Embed Size (px)

Citation preview

CONTENTS

PREFACE 02

INCOME TAX 03

INCOME TAX SCHEDULES 07

SALES TAX 14

FEDERAL EXCISE DUTY 20

ISLAMABAD CAPITAL TERRITORY ORDINANCE 22

23

KPK FINANCE ACT 25

PREFACE FINANCE ACTS, 2017

This document gives a brief insight of significant amendments made through Finance Acts 2017 and SRO’s relating to Sales Tax. This document also presents significant changes made in fiscal laws through respective Provincial Finance Acts except for Sindh and Balochistan. Changes in Custom laws are also not included in this document.

In order to understand the impact of a particular change, reference should be made to the specific wordings in the relevant statues. Expert opinion on specific change should be sought before taking decision having major economic significance.

This document can also be assessed on our website www.pkf.com.pk

July 14, 2017

02

INCOME TAX

Section 2(22A) Definition of fast moving consumer goods has been modified for the exclusion of durable goods.

Section 2(30C) Definition of Liaison Office along with the explanation has been inserted to explain the nature of business and activities required to be carried on by a liaison office.

Section 2(38B) Concept of “Online Marketplace” has been introduced to cover taxability of online transactions entered into by the persons through online portals and websites.

Section 2(62A) Definition of Start-ups has been inserted to provide incentives in the form of tax exemption for small to medium sized persons registered with Pakistan Software Export Board having turn-over of less than rupees one hundred million in each of last five years dealing in technology driven products and services.

Section 4B Applicability of Super tax has been extended to Tax Year 2018.

Section 5A Section 5A has been substituted and now 7.5 % tax on undistributed profits shall be payable by public companies who do not distribute at least 40 % of their profit through dividend or bonus shares before the due date of filing of return mentioned in section 118(2) without any condition of reserves being in excess of paid up capital.

Section 5AA Section 5AA was inserted vide Tax Laws (Amendment) Ordinance, 2016 to introduce separate tax regime for return on investment in Sukuks from special purpose vehicle. Now this regime has been extended to cover return on investment in Sukuks by a company also.

Section 7C & 7D Section 7C and 7D dealing with separate tax regime of builders and developers have been restricted to the projects undertaken for construction and sale of residential, commercial or other buildings initiated and approved during tax year 2017 only and subjected to payment of advance tax and issuance of installment schedules as per respective rules.

Section 13(7) The threshold of loan has been increased from five hundred thousand rupees to one million rupees on which either no profit is payable or the rate of profit on loan is less than the benchmark rate for treating the markup at differential rate as perquisite.

Section 21(o) The allowable limit for sales promotion related expense in case of Pharmaceutical Companies has been enhanced from 5% to 10%.

Section 22(15) Assets co-owned by a taxpayer and an Islamic financial institution licensed by SBP or SECP under Musharika Agreements, have been brought within the purview of depreciable assets in the hands of taxpayer.

Section 53 Certain powers have been assigned to the Board through Minister In charge to make rules and decisions which previously could be exercised only by the Federal Government with the approval of Economic Coordination Committee of the Cabinet.

Legal cover has been provided to the notifications issued from July 01, 2016 (which have not been earlier rescinded) up to June 30, 2018. This is in wake of decision of the Supreme Court where

03

04

notifications issued without Cabinet approval were declared illegal.

Section 60D

The threshold of maximum taxable income for deductible allowance for education expenses has been enhanced from rupees one million to rupees one and a half million.

Section 62 The scope of tax credit for acquiring new shares in public company listed on stock exchange and in respect to life insurance has been expanded to cover investment in Sukuks by the original allottee.

Further, in line with reversal of credit allowed for investment in newly issued shares which were disposed within twenty-four months, a new clause has been introduced to reverse the credit allowed for life insurance contribution where the policy is surrendered within two years of its acquisition.

Section 62A The limit for contribution for claiming tax credit for investment in health insurance has been enhanced from one hundred thousand rupees to one hundred and fifty thousand rupees.

Section 65A Tax credit of 3% under Section 65A for sales to sales tax registered persons has been withdrawn.

Section 65C Tax credit for enlistment on stock exchange under section 65C shall be further available for one tax year provided that the tax credit for the last two years shall be 10% of tax payable while the rate of 20% will remain valid for first year only.

Section 94 By omitting sub-section 3 of Section 94, now dividend paid by non-resident company to a resident person shall be taxed under section 5.

Section 100 Section 100 has been amended to include the profit and gains derived from Sui gas field within

the purview of Fifth Schedule from tax year 2017 onwards.

Section 100C

Restriction on the administrative and management expenditure up to 15% of the total receipts has been introduced for the non-profit organization excluding those organizations whose charitable activities have started for the first time within last three years and total receipts during the tax year are less than Rupees hundred million. Furthermore, surplus funds of No for Profit organizations shall be taxed at the rate of 10% subject to certain criteria.

Section 113 Minimum Tax under section 113 of the Ordinance has been increased to 1.25% from existing 1% for all other cases except for those whose rate for tax year 2017 is less than 1%. Persons engaged in running online market place have been placed in concessionary category of minimum tax at 0.5%.

Section 114 A correction has been made in Section 114 (6)(c) by omitting provisional assessments from the conditions for revising the returns as corresponding section 122C has been omitted.

Section 115 Through amendment in Section 115 relief has been granted to widows, orphans and disabled in filing of return on account of ownership of immovable property, flat and vehicle as per the requirements of Section 114.

Section 119 Amendment has been made in Section 119(4) to empower the Chief Commissioner to grant extension in time for filing of return in case the same has been refused by the Commissioner.

Section 121 Amendment has been made in Section 121 to allow Commissioner to make best judgment assessment on non-filing of return in response to notice under sub-sections (3) and (4) of section 114.

05

Section 122C Concept of provisional assessment has been aligned with best judgment assessment under section 121. Hence, section 122C being redundant has been omitted from statute books alongwith all references appearing in other provisions of the Ordinance.

Section 130 Section 130(3)(c) has been omitted through which FBR was authorized to appoint a law graduate officer of Inland Revenue Service in BS-20 or above as Judicial Member of Appellate Tribunal.

Section 147 The threshold for payment of advance tax u/s 147 has been enhanced from rupees five hundred thousand to rupees one million for individuals.

Section 148 Section 148(7) has been amended to make the tax withheld on import of fertilizer by the manufacturer as final tax.

Section 148(8) has been amended to make the tax withheld on import of Plastic Raw Material by the industrial undertaking as minimum tax.

Section 152 Section 152(B) has been amended to make the tax withheld from non-residents as final tax on the option of non-residents. This option was earlier available under clause 41 of Part IV of the Second Schedule to the Ordinance. Furthermore, the application for exemption or lower rate of tax withholding can now only be made by non-residents having their permanent establishment in Pakistan.

Section 153 A proviso to Section 153(1) has been added in which service provider has been made liable for collection of tax from service charge retained by 3rd party or agent for collection of their fee. It appears that this amendment is a result of dismissal of FBR appeal by Supreme Court against Pakistan Television and Distribution Companies.

Section 165

A provision has been inserted for revision of withholding tax statements under section 165 within 60 days of filing of the statement which is currently missing in the statute and causing many undue practical hurdles.

Section 176

Cost and Management firms declared eligible for tax audit under the provisions of section 176.

Section 182

Amendment has been made in Section 182 for penalty on Financial Institutions and reporting entities for failure to disclose certain information.

Section 205

Section 205 has been amended to cater the calculation of default surcharge in the case of persons having a special tax year. Default surcharge shall be calculated on and from the first day of the fourth quarter of tax year.

Section 206A

Advance ruling u/s 206A has been made applicable to non-residents having permanent establishment in Pakistan.

Section 207 & 2(38A)

Section 207 has been amended to add District Taxation Officer and Assistant Director Audit as officers of Inland Revenue.

Section 216

Section 216 has been amended for provision of information to Employees Old Age Benefit Institution regarding salaries in statements furnished under section 165.

Section 227B

Amendment has been made in Section 227B in order to reject the claim of reward by whistle blower if the information is not supported by any evidence.

06

Section 230D & 230E

Two new Sections have been inserted in the Ordinance for establishment of new Directorates

General namely Directorate-General of Broadening of Tax Base and Directorate-General of Transfer Pricing.

Section 231B

Amendment has been made in Section 231B so that the Modarabas, Islamic Banks and Shariah Compliant Schemes which shall now collect advance tax at the rate of 4% of the value of motor vehicle from non-filers.

Section 233

New sub-section has been added to determine the minimum amount of commission on which tax is required to be deducted for advertising agency. Now, the Payment to an advertisement agent/agency shall be made in two parts i.e. payment of commission and payment for advertisement. Tax on payment to media for advertisement shall be deducted under section 153 and tax on commission amount shall be deducted under section 233 and the amount of commission shall be calculated as under:

Payment to advertisement agency excluding commission x 15/85. Tax deducted as above shall be final tax on the income of advertising agency/agent.

Section 233A

Withholding tax under Section 233A by the Stock Exchange has been made final tax.

Section 234A

Tax deducted on electricity under section 235 will also be final tax on the income from CNG stations. Further, sales tax and other incidental charges appearing in the bill shall also be included for deduction of income tax under this section.

Section 235 & 235A

An explanation regarding electricity bill has been added in Section 235 & 235A to clarify that threshold of monthly bills would be inclusive of sales tax and all incidental charges. The threshold has also been increased from Rs.30,000 per

month to Rs. 360,000 per annum in order for tax withholding of commercial and industrial consumers.

Section 236C, 236K and 236W An explanation has been inserted in Section 236C, 236K and 236W to clarify that the said sections are applicable to person responsible for registering, recording or attesting transfer for local authority, housing authority, housing society, cooperative society and registrar of properties. Furthermore, tax withheld on the sale and purchase of immovable property within same tax year has been declared as minimum tax under Section 236K.

Section 236X A new Section 236X has been inserted requiring

Pakistan Tobacco Board or its contractors, at the

time of collecting cess on tobacco shall also collect advance tax at the rate of five percent of the purchase value of tobacco from every person purchasing tobacco including manufacturers of cigarettes.

Section 241 A new Section 241 has been added validating all notifications and orders issued and notified, before the first day of July, 2017 notwithstanding anything contained in any judgment of a High Court or the Supreme Court.

Upto

07

Income Tax Schedules Tax Rates for Business Individuals and AOPs

Taxable income Rate

From Upto

0 400,000 0%

400,001 500,000 7% of amount exceeding Rs. 400,000

500,001 750,000 Rs. 7,000 + 10% of amount exceeding Rs. 500,000

750,001 1,500,000 Rs. 32,000 + 15% of amount exceeding Rs. 750,000

1,500,001 2,500,000 Rs. 144,500 + 20% of amount exceeding Rs. 1,500,000

2,500,001 4,000,000 Rs. 344,500 + 25% of amount exceeding Rs. 2,500,000

4,000,001 6,000,000 Rs. 719,500 + 30% of amount exceeding Rs. 4,000,000

6,000,001 and above Rs. 1,319,500 + *35% of

amount exceedingRs.6,000,000

For AOP’s (Professional firms prohibited from incorporating by any law) rate of tax shall be at 32% from tax year 2016 and onwards.

Tax Rates for Salaried Individuals

Taxable Income Rate

From Upto

Taxable Income Rate

From

0 400,000 0%

400,001 500,000 2% of amount exceeding Rs. 400,000

500,001 750,000 Rs. 2,000 + 5% of amount exceeding Rs.500,000

750,001 1,400,000 Rs. 14,500 + 10% of amount exceeding Rs. 750,000

1,400,001 1,500,000 Rs. 79,500 + 12.5% of amount exceeding Rs. 1,400,000

1,500,001 1,800,000 Rs. 92,000 + 15% of amount exceeding Rs. 1,500,000

1,800,001 2,500,000 Rs. 137,000 + 17.5% of amount exceeding Rs. 1,800,000

2,500,001 3,000,000 Rs. 259,500 + 20% of amount exceeding Rs. 2,500,000

3,000,001 3,500,000 Rs. 359,500 + 22.5% of amount exceeding Rs. 3,000,000

3,500,001 4,000,000 Rs. 472,500 + 25% of amount exceeding Rs. 3,500,000

4,000,001 7,000,000 Rs. 597,000 + 27.5% of amount exceeding Rs. 4,000,000

7,000,001 and above

Rs. 1,422,000 + 30% of amount exceeding Rs. 7,000,000

Tax Rates for Companies

Description Rate

Banking company 35%

Small Company 25%

Other than banking company- TY- 2016 32%

Other than banking company- TY- 2017 31%

Other than banking company- TY- 2018 30%

Super Tax Rates

Description Rate

Banking company 4%

Other person having income equal to or exceeding Rs.500 Million 3%

08

Tax Rates for Dividend Income (including under Section 150 & 236S)

Tax rate including advance tax on dividend under section 150 and 236S paid by collective investment scheme, REIT Scheme or a mutual fund.

Person Stock Fund

Money market fund, income fund or REIT scheme or

any other fund

Filer Non-Filer

Individual 12.5% 12.5% 15%

Company 12.5% 25% 25%

AOP 12.5% 12.5% 15%

Tax Rates for Return on Investment in Sukuks

Sukuk holder Rate

Company 25%

Individual or AOP

10% If the return is less than Rs. 1 million and 12.5% if return is more

than Rs. 1 million Tax Rates for payment to Non-resident

Income Rate

Royalty 15% of gross amount

Fee for Technical Services 15% of gross amount

Tax Rates for Shipping or Air Transport Income of a Non-resident

Income Type Rate

Shipping Income 8% of Gross amount

Air Transport Income 3% of Gross amount

Property income. The same rates shall be applicable for withholding tax under section 155 for individual and AOPs.

Taxable Income Rate

From Upto

0 200,000 0%

200,001 600,000 5% of the gross amount of rent exceeding Rs.200,000

600,001 1,000,000 Rs.20,000 + 10 % of the gross amount exceeding Rs.600,000

1,000,001 2,000,000 Rs.60,000 + 15 % of the gross amount exceeding Rs.1,000,000

2,000,001 and above Rs.210,000 + 20% of the gross amount exceeding Rs.2,000,000

Dividend declared by Rate

Filer Non-Filer

Power generation sector Companies

7.5% 7.5%

Other Companies 15% 20%

Tax Rates for Profit on debt for Individuals and AOPs are as under:

Profit on debt Rate

From Up to

0 5,000,000 10%

5,000,001 25,000,000 12.5%

25,000,001 and above 15%

09

Minimum Tax under section 113

Sr. No Persons Rate

1

a) Oil Marketing Companies, Oil Refineries, SSGCL, SNGPL (where turnover exceeds Rs. 1 billion;

b) Pakistan Airlines; c) Poultry industry

including poultry breeding, broiler production, egg production & poultry feed production;

d) Dealers or distributors of fertilizers; and

e) Persons running online market place

0.50%

2

a) Distributors of pharmaceutical products, Fast moving consumer goods and cigarettes

b) Petroleum agents and distributors who are registered under the Sales Tax Act, 1990;

c) Rice mills and dealers; and

d) Flour Mills

0.20%

3 Motorcycle dealers registered under the Sales Tax Act, 1990

0.25%

4 In all other cases 1.25%

Tax Rates for Imports under Section 148

Category Filer Non Filer

Category Filer Non Filer

- Industrial undertaking importing re-meltable steel (PCT Heading 72.04) and directly reduced iron for its own use. - Manufacturers covered under

SRO 1125( I)/2011, dated 31-12-2011. 1% 1.5%

- Import of Potassic Fertilizer - Imports of Urea fertilizer - Import of gold

- Import of cotton - Import of LNG- designated

buyers

Import of pulses 2% 3%

Commercial importers covered under 3% 4.5% SRO 1125 (I) / 2011, dated 31-12- 2011

Ship breaker on import of ship 4.5% 6.5%

Tax to be collected from every importer of goods on the value of goods. a) In the case of Industrial

5.5% 8% undertaking not otherwise

covered b) all other cases of companies 5.5% 8%

c) In the case of persons other 6% 9% than those covered in a & b above

Plastic raw material under PCT Heading 39.01 to 39.12

1. if imported by Industrial undertaking for own use

2. commercial imports

1.75% 4.5%

8% 8%-9%

Capital Gain Tax on Immoveable properties 37(1A)

Category Filer Non-Filer

On sale by:

Dependent of Shaheed Armed Forces 0% 0%

Dependent of died person while in service of Federal or Provincial Govt. or Armed Forces

0% 0%

Original allotee where allotment is duly certified by official allotment authority

0% 0%

10

Category Filer Non-Filer

Any other sale whereby:

� holding period is upto 1 Year * 10% 10%

� holding period between 1 to 2 year * 7.5% 7.5%

� holding period between 2 to 3 year * 5% 5%

� holding period is more than 3 year 0% 0%

*Property acquired before July 01, 2016 where holding period is up to three years the rate of tax will be 5%.

These rates shall be reduced by 50% on first sale by the current and Ex-Government employees and Armed Forces personnel.

Rates of tax applicable under other provisions of the Ordinance are tabulated as under with distinction of filer and non-filer.

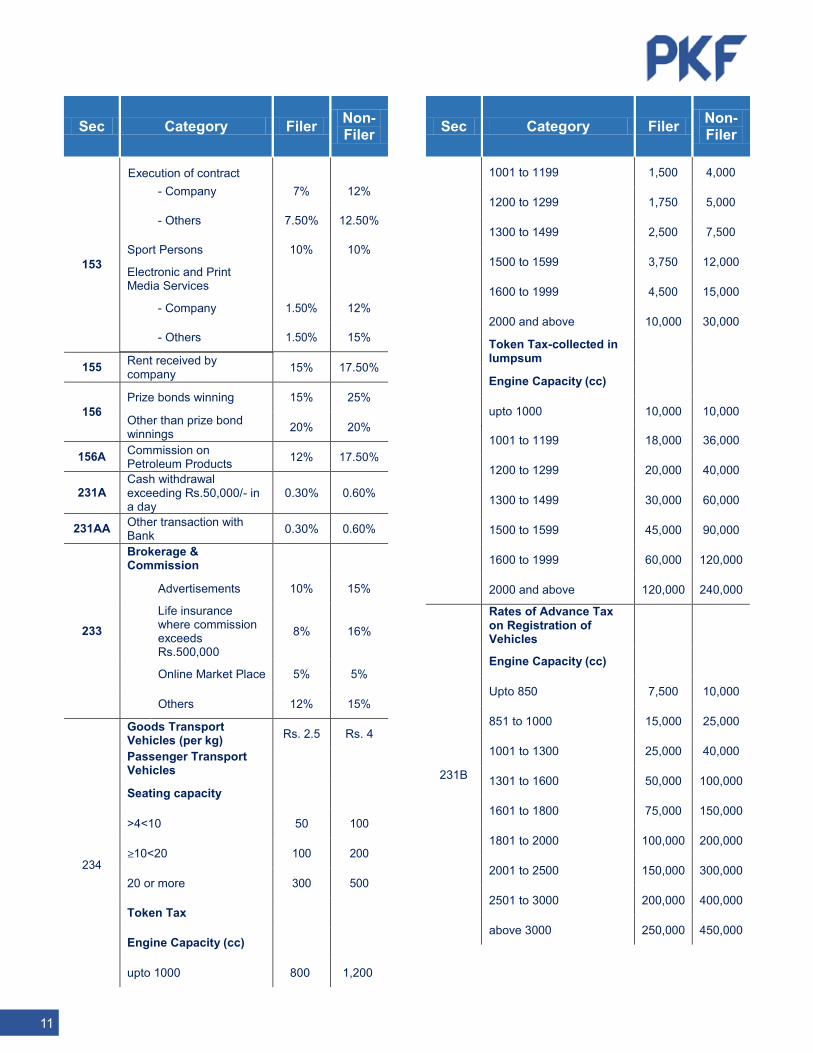

Sec Category Filer Non-Filer

Sec Category Filer Non-Filer

37A

Capital Gains Tax on

Securities acquired before 01.07.2016 where

Holding period less than 12 Months 15% 18%

Holding period 12 to 24 Months 12.50% 16%

Holding period more than 24 Months but purchased after 01-07-2013

7.50% 11%

Security purchased before 01-07-2013 0% 0%

Securities acquired after 01.07.2016 irrespective of holding period

15% 20%

Future Commodity Contracts 5% 5%

Derivatives traded on stock exchange settled through cash

5% 5%

151 Profit on Debit 10% 17.50%

152

Payments to Non-Residents for

Construction contracts and

7% 13% Advertisement services through Satellite T.V. Channels Payments to Permanent Establishment of Non- Residents

Supply of goods

- Company 4% 7%

- Others 4.50% 7.75%

Services

- Company 8% 14%

- Others 10% 17.50%

Transport services 2% 2%

Execution of contract

- Company 7% 13%

- Others 7% 13%

Sport persons 10% 10%

153

Payments to Residents

Supply of goods-

- Company 4% 7%

- Others 4.50% 7.75%

Supply of goods-FMCG distributors

- Company 2% 2%

- Others 2.50% 2.50%

Services

- Company 8% 14.50%

- Others 10% 17.50%

Transport services 2% 2%

11

Sec Category Filer Non-Filer Sec Category Filer Non-

Filer

153

- Company 7% 12%

- Others 7.50% 12.50%

Sport Persons 10% 10%

Electronic and Print Media Services

- Company 1.50% 12%

- Others 1.50% 15%

155 Rent received by company 15% 17.50%

156 Prize bonds winning 15% 25%

Other than prize bond winnings 20% 20%

156A Commission on Petroleum Products 12% 17.50%

231A Cash withdrawal exceeding Rs.50,000/- in a day

0.30% 0.60%

231AA Other transaction with Bank 0.30% 0.60%

233

Brokerage & Commission

Advertisements 10% 15%

Life insurance where commission exceeds Rs.500,000

8% 16%

Online Market Place 5% 5%

Others 12% 15%

234

Goods Transport Vehicles (per kg) Rs. 2.5 Rs. 4

Passenger Transport Vehicles

Seating capacity

>4<10 50 100

≥10<20 100 200

20 or more 300 500

Token Tax

Engine Capacity (cc)

upto 1000 800 1,200

1001 to 1199 1,500 4,000

1200 to 1299 1,750 5,000

1300 to 1499 2,500 7,500

1500 to 1599 3,750 12,000

1600 to 1999 4,500 15,000

2000 and above 10,000 30,000

Token Tax-collected in lumpsum

Engine Capacity (cc)

upto 1000 10,000 10,000

1001 to 1199 18,000 36,000

1200 to 1299 20,000 40,000

1300 to 1499 30,000 60,000

1500 to 1599 45,000 90,000

1600 to 1999 60,000 120,000

2000 and above 120,000 240,000

231B

Rates of Advance Tax on Registration of Vehicles

Engine Capacity (cc)

Upto 850 7,500 10,000

851 to 1000 15,000 25,000

1001 to 1300 25,000 40,000

1301 to 1600 50,000 100,000

1601 to 1800 75,000 150,000

1801 to 2000 100,000 200,000

2001 to 2500 150,000 300,000

2501 to 3000 200,000 400,000

above 3000 250,000 450,000

Execution of contract

12

Sec Category Filer Non-Filer Sec Category Filer Non-

Filer

231B

Rates of Advance tax on transfer of Vehicles

Engine capacity (cc)

up to 850 - 5,000

851 to 1000 5,000 15,000

1001 to 1300 7,500 25,000

1301 to 1600 12,500 65,000

1601 to 1800 18,750 100,000

1801 to 2000 25,000 135,000

2001 to 2500 37,500 200,000

2501 to 3000 50,000 270,000

above 3000 62,500 300,000

234A CNG station 4% 6%

236A Sale by auction 10% 15%

236B Purchase of domestic air ticket 5% 5%

236C Sale/transfer of immovable property 1% 2%

236D Functions and gatherings 5% 5%

236H

Sales to retailers

- Electronics 1% 1%

- Others 0.50% 1%

236G

Sales of Distributors, dealers or wholesaler

- Fertilizer 0.70% 1.40%

- Other than Fertilizer 0.10% 0.20%

236I Advance tax by educational Institutions 5% 5%

236J

Advance tax on dealers, commission agents and arhatis etc.

Group/Class A 100,000 100,000

Group/Class B 7,500 7,500

Group/Class C 5,000 5,000

Any other category 5,000 5,000

236K

Purchase of immovable property

Value 0-4million 0% 0%

Exceeding 4 million 2% 4%

236P

Transaction other than cash through Bank (exceeding 50,000 in a day)

Nil *0.60%

236Q Tax on Machinery rental 10% 10%

236R Education expenses remitted abroad 5% 5%

236U

Insurance premium

General 4% 4%

Life insurance exceeding 0.3 million/annum

1% 1%

Others 0% 0%

236V Extraction of minerals 0% 5%

*This rate has been reduced to 0.40% vide S.R.O. 602(I)/2017dated 03 July 2017 till 30th September 2017.

13

2nd Schedule

Exemptions/Concessions Introduced:

� Income of Asian Infrastructure Investment Bank and persons as provided in Article 51 of Chapter IX of the Articles of Agreement signed and ratified by the Pakistan is exempt from tax.

� Tax exemption granted for the income of Gulab Devi Chest Hospital, Pakistan Poverty Alleviation Fund, National Academy of Performing Arts, Pakistan Sweet Homes Angels and Fairies Place, and National Rural Support Program.

� Exemption from tax is granted to Japan International Cooperation Agency (JICA) on profit on debt earned from Islamabad-Burhan Transmission Reinforcement Project (Phase-I).

� Tax exemption including minimum tax and withholding under section 153 is allowed to startup businesses as defined under section 2(62A) of the Ordinance.

� Exemption granted from withholding of tax at import stage under section 148 of the Ordinance to Oil Marketing Companies licensed by the OGRA.

� Fixed tax Regime of Hajj Group Operators is extended up to Tax Year 2017.

� Limit for importing raw material without payment of advance tax under section 148 of the Ordinance is enhanced to 125% from existing 110% of the imported and consumed raw material of the preceding tax year. However, the said facility has been withdrawn from undertakings importing edible oil, packing materials and certain plastic raw materials.

� PCT headings for various agricultural equipment are harmonized in the wake of

implementation of new PCT codes with effect from July 01, 2017.

� Reduced rate of 2% for a company being a filer engaged in freight forwarding services, courier services, man power outsourcing services, hotel services, security guard services, software and IT related services, car rental services, building maintenance services, services rendered by Pakistan Stock Exchange etc. has been extended up to tax year 2018 subject to filing of irrevocable undertaking by November 2017 to present its accounts for audit.

� Reduced rate for withholding of tax at 5% for commission/brokerage of persons operating from online markets as defined in clause 38B of section 2 has been introduced

� Cash withdrawal made from Branchless Banking Agents’ Accounts is exempted from deduction of tax under section 231A of the Ordinance.

� Tax on motor vehicles to be collected by leasing companies from non-filers shall not be applicable on light commercial vehicles leased under the Prime Minister’s Youth Business Loan Scheme.

Exemptions/Concessions Withdrawn:

Exemption to steel re-rollers from tax withholding under section 153(1) has been withdrawn.

7th Schedule

Notional gain/loss shall not be allowed while computing taxable income of banking companies.

8th Schedule

NCCPL is now required to submit to FBR a statement of capital gains and tax computed therein within forty five days instead of existing thirty days.

14

Sales Tax Section 2 (43A) A new clause (43A) in section 2 has been inserted where the concept of Tier-1 “Retailers” existed in Rule-4 of Special Procedures which has been struck down by the Lahore High Court; has now been made as part of Definition clause. Following categories fall under Tier-1 Retailer:

a retailer operating as a unit of a national or international chain of stores;

a retailer operating in an air-conditioned shopping mall, plaza or center, excluding kiosks;

a retailer whose cumulative electricity bill during the immediately preceding twelve consecutive months exceeds rupees six hundred thousand; and

a wholesaler-cum-retailer, engaged in bulk import and supply of consumer goods on wholesale basis to the retailers as well as on retail basis to the general body of the consumers;

The retailers falling under above categories shall pay sales tax at normal rate and shall observe all the applicable provisions of the Act and rules made thereunder, including the requirement to file monthly sales tax returns.

However, the retailers making supplies of finished goods of the five sectors specified in Notification No. S.R.O. 1125(I)/2011, dated 31st December 2011 shall pay sales tax in respect of such supplies at the rates prescribed in the said Notification.

An option has been given to Tier-1 retailers, to pay sales tax under the turnover regime at the rate of two percent of their total turnover, including turnover relating to exempt supplies, without

adjustment of any input tax; in lieu of normal tax payable. Those retailers willing to pay sales tax on the basis of total turnover shall file an option to the Chief Commissioner of Regional Tax Office or Large Taxpayers Unit having jurisdiction by 15th day of July opting to pay sales tax on the basis of turnover and such an option shall remain in force for the whole financial year.

Section 3 Now the goods imported by the persons in areas where sales tax is not applicable, shall also be subject to sales tax at import stage. This appears in wake of judgment of Peshawar High Court declaring non-levy of sales tax at import stage on the goods imported for consumption in areas where provisions of the Sales Tax Act, 1990 are not applicable. The scope of Further Tax has been extended to Zero rated goods by adding section 4 at the end of Section 3(1A). In recent order, the Lahore High Court held that zero rated goods covered under SRO 1125 are not subject to further tax. To counter the implications of the said decision, corresponding amendments have been made in section 4 as well. Section 4, 7,7A,8 & 13 Various Sections have been amended whereby the power to notify to charge tax on taxable goods and manner to charge such higher or lower rate or rate as may be specified has been assigned to Board with the approval of Minister in Charge instead of the Federal Government. Similar amendments have been made in Section 4 to notify zero rating of taxable supplies and in section 7(3) and (4) to allow input tax against output tax to registered persons or class of persons and Section 7A for Levy and collection of tax on specified goods on value addition. Section 8 where tax credit is not allowed. The exemption notified u/s Section 13(2)(a) shall also be exercised by Board through Minister In Charge but the Board shall place all notification before the National Assembly

15

issued in financial year for approval at the year end. A legal protection has been given for the notifications issued with effect from 1st July 2016 which shall remain in force till 30th June 2018 unless rescinded earlier. Similar powers have been assigned to Board through Minister in Charge power to deliver certain goods without payment of tax under section 60 and exemption of tax not levied or short levied as a result of general practice under section 65. Previously “ Special Procedure” could only be prescribed by the Federal Government, now the Board through Minister in Charge has also been empowered to prescribe such Rules. Section 30 List of Sales tax authorities has been amended to include District Taxation Officer and Assistant Director Audit. Further the Chief Commissioners Inland Revenue shall perform their functions in respect of such persons or classes of persons of such areas as the Board may direct. Whereas, the Commissioners Inland Revenue shall perform their functions in respect of such persons or classes of persons of such areas as the Chief Commissioner, to whom they are sub-ordinate, may direct. Section 33 Measures against counterfeited or non-tax paid cigarette made further stringent by introducing specific penalty clause in section 33 with respect to manufacture, possession, transportation, distribution, storage and sale of such cigarette packs. Further, it shall be liable to confiscation, permanent seizure of vehicles and imprisonment up to 3 years plus 100% penalty.

Section 48

A proviso has been added in section 48(1)(f) that the Commissioner shall not issue notice for recovery of any tax due from a taxpayer if the said taxpayer has filed an appeal under section 45B in respect of the order under which the tax sought to be recovered has become payable and the appeal has not been decided by the Commissioner (Appeals), subject to the condition that twenty-five per cent of the amount of tax due has been paid by the taxpayer. Section 56 An order/notice sent electronically through email or to the e-folder maintained for e-filing of Sales Tax-Cum-Federal Excise returns by the Limited Companies, both public and private shall be treated as properly served. It means service of order in person would not be compulsory. Section 74A A new Section 74A has been added to give legal cover to all notifications and orders issued and notified in exercise of the powers conferred upon the Federal Government, before the commencement of Finance Act, 2017. These notifications/orders shall be deemed to have been validly issued and notified in exercise of those powers, notwithstanding anything contained in any judgment of the High Court or Supreme Court. Schedules

Pakistan being a signatory to HS Convention is obliged to adopt the latest HS 2017 effective internationally from January 2017. Pakistan is bound to adopt the new HS Code system from beginning of its financial year. Consequently, the HS Codes of various items are harmonized with the latest changes.

16

6th Schedule

Following exemptions have been introduced in Table 1 (Import or Supplies):

Goods received as gift or donation from foreign government or organization by the Federal or Provincials Governments or any public-sector organization subject to recommendations of the Cabinet Division and concurrence by the FBR. Sunflower and canola hybrid seeds meant for sowing Combined harvesters up to five years old

Exemption has been introduced in Table 2 (Local Supplies Only) on Single cylinder agriculture diesel engines of 3 to 36HP.

Entries with respect to alternate energy in Table 3 of the Sixth Schedule have been harmonized.

8th Schedule

Reduced rate of 5% introduced in Finance Act, 2016 for shifting existing analog cable to digital cable which expired on June 30, 2017 is extended for further one year i.e. up to June 30, 2018.

Reduced rates for fertilizers have been introduced as under.

Sr #

Description Rate / Amount (Rs) Conditions

Sr #

Description Rate / Amount (Rs) Conditions

35 DAP 100/50kg Nil

36 NP (22-20) 168/50kg

If Manufactured from Gas other than Imported LNG

37 NP (18-18) 165/50kg

38 NPK-I 251/50kg

39 NPK-II 222/50kg

40 NPK-III 341/50kg

41 SSP 31/50kg

42 CAN 98/50kg

43

Natural Gas 10% If supplied to fertilizer plants for manufacturing of UREA

44

Phosphoric Acid

5% If Imported by Fertilizer Company for Manufacturing of DAP

Sales tax on import of poultry machinery will be levied at reduced rate of 7% as under.

Sr # DESCRIPTION HS Codes Rate

45

i) Machinery for preparing feeding stuff

8436.1000 7%

ii) Poultry incubators and brooders

8436.2100 &

8436.2900

7%

iii) Insulated sandwich panels

Respective heading

7%

iv) Poultry Sheds 9406.1020

&

9406.9020

7%

v) Evaporative air cooling system

8479.6000 7%

Vi) Evaporative cooling pad

8479.9010 7%

Sales tax on import of multi-media projectors by educational institutions has been introduced at reduced rate of 10%. Sales tax on locally produced coal is chargeable at the higher of Rs.425 per metric ton or 17% ad valorem for HS Code 27.01

17

Sales tax on Liquefied Natural Gas imported by fertilizer manufacturers for use as feed stock shall be charged at reduced rate of 5%.

Sales tax on Fish feed against HS Code 2309.9090 shall be charged at 10%.

9th Schedule

Sales Tax on low and medium priced cellular mobile or satellite phones is chargeable now at Rs.650 instead of prevailing rates of Rs.300 & 1,000 respectively.

IMPACT OF SALES TAX SROS

S.R.O. 583(I)/2017 -

Amendment in the Sales Tax Special Procedure Rules, 2007

Tier-1 Retailers shall now pay sales tax under section 3(9A).

Sales tax rate for steel-melter, steel re-roller etc. has been revamped.

Extra Tax shall not apply on supply of lubricating oils made to registered Oil Marketing Companies(OMCs) and those made by OMCs to registered manufacturers for in-house consumption.

S.R.O. 584(I)/2017 -

Changes in SRO 1125(I)/2011 dated December 31, 2011 have been made in the following manner.

S. No.

Description of goods and

point of taxation

Rate of Sales Tax

w.e.f.July 1, 2017

Previous rate

1. Goods usable as industrial inputs, specified in Table I including fabric

i

Import for in-house consumption by registered manufacturers of the five sectors

0% 0%

ii Commercial imports excluding finished fabric

0% + 0% value addition tax

0% + 0% value addition tax

iii

Supplies to registered or unregistered persons of the said five sectors excluding supplies of finished fabric

0% 0%

iv Supplies to persons outside the said five sectors

17% 17%

v

Import by, or supply to, registered manufacturers, whether or not of the said five sectors, for the manufacture of goods specified in Table-I or Table-II

0% 0%

vi

Supplies of finished fabric to manufacturers of five sectors specified in condition (i) below

0% 0%

vii

Supply of finished fabric to and by retailers; supplies of finished fabric to end consumers; other supplies of finished fabric

6% 5%

viii Commercial imports of fabric

6% +2% VAT 0%

18

Other conditions mentioned in SRO 1125 are same except for following significant amendments

1. Zero rating on imported raw and ginned cotton allowed under this SRO with effect from July 15, 2017.

2. Benefit of this SRO for textile sector would

S. No.

Description of goods and

point of taxation

Rate of Sales Tax

w.e.f.July 1, 2017

Previous rate

2. Processed goods, including fabrics

. Processing of goods owned by other 0% of the 0% of the

persons, by registered manufacturers processing processing

of the five sectors mentioned in charges charges

condition (i) below.

3. Locally manufactured finished articles

of

Textiles and textile made-ups including carpets* and 6% 5%

b leather and artificial leather*

4. Imported finished goods ready for use by the general public

i Import 17%, plus 17%, plus

2% value 2% value addition addition tax tax ii Supply thereof 17% 17%

5. Machinery

Machinery, not manufactured locally, if imported by textile industrial units registered with Ministry of Textile Industry, as specified in Part IV of the Fifth Schedule to the Customs Act, 1969, subject to same conditions as specified therein

0% 0%

be allowed from spinning stage onwards.

3. Further tax at the rate of one percent for the supplies covered under this SRO excluding finished articles on which further tax shall be charged as levied under section 3(1A) which is currently 2%.

S.R.O. 585(I)/2017 -

Amendment in the SRO 648(I)/2013 dated July 09, 2013

Following further categories added where further tax will not be charged, levied or paid.

Fertilizers Supplies made by Steel Melters, Re-

Rollers and ship breakers operating under Chapter XI of Sales Tax Special Procedure Rules, 2007

Supplies covered under Fifth Schedule to the Sales Tax Act, 1990

S.R.O. 586(I)/2017 -

Amendment in the Sales Tax Special Procedure (Withholding) Rules, 2007

Withholding of sales tax shall not be applicable on supplies made by Active Taxpayer to another registered person except for advertisement services.

S.R.O. 587(I)/2017 -

Reduced rate for hybrid electric vehicles

50% reduction in applicable sales tax for vehicles with engine capacity upto 1800 CC and 75% reduction for vehicles with engine capacity from 1801 CC to 2500 CC.

19

S.R.O. 588(I)/2017 -

Amendment in the SRO 445(I)/2004 dated June 12, 2004.

Certain Islamic modes of transactions i.e. Murabaha, Musawamah, Bai Muajjal, Bai Salam, Istisna, Tijarah and Istijrar are excluded from the definition of supply. S.R.O. 591(I)/2017 & S.R.O. 592(I)/2017 -

Rescindment of SRO 491(I)/2015 dated June 30, 2015 and amendment in SRO 549(I)/2006 dated June 05, 2006.

No input tax adjustment will be allowed on locally produced coal where the value of supply does not exceed Rs.5,000/metric tone.

20

FEDERAL EXCISE DUTY Section 2, 3, 16 & 47C Various Sections have been amended whereby the power to notify/charge tax on taxable goods and manner to charge such at higher or lower rate or rate as may be specified which has been assigned to Board with the approval of Minister In Charge instead of the Federal Government. The exemption to be notified shall be exercised by Board through Minister-In Charge but the Board shall place all notification before the National Assembly issued in financial year. A legal protection has been provided to the notifications issued from 1st July 2016 shall remain in force till 30th June 2018 unless rescinded earlier. Now persons in areas where FED is not applicable, shall also be subjected to FED at import stage. Section 19 Where any person is engaged in the manufacture or production of cigarettes in the manner contrary to this Act or the rules made there under or otherwise evades duty of excise on cigarettes or is engaged in the manufacture or production of counterfeited cigarettes or tax stamps, banderoles, stickers, labels or barcodes, or is engaged in the manufacturing or production of cigarettes packs without affixing, or affixing counterfeited, tax stamps, banderoles, stickers, labels or barcodes,

the machinery, equipment’s, instruments or devices used in such manufacture or production shall, after outright confiscation, be destroyed in such manner as may be approved by the Commissioner and no person shall be entitled to any claim on any ground whatsoever, or be otherwise entitled to any compensation in respect of such machinery or equipments, instruments or devices and such confiscation or destruction shall be without prejudice to any other penal action which may be taken under the law against the person or in respect of the cigarettes, tax stamps, stickers, labels, barcodes or vehicles involved in or otherwise linked or connected with the case. Section 29 The List of authorities is amended to include “District Taxation Officer” and “Assistant Director Audit” . The Chief Commissioners Inland Revenue shall perform their functions in respect of such persons or classes of persons of such areas as the Board may direct. Whereas, the Commissioners Inland Revenue shall perform their functions in respect of such persons or classes of persons of such areas as the Chief Commissioner, to whom they are sub-ordinate, may direct. Section 37 A proviso has been added in section 37 that the Commissioner shall not issue notice for recovery of any duty due from a taxpayer if the said taxpayer has filed an appeal under section 33 in respect of the order under which the tax sought to be recovered has become payable and the appeal has not been decided by the Commissioner (Appeals), subject to the condition that twenty-five per cent of the amount of tax due has been paid by the taxpayer. Section 43A A new Section 43A has been added and all notifications and orders issued and notified in exercise of the powers conferred upon the

21

Federal Government, before the commencement of Finance Act, 2017, shall be deemed to have been validly issued and notified in exercise of those powers, notwithstanding anything contained in any judgment of the High Court or Supreme Court. Section 47 An order/notice sent electronically through email or to the e-folder maintained for the purpose of e-filing of Sales Tax-cum-Federal Excise returns by the Limited Companies, both public and private shall be treated as properly served. It means service of order/notice in person is not compulsory. Schedules First Schedule FED on locally produced cigarettes shall be charged at Rs. 3,740, Rs.1,670 and Rs.800 in the following manner:

Printed Retail Price Range (per thousand cigarettes)

FED

<2,920 Rs. 800

>2,920 < 4,500 Rs. 1,670

>4,500 Rs. 3,740

Federal Excise duty on cement has been increased from Rs.1 per kg to Rs.1.25 per kg Cigarette manufacturers cannot reduce retail price from the level adopted on the day of the announcement of latest budget. Further, no brand can be sold at retail price lower than forty five percent of Rs.4,500/thousand cigarette excluding sales tax.

FED on telecommunication services is reduced from 18.5% to 17%. FED shall not be charged for a period of twenty three years on the vehicles imported by China Overseas Ports Holding Company Limited and its operating companies subject to certain conditions and limitations prescribed under PCT heading 9917 (3).

22

Islamabad Capital Territory Tax on Services Ordinance 2001Through S.R.O. 589(I)/2017 and S.R.O. 590(I)/2017 dated July 01, 2017, following amendments have been introduced.

Services provided or rendered by marriage halls and lawns including “pandal” and “Shamiana” services and caterers shall be taxable at the rate of 5% subject to the condition that input tax paid by such service providers shall not be available for adjustment against output tax.

Exemption from the whole of tax has been

provided to the export of IT and IT-enabled services.

23

THE PUNJAB FINANCE ACT, 2017 STAMP ACT, 1899

CVT has been withdrawn and is now merged with the Stamp Duty. In this regard, stamp duty applicable on various items has been harmonized. PUNJAB SALES TAX ON SERVICES ACT, 2012

Section 2(17) Definition of Due Date has been modified for the purpose of specification of different dates for furnishing different parts or annexures of the return. This amendment seeks to introduce the concept of Sales Tax Real Time Invoice Verification as already introduced by the FBR whereby input tax adjustment would be allowed to a buyer subject to declaration of same value and output tax by the supplier. Section 2(30) Amendment has been made to extend the scope of Place of Business in order to bring persons carrying on economic activities in Punjab through virtual presence, web-sites, web portals, any other form of E-commerce or through liaison offices under the tax net. Section 11A A new section 11A has been inserted to the effect that where a registered person has not made payment of sales tax within specified due date or a registered recipient of service being a withholding agent or otherwise failed to pay the amount of tax to the supplier within 180 days of issuance of invoice, both the recipient and service provider

shall be jointly and severally liable for payment thereof. Section 14A A new concept for collection of tax has been introduced through insertion of Section 14A whereby PRA is empowered to require any person or class of persons not necessarily being a service provider and recipient to pay the whole or any amount of tax charged on any service or class of service in such a manner and at such time as the PRA requires.

Section 16 Certain procedural amendments have been made in section 16 to ensure proper control over claim of input tax by service providers especially with respect to tax paid under other Federal/ Provincial laws. Further, PRA subject to approval of Government, shall be empowered to prescribe limitations/ restrictions as to claim of input tax with respect to persons or class of persons.

Section 16C

Section 16C has been inserted which provides that the input tax paid on acquisition of specified capital goods, machinery and fixed assets shall be adjustable against the output tax in twelve equal monthly installments. Section 24(2) The time limit for assessment of sales tax by an officer of PRA has been increased from 5 to 8 years through amendment in Section 24(2). Section 39 List of authorities has been amended to include “Risk Compliance O�cer” and “Enforcement O�cer” who shall be subordinate to Deputy Commissioner or Assistant Commissioner. Section 48 The amount of penalty on account of obstruction in performance of duties of an officer of Authority has been increased from Rs. 25,000 to Rs. 100,000.

24

Section 70 A new clause has been inserted in Section 70(1) which extends the scope of tax recovery whereby recovery officer of Authority may give notice in writing to any person on account of legally enforceable relations created between the taxpayer and the other person. Further, no recovery of any tax due from a taxpayer shall be made if the said taxpayer has filed an appeal, subject to the condition that twenty-five per cent of the amount of tax due has been paid by the taxpayer. Section 76A A new Section 76A has been inserted, to empower PRA, with approval of Government, to restrain any other regulatory authority from renewing or granting any license/ permission to a person, to engage in a taxable economic activity, unless he obtains registration under the Act. Section 78 Section 78 has been amended to specify that notices and show-cause notices may be sent electronically. In the context of powers available with the PRA for condonation of time limits, an ‘explanation’ has been added that such powers are also available for the officers of the PRA as well. Second Schedules

Serial No. 6 – Telecommunication Services The following new services have been added in second schedule and now taxable at the rate of 19.5%:

1. Internet services, 2. Email services, data communication 3. Network services (DCNS) 4. Value added data services; 5. International leased lines or bandwidth

services

However, exemption has been restricted to Rs. 1,500 per month per student availing these services. Serial No. 14 – Construction Services The presently applicable rate of 16% on construction services’ has been reduced to 5%. Such reduced rate, however, shall be applicable without any input tax adjustment. Further, tax rate on construction services, rendered in respect of Federal/ Provincial Governments civil work projects including those of Cantonment Boards and funded through foreign loans, Public Sector Development Program of Federal Govt. or Annual Development Plan of the Punjab Govt. has been reduced as under:

A. Zero percent for projects launched prior to Financial Year 2016-17 and where negotiations were finalized as on 1st July 2016

B. One percent for projects launched during

Financial Year 2016-17 and where negotiations were finalized after 1st July 2016

Serial No. 16 – Contractual Execution Presently, the Contractual execution of works upto Rs 50 million was exempt. However, these services are taxable without any threshold

25

KHYBER PAKHTUNKHWA PROVINCIAL FINANCE ACT 2017 Urban Immovable Property Tax

Substantial increase in rates of property tax for residential properties has been made by substituting the Annexure II in its entirety. Summary of changes is as follows:

S. No. Description Increase %

1. Up to 5 Marlas (Other than self occupied) 44 to 100

2. Exceeding 5 marlas but not exceeding 10 Marlas 40 to 100

3. Exceeding 10 Marlas but not exceeding 15 Marlas 45 to 100

4. Exceeding 15 Marlas but not exceeding 18 Marlas 33 to 100

5. Exceeding 18 Marlas but not exceeding 20 Marlas 50 to 100

6. Exceeding 20 Marlas but not exceeding 30 Marlas 50 to 100

7. Exceeding 30 Marlas but not exceeding 40 Marlas 50 to 100

8. Exceeding 40 Marlas 50 to 100

However, for commercial properties increase in property tax is made only for properties used for Petrol Pumps, CNG stations and services stations for vehicles.

For Petrol pumps and CNG Stations with convenience store property tax has been enhanced from Rs. 15,000 to Rs. 22,500 whereas for Petrol pumps and CNG Stations without convenience store property tax has been enhanced from Rs. 7,500 to Rs. 11,250.

Property tax of service stations has been enhanced from Rs. 15,000 to Rs. 20,000.

Amendment in List of Sales Taxable Services

Scope of services related to facilities for travel has been enhanced by including “Ride hailing services” in the list of services on whom levy of sales tax would be notified by the Provincial Government through a notification.

Professional Tax

Professional tax rates have been adjusted for Companies with increase for Companies having paid up capital and reserves upto Rs. 50 million and reduction for Companies with paid up capital and reserves between Rs. 50 million to Rs. 200 million in the preceding years.

Professional tax rate scope has been widened and various trades which were not previously taxed separately have been specifically mentioned in the Finance Act which include dentists, wholesale dealers, agency holders, chemists, druggist, medical stores and tailor shops.

Furthermore, tax rates have been enhanced for non-specialist doctors “including medical practitioners, hakeem’s, homeopaths etc.”, Diagnostics and therapeutic Centers” including pathologic and chemical laboratories”, Petrol/Diesel/CNG establishments “including video shops, real estate shops/agencies, card dealers and net cafes” and Vehicles Service Stations.

filling stations, all

![Volunteer Income Tax Assistance “VITA” Earned Income Tax ... · Volunteer Income Tax Assistance “VITA” Earned Income Tax Credit “EITC” Revised 1/28/19 [DOCUMENT TITLE]](https://img.pdfslide.net/doc/110x75/5fa5a5c85aa0bb13122ce462/volunteer-income-tax-assistance-aoevitaa-earned-income-tax-volunteer-income.jpg)