Embed Size (px)

Citation preview

Contactless Banking Payment Pilot Contactless Banking Payment Pilot at MTA New York City Transitat MTA New York City Transit

Steve FrazziniSteve FrazziniProgram DirectorProgram Director

Paul KorczakPaul KorczakProject ManagerProject Manager

Card Tech Card Tech SecurTechSecurTechMay 2008May 2008

2

OverviewOverview

Business Strategy and New Payment Model for Transit

Opportunities: why consider an alternative approach?

Phase I Results

Next Steps

3

Potential Business Strategy: Potential Business Strategy: ““MerchantMerchant”” ApproachApproach

Participate as a “merchant” in the banking industry’s move to contactless form factors (cards, cell phones, key fobs, etc.) Layer on a contactless bank device payment “option” for customers at the point of entry (fare gates, bus fare boxes)Coordinate with regional transit partners (PA, NJT, PATH, others) to solve the regional fare payment question: - Adopt a uniform payment approach- “Speak with one voice” as a merchant category

4

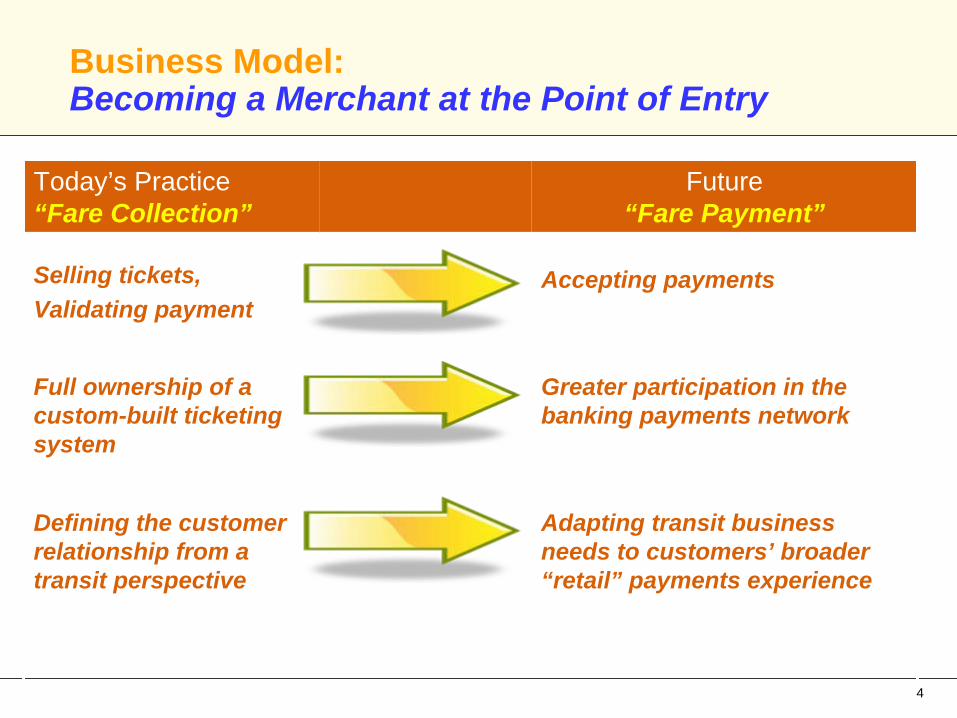

Business Model: Becoming a Merchant at the Point of Entry

Today’s Practice“Fare Collection”

Future“Fare Payment”

Selling tickets,Validating payment

Accepting payments

Full ownership of a custom-built ticketing system

Greater participation in the banking payments network

Defining the customer relationship from a transit perspective

Adapting transit business needs to customers’ broader “retail” payments experience

5

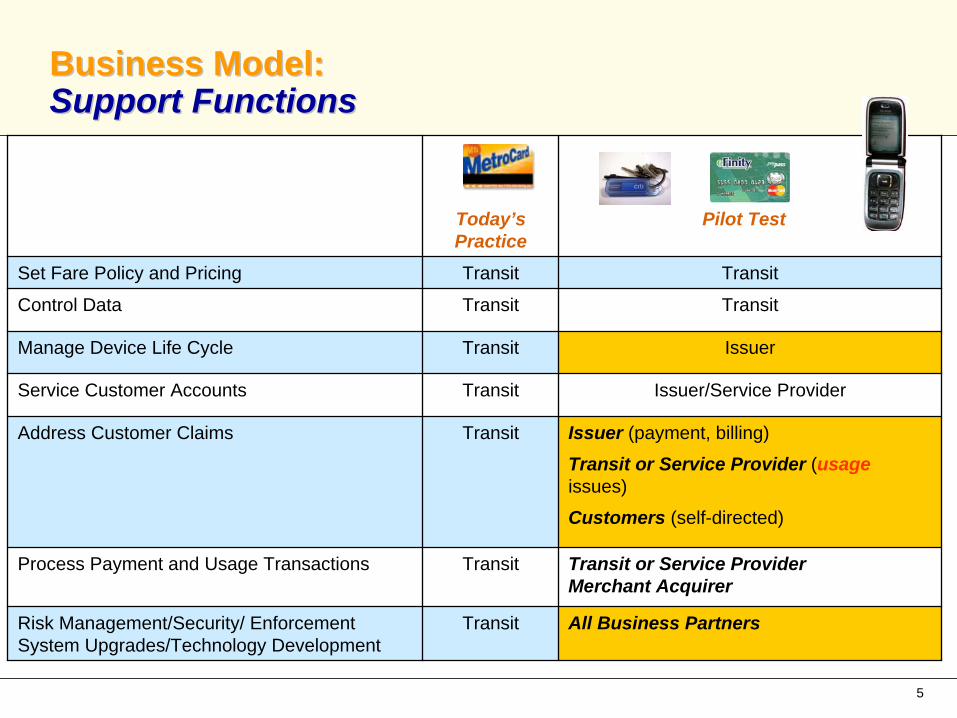

Business Model:Business Model: Support FunctionsSupport Functions

Today’s Practice

Pilot Test

Set Fare Policy and Pricing Transit Transit

Control Data Transit Transit

Manage Device Life Cycle Transit Issuer

Service Customer Accounts Transit Issuer/Service Provider

Address Customer Claims Transit Issuer (payment, billing)

Transit or Service Provider (usage issues)

Customers (self-directed)

Process Payment and Usage Transactions Transit Transit or Service ProviderMerchant Acquirer

Risk Management/Security/ Enforcement System Upgrades/Technology Development

Transit All Business Partners

6

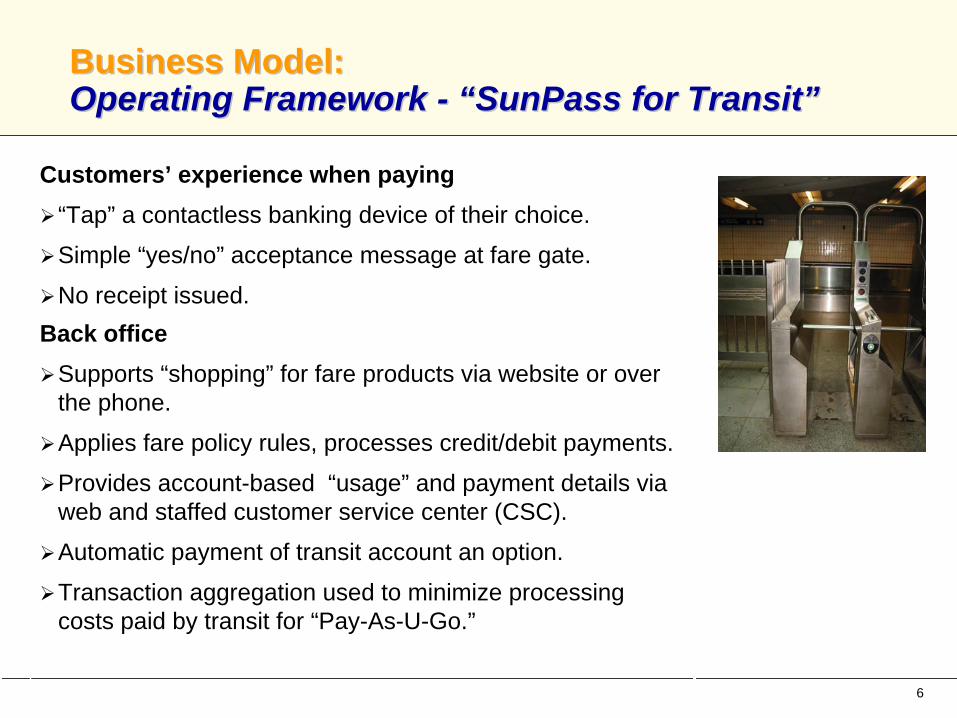

Business Model:Business Model: Operating Framework Operating Framework -- ““SunPassSunPass for Transitfor Transit””

Customers’ experience when paying“Tap” a contactless banking device of their choice.

Simple “yes/no” acceptance message at fare gate.

No receipt issued.Back office

Supports “shopping” for fare products via website or over the phone.

Applies fare policy rules, processes credit/debit payments.

Provides account-based “usage” and payment details via web and staffed customer service center (CSC).

Automatic payment of transit account an option.

Transaction aggregation used to minimize processing costs paid by transit for “Pay-As-U-Go.”

7

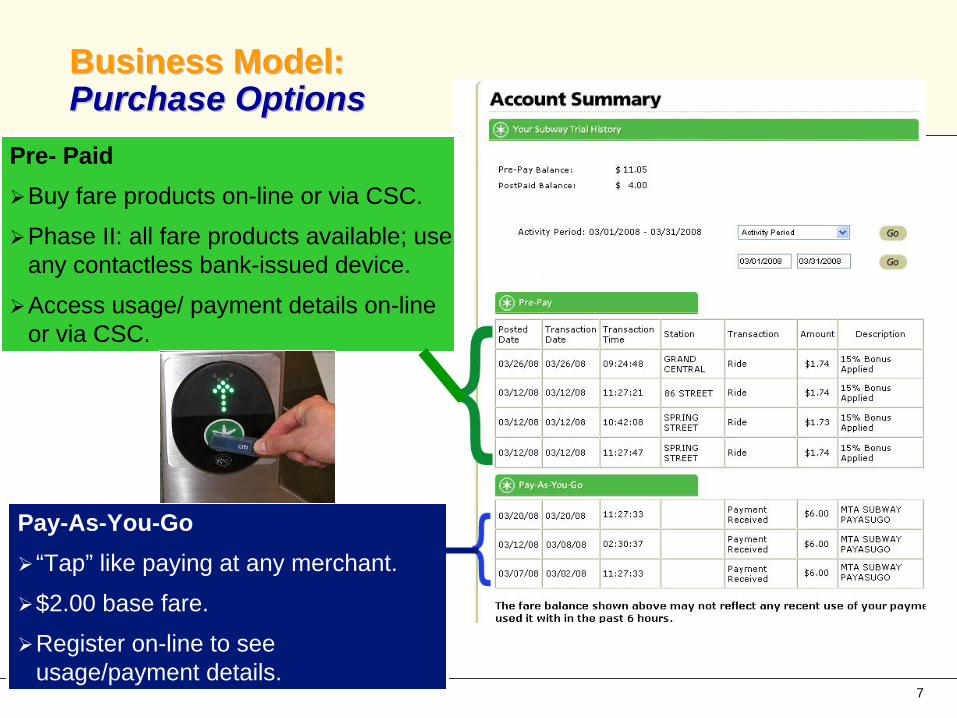

Business Model:Business Model: Purchase OptionsPurchase Options

Pay-As-You-Go“Tap” like paying at any merchant.

$2.00 base fare.

Register on-line to see usage/payment details.

Pre- PaidBuy fare products on-line or via CSC.

Phase II: all fare products available; use any contactless bank-issued device.

Access usage/ payment details on-line or via CSC.

8

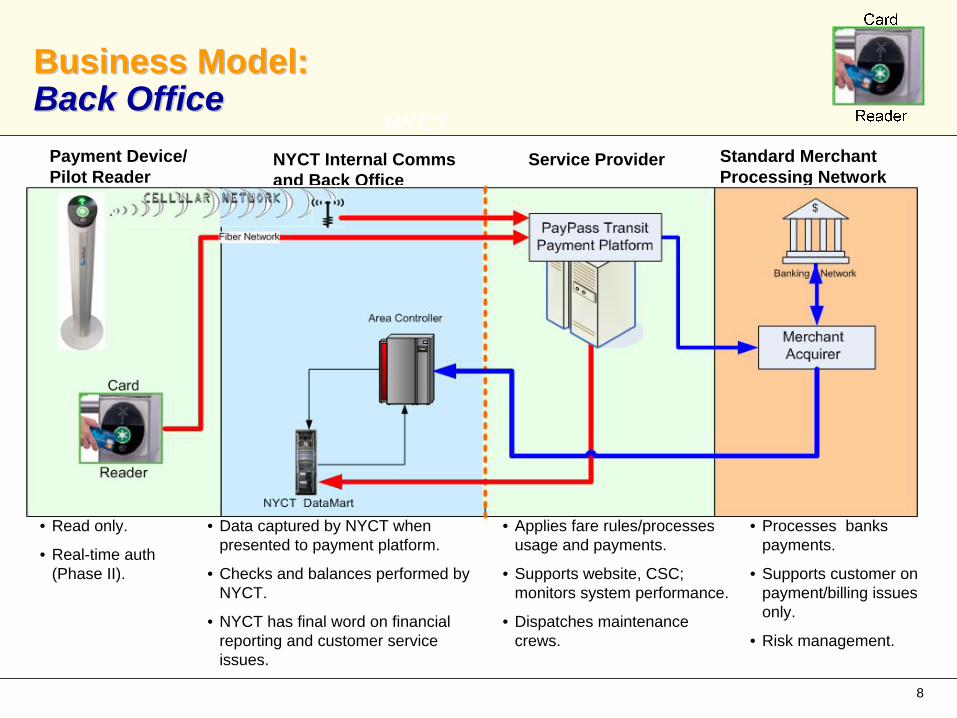

Business Model:Business Model: Back OfficeBack Office

• Data captured by NYCT when presented to payment platform.

• Checks and balances performed by NYCT.

• NYCT has final word on financial reporting and customer service issues.

• Read only.

• Real-time auth (Phase II).

• Applies fare rules/processes usage and payments.

• Supports website, CSC; monitors system performance.

• Dispatches maintenance crews.

• Processes banks payments.

• Supports customer on payment/billing issues only.

• Risk management.

Payment Device/Pilot Reader

NYCTNYCT Internal Comms and Back Office

Service Provider Standard MerchantProcessing Network

9

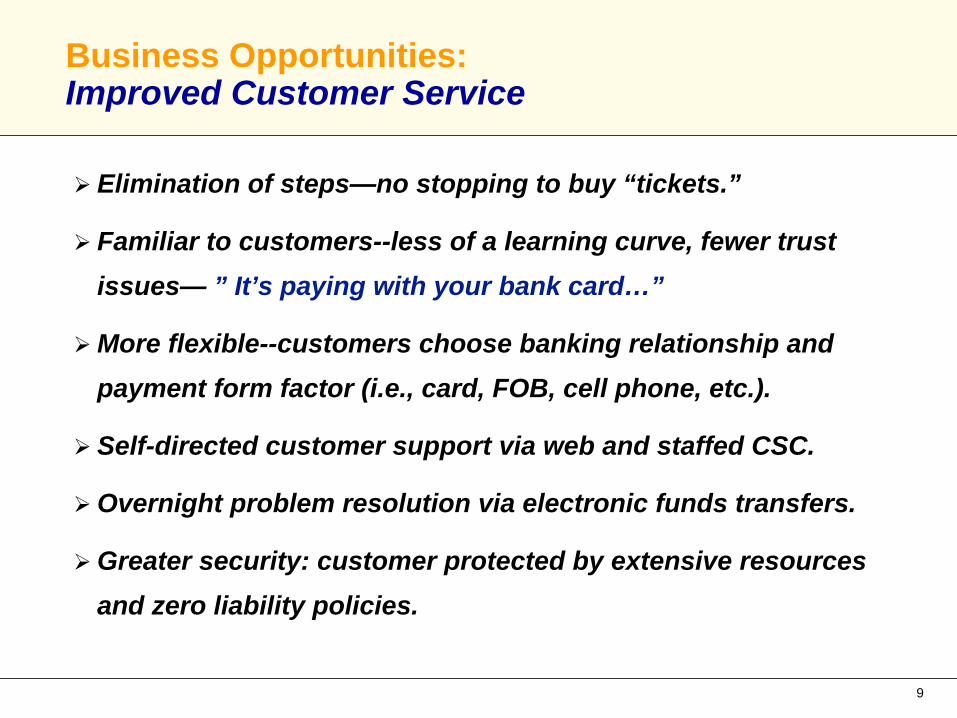

Business Opportunities: Improved Customer Service

Elimination of steps—no stopping to buy “tickets.”

Familiar to customers--less of a learning curve, fewer trust issues— ” It’s paying with your bank card…”

More flexible--customers choose banking relationship and payment form factor (i.e., card, FOB, cell phone, etc.).

Self-directed customer support via web and staffed CSC.

Overnight problem resolution via electronic funds transfers.

Greater security: customer protected by extensive resources and zero liability policies.

10

Business Opportunities : “Future Proof” the fare payment system

Reduce infrastructure investments, limiting exposure to potential issues of early obsolescence

— Fewer pieces of specialized equipment

— Simpler, decentralized infrastructure

Share cost of core technical upgrades and business process advances with broad range of stakeholders.

Tap into “open market” for equipment and services.

Concentrate functionality and major investment in a central back-office.

11

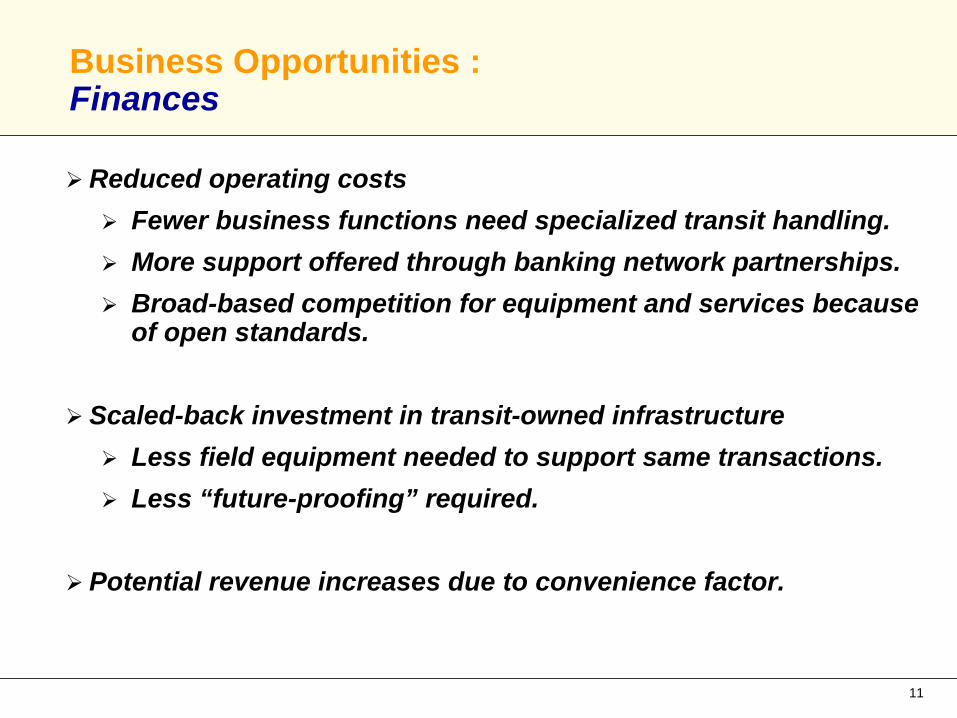

Business Opportunities : Finances

Reduced operating costsFewer business functions need specialized transit handling.More support offered through banking network partnerships.Broad-based competition for equipment and services because of open standards.

Scaled-back investment in transit-owned infrastructureLess field equipment needed to support same transactions.Less “future-proofing” required.

Potential revenue increases due to convenience factor.

12

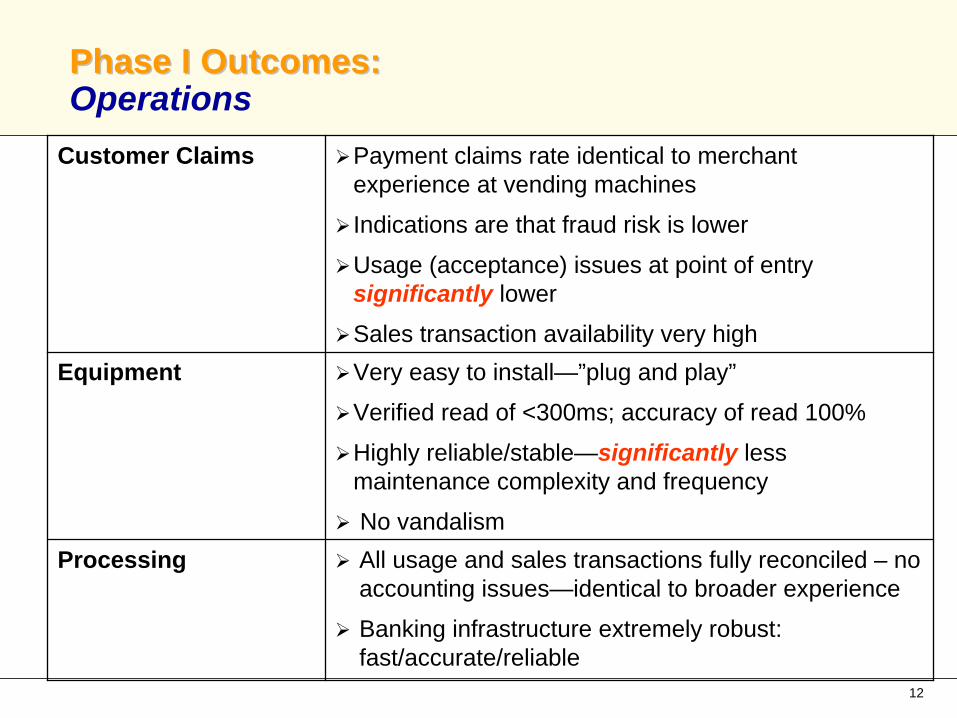

Phase I Outcomes: Phase I Outcomes: Operations

Customer Claims Payment claims rate identical to merchant experience at vending machines

Indications are that fraud risk is lower

Usage (acceptance) issues at point of entry significantly lower

Sales transaction availability very high Equipment Very easy to install—”plug and play”

Verified read of <300ms; accuracy of read 100%

Highly reliable/stable—significantly less maintenance complexity and frequency

No vandalismProcessing All usage and sales transactions fully reconciled – no

accounting issues—identical to broader experience

Banking infrastructure extremely robust: fast/accurate/reliable

13

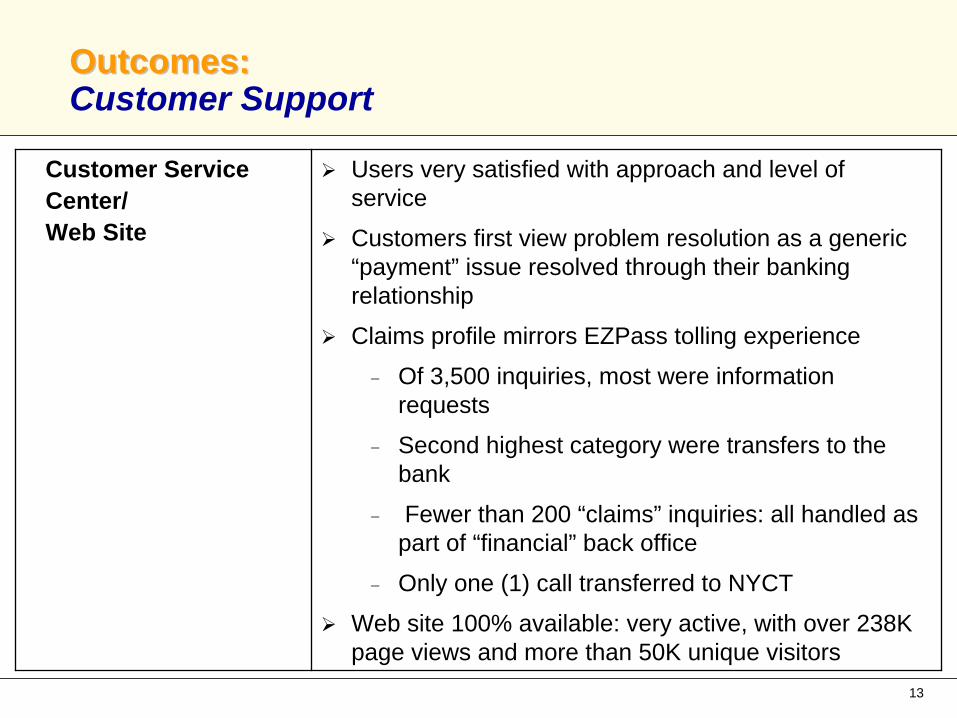

Outcomes: Outcomes: Customer Support

Customer ServiceCenter/ Web Site

Users very satisfied with approach and level of service

Customers first view problem resolution as a generic “payment” issue resolved through their banking relationship

Claims profile mirrors EZPass tolling experience

- Of 3,500 inquiries, most were information requests

- Second highest category were transfers to the bank

- Fewer than 200 “claims” inquiries: all handled as part of “financial” back office

- Only one (1) call transferred to NYCT

Web site 100% available: very active, with over 238K page views and more than 50K unique visitors

14

Myths Debunked

Transit fare policy is too complex to be programmed and managed by the financial services sector.

Transit agencies will lose “float” and/or expired card value.

A banking approach costs more than current systems.

Customers do not use debit/credit.

Accepting bank cards will be an added cost for transit; interchange will increase dramatically.

Transit will not have access to the same data as with a traditional AFC system.

Bank cards are less secure; privacy is a concern.

15

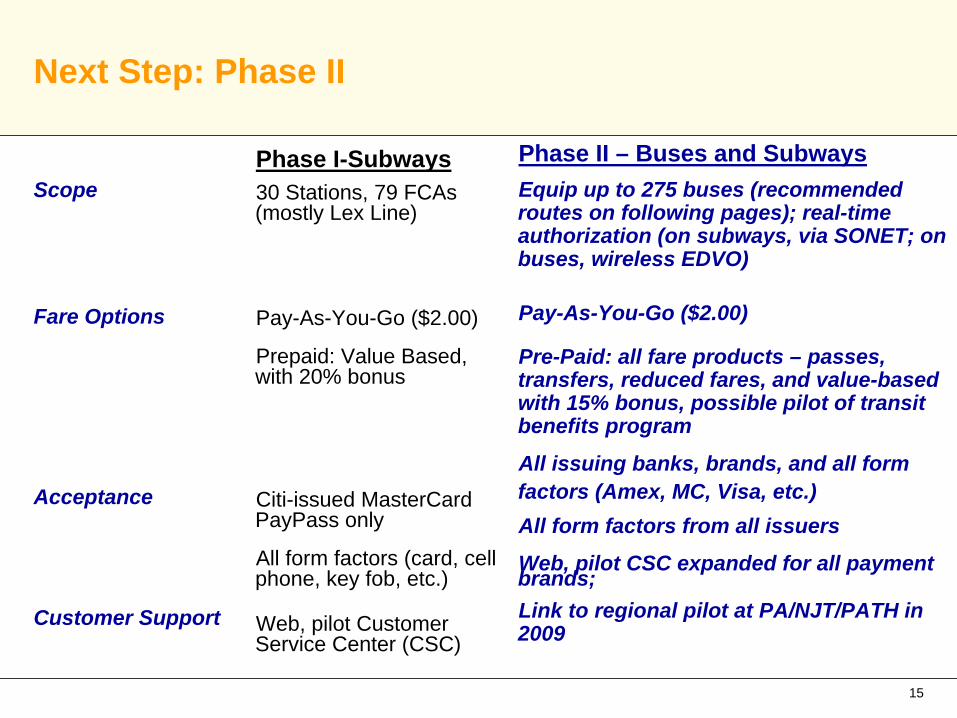

Next Step: Phase II

Scope

Fare Options

Acceptance

Customer Support

Phase I-Subways30 Stations, 79 FCAs (mostly Lex Line)

Pay-As-You-Go ($2.00)

Prepaid: Value Based, with 20% bonus

Citi-issued MasterCard PayPass only

All form factors (card, cell phone, key fob, etc.)

Web, pilot Customer Service Center (CSC)

Phase II – Buses and SubwaysEquip up to 275 buses (recommended routes on following pages); real-time authorization (on subways, via SONET; on buses, wireless EDVO)

Pay-As-You-Go ($2.00)

Pre-Paid: all fare products – passes, transfers, reduced fares, and value-based with 15% bonus, possible pilot of transit benefits program

All issuing banks, brands, and all form factors (Amex, MC, Visa, etc.)All form factors from all issuers

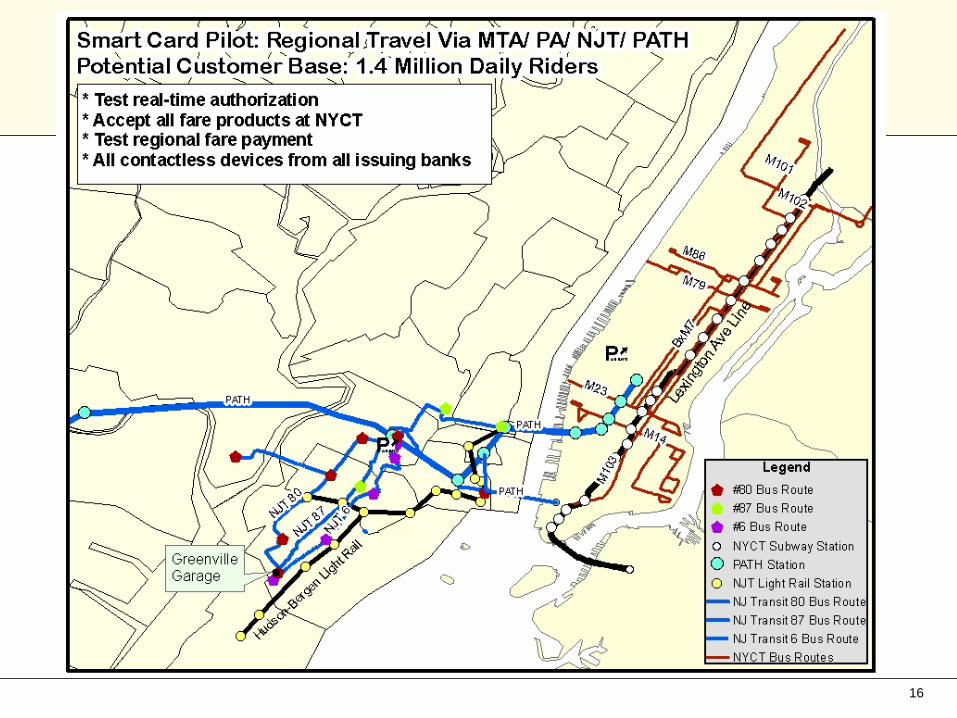

Web, pilot CSC expanded for all payment brands; Link to regional pilot at PA/NJT/PATH in 2009

16