Embed Size (px)

Citation preview

Coop Structure and Operation

Who runs the coop and how?

Teaser Questions

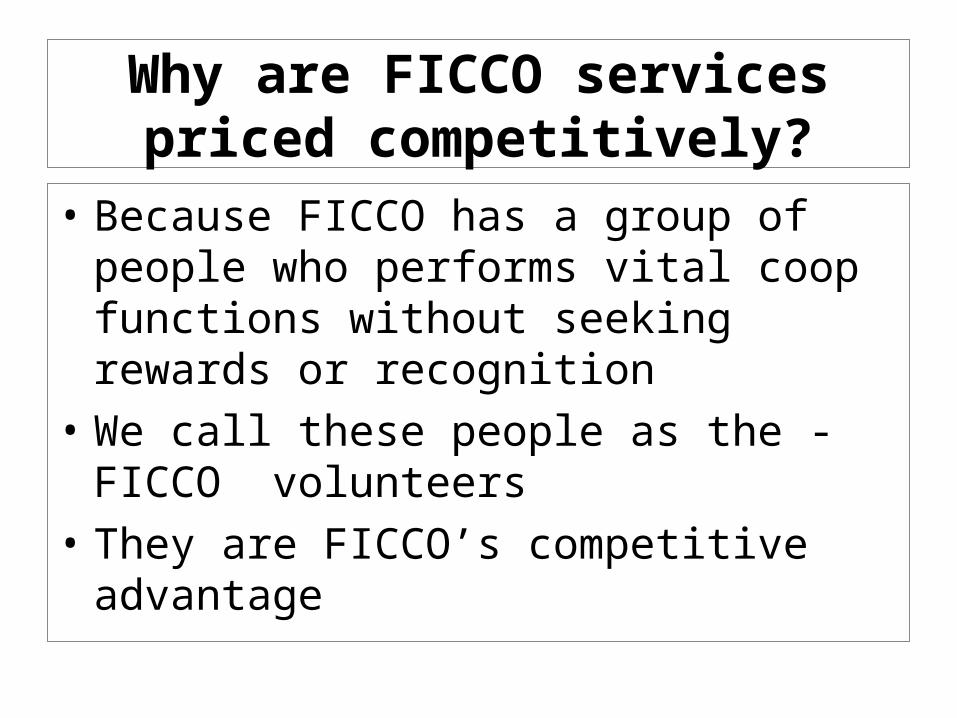

1. Why are FICCO services priced competitively?

2. Is it safe to deposit your money at FICCO?

Is our Money at FICCO Safe?

• It’s more than its 56 years track record• It is beyond being the biggest community type coop

in the whole country• Its diligence in making sure that doubtful accounts

are fully provided is contributory• More so the fact that, unlike banks, its members are

also the borrowers• FICCO has a tried and tested way of doing things –

we call it the FICCO culture.

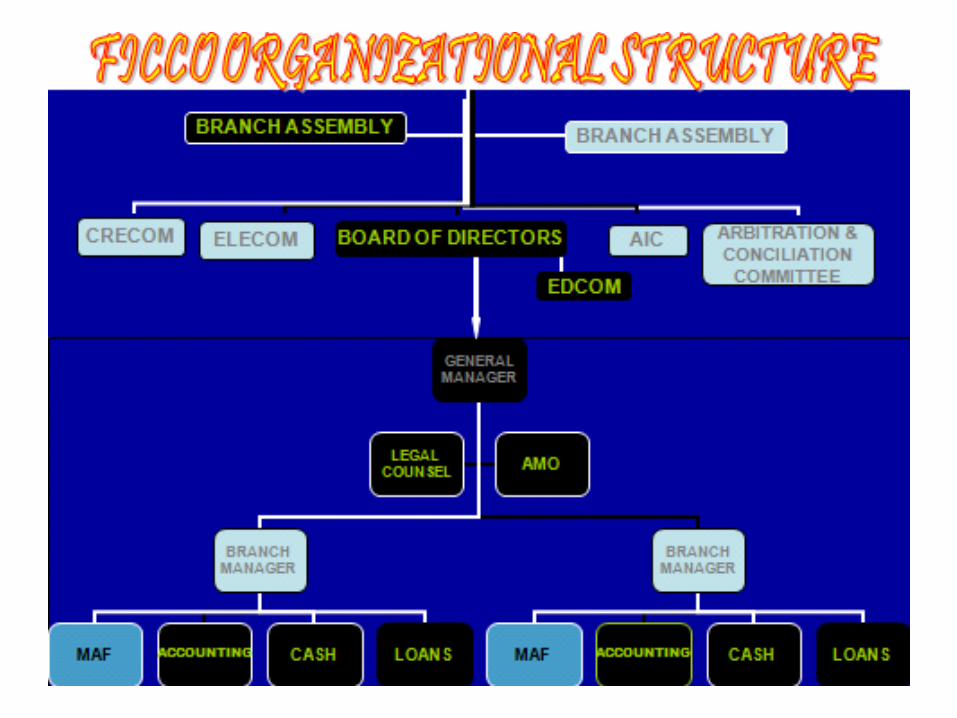

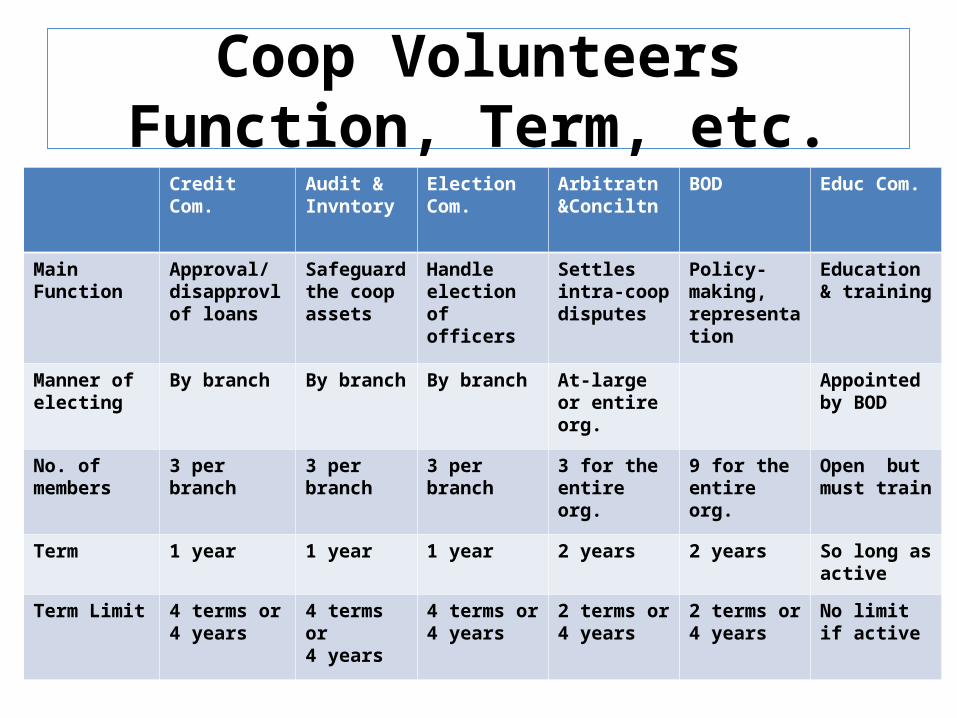

Coop Volunteers Function, Term, etc.

Credit Com.

Audit &Invntory

Election Com.

Arbitratn &Conciltn

BOD Educ Com.

Main Function

Approval/ disapprovl of loans

Safeguard the coop assets

Handle election of officers

Settles intra-coop disputes

Policy-making, representation

Education & training

Manner of electing

By branch By branch

By branch At-large or entire org.

Appointed by BOD

No. of members

3 per branch

3 per branch

3 per branch

3 for the entire org.

9 for the entire org.

Open but must train

Term 1 year 1 year 1 year 2 years 2 years So long as active

Term Limit 4 terms or4 years

4 terms or4 years

4 terms or4 years

2 terms or 4 years

2 terms or 4 years

No limit if active

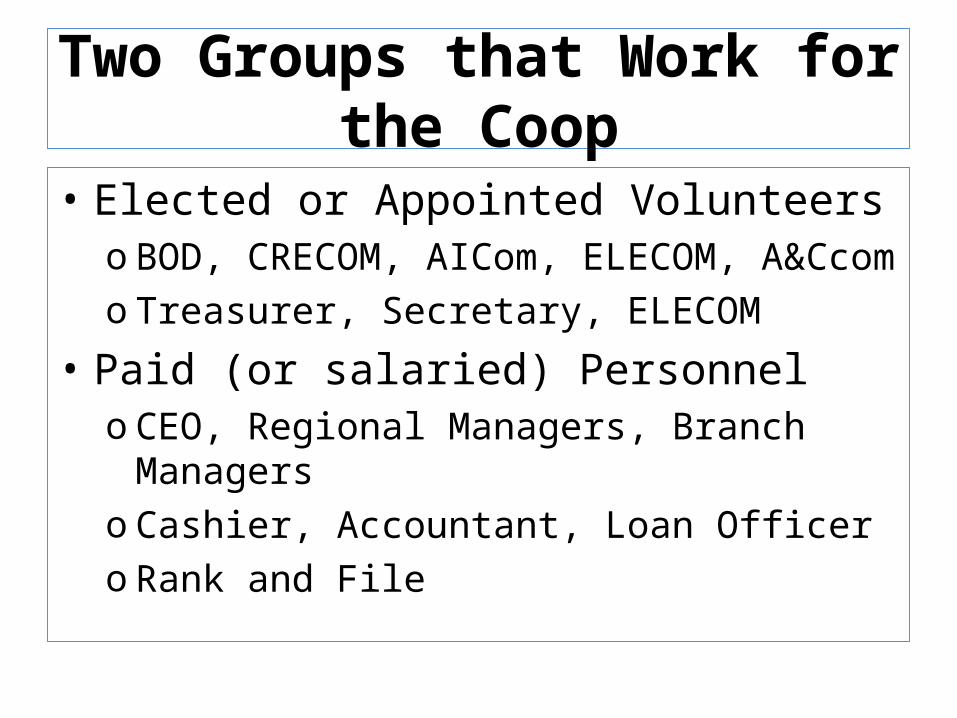

Two Groups that Work for the Coop

• Elected or Appointed Volunteerso BOD, CRECOM, AICom, ELECOM, A&Ccomo Treasurer, Secretary, ELECOM

• Paid (or salaried) PersonneloCEO, Regional Managers, Branch ManagersoCashier, Accountant, Loan OfficeroRank and File

Why are FICCO services priced competitively?

• Because FICCO has a group of people who performs vital coop functions without seeking rewards or recognition

• We call these people as the -FICCO volunteers

• They are FICCO’s competitive advantage

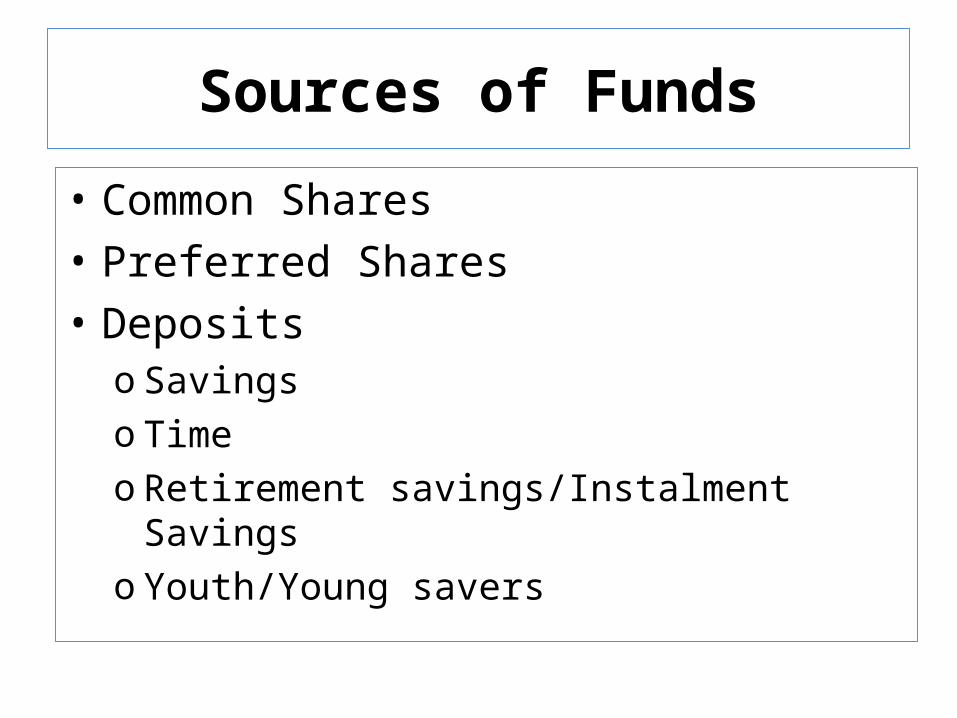

Sources of Funds

• Common Shares• Preferred Shares• Deposits

o Savingso TimeoRetirement savings/Instalment Savingso Youth/Young savers

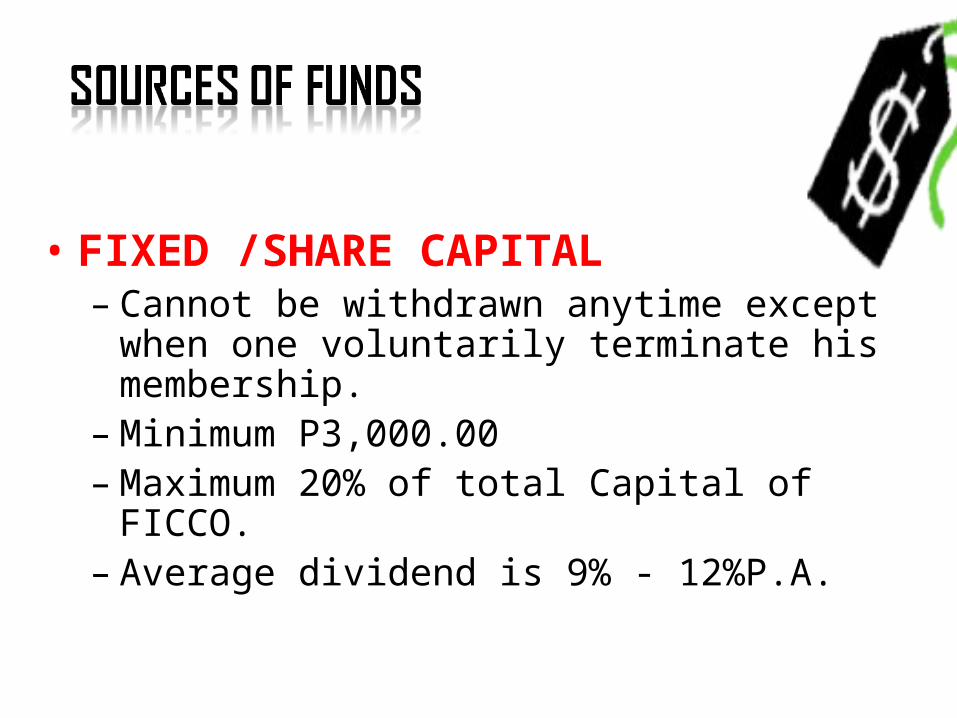

• FIXED /SHARE CAPITAL – Cannot be withdrawn anytime except when one

voluntarily terminate his membership.– Minimum P3,000.00– Maximum 20% of total Capital of FICCO. – Average dividend is 9% - 12%P.A.

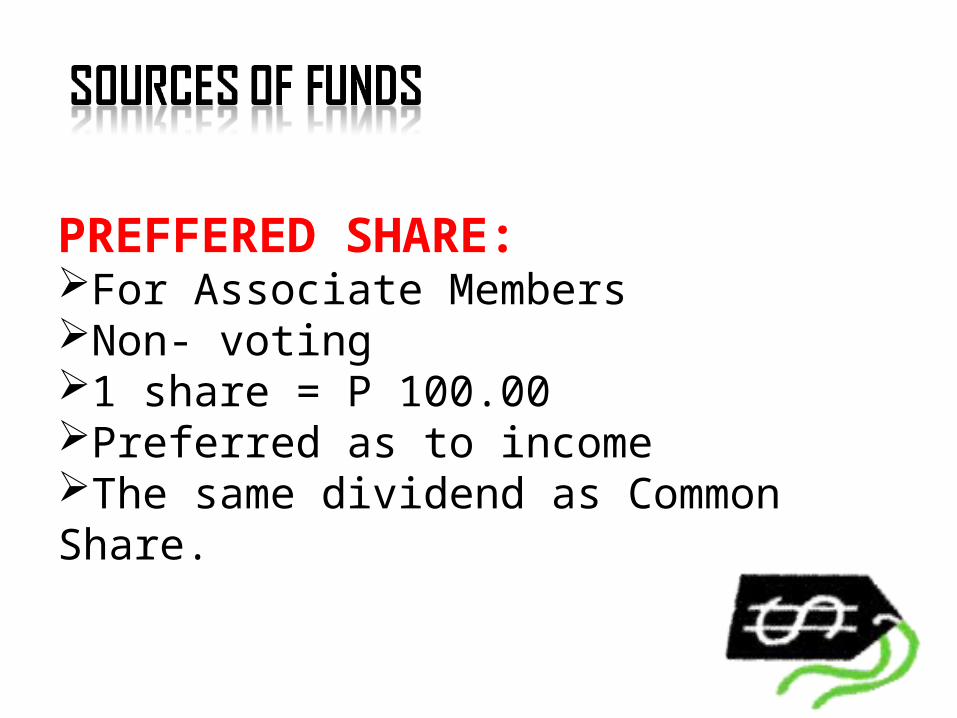

PREFFERED SHARE:For Associate MembersNon- voting 1 share = P 100.00Preferred as to incomeThe same dividend as Common Share.

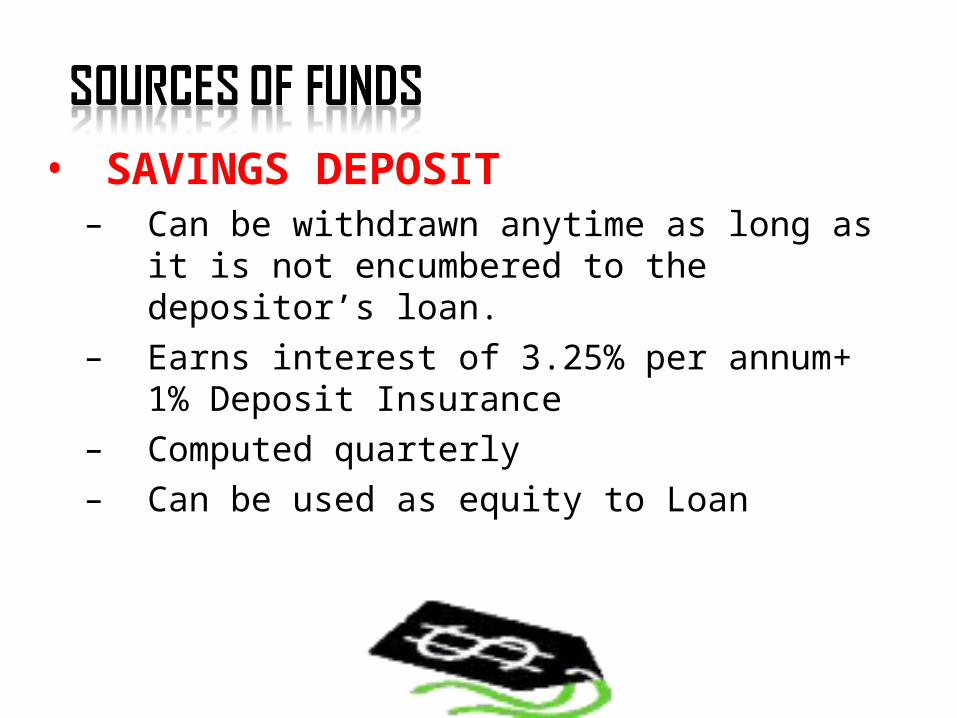

• SAVINGS DEPOSIT– Can be withdrawn anytime as long as it is not

encumbered to the depositor’s loan. – Earns interest of 3.25% per annum+ 1% Deposit

Insurance– Computed quarterly– Can be used as equity to Loan

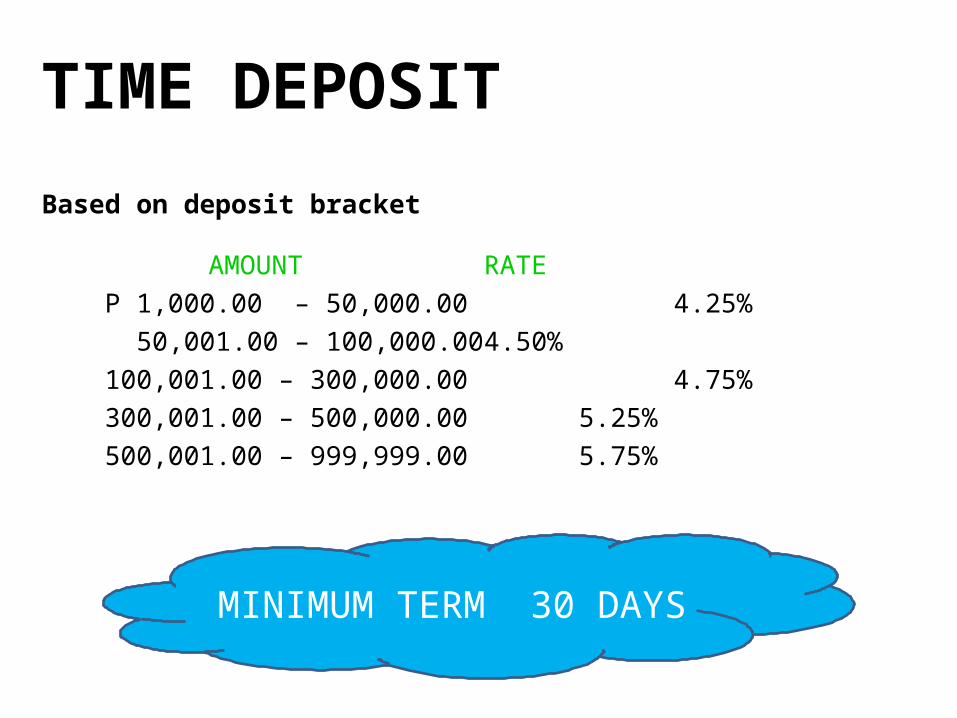

Based on deposit bracket

AMOUNT RATEP 1,000.00 – 50,000.00 4.25% 50,001.00 – 100,000.00 4.50%100,001.00 – 300,000.00 4.75%300,001.00 – 500,000.00 5.25%500,001.00 – 999,999.00 5.75%

TIME DEPOSIT

MINIMUM TERM 30 DAYS

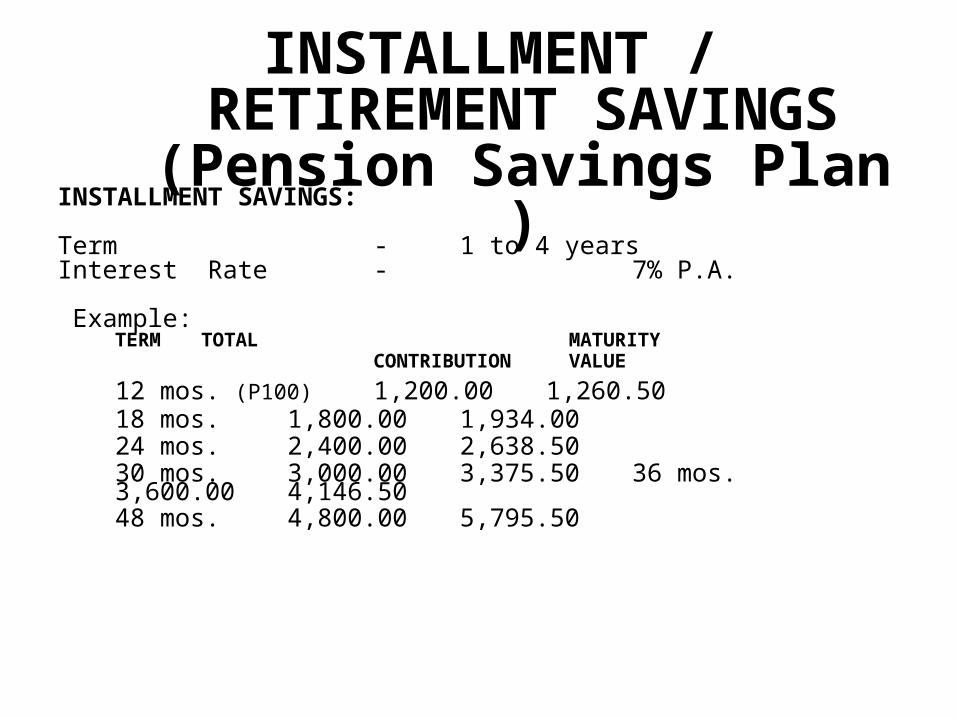

INSTALLMENT SAVINGS:

Term - 1 to 4 yearsInterest Rate - 7% P.A.

Example:TERM TOTAL MATURITY CONTRIBUTION VALUE

12 mos. (P100) 1,200.00 1,260.50

18 mos. 1,800.00 1,934.0024 mos. 2,400.00 2,638.50

30 mos. 3,000.00 3,375.5036 mos. 3,600.00

4,146.5048 mos. 4,800.00 5,795.50

INSTALLMENT / RETIREMENT SAVINGS (Pension Savings Plan

)

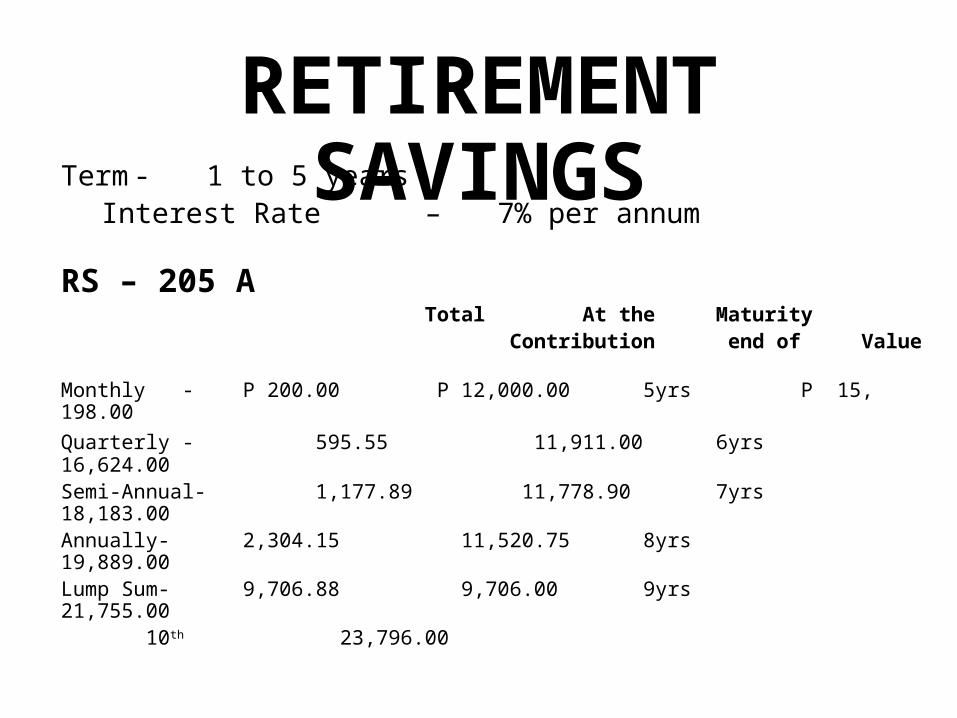

Term - 1 to 5 years Interest Rate – 7% per annum

RS – 205 A Total At the

Maturity Contribution end of

Value Monthly - P 200.00 P 12,000.00 5yrs P 15, 198.00

Quarterly - 595.55 11,911.00 6yrs 16,624.00Semi-Annual- 1,177.89 11,778.90 7yrs 18,183.00Annually- 2,304.15 11,520.75 8yrs 19,889.00Lump Sum- 9,706.88 9,706.00 9yrs 21,755.00

10th 23,796.00

RETIREMENT SAVINGS

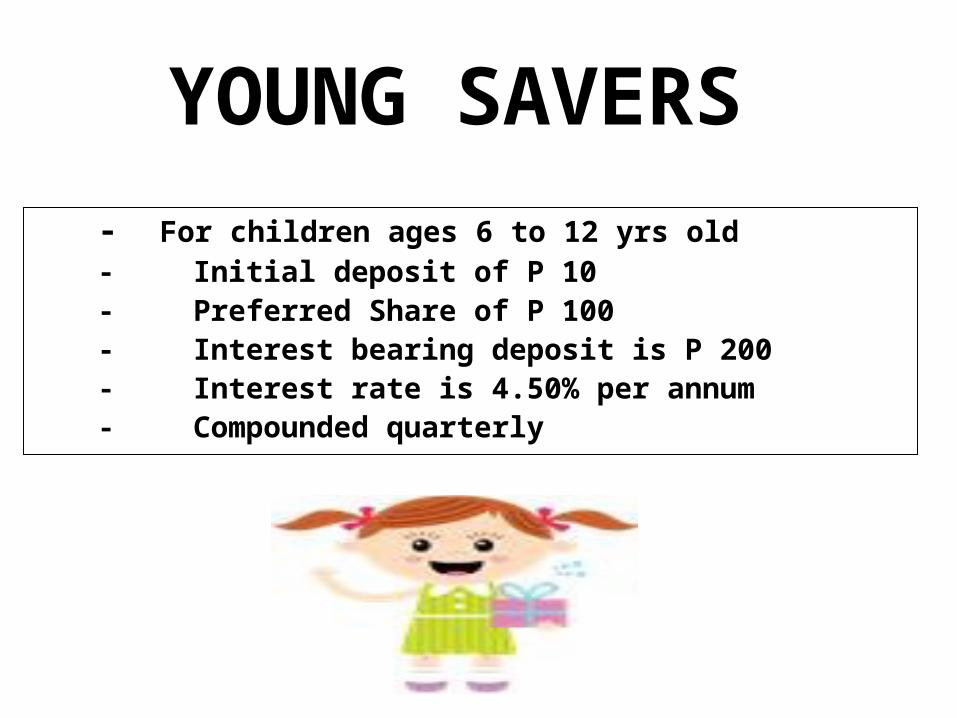

- For children ages 6 to 12 yrs old- Initial deposit of P 10- Preferred Share of P 100- Interest bearing deposit is P 200- Interest rate is 4.50% per annum - Compounded quarterly

YOUNG SAVERS

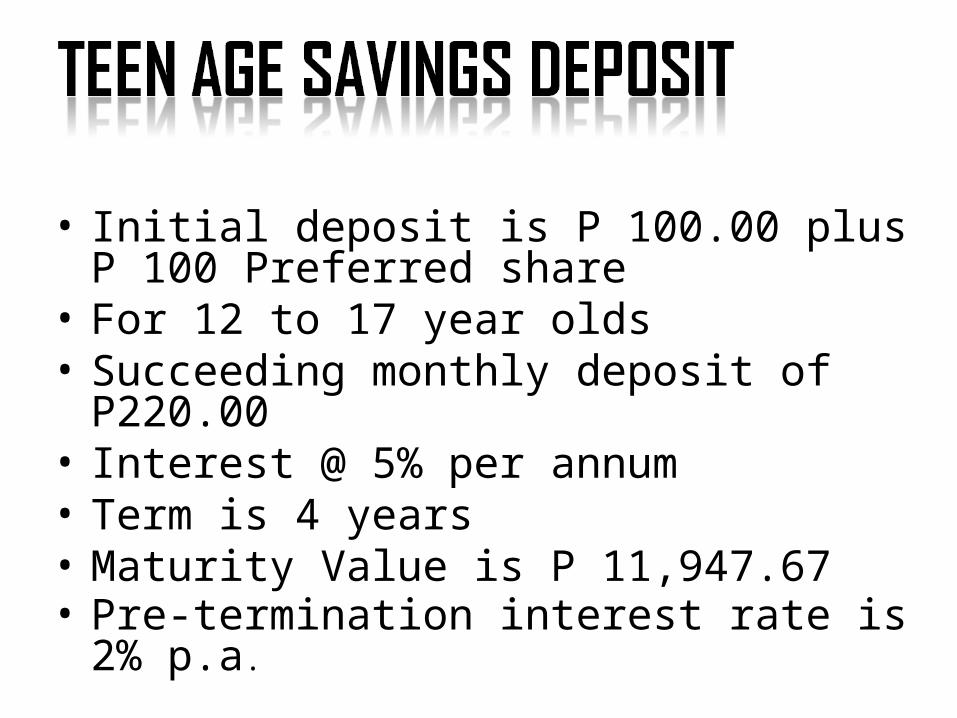

• Initial deposit is P 100.00 plus P 100 Preferred share

• For 12 to 17 year olds• Succeeding monthly deposit of

P220.00 • Interest @ 5% per annum• Term is 4 years• Maturity Value is P 11,947.67• Pre-termination interest rate is 2% p.a.

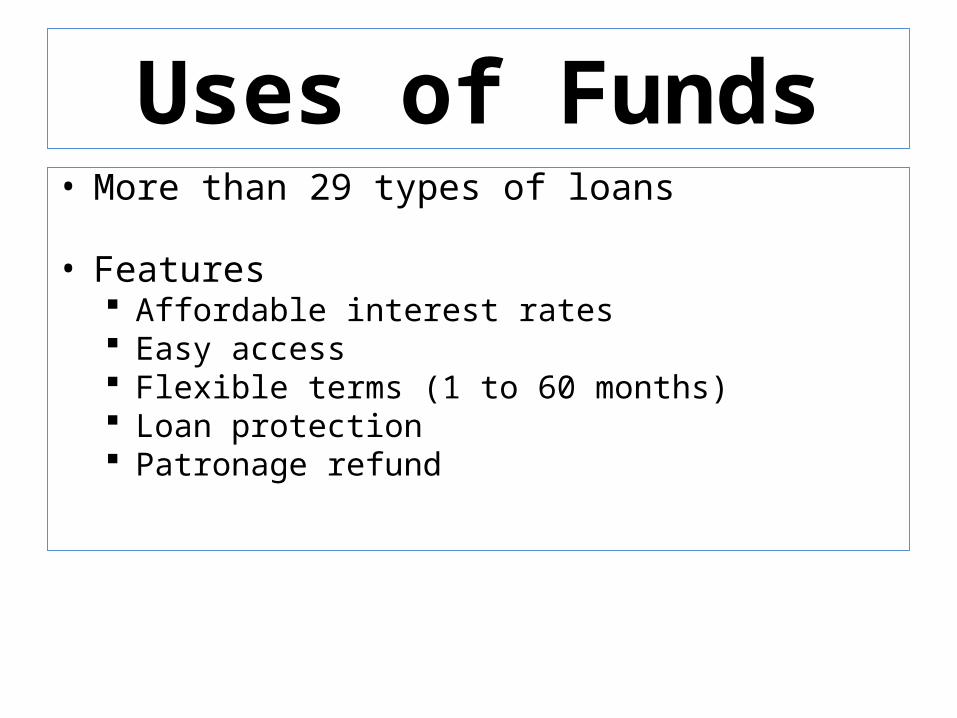

Uses of Funds• More than 29 types of loans

• Features Affordable interest rates Easy access Flexible terms (1 to 60 months) Loan protection Patronage refund

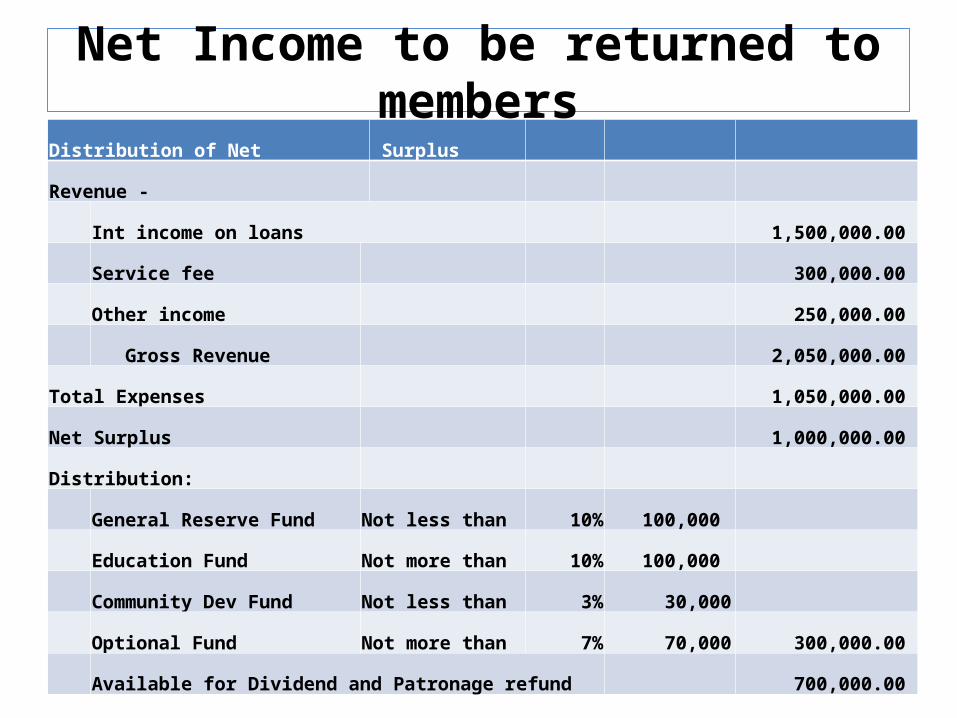

Net Income to be returned to members

Distribution of Net Surplus

Revenue -

Int income on loans 1,500,000.00

Service fee 300,000.00

Other income 250,000.00

Gross Revenue 2,050,000.00

Total Expenses 1,050,000.00

Net Surplus 1,000,000.00

Distribution:

General Reserve Fund Not less than 10% 100,000

Education Fund Not more than 10% 100,000

Community Dev Fund Not less than 3% 30,000

Optional Fund Not more than 7% 70,000 300,000.00

Available for Dividend and Patronage refund 700,000.00

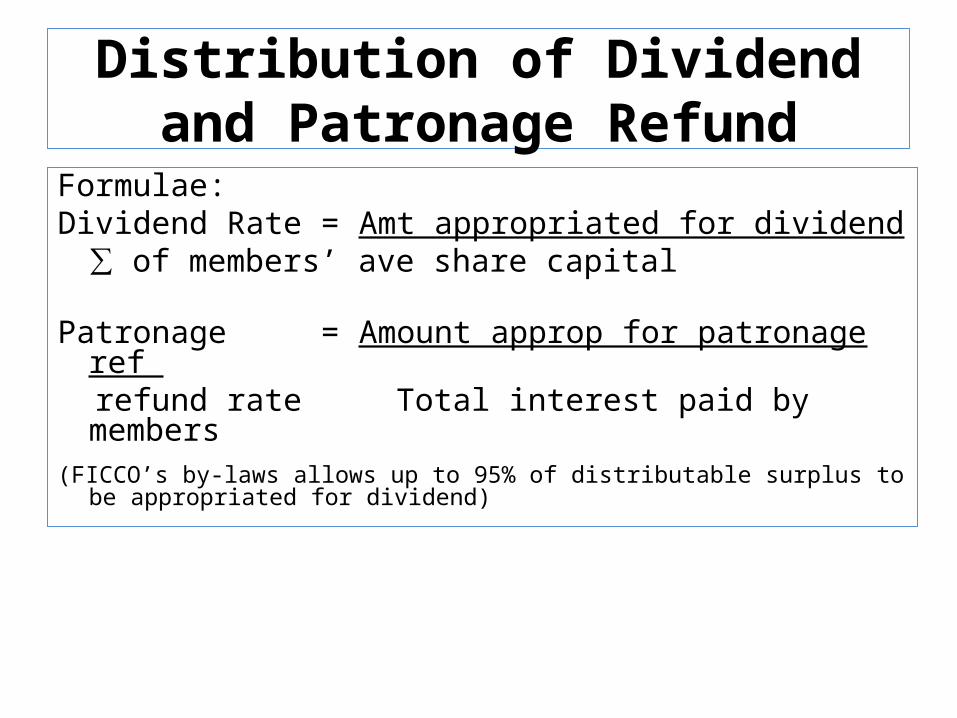

Distribution of Dividend and Patronage Refund

Formulae:Dividend Rate = Amt appropriated for dividend

∑ of members’ ave share capital

Patronage = Amount approp for patronage ref refund rate Total interest paid by members(FICCO’s by-laws allows up to 95% of distributable surplus to be

appropriated for dividend)

FICCO Services

In addition to its Loan services, we have many more!

The New FICCO Mutual Aid Fund

In compliance with the Joint Memorandum Circular of the Insurance Commission (IC) – Cooperative Development Authority (CDA) – Securities & Exchange Commission (SEC), FICCO MAF will be insured to FICCO’s co-owned insurance cooperative, CLIMBS Life & General Insurance Cooperative.

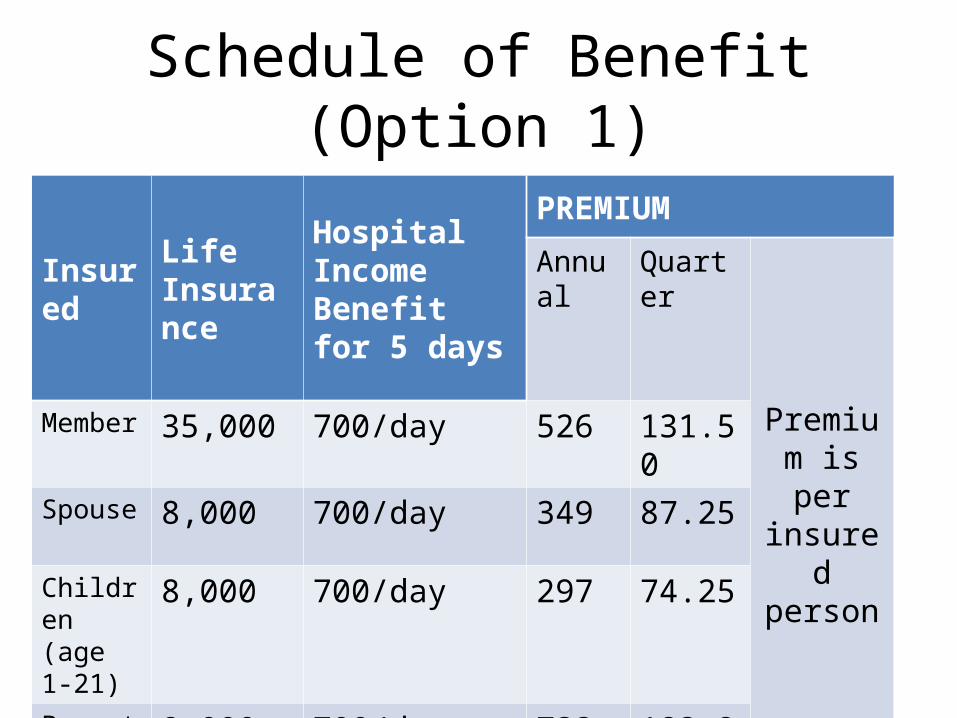

Schedule of Benefit (Option 1)

Insured Life Insurance

Hospital Income Benefit for 5 days

PREMIUMAnnual Quarter

Premium is per

insured person

Member 35,000 700/day 526 131.50

Spouse 8,000 700/day 349 87.25

Children (age 1-21)

8,000 700/day 297 74.25

Parents 8,000 700/day 733 183.25

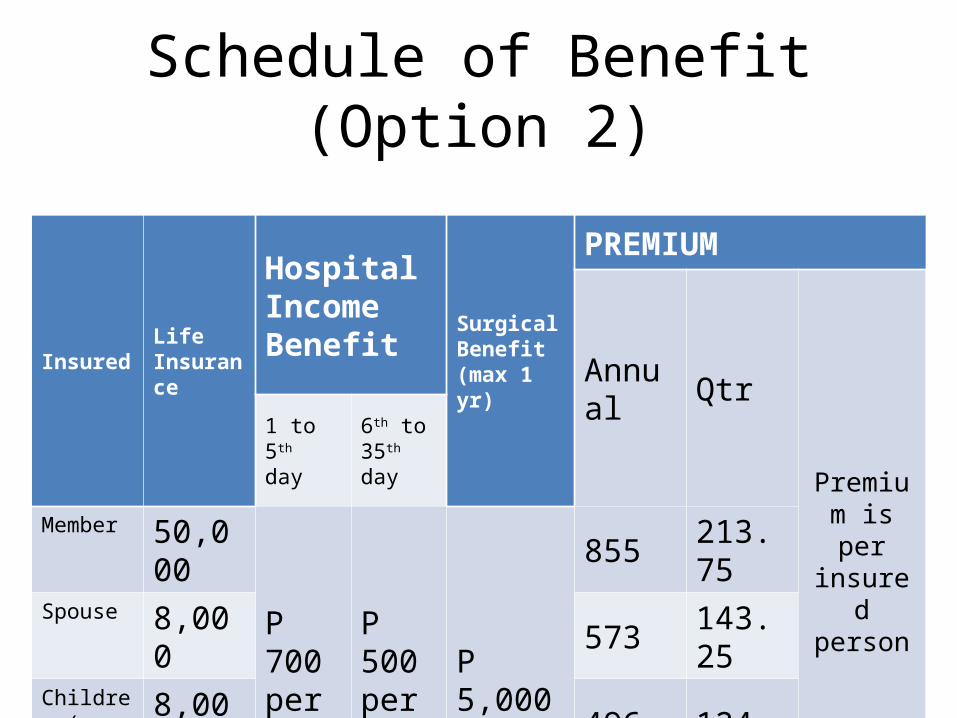

Schedule of Benefit (Option 2)

Insured Life Insurance

Hospital Income Benefit

Surgical Benefit (max 1 yr)

PREMIUM

Annual Qtr

Premium is per

insured person

1 to 5th day

6th to 35th day

Member 50,000P 700 per day

P 500 per day

P 5,000

855 213.75Spouse 8,000 573 143.25Children (age 1-21) 8,000 496 124Parents 8,000 1,045 261.25

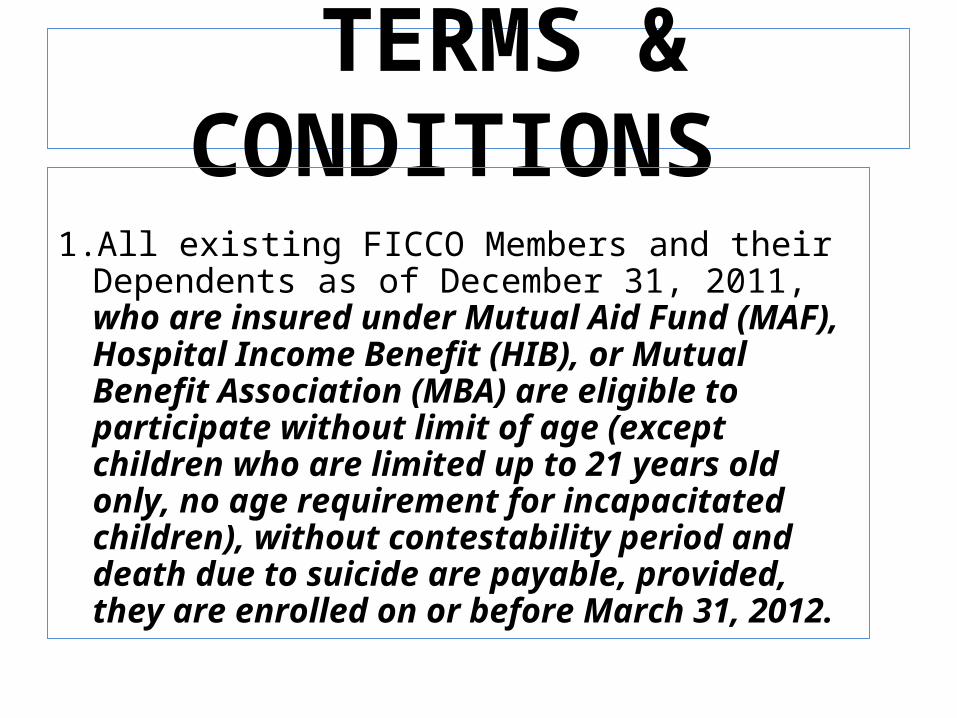

TERMS & CONDITIONS

1. All existing FICCO Members and their Dependents as of December 31, 2011, who are insured under Mutual Aid Fund (MAF), Hospital Income Benefit (HIB), or Mutual Benefit Association (MBA) are eligible to participate without limit of age (except children who are limited up to 21 years old only, no age requirement for incapacitated children), without contestability period and death due to suicide are payable, provided, they are enrolled on or before March 31, 2012.

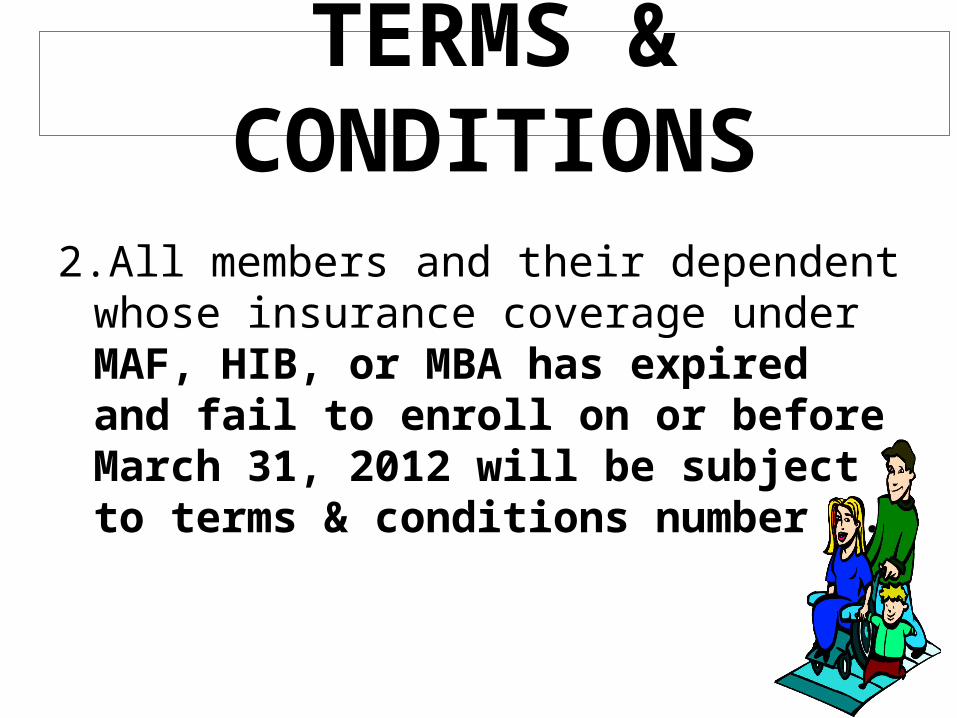

TERMS & CONDITIONS

2.All members and their dependent whose insurance coverage under MAF, HIB, or MBA has expired and fail to enroll on or before March 31, 2012 will be subject to terms & conditions number 4.

TERMS & CONDITIONS3. Member’s insurance under Hospital Income

Benefit (HIB) which are not expired, are not yet required to enroll until the last day of HIB coverage. Renewal of their insurance will be under Option 2 and will not be subject to contestability period, provided, they are insured within 30 days from the last day of the previous insurance coverage,

TERMS & CONDITIONS4. Existing FICCO Members and Dependents as

of March 31, 2012, who are not previously insured in any of the following: MAF, HIB, or MBA are eligible and encourage to participate to this insurance program but will subject to the following terms and conditions:

TERMS & CONDITIONSa) Member with or without loan are free to

choose from any of the two (2) options; b) Member who will avail a =P=50,000.00 loan

and above will be insured under Option 2; c) Age must below 69 years old:

TERMS & CONDITIONSd) Not suffering from any of the following:

Cancer, Epilepsy, HIV/AID and Stroke; e) Death due to Suicide in not payable within

one (1) year of coverage; f) Subject to Contestability period of Six (6)

Months:

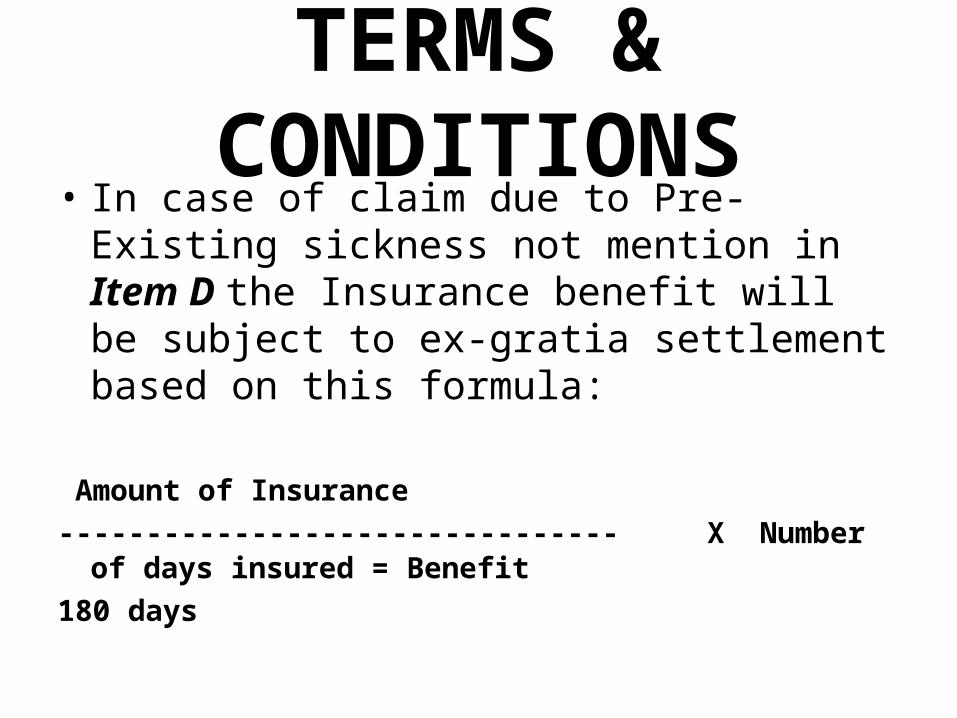

TERMS & CONDITIONS• In case of claim due to Pre-Existing sickness

not mention in Item D the Insurance benefit will be subject to ex-gratia settlement based on this formula:

Amount of Insurance -------------------------------- X Number of days insured = Benefit 180 days

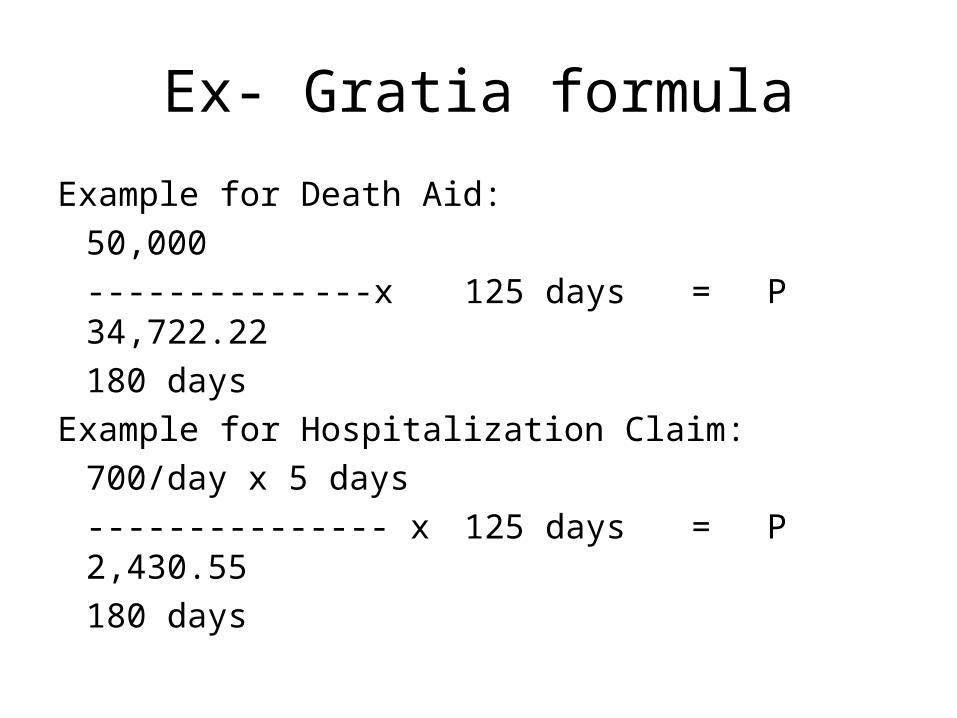

Ex- Gratia formula

Example for Death Aid:50,000----------- ---x 125 days = P 34,722.22180 days

Example for Hospitalization Claim:700/day x 5 days--------------- x 125 days = P 2,430.55180 days

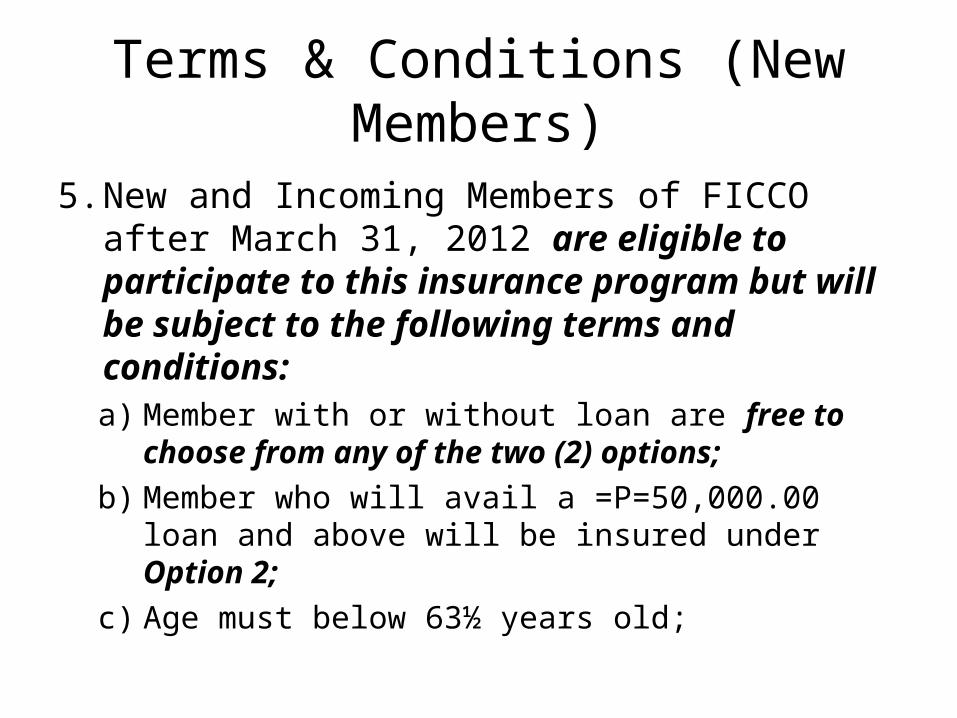

Terms & Conditions (New Members)

5. New and Incoming Members of FICCO after March 31, 2012 are eligible to participate to this insurance program but will be subject to the following terms and conditions:a) Member with or without loan are free to choose

from any of the two (2) options; b) Member who will avail a =P=50,000.00 loan and

above will be insured under Option 2; c) Age must below 63½ years old;

Terms & Conditions (New Members)

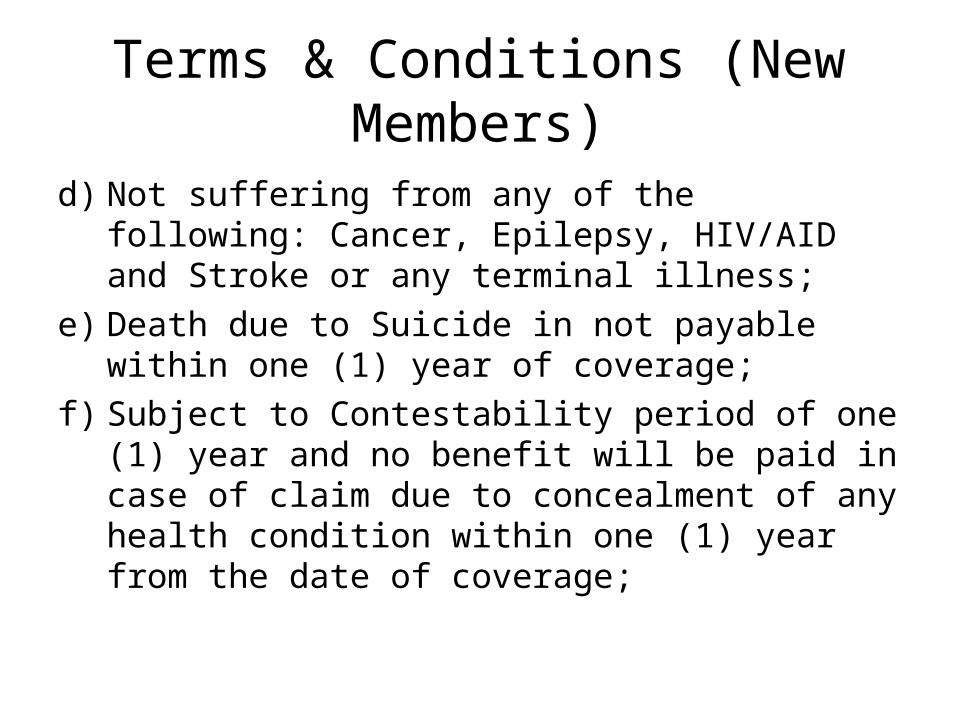

d) Not suffering from any of the following: Cancer, Epilepsy, HIV/AID and Stroke or any terminal illness;

e) Death due to Suicide in not payable within one (1) year of coverage;

f) Subject to Contestability period of one (1) year and no benefit will be paid in case of claim due to concealment of any health condition within one (1) year from the date of coverage;

TERMS & CONDITIONS

6. Effective date of Insurance coverage of : a) Insurance coverage of existing FICCO member

and their dependent as of March 31, 2012, shall be upon submission of application with authority to deduct for payment of premium from account of the insured or upon submission of application and over the counter payment of premium to any FICCO branch provided duly receipted;

Effectivity

b) Insurance coverage of New and Incoming Member of FICCO after March 31, 2012, will be subject to approval, if no notice after 90 days from the receipt of premium and application form from CLIMBS, the insurance policy is considered approved and effected on the application date.

Upgrading of plans

7. All insured member are allowed to upgrade their insurance coverage from option one (1) to option two (2) provided they will fill-up new application form and will be subject to approval by CLIMBS.

Double Insurance Coverage

8. In case a member has double insurance coverage, only one benefit with a higher coverage will be paid in case of claim. Excess premium will be applied to renewal of coverage or refunded upon request in writing by the insured member.

Applicability

9. Quarterly premium are applicable only for year 2012 during our transition period. Premium must be paid on or before the scheduled due to date to avoid termination of insurance coverage.

10. Members are required to fill-up and submit an Application Form

Other Insurance ProductsOther Insurance Product Available: • Individual Life Insurance (Permanent and Endowment Plan) • Fire Insurance with Allied Perils coverage such as Typhoon,

Flood, Earthquake, Robbery, Burglary and others • Motor Vehicle Insurance with coverage such as Typhoon,

Flood, Earthquake, Landslide and others

For your Insurance Protection and application form please see the MAF/MBA In-charge or any employee

Savings Protection Plan

(SPP)1. Maximum share plus savings to be covered is P300,000.00

2. Basic contribution of 1% of deposit up to the age of 70 years and 364 days.

3. On a member’s 71st birthday onward, reinsurance coverage shall cease. For this reason, the contribution shall be increased to 2.94 % of deposits covered.

Savings Protection Plan

(SPP)4. “Bundak” deposit will be covered provided it will not be more than 10 times the average monthly deposit for six months or the maximum amount of coverage which ever is lower.

Savings Protection Plan

(SPP)5. New & incoming member /depositor whose eligibility age for insurance is 55 to 63 years old will be subject to benefit settlement schedule based on years of membership after one year.– 5 years or less 50%– >5 years to 10 years 75%– >10 years 100%

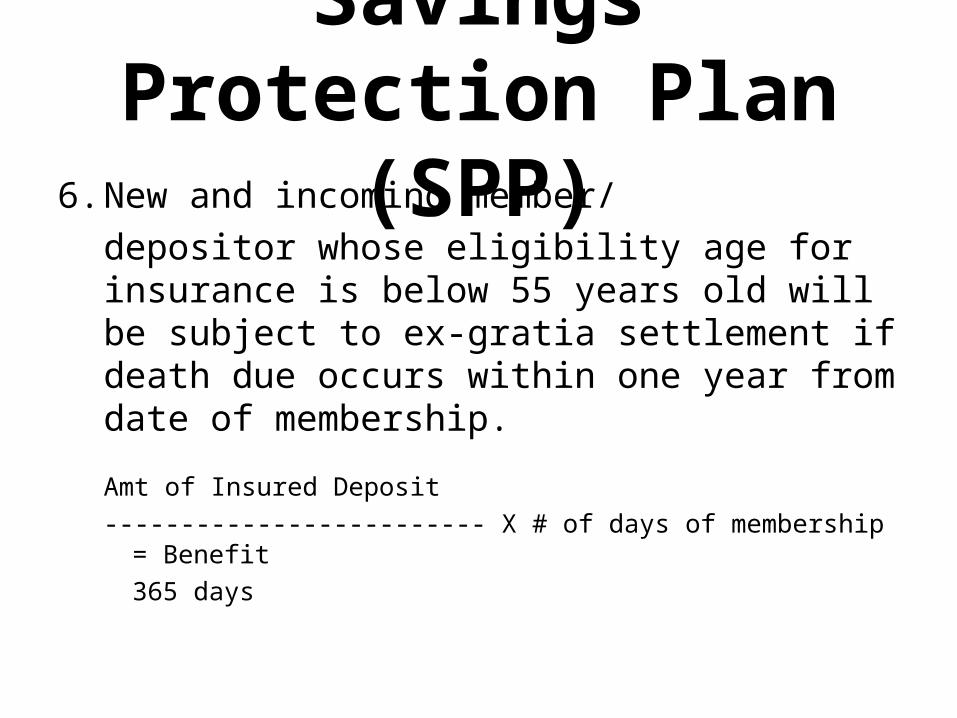

Savings Protection Plan

(SPP)6. New and incoming member/

depositor whose eligibility age for insurance is below 55 years old will be subject to ex-gratia settlement if death due occurs within one year from date of membership.

Amt of Insured Deposit

------------------------- X # of days of membership = Benefit

365 days

Savings Protection Plan

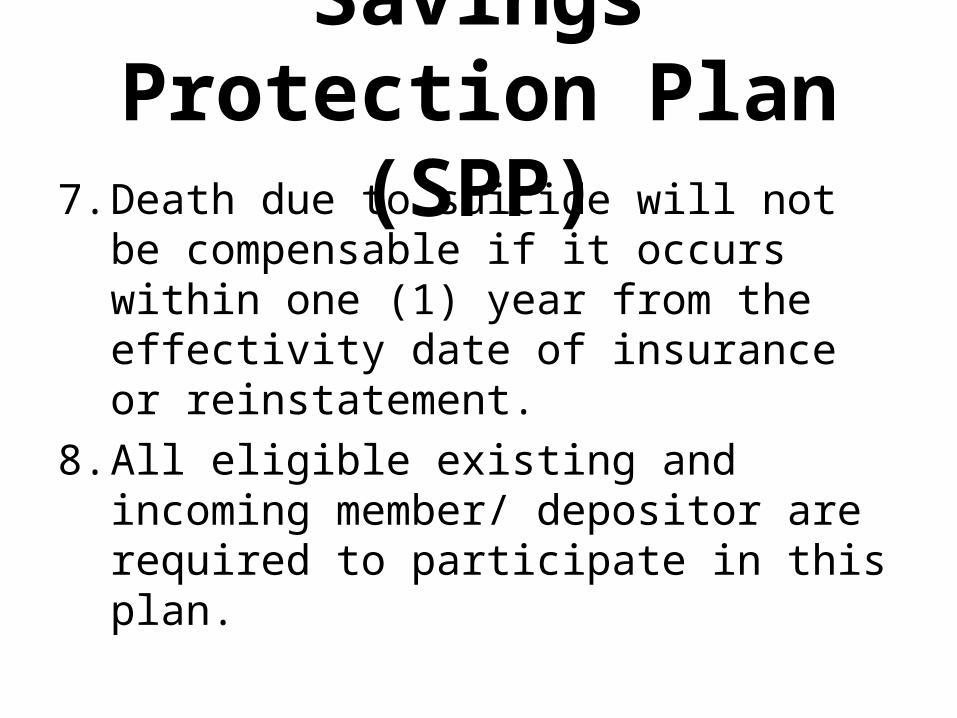

(SPP)7. Death due to suicide will not be compensable if it occurs within one (1) year from the effectivity date of insurance or reinstatement.

8. All eligible existing and incoming member/ depositor are required to participate in this plan.

Savings Protection Plan

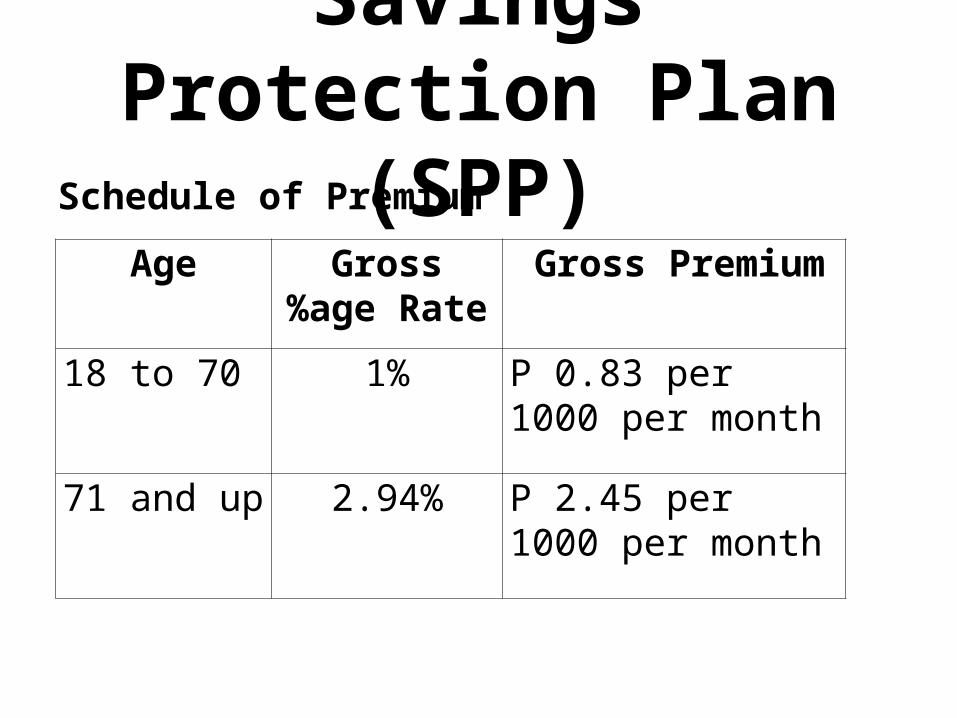

(SPP)Schedule of Premium

Age Gross%age Rate

Gross Premium

18 to 70 1% P 0.83 per 1000 per month

71 and up 2.94% P 2.45 per 1000 per month

Savings Protection Plan

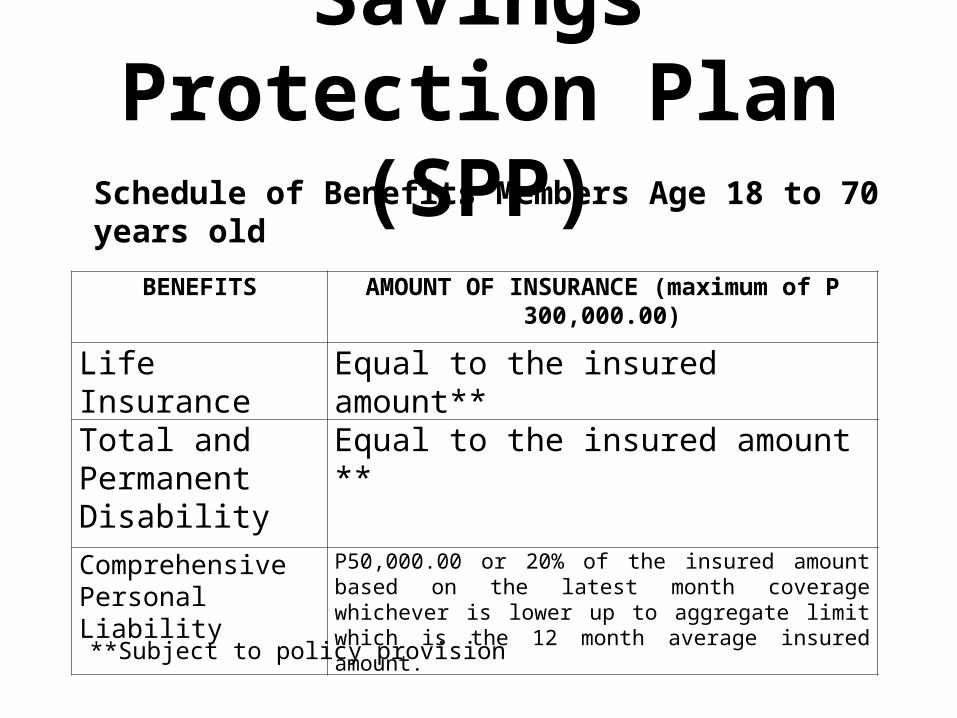

(SPP)Schedule of Benefits Members Age 18 to 70 years old

BENEFITS AMOUNT OF INSURANCE (maximum of P 300,000.00)

Life Insurance Equal to the insured amount**

Total and Permanent Disability

Equal to the insured amount **

Comprehensive Personal Liability

P50,000.00 or 20% of the insured amount based on the latest month coverage whichever is lower up to aggregate limit which is the 12 month average insured amount.

**Subject to policy provision

Savings Protection Plan

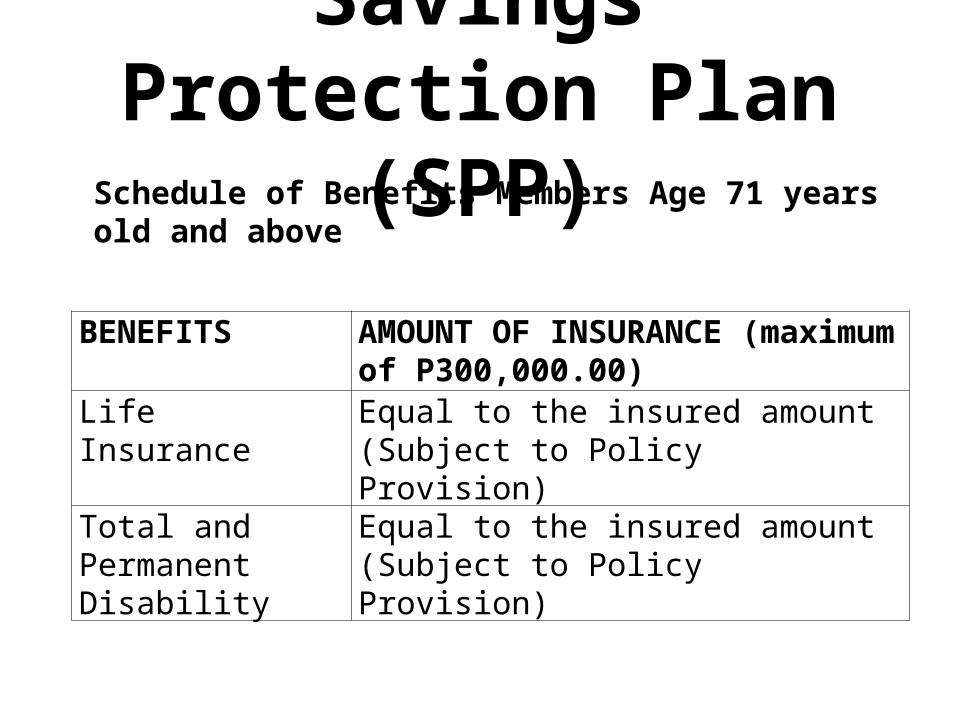

(SPP)Schedule of Benefits Members Age 71 years old and above

BENEFITS AMOUNT OF INSURANCE (maximum of P300,000.00)

Life Insurance Equal to the insured amount (Subject to Policy Provision)

Total and Permanent Disability

Equal to the insured amount (Subject to Policy Provision)

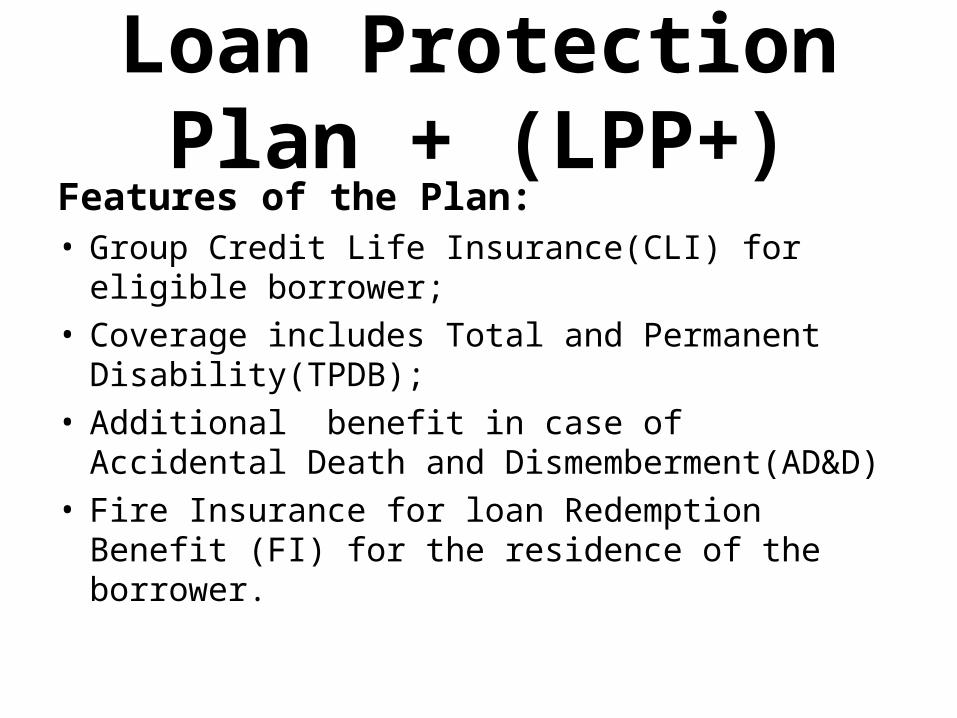

Loan Protection Plan + (LPP+)

Features of the Plan:• Group Credit Life Insurance(CLI) for eligible

borrower;• Coverage includes Total and Permanent

Disability(TPDB);• Additional benefit in case of Accidental Death

and Dismemberment(AD&D)• Fire Insurance for loan Redemption Benefit (FI)

for the residence of the borrower.

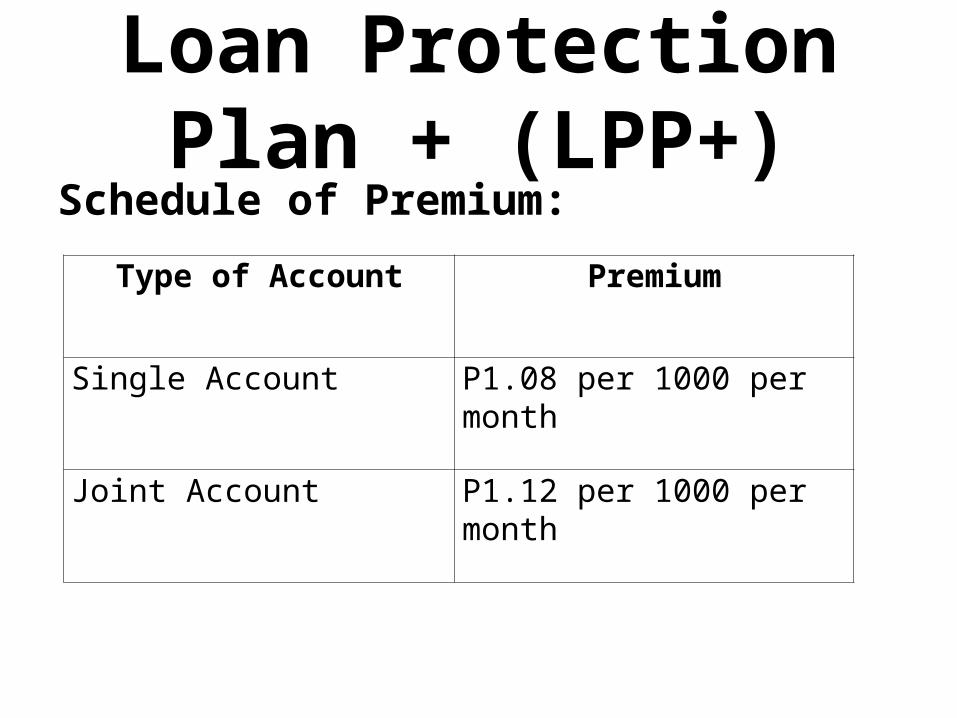

Loan Protection Plan + (LPP+)

Schedule of Premium:

Type of Account Premium

Single Account P1.08 per 1000 per month

Joint Account P1.12 per 1000 per month

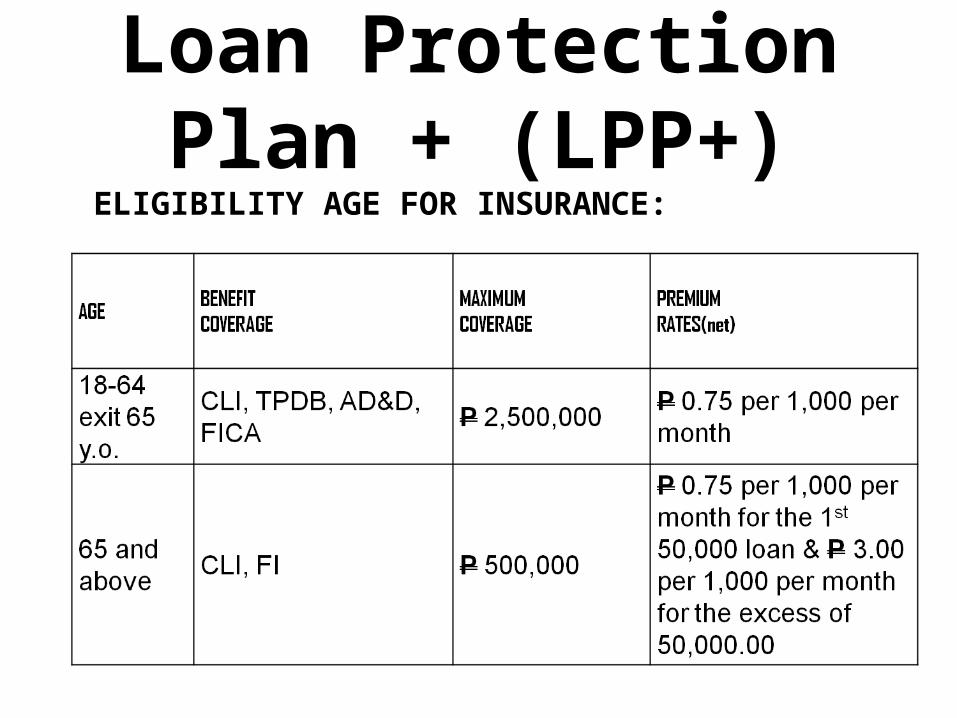

Loan Protection Plan + (LPP+)

SCHEDULE OF BENEFITS:

TYPE OF BENEFITS AMOUNT OF INSURANCECredit Life Insurance( CLI) 100% equal to the insured loan amount

Total and Permanent Disability Benefit(TPDB)

100% equal to the outstanding loan balance

Accidental Death and Dismemberment (AD&D )

100% equal to the Credit Life Insurance

Fire Insurance for loan Redemption Benefit (FI) for the residence of the borrower.

100% equal to the insured loan subject to the provision of losses: First 50,000 loss due to fire will be paid equal to the actual loss and the excess of 50,000 loss will subject to provisions of Fire Insurance Policy and shall not exceed the aggregate limit.

Loan Protection Plan + (LPP+)

ELIGIBILITY AGE FOR INSURANCE:

FICCO MBA(Mutual Benefit

Association)

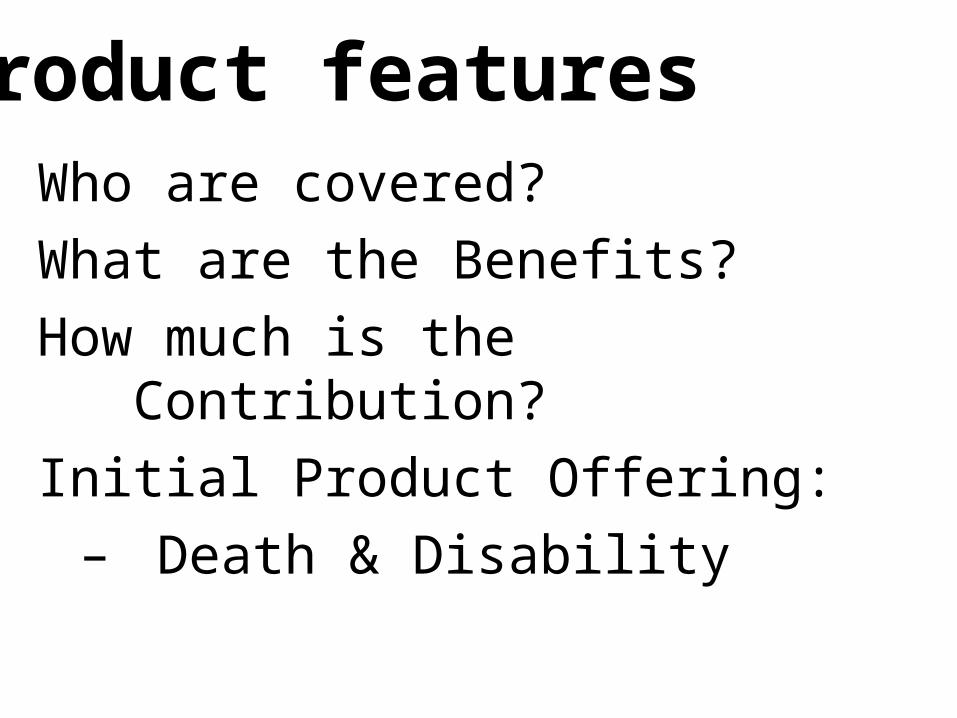

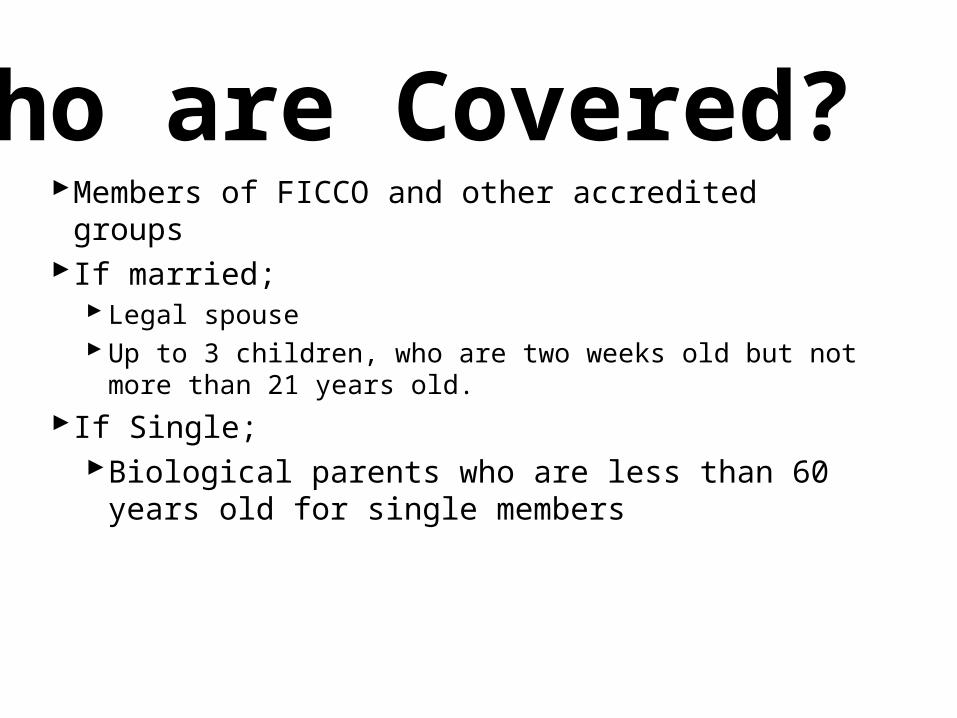

Who are covered?

What are the Benefits?

How much is the Contribution?

Initial Product Offering:

– Death & Disability

MBA product features

Members of FICCO and other accredited groupsIf married;

Legal spouse Up to 3 children, who are two weeks old but not more

than 21 years old.

If Single;Biological parents who are less than 60 years

old for single members

Who are Covered?

Benefits for One Unit Benefit

IF MEMBER/ DEPENDENT DIES: (in PhP)

a) w/in 3 months from membership 2,500

b) 3 mos. to 1 year 5,000

c) death under “a” or “b” is accident 20,000

d) dependent dies thru accident w/in 1 year of membership

5,000

e) member dies of natural causes after 1 year 40,000

f)member dies thru accident after 1 year 80,000

g) dependent dies due to natural cause after 1 year

10,000

h) dependent dies thru accident after 1 year 20,000

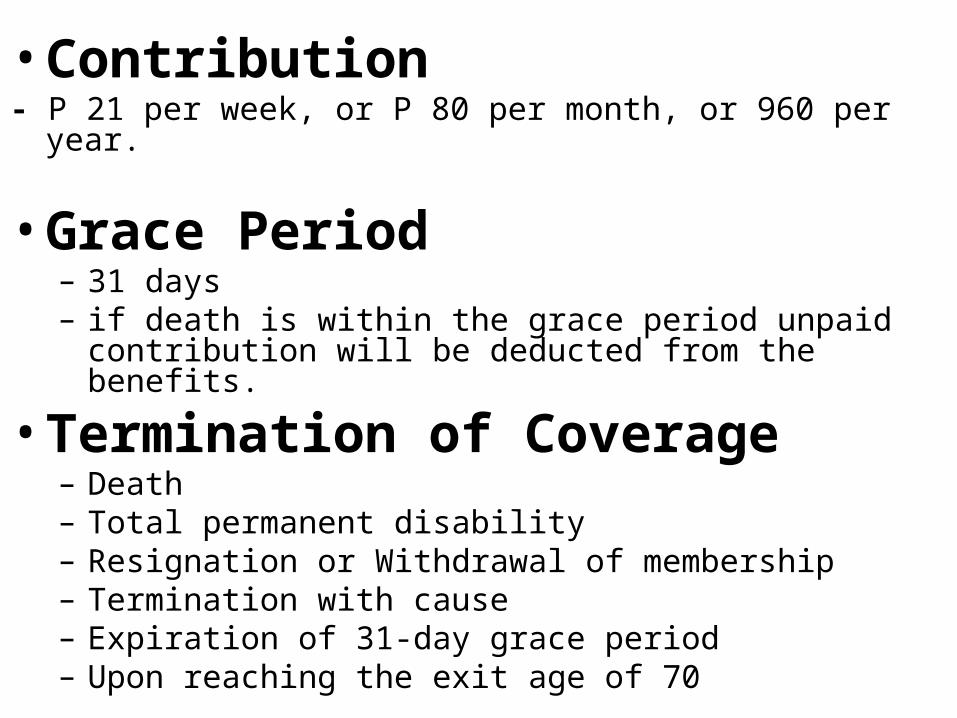

• Contribution - P 21 per week, or P 80 per month, or 960 per year.

• Grace Period – 31 days– if death is within the grace period unpaid contribution will be

deducted from the benefits.

• Termination of Coverage– Death– Total permanent disability– Resignation or Withdrawal of membership– Termination with cause– Expiration of 31-day grace period– Upon reaching the exit age of 70

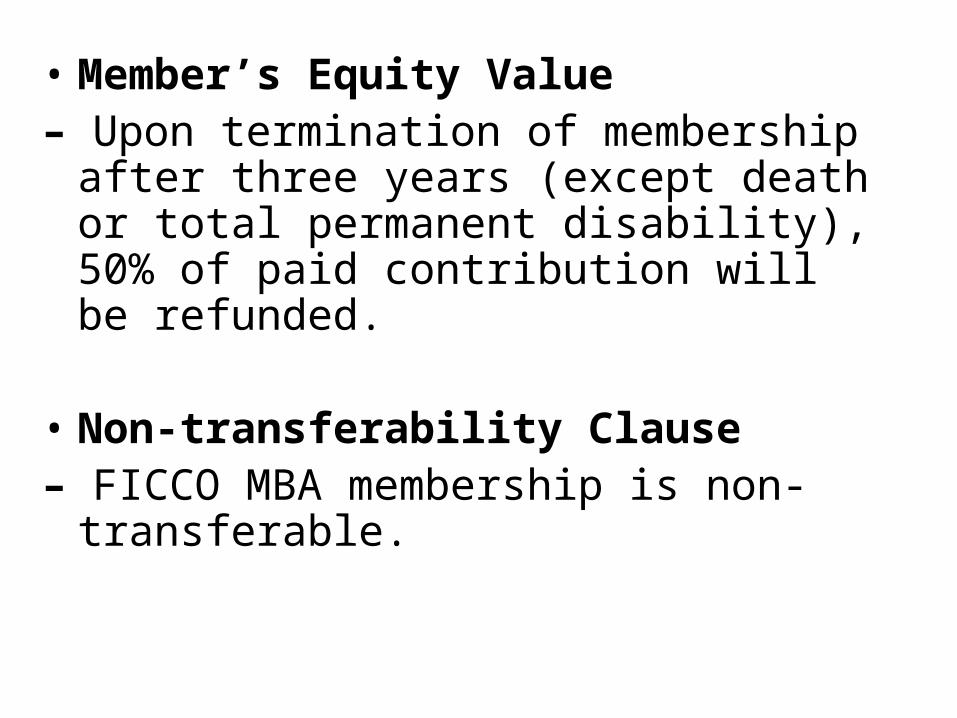

• Member’s Equity Value – Upon termination of membership after

three years (except death or total permanent disability), 50% of paid contribution will be refunded.

• Non-transferability Clause – FICCO MBA membership is non-

transferable.

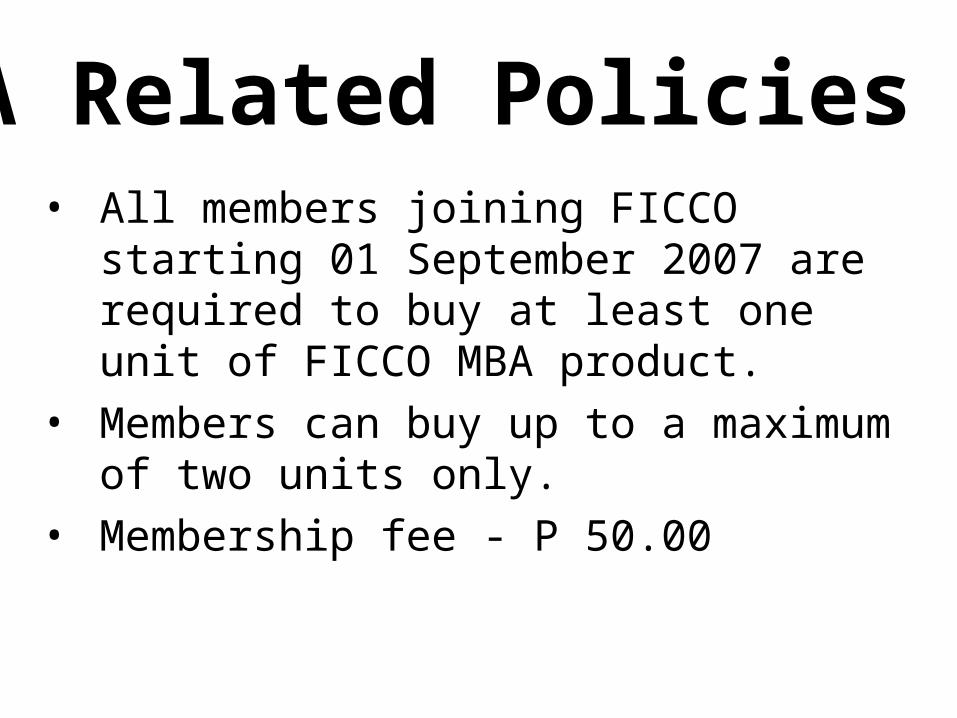

• All members joining FICCO starting 01 September 2007 are required to buy at least one unit of FICCO MBA product.

• Members can buy up to a maximum of two units only.

• Membership fee - P 50.00

MBA Related Policies

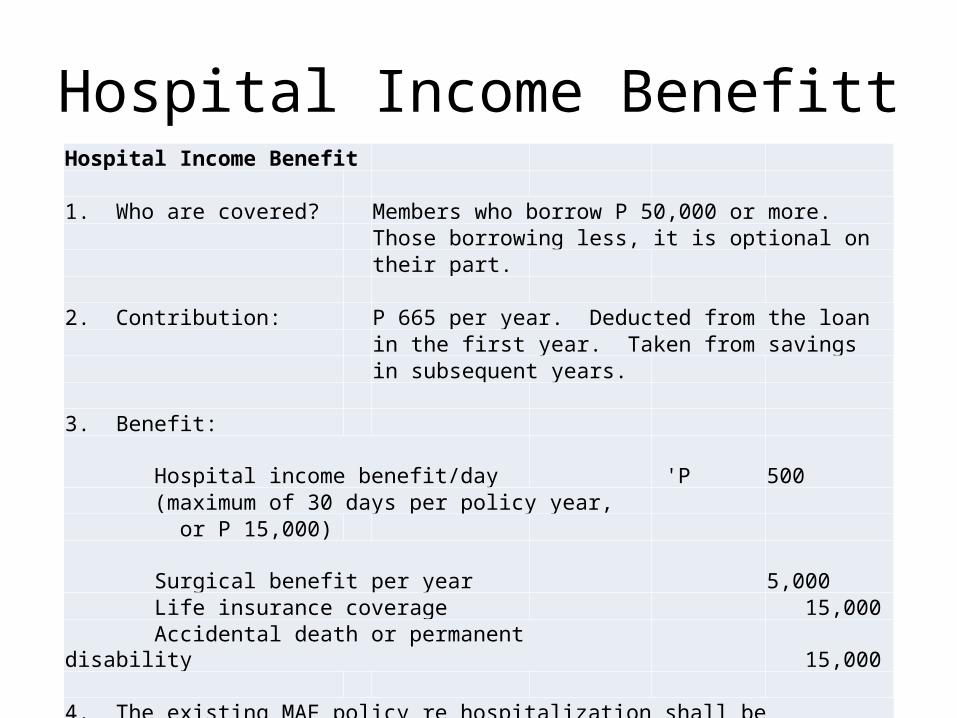

Hospital Income BenefittHospital Income Benefit

1. Who are covered? Members who borrow P 50,000 or more.Those borrowing less, it is optional on their part.

2. Contribution: P 665 per year. Deducted from the loanin the first year. Taken from savings in subsequent years.

3. Benefit: Hospital income benefit/day 'P 500 (maximum of 30 days per policy year, or P 15,000) Surgical benefit per year 5,000 Life insurance coverage 15,000 Accidental death or permanent disability 15,000

4. The existing MAF policy re hospitalization shall be observed.5. The MAF takes care of hospital bills. The HIB takes care of lost income.

Thank you!