Embed Size (px)

Citation preview

LAW 463 – Securities Regulation

Table of Contents

CONTEXT AND PHILOSOPHY............................................................................................................................................................3

TYPES OF SECURITIES..............................................................................................................................................................................3TYPES OF INVESTORS...............................................................................................................................................................................4WHERE AND HOW SECURITIES ARE FIRST SOLD.....................................................................................................................................4PURPOSES OF SECURITIES REGULATION..................................................................................................................................................4TECHNIQUES OF SECURITIES REGULATION..............................................................................................................................................5BASIC STRUCTURE OF THE MODERN REGIME..........................................................................................................................................5

SCOPE........................................................................................................................................................................................................5

DEFINITION: “SECURITY”.........................................................................................................................................................................5DEFINITION: “TRADE”..............................................................................................................................................................................7

Jurisdiction..........................................................................................................................................................................................8

DISTRIBUTION........................................................................................................................................................................................8

KINDS OF DISTRIBUTION..........................................................................................................................................................................9TYPES OF SECONDARY TRADING MARKETS..........................................................................................................................................10

MATERIALITY......................................................................................................................................................................................10

MATERIAL FACT....................................................................................................................................................................................10MATERIAL CHANGE...............................................................................................................................................................................11

MACHINERY..........................................................................................................................................................................................11

BC SECURITIES COMMISSION................................................................................................................................................................12NATIONAL INSTRUMENTS & POLICIES (HAVE LEGAL FORCE UNDER BCSA SS.184, 187).....................................................................12SELF-REGULATORY ORGANIZATIONS....................................................................................................................................................13PROCEDURAL FAIRNESS.........................................................................................................................................................................13ENFORCEMENT PROCEDURE OF COMMISSIONS......................................................................................................................................13

Reviews and Appeals (Part 19 BCSA)...............................................................................................................................................13Industry Best Practice.......................................................................................................................................................................14

NATIONAL AND COORDINATED APPROACHES TO SECURITIES REGULATION............................................................14

SYSTEMATIC RISK..................................................................................................................................................................................14Options After the Reference..............................................................................................................................................................14

THE PROSPECTUS PROCESS............................................................................................................................................................15

PROSPECTUS REQUIRED AND REPORTING ISSUER..................................................................................................................................15CONTENTS OF LONG FORM PROSPECTUS (IPO).....................................................................................................................................15REGULATORY DISCRETION.....................................................................................................................................................................16MECHANICS AND STAGES OF THE PROSPECTUS.....................................................................................................................................16THE PROSPECTUS PROCESS....................................................................................................................................................................18ALTERNATIVE FORMS OF PROSPECTUS..................................................................................................................................................19PASSPORT SYSTEM [+ PROSPECTUS REVIEW] AND MULTIJURISDICTIONAL DISCLOSURE SYSTEM.......................................................20MULTIJURISDICTIONAL DISCLOSURE SYSTEM (MJDS).........................................................................................................................20

CONTINUOUS DISCLOSURE.............................................................................................................................................................21

PERIODIC DISCLOSURE...........................................................................................................................................................................21Financial Disclosure.........................................................................................................................................................................21Management’s Discussion & Analysis (MD&A) (51-102 Part 5)....................................................................................................23Annual Reports and Annual Information Forms (AIFs) (NI 51-102 Part 6)....................................................................................23Certification Requirements...............................................................................................................................................................23Proxy and Information Circular - Relates to shares with voting rights attached.............................................................................23Communications/Delivery of Periodic Disclosure............................................................................................................................25

TIMELY DISCLOSURE.............................................................................................................................................................................26Material Change Reports (NI 51-102 Part 7/85(b)).........................................................................................................................26

SELECTIVE DISCLOSURE........................................................................................................................................................................27

THE EXEMPT MARKET......................................................................................................................................................................27

TYPES OF PROSPECTUS EXEMPTIONS.....................................................................................................................................................28(A) No Need to Know: Purchaser Already Familiar With Issuer or Securities................................................................................28(B) No Need to Know: Purchaser is Sophisticated or Otherwise Able to Protect Itself...................................................................29

1

(C) No Need to Know: Investment Very Safe....................................................................................................................................29(D) Redundancy or Dual Regulation: Prospectus-level info available from another source...........................................................29(E) Cost/Benefit Analysis: Ensuring Smaller Issuers and Not-for-Profits can access Capital Markets..........................................30Equity Crowdfunding Exemption (BCI 45-535)................................................................................................................................31Discretionary Exemptions.................................................................................................................................................................31Miscellaneous (Part of Div 2: Transaction Exemptions)..................................................................................................................31

RESALE OF SECURITIES EXEMPTION......................................................................................................................................................32

REGISTRANT REGULATION.............................................................................................................................................................33

REGISTRATION REQUIREMENTS.............................................................................................................................................................33Dealers and Advisers........................................................................................................................................................................33Investment Fund Managers (NI 31-103 s.7.3)..................................................................................................................................34

FIRM CATEGORIES FOR REGISTRATION..................................................................................................................................................34INDIVIDUAL CATEGORIES OF REGISTRATION.........................................................................................................................................35

Individual Registration Requirements...............................................................................................................................................35EXEMPTIONS FROM REGISTRATION........................................................................................................................................................36

International Dealers........................................................................................................................................................................36International Advisers.......................................................................................................................................................................36Client Mobility...................................................................................................................................................................................36Generic Advice..................................................................................................................................................................................36

REGISTRANT OBLIGATIONS....................................................................................................................................................................36REGISTRANT OVERSIGHT.......................................................................................................................................................................39

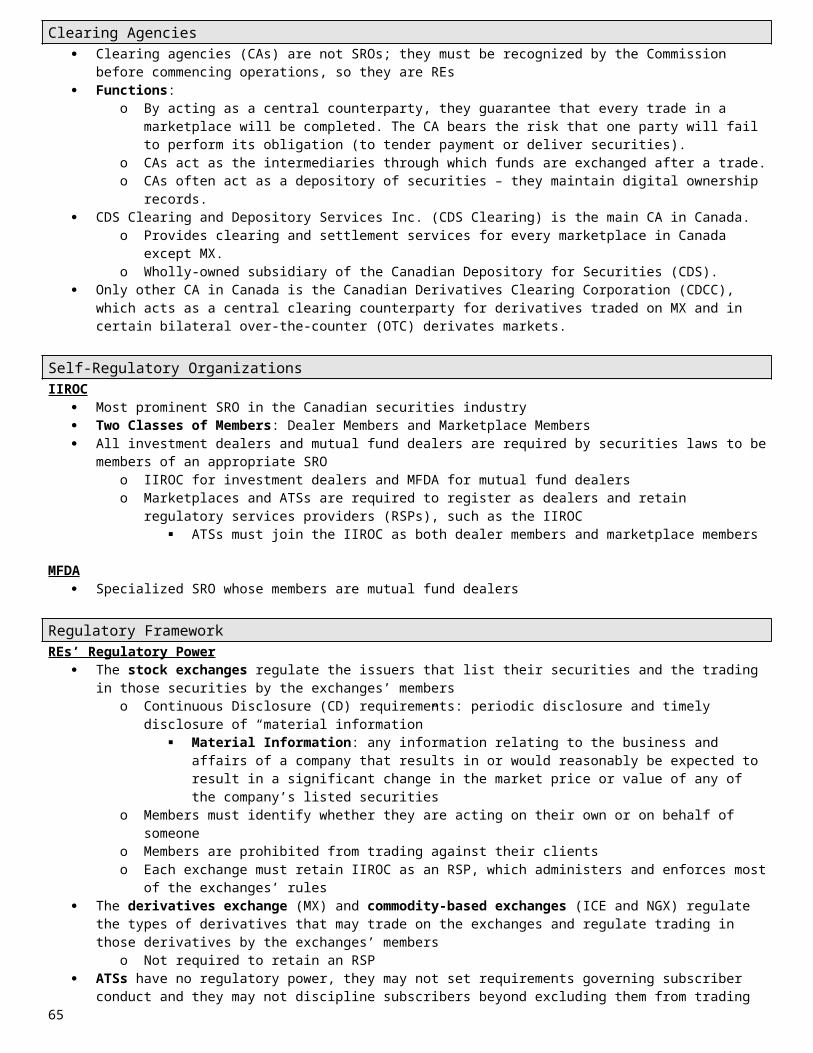

RECOGNIZED ENTITIES....................................................................................................................................................................39

MARKETPLACES.....................................................................................................................................................................................39CLEARING AGENCIES.............................................................................................................................................................................40SELF-REGULATORY ORGANIZATIONS....................................................................................................................................................41REGULATORY FRAMEWORK...................................................................................................................................................................41OVERSIGHT BY COMMISSIONS...............................................................................................................................................................41

CRYPTOCURRENCY (NOT ON THE EXAM)..................................................................................................................................41

VIRTUAL MARKETS INTEGRITY INITIATIVE REPORT (NY AG).............................................................................................................42CRYPTOCURRENCY OFFERINGS CSA STAFF NOTICE 46-307...........................................................................................................43SECURITIES LAW IMPLICATIONS FOR OFFERINGS OF TOKENS CSA STAFF NOTICE 46-308............................................................44

EVOLUTION OF THE REGULATION OF DERIVATIVES - GLOBAL FINANCIAL CRISIS.................................................44

RISKS OF DERIVATIVES..........................................................................................................................................................................45FINANCIAL CRISIS AND GLOBAL RESPONSE..........................................................................................................................................45TRADE REPOSITORIES AND DERIVATIVES DATA REPORTING: MI 96-101............................................................................................46CENTRAL COUNTERPARTY CLEARING HOUSES (CCP)..........................................................................................................................47

INSIDER TRADING...............................................................................................................................................................................48

LEGAL INSIDER TRADING (REPORTING ISSUER)....................................................................................................................................48ILLEGAL INSIDER TRADING/TIPPING/RECOMMENDING..........................................................................................................................51

[1]: X must be in a SPECIAL RELATIONSHIP with the reporting issuer.......................................................................................51[2] X traded based on knowledge of MATERIAL INFO...................................................................................................................52[3] The material info relied on was NOT GENERALLY DISCLOSED............................................................................................52Evidentiary Issues: Commission must prove each element of IT allegations on BofP (defense)......................................................53

DEFENSES...............................................................................................................................................................................................53CRIMINAL LIABILITY..............................................................................................................................................................................54SANCTIONS FOR ILLEGAL INSIDER TRADING/TIPPING (SEE BELOW FOR MORE DETAIL).....................................................................55

TAKE-OVER BIDS.................................................................................................................................................................................56

DEFINITION.............................................................................................................................................................................................57EXEMPTIONS FROM “FORMAL” TAKEOVER BID REQUIREMENTS (NI 62-104; PART 4 – DIV 1) (CATCH-THEN-EXCLUDE).................57TOB PROCEDURES.................................................................................................................................................................................58DEFENSES...............................................................................................................................................................................................60COMMISSION + COURT POWERS: REGULATORY RESPONSIBILITIES VS COURT POWERS......................................................................63EMERGING ISSUES..................................................................................................................................................................................63

ENFORCEMENT (NOT ON THE EXAM)..........................................................................................................................................63

ENFORCEMENT PROCEDURE...................................................................................................................................................................64INVESTIGATIVE PROVISIONS (PART 17 BCSA, SS 141-144)..................................................................................................................65OPTION 1: ADMINISTRATIVE SANCTIONS...............................................................................................................................................66

2

Enforcement Orders (BCSA 160-164):.............................................................................................................................................66Option 1(b): Civil Remedies – Applications to Court.......................................................................................................................68

OPTION 2: PENAL (QUASI-CRIMINAL PROVISIONS)...............................................................................................................................69OPTION 3: CRIMINAL..............................................................................................................................................................................70

Context and Philosophy2 MAIN GOALS OF SECURITIES REGULATION: 1) Protect investors; AND 2) Foster fair and efficient capital markets [contribute to financial stability/mitigate systemic risk] – Public Interest.

Capital Markets: Broader regulatory structure of securities, banking and insurance.o Primary objective of banking regulation is credential regulation to make sure the banks are solvent capital

requirementso Insurance is separately regulated; overlap between some insurance products and mutual funds (which are securities)

Financial Markets: All of the capital markets + anything else that may go into how markets move. Security Markets: About buying and selling securities.

Capital Market Efficiency FOSTERING FAIR AND EFFICIENT CAPITAL MARKETS: Requiring issuers to disclose information about

themselves to the investing public allows price to reflect value more accurately, which contributes to the fairness and efficiency of securities markets

o Securities value = function of issuer’s actual financial prospects; Securities price = reflects investors perceptions of the financial prospects Whether price reflects value is a function of investors perceptions of the financial prospects

o In order to foster fair and efficient capital markets, regulations must strike a balance such that investor protection schemes are not so onerous as to deter corporations from using capital markets to raise funds

o Efficient Markets Hypothesis: EMH asserts that capital markets are efficient when all available info about a security is reflected in its price – controversial aspects prediction that even though info not immediately and costlessly available to all market participants, the market will act as if it were + prices fluctuate in unpredictable ways

Critiques of Disclosure Paradigm 1) Behavioral Economics (assumes investors are perfectly rational, but no they aren’t, so disclosure cant guarantee market efficiency) 2) Volume of Mandatory Disclosure (volume is counterproductive, info overload not actually reading/accurately interpreting available info) 3) Complexity (capital markets are more complex than when disclosure became a reg req – issuers finance in more complex ways, new types of secs, interconnectedness)

Securities Market Public Markets: Companies selling stocks to the public. Exempt/private: Special rules that apply to a security, the general public cannot just buy. Can only sell to people with a

unique relationship to the company. Exempt market is bigger than the public.

Types of Regulation Entity Based Regulator: In Canada, we regulate banking, securities and insurance separately. Twin-Peaks Regulator: Gives up on entity-based structure (currently in Canada) and has one side deal with consumer

protection and the other focuses on safety and soundness (e.g. seen in Australia). Unified Regulator: Banking, Insurance and Securities all regulated by one organization. Other Option: If you do not have a unified regulator, try and get coordination between the regulators.

Regulatory Methods1) Disclosure-based re issuers2) Registration requirements for registrants (dealers & advisors)3) Anti-Fraud Provisions including criminal sanctions.

Types of Securities[1] DEBT: Commercial paper (short term), bonds and debentures; governed by securities regulation

Commercial Paper: IOU, investor buys, agreed on maturity date to pay back with interest, no interest along the way, and is unsecured, and is usually short term (<270 days)

Bond/Debenture: Secured against some asset, company would need to talk to a credit rating agency since they are long term commitments, get fixed income along the way, good way of raising steady low-risk money. But won’t get a large return. Priority in event of bankruptcy.

o Bonds and debentures carry a face value, a maturity date and an interest rate (=coupon rate)o Bonds are traded over the counter and have credit ratings attached to themo In the corporate sector, bonds are secured, and debentures are unsecured.

Government bonds are not secured against any assets3

[2] EQUITY: Buying a piece of a company. Anytime equity is sold, a prospectus must be filed (except for exempt distributions). Share: Share pro-rata in any future profits and rights to some proceeds of sales of assets if the company dissolves.

o Common Share: Get to vote, right to dividends, and liquidation rights. o Preferred: Usually for money partner i.e. venture capitalist // May get better dividend or asset rights than common

shares and certain preferred rights (e.g. participation rights, information rights, ROFR, pre-emptive rights) o Restricted: Cannot vote and restrictions on dividend rights.

Rights of Offering: A right allows existing shareholders to buy more shares.o Holders of a specified number of rights will have the right to buy a share in the company for a predetermined price

within a certain period of time // Rights to buy shares are normally tradable Business Trust or Partnership Unit: Comparable to a share of a corporation

[3] DERIVATIVE SECURITIES: Instrument whose value is derived by something else – can be equity, debt or mixed. Key their value off some reference share (some underlying thing) (Swaps + Options) or from a debt security.

Used for risk management, hedging and speculating Futures: financial contract obligating the purchaser to purchase the asset at a later date at a specified price Option: contract that entitles, but does not require, its holder either to buy or sell a particular entity on a particular date

(exercise date) at a specified price (exercise price) Swap: arrangement under which two parties agree to exchange particular cash flows over a fixed period of time

o E.g. Credit Default Swaps (CDS): the writer agrees to compensate the holder in the event that a specified “credit event” occurs, for example if a certain debt security goes into default.

[4] SECURITIZED PRODUCTS: Bundle of debt that gets bundled together and sold again.

Types of Investors[1] RETAIL: Everyday people

[2] INSTITUTIONAL: Sophisticated investors with a large staff.

Where and How Securities are First Sold Any corporation or other business organization that issues securities is an “issuer” Early-stage companies usually sell securities through an exempt distribution known as a “private placement” usually to

friends, family, management, venture capitalists, accredited investors or other sophisticated investors (investing $150,000+). Offering Memorandum: shorter, more plain language than the prospectus; can sell to anyone without restrictions; has

maximum amount thresholds in certain jurisdictions (no max in BC) “Issuer” (BCSA 1(1)): Means a person who

o (a) has a security outstandingo (b) is issuing a security, or o (c) proposes to issue a security.

“Reporting issuer” (BCSA 1(1)): o Means an issuer that:

(a) has issued securities in respect of which (i) a prospectus was filed and a receipt was issued; (ii) statement of material facts was filed and accepted; or (iii) a securities exchange take-over bid circular was filed …

(b) has filed a prospectus or statement of material facts and the Exe DIR has issued a receipt for it under this Act (see: (c)-(f)).

o Reporting issuer’s key personnel become “insiders” subject to insider trading regulation They can also become liable for misrepresentations in continuous disclosure documents or the failure to

disclose relevant informationo Have to make continuous disclosure (financial statements, MD&A, annual meetings, resale of securities by control

persons) on SEDAR and insider information must be disclosed on SEDIo Once you are a reporting issuer, you can still distribute securities through exempt offerings private placement.

However, there are restrictions on the resale of those securities. This is disclosed via a news release on SEDAR

Purposes of Securities Regulation Objectives of Securities Regulation:

o Investor Protection – giving investors the information they need to make informed decisions Also, by preventing dishonest practice

o Fair and Efficient Capital Markets – market integrity Optimal financial resource allocation; mobile and transferable capital; framework for valuing investments

4

Information about issuers must be given out at the same time to everyone Oversight of market intermediaries

E.g. credit rating agencies Securities regulation can require a lot of disclosure and make sure people know about risk, but they will not

stop an investor from investing in a risky business market economy Other Goals of Securities Regulation:

o Systemic Risk: aggregate of multiple smaller risks Involves “the risk of breakdown among institutions and other market participants in a chain-like fashion

that has the potential to affect the entire financial system negatively” Ideals:

Regulators should attempt to reduce the risk of failure by issuers and market intermediaries Regulators should strive to minimize disruption and losses to stakeholders in the event of failure Because events from other jurisdictions may cause instability, regulators should seek to cooperate

internationally and share information to facilitate stabilityo Public Confidence: requires trust in both the people and the institutions of the industry

Advisers and dealers must follow a strict set of rules and guidelines Regulators to prioritize and publicize enforcement Information disclosure feeds and shapes trust Individuals encouraged to participate in the securities markets People are gamblers at heart – if securities were unavailable or untrustworthy, gambling and lotteries would

absorb larger amounts of money

Techniques of Securities Regulation Registration of persons: everyone (individuals, corporations and unincorporated organizations) who acts as a dealer, adviser

or investment fund manager Registration of issuers and securities: must file a prospectus, make periodic and timely continuous disclosure, and directors

and officers must ensure proper disclosure and meet certain standards regarding personal trades in the issuer’s securities Anti-fraud measures: honor the anti-fraud rules found in corporate, securities and criminal legislation

Observations That Guide Interpretation: 1) Securities regulation is protective, not punitive; 2) Courts choose substance over form in interpreting the definition (i.e. they focus on the general economic effects of the whole transaction rather than the specific technical details) – Financial engineers use “securitization” to create new derivatives and this transforms the value of a given asset or pool into something that can be sold as a security

Basic Structure of the Modern Regime1. Legislation: Each of the 10 provinces and three territories has its own securities laws

a. High degree of cooperation between the provincesi. Each province has its own Securities Act

ii. Policies are harmonized and similarb. National Instruments are adopted by the provinces and are uniformc. Multi-Lateral Instruments – adopted by select provincesd. Local Rules – local economic developments, exemptions, grants, etc.e. Self-Regulated Investment Associations overseen by securities regulatorsf. Securities Regulators can regulate the Securities Actg. Role of the regulator is to monitor the markets, not to make sure victims are made wholeh. The CBCA regulates the conduct of federally incorporated companies (some overlap with provincial securities laws)i. Some provisions of the Criminal Code also govern securities regulationj. Takeover context: Competition Act and Investment Canada Act

2. Administration: each jurisdiction has its own administrative agencya. The Canadian Securities Administrators is an umbrella organization of all 13 Canadian securities regulatorsb. Top Tier (panel of commissioners): make orders and ruling, hear appeals from the lower tier, formulate policies and

make recommendations to the provincial government regarding legislative changesc. Lower Tier (administrative body): day-to-day aspects of the Commission

ScopeOBSERVATIONS THAT GUIDE INTERPRETATION:

1) Securities regulation is protective, not punitive2) Courts choose substance over form in interpreting the definition (i.e. they focus on the general economic effects of the whole

transaction rather than the specific technical details).

Definition: “Security” BCSA 61: One may not distribute securities without having filed a prospectus unless potentially exempt. 5

Security: Instrument issued to raise funds to capitalize an entity as a result, generate profits. Securitization: transforms the value of a given asset or pool of assets into something that can be sold as a security

o The securities created by securitizing cash flows from a set of assets are known as “asset backed securities” (ABS). Pacific emphasizes that the legislated definition is not exhaustive, and the categories are not exclusive

[1] Any document, instrument, or writing commonly known as a security (BCSA s.1(1)(a)) Common Knowledge: Need to determine the common knowledge among securities professionals (financial and legal

community), not lay persons (Gelderman). It need not be known to the man “in the street” – just must be knowledge common among members of the community (SEC v. Glen W Turner Enterprises (ponzi scheme)).

[2] A doc evidencing title to, or an interest in, the capital, assets, property, profits, earnings or royalties of a person or company (1(1)(b)).

TEST (look @ the purpose of the transaction) Does a “document” show some form of investment or speculation (e.g. looking for profit, business prospect, etc.)? (this is how courts have narrowed the broad definition under 1(b)).

o Title doc to ½ interest in breeding chinchillas to share in profits = security (Swain v. Boughner)o Scotch whiskey receipts are securities when they are bought and sold as an investment (Brigadoon)o Control can help determine whether something is a security or not (Raymond Lee – Co. got a 20% interest in

inventions where they helped with marketing and patents// Held: This is not a security, is a service. Reasons: 1) Inventors remained in control of inventions; 2) Inventors testified they did not think this was an investment; and 3) Primarily a transaction for patent processing and marketing)

[3] A document evidencing an option, subscription or other interest in or to a security (BCSA, s.1(1), “security” (c)) Option: Form of derivative. It is a contract that entitles but does not require its holder either to buy or sell a particular

security on a particular date at a specific price. Subscriptions: Sign-up forms for purchasing securities. Rights: Corps can raise capital quickly and with fewer regulatory requirements by granting existing security holders rights to

purchase a specific # of additional securities at a specific price and time. Warrants: attached to bonds, give warrant holder right to buy a specific # of corp’s equity sec at specific price & during

specific time period (referenced like an option).

[4] Debt Security: a bond, debenture, note or other evidence of indebtedness, share, stock, unit, unit certificate, etc. Other than: (i) contract of insurance and ii) evidence of deposit issued by savings institution (these are excluded as they are governed by insurance and banking) (1(1)(d))

Issue: Distinguishing a debt security from a document evidencing indebtedness that is not a security. Family Resemblance Test (BCSECCOM v Gill, BCCA citing Reves) – Rebuttable presumption that certain types of debt

instruments are securities, not banking products. Factors relevant whether presumption is rebutted:1. The Motivations that would prompt a reasonable seller and buyer to enter into the transaction: If the seller’s purpose

is to raise money and the buyer’s purpose is to profit from returns, it’s a security;2. The intended distribution of the instrument: if it is one in which there will be ‘common trading for speculation or

investment’, it’s a security;3. Reasonable expectations of the investing public: The more the public expects a security, the more likely it’s a

security;4. The existence of another regulatory scheme: If there is no other regulatory scheme that reduces the risk of the

instrument, it’s likely a security. Promissory Notes: substance over form; rebuttable presumption that promissory notes are securities; secured by assets may

just be a loan and not a security (CBM Canada's Best Mortgage Corp. (Re))BC Sec Com - 2 individuals gave large amounts of $ to Gill for his investment co., he then gave them receipts // Held: These were securities

[5] A Proportionate Interest in a Portfolio of Assets: agreement under which the interest of the purchaser is valued for purposes of conversion or surrender by reference to the value of a proportionate interest in a specified portfolio of assets

Captures “open-ended” investment funds (e.g. mutual funds): these funds sell units or shares to investors and invest the proceeds in various securities – investors can redeem their units at regular, specified intervals, in proportion to the net market value of the fund at that time

[6] Profit-Sharing Agreement or Certificate: similar to an investment contract, but as per Raymond Lee, there may be a profit-sharing arrangement that is not also an investment contract.

[7] *Investment Contract (BCSA, s.1(1)(l)) Catch-all Provision (e.g. Joiner Leasing (USSC) – Ppl bought potential oil-boom land expecting an investment return // Held: This is a security).

TEST (Pacific Coast, 1978 SCC – Bags of coins “on margin” = Investment Contract): While the Howey and Risk Capital tests are helpful, they are not necessary to determine whether an Investment Contract is a Security. What is necessary is that: ‘finding the contract in question to be an investment contract (and therefore a security) would support and advance the policy goals of securities regulation generally.’6

Policy of Securities Regulation: It is about protecting the public and “full and fair disclosure.” Substance, not form, governs the interpretation of what is a security. Look at whether people are at risk (Pacific – risk because investors dependent on PC on how to function in futures market)

Re Kustom Designs – Investments expecting negative earnings but resulting in a tax refund or lower tax bill, achieved through the efforts of others, was a financial benefit – which constitutes a profit for the purpose of investment contract.

Real Estate (Braun (Re)): not purchasing a beneficial interest in a property; ‘flipping’ scheme; profit through the increasing value of the property

What has been found to be an Investment Contract: Units in a citrus Grove Development, where investors were not from the area, not farms, stayed in guesthouse (Howey) // Retail store membership program (Hawaii) // Purchase of Silver Coins on Margin (Pacific) // Real Estate Ventures // Some franchise where the franchisor retains a huge degree of control relative to the franchisee.

Common Enterprise Test (Howey (citrus grove in Florida), cited in Pacific – criterion was met): 1. There must be a “common enterprise” (Pacific – Common enterprise found - must be commonality between investor and the

promotor (vertical), need not be commonality between investors themselves (horizontal)), in which2. Profits will come solely from the efforts of people other than the investors.

Pacific adopted a “more realistic” formulation of the second part: Holding that it was necessary only that “the efforts made by those other than the investor are the undeniably significant ones” (read out the word “solely”).

SBC Financial Group Inc. (Re): efforts of a third party and common enterprise not met; it was a real estate transaction, not a security

Risk Capital Test: Hawaii expands the Howey test for the existence of an Investment Contract (Hawaii, discussed in Pacific – criterion met):

1. An offeree furnishes initial value to the offeror [Hawaii - members required to contribute $320 or $820 > not simply a purchase of sewing machine, cookware, because these amounts far exceeded their wholesale value];

2. A portion of this initial value is subject to the risks of the enterprise [Hawaii - members’ ability to recoup initial investment and earn income inextricably bound to success of the enterprise // Pacific - Investors are subject to the risk that PC goes insolvent. Insolvency risk is that PC is incompetent or cannot buy futures contracts at a rate that makes the business work];

3. The furnishing of the initial value is induced by the offeror’s promises or representations that the offeree will gain some benefit, over and above the initial value, as a result of the enterprise’s operation [Hawaii - members were promised “commissions”/fixed returns]; and,

4. The offeree does not receive the right to exercise practical or actual control over the managerial decisions of the enterprise [Hawaii - members arguably participated in a minor way in operating the enterprise, but Court focused on the “quality” of participation, not the “quantity].

Distinguish: Pacific with Lazerman (this decision seems to “back-peddle” from Pacific and is likely a “better” decision). In Lazerman, the BCCA found that the contracts were not investment contracts (factual distinctions from Pacific: silver bars

instead of silver coins (there is a market for bars not coins) and Lazerman segregated purchasers’ funds instead of commingling with its own). The purchasers’ profits did not depend on Lazerman’s actions; they depended on the market price of silver. Segregating the funds meant that there was no sharing of each other’s profits or losses and were not engaged in a common enterprise.

[8] An interest in an Oil, Gas or Mining Claim: certificate of interest in an oil, natural gas or mining lease, claim or royalty voting trust certificate and oil or natural gas royalties or leases or fractional or other interest

Definition: “Trade” Whether or not a transaction qualifies as a “trade” determines whether that transaction is subject to securities regulation. Under s. 34 of the BCSA and NI 31-103, a “trade” triggers the requirement that a registered dealer be involved in the transaction, unless an exemption applies.

NB: BCSA 34: A person must not (a) trade in a security or exchange contract, (b) act as an adviser, (c) act as an investment fund manager, or (d) act as an UW, unless the person is registered in accordance with the regulations and in the category prescribed for the purpose of the activity.

BCSA, s.1(1)[a] a disposition (i.e. sell – a trade does not include a purchase; focus on the seller (e.g. Pacific Coast co.)) of a security for valuable consideration (no “other people’s money” issue if not) whether the terms of payment be on margin, installment or otherwise, but does not include a purchase of a security or a transfer, pledge, mortgage or other encumbrance of a security for the purpose of giving collateral for a debt ((a)).

Focus is on SELLING, it is a trade to sell a security but not a trade to buy a security (Hennig – Option exercise, from Hennig’s viewpoint, was effectively a purchase and, therefore, not a trade)

7

Must be a disposition for valuable consideration (Re Anchor – Gift of common shares to EE’s is not a trade if no valuable consideration).

o Gifts are not trades because there is no consideration Does not have to be in the form of money (Meyers Estate – assignment of mineral rights as consideration) Contemplated consideration is sufficient because it is an act in furtherance of a trade

[a.1] entering into a futures contract ((a.1)) + [b] entering into an option that is an exchange contract ((b)) Any ‘entering into a derivative or making a material amendment to, terminating, assigning, selling or otherwise acquiring or

disposing of a derivative is also a trade. o This INCLUDES acquiring derivatives.o No requirement that the disposition be for valuable consideration

[c] participation as a trader in a transaction in a security or exchange contract made on or through the facilities of an exchange or reported through the facilities of a quotation and trade reporting system ((c))

Captures: Activities of an agent of a broker executing securities traders through any stock exchange, quoting and trade reporting system or alternative trading system.

[d] the receipt by a registrant (i.e. dealer) of an order to buy or sell a security or exchange contract ((d)) A registrant includes traders but also anyone else engaged in the securities industries. Trade occurs when the broker receives the order, not when it is completed.

[e] a transfer of beneficial ownership of a security to a transferee, pledgee, mortgagee or other encumbrancer under a realization on collateral given for a debt ((e))

This transfer must be done by a “control person” (individual, corporation or a group holding more than 20% of an issuer’s voting rights)

[f] any act, advertisement, solicitation, conduct or negotiation directly or indirectly in furtherance of any of the other branches ((f))

LIMITS of this broad branch are difficult to establish. Takes a “contextual approach” in determining whether acts were acts in furtherance of trade OR “sufficient proximate connection” as described in Re Costello.

No actual trade need ever be completed for there to be a “trade” under this branch (E.g. if there is an ad for a trade, it is deemed to be a trade. Trying to protect ppl early on).

o E.g.: Meetings are trades, unless they are informational and not promotional // Advertising a security, I intend to issue later (as an issuer), is a trade. It is a solicitation in furtherance of a trade (very broad) // Bookkeepings and administrative functions performed by a trust company for mutual fund dealers are not trades (Re: OSC and CAP Ltd.)

Activities Found to Constitute Acts in Furtherance of Trades (Re MP Global): o (1) Accepting money from investorso (2) Depositing Cheques for Share Purchaseso (3) Providing investors with subscription agreementso (4) Distributing promotional materialso (5) Issuing share certificateso (6) Organizing meetings with investors to organize the purchasing of securities

Trade Not a Trade The granting of stock options to EE or DIRs (valuable

consideration being the EE/DIRs future or current services) Transferring shares from one company that you own to

another company that you own, provided there is valuable consideration

Converting a share from one form to another Advertising or solicitation directed at investors (even

though no securities have actually been sold yet) – this qualifies as an “act in furtherance”

A gift of securities as there is no consideration The inheritance of securities – no consideration Moving assets in divorce – no consideration A trust company managing the portfolios of mutual fund

dealers (doesn’t qualify under (f) because the trade already is already completed by the time the trust company becomes involved)

MAYBE: drafting an advertisement directed at investors or sending it to the printers, but before it’s actually published (could be argued that it’s not enough under (f))

Jurisdiction The courts tend to be liberal in granting jurisdiction – more than one province could have jurisdiction over the same

transaction o Key consideration – Where is the corporation doing business? (Bennet, Durante, World Stock) o Gregory & Co: promoter in Quebec who sent out a bulletin out of province Quebec jurisdictiono R v W McKenzie Securities: broker in Ontario who contacted Manitoba residents Manitoba jurisdiction

8

Locations Granting the Jurisdiction: reporting issuer (Torudag), corporation (Re Lehman), broker (Re Durante), investors (World Stock), promoter (Gregory)

More than one Commission can asset jurisdiction, which can lead to multiple proceedings over one occurrence (Bennett)

DistributionDEFINITION: “Distribution” (NB: Incorporates the word trade (defined above))

All distributions are trades in that they transfer securities for valuable consideration. Distributions only occur to the primary market.

o Primary Market: when an issuer issues securities directly to the publico Secondary Market: when the securities are subsequently traded between investors without involvement by the

issuer, including on stock exchanges, such as the TSX and TSX-V Distributions are a type of trade that triggers the prospectus process, which is why this characterization is important. The

definition set out in BCSA 1(1) is exhaustive. It is important to note that while all distributions involve trades, not all trades qualify as distributions.

o Prospectus: document that discloses a required set of information regarding the issuer and the securities being offered – information intended to benefit and protect potential investors

o The prospectus requirement is engaged when there is a trade that would be a distribution of a security While issuers have continuing disclosure obligations and potential liabilities in relation to secondary market purchasers, only

an issuance of securities from an issuer itself (primary market) constitutes a “distribution”.

BCSA S 1(1): A “Distribution” means, if used in relation to trading in securities,[a] Fresh Distributions of New Securities: a trade in securities that have not previously been issued (i.e. new to the market, primary market issuance) (BCSA, s. 1(1)(a))[b] Reissuances: a trade by the issuer in its own previously issued securities: trades by the issuer (or on its behalf) in securities that the issuer previously issued (incl. redeemed securities and securities purchased by the issuer on the market or donated to the issuer)[c] Distribution by Control Persons: a trade in a previously issued security of an issuer from the holdings of a control person (a person with more than 20% of the issuer’s outstanding voting securities is deemed a “control person”; however, a lower percentage than 20 may constitute control – each case must be evaluated on its particular circumstances) (BCSA, s. 1(1)(c))

When a control person trades securities, those securities must be qualified with a prospectus (Why: Control person has access to info where other security holders do not; Has vested interest to ensure selling at high price; etc.).

Someone can be a control person with less than 20% of the company’s shares (Re Deerhorn Mines/R v. Boyle)[d] Distributions by UW Before the Effective Date of Closed System: an underwriter’s trade in securities it acquired before the effective date of the closed system (no longer really relevant)[e] Commission Deemed Distributions: a trade deemed a distribution: i) in an order under s.76 by commission or executive DIR; OR ii) in the regulations (BCSA, s. 1(1)(e))

s.76(1) Residual discretion of Sec. Com. Senior staff to deem a distribution and force disclosure.[f] Transactions During/Incidental to Distribution: any transaction involving a purchase and sale or a repurchase and resale during distribution or incidental to distribution: this includes securities purchased by an underwriter during a distribution, where the underwriter plans to resell the securities (BCSA, s. 1(1)(f)). [g] a prescribed class of trade or transaction

Kinds of Distribution Registered Issuer (RI): If you make a distribution, you are a RI. Where a company wants to distribute to the public, do it either 1) Direct issue or 2) hire an underwriter (UW) (main route). This company is called an issuer. [1] Direct Issue: Issuer itself makes direct contact with potential purchasers without an investment dealer or broker (e.g. rights offerings, exempt offering with one or more institutional purchasers, crowdfunding)[2] UW Arrangements:

Underwriter Functions:o Advise on financial situation/how to structure the transactiono Assist in the distribution of their securities by finding investors & conducting the transaction with themo Perform risk-bearing function when they execute a firm commitment or bought deal by purchasing the issuers

security that they will then resello Give a “seal of approval” on IPO – solidifies company’s value to prospective investors.

How UWs are paid (UW Agreements):o Bought deal (full risk): company sells 100% of shares to the UW and the UW sells them out to the world (Kerr –

bought deal can be detrimental to investors because a purchaser has no remedy of L rescission against the issuer for misrepresentation in the prospectus, as it is the UW who sells the securities)

o Market Deal Offering (Medium Risk): Contract between issuer and UW and that the issuer cannot talk to other UWs, but the UW can test to see if can sell securities profitably

o Standby Offering (Med-Low Risk): UW commits only to purchase sec that are not sold to investors at a certain price – guarantees issuer, a minimum amount of total proceeds

9

o Best Efforts Agency Agreement (Low Risk): UW will make their “best efforts” to sell the shares, only get paid on commission.

How UWs Limit their Risk:o 1) Termination Clauses: The UW can include a market-out clause and a disaster-out clause in the underwriting

agreement. With a market-out clause, the UW can terminate the agreement if it determines, acting reasonably, that the securities cannot be marketed profitably.

These clauses are contained in an underwriting agreement, which usually is not signed until a day or two before the distribution takes place – underwriters begin their worked based on an engagement/bid letter

o 2) Invite other UWs: may have either joint and several liability or just several liability Lead underwriter handles negotiations, signatures and documentation

o 3) Disclosure of Conflicts of Interest: A potentially non-independent UW (i.e. where the UW is a subsidiary of a bank to which the issuer owes money) should make disclosers pursuant to NI 33-105, Underwriting Conflicts, and if necessary, involve an independent UW.

Underwriter Compensation: Dealers are compensated by “spreads”

Types of Secondary Trading Markets1. First Market: registered stock exchanges (e.g. TSX, TSX-V)2. Second Market: trading in securities not listed on a recognized exchange (unlisted market/over-the-counter (OTC) market) –

many debt securities and derivatives are OTC3. Third Market (upstairs-market): “face to face” or “computer to computer” trading of listed securities between institutional

investors with the help of dealers4. Fourth Market: same as the Third Market, but without dealers5. Money Market: related to, but distinct from, the second submarket; involves trades by major or primary money market

dealers (recognized by the Bank of Canada) in short-term debt securitiesa. The securities (often called “commercial paper”) issued are debt of governments and of corporations with strong credit

ratings

“Deep” secondary market: market in which many of the issuer’s securities are being traded“Liquid” secondary market: market in which there are many ready and willing buyers and sellers of the issuer’s securities“Market makers”: post bidding and asking prices to extend buying and selling prices for securities and the difference between the two prices is the “bid-ask spread”

MaterialityDEFINITION: “Materiality” BCSA 63 – must provide “full, true and pain disclosure of all material facts.” // “Misrepresentation” – means “an untrue statement of a material fact” // BCSA 85 – “provide disclosure of material change”

Material Fact (MF): Must disclose when talking about prospectuses and misrepresentation. Material Change (MC): Part of disclosure requirements and is an issue with insider trading. DIFFERENCES:

o 1) MC is narrowero 2) MC has a timing elemento 3) MC is inherently dynamic and not static like facts (e.g. doing business in a country that suffers a coup and the

government gets changed. This would be a material fact but not a material change. The fact is ambient in the world and does not individually affect you)

o 4) MF refers to the securities issued or proposed to be issued, while MC refers to any securities or a security of the issuer

Tests for Materiality: Market Impact Test (legally binding in Canada): Info is material if it is reasonable to expect that the release of that

information would have a significant impact the market price of the security. This is an objective inquiry (Coventree). o Reasonable Investor Test (used in the US + 51-102 Forms): Material fact or change is one that would be

important to a reasonable investor in making an investment decision with respect to the relevant security. Must guard against hindsight and reliance on actual market price changes (Coventree).

o Hindsight: Important to consider what could have been reasonably expected at the time the fact came to light, now what happened after – Subsequent events alone cannot determine whether something is material at the time that it occurred, but they may support or corroborate a finding of materiality found on other grounds (Re Kapusta)

Probability/magnitude test (YBM Magnex): When determining whether a contingent (future) event is material, you must weigh the likelihood of that event happening along with its severity on the stock price of the security (YBM – Probability of a formal charge in the US and look at the magnitude of that event on their business) Contextual analysis, but likely around 10% change in bottom line or employment, etc. (NB: Use as an aid to the assessment of materiality)

10

Contextual factors will be relevant to Materiality (NP 51-201, s.4.2): Consider the nature of info itself, price volatility of the issuer’s securities, the prevailing conditions in the market and the size and nature of the issuer itself.

Material Fact (BCSA s.1(1), NP 51-201 s.4.1): A fact that (when it arises) would reasonably be expected to have a significant effect on

the market price or value of the securities. Material fact is a broader idea than material change (Pezim). A change to a material fact is not necessarily a material change. It will only be if it concerns an issuer’s business, operations

or capital (i.e. Do not confuse a material change with a change in material fact) (Pezim). Letter advising of concerns by sole creditor before IPO was not a material fact, thus did not need disclosure in IPO

(Coventree) Negotiations can be a material fact – they may be material at an early stage, “well before the negotiations have reached a

point of commitment to be characterized as” a material change (AiT). Real potential for acquisition is a material fact (Re Holtby). Subsequent events alone cannot determine whether something is material at the time that it occurred, but they may

support or corroborate a finding of materiality made on other grounds (Re Kapusta)

Timing: Must consider what could have been reasonably expected at the time the fact came to light, not what happened after). External Developments (political, economic, geographic or social – such as political coup, natural disaster, etc.): may be a material fact, generally it will be a material change only if its effect on the particular issuer is both significant and uncharacteristic for the industry (NP 51-201, s.4.4)

Material Change (BCSA s.1(1)): (i) a change in the BUSINESS, OPERATIONS OR CAPITAL of the issuer that would reasonably be

expected to have a significant effect on the market price or value of a security of the issuer, or (ii) a decision to implement a change referred to in subparagraph (i) made by (A) the DIRs of the issuer, or (B) the senior

management of the issuer who believe that confirmation of the decision by the DIRs is probable … o NOT: External political, economic or social developments. o Do not engage in “super critical interpretation of the meaning of material change.” Should be willing to interpret it

broadly (Coventree). o Letter by sole crediting agency re policy change to not stop providing ratings for certain type of securities issued

= Material Change (Coventree – this was a major change in C’s biz). o Change in mineral assay results constitute material changes because it is new information about the value of an

asset (Pezim, SCC - From the point of view of investors, new information relating to a mining property (which is an asset) bears significantly on the Q of that property’s value).

o Negotiations are a material change when there is a sufficient degree of certainty that the transaction will be completed (Siddiqi – “sufficient degree of certainty” reached when parties made an informal hand shake deal).

A commitment from one party to proceed will not be sufficient to constitute material change (need both parties) (AiT).

o Intra-quarter results are not a material change as they are temporary. Only material changes needed to be disclosed b/w the prospectus receipt date and the distribution date. If it is a material change there is a legal obligation to disclose; if not a material change, it does not have to be disclosed (Kerr, SCC – Reduced jacket sales b/c warm weather).

Kerr arose out of a misrepresentation context and the analysis of materiality may be different in other contexts

Subsequent events alone cannot determine that a change is material at the time that it occurred, but they may support or corroborate a finding of materiality made on other grounds (e.g. found material based on all the evidence with increase in share price corroborating the determination (Re Kapusta – Public Oil co found oil, withheld results awaiting more tests, insiders bought shares. Share prices jump when discovery disclosed // Held: The test results had been sufficiently certain to give rise to a material change before some of the impugned trades by insiders (thus some engaged in insider trading)).

Investment Fund: A change in the business, operations or affairs of the investment fund that would be considered important by a reasonable

investor in determining whether to purchase or continue to hold a security of the investment fund Decision to implement a change by directors senior management (believe confirmation probable)

Events that may give rise to Material Change (NP 51-201 s.4.3): 1. Changes in corporate structure, such as take-overs, mergers or changes in share ownership that may affect control of the

corporation;2. Changes in capital structure (e.g. Poison Pill); 3. Changes in financial results, such as significant increase or decrease in earnings projections, changes in assets or in

accounting policies,

11

4. Changes in business and operations (e.g. significant change in corporate objectives, loss or gain of significant contracts, significant resource discoveries)

5. Acquisition or disposition, and6. Changes in credit arrangements.

Machinery BCSCn – for administrative/regulatory matters including compliance and enforcement BCSC – adjudicates on criminal & quasi-criminal matters; adjudicates on civil liability (i.e. investor lawsuits) incl. under BCSA

Part 16, 16.1

Securities Commissions- INDEPENDENT: Commissions are separate and independent from the departmental chain of command – this independence

was emphasized in the Kimber Report- PURPOSE : To administer the provincial securities act and other relevant legislation

o Regulatory purposes 1. Protect investors from unfair, improper or fraudulent practices + 2. Promote efficient capital markets and confidence in those markets

o Note: The proposed national securities act would have added a third purpose – to contribute, as part of the Canadian financial regulatory framework, to the integrity and stability of the financial system

- FUNDAMENTAL PRINCIPLES OF THE COMMISSIONS o The Ontario Securities Act has explicitly identified these principles for the OSC to consider

1. The commission may need to balance the two regulatory purposes 2. The purposes are to be achieved through ensuring timely, accurate, and efficient disclosure of

information, restricting fraud and unfair practices, and requiring high standards of fitness and business conduct

3. The commission must administer and enforce its statutory remit in a timely, open and efficient manner

4. Properly supervised SROs should be used for their enforcement capability and regulatory exercise 5. Securities regimes should be harmonized and coordinated

Applied in Re BioCapital Biotechnology – it is in public interest that the rules we administer be applied in a harmonious manner with the rules of other jurisdictions, unless there is a clear public police for a contrary application

6. Regulatory costs and restrictions should be proportionate to the regulatory objectives’ significance o Ontario’s 2003 Crawford Report – 4 more principles (not legislatively incorporated)

Advancing investor education, Maintaining Ontario’s competitive position in the face of increasing internationalization, Facilitating innovation, Facilitating and promoting competition among market participants

o 2009 Hockin Report – 6 more principles (not legislatively incorporated) Reducing systemic risk, proportionality between restrictions on market participants and the benefits

realized, fostering the competitiveness of Canada’s capital markets internationally, facilitating innovation in capital markets, promoting investor participation in securities regulation, recognizing regional markets and sectors

BC Securities Commission Regulatory commission can make Rules that are very similar to government regulations, but they can be created without

going through the legislative process. 2 Tier Structure: Separates Advocate (Staff – may seek order against some) + Judge (Commission – make order)

o Level 1 – “Official Commission”: Describes the first level of the commission which consists of up to 11 staff members. Appointed. They generate policy and make decisions in administrative enforcement proceedings (incl. appeals and hearings) (BCSA s.4)

Subject to term limits set out in the Administrative Tribunals Act and may be reappointed. Powers:

Appoint experts; Investigate and examine; Supervise registrants, trading in general (including advertising), prospectuses and distributions,

continuous disclosure, proxies, takeover and issuer bids, and insider trading and self-dealing; and Enforce the legislation and impose sanctions.

o Level 2 – Staff: Commission must appoint a person to be the executive director and chief administrative officer, who runs staff. Staff employed through contract. Powers include investigation, supervising registrants, trading, prospectuses, distribution, continuous disclosure, proxies, TOBs, insider trading, self-dealing, enforcement of legislation including sanctions, and delegating responsibility to SROs (BCSA s.8).

Rule Making Authority (BCSA 184-188): BC Sec Commission given rule making authority following the Ainsley Corp decision.

12

BCSA 184 – Commission can make binding law themselves (i.e. if signing onto a MI and NI) “Notice-and-comment” rule making (faster than legislation):

o Propose a rule and have to wait a certain amount of time (e.g. 60 days) for comments from people.o At the end of the comment period, they must issue another version of the rule and justify.o Publish the rule again and go through another comment period.o Then issue the rule and it becomes a binding piece of law.

BCSA 187 – Administrative powers re: Commission rules.

Organizational Bias Concerns: 1. Regulators attempt to increase their own power and influence, even if such expansion goes beyond their justifiable scope of

authority2. Agencies may over-regulate and be over-conservative to protect themselves from failure3. Policy will tend to focus on unquestioned internal rhetoric, perhaps discarding useful ideas from outside.

NB: Efforts to harmonize regulation across provinces (e.g. harmonizing definition of “insider trading”).

National Instruments & Policies (have legal force under BCSA ss.184, 187) NI: Binding law effective in all jurisdictions. MI: Binding law that not all the provinces have agreed to (anything on BC securities commission website has been agreed

to). o CP: Companion Policy – Explains the instrument (MI & NI)

NP: Not binding (policy) but provides guidance on how things are interpreted and it is national so everyone has agreed to it. MP: Multilateral Policy

Self-Regulatory OrganizationsCommissions delegate substantial “front line” regulatory responsibility to Self-Regulatory Organizations (SROs) and to the Exchanges.BCSA Part 4 – Self-regulating bodies, exchanges, Quotation and Trade Reporting systems and Clearing Agencies

s.23: Self-regulatory bodies include exchanges, self-regulating organizations, quotation and trade reporting systems, and clearing agencies // s.27: Powers of the Commission are broad, and can take actions to control SROs // s.28: Appeals from a regulatory body will go to the Executive for approval, who will in turn, have it heard by the upper level of the Commission // s.31: SROs must appoint an auditor.

Main SROs: Investment Industry Regulatory Organization of Canada (IIROC): Carries out its regulatory responsibilities through

setting and enforcing rules regarding the proficiency, business and financial conduct of dealer firms and their registered EEs and through setting and enforcing market integrity rules regarding trading activity on Canadian marketplaces.

Mutual Fund Dealers Association (MFDA): SRO for the distribution side of the Canadian mutual fund industry. The MFDA is structured as a not-for-profit corporation and its Members are mutual fund dealers that are licensed with provincial securities commissions.

Main Exchanges: TSX: Main exchange for senior issuers. Important listing requirements include: financial condition and prospects,

management, and sponsorship TSX-V: Pre-dominantly for emerging companies and their venture class securities.

Procedural FairnessThere is a presumption that administrative tribunals will operate in accordance with the principals of procedural fairness:

1. A person must have an adequate opportunity to be heard before the decision-maker reaches a conclusion2. The decision-maker must not have an interest in the outcome of the decision

Enforcement Procedure of Commissions1. Complaint2. Informal/Preliminary Investigation3. Formal Investigation

a. Reasons: due administration of securities law or regulation of capital markets in the provinceb. Must be initiated by an orderc. Investigator’s power: investigating the affairs and assets of the person being investigated, as well as past and

present assets, liabilities, financial relationships, etc., force attendance of any person, compel testimony, compel production of documents, inspect documents or other things on the business premises and search and seizure with a court order

d. Protections for those investigated: compelled testimony cannot be used against them in offence proceedings, investigators cannot compel production of materials protected by solicitor-client privilege, anyone giving evidence has the right to counsel and to other traditional privileges, private residences are not subject to search and seizure,

13

reports to the Chair or Commission are privileged and confidential and no disclosure is allowed of the examinee’s name or any information revealed in the examination.

4. Orders without a Full Hearinga. Initiating an investigationb. Applying to court for a declaration of non-compliance with the province’s securities lawsc. Freezing fundsd. Temporary orders in the public interest (e.g. suspending, restricting, terminating or imposing terms on registration or

recognition, ceasing trading in or purchasing of securities, removing exemptions)5. Hearing

a. Factors to consider when deciding to hold a joint hearing with a different jurisdiction:i. The issues and arguments are substantially the same in the jurisdictions

ii. There are urgent business reasonsiii. The issue is novel, such that the public interest favours a joint hearing to promote consistency across

jurisdictions6. Appeal to Court of Appeal

Reviews and Appeals (Part 19 BCSA)OVERVIEW: Enforcement by staff Appeal to BC Sec Comm (BCSA 165) Appeal to BCCA (BCSA 167) Appeal to SCC

1. Internal Review: Commission may review a decision of the executive director (BCSA 165(2))2. Review of SRO or Exchange Decision: Executive Director or person “directly affected” by a decision or instrument of an

exchange or SRO may apply to the Commission for a hearing and review or appeal (BCSA 28)3. Judicial Review of Commissions’ Decisions: Limited use given must exhaust statutory right of appeal (below).

a. Grounds: alleged failure of procedural fairness, substantial judicial review on the merits, based ona standard of review of either reasonableness or correctness

4. Statutory Right of Appeal to BCCA* (BCSA 167(1)): A person directly affected by a decision of the commission may appeal to the Court of Appeal with leave of a justice of that court. Exception: Cannot review a decision under 165 if connection w/ review of Ex Dir decision under s.48 or 76.

6 Factors the appellate body considers whether to grant leave to appeal from securities tribunal (Walker v. BCSCn):1. Whether there is a Q of general importance as to the tribunal’s jurisdiction; 2. Whether appeal is on Qs of law involving statutory application, interpretation important to parties or interpretation of

standard statutory wording;3. Whether previous decisions show marked differences of opinion;4. Whether prospect of success;5. Whether appeal will lead to any clear benefit; and6. Whether the issue has been considered by numerous appellate bodies.

SofR: that normally apply to Judicial Reviews have been imported into the statutory appeal context: 1) Reasonableness, or 2) Correctness.

Factors to Consider when Determining whether to grant a Stay:1. Whether there is a serious issue to be tried;2. Whether irreparable harm will occur if the stay is granted or not granted (some evidence is required); and3. Where the balance of convenience lies (harm to the public interest weighed against harm to the impugned party).

Industry Best PracticeCanadian Coalition of Good Governance (CCGG): Represents the interests of institutional investors; CCGG promotes good governance practices in Canadian public companies and the improvement of the regulatory environment to best align the interests of boards and management with those of their shareholders, and to promote the efficiency and effectiveness of the Canadian capital markets.

National and Coordinated Approaches to Securities RegulationSystematic Risk

Definition (SCC): risks that occasion a “domino effect” whereby the risk of default by one market participant will impact the ability of others to fulfil their legal obligations, setting off a chain of negative economic consequences that pervade an entire financial system

Definition (Financial Stability Board): the disruption to the flow of financial services that is (i) caused by an impairment of all or parts of the financial system; and (ii) has the potential to have serious negative consequences for the real economy

Definition (International Organization of Securities Commissions): the potential that an event, action, or series of events or actions will have a widespread adverse effect on the financial system and, in consequence, on the economy

Criteria:o Size: volume of financial services provided by the individual component in the financial system

14

o Substitutability: extent to which other components of the system can provide the same services in the event of a failure

o Interconnectedness: linkages with other components of the system Other important indicators of vulnerability: degree of leverage, liquidity risks and large maturity mismatches between assets

and structural complexity

Reference Re Securities Act Issue: whether the Proposed Act addresses a matter of genuine national importance and scope going to trade as a whole in a

way that is distinct and different from provincial concerns SCC held that the Proposed Act did not fall within the federal government’s general trade and commerce powers under s.

91(2) of the Constitution Act Fed gov’t can have a role in securities regulation because it has jurisdiction over managing systematic risk and national data

collection

Options After the Reference The federal government, with one or more provinces, can create a common regulator

o Wanting to create the Cooperative Capital Markets Regulator (CCMR) with a regulatory division, independent adjudicative division and a “regulatory policy forum for consultation on policy issues”

Federal government can create a scheme that does not intrude on day-to-day aspects of securities regulation, but touches on aspects relating to national concern, such as systematic risk

o If the plan of creating a common regulator fails, the federal government will allocate systematic risk responsibilities to an existing federal regulator

o Must do so with the provinces since managing systematic risk is part of the day-to-day operations of securities’ markets

Similar legislation can be introduced through the federal government’s power under the interprovincial and international trade branch of s. 91(2)

The Prospectus Process The prospectus is generally a lengthy document that sets out the details of the company, business, management, finances,

existing securities and the securities being offeredo Should be in narrative form and may include graphs, photographs, maps, artwork and other forms of illustration

PENALTIES FOR NON-DISCLOSURE: s.135 Failure to Deliver Documents: Right of action against a company that has failed to deliver or file a prospectus s.162 Administrative Penalty: if (a) Contravention and (b) in the Public Interest, the commission may order a penalty of not

more than $1million s.164 Failure of Filing Requirements: Cease trade order without hearing s.161 Enforcement Orders: Doesn’t even need a breach, just a preventative tactic s 155 Quasi-criminal for violation of s 61 s.155.1 Restitution to Securities Commission s.157 Orders of Compliance in the Public Interest Part 16 statutory civil liability: prospectus misrepresentation (s. 131) S 81: cease trade for defective PP (s 63 compliance)

Prospectus Required and Reporting IssuerProspectus Required BCSA s 61