Embed Size (px)

Citation preview

Copyright © 2015 Pearson Education, Inc. publishing as Prentice HallCopyright © 2015 Pearson Education, Inc. publishing as Prentice Hall7-7-11

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 7-2

Chapter 7

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Buying an existing business can help reduce risk for the entrepreneurBut, take your time!

Conduct a thorough analysis of the business and the opportunity it presents

Important questions:Does the business meet your lifestyle and financial

expectations?Do you have the ability to operate the business

successfully?

7-7-33

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Advantages of Buying an Existing BusinessBusiness may continue to be successfulLeverage the experience of the previous ownerOwning a business guarantees a jobThe turnkey businessSuperior locationEmployees and suppliers in placeEquipment installed with known production capacityInventory in place Trade credit establishedEasier access to financingHigh value

7-7-44

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

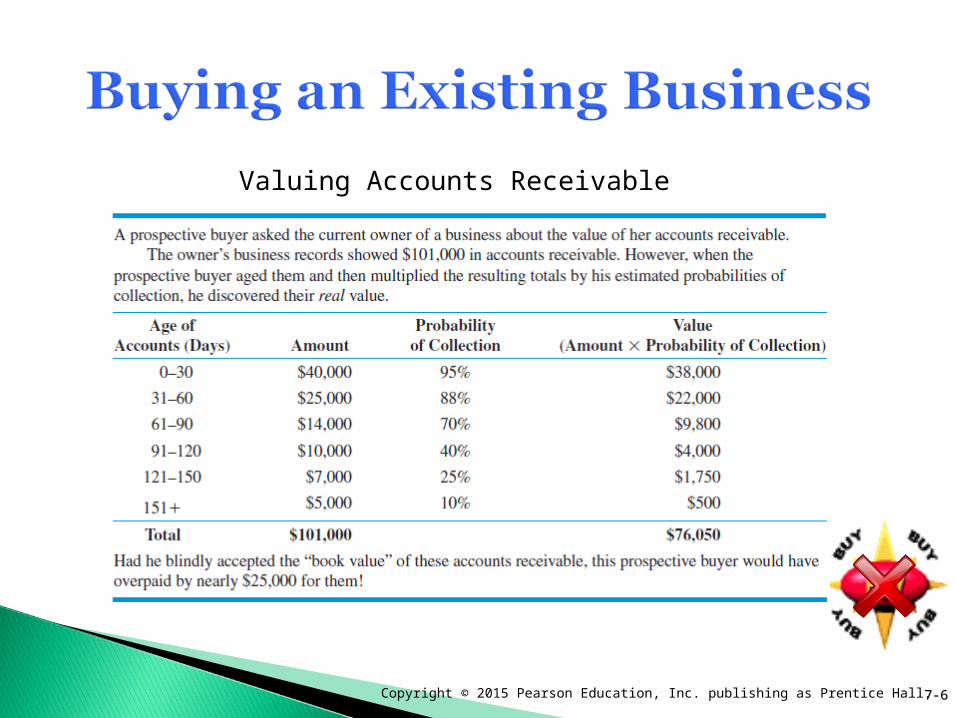

Disadvantages of Buying an Existing BusinessCash requirementsBusiness is losing moneyPaying for “ill will”Unsuitable employees Unsatisfactory location Obsolete or inefficient equipment and facilitiesCustomers may be loyal to previous ownerChange may be challenging to implementObsolete inventoryValue of accounts receivableBusiness is overpriced

7-7-55

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 7-7-66

Valuing Accounts Receivable

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 7-7-77

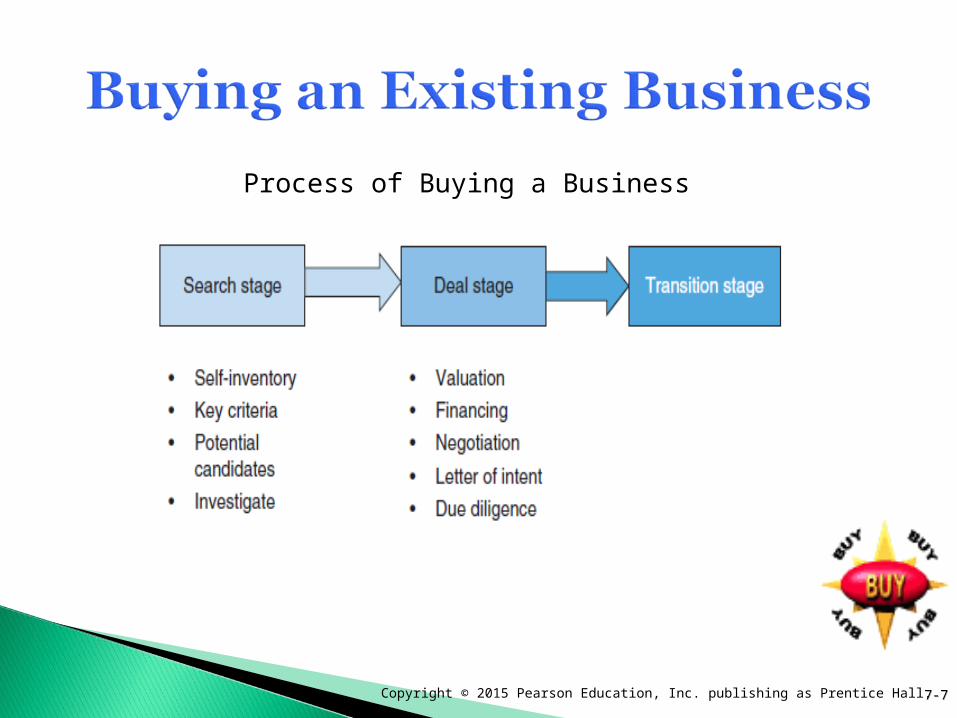

Process of Buying a Business

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

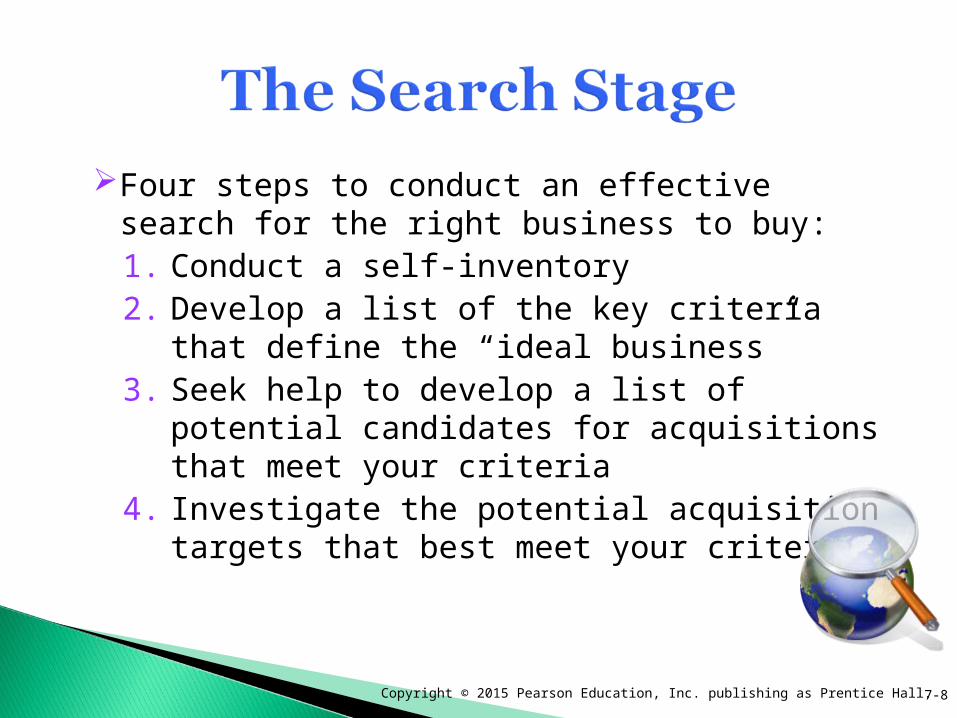

Four steps to conduct an effective search for the right business to buy:1. Conduct a self-inventory2. Develop a list of the key criteria that define the

“ideal business”3. Seek help to develop a list of potential candidates

for acquisitions that meet your criteria4. Investigate the potential acquisition targets that

best meet your criteria

7-8

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

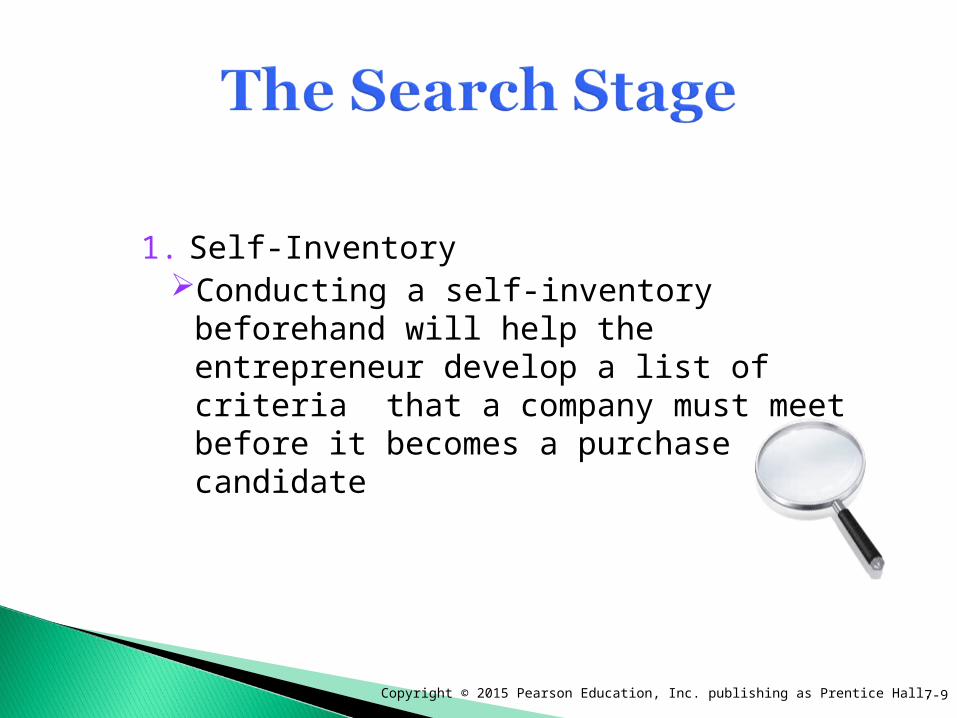

1. Self-InventoryConducting a self-inventory beforehand will

help the entrepreneur develop a list of criteria that a company must meet before it becomes a purchase candidate

7-9

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

2. Develop a List of CriteriaIdentify the characteristics of the “ideal

business” to focus on the viable candidates

7-10

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

3. Potential CandidatesBegin the search using:

The InternetBankersAccountantsAttorneysInvestment bankersTrade associationsContacting ownersNewspapers and trade journalsNetworking

7-11

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

4. InvestigationResearch the customer base

Existing and potential customersCompetitor analysis

Direct competitorsLevel of competition

Motivation of the sellerReal reason for selling

Review financesAt least three years of performance

7-12

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The deal stage includes:Valuing the businessFormalizing the financing of the purchaseNegotiating detailsLetter of intentDue diligence

7-13

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Methods for Determining the Value of a Business Assessing tangible assets is usually straightforwardValuing intangible assets is difficult

GoodwillNo single best method for determining value

Consider using severalDeal must work for both parties

7-14

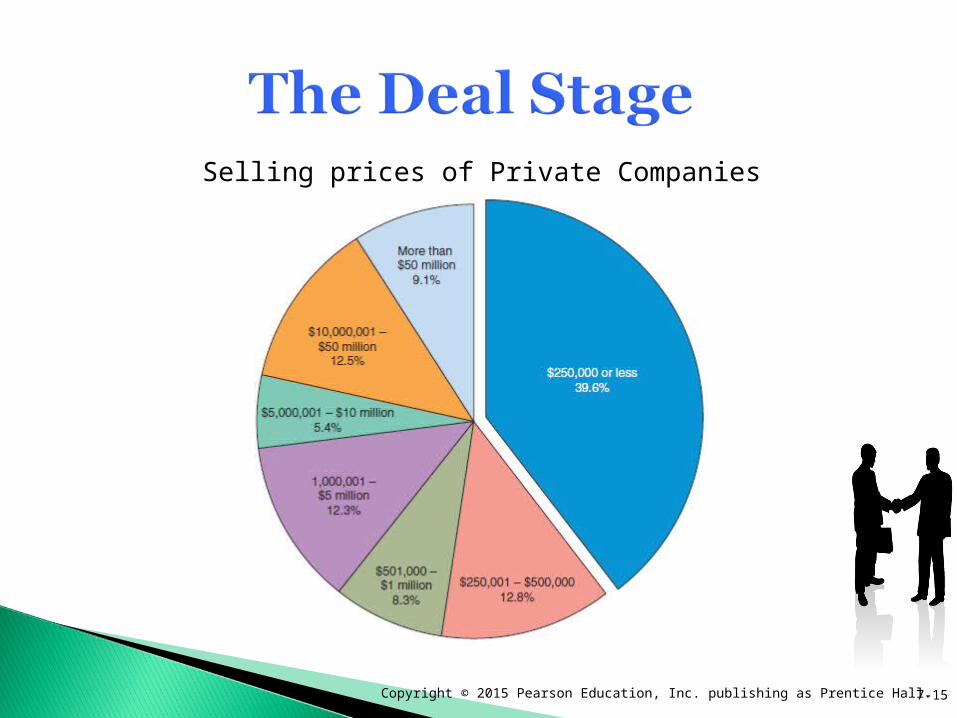

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 7-15

Selling prices of Private Companies

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

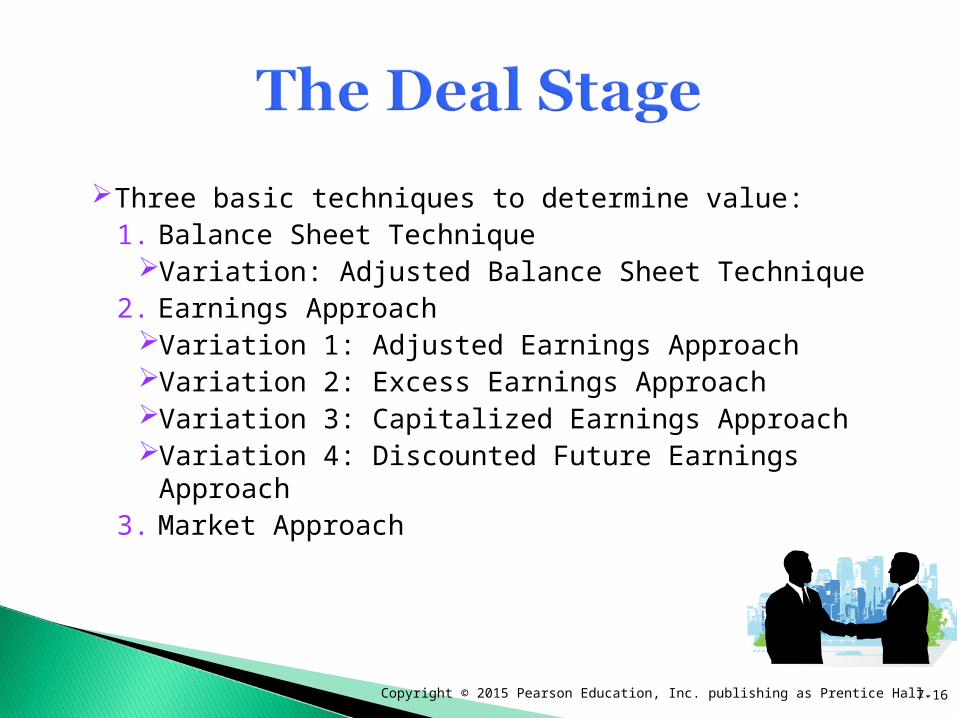

Three basic techniques to determine value: 1. Balance Sheet Technique

Variation: Adjusted Balance Sheet Technique2. Earnings Approach

Variation 1: Adjusted Earnings ApproachVariation 2: Excess Earnings ApproachVariation 3: Capitalized Earnings ApproachVariation 4: Discounted Future Earnings

Approach3. Market Approach

7-16

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

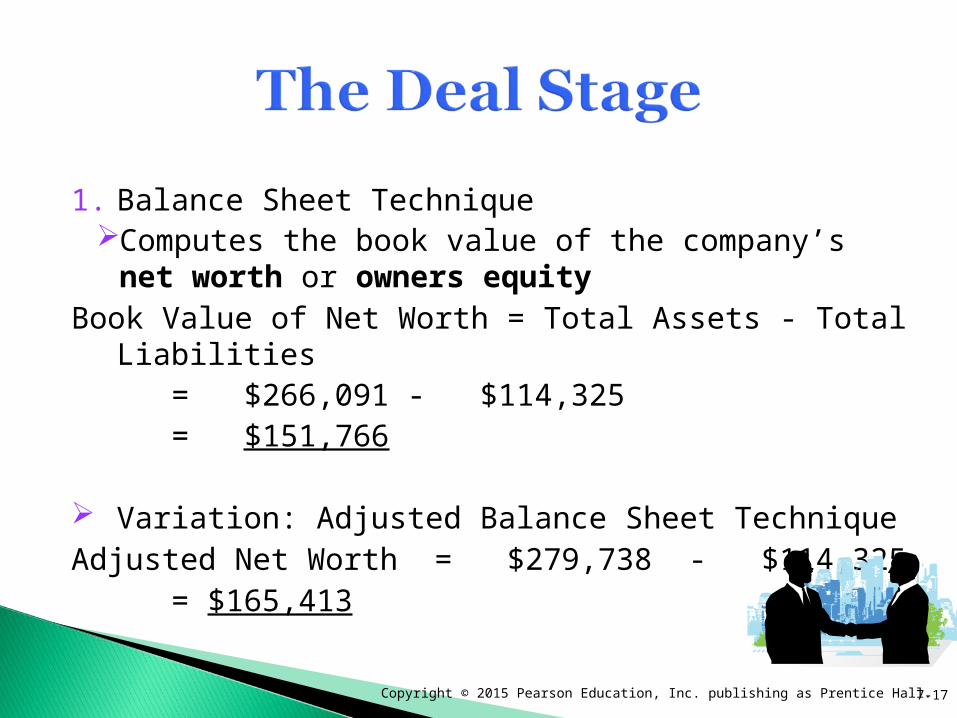

1. Balance Sheet Technique Computes the book value of the company’s net worth

or owners equityBook Value of Net Worth = Total Assets - Total

Liabilities= $266,091 - $114,325= $151,766

Variation: Adjusted Balance Sheet TechniqueAdjusted Net Worth = $279,738 - $114,325

= $165,413

7-17

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

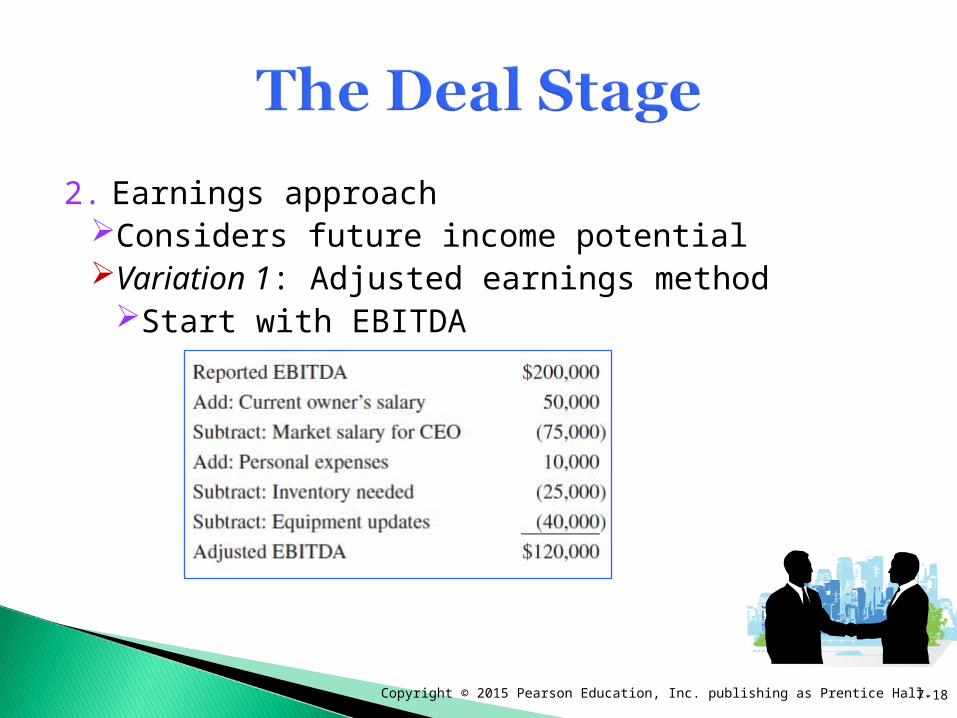

2. Earnings approachConsiders future income potentialVariation 1: Adjusted earnings method

Start with EBITDA

7-18

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

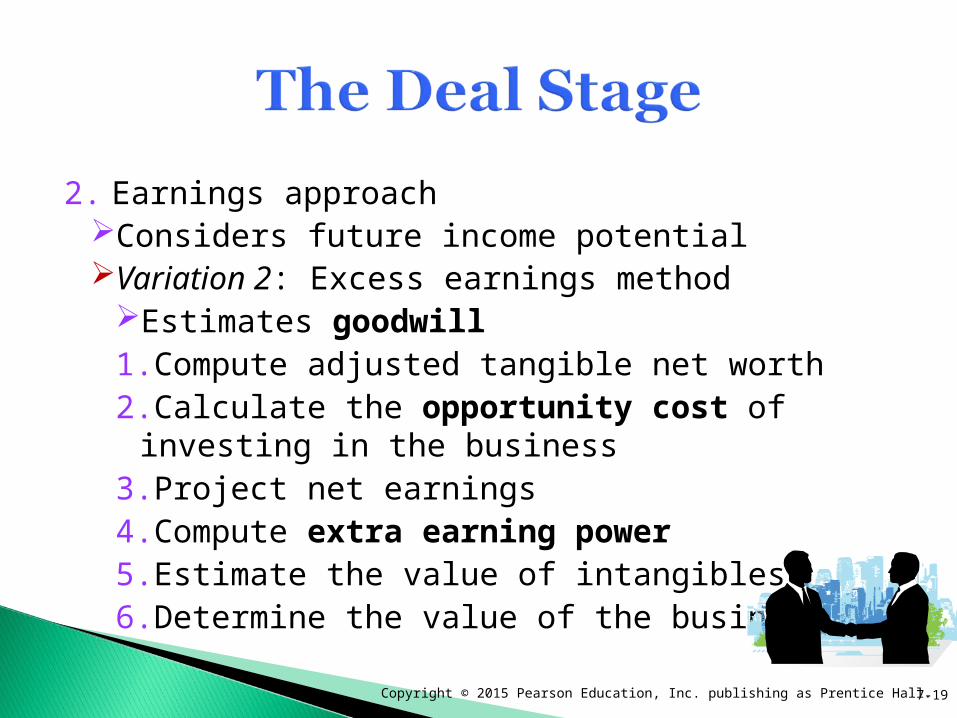

2. Earnings approachConsiders future income potentialVariation 2: Excess earnings method

Estimates goodwill 1.Compute adjusted tangible net worth2.Calculate the opportunity cost of investing in the

business3.Project net earnings4.Compute extra earning power5.Estimate the value of intangibles6.Determine the value of the business

7-19

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

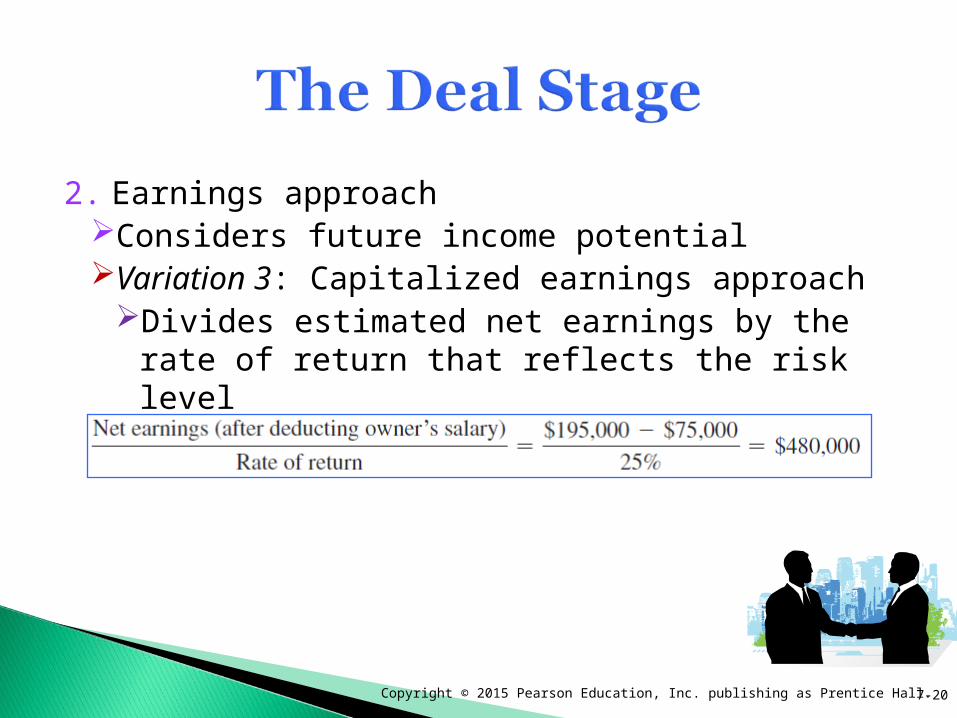

2. Earnings approachConsiders future income potentialVariation 3: Capitalized earnings approach

Divides estimated net earnings by the rate of return that reflects the risk level

7-20

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

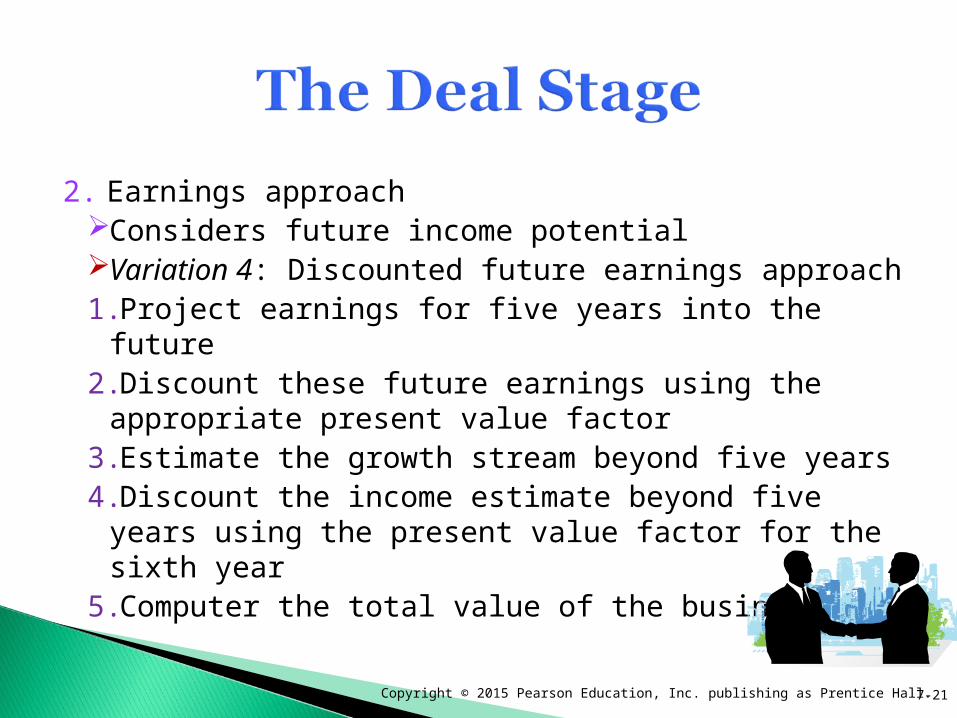

2. Earnings approachConsiders future income potentialVariation 4: Discounted future earnings approach1.Project earnings for five years into the future2.Discount these future earnings using the appropriate

present value factor3.Estimate the growth stream beyond five years4.Discount the income estimate beyond five years using

the present value factor for the sixth year5.Computer the total value of the business

7-21

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

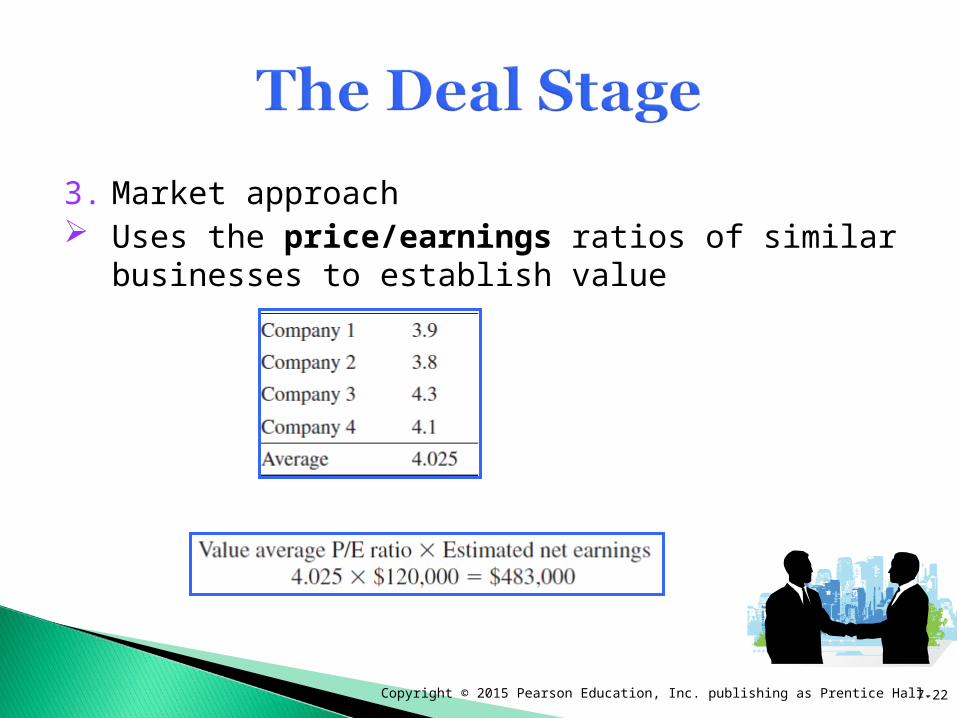

3. Market approach Uses the price/earnings ratios of similar businesses to

establish value

7-22

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

3. Market approach Disadvantages:

Necessary comparisons between publicly traded and privately owned companies

Unrepresentative earnings estimates Finding similar companies for comparison Applying the after-tax earnings of a private company to

determine its value

7-23

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The best method? There is no single best method

The final price will be based on the valuation used and the negotiating skills of both parties

7-24

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Negotiating the Deal The structure of the deal – the terms and

conditions of payment – is more important than the actual price the seller agrees to

The ‘art of the deal’ Both parties need to work to achieve their goals,

while making concessions to keep the negotiations alive

7-25

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 7-26

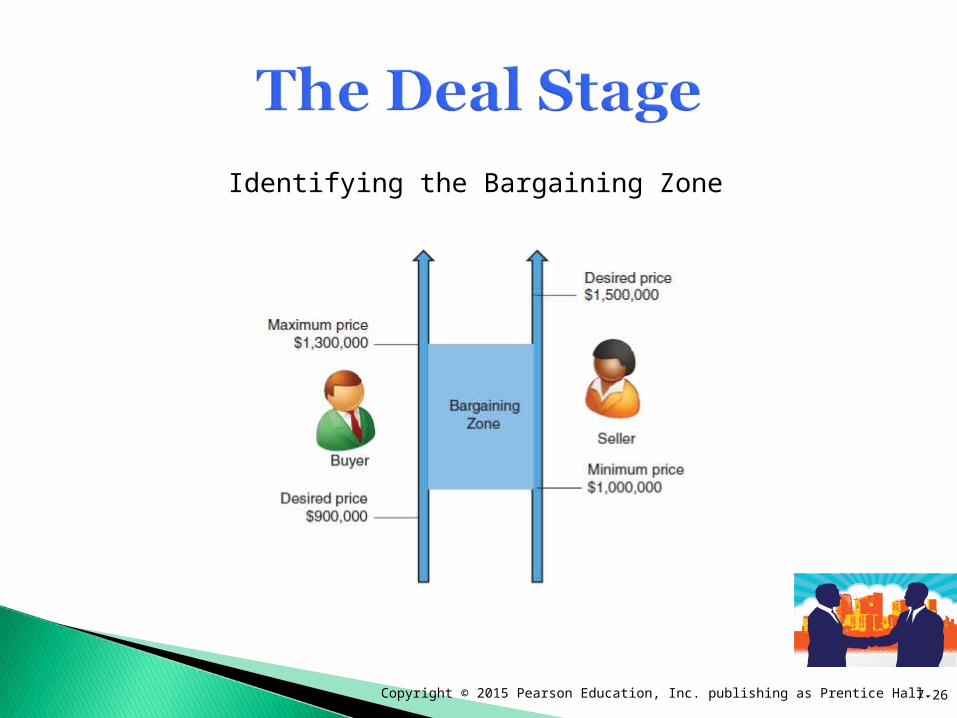

Identifying the Bargaining Zone

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Negotiating tips to help reach a mutually satisfying deal:

1. Establish the proper mindset2. Know what you want to have when you walk away

from the table 3. Develop a negotiating strategy4. Recognize the other party’s needs5. Be an empathetic listener

7-27

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

6. Avoid seeing the other side as “the enemy”7. Educate, don’t intimidate8. Be creative9. Keep emotions in check10.Be patient11. Don’t become a victim 12.Remember that “no deal” is an option

7-28

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The Buyer’s Goals:Get the business at the lowest price possibleNegotiate favorable payment terms, preferably over

timeGet assurances that he is buying the business he

thinks it isAvoid enabling the seller to open a competing

businessMinimize the amount of cash paid up front.

7-29

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The Seller’s Goals:Get the highest price possible for the companySever all responsibility for the company’s liabilitiesAvoid unreasonable contract terms that might limit

future opportunitiesMaximize the cash from the dealMinimize the tax burden from the saleMake sure the buyer will make all future payments

7-30

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The structure of the deal Straight business sale

Often the safest exit for an entrepreneur Usually the most expensive option Seller must be willing to finance part of the

purchase price Use a two-step sale

Business is purchased in two phases

7-31

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Letter of Intent A firm commitment by both sides that they are

ready to move toward closing the sale Only 25% of deals make it from the letter of

intent to the final closing

7-32

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The Due Diligence ProcessInvolves investigating three critical areas of the

business and the potential deal beyond those already evaluated earlier in the search and deal processes:1. Confirming valuation: What is the real value of

the business?2. Legal issues: What legal aspects of the

business are known or hidden risks?3. Financial state: Is the business financially

sound?

7-33

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

1. Confirming valuation Are the assets really useful, or are they obsolete? Will the assets require replacement soon? Do the assets operate efficiently?

Book value is not the same as market value Other factors:

Accounts receivableLease arrangementsBusiness recordsIntangible assetsLocation and appearance

7-34

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

2. Legal issues Liens Contract assignments

Due-on-sale clauses Covenants not to compete Ongoing legal liabilities

Physical premisesProduct liability claims

Product liability lawsuits Labor relations

7-35

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

3. Financial state Income statement and balance sheet for at

least three years Income tax return for at least three years Cash flow

Be wary if the seller refuses to disclose financial records!

7-36

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Closing the sale of a business is a complex legal process

Closing documents include: Asset purchase agreement Bill of sale Asset list Buyer’s disclosure statement Allocation of purchase price Non-compete agreement Consulting/Training agreement Transfer of subsidiaries associated with business

7-37

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Transfer of utilitiesTransfer of Web sites, social media addresses,

and phone numbersDocumentation of new entity that will own the

business and documentation of new bank account for that business

Transfer of merchant accountsNotice to creditorsLease assignments

7-38

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Financing documents, security agreement, promissory note, and UCC Financing Statement if seller is financing all or part of the sale

Sales tax and payroll tax clearanceEscrow instructionsClosing adjustments/prorationTransfer of any third party contractsCorporate resolution authorizing sale of the

corporate assets

7-39

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

To smooth the transition, a buyer should: Concentrate on communicating with employeesBe honest with employeesListen to employeesDevote time to selling the vision for the

company to key stakeholdersConsider asking the seller to serve as a

consultant until the transition is complete

7-40

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 7-7-4141