Embed Size (px)

Citation preview

Consolidated Financial Statements of

ALTERNA SAVINGS

December 31, 2005

AUDITORS' REPORT To the Members of Alterna Savings and Credit Union Limited (formerly “The Civil Service Co-operative Credit Society, Limited”): We have audited the consolidated balance sheet of Alterna Savings and Credit Union Limited (“Alterna Savings”) as at December 31, 2005 and the consolidated statements of income and reserves and cash flows for the year then ended. These financial statements are the responsibility of the management of Alterna Savings. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we plan and perform an audit to obtain reasonable assurance whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. In our opinion, these consolidated financial statements present fairly, in all material respects, the financial position of Alterna Savings as at December 31, 2005 and the results of its operations and its cash flows for the year then ended in accordance with Canadian generally accepted accounting principles. Ottawa, Canada March 31, 2006

Chartered Accountants

ALTERNA SAVINGS Consolidated Balance Sheet (in thousands of dollars) As at December 31

1

2005 2004

ASSETS (note 10)

Cash and cash equivalents 180,472$ 79,777$ Investments (note 4) 116,011 246,508 Loans, net of allowance for impaired loans (notes 5 and 6) 1,405,716 863,712 Property and equipment (note 7) 31,298 23,544 Other assets (note 8) 10,353 11,789

1,743,850$ 1,225,330$

LIABILITIES AND MEMBERS' EQUITY

Liabilities: Deposits (note 9) 1,597,208$ 1,120,391$ Future tax liability (note 18) 1,810 1,645 Other liabilities (notes 11 and 12) 18,496 12,982 Membership shares (note 13) 2,625 2,067

1,620,139 1,137,085 Members' Equity: Special shares (note 13) 29,025 15,358 Contributed surplus (note 3) 19,053 - Reserves 75,633 72,887

123,711 88,245 1,743,850$ 1,225,330$

On behalf of the Board:

……………………………………….., Director

……………………………………….., Director

On behalf of the Board:

Earl G. Campbell, Director Richard Neville, Director

(See accompanying notes to the consolidated financial statements)

ALTERNA SAVINGS Consolidated Statement of Income and Reserves (in thousands of dollars) Year ended December 31

2

2005 2004

Interest income (note 14) 71,154$ 53,358$ Investment income 9,475 9,046

80,629 62,404 Interest expense (note 14) 32,994 28,545 Net interest income 47,635 33,859 Loan costs 966 104

46,669 33,755 Other income (note 15) 14,120 11,267

60,789 45,022 Operating expenses (note 16) 54,726 39,016 Net income before integration costs and income taxes 6,063 6,006 Integration costs (note 3) 1,314 - Net income before income taxes 4,749 6,006

Provision for income taxes (note 18) Current 732 106 Future 165 1,010

897 1,116 Net income 3,852 4,890

Reserves, beginning of year 72,887 68,637 Dividend on special shares (net of tax) (note 13) 1,106 640 Reserves, end of year 75,633$ 72,887$

(See accompanying notes to the consolidated financial statements)

ALTERNA SAVINGS Consolidated Statement of Cash Flows (in thousands of dollars) Year ended December 31

3

2005 2004

Operating activities:Net income 3,852$ 4,890$ Add (deduct) non-cash items:

Gain on disposal of assets - (3) Amortization of property and equipment 4,950 4,297 Amortization of deferred charges 2,478 2,441 Allowance for impaired loans 530 (252) Future income taxes 165 1,010 Increase in interest receivable (1,064) (623) Increase (decrease) in interest payable 4,149 (996) Decrease (increase) in amount receivable on derivative financial instruments 249 (629) Other items, net 2,146 (1,997)

Cash provided by operating activities 17,455 8,138

Investing activities:Proceeds from maturity and sale of investments 221,130 9,662 Purchase of investments (50,295) (87,430) Net (increase) decrease in loans (41,167) 5,665 Acquisition of property and equipment (5,702) (7,459) Consideration paid on business combination, net of cash acquired 326 -

Cash provided by (applied to) investing activities 124,292 (79,562)

Financing activities:Net increase in deposits 949 8,881 Net decrease in membership shares (39) (55) Net decrease in special shares (818) - Dividend on special shares (1,106) (640) Net decrease in borrowings (40,038) (36,472)

Cash applied to financing activities (41,052) (28,286)

Increase (decrease) in cash and cash equivalents during the year 100,695 (99,710) Cash and cash equivalents, beginning of year 79,777 179,487 Cash and cash equivalents, end of year 180,472$ 79,777$

Supplemental information:Interest paid 28,845$ 31,550$ Income taxes paid 1,485$ 334$ Property and equipment acquired through capital leases 257$ 2,639$

(See accompanying notes to the consolidated financial statements)

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

4

1. NATURE OF OPERATIONS

On April 1, 2005, The Civil Service Co-operative Credit Society, Limited (“CS CO-OP”), a credit union operating primarily in the National Capital Region, amalgamated with Metro Credit Union (“Metro”), a credit union operating in the Greater Toronto Area, with the new entity commencing operations on that date as Alterna Savings and Credit Union Limited (“Alterna Savings”).

The transaction has been accounted for by the purchase method as prescribed under the Canadian Institute of Chartered Accountants’ (“CICA”) Section 1580, Business Combinations. As such, the financial results of former Metro are incorporated into the Alterna Savings’ financial statements for the nine-month period of April 1 to December 31, 2005. Refer to note 3 for additional information.

Alterna Savings is a credit union incorporated under The Credit Unions and Caisses Populaires Act (Ontario) and is a member of the Deposit Insurance Corporation of Ontario (“DICO”) and Credit Union Central of Ontario (“CUCO”).

2. SIGNIFICANT ACCOUNTING POLICIES

These consolidated financial statements have been prepared in accordance with Canadian generally accepted accounting principles (“GAAP”). The preparation of financial statements in accordance with GAAP requires management to make assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. The significant accounting policies are as follows: a) Basis of Consolidation The consolidated financial statements include the accounts and results of operations of CS Alterna Bank (“Alterna Bank”), a wholly-owned subsidiary. All significant intercompany balances and transactions have been eliminated on consolidation. b) Cash and Cash Equivalents Cash and cash equivalents include cash on hand, cash on deposit with other financial institutions, cheques and other items in transit, and marketable securities, including accrued interest, with original maturities at acquisition of 90 days or less. c) Investments Investments in bonds, commercial paper and residential mortgages purchased as investments are stated at amortized cost plus accrued interest with purchase premiums and discounts amortized over the term to maturity of the respective investments. Investments in co-operative organizations and other investments are stated at cost. Where applicable, investments are written down to fair value to recognize other than temporary declines in the underlying value. Gains and losses on disposals of investments are included in investment income. d) Loans Personal loans, residential mortgage loans and commercial loans are recorded at principal amounts plus accrued interest, less an allowance for impaired loans. Loan Interest Interest income from loans is recorded on an accrual basis except for loans classified as impaired. Loans are classified as impaired when, in management’s opinion, there is no longer reasonable assurance that the full amount of principal and interest will be collected. Generally loans on which repayment of principal or payment of interest is 90 days past due are automatically considered impaired. When a loan is classified as impaired, no further interest income is recognized and all accrued but uncollected interest is provided for. Until such time as collectibility is assured, subsequent interest receipts are applied to reduce the recorded investment in the loans. Loan Fees Commercial lending application fees and mortgage brokerage and incentive fees are deferred and amortized to interest income over the term of the loan. Mortgage prepayment penalties are recorded in income when charged. The net unamortized fees are included in the related loan balance in accordance with CICA’s Accounting Guideline 4 (AcG-4), Fees and Costs Associated with Lending Activities. Impaired Loans

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

5

Alterna Savings establishes and maintains an allowance for impaired loans that is considered the best estimate of probable credit-related losses existing in its loan portfolio giving due regard to current conditions. The allowance includes both specific and general provisions, reviewed on a regular basis by management. The allowance is increased by provisions for impaired loans which are charged to earnings and reduced by write-offs, net of recoveries. Specific allowances are established on individual loans in accordance with DICO By-law #6 and the Office of the Superintendent of Financial Institutions (“OSFI”) regulations. The specific allowance is the amount that is required to write down the loan to the discounted expected future cash flows at the effective interest rate and, if not measurable, to the fair value of any security, net of expected costs of realization. The general allowance is established by reviewing the credit portfolio’s inherent risks, economic conditions and trends. A general allowance is established when evidence of impairment losses within groups or classifications of loans exists but is not sufficient to allow the determination of specific allowances. Loan Costs Loan costs include the provision for loan losses and collection costs. e) Property and Equipment Property and equipment is presented at cost less accumulated amortization. Amortization is calculated on a straight-line basis over the estimated useful lives of the assets as follows:

Buildings 10 years Furniture and equipment 5 to 10 years Computer hardware and software 3 to 7 years Leasehold improvements Term of lease plus one option period f) Employee Benefit Plans Alterna Savings maintains three pension plans for current employees and retirees, and one post-retirement benefits program. Employees of former CS CO-OP are eligible to participate in the defined benefit (“DB”) career average pension plan that provides for an early retirement incentive; and, the senior executives are provided with a Supplementary Employee Retirement Plan (“SERP”). Both plans provide for pensions based on length of service and career average earnings. Employees of former Metro are eligible to participate in the defined contribution (“DC”) pension plan which prescribes both employer and employee contributions. An early retirement incentive is also provided, as well as a post-retirement benefits program to eligible retirees. All new eligible employees of Alterna Savings in 2005 have been offered a choice of participating in either one of the defined benefit or defined contribution pension plan. For the DB pension plan, the SERP and the post-retirement benefits program, plan assets are valued at market values. Benefits costs and accrued benefits are determined based upon actuarial valuations using the projected benefit method prorated on service and management’s best estimates. The expected return on plan assets is based on the fair value of plan assets. Actuarial gains and losses as well as past service costs are deferred and amortized over the expected average remaining service life of the employee group covered under the plans. The benefit plan expense is the net of the cost of the post-employment benefits for the current year’s service, interest expense on plan liabilities, interest revenue on plan assets, and the amortization of pension adjustments on a straight-line basis over the expected average remaining service life of the employee group covered under the plan. For the DC pension plan, annual pension expense is equal to Alterna Savings’ contribution to the plan.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

6

g) Deferred Charges Costs incurred in the start-up of Alterna Bank are included in deferred charges. They are amortized straight-line over a period of up to five years. Also included in deferred charges are prepaid administration fees, amortized straight-line over a five year period, and deferred acquisition costs, recorded as an other asset until the amalgamation with Metro on April 1, 2005. h) Income Taxes Alterna Savings uses the liability method of income tax allocation where temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes give rise to future income taxes. i) Other Income Service charges, ABM networks, commissions and other revenues are recognized as revenue when the related services are performed or are provided. j) Foreign Currency Monetary assets and liabilities denominated in a foreign currency are translated into Canadian dollars at the rate of exchange prevailing at year end; income and expenses are translated at the annual average rate. Foreign currency exchange gains and losses are recognized in other income during the year. k) Derivative Financial Instruments Alterna Savings follows the CICA’s Accounting Guideline 13 (AcG-13), Hedging Relationships, when accounting for its hedging relationships. AcG-13 sets out the criteria that must be met in order to apply hedge accounting for derivatives. The guideline also provides detailed guidance on the identification, designation, documentation and effectiveness of hedging relationships, for purposes of applying hedge accounting, and the discontinuance of hedge accounting.

Alterna Savings utilizes derivative financial instruments in its management of interest rate exposure, and not for trading or speculative purposes. Alterna Savings uses interest rate swaps to fix the interest rate received on a portion of its variable rate loan portfolio and purchased call options to offset the exposure related to its index-linked term deposits. All derivative financial instruments are accounted for using hedge accounting. Derivatives are generally recorded off-balance sheet as hedges with the realized and unrealized gains and losses resulting from these contracts recognized in income on a basis consistent with the hedged on-balance sheet financial asset or liability. These amounts are recorded within interest income on the statement of income and reserves. Where an interest rate swap agreement is terminated prior to its maturity, the resulting gain or loss is amortized over the original term of the agreement. In the event that the financial instrument is deemed no longer effective as a hedge, the derivative instrument would be accounted for at fair value, with changes in fair value recognized in current period earnings. Premiums on index call options are amortized to interest expense over the life of the contract.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

7

3. BUSINESS COMBINATION On April 1, 2005, CS CO-OP amalgamated with Metro commencing operations as of that date as Alterna Savings. The details of the exchange of former CS CO-OP and former Metro shares for Alterna Savings shares can be found in note 13. As the amalgamation was effected by an exchange of shares, the fair value of the net assets acquired is used to approximate the cost of purchase. The excess of the fair value of the net assets acquired over the book value of the shares issued has been recorded as contributed surplus. The transaction has been accounted for by the purchase method as prescribed under CICA Section 1580, Business Combinations and EIC-42, Costs Incurred on Business Combinations. Under Section 1580, the former CS CO-OP has been identified as the acquirer. The operating results for the former Metro subsequent to the date of the acquisition are included in the financial statements. In accordance with EIC-42, the costs directly incurred in effecting the business combination were included as part of the purchase price. Other merger-related expenses are included as integration costs on the statement of income and reserves. The following table summarizes the estimated fair values of Metro’s net assets acquired and the cost of purchase (in 000’s):

Assets acquired: Cash resources $3,458 Investments 41,649 Loans 499,857 Capital assets 7,002 Other assets 3,987

Total assets $555,953

Liabilities assumed: Deposits $471,719 Operating loan 40,038 Other liabilities 6,929

Total liabilities $518,686

Fair value of net assets acquired $37,267

Shares issued: Class A, Series 2 $10,135 Class B, Series 1 4,350 Membership shares 597 15,082

Acquisition costs 3,132 18,214

Contributed surplus 19,053

Cost of purchase $37,267

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

8

4. INVESTMENTS 2005

(000’s) 2004

(000’s)

Bonds $81,489 $155,609 Money market instruments - 66,932 Residential mortgages purchased as investments 13,719 13,798 Credit Union Central of Ontario (“CUCO”) shares 10,328 - Term deposits 5,132 5,132 Other 5,343 5,037 $116,011 $246,508 On April 1, 2005, Alterna Savings became a member of CUCO. As a condition of maintaining a membership in CUCO, Alterna Savings is required to maintain an investment in shares of CUCO equal to 0.60% of its total assets as at the preceding calendar year end. As a condition of maintaining membership in CUCO in good standing, Alterna Savings is also required to maintain on deposit in CUCO’s liquidity pool an amount equal to 7% of its own membership shares and deposits as at the preceding calendar year end. The deposits bear interest at variable rates and are included in cash equivalents.

5. LOANS 2005

(000’s) 2004

(000’s)

Personal loans $279,703 $198,550 Residential mortgage loans 817,088 477,641 Commercial loans 313,449 191,920 1,410,240 868,111

Less allowance for impaired loans (note 6) (4,524) (4,399) $1,405,716 $863,712

6. ALLOWANCE FOR IMPAIRED LOANS

2005 (000's)

2004 (000's)

Personal

Loans

Residential Mortgage

Loans Commercial

Loans Total Total

Balance, beginning of year $2,375 $76 $1,948 $4,399 $6,372 Add: Acquisition of Metro 620 - 131 751 - Less: Loans written off (1,565) - (3) (1,568) (2,065) Add: Recoveries on loans previously

written off 412 - - 412 344 Add: Allowance charged to operations 161 (28) 397 530 (252) Balance, end of year $2,003 $48 $2,473 $4,524 $4,399 The allowance for impaired loans includes a general allowance of $2,320,000 (2004 - $2,085,000): $2,158,000 (2004 – $1,840,000) pertains to commercial loans, $114,000 (2004 - $195,000) to personal loans and $48,000 (2004 - $50,000) to residential mortgage loans.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

9

The balance of loans identified as impaired, prior to any recovery from collateral on these loans, at the end of the year was as follows: 2005 2004 (000's) (000's)

Personal Loans $1,902 $1,621 Residential Mortgage Loans 1,128 1,450 Commercial Loans 2,488 108 $5,518 $3,179

Percentage of total loans 0.39% 0.37% No write-downs were made in respect of restructured loans during the year.

7. PROPERTY AND EQUIPMENT

2005(000’s)

2004 (000’s)

Cost

Accumulated Depreciation

Net Book Value Cost

Accumulated Depreciation

Net Book Value

Land $4,369 $- $4,369 $3,028 $- $3,028 Buildings 9,640 5,904 3,736 8,917 5,210 3,707 Furniture and equipment 10,055 5,267 4,788 7,571 4,312 3,259 Computer hardware and software 32,026 17,481 14,545 33,291 21,625 11,666 Leasehold improvements 6,490 2,630 3,860 3,865 1,981 1,884

$62,580 $31,282 $31,298 $56,672 $33,128 $23,544 Included in computer hardware and software costs in 2004 was $8,180,000 for the core banking system which was not placed into operation, and therefore did not begin amortization until July 1, 2005. Assets under capital leases totaling $5,495,000 (2004 - $6,450,000) are included in computer hardware and software. Amortization expense and accumulated amortization on capital leases were $933,000 and $3,321,000, respectively (2004 - $1,271,000 and $3,593,000, respectively). Assets acquired by means of capital leases are non-cash transactions for purposes of the cash flow statement, and consequently have not been presented as either a financing or an investing activity. Total amortization charged to income in 2005 was $4,950,000 (2004 - $4,297,000) and is included in operating expenses on the statement of income and reserves.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

10

8. OTHER ASSETS 2005

(000’s) 2004

(000’s)

Accrued benefit asset (note 17) $4,226 $5,321 Call options (note 20) 2,469 2,465 Deferred charges 616 1,474 Income tax receivable 539 386 Interest receivable - Swap agreements 388 637 Other 2,115 1,506 $10,353 $11,789

9. DEPOSITS 2005

(000’s) 2004

(000’s)

Demand deposits $551,273 $356,622 Term deposits 404,629 260,490 Registered plans 641,306 503,279 $1,597,208 $1,120,391

10. BORROWING FACILITIES Lines of Credit Alterna Savings has access to a $23,500,000 line of credit with the Royal Bank of Canada and lines of credit of $10,000,000 and U.S. $500,000 with CUCO. The $23,500,000 line of credit is payable on demand within 90 days, bears interest at prime rate and is collateralized by fixed income securities having a total face value of $23,000,000. The lines of credit at CUCO are payable on demand within 30 days, bear interest at prime and are secured by an assignment of book debt and a general security agreement. There was no outstanding balance on these lines of credit at the end of the year (2004 - $nil). Operating Loan Alterna Savings has an authorized operating term loan limit of $69,500,000 with CUCO. The operating term loan is payable on demand, bears interest at bankers acceptance rates plus 30 to 40 basis-points and is secured by an assignment of book debt and a general security agreement. There was no outstanding balance on the operating term loan at the end of the year (2004 - $nil).

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

11

11. OTHER LIABILITIES 2005

(000’s) 2004

(000’s)

Trade payables $7,372 $6,295 Certified and official cheques 2,870 1,273 Salaries and benefits payable 2,444 1,608 Capital lease obligations (note 12) 2,286 2,851 Acquisition costs payable 1,841 - Dividend payable 1,319 955 Deferred revenue 364 - $18,496 $12,982

12. CAPITAL LEASE OBLIGATIONS 2005

(000’s) 2004

(000’s) Capital lease obligations repayable monthly and maturing at various dates up

to January 2010, secured by related property and equipment with implicit interest rates from 3.61% to 12.74% (see note 7). $2,286 $2,851

Future minimum lease payments are as follows (in 000’s):

2006 $903 2007 730 2008 453 2009 405 2010 34 Thereafter - 2,525 Less implicit interest included above (239) $2,286

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

12

13. MEMBERS’ SHARE ACCOUNTS a) Authorized: The authorized share capital of Alterna Savings consists of the following:

i. an unlimited number of Class A special shares, issuable in series ii. an unlimited number of Class B special shares, issuable in series iii. an unlimited number of Class C special shares, issuable in series iv. an unlimited number of membership shares

b) Share Features: The rights, privileges, restrictions, terms and conditions attaching to the shares are as follows: Voting All Class A, Class B and Class C shares are non-voting. Membership shares are voting with each member being entitled to one vote, regardless of the number of membership shares held by the member, provided that the member is at least eighteen years of age. Each member under the age of eighteen is required, as a condition of membership, to own one membership share with an issue price of $1. All other members are required, as a condition of membership, to own one membership share with an issue price of $15. Dividends Holders of Class A, Class B, Class C and membership shares are entitled to non-cumulative dividends, when and if declared by the Board of Directors, in order of priority with Class A to receive dividends first, Class B, Class C then membership shares. All Series holders will rank equally within their class in terms of priority in payment of dividends. The dividend rate for Class A, Series 1, Class A, Series 2 and Class B, Series 1 was approved by the Board of Directors at 6.13%, 4.50% and 1.0%, respectively for 2005. Transferability No Class A, Class B, Class C or membership share is transferable to any person, other than a person who is a member of Alterna Savings, and then only on the approval of the Board of Directors. Participation upon Liquidation, Dissolution or Winding-Up Class A, Class B and Class C shareholders, in order of priority, are entitled to redeem their shares on liquidation, dissolution or wind-up. Holders of membership shares are entitled to the remaining property of Alterna Savings. Redemption or Cancellation Class A, Series 1 holders may not redeem their shares prior to the fifth anniversary of the 1st issuance of shares by the former CS CO-OP, or August 2007. All redemptions are subject to the discretion of the Board of Directors and will be limited annually to a maximum of 10% of the Class A, Series 1 shares outstanding at the end of the immediately preceding fiscal year. The redemption price will equal the shares’ face value, plus all declared and unpaid dividends thereon. Alterna Savings will also have the option to purchase for cancellation all or any part of the outstanding Class A, Series 1 shares at any time after the expiry of the five years from the issue date. Class A, Series 2 holders may request redemption of their shares on June 30th or December 31st annually. The Board of Directors will consider, approve, and if necessary prorate requests for redemption, with redemption requests of the estate of deceased members and expelled members taking priority. All redemption requests are subject to discretion by the Board. Redemptions will be limited semi-annually to a maximum of 5% and annually to a maximum of 10% of the Class A, Series 2 shares outstanding at the end of the immediately preceding fiscal year. The redemption price will equal the shares’ face value, plus all declared and unpaid dividends thereon. Alterna Savings will also have the option to purchase for cancellation all or any part of the outstanding Class A, Series 2 shares at any time. Class B, Series 1 holders can request redemption of their shares however all redemptions are subject to the discretion of the Board of Directors and will be limited annually to a maximum of 10% of the Class B, Series 1 shares outstanding at the end of the immediately preceding fiscal year. The redemption price will equal the shares’ face value, plus all

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

13

declared and unpaid dividends thereon. Alterna Savings will also have the option to purchase for cancellation all or any part of the outstanding Class B, Series 1 shares held by the estates of deceased members or expelled members at any time. As no Class C shares have been issued, no redemption rights or restrictions are attached to the shares at this time. Membership shares are redeemable at their issue price only when the member withdraws from membership in Alterna Savings. They are considered liabilities for accounting purposes because they are redeemable at the option of the holder. c) Issued and Outstanding: On the amalgamation with Metro on April 1, 2005, all 15,621,000 issued and outstanding Class A, Series 1 shares of CS CO-OP were exchanged for Class A, Series 1 shares of Alterna Savings on a one-for-one basis. Each $15 share issued and outstanding in the capital of former CS CO-OP was converted into fifteen one-dollar membership shares of Alterna Savings. The shares of Alterna Savings carry the same rights and restrictions as the shares of the former CS CO-OP. All 10,135,000 issued and outstanding Class A investment shares with an issue price of $1 per share in the capital of Metro were converted into 10,135,000 Class A, Series 2 of Alterna Savings at a price of $1 per share. All 718,000 issued and outstanding Class B bonus shares with an issue price of $1 per share in the capital of Metro were converted into 718,000 Class B, Series 1 of Alterna Savings at a price of $1 per share. Issued and outstanding five-dollar membership shares of Metro were converted into five one-dollar membership shares of Alterna Savings up to fifteen membership shares of Alterna Savings for each member. Thereafter each five-dollar membership share of Metro was converted into five one-dollar Class B, Series 1 shares of Alterna Savings. Of the 4,229,000 issued and outstanding membership shares of Metro, 3,632,000 were converted to Class B, Series 1 and 597,000 were converted to membership shares of Alterna Savings. The continuity of the members’ share accounts for the year ended December 31, 2005 is as follows (in 000’s):

Class A Special Shares

Class B Special Shares

Membership Shares

Series 1 Series 2 Series 1 Number

of Shares $

Number of

Shares $

Number of

Shares $

Number of

Shares $ Issued and outstanding as at December 31, 2003 15,621 $15,358 - $- - $- 144 $2,122

Net shares redeemed - - - - - - (3) (55)Issued and outstanding as at December 31, 2004 15,621 15,358 - - - - 141 2,067

Issued on amalgamation - - 10,135 10,135 4,350 4,350 2,514 597Net shares redeemed - - (288) (288) (530) (530) (30) (39)

Issued and outstanding as at December 31, 2005 15,621 $15,358 9,847 $9,847 3,820 $3,820 2,625 $2,625 d) Dividends Declared: In November 2005, the Board of Directors approved a $1,319,000 dividend to holders of record of 29,288,000 shares as of December 31, 2005 to be paid in January 2006. Class A, Series 1 shareholders will receive a cash dividend of $958,000, Class A, Series 2 shareholders will receive a dividend of $332,000 payable in cash and/or additional Class B, Series 1 shares and Class B, Series 1 shareholders will receive a dividend of $29,000 payable in additional Class B, Series 1 shares. As at December 31, 2005, this dividend is accrued for and presented net of income taxes of $213,000 in the financial statements, for a balance of $1,106,000 (2004 - $640,000).

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

14

14. INTEREST INCOME AND INTEREST EXPENSE 2005

(000’s) 2004

(000’s)

Interest Income: Personal loans $16,583 $14,244 Residential mortgage loans 37,083 27,078 Commercial loans 16,030 10,898 Swap agreements 1,458 1,138

$71,154 $53,358 Interest Expense:

Demand deposits $1,790 $892 Term deposits 10,973 7,989 Registered plans 19,960 17,378 Borrowings 271 2,286

$32,994 $28,545

15. OTHER INCOME 2005

(000’s) 2004

(000’s) Service charges $5,595 $4,596 ABM networks 3,516 3,326 Commissions 4,077 3,006 Other 932 339 $14,120 $11,267

16. OPERATING EXPENSES 2005

(000’s) 2004

(000’s) Salaries and benefits $26,518 $18,451 Administration 12,916 9,828 Data processing 7,252 5,315 Occupancy 5,586 3,539 Deposit insurance premiums 1,367 1,159 Marketing and community relations 1,087 724 $54,726 $39,016

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

15

17. EMPLOYEE BENEFIT PLANS Defined Pension and Benefits Plans The assets and accrued benefit obligation of the defined benefits pension plans (DB pension plan and SERP) and the post-retirement benefits program were measured as at December 31, 2005, and are detailed as follows:

2005

(000’s) 2004

(000’s)

Pension Benefits Total Total

Accrued benefit obligation:

Balance, beginning of year $21,762 $- $21,762 $19,349 Plan assumption - 1,325 1,325 - Current service cost 765 68 833 681 Interest cost 1,398 59 1,457 1,293 Employee contributions 535 - 535 496 Plan amendments - - - 334 Benefits paid (1,395) (27) (1,422) (1,444)Actuarial losses 3,456 143 3,599 1,053 Balance, end of year $26,521 $1,568 $28,089 $21,762

Plans’ assets:

Fair value, beginning of year $22,407 $- $22,407 $17,618 Actual return on plan assets 1,789 - 1,789 1,429 Employer contributions 1,186 27 1,213 4,308 Employee contributions 535 - 535 496 Benefits paid (1,395) (27) (1,422) (1,444)Fair value, end of year $24,522 $- $24,522 $22,407

Overfunded (underfunded) status of plans (1,999) (1,568) (3,567) 645 Unamortized net actuarial losses 7,286 142 7,428 4,310 Unamortized past service costs 785 - 785 928 Unamortized transitional gains (420) - (420) (562)Accrued benefit asset (liability) $5,652 ($1,426) $4,226 $5,321

As at December 31, 2005, the under funded status of the DB pension plan was $3,155,000 (2004 - $685,000) and the over funded status of SERP was $1,156,000 (2004 - $1,330,000). The post-retirement benefits program of Metro was assumed by Alterna Savings on amalgamation. The accrued benefit asset of $4,226,000 (2004 - $5,321,000) is included in other assets on the balance sheet. The following is a summary of the weighted average significant actuarial assumptions used in measuring the plans’ accrued pension benefit asset: 2005 2004 Pension Benefits Pension Discount rate 5.25% 5.25% 6.25% Rate of compensation increase 4.06% 3.25% 4.00% Expected long-term rate of return on plan assets 6.84% n/a 6.81% The per capita cost of covered medical benefits is expected to decrease 1% per year until the rate reaches 4.5%.

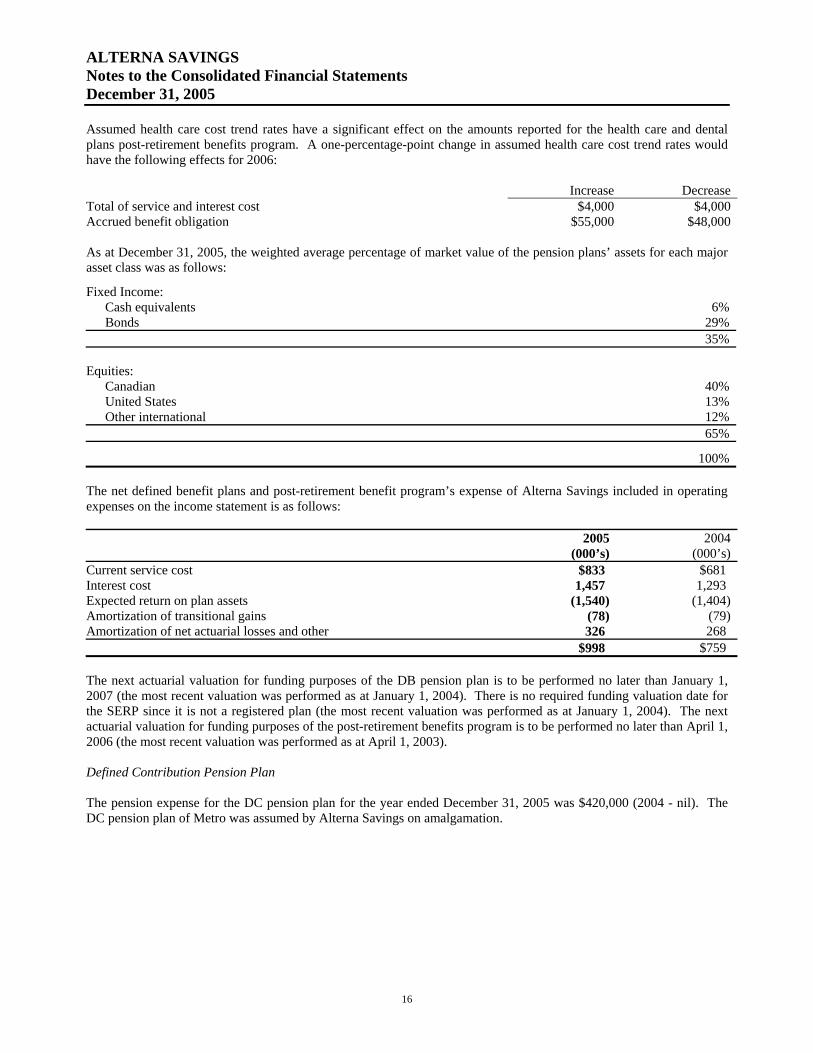

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

16

Assumed health care cost trend rates have a significant effect on the amounts reported for the health care and dental plans post-retirement benefits program. A one-percentage-point change in assumed health care cost trend rates would have the following effects for 2006: Increase Decrease Total of service and interest cost $4,000 $4,000 Accrued benefit obligation $55,000 $48,000 As at December 31, 2005, the weighted average percentage of market value of the pension plans’ assets for each major asset class was as follows:

Fixed Income: Cash equivalents 6% Bonds 29%

35% Equities:

Canadian 40% United States 13% Other international 12%

65% 100% The net defined benefit plans and post-retirement benefit program’s expense of Alterna Savings included in operating expenses on the income statement is as follows: 2005

(000’s) 2004

(000’s) Current service cost $833 $681 Interest cost 1,457 1,293 Expected return on plan assets (1,540) (1,404) Amortization of transitional gains (78) (79) Amortization of net actuarial losses and other 326 268 $998 $759 The next actuarial valuation for funding purposes of the DB pension plan is to be performed no later than January 1, 2007 (the most recent valuation was performed as at January 1, 2004). There is no required funding valuation date for the SERP since it is not a registered plan (the most recent valuation was performed as at January 1, 2004). The next actuarial valuation for funding purposes of the post-retirement benefits program is to be performed no later than April 1, 2006 (the most recent valuation was performed as at April 1, 2003). Defined Contribution Pension Plan The pension expense for the DC pension plan for the year ended December 31, 2005 was $420,000 (2004 - nil). The DC pension plan of Metro was assumed by Alterna Savings on amalgamation.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

17

Subsequent Event In January 2006, the Board of Directors of Alterna Savings approved changes to Alterna Savings’ employee benefit plans. Effective March 1, 2006, the post-retirement benefits program will cease for employees retiring after February 28, 2006 who have not retired and are not eligible to retire at that date. Effective January 1, 2008, a new defined contribution plan will be created. Pension benefits for employees participating in an Alterna Savings pension plan will henceforth accrue benefits under this new plan and all existing DC pension plan assets will be transferred into this new plan. As of that date, all benefits will cease to accrue under the existing DB pension plan and SERP. Early retirement benefits will be removed for all employees who are not eligible for retirement prior to January 1, 2008. The effect of the curtailments is not estimable at this time.

18. INCOME TAXES

Significant components of the future tax liability of Alterna Savings are as follows: 2005

(000’s) 2004

(000’s) Capital assets $1,100 $1,216 Deferred pension expense 912 1,001 Deferred start-up costs - 80 Fair value increment due to business combination 527 - Allowance for impaired loans (502) (439) Loss carryforward (124) - Other (103) (213) $1,810 $1,645 The reconciliation of income tax computed at the statutory rates to income tax expense is as follows:

2005 2004 Amount

(000’s) Percent Amount (000’s) Percent

Tax at combined federal and provincial rates $2,128 43% $2,494 43% Federal large corporations tax 352 8% 353 6% Credit Unions deduction (1,066) (25%) (1,271) (23%) Loss carryback - -% (322) (5%) Permanent differences (250) (4%) - -% Other - net (267) (4%) (138) (2%) $897 18% $1,116 19%

Non-capital losses are available for carryforward in the amount of $665,000 which will expire in 2012. The Ontario Corporate Minimum tax credits carried forward will also expire as follows (in 000’s):

2012 $74 2013 207 2014 21 2015 132 $434

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

18

19. FINANCIAL INSTRUMENTS

(a) Fair Value The amounts set out in the table below represent the estimated fair values of the financial instruments of Alterna Savings, including the fair values of loans calculated before allowance for impaired loans, using the valuation methods and assumptions described below.

2005

(000’s) 2004

(000’s) Book value Fair value Book value Fair value

Financial assets: Cash and cash equivalents $180,472 $180,459 $79,777 $79,775 Investments 116,011 116,220 246,508 248,698 Loans 1,410,240 1,411,954 868,111 872,295 Other assets -call options 2,469 10,367 2,404 4,698 Financial liabilities: Deposits (1,597,208) (1,604,669) (1,120,391) (1,135,676) The estimated fair value amounts approximate the amounts at which instruments could be exchanged in a current transaction between willing parties who are under no compulsion to act. Fair values are based on estimates using present value and other valuation techniques, which are significantly affected by the assumptions used concerning the amount and timing of estimated future cash flows and discount rates. Because of the estimation process and the need to use judgment, the aggregate fair value amounts should not be interpreted as being necessarily realizable in an immediate settlement of instruments. The fair values of financial instruments are generally determined as follows: Investments and call options - at market offer price quoted by investment dealers. Personal loans, residential mortgage loans and commercial loans, and deposits - at discounted cash flows using prevailing interest rates of instruments with similar remaining terms. The fair values of all types of loans are calculated before allowance for impaired loans. The fair values of financial instruments with a term of less than one year approximate their carrying values, due to their short term nature, except where otherwise indicated.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

19

(b) Interest Rate Risk Interest rate risk refers to the potential impact of changes in interest rates on Alterna Savings’ earnings when maturities of its financial liabilities are not matched with the maturities of its financial assets. The interest rate risk is being managed within Alterna Savings’ Asset/Liability Management policies. The following table sets out the carrying amounts (before allowance for impaired loans) and weighted average interest rates of rate sensitive financial instruments:

2005 (000’s)

2004 (000’s)

Maturity Variable

rate demand

Under 3 months

3 to 12 months

1 to 5 years Total Total

Cash and cash equivalents: Carrying Amount $35,390 $145,082 $- $- $180,472 $79,777 Interest Rates - 3.28% - - 2.63% 1.50% Investments: Carrying Amount $10,671 $- $5,633 $99,707 $116,011 $246,508 Interest Rates - - 3.49% 4.07% 4.04% 3.47% Personal loans: Carrying Amount $256,219 $5,536 $9,243 $8,705 $279,703 $198,550Interest Rates 6.83% 6.23% 7.36% 7.50% 6.86% 6.81% Residential mortgage loans: Carrying Amount $88,950 $29,781 $74,955 $623,402 $817,088 $477,641 Interest Rates 3.04% 4.61% 4.84% 5.02% 4.77% 5.31% Commercial loans: Carrying Amount $54,305 $12,543 $37,893 $208,708 $313,449 $191,920 Interest Rates 5.26% 6.92% 6.67% 6.10% 6.05% 6.04%

TOTAL $445,535 $192,942 $127,724 $940,522 $1,706,723 $1,194,396

Deposits: Carrying Amount $590,362 $164,482 $314,796 $527,568 $1,597,208 $1,120,391 Interest Rates 0.43% 2.82% 2.82% 3.55% 2.18% 2.32%

TOTAL $590,362 $164,482 $314,796 $527,568 $1,597,208 $1,120,391 In the event of a 1% decrease in interest rates, the expected net interest income would decline by $1,676,000 over the next 12 months. c) Credit Risk Loans Alterna Savings mitigates its credit risk exposure by defining its target market area, and by limiting the principal amount of credit to a borrower at any given time: $250,000 in personal loans per borrower, $1,500,000 in residential mortgage loans per borrower, $20,000,000 in commercial loans per borrower and $25,000,000 in aggregate loans per borrower and connected persons; by performing a credit analysis prior to approval of the loan; by obtaining collateral when appropriate; by employing risk based pricing; and for commercial loans by limiting the concentration by industry and geographic location.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

20

Investments Alterna Savings invests surplus liquidity in the short-term money market, securities that are secured by mortgages and in the bond market. All investments held in short-term instruments are rated R1-L or better by the Dominion Bond Rating Service. All securities that are secured by mortgages are guaranteed under the National Housing Act. All investments in bonds are rated A or better by Dominion/Moody’s Bond Rating Service. Investments are diversified by limiting investments in any one issuer to a maximum of 25% of the total portfolio for deposits other than those at the Government of Canada and its Crown Corporations, and a maximum dollar value of $5,000,000 to $50,000,000 depending on the credit risk of the issuer. d) Liquidity Risk Liquidity risk refers to the risk that Alterna Savings will encounter difficulty in raising funds to meet commitments associated with financial instruments. To mitigate this risk, Alterna Savings maintains, at all times, liquidity that is adequate in relation to the business carried on.

20. DERIVATIVE FINANCIAL INSTRUMENTS a) Swap Agreements Alterna Savings uses interest rate swap agreements to mitigate risks associated with interest rate fluctuations and to control the matching of the cash flow maturities and interest adjustment dates of its assets and liabilities. A summary of the fixed notional principal amounts on which Alterna Savings is obligated to pay a floating rate of interest and receive a fixed rate is given below:

2005(000’s)

2004 (000’s)

Maturity Notional

Principal Fixed Rate

Received

Year End Floating

Rate Notional Principal

Fixed Rate Received

Year End Floating

Rate 2006 $10,000 3.36% 3.27% $- - - 2007 25,000 3.44% 3.29% 25,000 3.44% 2.56% 2008 10,000 3.68% 3.37% 10,000 3.68% 2.59% 2009 50,000 3.97% 3.37% 50,000 3.97% 2.59% 2009 50,000 4.00% 3.32% 50,000 4.00% 2.59%

$145,000 3.82% 3.33% $135,000 3.86% 2.58% During the year, three swap agreements with notional principals totaling $42,000,000 matured. No swaps were disposed of in 2005 (2004 - one swap agreement of $50,000,000). As at December 31, 2005, the remaining balance of accumulated gains and losses on disposal are respectively included in other assets ($147,000; 2004 - $438,000) and other liabilities ($68,000; 2004 - $203,000). As at December 31, 2005, the net interest receivable amounted to $388,000 (2004 - $637,000). As at December 31, 2005, the swaps had a net unrealized loss of $401,000 (2004 – net unrealized gain of $1,795,000). The fair value has been determined by market offer prices quoted by investment dealers. b) Call Options As at December 31, 2005, Alterna Savings had issued $32,506,000 of indexed term deposits to its members (2004 - $30,288,000). These term deposits have maturities of 3 to 5 years and pay interest to the depositors, at the end of the term, based on the performance of the S&P/TSX60 Index, the proprietary G7 Equity Index, or the Euro North America Equity Index. Alterna Savings uses call options on the above indices with equivalent maturities to offset the exposure associated with these products. The unamortized cost of these call options is $2,469,000 and is included in other assets (see note 8). The options have fair values which fluctuate depending on the volatility of the respective Index and the general market outlook. As at December 31, 2005, the fair value of the call options amounted to $10,367,000 (2004 - $4,698,000).

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

21

21. COMMITMENTS AND CONTINGENCIES a) Operating Leases Alterna Savings has minimum annual payment obligations under operating leases as follows (in 000’s):

2006 $2,116 2007 1,781 2008 1,590 2009 1,432 2010 928 Thereafter 2,435 $10,282 b) Credit Instruments As at December 31, 2005, the credit instruments approved but not yet disbursed were as follows:

Total (000’s) Average term Average rate

Personal loans $200 3.6 years 9.76% Residential mortgage loans $6,956 4.8 years 4.94% Commercial term loans $7,485 1.0 years Prime plus 1% Commercial mortgage loans $13,918 5.0 years Prevailing rates on date disbursed Lines of credit unfunded $343,928 - Prevailing rates on date disbursed c) Contingencies In the normal course of operations, Alterna Savings becomes involved in various claims and legal proceedings. While the final outcome with respect of claims and legal proceedings pending at December 31, 2005 cannot be predicted with certainty, it is the opinion of management that their resolution will not have a material adverse effect on Alterna Savings’ financial position or results of operations. d) Guarantees Letters of Credit Arising through the normal course of business, Alterna Savings has guaranteed $1,196,000, representing the maximum potential amount of future payments it would be required to make under the guarantees, in support of commercial loans to members. Letters of credit are issued at the request of members in order to secure their payment or performance obligations to a third party. These guarantees represent an irrevocable obligation of Alterna Savings to pay the third party beneficiary upon presentation of the guarantee and satisfaction of the documentary requirements stipulated therein. In the event of a call on such commitments, Alterna Savings has recourse against the member. Generally the term of these guarantees do not exceed 1 year. The types and amount of collateral security held by Alterna Savings in support of guarantees and letters of credit is the same as is held for loans. As at December 31, 2005, no liability has been recorded on the balance sheet as no letters of credit have been called upon.

Credit Card Agreement In accordance with a credit card service agreement entered into in May 2005, Alterna Savings has guaranteed the credit card debt of its business account holders such that if a business account falls into arrears, the credit card service provider may request that Alterna Savings pay the amount due. Alterna Savings has legal recourse against the business account holder if required to pay any amounts in arrears. All credit decisions with respect to business accounts are made by Alterna Savings. As of December 31, 2005, no business accounts have been submitted to Alterna Savings for reimbursement by the credit card service provider.

ALTERNA SAVINGS Notes to the Consolidated Financial Statements December 31, 2005

22

22. SEGMENT DISCLOSURES Alterna Savings manages its business as one integrated operating segment as it operates principally in personal and commercial banking in the provinces of Ontario and Quebec. Accordingly, it has only one reporting segment for financial reporting purposes.

23. OTHER INFORMATION a) Restricted Party Transactions Alterna Savings employs the definition of restricted party contained in section 82 of Regulation 76/95 to the Credit Unions and Caisses Populaires Act. A restricted party includes a person who is, or has been within the preceding twelve months, a director, officer, committee member, or any corporation in which the person owns more than 10% of the voting shares, his or her spouse, their dependent relatives who live in the same household as the person, and any corporation controlled by such spouse or dependent relative. At the end of the year, the total amount of loans related to restricted parties, as defined, was approximately $2,772,000 (2004 - $938,000). There was approximately $114,000 (2004 - $49,000) in interest earned for the year. b) Expenses Relative to Board of Directors The Directors and members of the Credit Committee are remunerated at rates to be fixed annually at the beginning of each year by the Board, and are also entitled to be paid their travelling and other expenses properly incurred by them in connection with the affairs of Alterna Savings. During the year, remuneration paid to Directors and Credit Committee members amounted $311,000 (2004 - $192,000) and other expenses incurred totalled $61,000 (2004 - $32,000). As at December 31, 2005, Alterna Savings’ Board consisted of 23 Directors, while CS CO-OP’s Board included 12 Directors on December 31, 2004. In accordance with Alterna Savings’ by-laws, the number of Directors is to be reduced to 15 by 2008. c) Executive Remuneration Executives include the President & CEO, Executive VP & Chief Integration Officer (effective April 1, 2005), Senior VP Human Resources & CFO, Senior VP Service Delivery, Senior VP Business Development, VP Marketing and Communications (effective April 1, 2005), VP Organizational Effectiveness (effective April 1, 2005) and VP Corporate Affairs. Remuneration earned by executives during the year included the following: 2005

(000’s) 2004

(000’s) Base remuneration $1,023 $808 Performance incentives 226 189 Taxable benefits 60 86 $1,309 $1,083

24. COMPARATIVE AMOUNTS Certain 2004 comparative amounts have been reclassified to conform to the consolidated financial statement presentation adopted in 2005.