Embed Size (px)

Citation preview

Corporate BriefingFor the year ended

December 31, 2018

March 8, 2019

2

Sequence of Presentation

2018 Review

Corporate Awards

Thar Energy Limited

Future Outlook / Challenges

Q & A Session

1

2

3

4

5

2018 Review

4

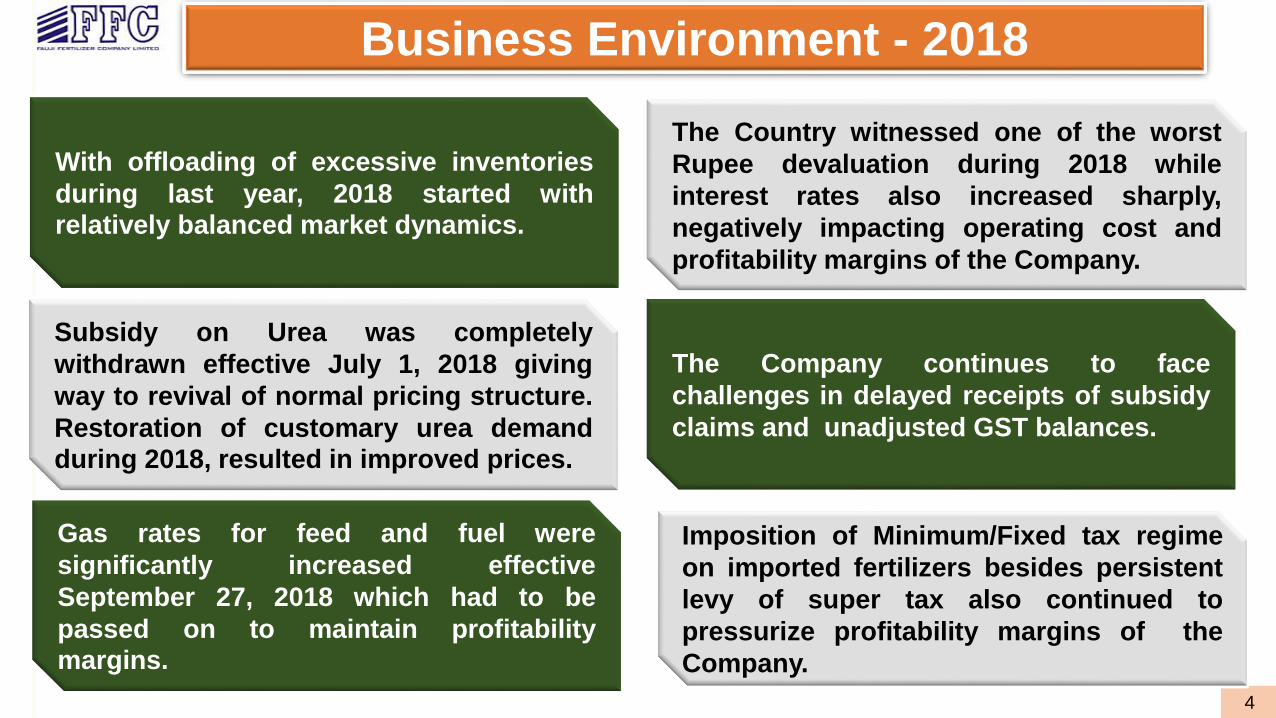

Business Environment - 2018

Business Environment - 2017

With offloading of excessive inventories

during last year, 2018 started withrelatively balanced market dynamics.

Subsidy on Urea was completely

withdrawn effective July 1, 2018 giving

way to revival of normal pricing structure.

Restoration of customary urea demandduring 2018, resulted in improved prices.

Gas rates for feed and fuel were

significantly increased effective

September 27, 2018 which had to be

passed on to maintain profitabilitymargins.

The Country witnessed one of the worst

Rupee devaluation during 2018 while

interest rates also increased sharply,

negatively impacting operating cost and

profitability margins of the Company.

Imposition of Minimum/Fixed tax regime

on imported fertilizers besides persistent

levy of super tax also continued to

pressurize profitability margins of the

Company.

The Company continues to face

challenges in delayed receipts of subsidy

claims and unadjusted GST balances.

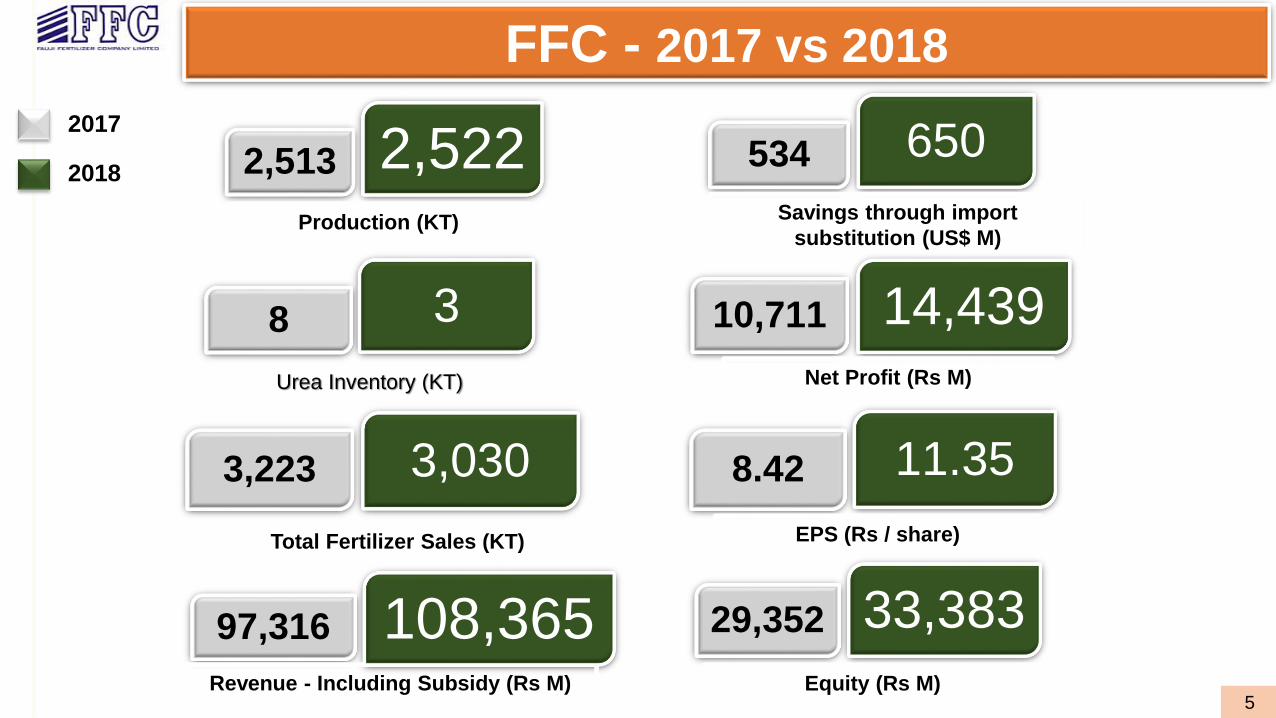

5

Savings through import

substitution (US$ M)

650534

3,0303,223

Total Fertilizer Sales (KT)

Equity (Rs M)

33,38329,352

14,439Net Profit (Rs M)

10,711

Urea Inventory (KT)

38

108,365Revenue - Including Subsidy (Rs M)

97,316

11.358.42

EPS (Rs / share)

FFC - 2017 vs 2018

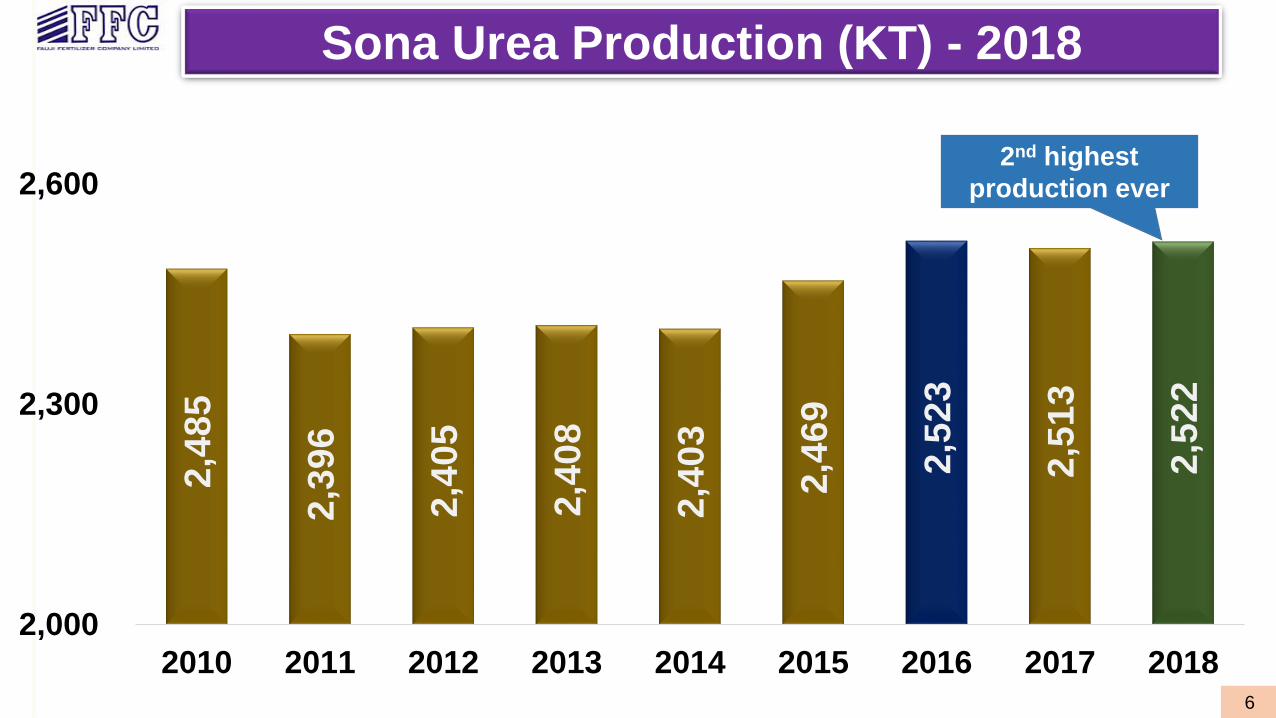

2,5222,513

Production (KT)

2017

2018

6

2nd highest

production ever

Sona Urea Production (KT) - 2018

2,4

85

2,3

96

2,4

05

2,4

08

2,4

03

2,4

69

2,5

23

2,5

13

2,5

22

2,000

2,300

2,600

2010 2011 2012 2013 2014 2015 2016 2017 2018

7

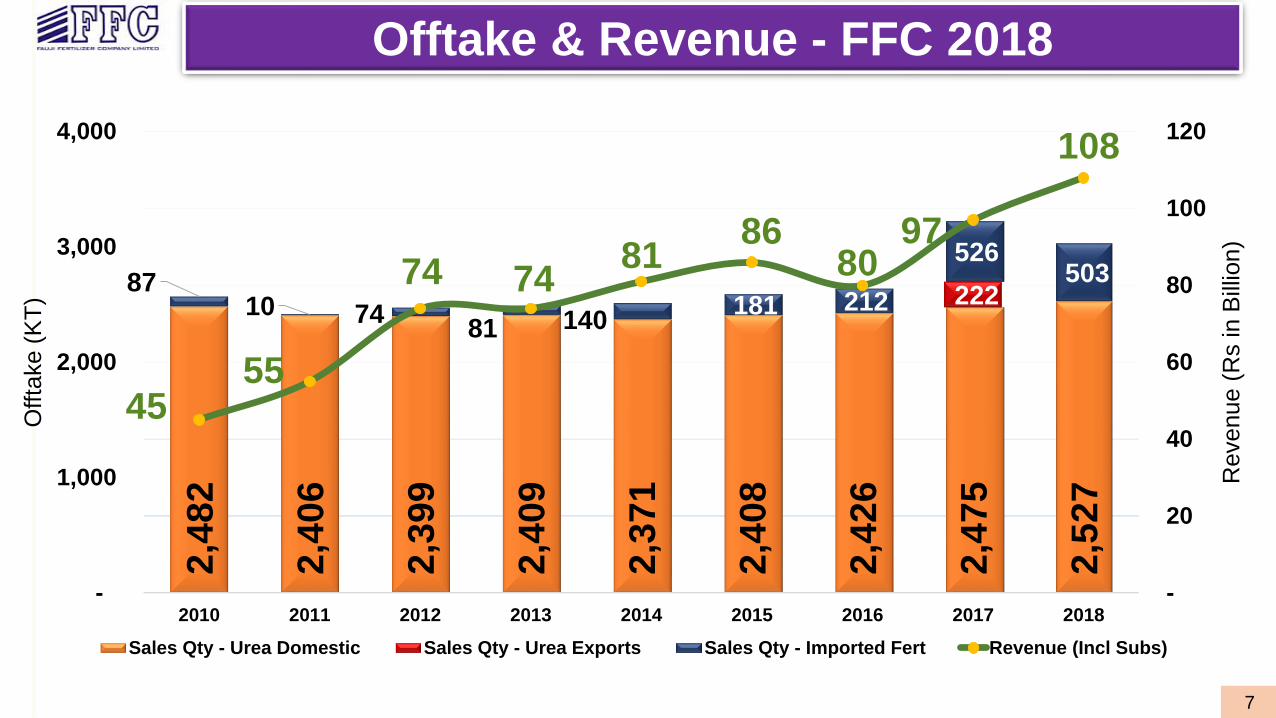

Offtake & Revenue - FFC 2018

2,4

82

2,4

06

2,3

99

2,4

09

2,3

71

2,4

08

2,4

26

2,4

75

2,5

27

222 87

10 74 81 140

181 212

526 503

45 55

74 74 81

86 80

97

108

-

20

40

60

80

100

120

-

1,000

2,000

3,000

4,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

Revenue (

Rs in B

illio

n)

Offta

ke (

KT

)

Sales Qty - Urea Domestic Sales Qty - Urea Exports Sales Qty - Imported Fert Revenue (Incl Subs)

8

Industry Urea Sales - Domestic (KT)

5,276 5,903

5,618 5,585 5,500 5,816 5,810

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2012 2013 2014 2015 2016 2017 2018

9

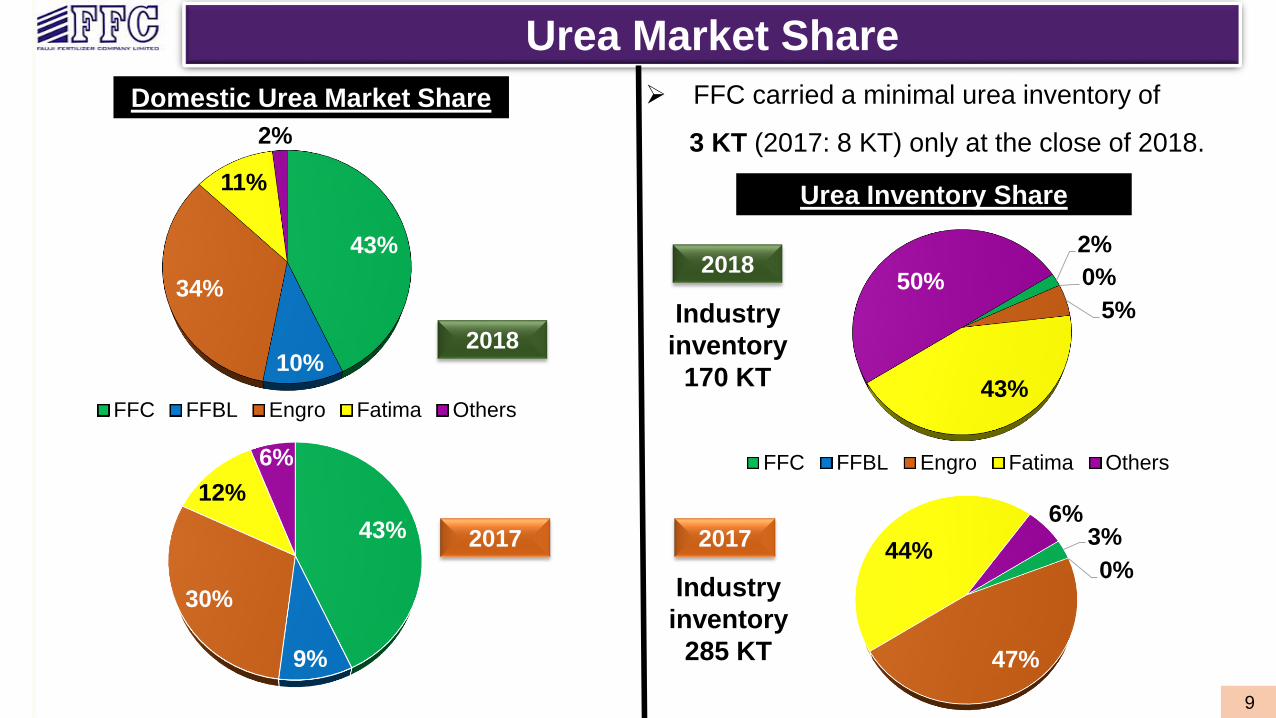

2%

43%

Domestic Urea Market Share

9%

4%

2017

Urea Market Share

43%

9%

30%

12%

6%

2018

43%

10%

34%

11%

2%

FFC FFBL Engro Fatima Others

3%

0%

47%

44%

6%2017

2018

Urea Inventory Share

2%

0%

5%

43%

50%

FFC FFBL Engro Fatima Others

FFC carried a minimal urea inventory of

3 KT (2017: 8 KT) only at the close of 2018.

Industry

inventory

170 KT

Industry

inventory

285 KT

10

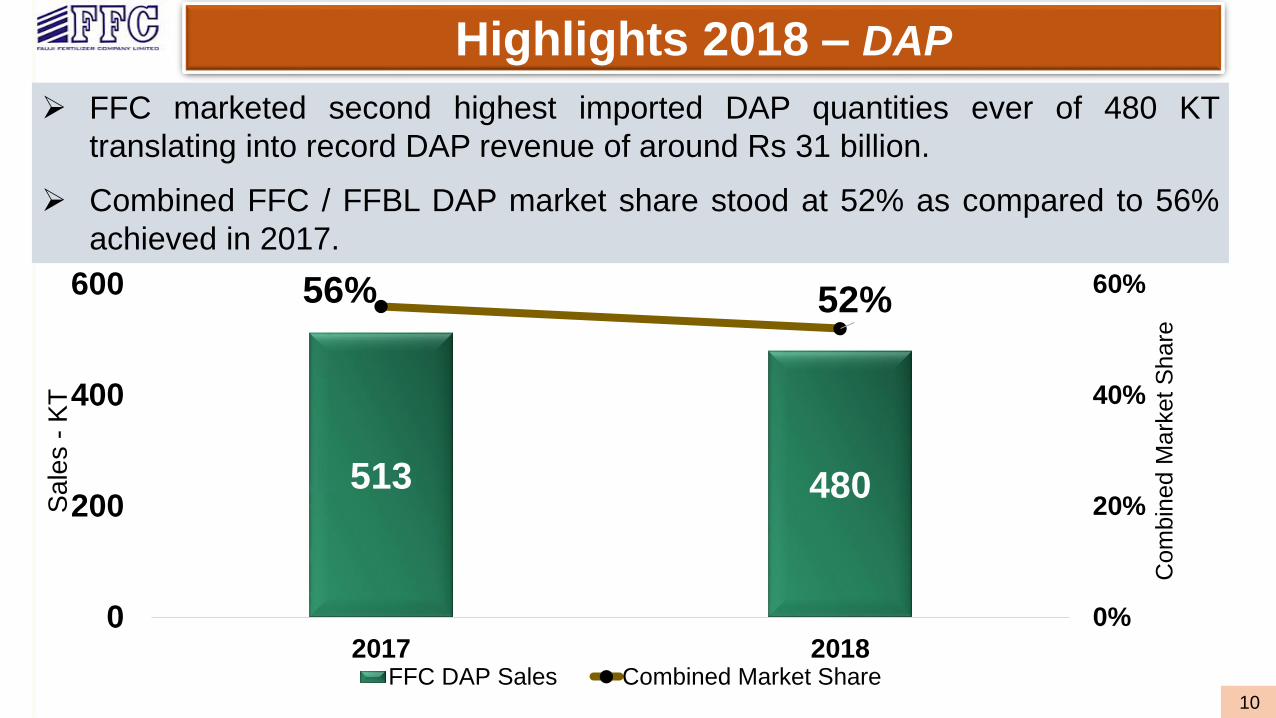

FFC marketed second highest imported DAP quantities ever of 480 KT

translating into record DAP revenue of around Rs 31 billion.

Combined FFC / FFBL DAP market share stood at 52% as compared to 56%

achieved in 2017.

35%

21%

Highlights 2018 – DAP

513 480

56% 52%

0%

20%

40%

60%

0

200

400

600

2017 2018

Com

bin

ed M

ark

et

Share

Sa

les -

KT

FFC DAP Sales Combined Market Share

11

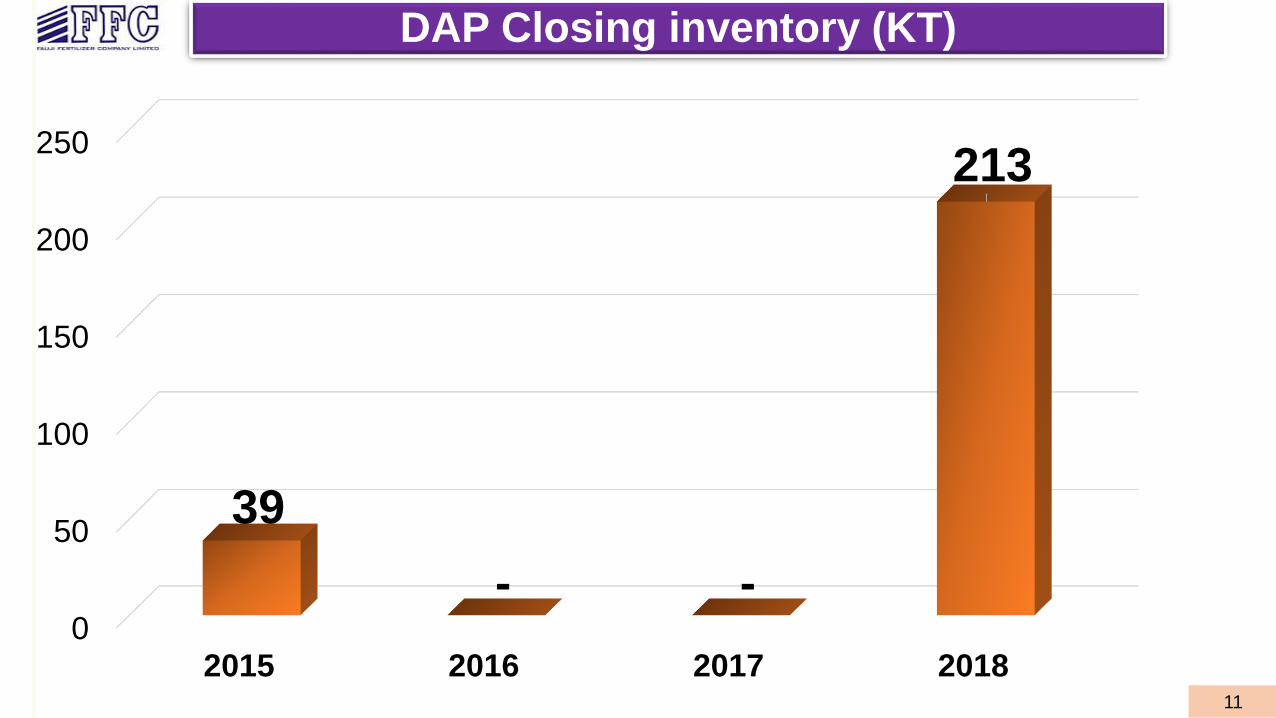

DAP Closing inventory (KT)

0

50

100

150

200

250

2015 2016 2017 2018

39

- -

213

12

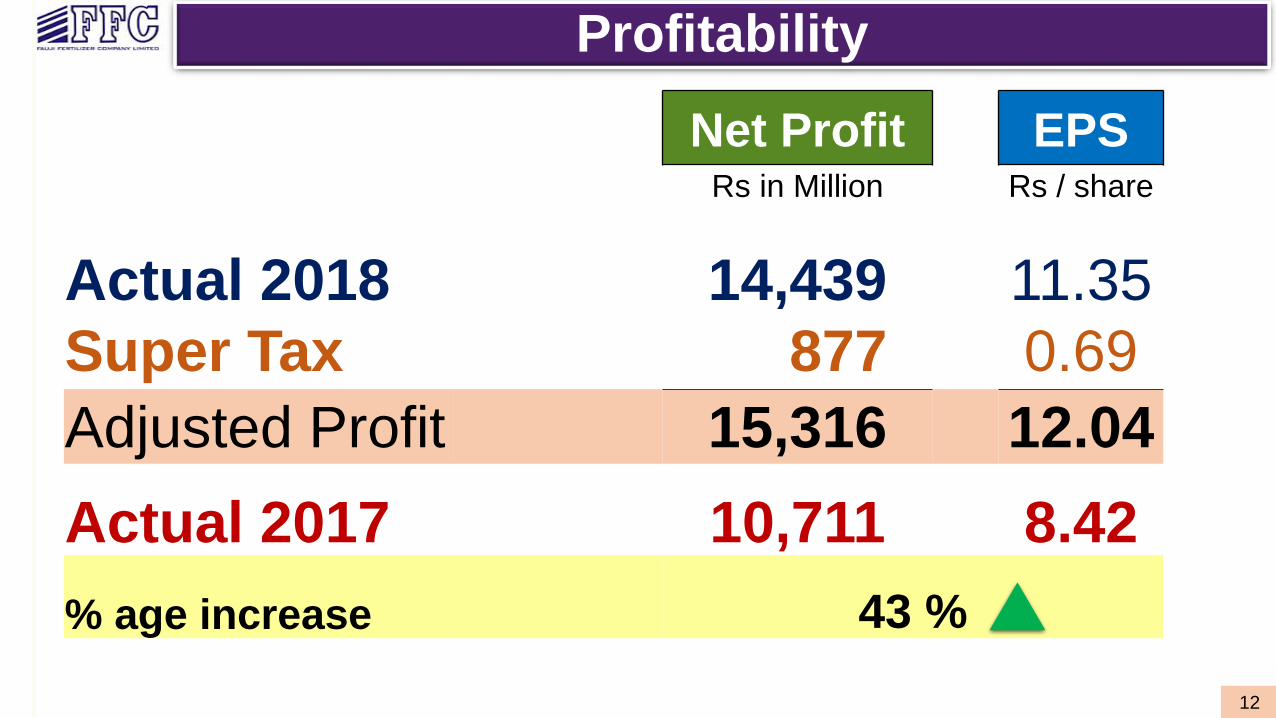

Profitability

Net Profit EPSRs in Million Rs / share

Actual 2018 14,439 11.35

Super Tax 877 0.69

Adjusted Profit 15,316 12.04

Actual 2017 10,711 8.42

% age increase 43 %

13

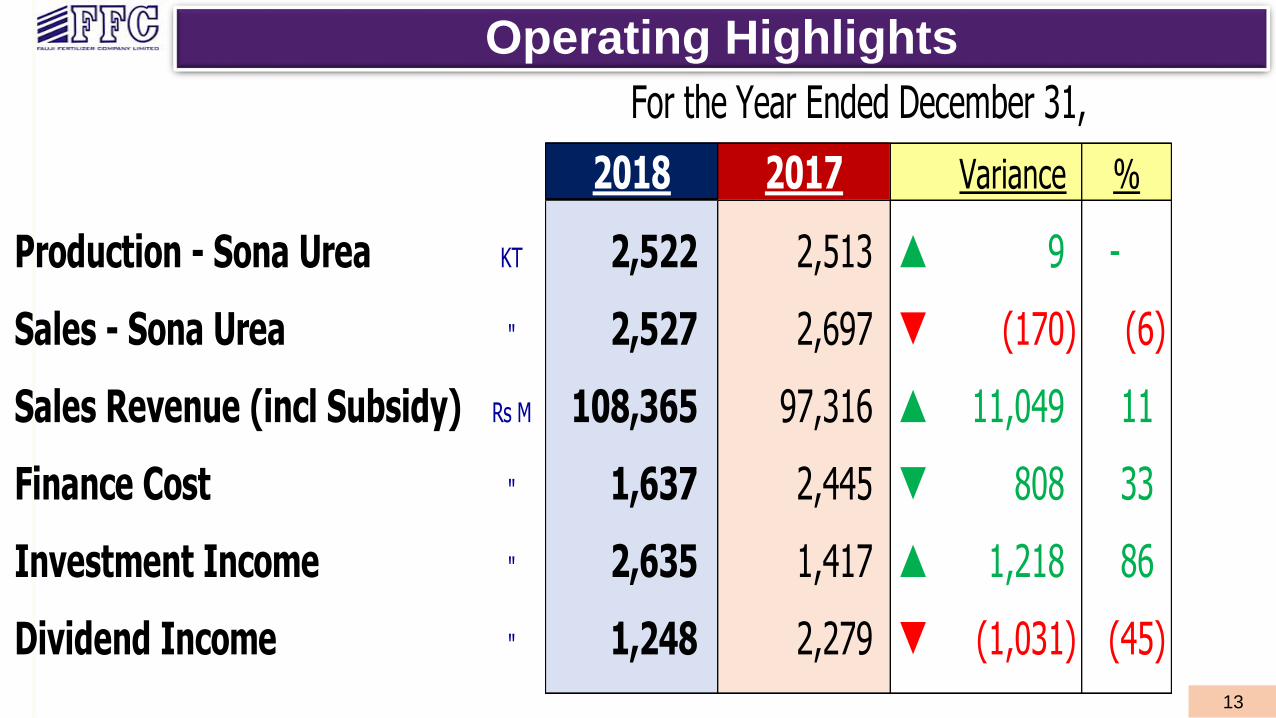

Operating Highlights

2018 2017 Variance %

Production - Sona Urea KT 2,522 2,513 p 9 -

Sales - Sona Urea " 2,527 2,697 q (170) (6)

Sales Revenue (incl Subsidy) Rs M 108,365 97,316 p 11,049 11

Finance Cost " 1,637 2,445 q 808 33

Investment Income " 2,635 1,417 p 1,218 86

Dividend Income " 1,248 2,279 q (1,031) (45)

For the Year Ended December 31,

Corporate Awards

15

Awards & Achievements

SAFA Award 2017

Ranked amongst the best under “Corporate Governance Disclosures” category

Best Corporate Report Award 2017 - ICAP / ICMAP

First position in “Chemical & Pharmaceuticals” sector

Best Sustainability Report Award 2017 - ICAP / ICMAPRanked amongst the best sustainability reports

PSX Award

Stood first on PSX Top 25 Companies list, for the year 2016 which was the

7th consecutive year for the top placement

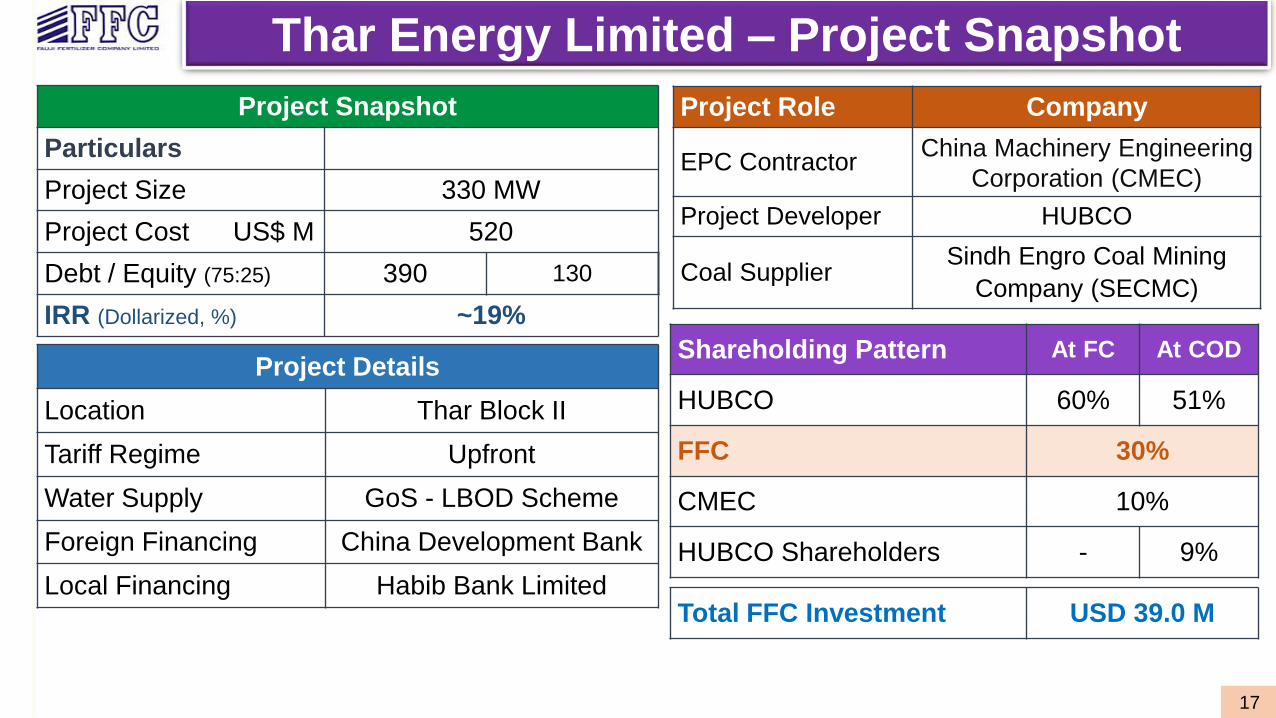

New VentureThar Energy Limited

17

Project Snapshot

Particulars

Project Size 330 MW

Project Cost US$ M 520

Debt / Equity (75:25) 390 130

IRR (Dollarized, %) ~19%

Shareholding Pattern At FC At COD

HUBCO 60% 51%

FFC 30%

CMEC 10%

HUBCO Shareholders - 9%

Total FFC Investment USD 39.0 M

Project Role Company

EPC ContractorChina Machinery Engineering

Corporation (CMEC)

Project Developer HUBCO

Coal SupplierSindh Engro Coal Mining

Company (SECMC)

Project Details

Location Thar Block II

Tariff Regime Upfront

Water Supply GoS - LBOD Scheme

Foreign Financing China Development Bank

Local Financing Habib Bank Limited

Thar Energy Limited – Project Snapshot

18

Thar Energy Limited (TEL)

Financing agreements signed on December 20, 2018.

The Company has invested Rs 1.46 billion in the projecttill December 31, 2018

EPC contractor mobilized on site and project completionactivities are progressing as per plan

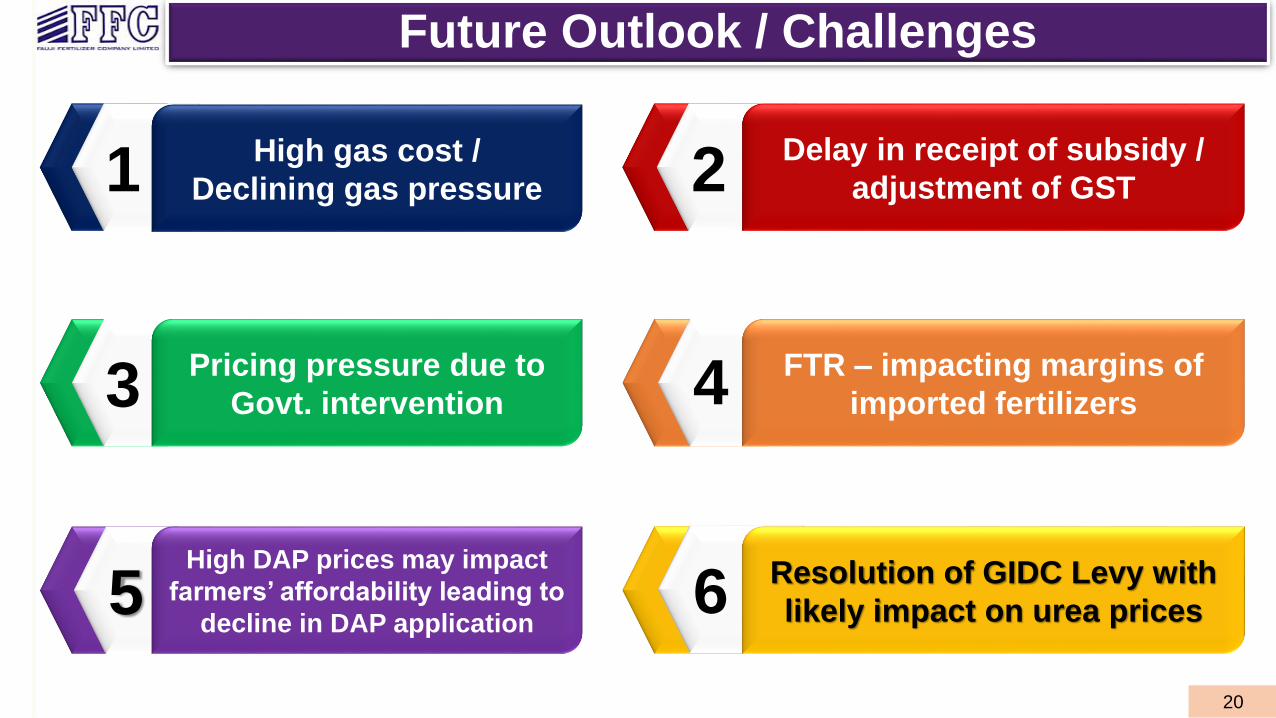

Future Outlook/

Challenges

20

11 High gas cost /

Declining gas pressure

13Pricing pressure due to

Govt. intervention

15High DAP prices may impact

farmers’ affordability leading to

decline in DAP application

12Delay in receipt of subsidy /

adjustment of GST

14 FTR – impacting margins of

imported fertilizers

16 Resolution of GIDC Levy with

likely impact on urea prices

Future Outlook / Challenges

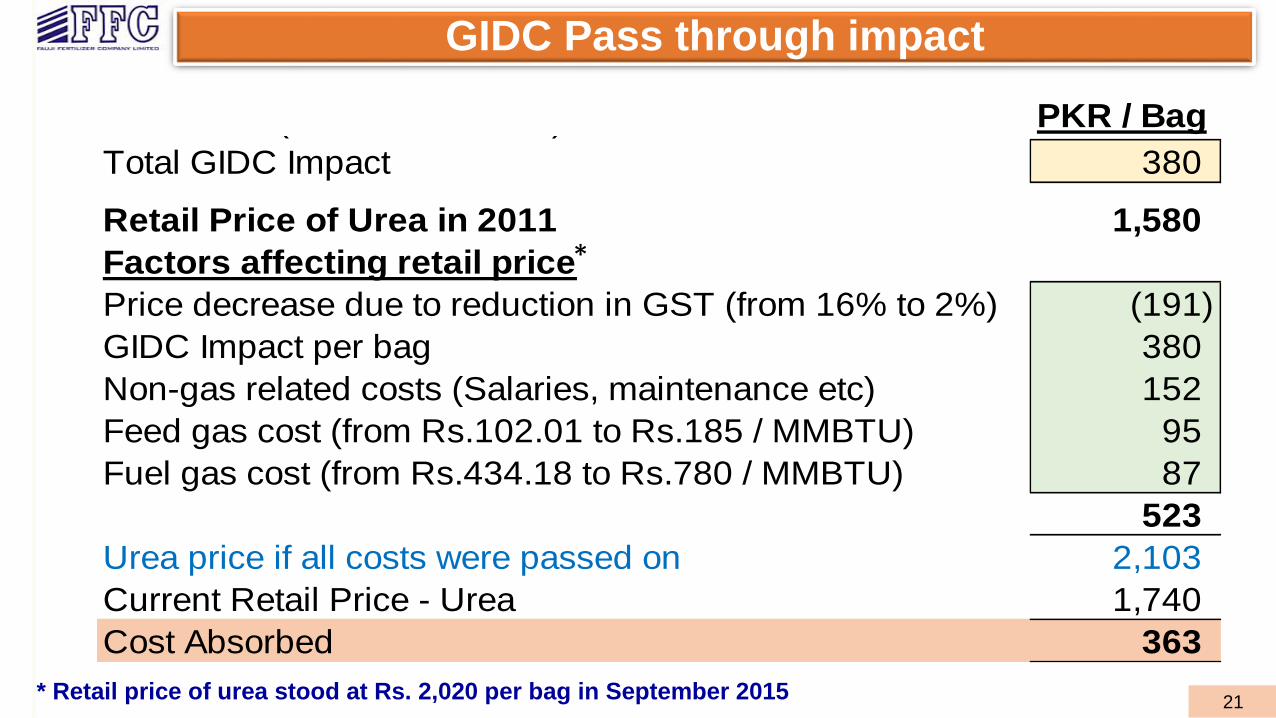

21

PKR / BagFuel GIDC (Rs. 150/MMBTU) 36

Total GIDC Impact 380

Retail Price of Urea in 2011 1,580

Factors affecting retail price

Price decrease due to reduction in GST (from 16% to 2%) (191)

GIDC Impact per bag 380

Non-gas related costs (Salaries, maintenance etc) 152

Feed gas cost (from Rs.102.01 to Rs.185 / MMBTU) 95

Fuel gas cost (from Rs.434.18 to Rs.780 / MMBTU) 87

523

Urea price if all costs were passed on 2,103

Current Retail Price - Urea 1,740

Cost Absorbed 363

GIDC Pass through impact

*

* Retail price of urea stood at Rs. 2,020 per bag in September 2015

Q & A Session

Thank you