Embed Size (px)

Citation preview

8

8

High Speed Rail Phase 2 / 357

Economic appraisal of the preferred HSR system

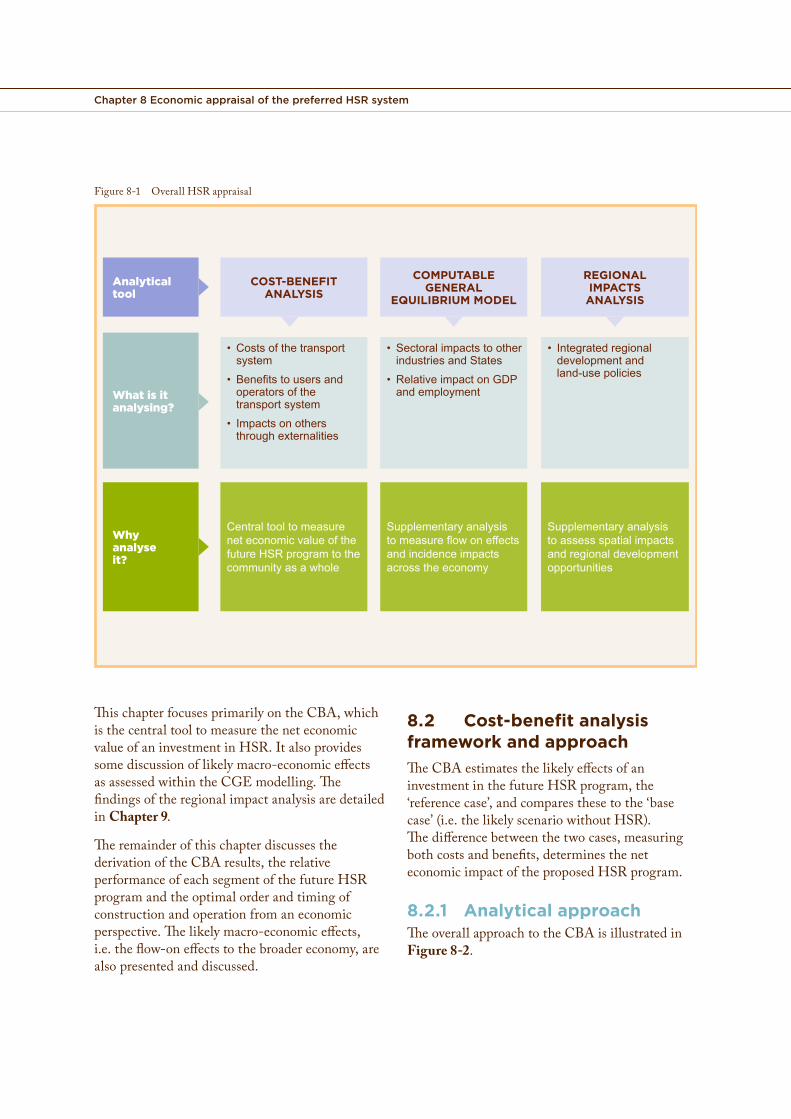

8.1 IntroductionTheeconomicappraisalbringstogetherdemandanduserbenefits,revenueandcostsdescribedinChapters 2and7toprovideanoverallappraisaloftheeconomicvalueofthefutureHSRprogram.TheoverallHSReconomicappraisalconsistsofthreecomponents,asoutlinedinFigure 8-1.

Insummary:• Thecost-benefit analysis (CBA)seeksto

provideacomprehensiveassessmentofthecostsandbenefitstousersandoperatorsofHSRthatcanbevaluedinmonetaryterms.Italsoincludesanassessmentofexternalities,suchasenvironmentalimpacts,accidentcostsavingsanddecongestionbenefits.TheCBAhelpsestablishtheoveralleconomicmeritofafutureHSRprogramand,asoutlinedinChapter 6,guidesdecisionsontheoptimalstagingoftheHSRprogram.

• Thecomputable general equilibrium(CGE)analysisexplorestheflow-oneffectstothebroaderAustralianeconomyofaninvestmentinHSR.Itidentifiesthetotal(directandindirect)economicimpactsoftheconstructionandoperationoftheHSRnetworkonnationalandregionalGrossDomesticProduct(GDP)andemployment.

• Theregional impacts analysisexplorestheimpactofHSRonregionsandregionaltownsandcitiesalongthepreferredcorridor,duetoimprovedaccessibilityandassesseswhetherfurtherbenefitscouldbeachievedthroughcomplementaryregionaldevelopmentpoliciesintegratedwiththeimplementationofHSR.

8.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-1 Overall HSR appraisal

• Costsofthetransportsystem

• Benefitstousersandoperatorsofthetransportsystem

• Impactsonothersthroughexternalities

COST-BENEFITANALYSIS

CentraltooltomeasureneteconomicvalueofthefutureHSRprogramtothecommunityasawhole

• SectoralimpactstootherindustriesandStates

• RelativeimpactonGDPandemployment

COMPUTABLE GENERAL

EQUILIBRIUM MODEL

Supplementaryanalysistomeasureflowoneffectsandincidenceimpactsacrosstheeconomy

• Integratedregionaldevelopmentandland-usepolicies

REGIONALIMPACTSANALYSIS

Supplementaryanalysistoassessspatialimpactsandregionaldevelopmentopportunities

Analyticaltool

What is itanalysing?

Why analyseit?

This chapter focuses primarily on the CBA, which is the central tool to measure the net economic value of an investment in HSR. It also provides some discussion of likely macro-economic effects as assessed within the CGE modelling. The findings of the regional impact analysis are detailed in Chapter 9.

The remainder of this chapter discusses the derivation of the CBA results, the relative performance of each segment of the future HSR program and the optimal order and timing of construction and operation from an economic perspective. The likely macro-economic effects, i.e. the flow-on effects to the broader economy, are also presented and discussed.

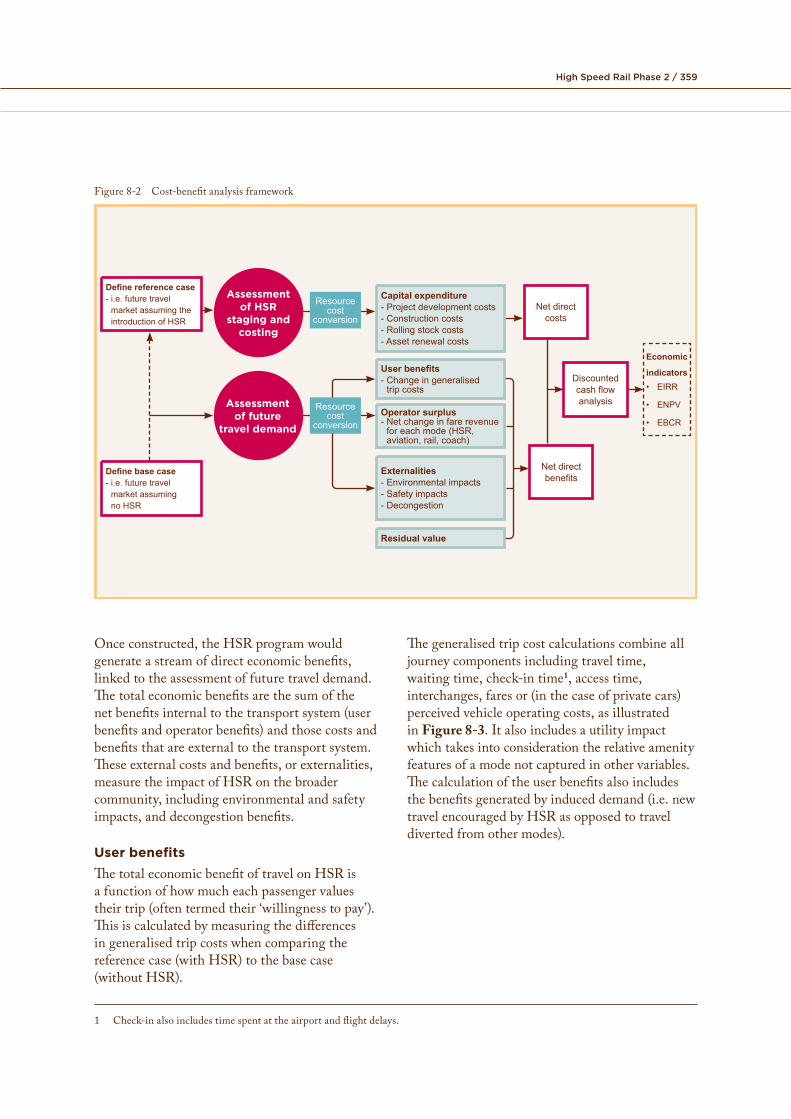

8.2 Cost-benefit analysis framework and approachThe CBA estimates the likely effects of an investment in the future HSR program, the ‘reference case’, and compares these to the ‘base case’ (i.e. the likely scenario without HSR). The difference between the two cases, measuring both costs and benefits, determines the net economic impact of the proposed HSR program.

8.2.1 Analytical approach The overall approach to the CBA is illustrated in Figure 8-2.

High Speed Rail Phase 2 / 359

Figure 8-2 Cost-benefit analysis framework

Discounted cash flow analysis

Economic

indicators• EIRR

• ENPV

• EBCR

Net direct benefits

Net direct costs

User benefits- Change in generalised

trip costs

Operator surplus- Net change in fare revenue

for each mode (HSR, aviation, rail, coach)

Externalities- Environmental impacts- Safety impacts- Decongestion

Residual value

Assessment of HSR

staging and costing

Capital expenditure- Project development costs- Construction costs- Rolling stock costs- Asset renewal costs

Define reference case- i.e. future travel

market assuming the introduction of HSR

Define base case- i.e. future travel

market assuming no HSR

Assessment of future

travel demand

Resource cost

conversion

Resource cost

conversion

Once constructed, the HSR program would generate a stream of direct economic benefits, linked to the assessment of future travel demand. The total economic benefits are the sum of the net benefits internal to the transport system (user benefits and operator benefits) and those costs and benefits that are external to the transport system. These external costs and benefits, or externalities, measure the impact of HSR on the broader community, including environmental and safety impacts, and decongestion benefits.

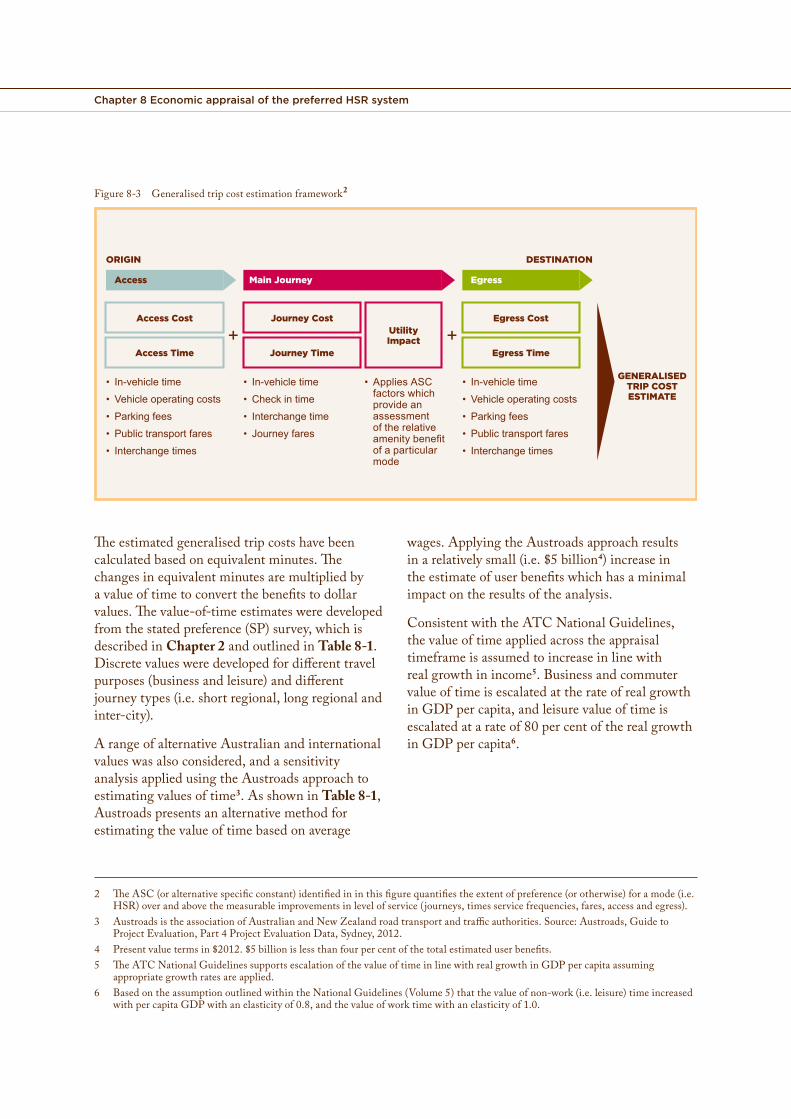

User benefitsThe total economic benefit of travel on HSR is a function of how much each passenger values their trip (often termed their ‘willingness to pay’). This is calculated by measuring the differences in generalised trip costs when comparing the reference case (with HSR) to the base case (without HSR).

The generalised trip cost calculations combine all journey components including travel time, waiting time, check-in time1, access time, interchanges, fares or (in the case of private cars) perceived vehicle operating costs, as illustrated in Figure 8-3. It also includes a utility impact which takes into consideration the relative amenity features of a mode not captured in other variables. The calculation of the user benefits also includes the benefits generated by induced demand (i.e. new travel encouraged by HSR as opposed to travel diverted from other modes).

1 Check-in also includes time spent at the airport and flight delays.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-3 Generalised trip cost estimation framework2

Access Cost Journey Cost Egress CostUtility Impact

Access Time Journey Time Egress Time

Access Main Journey Egress

+ +

• In-vehicletime

• Vehicleoperatingcosts

• Parkingfees

• Publictransportfares

• Interchangetimes

• In-vehicletime

• Checkintime

• Interchangetime

• Journeyfares

• AppliesASCfactorswhichprovideanassessmentoftherelativeamenitybenefitofaparticularmode

• In-vehicletime

• Vehicleoperatingcosts

• Parkingfees

• Publictransportfares

• Interchangetimes

ORIGIN DESTINATION

GENERALISED TRIP COST ESTIMATE

The estimated generalised trip costs have been wages. Applying the Austroads approach results calculated based on equivalent minutes. The in a relatively small (i.e. $5 billion4) increase in changes in equivalent minutes are multiplied by the estimate of user benefits which has a minimal a value of time to convert the benefits to dollar impact on the results of the analysis.values. The value-of-time estimates were developed

Consistent with the ATC National Guidelines, from the stated preference (SP) survey, which is the value of time applied across the appraisal described in Chapter 2 and outlined in Table 8-1. timeframe is assumed to increase in line with Discrete values were developed for different travel real growth in income5. Business and commuter purposes (business and leisure) and different value of time is escalated at the rate of real growth journey types (i.e. short regional, long regional and in GDP per capita, and leisure value of time is inter-city). escalated at a rate of 80 per cent of the real growth

A range of alternative Australian and international in GDP per capita6.values was also considered, and a sensitivity analysis applied using the Austroads approach to estimating values of time3. As shown in Table 8-1, Austroads presents an alternative method for estimating the value of time based on average

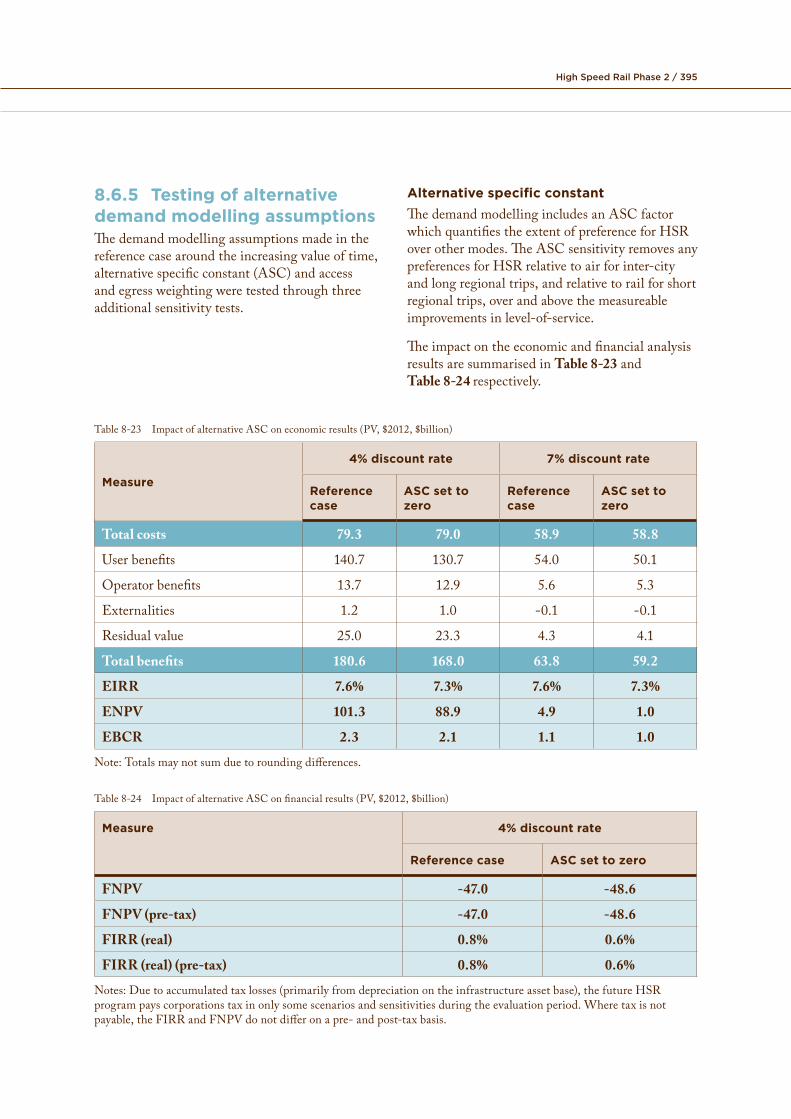

2 The ASC (or alternative specific constant) identified in in this figure quantifies the extent of preference (or otherwise) for a mode (i.e. HSR) over and above the measurable improvements in level of service (journeys, times service frequencies, fares, access and egress).

3 Austroads is the association of Australian and New Zealand road transport and traffic authorities. Source: Austroads, Guide to Project Evaluation, Part 4 Project Evaluation Data, Sydney, 2012.

4 Present value terms in $2012. $5 billion is less than four per cent of the total estimated user benefits.5 The ATC National Guidelines supports escalation of the value of time in line with real growth in GDP per capita assuming

appropriate growth rates are applied. 6 Based on the assumption outlined within the National Guidelines (Volume 5) that the value of non-work (i.e. leisure) time increased

with per capita GDP with an elasticity of 0.8, and the value of work time with an elasticity of 1.0.

High Speed Rail Phase 2 / 361

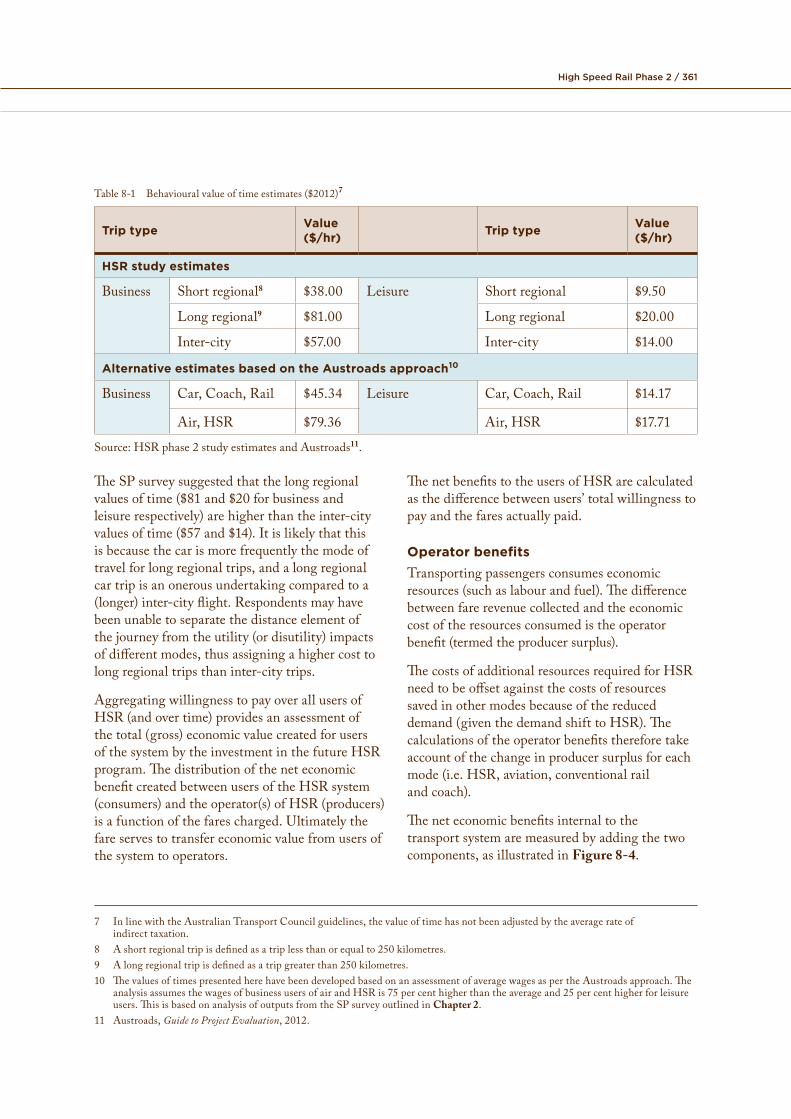

Table8-1 Behaviouralvalueoftimeestimates($2012)7

Trip type Value ($/hr) Trip type Value

($/hr)

HSR study estimates

Business Shortregional8 $38.00 Leisure Shortregional $9.50

Longregional9 $81.00 Longregional $20.00

Inter-city $57.00 Inter-city $14.00

Alternative estimates based on the Austroads approach10

Business Car,Coach,Rail $45.34 Leisure Car,Coach,Rail $14.17

Air,HSR $79.36 Air,HSR $17.71

Source:HSRphase2studyestimatesandAustroads11.

TheSPsurveysuggestedthatthelongregionalvaluesoftime($81and$20forbusinessandleisurerespectively)arehigherthantheinter-cityvaluesoftime($57and$14).Itislikelythatthisisbecausethecarismorefrequentlythemodeoftravelforlongregionaltrips,andalongregionalcartripisanonerousundertakingcomparedtoa(longer)inter-cityflight.Respondentsmayhavebeenunabletoseparatethedistanceelementofthejourneyfromtheutility(ordisutility)impactsofdifferentmodes,thusassigningahighercosttolongregionaltripsthaninter-citytrips.

AggregatingwillingnesstopayoverallusersofHSR(andovertime)providesanassessmentofthetotal(gross)economicvaluecreatedforusersofthesystembytheinvestmentinthefutureHSRprogram.ThedistributionoftheneteconomicbenefitcreatedbetweenusersoftheHSRsystem(consumers)andtheoperator(s)ofHSR(producers)isafunctionofthefarescharged.Ultimatelythefareservestotransfereconomicvaluefromusersofthesystemtooperators.

ThenetbenefitstotheusersofHSRarecalculatedasthedifferencebetweenusers’totalwillingnesstopayandthefaresactuallypaid.

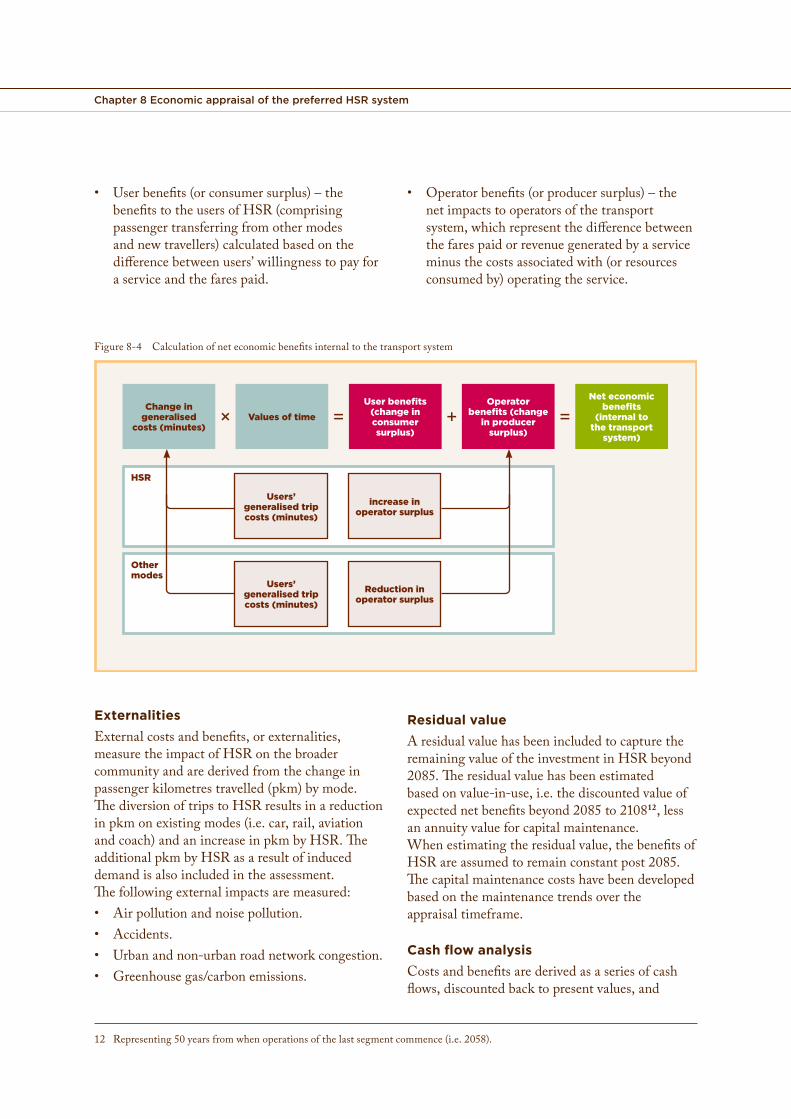

Operator benefitsTransportingpassengersconsumeseconomicresources(suchaslabourandfuel).Thedifferencebetweenfarerevenuecollectedandtheeconomiccostoftheresourcesconsumedistheoperatorbenefit(termedtheproducersurplus).

ThecostsofadditionalresourcesrequiredforHSRneedtobeoffsetagainstthecostsofresourcessavedinothermodesbecauseofthereduceddemand(giventhedemandshifttoHSR).Thecalculationsoftheoperatorbenefitsthereforetakeaccountofthechangeinproducersurplusforeachmode(i.e.HSR,aviation,conventionalrailandcoach).

Theneteconomicbenefitsinternaltothetransportsystemaremeasuredbyaddingthetwocomponents,asillustratedinFigure 8-4.

7 InlinewiththeAustralianTransportCouncilguidelines,thevalueoftimehasnotbeenadjustedbytheaveragerateofindirecttaxation.

8 Ashortregionaltripisdefinedasatriplessthanorequalto250kilometres.9 Alongregionaltripisdefinedasatripgreaterthan250kilometres.10 ThevaluesoftimespresentedherehavebeendevelopedbasedonanassessmentofaveragewagesaspertheAustroadsapproach.The

analysisassumesthewagesofbusinessusersofairandHSRis75percenthigherthantheaverageand25percenthigherforleisureusers.ThisisbasedonanalysisofoutputsfromtheSPsurveyoutlinedinChapter 2.

11 Austroads,Guide to Project Evaluation,2012.

Chapter 8 Economic appraisal of the preferred HSR system

• User benefits (or consumer surplus) – the • Operator benefits (or producer surplus) – the benefits to the users of HSR (comprising net impacts to operators of the transport passenger transferring from other modes system, which represent the difference between and new travellers) calculated based on the the fares paid or revenue generated by a service difference between users’ willingness to pay for minus the costs associated with (or resources a service and the fares paid. consumed by) operating the service.

Figure 8-4 Calculation of net economic benefits internal to the transport system

HSR

Other modes

Change in generalised

costs (minutes)Values of time

Users’ generalised trip costs (minutes)

increase in operator surplus

Users’ generalised trip costs (minutes)

Reduction in operator surplus

User benefits (change in consumer surplus)

Net economic benefits

(internal to the transport

system)

Operator benefits (change

in producer surplus)

+× = =

ExternalitiesExternal costs and benefits, or externalities, measure the impact of HSR on the broader community and are derived from the change in passenger kilometres travelled (pkm) by mode. The diversion of trips to HSR results in a reduction in pkm on existing modes (i.e. car, rail, aviation and coach) and an increase in pkm by HSR. The additional pkm by HSR as a result of induced demand is also included in the assessment. The following external impacts are measured:• Air pollution and noise pollution.• Accidents.• Urban and non-urban road network congestion.• Greenhouse gas/carbon emissions.

Residual valueA residual value has been included to capture the remaining value of the investment in HSR beyond 2085. The residual value has been estimated based on value-in-use, i.e. the discounted value of expected net benefits beyond 2085 to 210812, less an annuity value for capital maintenance. When estimating the residual value, the benefits of HSR are assumed to remain constant post 2085. The capital maintenance costs have been developed based on the maintenance trends over the appraisal timeframe.

Cash flow analysisCosts and benefits are derived as a series of cash flows, discounted back to present values, and

12 Representing 50 years from when operations of the last segment commence (i.e. 2058).

High Speed Rail Phase 2 / 363

alignedtotheproposedstagingoftheHSRprogramassetoutinChapter 6,withoperationscommencingin2035andnetbenefitsprojectedforwardover50yearsto2085.Additionalcapitalexpenditurerequiredtorenewassetsthatwearoutoverthatperiod,suchasrollingstockwhichhasaneconomiclifeof30years,isincludedinthecashflows.TheCBAhasbeenundertakenonaresourcecostbasiswhichmeansthattaxes,suchasGST,fuelexciseandthecarbontaxwereremoved.

Thecashflowsfromthecost-benefitanalysisproducethreekeyeconomicindicators:

• Theeconomicinternalrateofreturn(EIRR)whichrepresentsthediscountratethatmakesthenetpresentvalueofalleconomiccashflowsequaltozero.ThehighertheEIRR,thegreatertheneteconomicreturnsachievedbyaprojectrelativetoitscapitalresourcecosts.

• Theeconomicnetpresentvalue(ENPV)whichisthesumofthediscountedpresentvalueoftheeconomiccostsandbenefitsovertheappraisaltimeframe.AnENPVgreaterthanzerorepresentsapositiveeconomicreturn.

• Theeconomicbenefitcostratio(EBCR)whichistheratioofthepresentvalueofneteconomicbenefitstothepresentvalueofeconomicinvestmentcosts.AnEBCRgreaterthanoneimpliesthattheneteconomicbenefitsoutweightheneteconomiccosts,thusrepresentingapositiveeconomicreturn.

AcombinationoftheseindicatorsprovidesanoverallassessmentoftheeconomicvalueofHSR.

8.2.2 Defining the reference case and the base case

Reference caseThereferencecase(orthefutureHSRprogram)isthecentralcasefortheassessment.ItconsistsofthepreferredHSRsystemandspecificationsdescribedinChapters 3,4and5includingestimatesofcapitalandoperatingcosts.ItalsoincludesdemandandtravelimpactsoutlinedinChapter 2andthestagingprofileoutlinedin

Chapter 6.Thefirstyearofconstructionwasassumedtobe2027(financialyear2028),withservicesonLine1stage1(Sydney-Canberra)beginningin2035.

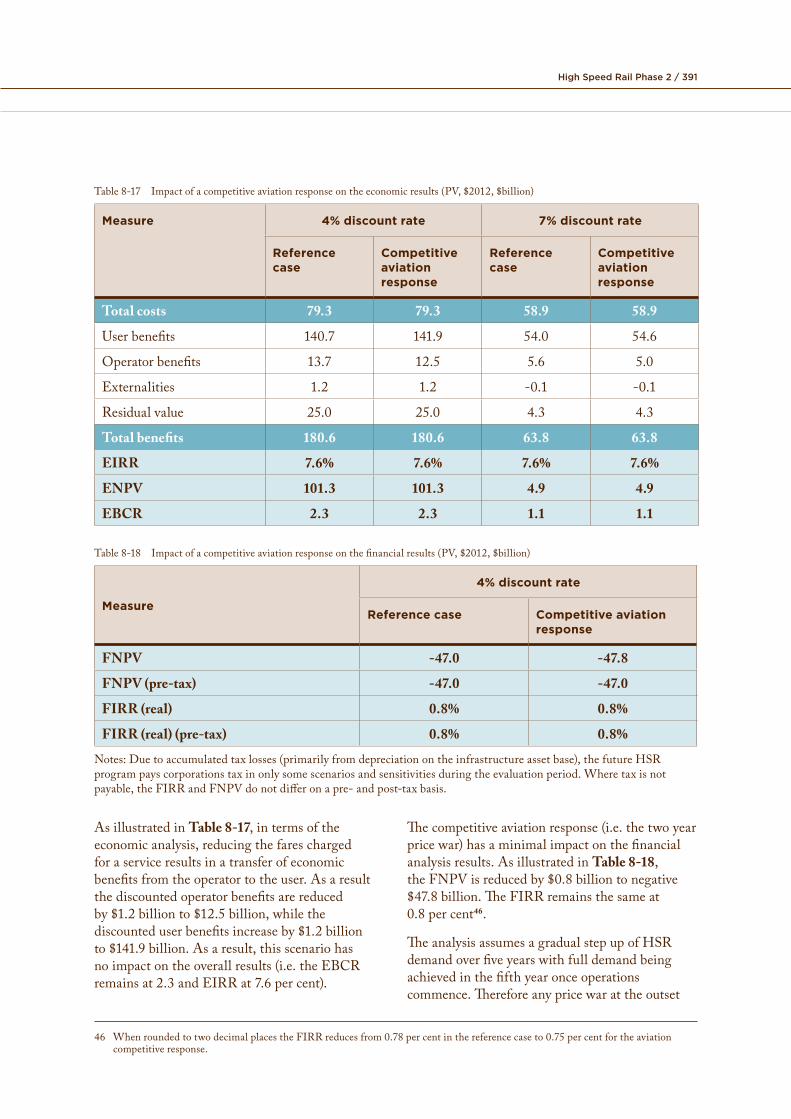

TheintroductionofthefutureHSRprogramwouldcompetevigorouslywithairtravel.TheaviationsectoristhereforelikelytobethemostheavilyimpactedbytheintroductionofthefutureHSRprogram.Ofthe83.6millionHSRtripsforecastfor2065,around55percentareforecasttobedivertedairtrips.Thiswoulddrivesignificantoperationalchangesintheaviationsector.

Airlineservicesaremobileinthesensethattherearefewsignificantsunkcapitalcostsinservicingparticularroutes,andassetscanbequicklyredeployedtootherroutes.Airlinesoperatingalongkeyregionalandinter-capitalroutesacrosstheeastcoastofAustraliaalreadycompetestronglyagainsteachother,andfarelevelsofmanyfareclasseshavedeclinedovertime,whichsuggeststhatairfarelevelsarealreadyhighlycompetitiveonmajorroutes.

Itisnotexpectedthatairlinescould,orwould,respondtoHSRcompetitionbyreducingtheirfaresonasustainablebasis.Rather,ithasbeenassumedthatairlineswouldquicklyreducecapacity,eitherbyreducingfrequenciesoraircraftsizes,tolocationswithintheHSRcorridorwherethereissignificantpassengerdiversiontoHSR13.Thisassumptionisconsistentwithoverseasexperiencewhere,followingtheintroductionofHSR,theairlineresponsehasgenerallybeentoreduceservicesonthecompetitiveroute.Forexample,AirFrancerespondedtotheParis–MarseilleHSRnetworkbyreducingservicesandEasyJetexitedtheroute.InJapantherewassomelimitedpricecompetitionfromtheairlinesoncompetingroutes,althougharguablytheJapanesedomesticairlinemarketwaslesscompetitivethanAustralia’sisnow.

GiventhatairfaresinAustraliaarealreadyhighlycompetitiveonmajorroutes,nosustainablereductioninairfareswouldbeexpectedfollowingtheintroductionofHSR.However,asensitivitytesthasbeenincludedinsection 8.6.3toassess

13 ItislikelythatanyavailablecapacitywillberedeployedtoroutesoutsidetheHSRcorridor.

Chapter 8 Economic appraisal of the preferred HSR system

theimpactthatatwoyearpricewarbetweenHSRandaviationwouldhaveontheeconomicandfinancialanalysisresultsforHSR.

Base caseThebasecaseassumesthat,withoutHSR,travellersontheeastcoastwillcontinuetorelyonexistingmodesoftransport:

• Aviationwillremaintheprimarymeansoftransportforlongdistanceinterstate(andsomeinter-regional)trips.

• Road-basedtravelandprivatevehicleusagewillremaintheprimarymodeforconnectionswithandbetweenregionalcentres.

• Publictransportwillplayanincreasinglyimportantroleinmeetingtraveldemandwithincities,servedbyconventionalrailandbus.

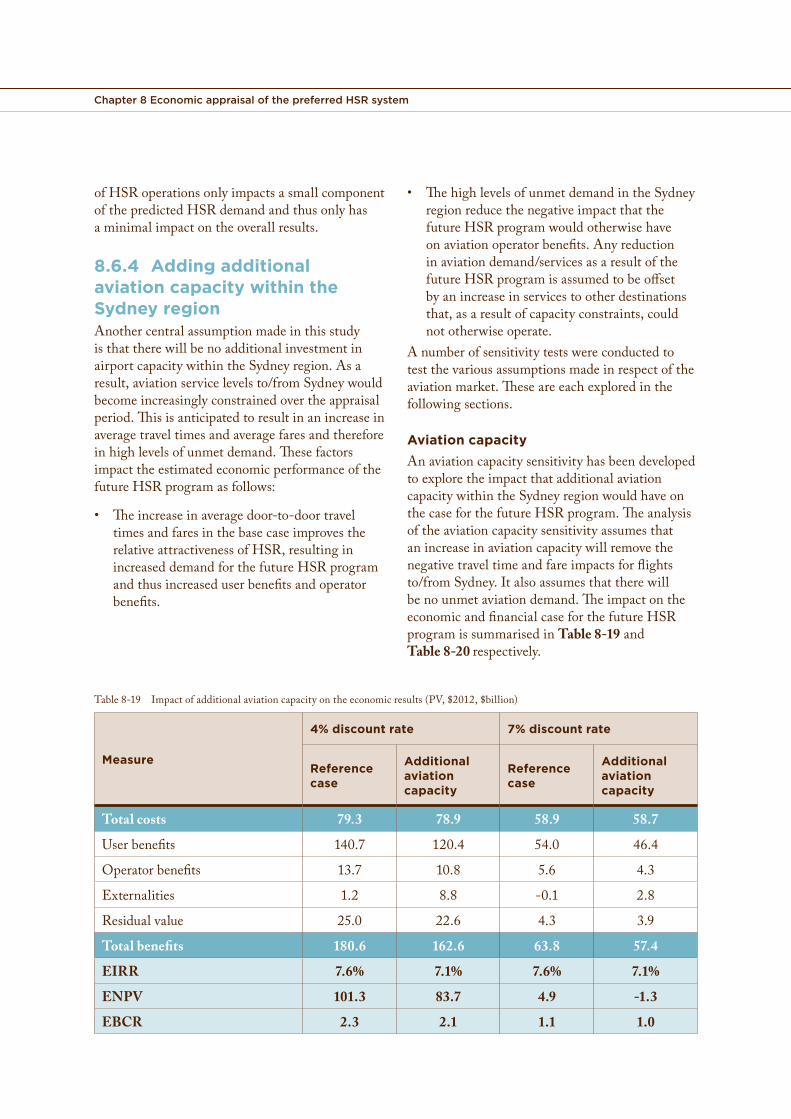

Forroadandrailmodes,thebasecaseassumesthatgovernmentswillcontinuetoaugmentsupplybyprovidinginfrastructureandservicestomeetfuturedemand.Foraviation,giventheuncertaintyaroundthefutureofairportcapacityintheSydneyregion,thebasecasehasassumedthatnoadditionalinvestmentinairportcapacityintheSydneybasinwouldoccur.Asaconsequence,thebasecaseassumesthatservicelevelswithintheSydneyregionwillbecomeincreasinglyconstrained.

AsoutlinedwithintherecentAustralian/NSWGovernmentJoint Study into Aviation Capacity in the Sydney Region14(hereafterreferredtoastheJointStudy),growthindemandforaviationservicesintheSydneyregionisexpectedtodoubleto88millionpassengertripsperyearby2035,andthendoubleagainby2060.Sydney(KingsfordSmith)Airportdoesnothavethecapacitytomeettheexpecteddemand,leadingto:• Slowerandgreaterunreliabilityinairjourney

timesasairlinesandairportsarefacedwithhigherlevelsofcongestion.

• Anincreasingrequirementforairpassengerstoshifttheirtraveltimeasaresultoflackofcapacityattheirpreferredtraveltime.

• Anincreasingnumberoftravellerswhoareforcedtotravelbyothermeansordonottravelatall(otherwiseknownasunmetand/orsupresseddemand).

ThisassumptionhasaddedcomplexitytothemodellingofthebasecasetotakeaccountoftheconstraintsatSydneyAirport.TobeconsistentwiththeassumptionsoutlinedwithintheJointStudy15,thebasecasemodellingofaviationtripsthroughSydneyhasincludedanadditionalunexpecteddelayfactorof11minutesperpassenger16andasevenpercentincreaseinfares17.

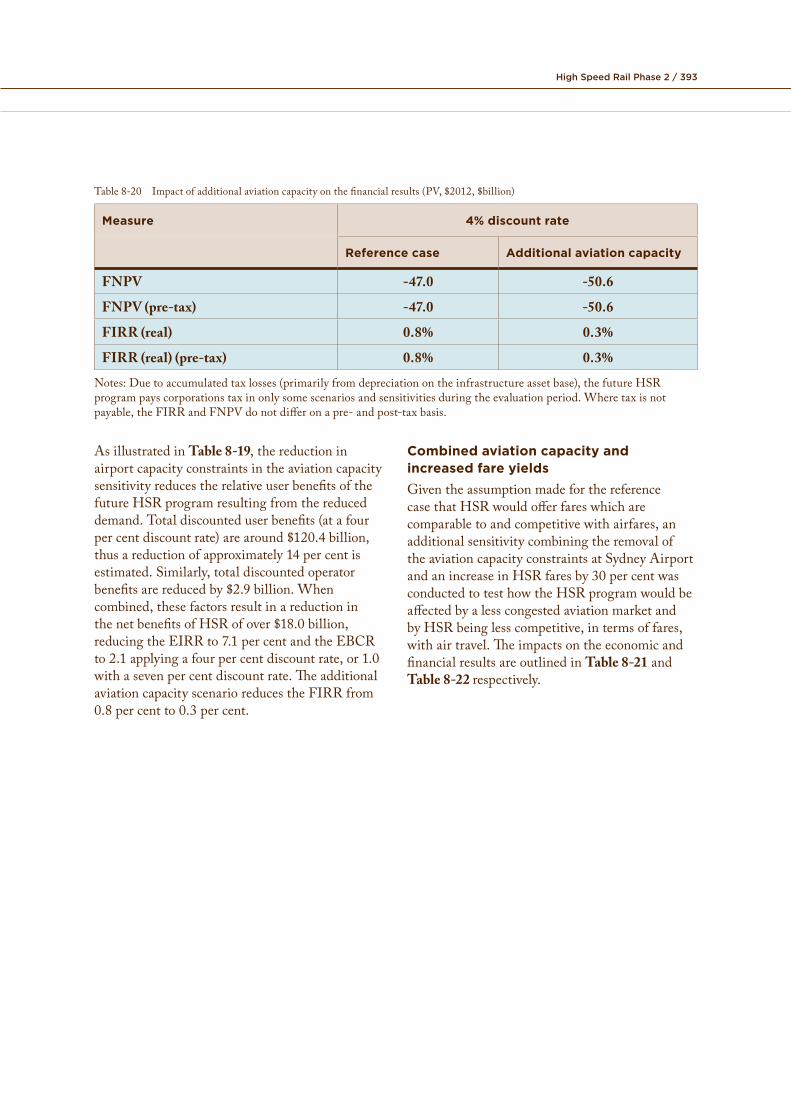

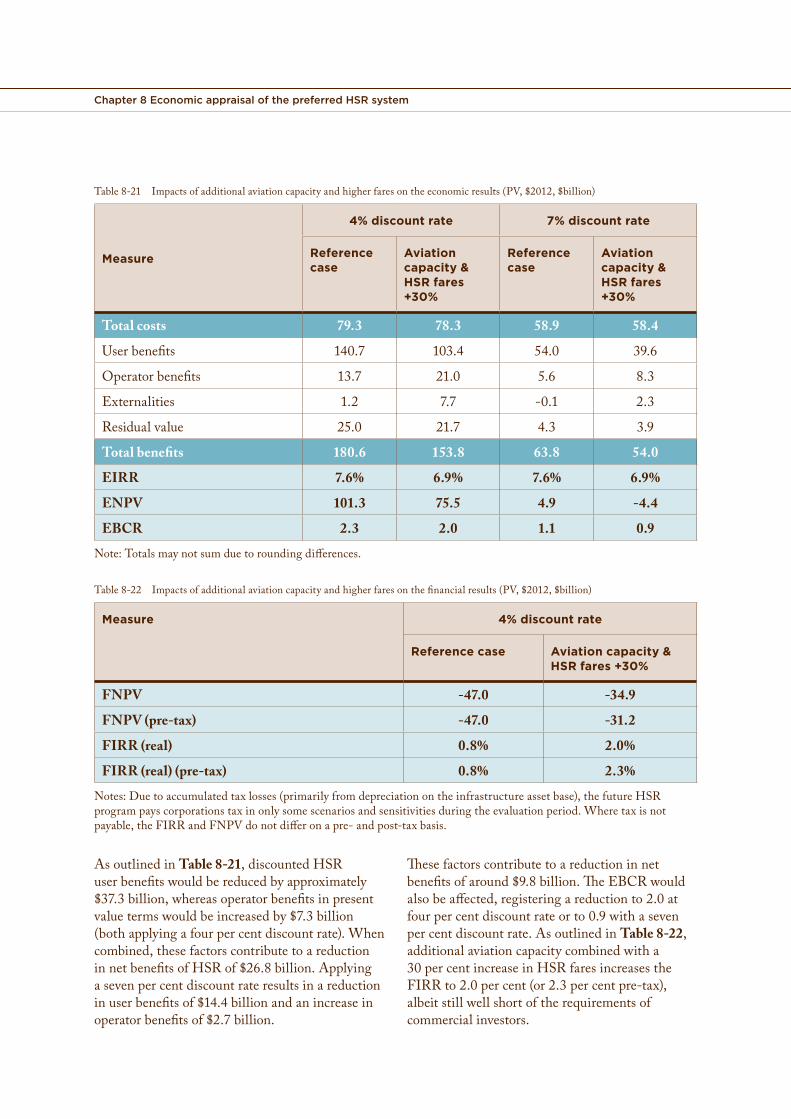

Giventhelikelysignificanceofthisassumption,asensitivitytestthatallowedforadditionalaviationcapacityinSydneywasincludedinsection 8.6.4totesttheimpactsofremovingtheeffectsoftheunexpecteddelayandfareincreasesfromthemodelling.

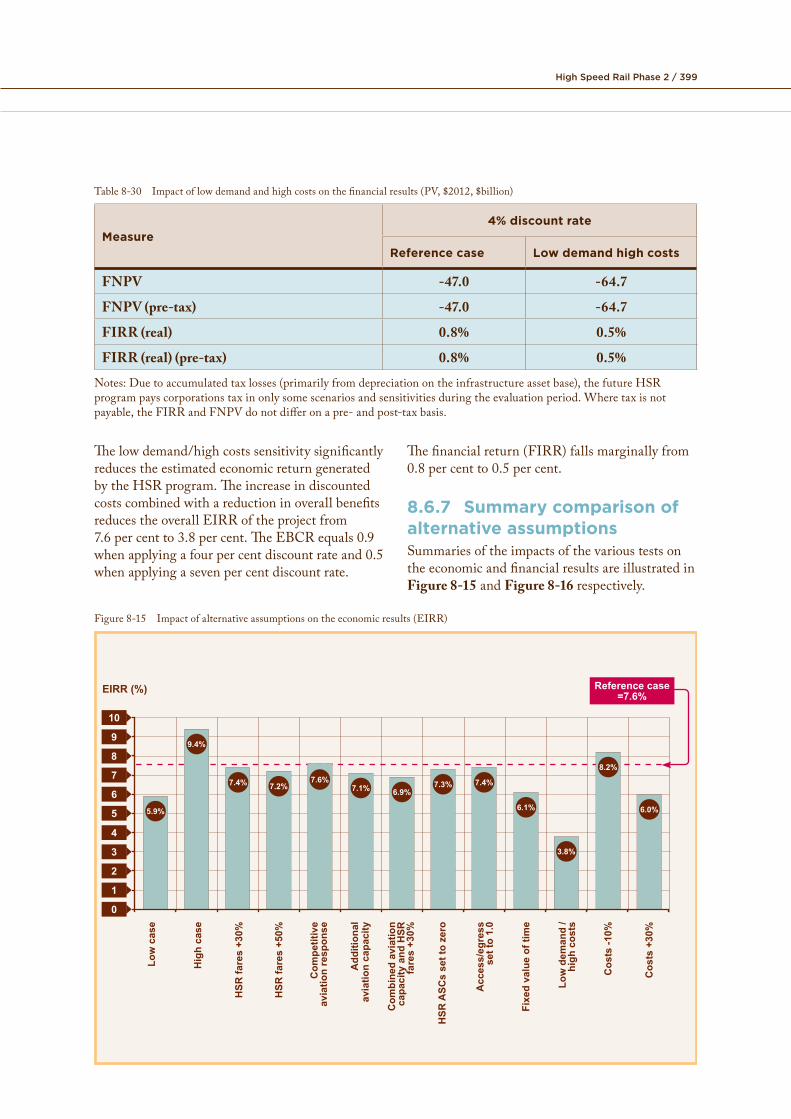

8.3 Cost-benefit analysis resultsTheCBAwasundertakeninrealtermsin$2012utilisingadiscountrateoffourpercentwithabaseyearof202818,reflectingthereferencecaseandthebasecasedefinedabove.This,takentogetherasasetofCBAresults,istheprimarycasefortheeconomicevaluation,againstwhichvarioussensitivitiesandscenarioswererun.

Afourpercentdiscountratehasbeenassessedassuitableforlargescaleandlong-lifeinfrastructureprojectssuchasHSR.ThisisconsistentwithinternationalexperienceandtheAustralianTransportCouncil(ATC)guidelinesandhasthereforebeenadoptedasthediscountratefortheprimaryevaluationofHSR.

14 AustralianGovernmentandNSWGovernment,loc.cit.15 ibid.16 The11minutesaverageincreaseinunexpecteddelayovertoday’sconditionsisweightedby3.0withintheanalysis.Thisisconsistent

withCivilAviationSafetyAuthority(CASA)(2007)Cost-BenefitAnalysisProceduresManual.17 Thesevenpercentincreaseinfaresrepresentstheaveragedisbenefitofairpassengershavingtochangetheirtimeoftraveltofitwith

theavailabilityofseatcapacity.18 Thebaseyearistheyeartowhichcostsandbenefitshavebeendiscounted.ConsistentwiththeATCguidelines,thebaseyearisset

totheyearofconstructioncommencement.

High Speed Rail Phase 2 / 365

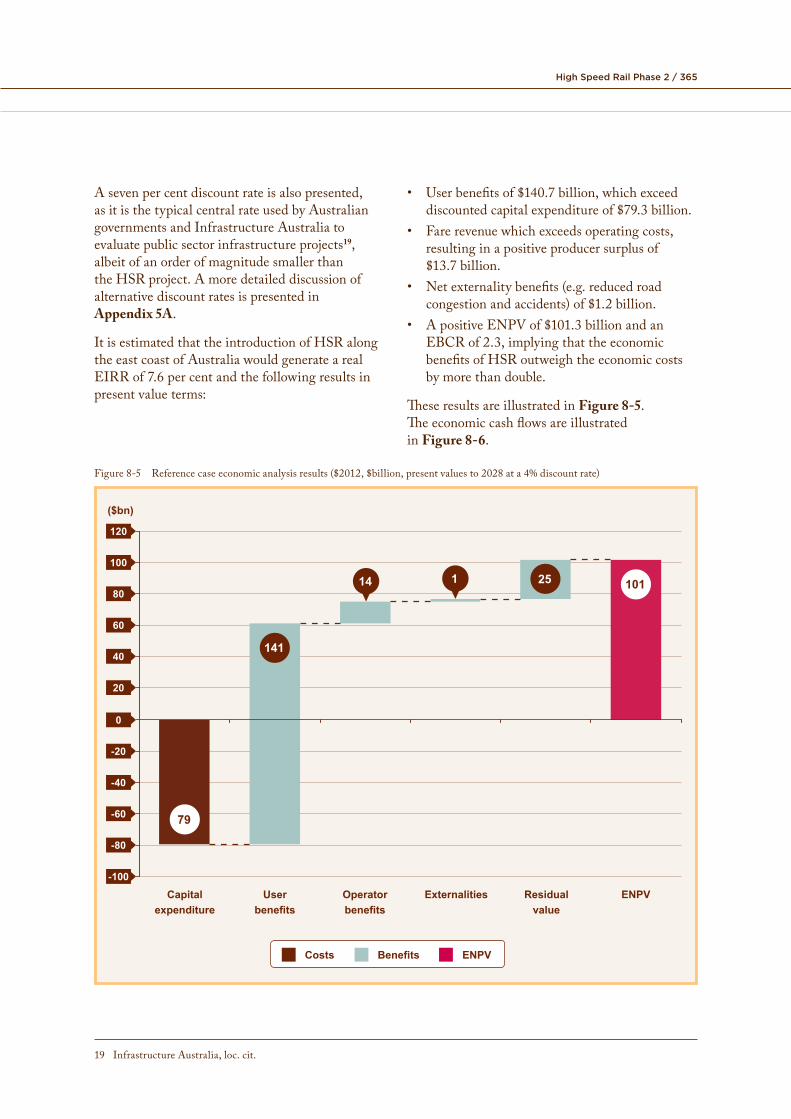

A seven per cent discount rate is also presented, • User benefits of $140.7 billion, which exceed as it is the typical central rate used by Australian discounted capital expenditure of $79.3 billion.governments and Infrastructure Australia to

19• Fare revenue which exceeds operating costs,

evaluate public sector infrastructure projects , resulting in a positive producer surplus of albeit of an order of magnitude smaller than $13.7 billion.the HSR project. A more detailed discussion of • Net externality benefits (e.g. reduced road alternative discount rates is presented in congestion and accidents) of $1.2 billion. Appendix 5A.

• A positive ENPV of $101.3 billion and an It is estimated that the introduction of HSR along EBCR of 2.3, implying that the economic the east coast of Australia would generate a real benefits of HSR outweigh the economic costs EIRR of 7.6 per cent and the following results in by more than double. present value terms:

These results are illustrated in Figure 8-5. The economic cash flows are illustrated in Figure 8-6.

Figure 8-5 Reference case economic analysis results ($2012, $billion, present values to 2028 at a 4% discount rate)

Costs Benefits ENPV

100

120

80

60

40

20

0

-40

-20

-60

-80

-100

Capitalexpenditure

Userbenefits

Operatorbenefits

Externalities Residual value

ENPV

($bn)

14 1

79

141

25 101

19 Infrastructure Australia, loc. cit.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-6 Reference case economic cash flows per year (undiscounted, $2012, $billion)

($20

12, $

billi

on)

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

-5

0

5

10

15

20

25

30

35

-10

Capital expenditure

Sydney to Canberra operational

Sydney to Melbourne operational

Newcastle to Melbourne operational

Brisbane to Gold Coast & Newcastle to Melbourne operational Network operational

User benefits Operational benefits Externalities

A

A B C

D E

B C D E

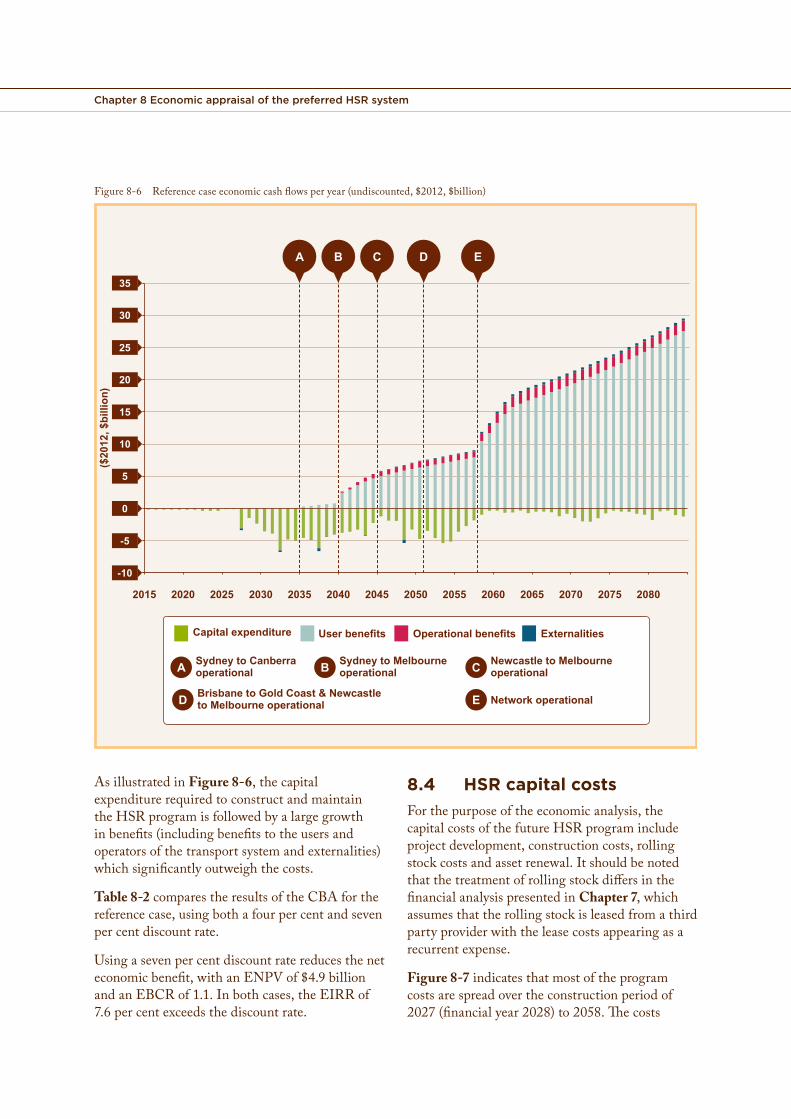

As illustrated in Figure 8-6, the capital expenditure required to construct and maintain the HSR program is followed by a large growth in benefits (including benefits to the users and operators of the transport system and externalities) which significantly outweigh the costs.

Table 8-2 compares the results of the CBA for the reference case, using both a four per cent and seven per cent discount rate.

Using a seven per cent discount rate reduces the net economic benefit, with an ENPV of $4.9 billion and an EBCR of 1.1. In both cases, the EIRR of 7.6 per cent exceeds the discount rate.

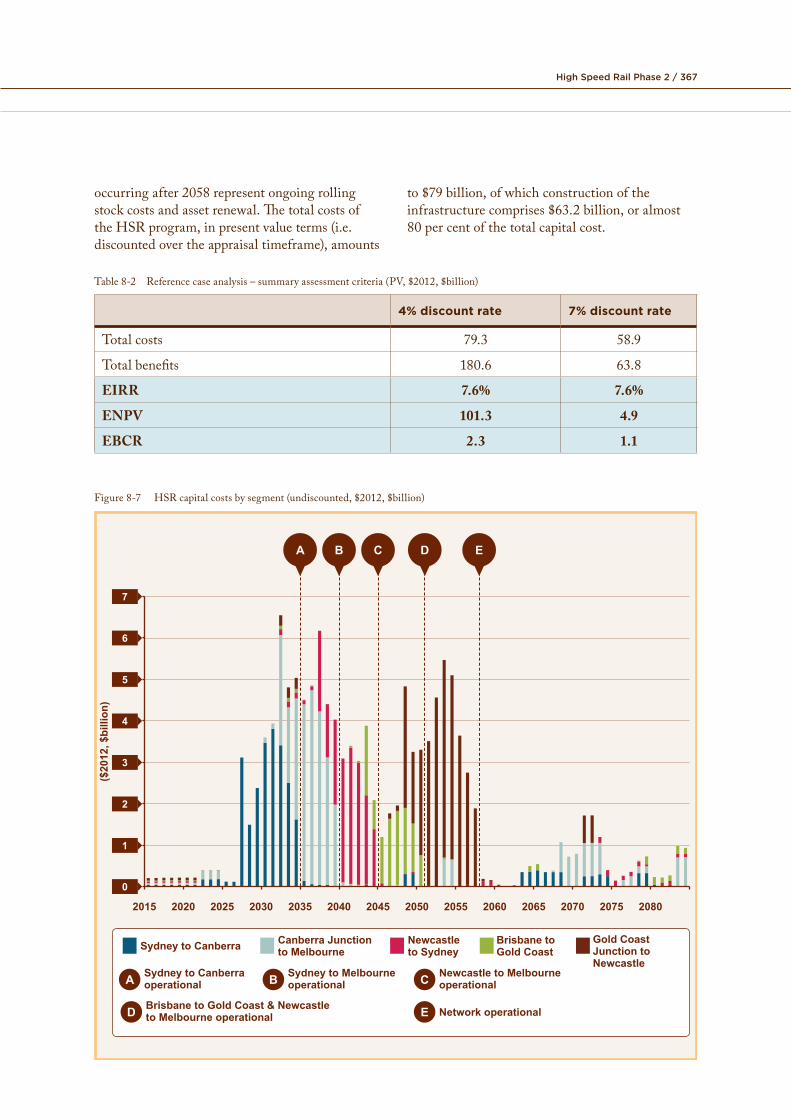

8.4 HSR capital costsFor the purpose of the economic analysis, the capital costs of the future HSR program include project development, construction costs, rolling stock costs and asset renewal. It should be noted that the treatment of rolling stock differs in the financial analysis presented in Chapter 7, which assumes that the rolling stock is leased from a third party provider with the lease costs appearing as a recurrent expense.

Figure 8-7 indicates that most of the program costs are spread over the construction period of 2027 (financial year 2028) to 2058. The costs

High Speed Rail Phase 2 / 367

occurring after 2058 represent ongoing rolling to $79 billion, of which construction of the stock costs and asset renewal. The total costs of infrastructure comprises $63.2 billion, or almost the HSR program, in present value terms (i.e. 80 per cent of the total capital cost.discounted over the appraisal timeframe), amounts

Table 8-2 Reference case analysis – summary assessment criteria (PV, $2012, $billion)

4% discount rate 7% discount rate

Total costs 79.3 58.9

Total benefits 180.6 63.8

EIRR 7.6% 7.6%

ENPV 101.3 4.9

EBCR 2.3 1.1

Figure 8-7 HSR capital costs by segment (undiscounted, $2012, $billion)

($20

12, $

billi

on)

0

1

2

3

4

5

6

7

Sydney to Canberra

Sydney to Canberra operational

Sydney to Melbourne operational

Newcastle to Melbourne operational

Brisbane to Gold Coast & Newcastle to Melbourne operational Network operational

Canberra Junction to Melbourne

Newcastle to Sydney

Brisbane to Gold Coast

Gold Coast Junction toNewcastle

A B C

D E

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

A B C D E

Chapter 8 Economic appraisal of the preferred HSR system

SignificantgovernmentcontributionswouldberequiredtofundtheconstructionofHSR.Iftaxeswereincreasedtofundthegovernmentspending,theDepartmentofFinanceandDeregulationHandbookofCost-benefitanalysis20suggeststhatanadjustmentfortheexcessburdenoftax21shouldbeincludedwiththefinancialcosts.AsdiscussedinChapter 7theanalysisdoesnotmakeanyassumptionsinregardtohowthefutureHSRprogramwouldbefundedorfinanced.Assuchnoadjustmentshavebeenincludedtothefinancialcoststocoverpotentialtaxationimplications.TheimpactsofgovernmentinvestmentintheHSRprogram,includingflowoneffectsonGDP,arediscussedinmoredetailintheCGEanalysispresentedinsection 8.8.

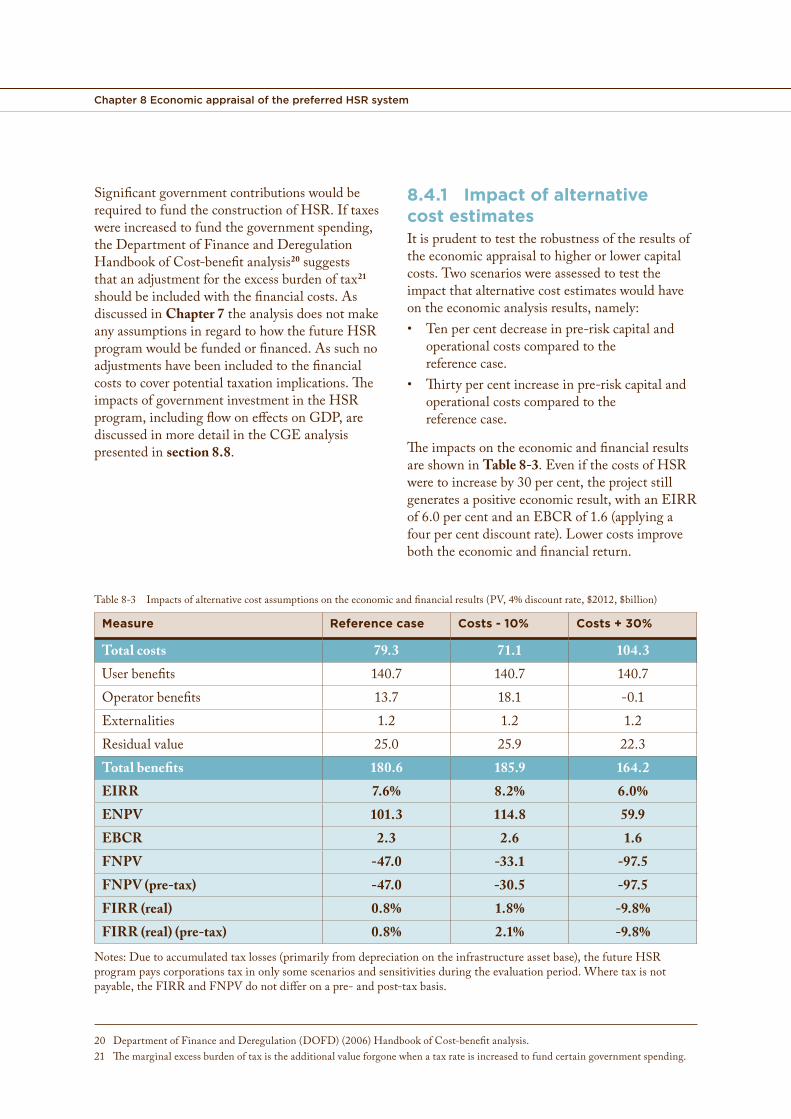

8.4.1 Impact of alternative cost estimatesItisprudenttotesttherobustnessoftheresultsoftheeconomicappraisaltohigherorlowercapitalcosts.Twoscenarioswereassessedtotesttheimpactthatalternativecostestimateswouldhaveontheeconomicanalysisresults,namely:• Tenpercentdecreaseinpre-riskcapitaland

operationalcostscomparedtothereferencecase.

• Thirtypercentincreaseinpre-riskcapitalandoperationalcostscomparedtothereferencecase.

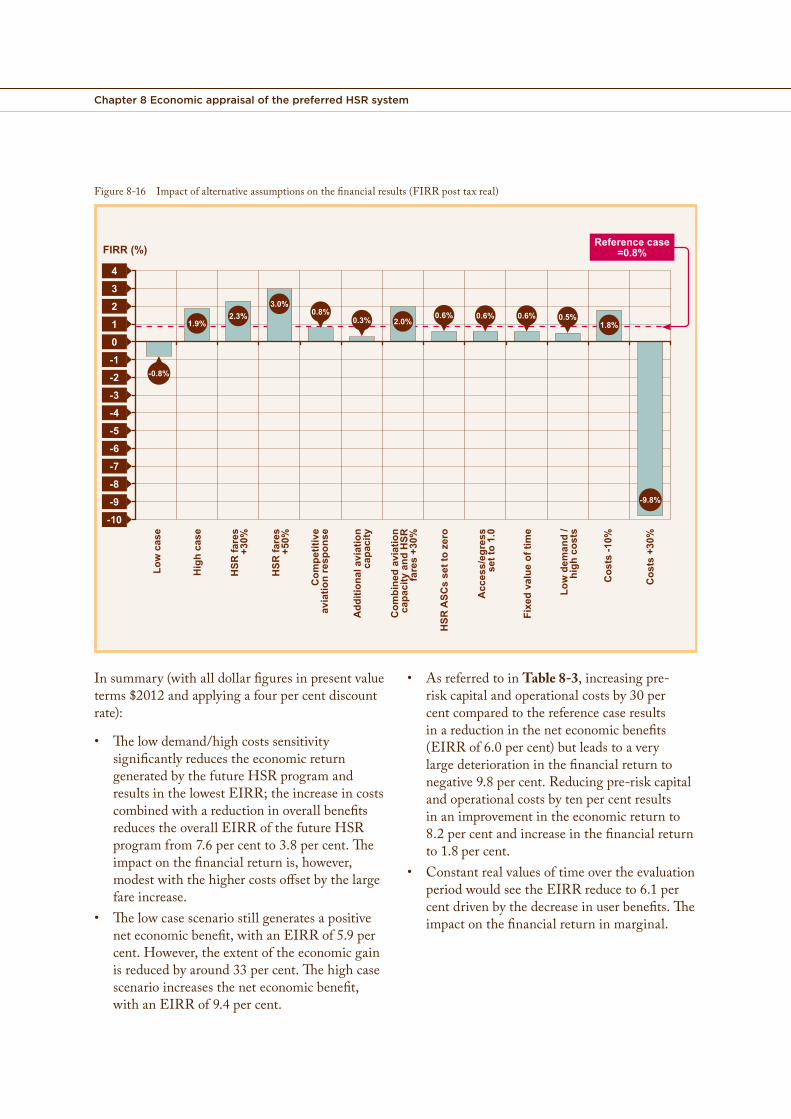

TheimpactsontheeconomicandfinancialresultsareshowninTable 8-3.EvenifthecostsofHSRweretoincreaseby30percent,theprojectstillgeneratesapositiveeconomicresult,withanEIRRof6.0percentandanEBCRof1.6(applyingafourpercentdiscountrate).Lowercostsimproveboththeeconomicandfinancialreturn.

Table8-3 Impactsofalternativecostassumptionsontheeconomicandfinancialresults(PV,4%discountrate,$2012,$billion)

Measure Reference case Costs - 10% Costs + 30%

Total costs 79.3 71.1 104.3Userbenefits 140.7 140.7 140.7Operatorbenefits 13.7 18.1 -0.1Externalities 1.2 1.2 1.2Residualvalue 25.0 25.9 22.3Total benefits 180.6 185.9 164.2EIRR 7.6% 8.2% 6.0%ENPV 101.3 114.8 59.9EBCR 2.3 2.6 1.6FNPV -47.0 -33.1 -97.5FNPV (pre-tax) -47.0 -30.5 -97.5FIRR (real) 0.8% 1.8% -9.8%FIRR (real) (pre-tax) 0.8% 2.1% -9.8%

Notes:Duetoaccumulatedtaxlosses(primarilyfromdepreciationontheinfrastructureassetbase),thefutureHSRprogrampayscorporationstaxinonlysomescenariosandsensitivitiesduringtheevaluationperiod.Wheretaxisnotpayable,theFIRRandFNPVdonotdifferonapre-andpost-taxbasis.

20 DepartmentofFinanceandDeregulation(DOFD)(2006)HandbookofCost-benefitanalysis.21 Themarginalexcessburdenoftaxistheadditionalvalueforgonewhenataxrateisincreasedtofundcertaingovernmentspending.

High Speed Rail Phase 2 / 369

8.5 HSR benefitsAsoutlinedinsection 8.2.1,thestreamofneteconomicbenefitscomprisesthreeparts:userbenefits,operatorbenefitsandexternalities.Eachisdiscussedbelow.

8.5.1 User benefitsTotaluserbenefitmeasurestheoverallchangein‘generalisedcostoftravel’asaresultofpeopleusingHSRcomparedtobasecasemodalchoices.‘Generalisedcost’includesthevariouscomponentsthatcontributetotheoverallcostofmakingatrip,e.g.thefare,thejourneytimeand,fortravelbycar,theoperatingcost.Italsoincludesautilityimpactwhichtakesintoconsiderationtherelativeamenityfeaturesofamodenotcapturedinothervariables(the‘alternativespecificconstant’).Thecalculationoftheuserbenefitsalsoincludesthebenefitsgeneratedbyinduceddemand(i.e.newtravelencouragedbyHSRasopposedtotraveldivertedfromothermodes).

Thecomputationoftheuserbenefitsisbasedonthe‘logsum’orcompositecost,whichisanoutputoftheproceduresusedforforecastingthepatronageonanewmodeoftransport(inthiscase,the‘logit’modelofthechoicebetweentransportmodes).Thesecomputationsofuserbenefitshavebeenindependentlyauditedandverifiedusingafirstprinciplesapproachtoestimatingtheconsumersurplusfromtheareaunderthedemandcurve.OneofthecharacteristicsofthechoicemodelusedinthedemandforecastsisthatitwillforecastasmallvolumeoftripsdivertingtoHSRevenwhentheexistingmodesremainbyfarthebestchoiceonaverage.Whilethiscanbeobservedinreallife,acheckontheresultsconfirmedthattheselow-volumediversionsdidnothaveamaterialeffectinaggregateontheestimateddemandandbenefits.

FourindicativecasestudyexamplesarepresentedtoillustratetheimpactthattheintroductionofHSRwouldhaveonatypicaljourney.Thecasestudiesalsooutlinehowtheuserbenefitsareestimated.ThefourexamplesarebusinesstripsfrominnereastMelbournetoinnerSydneyand

fromouternorthwestMelbournetoPortBotanyinSydney,andleisuretripsfromWaggaWaggatoSydneyCBDandfromTumuttoParramatta.ThesetripsaccountfordifferentproportionsoftheHSRdemandandbenefits,withMelbournetoSydneybeingthemostimportant.

Forbusinesstravel,themajorityofuserbenefits(about62percent)canbeattributedtoHSRprovidingadirectimprovementovertheexistingbest22transportmodes.Another24percentareduetothebenefitgainedbyhavinganadditionalmodeoftransportavailableinthecorridorwhich,whilenotthebestmode,neverthelessattractsashareofthetraveldemand23.Theremaining14percentareduetothebenefitsattributabletoinducedtraveldemand.

ForthosebusinessjourneysforwhichthecurrentmodeisairandHSRbecomesthebestmode,virtuallyall(94percent)oftheuserbenefitscanbeattributedtothereducedaccessandegresstimesandcoststo/fromtheHSRcitycentrestationsascomparedwiththeairports.

Withinthecapitalcities,mostvisitorsendtheirtripsinthecityCBDandsomeresidentsstarttheirtripsintheCBD.Forthesetripstheaccess/egressdistancesto/fromtheCBDaresubstantiallylessfromtheHSRcentralstationsthanfromtheairports.Hence,thereisasubstantialaccessbenefitwithHSRintermsofbothjourneytimesandtravelcosts.Giventheimportanceoftheaccess/egressbenefits,theaccess,egressandtraveltimeassumptionsandthegeneralisedcostformulationhavebeenindependentlyauditedandconfirmedtobereasonable.

Casestudy1illustratesabusinesstripfrominnereastMelbournetoinnerSydney.Inthiscasestudy,theaccessjourneyfromeastofMelbournetotheCBDismuchshorterthanthatthroughtheCBDtotheairport;thisisreflectedintheuserbenefit.SydneyAirportisclosertotheCBDandtheegressbenefitwithHSRiscorrespondinglyless.

AsillustratedinTable 8-4,HSRisonaverage92minutesbetteringeneralisedcosttermsthanair.Ifallairtripswereforecasttoswitch

22 WithoutHSR,themodethatoffersthelowestgeneralisedcostoftravel.23 EvenifHSRisnotthebestmode‘onaverage’,becauseindividualtravelpreferencesareassumedtobedistributedaroundtheaverage

itwillstillattractsometrips,asexplainedfurtherinthedescriptionofthecasestudies.

Chapter 8 Economic appraisal of the preferred HSR system

tothebettermode,thiswouldbethebenefit forwhomthebenefitsoftheHSRjourneyareeachwouldreceive.Withtwosuchdifferent significantlyhigherthantheaverageof92minutes.modesoftransport,suchasimplisticforecasting Inconsequence,theoverallaverageuserbenefitmethodologyisunrealisticandsomesplitofthe isforecasttobe129minutespertrip,highertripsbetweenthetwomodeswouldbeexpected. thantheaverageof92minutesduetotheutility

distribution.Usingthe2065valueofbusinessIntheforecastingprocedures,variationsin time,thisisequivalentto$231pertrip.Inadditionindividualpreferencesandtheapproximations tothedivertingtrips,therearebenefitstoinducedofmodellingarereflectedinadistributionof tripsonHSR.generalisedcost(orutility)foreachmode.Thatis,thegeneralisedcostisrepresentedbyanobserved Incasestudy2,abusinesstripfromouternorthcomponent(the‘average’generalisedcost,asgiven westMelbournetoPortBotanyinSydneyisainthecasestudytable)plusarandom,unobserved contrastinginter-capitaltripinwhichtheorigincomponentwhichrepresentstheindividual anddestinationaresimilarlyaccessibletothevariations.Consequently,ratherthandetermining airportandtheHSRstation,andthustheaccessthemodalallocationbasedonaverageutilities, andegressbenefitsarenotsignificant.Inthisthemodesharemodelaccountsforthe case,thelevel-of-serviceforairandHSRisutilitydistribution. virtuallyidentical.

Theconsequenceofthisisthat,incasestudy1, Inthissituation,thedistributionofgeneraliseddespiteHSRbeingconsiderablybetterthanair costsissuchthatforjustunder50percentoftripsonaverageingeneralisedcostterms,notallair theairgeneralisedcostisbetterthanthatofHSR,tripsareforecasttodiverttoHSR(theforecast andfortheremainingtripstheHSRgeneralisedHSRsharebeing70percent).Forthe3percent costisbetterthanthatofair.Theforecastisforaoftravellersremainingontheairservices,the broadlyequalshareoftripsonthetwomodes.airgeneralisedcostisbetter(lower)thanthat

ThedivertingtripsareattributedabenefitbasedforHSR,theindividualvariationsintheutilityonthedifferenceingeneralisedcostbetweenthedistributionusedinthemodelfortheseparticularHSRandairmodesasdeterminedfromtheutilitytravellersbeingsufficientlyinfavourofairtodistribution.Forallofthedivertingtrips,thenullifytheaverage92minutesgeneralisedcostdifferencebetweentheHSRandairgeneralisedadvantageofHSR.costsutilityishigherthanthedifferenceinthe

ThetripswhichdiverttoHSRareattributed averagegeneralisedcosts(whichisclosetozero).auserbenefitbasedonthedifferenceinutility ThetripsdivertingtoHSRthereforegainabetweentheHSRandairmodesasdetermined significantbenefit.Theoverallaverageuserbenefitfromtheutilitydistribution.Justastheutility is73minutespertrip,equivalentto$133in2065.distributionhasreducedthegeneralisedcost AgainthereareadditionaluserbenefitsarisingadvantageofHSRbelowtheaverageforsome frominducedHSRtravel.trips,italsoimpliesthattherearemanytravellers

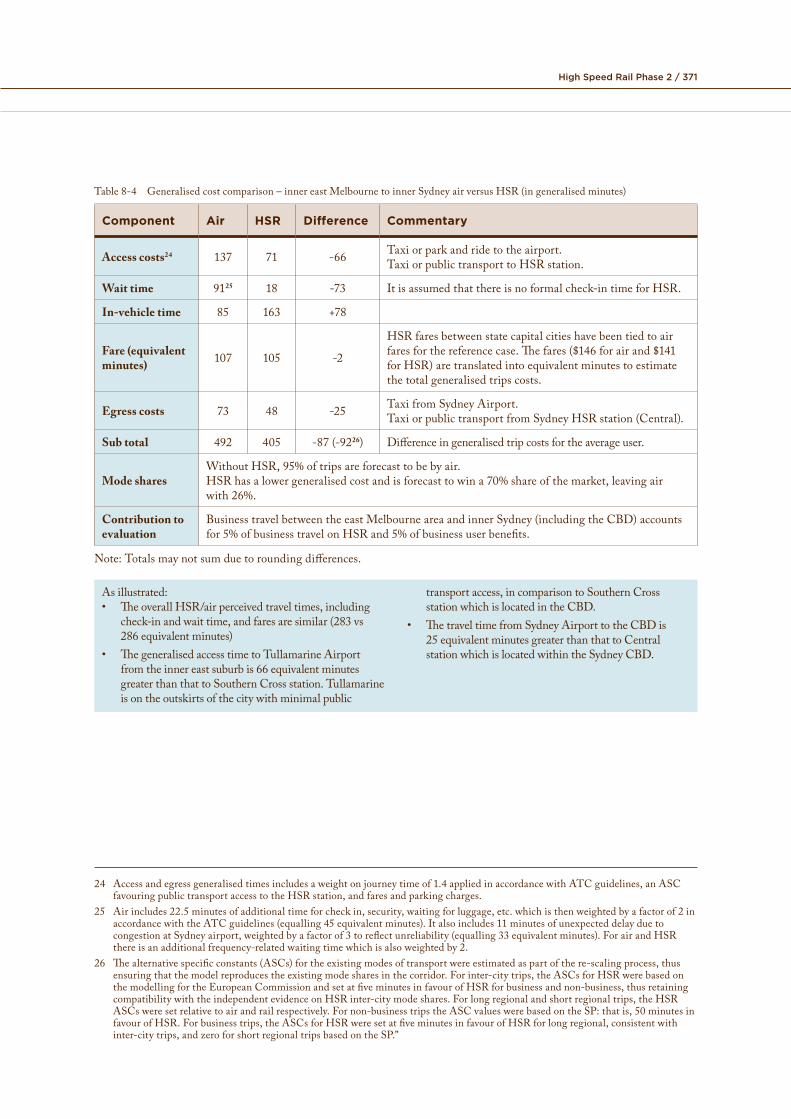

Case study 1 – Business trip from inner east Melbourne to inner SydneyIntheabsenceofHSRatypicalbusinesstripfrominnereast WiththefutureHSRprogram,atypicaljourneycouldMelbournetotheSydneyCBDcould involve: consistof:• AtaxiorparkandridetoMelbourne • AtaxiorpublictransporttoSouthernCrossstation.

(Tullamarine)airport. • Waitingtimeatthestation• Checkinattheairportandwaittimeuntilflight • HSRfromSouthernCrossstationMelbournetoCentral

departure,andpotentialdelaysduetocongestionat station/SydneyCBD.SydneyAirportorotherunexpectedfactors. • TaxiorpublictransportegressfromCentralstationto

• FlightfromMelbourneAirporttoSydneyAirport. SydneyCBD.• TaxifromSydneyAirporttoSydneyCBD.

Anindicativeassessmentofthegeneralisedcosts(expressedinequivalentminutes)associatedwitheachofthetripsisoutlinedbelowinTable 8-4.

High Speed Rail Phase 2 / 371

Table8-4 Generalisedcostcomparison–innereastMelbournetoinnerSydneyairversusHSR(ingeneralisedminutes)

Component Air HSR Difference Commentary

Access costs24 137 71 -66 TaxiTaxi

oror

parkandridetopublictransport

theairport.toHSRstation.

Wait time 9125 18 -73 Itisassumedthatthereisnoformalcheck-intimeforHSR.

In-vehicle time 85 163 +78

Fare (equivalent minutes) 107 105 -2

HSRfaresbetweenstatecapitalcitieshavebeentiedtoairfaresforthereferencecase.Thefares($146forairand$141forHSR)aretranslatedintoequivalentminutestoestimatethetotalgeneralisedtripscosts.

Egress costs 73 48 -25 TaxiTaxi

fromSydneyAirport.orpublictransportfromSydneyHSRstation(Central).

Sub total 492 405 -87(-9226) Differenceingeneralisedtripcostsfortheaverageuser.

Mode sharesWithoutHSR,95%oftripsareforecastHSRhasalowergeneralisedcostandiswith 26%.

tobebyforecast

air.towina70%shareofthemarket,leavingair

Contribution to evaluation

Businesstravelbetweenfor5%ofbusinesstravel

theon

eastMelbourneHSRand5%of

areaandbusiness

innerSydneyuserbenefits.

(includingtheCBD)accounts

Note:Totalsmaynotsumduetoroundingdifferences.

Asillustrated: transportaccess,incomparisontoSouthernCross• TheoverallHSR/airperceivedtraveltimes,including stationwhichislocatedintheCBD.

check-inandwaittime,andfaresaresimilar(283vs • Th etraveltimefromSydneyAirporttotheCBDis286 equivalentminutes) 25 equivalentminutesgreaterthanthattoCentral

• Th egeneralisedaccesstimetoTullamarineAirport stationwhichislocatedwithintheSydneyCBD.fromtheinnereastsuburbis66equivalentminutesgreaterthanthattoSouthernCrossstation.Tullamarineisontheoutskirtsofthecitywithminimalpublic

24 Accessandegressgeneralisedtimesincludesaweightonjourneytimeof1.4appliedinaccordancewithATCguidelines,anASCfavouringpublictransportaccesstotheHSRstation,andfaresandparkingcharges.

25 Airincludes22.5minutesofadditionaltimeforcheckin,security,waitingforluggage,etc.whichisthenweightedbyafactorof2inaccordancewiththeATCguidelines(equalling45equivalentminutes).Italsoincludes11minutesofunexpecteddelayduetocongestionatSydneyairport,weightedbyafactorof3toreflectunreliability(equalling33equivalentminutes).ForairandHSRthereisanadditionalfrequency-relatedwaitingtimewhichisalsoweightedby2.

26 Thealternativespecificconstants(ASCs)fortheexistingmodesoftransportwereestimatedaspartofthere-scalingprocess,thusensuringthatthemodelreproducestheexistingmodesharesinthecorridor.Forinter-citytrips,theASCsforHSRwerebasedonthemodellingfortheEuropeanCommissionandsetatfiveminutesinfavourofHSRforbusinessandnon-business,thusretainingcompatibilitywiththeindependentevidenceonHSRinter-citymodeshares.Forlongregionalandshortregionaltrips,theHSRASCsweresetrelativetoairandrailrespectively.Fornon-businesstripstheASCvalueswerebasedontheSP:thatis,50minutesinfavourofHSR.Forbusinesstrips,theASCsforHSRweresetatfiveminutesinfavourofHSRforlongregional,consistentwithinter-citytrips,andzeroforshortregionaltripsbasedontheSP.”

Chapter 8 Economic appraisal of the preferred HSR system

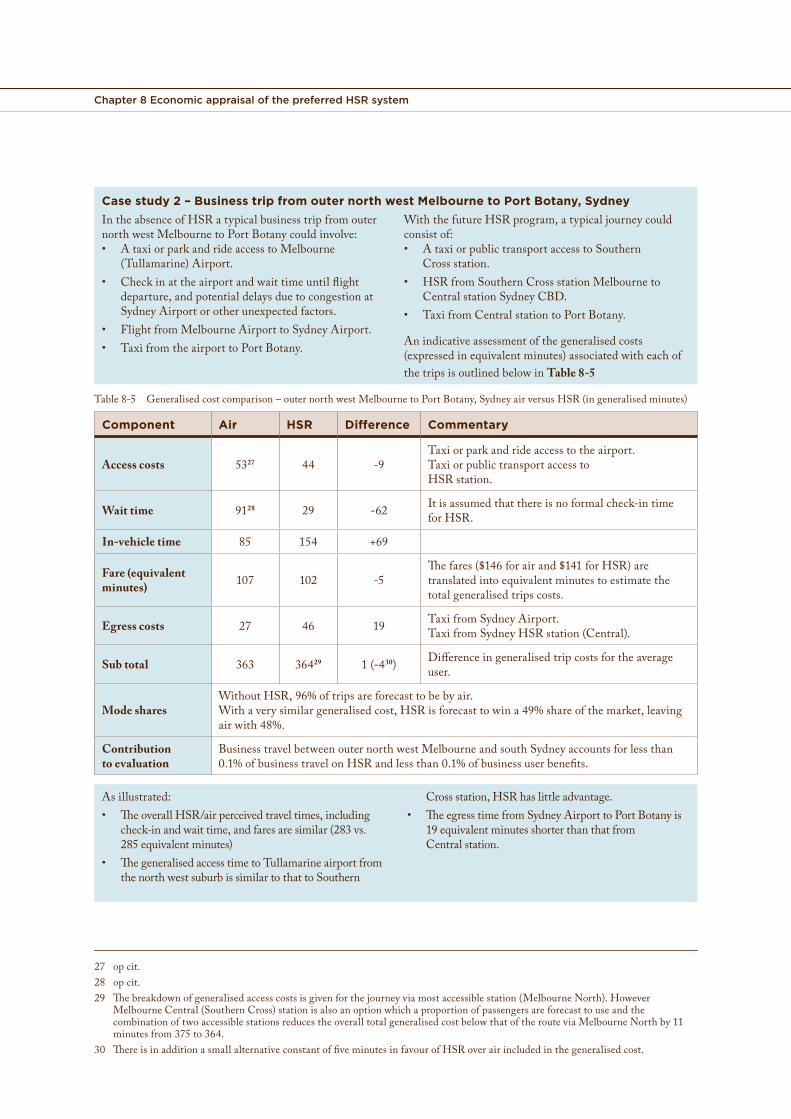

Case study 2 – Business trip from outer north west Melbourne to Port Botany, SydneyIntheabsenceofHSRatypicalbusinesstripfromouter WiththefutureHSRprogram,atypicaljourneycouldnorthwestMelbournetoPortBotanycould involve: consistof:• AtaxiorparkandrideaccesstoMelbourne • AtaxiorpublictransportaccesstoSouthern

(Tullamarine)Airport. Crossstation.• Checkinattheairportandwaittimeuntilflight • HSRfromSouthernCrossstationMelbourneto

departure,andpotentialdelaysduetocongestionat CentralstationSydneyCBD.SydneyAirportorotherunexpectedfactors. • TaxifromCentralstationtoPortBotany.

• FlightfromMelbourneAirporttoSydneyAirport.Anindicativeassessmentofthegeneralisedcosts• TaxifromtheairporttoPortBotany. (expressedinequivalentminutes)associatedwitheachofthetripsisoutlinedbelowinTable 8-5

Table8-5 Generalisedcostcomparison–outernorthwestMelbournetoPortBotany,SydneyairversusHSR(ingeneralisedminutes)

Component Air HSR Difference Commentary

Access costs 5327 44 -9TaxiorparkandrideaccesstoTaxiorpublictransportaccessHSRstation.

theto

airport.

Wait time 9128 29 -62 ItisassumedforHSR.

thatthereisnoformalcheck-intime

In-vehicle time 85 154 +69

Fare (equivalent minutes) 107 102 -5

Thefares($146forairand$141forHSR)aretranslatedintoequivalentminutestoestimatetotalgeneralisedtripscosts.

the

Egress costs 27 46 19 TaxiTaxi

fromfrom

SydneySydney

Airport.HSRstation(Central).

Sub total 363 36429 1(-430) Differenceingeneraliseduser.

tripcostsfortheaverage

Mode sharesWithoutHSR,96%oftripsareWithaverysimilargeneralisedairwith48%.

forecasttocost,HSR

bebyair.isforecasttowina49%shareofthemarket,leaving

Contribution to evaluation

Businesstravelbetweenouternorth0.1%ofbusinesstravelonHSRand

westMelbournelessthan0.1%of

andsouthSydneyaccountsbusinessuserbenefits.

forlessthan

Asillustrated: Crossstation,HSRhaslittleadvantage.• TheoverallHSR/airperceivedtraveltimes,including • TheegresstimefromSydneyAirporttoPortBotanyis

check-inandwaittime,andfaresaresimilar(283vs. 19equivalentminutesshorterthanthatfrom285equivalentminutes) Centralstation.

• ThegeneralisedaccesstimetoTullamarineairportfromthenorthwestsuburbissimilartothattoSouthern

27 opcit.28 opcit.29 Thebreakdownofgeneralisedaccesscostsisgivenforthejourneyviamostaccessiblestation(MelbourneNorth).However

MelbourneCentral(SouthernCross)stationisalsoanoptionwhichaproportionofpassengersareforecasttouseandthecombinationoftwoaccessiblestationsreducestheoveralltotalgeneralisedcostbelowthatoftherouteviaMelbourneNorthby11minutesfrom375to364.

30 ThereisinadditionasmallalternativeconstantoffiveminutesinfavourofHSRoverairincludedinthegeneralisedcost.

High Speed Rail Phase 2 / 373

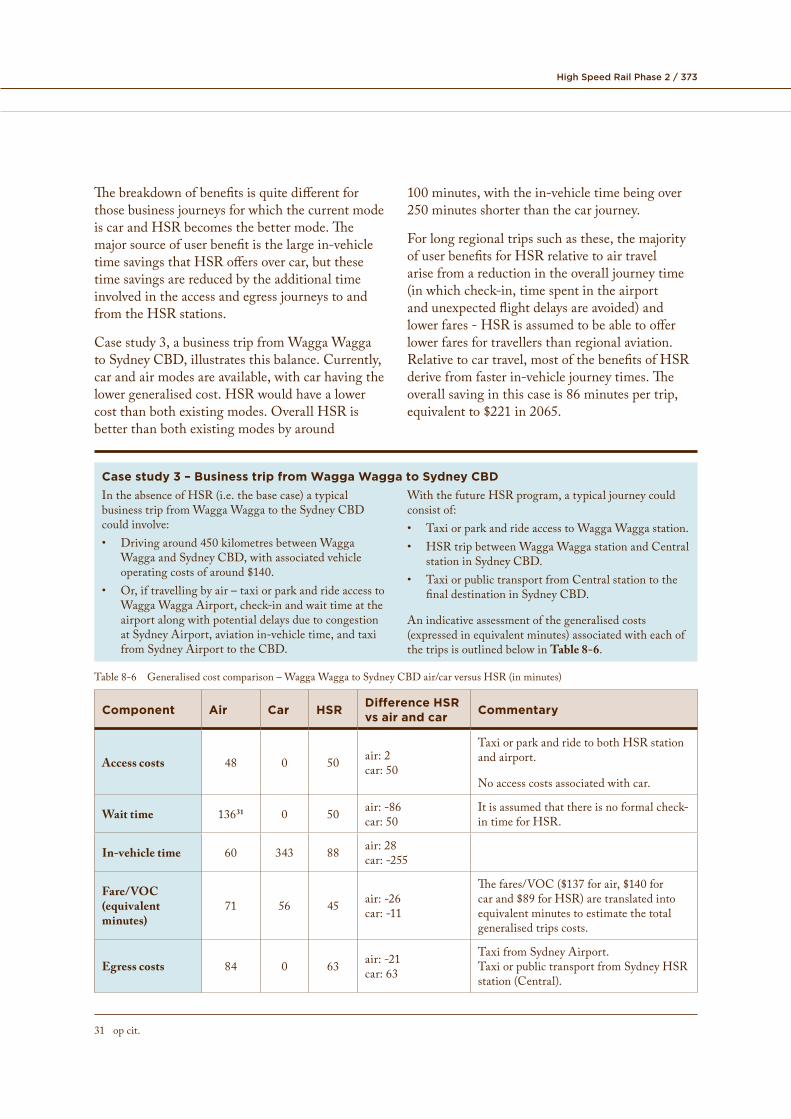

The breakdown of benefits is quite different for those business journeys for which the current mode is car and HSR becomes the better mode. The major source of user benefit is the large in-vehicle time savings that HSR offers over car, but these time savings are reduced by the additional time involved in the access and egress journeys to and from the HSR stations.

Case study 3, a business trip from Wagga Wagga to Sydney CBD, illustrates this balance. Currently, car and air modes are available, with car having the lower generalised cost. HSR would have a lower cost than both existing modes. Overall HSR is better than both existing modes by around

100 minutes, with the in-vehicle time being over 250 minutes shorter than the car journey.

For long regional trips such as these, the majority of user benefits for HSR relative to air travel arise from a reduction in the overall journey time (in which check-in, time spent in the airport and unexpected flight delays are avoided) and lower fares - HSR is assumed to be able to offer lower fares for travellers than regional aviation. Relative to car travel, most of the benefits of HSR derive from faster in-vehicle journey times. The overall saving in this case is 86 minutes per trip, equivalent to $221 in 2065.

Case study 3 – Business trip from Wagga Wagga to Sydney CBDIn the absence of HSR (i.e. the base case) a typical business trip from Wagga Wagga to the Sydney CBD could involve:• Driving around 450 kilometres between Wagga

Wagga and Sydney CBD, with associated vehicle operating costs of around $140.

• Or, if travelling by air – taxi or park and ride access to Wagga Wagga Airport, check-in and wait time at the airport along with potential delays due to congestion at Sydney Airport, aviation in-vehicle time, and taxi from Sydney Airport to the CBD.

With the future HSR program, a typical journey could consist of:• Taxi or park and ride access to Wagga Wagga station.• HSR trip between Wagga Wagga station and Central

station in Sydney CBD.• Taxi or public transport from Central station to the

final destination in Sydney CBD.

An indicative assessment of the generalised costs (expressed in equivalent minutes) associated with each of the trips is outlined below in Table 8-6.

Table 8-6 Generalised cost comparison – Wagga Wagga to Sydney CBD air/car versus HSR (in minutes)

Component Air Car HSR Difference HSR vs air and car Commentary

Access costs 48 0 50 air: 2 car: 50

Taxi or park and ride to both HSR station and airport.

No access costs associated with car.

Wait time 13631 0 50 air: -86 car: 50

It is assumed that there is no formal check-in time for HSR.

In-vehicle time 60 343 88 air: 28 car: -255

Fare/VOC (equivalent minutes)

71 56 45 air: -26 car: -11

The fares/VOC ($137 for air, $140 for car and $89 for HSR) are translated into equivalent minutes to estimate the total generalised trips costs.

Egress costs 84 0 63 air: -21 car: 63

Taxi from Sydney Airport. Taxi or public transport from Sydney HSR station (Central).

31 op cit.

Chapter 8 Economic appraisal of the preferred HSR system

Component Air Car HSR Difference HSR vs air and car Commentary

Sub total 399 399 296 air:car:

-103-103

(10832)(-9033)

Differenceinaverageuser.

generalisedtripcostsforthe

WithoutHSR,47%oftripsareforecasttobebyairand51%bycar.Mode shares Withalowergeneralisedcostthenbothairandcar,HSRisforecasttowina48%shareofthe

market,leavingairandcarwith13%and36%respectively,thegreaterimpactbeingonair.

Contribution to evaluation

BusinesstravelfromtheregionalareasbetweenCanberraandAlbury-Wodonga,encompassingWaggaWaggaandTumut,toSydneyCBDaccountsforlessthan0.1%ofbusinesstravelonHSRandlessthan0.1%ofbusinessuserbenefits.

Asillustrated: fourhoursshorter,whichisonlypartiallyoffsetbythe• Comparedwithair,HSRhasaloweroveralltime(wait accessandegresscostsforHSR.TheHSRfareisalso

andin-vehicle),alowerfareandloweregresscost. veryclosetothecostofusingcar.

• Comparedwithcar,thein-vehicletimebyHSRisover

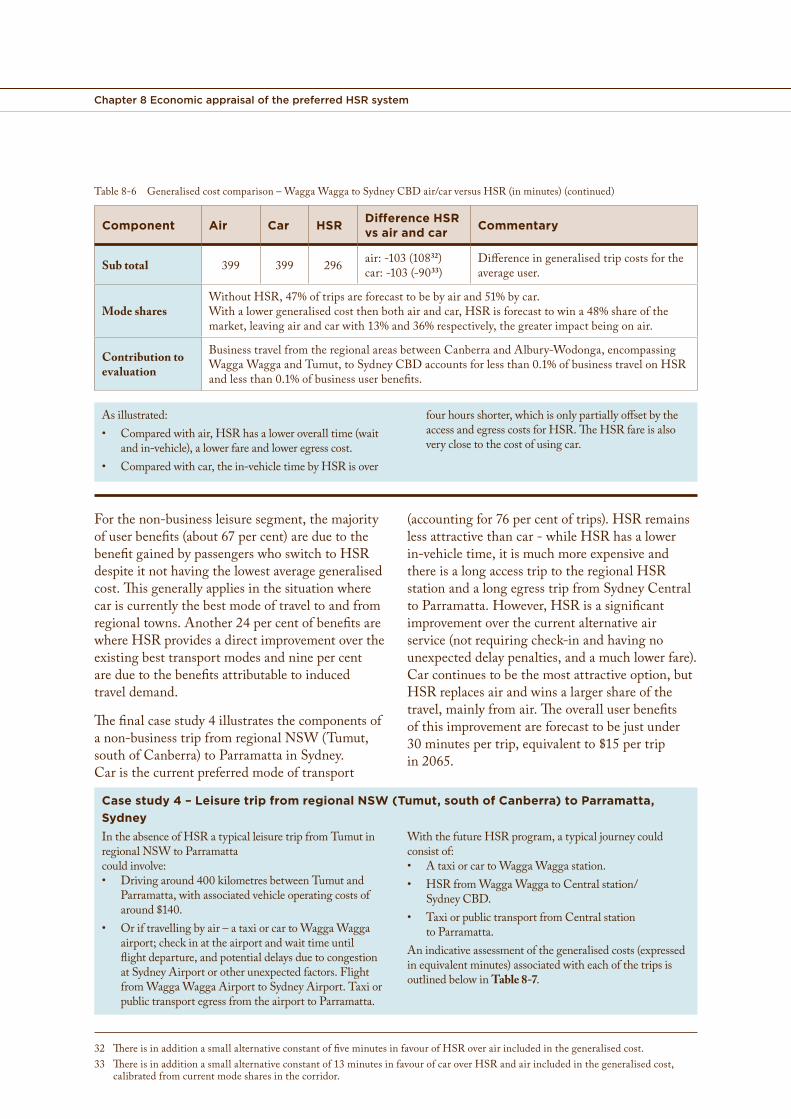

Forthenon-businessleisuresegment,themajority (accountingfor76percentoftrips).HSRremainsofuserbenefits(about67percent)areduetothe lessattractivethancar-whileHSRhasalowerbenefitgainedbypassengerswhoswitchtoHSR in-vehicletime,itismuchmoreexpensiveanddespiteitnothavingthelowestaveragegeneralised thereisalongaccesstriptotheregionalHSRcost.Thisgenerallyappliesinthesituationwhere stationandalongegresstripfromSydneyCentralcariscurrentlythebestmodeoftraveltoandfrom toParramatta.However,HSRisasignificantregionaltowns.Another24percentofbenefitsare improvementoverthecurrentalternativeairwhereHSRprovidesadirectimprovementoverthe service(notrequiringcheck-inandhavingnoexistingbesttransportmodesandninepercent unexpecteddelaypenalties,andamuchlowerfare).areduetothebenefitsattributabletoinduced Carcontinuestobethemostattractiveoption,buttraveldemand. HSRreplacesairandwinsalargershareofthe

travel,mainlyfromair.TheoveralluserbenefitsThefinalcasestudy4illustratesthecomponentsof ofthisimprovementareforecasttobejustunderanon-businesstripfromregionalNSW(Tumut, 30 minutespertrip,equivalentto$15pertripsouthofCanberra)toParramattainSydney. in2065.Caristhecurrentpreferredmodeoftransport

Case study 4 – Leisure trip from regional NSW (Tumut, south of Canberra) to Parramatta, SydneyIntheabsenceofHSRatypicalleisuretripfromTumutin WiththefutureHSRprogram,atypicaljourneycouldregionalNSWtoParramatta consistof:couldinvolve: • AtaxiorcartoWaggaWaggastation.• Drivingaround400kilometresbetweenTumutand • HSRfromWaggaWaggatoCentralstation/

Parramatta,withassociatedvehicleoperatingcostsof SydneyCBD.around$140. • TaxiorpublictransportfromCentralstation

• Oriftravellingbyair–ataxiorcartoWaggaWagga toParramatta.airport;checkinattheairportandwaittimeuntil Anindicativeassessmentofthegeneralisedcosts(expressedflightdeparture,andpotentialdelaysduetocongestion inequivalentminutes)associatedwitheachofthetripsisatSydneyAirportorotherunexpectedfactors.Flight outlinedbelowinTable 8-7.fromWaggaWaggaAirporttoSydneyAirport.TaxiorpublictransportegressfromtheairporttoParramatta.

32 ThereisinadditionasmallalternativeconstantoffiveminutesinfavourofHSRoverairincludedinthegeneralisedcost.33 Thereisinadditionasmallalternativeconstantof13minutesinfavourofcaroverHSRandairincludedinthegeneralisedcost,

calibratedfromcurrentmodesharesinthecorridor.

Table8-6 Generalisedcostcomparison–WaggaWaggatoSydneyCBDair/carversusHSR(inminutes)(continued)

High Speed Rail Phase 2 / 375

Table8-7 Generalisedcostcomparison–TumuttoParramattaair/carversusHSR(ingeneralisedminutes)

Component Air Car HSR Difference Air/Car Commentary

Access costs34 159 0 161 air:car:

2161

TaxiorparkandridetobothHSRstationandairport.Noaccesscostsassociatedwithcar.

Wait time 13635 0 50 air:car:

-8650

ItisassumedthattimeforHSR.

thereisnoformalcheck-in

In-vehicle time 60 309 88 air:car:

28-221

Fare/VOC (equivalent minutes)

264 64 118 air:car:

-14654

Thefares/VOC($137forair,$140forcarand$89forHSR)aretranslatedintoequivalentminutestoestimatethetotalgeneralisedtripscosts.

Egress costs 143 0 84 air:car:

-5984

TaxifromSydneyAirport.Taxiorpublictransportfromstation(Central).

SydneyHSR

Sub total 762 373 501 air:car:

-261128

(-31136)(27337)

Differenceinaverageuser.

generalisedtripcostsforthe

WithoutHSR,76%oftripsareforecasttobebycarand16%byair.Mode shares Withamuchreducedgeneralisedcostcomparedtoair,HSRwinsa29%shareofthemarket,

leavingairwith1%.Carremainsthelowestcostmodeandretainsa63%share.

Contribution to evaluation

Non-businesstravelfromtheregionalareasbetweenCanberraandAlbury-Wodonga,encompassingWaggaWaggaandTumutbetweenEasternMelbourneandSydneyCBDaccountsforlessthan0.1%ofnon-businesstravelonHSRandlessthan0.1%ofnon-businessuserbenefits.

Asillustrated: • TheegresstimeandcostfromSydneyAirportto• HSRprovidesbettertraveltimes,includingcheck-in Parramattais59equivalentminuteslongerthanthat

andwaittime,andlowercostcomparedtoair fromCentralstation.

• Thegeneralisedaccesstimesbyrailandairare • Carisbothquicker(afterallowingforwaitingandsimilarlylong. access/egresstimes)andcheaperthanairandHSR.

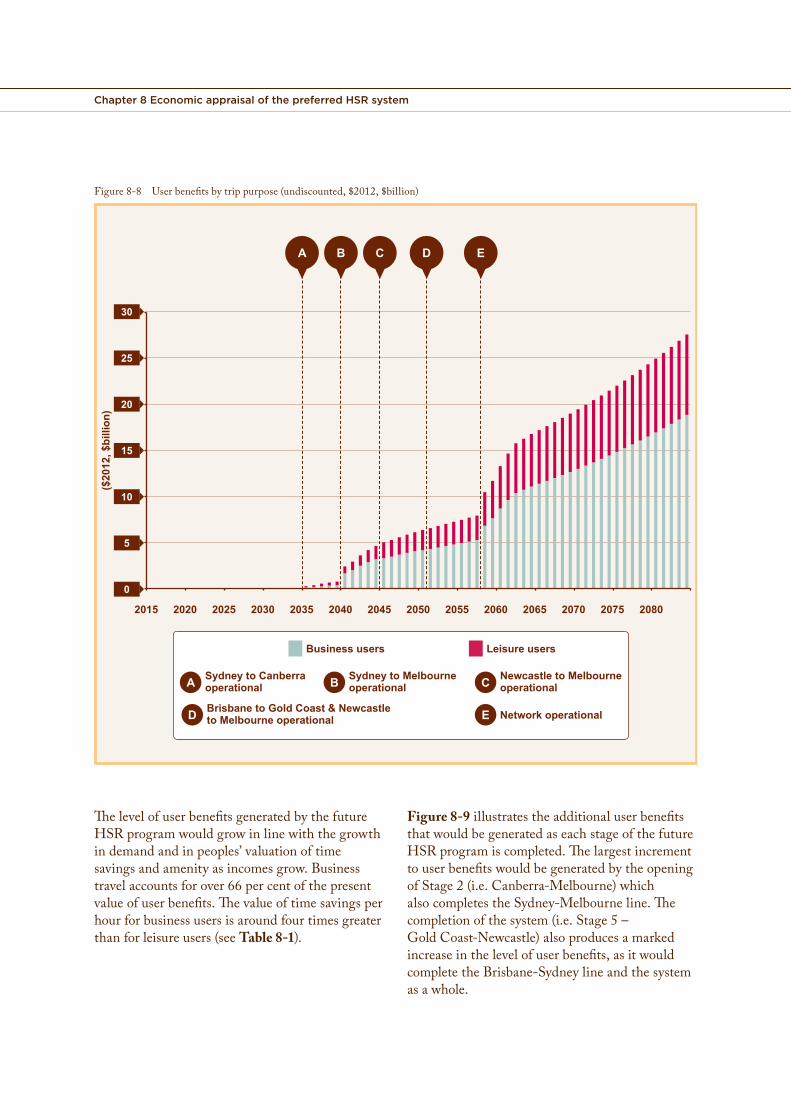

TheprocessoutlinedineachofthecasestudiesabovewasrepeatedforallpossiblecombinationsoftripsalongthecorridortoestimatetheaggregateuserbenefitsassociatedwiththeintroductionofthefutureHSRprogram.TheresultinguserbenefitsacrosstheappraisaltimeframeareillustratedbytrippurposeinFigure 8-8.

34 opcit.35 opcit.36 Thereisinadditionanalternativeconstantof50minutesinfavourofHSRoverairincludedinthegeneralisedcost,derivedfromthe

statedpreferencesurveysinthecorridor.37 Thereisinadditionanalternativeconstantof145minutesinfavourofcaroverHSRandairincludedinthegeneralisedcost,

calibratedfromcurrentmodesharesinthecorridor.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-8 User benefits by trip purpose (undiscounted, $2012, $billion)

($20

12, $

billi

on)

0

Sydney to Canberra operational

Sydney to Melbourne operational

Newcastle to Melbourne operational

Brisbane to Gold Coast & Newcastle to Melbourne operational Network operational

Business users Leisure users

A B C

D E

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

A B C D E

30

25

20

15

10

5

The level of user benefits generated by the future Figure 8-9 illustrates the additional user benefits HSR program would grow in line with the growth that would be generated as each stage of the future in demand and in peoples’ valuation of time HSR program is completed. The largest increment savings and amenity as incomes grow. Business to user benefits would be generated by the opening travel accounts for over 66 per cent of the present of Stage 2 (i.e. Canberra-Melbourne) which value of user benefits. The value of time savings per also completes the Sydney-Melbourne line. The hour for business users is around four times greater completion of the system (i.e. Stage 5 – than for leisure users (see Table 8-1). Gold Coast-Newcastle) also produces a marked

increase in the level of user benefits, as it would complete the Brisbane-Sydney line and the system as a whole.

High Speed Rail Phase 2 / 377

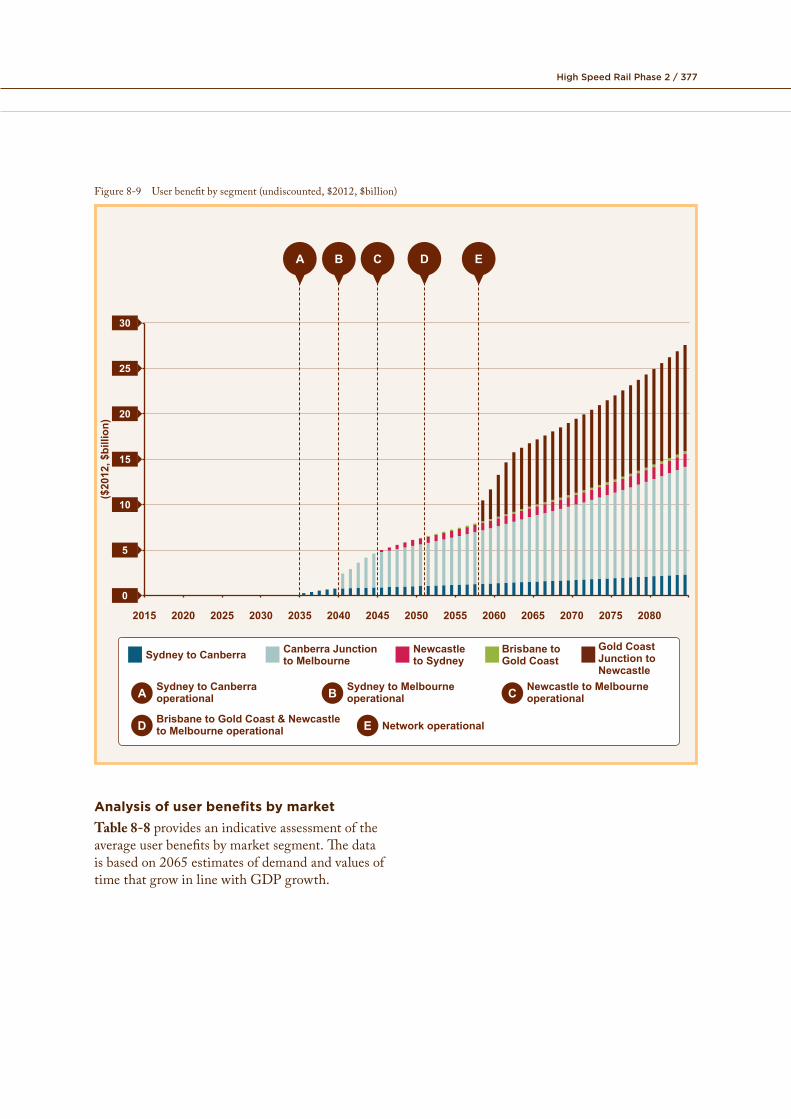

Figure 8-9 User benefit by segment (undiscounted, $2012, $billion)

($20

12, $

billi

on)

0

Sydney to Canberra operational

Sydney to Melbourne operational

Newcastle to Melbourne operational

Brisbane to Gold Coast & Newcastle to Melbourne operational Network operational

A B C

D E

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

A B C D E

30

25

20

15

10

5

Sydney to Canberra Canberra Junction to Melbourne

Newcastle to Sydney

Gold Coast Junction toNewcastle

Brisbane to Gold Coast

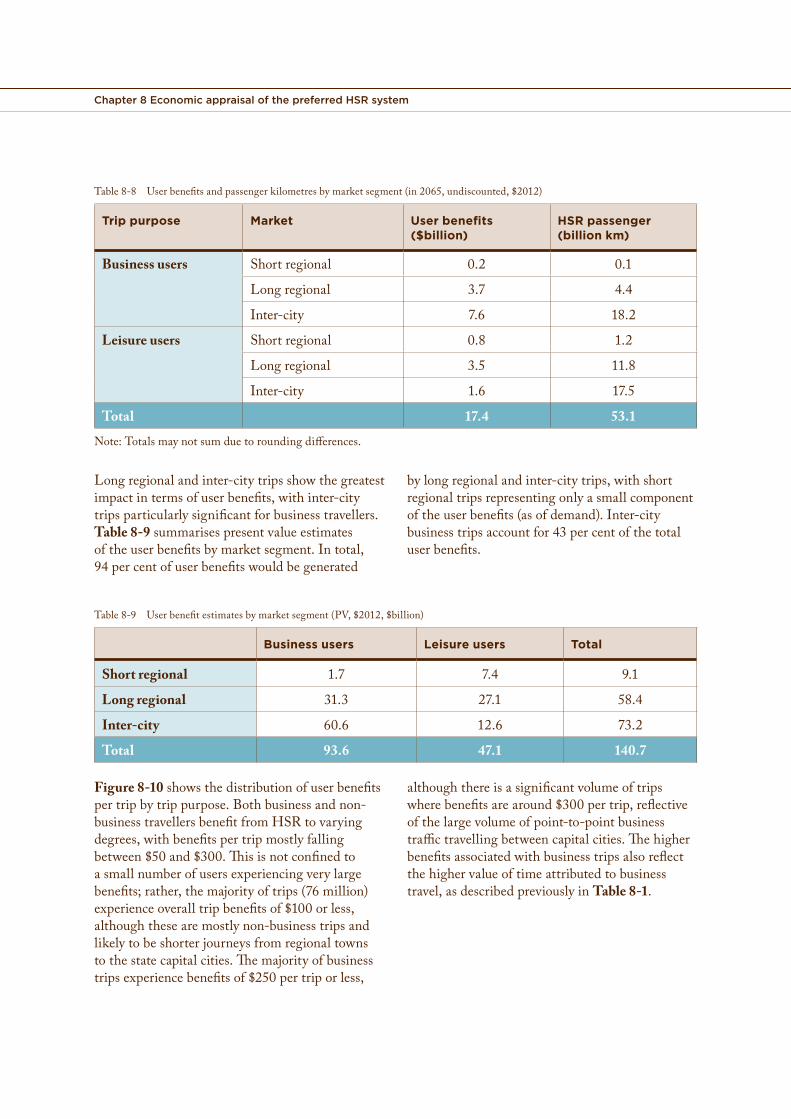

Analysis of user benefits by marketTable 8-8 provides an indicative assessment of the average user benefits by market segment. The data is based on 2065 estimates of demand and values of time that grow in line with GDP growth.

Chapter 8 Economic appraisal of the preferred HSR system

Table8-8 Userbenefitsandpassengerkilometresbymarketsegment(in2065,undiscounted,$2012)

Trip purpose Market User benefits ($billion)

HSR passenger (billion km)

Business users Shortregional 0.2 0.1

Longregional 3.7 4.4

Inter-city 7.6 18.2

Leisure users Shortregional 0.8 1.2

Longregional 3.5 11.8

Inter-city 1.6 17.5

Total 17.4 53.1

Note:Totalsmaynotsumduetoroundingdifferences.

Longregionalandinter-citytripsshowthegreatest bylongregionalandinter-citytrips,withshortimpactintermsofuserbenefits,withinter-city regionaltripsrepresentingonlyasmallcomponenttripsparticularlysignificantforbusinesstravellers. oftheuserbenefits(asofdemand).Inter-cityTable 8-9summarisespresentvalueestimates businesstripsaccountfor43percentofthetotaloftheuserbenefitsbymarketsegment.Intotal, userbenefits.94percentofuserbenefitswouldbegenerated

Table8-9 Userbenefitestimatesbymarketsegment(PV,$2012,$billion)

Business users Leisure users Total

Short regional 1.7 7.4 9.1

Long regional 31.3 27.1 58.4

Inter-city 60.6 12.6 73.2

Total 93.6 47.1 140.7

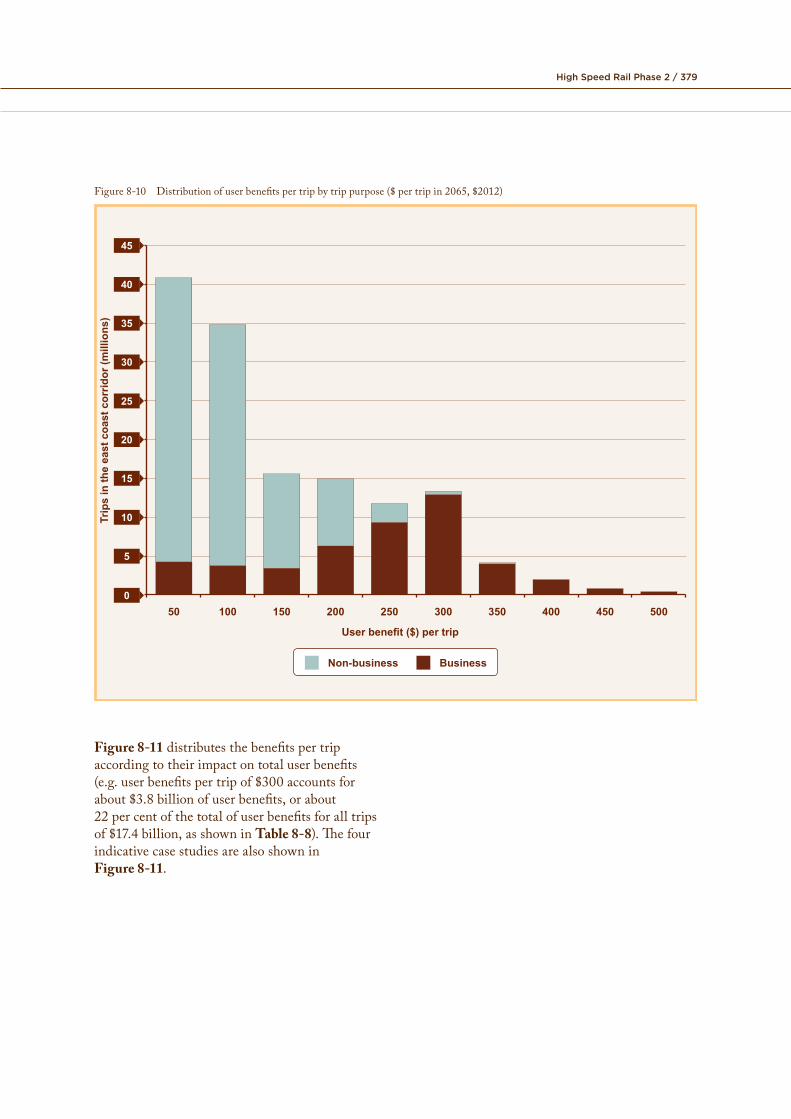

Figure 8-10showsthedistributionofuserbenefits althoughthereisasignificantvolumeoftripspertripbytrippurpose.Bothbusinessandnon- wherebenefitsarearound$300pertrip,reflectivebusinesstravellersbenefitfromHSRtovarying ofthelargevolumeofpoint-to-pointbusinessdegrees,withbenefitspertripmostlyfalling traffictravellingbetweencapitalcities.Thehigherbetween$50and$300.Thisisnotconfinedto benefitsassociatedwithbusinesstripsalsoreflectasmallnumberofusersexperiencingverylarge thehighervalueoftimeattributedtobusinessbenefits;rather,themajorityoftrips(76million) travel,asdescribedpreviouslyinTable 8-1.experienceoveralltripbenefitsof$100orless,althoughthesearemostlynon-businesstripsandlikelytobeshorterjourneysfromregionaltownstothestatecapitalcities.Themajorityofbusinesstripsexperiencebenefitsof$250pertriporless,

High Speed Rail Phase 2 / 379

Figure 8-10 Distribution of user benefits per trip by trip purpose ($ per trip in 2065, $2012)

Trip

s in

the

east

coa

st c

orrid

or (m

illio

ns)

0

5

10

15

20

25

30

35

40

45

50 100 150 200 250 300 350 400 450 500

Non-business Business

User benefit ($) per trip

Figure 8-11 distributes the benefits per trip according to their impact on total user benefits (e.g. user benefits per trip of $300 accounts for about $3.8 billion of user benefits, or about 22 per cent of the total of user benefits for all trips of $17.4 billion, as shown in Table 8-8). The four indicative case studies are also shown in Figure 8-11.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-11 Distribution of user benefits per trip by total impact on user benefits (in 2065, $2012)

Use

r ben

efits

($ m

illio

n)

User benefit ($) per trip

0

500

1000

1500

2000

2500

3000

3500

4000

4500

50 100 150 200 250 300 350 400 450 500

Non-business Business

Case study 4

Case study 2

Case studies 1 and 3

Comparison with the ‘rule of a half’The benefits associated with new users of transport improvements are generally calculated using the economic ‘rule of a half ’. For example, if a new line is being added to an urban metro network, benefits will arise through travellers experiencing shorter journey times and less crowding on the train and at stations. These benefits will result in extra passengers using the service. The rule of a half states that the benefit accruing to diverted or new users of a transport system is on average half of that accruing to the pre-existing users.

The rule of a half involves a simplifying assumption that the shape of the demand curve is linear. For the HSR benefit estimates, the calculation of induced travel benefits does not

make the simplifying assumption (for details, see Appendix 1E), but it has been confirmed that the two methods give almost identical benefit estimates.

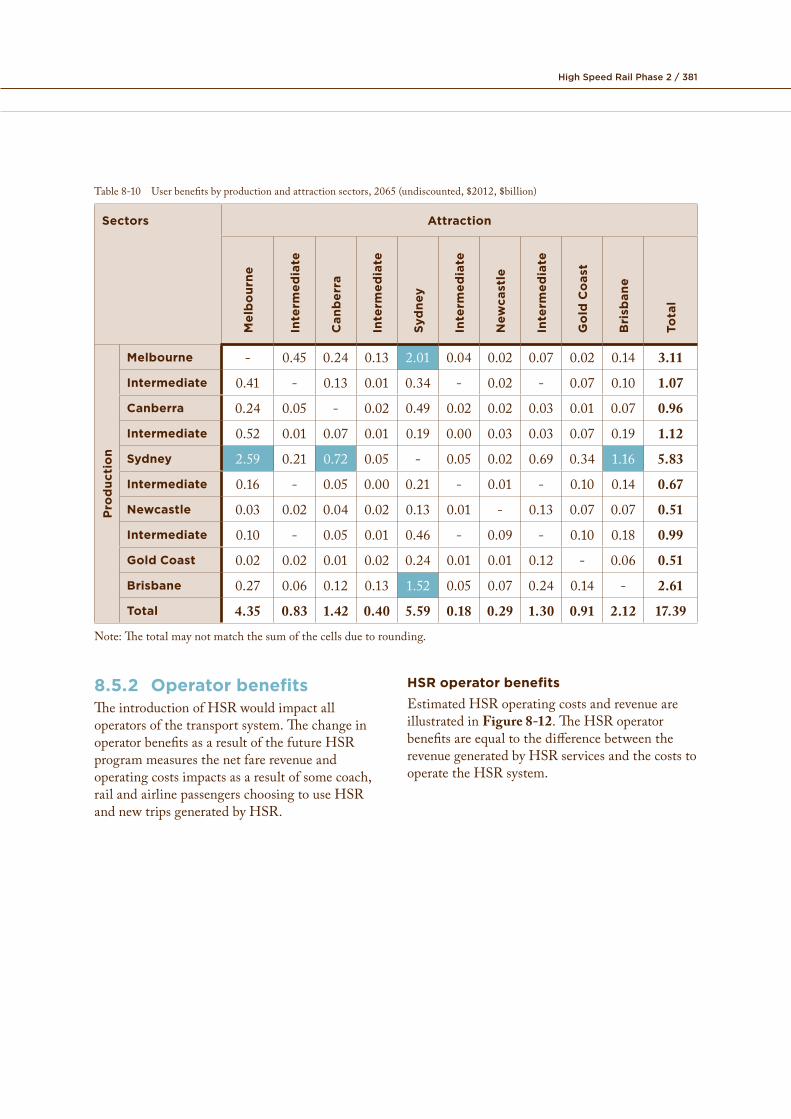

Geographic incidence of user benefitsThe majority of user benefits accrue to trips to/from NSW locations, with over 60 per cent of all benefits in 2065 involving a journey with an origin or destination in NSW. Table 8-10 presents the total user benefits (in 2065) between the trip production and attraction locations. The estimated top five journeys for scale of user benefits are Sydney-Melbourne, Melbourne-Sydney, Brisbane-Sydney, Sydney-Brisbane, and Sydney-Canberra. These are highlighted in the table.

High Speed Rail Phase 2 / 381

Table8-10 Userbenefitsbyproductionandattractionsectors,2065(undiscounted,$2012,$billion)

Sectors Attraction

Mel

bo

urne

Inte

rmed

iate

Can

ber

ra

Inte

rmed

iate

Syd

ney

Inte

rmed

iate

New

cast

le

Inte

rmed

iate

Go

ld C

oas

t

Bri

sban

e

Tota

l

Melbourne - 0.45 0.24 0.13 2.01 0.04 0.02 0.07 0.02 0.14 3.11

Intermediate 0.41 - 0.13 0.01 0.34 - 0.02 - 0.07 0.10 1.07

Canberra 0.24 0.05 - 0.02 0.49 0.02 0.02 0.03 0.01 0.07 0.96

Intermediate 0.52 0.01 0.07 0.01 0.19 0.00 0.03 0.03 0.07 0.19 1.12

tio

n Sydney 2.59 0.21 0.72 0.05 - 0.05 0.02 0.69 0.34 1.16 5.83

Pro

duc Intermediate 0.16 - 0.05 0.00 0.21 - 0.01 - 0.10 0.14 0.67

Newcastle 0.03 0.02 0.04 0.02 0.13 0.01 - 0.13 0.07 0.07 0.51

Intermediate 0.10 - 0.05 0.01 0.46 - 0.09 - 0.10 0.18 0.99

Gold Coast 0.02 0.02 0.01 0.02 0.24 0.01 0.01 0.12 - 0.06 0.51

Brisbane 0.27 0.06 0.12 0.13 1.52 0.05 0.07 0.24 0.14 - 2.61

Total 4.35 0.83 1.42 0.40 5.59 0.18 0.29 1.30 0.91 2.12 17.39

Note:Thetotalmaynotmatchthesumofthecellsduetorounding.

8.5.2 Operator benefitsTheintroductionofHSRwouldimpactalloperatorsofthetransportsystem.ThechangeinoperatorbenefitsasaresultofthefutureHSRprogrammeasuresthenetfarerevenueandoperatingcostsimpactsasaresultofsomecoach,railandairlinepassengerschoosingtouseHSRandnewtripsgeneratedbyHSR.

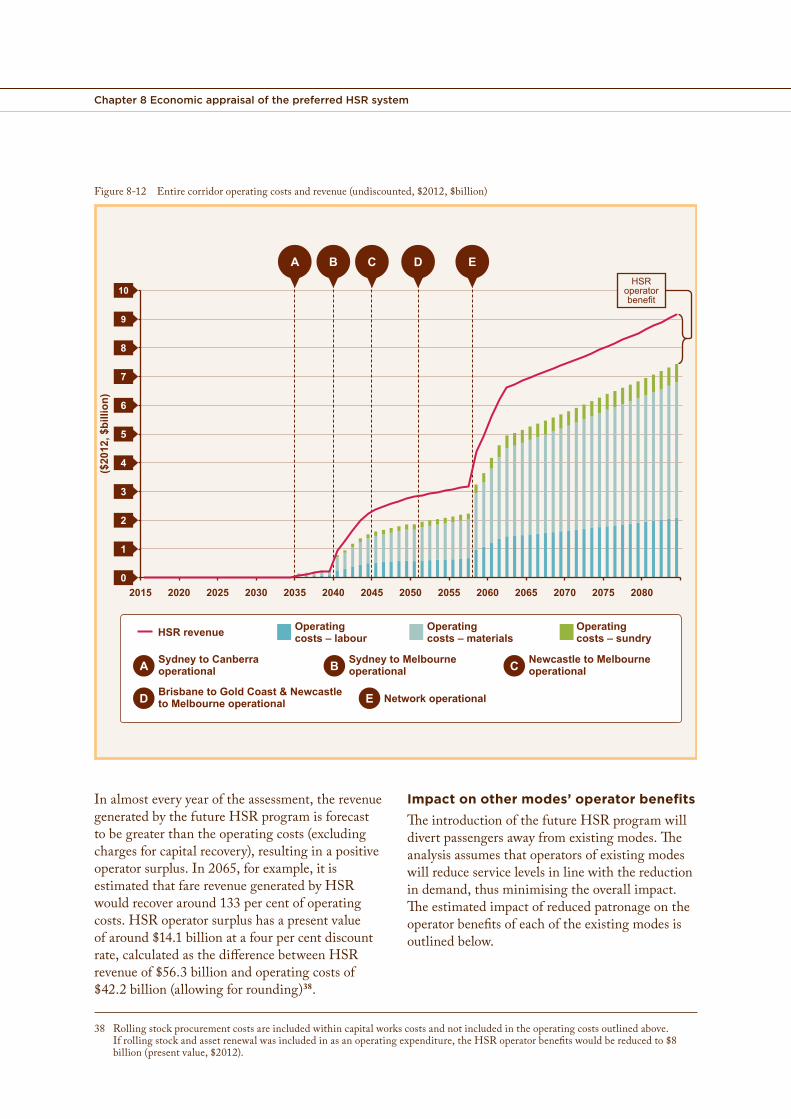

HSR operator benefitsEstimatedHSRoperatingcostsandrevenueareillustratedinFigure 8-12.TheHSRoperatorbenefitsareequaltothedifferencebetweentherevenuegeneratedbyHSRservicesandthecoststooperatetheHSRsystem.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-12 Entire corridor operating costs and revenue (undiscounted, $2012, $billion)

0

2

1

4

3

6

5

8

7

10

9

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

HSR operator benefit

($20

12, $

billi

on)

Operating costs – sundryHSR Revenue Operating costs – materials

Operating costs – labourSydney to Canberra operational

Sydney to Melbourne operational

Newcastle to Melbourne operational

Brisbane to Gold Coast & Newcastle to Melbourne operational Network operational

A B C

D E

A B C D E

Operating costs – labour

Operating costs – materials

Operating costs – sundryHSR revenue

In almost every year of the assessment, the revenue generated by the future HSR program is forecast to be greater than the operating costs (excluding charges for capital recovery), resulting in a positive operator surplus. In 2065, for example, it is estimated that fare revenue generated by HSR would recover around 133 per cent of operating costs. HSR operator surplus has a present value of around $14.1 billion at a four per cent discount rate, calculated as the difference between HSR revenue of $56.3 billion and operating costs of $42.2 billion (allowing for rounding)38.

Impact on other modes’ operator benefitsThe introduction of the future HSR program will divert passengers away from existing modes. The analysis assumes that operators of existing modes will reduce service levels in line with the reduction in demand, thus minimising the overall impact. The estimated impact of reduced patronage on the operator benefits of each of the existing modes is outlined below.

38 Rolling stock procurement costs are included within capital works costs and not included in the operating costs outlined above. If rolling stock and asset renewal was included in as an operating expenditure, the HSR operator benefits would be reduced to $8 billion (present value, $2012).

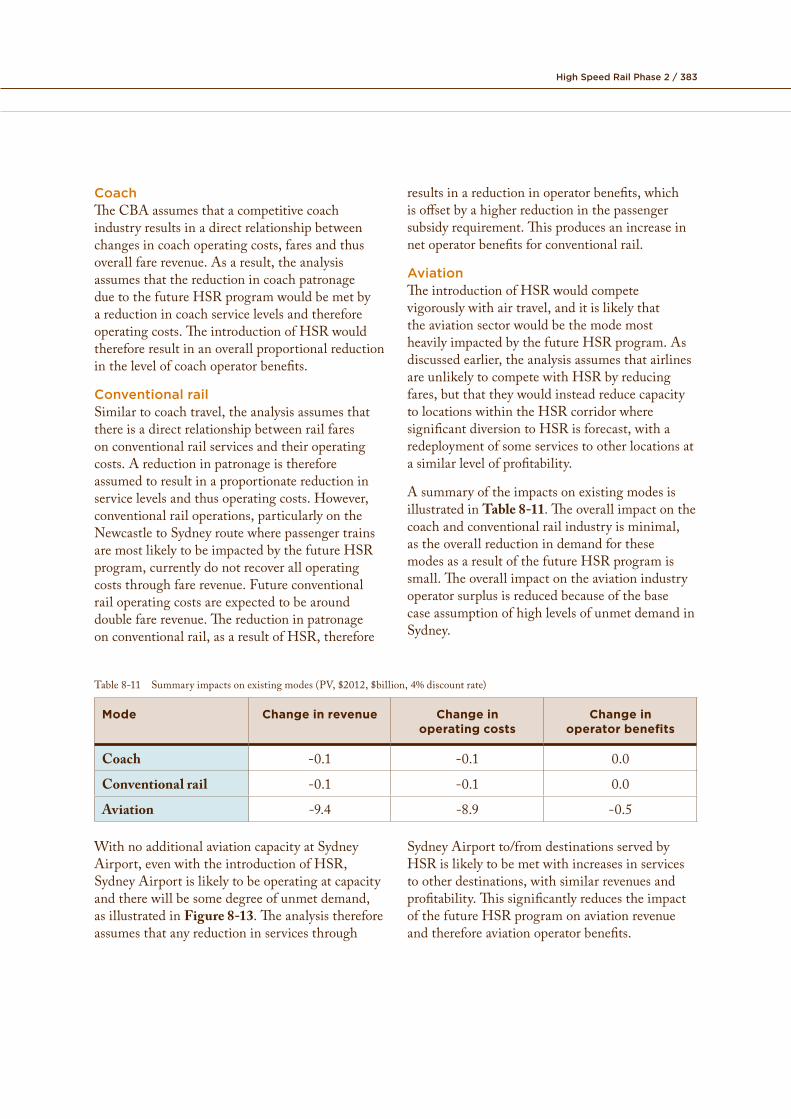

High Speed Rail Phase 2 / 383

CoachTheCBAassumesthatacompetitivecoachindustryresultsinadirectrelationshipbetweenchangesincoachoperatingcosts,faresandthusoverallfarerevenue.Asaresult,theanalysisassumesthatthereductionincoachpatronageduetothefutureHSRprogramwouldbemetbyareductionincoachservicelevelsandthereforeoperatingcosts.TheintroductionofHSRwouldthereforeresultinanoverallproportionalreductioninthelevelofcoachoperatorbenefits.

Conventional railSimilartocoachtravel,theanalysisassumesthatthereisadirectrelationshipbetweenrailfaresonconventionalrailservicesandtheiroperatingcosts.Areductioninpatronageisthereforeassumedtoresultinaproportionatereductioninservicelevelsandthusoperatingcosts.However,conventionalrailoperations,particularlyontheNewcastletoSydneyroutewherepassengertrainsaremostlikelytobeimpactedbythefutureHSRprogram,currentlydonotrecoveralloperatingcoststhroughfarerevenue.Futureconventionalrailoperatingcostsareexpectedtobearounddoublefarerevenue.Thereductioninpatronageonconventionalrail,asaresultofHSR,therefore

resultsinareductioninoperatorbenefits,whichisoffsetbyahigherreductioninthepassengersubsidyrequirement.Thisproducesanincreaseinnetoperatorbenefitsforconventionalrail.

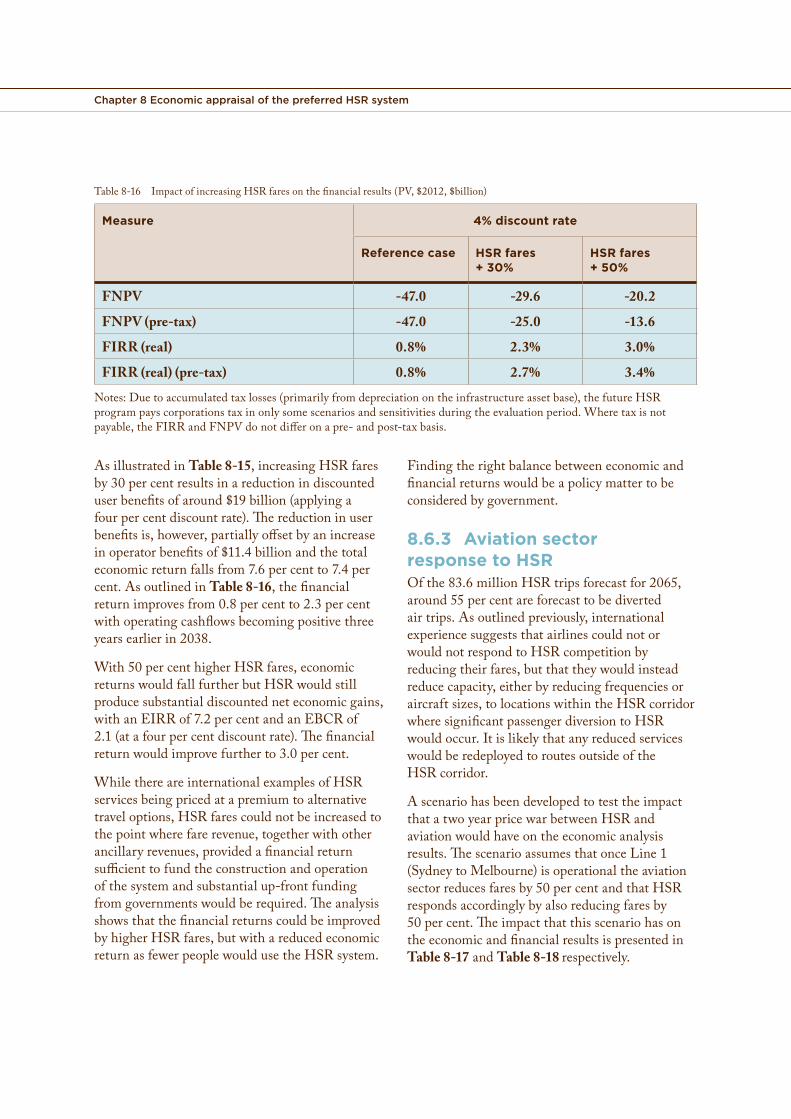

AviationTheintroductionofHSRwouldcompetevigorouslywithairtravel,anditislikelythattheaviationsectorwouldbethemodemostheavilyimpactedbythefutureHSRprogram.Asdiscussedearlier,theanalysisassumesthatairlinesareunlikelytocompetewithHSRbyreducingfares,butthattheywouldinsteadreducecapacitytolocationswithintheHSRcorridorwheresignificantdiversiontoHSRisforecast,witharedeploymentofsomeservicestootherlocationsatasimilarlevelofprofitability.

AsummaryoftheimpactsonexistingmodesisillustratedinTable 8-11.Theoverallimpactonthecoachandconventionalrailindustryisminimal,astheoverallreductionindemandforthesemodesasaresultofthefutureHSRprogramissmall.TheoverallimpactontheaviationindustryoperatorsurplusisreducedbecauseofthebasecaseassumptionofhighlevelsofunmetdemandinSydney.

Table8-11 Summaryimpactsonexistingmodes(PV,$2012,$billion,4%discountrate)

Mode Change in revenue Change in operating costs

Change in operator benefits

Coach -0.1 -0.1 0.0

Conventional rail -0.1 -0.1 0.0

Aviation -9.4 -8.9 -0.5

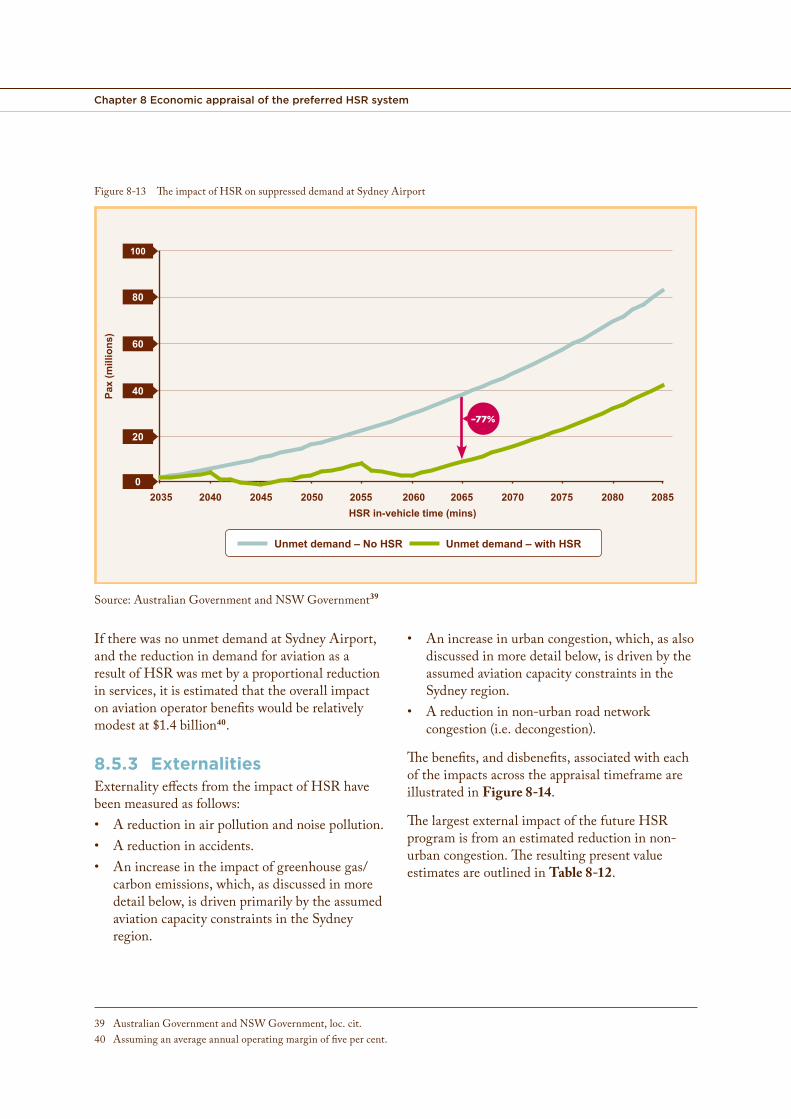

WithnoadditionalaviationcapacityatSydney SydneyAirportto/fromdestinationsservedbyAirport,evenwiththeintroductionofHSR, HSRislikelytobemetwithincreasesinservicesSydneyAirportislikelytobeoperatingatcapacity tootherdestinations,withsimilarrevenuesandandtherewillbesomedegreeofunmetdemand, profitability.ThissignificantlyreducestheimpactasillustratedinFigure 8-13.Theanalysistherefore ofthefutureHSRprogramonaviationrevenueassumesthatanyreductioninservicesthrough andthereforeaviationoperatorbenefits.

Chapter 8 Economic appraisal of the preferred HSR system

Figure 8-13 The impact of HSR on suppressed demand at Sydney Airport

0

20

40

60

80

100

–77%

HSR in-vehicle time (mins)

Pax

(mill

ions

)

2035 2040 2045 2050 2055 2060 2065 2070 2075 2080 2085

Unmet demand – No HSR Unmet demand – with HSR

Source: Australian Government and NSW Government39

If there was no unmet demand at Sydney Airport, and the reduction in demand for aviation as a result of HSR was met by a proportional reduction in services, it is estimated that the overall impact on aviation operator benefits would be relatively modest at $1.4 billion40.

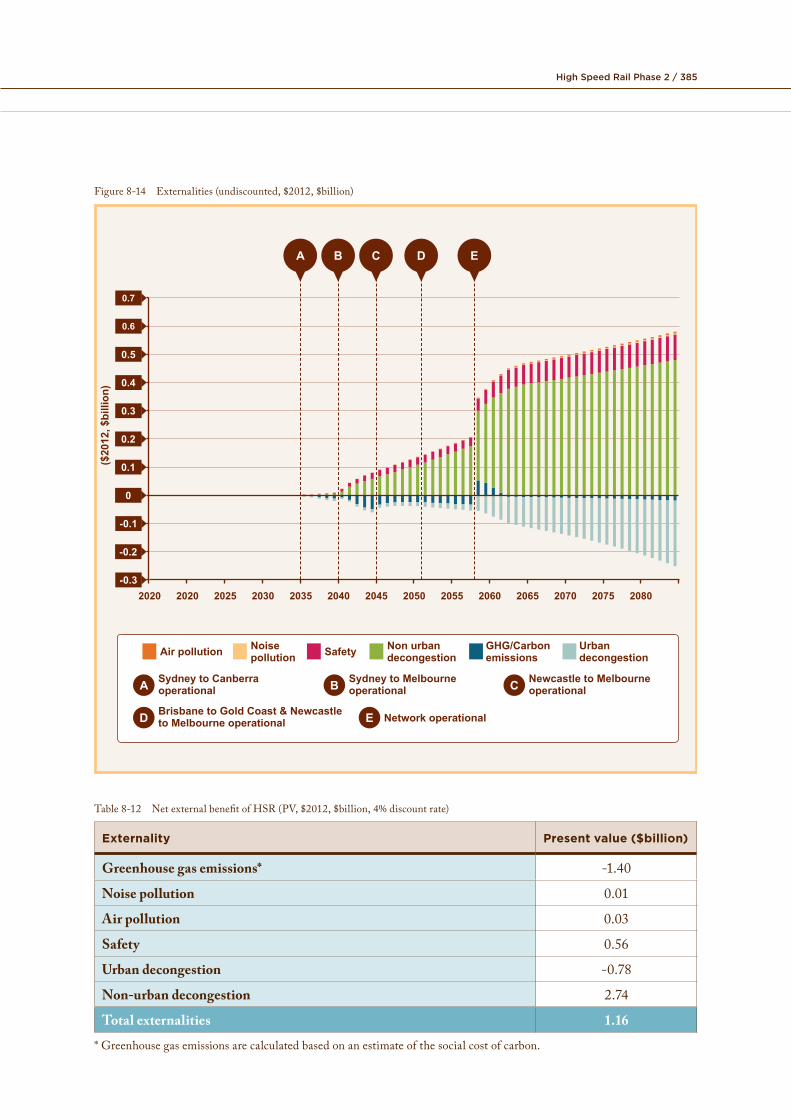

8.5.3 ExternalitiesExternality effects from the impact of HSR have been measured as follows:• A reduction in air pollution and noise pollution.• A reduction in accidents.• An increase in the impact of greenhouse gas/

carbon emissions, which, as discussed in more detail below, is driven primarily by the assumed aviation capacity constraints in the Sydney region.

• An increase in urban congestion, which, as also discussed in more detail below, is driven by the assumed aviation capacity constraints in the Sydney region.

• A reduction in non-urban road network congestion (i.e. decongestion).

The benefits, and disbenefits, associated with each of the impacts across the appraisal timeframe are illustrated in Figure 8-14.

The largest external impact of the future HSR program is from an estimated reduction in non-urban congestion. The resulting present value estimates are outlined in Table 8-12.

39 Australian Government and NSW Government, loc. cit.40 Assuming an average annual operating margin of five per cent.

High Speed Rail Phase 2 / 385

Figure 8-14 Externalities (undiscounted, $2012, $billion)

-0.2

-0.3

0.1

0

-0.1

0.3

0.2

0.5

0.4

0.7

0.6

20202020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080

($20

12, $

billi

on)

Operating costs – sundryHSR Revenue Operating costs – materials

Operating costs – labourSydney to Canberra operational

Sydney to Melbourne operational

Newcastle to Melbourne operational

Brisbane to Gold Coast & Newcastle to Melbourne operational Network operational

A B C

D E

A B C D E

Noise pollutionAir pollution Non urban

decongestionSafety Urban decongestion

GHG/Carbon emissions

Table 8-12 Net external benefit of HSR (PV, $2012, $billion, 4% discount rate)

Externality Present value ($billion)

Greenhouse gas emissions* -1.40

Noise pollution 0.01

Air pollution 0.03

Safety 0.56

Urban decongestion -0.78

Non-urban decongestion 2.74

Total externalities 1.16

* Greenhouse gas emissions are calculated based on an estimate of the social cost of carbon.

Chapter 8 Economic appraisal of the preferred HSR system

Eachcategoryofexternalitiesisdiscussedfurtherbelow.

Environmental impactsHighspeedrailproduceslessgreenhousegasemissionsforagiventransporttaskthanexistingtransportmodes,particularlyaviation41.Asaresult,ashiftindemandforHSRawayfromexistingmodeswouldresultinanetreductioningreenhousegasemissions,otherthingsbeingequal,andwouldgenerateabenefitofaround$2 billionovertheappraisaltimeframe42.

However,theassumptionregardingnonewcapacityatSydneyairportmakestheassessmentmorecomplex.Asdiscussedpreviously,thereferencecaseassumestherearehighlevelsofunmetaviationdemandatSydneyAirport.Thestudythereforeassumesthatanyreductioninaviationtripsto/fromSydneyduetotheintroductionofHSRwouldbemetbyanincreaseinaviationservicesto/fromdestinationsoutsidetheHSRcorridorwhichwaspreviouslyunmetduetoalackofcapacityatSydneyAirport.ThisadditionaltravelgeneratesadditionalgreenhousegasemissionswhichoffsettheenvironmentalbenefitsofashiftintravelfromaviationtoHSR,andresultsinanetincreaseingreenhousegasemissionsandapresentvaluedisbenefitofaround$1.4billionovertheappraisaltimeframe.

TheimpactofthefutureHSRprogramonairpollutionandnoisepollutionisrelativelyminimal,generatinganestimatedpresentvaluenetbenefitof$29millionfromreducedairpollutionand$13 millionfromreducednoisepollution.

DecongestionAfutureHSRprogramwouldleadtoareductioninurbanmotortrafficbyservingthecitycentre,whichistheultimatedestinationformanytravellers(whowouldnolongerneedtotraveltherefromtheairport;insteadtheirtripwouldconsistofHSRpluspublictransportorashort

taxiride).Itwouldalsodiverttravelfromcars(whosejourneysincludeanurbancomponent)toHSRpluspublictransport.Thereductioninurbancartravelislikelytoresultinareductionincongestion.However,theassumptionregardingaviationcapacityinSydneygeneratesadditionalurbancartravelforthosetravellersaccessingtheairportthatpreviouslycouldnottravel.Whenthisadditionaltravelistakenintoconsiderationthereisanetincreaseinurbancartravelandthusanetincreaseincongestion,whichrepresentsapresentvaluedisbenefitofaround$783millionovertheappraisaltimeframe.

Thedecongestionimpactswereestimatedbasedonanassessmentoftheimpactthatthereductioninurbanmotortrafficwouldhaveonthetravelenvironmentforremainingusers.Allowancewasmadeforgeneratedmotortrafficassociatedwithprovidingaccessto/fromurbanHSRstations.Non-urbanroaddecongestionhasbeenassessedinasimilarway,byconsideringtheimpactthatareductioninnon-urbanmotortraffic,generatedasaresultofcaruserstransferringtoHSR,wouldhaveonremainingusersoftheroadnetwork.Theexpectedpresentvaluebenefitfromnon-urbandecongestionis$2.7billionovertheappraisal timeframe.

8.5.4 Residual valueAsmentionedpreviously,aresidualvaluehasbeenincludedtocapturetheremainingvalueoftheinvestmentinHSRbeyond2085.Theresidualvaluehasbeenestimatedbasedonvalue-in-use,i.e.thediscountedvalueofexpectednetbenefitsbeyond2085to210843,lessanannuityvalueforcapitalmaintenance.TheresidualvalueofHSRisestimatedtobe$25.0billion,representingaround14percentofthetotalbenefits.By2085thepopulationalongtheeastcoastofAustraliaisestimatedtobeover30millionwhichdrivessignificantlevelsofdemandforHSRandhencehighuserbenefitsandrevenueandarelativelylargeresidualvalue.

41 AsdiscussedinmoredetailinAppendix 5G,theaveragecostimpactpertonneofcarbonistwotimeshigherforaviationbecauseairlinesemitmostoftheirgreenhousegasesdirectlyintotheupperatmosphere.

42 The$2billiondiscountedbenefitovertheappraisaltimeframealsotakesintoaccounttheadditionalgreenhousegasemissionsassociatedwithinduceddemandforHSR.

43 Representing50yearsfromwhenoperationsofthelastsegmentcommence(i.e.2058).

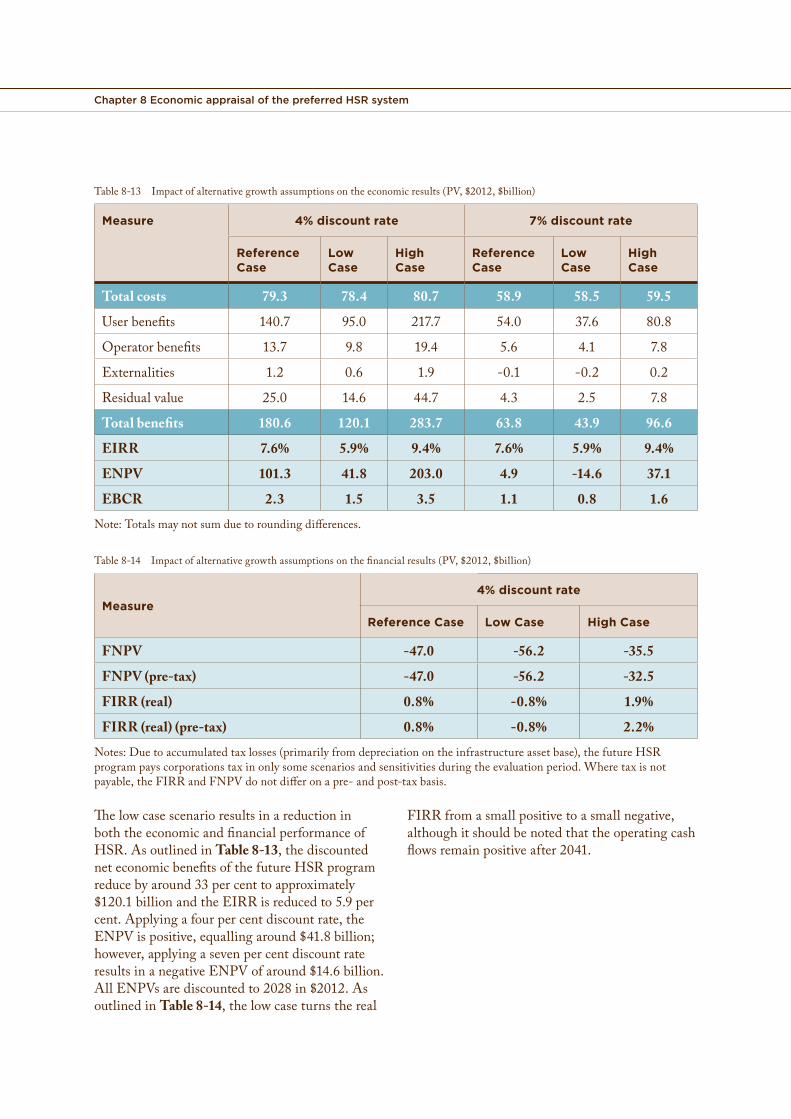

High Speed Rail Phase 2 / 387

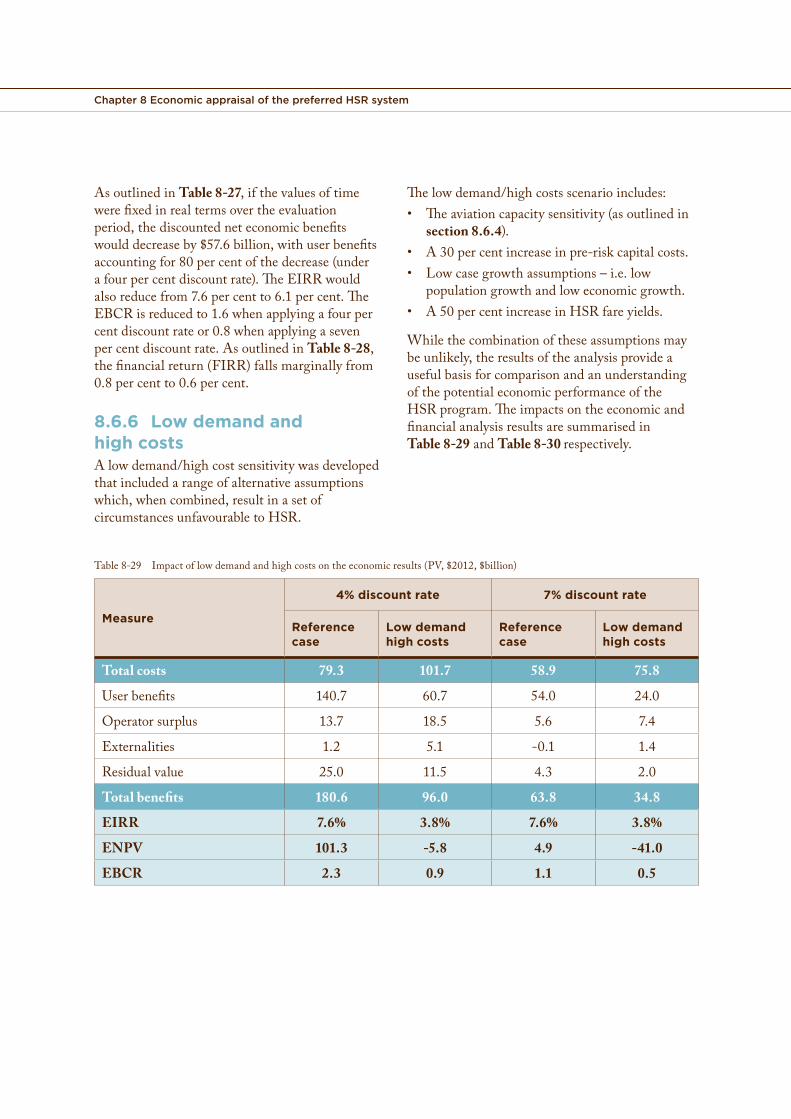

8.6 Sensitivity to alternative assumptionsTheresultsoftheanalysispresentapositiveeconomiccasefortheintroductionofthefutureHSRprogramandreflectanumberofimportantassumptionsandexpectations:• Stronggrowthinthebasetravelmarketover

theperiodbeforetheHSRprogrambecomesfullyoperational(travelontheeastcoastwillhavemorethandoubledfromexistinglevelsofaround152milliontripsto355milliontripsin206544)placingsignificantpressureonbase-casetransportnetworksthatwouldrelymainlyonaviationandprivatecar.

• HSRfareswouldbestructuredtobecompetitivewithalternativemodesoftransportforbothbusinessandleisurepurposes.HSRfareshavebeensettobecompetitivewithandcomparabletoairfaresonthemaininter-capitalroutesontheeastcoastandtoremainconstantafter2035.

• NoadditionalaviationcapacityintheSydneybasin,whichhastheeffectofincreasingdelayandthecostofairfares,generatinghighlevelsofunmetdemandforaviationtravel.

• Airlineservicesaremobileinthesensethatthereafewsignificantsunkcapitalcostsinservicingparticularroutes,andassetscanbereadilyredeployedtootherroutes.Inlinewithinternationalexperience,itisassumedthatairlineswouldadjustcapacitywithintheHSRcorridorratherthanreducepriceinresponsetotheintroductionofHSR.

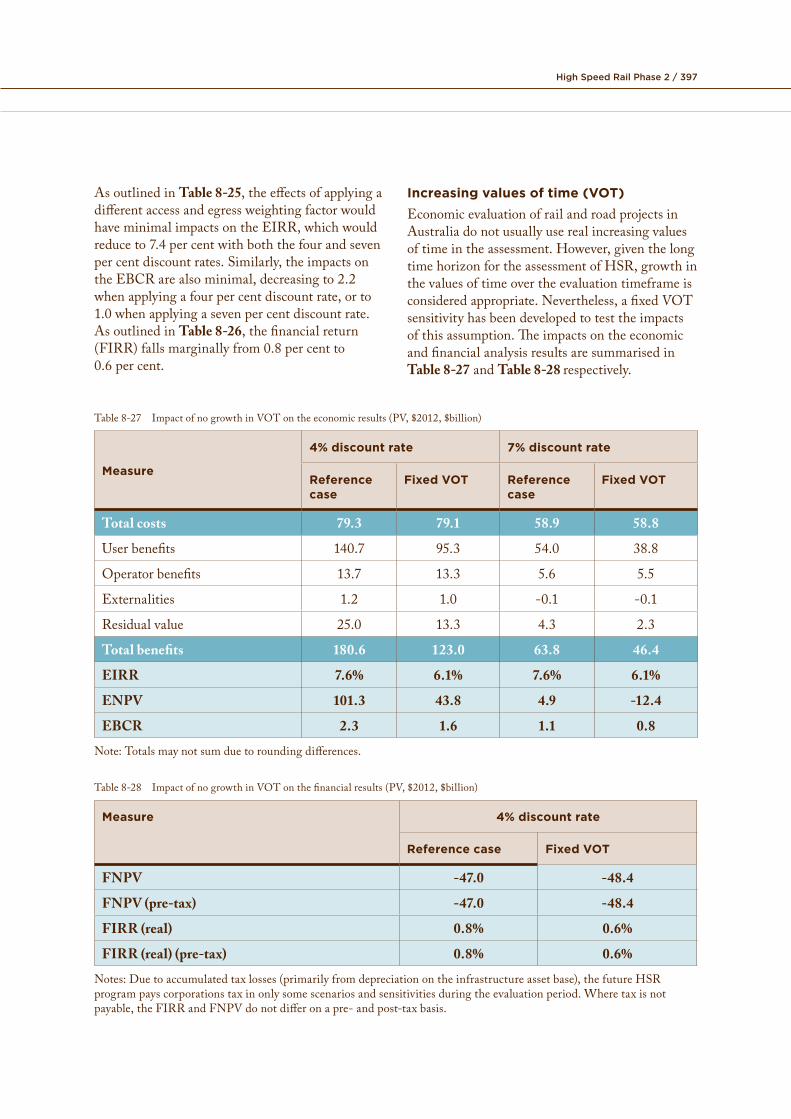

Theimpactsoftheseassumptionsontheresultsoftheeconomicanalysisaretestedinthescenariosandsensitivitiespresentedinthissection.ImplicationsforthefinancialresultspresentedinChapter 7arealsotested.FurtheranalysisispresentedinAppendix 5B andAppendix 6B.

Inaddition,givenitiscustomarytoincludefactorsinthedemandmodellingsuchastheAlternativeSpecificConstant(ASC)andegress/accessweightswhichmayfavourafutureHSRmarketshare,

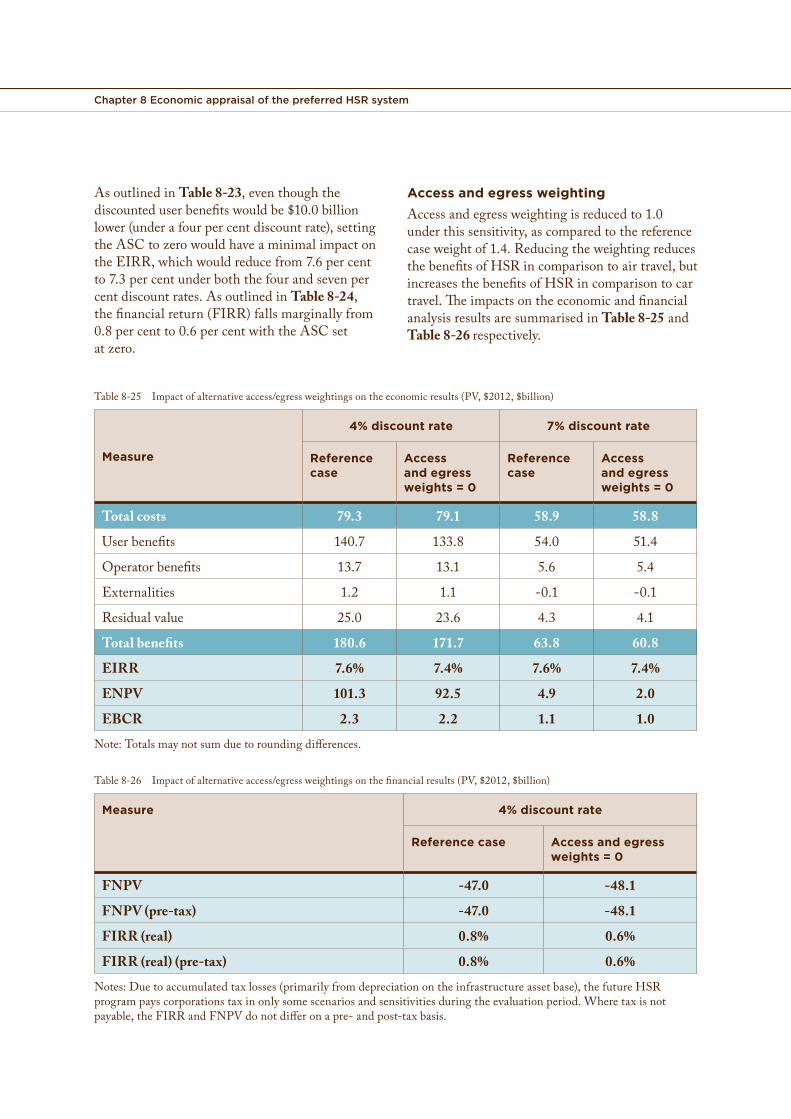

sensitivitytestingincludedtwoscenariostoexploretheimpactthatremovingtheseassumptionshasontheresults.

8.6.1 Impact of future growthAsmentionedabove,travelontheeastcoastofAustraliaisforecasttomorethandoublefromexistinglevelstoaround355milliontripsby2065.Populationandeconomicgrowtharetwokeydriversofdemandfortransport.Thepopulationandeconomicgrowthassumptionsappliedintheanalysishavebeendevelopedtorepresentthe‘mostlikely’case45.However,giventhelongtimeframefortheanalysis,thereisthepossibilitythatadifferentoutcomecouldprevail.LowandhighgrowthscenarioshavebeendevelopedtoexploretheimpactthatalternativegrowthassumptionsmayhaveontheeconomiccaseforHSR.

• The‘lowgrowth’scenarioassumesslowereconomicandpopulationgrowth(relativetothereferencecase).ThisscenarioresultsinloweroveralldemandfortransportandthuslowerdemandforHSR.PercapitaGDPgrowthratesareassumedtobe0.3percentperyearlowerthanthereferencecase,andpopulationgrowthisassumedtobe51percentbetween2010and2065,comparedto72percentinthereferencecase.

• The‘highgrowth’scenarioassumesthattheAustralianeconomyexperiencesstrongergrowthintothefuture,withhighpopulationgrowth.ThisscenarioresultsinhigheroveralldemandfortransportandthushigherdemandforHSR.PercapitaGDPgrowthratesareassumedtobe0.3percentperyearhigherthaninthereferencecase,andpopulationgrowthisassumedtobe103 percentbetween2010and2065,comparedto72percentinthereferencecase.

TheimpactsofthealternativegrowthscenariosontheeconomicresultsarepresentedinTable 8-13usingbothfourpercentandsevenpercentdiscountrates.Table 8-14 summarisestheimpactsofthealternativegrowthscenariosonthefinancialresultsusingafourpercentdiscountrate.

44 SeeChapter 2foradiscussionoftherelevantmarketandexpectedgrowth.45 FuturepopulationgrowthissourcedfromtheABSPopulationProjections(SeriesB)CatalogueNumber3222.0.TheGDP

projectionsarebasedonthesamemethodologyasusedintheAustralianGovernment’sIGR.Thatis,long-termprojectionsofeconomicgrowthtakecurrenteconomicconditionsandeconomicforecastsasabase.Trendgrowthratesoverthelongertermareafunctionofpopulation,productivityandparticipation(the3Psframework).

Chapter 8 Economic appraisal of the preferred HSR system

Table8-13 Impactofalternativegrowthassumptionsontheeconomicresults(PV,$2012,$billion)

Measure 4% discount rate 7% discount rate

Reference Case

Low Case

High Case

Reference Case

Low Case

High Case

Total costs 79.3 78.4 80.7 58.9 58.5 59.5

Userbenefits 140.7 95.0 217.7 54.0 37.6 80.8

Operatorbenefits 13.7 9.8 19.4 5.6 4.1 7.8

Externalities 1.2 0.6 1.9 -0.1 -0.2 0.2

Residualvalue 25.0 14.6 44.7 4.3 2.5 7.8

Total benefits 180.6 120.1 283.7 63.8 43.9 96.6

EIRR 7.6% 5.9% 9.4% 7.6% 5.9% 9.4%

ENPV 101.3 41.8 203.0 4.9 -14.6 37.1

EBCR 2.3 1.5 3.5 1.1 0.8 1.6

Note:Totalsmaynotsumduetoroundingdifferences.

Table8-14 Impactofalternativegrowthassumptionsonthefinancialresults(PV,$2012,$billion)

Measure4% discount rate

Reference Case Low Case High Case

FNPV -47.0 -56.2 -35.5

FNPV (pre-tax) -47.0 -56.2 -32.5

FIRR (real) 0.8% -0.8% 1.9%

FIRR (real) (pre-tax) 0.8% -0.8% 2.2%

Notes:Duetoaccumulatedtaxlosses(primarilyfromdepreciationontheinfrastructureassetbase),thefutureHSRprogrampayscorporationstaxinonlysomescenariosandsensitivitiesduringtheevaluationperiod.Wheretaxisnotpayable,theFIRRandFNPVdonotdifferonapre-andpost-taxbasis.

ThelowcasescenarioresultsinareductioninboththeeconomicandfinancialperformanceofHSR.AsoutlinedinTable 8-13,thediscountedneteconomicbenefitsofthefutureHSRprogramreducebyaround33 percenttoapproximately$120.1billionandtheEIRRisreducedto5.9percent.Applyingafourpercentdiscountrate,theENPVispositive,equallingaround$41.8billion;however,applyingasevenpercentdiscountrateresultsinanegativeENPVofaround$14.6billion.AllENPVsarediscountedto2028in$2012.AsoutlinedinTable 8-14,thelowcaseturnsthereal

FIRRfromasmallpositivetoasmallnegative,althoughitshouldbenotedthattheoperatingcashflowsremainpositiveafter2041.

High Speed Rail Phase 2 / 389

ThehighcasescenarioimprovesboththeeconomicandfinancialperformanceofHSR.AsoutlinedinTable 8-13,thehighcasescenarioincreasesthediscountedneteconomicbenefitsbyafactorof56 percentand,asaresult,theEIRRincreasesto9.4 percent.TheENPVisequallypositivebyapplyingafourpercentandsevenpercentdiscountrate,resultingin$203.0billionand$37.1 billionrespectively.AllENPVsarediscountedto2028in$2012.Similarly,asoutlinedinTable 8-14,thehighcaseonlymarginallyimprovestheoverallfinancialreturn(from0.8percentto1.9percent)andstillleavesitwellshortoftherequirementsofcommercialinvestors.

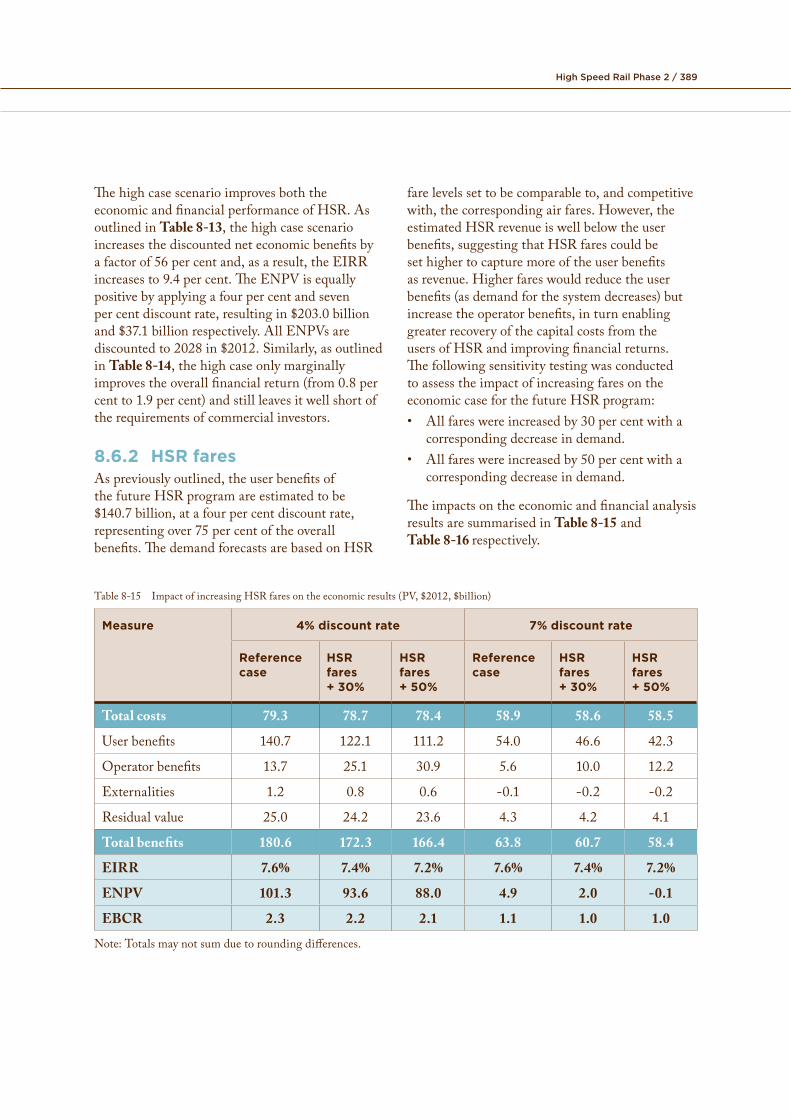

8.6.2 HSR faresAspreviouslyoutlined,theuserbenefitsofthefutureHSRprogramareestimatedtobe$140.7billion,atafourpercentdiscountrate,representingover75percentoftheoverallbenefits.ThedemandforecastsarebasedonHSR

farelevelssettobecomparableto,andcompetitivewith,thecorrespondingairfares.However,theestimatedHSRrevenueiswellbelowtheuserbenefits,suggestingthatHSRfarescouldbesethighertocapturemoreoftheuserbenefitsasrevenue.Higherfareswouldreducetheuserbenefits(asdemandforthesystemdecreases)butincreasetheoperatorbenefits,inturnenablinggreaterrecoveryofthecapitalcostsfromtheusersofHSRandimprovingfinancialreturns.ThefollowingsensitivitytestingwasconductedtoassesstheimpactofincreasingfaresontheeconomiccaseforthefutureHSRprogram:• Allfareswereincreasedby30percentwitha

correspondingdecreaseindemand.• Allfareswereincreasedby50percentwitha

correspondingdecreaseindemand.

TheimpactsontheeconomicandfinancialanalysisresultsaresummarisedinTable 8-15andTable 8-16 respectively.

Table8-15 ImpactofincreasingHSRfaresontheeconomicresults(PV,$2012,$billion)

Measure 4% discount rate 7% discount rate

Reference case

HSR fares + 30%

HSR fares + 50%

Reference case

HSR fares + 30%

HSR fares + 50%

Total costs 79.3 78.7 78.4 58.9 58.6 58.5

Userbenefits 140.7 122.1 111.2 54.0 46.6 42.3

Operatorbenefits 13.7 25.1 30.9 5.6 10.0 12.2

Externalities 1.2 0.8 0.6 -0.1 -0.2 -0.2

Residualvalue 25.0 24.2 23.6 4.3 4.2 4.1

Total benefits 180.6 172.3 166.4 63.8 60.7 58.4

EIRR 7.6% 7.4% 7.2% 7.6% 7.4% 7.2%

ENPV 101.3 93.6 88.0 4.9 2.0 -0.1

EBCR 2.3 2.2 2.1 1.1 1.0 1.0

Note:Totalsmaynotsumduetoroundingdifferences.

Chapter 8 Economic appraisal of the preferred HSR system

Table8-16 ImpactofincreasingHSRfaresonthefinancialresults(PV,$2012,$billion)

Measure 4% discount rate

Reference case HSR fares + 30%

HSR fares + 50%

FNPV -47.0 -29.6 -20.2

FNPV (pre-tax) -47.0 -25.0 -13.6

FIRR (real) 0.8% 2.3% 3.0%

FIRR (real) (pre-tax) 0.8% 2.7% 3.4%