Embed Size (px)

Citation preview

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 1/125

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 2/125

Opportunities of a Business Entity depends on nature of intended business

Example: Air line Industry wants to add an aircraft that generate more Cash Flows. (i.e.Opportunity and acquire an asset Plane)

Cargo Company - TrawlersPoints keep in view by Financial Manager & CB

Size of Investment Risk Timing

Evaluating Size, timing of CF and Risk associated with CF is essence of CB

QUESTION # 2:Where to get money from to Finance Investment?

Ans: CAP

IT

AL & IT

S ST

RUCT

URE Two ways to finance an Investment:

Owner¶s Equity Loans or External Sources

Terminology in Capital Raising

IPO¶s IPO¶s stands for Initial Public Offerings Company lunch their shares in market Offer general Public Share allotted on Draw

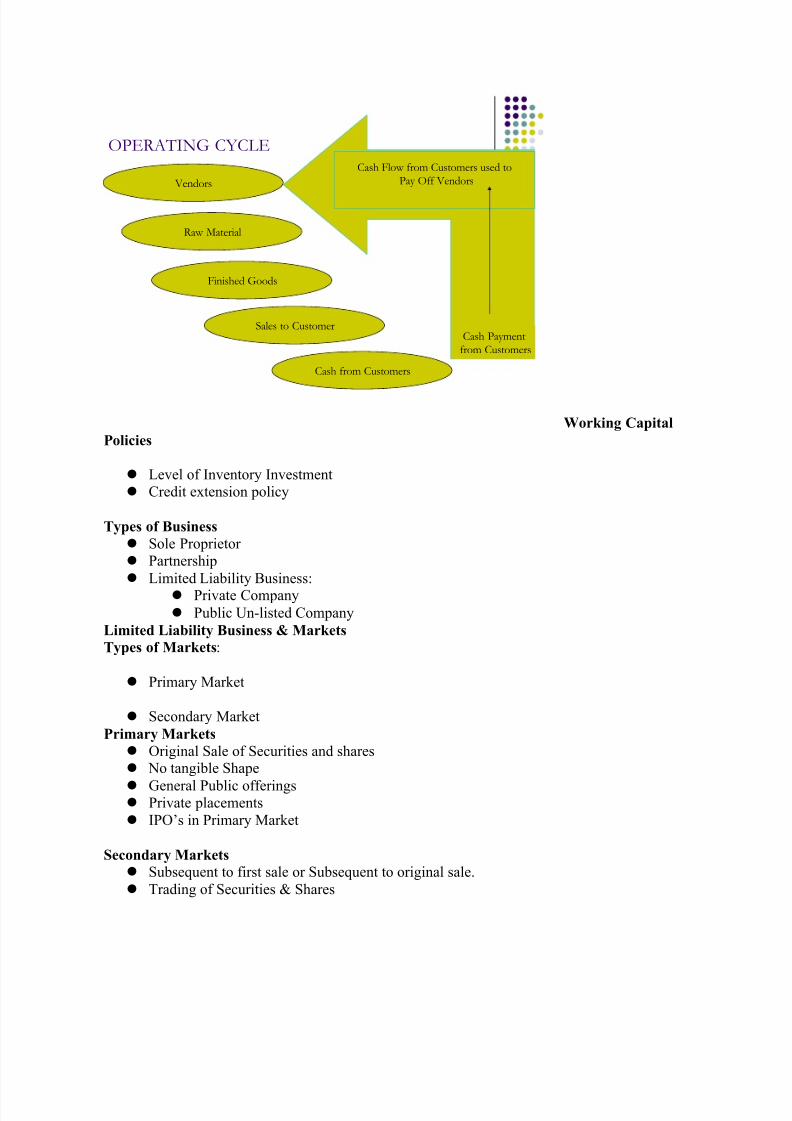

QUESTION # 3 How to manage routine financial activities?

Working Capital Basically Interaction between Current Assets & Current Liabilities Working Capital needs to meet financial expenses Current Assets + Current Liabilities = WC

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 3/125

Vendors

Finished Goods

Raw Material

Cash from Customers

Sales to Customer

OPERATING CYCLE

Cash Flow from Customers used to

Pay Off Vendors

Cash Payment

from Customers

Working CapitalPolicies

Level of Inventory Investment Credit extension policy

Types of Business Sole Proprietor Partnership Limited Liability Business:

Private Company Public Un-listed Company

Limited Liability Business & MarketsTypes of Markets:

Primary Market

Secondary MarketPrimary Markets

Original Sale of Securities and shares

No tangible Shape General Public offerings Private placements IPO¶s in Primary Market

Secondary Markets Subsequent to first sale or Subsequent to original sale. Trading of Securities & Shares

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 4/125

Tangible Markets Example stock Exchange

FINANCIAL STATEMENTS &COR PORATE FINANCE

THREE BASIC STATEMENTS

BALANCE SHEET INCOME STATEMENT CASH FLOW STATEMENT

BALANCE SHEET

Is a Statement of resources controlled by the business entity and obligations on a specificdate.

Contents of Balance Sheet

Assets = Fixed (tangible & intangible)& current assets

Liabilities = Long Term Liability + Current Or Short Term Liability Equity = shareholders¶ contribution + earnings

Fixed Assets: Earning assets Fixed Assets e.g. Plant, Machinery, Vehicles etc

Current Assets: Inventory, Prepayments, Cash & Bank Balance, Short Term Investment etc

Balance Sheet Format

Format of B/S in Pakistan is Governed by International Financial Reporting Standard or International Accounting Standard

B/S construction is Non-liquid or Illiquid Asset is at top

Two Conventions for B/S Construction

1st as in Pakistan IAS or IFRS 2nd Convention GAAP (General Accepted Accounting Principle) applicable in United

States GAAP ± In B/S top item is highly liquid asset i.e. cash or near money

Current Liabilities ingredients

Creditor, Accrued Liabilities, Short Term Finances Current Assets combine Current liabilities equal Working Capital

Liquidity

Conversion into cash without losing its value. Timing Loss of value

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 5/125

Example: Bonds

Equity & Long Term Liabilities Equity

Paid up Capital

Reserves Profit & Loss Long Term Liabilities

Loans OR Financial Leverage

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 6/125

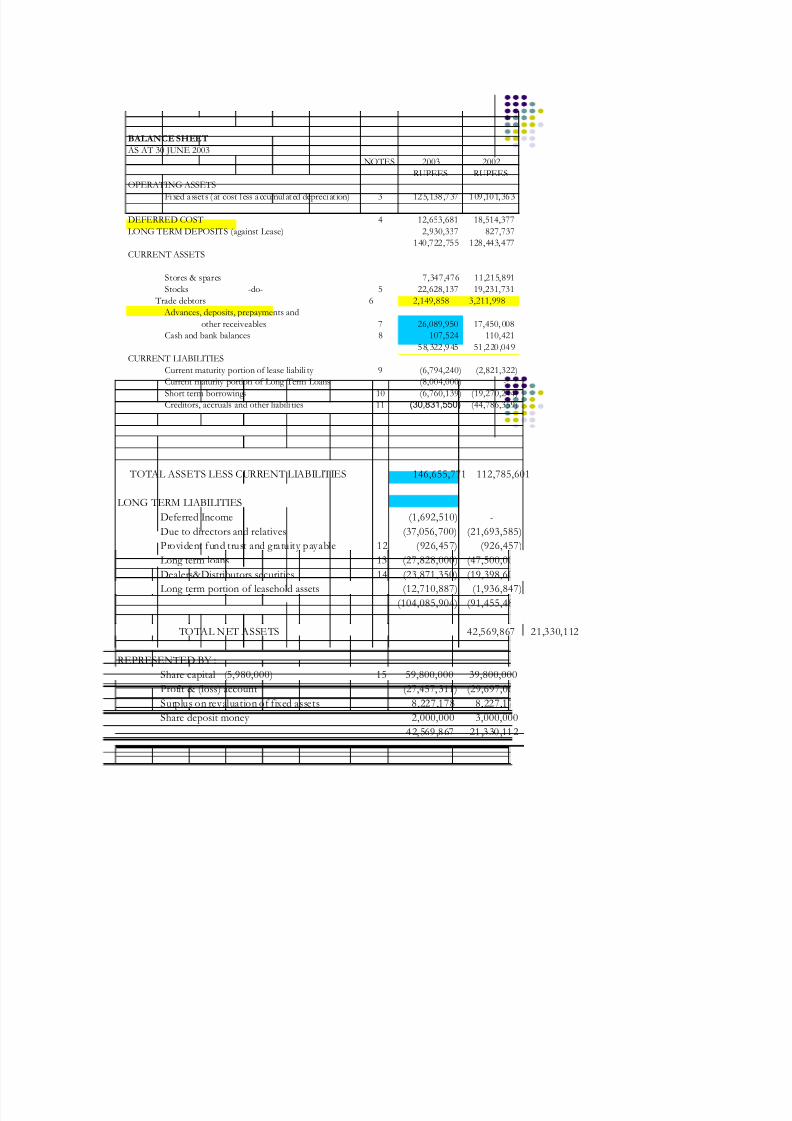

BALANCE SHEET

AS AT 30 JUNE 2003

NOTES 2003 2002

RUPEES RUPEES

OPERATING ASSETS

Fixed asset s ( at cost l ess accumulated depreci at ion) 3 125,138 ,737 109 ,101,363

DEFERRED COST 4 12,653,681 18,514,377

LONG TERM DEPOSITS (against Lease) 2,930,337 827,737

140,722,755 128,443,477

CURRENT ASSETS

Stores & spares 7,347,476 11,215,891

Stocks -do- 5 22,628,137 19,231,731

Trade debtors 6 2,149,858 3,211,998

Advances, deposits, prepayments and

other receiveables 7 26,089,950 17,450, 008

Cash and bank balances 8 107,524 110,421

58,322 ,945 51 ,220 ,049

CURRENT LIABILITIES

Current maturity portion of lease liabili ty 9 (6,794,240) (2,821,322)

Current maturity portion of Long Term Loans (8,004,000) - Short term borrowings 10 (6,760,139) (19,270,244)

Creditors, accruals and other liabili ties 11 (30,831,550) (44,786,359)

TOTAL ASSETS LESS CURRENT LIABILITIES 146,655,771 112,785,601

LONG TERM LIABILITIES

Deferred Income (1,692,510) -

Due to directors and relatives (37,056,700) (21,693,585)

Provident fund trust and gratuity payable 12 (926,457) (926,457)

Long term loans 13 (27,828,000) (47,500,000)

Dealers&Distributors securities 14 (23,871,350) (19,398,600) Long term portion of leasehold assets (12,710,887) (1,936,847)

(104,085,904) (91,455,489)

TOTAL NET ASSETS 42,569,867 21,330,112

REPRESENTED BY :

Share capital (5,980,000) 15 59,800,000 39,800,000

Profit & (loss) account (27,457,311) (29,697,066)

Surplus on revaluation of fixed assets 8,227,178 8,227,178

Share deposit money 2,000,000 3,000,000

42,569 ,867 21 ,330 ,112

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 7/125

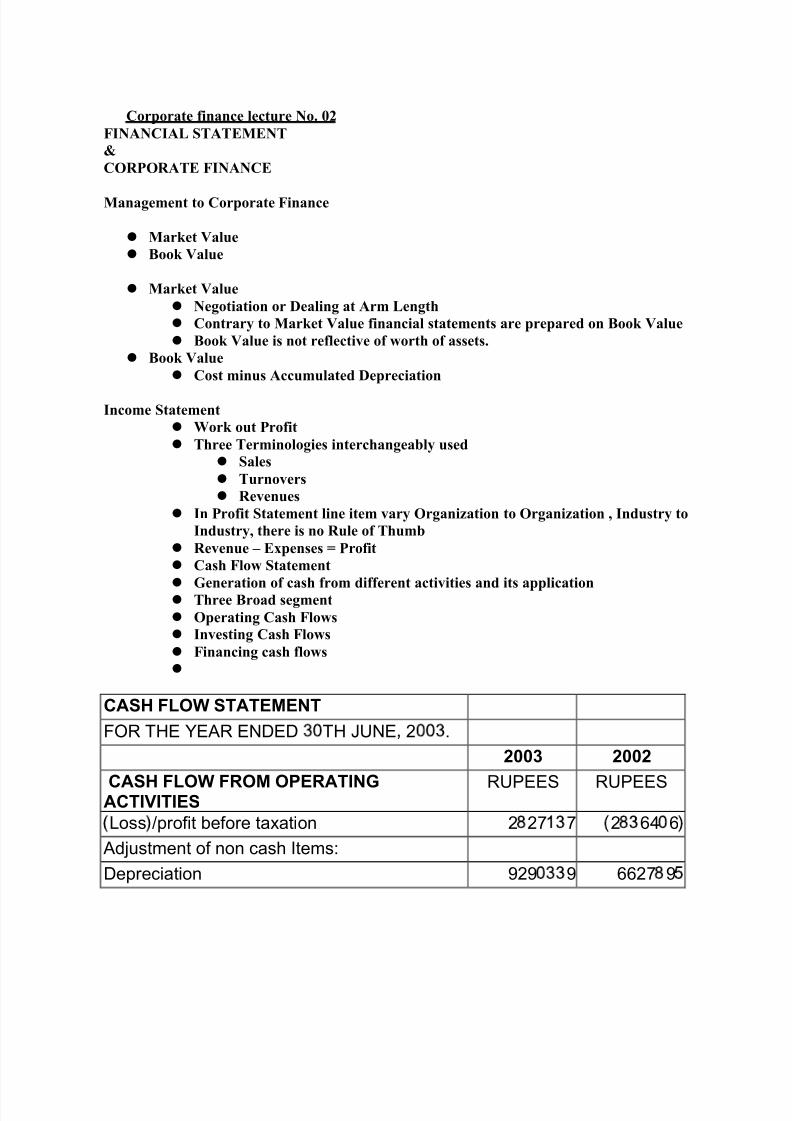

Corporate finance lecture No. 02

FINANCIAL STATEMENT &COR PORATE FINANCE

Management to Corporate Finance

Market Value Book Value

Market Value Negotiation or Dealing at Arm Length Contrary to Market Value financial statements are prepared on Book Value Book Value is not reflective of worth of assets.

Book Value

Cost minus Accumulated DepreciationIncome Statement

Work out Profit Three Terminologies interchangeably used

Sales Turnovers Revenues

In Profit Statement line item vary Organization to Organization , Industry toIndustry, there is no Rule of Thumb

Revenue ± Expenses = Profit Cash Flow Statement Generation of cash from different activities and its application Three Broad segment Operating Cash Flows Investing Cash Flows Financing cash flows

CASH FLOW STATEMENT

FOR THE YEAR ENDED TH JUNE 2 .

2003 2002 CASH FLOW FROM OPERATINGACTIVITIES

RUPEES RUPEES

Loss /profit before taxation 2 27 7 2 64 6

Adjustment of non cash Items:

Depreciation 929 9 6627 9

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 8/125

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 9/125

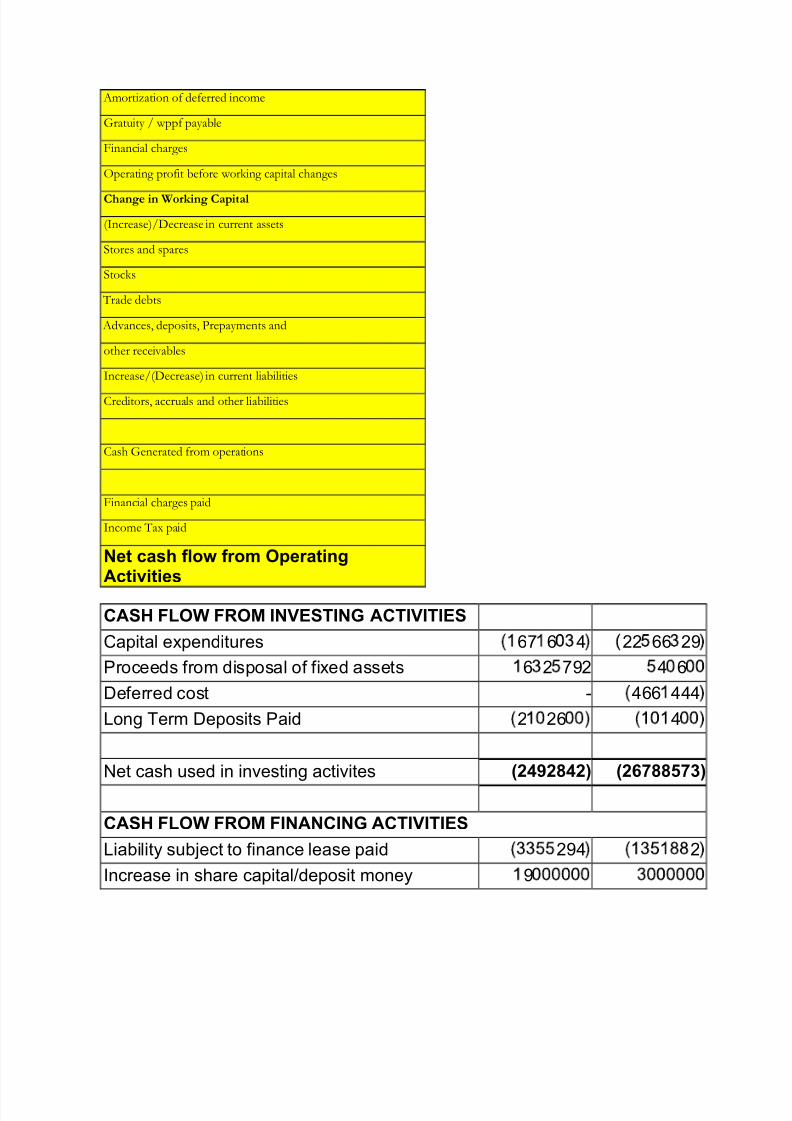

Amortization of deferred income

Gratuity / wppf payable

Financial charges

Operating prof it before work ing capital changes

Change in Working Capital

(Increase)/Decrease in current assets

Stores and spares

Stocks

Trade debts

Advances, deposits, Prepayments and

other recei vables

Increase/(Decrease) in current liabilitiesCreditors, accruals and other liabilities

Cash Generated from operations

Financial charges paid

Income Tax paid

Net cash flow from Operating

Activities

CASH FLOW FROM INVESTING ACTIVITIES

Capital expenditures 67 6 4 22 66 29

Proceeds from disposal of fixed assets 6 2 792 4 6

Deferred cost - 466 444

Long Term Deposits Paid 2 26 4

Net cash used in investing activites (2492842) (26788573)

CASH FLOW FROM FINANCING ACTIVITIES

Liability subject to finance lease paid 294 2

Increase in share capital/deposit money 9

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 10/125

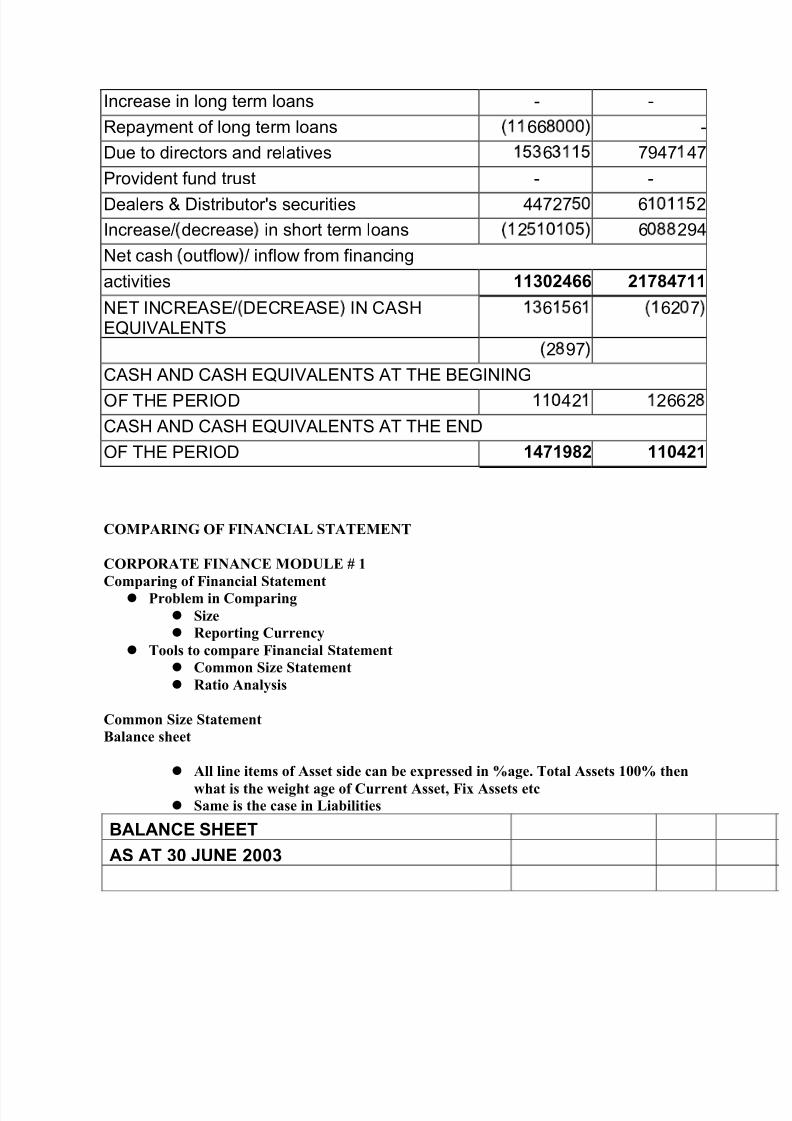

Increase in long term loans - -

Repayment of long term loans 66 -

Due to directors and relatives 6 7947 47

Provident fund trust - -

Dealers & Distributor's securities 44727 6 2

Increase/ decrease in short term loans 2 6 294

Net cash outflow / inflow from financing

activities 11302466 21784711

NET INCREASE/ DECREASE IN CASHEQUIVALENTS

6 6 62 7

2 97

CASH AND CASH EQUIVALENTS AT THE BEGININGOF THE PERIOD 42 2662

CASH AND CASH EQUIVALENTS AT THE END

OF THE PERIOD 1471982 110421

COMPARING OF FINANCIAL STATEMENT

COR PORATE FINANCE MODULE # 1Comparing of Financial Statement

Problem in Comparing Size Reporting Currency

Tools to compare Financial Statement Common Size Statement Ratio Analysis

Common Size StatementBalance sheet

All line items of Asset side can be expressed in %age. Total Assets 100% thenwhat is the weight age of Current Asset, Fix Assets etc

Same is the case in Liabilities

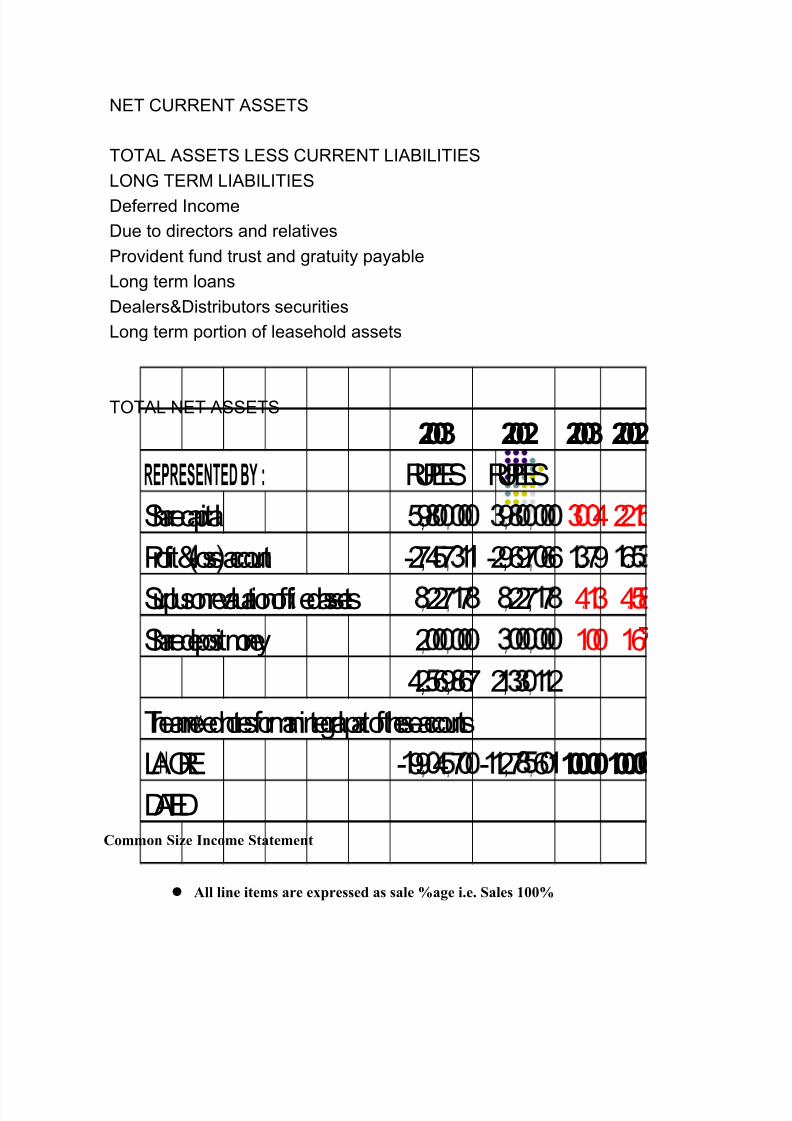

BALANCE SHEET

AS AT 30 JUNE 2003

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 11/125

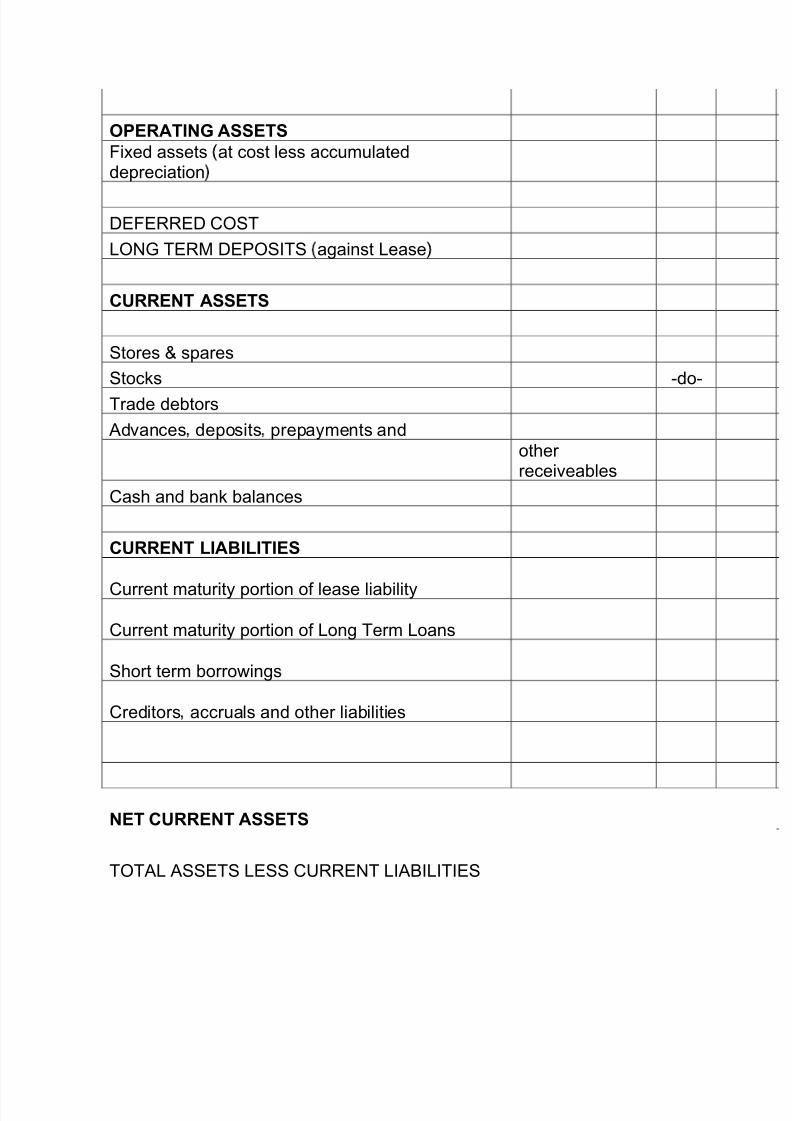

OPERATING ASSETS

Fixed assets at cost less accumulateddepreciation

DEFERRED COST

LONG TERM DEPOSITS against Lease

CURRENT ASSETS

Stores & spares

Stocks -do-Trade debtors

Advances deposits prepayments and

other receiveables

Cash and bank balances

CURRENT LIABILITIES

Current maturity portion of lease liability

Current maturity portion of Long Term Loans

Short term borrowings

Creditors accruals and other liabilities

NET CURRENT ASSETS

TOTAL ASSETS LESS CURRENT LIABILITIES

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 12/125

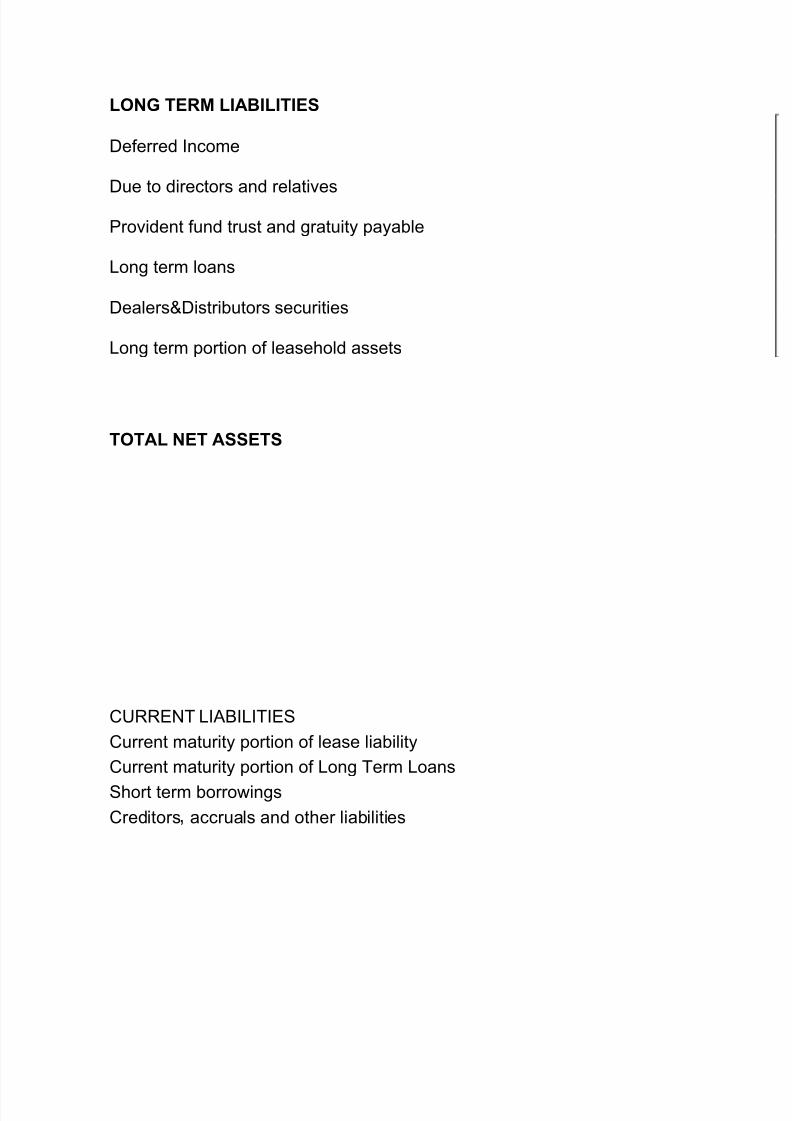

LONG TERM LIABILITIES

Deferred Income

Due to directors and relatives

Provident fund trust and gratuity payable

Long term loans

Dealers&Distributors securities

Long term portion of leasehold assets

TOTAL NET ASSETS

CURRENT LIABILITIES

Current maturity portion of lease liability

Current maturity portion of Long Term LoansShort term borrowings

Creditors accruals and other liabilities

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 13/125

NET CURRENT ASSETS

TOTAL ASSETS LESS CURRENT LIABILITIES

LONG TERM LIABILITIES

Deferred Income

Due to directors and relatives

Provident fund trust and gratuity payable

Long term loans

Dealers&Distributors securities

Long term portion of leasehold assets

TOTAL NET ASSETS

2003 2002 2003 2002

REPRESENTED BY : RUPEES RUPEES

Sharecapital 9 9 422

Profit &loss account -2747 -2969766 79 6Surplusonrevaluationof fiedassets 2277 2277 4 4

Sharedeposit money 2 6

426967 2 2

Theanneednotesformanintegral part of theseaccounts

LAORE -9947 - 27 6 100.00100.0DATED

Common Size Income Statement

All line items are expressed as sale %age i.e. Sales 100%

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 14/125

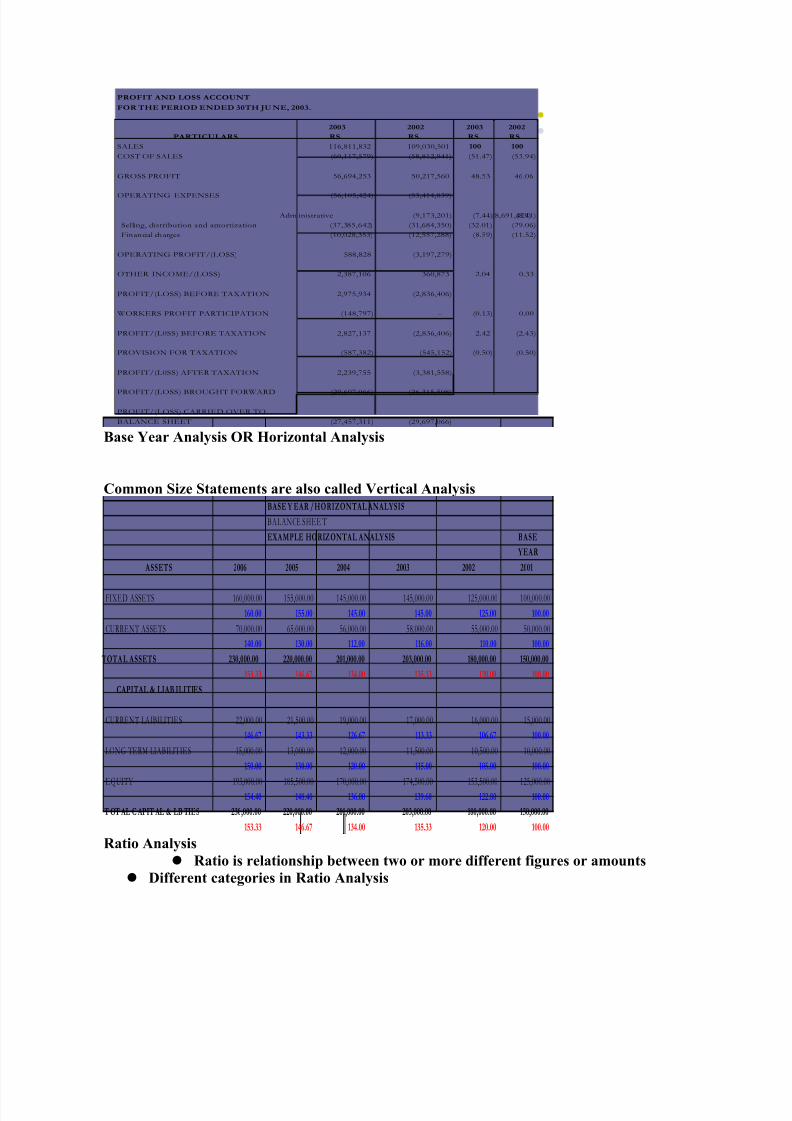

2003 2002 2003 2002

RS. RS. RS. RS.

116,811,832 109,030,501 100 100

(60,117,579) (58,812,941) (51.47) (53.94)

56,694,253 50,217,560 48.53 46.06

(56,105,424) (53,414,839)

Adm inistrative (8,691,429)(9,173,201) (7.44) (8.41)

Selling, distribution and amortization (37,385,642) (31,684,350) (32.01) (29.06)

Financial charges (10,028,353) (12,557,288) (8.59) (11.52)

588,828 (3,197,279)

2,387,106 360,873 2.04 0.33

2,975,934 (2,836,406)

(148,797) - (0.13) 0.00

2,827,137 (2,836,406) 2.42 (2.43)

(587,382) (545,152) (0.50) (0.50)

2,239,755 (3,381,558)

(29,697,066) (26,315,508)

(27,457,311) (29,697,066)

PROFIT AND LOSS ACCOUNT

FOR THE PERIOD ENDED 30TH JU NE, 2003.

SALES

COST OF SALES

PARTICULARS

GROSS PROFIT

OPERATING EXPENSES

OPERATING PROFIT/(LOSS)

OTHER INCOME/(LOSS)

PROFIT/(LOSS) BEFORE TAXATION

PROFIT/(LOSS) BROUGHT FORWARD

PROFIT/(LOSS) CARRIED OVER TO

BALANCE SHEET

WORKERS PROFIT PARTICIPATION

PROFIT/(L0SS) BEFORE TAXATION

PROVISION FOR TAXATION

PROFIT/(L0SS) AFTER TAXATION

Base Year Analysis OR Horizontal Analysis

Common Size Statements are also called Vertical AnalysisBASE Y EAR /HORIZONTAL ANALYSIS

BALANCE SHEE T

EXAMPLE HORIZONTAL ANALYSIS BASE

YEAR

ASSETS 2006 2005 2004 2003 2002 2001

FIXED ASSETS 160,000.00 155,000.00 145,000.00 145,000.00 125,000.00 100,000.00

160.00 155.00 145.00 145.00 125.00 100.00

CURRENT ASSETS 70,000.00 65,000.00 56,000.00 58,000.00 55,000.00 50,000.00

140.00 130.00 112.00 116.00 110.00 100.00

TOTAL ASSETS 230,000.00 220,000.00 201,000.00 203,000.00 180,000.00 150,000.00

153.33 146.67 134.00 135.33 120.00 100.00

CAPITAL & LIAB ILITIES

CURRENT LAIBILITIES 22,000.00 21,500.00 19,000.00 17,000.00 16,000.00 15,000.00

146.67 143.33 126.67 113.33 106.67 100.00

LONG TERM LIABILITIES 15,000.00 13,000.00 12,000.00 11,500.00 10,500.00 10,000.00

150.00 130.00 120.00 115.00 105.00 100.00

EQUITY 193,000.00 185,500.00 170,000.00 174,500.00 153,500.00 125,000.00

154.40 148.40 136.00 139.60 122.80 100.00

T OT AL C APIT AL & LB TIES 230,000.00 220,000.00 201,000.00 203,000.00 180,000.00 150,000.00

153.33 146.67 134.00 135.33 120.00 100.00

Ratio Analysis Ratio is relationship between two or more different figures or amounts

Different categories in Ratio Analysis

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 15/125

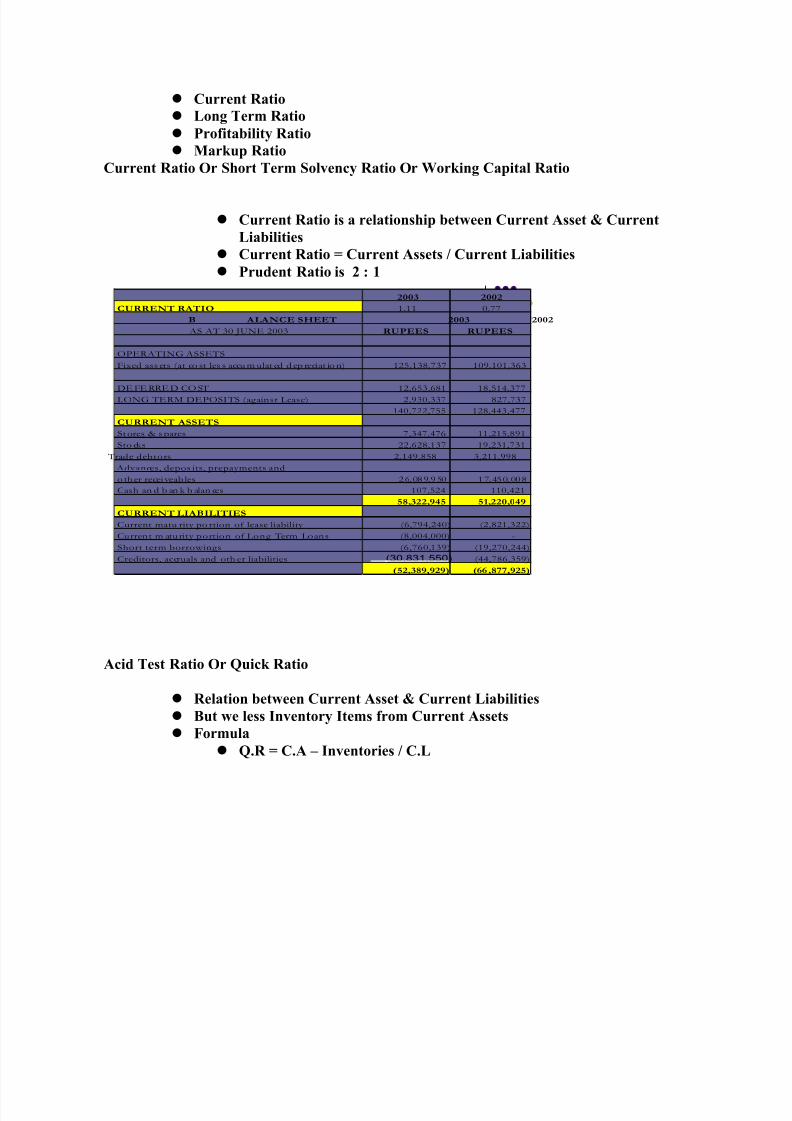

Current Ratio Long Term Ratio Profitability Ratio Markup Ratio

Current Ratio Or Short Term Solvency Ratio Or Working Capital Ratio

Current Ratio is a relationship between Current Asset & CurrentLiabilities

Current Ratio = Current Assets / Current Liabilities Prudent Ratio is 2 : 1

2003 2002

CURRENT RATIO 1.11 0.77

B ALANCE SHEET 2003 2002

AS AT 30 JUNE 2003 RUPEES RUPEES

OPERATING ASSETS

Fixed ass ets (at co st les s accu m ulat ed d ep reciat io n) 125,138,737 109,101,363

DEFERRED COST 12,653,681 18,514,377

LONG TERM DEPOSITS (against Lease) 2,930,337 827,737

140,722,755 128,443,477

CURRENT ASSETS

Stores & s pares 7,347,476 11,215,891

Sto cks 22,628,137 19,231,731

Trade debtors 2,149,858 3,211,998

Advances, depos its, prepayments and

other receiveab les 26,089,950 17,450,008

Cash an d b an k b alan ces 107,524 110,421

58,322,945 51,220,049

CURRENT LIA BILITIES

Current matu rity po rtion of lease liability (6,794,240) (2,821,322)

Current m aturity portion of Long Term Loans (8,004,000) -

Short term borrowings (6,760,139) (19,270,244)

Creditors, accruals and oth er liabilities (30,831,550) (44,786,359)

(52,389,929) (66 ,877,925)

Acid Test Ratio Or Quick Ratio

Relation between Current Asset & Current Liabilities But we less Inventory Items from Current Assets Formula

Q.R = C.A ± Inventories / C.L

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 16/125

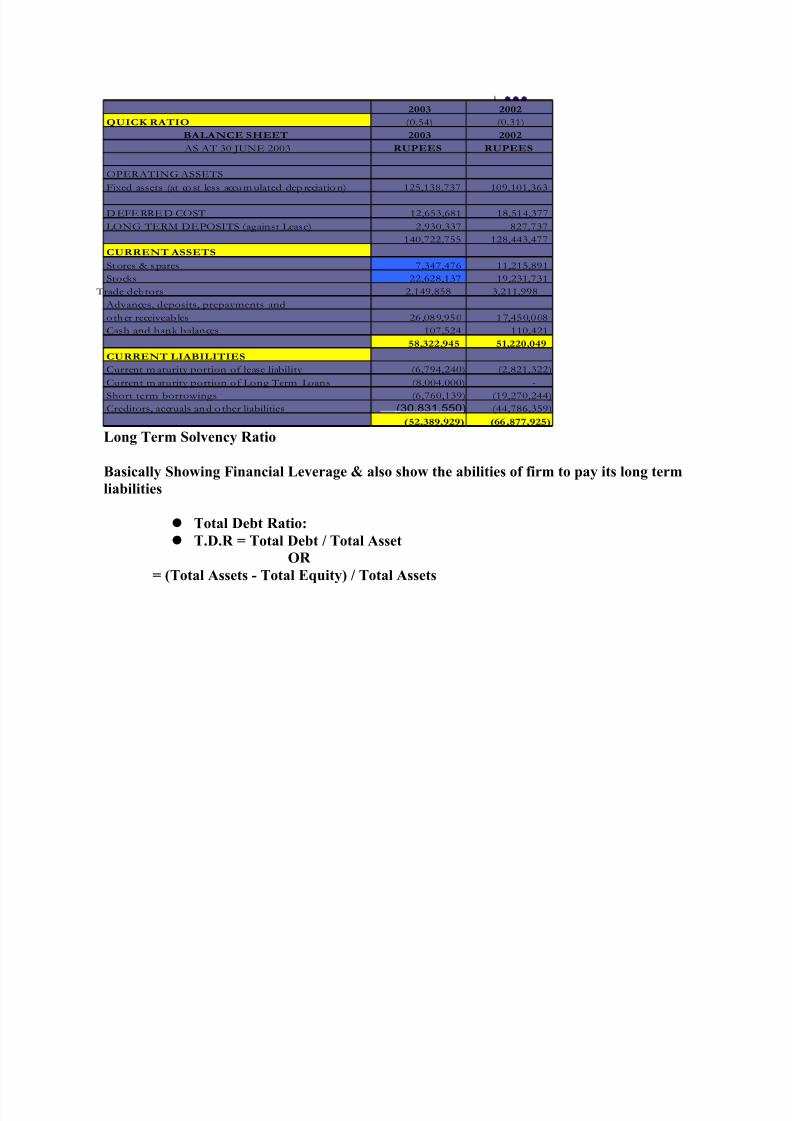

2003 2002

QUICK RATIO (0.54) (0.31)

BALANCE SHEET 2003 2002

AS AT 30 JUNE 2003 RUPEES RUPEES

OPERATING ASSETS

Fixed assets (at co st less accu m ulated dep reciatio n) 125,138,737 109,101,363

D EFE RRE D COST 12,653,681 18,514,377

LONG TERM DEPOSITS (against Lease) 2,930,337 827,737

140,722,755 128,443,477

CURRENT ASSETS

Stores & spares 7,347,476 11,215,891

Stocks 22,628,137 19,231,731

Trade debtors 2,149,858 3,211,998

Advances, deposits, prepayments and

other receiveables 26,089,950 17,450,008

Cash and bank balances 107,524 110,421

58,322,945 51,220,049

CURRENT LIABILITIES

Current m aturity portion of lease liability (6,794,240) (2,821,322)

Current m aturity portion of Long Term Loans (8,004,000) - Short term borrowings (6,760,139) (19,270,244)

Creditors, accruals and o ther liabilities (30,831,550) (44,786,359)

(52,389,929) (66 ,877,925)

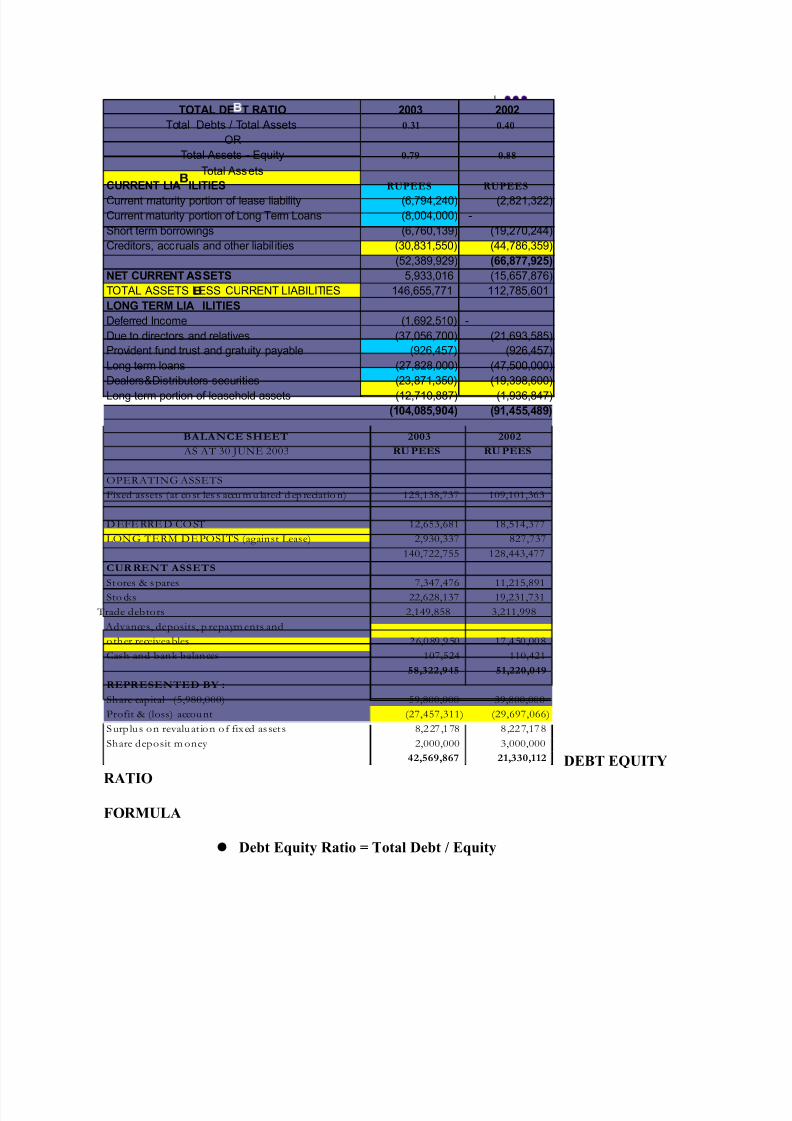

Long Term Solvency Ratio

Basically Showing Financial Leverage & also show the abilities of firm to pay its long termliabilities

Total Debt Ratio: T.D.R = Total Debt / Total Asset

OR

= (Total Assets - Total Equity) / Total Assets

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 17/125

TOTAL DE ¢ T RATIO 2003 2002

Total Debts / Total Assets 0.31 0.40

OR

Total Assets - Equity 0.79 0.88

Total Assets

CURRENT LIA

£

ILITIESRUPEES RUPEES

Current maturity portion of lease liability (6,794,240) (2,821,322)

Current maturity portion of Long Term Loans (8,004,000) -

Short term borrowings (6,760,139) (19,270,244)

Creditors, accruals and other liabil ities (30,831,550) (44,786,359)

(52,389,929) (66,877,925)

NET CURRENT ASSETS 5,933,016 (15,657,876)

TOTAL ASSETS LESS CURRENT LIABILITIES 146,655,771 112,785,601

LONG TERM LIA ¤ ILITIES

Deferred Income (1,692,510) -

Due to directors and relatives (37,056,700) (21,693,585)

Provident fund trust and gratuity payable (926,457) (926,457)

Long term loans (27,828,000) (47,500,000)

Dealers&Distributors securities (23,871,350) (19,398,600) Long term portion of leasehold assets (12,710,887) (1,936,847)

(104,085,904) (91,455,489)

BALANCE SHEET 2003 2002

AS AT 30 JUNE 2003 RUPEES RUPEES

OPERATING ASSETS

Fixed assets (at co st les s accu m u lated d ep reciatio n) 125,138,737 109,101,363

D EFE RRE D CO ST 12,653,681 18,514,377

LONG TERM DEPOSITS (against Lease) 2,930,337 827,737

140,722,755 128,443,477

CURR ENT ASSETS

Stores & s pares 7,347,476 11,215,891

Sto cks 22,628,137 19,231,731

Trade debtors 2,149,858 3,211,998

Advances, deposits, p repaym ents and

other receiveables 26,089 ,950 17 ,450 ,008

Cash and bank balances 107,524 110,421

58,322,945 51,220,049

R EPR ESENTED BY :

Share capital (5,980,000) 59,800,000 39,800,000

Profit & (loss) account (27,457,311) (29,697,066)

Surplus on revaluat ion of fixed as set s 8,227 ,178 8 ,227,178

Share deposit m oney 2,000,000 3,000,000

42,569,867 21,330,112

DEBT EQUITYRATIO

FORMULA

Debt Equity Ratio = Total Debt / Equity

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 18/125

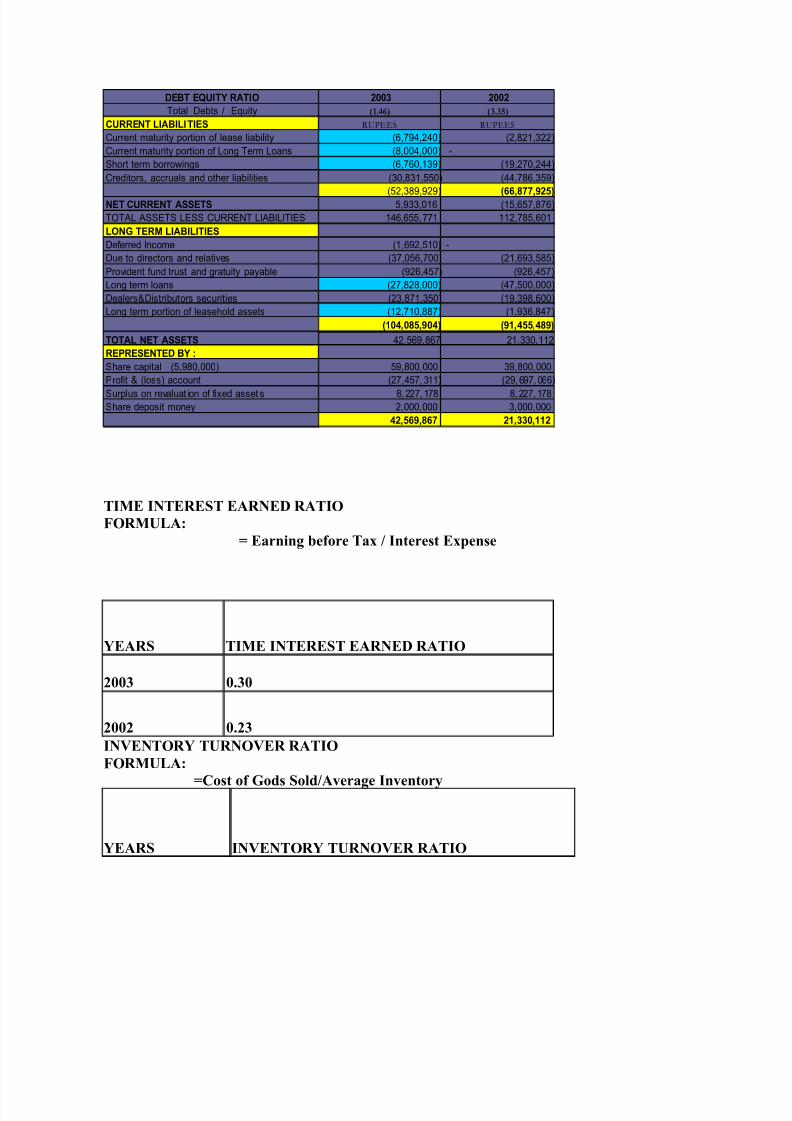

DEBT EQUITY RATIO 2003 2002

Total Debts / Equity (1.46) (3.35)

CURRENT LIABILITIES RUPEES RUPEES

Current maturity portion of lease liability (6,794,240) (2,821,322)

Current maturity portion of Long Term Loans (8,004,000) -

Short term borrowings (6,760,139) (19,270,244)

Creditors, accruals and other liabilities (30,831,550) (44,786,359)

(52,389,929) (66,877,925) NET CURRENT ASSETS 5,933,016 (15,657,876)

TOTAL ASSETS LESS CURRENT LIABILITIES 146,655,771 112,785,601

LONG TERM LIABILITIES

Deferred Income (1,692,510) -

Due to directors and relatives (37,056,700) (21,693,585)

Provident fund trust and gratuity payable (926,457) (926,457)

Long term loans (27,828,000) (47,500,000)

Dealers&Distributors securities (23,871,350) (19,398,600)

Long term portion of leasehold assets (12,710,887) (1,936,847)

(104,085,904) (91,455,489)

TOTAL NET ASSETS 42,569,867 21,330,112

REPRESENTED BY :

Share capital (5,980,000) 59,800,000 39,800,000

Profit & (loss) account (27,457,311) (29,697,066)Surplus on revaluat ion of fixed asset s 8,227,178 8,227,178

Share deposit money 2,000,000 3,000,000

42,569,867 21,330,112

TIME INTEREST EARNED RATIO FORMULA:

= Earning before Tax / Interest Expense

YEARS TIME INTEREST EARNED RATIO

2003 0.30

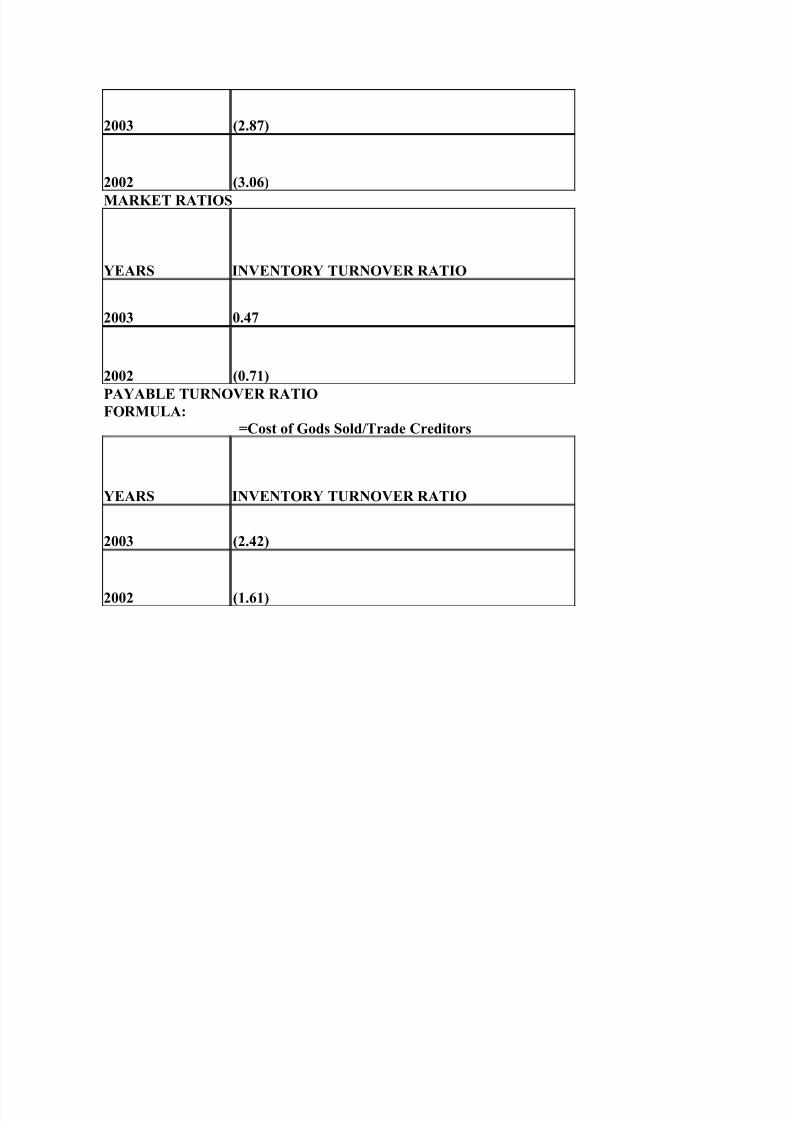

2002 0.23INVENTORY TURNOVER RATIO

FORMULA: =Cost of Gods Sold/Average Inventory

YEARS INVENTORY TURNOVER RATIO

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 19/125

2003 (2.87)

2002 (3.06)MARKET RATIOS

YEARS INVENTORY TURNOVER RATIO

2003 0.47

2002 (0.71)PAYABLE TURNOVER RATIO FORMULA:

=Cost of Gods Sold/Trade Creditors

YEARS INVENTORY TURNOVER RATIO

2003 (2.42)

2002 (1.61)

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 20/125

Corporate finance lecture No. 03

COR PORATE FINANCE - MODULE # 2VALUATION OF FUTURE CASH FLOWSCHEME OF STUDIES

THIS MODULE INCLUDES:

TIME VALUE OF MONEY - BASICS DISCOUNTED CASH FLOW VALUATION BOND VALUATION COMMON STOCK VALUATION

COR PORATE FINANCE - MODULE # 2VALUATION OF FUTURE CASH FLOW TIME VALUE OF MONEY

FUTURE VALUE

PRESENT VALUE

ANNUITIES

PERPETUITIESFUTURE VALUE

Depends on three factors

Size of Investment Time Period Interest Rate

FUTURE VALUE

TIME VALUE DEFINED A dollar or Rupee received today is better than a dollar or rupee to be received

after a year. Why?

Because the dollar or rupee received today will start earning profit right fromtoday

FUTURE VALUE

FV = (Investment, Time, Interest Rate)This can be written asFV = PV x (1 + r)t

(1 + r) t is known as Present Value Investment Factor (PVIF)

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 21/125

r = Rate of Interestt = Time periodExampleYou invest Rs. 1000 today and will get Rs. 1100 at the end of one year, if interest rate is 10% p.a.

= 1000 X (1 + 0.10)= 1100At the end of second year your investment is worth:

1100 x (1 + 0.10) = 1210

Alternatively: 1000 x (1 + 0.10)2 = 1210COMPOUND INTEREST

After One year: 1000 X (1.10) = 1100

After two years: 1100 X (1.10) = 1210

At the end of 2nd year total Investment 1210 that means we earned 210 in terms of Interest.

210 = 100+100+1010 is basically Compound InterestCOMPOUND INTEREST

This 1210 has four parts: 1000 original investment 100 interest ± 1 year 100 interest ± 2 year 10 interest on Year 1 interest

Earning interest on interest is know as compoundingInterest over period is reinvested to earn moreinterest.LONG PERIOD EXAMPLE : (Future Value)

An investment opportunity pays 12% pa and a business entity intends to invest 500,000.What will be the worth of this investment in 7 years time? How much interest will thecompany earn in this period? What portion of total interest represents compound interest?

Solution

Worth after 7 years:

FV = PV x (1 + r)t

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 22/125

FV =500000 x (1.12)7 =1105350

(1.12)7 = 2.21072nd Question: How much Interest will the Company earn in this period?

Total interest earned:1105350 ± 500000 = 605350Compound Interest:500000 x 12% x 7 = 420000=605350 ± 420000 = 185350

2nd Question: How much Interest will the Company earn in this period?

Total interest earned:1105350 ± 500000 = 605350Compound Interest:

500000 x 12% x 7 = 420000=605350 ± 420000 = 185350

PRESENT VALUE

You know that you will get 10000 at the end of 3rdyear from now. The interest rate is 10%. What is thePV of 10000 now?

FV = PV x (1+r)310000= PV x (1.10)3PV = 10000/ (1.10)3= 7513.14

We can find PV the other way too:PV = FV / (1 + r)t

1 / (1.10)3 = known as PVDFPV = FV X PVDFPV = 10000 X 0.7513*

= 7513

* From table A-3Comparison between two options

Option 1= Pay 4000 today and 6000 after 2 years to buy a computer

Option 2= Pay all today a get a credit of 500. (Net price today is 9500)

Interest rate is 10% at present. Which option is better?Option 1:

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 23/125

Finding PV:PV = 4000 + (6000 / (1.10)2PV = 4000 + 4958.68 = 8958.68

It means that 4958.68 invested today @ 10% will yield 6000 at the end of year 2,

enabling you to pay off your liability.Option 2:

PV = 9500Option 1 is better because it cost 8958.68 as compared to 9500 of option 2.

So far we come across four factors of Time Value of Money: PV FV Interest factor or discount factor Time period

Given three we can find the fourth.Finding interest rate

An opportunity requires 1000 investment today that will double at the end of 8th year.What is the implicit interest rate?

PV = FV / (1 +r)81000 = 2000 / (1 +r)8(1 +r)8 = 2000/1000(1 +r)8 = 2

r =9%

Three Ways to Solve: Mathematical Equation Financial Calculator Time Value of Money Tables

Look FV table 8 year row select and move towards right unless under the interest Rate%age you read 2 or nearest to 2.

Implicit Interest Rate = 9%PER PETUITYDefined: Stream of equal cash payments equally spaced that continues for ever.If you wish to help a welfare trust by providing 100,000/- per annum forever and the interestrate is 10%, how much amount must be set-aside today?Formula:

PV of Perpetuity = C/r = 100000/0.10= 1,000,000/-

And if you wish to start payments after 3rd year, then what is the PV of this delayedPerpetuity?

PV of Perpetuity = 1,000,000 / (1.10)3

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 24/125

= 751315ANNUITIES

Series of equal amount and equally spaced payments for limited period of time but not unlimited.

Valuation of Annuities: Using FV/PV tables Using formula

Example:You want to buy an asset for your business that willcost you 4000 per year for next three years.Assume interest rate of 10%. Find out the PV of thisannuity?Using table4000 x 1/(1.10)

4000 x 1/(1.10)24000 x 1/(1.10)3 = 9947.41Using Formula:

PV= Annuity x 1/0.1 ± 1/ 0.10(1.10)3

= 4000 x 2.4869 = 9947.60

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 25/125

Corporate finance lecture No. 04

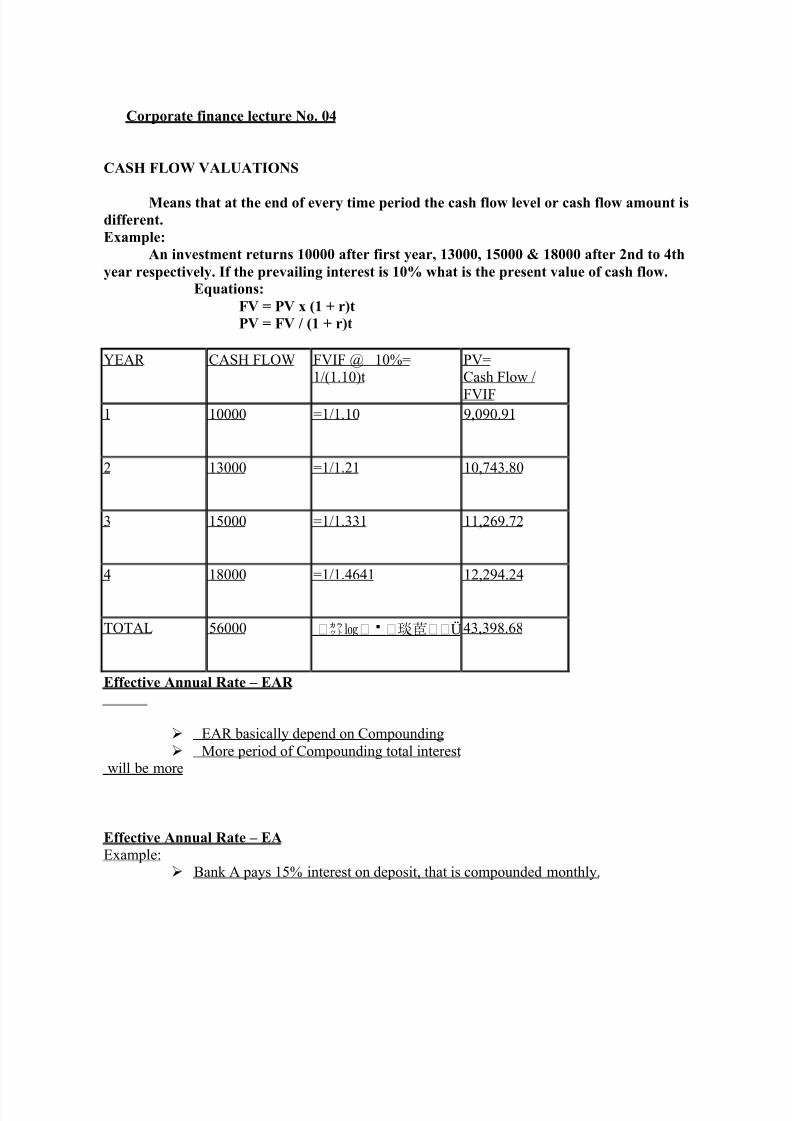

CASH FLOW VALUATIONS

Means that at the end of every time period the cash flow level or cash flow amount isdifferent.Example:

An investment returns 10000 after first year, 13000, 15000 & 18000 after 2nd to 4thyear respectively. If the prevailing interest is 10% what is the present value of cash flow.

Equations:FV = PV x (1 + r)tPV = FV / (1 + r)t

YEAR CASH FLOW FVIF @ 10%=

1/(1.10)t

PV=

Cash Flow /FVIF

1 10000 =1/1.10 9,090.91

2 13000 =1/1.21 10,743.80

3 15000 =1/1.331 11,269.72

4 18000 =1/1.4641 12,294.24

TOTAL 56000 Ü43,398.68

Effective Annual Rate ± EAR

EAR basically depend on Compounding More period of Compounding total interest

will be more

Effective Annual Rate ± EAExample:

Bank A pays 15% interest on deposit, that is compounded monthly.

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 26/125

Bank B pays 15% interest on deposit, which is compounded quarterly.

Bank C pays 15% interest on deposit, which is compounded half yearly.

Formula to find EAR

Bank A (Monthly Compounding)

EAR = 1 + i/n n - 1

Bank A = 1 + .15/12 12 - 1

=1.16075 ± 1= 16.075%

Bank B (Quarterly Compounding)

Bank B = 1 + .15/4 4 - 1=(1.0375) 4 ± 1

= 1.15865 ± 1

= 15.865%

Bank C (Half Yearly Compounding)

Bank C = (1 + .15/2) 2 - 1

= (1.075) 2 - 1

= 1.155625 ± 1

= 15.5625%

Example:

A bank offers 12% compounded quarterly. If you place 1000 in an account today, howmuch you have at the end of two years?

What is EAR (Effective Rate of Interest)?Solution:

EAR =(1 + i/n)n - 1

EAR = (1 + .12/4)4 ± 1= 12.55%= (1.1255)2 X 1000 = 1266.75

OR Quarterly interest is 12/4 = 3%

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 27/125

=(1.03)8 X 1000 = 1.2667 X 1000 =1266.77BOND VALUATION

� It¶s a debt security� Whenever Company needs Capital, different sources to raise Capital

IPO¶s of Shares in Primary Market Bank Loan

Bond Debt Financing (Different from bank loan)� Bonds have maturity date� Normally Bonds are Long Term like 10 years, 20 years & 30 years

Main Characteristics:

How much Interest will be paid? How many times?

MaturityTerminologies:

Coupon Payments: stated annual interest amounte.g. A Bond which pays Rs. 100 every year. So Coupon payment i.e. Rs. 100 per year.

Coupon Rate:Coupon Interest Rate = Interest / Investment

Face value: Also Par value, shows the nomination value. Maturity Date: date on which Companies pay back the principal Investment. Discount Bond: A bond which is sold less than the face or par value is discount

bond. Also called Zero Coupon Or Zeros. Premium Bond: A bond which has a price over and above its face value or its par

value is Premium Bond. Yield to Maturity (YTM): Interest rate required in market on a bond.

Or A Market phenomenon, Interest rate on particular Investment Current yield: Annual coupon payment(s) divided by bond price.

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 28/125

Corporate finance lecture No. 05

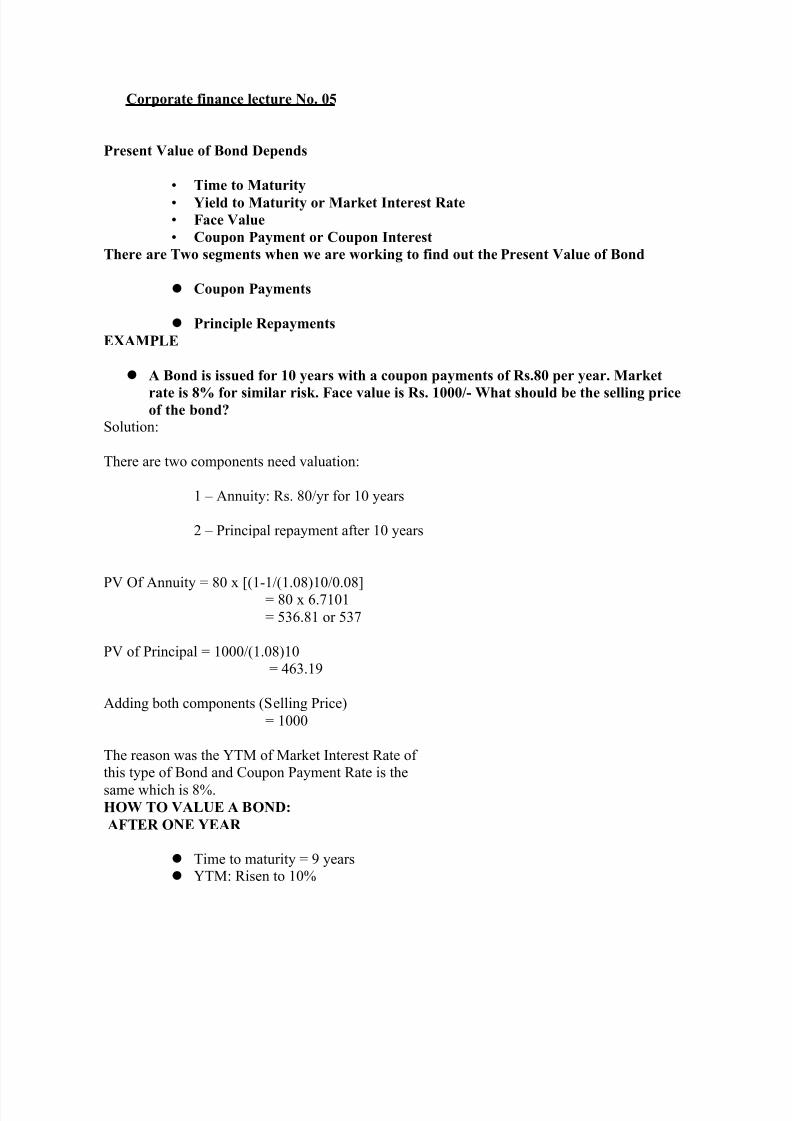

Present Value of Bond Depends

� T

ime to Maturity� Yield to Maturity or Market Interest Rate� Face Value� Coupon Payment or Coupon Interest

There are Two segments when we are working to find out the Present Value of Bond

Coupon Payments

Principle RepaymentsEXAMPLE

A Bond is issued for 10 years with a coupon payments of Rs.80 per year. Marketrate is 8% for similar risk. Face value is Rs. 1000/- What should be the selling price

of the bond?Solution:

There are two components need valuation:

1 ± Annuity: Rs. 80/yr for 10 years

2 ± Principal repayment after 10 years

PV Of Annuity = 80 x [(1-1/(1.08)10/0.08]= 80 x 6.7101= 536.81 or 537

PV of Principal = 1000/(1.08)10= 463.19

Adding both components (Selling Price)= 1000

The reason was the YTM of Market Interest Rate of this type of Bond and Coupon Payment Rate is thesame which is 8%.HOW TO VALUE A BOND:AFTER ONE YEAR

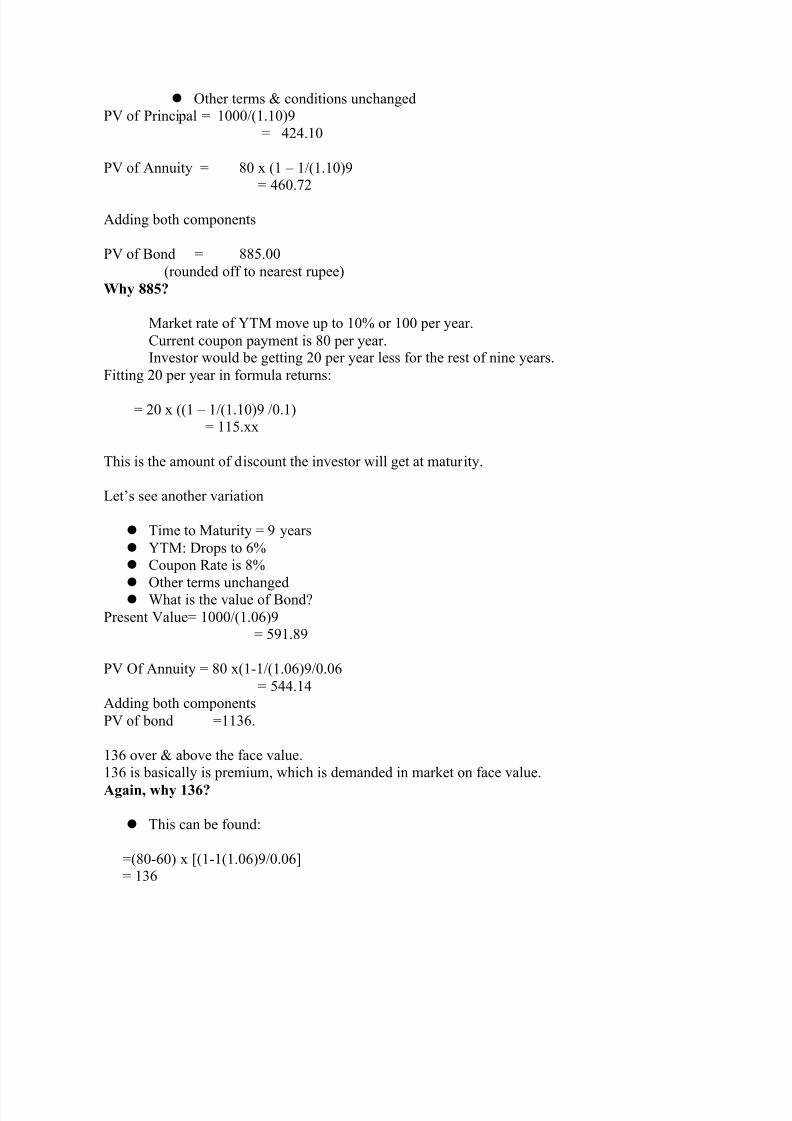

Time to maturity = 9 years YTM: Risen to 10%

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 29/125

Other terms & conditions unchangedPV of Principal = 1000/(1.10)9

= 424.10

PV of Annuity = 80 x (1 ± 1/(1.10)9

= 460.72

Adding both components

PV of Bond = 885.00 (rounded off to nearest rupee)

Why 885?

Market rate of YTM move up to 10% or 100 per year.Current coupon payment is 80 per year.Investor would be getting 20 per year less for the rest of nine years.

Fitting 20 per year in formula returns:= 20 x ((1 ± 1/(1.10)9 /0.1)

= 115.xx

This is the amount of discount the investor will get at maturity.

Let¶s see another variation

Time to Maturity = 9 years YTM: Drops to 6% Coupon Rate is 8% Other terms unchanged What is the value of Bond?

Present Value= 1000/(1.06)9= 591.89

PV Of Annuity = 80 x(1-1/(1.06)9/0.06= 544.14

Adding both componentsPV of bond =1136.

136 over & above the face value.136 is basically is premium, which is demanded in market on face value.Again, why 136?

This can be found:

=(80-60) x [(1-1(1.06)9/0.06]= 136

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 30/125

Summary:

YTM & Coupon Rate were same Result PV of Bond was exactly equal to the FV

YTM greater than Coupon Rate Results PV of the Bond less than the FV

YTM lower than Coupon Rate Result PV of the Bond was greater than FV

CONCLUSION:

A Bond will be sold on a discount when YTM is greater than coupon rate.

A bond will be sold on premium when YTM is lower than the coupon rate.

Current Yield Vs YTM

For a bond selling above the face value is said to sell at premium. It meansinvestor who buys it at a premium face a capital loss over the life of bond. Soreturn on bond will be less than the current yield.

For a bond selling below the face value is said to sell at discount. This meanscapital gain at maturity. The return on this bond is greater than its current yield.

EFFECTIVE YIELD

A bond pays semi-annual interest payments i.e., twice a year. Face value is Rs.1000/- andcoupon rate is 12%. This means two six-monthly payments of Rs. 60/- each. Bond matures in 7years and yield to maturity is 14%. What is the effective annual yield on this bond?1-PV = 1000/(1.07)14

= 1000 / 2.5785= 387.82

2- PV of annuity == 60 x (1 ± 1/(1.07)14/0.07= 60 x 8.745395= 524.72

Total PV of bond = 387.82+524.72= 912.55

Effective Yield = (1 + .07)2= 14.49%

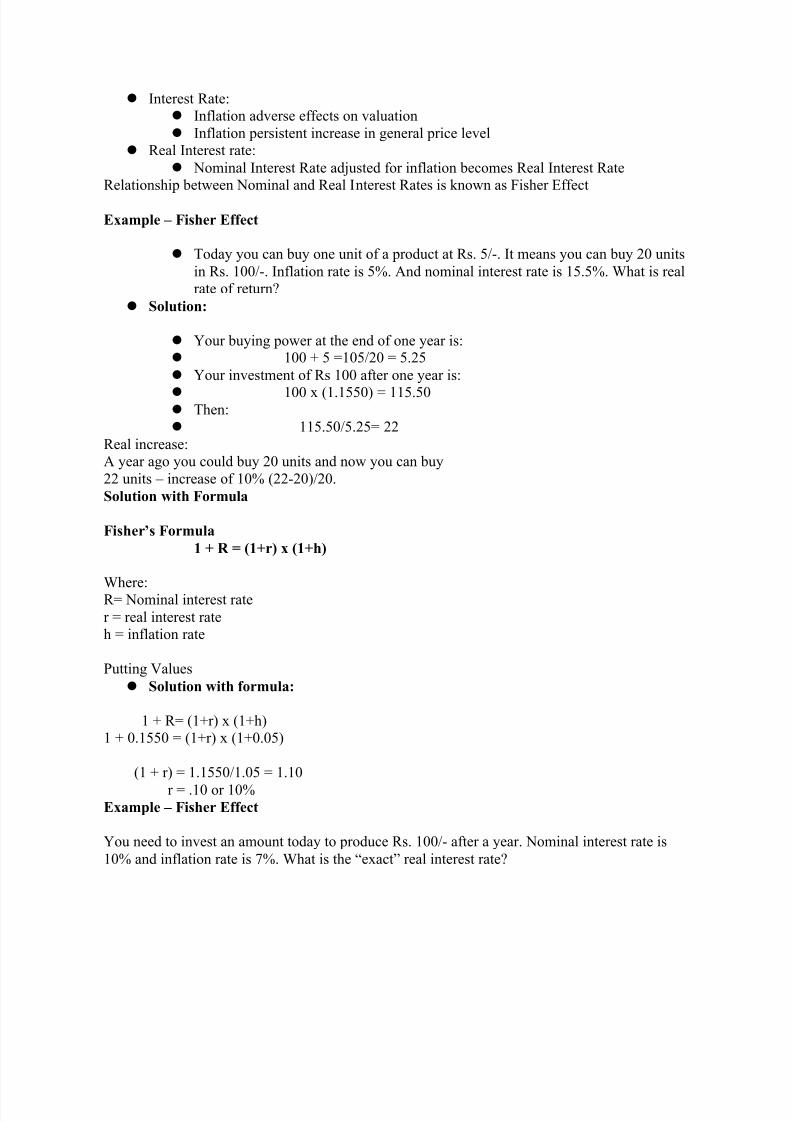

NOMINAL & REAL INTEREST RATE

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 31/125

Interest Rate: Inflation adverse effects on valuation Inflation persistent increase in general price level

Real Interest rate: Nominal Interest Rate adjusted for inflation becomes Real Interest Rate

Relationship between Nominal and Real Interest Rates is known as Fisher Effect

Example ± Fisher Effect

Today you can buy one unit of a product at Rs. 5/-. It means you can buy 20 unitsin Rs. 100/-. Inflation rate is 5%. And nominal interest rate is 15.5%. What is realrate of return?

Solution:

Your buying power at the end of one year is: 100 + 5 =105/20 = 5.25

Your investment of Rs 100 after one year is: 100 x (1.1550) = 115.50 Then: 115.50/5.25= 22

Real increase:A year ago you could buy 20 units and now you can buy22 units ± increase of 10% (22-20)/20.Solution with Formula

Fisher¶s Formula 1 + R = (1+r) x (1+h)

Where:R= Nominal interest rater = real interest rateh = inflation rate

Putting Values Solution with formula:

1 + R= (1+r) x (1+h)1 + 0.1550 = (1+r) x (1+0.05)

(1 + r) = 1.1550/1.05 = 1.10r = .10 or 10%

Example ± Fisher Effect

You need to invest an amount today to produce Rs. 100/- after a year. Nominal interest rate is10% and inflation rate is 7%. What is the ³exact´ real interest rate?

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 32/125

Solution:PV of Rs. 100= 100/(1.10)

=90.91If inflation rate is 7%, real value of Rs. 100 is therefore

= 100 / 1.07

= 93.46Real Interest Rate =1 + Nominal/1+Inflation= 1.10 / 1.07= 1.028 or 2.80%

If we discount real value of our Rs. 100 investment (93.46) by 2.8%, we get

PV = 93.46/1.028= 90.91

Point to Remember

Current Cash Flow must be discounted by NOMINAL INTEREST RATE

Real Cash Flow must be discounted byREAL INTEREST RATE

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 33/125

Corporate finance lecture No. 06

TERM STRUCTURE OF INTEREST RATES

Interest Rates in Short & Long terms are different.

Relationship between LT & ST Rates is known as Term Structure of Interest.

Term Structure tells us Nominal Interest Rate on default free securities.

When:LT > ST

Term Structure will be upward sloping

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 34/125

When:ST > LT Term Structure will be downward sloping

FACTORS OF TERM STRUCTURE

Real Interest Rate

Inflation Rate

Interest Rate Risk

REAL INTEREST RATEReal Interest Rate is basic component of Term Structure.When Real Interest Rate is high, all Interest Rates are high.Real Interest Rate remains constant regardless of maturity.

Real Interest Rates do not influence the shape of Term Structure of Interest.INFLATION RATEInflation Rate reduces the Time Value or Value of Money.If Interest Rate is high, Nominal Interest will increase.Due to Inflation, Investors demand compensation of the lost value. This is known asInflation Premium.Inflation Rate strongly influences the Term Structure of Interest.INTEREST RATE RISK

The fluctuation in Interest Rate also influences the Term Structure significantly.

Any slight fluctuation in Interest Rate can have a huge change in PV value due tocompounding effect.

Investors demand extra Risk Premium for change in Interest Rate. This is known as InterestRate Risk.

Yield Curve ± Coupon Based Bonds Three Factors Influence Yield Curve StructureDefault Risk Premium:

Coupon Base Bond is a promise with a risk that company may fail to pay interest.Taxability Premium:

Dividend bears TaxReturns are reduced by TaxesInvestor need this Premium

Liquidity Premium:If bond is more liquid, expected rate of return is low. For less liquid bonds,compensation is required as Liquidity Premium

TERM STRUCTURE YIELD CURVEMain Points:

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 35/125

Interest Rate Risk Inflation PremiumReal Interest RateDefault Risk PremiumTaxability Premium

Liquidity PremiumCOMMON STOCK VALUATION

Features:

No promised Cash Flow for Dividend No redemption or No Date of MaturityProblems in Determining Rate of Return

Expected Returns:

Total Return = Dividends + Capital Gains

= D1 + (P1 ± P0) / P0

Where:D1 = Dividend after 1 Year P1 = Price of Stock after Year 1P0 = Price of Stock Period 0 or Current Price

Expected Returns:

Total Return = Dividends + Capital Gains

= D1 + (P1 ± P0) / P0

Where:D1 = Dividend after 1 Year P1 = Price of Stock after Year 1P0 = Price of Stock Period 0 or Current Price

For Example:P0 = Rs. 20/-Dividend1 = Rs. 2 per shareP1 = Rs. 23/-

Then expected return is:= 2 + (23 ± 20) / 20=5 / 20= 25%

Putting it the other way:We are trying to calculate the price today if the expected rate of return is 25%:

Price Today = D1 + P1 / 1 + r

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 36/125

= 2 + 23 / 1.25= 25 / 1.25= 20

Putting it the other way:

We are trying to calculate the price today if the expected rate of return is 25%:

Price Today = D1 + P1 / 1 + r

= 2 + 23 / 1.25= 25 / 1.25= 20

If:Today Price > Rs. 20

Then the expected return should have been lower than

other shares of equivalent risk. If demand will lower, peopledispose off this share. It forces the price to settle on Rs. 20.

If:Today Price < Rs. 20

Then the expected return should have been higher thanother shares of same risk. Everyone will rush to buy it, thusforcing price to settle on Rs. 20.CONCLUSION

At each point in time of all shares of samerisk are priced to offer the same expectedrate of return.DIVIDEND DISCOUNT MODEL

It is not an easy job to predict or forecast Future Stock Price.

Dividend Discount Model states that today¶s Price is equal to the Present Value of all futureDividendsAfter One year:

P0 = Div + P1 / (1 + r)After 2 years the value of stock is:

=Div1/(1+r) + Div2+P2/(1+r)2After 3 years the value of stock is:=Div1/(1+r) + Div2/(1+r)2 + Div3 + P3/(1+r)3

When the time horizon is infinitely far, then we donot consider the final price as it has no Present

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 37/125

Value today.Present Value of Common Stock relay on streamsof future Dividend.DIVIDEND GR OWTH MODELS

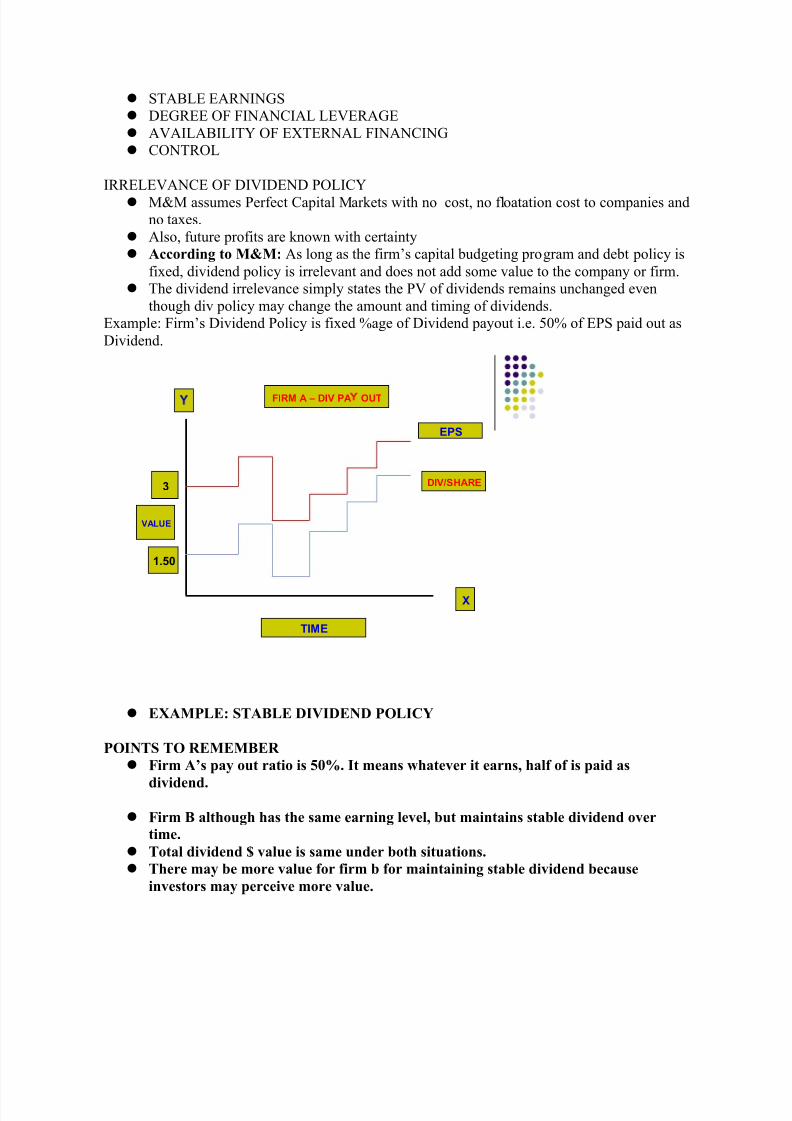

Assumptions:Assume NO GR OWTH by the Company.

Company pays out all as Dividend what it earns every year.

It means that NOTHING is reinvested in business.

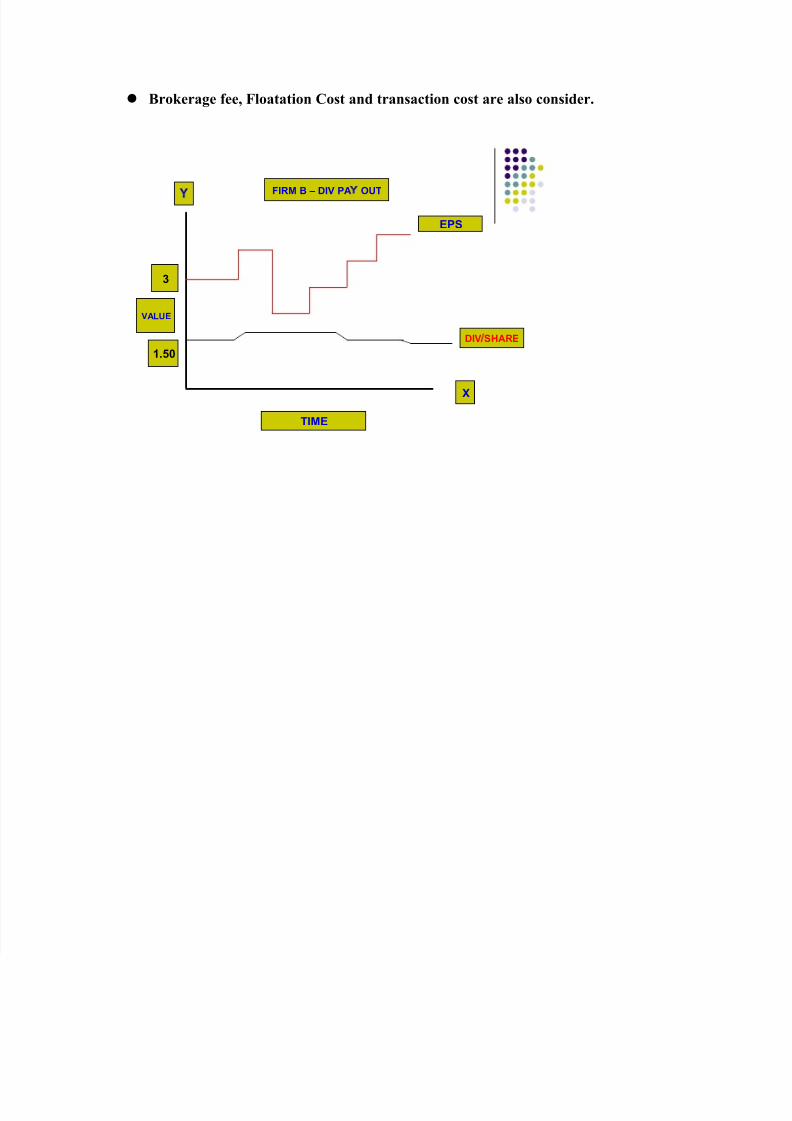

It means that Investors may forecast that future Dividends will not increase.Dividends over the years are at the same level ± PER PETUITY DIVIDEND GR OWTH MODELSNO GR OWTHMODEL

If the value of stock is the PV of all future Dividend then:PV = DIV / r

When company pays out everything as Dividend then earnings and Dividend will be equaland PV can be calculated as:

PV = EPS / rCONSTANT GR OWHT MODEL

Assume that Dividends will grow at a Constant GrowthRate. For example, 5% per year.It means that Dividend of Rs. 2 per share at 5%Constant Growth Rate will be:First year:

Div1 = 2Second year:

Div2 = 2 x 1.05 = 2.10Third year:

Div3 = 2 x (1.05)2 = 2.205By fitting these values into formula we get:

= D1/1+r + D1(1+g)/(1+r)2+ D1(1+g)2/(1+r)3 «.

= 2 /1.12 + 2.10/(1.12)2 + 2.205/(1.12)3

=1.79 + 1.67 + 1.57 + «.

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 38/125

Although the number of terms is infinite, the PV of Dividend is proportionately smaller thanthe preceding term and this will continue as long as Growth Rate is less than the DiscountRate.

Because the far Distant Dividends will be close to Zero, the sum of all of these terms is finite

despite of the fact that an infinite number of Dividends will be paid out.

Corporate finance lecture No. 07 DIVIDEND DISCOUNT MODEL CONSTANT GROWTHSo we can write equation as:

P0 = D1 x (1+g) / (r ± g)

This is known as Constant-Growth Dividend Discount Model Or Gordon Growth Model.

1. First calculate growth rate2. Than calculate price P03. Note that next dividend D1 has been used for valuation

Example:

The next dividend of a company will be Rs 4 per share. Investors demand 16 percent return onshare having same risk level as of this company. The dividend growth is 6% per year.

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 39/125

Calculate the value of this Company¶s stock today and in four years using Dividend GrowthModel.Solution:

Next Dividend has already been given:P0 = D1 / (r - g)

P0 = 4 /( .16 - .06)P0 = 40Price in 4 years: D4 = 4 x (1.06)3 = 4.764 Formula: P4 = D4 x (1+g) / (r ± g)

P4 = 4.764 x (1 + .06) / (0.16 - 0.06) = 50.50Non-Constant Growth

Example:Dividends for first, second and third year are expected in the amount of Rs. 1, 2 and 2.50respectively and after that dividends will grow at a constant rate of 5 % per year. Required rate is10%.

Calculate the value of stock after 3 years & today.Solution:P3 = D3 x (1+g) / (r - g) = 2.50 X 1.05 / (0.10 ± 0.05) P3 = Rs. 52.50Today¶s Price:

= d1/(1 + r) + d2 /(1+r)2 + d3/(1+r)3 + P3/ (1+r)3= 1/1.10 + 2/(1.10)2 + 2.50/(1.10)3+52.50/(1.10)3

Value of Stock today = Rs. 43.88

GR OWTH & INCOME STOCKS/SHARES

Investors trade stocks or share for two reasons:

y Capital Gains or Growth Stock y Dividends or Income Stock

GR OWTH & INCOME STOCKS/SHARES 1) Retention Policy:Retention of profit and then plowback or re-invest in the business.

2)P

ayout Ratio:Percent age of profit at which Dividend is declared by the business.Example:

Dividend1 = Rs. 3.50 per share r = 12%g = 7%EPS = Rs. 5 per share

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 40/125

Payout Ratio = 70%Retention Ratio= 30%

Company requires 20% Return on Plowback.If Payout is 100% or no Retention, and it means no growth:

g = 0 then P0: P0 = DIV / r ± g= 5 / .12 - 0 = 41.67

Mean that:EPS = div

Therefore we used:div = 5no growth = 0

If retention of 30% applied, and expected return is 12% (existing), then P0:

P0 = 3.50 / .12 - .036 = 41.67

0.036 or 3.60% is calculated as:= 0.30 x 12% = 3.60

If retention of 30% applied, and expected return is 20% on retention, then P0 :P0 = 3.50 / .12 - .06= 58.33

CONCLUSION

Plowing back earnings does not add value to current stock price, if thatreinvestment is not expected to earn higher returns than expected by investors.

Plowing earnings back will only push the current prices of the stock up if greater returns are expected by the investors.

Example:Div1 = Rs. 1Div2 = 1.20Div3 = 1.44 after that it grows 5% per year EPS3= 3.78

r = 10%P/E ratio = 8 for shares of same risk level

Price of stock after 3 years and today?Price today:

P0 = PV(div1-3) + PV(P3)PV(div1-3) = 1/1.10 + 1.2/(1.10)2+1.44/(1.10)3

= 2.98PV of P3 = P/E x EPS

= 8 x 3.78= 30.24= 30.24/(1.10)3

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 41/125

= 22.72Putting value of PV(div1-3) & PV of P3 in the main formula:

= 2.98 + 22.72P0 = 25.70

We can calculate P3 with Dividend Model:P

3 = div4 / (r ± g)

Div4 = div3 x (1+g)= 1.44 x 1.05 = 1.512

Putting value of Div4 in formula:P3 = 1.512 / (0.12 - .05)= 30.24

OTHER TOOLS OF STOCK EVALUATION

TECHNICAL ANALYSIS:

T

echnical analysis studies supply and demand in a market in a attempt todetermine what direction or trend will continue in future

Study of Market Sentiments

TECHNICAL ANALYSIS

Evaluating security by analyzing the statistics generated by market activity suchas Past Prices and Volume

Charts and other tools are used to identify patterns that suggest future activityTRENDS

A trend shows the general direction in which a security or market is headed

Types:Up-TrendsDown TrendsHorizontal Trends

TRENDS LENGTH Short TermMedium TermLong Term

Support & Resistance

Support is the lower ceiling price of a stock Resistance is the upper ceiling of stock

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 42/125

CHAR T

A series of prices over a time period presented graphicallyTime scale: intraday, daily, weekly, monthly & yearlyPrice scale: change in price presented as absolute terms. Change shown in % is known

as Logarithmic ScaleCHAR T PATTERN

A distinct formation of point on chart that create trading signals or a sign of future movementHead & Shoulder: reversal pattern when formed, and signals that the security islikely to move against the previous trendCups & handle: continuation of bullish patternCONCLUSION

Technical Analysis method of evaluating stocks by analyzing statistics generatedby market activity.Technical traders take a short term approach to analyzing chart.Product of Technical Analysis is a trend.

Corporate finance lecture No. 08

COMMON STOCK VALUATIONFUNDAMENTAL ANALYSIS:

Analyst is trying to reach near the intrinsic value of company¶s share by reading andanalyzing the financial, non-financial information and industry comparison.Three step process:Economic indicators: GDP, Interest Rates, Inflation, Exchange RateIndustry Comparison and CompetitionIndividual Company Analysis

FinancialsCEO ReportAudited AccountsAuditors Report

CAPITAL BUDGETINGDefinition:It is a process in which we can evaluate the investment opportunities in order toacquire some capital asset. Types:

New ProjectExpansion Project

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 43/125

Modernization / ReplacementOther / social responsibility ± Pollution control etc

Research & DevelopmentExploration

Capital Budgeting ProcessCB decisions are irreversible in nature

SWOT Analysis :S ± StrengthW ± WeaknessO ± OpportunitiesT ± Threats

CB targeted towards potential opportunitiesInvestment Opportunitie(s) is/are identifiedDifferent alternatives are considered

Every alternative is evaluatedThe best option (s) is/are undertakenPROJECT EVALUATION

Relevant Costs:Incremental costs and benefits are relevantCost incidental to the undertaking of a project

Non-Relevant Costs:Sunk Cost:

Which has been incurred in the pastCommitted Cost:

Future costOpportunity Cost:

Existing benefit surrendered in favor of next best alternativeOpportunity Cost is also a relevant cost

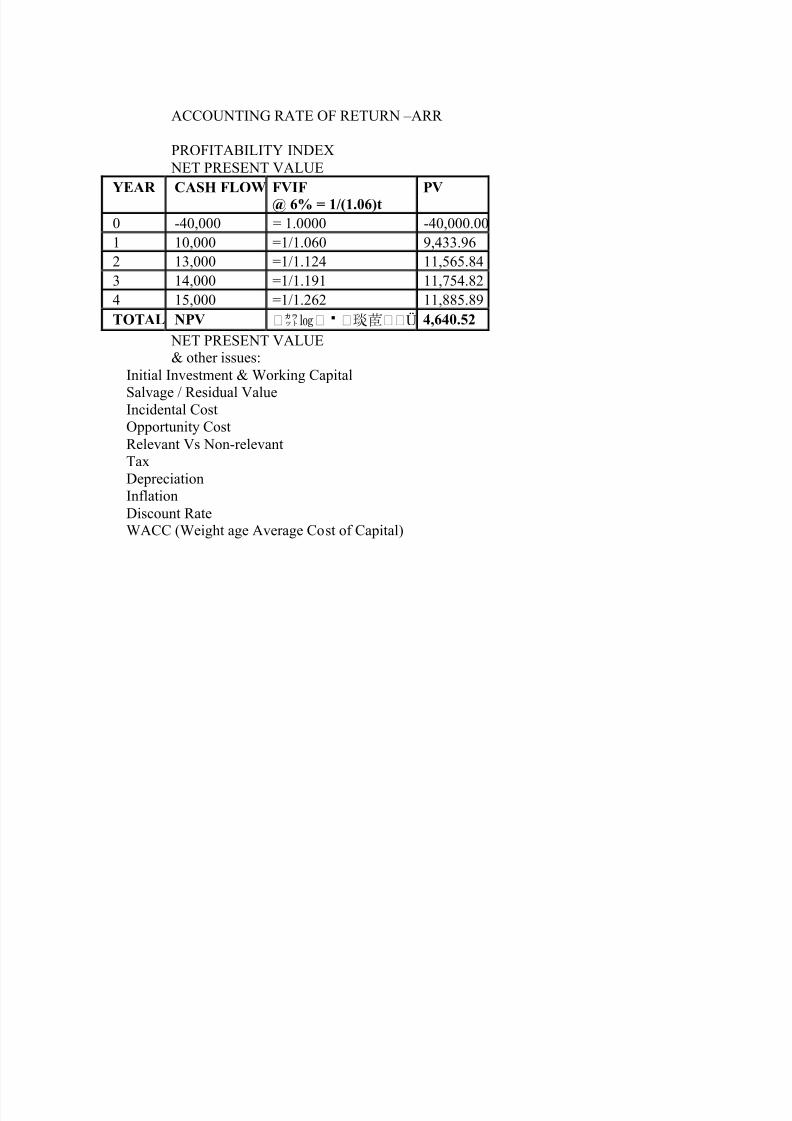

Profit Vs Cash Flow NET PRESENT VALUE NPV = Discounted Benefits ± Initial Investment

Example:An investment in an asset of Rs. 40,000 today returns 10000 after first year,13000, 14000 & 15000 after 2nd to 4th year respectively.If the prevailing interest is 6% what is the net present value of cash flow?

EVALUATING TECHNIQUES NET PRESENT VALUE / DCF

INTERNAL RATE OF RETURN ± IRR

PAYBACK PERIOD

DISCOUNTED PAYBACK PERIOD

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 44/125

ACCOUNTING RATE OF RETURN ±ARR

PROFITABILITY INDEX NET PRESENT VALUE

YEAR CASH FLOW FVIF @ 6% = 1/(1.06)t PV

0 -40,000 = 1.0000 -40,000.001 10,000 =1/1.060 9,433.962 13,000 =1/1.124 11,565.843 14,000 =1/1.191 11,754.824 15,000 =1/1.262 11,885.89TOTAL NPV Ü 4,640.52

NET PRESENT VALUE & other issues:

Initial Investment & Working CapitalSalvage / Residual ValueIncidental CostOpportunity CostRelevant Vs Non-relevantTaxDepreciationInflationDiscount RateWACC (Weight age Average Cost of Capital)

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 45/125

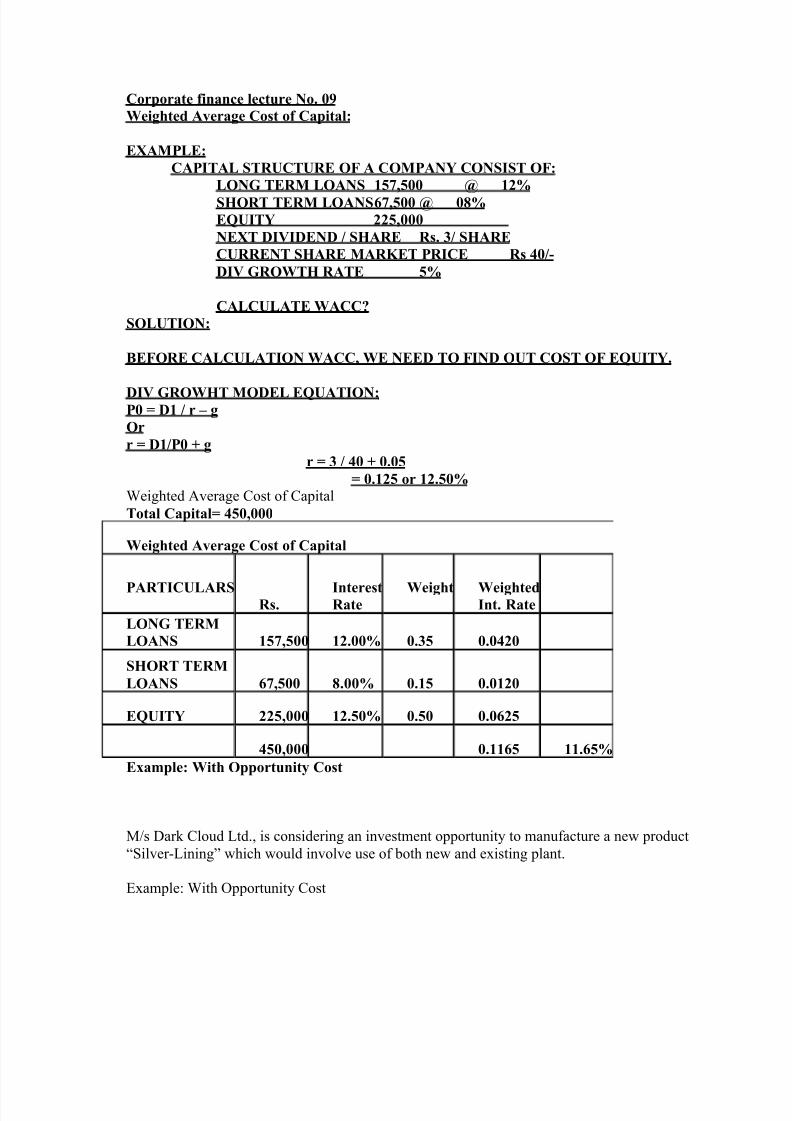

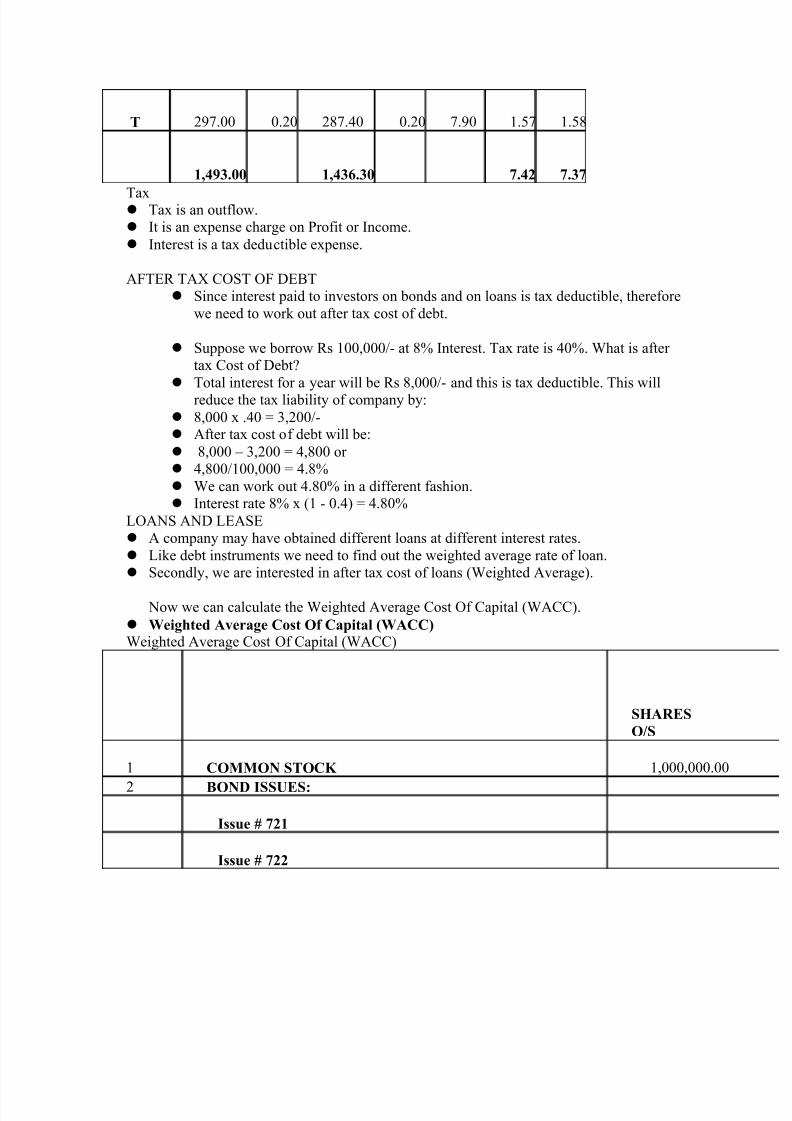

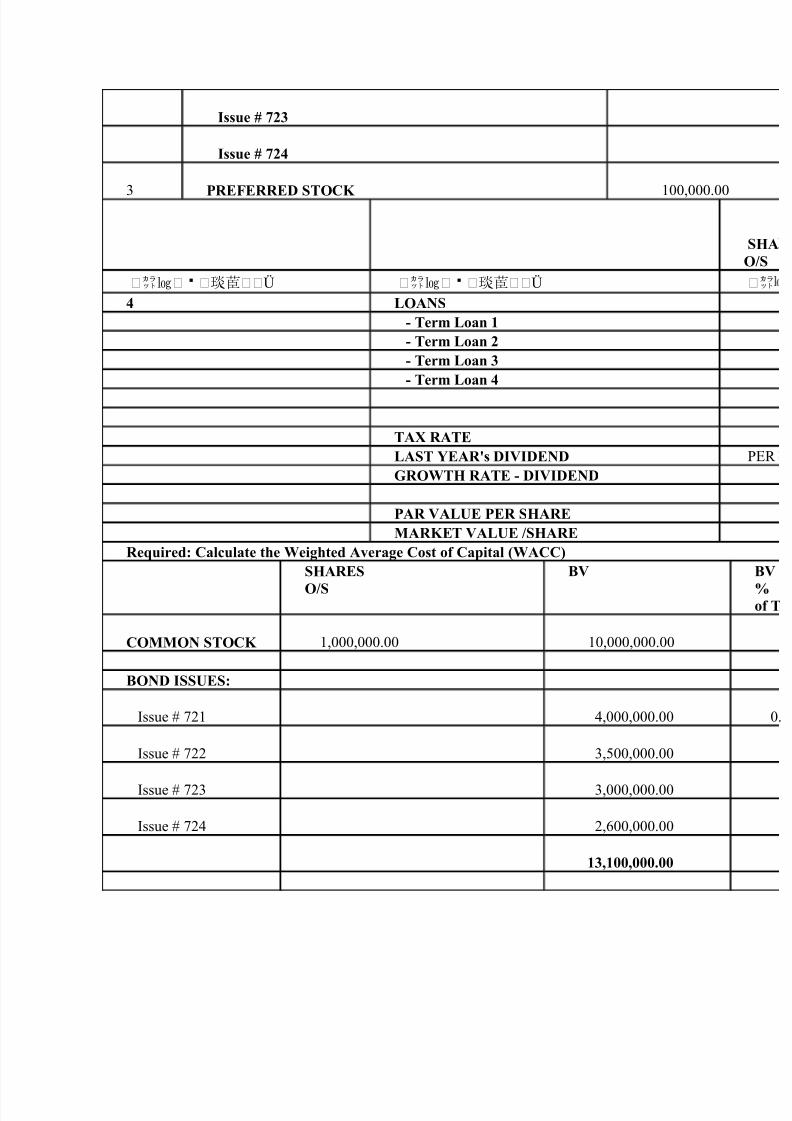

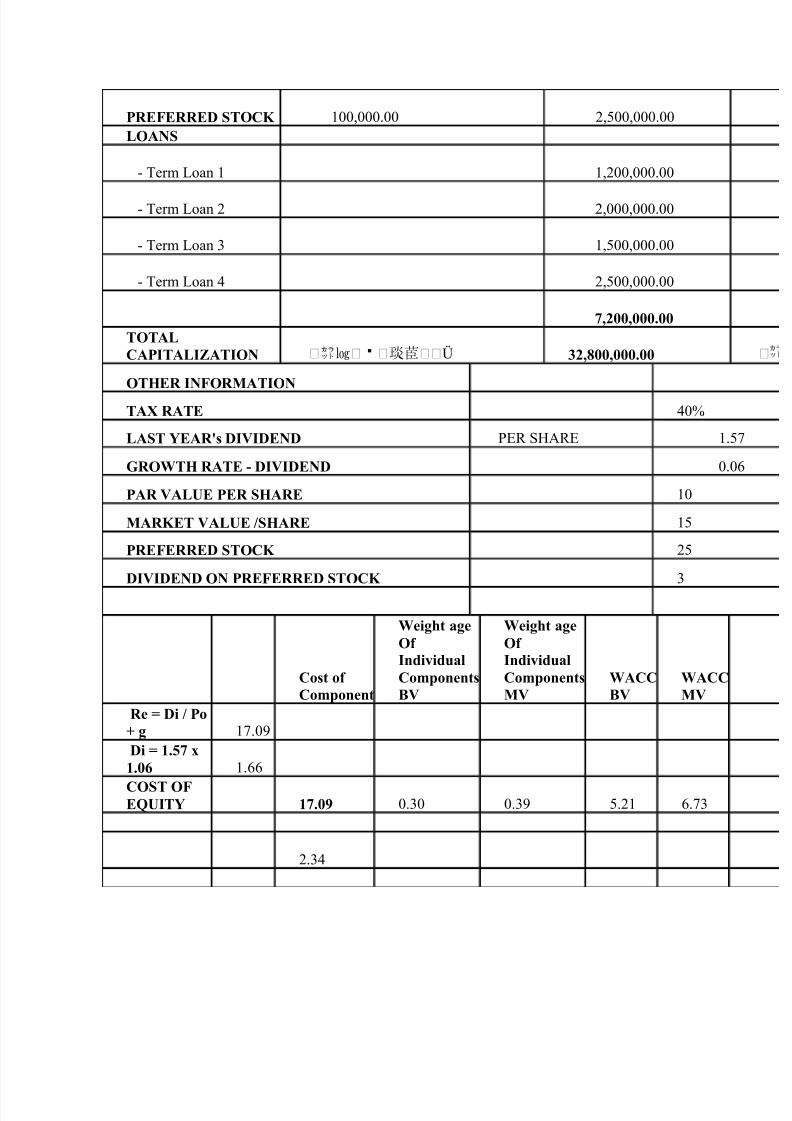

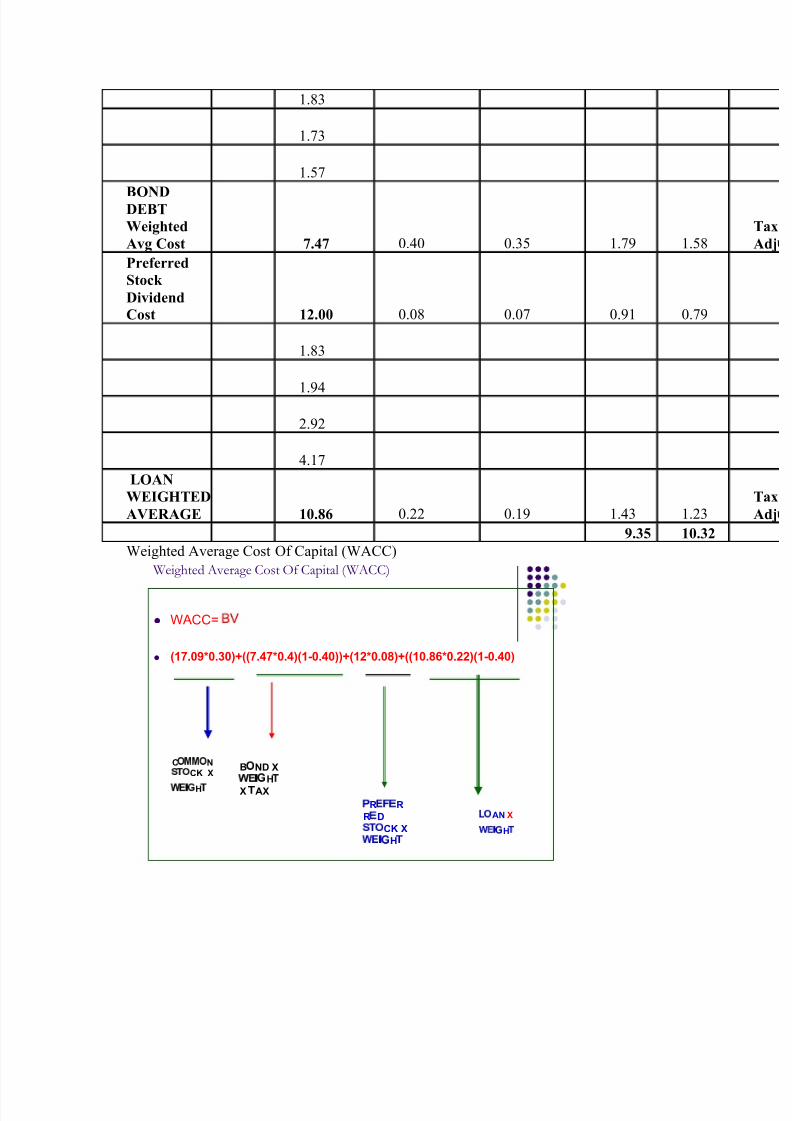

Corporate finance lecture No. 09Weighted Average Cost of Capital:

EXAMPLE:CAPITAL STRUCTURE OF A COMPANY CONSIST OF:

LO

NGT

ERM LO

ANS 157,500 @ 12%SHOR T TERM LOANS 67,500 @ 08%EQUITY 225,000NEXT DIVIDEND / SHARE Rs. 3/ SHARECURRENT SHARE MARKET PRICE Rs 40/-DIV GR OWTH RATE 5%

CALCULATE WACC?SOLUTION:

BEFORE CALCULATION WACC, WE NEED TO FIND OUT COST OF EQUITY.

DIV GR OWHT MODEL EQUATION:P0 = D1 / r ± gOrr = D1/P0 + g

r = 3 / 40 + 0.05= 0.125 or 12.50%

Weighted Average Cost of CapitalTotal Capital= 450,000

Weighted Average Cost of Capital

PAR TICULARS Rs.

Interest Rate

Weight Weighted Int. Rate

LONG TERMLOANS 157,500 12.00% 0.35 0.0420

SHOR T TERMLOANS 67,500 8.00% 0.15 0.0120

EQUITY 225,000 12.50% 0.50 0.0625

450,000 0.1165 11.65%

Example: With Opportunity Cost

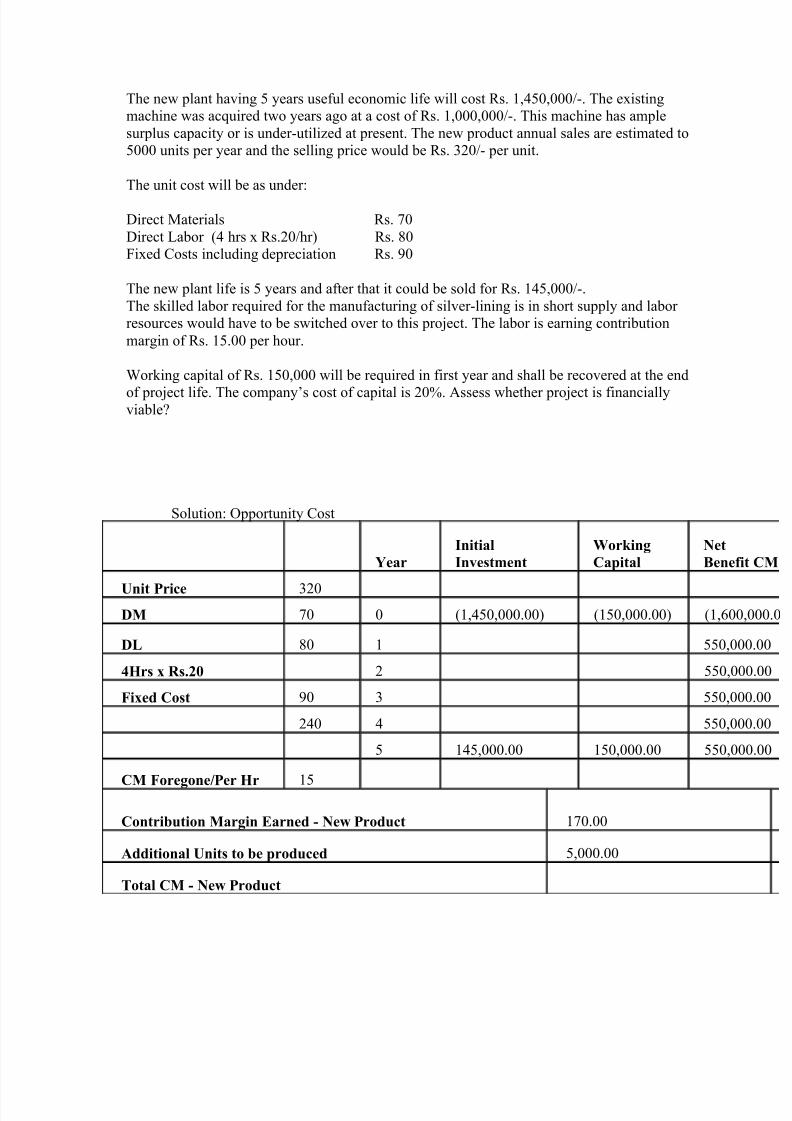

M/s Dark Cloud Ltd., is considering an investment opportunity to manufacture a new product³Silver-Lining´ which would involve use of both new and existing plant.

Example: With Opportunity Cost

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 46/125

The new plant having 5 years useful economic life will cost Rs. 1,450,000/-. The existingmachine was acquired two years ago at a cost of Rs. 1,000,000/-. This machine has amplesurplus capacity or is under-utilized at present. The new product annual sales are estimated to5000 units per year and the selling price would be Rs. 320/- per unit.

The unit cost will be as under:

Direct Materials Rs. 70Direct Labor (4 hrs x Rs.20/hr) Rs. 80Fixed Costs including depreciation Rs. 90

The new plant life is 5 years and after that it could be sold for Rs. 145,000/-.The skilled labor required for the manufacturing of silver-lining is in short supply and labor resources would have to be switched over to this project. The labor is earning contributionmargin of Rs. 15.00 per hour.

Working capital of Rs. 150,000 will be required in first year and shall be recovered at the endof project life. The company¶s cost of capital is 20%. Assess whether project is financiallyviable?

Solution: Opportunity Cost

Year InitialInvestment

WorkingCapital

NetBene

Unit Price 320

DM 70 0 (1,450,000.00) (150,000.00) (1,60

DL 80 1 550,0

4Hrs x Rs.20 2 550,

Fixed Cost 90 3 550,0

240 4 550,0

5 145,000.00 150,000.00 550,0

CM Foregone/Per Hr 15

Contribution Margin Earned - New Product 170.00

Additional Units to be produced 5,000.00

Total CM - New Product

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 47/125

CM surrendered

Labor hour required for New Product 20,000.00

CM lost / Hr 15.00

Total CM lost

Net CM - Benefit

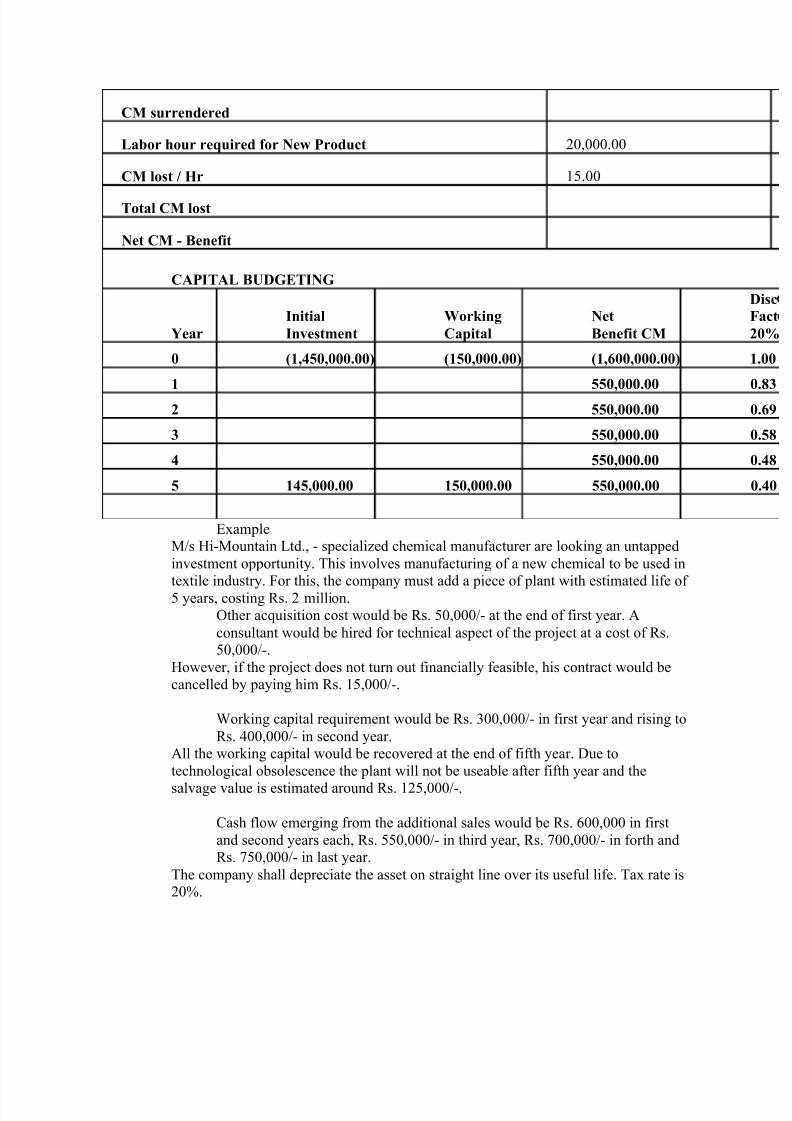

CAPITAL BUDGETING

Year Initial Investment

Working Capital

NetBenefit CM

0 (1,450,000.00) (150,000.00) (1,600,000.00)

1 550,000.00 2 550,000.00

3 550,000.00

4 550,000.00

5 145,000.00 150,000.00 550,000.00

ExampleM/s Hi-Mountain Ltd., - specialized chemical manufacturer are looking an untappedinvestment opportunity. This involves manufacturing of a new chemical to be used intextile industry. For this, the company must add a piece of plant with estimated life of 5 years, costing Rs. 2 million.

Other acquisition cost would be Rs. 50,000/- at the end of first year. Aconsultant would be hired for technical aspect of the project at a cost of Rs.50,000/-.

However, if the project does not turn out financially feasible, his contract would becancelled by paying him Rs. 15,000/-.

Working capital requirement would be Rs. 300,000/- in first year and rising toRs. 400,000/- in second year.

All the working capital would be recovered at the end of fifth year. Due totechnological obsolescence the plant will not be useable after fifth year and thesalvage value is estimated around Rs. 125,000/-.

Cash flow emerging from the additional sales would be Rs. 600,000 in firstand second years each, Rs. 550,000/- in third year, Rs. 700,000/- in forth andRs. 750,000/- in last year.

The company shall depreciate the asset on straight line over its useful life. Tax rate is20%.

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 48/125

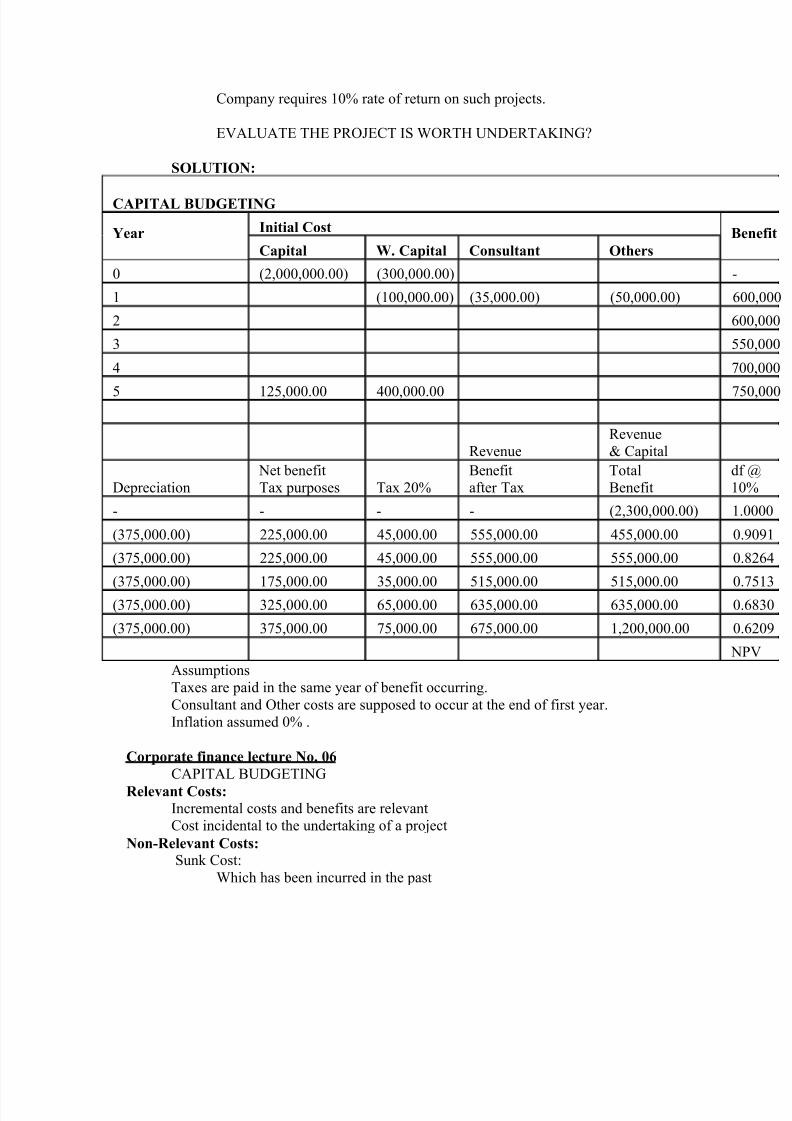

Company requires 10% rate of return on such projects.

EVALUATE THE PROJECT IS WORTH UNDERTAKING?

SOLUTION:

CAPITAL BUDGETING

Year Initial Cost

Capital W. Capital Consultant Others

0 (2,000,000.00) (300,000.00)

1 (100,000.00) (35,000.00) (50,000.00)

2

3

4

5 125,000.00 400,000.00

RevenueRevenue& Capital

Depreciation Net benefitTax purposes Tax 20%

Benefitafter Tax

TotalBenefit

- - - - (2,300,000.00)

(375,000.00) 225,000.00 45,000.00 555,000.00 455,000.00

(375,000.00) 225,000.00 45,000.00 555,000.00 555,000.00

(375,000.00) 175,000.00 35,000.00 515,000.00 515,000.00

(375,000.00) 325,000.00 65,000.00 635,000.00 635,000.00

(375,000.00) 375,000.00 75,000.00 675,000.00 1,200,000.00

AssumptionsTaxes are paid in the same year of benefit occurring.Consultant and Other costs are supposed to occur at the end of first year.Inflation assumed 0% .

Corporate finance lecture No. 06CAPITAL BUDGETING

Relevant Costs:Incremental costs and benefits are relevantCost incidental to the undertaking of a project

Non-Relevant Costs:Sunk Cost:

Which has been incurred in the past

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 49/125

Committed Cost:Future cost

Opportunity Cost:Existing benefit surrendered in favor of next best alternativeOpportunity Cost is also a relevant cost

Relevant Costs:Incremental costs and benefits are relevantCost incidental to the undertaking of a project

Non-Relevant Costs:Sunk Cost:

Which has been incurred in the pastCommitted Cost:

Future costOpportunity Cost:

Existing benefit surrendered in favor of next best alternativeOpportunity Cost is also a relevant cost

NET PRESENT VALUEDecision Rule:Accept the Project with Positive NPV

In case of more than one projectThe Project with Higher NPV can be under taken

INTERNAL RATE OF RETURN

Rate of Return that is used to calculate the EXACT DCF Rate of Return which the project isexpected to achieve. A rate at which NPV is zero.

If the IRR of a project is lower than the target return, the project is deemed unfeasible.

If the IRR of a project is greater than the target return, the project is deemed feasible.

Example ± IRR

Without computer program IRR is found by method called interpolationCalculate NPV using a whole number If positive, calculate second NPV using a higher discount rate that, preferably returnsthe NPV in negativeThen plug in these values in to formulaFormula to Learn:

IRR = a + [{A/(A-B)} x (b-a)}%

Where:a = Lower discount rate used to calculate NPV

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 50/125

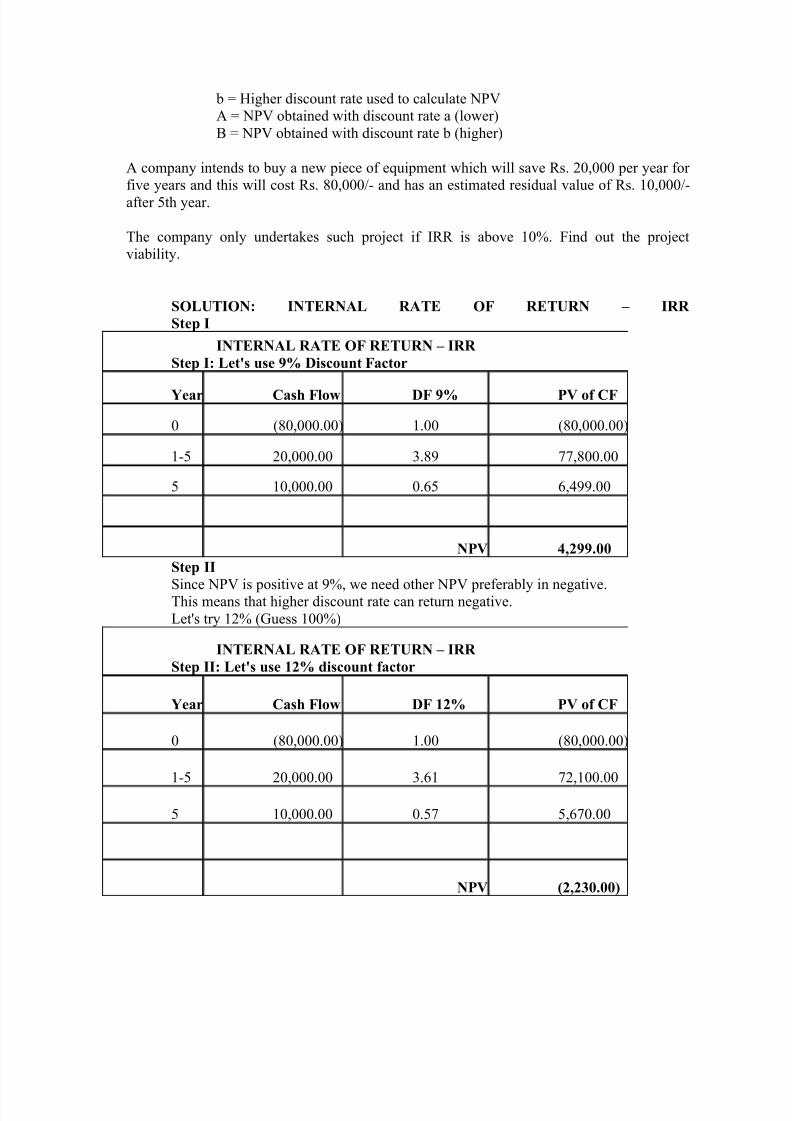

b = Higher discount rate used to calculate NPVA = NPV obtained with discount rate a (lower)B = NPV obtained with discount rate b (higher)

A company intends to buy a new piece of equipment which will save Rs. 20,000 per year for

five years and this will cost Rs. 80,000/- and has an estimated residual value of Rs. 10,000/-after 5th year.

The company only undertakes such project if IRR is above 10%. Find out the projectviability.

SOLUTION: INTERNAL RATE OF RETURN ± IRR Step I

INTERNAL RATE OF RETURN ± IRR Step I: Let's use 9% Discount Factor

Year Cash Flow DF 9% PV of CF

0 (80,000.00) 1.00 (80,000.00)

1-5 20,000.00 3.89 77,800.00

5 10,000.00 0.65 6,499.00

NPV 4,299.00

Step II Since NPV is positive at 9%, we need other NPV preferably in negative.This means that higher discount rate can return negative.Let's try 12% (Guess 100%)

INTERNAL RATE OF RETURN ± IRR Step II: Let's use 12% discount factor

Year Cash Flow DF 12% PV of CF

0 (80,000.00) 1.00 (80,000.00)

1-5 20,000.00 3.61 72,100.00

5 10,000.00 0.57 5,670.00

NPV (2,230.00)

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 51/125

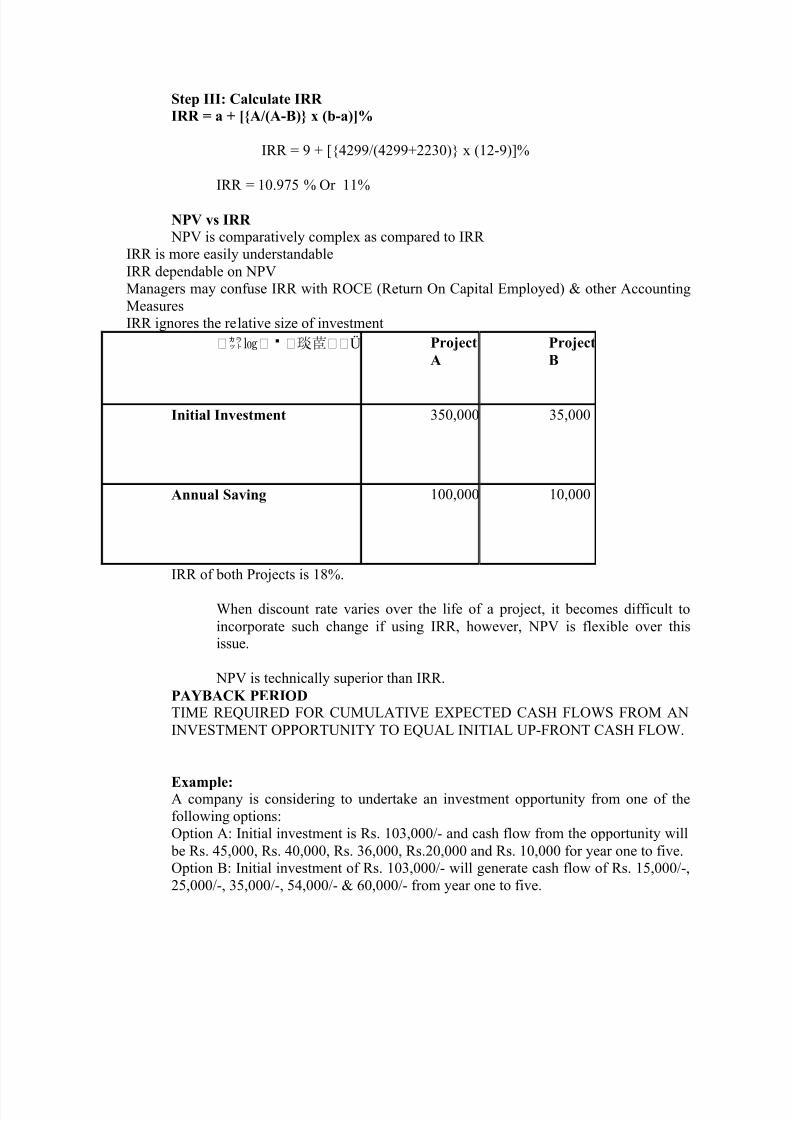

Step III: Calculate IRR IRR = a + [{A/(A-B)} x (b-a)]%

IRR = 9 + [{4299/(4299+2230)} x (12-9)]%

IRR = 10.975 % Or 11%

NPV vs IRR NPV is comparatively complex as compared to IRR

IRR is more easily understandableIRR dependable on NPVManagers may confuse IRR with ROCE (Return On Capital Employed) & other AccountingMeasuresIRR ignores the relative size of investment

Ü ProjectA

ProjectB

Initial Investment 350,000 35,000

Annual Saving 100,000 10,000

IRR of both Projects is 18%.

When discount rate varies over the life of a project, it becomes difficult toincorporate such change if using IRR, however, NPV is flexible over thisissue.

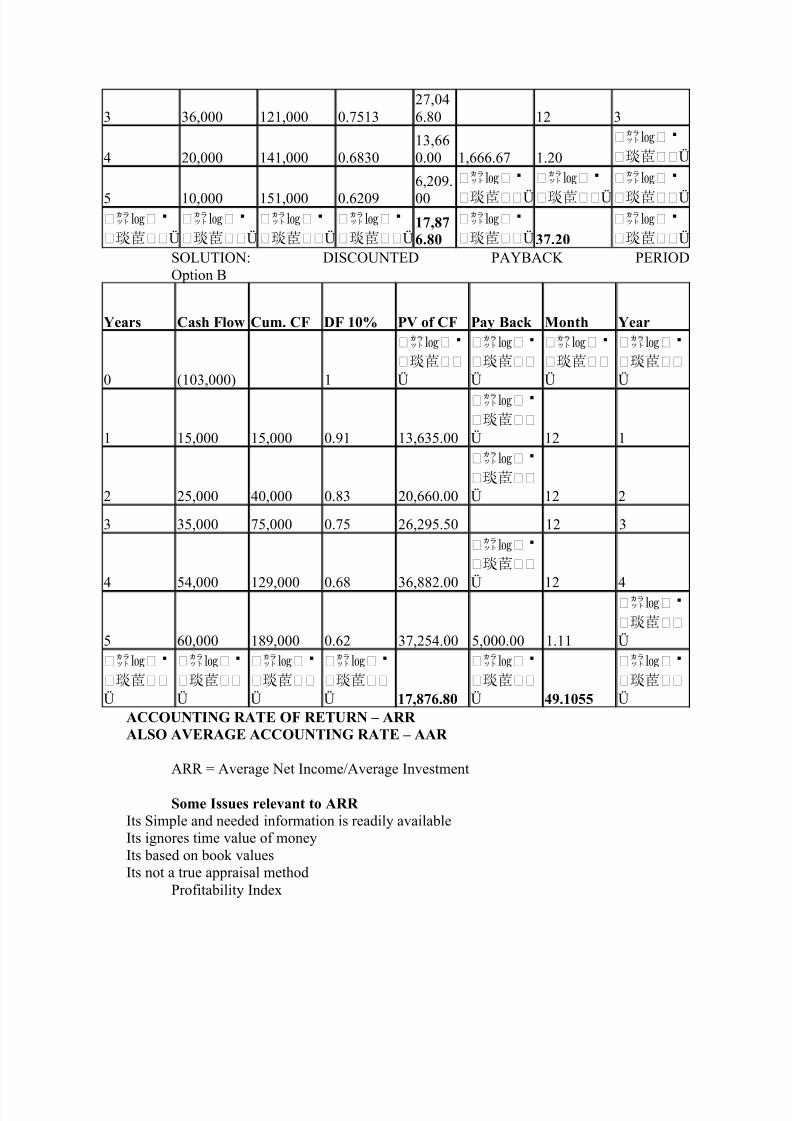

NPV is technically superior than IRR.PAYBACK PERIOD TIME REQUIRED FOR CUMULATIVE EXPECTED CASH FLOWS FROM ANINVESTMENT OPPORTUNITY TO EQUAL INITIAL UP-FRONT CASH FLOW.

Example:A company is considering to undertake an investment opportunity from one of thefollowing options:Option A: Initial investment is Rs. 103,000/- and cash flow from the opportunity will be Rs. 45,000, Rs. 40,000, Rs. 36,000, Rs.20,000 and Rs. 10,000 for year one to five.Option B: Initial investment of Rs. 103,000/- will generate cash flow of Rs. 15,000/-,25,000/-, 35,000/-, 54,000/- & 60,000/- from year one to five.

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 52/125

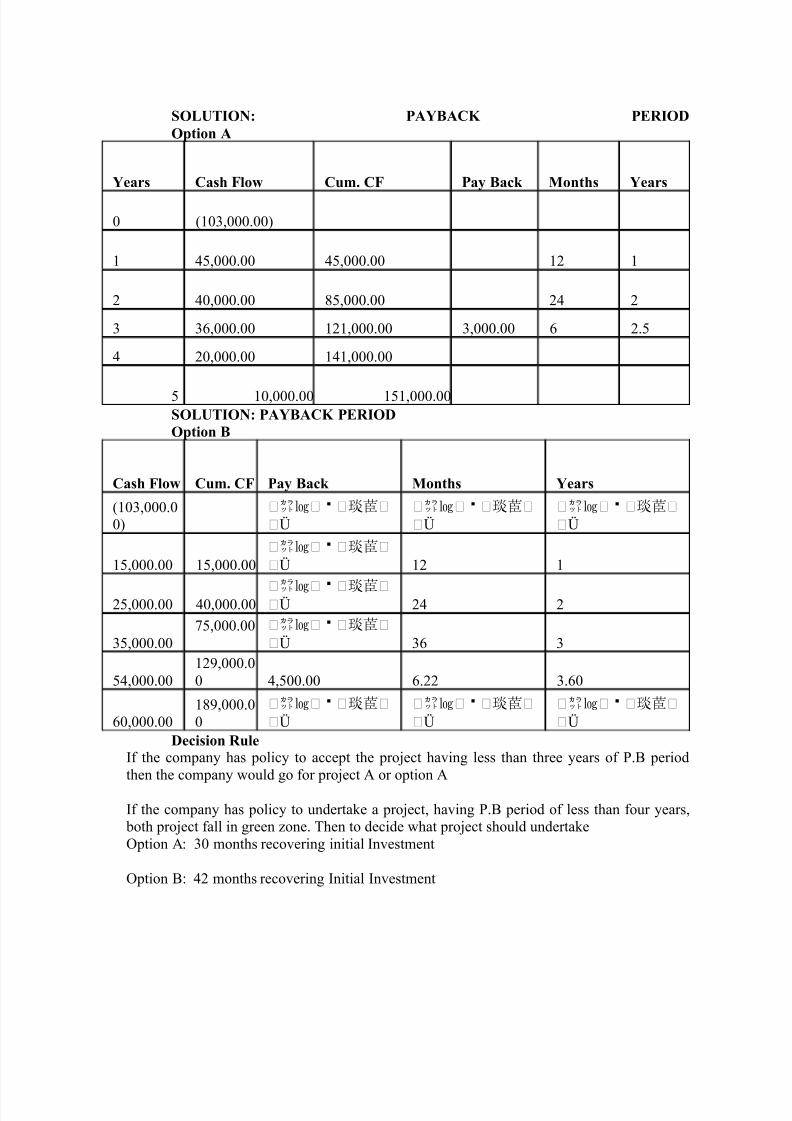

SOLUTION: PAYBACK PERIODOption A

Years Cash Flow Cum. CF Pay Back Months Years

0 (103,000.00)

1 45,000.00 45,000.00 12 1

2 40,000.00 85,000.00 24 2

3 36,000.00 121,000.00 3,000.00 6 2.5

4 20,000.00 141,000.00

5 10,000.00 151,000.00SOLUTION: PAYBACK PERIODOption B

Cash Flow Cum. CF Pay Back Months Years

(103,000.00)

Ü

Ü

Ü

15,000.00 15,000.00Ü 12 1

25,000.00 40,000.00Ü 24 2

35,000.0075,000.00

Ü 36 3

54,000.00129,000.00 4,500.00 6.22 3.60

60,000.00189,000.00

Ü

Ü

Ü

Decision Rule

If the company has policy to accept the project having less than three years of P.B periodthen the company would go for project A or option A

If the company has policy to undertake a project, having P.B period of less than four years, both project fall in green zone. Then to decide what project should undertakeOption A: 30 months recovering initial Investment

Option B: 42 months recovering Initial Investment

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 53/125

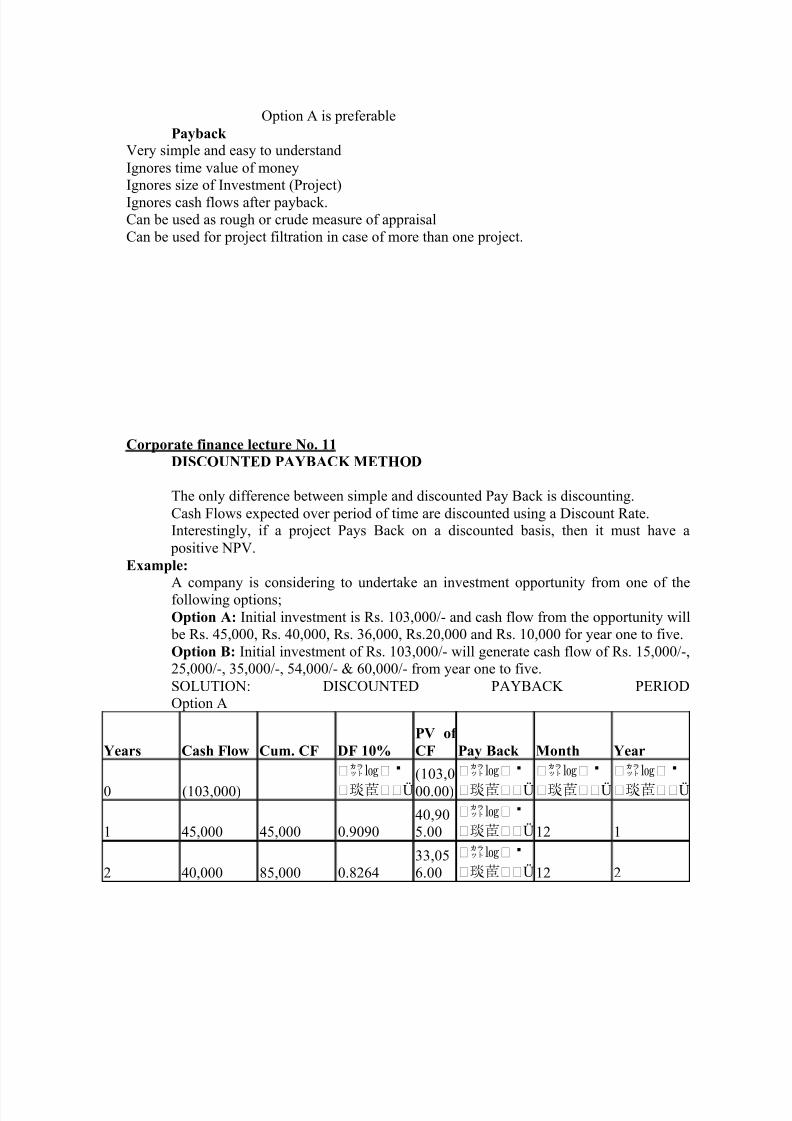

Option A is preferable

Payback Very simple and easy to understandIgnores time value of money

Ignores size of Investment (Project)Ignores cash flows after payback.Can be used as rough or crude measure of appraisalCan be used for project filtration in case of more than one project.

Corporate finance lecture No. 11DISCOUNTED PAYBACK METHOD

The only difference between simple and discounted Pay Back is discounting.Cash Flows expected over period of time are discounted using a Discount Rate.Interestingly, if a project Pays Back on a discounted basis, then it must have a positive NPV.

Example:A company is considering to undertake an investment opportunity from one of thefollowing options;Option A: Initial investment is Rs. 103,000/- and cash flow from the opportunity will be Rs. 45,000, Rs. 40,000, Rs. 36,000, Rs.20,000 and Rs. 10,000 for year one to five.Option B: Initial investment of Rs. 103,000/- will generate cash flow of Rs. 15,000/-,25,000/-, 35,000/-, 54,000/- & 60,000/- from year one to five.SOLUTION: DISCOUNTED PAYBACK PERIODOption A

Years Cash Flow Cum. CF DF 10% PV of CF Pay Back Month Year

0 (103,000)Ü

(103,000.00)

Ü

Ü

Ü

1 45,000 45,000 0.909040,905.00

Ü12 1

2 40,000 85,000 0.826433,056.00

Ü12 2

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 54/125

3 36,000 121,000 0.751327,046.80 12 3

4 20,000 141,000 0.683013,660.00 1,666.67 1.20

Ü

5 10,000 151,000 0.62096,209.00

Ü

Ü

Ü

Ü

Ü

Ü

Ü

17,876.80

Ü37.20

Ü

SOLUTION: DISCOUNTED PAYBACK PERIODOption B

Years Cash Flow Cum. CF DF 10% PV of CF Pay Back Month Year

0 (103,000) 1

Ü

Ü

Ü

Ü

1 15,000 15,000 0.91 13,635.00

Ü 12 1

2 25,000 40,000 0.83 20,660.00

Ü 12 2

3 35,000 75,000 0.75 26,295.50 12 3

4 54,000 129,000 0.68 36,882.00

Ü 12 4

5 60,000 189,000 0.62 37,254.00 5,000.00 1.11

Ü

Ü

Ü

Ü

Ü 17,876.80

Ü 49.1055

Ü

ACCOUNTING RATE OF RETURN ± ARR ALSO AVERAGE ACCOUNTING RATE ± AAR

ARR = Average Net Income/Average Investment

Some Issues relevant to ARR Its Simple and needed information is readily availableIts ignores time value of moneyIts based on book valuesIts not a true appraisal method

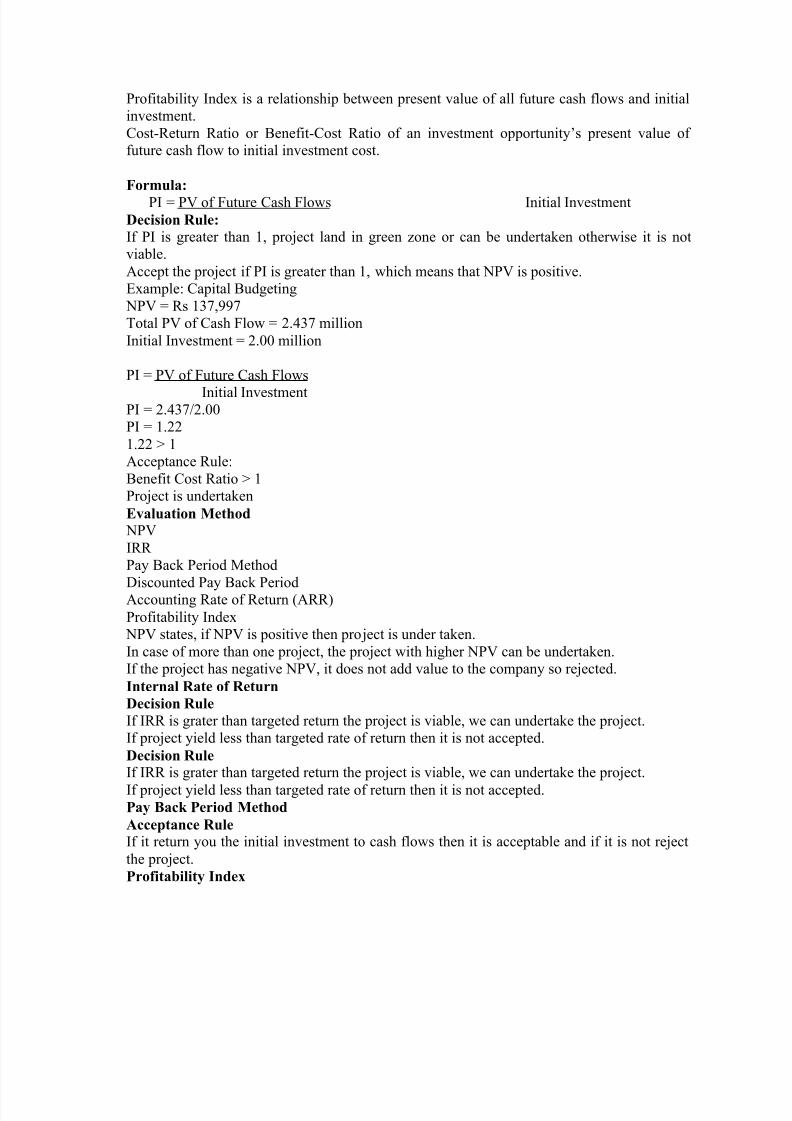

Profitability Index

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 55/125

Profitability Index is a relationship between present value of all future cash flows and initialinvestment.Cost-Return Ratio or Benefit-Cost Ratio of an investment opportunity¶s present value of future cash flow to initial investment cost.

F

ormula:PI = PV of Future Cash Flows Initial InvestmentDecision Rule:If PI is greater than 1, project land in green zone or can be undertaken otherwise it is notviable.Accept the project if PI is greater than 1, which means that NPV is positive.Example: Capital Budgeting NPV = Rs 137,997Total PV of Cash Flow = 2.437 millionInitial Investment = 2.00 million

PI = PV of Future Cash FlowsInitial InvestmentPI = 2.437/2.00PI = 1.221.22 > 1Acceptance Rule:Benefit Cost Ratio > 1Project is undertakenEvaluation Method NPVIRR Pay Back Period MethodDiscounted Pay Back PeriodAccounting Rate of Return (ARR)Profitability Index NPV states, if NPV is positive then project is under taken.In case of more than one project, the project with higher NPV can be undertaken.If the project has negative NPV, it does not add value to the company so rejected.Internal Rate of Return Decision RuleIf IRR is grater than targeted return the project is viable, we can undertake the project.If project yield less than targeted rate of return then it is not accepted.Decision RuleIf IRR is grater than targeted return the project is viable, we can undertake the project.If project yield less than targeted rate of return then it is not accepted.Pay Back Period Method Acceptance RuleIf it return you the initial investment to cash flows then it is acceptable and if it is not rejectthe project.Profitability Index

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 56/125

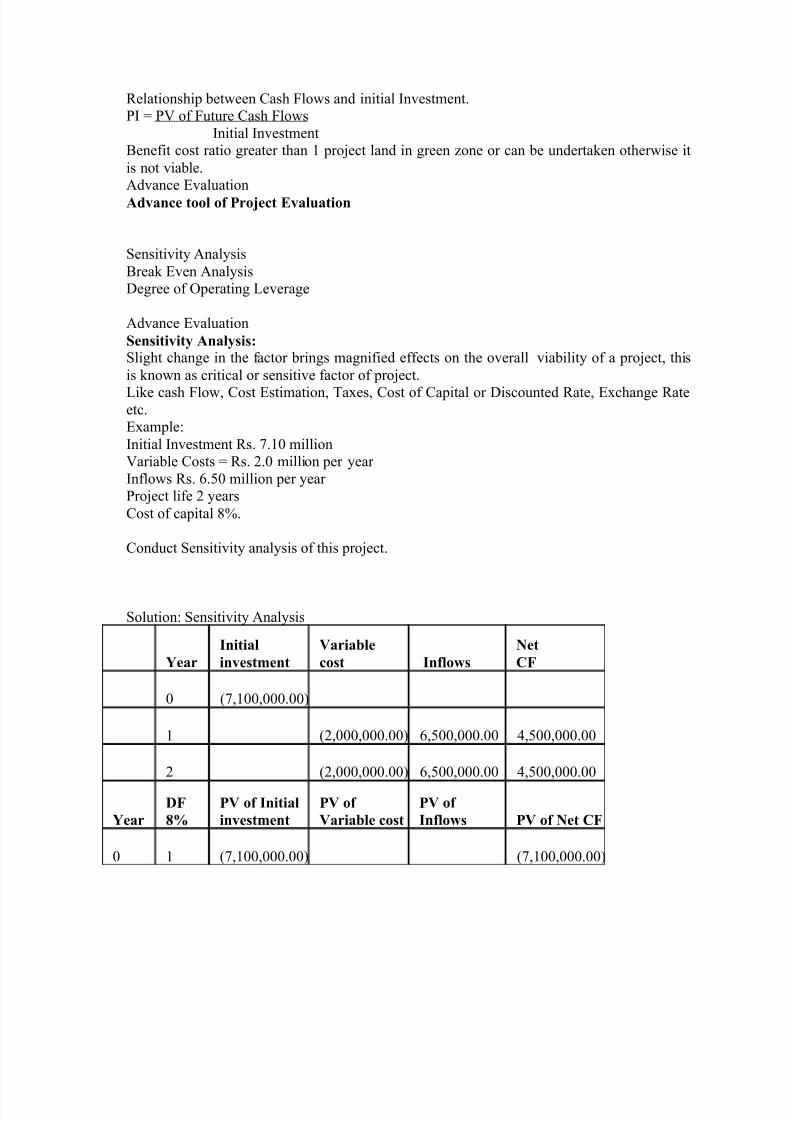

Relationship between Cash Flows and initial Investment.PI = PV of Future Cash Flows

Initial InvestmentBenefit cost ratio greater than 1 project land in green zone or can be undertaken otherwise itis not viable.

Advance EvaluationAdvance tool of Project Evaluation

Sensitivity AnalysisBreak Even AnalysisDegree of Operating Leverage

Advance EvaluationSensitivity Analysis:Slight change in the factor brings magnified effects on the overall viability of a project, this

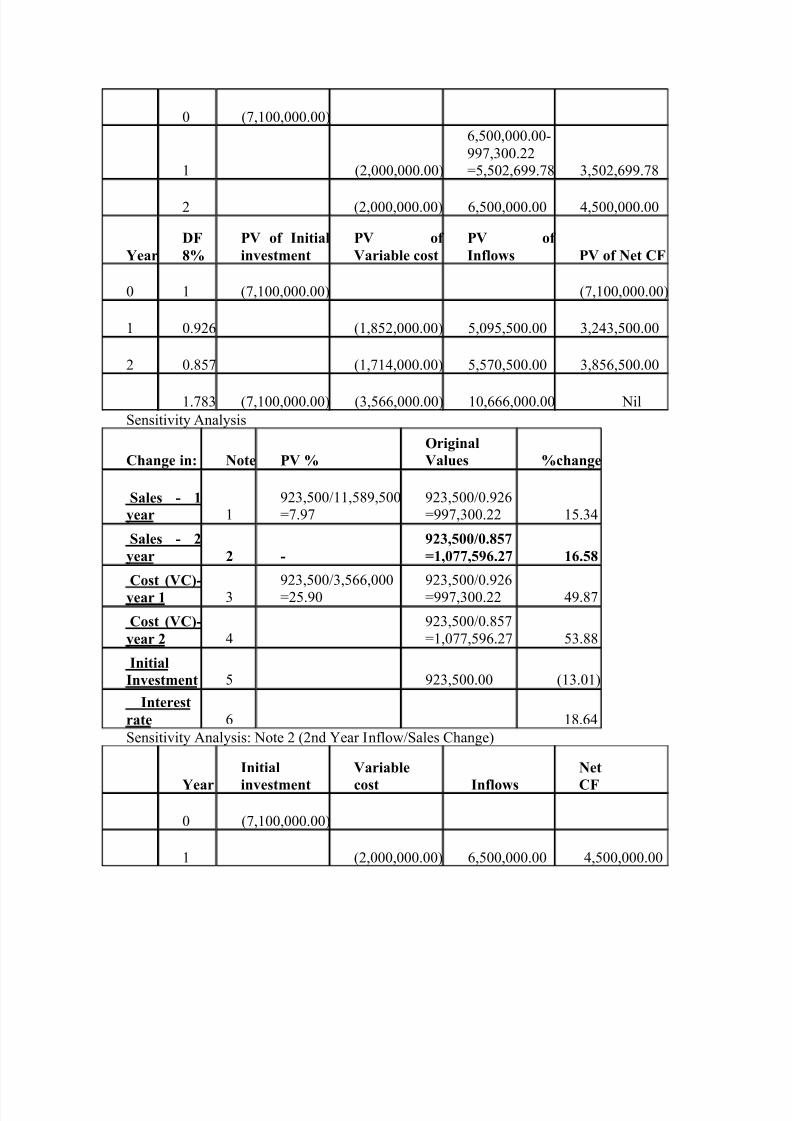

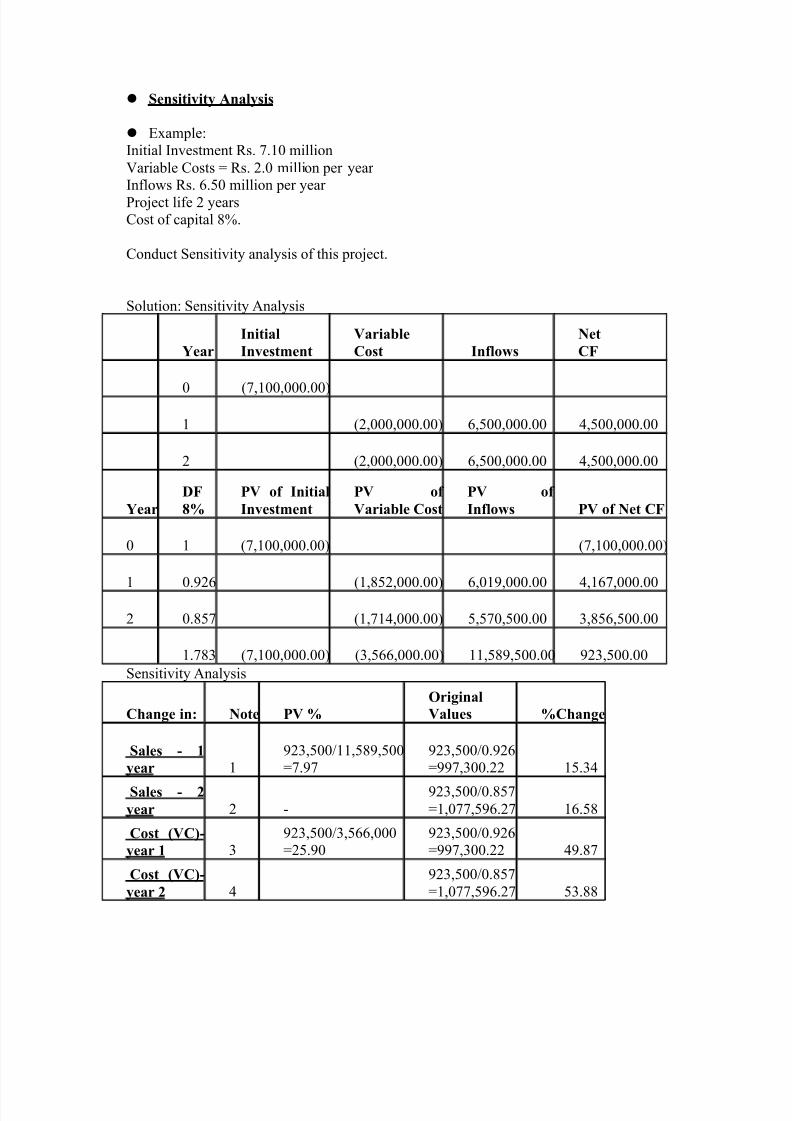

is known as critical or sensitive factor of project.Like cash Flow, Cost Estimation, Taxes, Cost of Capital or Discounted Rate, Exchange Rateetc.Example:Initial Investment Rs. 7.10 millionVariable Costs = Rs. 2.0 million per year Inflows Rs. 6.50 million per year Project life 2 yearsCost of capital 8%.

Conduct Sensitivity analysis of this project.

Solution: Sensitivity Analysis

Year Initialinvestment

Variablecost Inflows

NetCF

0 (7,100,000.00)

1 (2,000,000.00) 6,500,000.00 4,500,000.00

2 (2,000,000.00) 6,500,000.00 4,500,000.00

Year DF 8%

PV of Initialinvestment

PV of Variable cost

PV of Inflows PV of Net CF

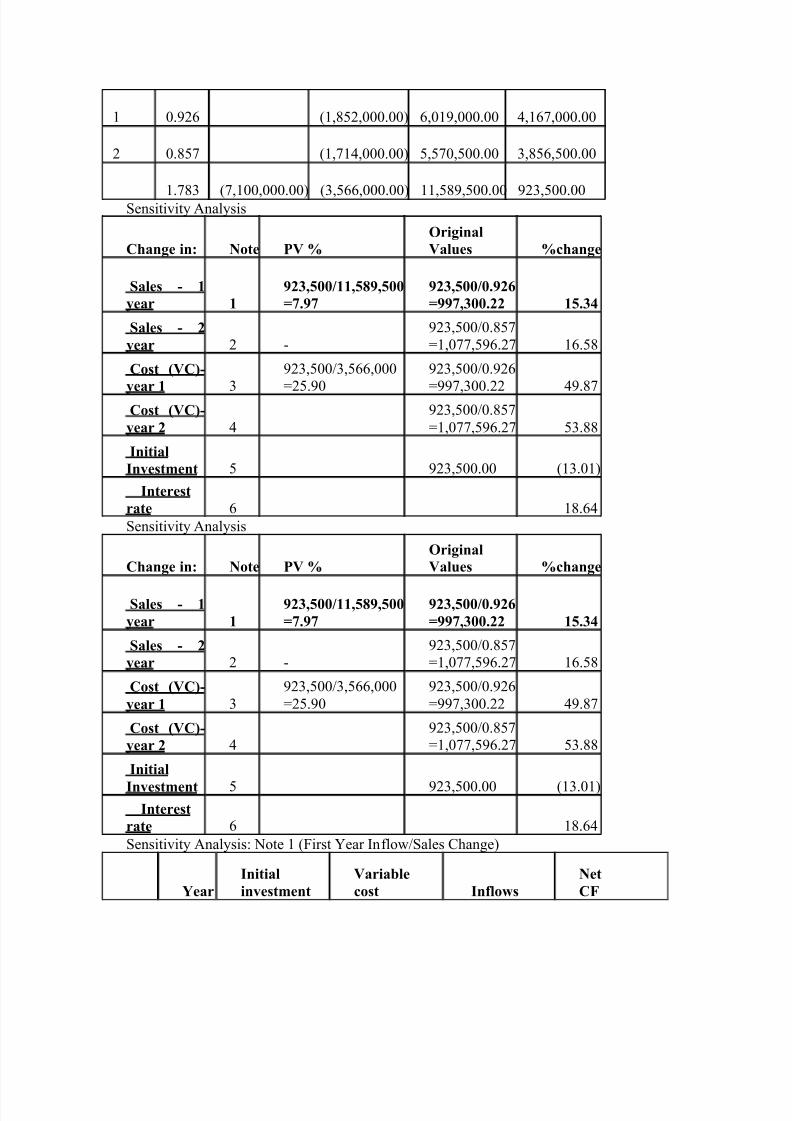

0 1 (7,100,000.00) (7,100,000.00)

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 57/125

1 0.926 (1,852,000.00) 6,019,000.00 4,167,000.00

2 0.857 (1,714,000.00) 5,570,500.00 3,856,500.00

1.783 (7,100,000.00) (3,566,000.00) 11,589,500.00 923,500.00Sensitivity Analysis

Change in: Note PV % OriginalValues %change

Sales - 1year 1

923,500/11,589,500=7.97

923,500/0.926=997,300.22 15.34

Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-

year 1 3

923,500/3,566,000

=25.90

923,500/0.926

=997,300.22 49.87

Cost (VC)-year 2 4

923,500/0.857=1,077,596.27 53.88

InitialInvestment 5 923,500.00 (13.01)

Interestrate 6 18.64Sensitivity Analysis

Change in: Note P

V %

Original

Values %change

Sales - 1year 1

923,500/11,589,500=7.97

923,500/0.926=997,300.22 15.34

Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-year 1 3

923,500/3,566,000=25.90

923,500/0.926=997,300.22 49.87

Cost (VC)-year 2 4

923,500/0.857=1,077,596.27 53.88

InitialInvestment 5 923,500.00 (13.01)

Interestrate 6 18.64Sensitivity Analysis: Note 1 (First Year Inflow/Sales Change)

Year Initialinvestment

Variablecost Inflows

NetCF

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 58/125

0 (7,100,000.00)

1 (2,000,000.00)

6,500,000.00-997,300.22=5,502,699.78 3,502,699.78

2 (2,000,000.00) 6,500,000.00 4,500,000.00

Year DF 8%

PV of Initialinvestment

PV of Variable cost

PV of Inflows PV of Net CF

0 1 (7,100,000.00) (7,100,000.00)

1 0.926 (1,852,000.00) 5,095,500.00 3,243,500.00

2 0.857 (1,714,000.00) 5,570,500.00 3,856,500.00

1.783 (7,100,000.00) (3,566,000.00) 10,666,000.00 NilSensitivity Analysis

Change in: Note PV % OriginalValues %change

Sales - 1year 1

923,500/11,589,500=7.97

923,500/0.926=997,300.22 15.34

Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-year 1 3

923,500/3,566,000=25.90

923,500/0.926=997,300.22 49.87

Cost (VC)-year 2 4

923,500/0.857=1,077,596.27 53.88

InitialInvestment 5 923,500.00 (13.01)

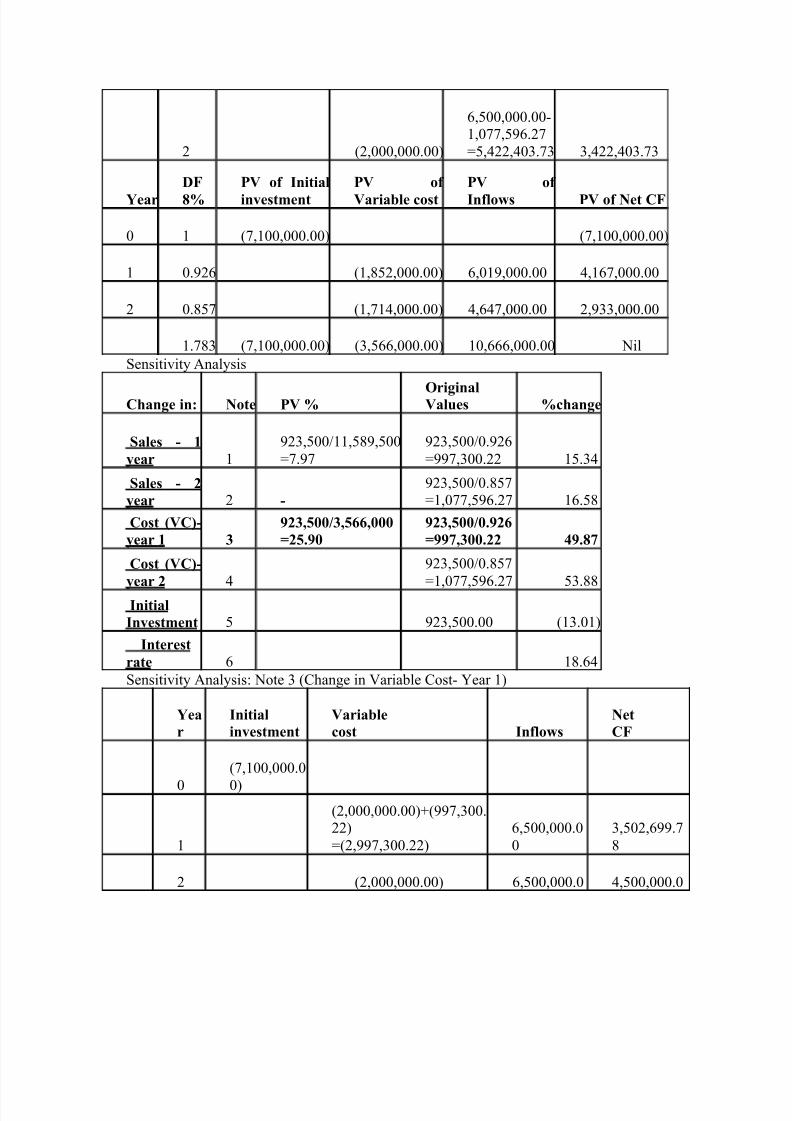

Interestrate 6 18.64Sensitivity Analysis: Note 2 (2nd Year Inflow/Sales Change)

Year Initialinvestment

Variablecost Inflows

NetCF

0 (7,100,000.00)

1 (2,000,000.00) 6,500,000.00 4,500,000.00

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 59/125

2 (2,000,000.00)

6,500,000.00-1,077,596.27=5,422,403.73 3,422,403.73

Year DF 8%

PV of Initialinvestment

PV of Variable cost

PV of Inflows PV of Net CF

0 1 (7,100,000.00) (7,100,000.00)

1 0.926 (1,852,000.00) 6,019,000.00 4,167,000.00

2 0.857 (1,714,000.00) 4,647,000.00 2,933,000.00

1.783 (7,100,000.00) (3,566,000.00) 10,666,000.00 NilSensitivity Analysis

Change in: Note PV % OriginalValues %change

Sales - 1year 1

923,500/11,589,500=7.97

923,500/0.926=997,300.22 15.34

Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-year 1 3

923,500/3,566,000=25.90

923,500/0.926=997,300.22 49.87

Cost (VC)-year 2 4

923,500/0.857=1,077,596.27 53.88

InitialInvestment 5 923,500.00 (13.01)

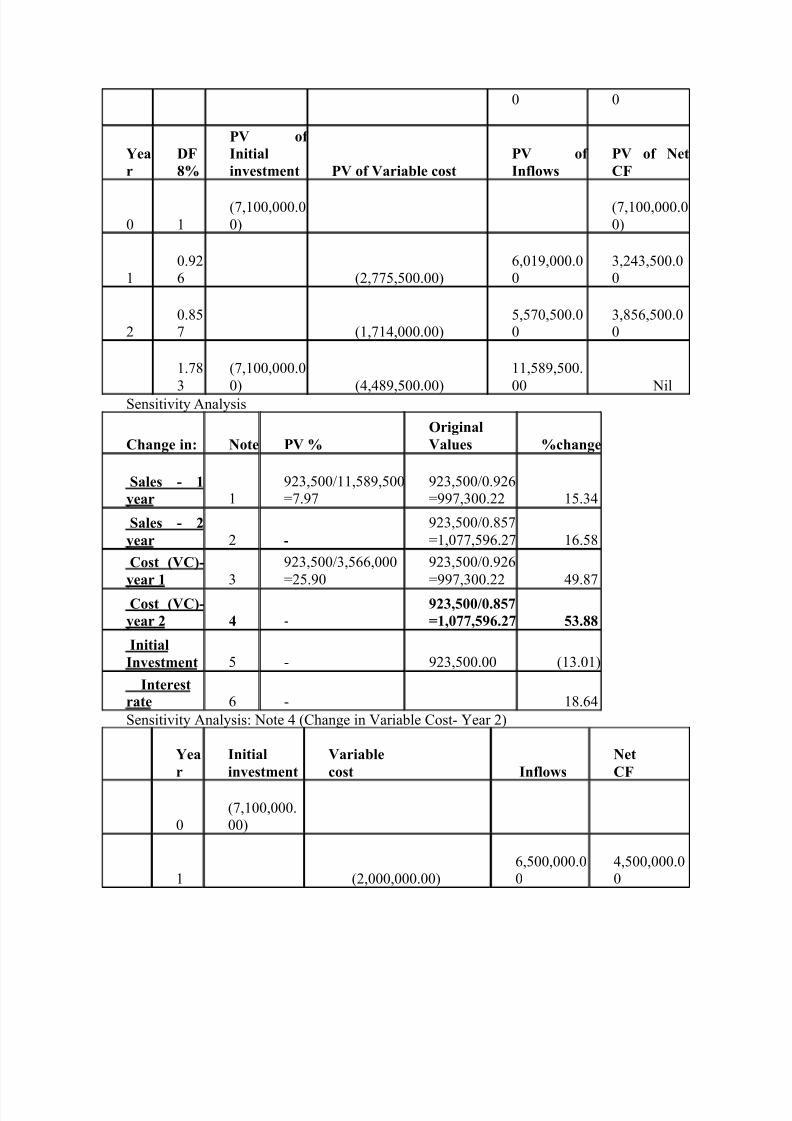

Interestrate 6 18.64Sensitivity Analysis: Note 3 (Change in Variable Cost- Year 1)

Year

Initialinvestment

Variablecost Inflows

NetCF

0(7,100,000.00)

1

(2,000,000.00)+(997,300.22)=(2,997,300.22)

6,500,000.00

3,502,699.78

2 (2,000,000.00) 6,500,000.0 4,500,000.0

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 60/125

0 0

Year

DF 8%

PV of Initialinvestment PV of Variable cost

PV of Inflows

PV of NetCF

0 1(7,100,000.00)

(7,100,000.00)

10.926 (2,775,500.00)

6,019,000.00

3,243,500.00

20.857 (1,714,000.00)

5,570,500.00

3,856,500.00

1.78

3

(7,100,000.0

0) (4,489,500.00)

11,589,500.

00 NilSensitivity Analysis

Change in: Note PV % OriginalValues %change

Sales - 1year 1

923,500/11,589,500=7.97

923,500/0.926=997,300.22 15.34

Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-year 1 3

923,500/3,566,000=25.90

923,500/0.926=997,300.22 49.87

Cost (VC)-year 2 4 -

923,500/0.857=1,077,596.27 53.88

InitialInvestment 5 - 923,500.00 (13.01)

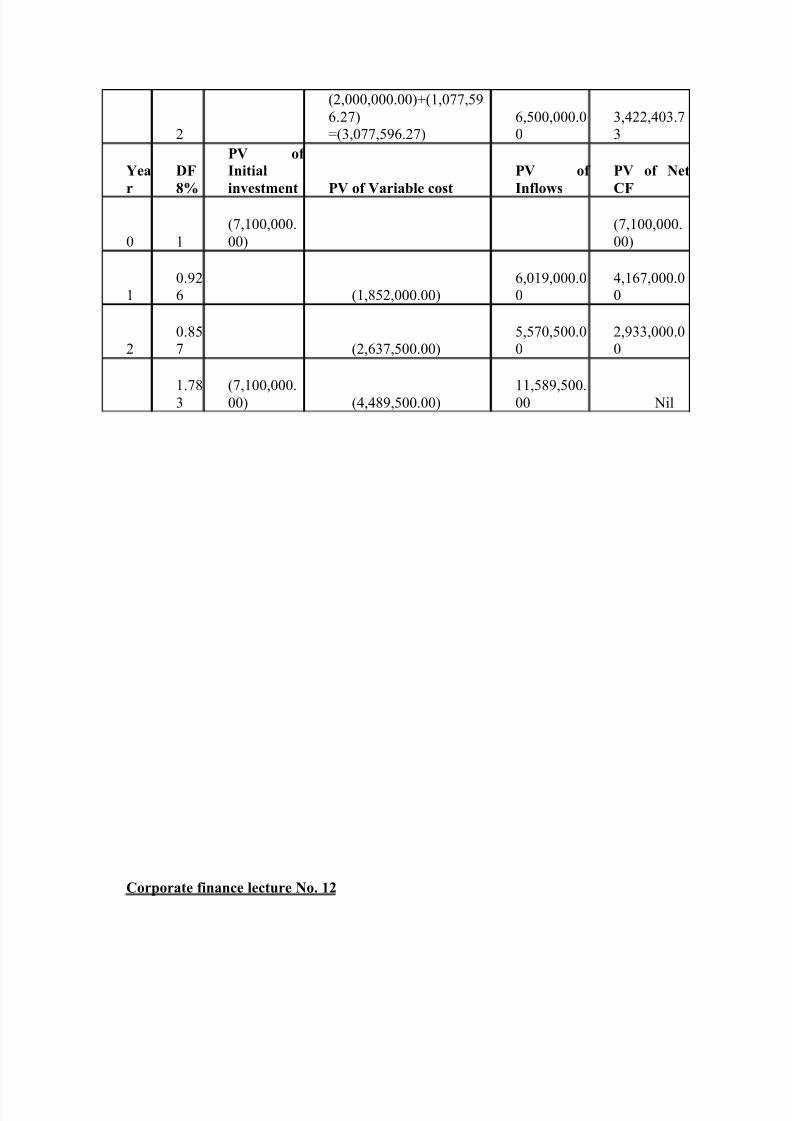

Interestrate 6 - 18.64Sensitivity Analysis: Note 4 (Change in Variable Cost- Year 2)

Year

Initialinvestment

Variablecost Inflows

NetCF

0(7,100,000.00)

1 (2,000,000.00)6,500,000.00

4,500,000.00

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 61/125

2

(2,000,000.00)+(1,077,596.27)=(3,077,596.27)

6,500,000.00

3,422,403.73

Yea

r

DF

8%

PV of Initial

investment PV of Variable cost

PV of

Inflows

PV of Net

CF

0 1(7,100,000.00)

(7,100,000.00)

10.926 (1,852,000.00)

6,019,000.00

4,167,000.00

20.857 (2,637,500.00)

5,570,500.00

2,933,000.00

1.783

(7,100,000.00) (4,489,500.00)

11,589,500.00 Nil

Corporate finance lecture No. 12

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 62/125

Sensitivity Analysis

Example:Initial Investment Rs. 7.10 millionVariable Costs = Rs. 2.0 million per year

Inflows Rs. 6.50 million per year Project life 2 yearsCost of capital 8%.

Conduct Sensitivity analysis of this project.

Solution: Sensitivity Analysis

Year InitialInvestment

VariableCost Inflows

NetCF

0 (7,100,000.00)

1 (2,000,000.00) 6,500,000.00 4,500,000.00

2 (2,000,000.00) 6,500,000.00 4,500,000.00

Year DF 8%

PV of InitialInvestment

PV of Variable Cost

PV of Inflows PV of Net CF

0 1 (7,100,000.00) (7,100,000.00)

1 0.926 (1,852,000.00) 6,019,000.00 4,167,000.00

2 0.857 (1,714,000.00) 5,570,500.00 3,856,500.00

1.783 (7,100,000.00) (3,566,000.00) 11,589,500.00 923,500.00Sensitivity Analysis

Change in: Note PV % OriginalValues %Change

Sales - 1

year 1

923,500/11,589,500

=7.97

923,500/0.926

=997,300.22 15.34Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-year 1 3

923,500/3,566,000=25.90

923,500/0.926=997,300.22 49.87

Cost (VC)-year 2 4

923,500/0.857=1,077,596.27 53.88

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 63/125

InitialInvestment 5 923,500.00 (13.01)

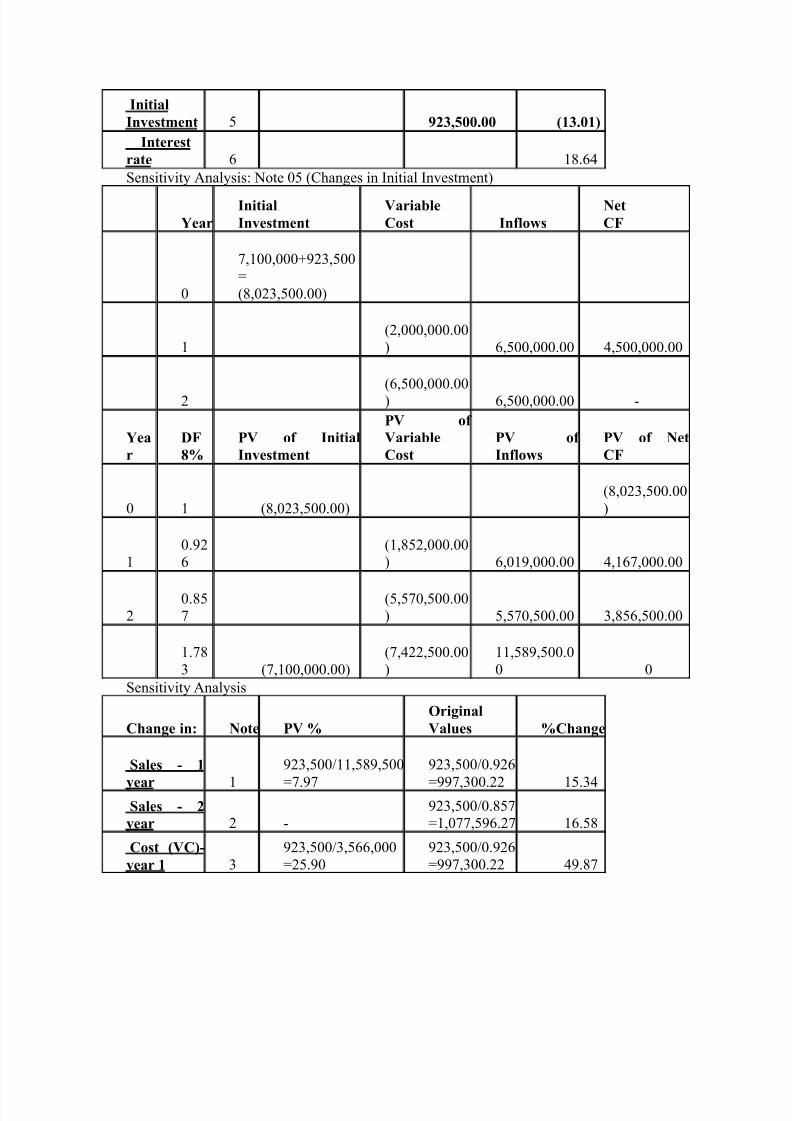

Interestrate 6 18.64Sensitivity Analysis: Note 05 (Changes in Initial Investment)

Year InitialInvestment

VariableCost Inflows

NetCF

0

7,100,000+923,500=(8,023,500.00)

1(2,000,000.00) 6,500,000.00 4,500,000.00

2(6,500,000.00) 6,500,000.00 -

Year

DF 8%

PV of InitialInvestment

PV of VariableCost

PV of Inflows

PV of NetCF

0 1 (8,023,500.00)(8,023,500.00)

10.926

(1,852,000.00) 6,019,000.00 4,167,000.00

20.857

(5,570,500.00) 5,570,500.00 3,856,500.00

1.783 (7,100,000.00)

(7,422,500.00)

11,589,500.00 0

Sensitivity Analysis

Change in: Note PV % OriginalValues %Change

Sales - 1year 1

923,500/11,589,500=7.97

923,500/0.926=997,300.22 15.34

Sales - 2year 2 -

923,500/0.857=1,077,596.27 16.58

Cost (VC)-year 1 3

923,500/3,566,000=25.90

923,500/0.926=997,300.22 49.87

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 64/125

Cost (VC)-year 2 4

923,500/0.857=1,077,596.27 53.88

InitialInvestment 5 923,500.00 (13.01)

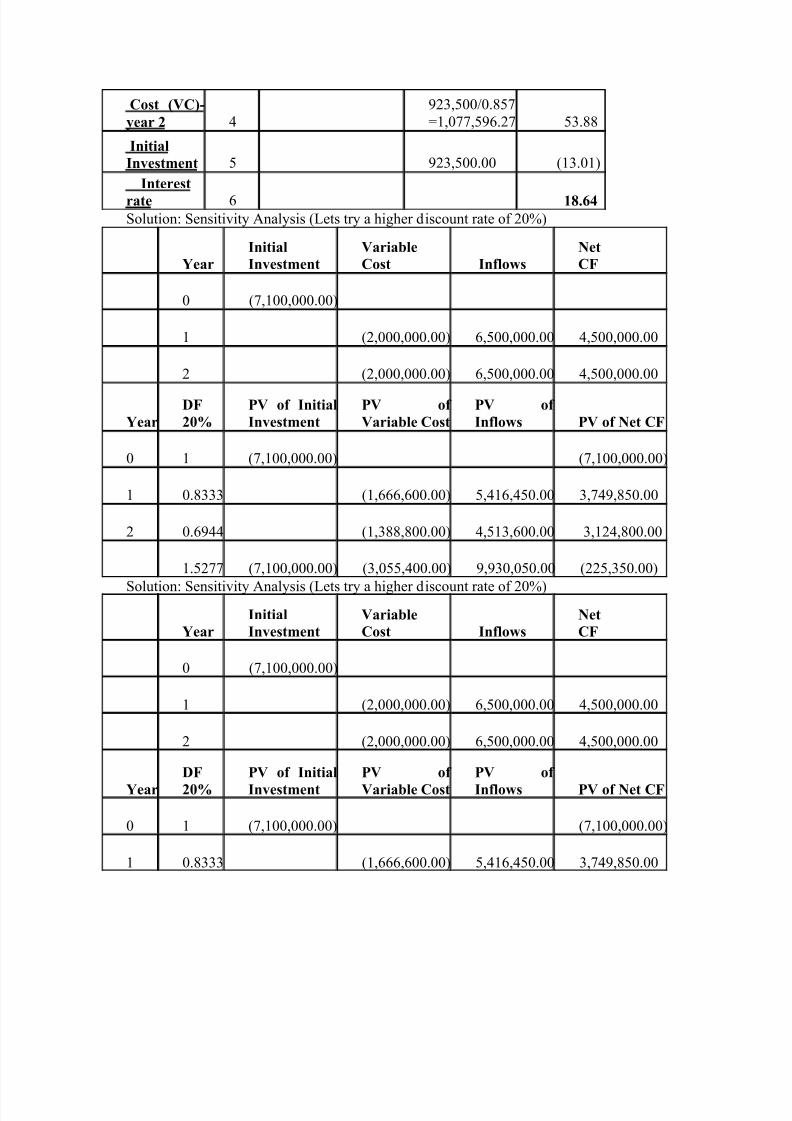

Interestrate 6 18.64Solution: Sensitivity Analysis (Lets try a higher discount rate of 20%)

Year InitialInvestment

VariableCost Inflows

NetCF

0 (7,100,000.00)

1 (2,000,000.00) 6,500,000.00 4,500,000.00

2 (2,000,000.00) 6,500,000.00 4,500,000.00

Year DF 20%

PV of InitialInvestment

PV of Variable Cost

PV of Inflows PV of Net CF

0 1 (7,100,000.00) (7,100,000.00)

1 0.8333 (1,666,600.00) 5,416,450.00 3,749,850.00

2 0.6944 (1,388,800.00) 4,513,600.00 3,124,800.00

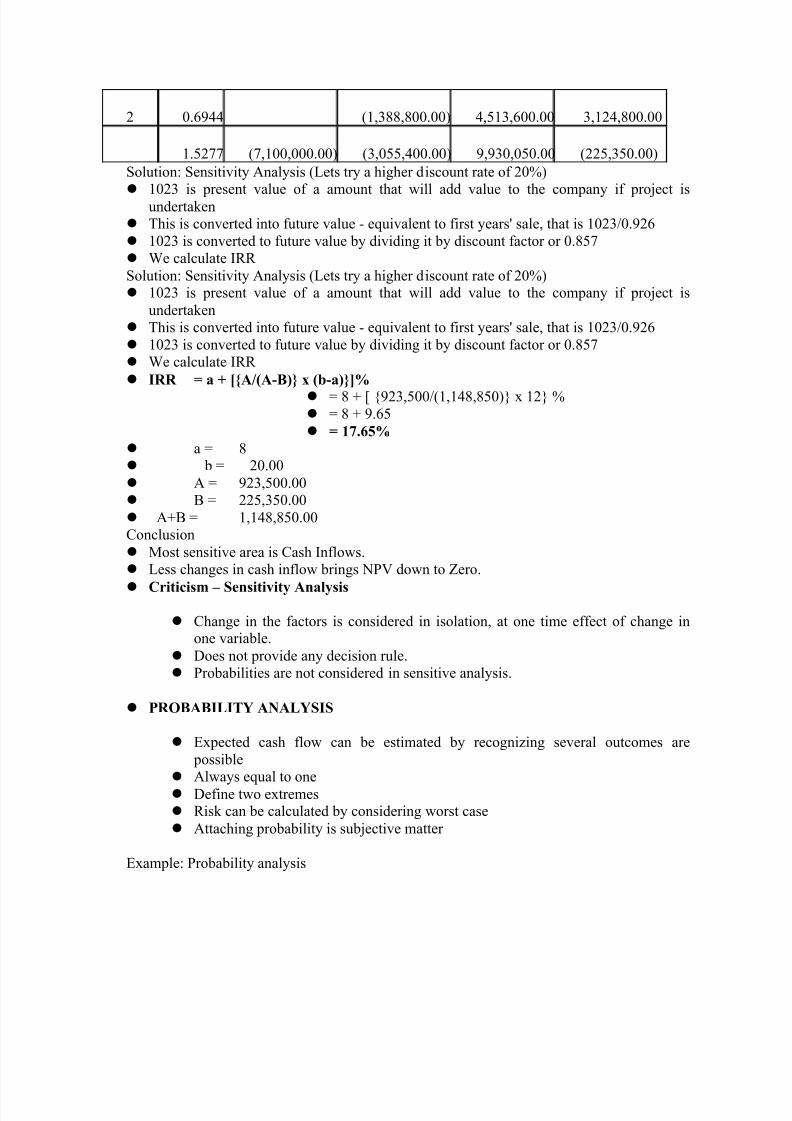

1.5277 (7,100,000.00) (3,055,400.00) 9,930,050.00 (225,350.00)Solution: Sensitivity Analysis (Lets try a higher discount rate of 20%)

Year InitialInvestment

VariableCost Inflows

NetCF

0 (7,100,000.00)

1 (2,000,000.00) 6,500,000.00 4,500,000.00

2 (2,000,000.00) 6,500,000.00 4,500,000.00

Year DF 20%

PV of InitialInvestment

PV of Variable Cost

PV of Inflows PV of Net CF

0 1 (7,100,000.00) (7,100,000.00)

1 0.8333 (1,666,600.00) 5,416,450.00 3,749,850.00

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 65/125

2 0.6944 (1,388,800.00) 4,513,600.00 3,124,800.00

1.5277 (7,100,000.00) (3,055,400.00) 9,930,050.00 (225,350.00)Solution: Sensitivity Analysis (Lets try a higher discount rate of 20%)

1023 is present value of a amount that will add value to the company if project isundertaken This is converted into future value - equivalent to first years' sale, that is 1023/0.926 1023 is converted to future value by dividing it by discount factor or 0.857 We calculate IRR Solution: Sensitivity Analysis (Lets try a higher discount rate of 20%) 1023 is present value of a amount that will add value to the company if project is

undertaken This is converted into future value - equivalent to first years' sale, that is 1023/0.926 1023 is converted to future value by dividing it by discount factor or 0.857 We calculate IRR

IRR = a + [{A/(A-B)} x (b-a)}]% = 8 + [ {923,500/(1,148,850)} x 12} % = 8 + 9.65 = 17.65%

a = 8 b = 20.00 A = 923,500.00 B = 225,350.00 A+B = 1,148,850.00Conclusion Most sensitive area is Cash Inflows.

Less changes in cash inflow brings NPV down to Zero. Criticism ± Sensitivity Analysis

Change in the factors is considered in isolation, at one time effect of change inone variable.

Does not provide any decision rule. Probabilities are not considered in sensitive analysis.

PR OBABILITY ANALYSIS

Expected cash flow can be estimated by recognizing several outcomes are

possible Always equal to one Define two extremes Risk can be calculated by considering worst case Attaching probability is subjective matter

Example: Probability analysis

8/6/2019 Corporate Finance Lecture

http://slidepdf.com/reader/full/corporate-finance-lecture 66/125

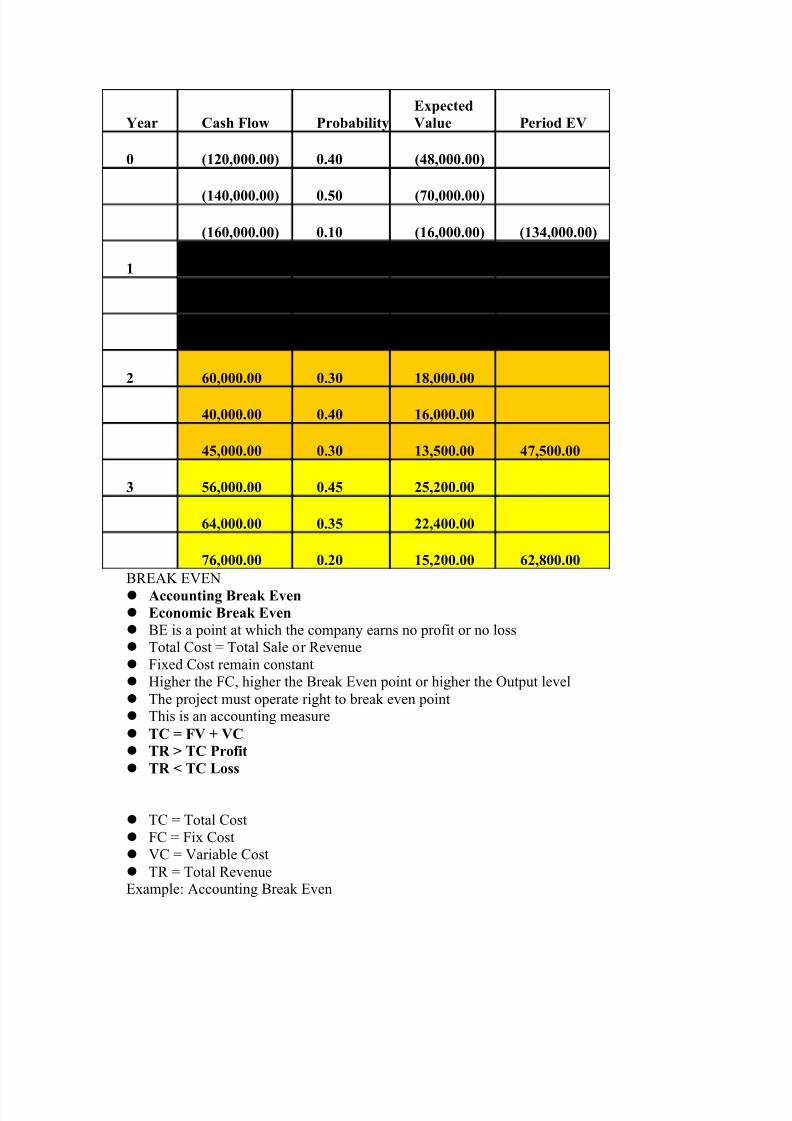

Year Cash Flow Probability ExpectedValue Period EV

0 (120,000.00) 0.40 (48,000.00)

(140,000.00) 0.50 (70,000.00)

(160,000.00) 0.10 (16,000.00) (134,000.00)

1 50,000.00 0.35 17,500.00

60,000.00 0.40 24,000.00

70,000.00 0.25 17,500.00 59,000.00

2 60,000.00 0.30 18,000.00

40,000.00 0.40 16,000.00

45,000.00 0.30 13,500.00 47,500.00

3 56,000.00 0.45 25,200.00

64,000.00 0.35 22,400.00

76,000.00 0.20 15,200.00 62,800.00

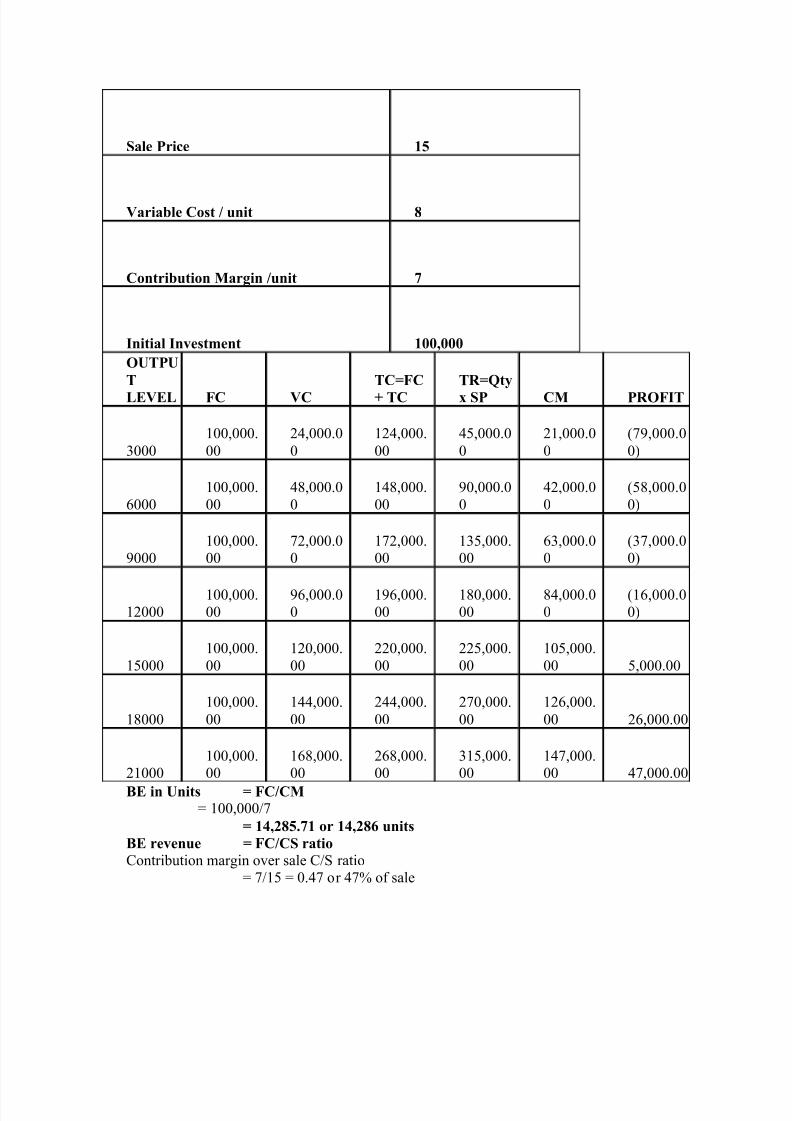

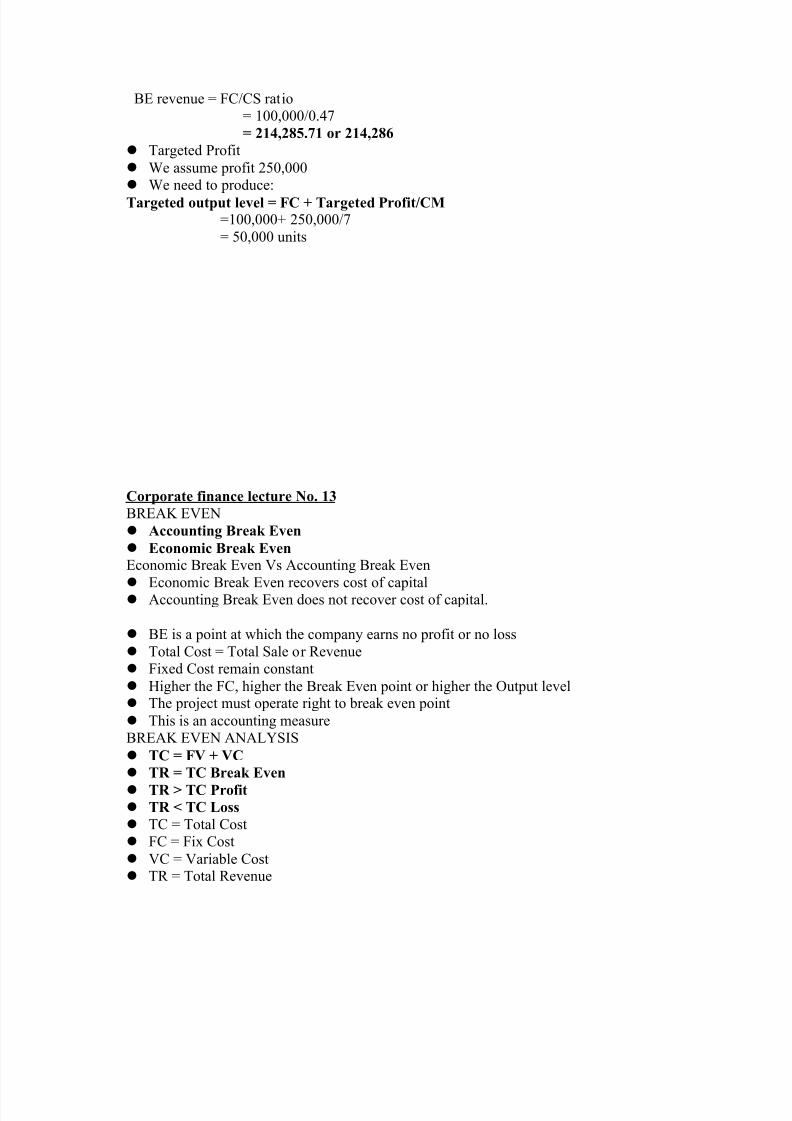

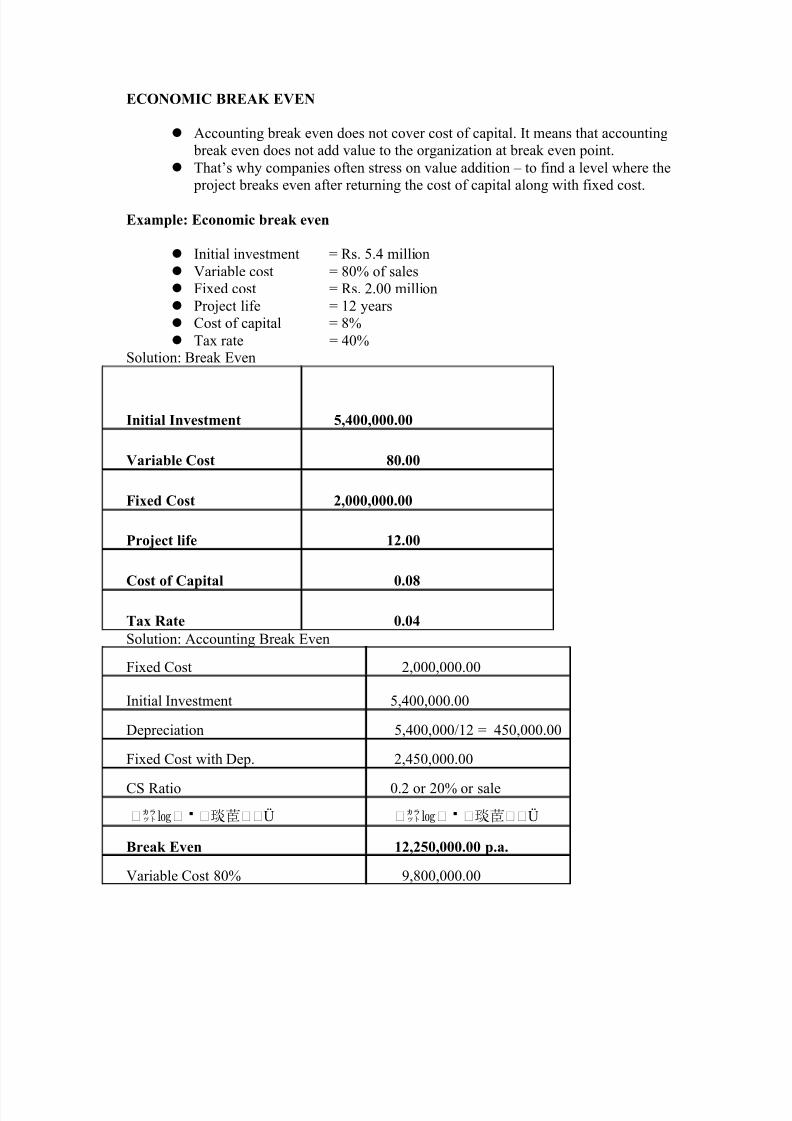

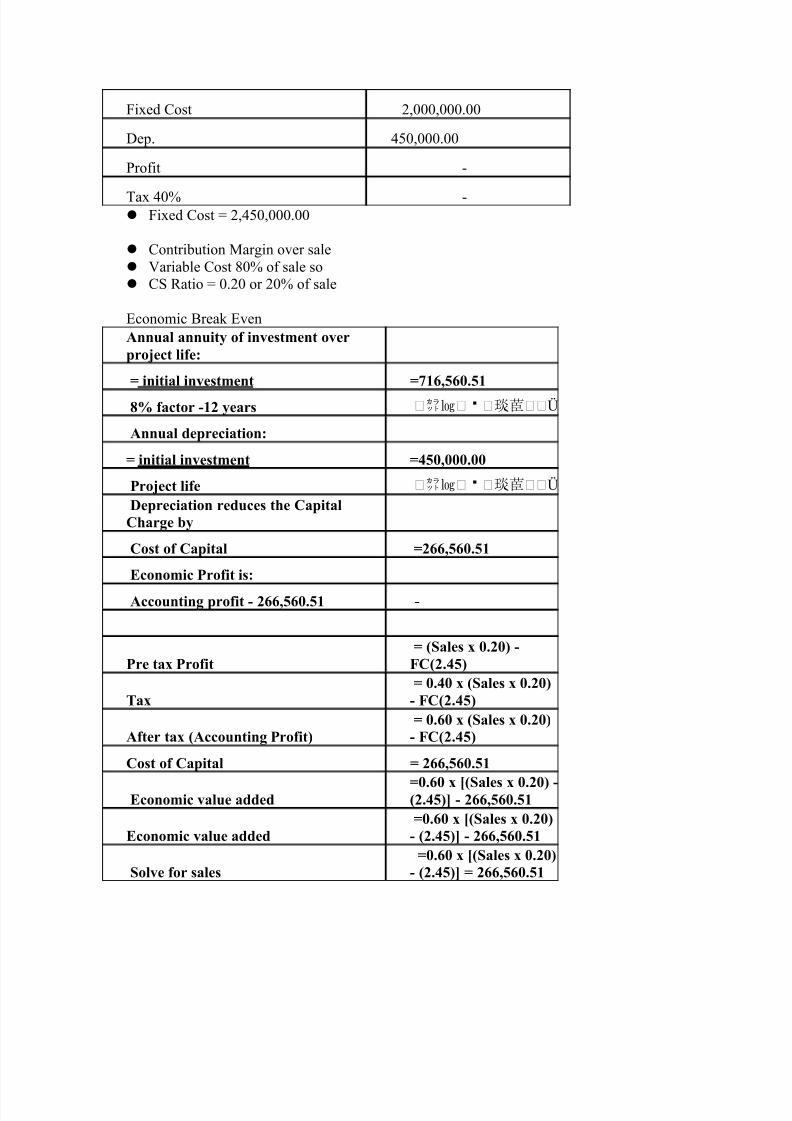

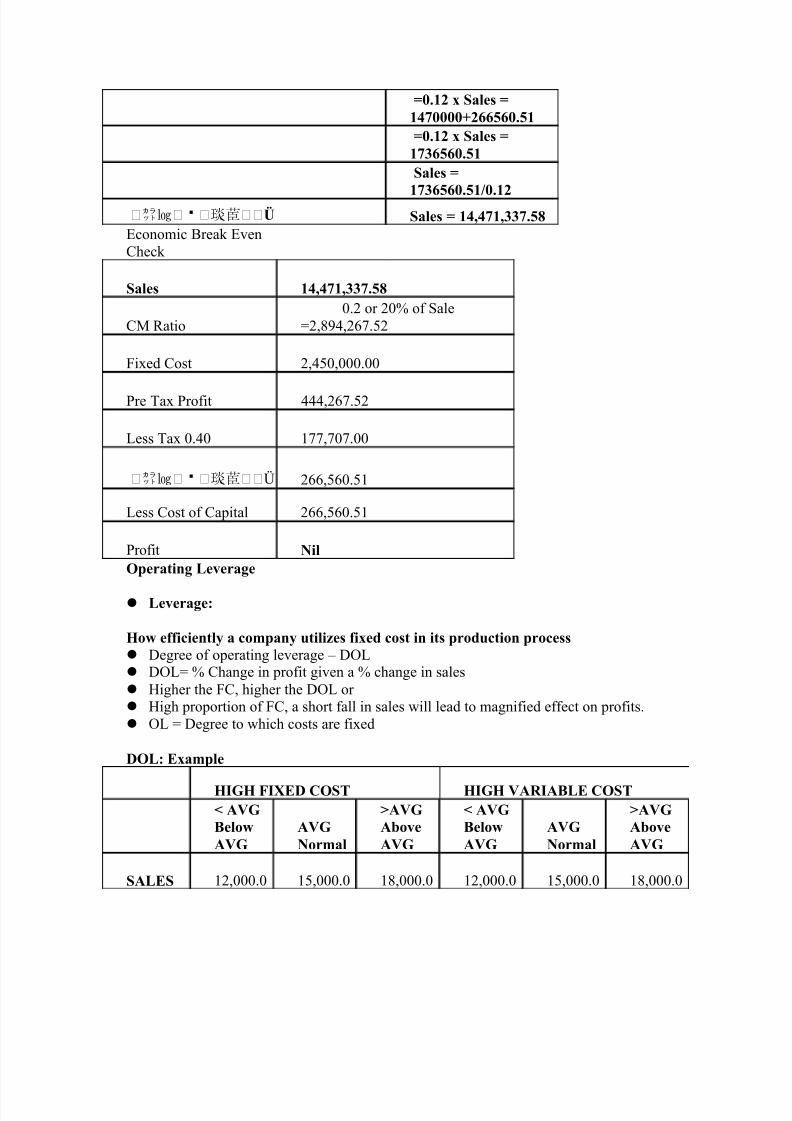

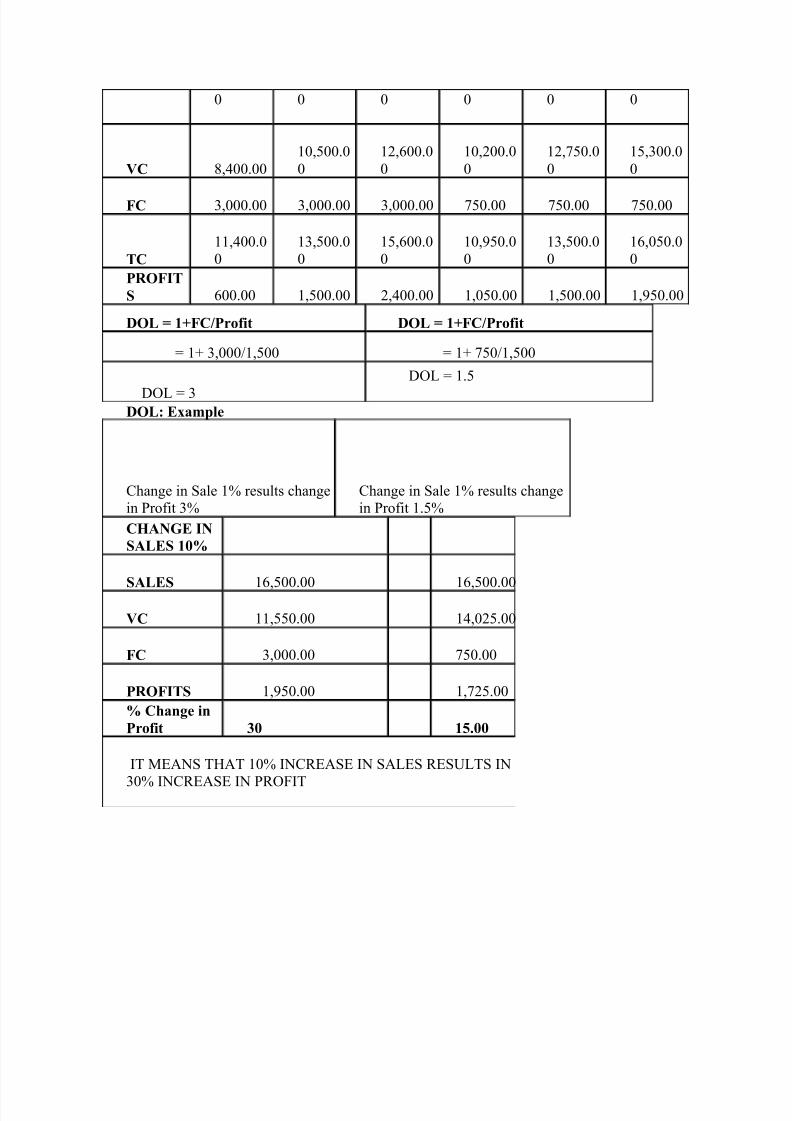

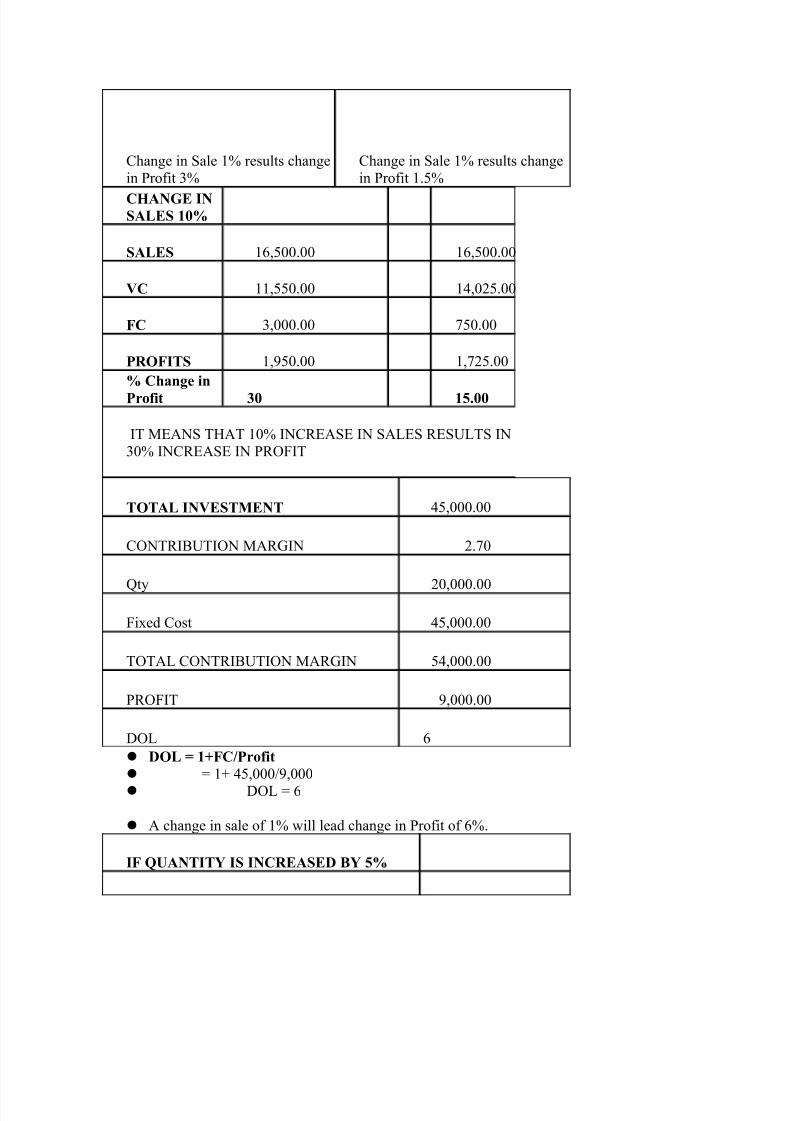

BREAK EVEN Accounting Break Even Economic Break Even BE is a point at which the company earns no profit or no loss Total Cost = Total Sale or Revenue Fixed Cost remain constant Higher the FC, higher the Break Even point or higher the Output level The project must operate right to break even point This is an accounting measure TC = FV + VC TR > TC Profit

TR < TC Loss