Embed Size (px)

Citation preview

Considerations for the Global Chemicals Industry Amid the COVID-19 Outbreak

April 2020

Introduction

2

Dear Clients and Friends,

Firstly, we hope this finds you and your families safe and well. We recognize that these are uncertain and

unprecedented times for you and your families, friends, colleagues, businesses, and investments. All of us are facing

unique challenges and threats in this new environment—some of you, quite acutely.

In recent weeks, markets have been facing significant volatility due to COVID-19 that is expected to continue for the

foreseeable future. Substantial disruptions to business operations, supply chains, demand, international trade flows,

and travel, along with lockdowns and collapsing stock prices have occurred—all resulting from the COVID-19

outbreak—and all sectors of the global economy have been impacted, including the chemicals sector.

What was a relatively benign low-growth, low-interest-rate environment before the outbreak has morphed into what is

expected to be a large-scale, negative-growth shock. Governments are trying to counter the impact by unprecedented

financial support programs (e.g. currently, the amount earmarked for cheap business loans and guarantees by

governments in the U.S., Britain, France, Germany, and Italy is at least $4 trillion, or a fifth of their outstanding non-

financial corporate debt).

The near-term outlook for the global chemical industry is deeply concerning, and uncertainty is likely to persist until the

duration and overall impact of COVID-19 can be determined. There is a glimmer of hope, however, as we see the

Chinese market getting back to operations and order volumes are selectively increasing again—keeping in mind that

China represents 30% of global petrochemicals production and 37% of the global demand, and that a 1% decline in

China GDP growth translates into c. 2.5mt lost base chemicals demand.(1)

At this point, it is impossible for us to know how long the outbreak and lockdown or the lingering effects on businesses,

the economy, and the credit and M&A markets, will last. However, we are hopeful that recent actions will have the

positive effect of “flattening the curve” for new cases in the short term and minimize the impact of business operations.

We understand the anxiety created by these uncertain times, and as COVID-19 and the resulting economic

consequences continue to evolve, we are here to share our perspective based on our real-time conversations with

industry executives and business owners across the chemicals industry as well as our comprehensive views on the

M&A and capital markets.

Even in far less trying times, our firm specializes in helping clients navigate change and uncertainty. We will continue

to be a sounding board for our clients and other market participants as we collectively assess opportunities and

challenges in the current environment. We bring to bear a broad range of product and service solutions across the

capital structures, and we stand ready to discuss the impact and potential opportunities created by this crisis on the

industry and your business.

Martin Bastian

Managing Director

+49 (0) 69 256 246 171

Leland Harrs

Managing Director

212.497.7842

Steve Wang

Senior Vice President

212.497.7807

Houlihan Lokey Chemicals Team Contacts

(1) IHS Markit

Market Update (1/2)

1. Weakness in key end markets, such as automotive, construction, and oil and gas, will increase over the next 12

months, driving low-capacity utilizations.

o The PMI indexes as of February/March 2020 of major geographic markets, as well as key chemicals end

markets, have fallen in the range of 20% to 50% since the beginning of 2020.

o February data signaled widespread disruption across sectors stemming from the COVID-19 outbreak.

Eight sectors posted the fastest falls in output on record during the month, since the global sector data

were first compiled in October 2009. Automobiles and auto parts, construction, metals and mining, and

chemicals registered the strongest rates of decline.

o This is also reflected in the respective share price developments of companies in the major end markets

(auto minus 26%, construction minus 37%, metals and mining minus 31%, industrial goods minus 26%,

chemicals minus 27%).

2. Chemical product supply chains are globally facing pressure. High volatility in inventory levels will filter through

to downstream chemicals over the next two quarters and beyond. Crisis planning has included inventory build-

up for raw materials that could experience supply chain interruptions from COVID-19.

o Manufacturers are taking actions to protect employees and ensure there is business continuity, while

distributors are realigning logistics and redirecting shipments towards key supply shortages for critical

product chains.

o Many of the chemical plants are still running, and white-collar employees operate remotely.

o For downstream chemicals companies, the disruption to global supply chains—notably from mainland

China and India—is expected to be a further catalyst to the trend toward relocating of fine chemicals

production.

3. Given the precipitous drop in oil prices and unprecedented oil supply surplus over the last few weeks, the

chemicals sector—in particular, the commodity chemicals companies—is facing a “double-whammy” impact to

valuation in line with the oil price drop (minus 59% since mid-February).

4. In the short term, the oil-price collapse is expected to trigger a sharp and broad decline in the prices of

petrochemicals, accentuating the recent trend.

o In Asia, naphtha prices hit 18-year lows, while paraxylene (PX) values reached levels not seen since

2008. A similar development has taken place in Europe and the U.S., where chemicals such as

ethylene, propylene, and toluene stand at lows not seen since 2008 or earlier.

o However, not every market is dropping; some raw materials that are key to fighting the pandemic (e.g.

masks, filters, disinfectants, microbial, etc.) are seeing high demand and thus higher prices.

o For example, isopropanol (IPA), a key component in the production of hand sanitizers, is in such high

demand that IPA prices in Europe and the U.S. have increased in recent weeks—doubling in some

instances.

o Several manufacturers have taken initiatives, are diverting workforce and production capacity to these

areas, and support local communities.

5. Estimates for the oil-supply surplus in the first half of 2020 are currently difficult to forecast and range from 770

million to 1.3 billion barrels. Even at the low end, this surplus is more than double the previous record-high

surplus of 320 million barrels in the first half of 2015, during the 2014–2015 oil-price collapse (while the global

oil demand was still increasing, not falling).(1)

(1) IHS Markit3

Based on multiple touchpoints with sector companies, industry consultants, and financial market sources, the

following summarizes some industry perspectives and key developments affecting companies and investors:

1

2

3

4

5

Market Update (2/2)

6. Monthly global oil demand from February through May is expected to be as much as 4 million to 10 million

barrels per day (c. 4%–10% of total daily demand) fewer than year-earlier levels.

o These will be the largest declines in oil demand ever.

o Immediate and steep production cuts and international collaboration are selectively taken to somewhat

mitigate the impact.

o In addition, capex budgets getting revisited and create additional uncertainty over medium-term demand.

o Regardless of potential benefits to the competitiveness of oil-derived products such as plastics and

synthetic fibers, it is also expected to lead to a short-term drop in chemical demand as companies

throughout the chain destock in anticipation of lower prices to come.

7. Since mid-February, share prices are down 8%–45%, whereas the commodity and catalyst chemicals stocks as

well as the more leveraged companies have been hit the hardest, and the more defensive subsegments like industrial gases or ingredients fared relatively better (commodity minus 38%, catalysts minus 36%, coatings minus 30%, diversified/industrial chemicals minus 34% vs. ingredients minus 19%, and industrial gases minus 25%). The impact of the COVID-19 outbreak has not yet been fully reflected in EBITDA estimate changes, with the largest earnings revisions to diversified/industrial chemicals and commodity chemicals companies.

8. So far, selective companies have announced cuts or postponements to dividends and share buy-backs. Many

companies have significantly cut back capex spending. However, few have stated exactly how much cash flow

they expect to burn.

o Companies are scenario testing adequacy of cash buffers and maximizing liquidity by drawing on lines

of credit and evaluating all cash outflows, including capital expenditure programs, labor costs, and debt

payments.

o Further, lack of vendor financing, unhedged FX risks, and unwinding factoring facilities (among others)

need to be taken into consideration as well.

9. Due to current market volatility, many opportunistic refinancing transactions have been shelved as issuers and

underwriters opt to wait to understand how the financial performance will be impacted and for stable markets.

o The direct lending community continues to be a focus as the syndicated market has seen an effective

shutdown.

o A limited number of unitranche providers will opportunistically invest in new companies with potential for

higher return over the long term.

10. Most private equity firms are foremost focused on their existing portfolio companies, while also seeking

opportunities to deploy significant dry powder in their funds to meet liquidity and balance-sheet needs and seek

value and dislocation opportunities.

11. Most of the M&A processes have been put on hold, and new launches have been postponed until there is more

visibility on the financial impact of the crisis as well as overall business performance and valuation levels.

o As valuations fall and capital gets pricier, we do expect a healthy pipeline of chemicals M&A, particularly

non-core and/or underperforming businesses

o Some (well-capitalized) companies are also expected to pursue takeovers—encouraged by

governments—which put the survival of foundering companies (and jobs) ahead of antitrust concerns.

4

6

7

8

9

10

11

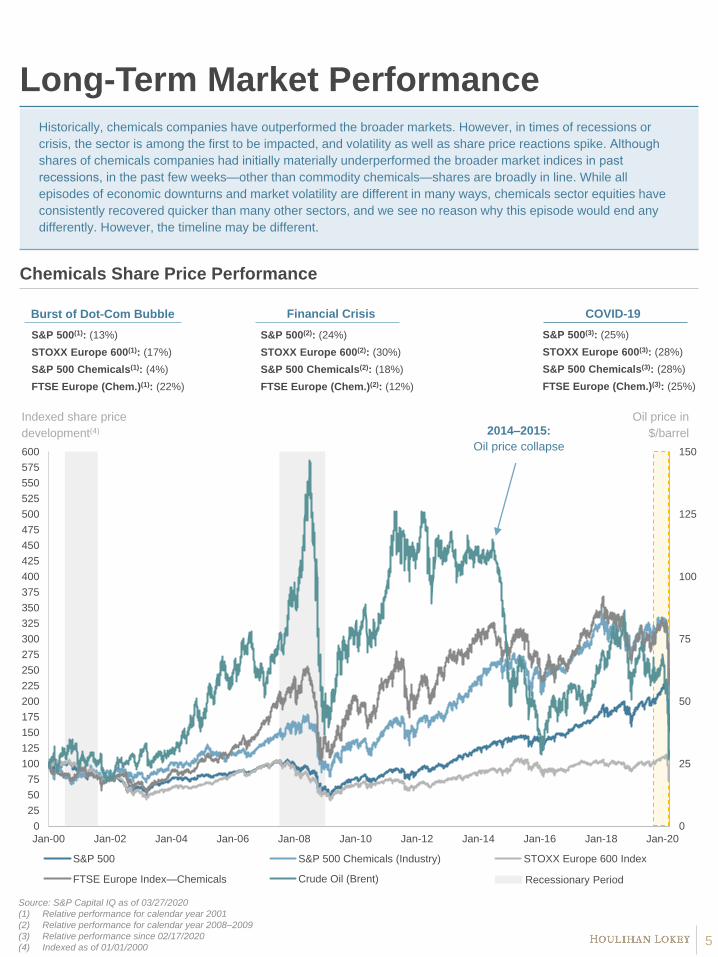

Long-Term Market Performance

Chemicals Share Price Performance

Source: S&P Capital IQ as of 03/27/2020

(1) Relative performance for calendar year 2001

(2) Relative performance for calendar year 2008–2009

(3) Relative performance since 02/17/2020

(4) Indexed as of 01/01/2000

Indexed share price

development(4)

Historically, chemicals companies have outperformed the broader markets. However, in times of recessions or

crisis, the sector is among the first to be impacted, and volatility as well as share price reactions spike. Although

shares of chemicals companies had initially materially underperformed the broader market indices in past recessions, in the past few weeks—other than commodity chemicals—shares are broadly in line. While all

episodes of economic downturns and market volatility are different in many ways, chemicals sector equities have

consistently recovered quicker than many other sectors, and we see no reason why this episode would end any

differently. However, the timeline may be different.

Burst of Dot-Com Bubble Financial Crisis

2014–2015:

Oil price collapse

5

S&P 500(1): (13%)

STOXX Europe 600(1): (17%)

S&P 500 Chemicals(1): (4%)

FTSE Europe (Chem.)(1): (22%)

S&P 500(2): (24%)

STOXX Europe 600(2): (30%)

S&P 500 Chemicals(2): (18%)

FTSE Europe (Chem.)(2): (12%)

Oil price in

$/barrel

COVID-19

S&P 500(3): (25%)

STOXX Europe 600(3): (28%)

S&P 500 Chemicals(3): (28%)

FTSE Europe (Chem.)(3): (25%)

0

25

50

75

100

125

150

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

400

425

450

475

500

525

550

575

600

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16 Jan-18 Jan-20

S&P 500 S&P 500 Chemicals (Industry) STOXX Europe 600 Index

FTSE Europe Index—Chemicals Crude Oil (Brent) Recessionary Period

Performance of Selected Chemicals End Markets

Automobiles

and Parts

Construction

Materials

Household

and

Personal-

Use

Products

Industrial

Goods

Pharma-

ceuticals

Metals and

Mining

Chemicals

Select Chemicals

End Markets PMI Output (Feb ‘20) Stock Mkt. Perf.(1)(vs. PMI Dec ’19)

Note: PMI = Purchasing manager index

Source: IHS Markit, Bloomberg

(1) Utilizes MSCI world index

(2) Current PMI Output data for U.S. and Europe (as of March) and China (as of February)

Since Jan-20

6

(17%)

(20%)

(18%)

(12%)

(14%)

2%

2%

(26%)

(31%)

(27%)

(26%)

(10%)

(37%)

(15%)

39

40

41

43

43

51

55

20 25 30 35 40 45 50 55 60

Regional PMI Output(2)

Weakness in key end markets, such as automotive, construction, and chemicals, will increase over the next 12

months, driving low capacity utilizations.

28 31 41

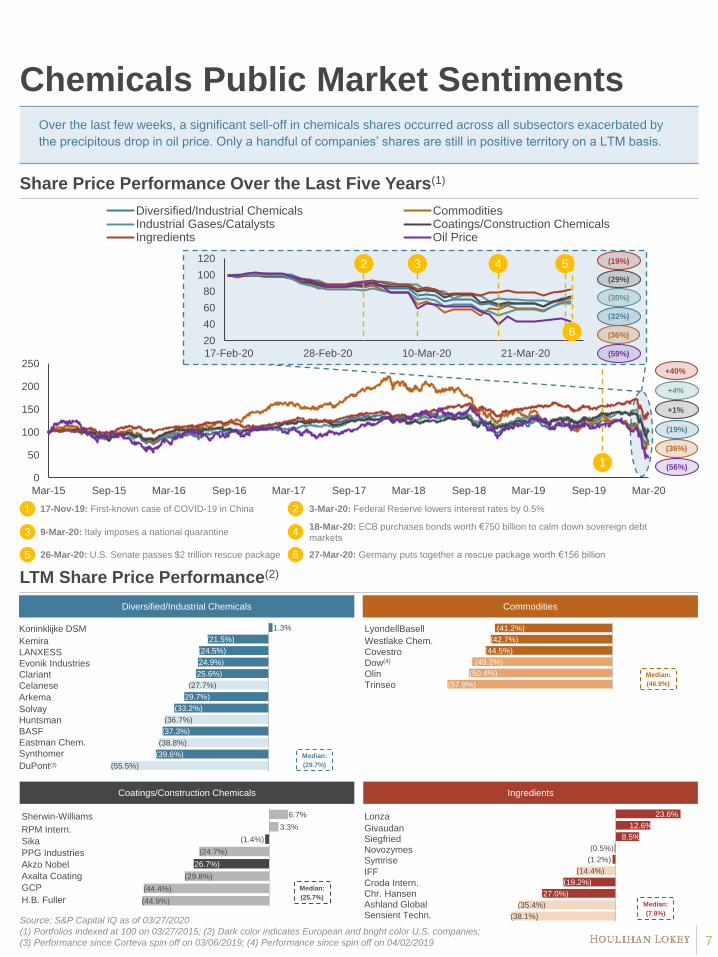

Chemicals Public Market Sentiments

Share Price Performance Over the Last Five Years(1)

LTM Share Price Performance(2)

Source: S&P Capital IQ as of 03/27/2020

(1) Portfolios indexed at 100 on 03/27/2015; (2) Dark color indicates European and bright color U.S. companies;

(3) Performance since Corteva spin off on 03/06/2019; (4) Performance since spin off on 04/02/2019

(19%)

+4%

+1%

(36%)

+40%

(56%)

Diversified/Industrial Chemicals

(55.5%)

(38.8%)

(36.7%)

(27.7%)

(39.6%)

(37.3%)

(33.2%)

(29.7%)

(25.6%)

(24.9%)

(24.5%)

(21.5%)

1.3% Koninklijke DSM

Kemira

Evonik Industries

Clariant

Celanese

Arkema

DuPont(3)

Synthomer

Eastman Chem.

BASF

Huntsman

Solvay

LANXESS

Median:

(29.7%)

0

50

100

150

200

250

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20

Diversified/Industrial Chemicals CommoditiesIndustrial Gases/Catalysts Coatings/Construction ChemicalsIngredients Oil Price

20

40

60

80

100

120

17-Feb-20 28-Feb-20 10-Mar-20 21-Mar-20

2 3

(32%)

(30%)

(29%)

(36%)

(19%)

(59%)

Commodities

(57.9%)

(50.4%)

(49.2%)

(42.7%)

(44.5%)

(41.2%)LyondellBasell

Westlake Chem.

Covestro

Dow(4)

Olin

Trinseo

Median:

(46.9%)

Coatings/Construction Chemicals

(44.9%)

(44.4%)

(29.8%)

(24.7%)

3.3%

6.7%

(26.7%)

(1.4%)

Sherwin-Williams

RPM Intern.

Sika

PPG Industries

Akzo Nobel

GCP

H.B. Fuller

Axalta Coating

Median:

(25.7%)

Ingredients

(38.1%)

(35.4%)

(14.4%)

(27.0%)

(19.2%)

(1.2%)

(0.5%)

8.5%

12.6%

23.6% Lonza

GivaudanSiegfriedNovozymesSymrise

IFF

Croda Intern.Chr. HansenAshland GlobalSensient Techn.

Median:

(7.8%)

7

Over the last few weeks, a significant sell-off in chemicals shares occurred across all subsectors exacerbated by

the precipitous drop in oil price. Only a handful of companies’ shares are still in positive territory on a LTM basis.

2 3-Mar-20: Federal Reserve lowers interest rates by 0.5%1 17-Nov-19: First-known case of COVID-19 in China

18-Mar-20: ECB purchases bonds worth €750 billion to calm down sovereign debt

markets43 9-Mar-20: Italy imposes a national quarantine

4

1

27-Mar-20: Germany puts together a rescue package worth €156 billion5 26-Mar-20: U.S. Senate passes $2 trillion rescue package 6

6

5

(20%)(20%)

(19%)

(18%)(15%)

(10%)(8%)

(37%)(25%)

(19%)

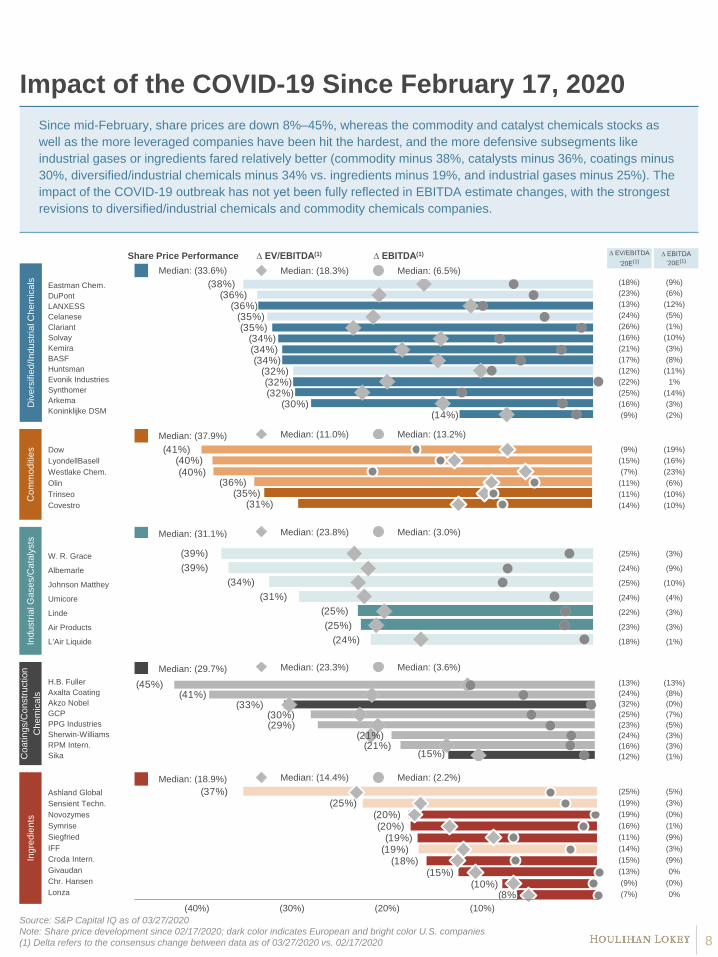

Impact of the COVID-19 Since February 17, 2020

Since mid-February, share prices are down 8%–45%, whereas the commodity and catalyst chemicals stocks as

well as the more leveraged companies have been hit the hardest, and the more defensive subsegments like

industrial gases or ingredients fared relatively better (commodity minus 38%, catalysts minus 36%, coatings minus

30%, diversified/industrial chemicals minus 34% vs. ingredients minus 19%, and industrial gases minus 25%). The

impact of the COVID-19 outbreak has not yet been fully reflected in EBITDA estimate changes, with the strongest

revisions to diversified/industrial chemicals and commodity chemicals companies.

Source: S&P Capital IQ as of 03/27/2020

Note: Share price development since 02/17/2020; dark color indicates European and bright color U.S. companies

(1) Delta refers to the consensus change between data as of 03/27/2020 vs. 02/17/2020 8

Ind

ustr

ial G

ase

s/C

ata

lysts

Ing

red

ien

tsC

oa

tin

gs/C

onstr

uction

Ch

em

ica

ls

Median: (37.9%)

Median: (29.7%)

Median: (11.0%) Median: (13.2%)

Median: (23.3%) Median: (3.6%)

Median: (18.9%) Median: (14.4%) Median: (2.2%)

Median: (31.1%) Median: (23.8%) Median: (3.0%)

Median: (33.6%) Median: (18.3%) Median: (6.5%)

(18%) (9%)

(23%) (6%)

(13%) (12%)

(24%) (5%)

(26%) (1%)

(16%) (10%)

(21%) (3%)

(17%) (8%)

(12%) (11%)

(22%) 1%

(25%) (14%)

(16%) (3%)

(9%) (2%)

(9%) (19%)

(15%) (16%)

(7%) (23%)

(11%) (6%)

(11%) (10%)

(14%) (10%)

(25%) (3%)

(24%) (9%)

(25%) (10%)

(24%) (4%)

(22%) (3%)

(23%) (3%)

(18%) (1%)

∆ EBITDA

‘20E(1)

∆ EV/EBITDA

‘20E(1)

(10%)(20%)(30%)(40%)

Share Price Performance ∆ EBITDA(1)∆ EV/EBITDA(1)

Co

mm

od

itie

sD

ive

rsifie

d/I

nd

ustr

ial C

he

mic

als

(35%)(31%)

(41%)(40%)

(40%)(36%)

(25%)

(25%)

(39%)

(39%)

(34%)

(31%)

(24%)

(33%)

(15%)

(45%)(41%)

(30%)(29%)

(21%)(21%)

Eastman Chem.

DuPont

LANXESS

Celanese

Clariant

Solvay

Kemira

BASF

Huntsman

Evonik Industries

Synthomer

Arkema

Koninklijke DSM

Dow

LyondellBasell

Westlake Chem.

Olin

Trinseo

Covestro

W. R. Grace

Albemarle

Johnson Matthey

Umicore

Linde

Air Products

L'Air Liquide

H.B. Fuller

Axalta Coating

Akzo Nobel

GCP

PPG Industries

Sherwin-Williams

RPM Intern.

Sika

Ashland Global

Sensient Techn.

Novozymes

Symrise

Siegfried

IFF

Croda Intern.

Givaudan

Chr. Hansen

Lonza

(25%) (5%)

(19%) (3%)

(19%) (0%)

(16%) (1%)

(11%) (9%)

(14%) (3%)

(15%) (9%)

(13%) 0%

(9%) (0%)

(7%) 0%

(13%) (13%)

(24%) (8%)

(32%) (0%)

(25%) (7%)

(23%) (5%)

(24%) (3%)

(16%) (3%)

(12%) (1%)

(36%)

(35%)(34%)(34%)(34%)

(32%)(32%)

(30%)(14%)

(38%)(36%)

(35%)

(32%)

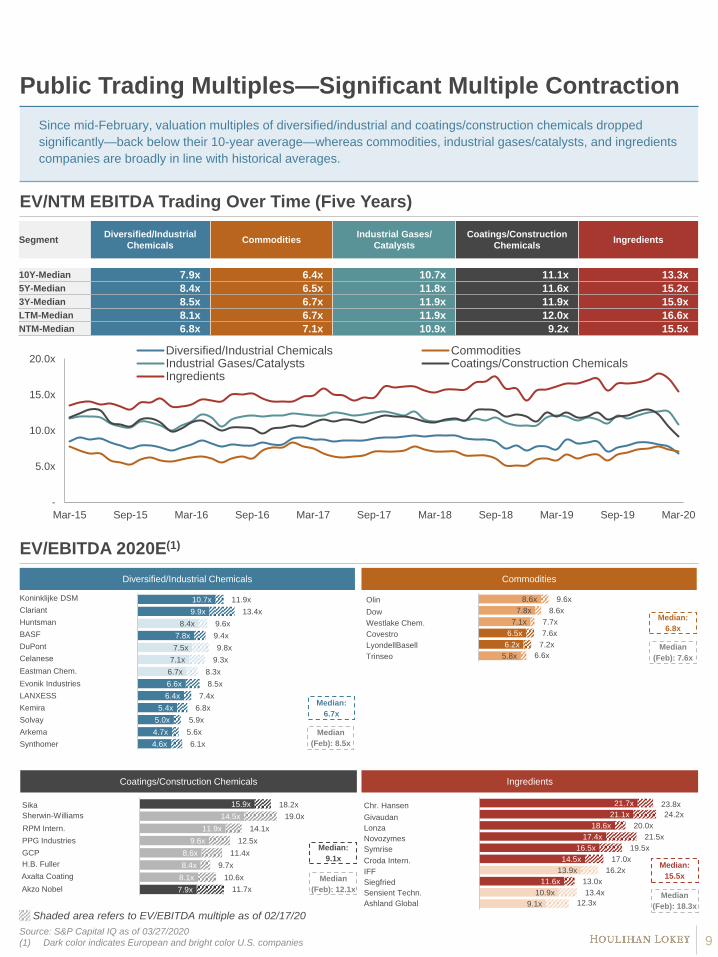

Public Trading Multiples—Significant Multiple Contraction

EV/NTM EBITDA Trading Over Time (Five Years)

Shaded area refers to EV/EBITDA multiple as of 02/17/20

Source: S&P Capital IQ as of 03/27/2020

(1) Dark color indicates European and bright color U.S. companies

Ingredients

Diversified/Industrial Chemicals

6.7x

7.1x

7.5x

8.4x

4.6x

4.7x

5.0x

5.4x

6.4x

6.6x

7.8x

9.9x

10.7x

6.1x

5.6x

5.9x

6.8x

7.4x

8.5x

9.4x

13.4x

11.9x

8.3x

9.3x

9.8x

9.6x

Median

(Feb): 8.5x

Median:

6.7x

Koninklijke DSM

Clariant

BASF

DuPont

Celanese

Eastman Chem.

Synthomer

Arkema

Solvay

Kemira

LANXESS

Evonik Industries

Huntsman

Commodities

5.8x

7.1x

7.8x

8.6x

6.2x

6.5x

7.2x

7.6x

6.6x

7.7x

8.6x

9.6x Olin

Dow

Westlake Chem.

Covestro

LyondellBasell

Trinseo

Median

(Feb): 7.6x

Median:

6.8x

Coatings/Construction Chemicals

8.1x

8.4x

8.6x

9.6x

11.9x

14.5x

7.9x

15.9x

11.7x

18.2x

10.6x

9.7x

11.4x

12.5x

14.1x

19.0x

Sika

Sherwin-Williams

RPM Intern.

PPG Industries

GCP

H.B. Fuller

Axalta Coating Median

(Feb): 12.1xAkzo Nobel

Median:

9.1x

9.1x

10.9x

13.9x

11.6x

14.5x

16.5x

17.4x

18.6x

21.1x

21.7x

13.0x

17.0x

19.5x

21.5x

20.0x

24.2x

23.8x

12.3x

13.4x

16.2x

Chr. Hansen

Givaudan

Lonza

Novozymes

Symrise

Croda Intern.

IFF

Siegfried

Sensient Techn.

Ashland GlobalMedian

(Feb): 18.3x

Median:

15.5x

EV/EBITDA 2020E(1)

-

5.0x

10.0x

15.0x

20.0x

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20

Diversified/Industrial Chemicals CommoditiesIndustrial Gases/Catalysts Coatings/Construction ChemicalsIngredients

9

Since mid-February, valuation multiples of diversified/industrial and coatings/construction chemicals dropped

significantly—back below their 10-year average—whereas commodities, industrial gases/catalysts, and ingredients

companies are broadly in line with historical averages.

SegmentDiversified/Industrial

ChemicalsCommodities

Industrial Gases/

Catalysts

Coatings/Construction

ChemicalsIngredients

10Y-Median 7.9x 6.4x 10.7x 11.1x 13.3x

5Y-Median 8.4x 6.5x 11.8x 11.6x 15.2x

3Y-Median 8.5x 6.7x 11.9x 11.9x 15.9x

LTM-Median 8.1x 6.7x 11.9x 12.0x 16.6x

NTM-Median 6.8x 7.1x 10.9x 9.2x 15.5x

50

100

150

200

250

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20

Diversified/Industrial Chemicals Commodities

Industrial Gases/Catalysts Coatings/Construction Chemicals

Ingredients

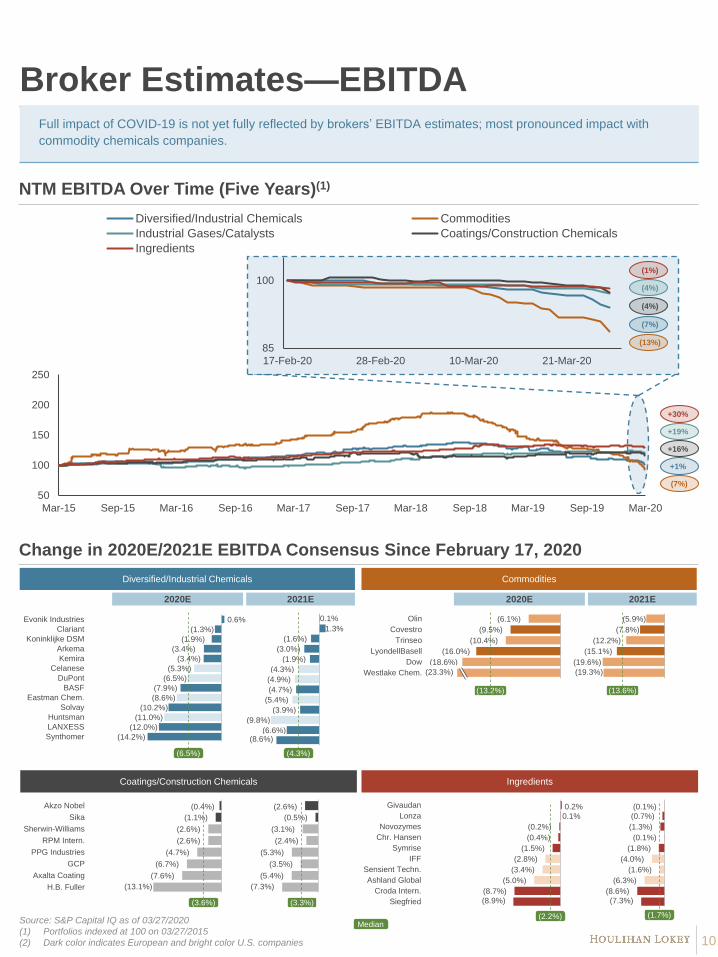

Broker Estimates—EBITDAFull impact of COVID-19 is not yet fully reflected by brokers’ EBITDA estimates; most pronounced impact with

commodity chemicals companies.

NTM EBITDA Over Time (Five Years)(1)

2020E 2021E

Median

0.6%

(1.3%)

(1.9%)

(3.4%)

(3.4%)

(5.3%)

(6.5%)

(7.9%)

(8.6%)

(10.2%)

(11.0%)

(12.0%)

(14.2%)

Evonik Industries

Clariant

Koninklijke DSM

Arkema

Kemira

Celanese

DuPont

BASF

Eastman Chem.

Solvay

Huntsman

LANXESS

Synthomer (8.6%)

0.1%

1.3%

(1.6%)

(3.0%)

(1.9%)

(4.3%)

(4.9%)

(4.7%)

(5.4%)

(3.9%)

(9.8%)

(6.6%)

(6.5%) (4.3%)

(0.1%)

(0.7%)

(1.3%)

(0.1%)

(1.8%)

(4.0%)

(1.6%)

(6.3%)

(8.6%)

(7.3%)

0.2%

0.1%

(0.2%)

(0.4%)

(1.5%)

(2.8%)

(3.4%)

(5.0%)

(8.7%)

(8.9%)

Givaudan

Lonza

Novozymes

Chr. Hansen

Symrise

IFF

Sensient Techn.

Ashland Global

Croda Intern.

Siegfried

(2.2%) (1.7%)Source: S&P Capital IQ as of 03/27/2020

(1) Portfolios indexed at 100 on 03/27/2015

(2) Dark color indicates European and bright color U.S. companies

(16.0%)

(18.6%)

(23.3%)

(6.1%)

(9.5%)

(10.4%)

Olin

Covestro

Trinseo

LyondellBasell

Dow

Westlake Chem.

(13.2%)

(19.6%)

(19.3%)

(5.9%)

(7.8%)

(12.2%)

(15.1%)

(13.6%)

(2.6%)

(0.5%)

(3.1%)

(2.4%)

(5.3%)

(3.5%)

(5.4%)

(7.3%)(13.1%)

(0.4%)

(1.1%)

(2.6%)

(2.6%)

(4.7%)

(6.7%)

(7.6%)

Akzo Nobel

Sika

Sherwin-Williams

RPM Intern.

PPG Industries

GCP

Axalta Coating

H.B. Fuller

(3.6%) (3.3%)

85

100

17-Feb-20 28-Feb-20 10-Mar-20 21-Mar-20

+30%

Change in 2020E/2021E EBITDA Consensus Since February 17, 2020

10

+1%

+19%

+16%

(7%)

Ingredients

Diversified/Industrial Chemicals Commodities

Coatings/Construction Chemicals

2020E 2021E

(7%)

(4%)

(4%)

(13%)

(1%)

50

100

150

200

250

300

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20

Diversified/Industrial Chemicals CommoditiesIndustrial Gases/Catalysts Coatings/Construction ChemicalsIngredients

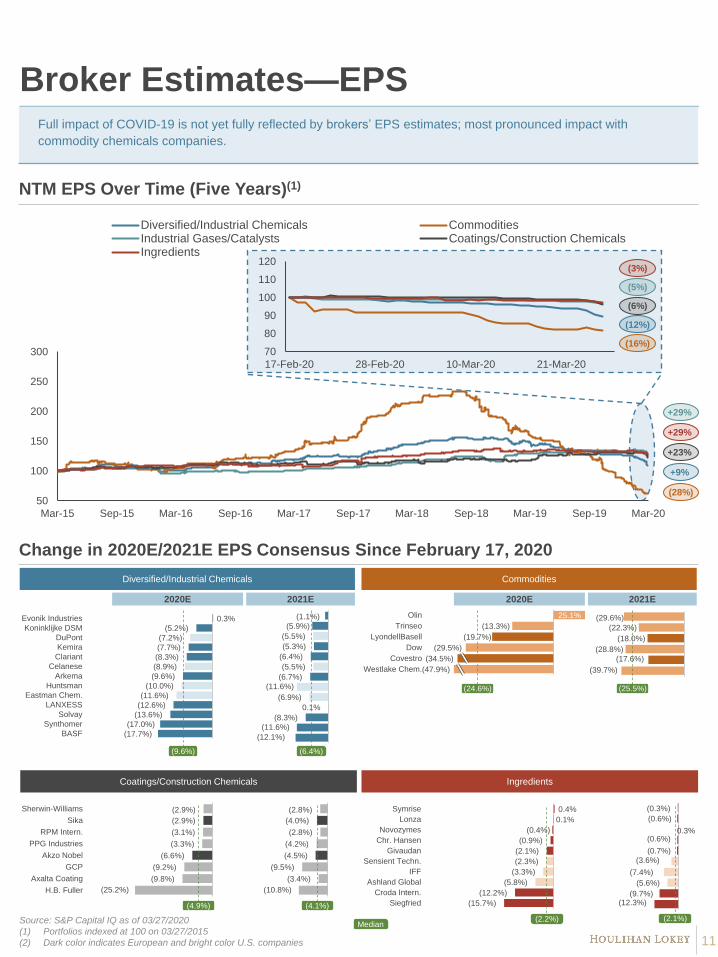

Broker Estimates—EPSFull impact of COVID-19 is not yet fully reflected by brokers’ EPS estimates; most pronounced impact with

commodity chemicals companies.

NTM EPS Over Time (Five Years)(1)

Source: S&P Capital IQ as of 03/27/2020

(1) Portfolios indexed at 100 on 03/27/2015

(2) Dark color indicates European and bright color U.S. companies

Change in 2020E/2021E EPS Consensus Since February 17, 2020

+9%

+29%

+23%

(28%)

+29%

70

80

90

100

110

120

17-Feb-20 28-Feb-20 10-Mar-20 21-Mar-20

(12%)

(5%)

(6%)

(16%)

(3%)

25.1%

(47.9%)

(13.3%)

(19.7%)

(29.5%)

(34.5%)

Olin

Trinseo

LyondellBasell

Dow

Covestro

Westlake Chem.

(24.6%)

(29.6%)

(28.8%)

(39.7%)

(22.3%)

(18.0%)

(17.6%)

(25.5%)

0.3%

(5.2%)

(7.2%)

(7.7%)

(8.3%)

(8.9%)

(9.6%)

(10.0%)

(11.6%)

(12.6%)

(13.6%)

(17.0%)

(17.7%)

Evonik Industries

Koninklijke DSM

DuPont

Kemira

Clariant

Celanese

Arkema

Huntsman

Eastman Chem.

LANXESS

Solvay

Synthomer

BASF

(9.6%) (6.4%)

(1.1%)

(5.9%)

(5.5%)

(5.3%)

(6.4%)

(5.5%)

(6.7%)

(11.6%)

(6.9%)

0.1%

(8.3%)

(11.6%)

(12.1%)

(2.8%)

(4.0%)

(2.8%)

(4.2%)

(4.5%)

(9.5%)

(3.4%)

(10.8%)(25.2%)

(2.9%)

(2.9%)

(3.1%)

(3.3%)

(6.6%)

(9.2%)

(9.8%)

Sherwin-Williams

Sika

RPM Intern.

PPG Industries

Akzo Nobel

GCP

Axalta Coating

H.B. Fuller

(4.9%) (4.1%)

0.4%

0.1%

(0.4%)

(0.9%)

(2.1%)

(2.3%)

(3.3%)

(5.8%)

(12.2%)

(15.7%)

Symrise

Lonza

Novozymes

Chr. Hansen

Givaudan

Sensient Techn.

IFF

Ashland Global

Croda Intern.

Siegfried

(2.2%)

(0.3%)

(0.6%)

0.3%(0.6%)

(0.7%)

(3.6%)

(7.4%)

(5.6%)

(9.7%)(12.3%)

(2.1%)

11

Median

2020E 2021E

Ingredients

Diversified/Industrial Chemicals Commodities

Coatings/Construction Chemicals

2020E 2021E

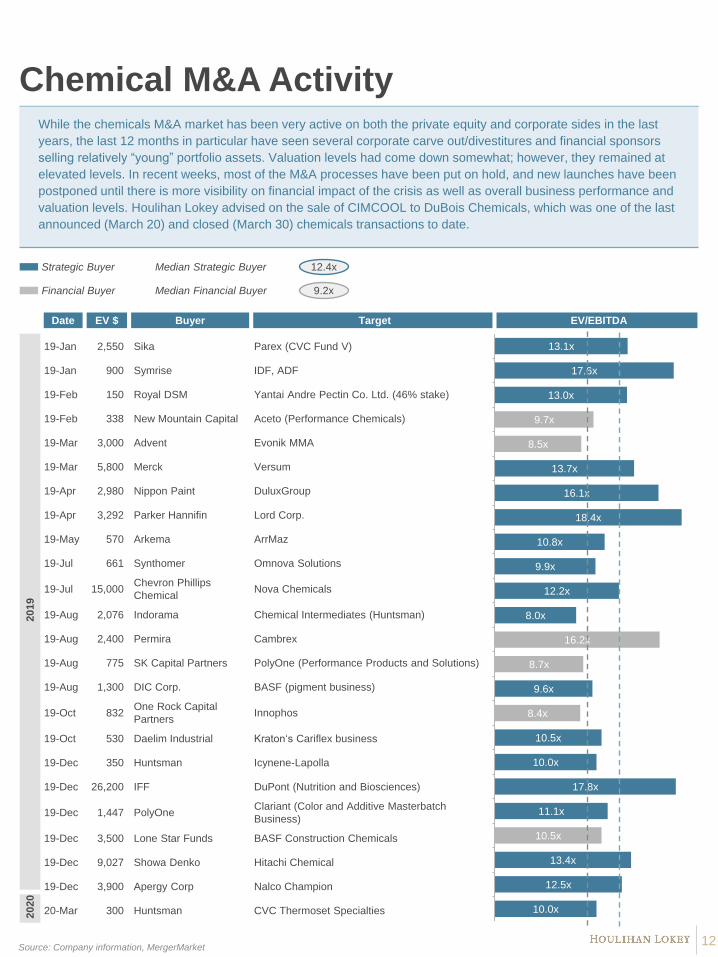

Chemical M&A Activity

19-Jan 2,550 Sika Parex (CVC Fund V)

19-Jan 900 Symrise IDF, ADF

19-Feb 150 Royal DSM Yantai Andre Pectin Co. Ltd. (46% stake)

19-Feb 338 New Mountain Capital Aceto (Performance Chemicals)

19-Mar 3,000 Advent Evonik MMA

19-Mar 5,800 Merck Versum

19-Apr 2,980 Nippon Paint DuluxGroup

19-Apr 3,292 Parker Hannifin Lord Corp.

19-May 570 Arkema ArrMaz

19-Jul 661 Synthomer Omnova Solutions

19-Jul 15,000Chevron Phillips

ChemicalNova Chemicals

19-Aug 2,076 Indorama Chemical Intermediates (Huntsman)

19-Aug 2,400 Permira Cambrex

19-Aug 775 SK Capital Partners PolyOne (Performance Products and Solutions)

19-Aug 1,300 DIC Corp. BASF (pigment business)

19-Oct 832One Rock Capital

PartnersInnophos

19-Oct 530 Daelim Industrial Kraton‘s Cariflex business

19-Dec 350 Huntsman Icynene-Lapolla

19-Dec 26,200 IFF DuPont (Nutrition and Biosciences)

19-Dec 1,447 PolyOneClariant (Color and Additive Masterbatch

Business)

19-Dec 3,500 Lone Star Funds BASF Construction Chemicals

19-Dec 9,027 Showa Denko Hitachi Chemical

19-Dec 3,900 Apergy Corp Nalco Champion

20-Mar 300 Huntsman CVC Thermoset Specialties

13.1x

17.6x

13.0x

9.7x

8.5x

13.7x

16.1x

18.4x

10.8x

9.9x

12.2x

8.0x

16.2x

8.7x

9.6x

8.4x

10.5x

10.0x

17.8x

11.1x

10.5x

13.4x

12.5x

10.0x

20

19

20

20

Source: Company information, MergerMarket12

While the chemicals M&A market has been very active on both the private equity and corporate sides in the last

years, the last 12 months in particular have seen several corporate carve out/divestitures and financial sponsors

selling relatively “young” portfolio assets. Valuation levels had come down somewhat; however, they remained at

elevated levels. In recent weeks, most of the M&A processes have been put on hold, and new launches have been

postponed until there is more visibility on financial impact of the crisis as well as overall business performance and

valuation levels. Houlihan Lokey advised on the sale of CIMCOOL to DuBois Chemicals, which was one of the last

announced (March 20) and closed (March 30) chemicals transactions to date.

Strategic Buyer

Financial Buyer

Median Strategic Buyer

Median Financial Buyer 9.2x

12.4x

BuyerEV $Date Target EV/EBITDA

Case Study: CIMCOOLCimcool is a leading global formulator and manufacturer of high-performance specialty metalworking fluids,

including removal, forming, protective, and cleaning fluids

Business and Transaction Highlights

On March 20, 2020, Hillenbrand, Inc. (NYSE:HI; “Hillenbrand” or the “company”)

announced the signing of an agreement to sell Cimcool to DuBois Chemicals, Inc.

(DuBois), a portfolio company of Altas Partners. The transaction closed on March 30

DuBois acquired Cimcool at a purchase price of approximately $224 million in cash.

In addition, DuBois has agreed to pay up to $26 million in contingent purchase price,

upon the future sale of the combined DuBois and Cimcool businesses

Cimcool is a leading global manufacturer of high-performance specialty

metalworking fluids, including removal, forming, protective, and cleaning fluids

Serves a global and wide range of customers across diverse end markets

Four manufacturing facilities in the U.S., the Netherlands, China, and South Korea

Transaction expands DuBois’ facility footprint into Europe and Asia

Keys to Process and Valuation Success

Conducted a highly competitive and global sales process with a focus on U.S. and European strategics and

sponsors

Customized and tight process timeline to drive competitive tension throughout the process

Significant upfront preparation of diligence deliverables, including a QoE report and a robust data room allowed

for immediate due diligence on an accelerated timeline

Maintained significant deal momentum to drive both valuation and speed to signing, even after the outbreak of

COVID-19

Limited incremental stand-alone costs simplified carve-out complexities

Nov 2019

Closing of Milacron/

Hillenbrand transaction;

announcement of review of

strategic options for Cimcool

Nov 2019 Mar 2020Jan 2020 Feb 2020

Feb 2020

IOI submission

deadline

Mar 2020

Rapid COVID-

19 outbreak in

Western

Hemisphere

Jan 2020

Market

outreach

Mar 2020

Closing

Dec 2019

Mar 2020

Signed definitive

agreement

Dec 2019

Thorough

process

preparation

13

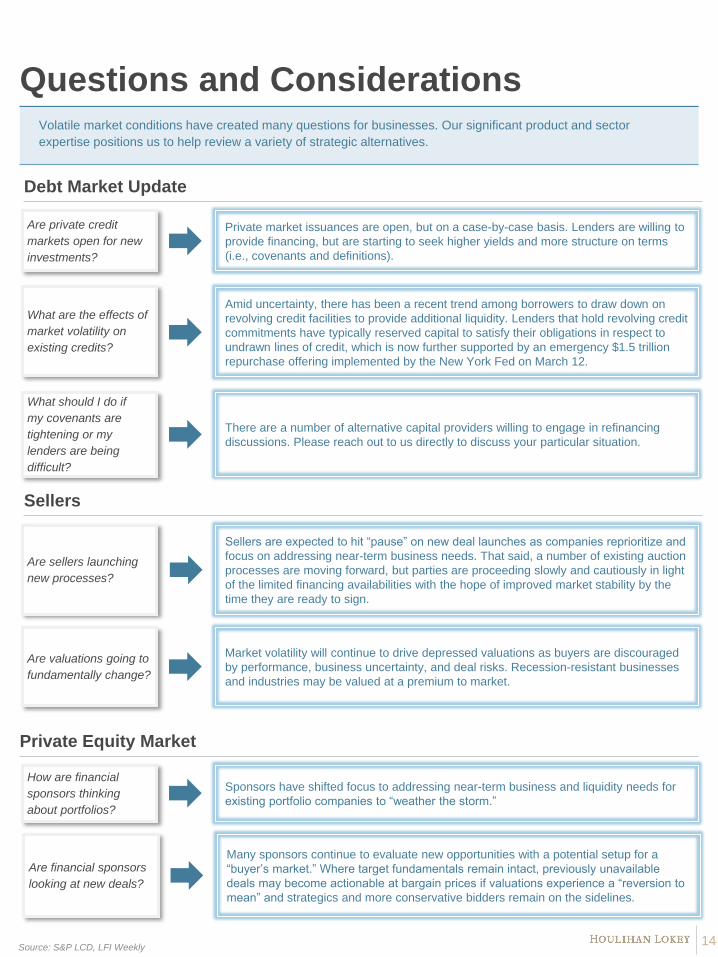

Questions and Considerations

Are private credit

markets open for new

investments?

Private market issuances are open, but on a case-by-case basis. Lenders are willing to

provide financing, but are starting to seek higher yields and more structure on terms

(i.e., covenants and definitions).

What are the effects of

market volatility on

existing credits?

Amid uncertainty, there has been a recent trend among borrowers to draw down on

revolving credit facilities to provide additional liquidity. Lenders that hold revolving credit

commitments have typically reserved capital to satisfy their obligations in respect to

undrawn lines of credit, which is now further supported by an emergency $1.5 trillion

repurchase offering implemented by the New York Fed on March 12.

Are sellers launching

new processes?

Sellers are expected to hit “pause” on new deal launches as companies reprioritize and

focus on addressing near-term business needs. That said, a number of existing auction

processes are moving forward, but parties are proceeding slowly and cautiously in light

of the limited financing availabilities with the hope of improved market stability by the

time they are ready to sign.

Are valuations going to

fundamentally change?

Market volatility will continue to drive depressed valuations as buyers are discouraged

by performance, business uncertainty, and deal risks. Recession-resistant businesses

and industries may be valued at a premium to market.

Volatile market conditions have created many questions for businesses. Our significant product and sector

expertise positions us to help review a variety of strategic alternatives.

How are financial

sponsors thinking

about portfolios?

Sponsors have shifted focus to addressing near-term business and liquidity needs for

existing portfolio companies to “weather the storm.”

Source: S&P LCD, LFI Weekly14

Debt Market Update

Sellers

Private Equity Market

Are financial sponsors

looking at new deals?

Many sponsors continue to evaluate new opportunities with a potential setup for a

“buyer’s market.” Where target fundamentals remain intact, previously unavailable

deals may become actionable at bargain prices if valuations experience a “reversion to

mean” and strategics and more conservative bidders remain on the sidelines.

What should I do if

my covenants are

tightening or my

lenders are being

difficult?

There are a number of alternative capital providers willing to engage in refinancing

discussions. Please reach out to us directly to discuss your particular situation.

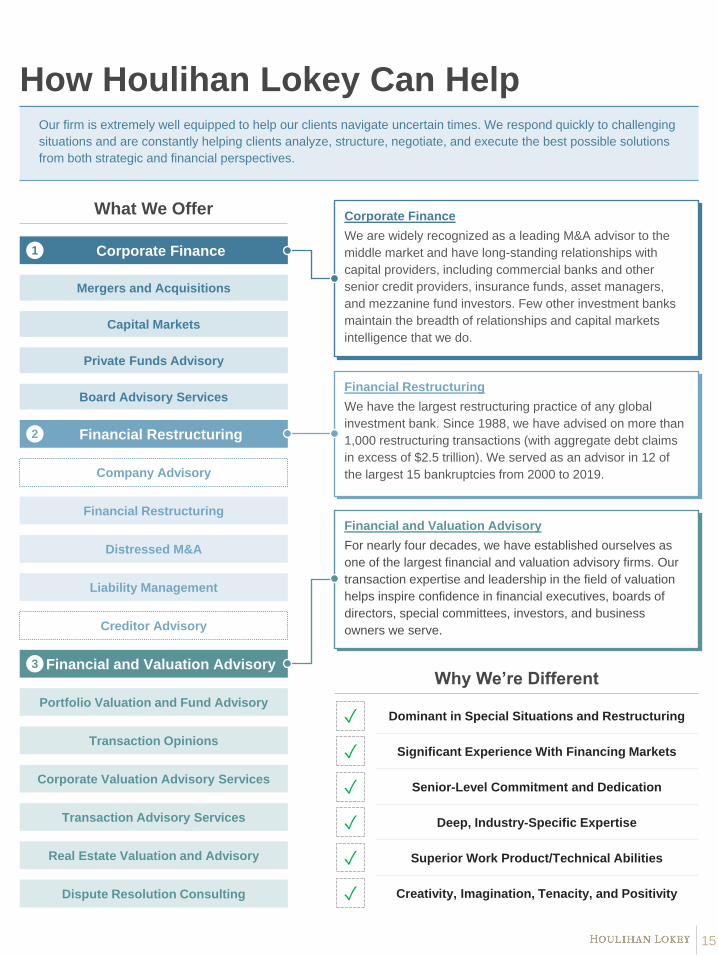

Our firm is extremely well equipped to help our clients navigate uncertain times. We respond quickly to challenging

situations and are constantly helping clients analyze, structure, negotiate, and execute the best possible solutions

from both strategic and financial perspectives.

How Houlihan Lokey Can Help

What We Offer

Superior Work Product/Technical Abilities

Creativity, Imagination, Tenacity, and Positivity

Deep, Industry-Specific Expertise

Senior-Level Commitment and Dedication

Portfolio Valuation and Fund Advisory

Significant Experience With Financing Markets

Dominant in Special Situations and Restructuring

Corporate Finance

Financial Restructuring

Financial and Valuation Advisory

Transaction Opinions

Corporate Valuation Advisory Services

Transaction Advisory Services

Real Estate Valuation and Advisory

Dispute Resolution Consulting

Mergers and Acquisitions

Capital Markets

Private Funds Advisory

Board Advisory Services

Corporate Finance

We are widely recognized as a leading M&A advisor to the

middle market and have long-standing relationships with

capital providers, including commercial banks and other

senior credit providers, insurance funds, asset managers,

and mezzanine fund investors. Few other investment banks

maintain the breadth of relationships and capital markets

intelligence that we do.

Company Advisory

Creditor Advisory

Financial Restructuring

We have the largest restructuring practice of any global

investment bank. Since 1988, we have advised on more than

1,000 restructuring transactions (with aggregate debt claims

in excess of $2.5 trillion). We served as an advisor in 12 of

the largest 15 bankruptcies from 2000 to 2019.

Financial Restructuring

Distressed M&A

Liability Management

Financial and Valuation Advisory

For nearly four decades, we have established ourselves as

one of the largest financial and valuation advisory firms. Our

transaction expertise and leadership in the field of valuation

helps inspire confidence in financial executives, boards of

directors, special committees, investors, and business

owners we serve.

Why We’re Different

1

2

3

✓

✓

✓

✓

✓

✓

15

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

70

80

90

100

110

Jan-20 Feb-20 Mar-20

Average European Leveraged Loan Flow-Name Bid

Average European High-Yield Bond Flow-Name Bid

Average European High-Yield Bond Yield

Leveraged Finance Market Impact From COVID-19

Leveraged Loans and High-Yield Issuance Volume

European Leveraged Loans and

High-Yield: Average Bid and Yield(1)

U.S. Leveraged Loans and High-

Yield: Average Bid and Yield

Primary Deals Getting Pulled Because of

Adverse Market Conditions

Date Issuer UoP Sponsor Sector CFR

Tranche

Size

Proposed

Pricing

Mar-20Micro

FocusRefinancing - Services

B1/

BB-

$500M

€500M

L+375-400/

99.0

E+325-350/

99.5

Feb-20Messer

IndustriesRepricing CVC Industrials

BB-/

B1

€540M

$2,200M

E+225/

99.875-100

L+225/ 99.875

Feb-20Alix

PartnersRepricing

CPPIB &

CDPQConsulting

B+/

B2€348M

E+275-300/

Par

Feb-20 Minimax Repricing KIRKBIFire Safety

Equipment

B+/

B1

€506M

$590M

E+250/Par

L+225/Par

Volatility Index (U.S. and Europe)

Note: Market data retrieved as of 03/27/2020

Source: Bloomberg, S&P Capital IQ, LCD

(1) Yield data for European leveraged loans not available on a weekly basis

65.5

61.0

0

20

40

60

80

100

Jan-20 Feb-20 Mar-20

U.S. (CBOE Volatility S&P 500 Index) EU (EURO STOXX 50 Volatility Index)

27-Mar-20

European Market (€B) U.S. Market ($B)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Leverage Loan Issuance Volume

High-Yield Bond Issuance Volume

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Leverage Loan Issuance Volume

High-Yield Bond Issuance Volume

2.0%

4.0%

6.0%

8.0%

10.0%

70

80

90

100

110

Jan-20 Feb-20 Mar-20

Average U.S. Leveraged Loan Flow-Name Bid Average U.S. High-Yield Bond Flow-Name Bid Average U.S. High-Yield Bond Yield

Average U.S. Leveraged Loan New-Issue Yield

16

Disclaimer

© 2020 Houlihan Lokey. All rights reserved. This material may not be reproduced in any format by any means

or redistributed without the prior written consent of Houlihan Lokey.

Houlihan Lokey gathers its data from sources it considers reliable; however, it does not guarantee the

accuracy or completeness of the information provided within this presentation. The material presented

reflects information known to the authors at the time this presentation was written, and this information is

subject to change. Houlihan Lokey makes no representations or warranties, expressed or implied, regarding

the accuracy of this material. The views expressed in this material accurately reflect the personal views of the

authors regarding the subject securities and issuers and do not necessarily coincide with those of Houlihan

Lokey. Officers, directors, and partners in the Houlihan Lokey group of companies may have positions in the

securities of the companies discussed. This presentation does not constitute advice or a recommendation,

offer, or solicitation with respect to the securities of any company discussed herein, is not intended to provide

information upon which to base an investment decision, and should not be construed as such. Houlihan

Lokey or its affiliates may from time to time provide investment banking or related services to these

companies. Like all Houlihan Lokey employees, the authors of this presentation receive compensation that is

affected by overall firm profitability.

Houlihan Lokey is a trade name for Houlihan Lokey, Inc., and its subsidiaries and affiliates, which include

those in (i) the United States: Houlihan Lokey Capital, Inc., an SEC-registered broker-dealer and member of

FINRA (www.finra.org) and SIPC (www.sipc.org) (investment banking services); Houlihan Lokey Financial

Advisors, Inc. (financial advisory services); HL Finance, LLC (syndicated leveraged finance platform); and

Houlihan Lokey Real Estate Group, Inc. (real estate advisory services); (ii) Europe: Houlihan Lokey EMEA,

LLP, and Houlihan Lokey (Corporate Finance) Limited, authorized and regulated by the U.K. Financial

Conduct Authority; Houlihan Lokey S.p.A.; Houlihan Lokey GmbH; Houlihan Lokey (Netherlands) B.V.;

Houlihan Lokey (España), S.A.; and Houlihan Lokey (Corporate Finance), S.A.; (iii) the United Arab Emirates,

Dubai International Financial Centre (Dubai): Houlihan Lokey (MEA Financial Advisory) Limited, regulated by

the Dubai Financial Services Authority for the provision of advising on financial products, arranging deals in

investments, and arranging credit and advising on credit to professional clients only; (iv) Singapore: Houlihan

Lokey (Singapore) Private Limited, an “exempt corporate finance adviser” able to provide exempt corporate

finance advisory services to accredited investors only; (v) Hong Kong SAR: Houlihan Lokey (China) Limited,

licensed in Hong Kong by the Securities and Futures Commission to conduct Type 1, 4, and 6 regulated

activities to professional investors only; (vi) China: Houlihan Lokey Howard & Zukin Investment Consulting

(Beijing) Co., Limited (financial advisory services); (vii) Japan: Houlihan Lokey K.K. (financial advisory

services); and (viii) Australia: Houlihan Lokey (Australia) Pty Limited (ABN 74 601 825 227), a company

incorporated in Australia and licensed by the Australian Securities and Investments Commission (AFSL

number 474953) in respect of financial services provided to wholesale clients only. In the European Economic

Area (EEA), Dubai, Singapore, Hong Kong, and Australia, this communication is directed to intended

recipients, including actual or potential professional clients (EEA and Dubai), accredited investors

(Singapore), professional investors (Hong Kong), and wholesale clients (Australia), respectively. Other

persons, such as retail clients, are NOT the intended recipients of our communications or services and should

not act upon this communication.

17

CORPORATE FINANCE

FINANCIAL RESTRUCTURING

FINANCIAL AND VALUATION ADVISORY

HL.com