Embed Size (px)

Citation preview

The Consultant’s final report is a document of a team of consultants. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention

is directed to the “Terms of Use” section of this website.

Consultant’s Final Report Project No. 43224 Final Report Jun 2013

RETA 7529- Study on South Asia Regional Power Exchange Prepared with the Assistance from Asian Development Bank

ADB RDTA 7529: South Asia Regional Power Exchange Study Page ii

Study on a South Asia Regional Power Exchange

Prepared with assistance from

Asian Development Bank

June 2013

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 3

Disclaimer

The views expressed in this publication are those of the RDTA 7529 Project Team consisting of

external consultants appointed by the Asian Development Bank (ADB), and do not necessarily

reflect the views and policies of South Asia Association for Regional Cooperation (SAARC), ADB,

its Board of Governors, or the governments they represent.

This Final Report (“Report) is prepared for the purpose of disseminating findings under the RDTA.

The project team incorporated feedback from representatives of the SAARC Member States and

the SAARC Energy Centre to finalise the report.

By making any designation of or reference to a particular territory or geographic area, or by using

the term “country”in this document, SAARC or ADB does not intend to make any judgments as to

the legal or other status of any territory or area.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 4

Preface

Since the 12th SAARC Summit in 2004, the political leadership in SAARC Member States has put Energy Cooperation on top of its agenda. The SAARC Heads of States have emphasized that for accelerated and balanced economic growth, it is essential to strengthen energy cooperation in the South Asia region.

The SAARC Regional Energy Trade Study (SRETS), carried out with the

assistance of Asian Development Bank (ADB) and published in March 2010, recognized the benefits of establishing a regional power market for enhancing regional energy trade in the SAARC region. Upon SAARC Secretariat’s request, ADB submitted a Concept Paper for Technical Assistance (TA) to undertake a study on a Regional Power Exchange. The 37th session of the Standing Committee, held in Thimphu in April 2010 approved ADB’s proposal to undertake this study.

The SAARC Regional Power Exchange Study (SARPES) has thus been carried out with the assistance of the Asian Development Bank (ADB). The SARPES Report analyzes the mutually beneficial economics of a SAARC-wide interconnected ‘power system’ towards the utilization of the vast hydro-electric potential in Nepal, Bhutan, and Central Asia to meet growing demand in other parts of the system. The Study has conducted a thorough techno-economic analysis of cross-border power trading around six proposed interconnection and grid reinforcement projects covering almost all SAARC Member States. Given the huge potential of enhancing cooperation within the region through SAARC’s platform, I believe that implementation of the recommendations contained in this Study, will be a big step forward in bringing the Member States further closer together and reaping the economic benefits of such a collaboration. I commend the consultants for their efforts in collecting and analyzing the relevant data and finalization of the draft. Especially, I would like to commend the Energy Experts from SAARC Member States for their inputs and invaluable comments, and the Lead Consultants for playing a vital role in preparing this Study. We have always received all-out support and cooperation of the ADB, which I fully appreciate, and believe that this cooperation will continue in the future as well, towards a more developed South Asian Region.

Ahmed Saleem Secretary General of SAARC

June 2013

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 5

Acknowledgement

The South Asia Regional Power Exchange Study (SARPES) was conducted and

the final report was prepared under the overall guidance of Asian Development Bank

(ADB) team led by Dr. Priyantha Wijayatunga, Unit Head, Portfolio Management Unit,

Nepal Resident Mission (formerly with the South Asia Energy Division) supported by

Dr. P. N. Fernando (Senior Advisor to ADB on the study) who provided overall guidance

and valuable inputs on technical matters.

The team of experts led by Dr. Debabrata Chattopadhyay (Team Leader and

Power System Economist) and consisted of Dr. Anoop Singh (Power Sector Legal and

Regulatory Specialist) and Mr. Ricardo Austria (Power System Planning and Control

Specialist) conducted the study. Mr. Ravinder (Chief Engineer, Central Electricity

Authority, India) made available the load flow and planning data for the Indian power

system which were central to the analysis carried out in the study. Mr. S.K. Soonee (Power

Grid Cooperation Limited, India) provided extremely useful insights on the Draft Final

Report.

The administrative support from ADB was coordinated by Ms. Carmencita Roque,

Project Officer, South Asia Energy Division along with Ms. Annie Vizcarra (Consultant)

during all the activities of the technical assistance project.

Officials, individuals and organizations of the SAARC Member States, SAARC

Energy Centre led by Mr. Hilal Raza provided their support in different forms in carrying

out this study. Their critique, as well as endorsement, assisted in better articulation of the

analysis, conclusions and recommendations presented in this report. The overall

coordination on behalf of the SAARC Secretariat was carried out at the initial stages of the

study by Mr. Ghulam Dastgir (former Director Pakistan) and later by Mr. Ahmar Ismail

(Director Pakistan) with the support of Mr. Shabbir Ahmad.

South Asia Energy Division of the Asian Development Bank (ADB) extended the

required financial and coordination support for undertaking and successfully completing

this study.

SAARC Secretariat gratefully acknowledges the support extended by all these

individuals and institutions for their respective inputs in finalising the SARPES report.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 6

List of Abbreviations AERA Afghanistan Electricity Regulatory Authority ATE Appellate Tribunal for Electricity BEA Bhutan Electricity Authority BERC Bangladesh Energy Regulatory Commission BPC Bhutan Power Corporation BPDB Bangladesh Power Development Board CEA Central Electricity Authority CEB Ceylon Electricity Board CERC Central Electricity Regulatory Commission CPGCL Central Power Generation Company Limited DABM Da Afghanistan Breshna Moassessa DABS Da Afghanistan Breshna Sherkat DVC Damodar Valley Corporation ETFC Electricity Tariff Fixation Commission USE Expected Unserved Energy (or USE – unserved enrgy) GJ Giga Joule GW Giga Watt IEX Indian Energy Exchange IGCs Isolated Generation Companies IPP Independent Power Producer JPCL Jamshoro Power Company Limited KESC Karachi Electric Supply Company Limited LECO Lanka Electricity Company (Pvt) Ltd LPGCL Lakhra Power Generation Company Limited MW Mega Watt NEA Nepal Electricity Authority NEEPCO North Eastern Electric Power Corporation NEPRA National Electric Power Regulatory Authority NHPC National Hydro Power Corporation NLDC National Load Despatch Centre NPC Nuclear Power Corporation NPGCL Northern Power Generation Company Limited NPPs Nuclear Power Producers NTDC National Transmission and Dispatch Company PGCB Power Grid Corporation of Bangladesh PGCIL Power Grid Corporation of India Limited PPA Power Purchase Agreement PSS/E Power System Simulator for Engineers PUCSL Public Utilities Commission, Sri Lanka PXIL Power Exchange India Ltd. RLDC Regional Load Despatch Centre SAARC South Asian Association for Regional Cooperation SAME SAARC Market for Electricity SEB State Electricity Board SERCs State Electricity Regulatory Commissions SHYDO Sarhad Hydel Development Organization SLDC State Load Despatch Centre SLEA Sri Lanka Electricity Act, No. 20 of 2009 TWh Terra (Trillion or 10

12) Watt hours

WAPDA Water and Power Development Authority

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 7

Executive Summary

This Final Report (FR) summarises the findings of the RDTA 7529: South Asian Regional

Power Exchange Study by refining and enhancing the analysis given in our Draft Final

Report based on the comments received on it at the Inter-governmental Meeting held in

Manila on 1-2 November, 2012. The study focuses on cross-border power trading among

the Member States in the SAARC region to efficiently balance available resources and

demand throughout the region. It also considers the possibility of the SAARC region

benefitting from power trade with Central Asia through the proposed Central Asia-South

Asia (CASA 1000) transmission development. We have analysed the economics of a

SAARC-wide interconnected power system to utilise major hydro potential in Nepal,

Bhutan, and Central Asia to meet growing demand in other parts of the system including

India and Pakistan. We have conducted a techno-economic analysis of cross-border

power trading for 2016/17 around six proposed interconnection and grid reinforcement

projects covering all SAARC Member States except Maldives, which is unlikely to be

connected to other power systems given its low load (below 100 MW) and remote location.

Our analysis includes power flow studies to establish power transfer limits among India

and its neighbouring countries. We have relied on the CASA 1000 study to define power

transfer capability between Afghanistan and its neighbouring countries including Pakistan.

Cost-benefit analysis of the proposed interconnection and grid reinforcement projects

forms the core of the study. The study concludes with identification of areas where the

legal and regulatory frameworks of the seven SAARC member countries involved need to

change to facilitate large-scale cross-border power trading in future.

Interconnected power systems can deliver significant economic, reliability and

environmental benefits for all sub-systems. Interconnection among SAARC country power

systems presents a potent opportunity given the proximity of the transmission networks of

its Member States in many cases, and the significant variation in natural resources and

demand across the regions. The power systems of India, Bhutan and Nepal are already

interconnected, but have so far elicited only a small part of the potential benefits. If we

consider a closely interconnected India-Bhutan-Nepal system, for instance, it would help to

unleash the significant hydro potential that exists in Bhutan (10 Giga Watts or GW in this

decade) and Nepal (42GW of hydro potential) to meet rapidly escalating demand in India.

Cross-border power trading can even extend beyond the SAARC region. For instance, if

we consider the proposed Central Asia-South Asia power transmission development

(CASA 1000) in conjunction with the proposed transmission link between India and

Pakistan, it is possible for surplus hydro from Tajikstan, Afghanistan and Kyrgyz Republic

to feed rising demand for power in Pakistan and India. Power exports from the hydro-rich

regions can not only reduce growing power shortages in India/Pakistan due to coal/gas

supply constraints, but also contribute to a significant reduction in environmental

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 8

emissions. Interconnectors also provide a cost effective way to enhance reliability for all

sub-systems, and delay, or reduce,the longer term need for capacity to maintain reliability

standard for individual sub-systems.

The present study is a continuation of ADB’s efforts to encourage an interconnected

SAARC grid that started with its South Asia Regional Cooperation Strategy Program in late

2006. The high voltage transmission networks among some of the SAARC countries are

already interconnected. Additional high capacity lines and grid reinforcement projects are

in various stages of development. However, these developments have come about in a

sporadic fashion. A well-orchestrated effort to maximise economic, reliability and

environmental benefits for the overall system is lacking. With the exception of India-

Bhutan, rest of the interconnection opportunities have at best been ad-hoc arrangements

with a short-term focus, or projects in concept stage for many years. There have been

limited efforts to develop an interconnected SAARC grid that offers significant benefits to

all participating countries/regions, and augment wider transmission developments such as

CASA 1000.

There are indeed technical, commercial, economic and regulatory/legal issues that need to

be addressed to support the development of an interconnected SAARC grid. Nonetheless,

as the limited interconnection experience between India and Bhutan/Nepal shows, it is

certainly feasible to tackle these issues. If an interconnected mode of operation

endangers system security because of frequency problems in one or more sub-systems,

there are established technology options, such as asynchronous HVDC links, to enable

such systems to exchange power. Development of independent power producers in all

countries and power trading firms in India provides a supporting mechanism to achieve the

economic benefits. These developments have already shown that given the abundance of

relatively inexpensive power in one region and demand in the other, commercial

arrangements can be put in place for both sides to enjoy the gains of trade in a mutually

acceptable manner. Regulatory processes and legal frameworks would also need to

embrace these developments to ensure that the regulatory/legal regimes can co-exist and

be harmonised to form a common framework that supports interconnected operation and

significant investment that would go in enhancing such interconnections in future.

A promising development that has taken place in recent years is the introduction of Power

Exchanges in India including the Indian Energy Exchange (IEX) and Power Exchange

India Limited (PXIL). These developments go some way in addressing the commercial and

regulatory/legal issues, albeit the operation of those exchanges currently deal with inter-

regional/state issues within India, rather than at an international level. Nevertheless, a

modern power exchange framework provides a “fair, efficient, robust and quick” price

discovery process creating an orderly market place for all buyers and sellers. Extension of

existing Power Exchanges is considered a feasible option to deal with cross-border power

trades. Assuming that the regulatory/legal developments would allow such trades, it would

immediately present producers/buyers in other countries to sell/buy power through an

open and competitive market.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 9

The long-term prospect of large-scale power trading among SAARC countries would,

however, ultimately be driven by sound economics that would in turn depend on the

demand-supply balance in each of these countries. Hydro resource development in

Bhutan, Afghanistan and Nepal would, for instance, be an attractive proposition only if

demand in India is sufficiently high and the delivered cost of power is economic relative to

India’s own (predominantly thermal) resources. The economic rationale would differ from

country to country. For instance, power exchange prospect between India and Pakistan

have been officially revisited since April 2012 in light of significant power shortage in

Pakistan. There is a proposal for transfer of power in the short term driven primarily by the

need to improve supply reliability in Pakistan. Power exchange between Sri Lanka and

India may involve more of a “two-way” exchange with India providing peaking support to

Sri Lanka. On the other hand, Sri Lanka may have surplus off-peak power that may

economically be utilised to displace thermal generation in India. While some analyses

have been undertaken in the past to quantify economic benefits, including a Pre-feasibility

Study for a India Sri Lanka HVDC Link in 2006, the full extent of benefits from cross-border

trading has not been comprehensively studied to the best of our knowledge. Also, factoring

in the increased hydro power export opportunities for Bhutan and Nepal, as well as

possible two-way power flow between India and Bangladesh in the longer term, we note

the importance of a holistic consideration of power trading among all SAARC regions, with

the exception of Maldives due to its location and very small load. In fact, cross-border

power trading in the SAARC region can complement other developments in Central and

West Asia. To this end, it is also useful to consider the possibility of surplus hydro from

Tajisktan and Kyrgyzstan during summer to augment peaking supply in Pakistan and

India.

In the context of the current nascent state of cross-border power trading among the

SAARC nations, and the development of Power Exchanges in India, the RDTA 7529 study

has addressed a key set of economic/commercial, technical and legal/regulatory issues.

The study included extensive data collection, load flow modelling, economic analysis and a

review of the legal/regulatory framework. We have focused on the potential development

of a “Regional Power Exchange” that would facilitate cross-border power trading through a

market driven process. In particular, the scope of the study included six core tasks that are

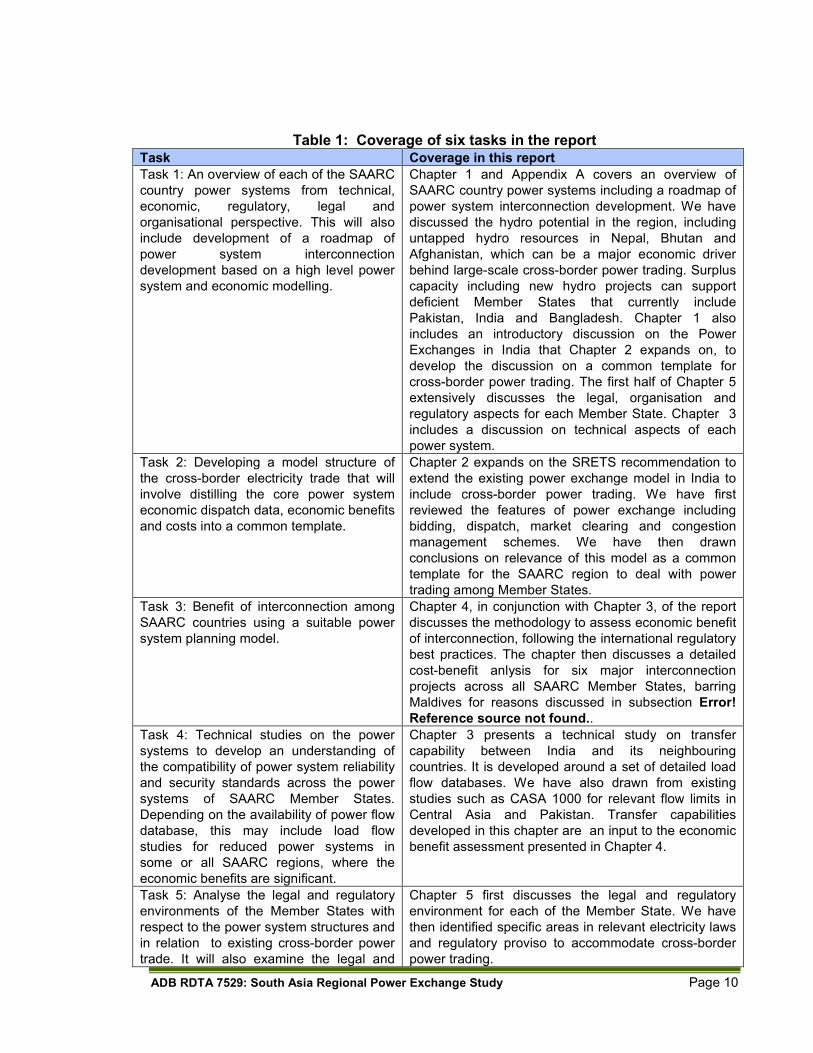

addressed in this Final Report as shown in Table 1.

In the remainder of this Executive Summary, we have summarised five key questions and

answers below that also directly represent the structure of the main report, and summarise

our key conclusions and recommendations.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 10

Table 1: Coverage of six tasks in the report Task Coverage in this report

Task 1: An overview of each of the SAARC

country power systems from technical,

economic, regulatory, legal and

organisational perspective. This will also

include development of a roadmap of

power system interconnection

development based on a high level power

system and economic modelling.

Chapter 1 and Appendix A covers an overview of

SAARC country power systems including a roadmap of

power system interconnection development. We have

discussed the hydro potential in the region, including

untapped hydro resources in Nepal, Bhutan and

Afghanistan, which can be a major economic driver

behind large-scale cross-border power trading. Surplus

capacity including new hydro projects can support

deficient Member States that currently include

Pakistan, India and Bangladesh. Chapter 1 also

includes an introductory discussion on the Power

Exchanges in India that Chapter 2 expands on, to

develop the discussion on a common template for

cross-border power trading. The first half of Chapter 5

extensively discusses the legal, organisation and

regulatory aspects for each Member State. Chapter 3

includes a discussion on technical aspects of each

power system.

Task 2: Developing a model structure of

the cross-border electricity trade that will

involve distilling the core power system

economic dispatch data, economic benefits

and costs into a common template.

Chapter 2 expands on the SRETS recommendation to

extend the existing power exchange model in India to

include cross-border power trading. We have first

reviewed the features of power exchange including

bidding, dispatch, market clearing and congestion

management schemes. We have then drawn

conclusions on relevance of this model as a common

template for the SAARC region to deal with power

trading among Member States.

Task 3: Benefit of interconnection among

SAARC countries using a suitable power

system planning model.

Chapter 4, in conjunction with Chapter 3, of the report

discusses the methodology to assess economic benefit

of interconnection, following the international regulatory

best practices. The chapter then discusses a detailed

cost-benefit anlysis for six major interconnection

projects across all SAARC Member States, barring

Maldives for reasons discussed in subsection Error!

Reference source not found..

Task 4: Technical studies on the power

systems to develop an understanding of

the compatibility of power system reliability

and security standards across the power

systems of SAARC Member States.

Depending on the availability of power flow

database, this may include load flow

studies for reduced power systems in

some or all SAARC regions, where the

economic benefits are significant.

Chapter 3 presents a technical study on transfer

capability between India and its neighbouring

countries. It is developed around a set of detailed load

flow databases. We have also drawn from existing

studies such as CASA 1000 for relevant flow limits in

Central Asia and Pakistan. Transfer capabilities

developed in this chapter are an input to the economic

benefit assessment presented in Chapter 4.

Task 5: Analyse the legal and regulatory

environments of the Member States with

respect to the power system structures and

in relation to existing cross-border power

trade. It will also examine the legal and

Chapter 5 first discusses the legal and regulatory

environment for each of the Member State. We have

then identified specific areas in relevant electricity laws

and regulatory proviso to accommodate cross-border

power trading.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 11

regulatory requirements and procedures

needed for proposed cross-border power

trade enhancement.

Task 6: The final task would be to collate

findings of the five tasks and the Interim

Report into a final report and proceedings

of the dissemination seminar.

This Final Report refines and extends the analyses

presented in the Draft Final Report and the Interim

Report. In addition to Chapters 1-5 that address Tasks

1-5, we have discussed our conclusions and way

forward to give shape to a SAARC-wide grid that was

envisioned in SRETS.

Why should one consider a South Asian Regional Power Exchange to enhance the present status of cross-border power trading and what would be the key drivers for such enhancement?

• An overall reduction in UnServed (electrical) Energy, or USE, in the SAARC region can

potentially avoid economic loss worth billions of dollars every year. At present, some of

the countries experience significant power shortages. As the demand for power is likely

to rise significantly over the years, it would immensely help to harness economic power

generation potential (including mega hydropower projects) and develop “scale-efficient”

transmission to bring the generated power to major load centres. The extent to which

USE benefits are recognised, however, is a policy decision in the hands of policy

makers in individual countries.

• Nepal, for instance, faces significant peak and energy shortages at present and could

benefit from access to surplus power if there were a Regional Power Exchange already

in operation. Also, the development of its significant hydro potential in future could be

supported through such a Power Exchange for other countries to buy power on a fair,

transparent and equitable basis.

• Power exchange between India and Bhutan, currently at around 5,600 GWh pa, is far

in excess of Bhutan’s own electricity requirements,and provides an indication of the

potential for large-scale power transfers. It also demonstrates the technical and

commercial feasibility of such power trade.

• Although Bhutan has already commenced the process of tapping its excellent hydro

potential in joint collaboration with the Indian authorities, the current capacity

represents a fraction of what can be achieved in the long run. The National

Transmission Master Plan for Bhutan prepared by Central Electricity Authority (India),

for instance, identified more than 10,000 MW of new hydro potential that can be

delivered through a large grid reinforcement project by 2020, as part of a larger

development for the period leading up to 2030. An efficient multilateral trading platform

such as a Regional Power Exchange would facilitate the commercial transactions and

support such development to its fullest potential. A Regional Power Exchange would

facilitate a natural progression of bilateral power trading arrangements, such as the

India-Bhutan trade, to a multilateral trading environment through proven market-based

efficient price discovery processes, to the benefit of all buyers and sellers in the region.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 12

• Indian power demand is anticipated to grow from the FY 2011 level of 933 TWh pa to

1,390 TWh pa in about five years, i.e., an increase that would require the addition of

nearly 100,000 MW of new capacity. Two-third of India’s electricity generation comes

from thermal resources predominantly in the form of coal. There is already a significant

gap between demand for coal and what Coal India Limited (CIL) can provide. This is

likely to lead to a situation where part of the coal-based generation capacity is partly, or

fully, stranded. In fact, it has been estimated that up to 42,000 MW of coal-based

capacity may face coal shortage by 2016/17. If this leads to a supply shortfall, the cost

to the economy can be very high and cross-border power import can be very

beneficial. Eliminating an unserved demand of just 0.1% of the total electricity demand

in 2016/17, translates into 1,390 GWh. Valued conservatively at USD 555 per MWh

(or Indian Rs 25 per unit), this equates to an annual benefit of USD 771 million.1

• Although Pakistan and Bangladesh at present have no interconnection with India, or

other SAARC countries, these countries have relatively limited local generation

development potential. Pakistan and Bangladesh currently face severe peak and

energy shortages. Sri Lanka does not have any major shortage at present, but it has to

rely on imported coal to meet its future demand growth. Electrical interconnection with

India can provide relief for these countries. There have been policy discussions

underway to support the development of a regional power exchange.The SAARC

Regional Energy Trade Study (SRETS) had, for instance, identified the options,

benefits and constraints of increased energy trade in South Asia that included the

potential for cross-border power trading to, inter alia, reduce unserved energy.2 One of

the specific recommendations of the March 2010 SRETS Report included fast-tracking

of cross-border interconnection projects that had already been identified.

• Major transmission infrastructure that exists today for cross-border power trading is

limited to India-Bhutan interconnectors that consists of three 220 kV lines for the

Chukha hydro project, and two 400 kV double-circuit lines that connect the Tala hydro

project with India (West Bengal). There are also three 132 kV lines between Nepal and

India.

• There are several major interconnection projects that are in different stages of

development from a conceptual stage to pre-feasibility/feasibility, and construction. All

these (proposed) projects are being developed around the major power market in India

connecting India with Bhutan, Nepal, Bangladesh, Pakistan and Sri Lanka. An HVDC

back-to-back asynchronous link between India and Bangladesh is currently under

construction and is scheduled to be commissioned in July, 2013. There are extensive

1 Tata Energy Research Institiute, Cost of Unserved Energy, prepared for the World Bank, TERI Report #98PG42.

Chattopadhyay and Schnittger (2008) present a wider review of cost of unserved energy that is specifically used for transmission planning in different countries. It shows even in developing nations such as Thailand, the value of USE/USE is higher, e.g., around USD 1500 per MWh in Thailand in 2001. Developed nations use much higher value of unserved energy in several thousand dollars per MWh. See Investigation of Value of Unserved Energy, prepared for the Electricity Commission of New Zealand, http://www.ea.govt.nz/.../our.../investigation-of-the-value-of-unserved-energy/ 2 SAARC Secretariat, SAARC Regional Energy Trade Study, March 2010, Kathmandu, Nepal.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 13

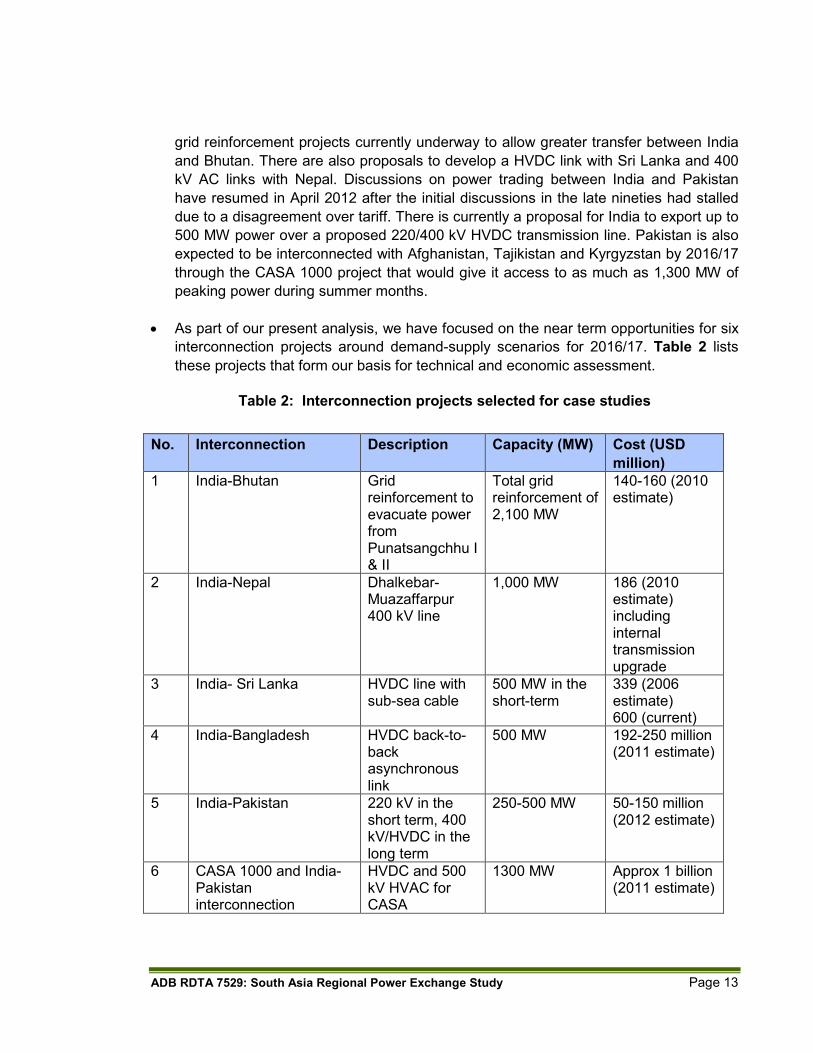

grid reinforcement projects currently underway to allow greater transfer between India

and Bhutan. There are also proposals to develop a HVDC link with Sri Lanka and 400

kV AC links with Nepal. Discussions on power trading between India and Pakistan

have resumed in April 2012 after the initial discussions in the late nineties had stalled

due to a disagreement over tariff. There is currently a proposal for India to export up to

500 MW power over a proposed 220/400 kV HVDC transmission line. Pakistan is also

expected to be interconnected with Afghanistan, Tajikistan and Kyrgyzstan by 2016/17

through the CASA 1000 project that would give it access to as much as 1,300 MW of

peaking power during summer months.

• As part of our present analysis, we have focused on the near term opportunities for six

interconnection projects around demand-supply scenarios for 2016/17. Table 2 lists

these projects that form our basis for technical and economic assessment.

Table 2: Interconnection projects selected for case studies

No. Interconnection Description Capacity (MW) Cost (USD

million)

1 India-Bhutan Grid reinforcement to evacuate power from Punatsangchhu I & II

Total grid reinforcement of 2,100 MW

140-160 (2010 estimate)

2 India-Nepal Dhalkebar-Muazaffarpur 400 kV line

1,000 MW 186 (2010 estimate) including internal transmission upgrade

3 India- Sri Lanka HVDC line with sub-sea cable

500 MW in the short-term

339 (2006 estimate) 600 (current)

4 India-Bangladesh HVDC back-to-back asynchronous link

500 MW 192-250 million (2011 estimate)

5 India-Pakistan 220 kV in the short term, 400 kV/HVDC in the long term

250-500 MW 50-150 million (2012 estimate)

6 CASA 1000 and India-Pakistan interconnection

HVDC and 500 kV HVAC for CASA

1300 MW Approx 1 billion (2011 estimate)

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 14

What are the salient features of the current power exchanges in India and can these be generalised to form the basis of a Regional Power Exchange to support cross-border power trading?

• Once the SAARC Member States form an interconnected system, cross-border power

trading would benefit immensely from an open market place that facilitates efficient,

close to real time, transparent and reliable prices. It would also boost investor

confidence to develop generation projects. In fact, one could argue that the price

discovery mechanism may even virtually precede the physical interconnection to pre-

emptively develop an idea of what prices in neighbouring systems may eventually

transpire. Even the mere presence of a price for a commodity sends useful signals to

prospective buyers and sellers who can make informed business decisions to engage

in a trade once the physical interconnection is put in place. There is little doubt that a

SAARC-wide system would benefit from having power traded through some form of

market mechanism. It however raises the question on the form of market mechanism

that is suited for the region. As the SRETS had envisioned, SAARC Regional Power

Exchange in all probability is likely to be an extension of the current Indian Power

Exchange model including one, or more, of the current Exchanges extending its

function to include cross-border power trading. Our own review of the power markets

also suggest there are two broad paradigms, namely a pool model and a power

exchange/contract trading model. Although they differ to some degree, they both

ultimately serve the purpose of efficient price setting and both have demonstrably been

successful models. We have also noted that in a vast majority of the cases, countries

have adhered to a single model because, as the example of Great Britain showed, a

switch can be a rather expensive affair. Given that India has already embarked on

developing an internal power market, and that there are successfully operating Power

Exchanges for more than three years, it is prudent to explore how/whether cross-

border power trading can develop around the existing Power Exchanges in India.

• A SAARC-wide Regional Power Exchange would ultimately need to serve two main

objectives, namely:

o Short term day-to-day dispatch and pricing functions. We need to know what is

the form of data that participating Member State power system bodies need to

furnish and how the market clearing process works. We have reviewed below

the existing Power Exchanges in India in order to address these issues and

further explored how these Power Exchanges can provide a common template

for economic dispatch and associated cross-border power trading; and

o The longer term economic regulatory framework to identify and encourage

efficient investment in new interconnection. While the short-term processes of

setting efficient locational prices in real-time in itself paves the way for new

interconnection, there are often explicit regulatory mechanisms to test the

efficacy of specific investment proposals. Developing a template for

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 15

interconnectors to continue and enhance cross-border power trading going

forward is, therefore, an important aspect of the current work. The following two

sub-sections in this Executive Summary addresses the economic cost-benefit

analysis for a set of proposed/anticipated cross-border transmission projects.

• Power Exchanges in India represent one of the two mainstream electricity market

models around the world. There are two Power Exchanges in India that act as clearing

houses for a range of electricity contracts including day-ahead, term-ahead and

renewable energy certificates. Participation in the exchanges is voluntary. A third

Power Exchange is being set up.

• Basic objectives of a power exchange that are enshrined in the Regulatory Framework

under the Electricity Act, 2003 are as follows:

1) Ensure fair, neutral and robust price discovery;

2) Provide extensive and quick price dissemination; and

3) Design standardized contracts and work towards increasing liquidity in such

contracts

These objectives mark an improvement over the efficacy of a bilateral trading

arrangement between two parties, although Power Exchanges also retain the flexibility

to engage into such trades. Nevertheless, the full potential of a Power Exchange does

involve striking a trading deal that is highly transparent to the market with a dynamic

discovery of price, subject to a set of rules of the game that applies to all players in the

market. These are indeed very attractive features for both buyers and sellers of power

that sets apart an electricity market from purely bilateral contracts. Market

arrangements and prices provide a level playing field and a useful benchmark for

investors, generators and purchasers. An extension of Power Exchanges to deal with

cross-border trading has its attractions because the vast potential for such trading

could only be unleashed if developers of generation and buyers of power could both

have confidence in a system that is fair, transparent, reliable and represents the state-

of-the-art technology.

• The operations of power exchanges are segregated into Day Ahead Markets (DAM),

Term Ahead Markets (TAM) and Renewable Energy Contracts (REC) Market. The

exchanges provide automated trading facility to all their members. A trading session in

the day-ahead market typically involves the following steps:

1) Order accumulation: The trading platform receives buy and sell bids from

members/traders.

2) Provisional bid matching process: The received bids are then matched in

accordance with the “order matching algorithm” that is governed by the market

rules.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 16

3) Accounting for constraints in transmission infrastructure: All trades are adjusted

as per the requisition submitted by the exchange and scheduled by the National

Load Dispatch Centre (NLDC)/Regional LDCs/State LDCs.

4) Final bid matching process: The final trades are determined and sanctioned

after transmission constraints are accounted for.

• There are three main segments of the market, namely:

o The Day Ahead Market (DAM) deals with daily contracts;

o Term Ahead Markets (TAM) include day ahead contingency, intraday, daily and

weekly contracts. The market clearing process for each of these contracts differs

as defined in the detailed market rules set by the Central Electricity Regulatory

Commission (CERC, India). There are also provisions for introducing new products

within the parameters of the rules which offer additional flexibility; and

o Renewable Energy Certificates (REC) market allows for trades in renewable

certificates.These certificates are introduced to support the renewable energy

target in India. Operations in this market commenced in July 2011. The rules in the

REC market are different from DAM and TAM. The presence of a market for

renewable is an encouraging development for small hydro, solar and wind

generation developers in the region.

• The bids or orders that can be placed by the traders/members on the automated

trading facility of the exchanges can be classified into the following categories:

o Single/Normal Bid: Single or normal bids specify multiple sequences of price and

quantity pairs to form a portfolio.

o Block Bid: Block bids specify one price and one quantity for a combination of

continuous hourly time blocks i.e., same quantity, at one particular price for multiple

time slots.

o Other Bids: The exchanges can, and do, introduce other types of bids as per the

requirement of the market. These are often driven by the need to distinguish

between the priority of orders (e.g., fixed and optional orders at PXIL), or orders

restricted by time and execution (e.g., in Term Ahead Markets of IEX).

• The trading mechanisms available in the existing power exchanges are summarised

below:

o Uniform price auction: All buy bids are summed at each price point and similarly for

the sell bids to obtain the aggregate demand and supply curves.

o Continuous bidding: Participants submit buy and sale offers on a continuous basis

during the trading period and they are matched on immediately with

price/time/volume priority, or on a pro-rata basis.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 17

o Discriminatory price-double sided auction: Buyers place orders by specifying their

priority. High priority buy orders are considered first and the matching proceeds in

that order from high to low priority buy orders.

• As the discussion above suggests, the existing Power Exchanges offer considerable

flexibility in product offering, timeframe and auctioning modes. Given the nascent

nature of trading among the states/regions in India, such flexibility is highly desirable to

ensure greater participation and increasing the liquidity in the market over time. The

experience to date suggests both exchanges are functioning well to this end.

• The potential for current power exchanges to take regional power trading to the next

level was noted in the SRETS – for instance: “In the case of SAARC, bilateral trade

arrangements, though limited to a few Member States, already exist. Applying the

same approach in the region, the Member States may consider graduating these

bilateral trade arrangements to multilateral trade arrangements. For instance, in case

of electricity, interconnections already exist between India-Bhutan and India-Nepal.

Further, India already has two working level exchanges namely Indian Energy

Exchange (IEX) and Power Exchange India Limited (PXIL). Various power producers

and buyers in all the Member States within SAARC may consider participating in these

exchanges for promoting regional electricity trade”.

• However, a power trading platform is only one of the components necessary for

regional cooperation. As developments in other parts of the world have demonstrated,

the need for targeted policy formulation to eventually drive institutional developments

such as transmission system operators, streamlining the regulatory and legal

framework for rules to be uniformly applicable across all jurisdictions and coordination

of planning to ensure efficient investment, are important issues that need to precede a

successful integration. The technical feasibility, i.e., adequate transfer capability in the

high voltage (HV) network, and economic desirability are also paramount.

Is cross-border trading feasible given the demand-supply balance in India and the transfer capability among states and at the borders?

Power transfer capabilities are a measure of the ability of the transmission system to

support power exchanges. For this reason, determining the transmission grid’s power

transfer capacity is important to establish viability of a market framework. Power transfer

limits function like traffic signals that identify whether transactions are supported by the

transmission system infrastructure, or not. Unsupported transactions may lead to

uneconomic alternative transactions, or unserved load.

For our present assessment, transfer capacities are calculated for 2016/17, with a grid that

interconnects India, Bhutan, Bangladesh, Nepal and Sri Lanka. We have derived a load

flow dataset in PSS/E© (Power System Simulator for Engineers – a proprietary software of

Siemens Power Transmission and Distribution, USA) format to undertake our analysis.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 18

The load flow data has been primarily sourced from the Central Electricity Authority (CEA)

in India. This “future system” features a combined grid which is more than double the size

of the individual grids of 2009. A major effort is involved in the development of an

appropriate model that incorporates projections for future generation and transmission

expansion of all sub-systems.

This composite model is organised into nodes that represent states, territories and

countries in the future Exchange market. Each node may undertake power exchange with

any other node if there is sufficient power transfer capability to render such transfers both

economic and secure. An analytical method determines the transfer capacity of all

possible transactions. The methodology involves a two-step technical process. First, the

thermal transfer capability limit dependency is checked using a technique that increases

the flow on an interchange, while holding all other interchanges constant, until the

operating limit for thermal loading for any link of the whole transmission system is reached.

Second, “loadability curves” are applied to account for the effects of transmission distance,

voltage level and use of technology such as, static VAr compensators (SVC) and

series/shunt compensation on the transfer capability limit. Finally, a reduced equivalent of

the composite grid is developed to support the economic cost-benefit analysis (using the

NATGRID, an optimisation-based planning model, as discussed later).

The power transfer limits for the cross-border trading are summarised in Table 3. This list

includes only those maximum transfers that may occur between neighbouring

countries/sub-regions. Table 3: Summary of transfer limits for 2016/17 system model

FROM Zone (A) TO Zone (B) A����B B����A

Zone # Name Zone # Name MW MW

65 Bhutan 43 India (Sikim) 4200 5300

65 Bhutan 51 India (Assam) 2100 2600

65 Bhutan 52 India (Northeast India) 1800 1500

70 Bangladesh 41 India (West Bengal) 500 500

90 Sri Lanka 34 India (Tamil Nadu) 500 500

40 India (Bihar) 80 Nepal 1000 1000

12 India (Punjab) 100 Pakistan 250/500 250/500

100 Pakistan 101 Afghanistan 1300 1300

The next step in the analysis is to incorporate the power transfer limits into a reduced

equivalent power system model for the NATGRID model to undertake an economic

analysis of new cross-border interconnectors.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 19

What are the economic benefits of cross-border trading in the near term?

As discussed at the outset, merely ensuring technical feasibility or having a trading

platform ready, does not provide sufficient rationale for cross-border trading. Economics of

cross-border trades need to be understood taking into account demand-supply scenarios

and cost of generation in each region. We have undertaken a detailed modeling study to

assess economic benefits that provides the basis for a cost-benefit analysis of

interconnection projects.

Methodology for Economic Benefit Assessment

There are two main analytical components underlying the economic analysis:

1) An AC load flow analysis undertaken using PSS/E that considers the power flows

in India with its neighbouring countries including Sri Lanka, Nepal, Bhutan and

Bangladesh represented as external nodes. We obtained the PSS/E database for

2016/17 from CEA, India and used it to develop an equivalent network for the

Indian power system. We have added Pakistan and Afghanistan as additional

external nodes for our case studies on Pakistan and CASA, respectively; and

2) An investment planning model (NATGRID) that also simulates the optimal

operation of the system. We have run the transmission constrained NATGRID

investment/dispatch optimisation for 2016/17 with and without each of the six

interconnection projects. The benefit of each project is calculated as the reduction

in system cost, i.e., the difference in system cost between these two scenarios.

We have considered each interconnector as a stand-alone development, i.e., we do not

consider the combination of interconnector projects, except for India-Pakistan together

with CASA 1000. The latter case study shows the potential for significant hydro from

Afghanistan, Tajikstan and Kyrgyzstan to meet demand not only in Pakistan but also in

India. While it would indeed make sense to consider additional combinations, , e.g.,

Bangladesh-India-Nepal and Bangladesh-India-Bhutan because there may be some

interaction among these projects, the time and effort involved would be very significant for

the incremental knowledge sought. We also note that in comparison to the size of the

Indian power system, each of these projects is relatively small (by almost two orders of

magnitude). Any inaccuracy introduced in the benefit due to a lack of consideration of

multiple interconnection benefits is therefore unlikely to be material to invalidate the broad

outcomes.

The NATGRID model is chosen because the model has been deployed in the past for cost-

benefit analysis of an Indian national grid in the nineties and the project team has ready access

to the model. NATGRID uses a linear programming model for investment and dispatch with a

DC approximation of load flow constraints embedded in the optimisation model. The

methodology used in NATGRID has been peer reviewed and well documented in leading

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 20

power system journals. We have also provided an extensive discussion on the mathematical

details of the model and a comparison with commercially available software so that individual

Member States may employ suitable models for their own analysis.

A power system interconnection asset would ultimately deliver benefits in one or more of

three major forms, that we have assessed using NATGRID, namely:

1) Reliability benefit: Avoided unserved energy costs to the extent the new

transmission asset lowers peak and energy curtailment in the importing region;

2) Operating cost benefits: Avoided cost of expensive fuel and operation and

maintenance (O&M) costs that the flows on the new line may displace in the

importing region; and

3) Capacity benefits: Any avoided cost of new capacity that the line renders

unnecessary that may include capacity needed to produce energy in the importing

region, or reserve capacity needed.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 21

Estimates of Economic Benefits

Table 4 presents a summary of the most significant assumption and benefit/cost

estimates.

Table 4: Summary of all six case studies Case study Key assumption Total and annualised cost of

transmission

(USD million)

Annual benefit in 2016/17

(USD million)

India-Bhutan

grid

reinforcement

Puna I & II,

Mangdechhu and

Dagachhu (3,066

MW) power

evacuation to India

Total cost USD 140-160 million.

Annualised cost USD 18-20

million pa

Up to USD 1,840 million pa

including USD 336 million in

opex benefit and USD

1,504 million in unserved

energy reduction benefit

Nepal-India400

kV link

Two scenarios: (1)

Nepal builds all

planned projects

(2000 MW) to reach

surplus state; and

(2) 650 MW of

planned capacity

addition is delayed

i.e., deficit state

Total cost USD 186 million

including internal transmission

upgrade costs

Annualised cost USD 20 million

pa

Surplus state benefit of

USD 105 million pa(71

million in unserved energy

reduction and 34 million in

opex benefits)

Deficit state benefit of USD

215 million (173 million in

unserved energy reduction

and 42 million in opex

benefits)

India-Sri Lanka

HVDC link

Puttalam Stage 2

and 400 MW in new

hydro is added by

2016. But Trinco

(1,000 MW) coal

station is not

considered

Total cost USD 339 million (2006

estimate)

Annualised cost USD 50 million

pa (2010 estimate)

USD 186 million pa

comprising 96 million in

unserved energy reduction,

and 90 million in

fuel/capacity benefits

India-

Bangladesh

HVDC link

Three scenarios

around demand

growth in

Bangladesh that

range between

9,000 MW to 12,000

MW in 2016/17

Total cost range between USD

192 million to USD 250 million

Annualised cost of USD 25

million pa assumed for

cost/benefit analysis

Annual benefits range

between USD 145 million to

USD 389 million, depending

upon demand-supply

assumptions

India-Pakistan

220/400 kV

Link

Two scenarios both

using HVDC

technology: (a) Short

term 250 MW

transfer at 220 kV

(b) Medium/long

term 400 kV transfer

of 500 MW

Total cost of option (a) max USD

50 million for 220 kV option (45

km); and (b) Maximum USD 150

million for 400 kV option (similar

to Bangladesh line)Annualised

cost of (a) USD 6 million for 220

kV (b) USD 18 million for 400 kV

Annual benefit for 220 kV

transfer is USD 335 million

including USD 122 million in

fuel cost savings

Higher transfer via 400 kV

increases benefits to USD

491 million including USD

163 million in fuel cost

savings

CASA 1000 and

India-Pakistan

400 kV link

Two scenarios (a)

Base Case CASA

1000; and (b)

Additional 850 MW

hydro in Afghanistan

Cost of CASA project is USD 893

million and that for India-Pakistan

link max USD 195 million

Annualised cost of two projects

USD 110 million

Annual combined benefit of

two projects is USD 1,250

million for Base Case

including USD 906 in USE

cost reduction and USD 306

million in fuel cost savings

Annual benefit increases to

USD 1,340 million for

additional hydro scenario.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 22

Note: Annualised cost includes capital cost of transmission projects calculated using a Weighted Average Cost of Capital of 7.5% and life of 30 years, and operation and maintenance costs (O&M) costs. We have also used annualised cost estimates directly for (a) India-Sri Lanka line based on PGCIL pre-feasibility study (2006); (b) CASA project cost estimates based on SNC Lavalin (2011); and part of the India-Nepal costs based on NEA (2011)

All six interconnection/grid reinforcement projects have significantly higher annual benefits

compared to the (annualised) costs of these projects. The India-Bhutan grid reinforcement

stands out as the most beneficial of the six projects mainly because it facilitates as much

as 2,100 MW of hydro capacity to become available at a modest (annualised cost of

transmission) of USD 20 million pa. Since the grid reinforcement actually allows for

additional surplus hydro energy from Western Bhutan, the project has the potential to

achieve USD 336 million pa in opex savings alone, even before we consider the enormous

savings that may result from a reduction in unserved energy. High benefits of India-Bhutan

interconnection amply demonstrate the ability of a Regional Power Exchange to unleash

the vast potential in the region. Short term power transfers between India and Pakistan

also has significant economic potential. In partcular, we have noted that the fuel cost

savings for a single year alone may pay for the transmission development. The CASA

1000 project in conjunction with an India-Pakistan 400 kV/HVDC link can also yield very

substantial savings exceeding USD 1 billion, primarily through a reduction in unserved

energy in Afghanistan, Pakistan and India. The other three projects also have very

attractive benefit-to-cost ratio, if USE benefits are included.

However, if USE benefits are not considered as part of overall benefits, the latter would be

confined largely to fuel (or “dispatch”) related cost savings. Then the break-even utilisation

level for a high cost link to recover an acceptable return on the investment may potentially

be very high. For example, if the India – Sri Lanka link costs USD 600 million and a pre-

tax real return of 8.5% is needed, the link will need to achieve an average utilisation in

excess of 80% for an average power generating cost differential of USD 15 per MWh

between the two countries. Since both systems will become pre-dominantly thermal over

the medium term with relatively expensive peaking generation on both sides, an average

price differential of USD 15 per MWh may not necessarily occur. In other words, absent

some way of recognising the USE benefits, the economics of the link are unlikely to be

favourable for the HVDC link connecting India and Sri Lanka, unless of course design

changes bring down the cost. The extent to which USE benefits are recognised is basically

a policy decision in the hands of the two countries.

What are the required changes to the regulatory and legal framework for the Regional Power Exchange to function?

Most of the countries in South Asia have a similar legacy as far as the power sector is

concerned. The power sector has historically been dominated by public ownership with

greater relevance for vertically integrated monopolies that generate, transmit and distribute

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 23

electricity to consumers. Changes in the policy and regulatory environment have led to

restructuring and reforms in the sector. These were aimed at improving the sectoral

performance and creating a space for private investment. While this has been more or less

a common feature across most of the South Asian countries, there is a mixed experience

as far as approach to introducing competition is concerned. Opening up of the sector to

competition in India has led to increased trading activities. This was supported with

significant policy and regulatory reforms that reduced entry barriers and, enabled open

access of transmission and distribution network. Recognition and licensing for trading

activities, and setting up Power Exchanges have led to the creation of a competitive

environment.

Given the difference in the stage of market reform across South Asian countries, the

approach to develop a regional market could begin by identifying a nodal agency to

engage in cross border trade to be followed by enhanced participation by identified

deemed licensees till the licensing is opened up. Given that participation on a Power

Exchange is feasible without a trading license as well, access to Power Exchanges in India

would accelerate regional power trading activity through such a competitive platform.

Given disparity in geenration profile, and load profile across the time of the day, day of the

week, season of the year as well as festivities, there is ample scope for trading of

electricity even in the presence of overall power shortages to ensure optimal utilisation of

existing generation resources. Development of cross-border transmission interlinakges

with adequate margin capacity to accommodate such trade beyond the bilateral

agreements would play a very instrumental role in this context.

Development of a regional power market in South Asia would enable optimal utilisation of

the region’s resources and help attract greater private investment in the power sector in

the region. The development of a Regional Power Exchange is dependent on a number of

legal and regulatory prerequisites. We have identified nine specific legal/regulatory

provisions to be added/ modified in the existing framework, or to be presented as a part of

new legislative initiatives in respective countries. Our views are summarised in Table 5

including merits/opportunities and demerits/challenges for priority areas.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 24

Table 5: Important Regulatory/Legal Changes: Merits and Demerits/Challenges

Regulatory/Legal

changes

Merits / Opportunities Demerits / Challenges

1 Nodal Agency to

engage in cross-

border trading

An early takeoff for regional trade

possible.

Reduce shortage of electricity.

Help optimal use of idle/excess

generation capacity in the region.

Limited market access and

competition till

deemed/trading licenses

enhances participation.

2 Trading License

and Generation

De-licensing

Generation de-licensing would bring

greater investment.

Trading license would open avenues

to use unutilised generation capacity.

Reduce shortage of electricity.

Enhance competition in power

markets.

Scheduling trading

transactions would need

improvement in system

operation procedure and

energy accounting.

3 Open Access of

Transmission

Network

This would truly operationalise

competition and access to electricity.

Need to develop transparent

regulations for granting open

access.

System operation to take care

of open access customers.

4 Coordinated

System Operation

and Treatment of

System

Imbalances

Improved grid discipline.

Low equipment failure due to grid

stability.

Adoption of region’s best practices and

experience sharing.

Metering and IT integration

5 Regulatory

Framework and

Transmission

Planning

Improvement in system reliability due

to system integration including support

during power crisis.

Bilateral transmission linkages to have

excess capacity to support cross-

border trade.

Investment in transmission

interconnections and system

strengthening.

Land acquisition.

6 Energy

Accounting,

Clearing and

Settlement

Advantage of improved system for

domestic energy accounting and

settlement as well.

Adoption of region’s best practices and

experience sharing.

IT integration, training and

migration to improved system.

7 Policy for Regional

Electricity Trade

Better economic development of South

Asian region.

Improved access to power in South

Asian region.

Better utilisation of region’s resources.

Increased investment in power sector

in the region.

Graduation from bilateral to

regional agreement.

8 Import Duty, Export

Tax and Transit

Enhanced energy trade across region. Expected loss in tax revenue

could be offset by economic

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 25

Regulatory/Legal

changes

Merits / Opportunities Demerits / Challenges

Tax gains due to higher economic

growth, better electricity

access and greater

investment in the sector.

9 Dispute Resolution Overall improvement in investment

climate in the power sector as

investors’ risk perception would

reduce.

Graduation from bilateral to

regional agreement.

Based on identified pre-requisites, a number of specific legal/regulatory changes in the existing/proposed laws/regulations are proposed for Afghanistan, Bangladesh, Bhutan, India, Nepal, Pakistan and Sri Lanka. These have been further classified as short-term, medium-term and long-term. The key priority areas are highlighted below.

Afghanistan

• Draft Law on Electricity should recognise electricity trading and provide for

trading license, and provide for deemed trading licensee status for generation

and distribution licensees.Da Afghanistan Breshna Sherkat (DABS) may be

identified as a nodal agency to engage in cross-border trade in the short-run till

trading licenses are issued.

• Draft Law on Electricity should provide for non-discriminatory open access for

transmission. DABS needs to develop a grid code for coordinated system

operation with neighbouring countries. Afghanistan Electricity Regulatory

Authority (AERA), the proposed regulator, to establish transmission charges for

access to the transmission network for electricity trading.

• Procurement/sale of electricity through a regional power exchange to be

exempted from prior-approval and price determination by the proposed

regulator.

• Trade Policy should exempt cross-border electricity trade including that through

a power exchange from custom duty, export tax or transit tax. Export, import

and transit of electricity should be exempted from licensing from relevant

commerce ministry/department.

• DABS should initially develop cross-border interlinkages with excess capacity

to facilitate electricity trading. Later, it should develop a plan for cross-border

transmission linkages (including transit of electricity) in coordination with

entities in participating countries.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 26

Bangladesh

• Electricity Act 1910 (or a new legislation) should provide for trading license,

non-discriminatory open access for transmission, and bilateral resolution of

dispute in case of cross-border power trades and strive towards a regional

mechanism.

• Bangladesh Energy Regulatory Commission (BERC) Act, 2003 should enable

BERC to issue trading license and formulate regulations for non-discriminatory

open access to transmission. BERC should develop a mechanism to deal with

any system imbalances from scheduled transactions.

• BPDB may be identified as a nodal agency to engage in cross-border trade until

trading is licensed.

• Procurement/sale of electricity through a regional power exchange to be

exempted from prior-approval and price determination by the BERC.

• BERC should develop a regionally coherent commercial mechanism to treat

system imbalances.

• Amendment in BERC Act (Sec. 22(f)) for development of a grid code should

allow the national load dispatch agency to coordinate system operation with

cross-border entities.

• Power Grid Corporation of Bangladesh, the transmission licensee, should

develop cross-border linkages with excess capacity and a plan for cross-border

transmission linkages in coordination with entities in participating countries.

• Trade Policy should exempt cross-border electricity trade including that through

a power exchange from custom duty, export tax or transit tax. Export, import

and transit of electricity should be exempted from licensing from relevant

commerce ministry/department. Bhutan

• The BPC owns and operates the transmission network in the country under

license from BEA. BPC is responsible for distribution of electricity in the

country. As per the Electricity Act of Bhutan 2001, BPC is also designated to be

the system operator, although BPC has not yet received the license to be the

system operator.

• Generation licensees are already permitted to engage in export and import of

electricity as per the comprehensive license issues by BEA. Electricity Act of

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 27

Bhutan, 2001 provides for a trading (i.e., import/export) license (Sec. 22.1).

However, BEA is authorised to designate a single “bulk supplier” for

import/export of electricity (Sec. 40). This significantly limits market

participation. Amendment to Section 40 should limit the role of the designated

“bulk supplier” only in the context of generation plants owned by the Royal

Government of Bhutan.

• Section 38.1, which enables open access, should be amended to introduce

“non-discrimination”.

• Sections 11.1 (i) (b) and 14.1 (iv) should explicitly exempt determination of tariff

for electricity sold through a Power Exchange. Procurement/sale of electricity

through a Regional Power Exchange to be exempted from prior-approval and

price determination by the BEA.

• There should be a provision for bilateral dispute resolution for cross-border

trade. There is also a need to work towards a regional mechanism for dispute

resolution in future.

• Bhutan Electricity Authority (BEA) should formulate a regionally coherent

commercial mechanism for treatment of system imbalances.

• Bhutan Sustainable Hydropower Development Policy (BSHDP) 2008 - As per

Section 5.2 of the policy, the Royal Government of Bhutan (RGoB) has the

option to avail the royalty energy either as energy, or as cash in lieu thereof,

based on the highest off-take rate at which the power/energy from the plant is

sold by the developer to its buyers. The above mentioned proviso should

exclude power sold through a regional power exchange. It should be suitably

amended to consider higher of the ‘average’ price of sale of electricity through a

power exchange and the maximum off-take rate for rest of the power sold. This

would make the mechanism fair to a generator in case a small quantum of

electricity is sold at a very high price on a power exchange.

• The trade policy should also provide for exemption from export tax/import

duty/transit tax for cross-border trade of electricity including that through a

power exchange. Export, import and transit of electricity should be exempted

from licensing from relevant commerce ministry/department.

India

• The Power Exchanges in India to be allowed to accept/and allow participation

by entities located and registered in the participating SAARC countries. This will

need amendment to respective By-laws/Rules of each exchange and be

approved by the CERC.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 28

• There should be a mechanism for bilateral resolution of dispute in the case of

cross-border power trade. In particular, imbalance settlement is an essential

prerequisite. A regional dispute resolution mechanism should subsequently be

developed in cooperation with participating member countries.

• As a central policy, National Electricity Policy (NEP) should highlight

development of a competitive market in South Asia through cross-border trade

as an integral part of the development of the national energy scene.

• The trade policy should grant exemption from export tax, import duty and transit

tax to cross-border trade of electricity including that through power

exchange(s). Export, import and transit of electricity should be exempted from

licensing from relevant commerce ministry/department. Repeal/modification of

DGFT Notification No 09/2009-2014 (dated 10 September 2009) which restricts

import of electricity.

• National Transmission Plan should seek coordination with entities in

participating countries for developing cross-border transmission linkages.

Nepal

• Electricity Act 2049 (1992) (or a new legislation) should recognise electricity

trading and provide for trading license, non-discriminatory open access for

transmission and appropriate mechanism for bilateral resolution of dispute in

case of cross-border power trades with an aim to develop a regional

mechanism.

• Nepal Electricity Authority (NEA) Act , 2041 (1984)) and/or Nepal Electricity

Regulatory Commission Bill 2065 (2008) should empower the proposed

regulator, NERC, to issue license for trading including terms and conditions for

the same, and introduce provision for deemed trading licensee status for

generation and distribution licensees. Electricity Tariff Fixation Commission

(ETFC)/proposed regulator should not determine tariff for electricity sold

through a Power Exchange. Procurement/sale of electricity through a regional

power exchange to be exempted from prior-approval and price determination

by the proposed regulator, although this could be avoided with appropriate

guidelines and procedures.3 Further, special provision may be needed for

cases where the Regulatory Commission shall not determine the tariff, as per

the current legal provision, where royalty is also associated with tariff of

electricity.

3Based on comments made by the Nepal delegates at the Final Meeting in Manila, November, 2012.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 29

• The Government of Nepal (GON) should develop a plan for cross-border

transmission linkages in coordination with entities in participating countries. The

Nepal Electricity Regulatory Commission Bill 2065 (2008) should account for

the proposed changes suggested.

• GON/proposed regulator to develop a regionally coherent commercial

mechanism to treat system imbalances. The commercial mechanism needs to

address how under and overdrawn by one, or more, jurisdictions would be

handled. The Unscheduled Interchange (UI) mechanism in India is one such

mechanism that penalises any deviation from scheduled interchange. The

significance of the UI mechanism is explained in good detail by Soonee et al

(2006).4

• Trade policy should exempt from export tax/import duty/transit tax for cross-

border trade of electricity including that through a power exchange. Export,

import and transit of electricity should be exempted from licensing from relevant

commerce ministry/department.

4S. Soonee et al, Significance of Unscheduled Interchange Mechanism in the IndianElectricity Supply Industry, ICPSODR-

2006, Available online: http://www.nrldc.in/docs/documents/Papers/Significance_of_UI.pdf

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 30

Pakistan

• Regulation of Generation, Transmission and Distribution of Electric Power Act

1997 should be amended to recognise trading as a distinct activity and

licensing for trading by the National Electric Power Regulatory Authority

(NEPRA). These license provisions should enable cross-border electricity trade

including that through a Power Exchange. This should provide for deemed

licensee status for generation and distribution licensees.

• Karachi Electric Supply Company Limited (KESC) and the eight distribution

companies of erstwhile Water and Power Development Authority (WAPDA)

should be allowed to exchange power through cross-border trade. Price of

power determined competitively through a Power Exchange should not be

regulated by NEPRA. National Transmission and Dispatch Company (NTDC)

should develop a plan for cross-border transmission linkages in coordination

with other participating countries. In the interim, develop cross-border links with

excess capacity to accommodate trade of electricity.

• Procurement/sale of electricity through a Regional Power Exchange to be

exempted from prior-approval and price determination by the NEPRA (Section

32).

• Policy for Power Generation Projects (last issued in 2002) should provide for

export of power.

• Cross-border trade of electricity including that through a Power Exchange

should be exempted from export tax, import duty or transit tax by the trade

policy. Export, import and transit of electricity should be exempted from

licensing from relevant commerce ministry/department.

• NTDC is currently empowered as the Central Power Purchasing Agency

(CPPA) to procure power on behalf of the eight distribution companies of

erstwhile WAPDA. The independence of distribution companies is a critical

element. Until such independence is allowed, NTDC’s mandate, as a identified

nodal agency, should account for power procurement under cross-border trade

including through a regional power exchange.

• NEPRA should develop a regionally coherent commercial mechanism to treat

system imbalances.

• Incorporate a mechanism for bilateral dispute resolution for cross-border trade.

Later, to work towards a regional mechanism for the same.

ADB RDTA 7529: South Asia Regional Power Exchange Study Page 31

• NEPRA should determine a separate price for use of transmission assets of a

transmission licensee for electricity trade and procedure for determination of

transmission loss associated with power exchanges.

Sri Lanka

• Sri Lanka Electricity Act (SLEA), No. 20 of 2009 and Public Utilities

Commission of Sri Lanka (PUCSL) Act 2002 should be suitably amended to

provide for trading license (including amendment in Section 17 of PUCSL Act),

non-discriminatory open access for transmission (Section 23 of PUCSL Act),

and bilateral resolution of disputes in case of cross-border power trades while

working to develop a regional mechanism. Amendment to Section 16 (b) of

(SLEA, 2009), which obligates a generation licensee to sell all electricity

generated to a transmission licensee, should allow a generation licensee to sell

electricity through a competitive platform such as a power exchange.

• Amendment to Section 43.2 (SLEA, 2009), which allows the Transmission and

Bulk Supply Licensee to procure electricity only through a competitive tendering

process, is required to include power procurement from a regional power

exchange as a means of competitive power procurement. Procurement/sale of

electricity through a regional power exchange to be exempted from prior-