Embed Size (px)

Citation preview

Consumers are Ready for the Digital Revolution, Are You?

Eric Leiserson, Sr. Research Analyst, Fiserv

© 2011 Fiserv, Inc. or its affiliates.

Agenda

2

• Why 2012 Will Be An Incredible Year in Payments

• Significant Findings in Changes in Consumer Bill Payment and Impacts

• Mobile and Tablets – how will they are used now and in the future

• Ways to market ebills and Person to Person Payments

• Conclusion

© 2011 Fiserv, Inc. or its affiliates.

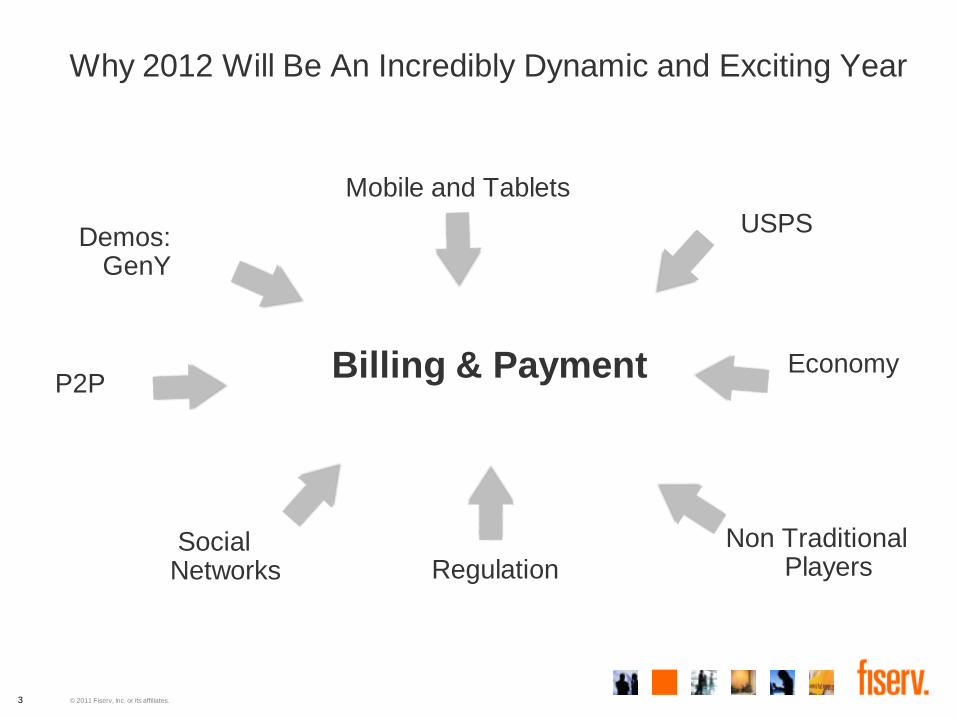

Why 2012 Will Be An Incredibly Dynamic and Exciting Year

Billing & Payment

3

Regulation

USPS

Non Traditional Players

Social Networks

Mobile and Tablets

Demos: GenY

P2P Economy

© 2011 Fiserv, Inc. or its affiliates.

What’s At Stake?

Meeting Demand and Expectations

Customer Engagement

Retention

Customer Satisfaction

Reduction of Costs

Online Self-Care

Brand Perception

Share of Wallet

Profit

4

© 2009 Fiserv, Inc. or its affiliates.

Overview of the 11th Annual Consumer Survey Program

Fiserv sponsored two consumer surveys:

• Consumer Trends Survey

• Completed by 3,000 respondents representative of 96.4M households using the internet among 121M U.S. households (Forrester, 2010)

• The margin of error is +/-1.7% for %s based on 3000 respondents

• Billing Household Survey

• Completed by 2,500 respondents representative of 96.4M households using the internet among 121M U.S. households (Forrester, 2010)

• The margin of error is +/-2% for %s based on 2500 respondents

• Surveys designed to provide current view of the consumer billing and payment marketplace

• Results compared to similar surveys sponsored by Fiserv to capture ongoing and emerging trends

• Marketing Workshop managed this survey and previous surveys to maintain continuity

5

© 2011 Fiserv, Inc. or its affiliates.

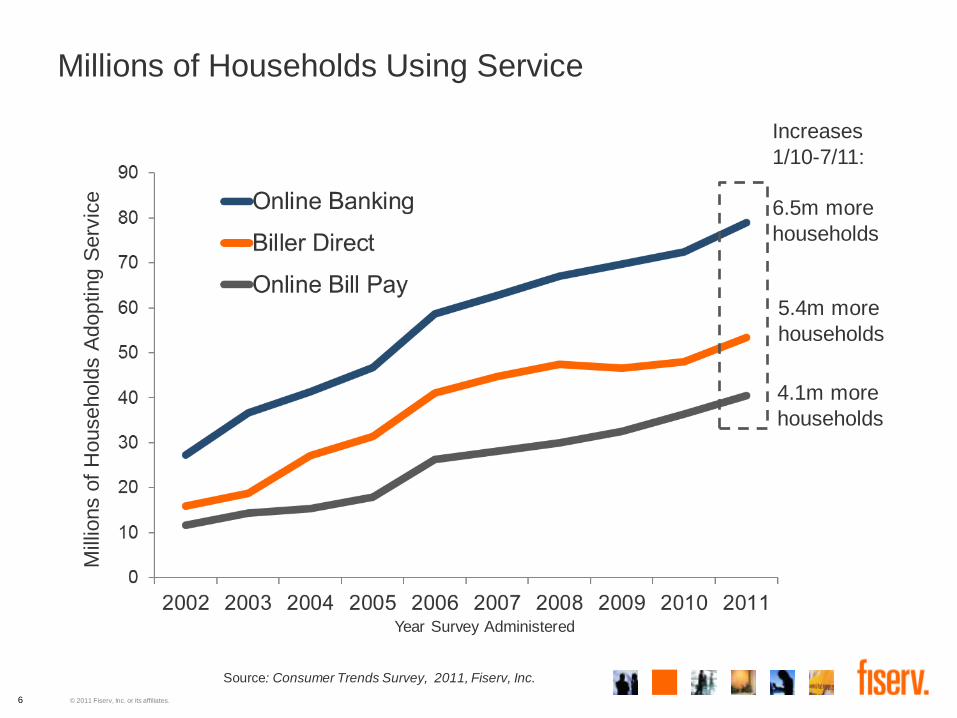

Millions of Households Using Service

6

Mill

ions o

f H

ousehold

s A

dop

ting

Serv

ice

Year Survey Administered

Increases

1/10-7/11:

6.5m more

households

4.1m more

households

5.4m more

households

Source: Consumer Trends Survey, 2011, Fiserv, Inc.

© 2011 Fiserv, Inc. or its affiliates.

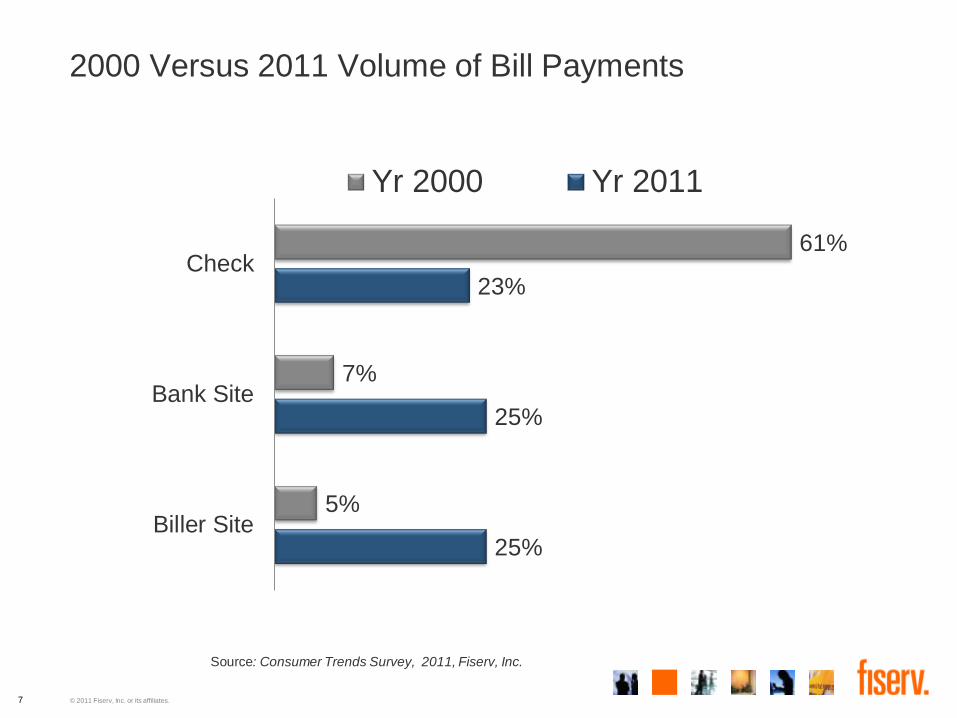

2000 Versus 2011 Volume of Bill Payments

7

25%

25%

23%

5%

7%

61%

Biller Site

Bank Site

Check

Yr 2000 Yr 2011

Source: Consumer Trends Survey, 2011, Fiserv, Inc.

© 2009 Fiserv, Inc. or its affiliates.

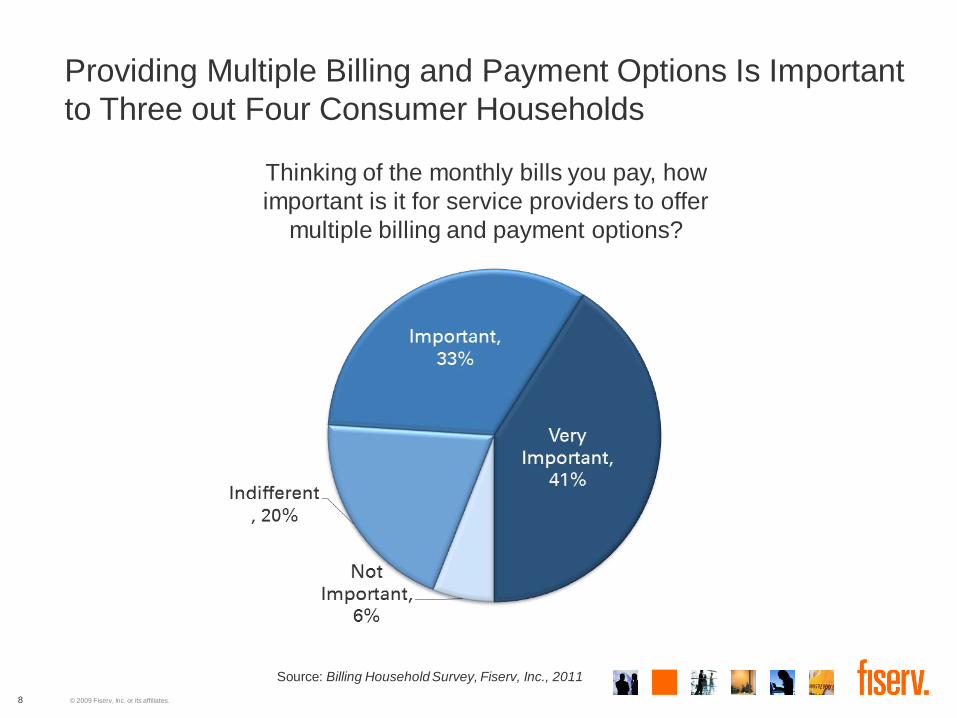

Providing Multiple Billing and Payment Options Is Important

to Three out Four Consumer Households

Thinking of the monthly bills you pay, how

important is it for service providers to offer

multiple billing and payment options?

8

Source: Billing Household Survey, Fiserv, Inc., 2011

© 2009 Fiserv, Inc. or its affiliates. 9

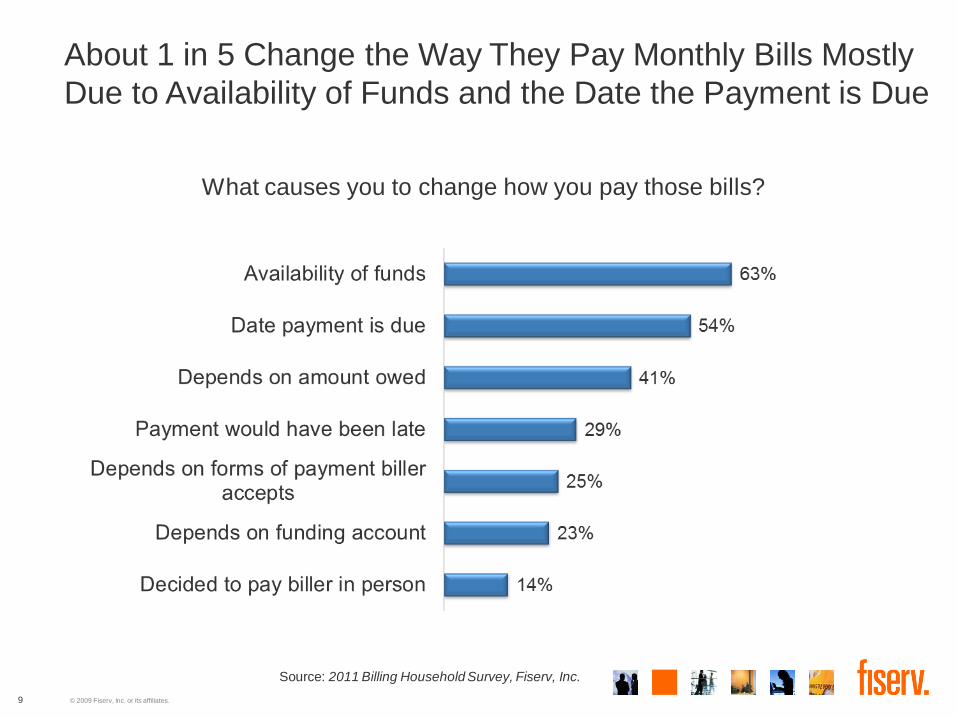

About 1 in 5 Change the Way They Pay Monthly Bills Mostly

Due to Availability of Funds and the Date the Payment is Due

What causes you to change how you pay those bills?

Source: 2011 Billing Household Survey, Fiserv, Inc.

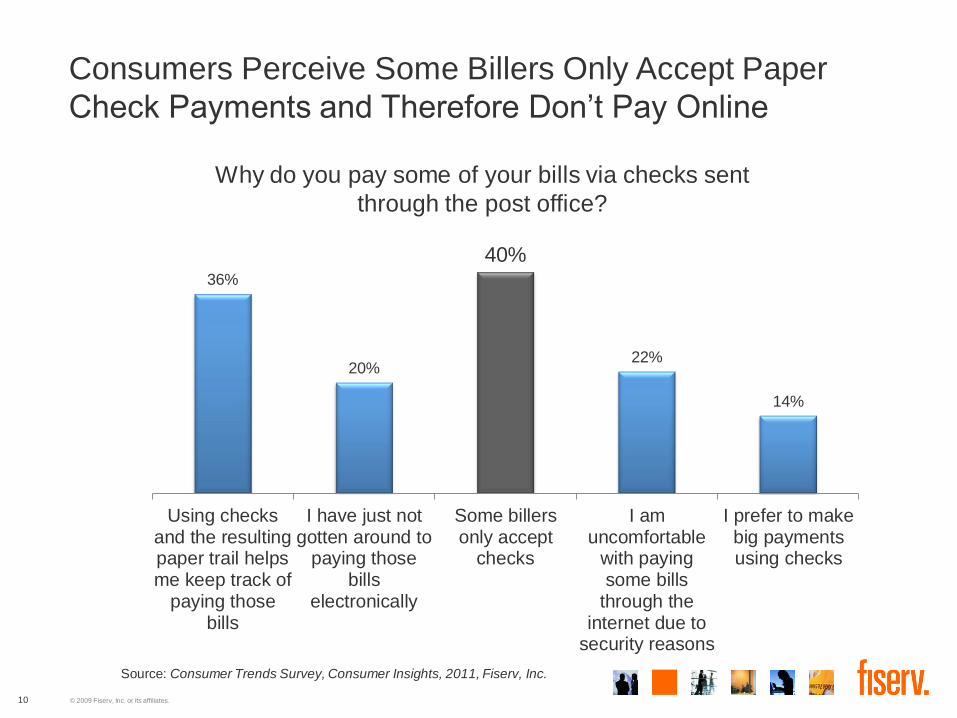

© 2009 Fiserv, Inc. or its affiliates. 10

Why do you pay some of your bills via checks sent

through the post office?

36%

20%

40%

22%

14%

Using checksand the resultingpaper trail helpsme keep track of

paying thosebills

I have just notgotten around to

paying thosebills

electronically

Some billersonly accept

checks

I amuncomfortable

with payingsome bills

through theinternet due to

security reasons

I prefer to makebig paymentsusing checks

Consumers Perceive Some Billers Only Accept Paper

Check Payments and Therefore Don’t Pay Online

Source: Consumer Trends Survey, Consumer Insights, 2011, Fiserv, Inc.

© 2009 Fiserv, Inc. or its affiliates. 11

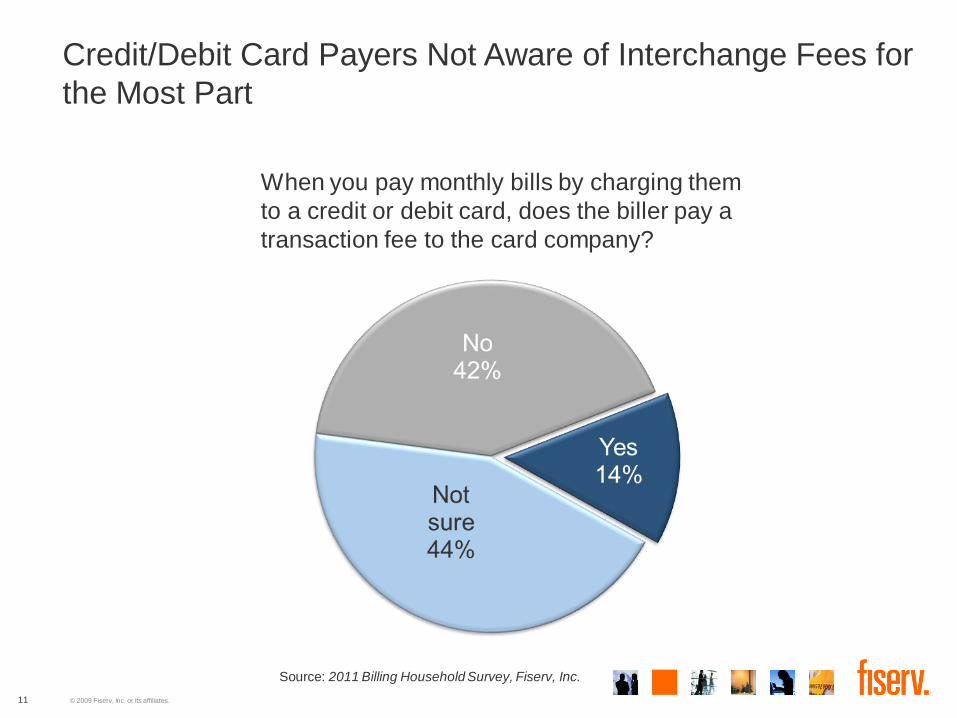

Credit/Debit Card Payers Not Aware of Interchange Fees for

the Most Part

When you pay monthly bills by charging them

to a credit or debit card, does the biller pay a

transaction fee to the card company?

Source: 2011 Billing Household Survey, Fiserv, Inc.

© 2009 Fiserv, Inc. or its affiliates.

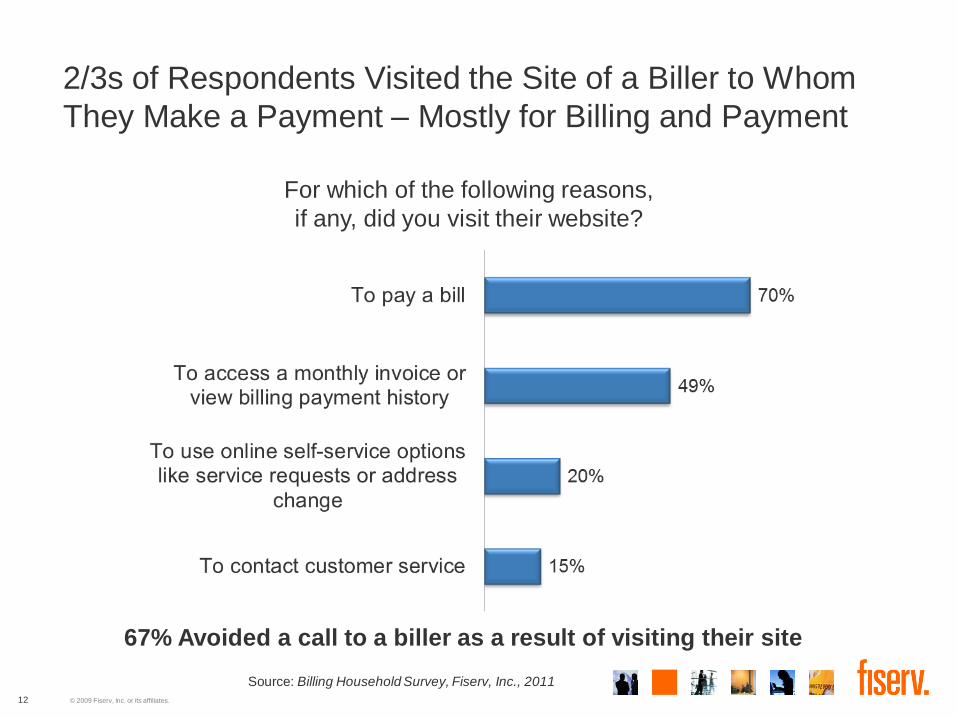

2/3s of Respondents Visited the Site of a Biller to Whom

They Make a Payment – Mostly for Billing and Payment

For which of the following reasons,

if any, did you visit their website?

12

67% Avoided a call to a biller as a result of visiting their site

Source: Billing Household Survey, Fiserv, Inc., 2011

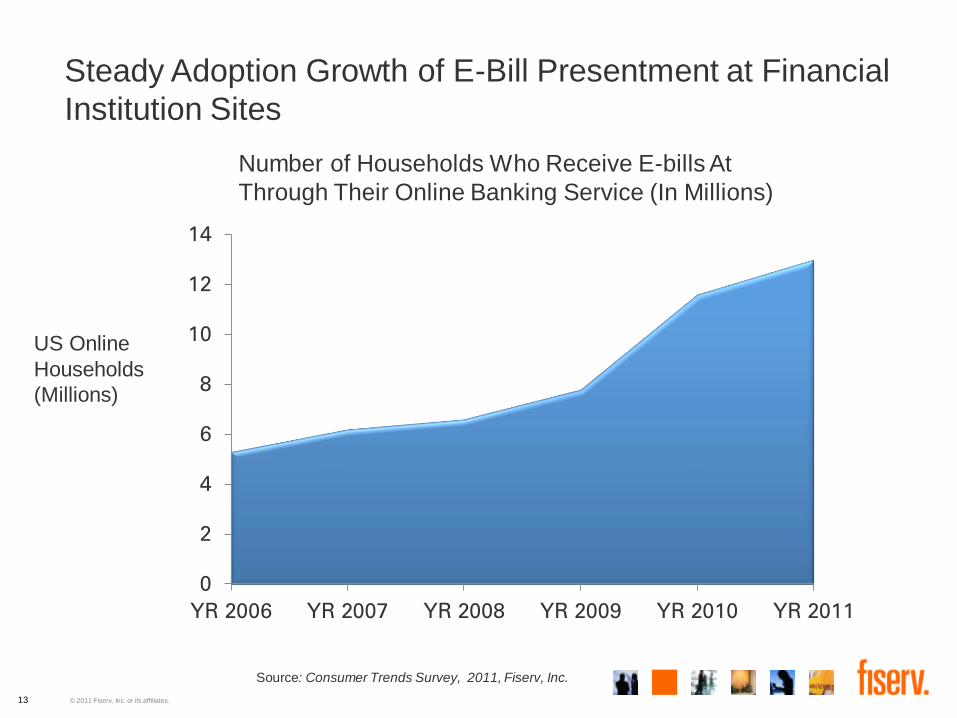

© 2011 Fiserv, Inc. or its affiliates. 13

Steady Adoption Growth of E-Bill Presentment at Financial

Institution Sites

0

2

4

6

8

10

12

14

YR 2006 YR 2007 YR 2008 YR 2009 YR 2010 YR 2011

US Online

Households

(Millions)

Number of Households Who Receive E-bills At

Through Their Online Banking Service (In Millions)

Source: Consumer Trends Survey, 2011, Fiserv, Inc.

© 2011 Fiserv, Inc. or its affiliates.

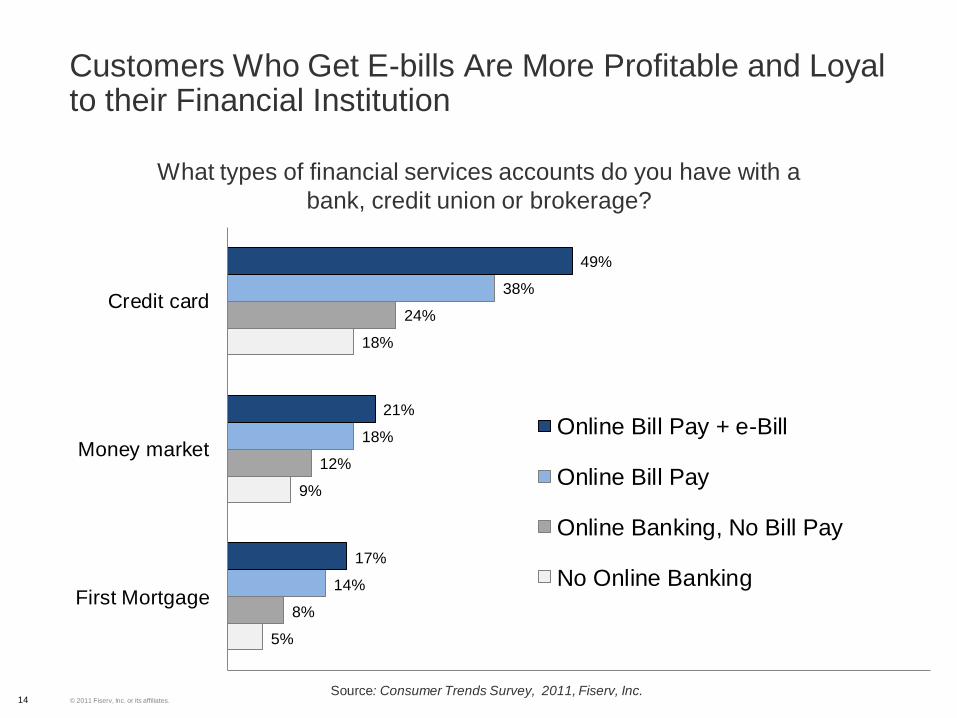

Customers Who Get E-bills Are More Profitable and Loyal to their Financial Institution

14

5%

9%

18%

8%

12%

24%

14%

18%

38%

17%

21%

49%

First Mortgage

Money market

Credit card

Online Bill Pay + e-Bill

Online Bill Pay

Online Banking, No Bill Pay

No Online Banking

Source: Consumer Trends Survey, 2011, Fiserv, Inc.

What types of financial services accounts do you have with a

bank, credit union or brokerage?

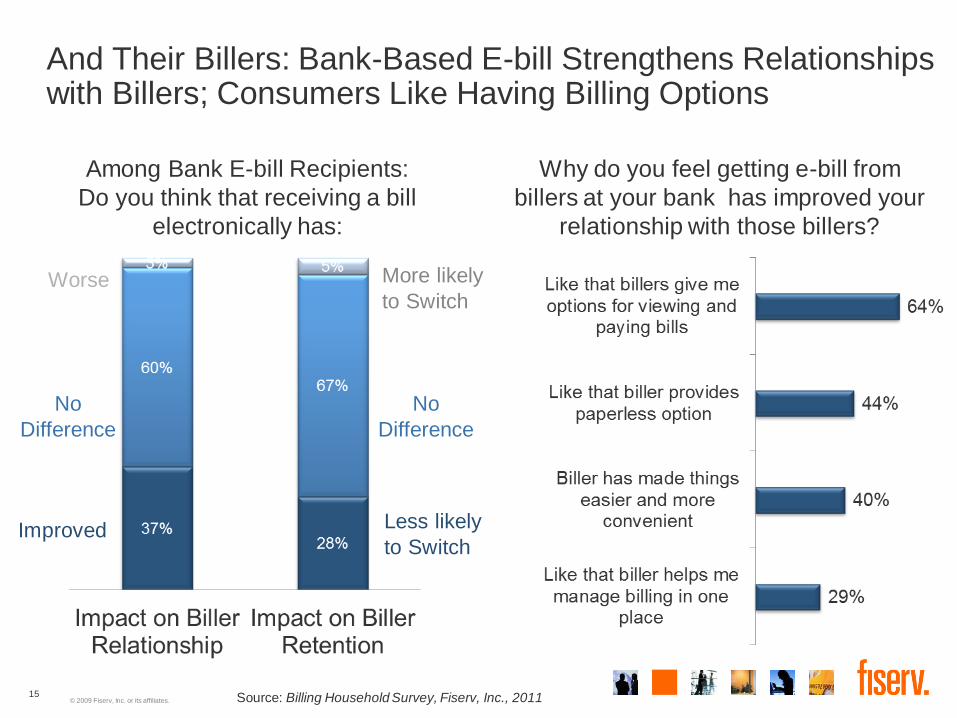

© 2009 Fiserv, Inc. or its affiliates. 15

No

Difference

Among Bank E-bill Recipients:

Do you think that receiving a bill

electronically has:

Why do you feel getting e-bill from

billers at your bank has improved your

relationship with those billers?

Source: Billing Household Survey, Fiserv, Inc., 2011

And Their Billers: Bank-Based E-bill Strengthens Relationships with Billers; Consumers Like Having Billing Options

Improved

Worse More likely

to Switch

No

Difference

Less likely

to Switch

© 2011 Fiserv, Inc. or its affiliates.

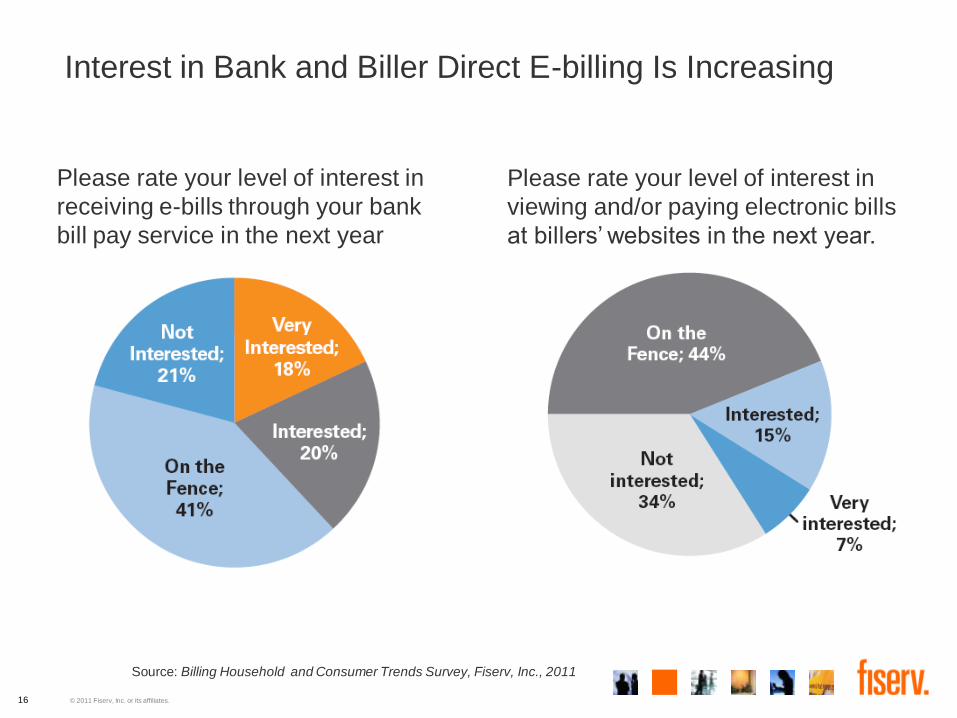

Interest in Bank and Biller Direct E-billing Is Increasing

16

Source: Billing Household and Consumer Trends Survey, Fiserv, Inc., 2011

Please rate your level of interest in

viewing and/or paying electronic bills

at billers’ websites in the next year.

Please rate your level of interest in

receiving e-bills through your bank

bill pay service in the next year

© 2011 Fiserv, Inc. or its affiliates.

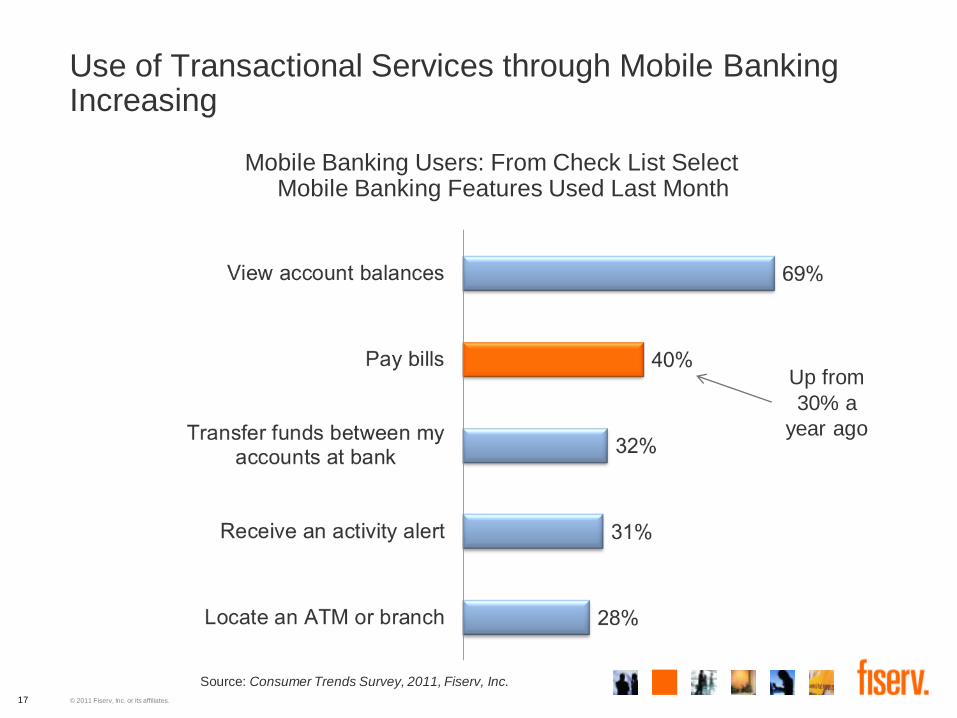

Use of Transactional Services through Mobile Banking Increasing

17

Mobile Banking Users: From Check List Select Mobile Banking Features Used Last Month

Up from

30% a

year ago

Source: Consumer Trends Survey, 2011, Fiserv, Inc.

© 2011 Fiserv, Inc. or its affiliates. 18

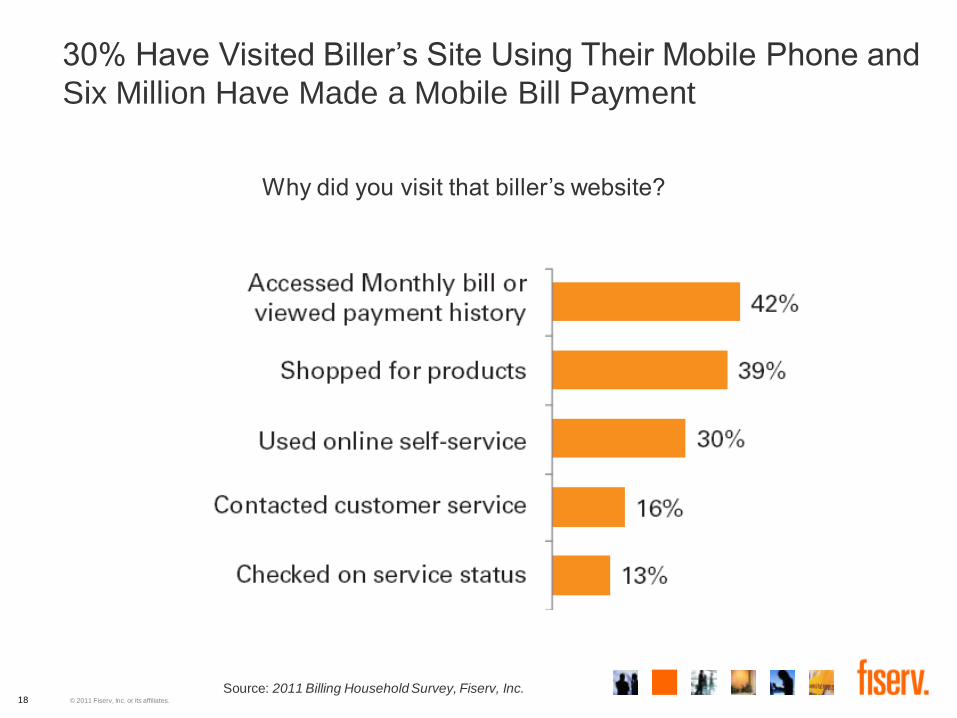

30% Have Visited Biller’s Site Using Their Mobile Phone and

Six Million Have Made a Mobile Bill Payment

Source: 2011 Billing Household Survey, Fiserv, Inc.

Why did you visit that biller’s website?

© 2011 Fiserv, Inc. or its affiliates. 19

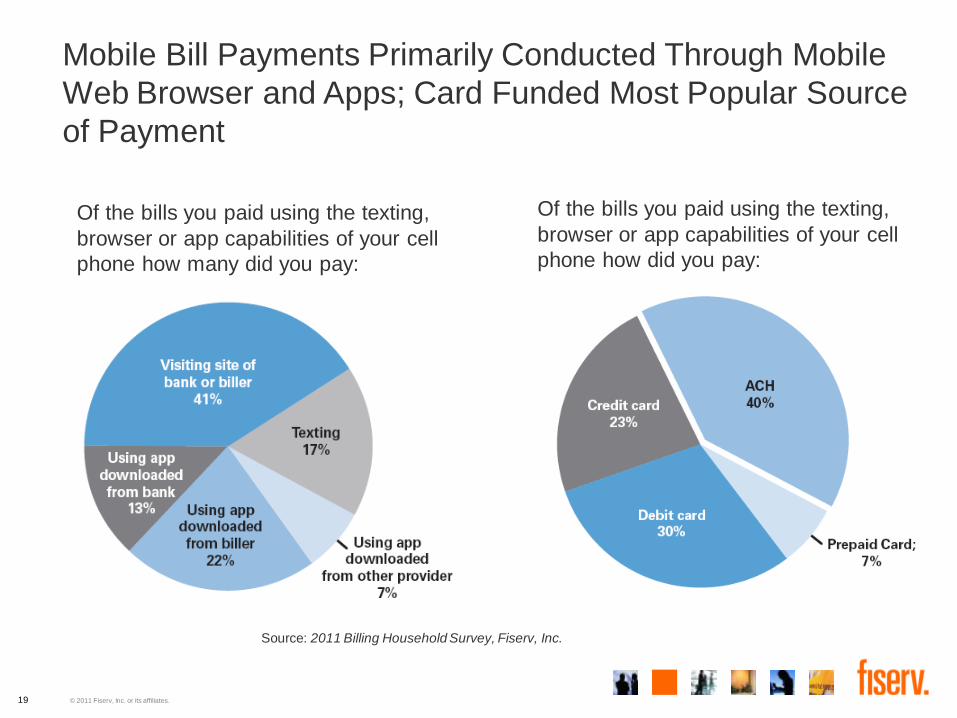

Of the bills you paid using the texting,

browser or app capabilities of your cell

phone how many did you pay:

Mobile Bill Payments Primarily Conducted Through Mobile

Web Browser and Apps; Card Funded Most Popular Source

of Payment

Of the bills you paid using the texting,

browser or app capabilities of your cell

phone how did you pay:

Source: 2011 Billing Household Survey, Fiserv, Inc.

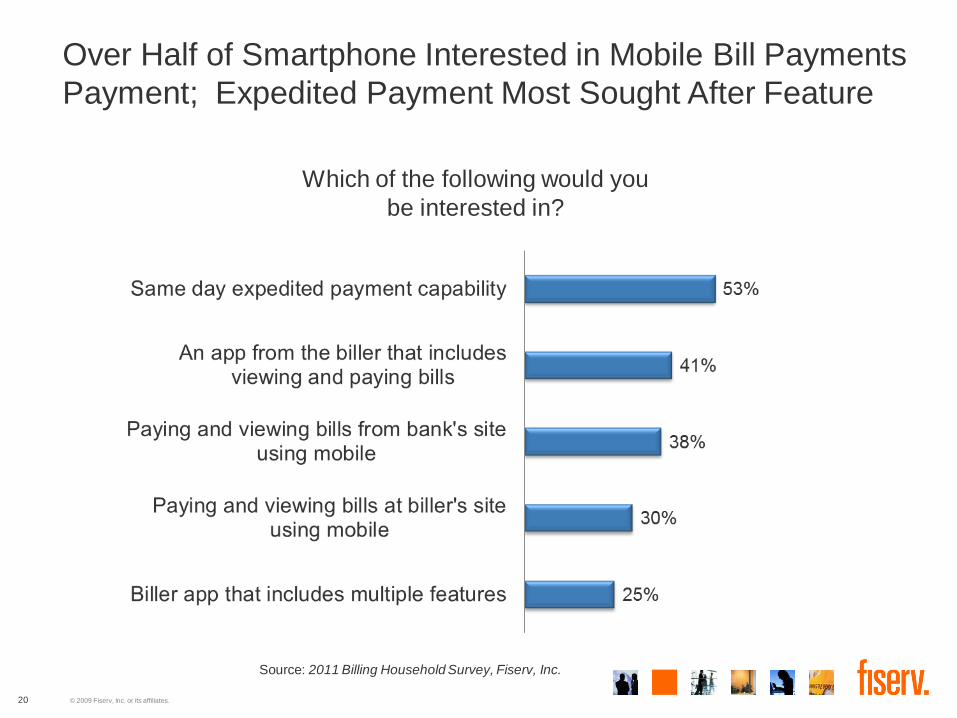

© 2009 Fiserv, Inc. or its affiliates. 20

Which of the following would you

be interested in?

Source: 2011 Billing Household Survey, Fiserv, Inc.

Over Half of Smartphone Interested in Mobile Bill Payments

Payment; Expedited Payment Most Sought After Feature

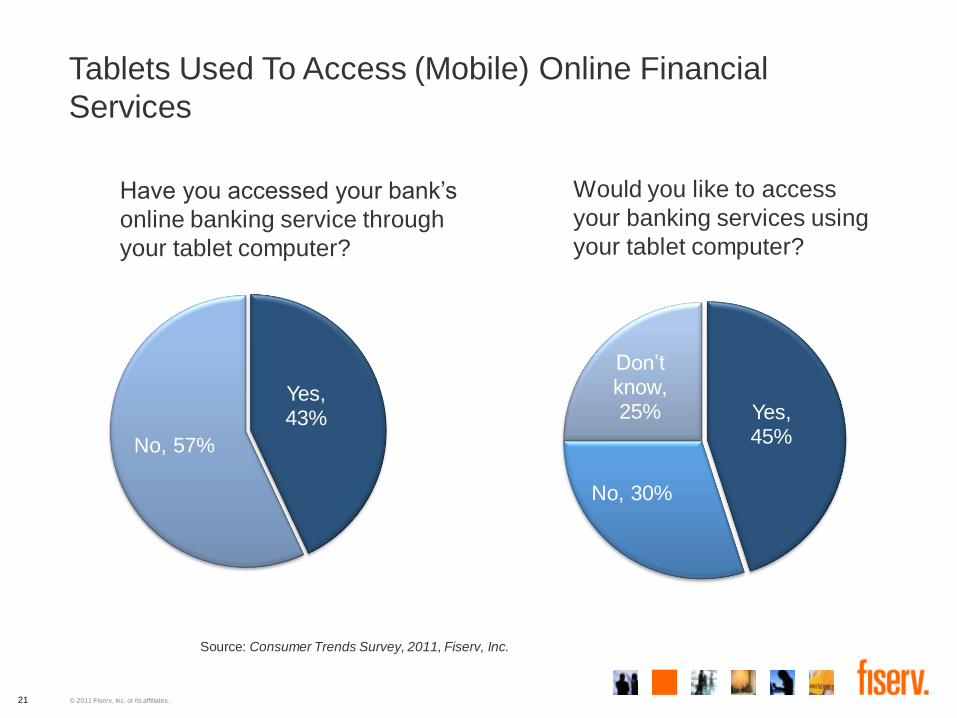

© 2011 Fiserv, Inc. or its affiliates. 21

Yes, 43%

No, 57%

Have you accessed your bank’s

online banking service through

your tablet computer?

Tablets Used To Access (Mobile) Online Financial

Services

Source: Consumer Trends Survey, 2011, Fiserv, Inc.

Yes, 45%

No, 30%

Don’t know, 25%

Would you like to access

your banking services using

your tablet computer?

© 2011 Fiserv, Inc. or its affiliates.

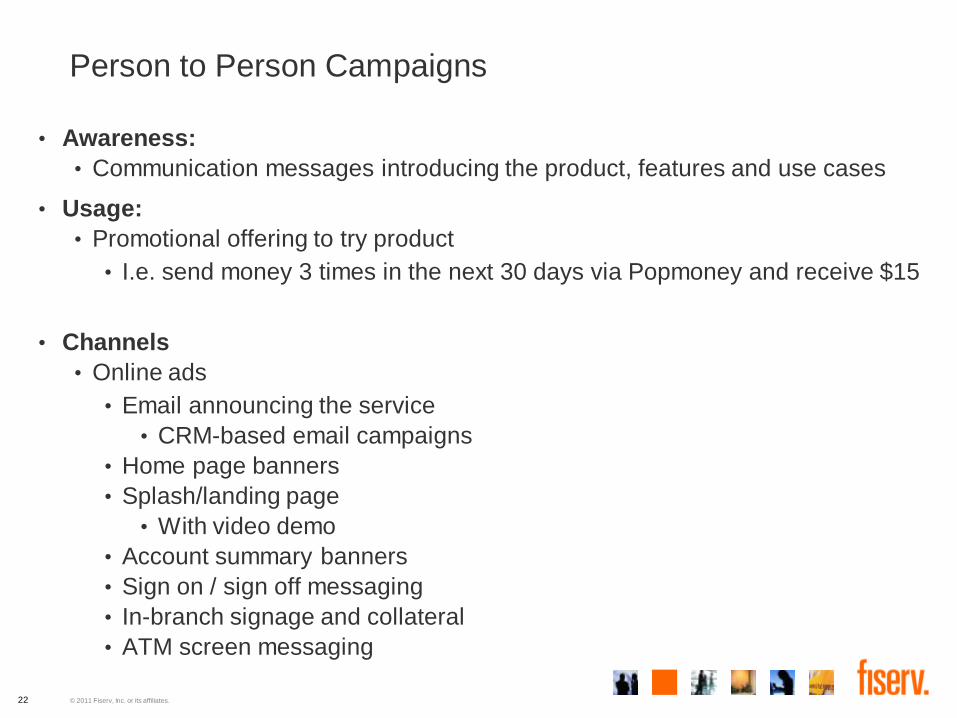

Person to Person Campaigns

• Awareness:

• Communication messages introducing the product, features and use cases

• Usage:

• Promotional offering to try product

• I.e. send money 3 times in the next 30 days via Popmoney and receive $15

• Channels

• Online ads

• Email announcing the service

• CRM-based email campaigns

• Home page banners

• Splash/landing page

• With video demo

• Account summary banners

• Sign on / sign off messaging

• In-branch signage and collateral

• ATM screen messaging

22

© 2011 Fiserv, Inc. or its affiliates.

Using “Tryvertising” to Increase e-Bill Adoption

• Takes product placement to the real world, integrating products into the daily life of consumers so they can make up their minds based on their actual experience with the products.

• It comprises of activities that are a natural fit with consumers.

• When the consumer actually tries the product, their experience is much stronger than just hearing about it or seeing someone else use it in the media.

23

Try-ver-tis-ing: growing trend of experience-based

consumption, or a kind of "test-driving” of products

© 2011 Fiserv, Inc. or its affiliates.

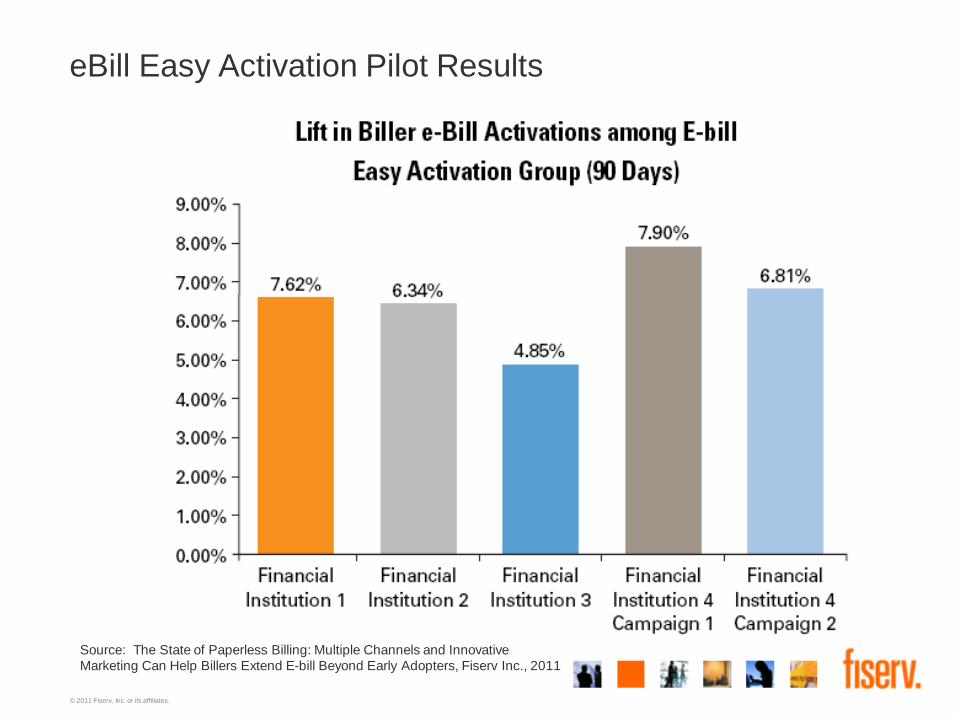

eBill Easy Activation Pilot Results

Source: The State of Paperless Billing: Multiple Channels and Innovative

Marketing Can Help Billers Extend E-bill Beyond Early Adopters, Fiserv Inc., 2011

Consumers are Ready for the Digital Revolution, Are You?

Eric Leiserson, Sr. Research Analyst, Fiserv