Embed Size (px)

Citation preview

Philippine ANALYST February 2014

Contents

THE MONTH’S HIGHLIGHTS

WORD FOR WORD

COMMENTARY

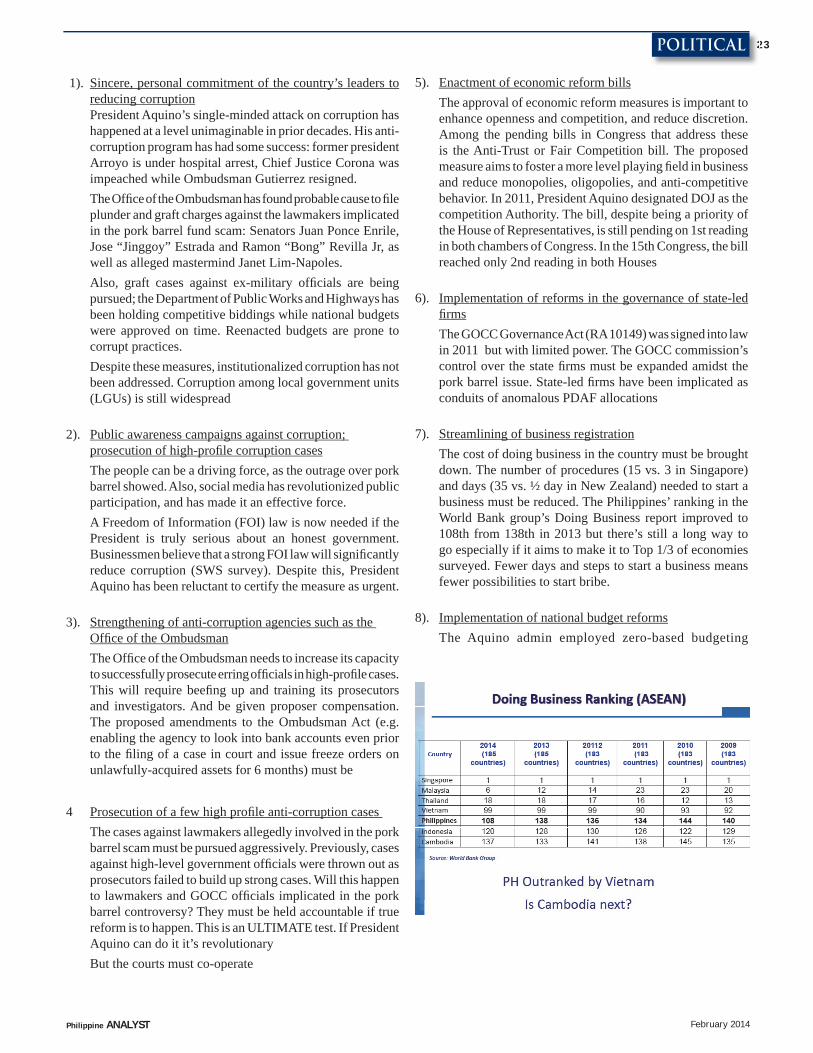

SPECIAL REPORTS

POLITICAL

21 Gov’t, MILF sign fi nal peace pact

22 Philippines’ anti-corruption eff orts still wanting

THE ECONOMY

25 Updated PH Development Plan takes a diff erent tack

26 Joblessness rise in 4th Q, but whole year 2013 results still better than previous year

27 Economists support amendment to economic provisions of the Constitution

PHILIPPINE REGIONAL UPDATE BUSINESS

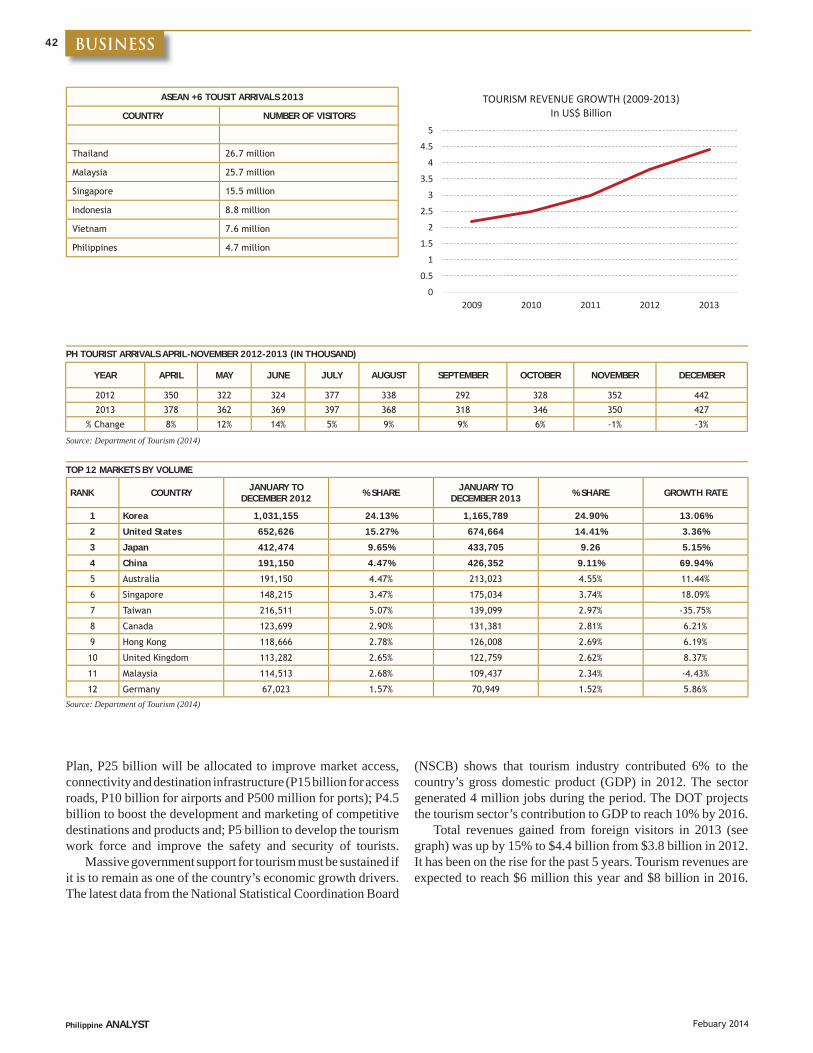

41 PH tourism misses 2013 target

Mining, Oil and Gas

43 Glencore remains committed to Tampakan dev’t

IT Update

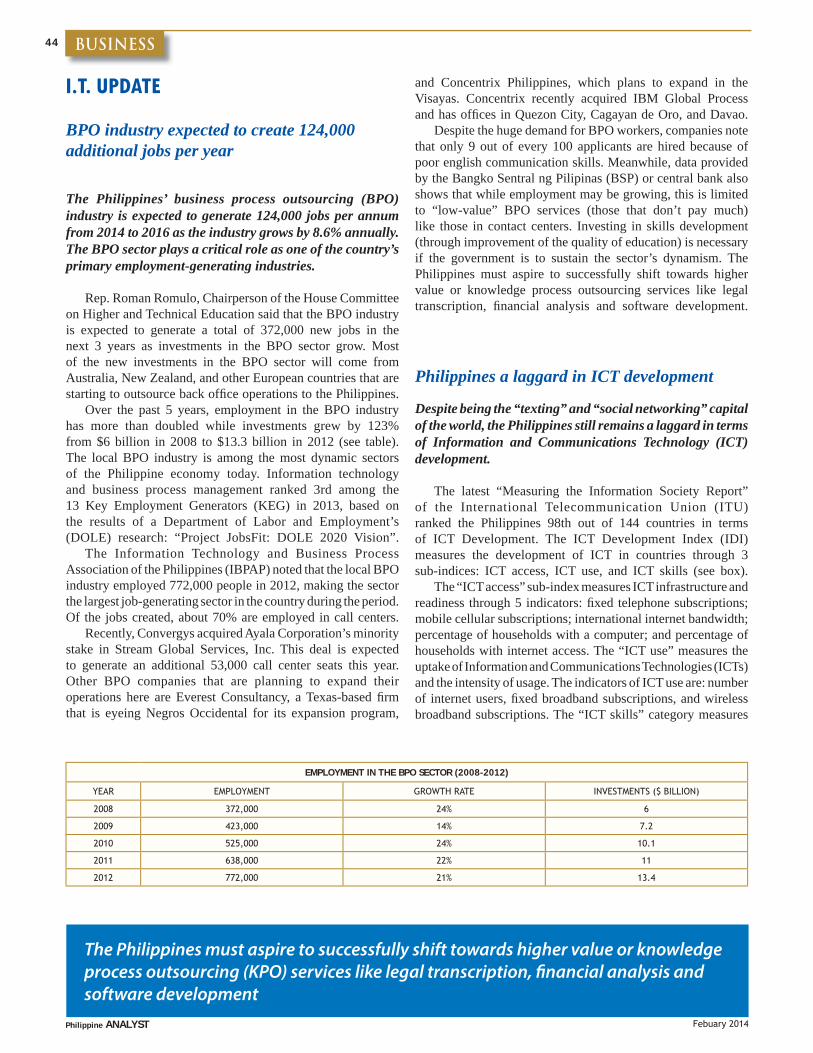

44 BPO industry expected to create 124,000 additional jobs per year

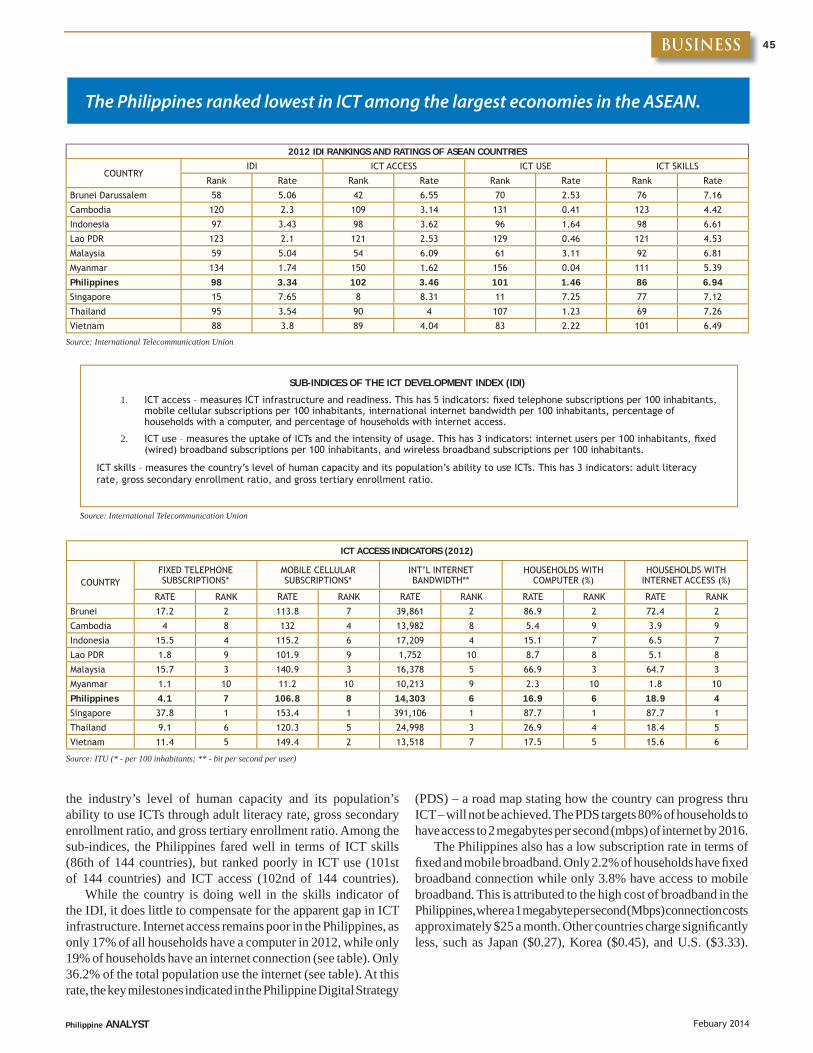

45 Philippines a laggard in ICT development

BUSINESS CLIMATE INDEX

CORPORATE BRIEFS

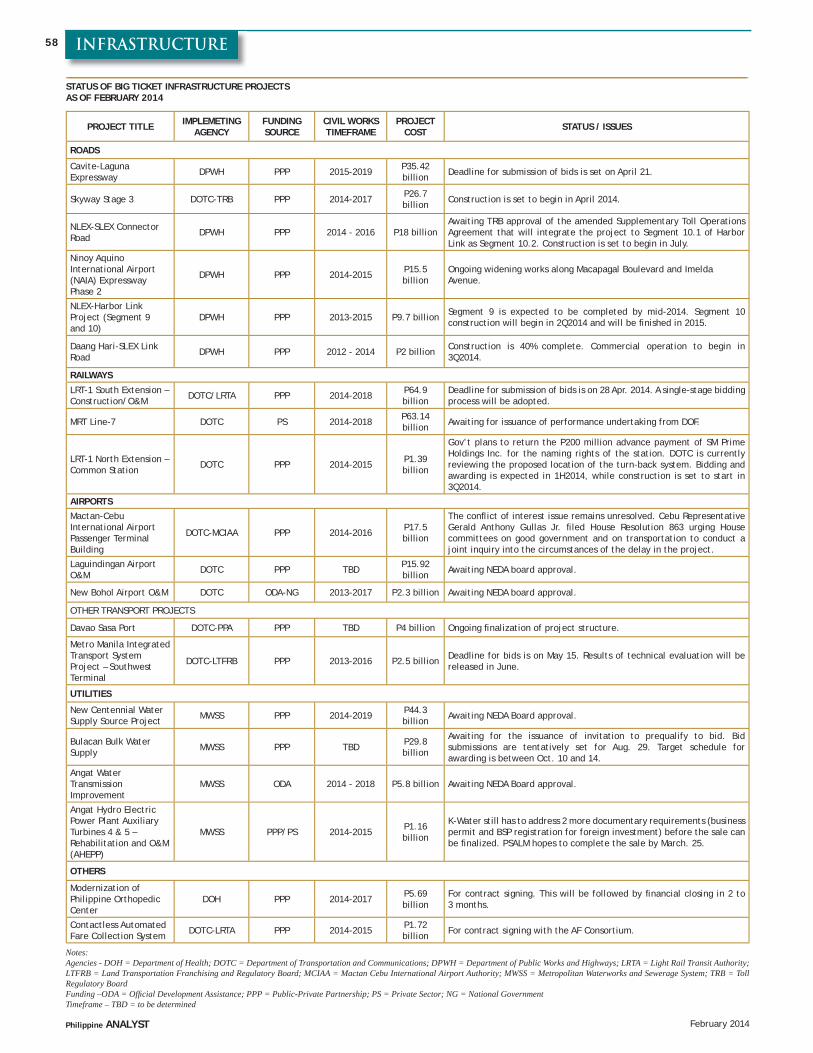

INFRASTRUCTURE

53 DOE says power rate hike due to an ‘artifi cial shortage’ in WESM

54 ERC approved rules on Feed-in-Tariff collection

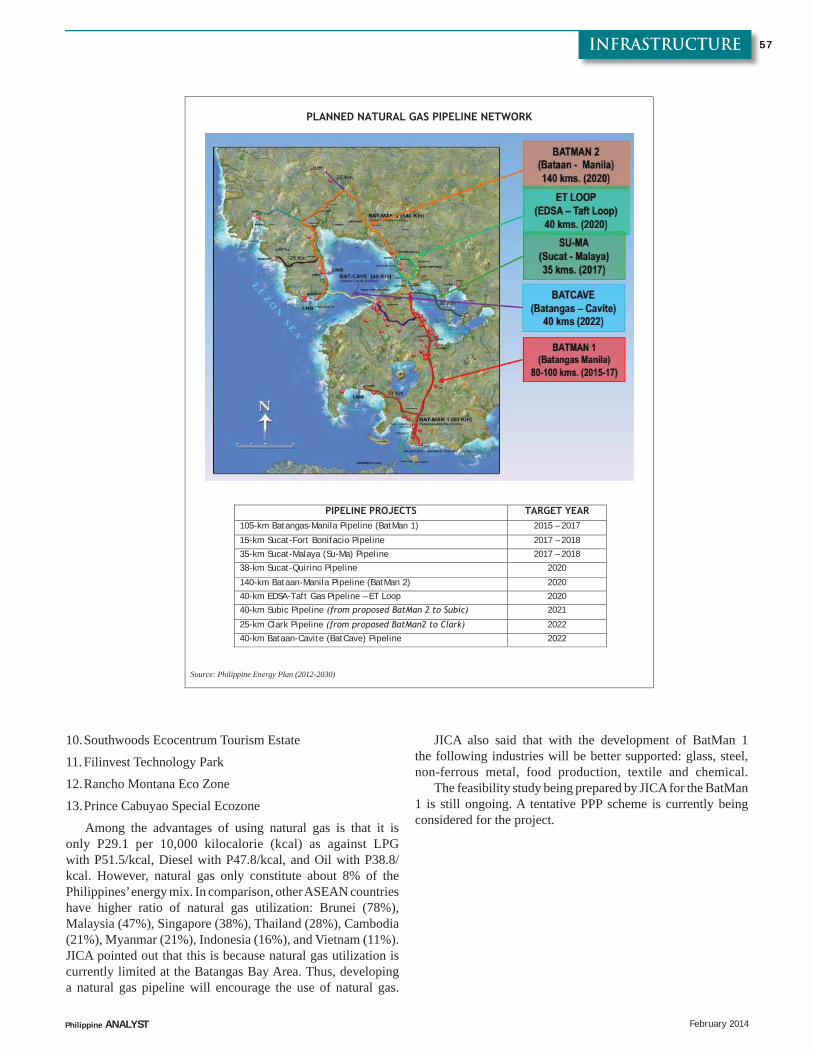

55 DOE eyes natural gas network

CONGRESSWATCH

59 Bill amending Anti-Graft Law fi led in Congress

60 BSP seeks to remove limit on foreign bank entry

61 Asia Pacifi c Executive Brief79 Asia Brief contributors

PUBLISHER: Peter Wallace

EDITOR - Bing Icamina

SENIOR- RESEARCH STAFF:

Joey Roi Bondoc

Francesca Rey

Steven Baria

Vanni Bertillo

Samantha Castro

Rachel Rodica

PRODUCTION–LAYOUT

Larry Sagun

Efs Salita

To read Philippine ANALYST online, go to http://www.wallacebusinessforum.com

For information, send an email to [email protected] or [email protected]

For publications, visit our website: wallacebusinessforum.com

Online

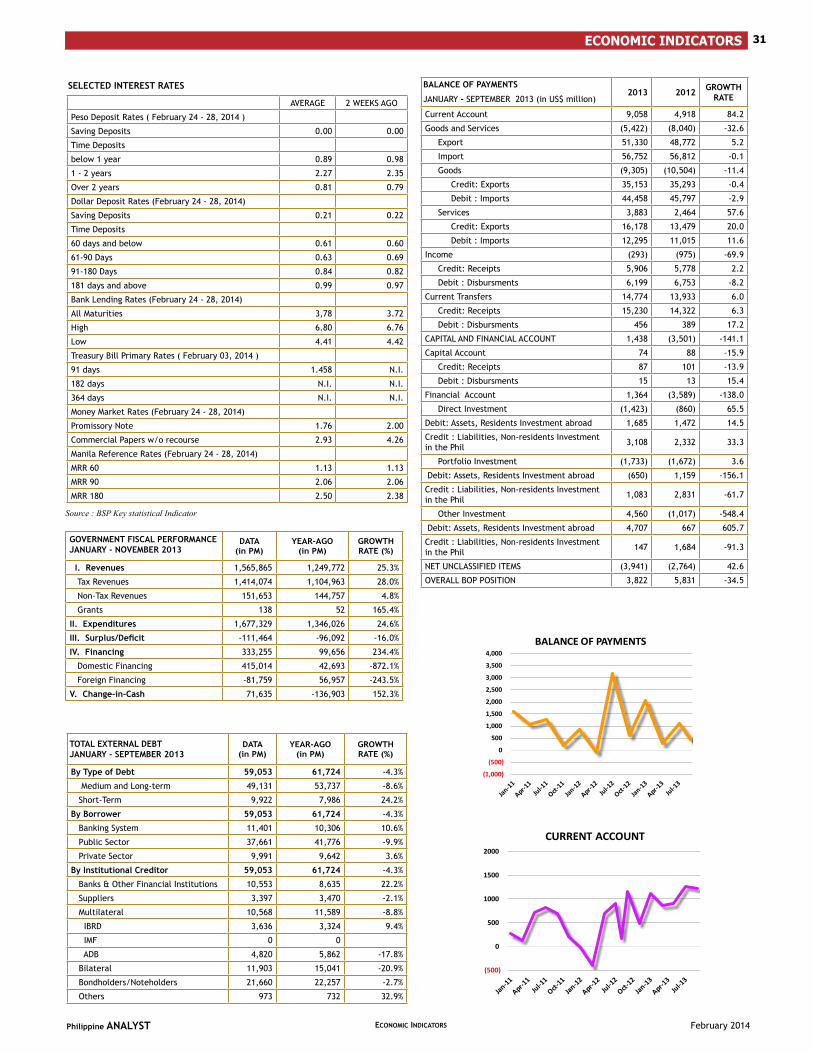

11

18

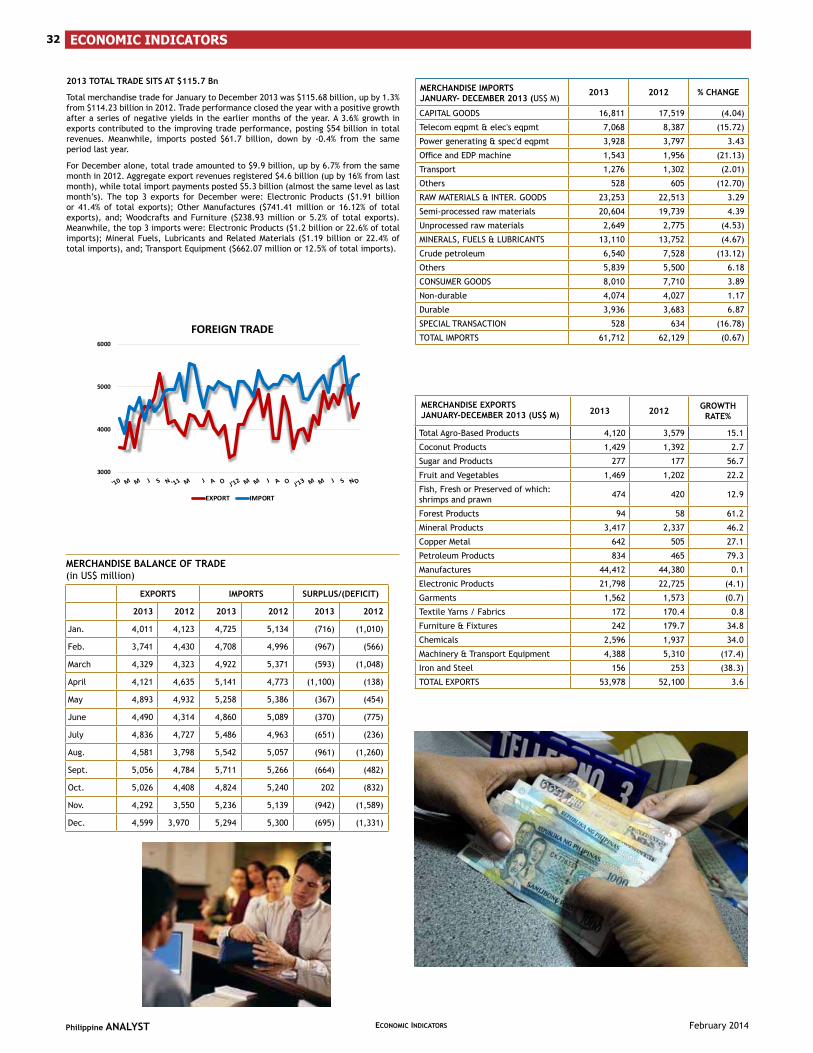

32

55

60

Philippine ANALYST

the month’s highlights 1

February 2014

Political

PAST DEVELOPMENTS

Gov’t, MILF sign fi nal peace pact The signing of the Comprehensive Agreement on the Bangsamoro (CAB) comes after 17 years of negotiations between the Philippine government and the Moro Islamic Liberation Front (MILF). In 1984, the MILF was formed to split away from the main body, the Moro National Liberation Front (MNLF), as they did not agree with the conditions of the Tripoli Agreement that provided merely “nominal autonomy for the Bangsamoro” as they saw it. The breakaway group was formed by members who were disgruntled over what they thought was the MNLF’s departure from its religious roots, its secularist mindset, and surrendering of demands for autonomy.(see story page on p21)

Philippines’ anti-corruption eff orts still wantingThe Philippines’ ranking in Transparency International’s (TI) Corruption Perceptions Index (CPI) has been improving under the Aquino administration. However, much remains to be done if the Philippines is to achieve its goal of breaking into the top one-third of all economies surveyed.(see story page on p22)

Economy

PAST DEVELOPMENTS

Updated PH Development Plan takes a diff erent tackSocio-economic Planning Secretary and National Economic and Development Authority (NEDA) Director General Arsenio Balisacan unveiled the Updated Philippine Development Plan covering the remaining 3 years of the original Plan, or 2014-2016, which stresses the urgency of addressing poverty and raising private investment in the most productive sectors – areas where the economy failed despite its rapid growth during the past 3 years. (see story page on p25)

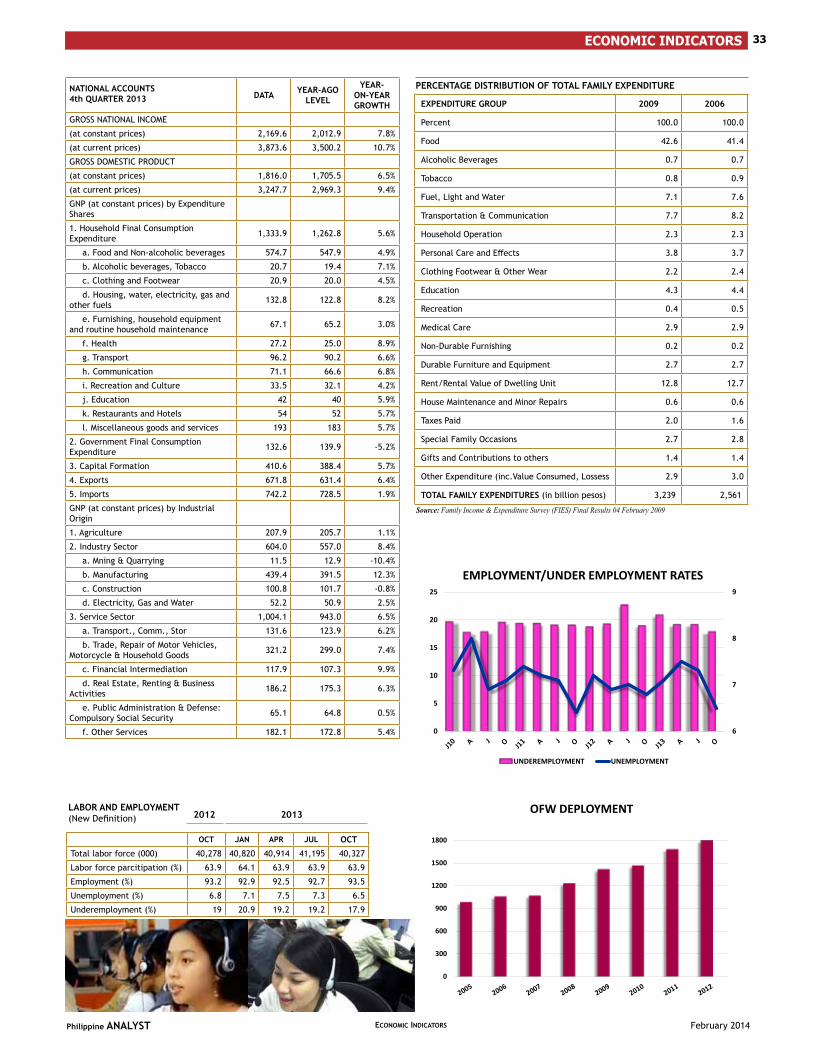

Joblessness rise in 4th Q, but whole year 2013 results still better than previous year The number of jobless adults reached 12.1 million (27.5% of the adult labor force) in December (4th quarter) 2013 from 9.6 million (21.7%) in September (3rd quarter), the Fourth Quarter 2013 Social Weather Survey of the Social Weather Stations (SWS) disclosed. It was also worse than the 10.1 million (24.6%) recorded in 4Q12. (see story page on p26)

Economists support amendment to economic provisions of the ConstitutionThe Foundation for Economic Freedom (FEF) has expressed its support to the proposal in the House of Representatives to amend the economic provisions of the Constitution by inserting the phrase “unless provided by law” to the foreign ownership restrictions in the Constitution in public utilities, land, mass media and advertising, educational institutions, and development of natural resources.(see story page on p27)

Business

PAST DEVELOPMENTS

PH tourism misses 2013 targetThe country failed to meet its tourist arrival target for 2013. Despite this, the Tourism department is still optimistic that the Philippines will achieve its target of 10 million international tourists by 2016. The Philippines is trumped by its ASEAN neighbors in terms of tourist arrivals. Massive government support for the sector must be sustained if it is to remain as one of the country’s primary revenue and job generating sectors.(see story page on p41)

Mining, Oil and Gas

Glencore remains committed to Tampakan dev’tSagitarrius Mines, Inc. (SMI), the operator of the $6 billion Tampakan copper-gold project, said its major shareholder Glencore Xstrata is still committed to the development of the mine despite an earlier report that it is pulling out from the project. (see story page on p43)

IT Update

BPO industry expected to create 124,000 additional jobs per year The Philippines’ business process outsourcing (BPO) industry is expected to generate 124,000 jobs per annum from 2014 to 2016 as the industry grows by 8.6% annually. The BPO sector plays a critical role as one of the country’s primary employment-generating industries. (see story page on p44)

Philippines a laggard in ICT developmentDespite being the “texting” and “social networking” capital of the world, the Philippines still remains a laggard in terms of Information and Communications Technology (ICT) development.(see story page on p45)

Infrastructure

PAST DEVELOPMENTS

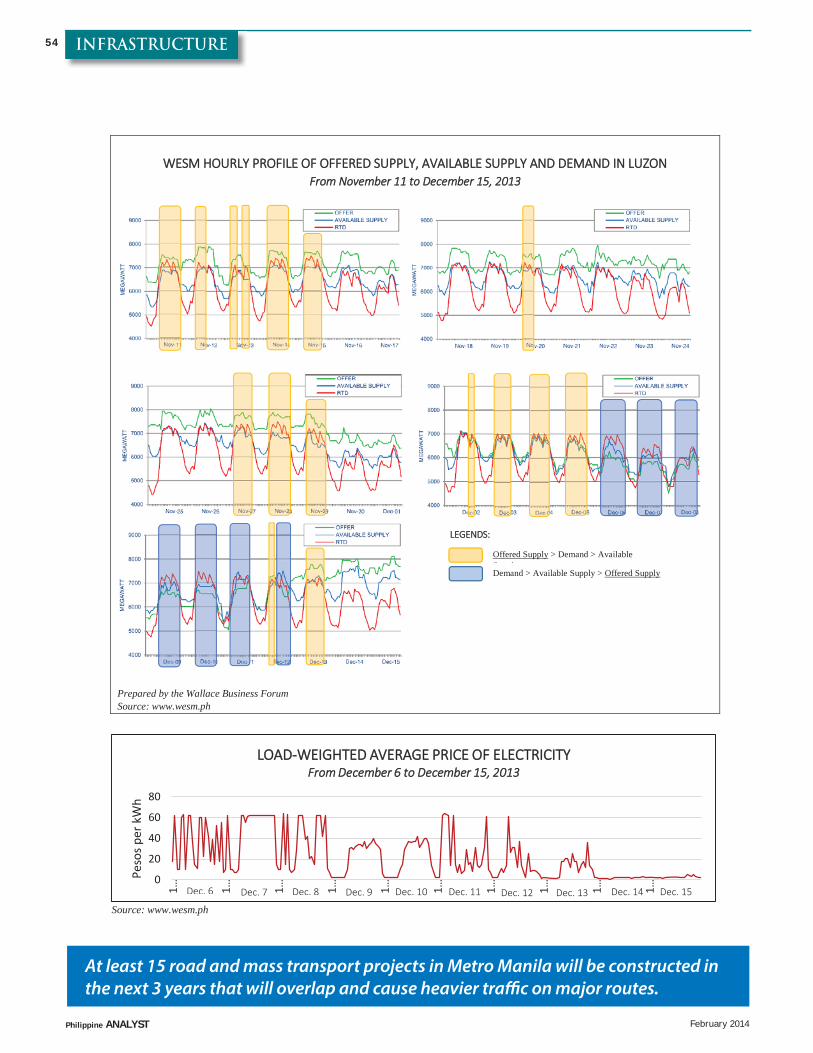

DOE says power rate hike due to an ‘artifi cial shortage’ in WESMThe energy department released a report on the power rate hike in December stating that an “artifi cial shortage” in power supply caused prices at the electricity spot market to rise during the 1-month maintenance shutdown of the Malampaya natural gas platform. The department has indicated that the shortage may have been the result of a violation of spot market rules or an outdated data on the actual capacity of listed power plants. (see story page on p53)

the month’s highlights 2

February 2014Philippine ANALYST

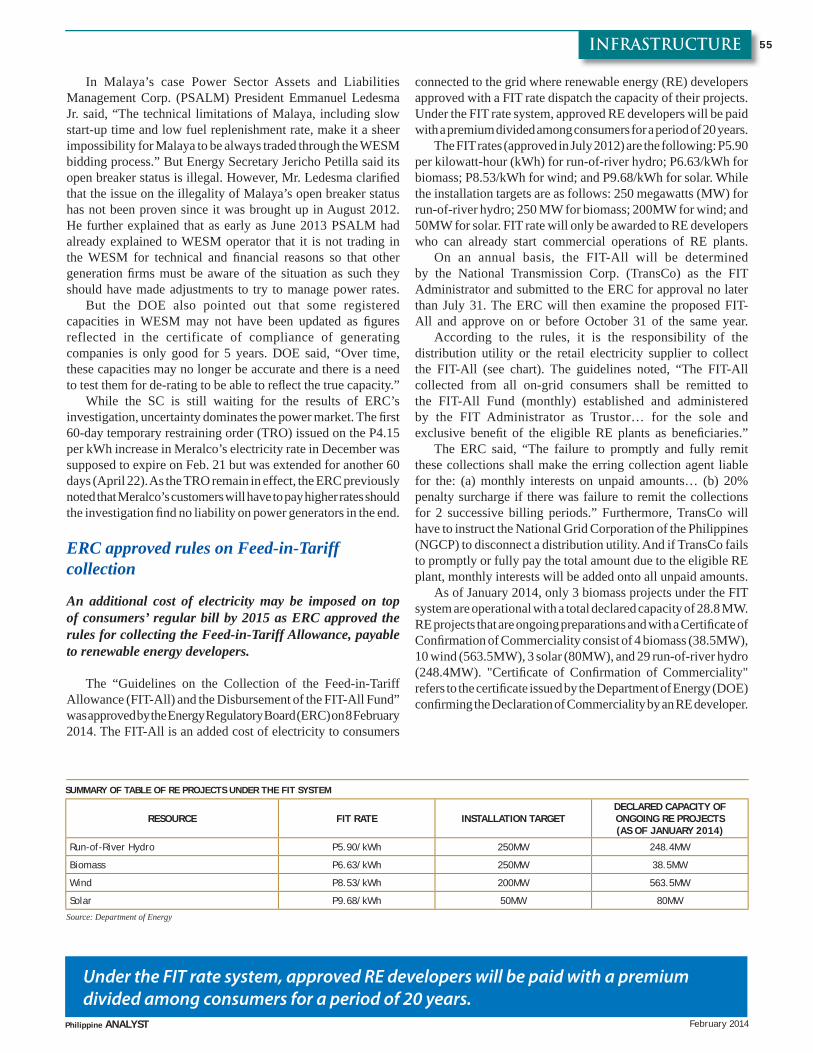

ERC approved rules on Feed-in-Tariff collectionAn additional cost of electricity may be imposed on top of consumers’ regular bill by 2015 as ERC approved the rules for collecting the Feed-in-Tariff Allowance, payable to renewable energy developers. (see story page on p54)

FUTURE DEVELOPMENTS

DOE eyes natural gas networkThe energy department is eyeing to build a natural gas pipeline network to increase utilization of natural gas in Metro Manila.(see story page on p55)

CongressWatch

Bill amending Anti-Graft Law fi led in CongressSenate President Franklin M. Drilon and Senator Aquilino “Koko” Pimentel III have endorsed a bill that aims to decongest the clogged dockets of the country’s anti-graft court, the Sandiganbayan. (see story page on p59)

BSP seeks to remove limit on foreign bank entryThe Bangko Sentral ng Pilipinas (central bank) said it will endorse a bill to Congress that will remove the limit on the number of foreign banks that may enter the country. The liberalization aims to attract more investments into the Philippines and is also in line with the ASEAN economic integration in 2015. (see story page on p60)

CORPORATE BRIEFS 3

February 2014Philippine ANALYST

“We never had an Internet [or] onIine libel. The position of the DOJ has been very consistent: Online libel is not needed. Cybercrime prevention has to do with core cybercrimes. What are these? Hacking, phishing, using it for child pornography. Those are the bigger cases, so that’s where we must divert our attention and resources,” DOJ Assistant Secretary Geronimo Sy in saying that online libel is unnecessary, given that it is still covered by libel penal provisions in the Revised Penal Code.

“We remain mindful of the potential challenges that may hamper our progress this year, especially with respect to providing quality education to Filipino students. The 2014 National Budget considers these possible setbacks—such as typhoons and calamities—so that emergencies don’t endanger our broader goal of establishing a robust public education system,”

Budget secretary Butch Abad on the need to prioritize public education funding in the 2014 national budget

“I hope they are able to show why the Constitution, the bedrock of our laws, should be amended. There will be disruption in the short term. Is the disruption worth the anticipated benefi ts?”

President Benigno Aquino III saying that proponents of the Charter change should demonstrate the “positive benefi ts” of amending the supposed restrictive economic provisions.

COMMENTARY

Philippine ANALYST

COMMENTARY4

February 2014

CCOOMMMMEENNTTAARRYYCOMMENTARY

Idon’t know what it takes to get politicians to recognize reality, they just seem incapable of taking their rose colored glasses off . The Philippines is NOT attracting foreign investment, that’s the factual reality. If you recognize that you react diff erently to how you would if you think all is going well. And going well is

what the President is told. With extreme reluctance the government is only now beginning to recognize that the impressive growth—the second best in Asia they crow—hasn’t created enough jobs, hasn’t lifted people out of poverty. The President was “surprised” that the growth hadn’t trickled down and called a far too rare all day cabinet meeting to fi nd out why— 3 years after he should have.

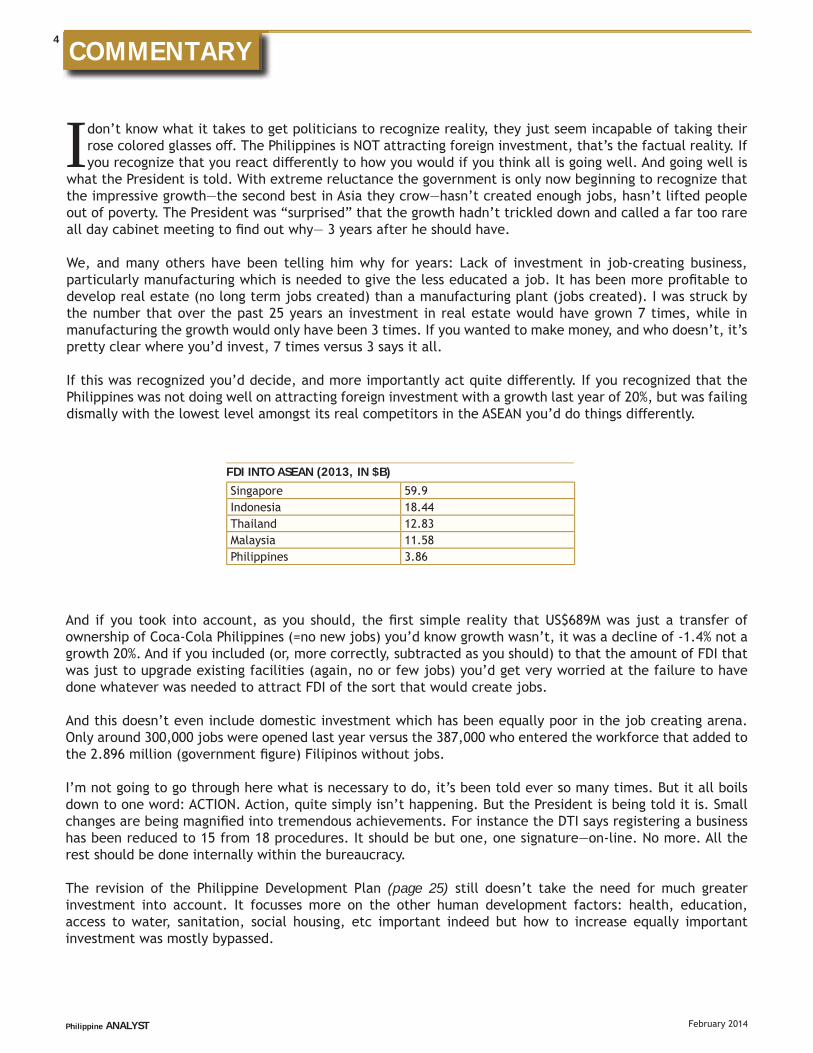

We, and many others have been telling him why for years: Lack of investment in job-creating business, particularly manufacturing which is needed to give the less educated a job. It has been more profi table to develop real estate (no long term jobs created) than a manufacturing plant (jobs created). I was struck by the number that over the past 25 years an investment in real estate would have grown 7 times, while in manufacturing the growth would only have been 3 times. If you wanted to make money, and who doesn’t, it’s pretty clear where you’d invest, 7 times versus 3 says it all.

If this was recognized you’d decide, and more importantly act quite diff erently. If you recognized that the Philippines was not doing well on attracting foreign investment with a growth last year of 20%, but was failing dismally with the lowest level amongst its real competitors in the ASEAN you’d do things diff erently.

And if you took into account, as you should, the fi rst simple reality that US$689M was just a transfer of ownership of Coca-Cola Philippines (=no new jobs) you’d know growth wasn’t, it was a decline of -1.4% not a growth 20%. And if you included (or, more correctly, subtracted as you should) to that the amount of FDI that was just to upgrade existing facilities (again, no or few jobs) you’d get very worried at the failure to have done whatever was needed to attract FDI of the sort that would create jobs.

And this doesn’t even include domestic investment which has been equally poor in the job creating arena. Only around 300,000 jobs were opened last year versus the 387,000 who entered the workforce that added to the 2.896 million (government fi gure) Filipinos without jobs.

I’m not going to go through here what is necessary to do, it’s been told ever so many times. But it all boils down to one word: ACTION. Action, quite simply isn’t happening. But the President is being told it is. Small changes are being magnifi ed into tremendous achievements. For instance the DTI says registering a business has been reduced to 15 from 18 procedures. It should be but one, one signature—on-line. No more. All the rest should be done internally within the bureaucracy.

The revision of the Philippine Development Plan (page 25) still doesn’t take the need for much greater investment into account. It focusses more on the other human development factors: health, education, access to water, sanitation, social housing, etc important indeed but how to increase equally important investment was mostly bypassed.

Singapore 59.9Indonesia 18.44Thailand 12.83Malaysia 11.58Philippines 3.86

FDI INTO ASEAN (2013, IN $B)

Philippine ANALYST

COMMENTARY 5

February 2014

The Plan’s success will be measured in terms of effi ciency and eff ectiveness. Effi ciency is its ability to steer private activity into the direction laid out in the Plan. Eff ectiveness is the extent in which quality of life is improved. Quality of life needs a job, that will be the real measure of success of the plan. Even on paper it doesn’t look too good for the success needed.

****

The fi ght to change the constitution to further open up the economy is growing, and I sense the President’s opposition is softening. But there’ll still be much opposition, much controversy with the simple solution of adding “unless otherwise provided by law” opposed on the grounds it gives lawmakers too much power and could lead to capricious change under a diff erent administration in the future, even change that further restricts instead of opening up. And it could as change would not be constrained by a general policy/philosophy statement as a constitution would normally provide. This is a defi nite theoretical weakness of this approach, but I think in actual practice would not arise.

It becomes a “compromise constitution”, not a good thing, but better than leaving it as is. Making the more fundamental and better change of replacing all the specifi c strictures with a general policy would need the active leadership of Aquino. Something unlikely as it now stands.

The other opposition will be the usual emotional stuff based on a misunderstanding of nationalism and what “Filipino First” really means. Myopia will interpret it as what’s best for the Filipino businessman, not what’s best for the Filipino consumer and job seeker.

This is where time will be eaten up. This is where getting it through in the next year, or so is diffi cult. But the swift passage in the House so far, it’s already gone to plenary debate, gives some hope it just might pass early. Coincident with the mid-2016 elections is when a plebiscite could be most expected. Then, of course, the phrases in the constitution will have to be amended by law. That will add another year or three.

The next 6 months should defi ne the likelihood more clearly. Surprisingly, we’re hopeful (a word I promised myself never to use when discussing the Philippines).

SPECIAL REPORT6

February 2014Philippine ANALYST

Cons tu onal Change Isn’t Only Desirable,

It’s Essen al:

It IS Time to Change the Cons tu on

Inclusive growth is the new buzz phrase, but it’s too general. What does it mean? I prefer “jobs focus”, it more specifi cally says what is needed over and above almost everything else: Jobs. Over the past 13 years (since 2000) the economy measured by real gross domes c product (GDP) has grown cumula vely 63%. However, instead of a

similar growth in jobs created not only was there no growth, there was actually a decline. Using the same defi ni on of unemployment (it was changed in 2005) which for comparison you must do, the number of jobless Filipinos rose to an es mated 4.2 million from 3.5 million in 2000, which translates to some 700,000 more without work today. And these are government fi gures which I believe are grossly understated, par cularly if you consider that many of the so-called jobs are unpaid (helping dad on the farm) or grossly underpaid. Whatever it is, it’s unacceptably high, and ge ng worse. A more believable Social Weather Sta ons says that there are 12.1 million unemployed Filipinos as of end-2013, this is much higher compared to 9.9 million without a job in November 2010. The country’s unemployment situa on is worsening because there aren’t enough businessmen expanding or building new businesses.

Many things need to be done to fi x this state of aff airs and they have been discussed endlessly—with far too li le eff ort to correct them. But the one I wish to focus on here is the cons tu on, because if the restric ons on foreign investment are removed it WILL lead to more jobs created. There is inescapable logic to this. If CNN puts an offi ce in Manila it hires people. But more importantly it puts more focus on the Philippines so other foreign companies take interest, and end up inves ng thus crea ng more jobs. This cycle occurs with all investments. The mul plier eff ects to the local economy are realized. If a foreign construc on fi rm wins a government project it not only hires workers it needs caterers for the food, suppliers of materials and equipment and so on where more jobs are created too. Not only in businesses that come into those once closed sectors, but into many other sectors as the world takes no ce of a country that is now vastly diff erent, is open and welcoming. Foreign companies now decide to come and look where before they were preferring elsewhere.

Opening up will get the CNN and the BBC to take no ce: “In this world of controversy and turmoil today here is a country, the Philippines, that is proving its stability and confi dence in itself by opening up to the world. A true democracy with fair labor laws and a talented people, it must be on your list of places to look at as you expand or relocate your business.”

A MORE OPEN ECONOMY WILL PROVIDE JOBS

SPECIAL REPORT 7

February 2014Philippine ANALYST

There’s a huge inequality that exists today—79% of the popula on belong to the low-income group, while only 5% is in the high-income group, and the middle class is way too small at only 16%—that badly and urgently needs leveling. This can only be done through job crea on and good, well-paying jobs; there is no other way. And everything that will help create jobs must be done. It’s no good saying things are going well so we don’t need further change because even if it were only 100 people without a job it’s 100 people who shouldn’t be. And when the fact is that there are more jobless people today than 10 years ago, than 3 years ago everything that can create jobs must be tried. If opening the economy through cons tu onal change will only create a few thousand jobs, that’s a few thousand jobs, but I believe based on evidence elsewhere it will be hundreds of thousands of jobs, possibly millions.

JOB CREATION IS THE ONLY WAY TO SOLVE POVERTY.

President Aquino seemed to have recognized the need to create jobs when he said he wants to create a Daang Matuwid (straight path) where the economy is opened up, expanded, jobs created in a fair and honest manner. As we’ve seen in the past couple of decades Filipino businessmen have done a great job, however their capital is limited, the amount they can do is limited and too few of them capture too much in several key sectors where wider ownership could provide a more compe ve environment for be er products or services. So I’m at a complete loss to understand the president—if he’s correctly reported—as to why he doesn’t want to review the cons tu on, when it fi ts in with his overall vision.

The president wants proof that foreign investment will benefi t Filipinos. He said: “Then with regards to our cons tu on, it’s important that it serves our interest, to make sure it serves our interest before the interest of foreigners”. I couldn’t agree more. It has been proven incontrover bly that foreign investment serves the interest of a country’s people more than it does the foreigner. The most drama c example nearby is China. China was a backwater (GDP per capita of $193 in 1980, the Philippines was a much higher $685) un l it opened up to foreign investment. US$2 trillion poured in (the Philippines received a measly $36 billion), it was the trigger to explosive growth, to a GDP per capita today of $7,784 P.A. or a 3,933% increase from the 1980 level. The Philippine GDP per capita grew by only 278% during the comparable period to reach an unacceptably low $2,587.

He added: “Nobody has demonstrated with absolute certainty that if we overhaul the Cons tu on, we’ll have corresponding economic gain,” Nothing is absolutely certain into the future (except death), but example a er example worldwide shows that open economies fare best, their people are be er off in an economy. The odds are very high that opening up the economy further will lead to more rapid growth in the Philippines. Noted, respected Philippine economists all support this change (the Founda on for Economic Freedom has come out openly and strongly in support), businessmen support this change (average of 90%) in three surveys we conducted (15 business chambers, Rotary Club of Maka West, and the Wallace Business Forum members, see Annex A). Congress supports this change, it was the fi rst bill fi led by the Speaker. The communist or le group that is vocal on issues where its stance opposes free market etc. is against it. That must tell you something. Look at the people that support versus those that oppose and decide which side you’d rather be on.

THE PRESIDENT’S REASONS FOR RELUCTANCE1. “The economy is doing well (it is consumption-led, enough jobs aren’t being created)”

2. Investment is pouring in “Prove to me we need it.” (FDI in the past 18 months $3.6B, Vietnam $14.2B).

3. It will distract Congress from passing laws

• It won’t, diff erent committee

• This is of equal or higher importance than most proposed laws.

• We have enough laws

4. Congress will open it up to change in the political structure

• He can control Congress

• The public can oppose it through an active internet (social media)

• A parliamentary system would be better anyway

SPECIAL REPORT8

February 2014Philippine ANALYST

OVER 80% OF BUSINESSMEN WANT AN OPEN CONSTITUTION

As the members of the highly respected Founda on for Economic Freedom (FEF) said: “We want our growth transformed from a consump on-driven one to an investment-driven one because only an investment-driven growth will grow jobs and reduce unemployment, increase produc ve capacity, improve compe veness, and put the country on a higher plane of sustainable growth,” They went on to say: “Timing is right because [Aquino] enjoys a high trust ra ng and there’s no fear he will use Cha-Cha to extend his power,” “Moreover, globaliza on has made liberalizing economic provisions in the Cons tu on more obvious and urgent.” And this is a point the President may have missed. The high GDP growth is not because of produc ve, job-crea ng ac vi es, but consump on. Consumer spending accounts for more than two thirds of Philippine GDP. That is not a sound base for an economy. In the three years Mr. Aquino has been in power unemployment has risen from 2.8 million in 2010 to 3 million today despite GDP growth breaching the 7% mark in 2010 and averaging 6% from 2010 to 2012. And these are offi cial fi gures, which have redefi ned a large numbers of jobless out of the labor force. Clearly GDP is not a good indicator of the well-being of a people. And it is the well-being of his people that I’m sure he’d be most concerned about.

GDP IS NOT A GOOD INDICATOR OF THE WELL BEING OF A PEOPLE.

Surely if these experts on studying the economy, who are Filipinos that care for their country, think a more open economy is desirable then they should be listened to.

FEF WANTS AN OPEN CONSTITUTION

The President wants facts to prove cons tu onal change is necessary. Well the facts are there, opening up an economy leads to rapid growth. Now it may not have been through cons tu onal change, as in most countries such changes are not needed, it can be done by law or execu ve fi at, but in the Philippines it is. Which in itself tells you the need to change the cons tu on—it’s out of step with other democracies. The cons tu on is restric ng FDI infl ows. There are other factors too to be addressed, oh most are being, but too slowly. And that’s the point, opening up the cons tu on is not a magic wand that solves all, it’s just one important factor amongst several that are necessary in an overall opening up and improving of the economy. But it is an important factor and should not be le out.

In country a er country foreign investment has led to much more rapid growth (look at Singapore and South Korea), and a wider ownership of the growth. Exports increase drama cally as the foreigner creates products for their own market that they know so well.

BENEFITS OF FDI

Quality employment creation

Transfer of technology, skills & know-how

Managerial capacity is enhanced

Infl ow of capital

Wider ownership of sectors

Greater access to world market

SPECIAL REPORT 9

February 2014Philippine ANALYST

SPECIAL REPORT10

February 2014Philippine ANALYST

THE OECD AND UNCTAD HAVE EMPHASIZED THE BENEFITS OF AN OPEN CONSTITUTION

As a well-researched paper says: “The overall benefi ts of FDI for developing countries’ economies are well documented. Given the appropriate host-country policies and a basic level of development, a preponderance of studies shows that FDI triggers technology spillovers, assists human capital forma on, contributes to interna onal trade integra on, helps create a more compe ve business environment and enhances enterprise development. All of these contribute to higher economic growth, which is the most potent tool for allevia ng poverty in developing countries. Moreover, beyond the strictly economic benefi ts, FDI may help improve environmental and social condi ons in the host country by, for example, transferring ‘cleaner’ technologies and leading to more socially responsible corporate policies.” (“Foreign Direct Investment for Development, Maximising Benefi ts, Minimising Costs,” OECD, 2002)

In another por on ci ng the United Na ons Conference on Trade and Development’s Midrand Declara on in 1996, the paper says: “[T]he Philippines expressly supported the proposi on that FDI is a driver of growth. Paragraph 36 of that Declara on states, ‘Foreign direct investment can play a key role in the economic growth and development process. The importance of FDI for development has drama cally increased in recent years. FDI is now considered to be an instrument through which economies are being integrated at the level of produc on into the globalizing world economy by bringing a package of assets, including capital, technology, managerial capaci es and skills, and access to foreign markets. It also s mulates technological capacity-building for produc on, innova on and entrepreneurship within the larger domes c economy through catalyzing backward and forward linkages.”

The paper says further: “Arguing that restric ons on foreign ownership are not a factor in aff ec ng FDI is illogical. If a foreign fi rm faces a nega ve list where investment cannot take place or is very restricted, then of course there can be no or only limited investment in those areas, immediately limi ng the range of prospects. Addi onally, it defi es logic to say that li ing restric ons will not open new doors as those doors are then open.”

There’s been some argument that foreign investment isn’t needed. I haven’t seen any research done that links FDI (Foreign Direct Investment) to economic (measured by GDP) growth, but I don’t think anyone would dispute but that China got rapidly and massively started to rise to number 2 in the world by foreign investment whilst the Philippines has been the slowest growing economy amongst its comparable neighbors, and has a racted the least foreign investment. And has the most foreign ownership restric ons. Surely that alone says it is needed. Or, at the very least is worth the try given the failure to provide enough jobs as the economy is currently structured. What a er all do you have to lose.

SPECIAL REPORT 11

February 2014Philippine ANALYST

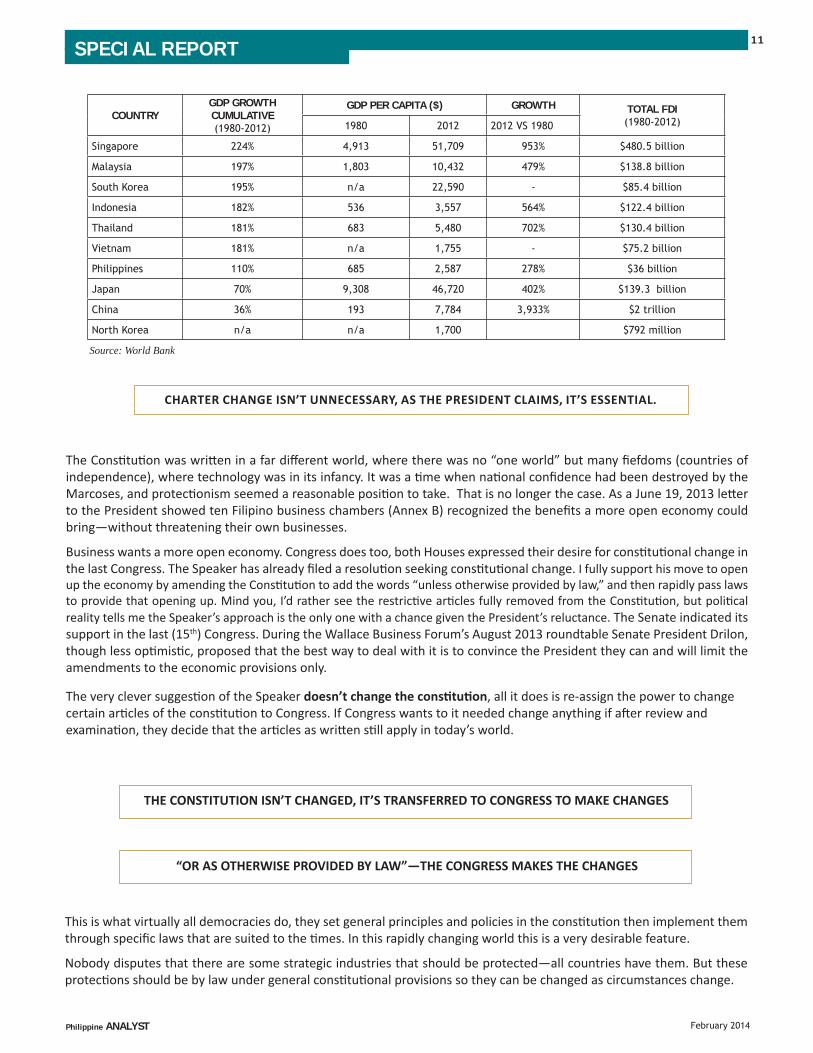

COUNTRYGDP GROWTH CUMULATIVE(1980-2012)

GDP PER CAPITA ($) GROWTH TOTAL FDI(1980-2012)1980 2012 2012 VS 1980

Singapore 224% 4,913 51,709 953% $480.5 billion

Malaysia 197% 1,803 10,432 479% $138.8 billion

South Korea 195% n/a 22,590 - $85.4 billion

Indonesia 182% 536 3,557 564% $122.4 billion

Thailand 181% 683 5,480 702% $130.4 billion

Vietnam 181% n/a 1,755 - $75.2 billion

Philippines 110% 685 2,587 278% $36 billion

Japan 70% 9,308 46,720 402% $139.3 billion

China 36% 193 7,784 3,933% $2 trillion

North Korea n/a n/a 1,700 $792 million

Source: World Bank

CHARTER CHANGE ISN’T UNNECESSARY, AS THE PRESIDENT CLAIMS, IT’S ESSENTIAL.

The Cons tu on was wri en in a far diff erent world, where there was no “one world” but many fi efdoms (countries of independence), where technology was in its infancy. It was a me when na onal confi dence had been destroyed by the Marcoses, and protec onism seemed a reasonable posi on to take. That is no longer the case. As a June 19, 2013 le er to the President showed ten Filipino business chambers (Annex B) recognized the benefi ts a more open economy could bring—without threatening their own businesses.

Business wants a more open economy. Congress does too, both Houses expressed their desire for cons tu onal change in the last Congress. The Speaker has already fi led a resolu on seeking cons tu onal change. I fully support his move to open up the economy by amending the Cons tu on to add the words “unless otherwise provided by law,” and then rapidly pass laws to provide that opening up. Mind you, I’d rather see the restric ve ar cles fully removed from the Cons tu on, but poli cal reality tells me the Speaker’s approach is the only one with a chance given the President’s reluctance. The Senate indicated its support in the last (15th) Congress. During the Wallace Business Forum’s August 2013 roundtable Senate President Drilon, though less op mis c, proposed that the best way to deal with it is to convince the President they can and will limit the amendments to the economic provisions only.

The very clever sugges on of the Speaker doesn’t change the cons tu on, all it does is re-assign the power to change certain ar cles of the cons tu on to Congress. If Congress wants to it needed change anything if a er review and examina on, they decide that the ar cles as wri en s ll apply in today’s world.

THE CONSTITUTION ISN’T CHANGED, IT’S TRANSFERRED TO CONGRESS TO MAKE CHANGES

“OR AS OTHERWISE PROVIDED BY LAW”—THE CONGRESS MAKES THE CHANGES

This is what virtually all democracies do, they set general principles and policies in the cons tu on then implement them through specifi c laws that are suited to the mes. In this rapidly changing world this is a very desirable feature.

Nobody disputes that there are some strategic industries that should be protected—all countries have them. But these protec ons should be by law under general cons tu onal provisions so they can be changed as circumstances change.

SPECIAL REPORT12

February 2014Philippine ANALYST

SECTORS THAT NEED PROTECTION SHOULD BE PROTECTED BY LAW NOT A CONSTITUTION

So we need to amend the Cons tu on. To allow the economic provisions to be overhauled; they’re too inward-looking and out of touch with the 21st-century reality of global interdependence and interrela onships. And they need to adapt to changes in the economic environment—e.g., labor fl exibility, informa on age, etc. As they’re currently wri en, these provisions promote an economic structure that doesn’t refl ect and best use the strengths of the Philippine economy and its people.

THE 1987 CONSTITUTION DOESN’T BEST USE THE STRENGTHS OF THE ECONOMY AND ITS PEOPLE.

The one fundamental change I’d like to see is: GET RID OF THE SPECIFICS. The Cons tu on is the fundamental document of the land and should set the general policies and philosophies of the country; the details should be defi ned by law that can change as the world changes. The economic clauses in the present Cons tu on are far too detailed and restric ve as to belong in a Cons tu on. Today there are no (economic) borders in the world, except as arbitrarily dictated by a country’s leaders. Or, in our case, by an overly restric ve Cons tu on. The Cons tu on should establish the general principles and grand objec ves that a na on should strive for in a general way that can withstand the passage of me. Congress can then pass laws that can be changed as the world changes. As the needs of the people change. And both are changing rapidly in today’s modern technological world.

THE CONSTITUTION SHOULD ESTABLISH THE GENERAL PRINCIPLES AND GRAND OBJECTIVES

I believe the current economic provisions are one of the root causes of our economic problems. These restric ve provisions have essen ally shaped the country’s inward-looking and “na onalis c” economic policies for decades. They are major barriers to economic progress as they have made doing business here costly and limited. And led to regulatory capture by too few companies in some sectors. Foreign capital is needed to spur business, bring in new technology, provide healthy compe on, generate jobs, provide income, and ul mately li many Filipinos from poverty.

We need massive job crea on. Strictly Philippine investment just can’t do it, that’s a proven fact as more Filipinos without a job today than a decade ago shows. We need to revive the manufacturing sector to create many of the jobs. Domes c demand for products won’t do it, we must interna onalize.

CONSTITUTIONAL REFORMS

Economic Provisions of the Constitution need to be overhauled.

They’re too inward-looking and out of touch with the 21st century reality of global interdependence

They need to adapt to changes in the economic environment, e.g., labor fl exibility, information age, etc.

They promote an economic structure that doesn’t best utilize the strengths of the RP economy

The Constitution should set the general policy/philosophy

Law should defi ne the specifi c limits.

SPECIAL REPORT 13

February 2014Philippine ANALYST

SPECIAL REPORT14

February 2014Philippine ANALYST

WE NEED GREATER COMPETITION, WIDER OWNERSHIP OF PUBLIC UTILITIES.

Building of public services can expand much, much more rapidly as more companies become available to provide them. One of my clients would like to help computerize government services (a growing essen al) as they have the exper se and experience of elsewhere, but they can’t because they can’t fi nd a 60% partner. A partner they don’t need, except the cons tu on mandates it.

One argument raised against opening up is the fear that if you allow foreigners to control businesses they’ll dominate them, and take all their profi ts out. They’ll gouge the country for their own gain. Not true. The fi gures from the Business World Top 1,000 Corpora ons show that in the last two to three years, mul na onal companies (MNCs) have made an average of about P80 billion annually in profi t, but Central Bank fi gures show that only 30-40 percent of it was remi ed overseas during that period. The rest was ploughed back into expansion — crea ng more jobs for Filipinos.

MNC’S RE-INVEST 60-70% OF THEIR EARNINGS BACK INTO THE COUNTRY.

PROTECTIONIST ECONOMIES QUITE SIMPLY DON’T WORK.

MNCs employ an es mated 1 million Filipinos directly, many, many more when you add the jobs they provide for subcontractors, suppliers, distributors, dealers, retailers, etc. In the BPO sector alone the entry and expansion of more US-based and European-based call centers and other services over the next few years could lead to direct employment by MNCs of up to 2 million Filipinos. And they pay at least 30 percent more than do most local companies.

Over 10 million Filipinos have had to leave their families, separate from their spouses to seek a living overseas. In many, many of those cases that living overseas is working for a foreign company. Wouldn’t it be far, far be er (and kinder to the family) to bring the companies here?

Protec onist economies quite simply don’t work, and I challenge those who think they do to give me some examples. I’ll give them just one to make my point: Korea. Open South Korea is one of the world’s most dynamic countries with a per capita GDP of $22,590. While protec onist North Korea is one of the world’s unmi gated disasters. No one knows its per capita GDP, or even if it has one. Some guess mates place North Korea’s GDP per head at $1,700 only. But it’s the same people, with the same ethnic background. South Korea a racted US$56 billion in FDI’s from 2000 to 2012. North Korea started allowing foreign investment in the mid-1980’s, but retained most of its restric ve policies. Despite opening up selected sectors to FDIs, the country of some 24 million people failed to a ract any major investment. According to World Bank, NoKor a racted a measly $560M from 2000 to 2012, accoun ng for a paltry 1% of South Korea’s FDIs during the period.

There is only one closed economy in the world today, North Korea the rest are open or semi-open economies. China is now obviously an open economy, having joined the WTO in 2001. And having taken off drama cally since it opened up. Vietnam is opening up too, and has been compe ng aggressively for FDI’s during the past 5-10 years. In the past 5 it garnered some $39 billion of FDI, the Philippines only one fourth of that at $11 billion.

It will soon overtake the Philippines the way it is going. Which all proves that a closed economy is an archaic concept that, quite simply and provably doesn’t work today.

“Simplifying procedures and providing incen ves” and “keeping a level playing fi eld” with “a determined push for good governance by the na onal leadership…” are indeed needed as the president rightly acknowledges. But they aren’t suffi cient; wider, more drama c change is needed.

SPECIAL REPORT 15

February 2014Philippine ANALYST

OPENING THE ECONOMY BY CONSTITUTIONAL CHANGE WILL GET GLOBAL HEADLINES, FIDDLING WITH LAWS WON’T.

The businessmen of the world need to be jolted into awareness and interest that the Philippines even exists. Fiddling with bits and pieces here and there is too nebulous, too incremental—you don’t no ce the changes. But a sudden: “We have fully opened our economy” brings instant interest. It will get global front page a en on: “Here’s a country worth looking at” that fi ddling with a few laws won’t do. CNN will report some good news on the Philippines for a change. The idea of changing laws to create greater openness won’t work anyway. There are areas where opening up with issuance of a law can’t be done. The cons tu on is very specifi c on what is not allowed, so no law can be created that violates the prohibi on. So to say change can be done “…without the need to amend the 1987 cons tu on” is just not possible.

THE IMF IS A DISINTERESTED THIRD PARTY, IT BELIEVES CONSTITUTIONAL CHANGE IS NEEDED

The IMF Execu ve Board in its report on consulta on with the Philippine government said (and I quote):

“Unemployment is around 6¾ percent—high from a regional perspec ve—and the poverty rate remains stubbornly elevated. The weak investment climate of poor infrastructure, limited compe on due to ght restric ons on foreign investment and concentrated ownership, and con nued red tape and corrup on are seen as contribu ng factors.”

The President is trying to fi ght corrup on (a Herculean task if ever there was one), has doubled the infrastructure budget and given importance to PPP, however reducing red tape is s ll only promised, too li le has actually been done, but at least it’s being a empted. Opening up the economy with cons tu onal change though is s ll being resisted by the President.

The IMF directors went on to say: “To catalyze private investment, directors encouraged the authori es to relax limits on foreign ownership, execute public-private partnership in a transparent manner, and strengthen the medium-term fi scal framework.”

The IMF has nothing to gain by these recommenda ons (there were more good ones, but not relevant to this discussion), it has no vested self-serving interests. It is a genuinely disinterested, impar al, knowledgeable third party. It believes cons tu onal change is necessary for faster and, importantly, wider growth of the economy.

AN OPEN ECONOMY WILL BE NEEDED TO JOIN TPP

In 2011, the broad framework for a Trans-Pacifi c Partnership (TPP) was developed, which aims to build a high-standard, comprehensive and ambi ous agreement that will enhance trade and investment, promote innova on, boost growth and create more jobs in TPP partner countries. Fourteen countries so far are ac ve par cipants in the TPP, including the U.S. and Asian countries specifi cally Brunei, Japan, Malaysia, Singapore and Vietnam. The goal is to further expand membership. Nego a ons on various issues such as compe on, coopera on, E-commerce, labor, cross border and legal issues are making substan al progress as par cipants are eager to conclude an agreement as soon as possible.

For the Philippines to be eligible to par cipate in this grand undertaking that is likely to emerge as the world’s most dynamic economic bloc it must ease foreign ownership restric ons on various areas of investment. The Philippine must belong to this partnership if it is to grow. But it won’t be able to if its cons tu on is not changed and con nues to protect.

SPECIAL REPORT16

February 2014Philippine ANALYST

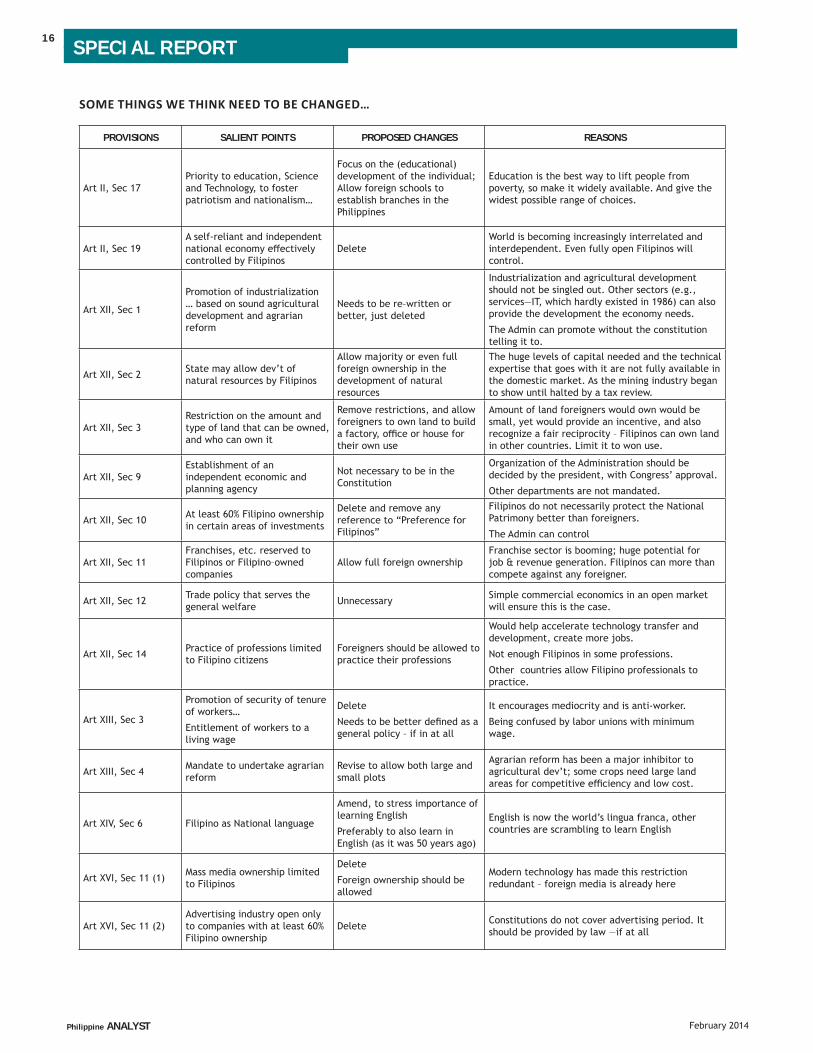

PROVISIONS SALIENT POINTS PROPOSED CHANGES REASONS

Art II, Sec 17Priority to education, Science and Technology, to foster patriotism and nationalism…

Focus on the (educational) development of the individual; Allow foreign schools to establish branches in the Philippines

Education is the best way to lift people from poverty, so make it widely available. And give the widest possible range of choices.

Art II, Sec 19A self-reliant and independent national economy eff ectively controlled by Filipinos

DeleteWorld is becoming increasingly interrelated and interdependent. Even fully open Filipinos will control.

Art XII, Sec 1

Promotion of industrialization … based on sound agricultural development and agrarian reform

Needs to be re–written or better, just deleted

Industrialization and agricultural development should not be singled out. Other sectors (e.g., services—IT, which hardly existed in 1986) can also provide the development the economy needs.

The Admin can promote without the constitution telling it to.

Art XII, Sec 2 State may allow dev’t of natural resources by Filipinos

Allow majority or even full foreign ownership in the development of natural resources

The huge levels of capital needed and the technical expertise that goes with it are not fully available in the domestic market. As the mining industry began to show until halted by a tax review.

Art XII, Sec 3Restriction on the amount and type of land that can be owned, and who can own it

Remove restrictions, and allow foreigners to own land to build a factory, offi ce or house for their own use

Amount of land foreigners would own would be small, yet would provide an incentive, and also recognize a fair reciprocity – Filipinos can own land in other countries. Limit it to won use.

Art XII, Sec 9Establishment of an independent economic and planning agency

Not necessary to be in the Constitution

Organization of the Administration should be decided by the president, with Congress’ approval.

Other departments are not mandated.

Art XII, Sec 10 At least 60% Filipino ownership in certain areas of investments

Delete and remove any reference to “Preference for Filipinos”

Filipinos do not necessarily protect the National Patrimony better than foreigners.

The Admin can control

Art XII, Sec 11Franchises, etc. reserved to Filipinos or Filipino–owned companies

Allow full foreign ownershipFranchise sector is booming; huge potential for job & revenue generation. Filipinos can more than compete against any foreigner.

Art XII, Sec 12 Trade policy that serves the general welfare Unnecessary Simple commercial economics in an open market

will ensure this is the case.

Art XII, Sec 14 Practice of professions limited to Filipino citizens

Foreigners should be allowed to practice their professions

Would help accelerate technology transfer and development, create more jobs.

Not enough Filipinos in some professions.

Other countries allow Filipino professionals to practice.

Art XIII, Sec 3

Promotion of security of tenure of workers…

Entitlement of workers to a living wage

Delete

Needs to be better defi ned as a general policy – if in at all

It encourages mediocrity and is anti-worker.

Being confused by labor unions with minimum wage.

Art XIII, Sec 4 Mandate to undertake agrarian reform

Revise to allow both large and small plots

Agrarian reform has been a major inhibitor to agricultural dev’t; some crops need large land areas for competitive effi ciency and low cost.

Art XIV, Sec 6 Filipino as National language

Amend, to stress importance of learning English

Preferably to also learn in English (as it was 50 years ago)

English is now the world’s lingua franca, other countries are scrambling to learn English

Art XVI, Sec 11 (1) Mass media ownership limited to Filipinos

Delete

Foreign ownership should be allowed

Modern technology has made this restriction redundant – foreign media is already here

Art XVI, Sec 11 (2)Advertising industry open only to companies with at least 60% Filipino ownership

Delete Constitutions do not cover advertising period. It should be provided by law —if at all

SOME THINGS WE THINK NEED TO BE CHANGED…

SPECIAL REPORT 17

February 2014Philippine ANALYST

Some of these provisions weren’t wri en for the 1987 cons tu on. They were just extracted, with some minor amendments from the 79-year old 1935 cons tu on. This is the case par cularly on cons tu onal restric ons on land ownership; explora on, development, and u liza on of natural resources; and opera on and management of public u li es; and ownership of educa onal ins tu ons. (see Annex C).

The dream of many Filipinos is to gain a foreign educa on to add to what they’ve learnt here. They dream of going to Harvard, but the cost is prohibi ve. Why not bring Harvard here? What it will have to charge will, alone, be enough to make it no threat to local colleges. Anyway, do we want to protect colleges or open up opportuni es for students? Foreign colleges can bring research and new technologies to the Philippines, too, an area where we have been par cularly weak as a survey ranking universi es showed. Indonesia recently passed a law (it does not need cons tu onal change) to allow foreign ownership of educa onal establishments. The world has changed, changed drama cally, we cannot be trapped in history.

SOME ECONOMIC RESTRICTIONS ARE 79 YEARS OLD

PROTECT COLLEGES FROM COMPETITION OR GIVE STUDENTS THE WIDEST CHOICE

Interna onal news is on our LED screens at home, but they can’t have an offi ce. Interna onal news networks can’t operate and invest here because the cons tu on bans media 100%. A law can’t change that. A level playing fi eld, innumerable incen ves even good governance are of absolutely no relevance, CNN can’t come. Yet I watch it everyday, it’s in my home.

Twenty seven years ago, we didn’t have cellphones; today, we can’t leave the house without them. Imagine if the Cons tu on had banned mobile communica ons in the name of protec ng na onal security.

Technology has removed borders. Satellite communica ons, fi ber op c cables, digital technology were just emerging from the labs in 1987. They are a part of our lives today, so we may as well let the foreigners in as they’re already in.

Another prohibi on that makes no sense is to not allow foreigners to prac ce their profession. For law, I’d agree. We’ve got enough lawyers (I’m hesitant to say too many as I might upset some of my lawyer friends—and they might sue me). Why can’t a professional prac ce his profession here? Filipino professionals are excellent. A foreigner is no threat to them they can hold their own against anyone. Just ask all those Filipino professionals who prac ce their profession in someone else’s country. And there’s that same damning point: Filipinos can prac ce in another country, but that country’s professionals can’t prac ce here. That’s not fair. I suspect if you want Japanese to re re here they’ll want Japanese doctors to look a er them.

Mind you in this case the Cons tu on allows enabling laws to make exemp ons. I suggest our lawmakers move rapidly (a word they may wish to look up in the dic onary) to pass a law to open up all professions, not just a select few as the move to do this in congress may end up doing. There will not be a sudden fl ood of foreign professionals I can assure you. But a few gaps where need exists might be fi lled. And the exchange of exper se and experience could only further improve the already impressive creden als of Filipino professionals.

Where local knowledge is essen al, passing a local exam can be a necessary condi on. Lawyers, for instance must know local law. But there’s li le else where local knowledge is needed. All human bodies are pre y much the same (some just look be er than others) so as long as a doctor has passed an exam that is recognized in the Philippines he should be able to prac ce.

Even if all the wondrous promises of improvement of the investment scene were achieved, it wouldn’t ma er a foreigner can’t operate tollroads, railways, and telecom sta ons except as a minority partner. The cons tu on won’t allow it, and you can’t get around that if you are to operate honestly within the spirit and le er of the cons tu on. And we certainly need a lot more infrastructure.

SPECIAL REPORT18

February 2014Philippine ANALYST

INABILITY TO OWN LAND IS A DETERRENT TO INVESTMENT.

Maybe a 75-year lease on land seems enough, but would you want to be able to only lease the land for your house? No, you’d want to own it, passionately so. Well, foreigners don’t think in some strange foreign way; they want to own, too. Filipinos can, and do, own land in America and almost everywhere else, so why not here, at the very least on a reciprocal basis? For “own use” would be fair enough. The agrarian reform law has destroyed the ability to own agricultural land, so farmers are under no “threat.” And if limited to own use for house or factory, the amount of land taken would be infi nitesimal.

I’m willing to bet many of those who are against foreign ownership of land have rela ves who own land in other countries. So, apart from anything else, it would be only fair to have reciprocity. But that’s not so much the point. What is the point is that if we want to achieve more rapid growth, allowing foreigners to own land at least for their own house, offi ce or factory will help achieve that. As it is now, that inability to own land is seen as a deterrent to a rac ng investment.

OWN USE OWNERSHIP OF LAND WON’T TAKE LAND AWAY FROM FILIPINOS.

The preference given to Filipinos in the grant of concessions covering the na onal economy and patrimony should either be, preferably, deleted or amended to remove the “preference for Filipinos.” As the Manila Hotel case so amply demonstrated, Filipinos do not necessarily protect the na onal patrimony be er than foreigners might. But more importantly, dis nguishing between Filipinos and foreigners should no longer be an issue in today’s modern world. Whoever helps to provide jobs, to increase na onal wealth should be welcome. Laws can provide whatever specifi c protec on may be necessary.

Not in the economic sec on, but one area the cons tu on unreasonably protects is the judiciary, at least as related to business. Philippine courts, par cularly the Supreme Court, have almost unlimited discre on to interpret and decide on cases as they see it, too o en without being fully informed of the impact on business. Or even understanding the role of business. There have been a number of cases (e.g. SC ruled in 1991 that a naphtha cracker plant should be built in Bataan, as pe oned by a poli cian who wanted to have the project in his hometown, not in Batangas as the proponents preferred based on their business assessment. They le the country, as they certainly should) where business has been badly hurt to the detriment of society by decisions that didn’t appreciate all factors in conduc ng business.

Nothing could send a more drama c message than this. “We have truly opened our country to you to join us in our quest for a be er life for our people. Come, help us build a great country”.

The ideal way to review the Cons tu on is through a cons tu onal conven on. The argument that it costs more and takes more me is true, but we are talking about the Cons tu on, the fundamental document of the na on. You don’t consider the cost, which is small on the na onal scale of things, anyway.

A CONSTITUENT ASSEMBLY BY BOTH HOUSES IS THE WAY TO GO.

But the more prac cal way, given poli cal reali es, is for Congress as a cons tuent assembly to do the review, with both chambers vo ng separately before it goes to a plebiscite of the people. And don’t raise this nonsense that it’s not clear if both houses must meet jointly (which would make the Senate role meaningless) or separately, and then get together. Not making the dis nc on clear was an oversight of some not too bright lawyers in the 1986 con-con.There’s concern that

SPECIAL REPORT 19

February 2014Philippine ANALYST

SPECIAL REPORT20

February 2014Philippine ANALYST

The cons tu on should state general principles only and in a very general manner. A cons tu on should be wri en to last decades, even centuries in a fast-changing world.

Specifi cs should be by law or execu ve ac on. An open society provably works best.

the review would not be restricted to the economic provisions but would shi to the poli cal arena as well, and end up extending the terms of poli cians. Maybe, but it may also lead to a serious re-think of the whole system—something that I think is needed. For instance, a parliamentary system would be er suit Philippine culture. Having come from one, I think it’s a be er system, anyway. You don’t ques on, or disagree with, the boss just because he’s the boss. Well, I disagree with that. Rising to the top through a poli cal process does not make you a greater expert than everyone else. The fact that you need the president’s support if cons tu onal change is to be eff ected is a perfect example of this fundamental weakness in a presiden al system, Philippine-style. Think about it: Why should you need (as in this system you do) the President’s—one man’s—support for something to succeed? In a parliamentary system, the majority decides, the prime minister can’t override it. That’s as it should be. So I wouldn’t object if the style of government were included in the review.

CONGRESS CAN RESTRICT ITSELF TO REVIEW OF THE ECONOMIC PROVISIONS ONLY.

Whether the president agrees with it or not he shouldn’t disagree that bringing it into public debate now a er 27 years of phenomenal change in the world would be a healthy thing to do. And there are safeguards, it’s no easy task to change the cons tu on. It doesn’t require just the 50% plus one majority other laws need, it requires a 75% agreement in both houses, then 75% of a joint vote. Then a majority of all Filipinos vo ng in a plebiscite for any change to pass.

Some say, “Not now,” it’s too open to risk of poli cal machina on (to extend terms, for example). But if not now, when? With a President disinterested in a con nuance in power—something that’s unlikely to be ever repeated—this seems an ideal me. But if it’s too controversial and will derail eff orts to amend the economic sec ons only, let’s drop it. The President with the support of business and the public can easily control that the poli cal side doesn’t get included. He has strong majori es in both Houses. He can dictate (look at the examples in the last congress where he did). Whichever is agreed to—a full review, or just the economic sec ons—let’s do it now. We’ll never have a more favorable me. And let’s do it through a two-House cons tuent assembly that focuses on only the economic sec ons. It’s the most feasible op on for now.

THIS IS THE ONLY TIME IT CAN BE DONE.

It would be good if it could be done this year with a plebiscite at year’s end, but holding a plebiscite concurrent with the 2016 elec ons is an acceptable albeit less a rac ve, alterna ve. Either way, as long as it’s done. But the president may wish to consider that if done in 2014 he’s got almost two years of faster growth to his credit.

He’ll leave a country in be er shape than if it’s delayed to 2016, or worse nothing is done.

LET’S HAVE A 2 HOUSE CONSTITUENT ASSEMBLY NOW.

I have been a senior execu ve in business for over 50 years now. I’ve served Aussie companies, U.S. mul na onals (with a 6-year s nt as a regional manager for the Asia Pacifi c) and run my own successful business for 31 years analyzing the Philippines and its opera ng environment. I have nearly a hundred CEO’s who listen to my comments and advice. So it’s just possible I may know a li le about what investors fi nd a rac ve and necessary. They would more than welcome an opening of the Philippine cons tu on, even if the restric ons wouldn’t apply to their business. It would be a strong message of a dis nctly diff erent country that would now be worth a look.

IT’S TIME.

21POLITICAL

Philippine ANALYST February 2014

Gov’t, MILF sign fi nal peace pact The signing of the Comprehensive Agreement on the Bangsamoro (CAB) comes after 17 years of negotiations between the Philippine government and the Moro Islamic Liberation Front (MILF). In 1984, the MILF was formed to split away from the main body, the Moro National Liberation Front (MNLF), as they did not agree with the conditions of the Tripoli Agreement that provided merely “nominal autonomy for the Bangsamoro” as they saw it. The breakaway group was formed by members who were disgruntled over what they thought was the MNLF’s departure from its religious roots, its secularist mindset, and surrendering of demands for autonomy.

The CAB covers all signed agreements, including the framework peace agreement signed in October 2012 as well as the 4 annexes and an addendum.

The signing of the CAB has been generally well-accepted. This is a major achievement of the Aquino government, an achievement two previous administrations couldn’t achieve. President Estrada launched an “all out” (unsuccessful) war while Pres. Arroyo brokered a deal that was so obviously unconstitutional it is diffi cult to imagine why it was agreed to. The Supreme Court struck it down.

After 4 decades of Moro rebellion and more than 150,000 recorded deaths (including the death toll from skirmishes with other Muslim rebel groups), it’s certainly a welcome development, and there does seem to be sincerity and a mutual trust that the peace deal could succeed and achieve its objectives for the region.

ANNEX HIGHLIGHTS

Transi onal Arrangements and Modali es

Lays out the road map to the crea on of Bangsamoro from the signing of the peace framework agreement to the establishment of the Bangsamoro government with the passage of the Bangsamoro Basic Law and its new offi cials during the 2016 na onal elec ons.

Normaliza on Deals with the decommissioning of the armed wing of the MILF; disbanding of private armies; redeployment of the Armed Forces of the Philippines (AFP) and provision of socio-economic development programs for former combatants.

Power sharing Outlines the powers reserved for the na onal government, powers exclusive to Bangsamoro, and powers shared by both.

Revenue genera on and wealth sharing

The Bangsamoro has the power to create its own sources of revenue and to levy taxes, fees and charges (75% for Bangsamoro); an equitable share in the revenues derived from the u liza on and development of natural resources within its territory; and the authority to receive grants and dona ons from domes c and foreign sources.

Addendum on Bangsamoro waters Delineates the jurisdic on of the envisioned Bangsamoro government over the waters in its territories.

22 POLITICAL

Philippine ANALYST February 2014

Several groups are optimistic that the remaining crucial steps (e.g. endorsement and approval of the Bangsamoro Basic Law in Congress; holding of a plebiscite to ratify the law; and promulgation and ratifi cation of the statute) would be completed on time and the agreement could truly foster enduring peace in Mindanao.

But already there is a splinter group, the Bangsamoro Islamic Freedom Movement (BIFM) which said it won’t support the agreement. Also, Nur Misuari, the discredited leader of the MNLF, has long questioned it. This “infi ghting” within the MILF, like its rift with the MNLF, shows the limitations of a peace agreement in bringing actual peace and development to a confl ict zone.

The signing of the CAB is an important step. But more crucial now would be the implementation of various development efforts that would complement the fi nal peace accord. The delivery of basic social services (e.g. basic education, skills training, PhilHealth coverage) and access to microfi nancing must be expanded and improved. There must be strict enforcement of the law to keep the public safe. The disbursement of public funds must be transparent and social justice must be provided to all, regardless of socio-economic status.

If these elements are in place, insurgencies become irrelevant. But putting them in place will be quite a challenge, and will be the real test of the success of this peace deal.

Some groups might challenge the constitutionality of the peace accord (i.e. the existence of a ministerial system within a presidential one) in the Supreme Court. But the Philippine government is confident that the peace deal would be able to survive any legal challenge.

Perhaps the most important thing that will be achieved is to break the relationship with al-Qaeda and training for international terrorism. It is the primary reason other governments have come out so strongly in support of the agreement. Access for government troops into currently guarded Muslim encampments will be what will help achieve this.

Congress approval is needed and this will lead to much discussion and compromises to hammer out, taking much of this year to achieve. But the measure is likely to be approved before the end of the year, as President Aquino has already certifi ed the proposed Bangsamoro Basic Law as urgent. The measure can then be ratifi ed by early-2015.

However, approval of the bill in Congress might be challenged by some lawmakers. Power and wealth sharing does not sit well with some non-Muslim representatives from the South since the deal might diminish their clout in the region.

A very complex issue where high passions run has arrived at a remarkable breakthrough. One that, this time, looks likely to prevail. President Aquino can be given much credit for this as he added that level of trust that was missing in previous attempts.

It’s a fragile, complex situation with the implementation of the approved annexes among the major obstacles. Despite these challenges, there’s a level of optimism here that was absent before that gives the peace agreement a fair chance of success.

Philippines’ anti-corruption efforts still wanting

The Philippines’ ranking in Transparency International’s (TI) Corruption Perceptions Index (CPI) has been improving under the Aquino administration. However, much remains to be done if the Philippines is to achieve its goal of breaking into the top one-third of all economies surveyed.

The Transparency International’s CPI is the most widely-recognized indicator of the perceived extent of corruption. It provides inter-country comparisons and rankings that are recognized as fair assessments. The CPI measures the degree to which corruption is perceived to exist among public offi cials and politicians, and the perceived performance in controlling corruption.

In the Transparency International’s latest anti-corruption survey, the Philippines scored a measly 36 out of 100 where where 0 means a country is perceived as highly corrupt, and 100 means it is perceived as very clean. The score indicates that the country still has a serious corruption problem.

Last year the Philippines ranked 94th out of 177 countries, an improvement from 139th in 2009 and 105th in 2012.

Among the 10 Southeast Asian economies covered by the annual global survey the Philippines placed fourth behind Singapore (5th overall with 86 points); Brunei (38th with 60 points); and Malaysia (53rd with 50 points). This year, the Philippines outranked Thailand, Indonesia, Vietnam, Laos, Myanmar, and Cambodia. For the Philippines to break into the Top 1/3 of countries surveyed,

there must be –

232POLITICAL

Philippine ANALYST February 2014

1). Sincere, personal commitment of the country’s leaders to reducing corruption

President Aquino’s single-minded attack on corruption has happened at a level unimaginable in prior decades. His anti-corruption program has had some success: former president Arroyo is under hospital arrest, Chief Justice Corona was impeached while Ombudsman Gutierrez resigned.

The Offi ce of the Ombudsman has found probable cause to fi le plunder and graft charges against the lawmakers implicated in the pork barrel fund scam: Senators Juan Ponce Enrile, Jose “Jinggoy” Estrada and Ramon “Bong” Revilla Jr, as well as alleged mastermind Janet Lim-Napoles.

Also, graft cases against ex-military offi cials are being pursued; the Department of Public Works and Highways has been holding competitive biddings while national budgets were approved on time. Reenacted budgets are prone to corrupt practices.

Despite these measures, institutionalized corruption has not been addressed. Corruption among local government units (LGUs) is still widespread

2). Public awareness campaigns against corruption; prosecution of high-profi le corruption cases

The people can be a driving force, as the outrage over pork barrel showed. Also, social media has revolutionized public participation, and has made it an effective force.

A Freedom of Information (FOI) law is now needed if the President is truly serious about an honest government. Businessmen believe that a strong FOI law will signifi cantly reduce corruption (SWS survey). Despite this, President Aquino has been reluctant to certify the measure as urgent.

3). Strengthening of anti-corruption agencies such as the Offi ce of the Ombudsman

The Offi ce of the Ombudsman needs to increase its capacity to successfully prosecute erring offi cials in high-profi le cases. This will require beefi ng up and training its prosecutors and investigators. And be given proposer compensation. The proposed amendments to the Ombudsman Act (e.g. enabling the agency to look into bank accounts even prior to the fi ling of a case in court and issue freeze orders on unlawfully-acquired assets for 6 months) must be

4 Prosecution of a few high profi le anti-corruption cases The cases against lawmakers allegedly involved in the pork

barrel scam must be pursued aggressively. Previously, cases against high-level government offi cials were thrown out as prosecutors failed to build up strong cases. Will this happen to lawmakers and GOCC offi cials implicated in the pork barrel controversy? They must be held accountable if true reform is to happen. This is an ULTIMATE test. If President Aquino can do it it’s revolutionary

But the courts must co-operate

5). Enactment of economic reform bills The approval of economic reform measures is important to

enhance openness and competition, and reduce discretion. Among the pending bills in Congress that address these is the Anti-Trust or Fair Competition bill. The proposed measure aims to foster a more level playing fi eld in business and reduce monopolies, oligopolies, and anti-competitive behavior. In 2011, President Aquino designated DOJ as the competition Authority. The bill, despite being a priority of the House of Representatives, is still pending on 1st reading in both chambers of Congress. In the 15th Congress, the bill reached only 2nd reading in both Houses

6). Implementation of reforms in the governance of state-led fi rms

The GOCC Governance Act (RA 10149) was signed into law in 2011 but with limited power. The GOCC commission’s control over the state fi rms must be expanded amidst the pork barrel issue. State-led fi rms have been implicated as conduits of anomalous PDAF allocations

7). Streamlining of business registration The cost of doing business in the country must be brought

down. The number of procedures (15 vs. 3 in Singapore) and days (35 vs. ½ day in New Zealand) needed to start a business must be reduced. The Philippines’ ranking in the World Bank group’s Doing Business report improved to 108th from 138th in 2013 but there’s still a long way to go especially if it aims to make it to Top 1/3 of economies surveyed. Fewer days and steps to start a business means fewer possibilities to start bribe.

8). Implementation of national budget reforms The Aquino admin employed zero-based budgeting

24 POLITICAL

Philippine ANALYST February 2014

scheme from the beginning and terminated ineffi cient and questionable programs and increased funding for key initiatives. It also did away with re-enacted budgets, which were vulnerable to corrupt practices.

In that 2014 budget, the corruption-prone Special Allotment Release Order (SARO) system was abolished

9). Push for the enactment of the Freedom of Information bill and other anti-corruption measures.

The measure aims to promote transparency in government transactions. It has been pending in Congress for 22 years. The Senate has approved its version on 3rd and fi nal reading but the counterpart measure in the House of Representatives is still pending on 1st reading. President Aquino must certify the bill as urgent, like what he did with other landmark laws – the Reproductive Health and the Sin Tax Reform.

The Aquino administration must implement these measures if it wants to give the impression that it is serious in combatting corruption.

The Philippine government must seriously address corruption if it wants to attract more job-generating investments. Businessmen would be hesitant to transact with agencies riddled with corruption and with a government that is unable to prosecute corrupt offi cials. President Aquino’s anti-corruption agenda must be anchored with his goal of achieving ‘inclusive growth’ or economic growth that benefi ts the poor.

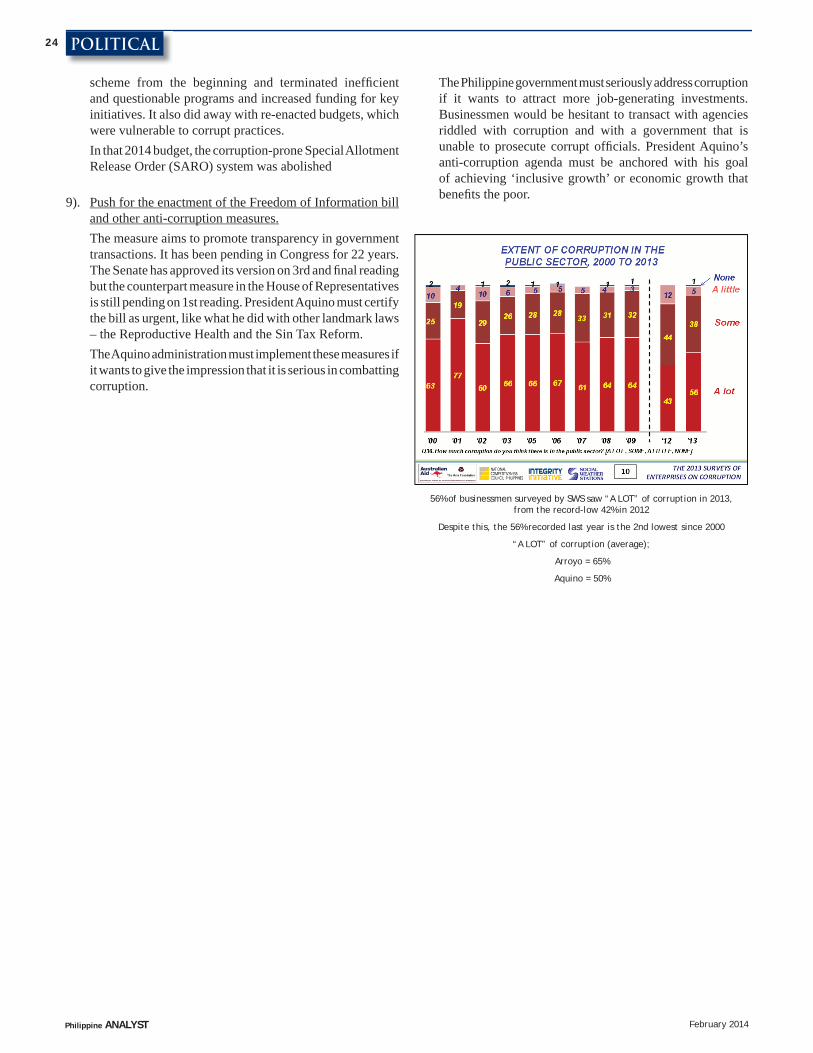

56% of businessmen surveyed by SWS saw “A LOT” of corruption in 2013, from the record-low 42% in 2012

Despite this, the 56% recorded last year is the 2nd lowest since 2000

“A LOT” of corruption (average);

Arroyo = 65%

Aquino = 50%

25ECONOMY

Philippine ANALYST February 2014

Updated PH Development Plan takes a different tackSocio-economic Planning Secretary and National Economic and Development Authority (NEDA) Director General Arsenio Balisacan unveiled the Updated Philippine Development Plan covering the remaining 3 years of the original Plan, or 2014-2016, which stresses the urgency of addressing poverty and raising private investment in the most productive sectors – areas where the economy failed despite its rapid growth during the past 3 years.

Secretary Balisacan noted the attainment of the Plan’s annual economic (gross domestic product) growth target of 7% in 2010-2012, making the Philippines one of

Asia’s best performers during the period. This was supported by strong macroeconomic fundamentals like low infl ation, interest rates and budget defi cit and sustained current account surpluses, which earned the country its fi rst-ever investment grade rating. The country also dramatically raised its rankings in global competitiveness and ease of doing business.

Despite this success, the level of investment relative to the size of the economy remained the lowest among ASEAN members. Worse, the underemployment rate stayed high at close to 20%, and “an even bigger challenge” is bringing down the poverty rate to the targeted 16.6% by 2016. If at all, the lessons learned in implementing the Plan, according to Sec. Balisacan, would be:

Good governance is an effective platform in the pursuit of development strategies

Macroeconomic and political stability can boost confi dence Economic growth isn’t enough to solve poverty Development strategies must be more focused geographically

and sector-wise for growth to be more inclusive Disasters can negate the gains and push back development

FDI remained the lowest among ASEAN members.

The update of the Philippine Development Plan 2011-2016 for the last 3 years of its implementation takes these lessons in stock and was re-designed to address them.

The government’s GDP growth target remains at 7-8% p.a.; with an unemployment rate retained at 6.5-6.7% but with lower underemployment of 17% (from 19.7% today) by 2016. The poverty incidence target was re-adjusted to 16-18%, which allows for a slight slippage from the country’s Millennium Development Goal (MDG) of 16.6%.

26 ECONOMY

Philippine ANALYST February 2014

A new feature of poverty targeting under the updated Plan is the focus on “multi-dimensional poverty incidence,” which looks at other dimensions of poverty – health, education, access to water, sanitation, social housing, etc. – rather than just the traditional income poverty concept on which the 16-18% target was set. Whilst the new concept may have its merits, it might divert some attention away from a likely shortfall in the income-based target, which is the basis in international poverty comparison and is in fact a key indicator in the MDG. An indicator like the Human Development Index (HDI) probably fi ts better in measuring multi-dimensional poverty, but no target has been set for this in the updated Plan.

Another innovation is implementing appropriate interventions to attain inclusive growth based on specifi c categories of geographic areas:

For Category 1 cities and provinces, which are growing rapidly but with large absolute number of poor (but not necessarily high percentage incidence of poor households) which are being left behind by the growth, the intervention will essentially consist of skills development and matching; promotion of industries where global competitiveness can be potentially developed for increased job creation (IT-BPO, tourism, construction, manufacturing and logistics); and providing other support social services for the poorest households. These provinces include Cebu, Pangasinan, Negros Occidental, Iloilo and Davao del Sur.

For Category 2 areas with slow economic progress and high poverty incidence, the approach will be to provide basic social services, promoting livelihood and small businesses, and improving access and connections to centers of opportunity. These provinces include Lanao del Sur, Maguindanao, Eastern Samar, Saranggani, North Cotabato, Masbate and Northern Samar.

For Category 3 which refer to those most vulnerable to major natural catastrophes, the objective is to make them resilient to the impact of disasters by updating geo-hazard maps, land use plans, training them for disaster response, and building more resilient and stronger structures. Thirty vulnerable provinces have been identifi ed to benefi t from these interventions.

For the whole country, the thrusts are for the government to establish a policy and regulatory framework that will catalyze private initiative and encourage effi ciency improvements. The government says it will intervene strategically where the private sector is unable to deliver the goods, services and facilities needed by the poor.The Plan’s success will be measured in terms of

efficiency and effectiveness. Efficiency is its ability to steer private activity into the direction laid out in the Plan. Effectiveness is the extent in which quality of life is improved.

Joblessness rise in 4th Q, but whole year 2013 results still better than previous year

The number of jobless adults reached 12.1 million (27.5% of the adult labor force) in December (4th quarter) 2013 from 9.6 million (21.7%) in September (3rd quarter), the Fourth Quarter 2013 Social Weather Survey of the Social Weather Stations (SWS) disclosed. It was also worse than the 10.1 million (24.6%) recorded in 4Q12.

The focus is on addressing “multidimensional poverty incidence”.

The natural disasters have largely contributed to the increase in joblessness.

The loss of livelihood and shutdown of fi rms damaged by the natural disasters in the Visayas islands in 4Q13 may have largely contributed to the increase in joblessness. The number and percentage of Filipinos without jobs were on the downtrend during the fi rst three quarters, so the rise in the 4th quarter appeared to be unusual, if not an outlier, and the only abnormalities that occurred during the period were the Cebu-Bohol earthquake and Typhoon Haiyan.

In fact, despite the slippage in the 4th quarter, the whole year 2013 average of jobless adults was 11.1 million (25.2%), still better than the 11.6 million (28.8%) in 2012.

Also, net optimism on job availability, or the difference between the percentage of those who believed there would be more jobs in the next 12 months and those who thought there would be fewer jobs, rose to +19 in 4Q123, up from +4 in 3Q13 and the highest since the “very high” +36 in November 2010. Those who expected more jobs were 40%, while those who said there would be fewer jobs reached 21%. Another 31% thought job availability will be the same in the next 12 months.

272ECONOMY

Philippine ANALYST February 2014