Embed Size (px)

Citation preview

Chapter 1

Introduction

In 2009, with more than 90 stores across India, Fabindia is looking towards

expanding its operations overseas. Initially an export house, Fabindia has emerged as one of

the leading players in the ready to wear segment, with the image of a quintessential ‘Indian’

brand. The questions now confronting Fabindia are how it is supposed to take its expansion

plans forward and increase its global reach, and whether the ‘Indian’ brand can gain enough

of a foothold in the international market. Fabindia has become a fashion statement in the

“elite” and “intellectual” customer segments. It had also come to represent organic products.

“Fabindia was founded with the strong belief that there was a need for a vehicle to market

the vast and diverse craft traditions of India and thereby help fulfil the need to provide and

sustain rural employment.”

“Our endeavour is to provide customers with hand crafted products which help support and

encourage good craftsmanship.”

John Bissell

History

John Bissell who founded Fabindia was born in Hartford in Connecticut and was

educated at the Brooks School in North Andover, Massachusetts, and at Yale. He was

introduced to India by his father, who told him stories of his time in India when he was

posted there during the Second World War. John Bissell worked as a buyer for the American

departmental store, Macy’s. In 1958, under a programme run by the Ford Foundation, he

came to India to advise the Central Cottage Industries Corporation created by the Indian

government, on showcasing Indian handlooms and handicrafts. His role was to advise on

issues relating to marketing Indian handicrafts. He was new to India and he did not know any

Indian language. In spite of these inconveniences, he travelled extensively over India and met

several craftsmen. He came across a lot of skill, among craftsmen but he also observed that

they had no idea about marketing their products and they were in no position to access distant

urban or international markets. He liked his experiences in India and hence kept coming

back. What Bissell discovered was a village-based industry with a profusion of skills hidden

from the world. However, they lacked the skills to market their products and access the large

1

urban and foreign markets. Determined to showcase Indian handloom textiles, and providing

equitable employment to traditional artisans, and sensing an entrepreneurial venture, Bissell

established Fabindia in 1960. It was also to fuse the best aspects of East & West

collaboration. Initially, Fabindia started as a wholesale export company, concentrating on the

export of upholstery fabrics, durries and rugs. Initially his goal was to export to the US and to

other western countries. With that aim in mind, he incorporated Fabindia in 1960. The

company operated from Bissell’s residence in the posh Golf Greens locality in New Delhi.

Growth was initially slow for the company and in 1965 the company moved out of his house

into a proper office. By then, Fabindia had an annual turnover of Rupees 20 lakhs. Most of

this turnover was accounted for by a single buyer and a single supplier. A. S. Khera made

durries and other home furnishings in his workshop in Panipat and most of the output was

purchased by the UK based Habitat, which was founded by a famous interior designer, Sir

Terence Conran.

Retail Foray

Bissell’s Greater Kailash shop was a success. It attracted a distinct category of

customers. But in spite of such success in its direct retail business, Fabindia remained

dependent on exporting and Habitat continued to be their single major buyer. In the early

80’s, Fabindia made a significant addition to its product range by adding ready to wear

garments too in their retail offerings. In an interview in 1977, Bissell said, ‘’the greatest thing

that happened to our business was the move in Europe and America a few years back to the

natural look – natural textures, natural fibres - and away from things like polyester and

nylon’’. Similarly, like in Europe and America in India, a distinct group was emerging. Some

of India’s new young politicians, media stars and other celebrities patronized Fabindia and

were able to provide Fabindia with nationwide exposure for its products. In spite of all that,

its domestic retail business grew slowly. It continued to focus on export business. However

as time passed Fabindia's marketing shifted from exports, to the local Indian retail market.

This was especially so from 1990s. In 1999, on John Bissell’s death, his son William aged

32, formally took over as the Managing Director of Fabindia. The Company’s domestic

expansion had been spectacular after William took over. By 2001, Fabindia had six stores

concentrated in the metro cities. By the end of 2004, these had increased to 20, and the

company was seriously considering expanding its stores into the tier-II and tier-III, cities as

2

well as overseas. By the end of 2007 Fabindia had 75 retail stores across India and in

addition, stores in Dubai, Rome and Guangzhou in China.

Fabindia across India

What started as an export house has today become a successful retail business

presenting Indian textiles in a variety of natural fibres, and home products including

furniture, lights and lamps, stationery, home accessories, pottery and cutlery. In 2004, food

products range was launched and in 2006, Fabindia Sana, their authentic body care products

range, was launched. Recently, it has also ventured into the jewellery segment. However, the

major chunk of Fabindia’s product range is textile-based. The company has continued its

focus mainly on the artisans and sources its products from over 15,000 craftsmen across

India. With a strong foundation, the company has been successful in increasing its presence

all over India.

3

Chapter 2

Research Methodology

Research Topic – A Study of Consumer Behaviour towards “Fabindia” in Mumbai

Why the study:

• The study is aimed at understanding the consumer’s behaviour towards “Fabindia” and its marketing strategies.

The scope of the study would include:

• Understanding the consumers of Fabindia in different segments and in different locations.

• Doing a Market Research of different targeted consumers of Fabindia

• Conduct a SWOT analysis of Fabindia

What is it about

The objective of the study is:

• To study consumer behaviour towards Fabindia.

• To know about the marketing strategies of Fabindia which includes 4P’s of marketing

• Conduct a SWOT analysis of Fabindia

Where was the study carried out

The study will be carried out in the stores of Mumbai only.

What research design we followed

Primarily we have conducted exploratory research. Since the object of exploratory research is to find out new ideas, flexibility and ingenuity characterize the investigation. Since we had to analyse, that despite of so many strengths India is still not the market leader in home textiles export sector. We had to continuously change the focus of investigation as new possibilities acme into attention.

What data sources are used

Primary data: Obtained from people in major shopping areas of Mumbai, viz Phoenix Mall, Worli; Chembur; Inorbit Mall, Vashi and Colaba.

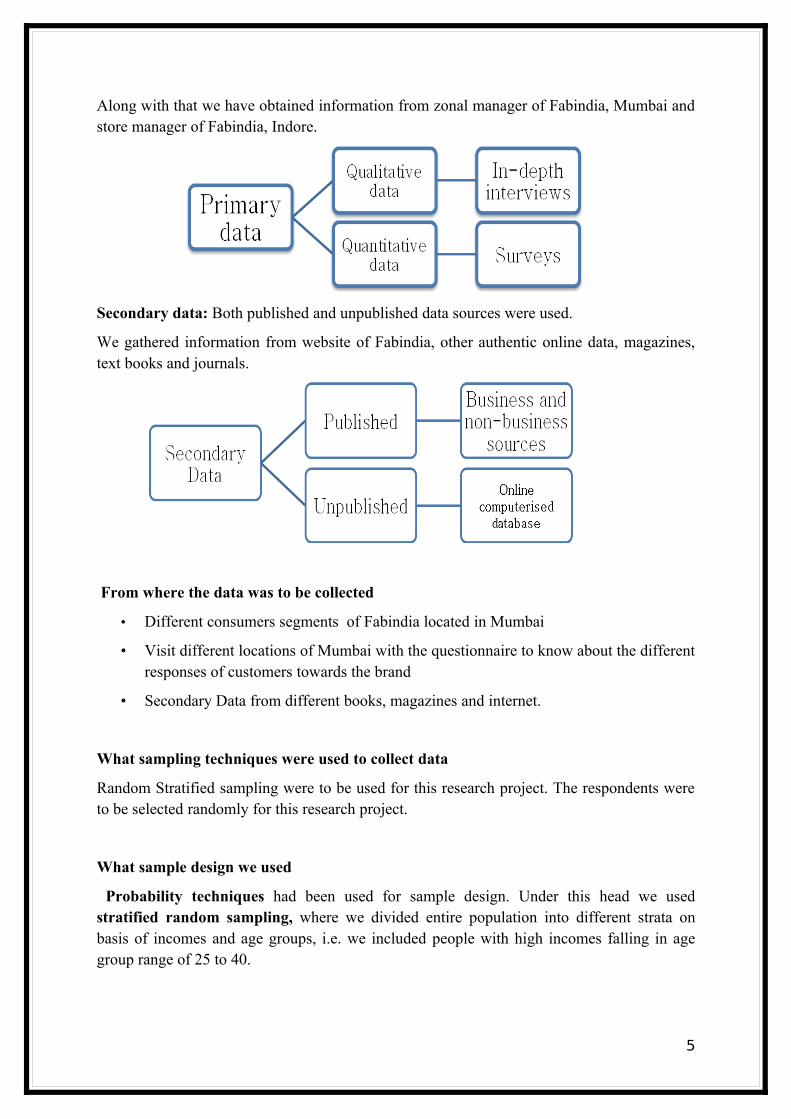

4

Along with that we have obtained information from zonal manager of Fabindia, Mumbai and store manager of Fabindia, Indore.

Secondary data: Both published and unpublished data sources were used.

We gathered information from website of Fabindia, other authentic online data, magazines, text books and journals.

From where the data was to be collected

• Different consumers segments of Fabindia located in Mumbai

• Visit different locations of Mumbai with the questionnaire to know about the different responses of customers towards the brand

• Secondary Data from different books, magazines and internet.

What sampling techniques were used to collect data

Random Stratified sampling were to be used for this research project. The respondents were to be selected randomly for this research project.

What sample design we used

Probability techniques had been used for sample design. Under this head we used stratified random sampling, where we divided entire population into different strata on basis of incomes and age groups, i.e. we included people with high incomes falling in age group range of 25 to 40.

5

What was our sample size

100 respondents had been selected as the sample size for this study of consumer behaviour located in Mumbai only.

What scaling techniques were to be used

In our study, Ordinal scales had been used where the respondents had to rank their attitudes towards Fab india in terms of provided options. We used comparative scaling techniques, namely rank order scaling (respondents had to rank their preferences) and semantic differential scaling (where the respondents had to define their choice between highly satisfied and highly unsatisfied)

How the data to be analyzed

Data analysis was to be done from the responses that we had collected from various consumers based on the questionnaire. Columns chart & Pie chart was used for the representation of the interpreted data.

How will the report be presented

A report in the form of hardcopy will be submitted along with a presentation of the results of the research.

6

Chapter 3

Literature survey

Fabindia has created a visibility in the international market either through its own stores or

through other retailers and boutiques and also through institutional sales. The main advantage

Fabindia has enjoyed is that its products have a distinctive and quintessential style and it can

easily be identified by potential customers.

Retail Outlets

The retail channel is already developed within India with almost 100 stores in Tier 1 and Tier

II cities. As of today, internationally Fabindia owns stores in Rome (Italy), Guangzhou

(China), Dubai (UAE), Manama (Bahrain) and Doha (Qatar). The product range consists of

garments for men, women, children and infants; garment accessories; home furnishings –

bed, bath, table and kitchen linen, upholstery fabric, curtains, floor coverings and a range of

non textile products like furniture, lights, lamps and stationery. In addition to handcrafted

clothing and home furnishings, Fabindia’s product line includes organic foods and body care

products.

Wholesale exports

As of today, Fabindia exports to more than 34 countries. The clients are wholesalers as well

as secondary retailers. Products exported include home linens as well as garments. Exports

are done as per the Terms and Conditions agreed by Fabindia and the customer. The export

being a very lucrative market, Fabindia develops a special collection for exports markets

twice every year. The special collections are showcased at the Indian Handicrafts and Gifts

Fair, New Delhi in Spring and Autumn. This collection draws on different techniques to

present a range of home furnishings comprising bed and table linen, with a focus on textures

– both visual and tactile. As different wholesalers and retailers flock to these fairs to address

their sourcing needs, Fabindia is able to reach out to potential clients.

Institutional Sales

Fabindia envisages servicing high business institutional segment especially the heritage

hotels and multinational corporate houses. It provides customization and interior designing

consulting for clients like heritage hotels, resorts and corporate houses.

7

Merchandise Mix:

During the early days, merchandising was not a planned activity. Whenever Bissell saw

something of interest, he procured it for display at the store. Sometimes he would also invite

the craftsmen, to display the products and assist in the sale. This orientation of customer

relationship later became a part of the company culture. The expansion in merchandize mix is

mainly done through customer feedback especially that of its loyal customers. Fabindia

believes: “A delighted Customer is our Best Brand Ambassador”

Fabindia does not follow any customer acquisition strategy. It instead focuses on customer

retention. Fabindia creates its market through its existing customers which is quite evident

from the fact that about 85% of its customers are repeat customers. The Unique Selling

Proposition of Fabindia is the quality of the fabric and the traditional style, which is always

in vogue. It has designed the stores’ decor and ambience keeping this in mind. It constantly

attempts to improve the quality of the products in order to retain its customers.

The company concentrates on customer feedback by maintaining a visitors’ register to record

customer views. The store managers prepare a report on buying pattern among consumers

which is periodically reviewed by the Product Selection Committee at Fabindia. Recently,

the CRM software has been implemented in a select few stores which aims to help in

maintaining a centralized database. This will help Fabindia in retaining customers by

building lasting relationships and improving loyalty. The implementation, however, is still in

its nascent stage, but is soon expected to be spread across all the stores in the country.

Fabindia also has the Mystery Shopper Program to gauge the customer satisfaction level.

Mystery shoppers posing as normal customers perform specific tasks such as purchasing a

product, asking questions, registering complaints or behaving in a certain way and then

provide detailed reports or feedback on their shopping experiences to the management. It

serves as an effective tool to improve the customer experience. Moreover, the brand

managers at Fabindia rely upon a concept of intuition. If a new line of traditional kurtis is

launched, the jewellery which suits the attire also gets launched. It automatically gets sold

without any promotion. Before launching any new product, be it traditional, western,

organics, jewellery or furniture, Fabindia looks into the value which a customer may feel by

having the product as a part of his/her life. Some customers are so inclined to Fabindia that

they just don’t believe in going elsewhere else, and don’t even tell other people that they

have purchased the particular item from Fabindia. This helps them create an image of

8

exclusiveness. Hence, uniqueness, innovation and intuition are the most important aspects of

Fabindia’s product planning.

Store layout and location:

The store layout in Fabindia depends upon the type of store. Fabindia works on various types

of stores which include concept stores as well as full fledged store. In a posh locality in a

metropolitan city, Fabindia works as a full fledged store which has almost all the product

lines. On the other hand, in a concept store, the place specific products are retailed. Market

potential determines store location for Fabindia, which is fast expanding in Tier II cities like

Bhopal where still mall culture is nonexistent. The layout usually keeps clothes section at the

back of the store and the entrance area is utilized for home products. The exclusive jewellery

counter is also kept in the fronts.

Why Fabindia?

Fabindia since its inception has concentrated on cultivating an image of ‘Indianness’.

Relying on its word of mouth publicity, Fabindia has been highly successful in creating a

pool of repeat customers, who come again and again for the unique Fabindia experience. The

core values of Fabindia have always been to provide its customers with quality products

which reflect the unique Indian culture and tradition. Since most of Fabindia’s customers are

repeat customers, the motivating factor for the customer remains the quality and consistency

of product and the service provided by Fabindia.

The major problems for Fabindia occur in the maintaining the consistency of the products.

Since the supply and the manufacturing happen on a small scale over a large geographical, it

becomes difficult for the firm to maintain the same level of quality. Fabindia makes sure that

a minimum level of quality is maintained, but it also has strong relationships with all its

suppliers. It makes sure that a supplier does not suffer due to marginal quality lapses. The

Fabindia customers also understand this and are largely tolerant of the discrepancies in

garment in terms of size & prints etc. In fact, over 77% of the customers buy Fabindia,

because of the ‘Fabindia’ brand and its contribution to improving the life of rural artisans.

Fabindia has in store posters which educate customers about the dyes used in the products,

and also the possible problems which could be faced in washing and using them. Thus,

Fabindia has succeeded in making the inherent inconsistency of the product into an appeal

factor by positioning each garment as ‘unique’. Also, even though the products sometimes

9

have problems due to the fading of colours, or shrinkage, the service personnel make sure

that the customers are not inconvenienced on account of such problems. The general

response is to exchange the garment for another, which makes sure that the customer goes

back happy, and remains a loyal customer.

In case of organic products, it is still a nascent market. Its appeal is mostly to people who are

already aware of the product offering and have been using similar products. The major

problem there is erratic delivery and product availability, which does lead to customer

dissatisfaction. But this is a very small part of the clientele. Over 83% of Fabindia’s

customers go back satisfied, with 58% being highly satisfied with the brand and its offerings.

Fabindia has been expanding its product range to include jewellery, home furnishings, Body

care products, etc. This has mostly been done as an extension of the Garment brand. For

example, the men’s garment range was started because the founder, John Bissell, needed

shirts. Therefore, for quite some time, the Fabindia men’s garment line was restricted to

shirts and that too in only one size, because it was John’s shirt size! Although Fabindia

appeals to the Indian customer’s need to remain rooted with the tradition and culture, it has

made sure that it changes with the times. It had inculcated a large number of western fashions

and garments into its range. This is done keeping in mind the customer feedback received

and the inputs given by the store managers. Fabindia relies on its managers to identify client

needs and trim the store offerings accordingly.

International Presence

Fabindia has gradually attained a strong foothold in India. It has become the niche player of

choice for the urban and semi-urban masses when it comes to buying something with “Indian

flavour” added. The constant product innovations and agility in identifying associated

product lines has been the key. Be it garments with distinctive folk patterns to furniture with

carvings and designs reflective of rich Indian heritage, the products have an intrinsic appeal

to customers. As of January 2009, they have 97 stores across the length of the country. They

have also opened international stores in Italy, UAE, Qatar and China. Their network is spread

across 34 countries worldwide and 511 destinations in India.

10

Market

From a turnover of 36 crore rupees in 2000-01, Fabindia has grown to having a turnover of

Rs.130 crore in 2005-06. It registered a CAGR of about 38% in the period 2002-06. Such

phenomenal growth has not come at the cost of profits. The profitability has been maintained

at a rate of 6% for the entire period. For Fabindia William Bissell has set a very ambitious

target of reaching 250 stores and a turnover of Rs.1000 crore by 2011. The growth is

expected to come from new stores as well as increase in sales from existing stores. That

increase will be achieved by increased emphasis on premium products. Also, Fabindia has

attempted to decrease its dependence on fabric based businesses by increasing its other

product lines. Currently organic foods, body care products and handicrafts form a significant

part of its total sales. Growth in locations was expected to come from expansion in overseas

markets as well as a greater penetration of the markets in smaller towns in India. As

mentioned earlier, Fabindia planned to expand significantly in tier-II and tier-III cities in

India. India has a flourishing retail business but most of it is in the unorganized sector. There

are estimated to be over 120 lakh stores in the country. Of this, organized retail is only 3%

but is growing at the rate of 18%. This organized retail sector is vying for a share of the

spending of India’s rapidly growing middle class whose purchasing power is estimated to be

around Rs. 10 lakh crore. An estimate made by a professional demand forecaster shows that

out of the total retail business potential, the Indian market for ethnic wear is likely to be a

about Rs. 9000 crore.For geographies outside of India, there is a strong mysticism about

Indian culture and hence the products reflective of Indian folk art hold great potential in

those markets. Given the over 8% growth in the Indian market and an upwardly mobile India

consumer, it was quite clear that product and services enable a customer to make a statement,

are going to grow in volume and value. The question before Fabindia Management is that of

making Fabindia product exclusive or mass product. If he decided to make it exclusive, then

it will have to look at issues of product design, store layout and even the store ambiance.

Increasingly, its competitors were using ethnic themes for their store layouts as also for

designing garments.

11

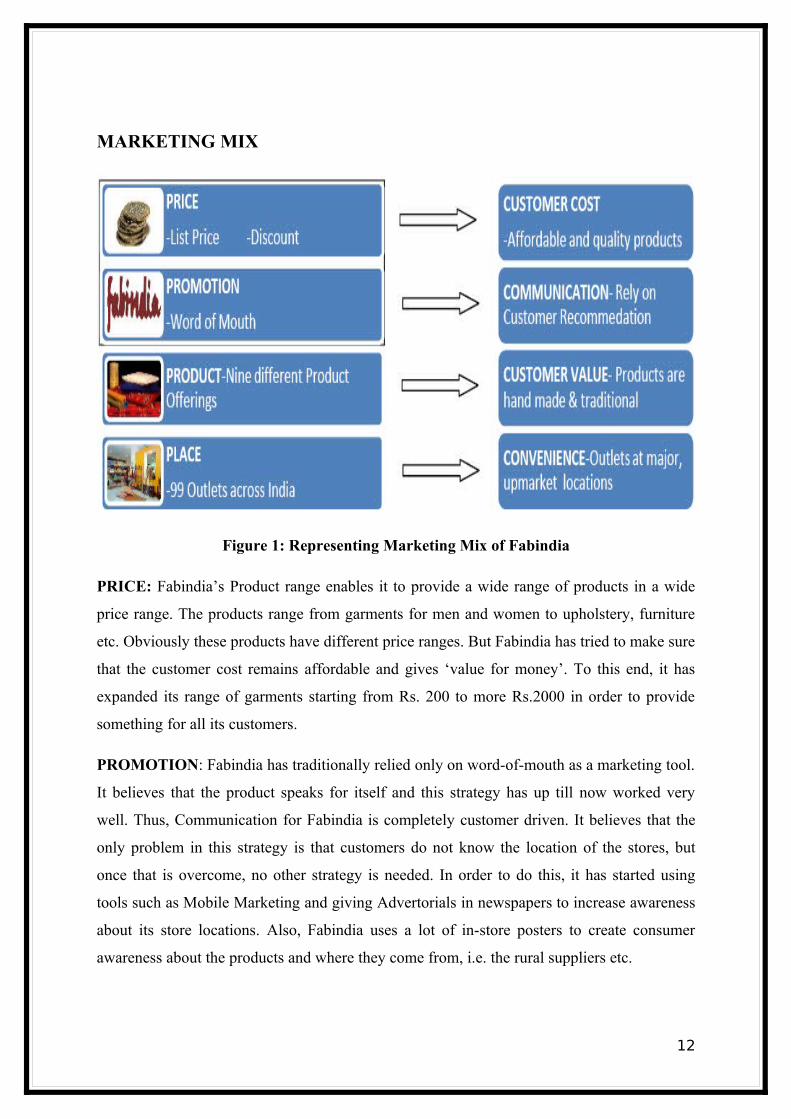

MARKETING MIX

Figure 1: Representing Marketing Mix of Fabindia

PRICE: Fabindia’s Product range enables it to provide a wide range of products in a wide

price range. The products range from garments for men and women to upholstery, furniture

etc. Obviously these products have different price ranges. But Fabindia has tried to make sure

that the customer cost remains affordable and gives ‘value for money’. To this end, it has

expanded its range of garments starting from Rs. 200 to more Rs.2000 in order to provide

something for all its customers.

PROMOTION: Fabindia has traditionally relied only on word-of-mouth as a marketing tool.

It believes that the product speaks for itself and this strategy has up till now worked very

well. Thus, Communication for Fabindia is completely customer driven. It believes that the

only problem in this strategy is that customers do not know the location of the stores, but

once that is overcome, no other strategy is needed. In order to do this, it has started using

tools such as Mobile Marketing and giving Advertorials in newspapers to increase awareness

about its store locations. Also, Fabindia uses a lot of in-store posters to create consumer

awareness about the products and where they come from, i.e. the rural suppliers etc.

12

PRODUCT: Fabindia’s products are its differentiating factor and it has made sure over the

years that the quality and the style of the products is maintained. It has a large product range

which includes -Garments for men and women, Accessories, Home Linen and Furnishings,

Home Products, Floor Coverings, Body Care Products and more recently, Organic Food

Products and ethnic Jewellery. All the products have at least one factor which is handmade

and thus, supports artisans. This is a very strong customer value leveraged by Fabindia,

which is that of traditional, ethnic products which support poor artisans and provide

livelihood to a large number of people.

PLACE: Fabindia has stores in more than 95 locations across India. The stores include the

premium, regular and concept stores. It is trying to increase coverage in order to make sure

that the products are available at the largest number of places possible. It also differentiates

its stores according to the products stored. For eg. In Mumbai the Khar Store is only a

Furniture and Upholstery while the nearby Pali Hill stores Garments, organic products, Body

products and Jewellery. This also ensures convenience for the customers since the products

are either available in the same store or in nearby stores.

COMPETITION:

Competition Faced by Fabindia is from both the organised and unorganised retail sector. The

unorganised sector has the local tailors who provide customised garments to the customers

at reasonable prices and the local NGOs selling wares. However, the scale of operations does

not pose a major threat to Fabindia. One such competitor is the Delhi Haat, an upgraded

traditional weekly market, located in the hub of south Delhi. The place has been developed

by the Tourist Department of Delhi to enhance the craftsmanship of our country. It is an

amalgamation of craft, food and cultural activities. Unlike the village haat, the Delhi haat is a

permanent haat that offers a kaleidoscopic view of the richness and diversity of the Indian

handicrafts and artefacts. Spread over a spacious six acre area, imaginative landscaping,

creative planning, and the traditional village architectural style provide for a major tourist

attraction. One is very happy to get goods at a very nominal price here. Another such

regional competitor is the market outside the law garden in Ahmadabad. The law garden is a

famous place for buying handicrafts and Gujarati outfits from local hawkers. This garden

provides one with various recreational options like music, theatre, rides for kids and a great

variety of Gujarati food. The common thread that links both the Delhi Haat and the Law

Garden is the experience they create for the customer by combining crafts, food and cultural

13

activities. Such an experience is lacking in case of Fabindia. A tourist would be lured by the

overall ambience he gets in the former case.

However, a far greater threat is posed by the organised sector especially Government owned

Khadi Gram Udyog outlets and Cottage Industries Emporiums across the country. The

product mix offered by both is similar to Fabindia. Also, they have the backing of the

governments. However, the quality of products and service provided by Fabindia is perceived

to be higher than that of the government run outlets. Fabindia’s main competitors are the

ethnic wear retailers like Khadder, W and Good Things, who are also expanding at a rapid

pace. W, for example, has well over 30 exclusive stores now, in addition to being available at

some multi-brand outlets.. There is also severe competition from the ethnic wear labels of

modern Indian retail chains, such as Shoppers Stop and Pantaloons. Stand alone stores like

Shristi and Biba in Bangalore, Prapti in Kolkata and Sadka and Shoma in Delhi have been

doing well for a while and could pose a challenge by expanding. New competition is

expected from overseas retailers also. The government has already permitted single brand

retailers to set up shop and others like Carrefour, Walmart and Metro have devised ways to

get into the Indian market. Powerful Indian business houses like Tata, Reliance and Birla are

expanding their retail businesses.

The organised retail sector also includes outlets by corporate houses like Lifestyle and

Westside which cater to the same demographic profile. However, the products served are

more contemporary in nature and does not aim at the same target audience. Stores like

Hansiba have the same target audience, but do not have the reach of Fabindia.

14

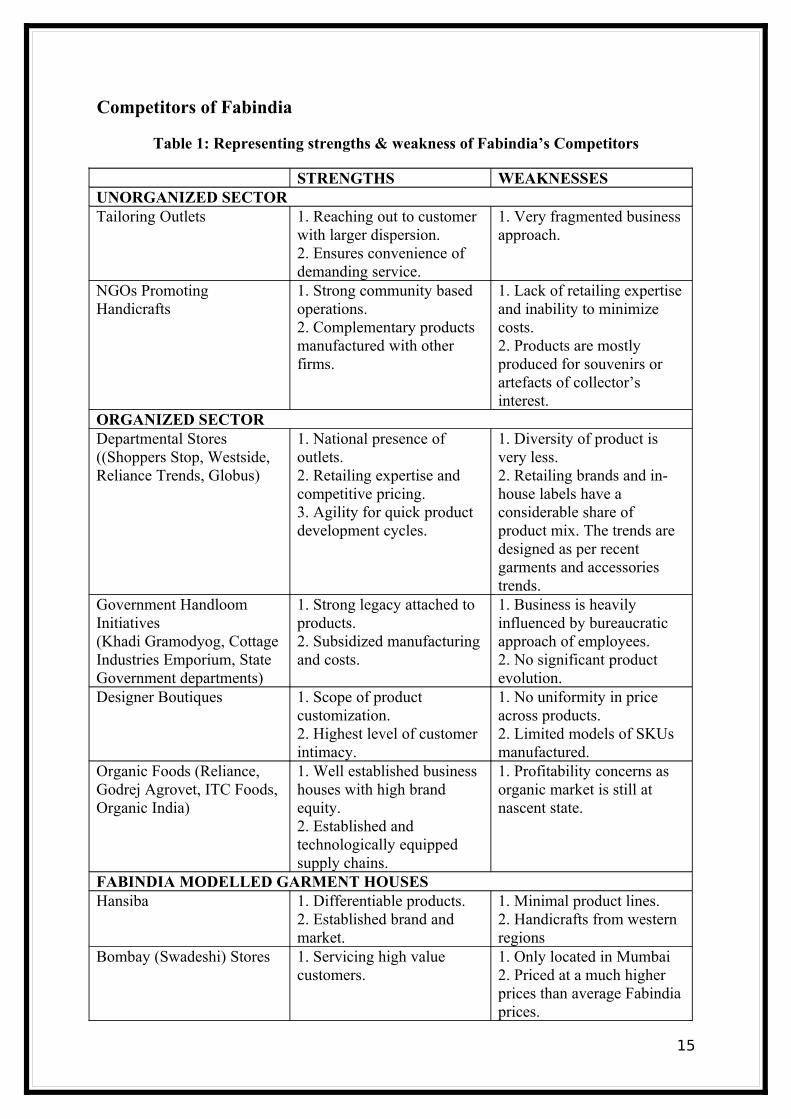

Competitors of Fabindia

Table 1: Representing strengths & weakness of Fabindia’s Competitors

STRENGTHS WEAKNESSESUNORGANIZED SECTORTailoring Outlets 1. Reaching out to customer

with larger dispersion.2. Ensures convenience of demanding service.

1. Very fragmented business approach.

NGOs PromotingHandicrafts

1. Strong community based operations.2. Complementary products manufactured with other firms.

1. Lack of retailing expertise and inability to minimize costs.2. Products are mostly produced for souvenirs or artefacts of collector’s interest.

ORGANIZED SECTORDepartmental Stores ((Shoppers Stop, Westside, Reliance Trends, Globus)

1. National presence of outlets.2. Retailing expertise and competitive pricing.3. Agility for quick product development cycles.

1. Diversity of product is very less.2. Retailing brands and in-house labels have a considerable share of product mix. The trends are designed as per recent garments and accessories trends.

Government HandloomInitiatives(Khadi Gramodyog, CottageIndustries Emporium, StateGovernment departments)

1. Strong legacy attached to products.2. Subsidized manufacturing and costs.

1. Business is heavily influenced by bureaucratic approach of employees.2. No significant product evolution.

Designer Boutiques 1. Scope of product customization.2. Highest level of customer intimacy.

1. No uniformity in price across products.2. Limited models of SKUs manufactured.

Organic Foods (Reliance,Godrej Agrovet, ITC Foods,Organic India)

1. Well established business houses with high brand equity.2. Established and technologically equipped supply chains.

1. Profitability concerns as organic market is still at nascent state.

FABINDIA MODELLED GARMENT HOUSESHansiba 1. Differentiable products.

2. Established brand and market.

1. Minimal product lines.2. Handicrafts from westernregions

Bombay (Swadeshi) Stores 1. Servicing high value customers.

1. Only located in Mumbai2. Priced at a much higherprices than average Fabindia prices.

15

SWOT Analysis

STRENGTHS

The product mix available at Fabindia can be easily differentiated by the customer. The uniqueness of the fabric or styling has created a new category as identified by the customer as ethnic wear. This leads to a very high brand recognition and connects with the customer value. It has an enviable presence in diverse product lines as garments, furniture, furnishing and upholstery, body care, organic foods and the very recently introduced jewellery line. Due to its variety of stores, it can reach to different categories of customers.

WEAKNESS

This absence of promotions strategy is believed to be resulting in sales below its potential levels. The sourcing strategy followed for accepting raw materials is heavily supplier centric. In the past there have been incidences when due to delay in sending supplies for winter garments manufacture, inventory was carried over to the next year and suppliers were not made to share the damage. It operates through its own stores and that too fed by a centralized hub model of supply chain management.

OPPORTUNITIES

Merchandising within stores is still in a rudimentary stage. The shopper navigation can be greatly enhanced by focusing on the store layout and appropriate merchandising techniques which succinctly create individual product areas. There is great opportunity to grow along with the fast growing organic foods department. Out of the total customer base for Fabindia, a high percentage comprises repeat customers. This leads to an inference that Fabindia can focus on customer acquisition strategies.

THREATS

Already many firms have tried to recreate the model of Fabindia. Hence, .Fabindia needs to innovate and diversify into different product categories. It should be nimble and responsive to changing tastes of its customers. Also as it is suppliers are mostly artisans and manufacturing is labour driven, controlling costs can be a challenge. Also it needs to ensure that the customer service provided and the quality of products is consistent.

16

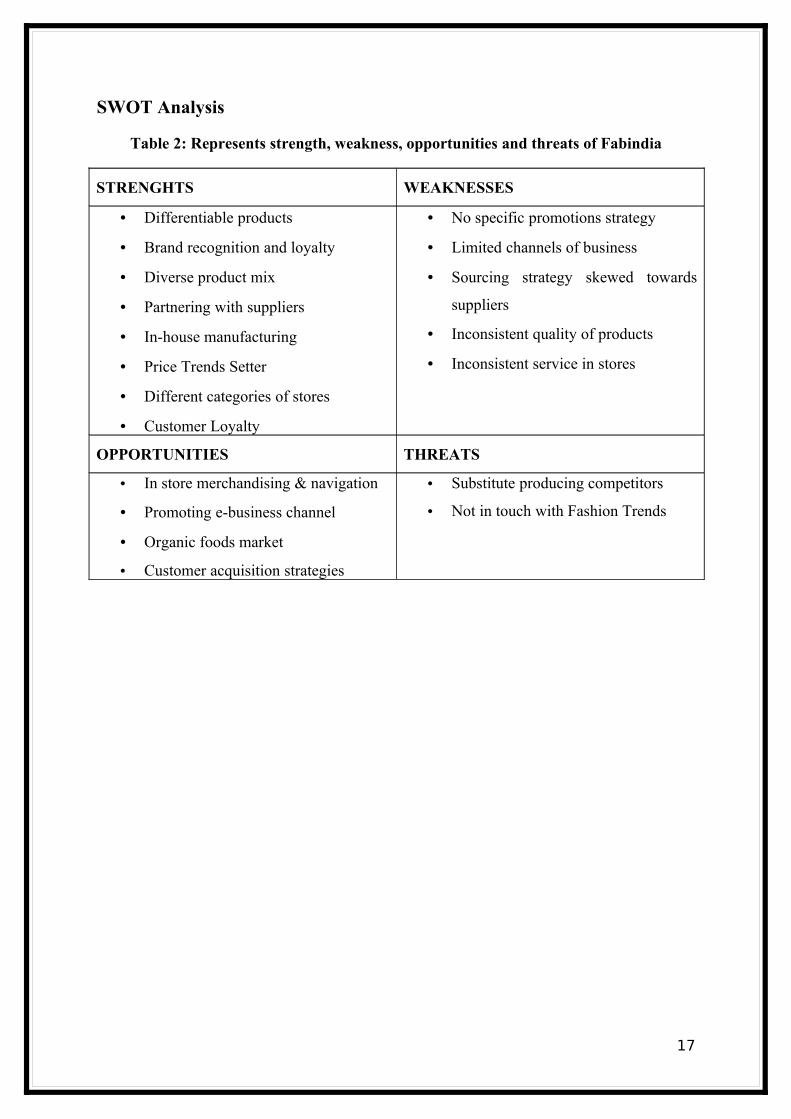

SWOT Analysis

Table 2: Represents strength, weakness, opportunities and threats of Fabindia

STRENGHTS WEAKNESSES

• Differentiable products

• Brand recognition and loyalty

• Diverse product mix

• Partnering with suppliers

• In-house manufacturing

• Price Trends Setter

• Different categories of stores

• Customer Loyalty

• No specific promotions strategy

• Limited channels of business

• Sourcing strategy skewed towards

suppliers

• Inconsistent quality of products

• Inconsistent service in stores

OPPORTUNITIES THREATS

• In store merchandising & navigation

• Promoting e-business channel

• Organic foods market

• Customer acquisition strategies

• Substitute producing competitors

• Not in touch with Fashion Trends

17

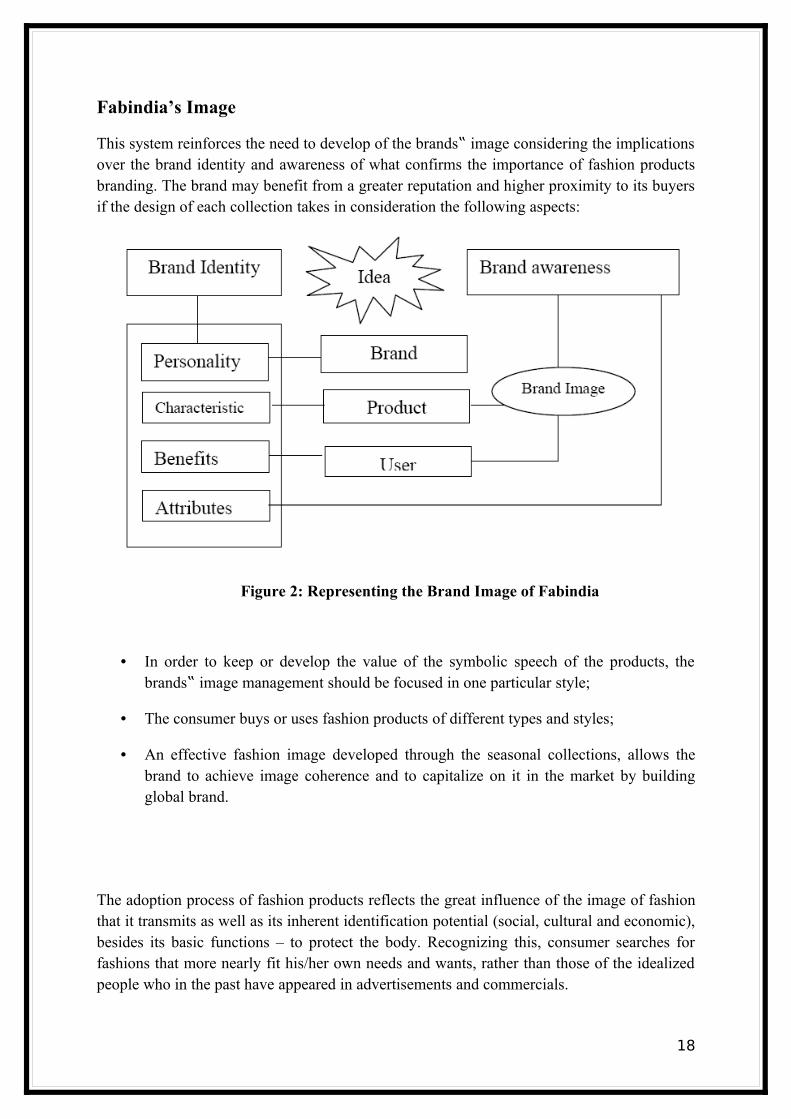

Fabindia’s Image

This system reinforces the need to develop of the brands image considering the implications‟ over the brand identity and awareness of what confirms the importance of fashion products branding. The brand may benefit from a greater reputation and higher proximity to its buyers if the design of each collection takes in consideration the following aspects:

Figure 2: Representing the Brand Image of Fabindia

• In order to keep or develop the value of the symbolic speech of the products, the brands image management should be focused in one particular style; ‟

• The consumer buys or uses fashion products of different types and styles;

• An effective fashion image developed through the seasonal collections, allows the brand to achieve image coherence and to capitalize on it in the market by building global brand.

The adoption process of fashion products reflects the great influence of the image of fashion that it transmits as well as its inherent identification potential (social, cultural and economic), besides its basic functions – to protect the body. Recognizing this, consumer searches for fashions that more nearly fit his/her own needs and wants, rather than those of the idealized people who in the past have appeared in advertisements and commercials.

18

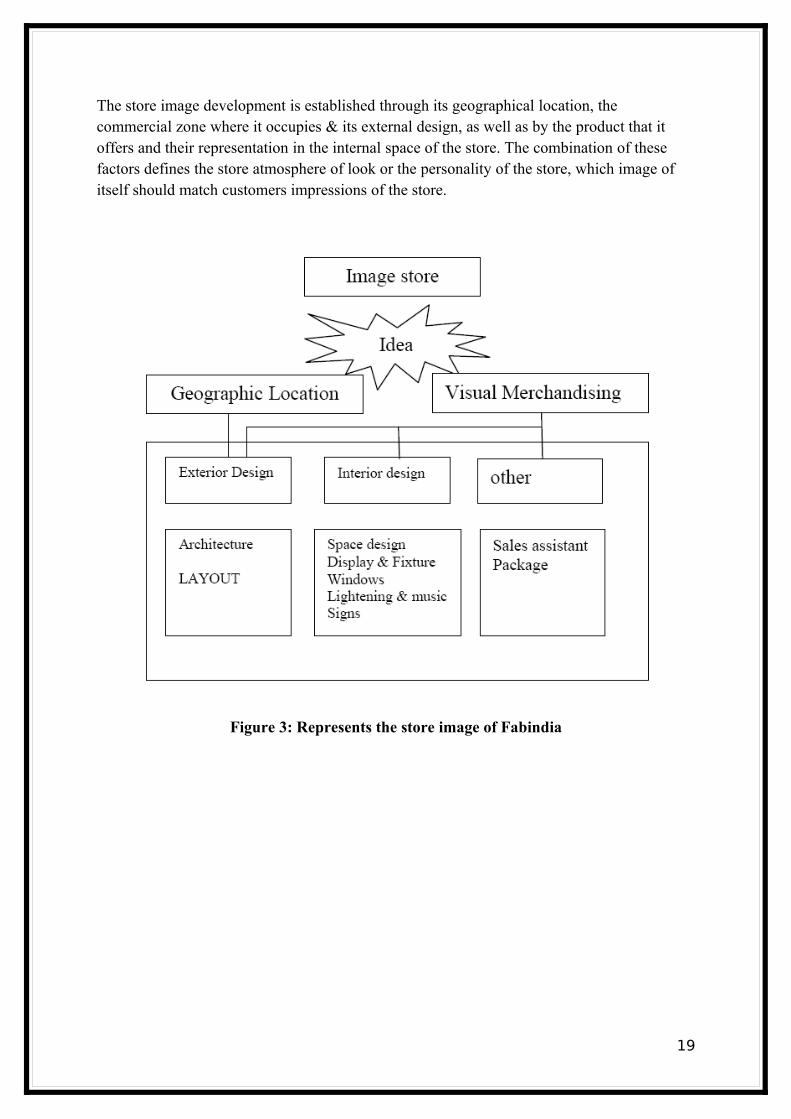

The store image development is established through its geographical location, the commercial zone where it occupies & its external design, as well as by the product that it offers and their representation in the internal space of the store. The combination of these factors defines the store atmosphere of look or the personality of the store, which image of itself should match customers impressions of the store.

Figure 3: Represents the store image of Fabindia

19

Consumer Segmentation

Fab India has used following bases of segmentation

Demographic: They used disposable incomes as criteria to segment their customer bases. Fab India caters to only Upper middle class and upper class. Since education, occupation and incomes go hand in hand so they target highly educated people in good professions who have their own set of groups, hence Fab India does not advertise, they believe in word of mouth of this group of people.

Figure 4: Represents the Segment to which Fabindia Caters

Psychographic: Psychographic profile of a customer comprises his activities, interests and opinions (AIO). Fab India has focussed on people who have genuine interest in ethnic wear and handicrafts and the people who hold positive and strong opinions about handicrafts, Indian craftsmen and this entire effort and concept.

Lifestyle segmentation: According to lifestyle segmentation there are 8 classes of people: Actualisers, fulfillers, achievers, experiencers, believers, strivers, makers and strugglers. Fab India targets Achievers and Believers. Achievers are attracted to distinct and premium products. Believers have strong opinions about certain issues and attracted to a particular category of product like handicrafts.

Thus Fab India targets on its culture loving, people of high income groups.

20

Personality Straits of Fabindia Consumers

Personality of an individual reflects individual differences. Personality is an important tool of consumer behaviour as it helps in categorisation of consumers into different groups on basis of their traits.

Fab India has a brand personality conveying traditions, stability, sticking to your roots, appraising Indian factor, social responsiveness so people whose personality conforms to these traits are likely to be brand loyal to Fab India.

Even the color of the logo of Fab India i.e. RED is chosen to convey Indianness, since red is a holy color of India. Moreover red conveys royal, richness, ethnic so people whose personality coincides with these traits are the target

of the brand. This color further strengthens the brand personality of Fab India as a Handicraft Outlet.

According to Non-Freudian Personality theory, Fab India focuses on people with detatched personalities, what ever be the latest trend in western wear they still go for centuries old Chanderi prints. Such individuals are independent, self reliant, and want to be free from obligations.

According to Trait theory, Fab India focuses on people who are

• High on consumer ethnocentrism, i.e. such customers are more rigid and attracted towards their culture.

• Verbalisers (prefer written and verbal information) rather than visualizers (prefer only visual information of product). Usually Fab India consumers are aware of the history or belonging or at least worth of the piece they are purchasing.

• High in NC (Need for cognition) are more responsive to product related description and are more responsive to written message, while customers who are low in NC are more influenced with the glamour associated by the product rather than stressing on knowing what actually the product is.

• High on consumer materialism as their customers seek their possessions for greater personal satisfaction. They want to have a unique collection of possessions like Kota Doria fro Rajasthan, Bidri work from Andhra Pradesh.

• Highly dogmatic since these customers are more likely to prefer traditional alternatives over traditional products.

• Low on consumer innovativeness as they are more likely to stick to their favourite prints or fabrics or even styles. A person who is loyal to Lucknawi Chickankari is less likely to accept deviations from traditional chikan kari.

21

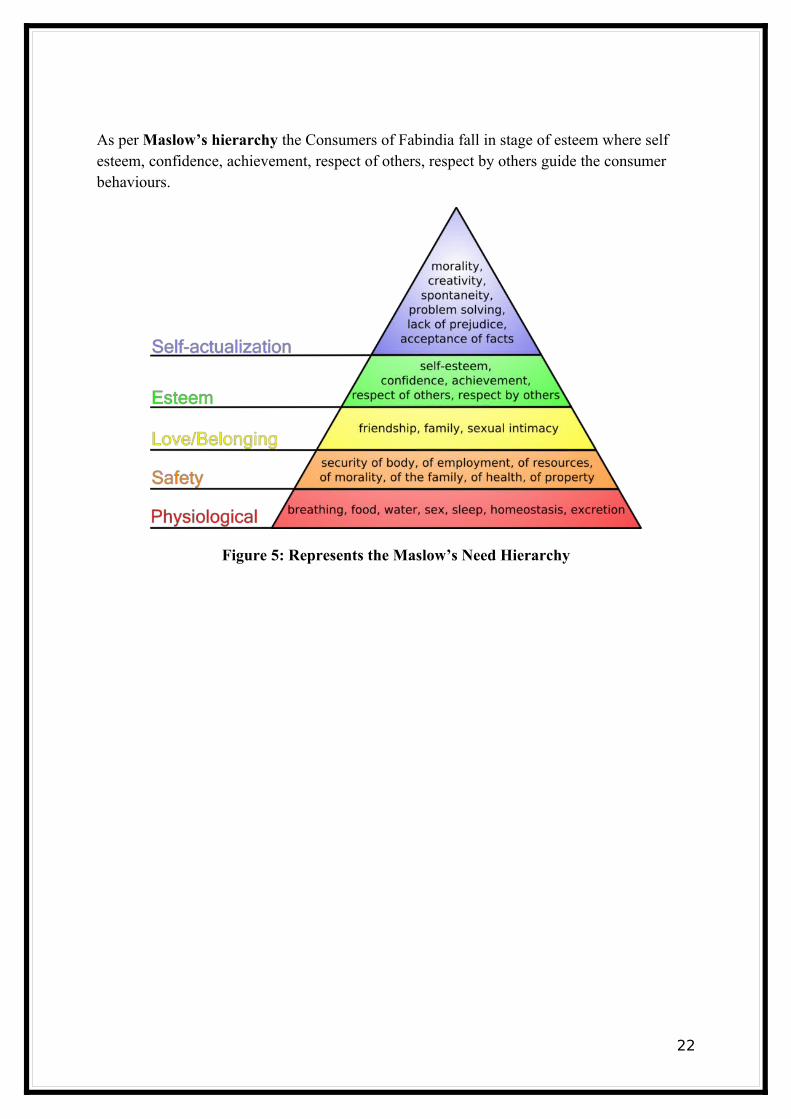

As per Maslow’s hierarchy the Consumers of Fabindia fall in stage of esteem where self esteem, confidence, achievement, respect of others, respect by others guide the consumer behaviours.

Figure 5: Represents the Maslow’s Need Hierarchy

22

Chapter 4

Data Analysis and findings

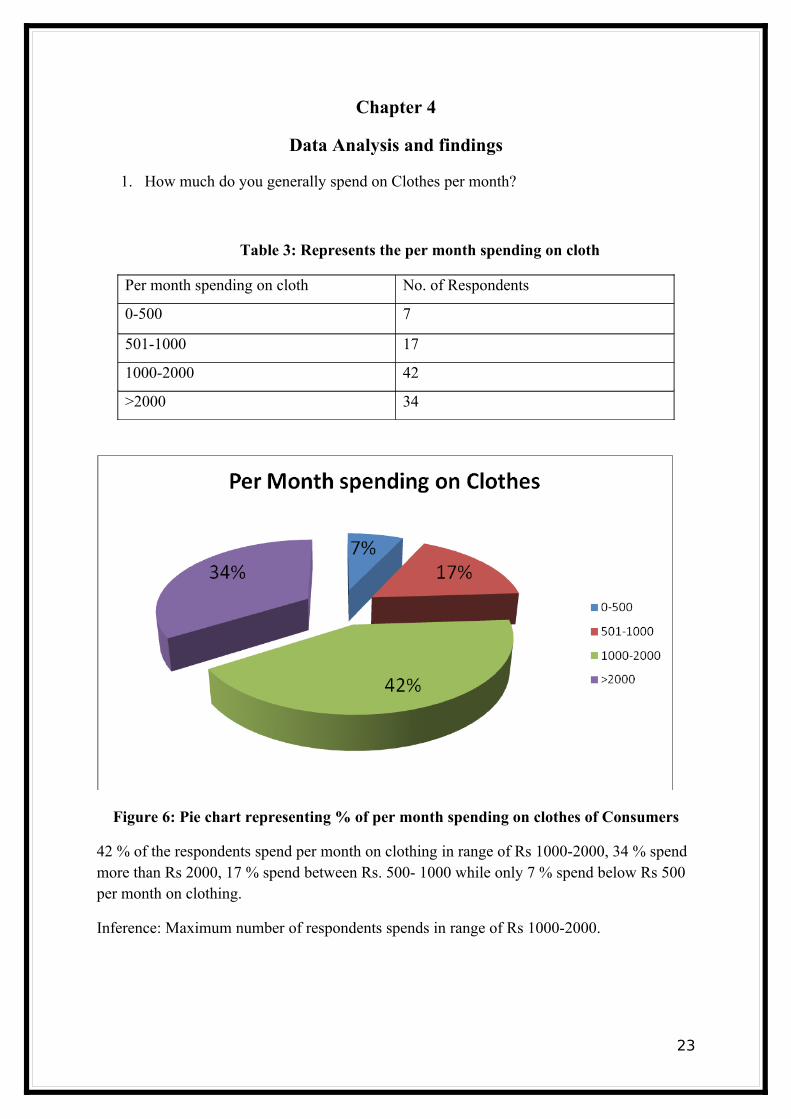

1. How much do you generally spend on Clothes per month?

Table 3: Represents the per month spending on cloth

Per month spending on cloth No. of Respondents

0-500 7

501-1000 17

1000-2000 42

>2000 34

Figure 6: Pie chart representing % of per month spending on clothes of Consumers

42 % of the respondents spend per month on clothing in range of Rs 1000-2000, 34 % spend more than Rs 2000, 17 % spend between Rs. 500- 1000 while only 7 % spend below Rs 500 per month on clothing.

Inference: Maximum number of respondents spends in range of Rs 1000-2000.

23

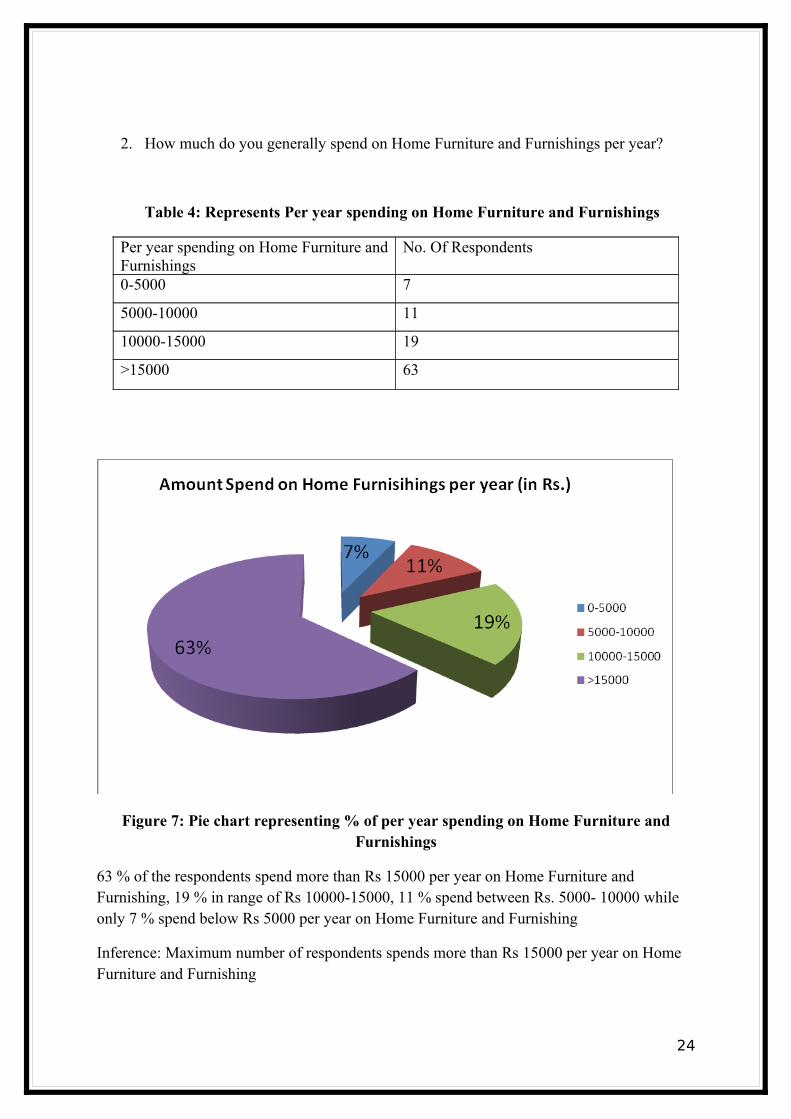

2. How much do you generally spend on Home Furniture and Furnishings per year?

Table 4: Represents Per year spending on Home Furniture and Furnishings

Per year spending on Home Furniture and Furnishings

No. Of Respondents

0-5000 7

5000-10000 11

10000-15000 19

>15000 63

Figure 7: Pie chart representing % of per year spending on Home Furniture and Furnishings

63 % of the respondents spend more than Rs 15000 per year on Home Furniture and Furnishing, 19 % in range of Rs 10000-15000, 11 % spend between Rs. 5000- 10000 while only 7 % spend below Rs 5000 per year on Home Furniture and Furnishing

Inference: Maximum number of respondents spends more than Rs 15000 per year on Home Furniture and Furnishing

24

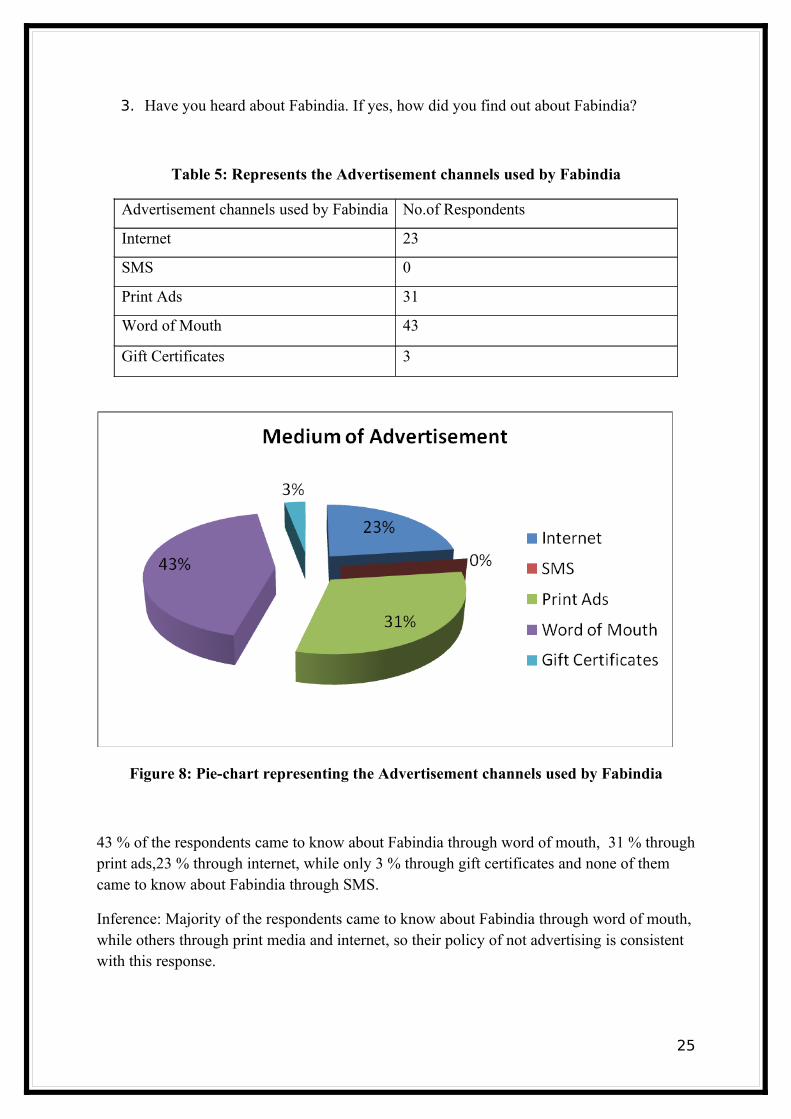

3. Have you heard about Fabindia. If yes, how did you find out about Fabindia?

Table 5: Represents the Advertisement channels used by Fabindia

Advertisement channels used by Fabindia No.of Respondents

Internet 23

SMS 0

Print Ads 31

Word of Mouth 43

Gift Certificates 3

Figure 8: Pie-chart representing the Advertisement channels used by Fabindia

43 % of the respondents came to know about Fabindia through word of mouth, 31 % through print ads,23 % through internet, while only 3 % through gift certificates and none of them came to know about Fabindia through SMS.

Inference: Majority of the respondents came to know about Fabindia through word of mouth, while others through print media and internet, so their policy of not advertising is consistent with this response.

25

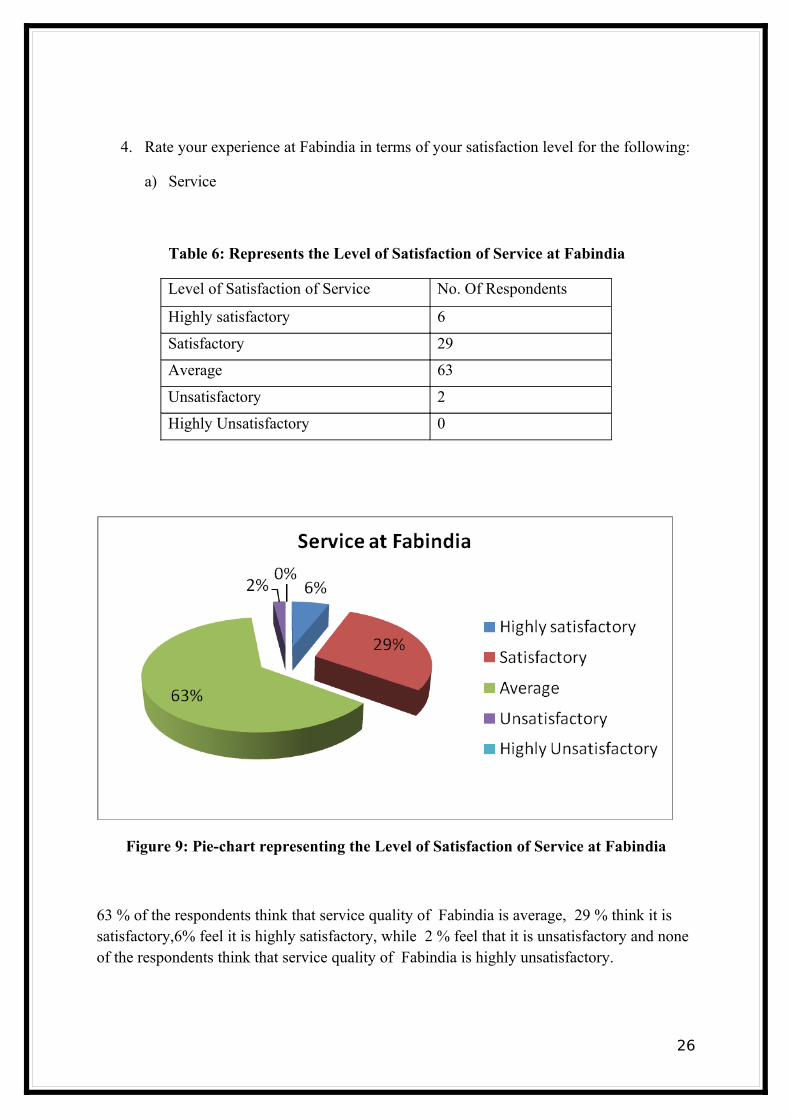

4. Rate your experience at Fabindia in terms of your satisfaction level for the following:

a) Service

Table 6: Represents the Level of Satisfaction of Service at Fabindia

Level of Satisfaction of Service No. Of Respondents

Highly satisfactory 6

Satisfactory 29

Average 63

Unsatisfactory 2

Highly Unsatisfactory 0

Figure 9: Pie-chart representing the Level of Satisfaction of Service at Fabindia

63 % of the respondents think that service quality of Fabindia is average, 29 % think it is satisfactory,6% feel it is highly satisfactory, while 2 % feel that it is unsatisfactory and none of the respondents think that service quality of Fabindia is highly unsatisfactory.

26

Inference: Majority of the respondents think that service quality of Fabindia is average,while a small chunk feels it is unsatisfactory so services policy of Fab India has been doing good but they further need to work on this aspect.

27

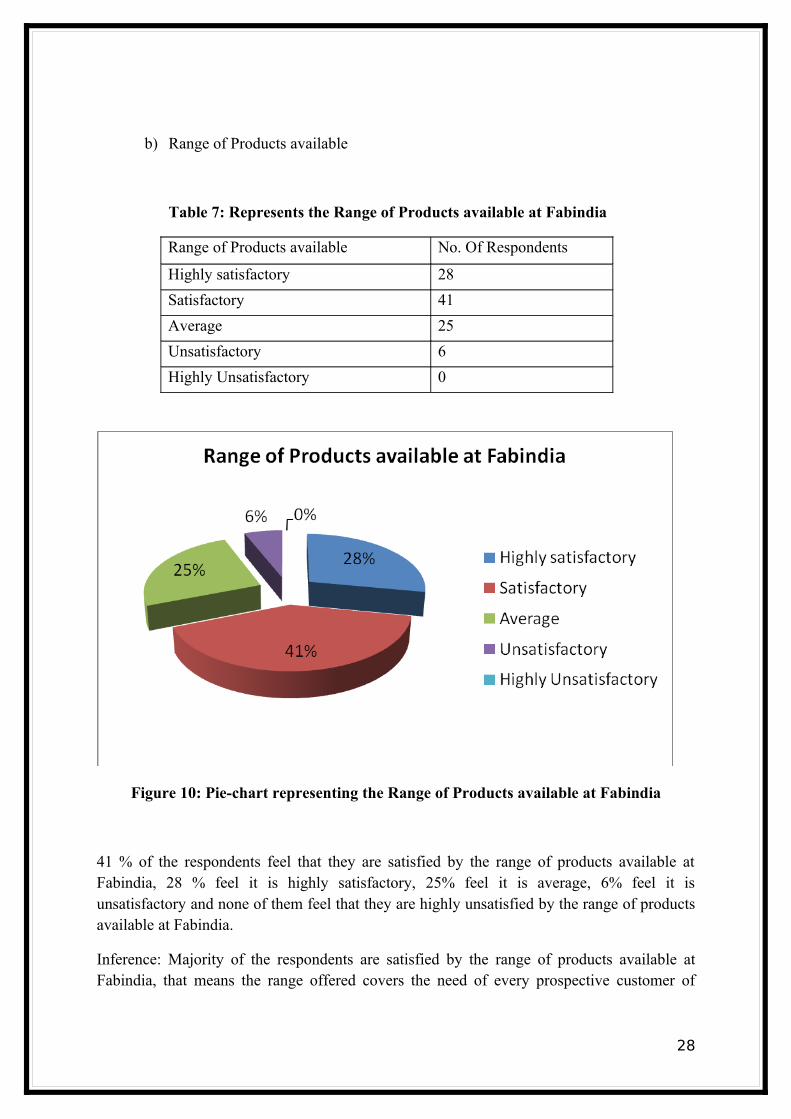

b) Range of Products available

Table 7: Represents the Range of Products available at Fabindia

Range of Products available No. Of Respondents

Highly satisfactory 28

Satisfactory 41

Average 25

Unsatisfactory 6

Highly Unsatisfactory 0

Figure 10: Pie-chart representing the Range of Products available at Fabindia

41 % of the respondents feel that they are satisfied by the range of products available at Fabindia, 28 % feel it is highly satisfactory, 25% feel it is average, 6% feel it is unsatisfactory and none of them feel that they are highly unsatisfied by the range of products available at Fabindia.

Inference: Majority of the respondents are satisfied by the range of products available at Fabindia, that means the range offered covers the need of every prospective customer of

28

Fabindia, still 6% think it is unsatisfactory, so they can ask their unsatisfied customers and launch the required products.

29

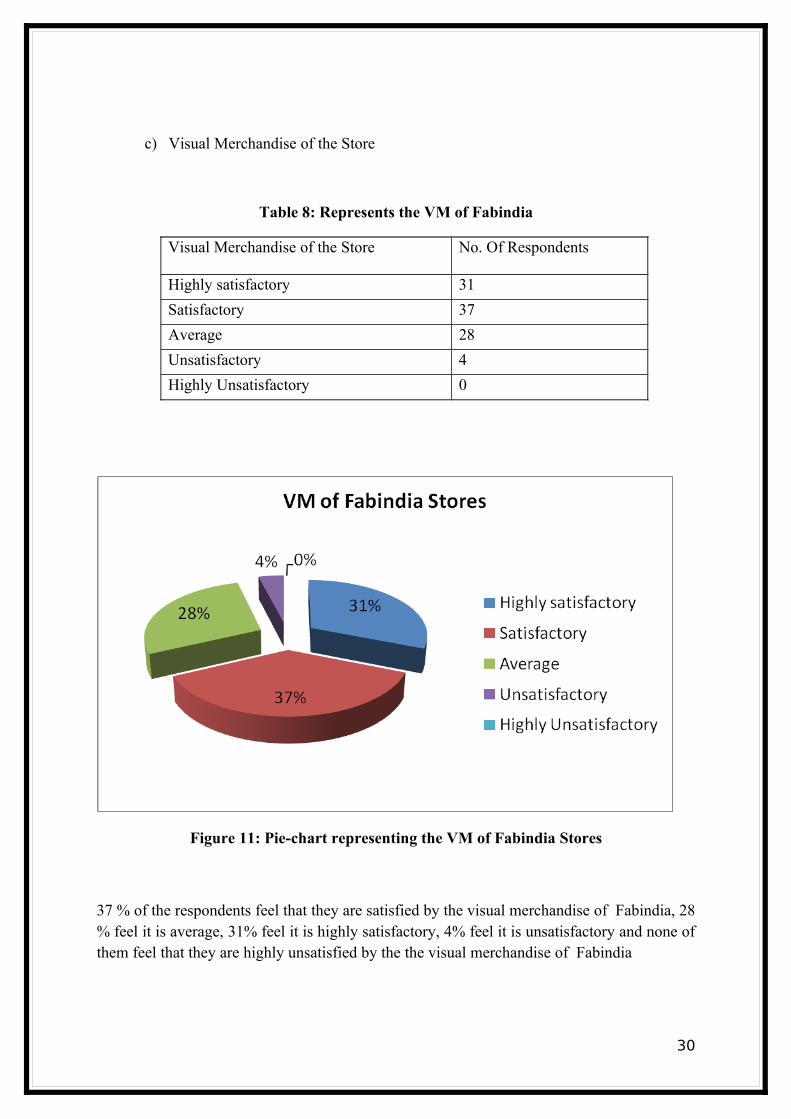

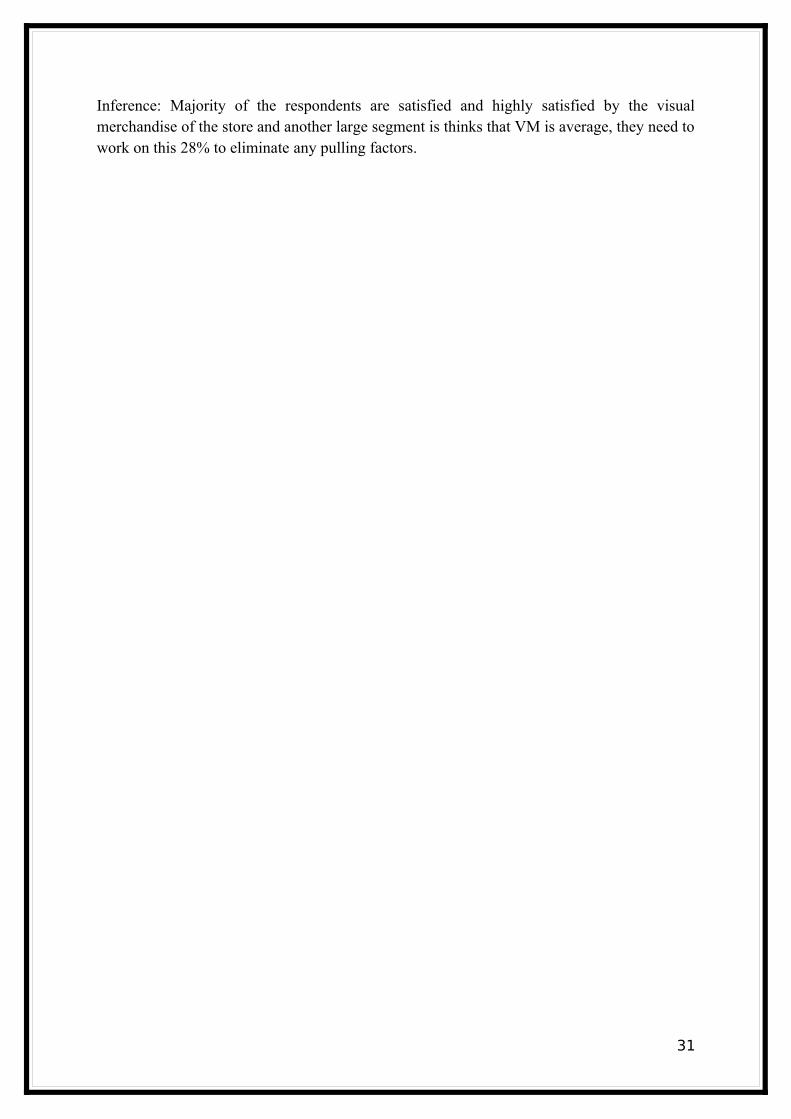

c) Visual Merchandise of the Store

Table 8: Represents the VM of Fabindia

Visual Merchandise of the Store No. Of Respondents

Highly satisfactory 31

Satisfactory 37

Average 28

Unsatisfactory 4

Highly Unsatisfactory 0

Figure 11: Pie-chart representing the VM of Fabindia Stores

37 % of the respondents feel that they are satisfied by the visual merchandise of Fabindia, 28 % feel it is average, 31% feel it is highly satisfactory, 4% feel it is unsatisfactory and none of them feel that they are highly unsatisfied by the the visual merchandise of Fabindia

30

Inference: Majority of the respondents are satisfied and highly satisfied by the visual merchandise of the store and another large segment is thinks that VM is average, they need to work on this 28% to eliminate any pulling factors.

31

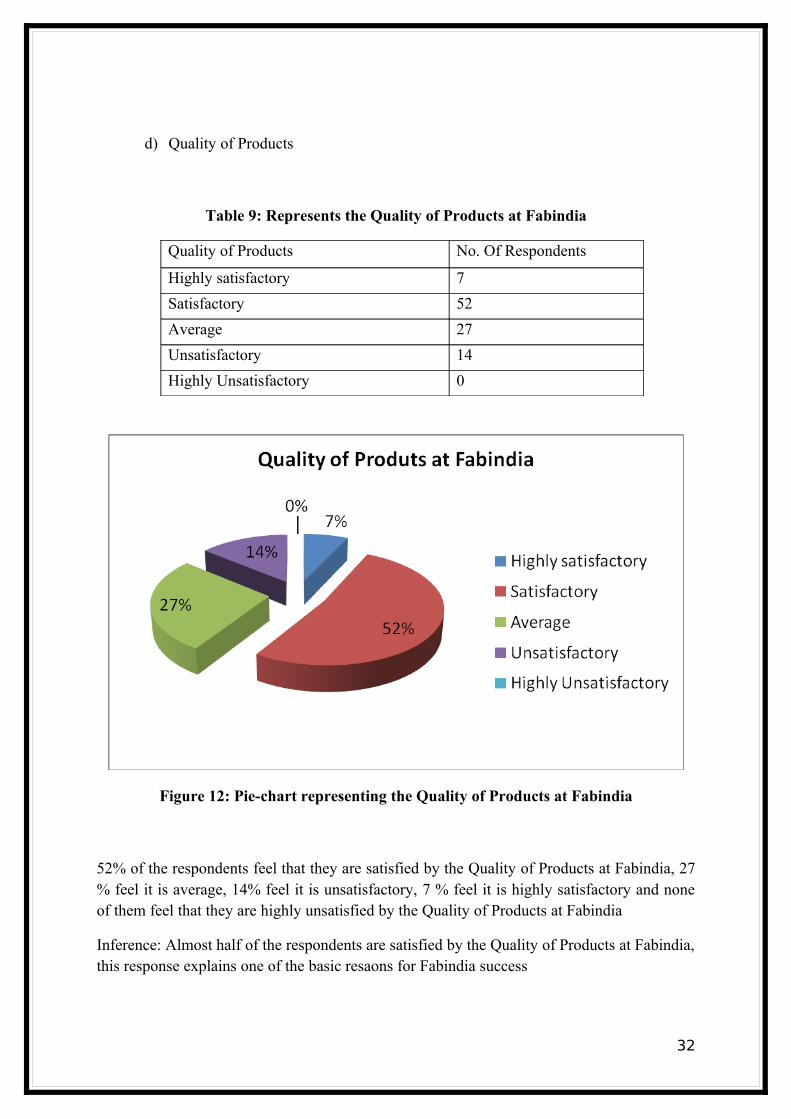

d) Quality of Products

Table 9: Represents the Quality of Products at Fabindia

Quality of Products No. Of Respondents

Highly satisfactory 7

Satisfactory 52

Average 27

Unsatisfactory 14

Highly Unsatisfactory 0

Figure 12: Pie-chart representing the Quality of Products at Fabindia

52% of the respondents feel that they are satisfied by the Quality of Products at Fabindia, 27 % feel it is average, 14% feel it is unsatisfactory, 7 % feel it is highly satisfactory and none of them feel that they are highly unsatisfied by the Quality of Products at Fabindia

Inference: Almost half of the respondents are satisfied by the Quality of Products at Fabindia, this response explains one of the basic resaons for Fabindia success

32

33

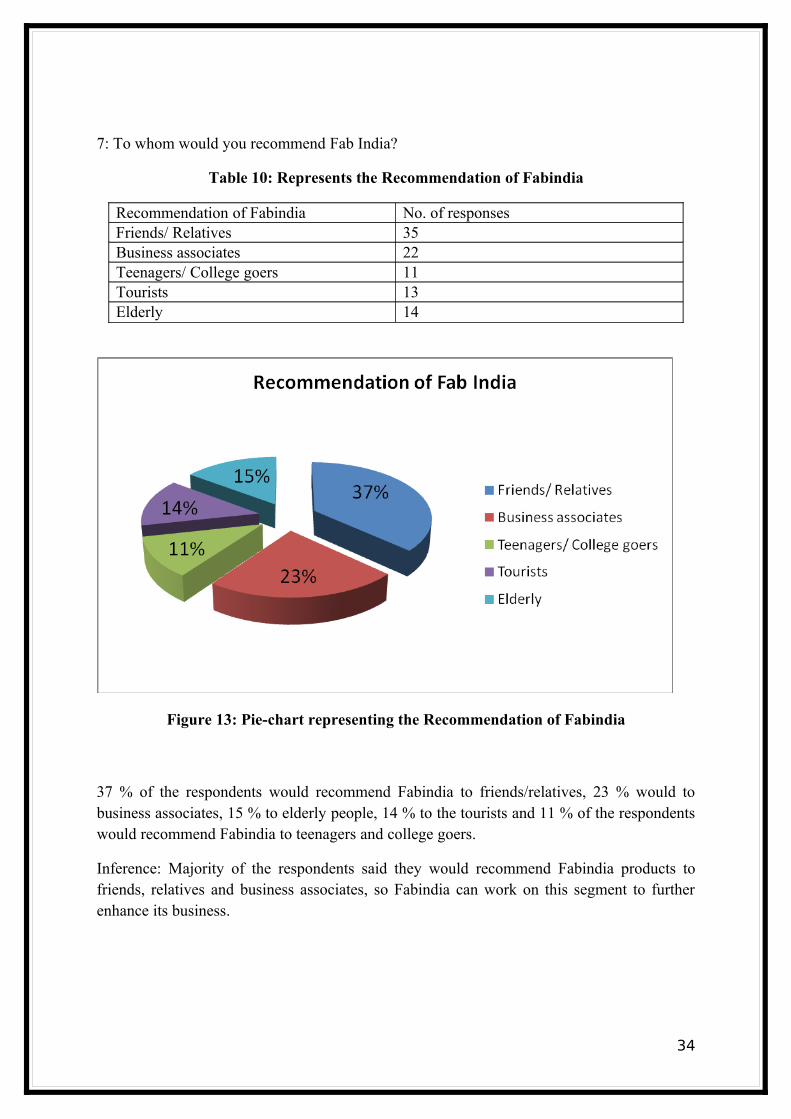

7: To whom would you recommend Fab India?

Table 10: Represents the Recommendation of Fabindia

Recommendation of Fabindia No. of responsesFriends/ Relatives 35Business associates 22Teenagers/ College goers 11Tourists 13Elderly 14

Figure 13: Pie-chart representing the Recommendation of Fabindia

37 % of the respondents would recommend Fabindia to friends/relatives, 23 % would to business associates, 15 % to elderly people, 14 % to the tourists and 11 % of the respondents would recommend Fabindia to teenagers and college goers.

Inference: Majority of the respondents said they would recommend Fabindia products to friends, relatives and business associates, so Fabindia can work on this segment to further enhance its business.

34

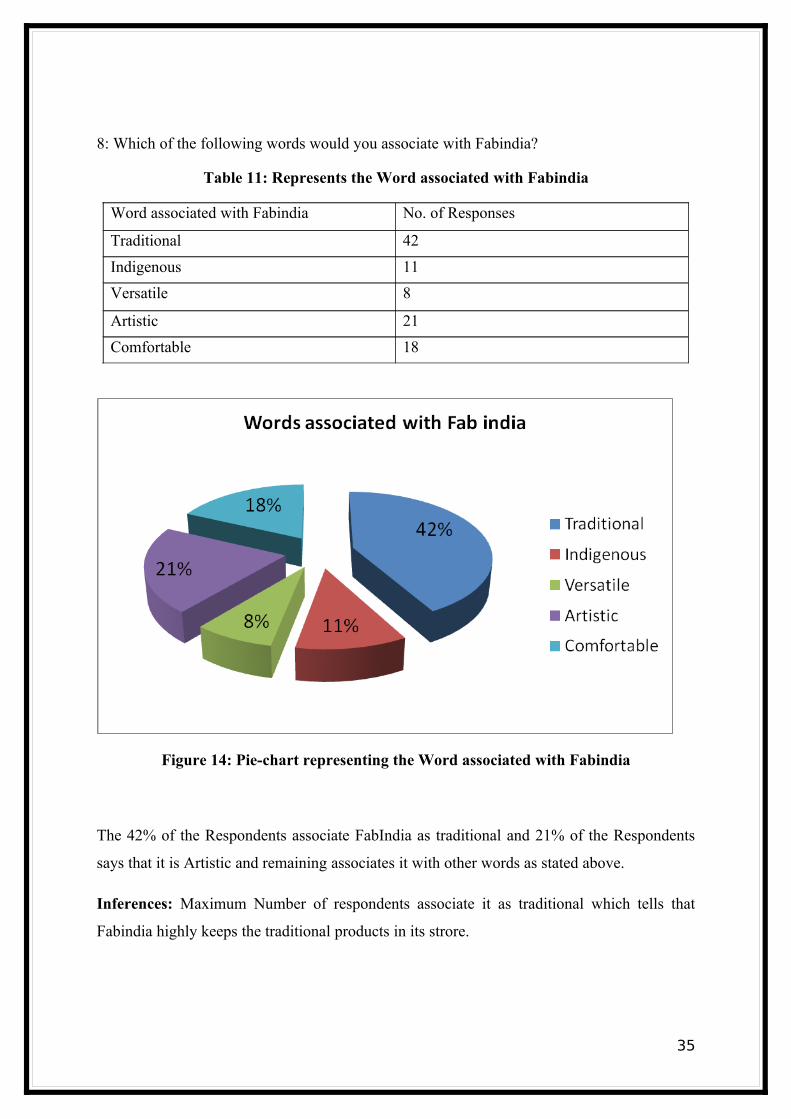

8: Which of the following words would you associate with Fabindia?

Table 11: Represents the Word associated with Fabindia

Word associated with Fabindia No. of Responses

Traditional 42

Indigenous 11

Versatile 8

Artistic 21

Comfortable 18

Figure 14: Pie-chart representing the Word associated with Fabindia

The 42% of the Respondents associate FabIndia as traditional and 21% of the Respondents

says that it is Artistic and remaining associates it with other words as stated above.

Inferences: Maximum Number of respondents associate it as traditional which tells that

Fabindia highly keeps the traditional products in its strore.

35

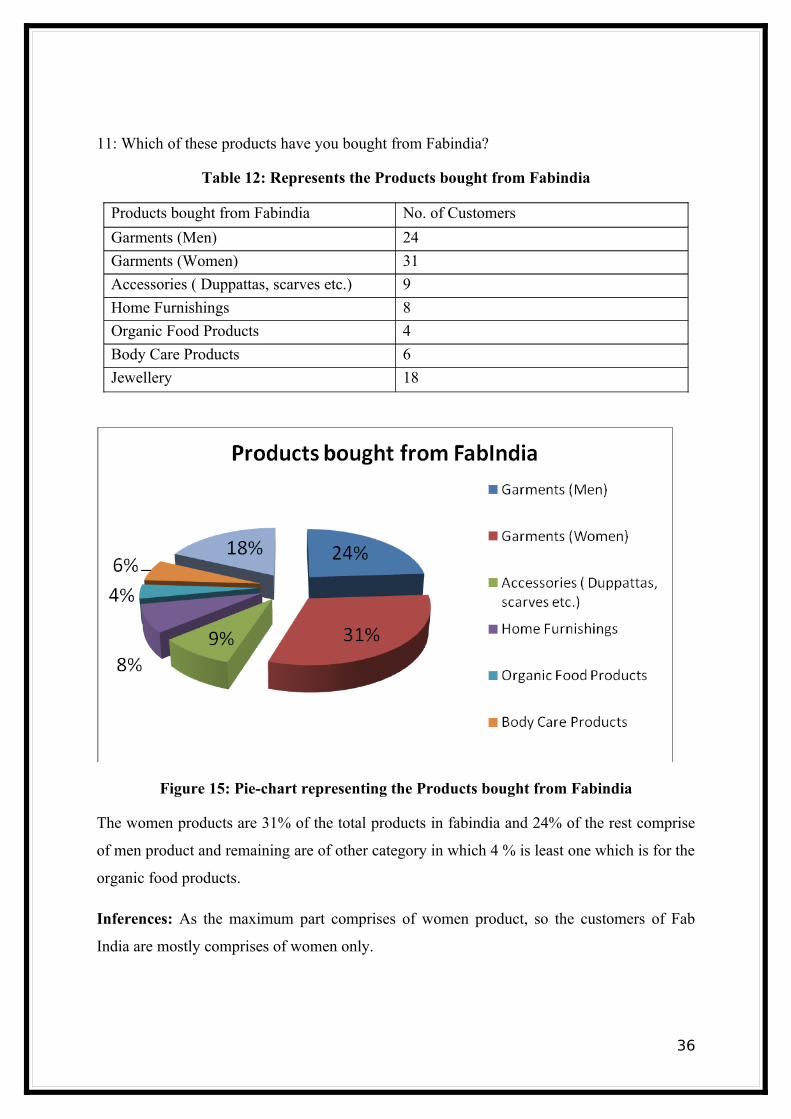

11: Which of these products have you bought from Fabindia?

Table 12: Represents the Products bought from Fabindia

Products bought from Fabindia No. of Customers

Garments (Men) 24

Garments (Women) 31

Accessories ( Duppattas, scarves etc.) 9

Home Furnishings 8

Organic Food Products 4

Body Care Products 6

Jewellery 18

Figure 15: Pie-chart representing the Products bought from Fabindia

The women products are 31% of the total products in fabindia and 24% of the rest comprise

of men product and remaining are of other category in which 4 % is least one which is for the

organic food products.

Inferences: As the maximum part comprises of women product, so the customers of Fab

India are mostly comprises of women only.

36

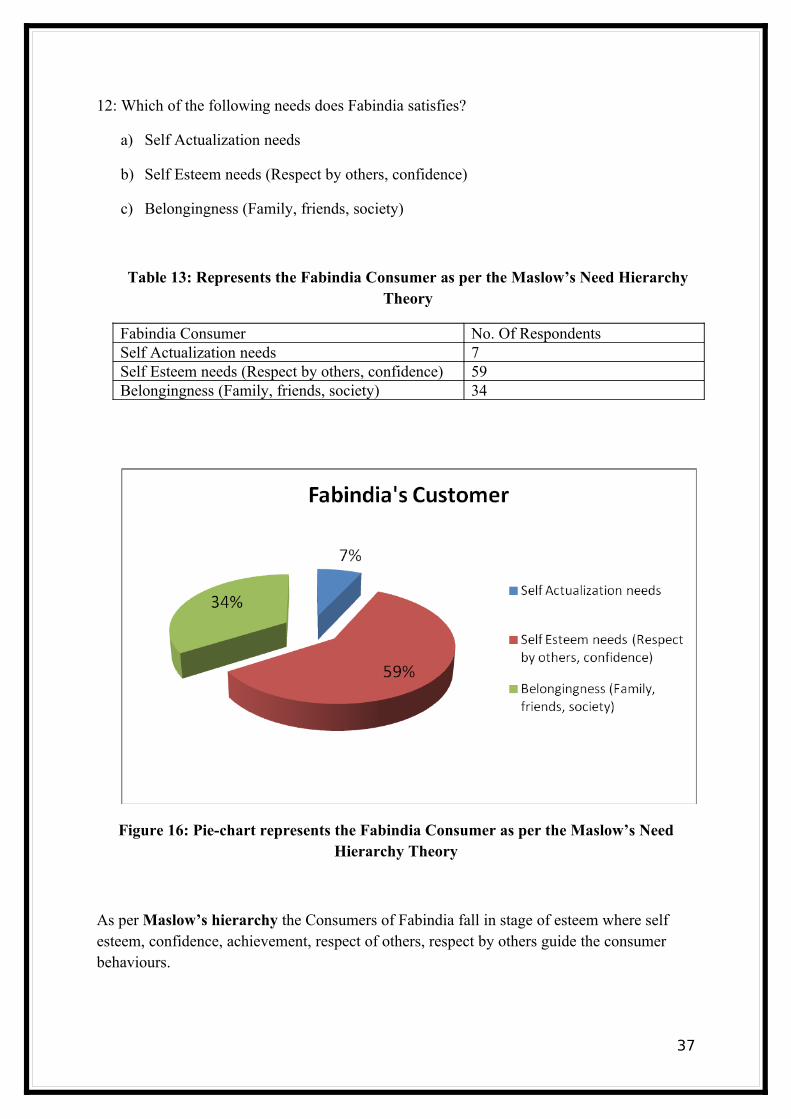

12: Which of the following needs does Fabindia satisfies?

a) Self Actualization needs

b) Self Esteem needs (Respect by others, confidence)

c) Belongingness (Family, friends, society)

Table 13: Represents the Fabindia Consumer as per the Maslow’s Need Hierarchy Theory

Fabindia Consumer No. Of RespondentsSelf Actualization needs 7Self Esteem needs (Respect by others, confidence) 59Belongingness (Family, friends, society) 34

Figure 16: Pie-chart represents the Fabindia Consumer as per the Maslow’s Need Hierarchy Theory

As per Maslow’s hierarchy the Consumers of Fabindia fall in stage of esteem where self esteem, confidence, achievement, respect of others, respect by others guide the consumer behaviours.

37

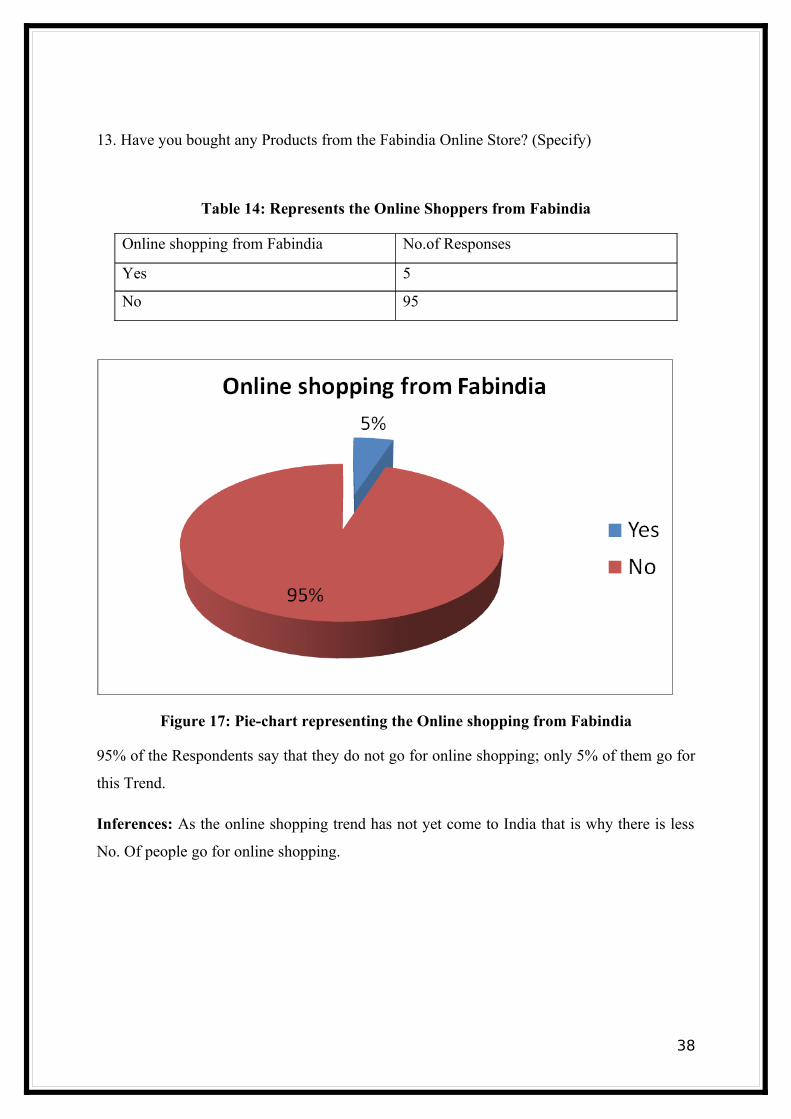

13. Have you bought any Products from the Fabindia Online Store? (Specify)

Table 14: Represents the Online Shoppers from Fabindia

Online shopping from Fabindia No.of Responses

Yes 5

No 95

Figure 17: Pie-chart representing the Online shopping from Fabindia

95% of the Respondents say that they do not go for online shopping; only 5% of them go for

this Trend.

Inferences: As the online shopping trend has not yet come to India that is why there is less

No. Of people go for online shopping.

38

Interview of Fabindia Store Manager

39

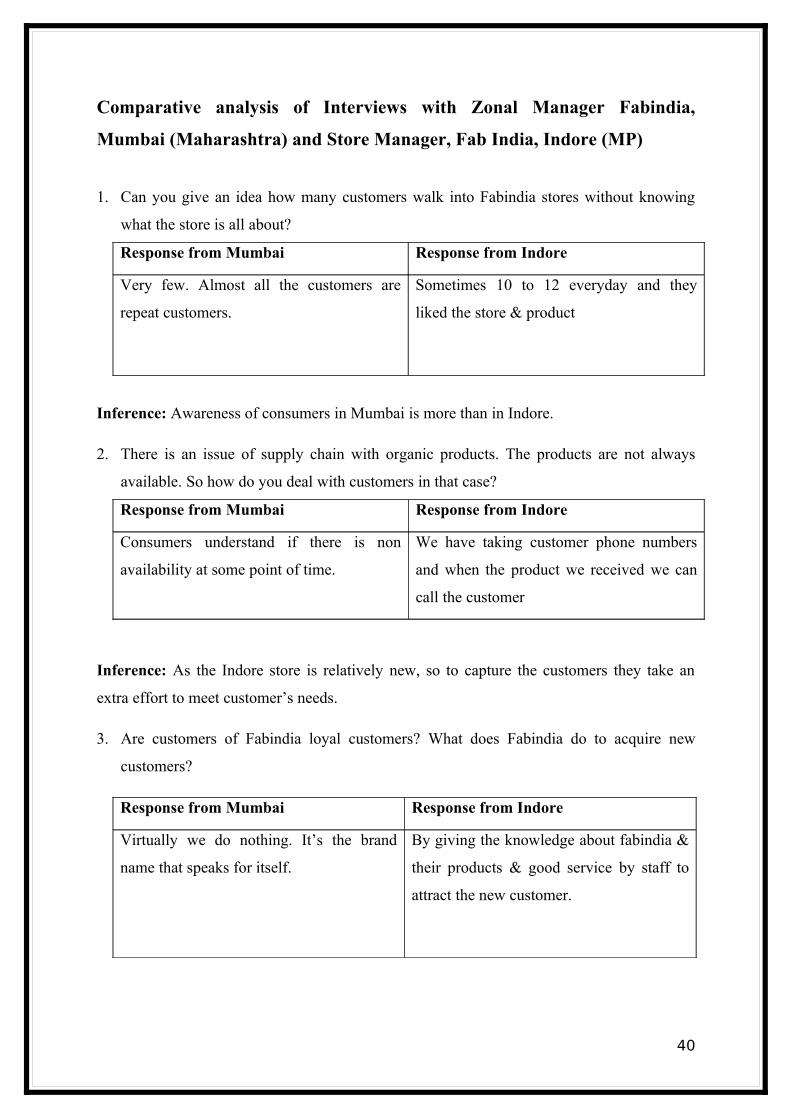

Comparative analysis of Interviews with Zonal Manager Fabindia,

Mumbai (Maharashtra) and Store Manager, Fab India, Indore (MP)

1. Can you give an idea how many customers walk into Fabindia stores without knowing

what the store is all about?

Response from Mumbai Response from Indore

Very few. Almost all the customers are

repeat customers.

Sometimes 10 to 12 everyday and they

liked the store & product

Inference: Awareness of consumers in Mumbai is more than in Indore.

2. There is an issue of supply chain with organic products. The products are not always

available. So how do you deal with customers in that case?

Response from Mumbai Response from Indore

Consumers understand if there is non

availability at some point of time.

We have taking customer phone numbers

and when the product we received we can

call the customer

Inference: As the Indore store is relatively new, so to capture the customers they take an

extra effort to meet customer’s needs.

3. Are customers of Fabindia loyal customers? What does Fabindia do to acquire new

customers?

Response from Mumbai Response from Indore

Virtually we do nothing. It’s the brand

name that speaks for itself.

By giving the knowledge about fabindia &

their products & good service by staff to

attract the new customer.

40

Inference: As discussed above, the Indore store is relatively new, so to attarct the new

customers they take an extra effort.

41

Chapter 9 Conclusion

Recommendations

Since the number of stores has more than doubled in the last four years, it needs to consolidate its position and make sure that the supply chain problems are overcome. Also, as the survey and the interview have pointed out, the visual merchandising of the stores needs to be improved dramatically. In order to increase awareness about the location of the stores, it needs to market itself more aggressively. It also needs to develop the online store and increase awareness about it.

42

Chapter 10

Limitations of the study

1. TIME:We have to submit project within three months as well as we have to do our academic

work, It was not possible to do deep study with in short period of time, so we will be extending our research further in our next semester.

2. MONETARY:

As our study is self funded, we cannot invest too much amount for this project.

3. SAMPLE SIZE & SAMPLING:

4. PLACE CONSTRAINT:

43

Annexures

Questionnaire

QUESTIONNAIRE FOR CONSUMERS

LOCATION:

SEX:

AGE:

CURRENTLY WORKING AS:

QUESTIONS:

1: How much do you generally spend on Clothes per month?

- 0-500

- 501-1000

- 1000-2000

- >2000

2: How much do you generally spend on Home Furniture and Furnishings per year?

- 0-5000

- 5000-10000

- 10000-15000

- >15000

3: Have you heard about Fabindia

If yes, how did you find out about Fabindia?

- Internet

- SMS

- Print Ads

44

- Word of Mouth

- Gift certificates

4: Rate your experience at Fabindia in terms of your satisfaction level for the following:

Highly Satisfactory Satisfactory Average

Unsatisfactory Highly Unsatisfactory

Service

Range of

products

available

Visual Merchandise of the Store

Quality of

Products

5: To whom would you recommend Fabindia ?

(Tick whichever is appropriate)

- Friends/ Relatives

- Business associates

- Teenagers/ College goers

- NRIs/ Tourists

- Elderly

6: Which of the following do you think was instrumental in your choosing to buy the products?

Rank them on scale of 1 to 5 with 1 being the most important.

- Traditional work

- Support to poor artisans

45

- Quality of the product

- Price

- Range of products available

- Convenient Location of the store

- Service provided by the staff

- The ‘Fabindia’ Brand

7: Which of the following words would you associate with Fabindia?

- Traditional

- Indigenous

- Versatile

- Artistic

- Comfortable

8: Which of these products would you buy from Fabindia?

- Garments (Men)

- Garments (Women)

- Accessories ( Duppattas, scarves etc.)

- Home Furnishings

- Organic Food Products

- Body Care Products

- Jewellery

9: Have you bought any Products from the Fabindia Online Store? (Specify)

- Yes _______________________________________________________________

46

- No________________________________________________________________

47

Appendices

Annexure

Bibliography

48

![[PPT]Consumer Behavior and Marketing Strategy - Lars … to CB.ppt · Web viewIntro to Consumer Behavior Consumer behavior--what is it? Applications Consumer Behavior and Strategy](https://img.pdfslide.net/doc/110x75/5af357b67f8b9a74448b60fb/pptconsumer-behavior-and-marketing-strategy-lars-to-cbpptweb-viewintro.jpg)