises individuals domestically and internationally on all aspects of wealth structures and tax planning for their personal and business assets. He is specialized in matrimonial and inheritance issues as well as succession vehicles. He also administers cross-border estates and acts in family disputes including mediation. His additional areas of expertise include anti-money laundering (AML) and art law. David has been named as one of the global top 100 practitioners by Legal Week’s International Trust & Private Client Elite 2012 and has

acted as a presiding judge of the STEP Private Client Awards (2011/12 and 2012/13). David currently serves as officer of STEP Geneva and as board member of the Swiss Advanced Certificate in Trust Management. He is one of the editors of the Trust Quarterly Review and the founder of the leading website on trusts in Switzerland (www.trusts.ch). Furthermore, he is frequently quoted in the specialized press and lectures extensively.

The Giacometti Cases (Switzerland)

David Wallace Wilson

Contentious Trusts and Estates: Fights and Friction in Global Trusts and Estates

The Giacometti Cases 5 December 2013 Page 2/24

AREAS OF PRACTICEPrivate Clients & Estates, Taxation, White-Collar Crime and Compliance

PERSONAL INFORMATIONOffice: GenevaLanguages: English, French, German

David Wallace WilsonTEP, MCJ (NYU)

> Vice-chairman, STEP Geneva

> Member of the scientificcommittee, SACTM

> Editorial board, Trust QuarterlyReview

The Giacometti Cases

The Giacometti Cases 5 December 2013 Page 3/24

Table of Contents

1. Facts2. First case3. Second case4. Third case5. Conclusion

The Giacometti Cases 5 December 2013 Page 4/24

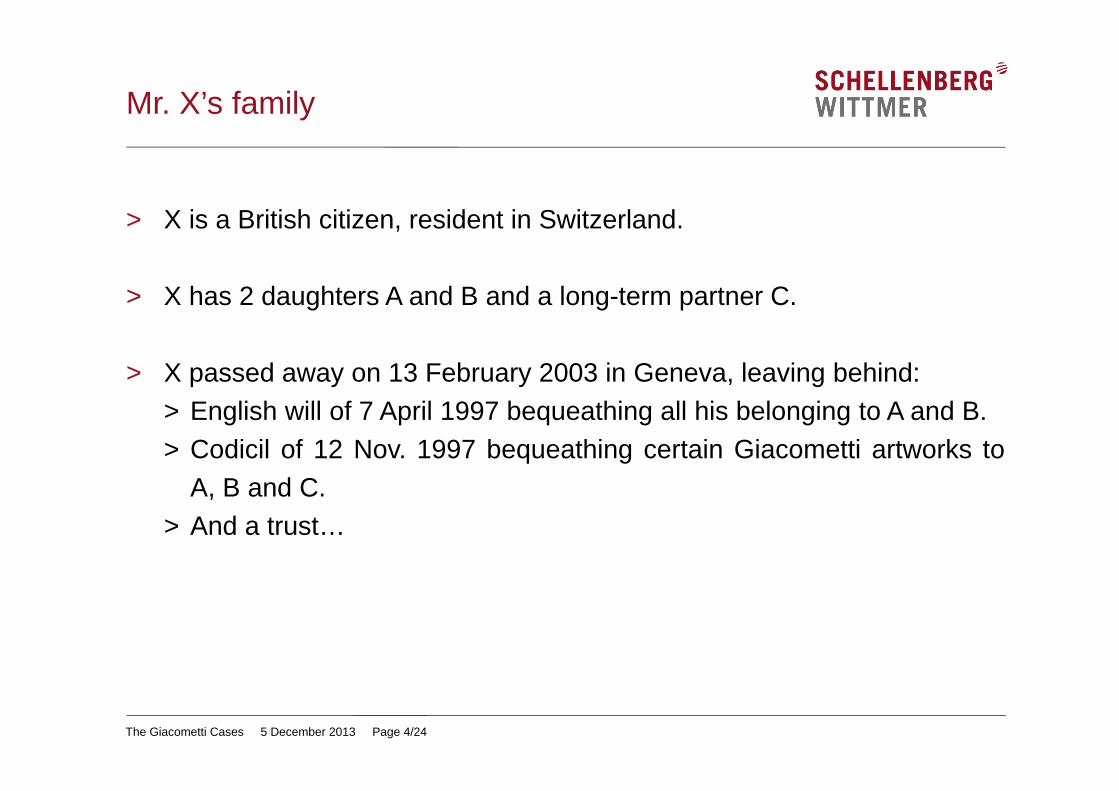

Mr. X’s family

> X is a British citizen, resident in Switzerland.

> X has 2 daughters A and B and a long-term partner C.

> X passed away on 13 February 2003 in Geneva, leaving behind:> English will of 7 April 1997 bequeathing all his belonging to A and B.> Codicil of 12 Nov. 1997 bequeathing certain Giacometti artworks to

A, B and C.> And a trust…

The Giacometti Cases 5 December 2013 Page 5/24

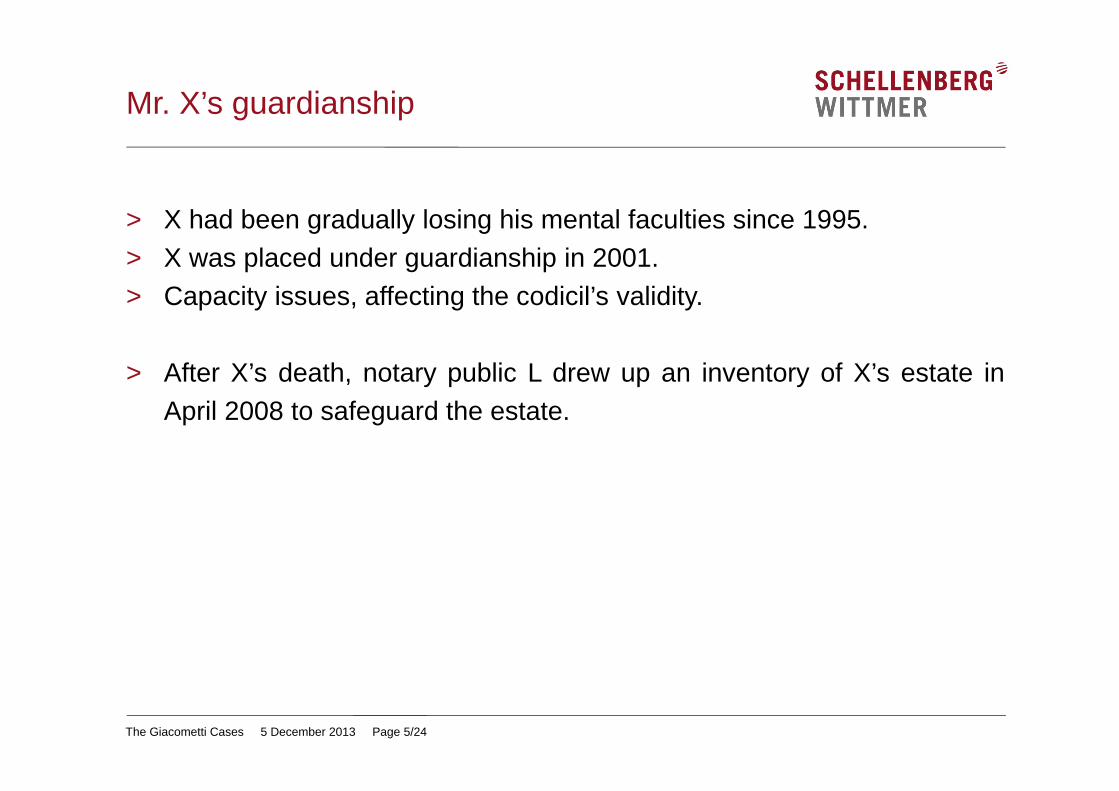

Mr. X’s guardianship

> X had been gradually losing his mental faculties since 1995.> X was placed under guardianship in 2001.> Capacity issues, affecting the codicil’s validity.

> After X’s death, notary public L drew up an inventory of X’s estate inApril 2008 to safeguard the estate.

The Giacometti Cases 5 December 2013 Page 6/24

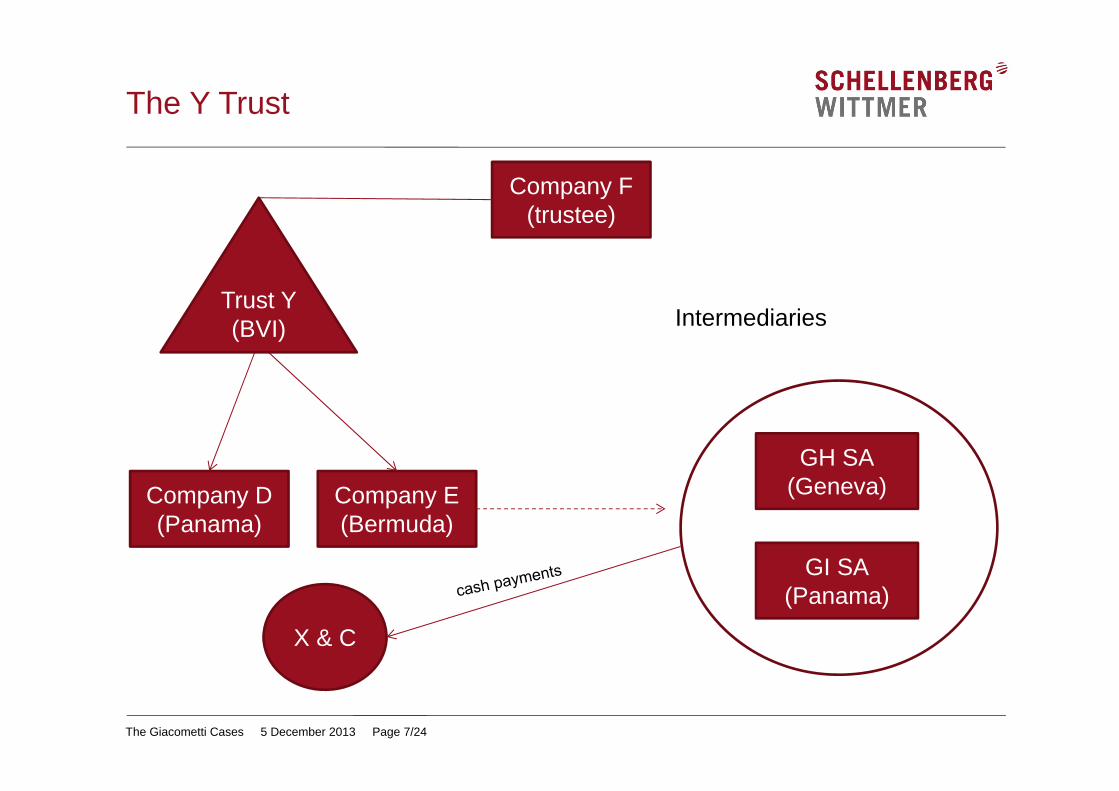

The Y Trust

> BVI discretionary trust.> Trust holds 2 underlying companies.> “The trust was managed by financiers who had little knowledge of trust

law."> X was named neither as settlor nor as beneficiary of the Y Trust.> X’s and C’s living were financed by the Trust from 1997-2003.> All trust payments were made upon X’s wishes as communicated to

intermediaries connected with the offshore companies.

The Giacometti Cases 5 December 2013 Page 7/24

The Y Trust

Company F(trustee)

Company D(Panama)

Company E (Bermuda)

X & C

GI SA(Panama)

GH SA(Geneva)

IntermediariesTrust Y(BVI)

The Giacometti Cases 5 December 2013 Page 8/24

The First Case

The Giacometti Cases 5 December 2013 Page 9/24

The First Claim: Heirs v. partner

> After X’s death, daughters A and B sue C, amongst others, forreimbursement of the funds C consumed during her time with X.

> They allege the funds belonged to X although they were distributedthrough intermediaries.

> As these funds were neither donated by X to C nor used for his livingexpenses, they must be returned to X’s estate, thus to A and B as soletestamentary heirs.

The Giacometti Cases 5 December 2013 Page 10/24

Lower Court Decision

> Relying on a foreign legal opinion, the lower court found that Trust Ywas a sham trust as:

> Trust regularly paid large amounts to X, although he was not a beneficiary.> Trust expenditures were systematically made as per with X’s wishes.

> Therefore, X had never lost control of the funds held by the Trust or itsunderlying companies.

> The funds used by C came from X’s fortune and were to be returned toA and B.

The Giacometti Cases 5 December 2013 Page 11/24

Supreme Court Decision5A_436/2011 and 5A_443/2011 of 12th April 2012

> The Swiss Supreme Court’s review was limited to arbitrariness, as theapplication of foreign law is deemed a question of fact for which theCourt’s cognition is limited.

> The Court correctly applied the Hague Trust Convention: As a rule, atrust is recognised in Switzerland, but one needs to look as to whetherit is valid under its own governing law (art.11§1 HTC).

> The Court confirmed the Lower Court’s decision:> Trust becomes a sham when the settlor uses it “in an artificial manner”.> E.g. when the settlor retains de facto control over the trust assets, which

he ultimately plans to recover.> Such a trust is ineffective as “he who comes to equity must come with

clean hands”.

The Giacometti Cases 5 December 2013 Page 12/24

Open questions

> Trust details: settlor? irrevocable? date of settlement?> Were the payments proper distributions by the trustee? Out of which

funds? To whom were these payments made? Were the recipients trustbeneficiaries?

> We don’t know as C didn’t disclose any facts and trustee wasn’t joinedas defendant.

The Giacometti Cases 5 December 2013 Page 13/24

The Second Case

The Giacometti Cases 5 December 2013 Page 14/24

The Second Claim: Heirs v. notary public

> On 14 November 2011, A and B acted against the notary public L,requesting that he completes the 2008 inventory of X’s estate (art.553Civil Code).

> They requested that L :1. Includes in the inventory all assets uncovered during the first

proceeding, including all payments made by the Trust from 1999 to2003, and

2. Requests the production of all relevant documents from thirdparties.

The Giacometti Cases 5 December 2013 Page 15/24

Lower Court Decision

> The Lower Court ordered L to include all assets held by Trust Y and itsunderlying companies in X’s inventory and to value these assets on thebasis of documents to be requested from third parties.

> However, the Court rejected the heirs’ request to include all paymentsmade by the Trust to third parties from 1999 to 2003.

> Hence, the daughters appealed to the Supreme Court…

The Giacometti Cases 5 December 2013 Page 16/24

Supreme Court Decision5A_434/2012 of 18 December 2012

> The Supreme Court confirmed the Lower Court’s decision.

> A and B cannot rely on the finding of a sham in the first proceeding tojustify the existence of succession claims that they seek to be added toX’s inventory, as that judgment only produced effects inter partes (heirsand partner).

> Moreover, while it is possible to obtain information from third parties tohelp draw up the inventory, this only applies to the decedent’s estate atthe date of his death (2003) and not to prior events.

The Giacometti Cases 5 December 2013 Page 17/24

Supreme Court Decision5A_434/2012 of 18 December 2012

> Furthermore, an inventory aims at safeguarding the succession’ssubstance, so the right to obtain information from third parties cannotgo beyond this aim.> Thus, third parties can be compelled to cooperate when there is an obvious

right to information (e.g. the decedent held a personal bank account), but notif the decedent is only the beneficial owner of assets and the right toinformation is disputed.

> Here, X is, at best, the beneficial owner of the Trust’s assets and the right toinformation is in dispute, so the notary is not empowered to obtaininformation from the Trustee or its intermediaries.

> Therefore, any succession claim resulting from payments made by theTrust cannot be included in the inventory.

The Giacometti Cases 5 December 2013 Page 18/24

The Third Case

The Giacometti Cases 5 December 2013 Page 19/24

ClaimHeirs’ non-contentious application

> On 8 June 2012, A and B requested from the local probate court toorder by interim relief the delivery in its hands of all assets held byTrust Y and its underlying companies (art.551-552 Civil Code).

The Giacometti Cases 5 December 2013 Page 20/24

Lower Court Decision

> Both lower courts rejected the request, considering it to be without alegal basis.

> A and B appealed to the Supreme Court, claiming that their right to beheard had been infringed and that the lower courts’ decisions werearbitrary.

The Giacometti Cases 5 December 2013 Page 21/24

Supreme Court Decision5A_763/2012 of 18 March 2013

> The Supreme Court confirmed the Lower Court’s decision.> Interim measures, such as those requested, are taken in a non-

contentious procedure, whose sole aim is to guarantee the devolutionof the decedent’s estate and not to settle disputes among his survivors.

> Further, affixing seals or ordering alternative measures are onlypossible over assets that the decedent possessed, not over assets heldby third parties.

> Again, A and B cannot rely on the first proceeding as it was notopposable to Trust Y or its intermediaries who were not parties to thatdispute.

The Giacometti Cases 5 December 2013 Page 22/24

Conclusions

The Giacometti Cases 5 December 2013 Page 23/24

Conclusions

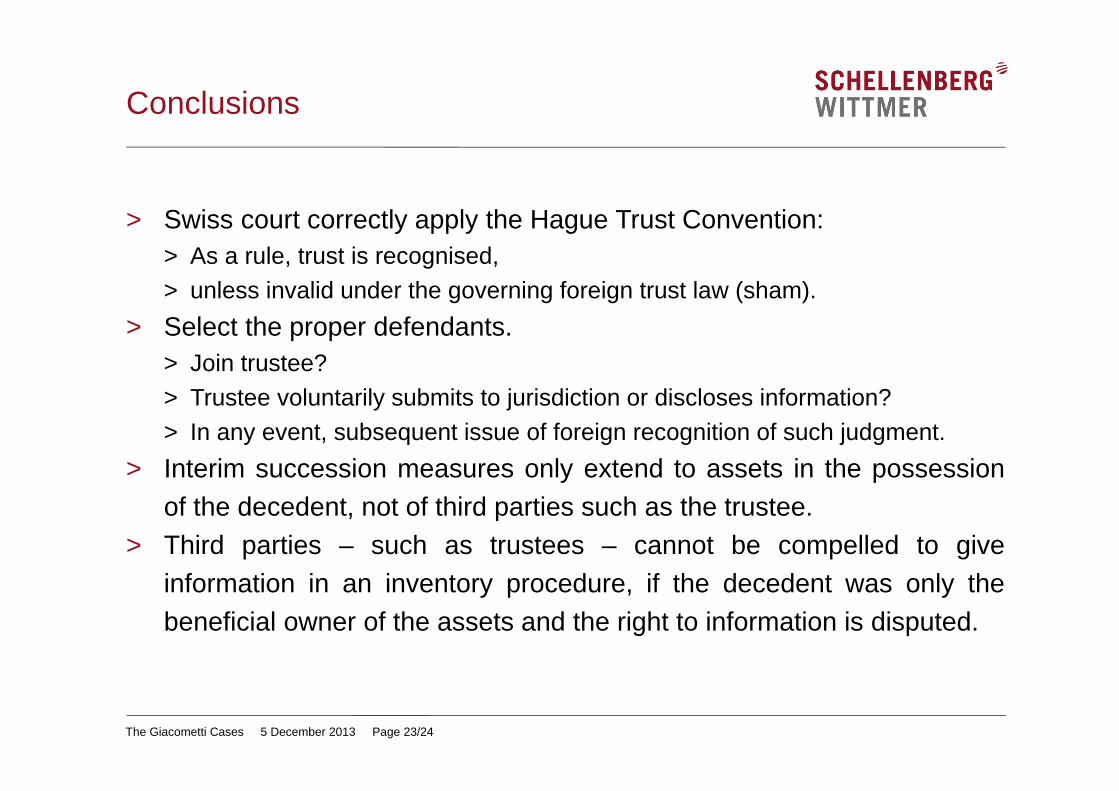

> Swiss court correctly apply the Hague Trust Convention:> As a rule, trust is recognised,> unless invalid under the governing foreign trust law (sham).

> Select the proper defendants.> Join trustee?> Trustee voluntarily submits to jurisdiction or discloses information?> In any event, subsequent issue of foreign recognition of such judgment.

> Interim succession measures only extend to assets in the possessionof the decedent, not of third parties such as the trustee.

> Third parties – such as trustees – cannot be compelled to giveinformation in an inventory procedure, if the decedent was only thebeneficial owner of the assets and the right to information is disputed.

The Giacometti Cases 5 December 2013 Page 24/24

David Wallace [email protected]

Schellenberg Wittmer Ltd / Attorneys at Law15bis, rue des AlpesP.O. Box 20881211 Geneva 1 / SwitzerlandT +41 22 707 8000 F +41 22 707 8001

Cases & more: www.trusts.ch

Thank you for your attention.

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 _____________________________________________________________________________

Nicholas Le Poidevin QC TEP, New Square Chambers - UK

Nicholas Le Poidevin, Q.C.’s practice is largely contentious and the focus is on trusts, wills and estates, and real property, together with the associated professional negligence and conflicts of laws. Recent cases are Marley v. Rawlings [2013] Ch. 271, CA (switched wills; in the Supreme Court in December 2013) and Re A Trust [2012] Bda L.R. 79, Bermuda (jurisdiction clause in trust). Current work includes investment claims on behalf of trusts, fiduciary duties and confidentiality within a complex trust structure, and unravelling problems with past trust administration. He regularly appears in courts offshore and accepts instructions from Jersey, Guernsey, the Isle of

Man, Bermuda, the Cayman Islands and the B.V.I. He is also an editor of Lewin on Trusts (18th ed., 2008; Third Supplement 2012) and has contributed chapters to Sham Transactions (2013) and A Practical Guide to the Transfer of Trusteeships (2nd ed., 2011). He sits as a deputy high Court judge.

STEPContentiousTrustsandEstates

SpecialInterestGroupConference‐ December5,2013

DisputesaboutForeignTaxNicholasLePoidevin,Q.C.NewSquareChambersLincoln’sInn,London

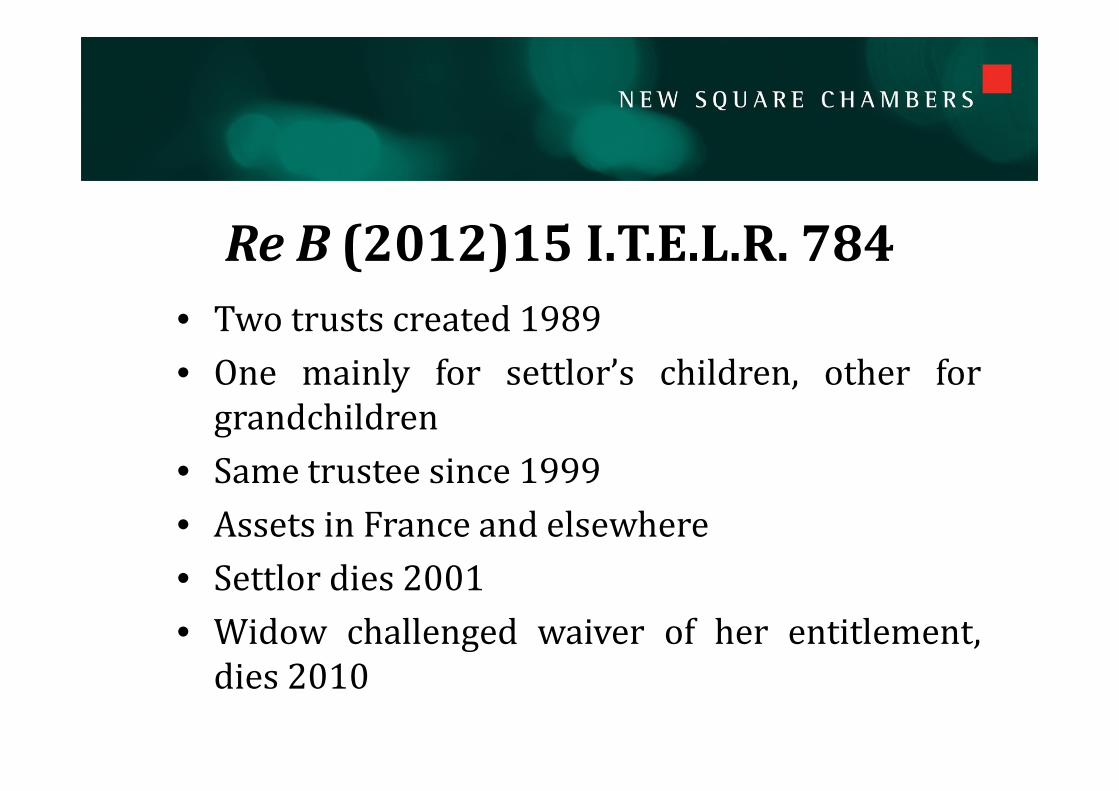

ReB(2012)15I.T.E.L.R.784• Two trusts created 1989• One mainly for settlor’s children, other forgrandchildren

• Same trustee since 1999• Assets in France and elsewhere• Settlor dies 2001• Widow challenged waiver of her entitlement,dies 2010

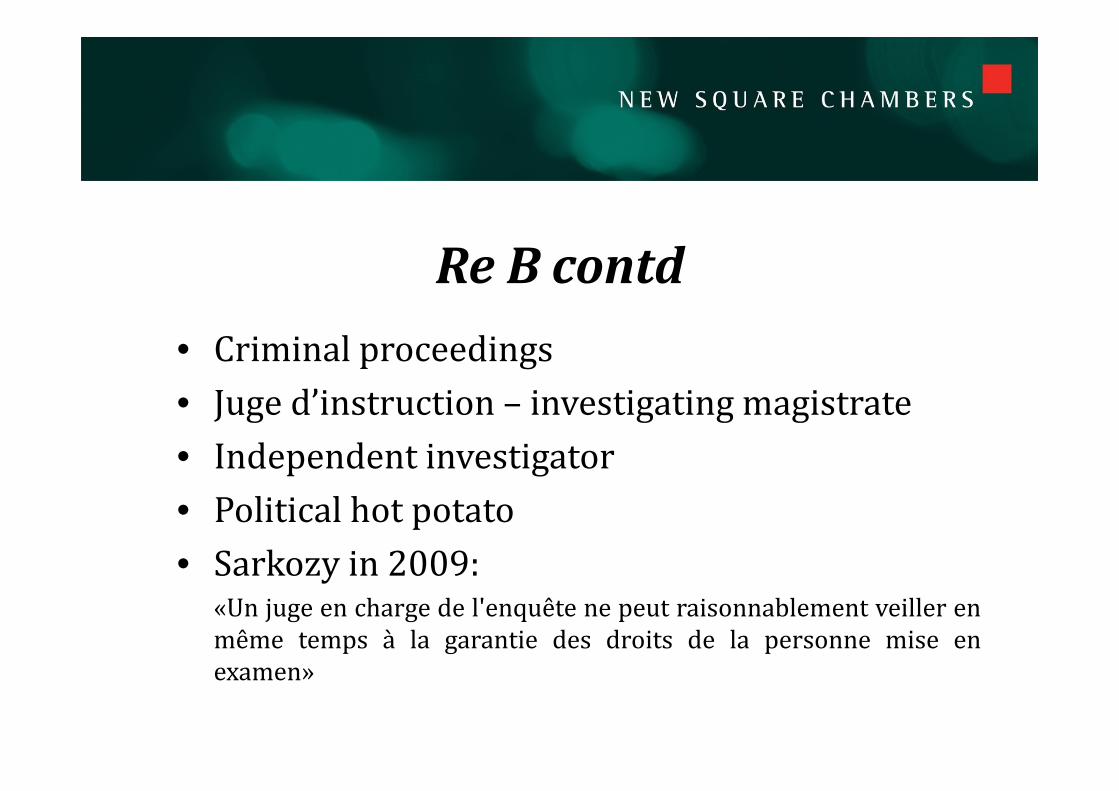

ReBcontd• Criminal proceedings• Juge d’instruction – investigating magistrate• Independent investigator• Political hot potato• Sarkozy in 2009:

«Un juge en charge de l'enquête ne peut raisonnablement veiller enmême temps à la garantie des droits de la personne mise enexamen»

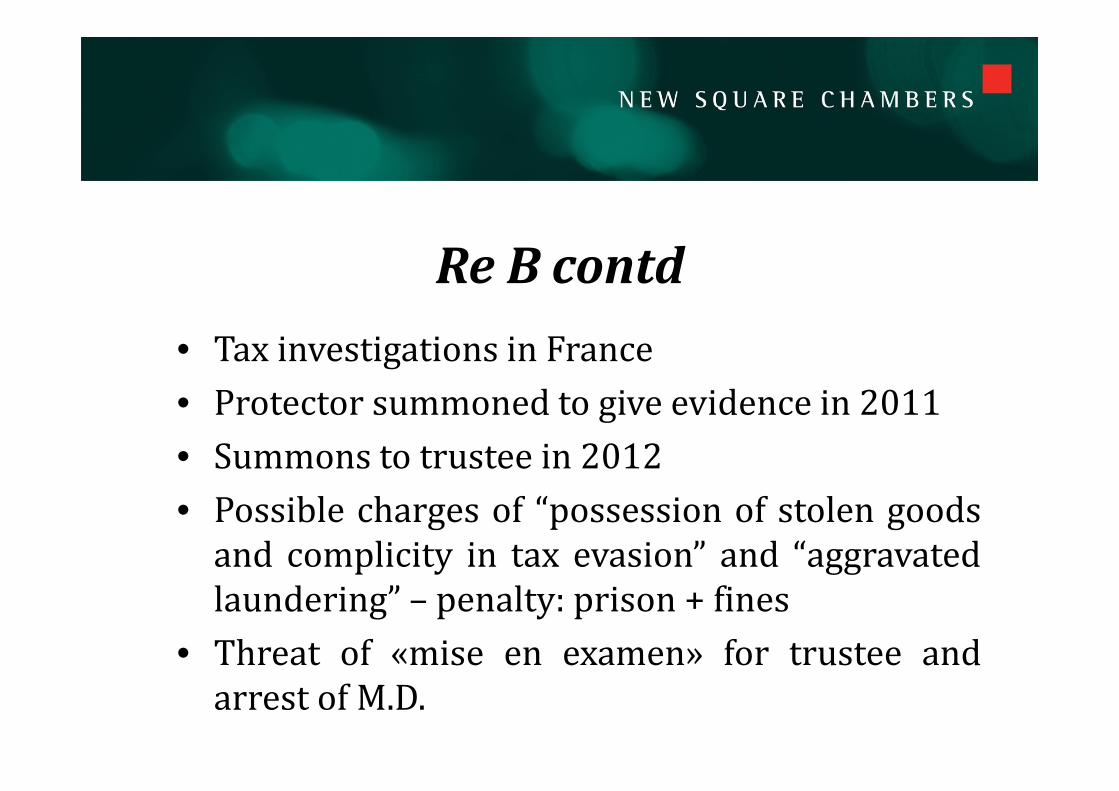

ReBcontd• Tax investigations in France• Protector summoned to give evidence in 2011• Summons to trustee in 2012• Possible charges of “possession of stolen goodsand complicity in tax evasion” and “aggravatedlaundering” – penalty: prison + fines

• Threat of «mise en examen» for trustee andarrest of M.D.

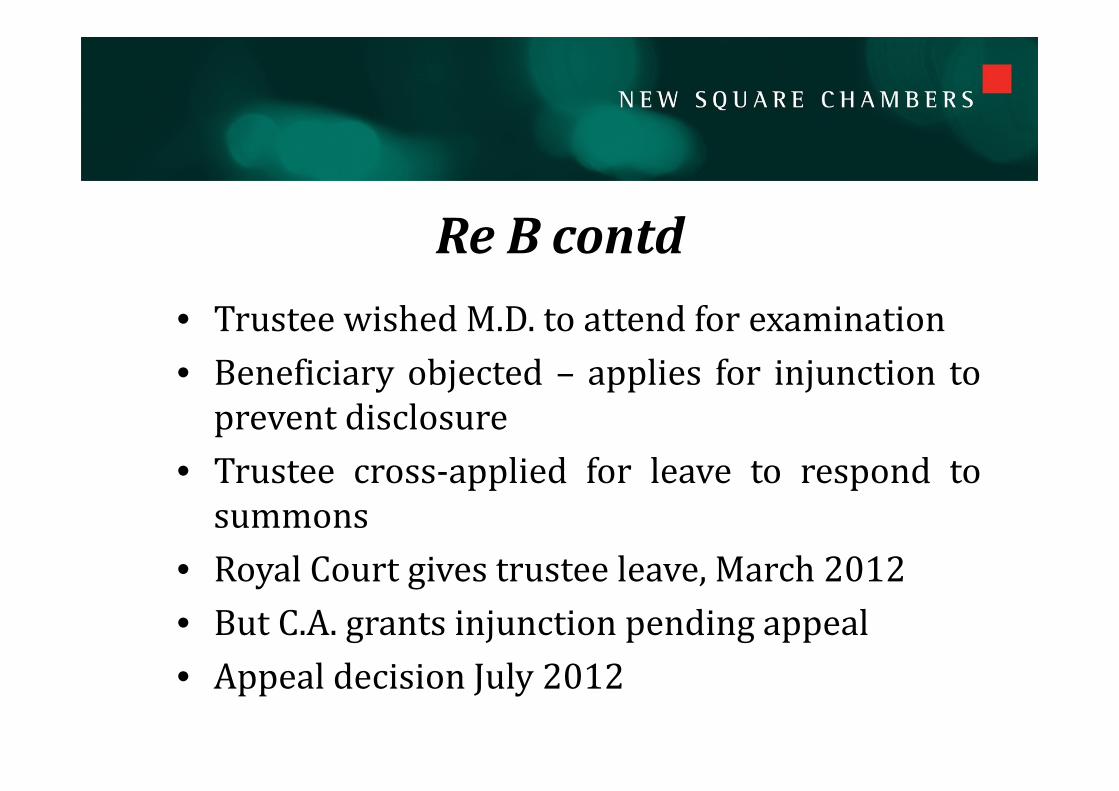

ReBcontd• Trustee wished M.D. to attend for examination• Beneficiary objected – applies for injunction toprevent disclosure

• Trustee cross‐applied for leave to respond tosummons

• Royal Court gives trustee leave, March 2012• But C.A. grants injunction pending appeal• Appeal decision July 2012

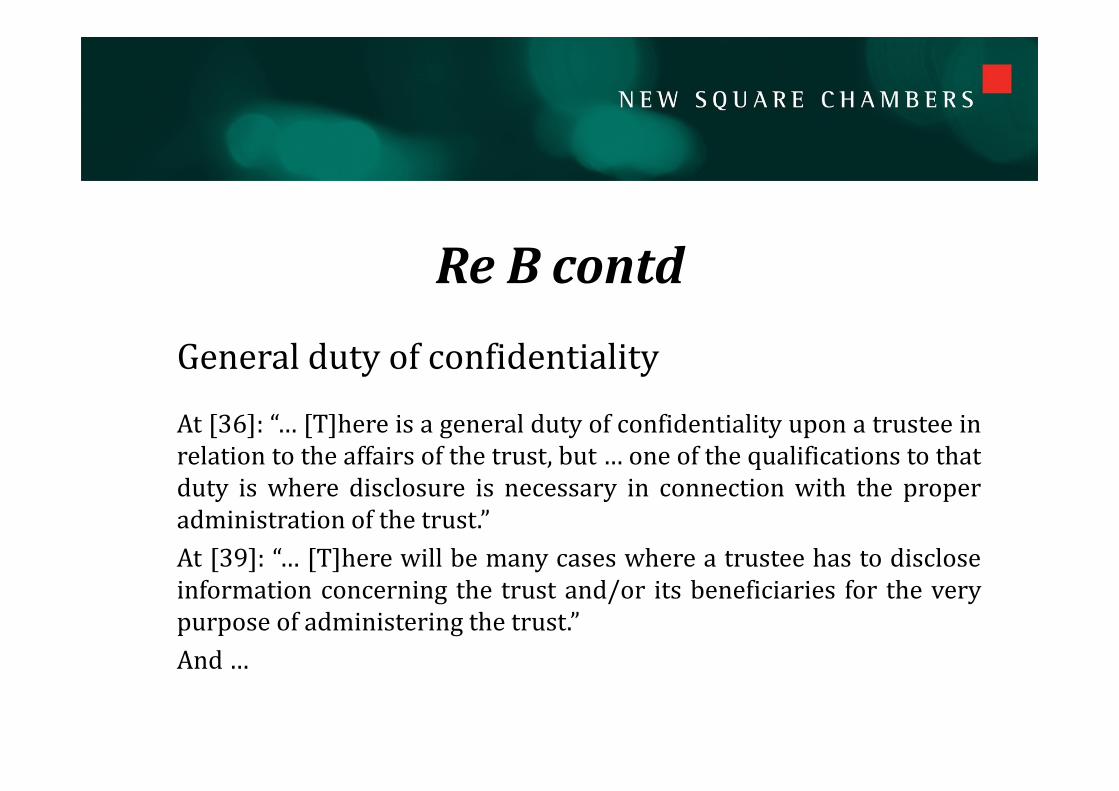

ReBcontdGeneraldutyofconfidentiality

At [36]: “… [T]here is a general duty of confidentiality upon a trustee inrelation to the affairs of the trust, but … one of the qualifications to thatduty is where disclosure is necessary in connection with the properadministration of the trust.”At [39]: “… [T]here will be many cases where a trustee has to discloseinformation concerning the trust and/or its beneficiaries for the verypurpose of administering the trust.”And…

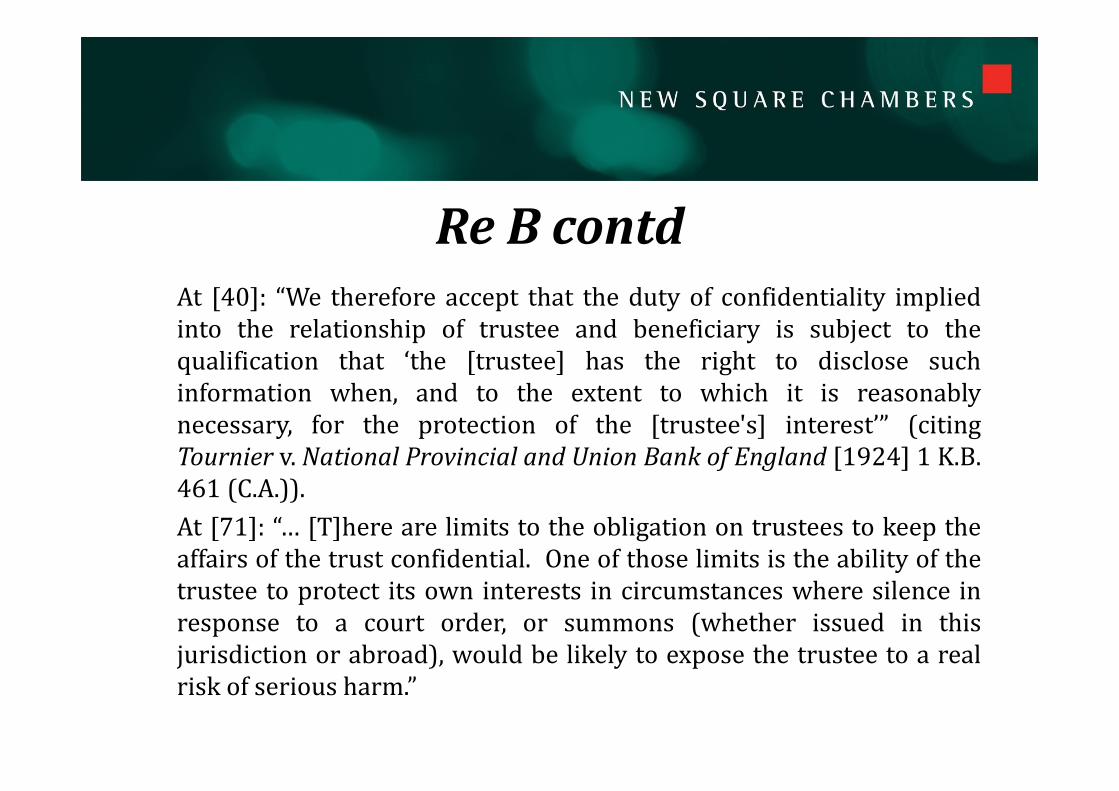

ReBcontdAt [40]: “We therefore accept that the duty of confidentiality impliedinto the relationship of trustee and beneficiary is subject to thequalification that ‘the [trustee] has the right to disclose suchinformation when, and to the extent to which it is reasonablynecessary, for the protection of the [trustee's] interest’” (citingTournier v. National Provincial and Union Bank of England [1924] 1 K.B.461 (C.A.)).At [71]: “… [T]here are limits to the obligation on trustees to keep theaffairs of the trust confidential. One of those limits is the ability of thetrustee to protect its own interests in circumstances where silence inresponse to a court order, or summons (whether issued in thisjurisdiction or abroad), would be likely to expose the trustee to a realrisk of serious harm.”

ReBcontdBalancingexercisecarriedoutbycourt

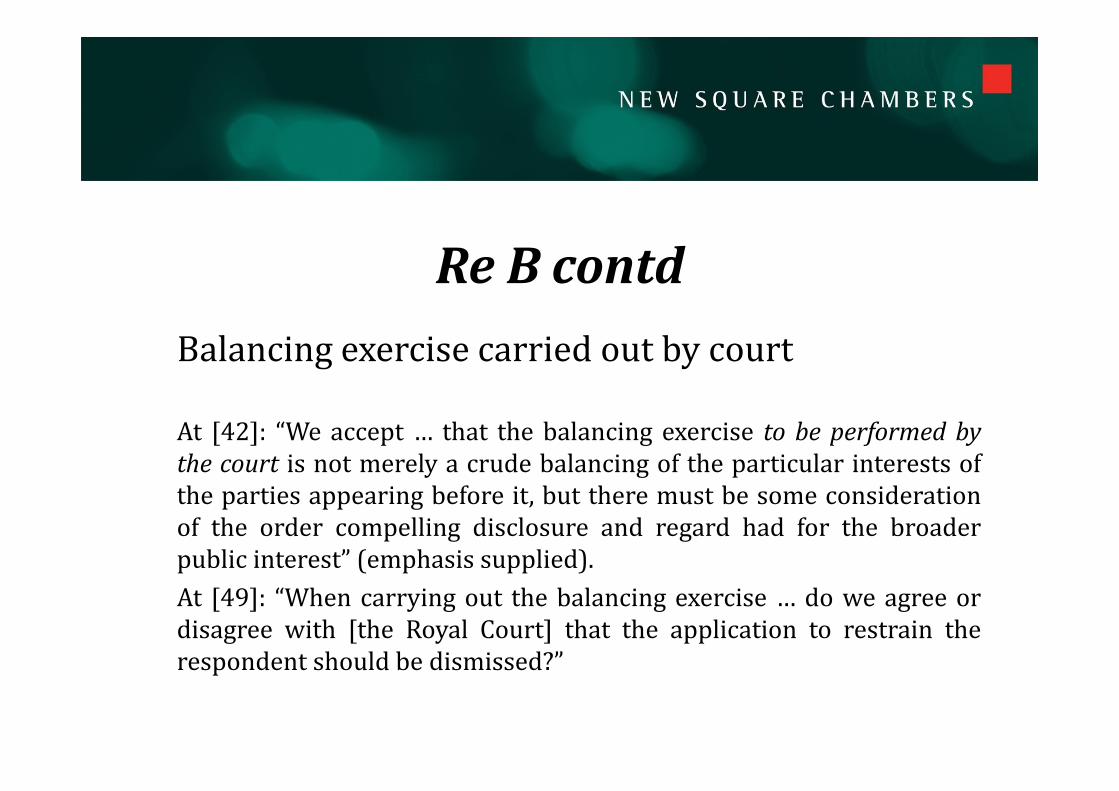

At [42]: “We accept … that the balancing exercise to be performed bythe court is not merely a crude balancing of the particular interests ofthe parties appearing before it, but there must be some considerationof the order compelling disclosure and regard had for the broaderpublic interest” (emphasis supplied).At [49]: “When carrying out the balancing exercise … do we agree ordisagree with [the Royal Court] that the application to restrain therespondent should be dismissed?”

ReBcontd

Queries

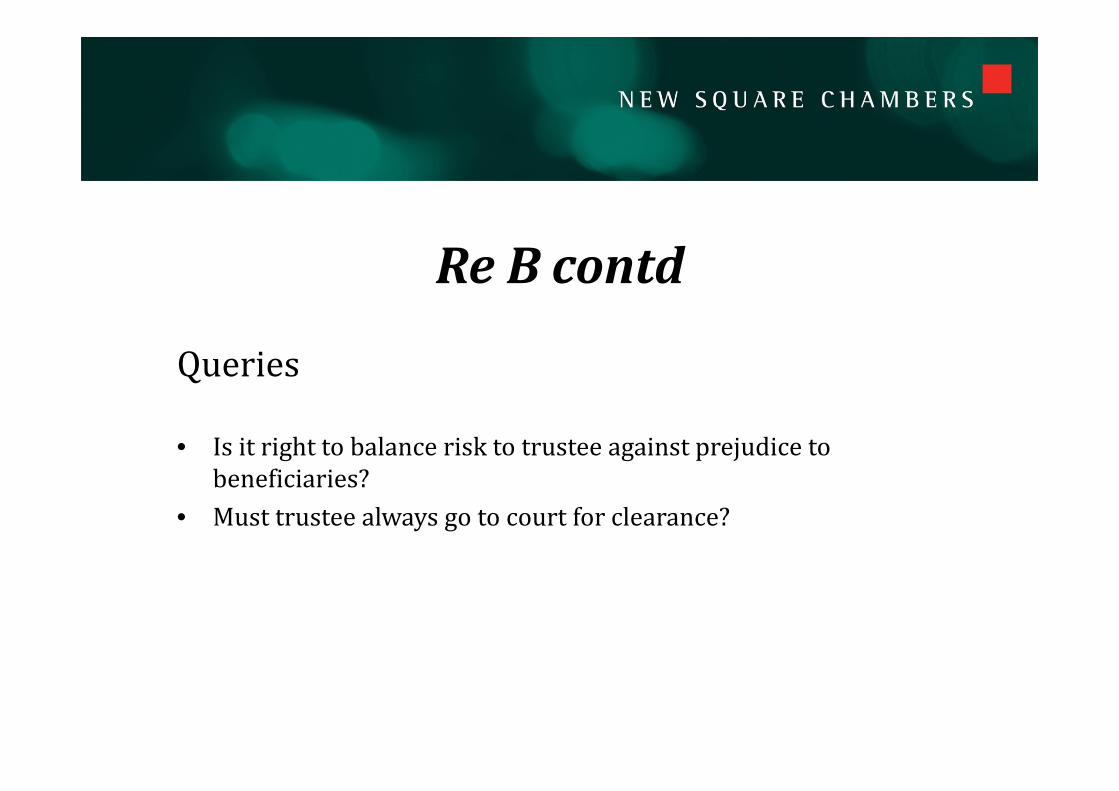

• Isitrighttobalancerisktotrusteeagainstprejudicetobeneficiaries?

• Musttrusteealwaysgotocourtforclearance?

Foreigntaxliabilities

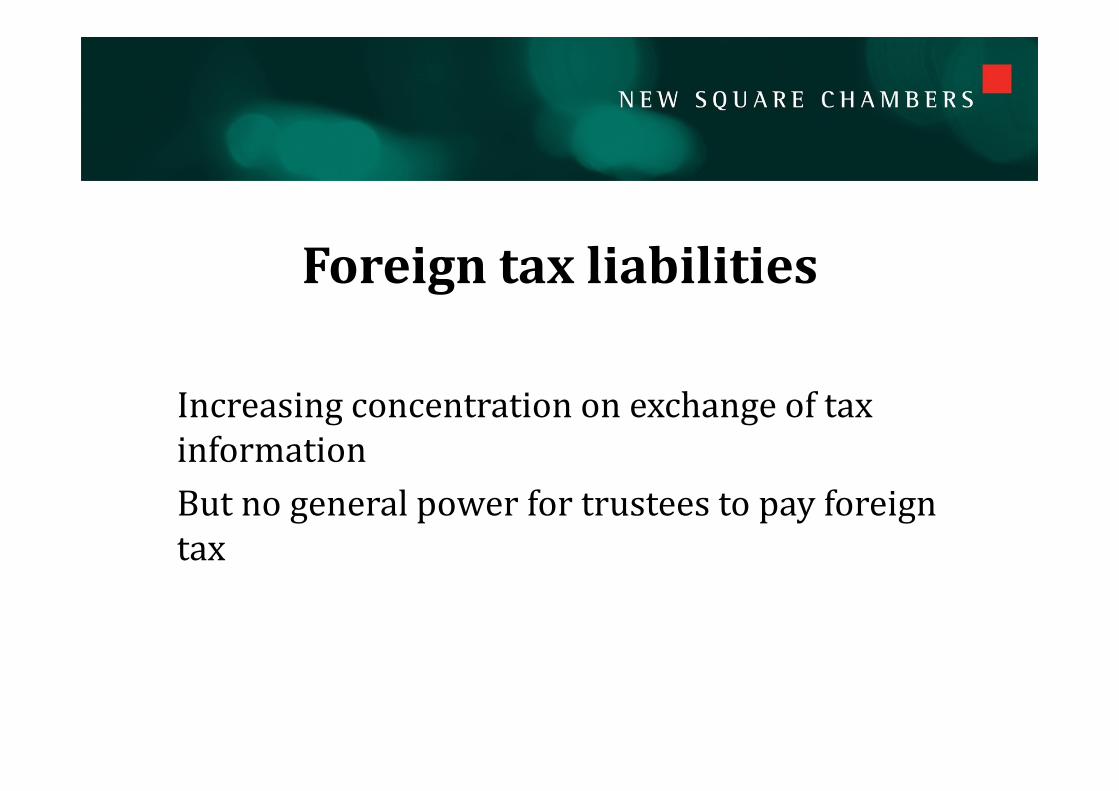

IncreasingconcentrationonexchangeoftaxinformationButnogeneralpowerfortrusteestopayforeigntax

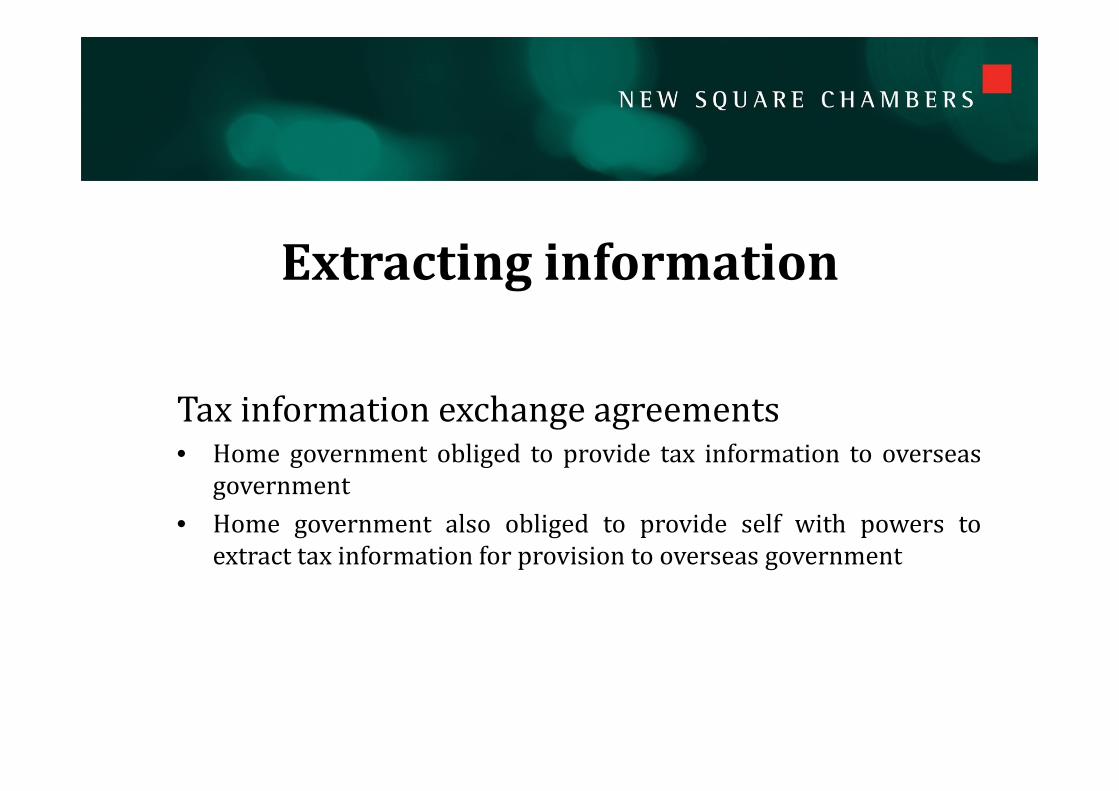

Extractinginformation

Taxinformationexchangeagreements• Home government obliged to provide tax information to overseas

government• Home government also obliged to provide self with powers to

extract tax information for provision to overseas government

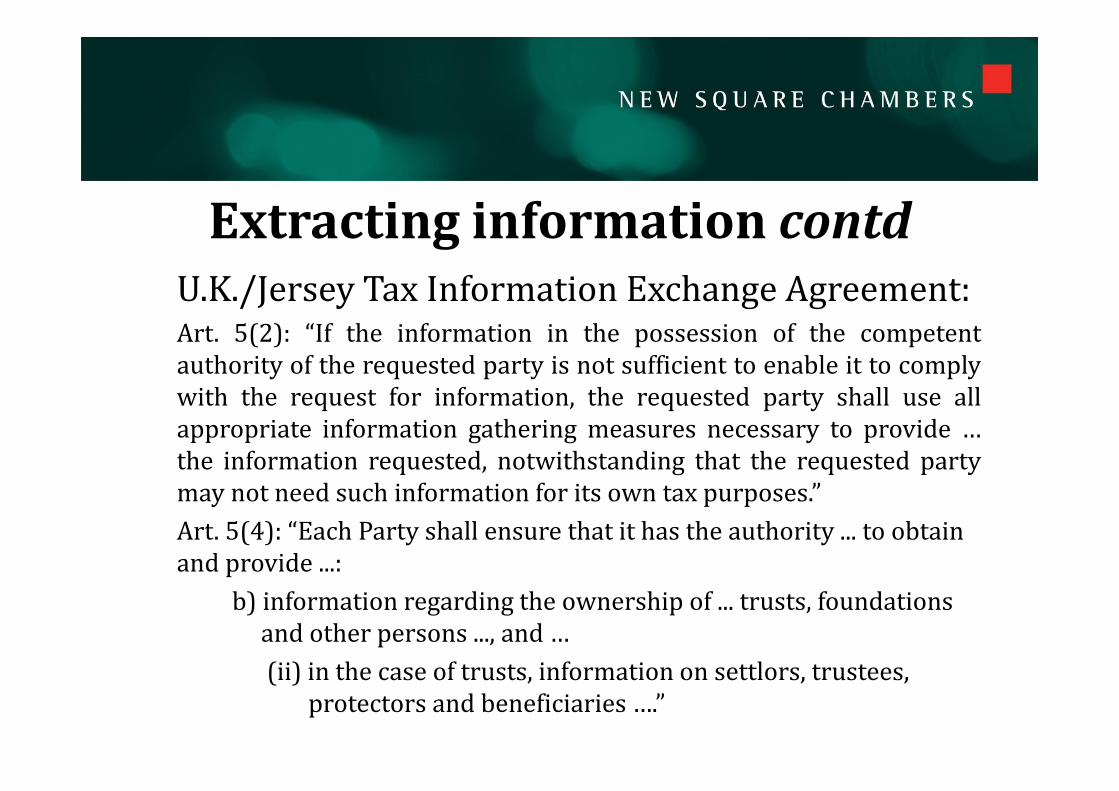

ExtractinginformationcontdU.K./Jersey Tax Information Exchange Agreement:Art. 5(2): “If the information in the possession of the competentauthority of the requested party is not sufficient to enable it to complywith the request for information, the requested party shall use allappropriate information gathering measures necessary to provide …the information requested, notwithstanding that the requested partymay not need such information for its own tax purposes.”Art.5(4):“EachPartyshallensurethatithastheauthority...toobtainandprovide...:

b)informationregardingtheownershipof...trusts,foundationsandotherpersons...,and…(ii)inthecaseoftrusts,informationonsettlors,trustees,

protectorsandbeneficiaries….”

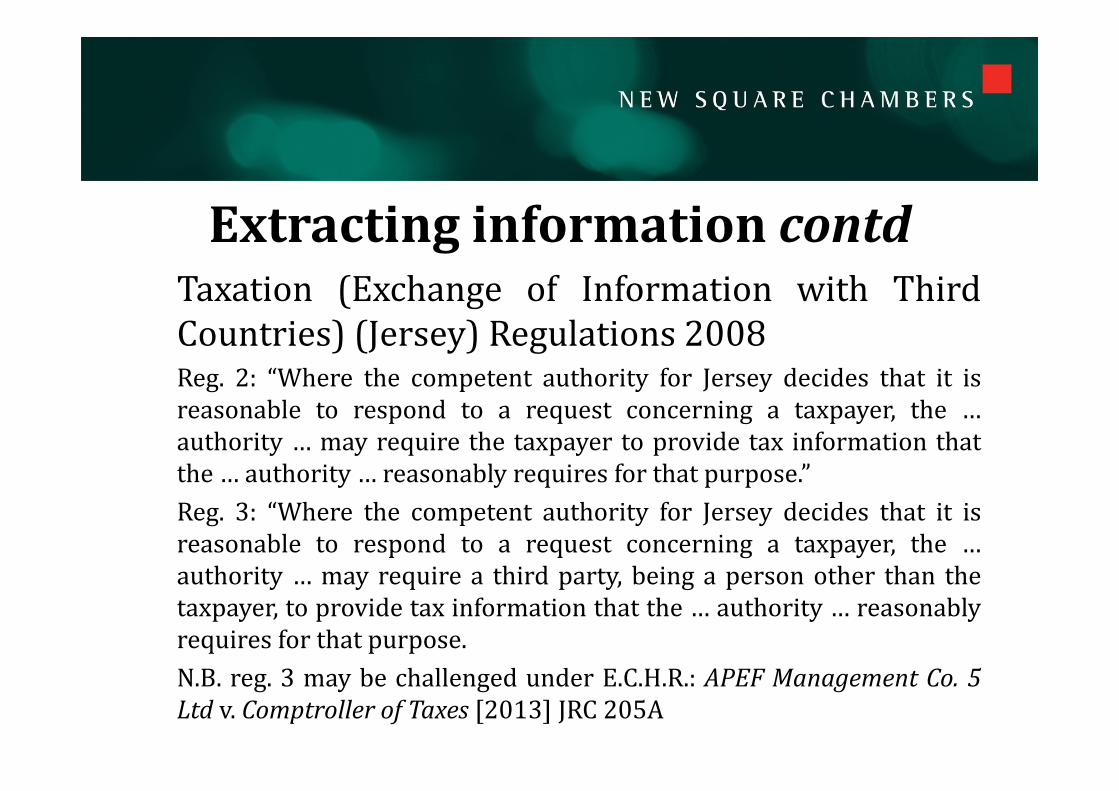

ExtractinginformationcontdTaxation (Exchange of Information with ThirdCountries) (Jersey) Regulations 2008Reg. 2: “Where the competent authority for Jersey decides that it isreasonable to respond to a request concerning a taxpayer, the …authority … may require the taxpayer to provide tax information thatthe … authority … reasonably requires for that purpose.”Reg. 3: “Where the competent authority for Jersey decides that it isreasonable to respond to a request concerning a taxpayer, the …authority … may require a third party, being a person other than thetaxpayer, to provide tax information that the … authority … reasonablyrequires for that purpose.N.B. reg. 3 may be challenged under E.C.H.R.: APEF Management Co. 5Ltd v. Comptroller of Taxes [2013] JRC 205A

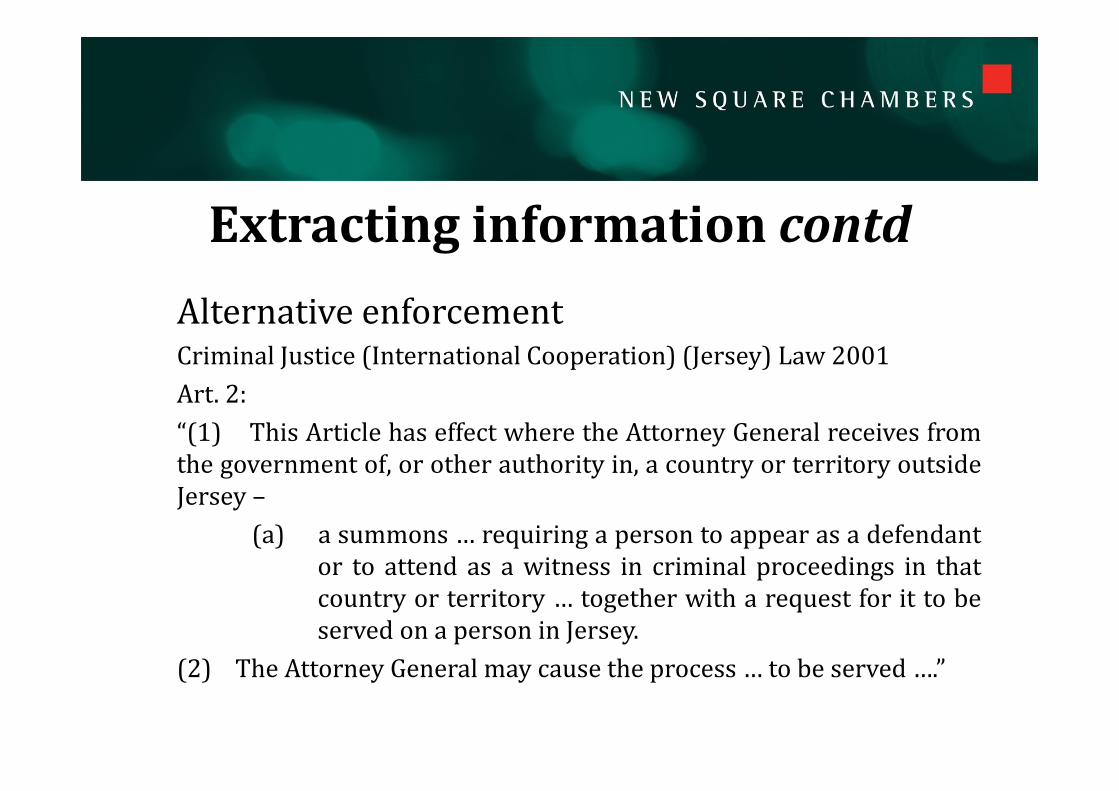

ExtractinginformationcontdAlternative enforcementCriminal Justice (International Cooperation) (Jersey) Law 2001Art. 2:“(1) This Article has effect where the Attorney General receives fromthe government of, or other authority in, a country or territory outsideJersey –

(a) a summons … requiring a person to appear as a defendantor to attend as a witness in criminal proceedings in thatcountry or territory … together with a request for it to beserved on a person in Jersey.

(2) The Attorney General may cause the process … to be served ….”

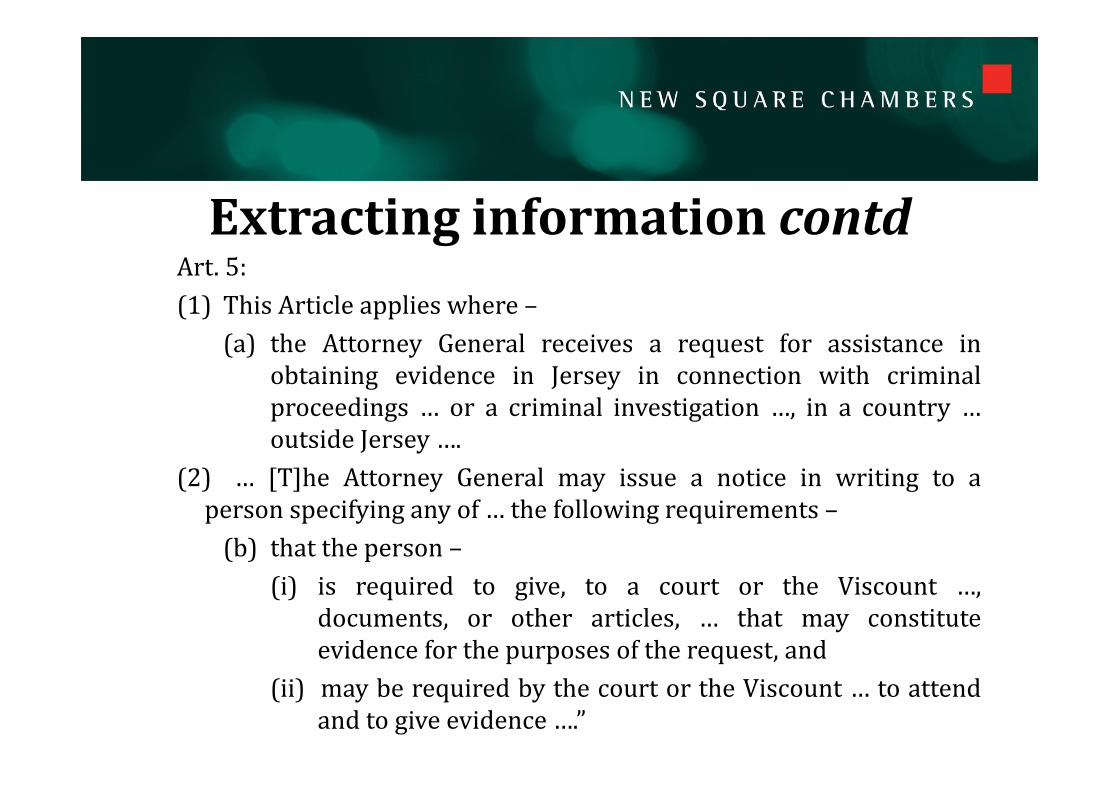

ExtractinginformationcontdArt. 5:(1) This Article applies where –

(a) the Attorney General receives a request for assistance inobtaining evidence in Jersey in connection with criminalproceedings … or a criminal investigation …, in a country …outside Jersey ….

(2) … [T]he Attorney General may issue a notice in writing to aperson specifying any of … the following requirements –(b) that the person –

(i) is required to give, to a court or the Viscount …,documents, or other articles, … that may constituteevidence for the purposes of the request, and

(ii) may be required by the court or the Viscount … to attendand to give evidence ….”

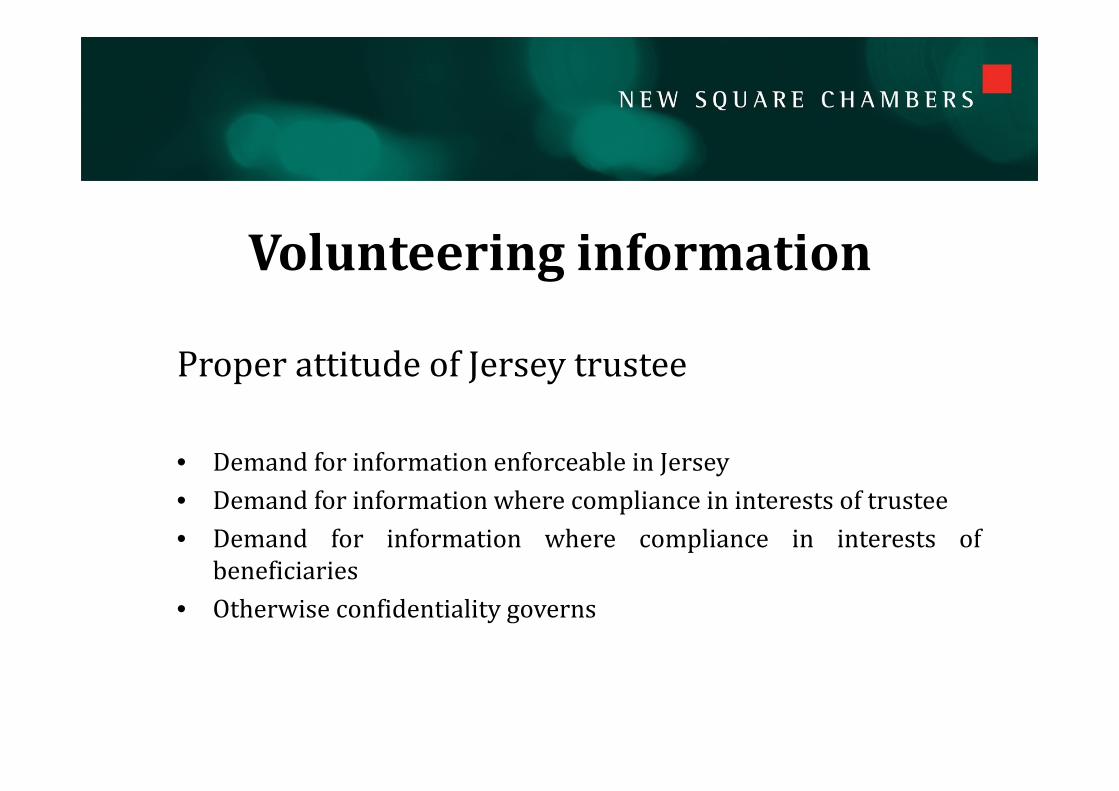

Volunteeringinformation

Proper attitude of Jersey trustee

• Demand for information enforceable in Jersey• Demand for information where compliance in interests of trustee• Demand for information where compliance in interests of

beneficiaries• Otherwise confidentiality governs

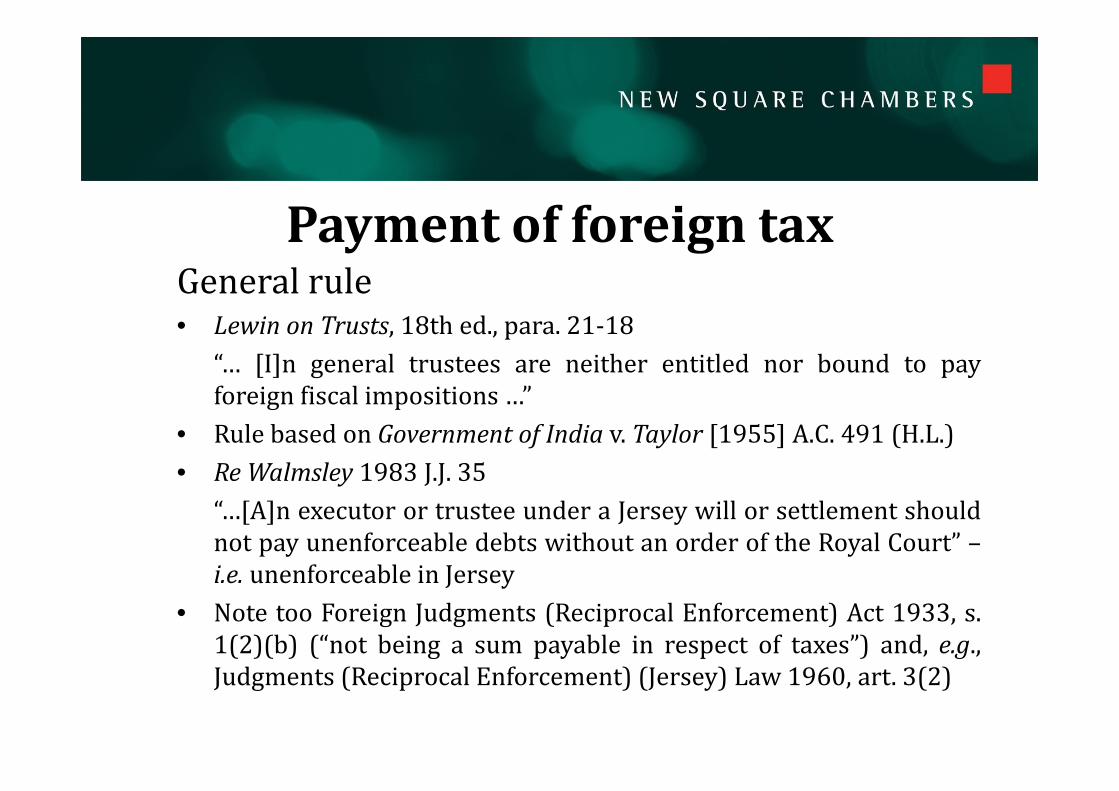

PaymentofforeigntaxGeneral rule• Lewin on Trusts, 18th ed., para. 21‐18

“… [I]n general trustees are neither entitled nor bound to payforeign fiscal impositions …”

• Rule based on Government of India v. Taylor [1955] A.C. 491 (H.L.)• Re Walmsley 1983 J.J. 35

“…[A]n executor or trustee under a Jersey will or settlement shouldnot pay unenforceable debts without an order of the Royal Court” –i.e. unenforceable in Jersey

• Note too Foreign Judgments (Reciprocal Enforcement) Act 1933, s.1(2)(b) (“not being a sum payable in respect of taxes”) and, e.g.,Judgments (Reciprocal Enforcement) (Jersey) Law 1960, art. 3(2)

Paymentofforeigntaxcontd

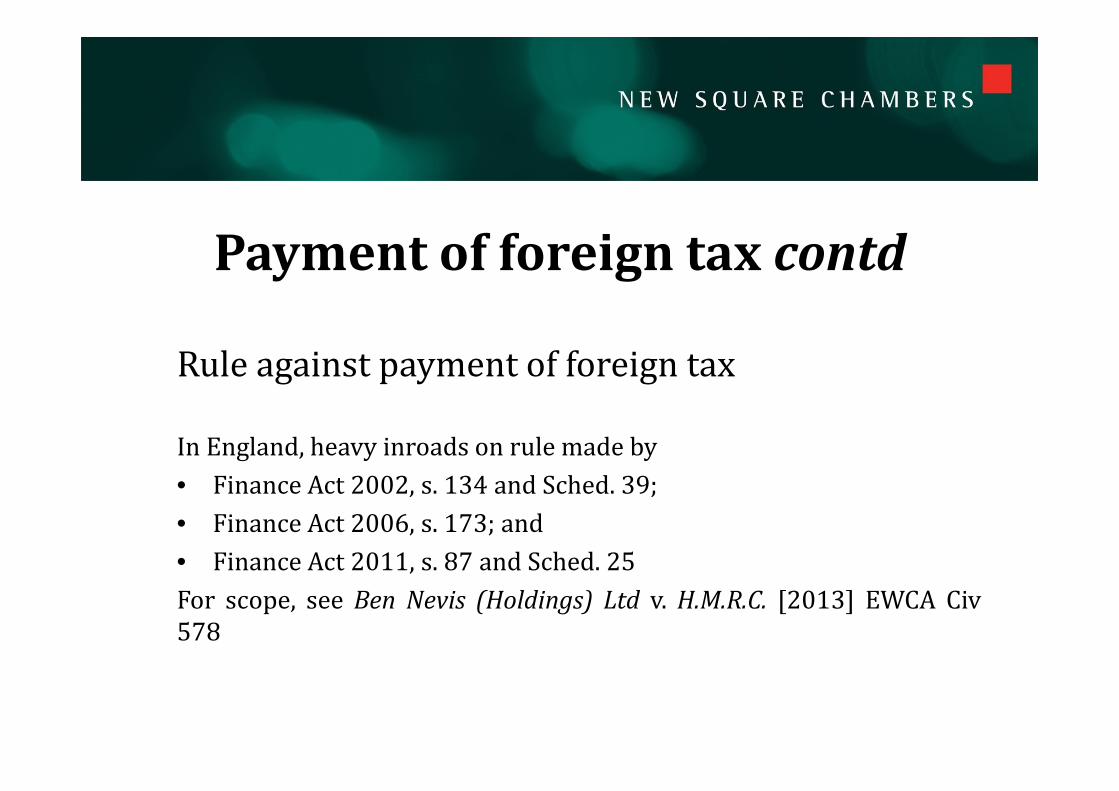

Rule against payment of foreign tax

In England, heavy inroads on rule made by• Finance Act 2002, s. 134 and Sched. 39;• Finance Act 2006, s. 173; and• Finance Act 2011, s. 87 and Sched. 25For scope, see Ben Nevis (Holdings) Ltd v. H.M.R.C. [2013] EWCA Civ578

Paymentofforeigntaxcontd

Rule against payment of foreign tax

• Consistent with rule against voluntary compliance with foreigndemands for trust information

• Hard to reconcile with extensive powers to compel disclosure

Paymentofforeigntaxcontd

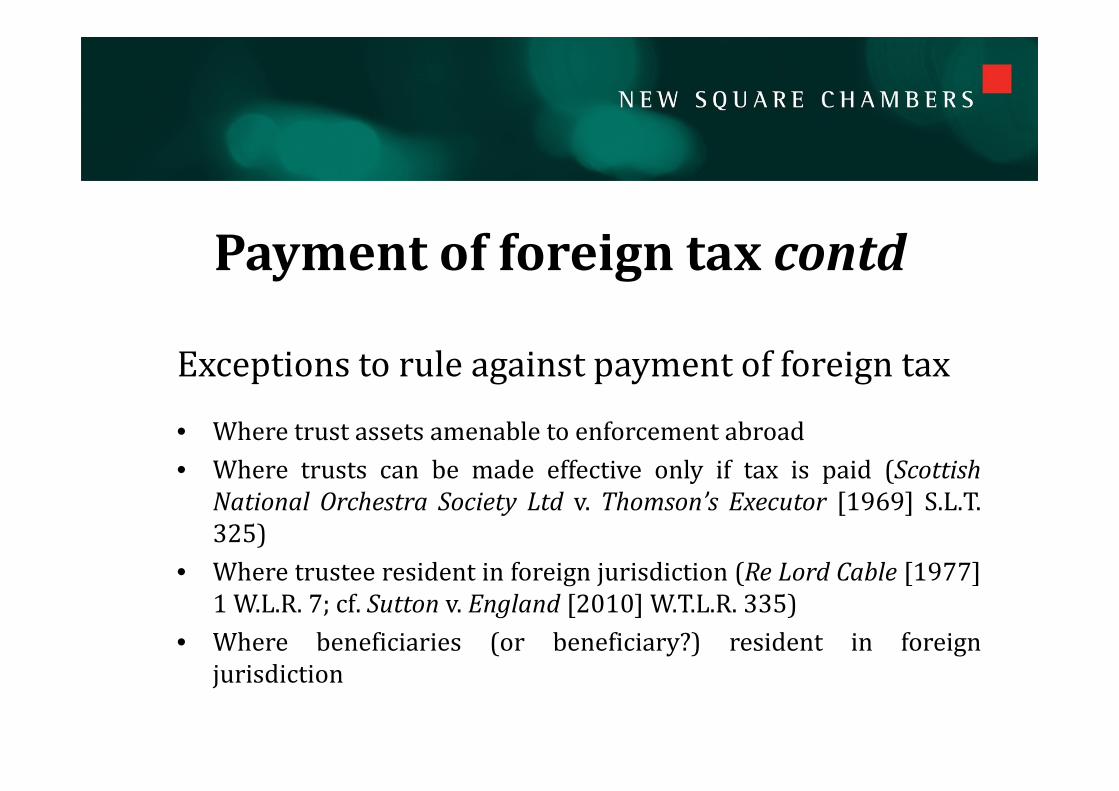

Exceptions to rule against payment of foreign tax

• Where trust assets amenable to enforcement abroad• Where trusts can be made effective only if tax is paid (Scottish

National Orchestra Society Ltd v. Thomson’s Executor [1969] S.L.T.325)

• Where trustee resident in foreign jurisdiction (Re Lord Cable [1977]1 W.L.R. 7; cf. Sutton v. England [2010] W.T.L.R. 335)

• Where beneficiaries (or beneficiary?) resident in foreignjurisdiction

Paymentofforeigntaxcontd

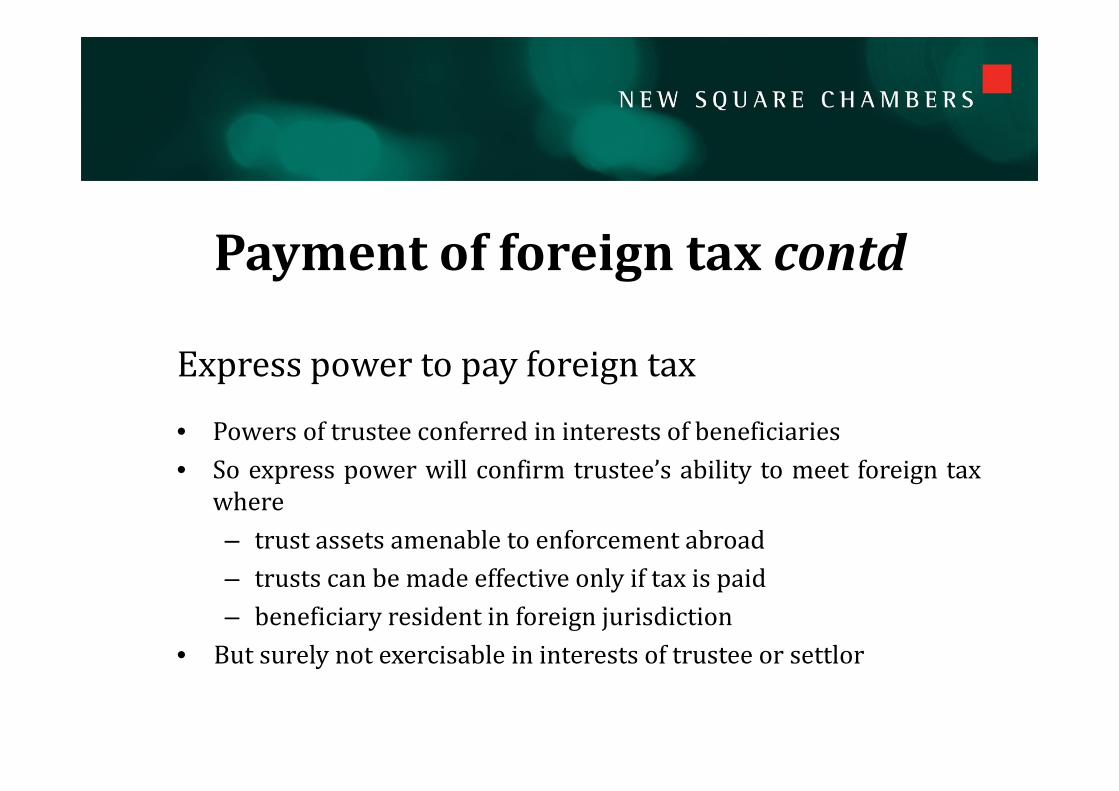

Express power to pay foreign tax

• Powers of trustee conferred in interests of beneficiaries• So express power will confirm trustee’s ability to meet foreign tax

where– trust assets amenable to enforcement abroad– trusts can be made effective only if tax is paid– beneficiary resident in foreign jurisdiction

• But surely not exercisable in interests of trustee or settlor

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 _____________________________________________________________________________

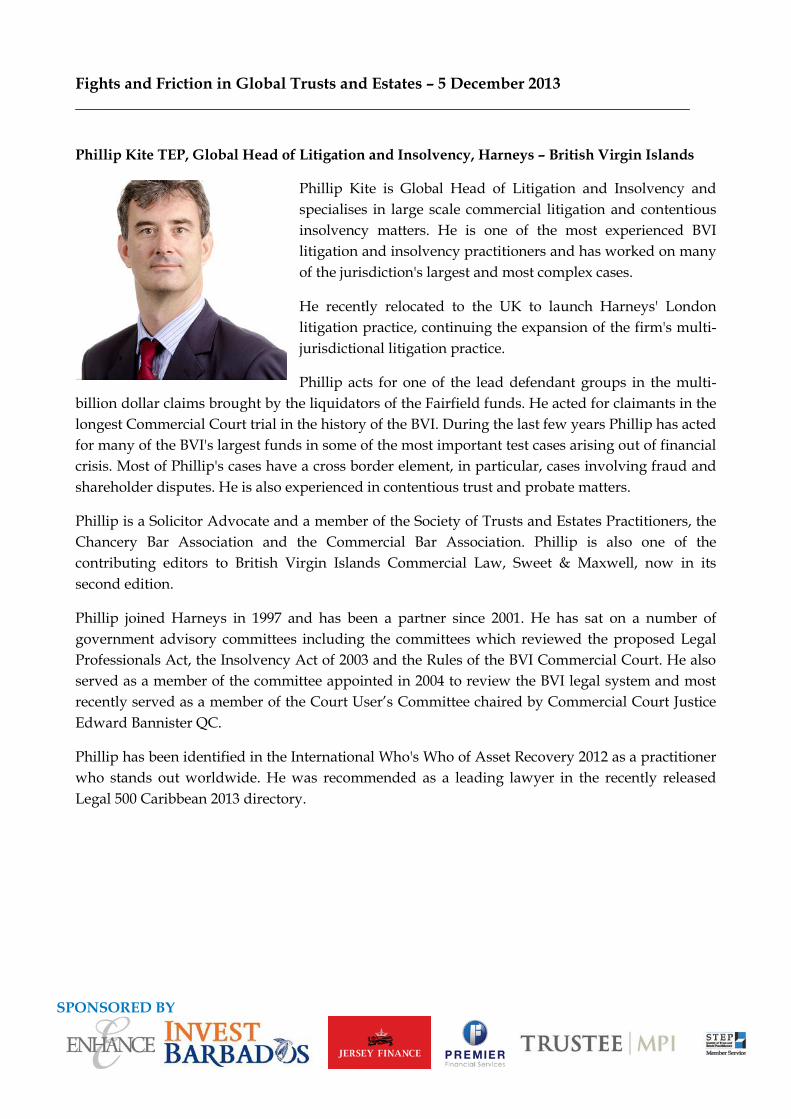

Phillip Kite TEP, Global Head of Litigation and Insolvency, Harneys – British Virgin Islands

Phillip Kite is Global Head of Litigation and Insolvency and specialises in large scale commercial litigation and contentious insolvency matters. He is one of the most experienced BVI litigation and insolvency practitioners and has worked on many of the jurisdiction's largest and most complex cases.

He recently relocated to the UK to launch Harneys' London litigation practice, continuing the expansion of the firm's multi-jurisdictional litigation practice.

Phillip acts for one of the lead defendant groups in the multi-billion dollar claims brought by the liquidators of the Fairfield funds. He acted for claimants in the longest Commercial Court trial in the history of the BVI. During the last few years Phillip has acted for many of the BVI's largest funds in some of the most important test cases arising out of financial crisis. Most of Phillip's cases have a cross border element, in particular, cases involving fraud and shareholder disputes. He is also experienced in contentious trust and probate matters.

Phillip is a Solicitor Advocate and a member of the Society of Trusts and Estates Practitioners, the Chancery Bar Association and the Commercial Bar Association. Phillip is also one of the contributing editors to British Virgin Islands Commercial Law, Sweet & Maxwell, now in its second edition.

Phillip joined Harneys in 1997 and has been a partner since 2001. He has sat on a number of government advisory committees including the committees which reviewed the proposed Legal Professionals Act, the Insolvency Act of 2003 and the Rules of the BVI Commercial Court. He also served as a member of the committee appointed in 2004 to review the BVI legal system and most recently served as a member of the Court User’s Committee chaired by Commercial Court Justice Edward Bannister QC.

Phillip has been identified in the International Who's Who of Asset Recovery 2012 as a practitioner who stands out worldwide. He was recommended as a leading lawyer in the recently released Legal 500 Caribbean 2013 directory.

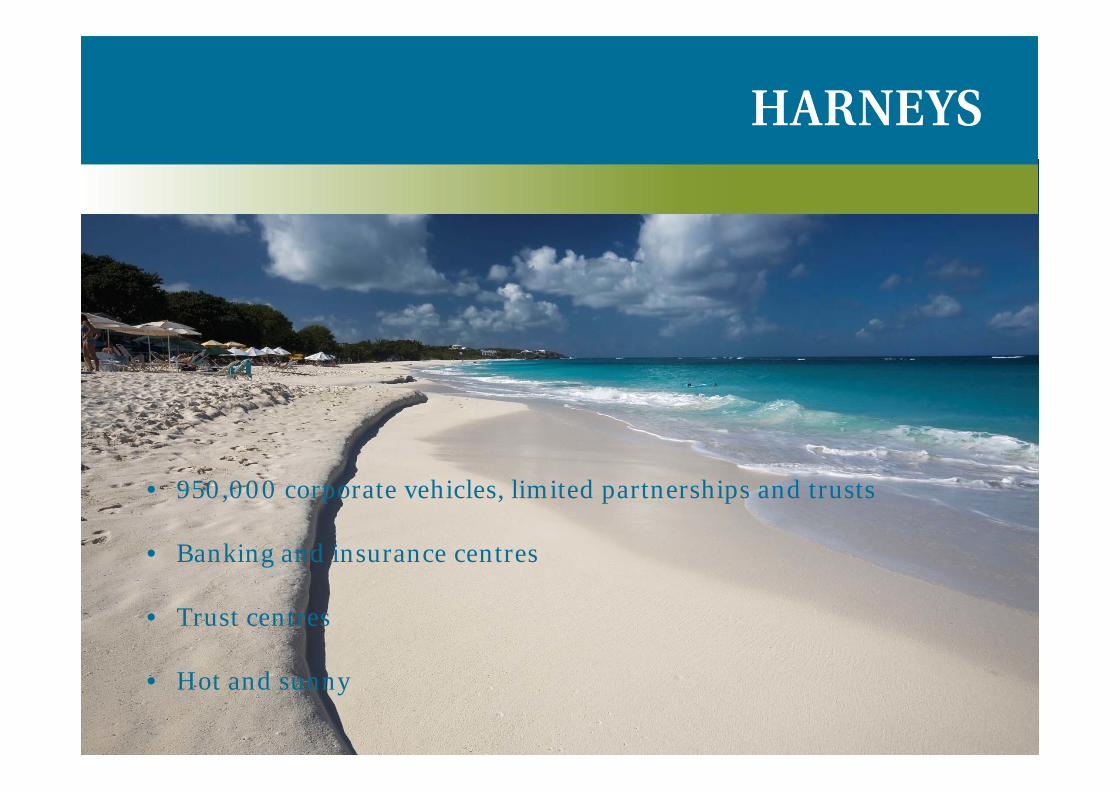

www.harneys.com

• 950,000 corporate vehicles, limited partnerships and trusts

• Banking and insurance centres

• Trust centres

• Hot and sunny

www.harneys.com

• Trustee long term confidant

• Trust assets substantial

• Fall out– loss of trust by beneficiaries– ignored requests for information– drafting of settlement– fees– misleading information

www.harneys.com

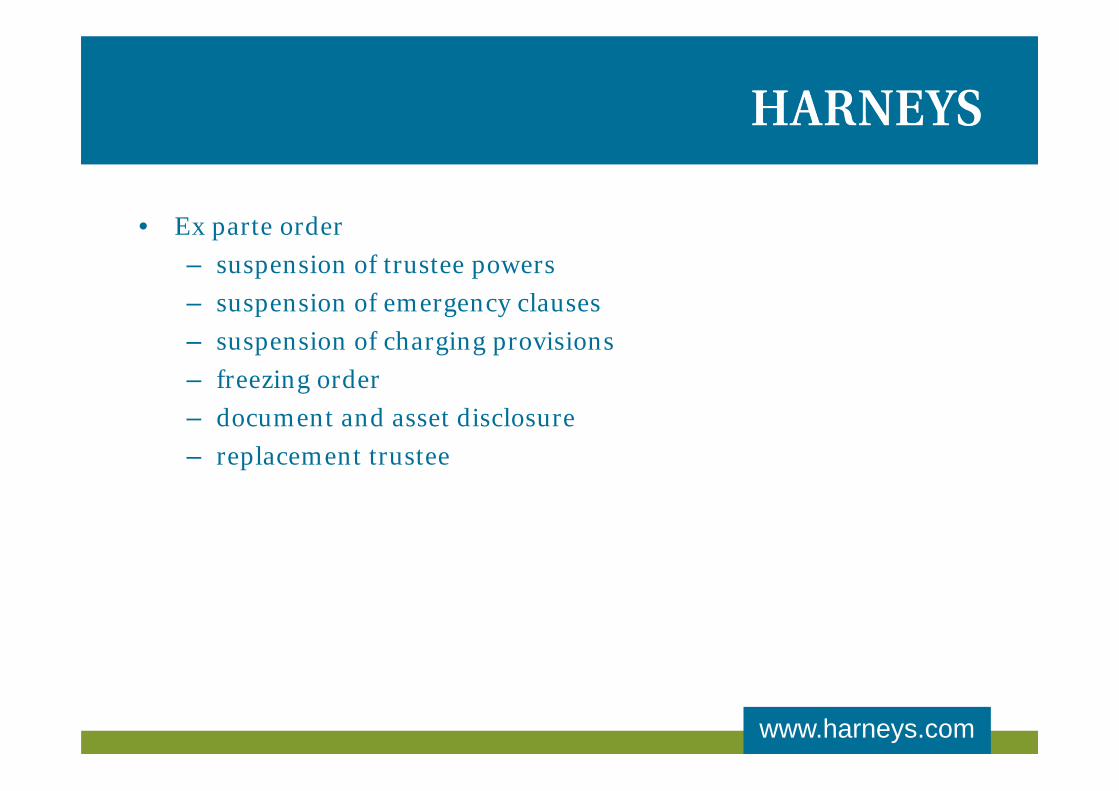

• Ex parte order– suspension of trustee powers– suspension of emergency clauses– suspension of charging provisions– freezing order– document and asset disclosure– replacement trustee

www.harneys.com

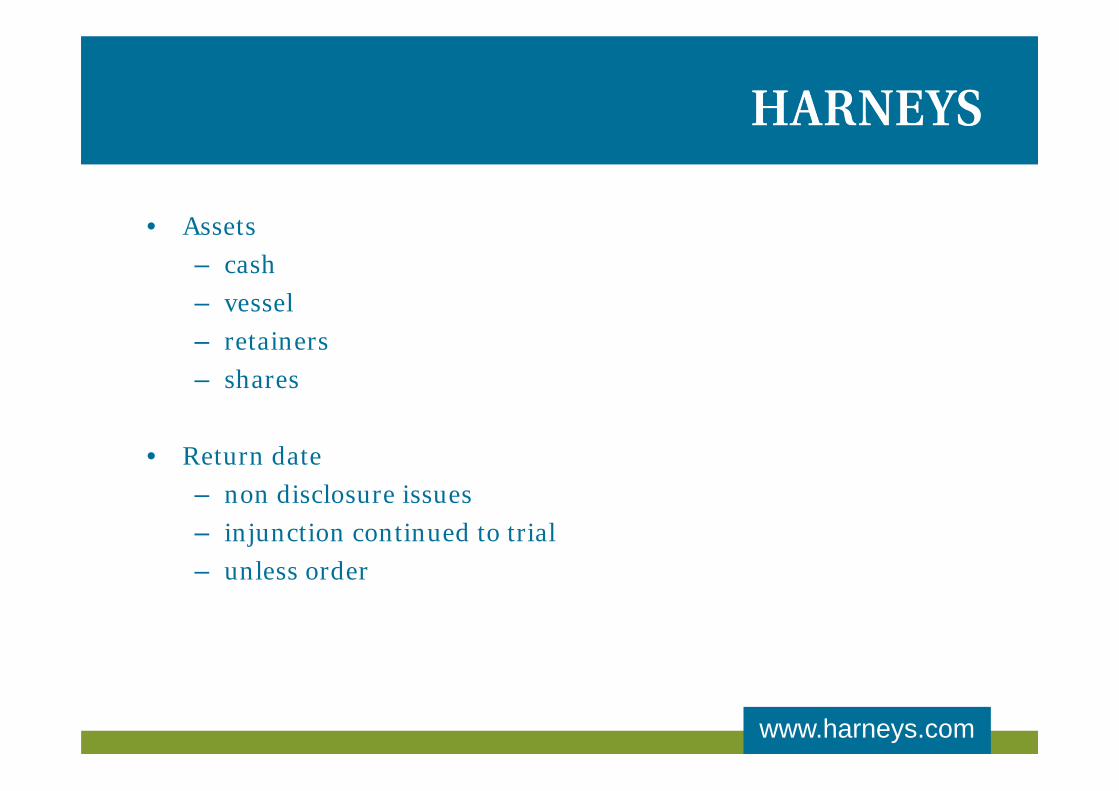

• Assets– cash– vessel– retainers– shares

• Return date– non disclosure issues– injunction continued to trial– unless order

www.harneys.com

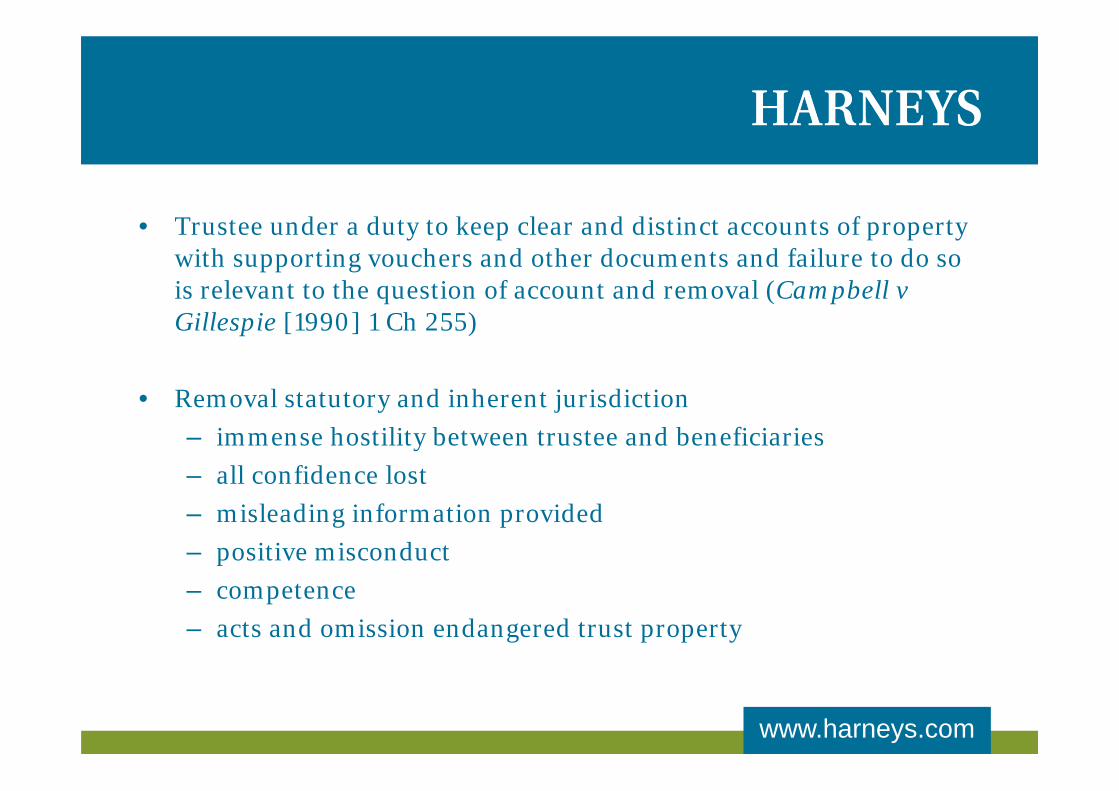

• Trustee under a duty to keep clear and distinct accounts of property with supporting vouchers and other documents and failure to do so is relevant to the question of account and removal (Campbell v Gillespie [1990] 1 Ch 255)

• Removal statutory and inherent jurisdiction– immense hostility between trustee and beneficiaries– all confidence lost– misleading information provided– positive misconduct– competence– acts and omission endangered trust property

SPONSORED BY

Fights and Friction in Global Trusts and Estates – 5 December 2013 _____________________________________________________________________________

David Russell AM QC TEP, Wentworth Chambers – Sydney, Australia

David was admitted as a solicitor in 1974 and called to the Bar in 1977. He is admitted to practise in Australia, England and Wales, the Courts of the Dubai International Financial Centre, New Zealand and Papua New Guinea. He was appointed Queen’s Counsel in 1986, practises in Sydney and is an associate member of chambers in London, New York and Abu Dhabi.

David was President of the Taxation Institute of Australia (1993-5), and the Asia Oceania Tax Consultants’ Association (1996- 2000).

He is Chairman of STEP Australia, a STEP Council member and Committee member of the Contentious Trusts and Estates SIG, a co-chair of the Australian Chapter of the International Section of the New York State Bar Association, an Academician of The International Academy of Estate and Trust Law, the Australian correspondent for Trusts & Trustees, and a Fellow Member of the Chartered Institute of Taxation.

David is listed in the Taxation Category in the Australian Financial Review/Best Lawyers review of the Australian Legal Profession in 2008 and all later years. In 2012, he was made a Member of the Order of Australia for, amongst other things, “service … to taxation law and legal education”.

MANUFACTURING

FRICTION

AS A GROUND OF

TRUSTEE REMOVAL

DAVID RUSSELL QC

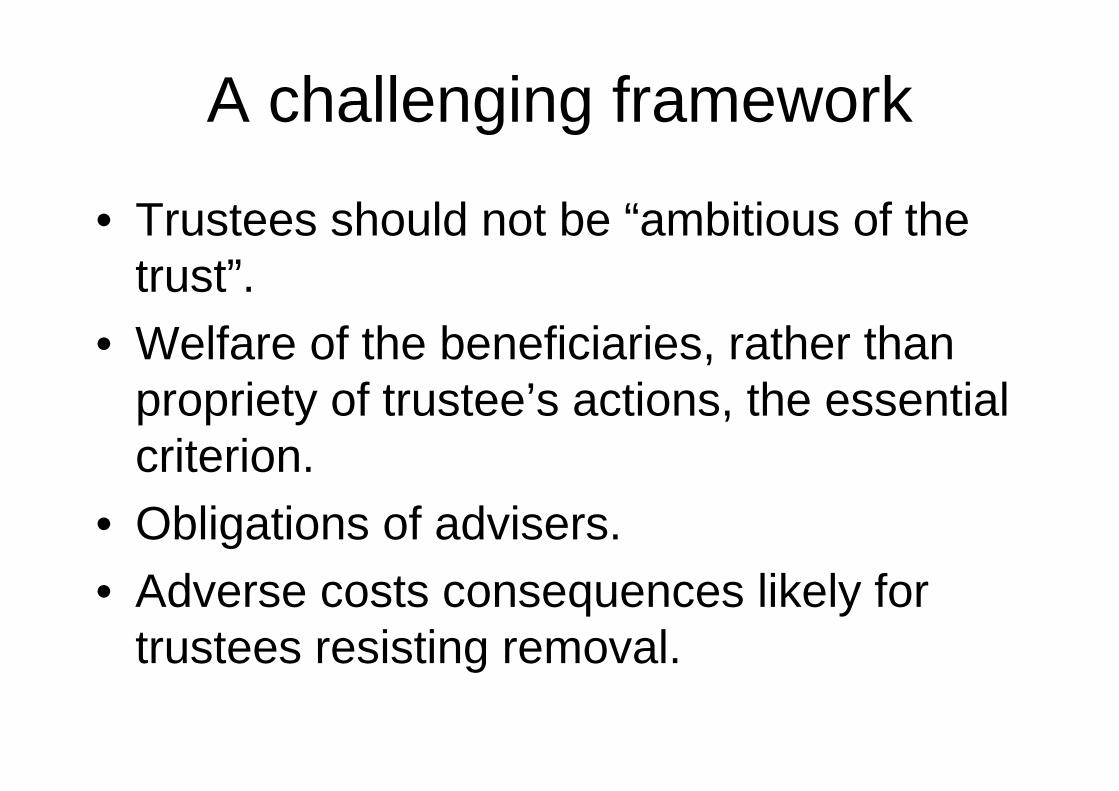

A challenging framework

• Trustees should not be “ambitious of the trust”.

• Welfare of the beneficiaries, rather than propriety of trustee’s actions, the essential criterion.

• Obligations of advisers.• Adverse costs consequences likely for

trustees resisting removal.

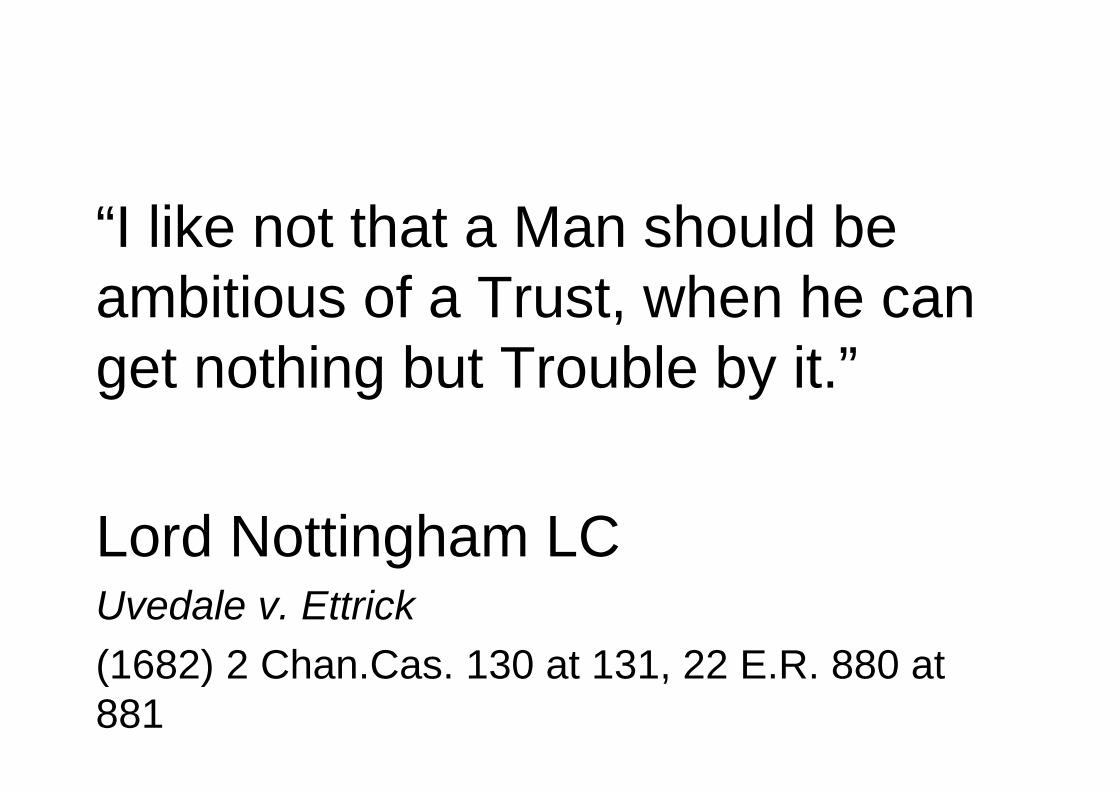

“I like not that a Man should be ambitious of a Trust, when he can get nothing but Trouble by it.”

Lord Nottingham LCUvedale v. Ettrick(1682) 2 Chan.Cas. 130 at 131, 22 E.R. 880 at 881

… without any Reflection on Ettrick, he should meddle no further in the Trust.

Ibid.

“In exercising so delicate a jurisdiction as that of removing trustees, their lordships do not venture to lay down any general rule beyond the very broad principle... that their main guide must be the welfare of the beneficiaries…”

Lord Blackburn, Letterstedt v. Broers (1884) 9 App Cas 371 at 386, 387

… If it appears clear that the continuance of the trustee would be detrimental to the execution of the trusts, even if for no other reason than that of human infirmity would prevent those beneficially interested, or those who act for them, from working in harmony with the trustee, and if there is no reason to the contrary from the intentions of the framer of the trust to give this trustee a benefit or otherwise …Ibid.

”

… the trustee is always advised by his own counsel to resign, and does so. If, without any reasonable ground, he refused to do so, it seems to their lordships that the court might think proper to remove him.Ibid.

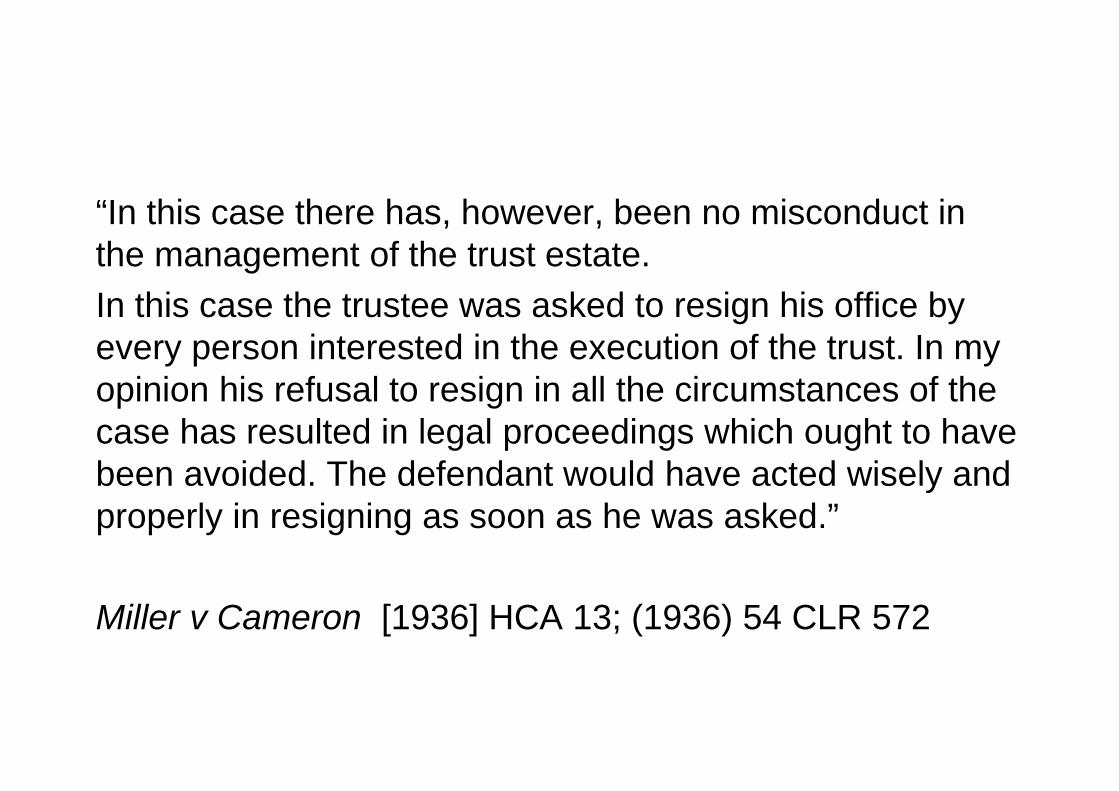

“In this case there has, however, been no misconduct in the management of the trust estate.In this case the trustee was asked to resign his office by every person interested in the execution of the trust. In my opinion his refusal to resign in all the circumstances of the case has resulted in legal proceedings which ought to have been avoided. The defendant would have acted wisely and properly in resigning as soon as he was asked.”

Miller v Cameron [1936] HCA 13; (1936) 54 CLR 572

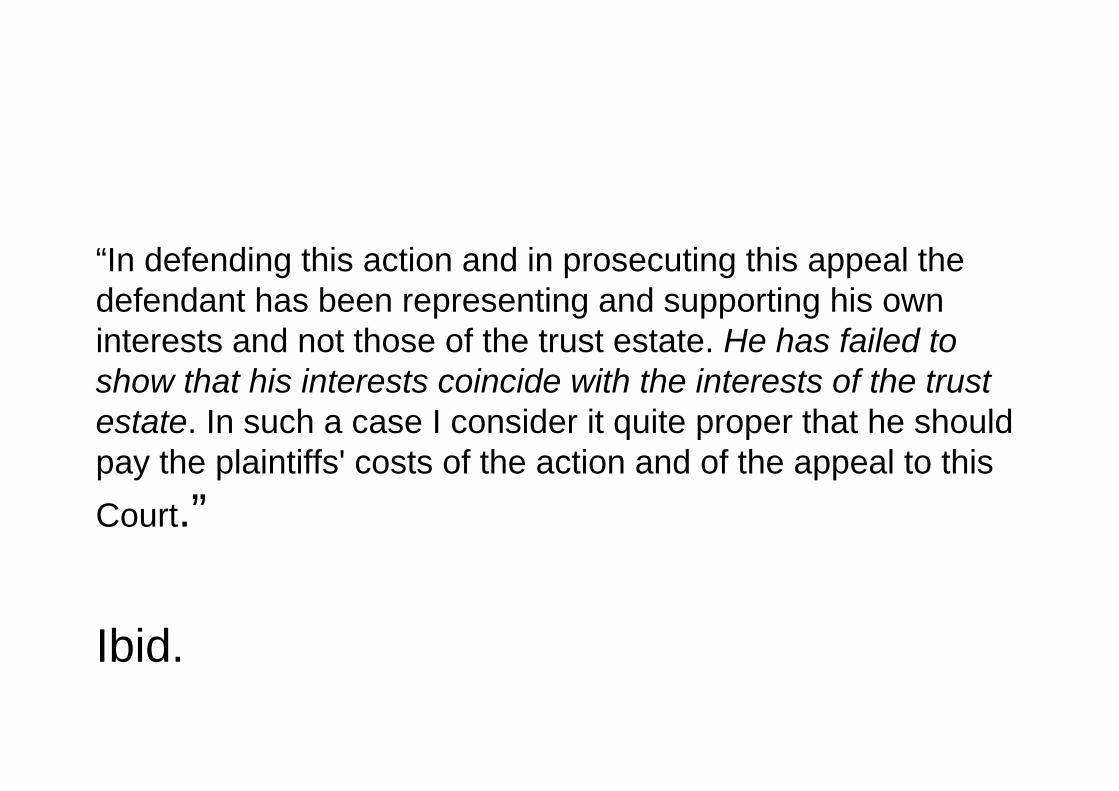

“In defending this action and in prosecuting this appeal the defendant has been representing and supporting his own interests and not those of the trust estate. He has failed to show that his interests coincide with the interests of the trust estate. In such a case I consider it quite proper that he should pay the plaintiffs' costs of the action and of the appeal to this Court.”

Ibid.

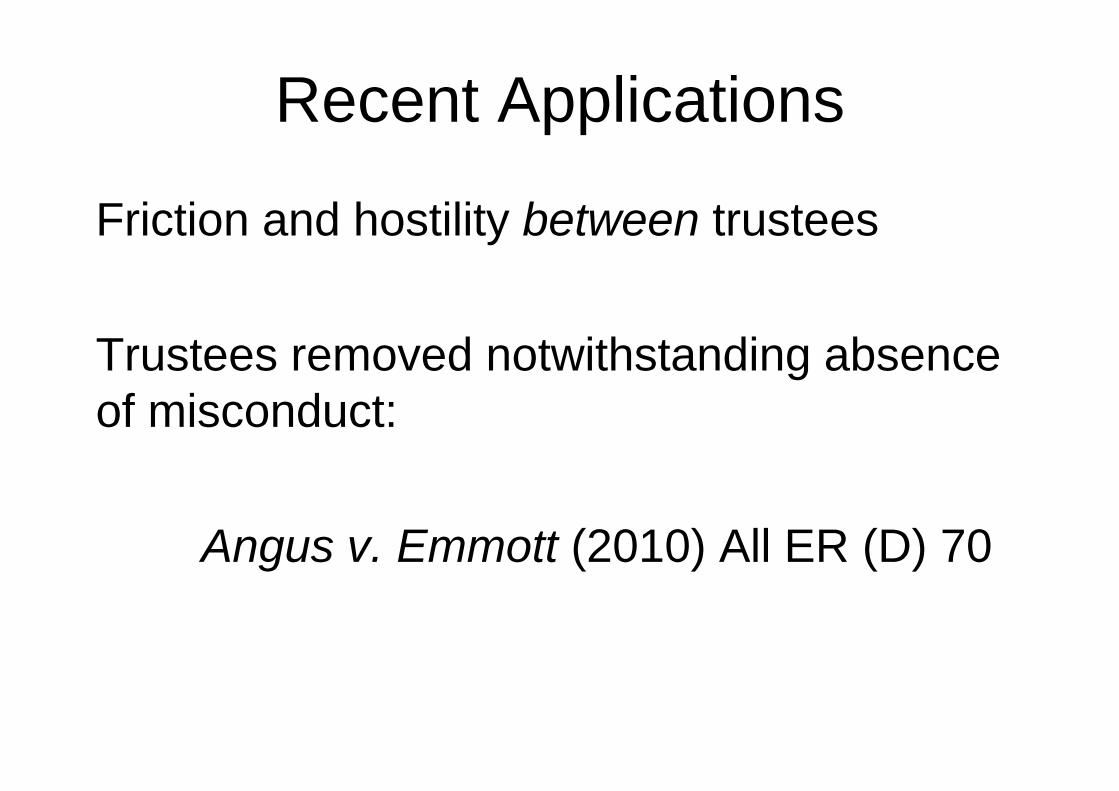

Recent Applications

Friction and hostility between trustees

Trustees removed notwithstanding absence of misconduct:

Angus v. Emmott (2010) All ER (D) 70

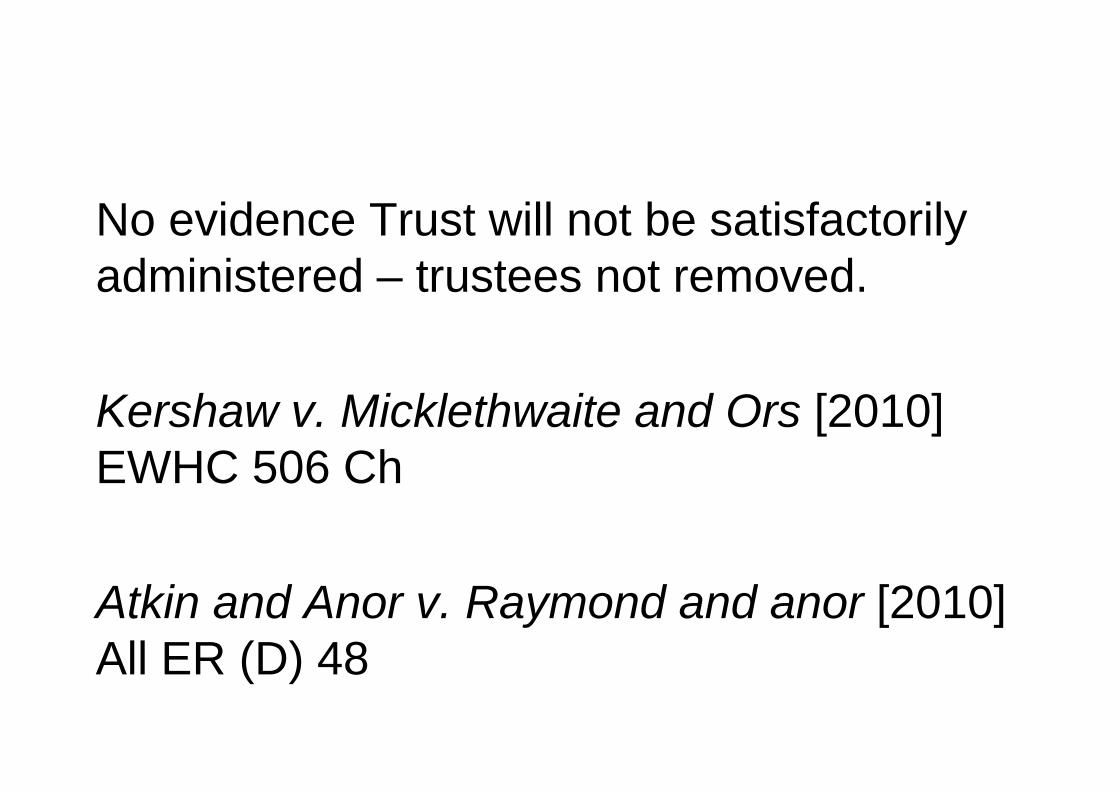

No evidence Trust will not be satisfactorily administered – trustees not removed.

Kershaw v. Micklethwaite and Ors [2010] EWHC 506 Ch

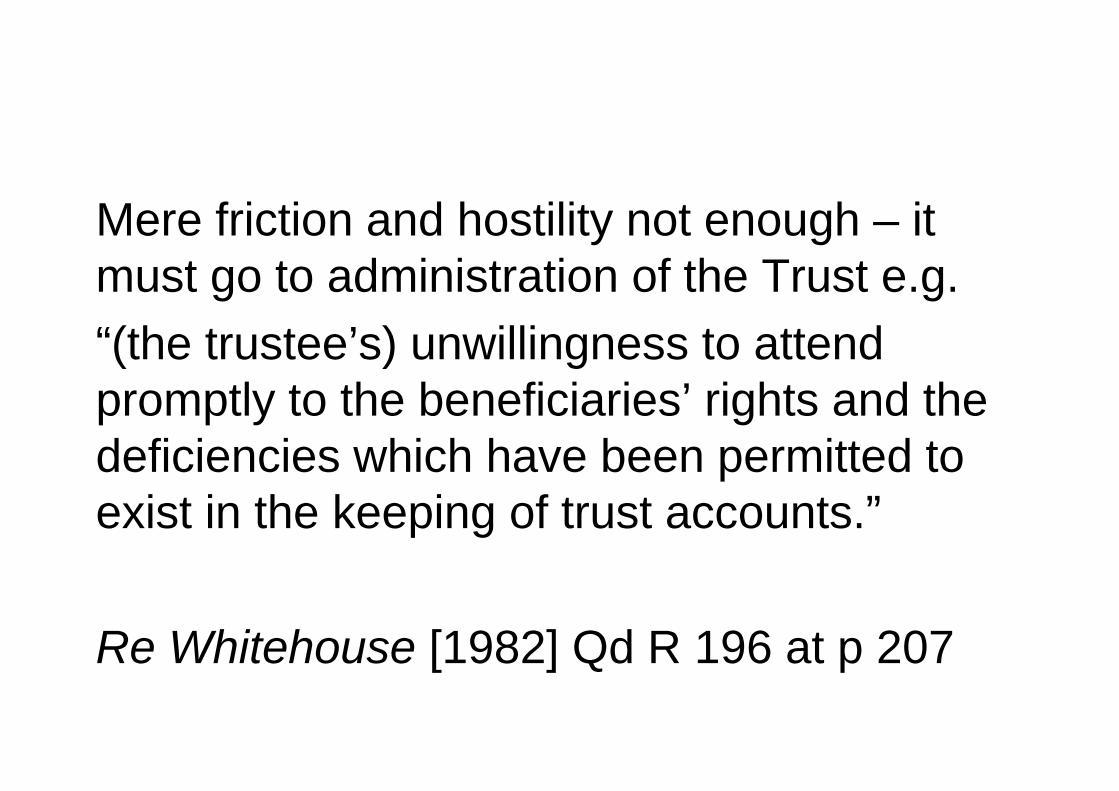

Atkin and Anor v. Raymond and anor [2010] All ER (D) 48

Mere friction and hostility not enough – it must go to administration of the Trust e.g.“(the trustee’s) unwillingness to attend promptly to the beneficiaries’ rights and the deficiencies which have been permitted to exist in the keeping of trust accounts.”

Re Whitehouse [1982] Qd R 196 at p 207

The result in practice

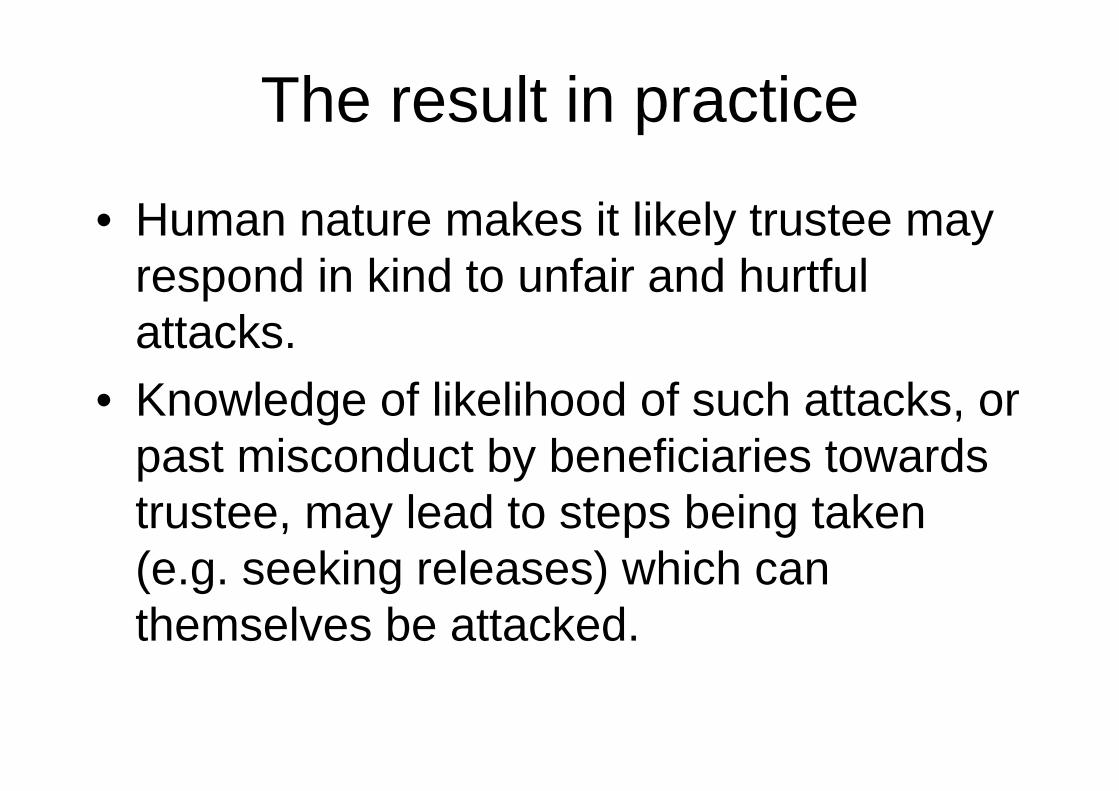

• Human nature makes it likely trustee may respond in kind to unfair and hurtful attacks.

• Knowledge of likelihood of such attacks, or past misconduct by beneficiaries towards trustee, may lead to steps being taken (e.g. seeking releases) which can themselves be attacked.

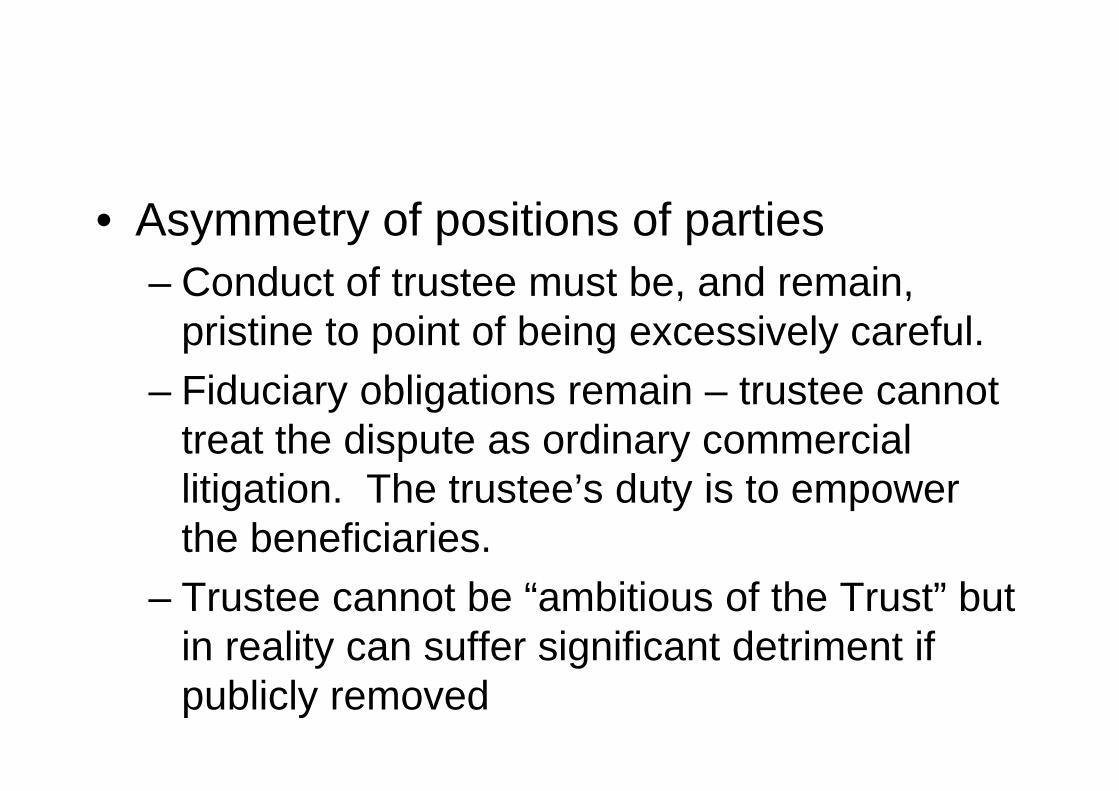

• Asymmetry of positions of parties– Conduct of trustee must be, and remain,

pristine to point of being excessively careful.– Fiduciary obligations remain – trustee cannot

treat the dispute as ordinary commercial litigation. The trustee’s duty is to empower the beneficiaries.

– Trustee cannot be “ambitious of the Trust” but in reality can suffer significant detriment if publicly removed

• Beneficiary is free act as he/she thinks fit, disregarding prior agreements, involving media in a high profile case (unless seeking to be appointed replacement trustee), and pursue wider agendas.

• Discovery obligations one sided – trustee will have to make substantial disclosure in relation to disputed issues, beneficiary very little since the issue always centres on the trustee.

• Costs a real problem – trustee effectively show that he/she has no personal interest in seeking to retain the office, but has interests aligned with those of the Trust (and beneficiary who is attacking the Trustee)

• But open to attack for abandoning office if that is not the right thing to do

A proactive strategy?

• Settlors to consider possible future conflicts and record intentions in Trust instrument

• Appointment of independent advisory trustee or co-trustee

• Appointment of replacement trustee• Application for judicial advice

THE END

Unfortunately, the risk of trustees becoming involved in court proceedings appears to be on the increase. The STEP Contentious Trusts and Estates Special Interest Group has been set up with the following aims:

• To provide a forum for sharing international trust and estate jurisprudence. • To facilitate networking and communication amongst individuals with an

interest in contentious trust and estate matters. • To provide a forum for training and education. • To marshal expertise and promote best practices (including the use of

Alternative Dispute Resolution) in dealing with contentious trust and estate disputes.

• To help non-contentious practitioners avoid pitfalls encountered in trust and estate litigation.

Visit the Contentious Trusts and Estates Special Interest Group web-pages: www.step.org/contentious-trusts-and-estates www.step.org/SIGs Forum: www.step.org/forums/contentious-trusts-and-estates Join the LinkedIn group: Contentious Trusts and Estates Special Interest Group www.linkedin.com/groups/Contentious-Trusts-Estates-Special-Interest-4861427 Become a Member: Membership of STEP’s Special Interest Groups is open to STEP members and non-members alike and there is currently no fee to join. If you wish to become a member of the Contentious Trusts and Estates group and receive updates about their news, events and activities, please visit www.step.org/SIGs. Alternatively you can complete a joining form at today’s registration desk.

Contentious Trusts and Estates Special Interest Group Society of Trust and Estate Practitioners (STEP)

Artillery House (South) 11-19 Artillery Row London SW1P 1RT United Kingdom

Tel: +44 (0)20 7340 0537 Fax: +44 (0)20 7340 0501

Email: [email protected]

Course provider

Add value to your business with this professional qualification

A practical course which aims to give you an understanding of how to anticipate, and therefore avoid, the common pitfalls which can lead to trust litigation and arm you with litigation nous.

Top 4 reasons to study for this Certificate:1. Provide an A to Z coverage of trust disputes.2. Help you to ‘future-proof’ trusts against litigation.3. Provide you with a practical overview of the themes

commonly encountered in trust disputes and an understanding of the overarching principles.

4. Help you to identify the potential risks involved in the creation and administration of trusts and how to manage those risks.

Completion of the Certificate enables you to meet your full annual STEP and SRA CPD requirement.Course content written by Toby Graham TEP.

STEP Advanced Certificate in Trust DisputesTrust disputes – anticipating and avoiding the pitfalls

View the syllabus at www.step.org/pd or www.cltint.com/stepcerttrustdisputes

A qualification for practitioners worldwide

WITH THANKS TO OUR SPONSORS

Enhance is an independent investment consultancy business. The services provided through the Enhance group of companies are portfolio monitoring, investment manager selection services, and investment consultancy as well as treasury and cash management solutions. Enhance also operate a Member Service for STEP, the Trustee Managed Portfolio Indices. Enhance Group services are typically provided to fiduciary structures, high net worth individuals and charities. Enhance endeavour to ensure clients of the group experience integrity and professionalism across all business lines and in engaging with their chosen investment providers, experience positive, effective investment solutions. The Group’s status as an independent company ensures a genuinely impartial approach in all aspects of client work.

For more information on:

Please contact:

James Painter

Managing Director

Tel: +44 1534 761510

Email: [email protected]

This document is for information purposes only and is not to be construed as a solicitation or an offer for financial services.

The information contained herein is based on materials and sources that we believe to be reliable, however, EGL make no representation or warranty, either express or implied, in relation to the accuracy, completeness or reliability of the information contained herein. All opinions and estimates included in this document are subject

to change without notice and EGL are under no obligation to update the information contained herein.

None of EGL employees shall have any liability whatsoever for any indirect or consequential loss or damage arising from any use of this document.

This document is issued by Enhance Group Limited (EGL) Registered Office: 1st Floor, Charles Bisson House, 30-32 New Street, St Helier, Jersey JE2 3TE

www.investbarbados.org

THE BARBADOS DOMICILE

Barbados’ international business and financial centre is unique, offering investors the combination of a secure and reputable jurisdiction, cost effective treaty-based tax planning opportunities and a high quality of life. Located in a similar time zone to the eastern US, it provides a secure environment for international business companies, banking, insurance, trust and wealth management. Multi-nationals with significant business interest in the Caribbean and Latin America find Barbados attractive for establishment of their regional headquarters.

A low tax jurisdiction, the Barbados business environment and regulatory infrastructure attracts businesses of substance. It adheres to standards of transparency, disclosure and procedures for tax information exchange and has been credited by the OECD Global Forum as having substantially implemented the current internationally agreed tax standard.

What distinguishes Barbados is its expanding network of double taxation treaties with emerging economies in the Americas, Europe, Asia and Africa. This treaty advantage makes Barbados an attractive base from which to launch an international venture or provide cross-border services to key emerging markets.

Recent legislative amendments also strategically position Barbados as a preferred choice for wealth management solutions, particularly for high net worth individuals and entrepreneurs. In fact, Barbados aims to become a global entrepreneurial hub by 2020.

Combined with the above advantages, the country’s good health care, educational services, sports facilities, excellent restaurants, private accommodation, exciting night life, appealing year-round climate and ease of access from international gateways make Barbados the ideal place for investors to live and work.

Invest Barbados is Government’s investment promotional agency with offices in the following locations:

BARBADOS Trident Insurance Financial Centre Hastings, Christ Church BB15156, Barbados Tel: (246) 626 2000 [email protected]

NEW YORK 820 Second Avenue, 5th Avenue New York, NY 10017, USA Tel: (212) 551 4395 [email protected]

LONDON

1 Great Russell Street London WC1B 3ND Tel: 020 7299 7196 [email protected]

TORONTO 105 Adelaide Street West Suite 1010 Toronto, ON M5H 1P9 Canada Tel: (416) 216 5414 [email protected]

Jersey for Private WealthJersey is a prominent player in delivering private client services, with the emphasis today shifting away from the simple

trust and underlying company structures, to high value and more complex structures involving trusts, companies, limited partnerships and now foundations for international families.

As the number one jurisdiction globally for trusts, the Trusts (Jersey) Law 1984 was used as the basis for the Hague Convention on trusts and is still used as a ‘blueprint’ by other jurisdictions. With an international client base, clients

and trustees have access to a variety of service providers from large banks and independently-owned trust companies to smaller, niche providers, as well as legal support from experienced law firms. Jersey’s highly-skilled service providers

work closely with counterparts in all of the world’s major centres to deliver structures and solutions that meet a wide range of sophisticated financial and investment objectives.

Rated the world’s leading offshore centre - Global Financial Centres Index, September 2013 – Jersey remains the jurisdiction of choice for corporate and private clients alike.

For further information, please visit www.jerseyfinance.je

www.linkedin.com/company/jersey-finance @jerseyfinance www.youtube.com/jerseyfinance

Vimal Damry TEPManaging [email protected]+230 245 6703

Sanjeev Lutchumun [email protected]+230 245 6703

To find out how we can help you, please do contact:

• Foundation Services • Trusts including:

» Discretionary Trusts » Employee Benefit Trusts / Pension Schemes » Charitable / Purpose Trusts

• Tax planning and Double Taxation Treaty Advice

• Wealth Management and Asset Protection

• Cross border Investment Holding and Financing Solutions

• International Trade Structures and Services • Residence Permit Applications • Investment Funds Administration, NAV

Calculations, Compliance and Accounting • Limited Partnership (LP) Structuring • Limited Liability Partnerships (LLP)Structuring

www.premier.mu Mauritius|London|Singapore|Hong Kong|Seychelles

With Premier, no need for you to ask for it, clients get the best services!

LeadingCorporate and Trust Services Provider

Providing Mauritius companies, Trusts, Foundations and Fund administration

Powered by a team of enthusiastic and dynamic service-oriented specialist with excellent credentials in legal, financial and accounting.

Backed with our experience, our deep network and our membership of INAA Group.

We are committed to provide effective tailor-made solutions for all business needs or challenges.

Licensed by the Financial Services Commission of Mauritius, Premier has the necessary experience and expertise in providing customized and cost effective solutions to clients with varying profiles to meet wide range of objectives.

We do :

Company Formation, Advisory Firm of the Year in Mauritius

Company Formations Accountancy Firm of the Year in Mauritius for 2013

GL

OBAL LAW EXPER

TS

PRACTICE AWARDS