Embed Size (px)

Citation preview

A transformation journey to a “Future-ready” Banking model

WHITEPAPER JunE 2015

CORE BANKING MODERNIZATION

www.hcltech.com

AuthOr:John J. Norman

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 2

John J. Norman is a Senior Banking Principal for HCL, America for Financial Services North America. Prior to joining HCL, he was a Senior Management Consultant at IBM Global Business Services North America Banking Practice providing high level strategic technology guidance to financial institutions. Mr. Norman has broad domestic and international experience in the Information Technology industry, with particular emphasis on the planning, design, sales and management of strategic business applications and technology solutions in the Financial Services sector globally. He has built, rehabilitated and modernized major

financial institutions including private and commercial banks, State owned banks, government ministries and Central Banks around the world.Mr. Norman has exercised leadership roles in substantive engagements at every stage of the systems life cycle, including software development and sales, design of hardware/software solutions, systems integration, systems implementation and outsourcing, as well as management consulting and sales and marketing of Financial Services solutions (Core banking systems, Retail FS applications, BPO, etc.).Mr. Norman began his career as a systems analyst in London, England for the Phoenix of London Assurance Co. Ltd. in 1974. He returned to the United States in 1976 to assume a similar position with the Fireman’s Fund Insurance Co. before leaving to enter banking in 1978. He remained in California for several years with both Crocker Bank and Bank of America primarily in the role of Technical Planner for both retail and global commercial banking. In 1987, Mr. Norman entered management consulting working with firms such as Ernst & Young, CSC and KPMG. The majority of these engagements were global and brought him to a wide range of cultures and challenges, amongst them New Zealand, Columbia, Mexico, Germany, Saudi Arabia and Iraq. He was also CIO of Banco Capital in Mexico, Resident Senior Advisor to USAID in Bosnia and before joining EDS, Vice President at JP Morgan Chase Bank in Houston. He also served as Vice President of Retail Banking Consulting at Cognizant Technology Solutions. In 1989 to 1990, Mr. Norman was Project Director for the rehabilitation and modernization of the Rasheed Bank in Baghdad, Iraq, under the overall direction of the Minister of Finance and the Central Bank of Iraq. He led a combined team of subject matter experts from both Ernst and Young and Citibank to improve overall quality of service levels to the public, implement a state of the art electronic banking system throughout the country and upgrade the competitive image of the bank as a member of the international financial community. On August 2nd of 1990, he was taken hostage by the regime of Saddam Hussien and led a successful escape five days later, bringing along several of his colleagues to freedom.While employed by EDS Ltd. in London (2006), Mr. Norman served as an advisor to the Prince of Wales Trust Fund, overseeing the charitable donation of 60,000 used desktop computers to schools and hospitals in several African nations and depressed areas of Northern England (Tools for Schools). Prior to joining Accenture Software Group in 2010 where he supported business development of the Alnova banking system, Mr. Norman was an Independent Consultant to the International Finance Company, a division of the World Bank. He provided Information Technology expertise to IFC clients globally to develop and improve their SME banking operations, ensure consistent delivery of SME banking knowledge and advisory services in emerging markets, He established strong knowledge management and dissemination functions to formalize and share IFC’s experience and best practices. His client list also includes Development Alternatives International, USAID and Mercy Corp. to name but a few. Mr. Norman is a member of the Board of Directors of the ZOR Foundation, a Washington, D.C. non- profit organization that has raised monies to foster peace, international conflict resolution and financial support for victims of human rights abuses in the Middle East. The Zor Foundation played a strategic role in obtaining financial awards from the United States government to benefit U.S. servicemen and their families afflicted with Gulf War Syndrome as a result of the on-going war with Iraq.

ABOUT THE AUTHOR

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 3

TABLE OF CONTENTS

1. CORE BANKING SYSTEMS MODERNIZATION METHODOLOGY 41.1 PROGRESSIVE MODERNIZATION APPROACH TO

CORE BANKING MODERNIZATION 5

2. CORE BANKING SYSTEMS MODERNIZATION ROLES AND RESPONSIBILITIES 6

3. BUSINESS CASE COMPONENTS 73.1 BUSINESS CHALLENGES/ISSUES 7

3.2 PROJECT DEFINITION INCLUDING SCOPE & OPTIONS 7

3.3 LESSONS LEARNED 8

3.4 CLIENT COST/BENEFITS ANALYSIS 8

4. APPENDIX 9

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 4

1. CORE BANKING SYSTEMS MODERNIZATION METHODOLOGY

Changes within the market are forcing a different point of view

y Increased Regulatory requirement – financial institutions have experienced a significant increase in regulatory requirements (e.g. Dodd Frank, Consumer Financial Protection Bureau, SOX, Basel, etc.). To help insure integrity of their regulatory reporting, banks must confirm that their systems are properly integrated.

y Increased Competition – Banks must bring new functionality and products/services (mobile, social media, etc.) to market quickly. Existing I.T. systems hinder product development and time-to-market because every new product requires custom coding and significant integration effort.

y Increased Customer demands – Customers want to purchase products and view accounts across applications, channels, and geographies. The challenge of integrating ancillary solutions with today’s heavily customized Core systems can hamper a bank’s ability to provide customers with a unified view of their financial information.

Internal pressures are also driving banks to consider core system modernization

y Need for greater system flexibility – Expansion into new product lines requires a platform that is flexible and easily extendable. Legacy Core systems are today heavily customized after years of modifications which can severely limit a bank’s ability to execute its strategies.

y Outdated and costly systems and processes – Many banks are still running on technology developed in the 70’s and 80’s which limit front and back office staff facing many redundancies and slow system response times with requisite time frames for changes and updates and regression testing.

y Need for Improved System stability – Legacy systems are responding poorly in response to today’s complex demands, which include expanded data volumes and proliferation of product lines and channels.

y Diminished Legacy technology skills – Core banking skills are often poorly documented, forcing banks to rely on the knowledge and experience of a generation of workers who are nearing retirement or finding a vendor willing to “train up” for staff augmentation which unto itself is rare with all of the choice of new systems and technologies.

The challenge of core system legacy modernization

y Business/I.T. Alignment – Core system modernization strategies must be developed in conjunction with process rationalization and optimization. The business must clearly communicate its needs to I.T. to ensure adequate capacity planning and budgeting.

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 5

y Governance and stakeholder management – A robust governance structure is required to conceive, plan, design and execute the modernization program across multiple business lines.

y Requirements definition – All affected regions and departments need to define a set of business and regulatory requirements that are clear, accurate and comprehensive with participation sign-off from key stakeholders and are key contributors and participants from the beginning, not just tacked on at the end.

y Change management and communications – Communicate key project drivers and ongoing progress to all affected departments and business units with a regular communication vehicle to keep stakeholders apprised of the status and any changes as well as informing them of what is forthcoming.

y Risk Management – Core system modernization involves critical changes to a bank’s basic infrastructure. The associated large scale risks need to be actively managed and anticipated at every stage as well as contingency plans built accordingly.

1.1 PROGRESSIVE MODERNIZATION APPROACH TO CORE BANK-ING MODERNIZATION

HCL supports the progressive modernization approach – modernizing existing assets with a well- defined transformational roadmap. The modernized environment could be a mix of old and new co-existing together:

y Old legacy system codes – wrapped as services

y Old legacy code transformed into new code base

y Newly developed capabilities

y 3rd party integrated capabilities

1. Transformational Planning

– Business and Application Scope

– Applications analysis and architecture design

– Execution Roadmap

– Business case

2. Foundational Architecture

– Master Data

– Integration layer

– Service oriented design

– Separation of application concerns (UI, logic, integration, data access, etc.)

3. Legacy Modernization

– Legacy harvesting of business rules, workflow abstraction and modeling

– Data migration, code modernization

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 6

4. New Capability Development

– Model driven development

– Business service modeling to support business processes

5. Execution through a modernization factory

– Tools, assets, accelerators and methods

– Software modeling, development, and testing

6. Governance and change control

– Identify, design, develop, publish and maintain services

– Program management

– Change configuration management

2. CORE BANKING SYSTEMS MODERNIZATION ROLES AND RESPONSIBILITIES

Executive Sponsor

y Provide access to the appropriate parties, e.g., subject matter experts (SME’s), executive stakeholders

y Champion recommendations and ideas for improvement

y Provide subject matter expertise, guidance and governance to the Project Team

y 3-4 hours per week

Project Manager

y Coordinate interactions and questions with the Core banking system team

y Provide access to the appropriate parties, e.g. subject matter experts (SME’S), executive stakeholders

y Participate in gathering sessions; review and provide input to project deliverables

y Monitor progress, identify issues/risks and initiate corrective action

y Coordinate activities with bank’s staff and 3rd parties (as needed); provide additional administrative support/coordination, etc.

y 50% average time commitment throughout diagnostic evaluation

Architects (Enterprise, Application, Data, Security, Integration)

y Provide specific knowledge and insight into legacy system architecture component capabilities and challenges. Participate in information gathering sessions and contribute to work product development

y 15% - 20% average time commitment

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 7

Subject Matter Experts (SME)

y Provide insight and subject matter expertise on current state business and I.T. environments, potential target state strategies, priorities, challenges, etc.

y Participate in interviews, facilitated working sessions, and other information gathering activities

y Provide input into analysis and project work products

y As needed basis, average 1 day per week depending on project activities

Business Analyst

y Identify opportunities for improvement in business operations and processes

y Support design or modification of business and IT systems

y Interacts with the business stakeholders and subject matter experts in order to understand their problems and needs

y The analyst interacts with system architects to provide business knowledge

3. BUSINESS CASE COMPONENTS

3.1 BUSINESS CHALLENGES/ISSUES

y These could range anywhere from a bank merged with another leading domestic bank with each having a legacy Core system that were account centric and not customer centric

y Legacy systems were old and product was siloed and did not allow the bank to introduce new products and services to its customers on a timely basis

y Very limited capability to get full customer insight across channels thereby restricting abilities to cross-sell

y High Cost to Income ratio (CIR)> 50%

3.2 PROJECT DEFINITION INCLUDING SCOPE & OPTIONS

y After an analysis or the existing packages in the market, the bank decided to undertake a multi-year “progressive renovation” of the existing Core system

y The also choose to pursue a “master data” strategy focused on Customer, Product and Contract and developed new enterprise components to serve these domains

y The bank also used a Component model approach to design the business, application and enterprise architectures

y The bank adopted the transformation to the new architecture as the new way of life from the very top and mandated all stakeholders to support the transformation journey

y Potential risks and issues through the transformation journey

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 8

3.3 LESSONS LEARNED

y Strong support from all stakeholders

y Achievement of transformation benefits progress were factored in executive performance and a strong business case drove the need to achieve modernization

y Architecture simplification was at the core of the modernization journey

y The roadmap set clear achievable, financial and technical goals to measure progress

3.4 CLIENT COST/BENEFITS ANALYSIS

y Reducing CIR from >50% to <40%

y Adding >8% to operating leverage

y Significantly boosting revenue and cut down on technology cost

y Unlocked almost 20% from the net operating cost of the bank

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 9

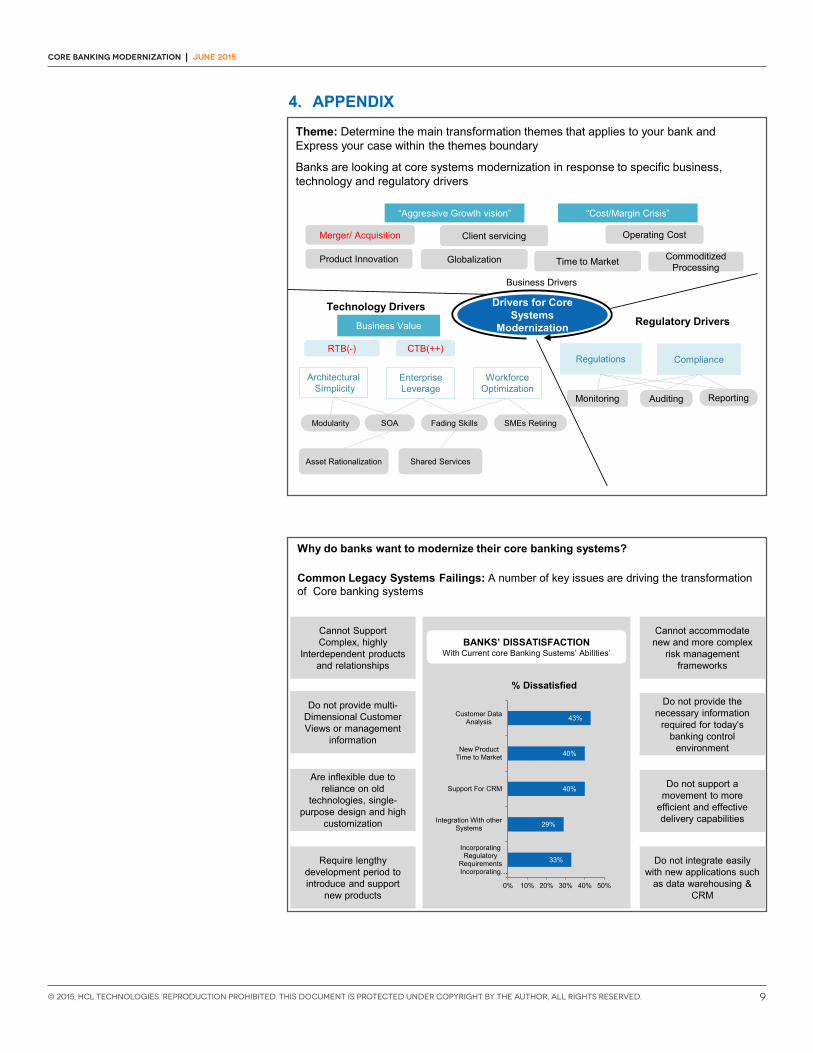

4. APPENDIX

Theme: Determine the main transformation themes that applies to your bank and Express your case within the themes boundary

Banks are looking at core systems modernization in response to specific business, technology and regulatory drivers

“Aggressive Growth vision” “Cost/Margin Crisis”

Merger/ Acquisition Client servicing

Product Innovation Globalization Time to Market

Operating Cost

Commoditized Processing

Business Drivers

Regulatory DriversTechnology Drivers

Business Value

CTB(++)

ArchitecturalSimplicity

Enterprise Leverage

WorkforceOptimization

Regulations Compliance

Modularity

Asset Rationalization

SOA Fading Skills

Shared Services

Monitoring Auditing Reporting

RTB(-)

Drivers for CoreSystems

Modernization

SMEs Retiring

Why do banks want to modernize their core banking systems?

Common Legacy Systems Failings: A number of key issues are driving the transformation of Core banking systems

BANKS’ DISSATISFACTIONWith Current core Banking Sustems’ Abilities’

Cannot Support Complex, highly

Interdependent productsand relationships

Do not provide multi-Dimensional CustomerViews or management

information

Are inflexible due to reliance on old

technologies, single-purpose design and high

customization

Require lengthy development period to introduce and support

new products

Cannot accommodate new and more complex

risk management frameworks

Do not provide the necessary information

required for today’s banking control

environment

Do not support a movement to more

efficient and effective delivery capabilities

Do not integrate easily with new applications such

as data warehousing & CRM

% Dissatisfied

33%

29%

40%

40%

43%

0% 10% 20% 30% 40% 50%

IncorporatingRegulatory

RequirementsIncorporating…

Integration With otherSystems

Support For CRM

New ProductTime to Market

Customer DataAnalysis

CORE BANKING MODERNIZATION | JuNE 2015

© 2015, HCL TECHnOLOGIES. REPRODuCTIOn PROHIBITED. THIS DOCuMEnT IS PROTECTED unDER COPYRIGHT BY THE AuTHOR, ALL RIGHTS RESERVED. 10

To Exploit New Architectural/Technological

Constructs

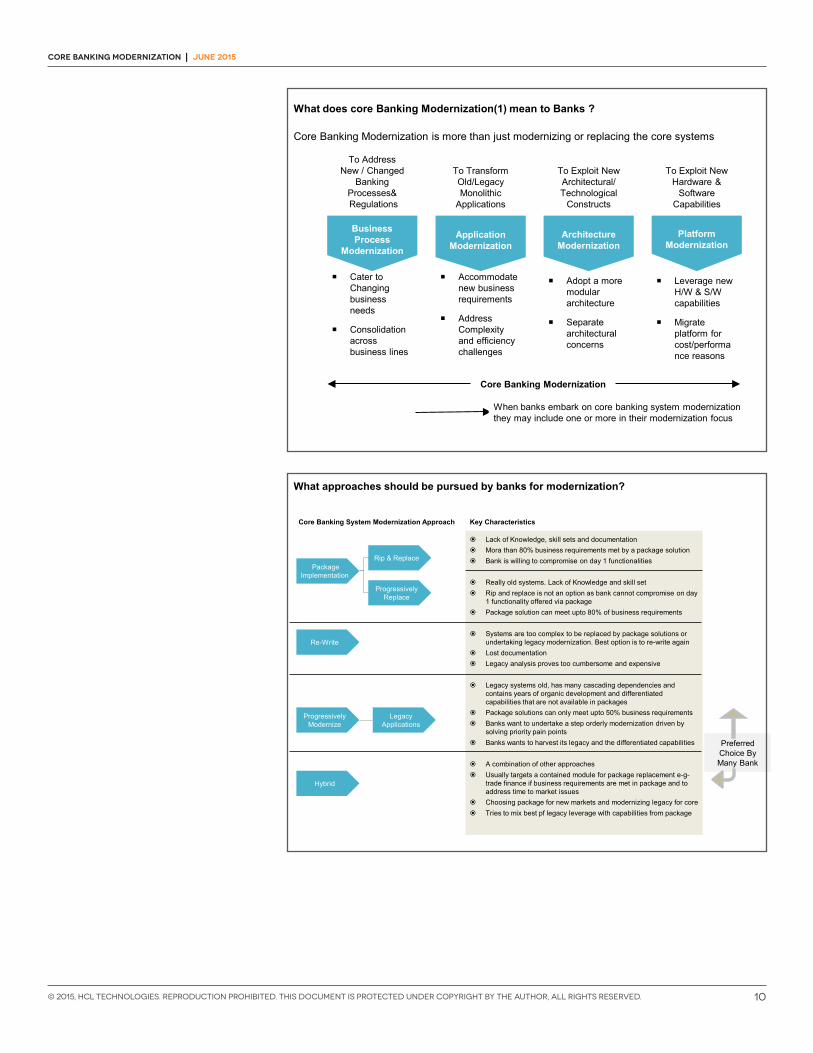

What does core Banking Modernization(1) mean to Banks ?

Core Banking Modernization is more than just modernizing or replacing the core systems

To Address New / Changed

Banking Processes&Regulations

To TransformOld/LegacyMonolithic

Applications

To Exploit New Hardware &

SoftwareCapabilities

BusinessProcess

Modernization

ApplicationModernization

ArchitectureModernization

PlatformModernization

Cater to Changing business needs

Consolidation across business lines

Accommodate new business requirements

Address Complexity and efficiency challenges

Leverage new H/W & S/W capabilities

Migrate platform for cost/performance reasons

Adopt a more modular architecture

Separate architectural concerns

Core Banking Modernization

When banks embark on core banking system modernization they may include one or more in their modernization focus

What approaches should be pursued by banks for modernization?

Core Banking System Modernization Approach Key Characteristics

PackageImplementation

Rip & Replace

ProgressivelyReplace

LegacyApplications

Re-Write

ProgressivelyModernize

Hybrid

Preferred Choice By Many Bank

Lack of Knowledge, skill sets and documentation Mora than 80% business requirements met by a package solution Bank is willing to compromise on day 1 functionalities

Really old systems. Lack of Knowledge and skill set Rip and replace is not an option as bank cannot compromise on day

1 functionality offered via package Package solution can meet upto 80% of business requirements

Systems are too complex to be replaced by package solutions or undertaking legacy modernization. Best option is to re-write again

Lost documentation Legacy analysis proves too cumbersome and expensive

Legacy systems old, has many cascading dependencies and contains years of organic development and differentiated capabilities that are not available in packages

Package solutions can only meet upto 50% business requirements Banks want to undertake a step orderly modernization driven by

solving priority pain points Banks wants to harvest its legacy and the differentiated capabilities

A combination of other approaches Usually targets a contained module for package replacement e-g-

trade finance if business requirements are met in package and to address time to market issues

Choosing package for new markets and modernizing legacy for core Tries to mix best pf legacy leverage with capabilities from package

ABOUT HCL

About HCL Technologies

HCL Technologies is a leading global IT services company working with clients in the areas that impact and redefine the core of their businesses. Since its emergence on the global landscape, and after its IPO in 1999, HCL has focused on ‘transformational outsourcing’, underlined by innovation and value creation, offering an integrated portfolio of services including software-led IT solutions, remote infrastructure management, engineering and R&D services and business services. HCL leverages its extensive global offshore infrastructure and network of offices in 31 countries to provide holistic, multi-service delivery in key industry verticals including Financial Services, Manufacturing, Consumer Services, Public Services and Healthcare & Life sciences. HCL takes pride in its philosophy of ‘Employees First, Customers Second’ which empowers its 104,184 transformers to create real value for customers. HCL Technologies, along with its subsidiaries, had consolidated revenues of US$ 5.8 billion, for the Financial Year ended as on 31st March 2015 (on LTM basis). For more information, please visit www.hcltech.com

About HCL Enterprise

HCL is a $6.8 billion leading global technology and IT enterprise comprising two companies listed in India – HCL Technologies and HCL Infosystems. Founded in 1976, HCL is one of India’s original IT garage start-ups. A pioneer of modern computing, HCL is a global transformational enterprise today. Its range of offerings includes product engineering, custom & package applications, BPO, IT infrastructure services, IT hardware, systems integration, and distribution of information and communications technology (ICT) products across a wide range of focused industry verticals. The HCL team consists of over 109,643 professionals of diverse nationalities, who operate from 31 countries including over 505 points of presence in India. HCL has partnerships with several leading global 1000 firms, including leading IT and technology firms. For more information, please visit www.hcl.com

Hello there! I am an Ideapreneur. I believe that sustainable business outcomes are driven by relationships nurtured through values like trust, transparency and flexibility. I respect the contract, but believe in going beyond through collaboration, applied innovation and new generation partnership models that put your interest above everything else. Right now 105,000 Ideapreneurs are in a Relationship Beyond the Contract™ with 500 customers in 31 countries. How can I help you?