Embed Size (px)

Citation preview

CONTRA COSTA COUNTY ASSESSMENT PRACTICES SURVEY

MARCH 2015

CALIFORNIA STATE BOARD OF EQUALIZATION SEN. GEORGE RUNNER (RET.), LANCASTER FIRST DISTRICT FIONA MA, CPA, SAN FRANCISCO SECOND DISTRICT JEROME E. HORTON, LOS ANGELES COUNTY THIRD DISTRICT DIANE L. HARKEY, ORANGE COUNTY FOURTH DISTRICT BETTY T. YEE STATE CONTROLLER

______________

CYNTHIA BRIDGES, EXECUTIVE DIRECTOR

STATE OF CALIFORNIA

STATE BOARD OF EQUALIZATION PROPERTY TAX DEPARTMENT 450 N STREET, SACRAMENTO, CALIFORNIA PO BOX 942879, SACRAMENTO, CALIFORNIA 94279-0064 1-916-274-3350 FAX 1-916-285-0134 www.boe.ca.gov March 18, 2015

TO COUNTY ASSESSORS:

CONTRA COSTA COUNTY ASSESSMENT PRACTICES SURVEY

A copy of the Contra Costa County Assessment Practices Survey Report is enclosed for your information. The Board of Equalization (BOE) completed this survey in fulfillment of the provisions of sections 15640-15646 of the Government Code. These code sections provide that the BOE shall make surveys in each county and city and county to determine that the practices and procedures used by the county assessor in the valuation of properties are in conformity with all provisions of law.

The Honorable Gus S. Kramer, Contra Costa County Assessor, was provided a draft of this report and given an opportunity to file a written response to the findings and recommendations contained therein. The report, including the assessor's response, constitutes the final survey report, which is distributed to the Governor, the Attorney General, and the State Legislature; and to the Contra Costa County Board of Supervisors, Grand Jury, and Assessment Appeals Board.

Fieldwork for this survey was performed by the BOE's County-Assessed Properties Division from March through April 2013. The report does not reflect changes implemented by the assessor after the fieldwork was completed.

Mr. Kramer and his staff gave their complete cooperation during the survey. We gratefully acknowledge their patience and courtesy during the interruption of their normal work routine.

Sincerely,

/s/ Dean R. Kinnee

Dean R. Kinnee Deputy Director Property Tax Department

DRK:dcl Enclosure

SEN. GEORGE RUNNER (RET.) First District, Lancaster

FIONA MA, CPA Second District, San Francisco

JEROME E. HORTON Third District, Los Angeles County

DIANE L. HARKEY Fourth District, Orange County

BETTY T. YEE State Controller

_______

CYNTHIA BRIDGES Executive Director

No. 2015/015

Contra Costa County Assessment Practices Survey March 2015

i

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................... 1 OBJECTIVE ................................................................................................................................. 2 SCOPE AND METHODOLOGY ............................................................................................... 2 EXECUTIVE SUMMARY .......................................................................................................... 4 OVERVIEW OF CONTRA COSTA COUNTY ........................................................................ 6 FINDINGS AND RECOMMENDATIONS ............................................................................... 7 ASSESSMENT OF REAL PROPERTY .................................................................................... 8

CHANGE IN OWNERSHIP ............................................................................................................... 8 MINERAL PROPERTY .................................................................................................................... 9

ASSESSMENT OF PERSONAL PROPERTY AND FIXTURES ......................................... 11 BUSINESS PROPERTY STATEMENT PROGRAM ............................................................................. 11

APPENDIX A: STATISTICAL DATA .................................................................................... 12 TABLE 1: ASSESSMENT ROLL ...................................................................................................... 12 TABLE 2: CHANGE IN ASSESSED VALUES ..................................................................................... 12 TABLE 3: GROSS BUDGET AND STAFFING .................................................................................... 13 TABLE 4: ASSESSMENT APPEALS ................................................................................................. 13 TABLE 5: CHANGE IN OWNERSHIP ............................................................................................... 14 TABLE 6: NEW CONSTRUCTION ................................................................................................... 14 TABLE 7: DECLINES IN VALUE .................................................................................................... 15

APPENDIX B: COUNTY-ASSESSED PROPERTIES DIVISION SURVEY GROUP ...... 16 APPENDIX C: RELEVANT STATUTES AND REGULATIONS ....................................... 17 ASSESSOR'S RESPONSE TO BOE'S FINDINGS ................................................................ 18

Contra Costa County Assessment Practices Survey March 2015

1

INTRODUCTION Although county government has the primary responsibility for local property tax assessment, the State has both a public policy interest and a financial interest in promoting fair and equitable assessments throughout California. The public policy interest arises from the impact of property taxes on taxpayers and the inherently subjective nature of the assessment process. The financial interest derives from state law that annually guarantees California schools a minimum amount of funding; to the extent that property tax revenues fall short of providing this minimum amount of funding, the State must make up the difference from the general fund.

The assessment practices survey program is one of the State's major efforts to address these interests and to promote uniformity, fairness, equity, and integrity in the property tax assessment process. Under this program, the State Board of Equalization (BOE) periodically reviews the practices and procedures (surveys) of every county assessor's office. This report reflects the BOE's findings in its current survey of the Contra Costa County Assessor's Office.

The assessor is required to file with the board of supervisors a response that states the manner in which the assessor has implemented, intends to implement, or the reasons for not implementing the recommendations contained in this report. Copies of the response are to be sent to the Governor, the Attorney General, the BOE, and the Senate and Assembly; and to the Contra Costa County Board of Supervisors, Grand Jury, and Assessment Appeals Board. That response is to be filed within one year of the date the report is issued and annually thereafter until all issues are resolved. The Honorable Gus S. Kramer, Contra Costa County Assessor, elected to file his initial response prior to the publication of our survey; it is included in this report following the Appendixes.

Contra Costa County Assessment Practices Survey March 2015

2

OBJECTIVE The survey shall "…show the extent to which assessment practices are consistent with or differ from state law and regulations."1 The primary objective of a survey is to ensure the assessor's compliance with state law governing the administration of local property taxation. This objective serves the three-fold purpose of protecting the state's interest in the property tax dollar, promoting fair treatment of taxpayers, and maintaining the overall integrity and public confidence in the property tax system in California.

The objective of the survey program is to promote statewide uniformity and consistency in property tax assessment, review each county's property assessment practices and procedures once every five years, and publish an assessment practices survey report. Every assessor is required to identify and assess all properties located within the county – unless specifically exempt – and maintain a database or "roll" of the properties and their assessed values. If the assessor's roll meets state requirements, the county is allowed to recapture some administrative costs.

SCOPE AND METHODOLOGY Government Code sections 15640 and 15642 define the scope of an assessment practices survey. As directed by those statutes, our survey addresses the adequacy of the procedures and practices employed by the assessor in the valuation of property, the volume of assessing work as measured by property type, and the performance of other duties enjoined upon the assessor.

Pursuant to Revenue and Taxation Code2 section 75.60, the BOE determines through the survey program whether a county assessment roll meets the standards for purposes of certifying the eligibility of the county to continue to recover costs associated with administering supplemental assessments. Such certification is obtained either by satisfactory statistical result from a sampling of the county's assessment roll, or by a determination by the survey team—based on objective standards defined in regulation—that there are no significant assessment problems in the county.

This survey included an assessment sample of the 2012-13 assessment roll to determine the average level (ratio) of assessment for all properties and the disparity among assessments within the sample. The ideal assessment ratio is 100 percent, and the minimum acceptable ratio is 95 percent. Disparity among assessments is measured by the sum of absolute differences found in the sample; the ideal sum of absolute differences is 0 percent and the maximum acceptable number is 7.5 percent. If the assessment roll meets the minimum standards for ratio and disparity, the county is eligible to continue to recover the administrative cost of processing supplemental assessments.3

1 Government Code section 15642. 2 Unless otherwise stated, all statutory references are to the California Revenue and Taxation Code and all rule references are to sections of California Code of Regulations, Title 18, Public Revenues. 3 For a detailed description of the scope of our review of this topic, please refer to the document entitled Assessment Sampling Program, available on the BOE's website at http://www.boe.ca.gov/Assessors/pdf/assessmentsamplingprogram.pdf. Additionally, detailed descriptions of

Contra Costa County Assessment Practices Survey March 2015

3

Our survey methodology of the Contra Costa County Assessor's Office included reviews of the assessor's records, interviews with the assessor and his staff, and contacts with officials in other public agencies in Contra Costa County who provided information relevant to the property tax assessment program.

For a detailed description of the scope of our review of county assessment practices, please refer to the document entitled Scope of Assessment Practices Surveys, available on the BOE's website at http://www.boe.ca.gov/Assessors/pdf/Scopemaster.pdf.

We conducted reviews of the following areas:

• Administration

We reviewed the assessor's administrative policies and procedures that affect both the real property and business property assessment programs. Specific areas reviewed include the assessor's budget and staffing, workload, staff property and activities, and assessment appeals.

• Assessment of Real Property

We reviewed the assessor's program for assessing real property. Specific areas reviewed include properties having experienced a change in ownership, new construction assessments, decline-in-value assessments, and certain properties subject to special assessment procedures, such as mineral property.

• Assessment of Personal Property and Fixtures

We reviewed the assessor's program for assessing personal property and fixtures. Specific areas reviewed include conducting audits, processing business property statements, and business equipment valuation.

assessment practices survey topics, authoritative citations, and related information can be found at http://www.boe.ca.gov/proptaxes/apscont.htm.

Contra Costa County Assessment Practices Survey March 2015

4

EXECUTIVE SUMMARY This report offers recommendations to help the assessor correct assessment problems identified by the survey team. The survey team makes recommendations when assessment practices in a given area are not in accordance with property tax law or generally accepted appraisal practices. An assessment practices survey is not a comprehensive audit of the assessor's entire operation. The survey team does not examine internal fiscal controls or the internal management of an assessor's office outside those areas related to assessment. In terms of current auditing practices, an assessment practices survey resembles a compliance audit – the survey team's primary objective is to determine whether assessments are being made in accordance with property tax law.

Over the past several years, the assessor has developed and instituted a number of technological enhancements to improve and streamline the office workload, as well as improve customer service to taxpayers. Some of the enhancements made by the assessor are:

• Completed programming changes and finished training staff on the new transaction-based Land Information System (LIS) upgrade, which has improved efficiencies and streamlined the workflow between the appraisal staff and support staff.

• Created a computer application to automate the assessor's direct enrollment process, which resulted in eliminating the need to manually encode individual direct enrollment transactions.

• Developed a computer program to identify and streamline the reappraisal of commercial and multi-family residence property types due to temporary declines in value.

• Created a preset filing template to enable taxpayers who report leased equipment to file their business property statements by email.

• Developed an online transaction report to assist supervisors and managers in monitoring staff's progress in completing work activities throughout the assessment year.

• Updated the assessor's website to include online forms, information on tax savings programs, and key links to other Contra Costa County departments' websites, outside agencies' websites, and the county's Geographic Information System (GIS) website.

• Partnered with the clerk-recorder's office to image all Preliminary Change of Ownership Reports (PCOR) received in order to make the PCORs available electronically through a newly created database.

The following areas concern portions of programs which are currently effective, but need improvement. In many instances, the assessor is already aware of the need for improvement and is considering changes as time and resources permit.

Contra Costa County Assessment Practices Survey March 2015

5

In the area of administration, the assessor is effectively managing staffing, workload, staff property and activities, and assessment appeals.

In the area of real property assessment, the assessor has effective programs for new construction and declines in value. However, we made recommendations for improvement in the change in ownership and mineral property programs.

In the area of personal property and fixtures assessment, the assessor has effective programs for audits and business equipment valuation. However, we made a recommendation for improvement in the business property statement program.

Despite the recommendations noted in this report, we found that most properties and property types are assessed correctly, and that the overall quality of the assessment roll meets state standards.

The Contra Costa County assessment roll meets the requirements for assessment quality as established by section 75.60. Our sample of the 2012-13 assessment roll indicated an average assessment ratio of 99.88 percent, and the sum of the absolute differences from the required assessment level was 0.12 percent. Accordingly, the BOE certifies that Contra Costa County is eligible to receive reimbursement of costs associated with administering supplemental assessments.

Contra Costa County Assessment Practices Survey March 2015

6

d it Bay iles, iles

ne of

San an e

8,257. There are

OVERVIEW OF CONTRA COSTA COUNTY Contra Costa County is located in northwest California, anis one of the nine counties that make up the San Francisco Area. The county encompasses a total area of 804 square mconsisting of 716 square miles of land area and 88 square mof water area. Created in 1850, Contra Costa County was oCalifornia's original 27 counties. Contra Costa County is bordered by Solano and Sacramento Counties to the north,Joaquin County to the east, Alameda County to the south, SFrancisco County to the southwest, and Marin County to thnorthwest.

As of 2012, Contra Costa County had a population of 1,0719 incorporated cities in Contra Costa County. The county seat is Martinez. The Mount Diablo State Park and the John Muir National Historic Site are points of interest located in Contra Costa County.

Contra Costa County Assessment Practices Survey March 2015

7

FINDINGS AND RECOMMENDATIONS As noted previously, our review concluded that the Contra Costa County assessment roll meets the requirements for assessment quality established by section 75.60. This report does not provide a detailed description of all areas reviewed; it addresses only the deficiencies discovered.

Following is a list of the formal recommendations contained in this report.

RECOMMENDATION 1: Improve the change in ownership program by not sending a notice of penalty letter to a property owner when making an initial request for completion of a COS........................................................................................9

RECOMMENDATION 2: Measure declines in value for mineral properties using the entire appraisal unit as required by Rule 469. ............................10

RECOMMENDATION 3: Conduct an audit or field review when property owners fail to file a BPS for three or more consecutive years. ...............11

Contra Costa County Assessment Practices Survey March 2015

8

ASSESSMENT OF REAL PROPERTY Change in Ownership

Section 60 defines change in ownership as a transfer of a present interest in real property, including the beneficial use thereof, the value of which is substantially equal to the value of the fee simple interest. Sections 61 through 69.5 further clarify what is considered a change in ownership and what is excluded from the definition of a change in ownership for property tax purposes. Section 50 requires the assessor to enter a base year value on the roll for the lien date next succeeding the date of the change in ownership; a property's base year value is its fair market value on the date of the change in ownership.4

We examined several recorded documents and found that the assessor conducts a proper and thorough review of recorded documents experiencing a change in ownership. In addition, we reviewed several property records recently involving a change in ownership and found that the assessor is following proper valuation procedures. However, we found an area in the change in ownership program that is in need of improvement.

Penalties

When a recorded document is received without a BOE-502-A, Preliminary Change of Ownership Report (PCOR), or the PCOR is incomplete, the assessor will send the property owner a county-developed Change in Ownership Statement questionnaire, along with a cover letter requesting that the property owner return the questionnaire within 15 days from the date of the letter. The questionnaires are tracked in the computer system. After approximately 30 days, if the questionnaire is not returned, the assessor will send a second questionnaire. No time-limit is given on the second request. Once a year, the assessor sends out BOE-502-AH, Change in Ownership Statements (COS), to all property owners who failed to return a second requested questionnaire. If the property owner fails to return the requested COS within 90 days, a penalty is applied. The county board of supervisors has adopted Resolution No. 87-61 pursuant to section 483(b), which allows the assessor to automatically abate penalties if the COS is returned to the assessor within 60 days from the date of the notice of penalty.

We found an area in need of improvement when applying the penalty abatement process.

4 For a detailed description of the scope of our review of this topic, please refer to the document entitled Change in Ownership, available on the BOE's website at http://www.boe.ca.gov/Assessors/pdf/cio_general.pdf. Additionally, detailed descriptions of assessment practices survey topics, authoritative citations, and related information can be found at http://www.boe.ca.gov/proptaxes/apscont.htm.

Contra Costa County Assessment Practices Survey March 2015

9

RECOMMENDATION 1: Improve the change in ownership program by not sending a notice of penalty letter to a property owner when making an initial request for completion of a COS.

When a property owner fails to return a second requested county-developed Change in Ownership Statement questionnaire, the assessor sends a COS to the property owner, along with a cover letter stamped "PENALTY NOTICE." This is the assessor's first request to have the property owner file a COS. The assessor's penalty notice letter states, in part:

This is to notify you that the change in ownership statement requested pursuant to Section 480 (on back) of the California Revenue and Taxation Code has not been received by this office.

However, this is the assessor's first request to have the property owner file a COS. The assessor's notice of penalty letter goes on to state:

Failure to file this statement in a timely manner requires the penalty prescribed by the provisions of Section 482 (on back) of the Revenue and Taxation Code be imposed. Under the requirements of law, we are enrolling the penalty and it will be added to the current year's property taxes.

However, the property owner has 90 days to file the requested COS before a penalty may be applied. The assessor's notice of penalty letter is incorrectly informing the property owner that a penalty is already applicable at the time of request to file the COS.

Section 482(a) provides that if a person or legal entity required to file a change in ownership statement as described in section 480 fails to do so within 90 days from the date of a written request from the assessor, a specific penalty applies. The assessor should revise his procedure and send the notice of penalty letter only after 90 days have passed and the property owner has failed to respond to the assessor's request to file a COS.

Mineral Property

By statute and case law, mineral properties are taxable as real property. They are subject to the same laws and appraisal methodology as all real property in the state. However, there are three mineral-specific property tax rules that apply to the assessment of mineral properties. They are Rule 468, Oil and Gas Producing Properties, Rule 469, Mining Properties, and Rule 473, Geothermal Properties. These rules are interpretations of existing statutes and case law with respect to the assessment of mineral properties.5

After reviewing the assessor's mineral property program, we have the following recommendation: 5 For a detailed description of the scope of our review of this topic, please refer to the document entitled Mineral Property, available on the BOE's website at http://www.boe.ca.gov/Assessors/pdf/mineralprop_general.pdf. Additionally, detailed descriptions of assessment practices survey topics, authoritative citations, and related information can be found at http://www.boe.ca.gov/proptaxes/apscont.htm.

Contra Costa County Assessment Practices Survey March 2015

10

RECOMMENDATION 2: Measure declines in value for mineral properties using the entire appraisal unit as required by Rule 469.

We found that when measuring for declines in value for mineral properties, the assessor does not combine the values for mineral rights, improvements (including fixtures), and land into one value for a total appraisal unit value when determining whether to enroll the adjusted base year value or the current market value. The assessor's real property section determines the value of the mineral rights using the royalty method, while the business property section determines the value of the fixtures associated with the mineral property. These values determined by the two separate sections are not combined into a single appraisal unit value. Instead, fixtures are treated as a separate appraisal unit for the purpose of determining a decline in value of such fixtures. This procedure conflicts with Rule 469(e)(2)(C).

Under article XIII A, all real property receives a base year value and, on each lien date, the taxable value of the real property unit should be the lesser of its adjusted base year value or current market value. Section 105 defines fixtures as a type of improvement and, hence, as real property.

For most properties, fixtures are treated as a separate appraisal unit for the purpose of determining a decline in value. Mineral properties, however, are treated differently. Rule 469(e)(2)(C) specifically defines the appraisal unit of a mineral property to include land, improvements including fixtures, and reserves. The assessor should use this unit for the purpose of measuring a possible decline in value.

In order for the assessor to determine which value to enroll, the assessor should determine the current market value of the entire appraisal unit and compare it to the adjusted base year value of the entire appraisal unit, enrolling the lower of the two values. To properly determine the adjusted base year value of the appraisal unit, the adjusted base year value of the fixtures needs to be tracked and added to the adjusted base year value of the other components of the appraisal unit.

Failure to properly determine the decline in value of a mineral property by not comparing the adjusted base year value of the entire appraisal unit to the current market value of the entire appraisal unit is contrary to Rule 469 and may cause the assessor to enroll incorrect assessments.

Contra Costa County Assessment Practices Survey March 2015

11

ASSESSMENT OF PERSONAL PROPERTY AND FIXTURES

Business Property Statement Program

Section 441 requires that each person owning taxable personal property (other than a manufactured home) having an aggregate cost of $100,000 or more annually file a business property statement (BPS) with the assessor; other persons must file a BPS if requested by the assessor. Property statements form the backbone of the business property assessment program.6

We reviewed all major aspects of the assessor's BPS program, including processing procedures, use of Board-prescribed forms, application of penalties, coordination with the real property division, and record storage and retention. In addition, we reviewed several recently processed BPSs. We found that in all cases observed, BPSs accepted by the assessor evidenced the proper usage of Board-prescribed forms, were completed in sufficient detail, and were properly signed.

Our review also included verifying the assessor's procedures for processing late and non-filed BPSs. We found that the assessor properly applies the late-filing penalty as required by section 463. Overall, the assessor's BPS processing program is effectively managed. However, we found an area in need of improvement.

RECOMMENDATION 3: Conduct an audit or field review when property owners fail to file a BPS for three or more consecutive years.

We found that the assessor sets no formal limits on the number of consecutive years a business property owner may fail to file a BPS before the assessor either visits the location of the taxable property or conducts an audit.

Section 501 requires the assessor to estimate the value of business property belonging to anyone who does not comply with the reporting requirements. If a BPS was received during the previous year, it is usually reasonable to use the reported cost data as a basis for estimating the current year's value. However, when allowing estimated assessments to continue for several years without any new information, the values become increasingly susceptible to error. This practice may lead to erroneous value conclusions. Therefore, estimated assessments based on prior years reporting should be limited to three consecutive roll years.

6 For a detailed description of the scope of our review of this topic, please refer to the document entitled Business Property Statement Program, available on the BOE's website at http://www.boe.ca.gov/Assessors/pdf/businesspropstatement_general.pdf. Additionally, detailed descriptions of assessment practices survey topics, authoritative citations, and related information can be found at http://www.boe.ca.gov/proptaxes/apscont.htm.

Contra Costa County Assessment Practices Survey March 2015

12 Appendix A

APPENDIX A: STATISTICAL DATA Table 1: Assessment Roll

The following table displays information pertinent to the 2012-13 assessment roll:7

PROPERTY TYPE ENROLLED VALUE

Secured Roll Land $56,013,341,489

Improvements $83,268,482,327

Personal Property $1,678,673,618

Total Secured $140,960,497,434

Unsecured Roll Land $217,271,524

Improvements $3,279,646,332

Personal Property $2,225,809,575

Total Unsecured $5,722,727,431

Exemptions8 ($4,916,193,721)

Total Assessment Roll $141,767,031,144

Table 2: Change in Assessed Values

The next table summarizes the change in assessed values over recent years:9

ROLL YEAR

TOTAL ROLL VALUE

CHANGE STATEWIDE CHANGE

2012-13 $141,767,031,000 1.2% 1.4%

2011-12 $140,127,254,000 -0.5% 0.1% 2010-11 $140,846,079,000 -3.4% -1.9% 2009-10 $145,817,480,000 -7.2% -2.4% 2008-09 $157,095,329,000 0.2% 4.7%

7 Statistics provided by BOE-822, Report of Assessed Values By City, 7 Contra Costa County, for year 2012. 8 The value of the Homeowners' Exemption is excluded from the exemptions total. 9 State Board of Equalization Annual Report, Table 7.

Contra Costa County Assessment Practices Survey March 2015

13 Appendix A

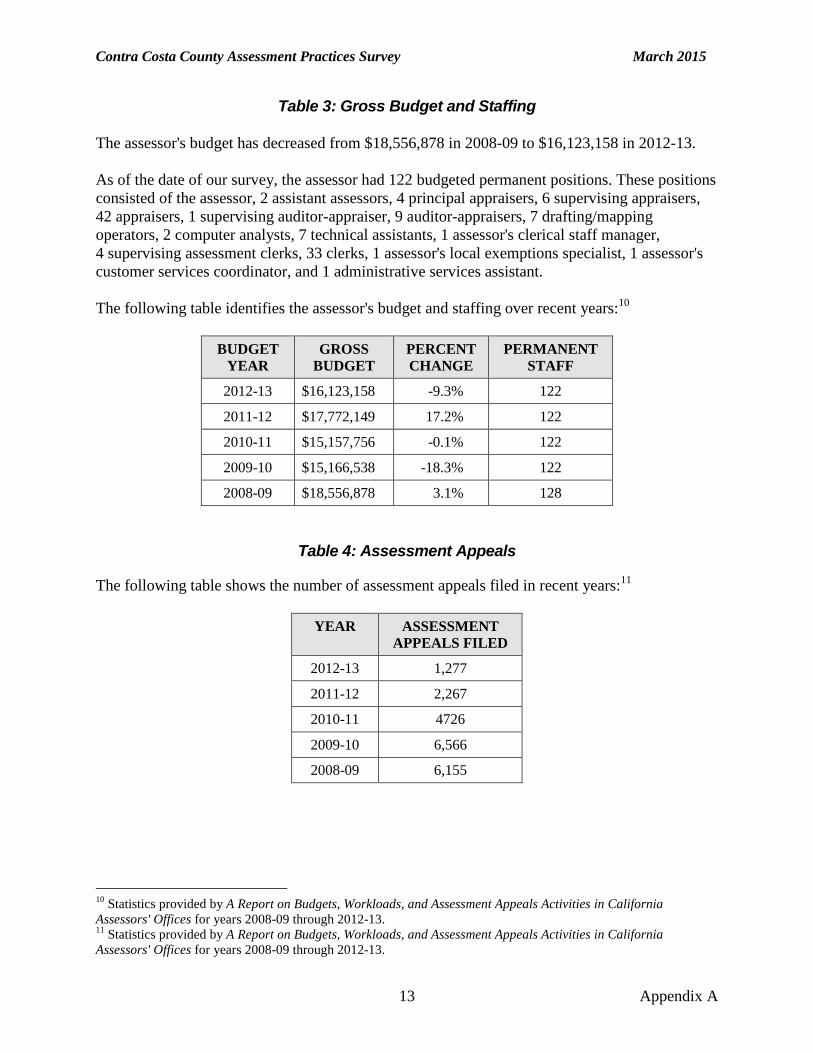

Table 3: Gross Budget and Staffing The assessor's budget has decreased from $18,556,878 in 2008-09 to $16,123,158 in 2012-13. As of the date of our survey, the assessor had 122 budgeted permanent positions. These positions consisted of the assessor, 2 assistant assessors, 4 principal appraisers, 6 supervising appraisers, 42 appraisers, 1 supervising auditor-appraiser, 9 auditor-appraisers, 7 drafting/mapping operators, 2 computer analysts, 7 technical assistants, 1 assessor's clerical staff manager, 4 supervising assessment clerks, 33 clerks, 1 assessor's local exemptions specialist, 1 assessor's customer services coordinator, and 1 administrative services assistant. The following table identifies the assessor's budget and staffing over recent years:10

BUDGET YEAR

GROSS BUDGET

PERCENT CHANGE

PERMANENT STAFF

2012-13 $16,123,158 -9.3% 122

2011-12 $17,772,149 17.2% 122

2010-11 $15,157,756 -0.1% 122

2009-10 $15,166,538 -18.3% 122

2008-09 $18,556,878 3.1% 128

Table 4: Assessment Appeals

The following table shows the number of assessment appeals filed in recent years:11

YEAR ASSESSMENT APPEALS FILED

2012-13 1,277

2011-12 2,267

2010-11 4726

2009-10 6,566

2008-09 6,155

10 Statistics provided by A Report on Budgets, Workloads, and Assessment Appeals Activities in California Assessors' Offices for years 2008-09 through 2012-13. 11 Statistics provided by A Report on Budgets, Workloads, and Assessment Appeals Activities in California Assessors' Offices for years 2008-09 through 2012-13.

Contra Costa County Assessment Practices Survey March 2015

14 Appendix A

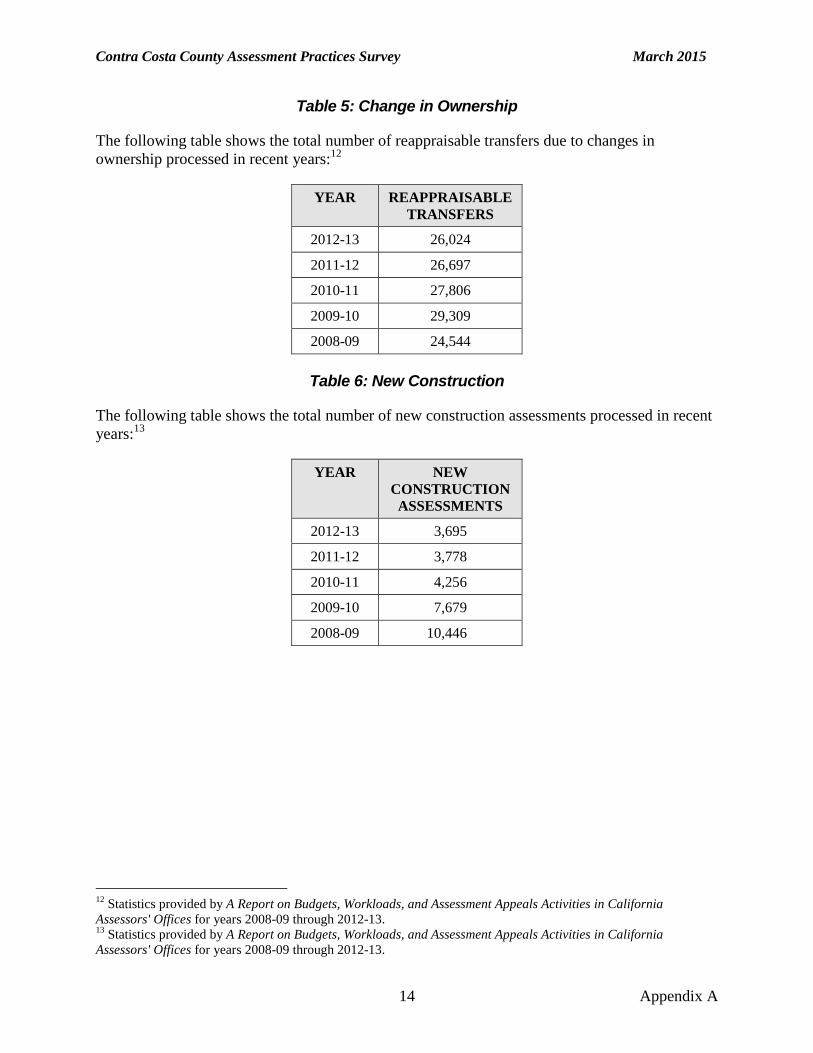

Table 5: Change in Ownership

The following table shows the total number of reappraisable transfers due to changes in ownership processed in recent years:12

YEAR REAPPRAISABLE TRANSFERS

2012-13 26,024

2011-12 26,697

2010-11 27,806

2009-10 29,309

2008-09 24,544

Table 6: New Construction

The following table shows the total number of new construction assessments processed in recent years:13

YEAR NEW CONSTRUCTION ASSESSMENTS

2012-13 3,695

2011-12 3,778

2010-11 4,256

2009-10 7,679

2008-09 10,446

12 Statistics provided by A Report on Budgets, Workloads, and Assessment Appeals Activities in California Assessors' Offices for years 2008-09 through 2012-13. 13 Statistics provided by A Report on Budgets, Workloads, and Assessment Appeals Activities in California Assessors' Offices for years 2008-09 through 2012-13.

Contra Costa County Assessment Practices Survey March 2015

15 Appendix A

Table 7: Declines In Value

The following table shows the total number of decline-in-value assessments in recent years:14

YEAR DECLINE-IN-VALUE ASSESSMENTS

2012-13 153,289

2011-12 188,477

2010-11 171,349

2009-10 175,504

2008-09 159,857

14 Statistics provided by A Report on Budgets, Workloads, and Assessment Appeals Activities in California Assessors' Offices for years 2008-09 through 2012-13.

Contra Costa County Assessment Practices Survey March 2015

16 Appendix B

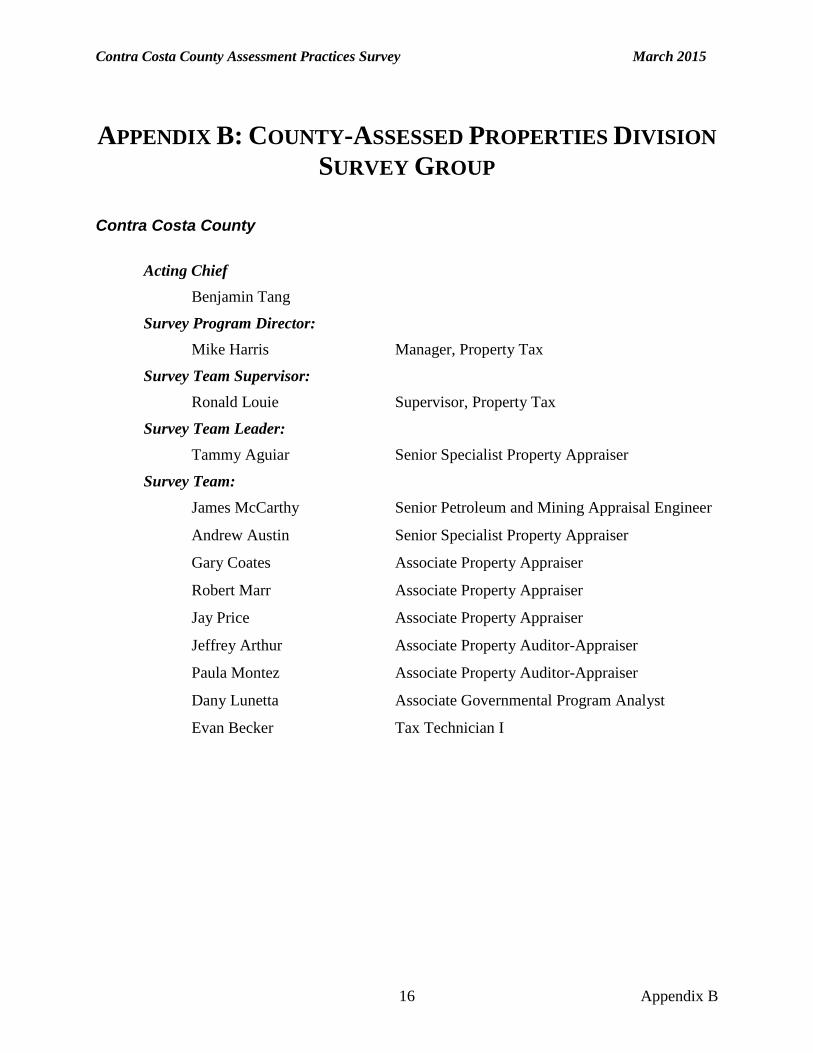

APPENDIX B: COUNTY-ASSESSED PROPERTIES DIVISION SURVEY GROUP

Contra Costa County

Acting Chief Benjamin Tang

Survey Program Director: Mike Harris Manager, Property Tax

Survey Team Supervisor: Ronald Louie Supervisor, Property Tax

Survey Team Leader: Tammy Aguiar Senior Specialist Property Appraiser

Survey Team: James McCarthy Senior Petroleum and Mining Appraisal Engineer

Andrew Austin Senior Specialist Property Appraiser

Gary Coates Associate Property Appraiser

Robert Marr Associate Property Appraiser

Jay Price Associate Property Appraiser

Jeffrey Arthur Associate Property Auditor-Appraiser

Paula Montez Associate Property Auditor-Appraiser

Dany Lunetta Associate Governmental Program Analyst

Evan Becker Tax Technician I

Contra Costa County Assessment Practices Survey March 2015

17 Appendix C

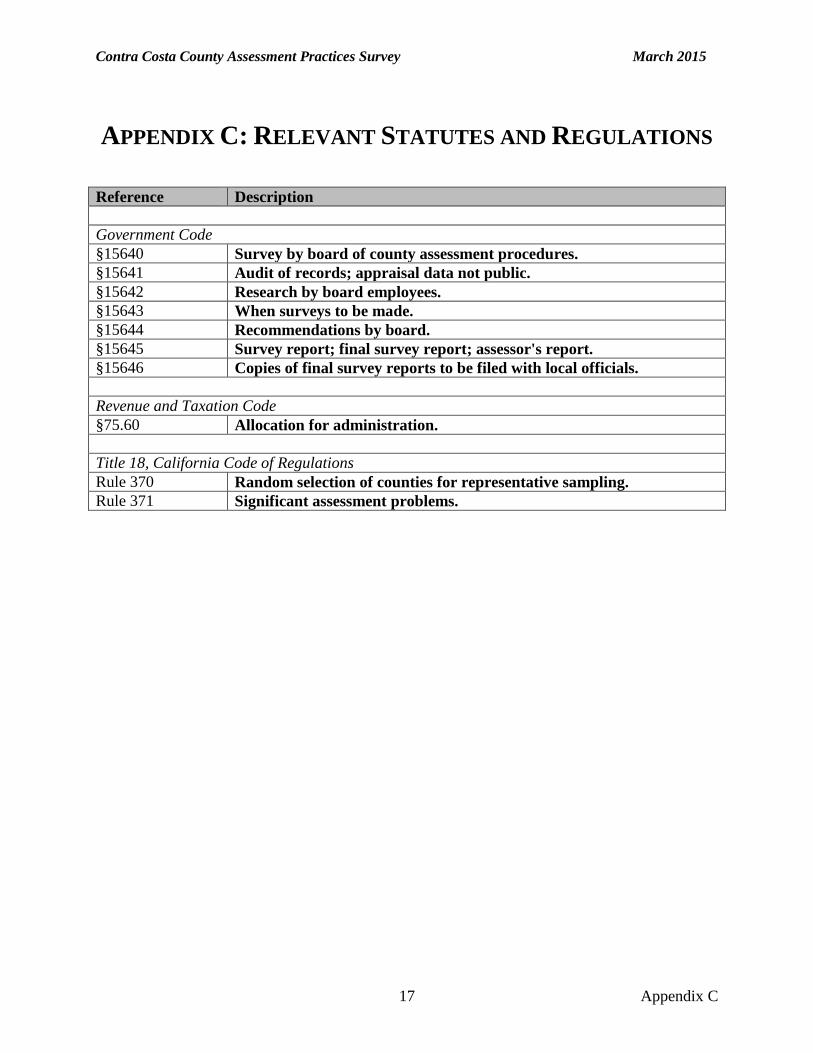

APPENDIX C: RELEVANT STATUTES AND REGULATIONS Reference Description Government Code §15640 Survey by board of county assessment procedures. §15641 Audit of records; appraisal data not public. §15642 Research by board employees. §15643 When surveys to be made. §15644 Recommendations by board. §15645 Survey report; final survey report; assessor's report. §15646 Copies of final survey reports to be filed with local officials. Revenue and Taxation Code §75.60 Allocation for administration. Title 18, California Code of Regulations Rule 370 Random selection of counties for representative sampling. Rule 371 Significant assessment problems.

Contra Costa County Assessment Practices Survey March 2015

18

ASSESSOR'S RESPONSE TO BOE'S FINDINGS Section 15645 of the Government Code provides that the assessor may file with the Board a response to the findings and recommendations in the survey report. The survey report, the assessor's response, and the BOE's comments on the assessor's response, if any, constitute the final survey report.

The Contra Costa County Assessor's response begins on the next page. The BOE has no comments on the response.

Contra Costa County

Office of Assessor 2530 Arnold Drive, Sui te 400

Martinez, California 94553-4359 FAX: (925) 313-7660

Telephone: (925) 3 13-7500

RECEIVED

FEB 19 2015 ssessea PM..... . . . e ao-·or'- ·'-E~ rf!es p1vts1on

Cll'll Qualtzation

Valua

County·AStat

tion

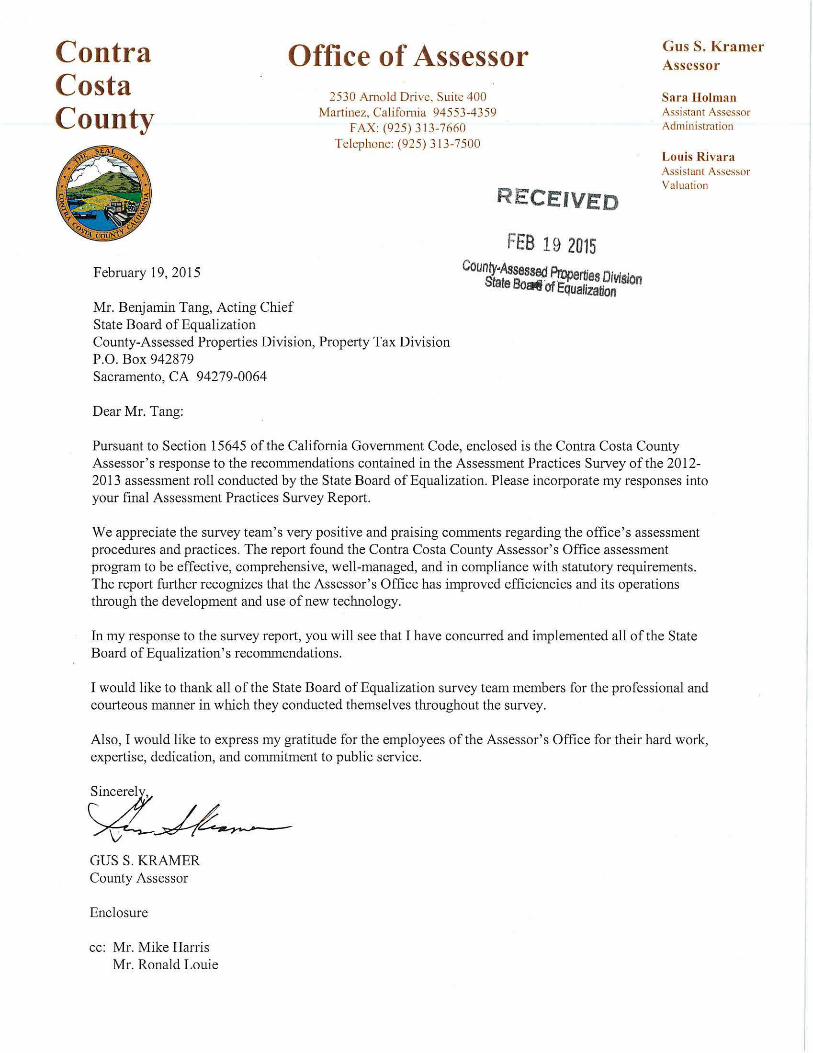

February 19, 2015

Mr. Benjamin Tang, Acting Chief State Board of Equalization County-Assessed Properties Division, Property Tax Division P.O. Box 942879 Sacramento, CA 94279-0064

Dear Mr. Tang:

Pursuant to Section 15645 of the California Government Code, enclosed is the Contra Costa County Assessor's response to the recommendations contained in the Assessment Practices Survey of the 2012-2013 assessment roll conducted by the State Board of Equalization. Please incorporate my responses into your final Assessment Practices Survey Report.

We appreciate the survey team's very positive and praising comments regarding the office's assessment procedures and practices. The report found the Contra Costa County Assessor's Office assessment program to be effective, comprehensive, well-managed, and in compliance with statutory requirements. The report further recognizes that the Assessor's Office has improved efficiencies and its operations through the development and use of new technology.

In my response to the survey report, you will see that I have concurred and implemented all of the State Board of Equalization's recommendations.

I would like to thank all of the State Board of Equalization survey team members for the professional and courteous manner in which they conducted themselves throughout the survey.

Also, I would like to express my gratitude for the employees of the Assessor' s Office for their hard work, expertise, dedication, and commitment to public service.

Gus S. Kramer Assessor

Sara Holman Assistant Assessor Administration

Louis Rivara Assistant Assessor

~_,h/~GUS S. KRAMER County Assessor

Enclosure

cc: Mr. Mike Harris Mr. Ronald Louie

CONTRA COSTA COUNTY STATE BOARD OF EQUALIZATION ASSESSMENT PRACTICES SURVEY RESPONSES - JANUARY 2015

RECOMMENDATION 1: Improve the change in ownership program by not sending a notice of penalty letter to a property owner when making an initial request for completion of a COS.

Response: We concur. The letter accompanying the initial request for completion of a COS has been revised.

RECOMMENDATION 2: Measure declines in value for mineral properties using the entire appraisal unit as required by Rule 469.

Response: We concur. This only affected 2 parcels in the whole county. A new procedure has been implemented for these parcels.

RECOMMENDATION 3: Conduct an audit or field review when property owners fail to file a BPS for three or more consecutive years.

Response: We concur. A new procedure has been implemented to review assessments of businesses that failed to file a BPS statement for three or more consecutive years .