Embed Size (px)

Citation preview

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-1

Responsibility Centers

A responsibility center is the point in an organization where the control over revenue or expense is located, e.g. division,department or a single machine.

A responsibility center may be divided into three categories cost profit investment

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-2

Cost

Types of Responsibility Centers

Cost Center A business segment that

incurs expenses but does not

generate revenue.

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-3

Profit Center A part of the

business that has control over both

revenues and expenses, but no

control over investment funds.

RevenuesSalesInterestOther

ExpensesManufacturingCommissionsSalariesOther

Types of Responsibility Centers

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-4

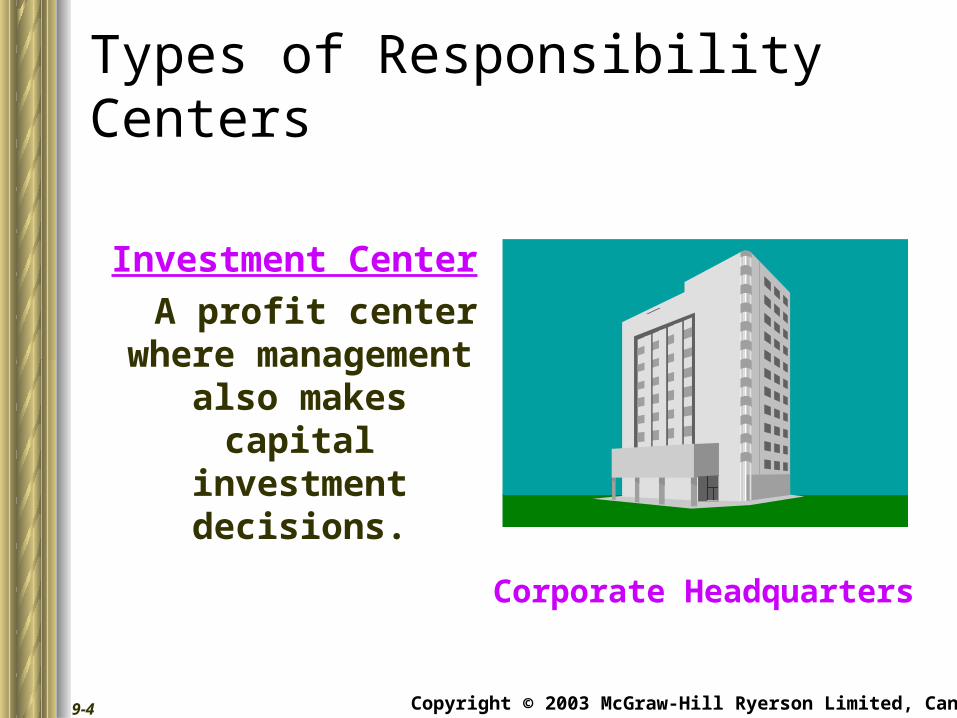

Investment Center

A profit center where

management also makes capital

investment decisions.

Corporate Headquarters

Types of Responsibility Centers

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-5

Measuring Managerial Performance

Return on investment (ROI) Residual income (RI)

CostCenter

Cost controlQuantity and qualityof services

ProfitCenter

InvestmentCenter

Evaluation Measures

Profitability

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-6

Return on investment is the ratio of income to the investment used to

generate the income.

ROI = Net Income Investment

Return on Investment

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-7

ROI = Net IncomeInvestment

ROI = Net IncomeSales

× SalesInvestment

MarginMargin TurnoverTurnover

Return on Investment

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-8

Cola Company reports the following:

Net Income $ 30,000

Sales $ 500,000

Investment $ 200,000

Let’s calculate ROI.

Return on Investment

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-9

ROI = 6% × 2.5 = 15%

Return on Investment

ROI = Net IncomeSales

× SalesInvestment

ROI = $30,000$500,000

× $500,000$200,000

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-10

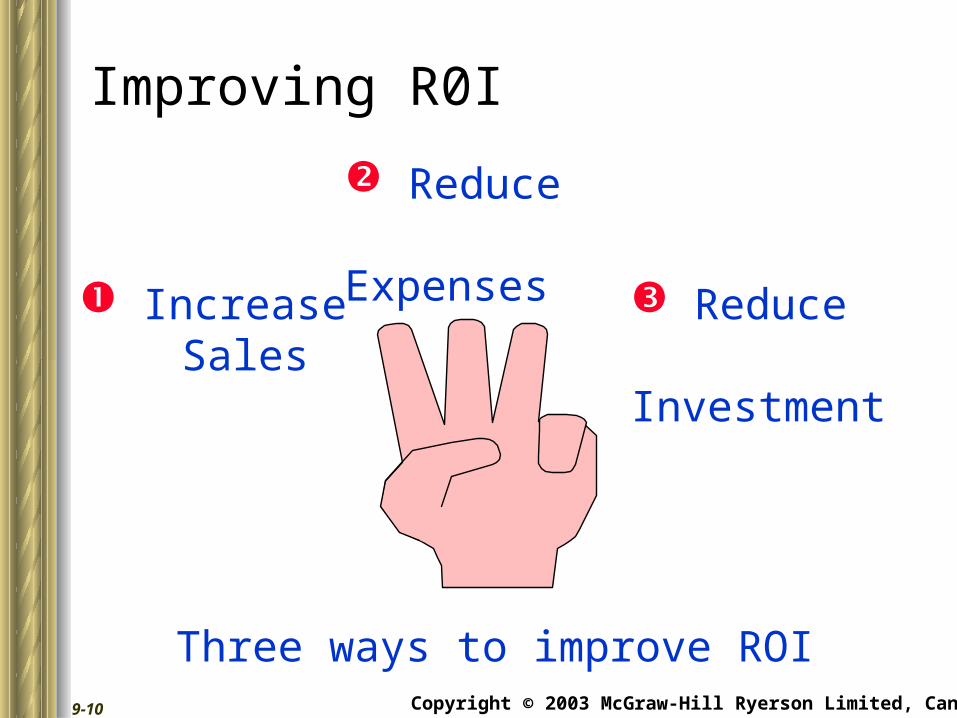

Improving R0I

Three ways to improve ROI

Increase Sales

Reduce Expenses

Reduce Investment

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-11

Cola Company’s manager was able to increase sales to $600,000 which increased net income to $42,000.

There was no change in investment.

Let’s calculate the new ROI.

Improving R0I

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-12

Cola Company increased ROI from 15% to 21%.

ROI = 7% × 3 = 21%

ROI = Net IncomeSales

× SalesInvestment

ROI = $42,000$600,000

× $600,000$200,000

Improving R0I

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-13

ROI - A Major Drawback As division manager at Cola Company,

your compensation package includesa salary plus bonus based on your division’sROI -- the higher your ROI, the bigger your bonus.

The company requires an ROI of 20% on all new investments -- your division has been producing an ROI of 30%.

You have an opportunity to invest in a new project that will produce an ROI of 25%.

As division manager would you invest in this project?

Copyright © 2003 McGraw-Hill Ryerson Limited, Canada9-14

ROI - A Major Drawback

As division manager,I wouldn’t invest in

that project becauseit would lower my pay!

Gee . . .I thought we were

supposed to do what was best for the

company!