Embed Size (px)

DESCRIPTION

Corporate Governance and Family-Owned Businesses. Professor Chris Pierce Bahrain February 2010. What are family owned businesses?. There are different definitions……… Family owned businesses are companies … … where the dominant shareholder is a family member ( broad view ) - PowerPoint PPT Presentation

Citation preview

PROFESSOR CHRIS PIERCEBAHRAIN

FEBRUARY 2010

Corporate Governance and Family-Owned Businesses

1

What are family owned businesses?

There are different definitions………

Family owned businesses are companies …

… where the dominant shareholder is a family member (broad view)

… which are run by heirs of the people previously in charge, or by families that are clearly in the process of transferring control to heirs (narrow view)

2

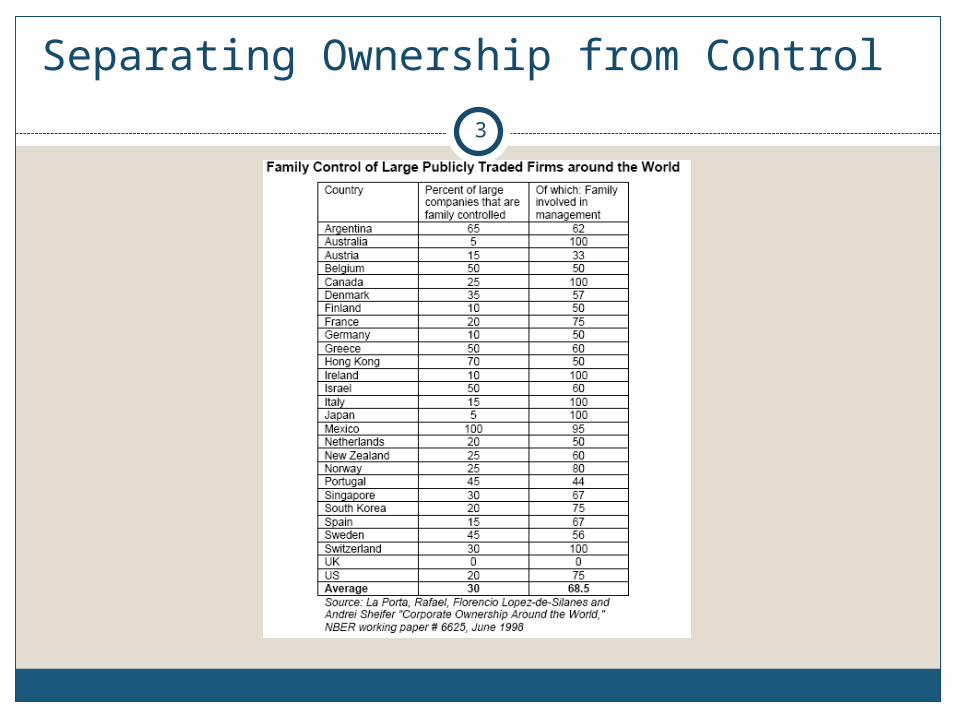

Separating Ownership from Control

3

Non Listed Businesses

“Family businesses constitute more than 85% of non listed businesses in the MENA region.”

Pierce (2008) Corporate Governance in MENA

“Family businesses constitute more than 85% of non listed businesses in the EU.”

Pierce (2010) Corporate Governance in the European Union

4

Listed Companies

“The top 5 families had 17% of the total board seats on listed companies in the UAE.”

Pierce (2008) Corporate Governance in MENA

“One third of all companies in the S & P 500 index and 40 % of the 250 largest

companies in France and Germany are family businesses.”

McKinsey, January 2010

5

Strengths of family owned businesses

Strong set of values: Identity

Long-term view in decision-making: Consistency

Possibility of unconventional strategy: Flexibility

Desire to build a business for future generations: Sustainability

Commitment of family management to their company: Continuity

6

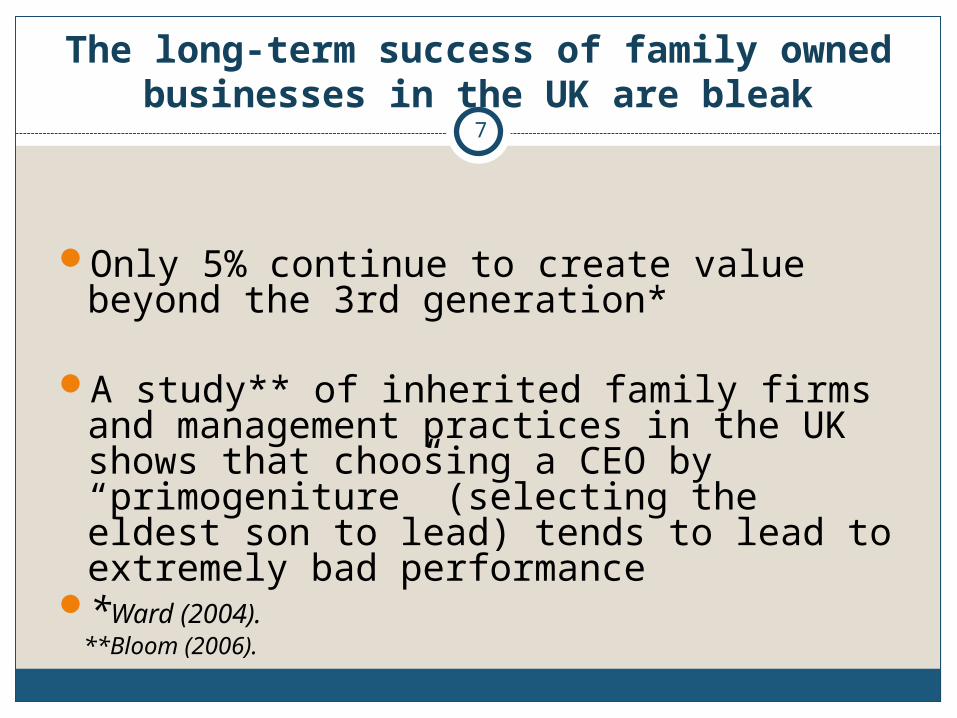

The long-term success of family owned businesses in the UK are bleak

Only 5% continue to create value beyond the 3rd generation*

A study** of inherited family firms and management practices in the UK shows that choosing a CEO by “primogeniture” (selecting the eldest son to lead) tends to lead to extremely bad performance

*Ward (2004). **Bloom (2006).

7

Key Success Factors for FOEs: Define Relationships and Structures within Family and with Outside

Stakeholders

Create clarity of roles within the familyCreate fair playing field for non-family

membersFair treatment of outside financial

stakeholders

8

Create clarity of roles within the family

Family constitution Family values, philosophy, principles and beliefs Family code of conduct Family Assembly / Forums Family Councils Family Advisory Board Family’s long-term role as shareholder (share

retention/voting) Family salary-earners vs. dividend receivers Self dealing and conflict of interest policies Strategy for philanthropy and third party foundations Family training and education strategy Family employment committee Wealth management and other family services

9

Create fair playing field for non-family members

Succession planning clear from the startFamily employment policyEquality of opportunity in recruitment

and promotionIncentives for non-family managers

10

Fair treatment of outside financial stakeholders

Shareholder agreements Legal structures and tax planning Disclosure of information Rights to information Voting rights at AGM Control enhancing mechanisms

11

Key Success Factors for FOEs: Set Formal Corporate Governance Structure

Formalities - They Really Do Matter! Clarify roles and responsibilities between board, management and

shareholders Codify structures and processes for all to see

Create strong Advisory Board Guarantees non-compromising standards of meritocracy in

personnel decisions Allows clear lines of authority for different areas of business Ensures the stability and continuity of family policies and values Distinction made between matters of day-to-day mgmt. and

strategy Allows strategic issues to be properly & objectively addressed

Nominate outside directors To complement the family’s business skills with the fresh strategic

perspectives Infusion of new ideas due to a broader range of expertise Ensure equal treatment between family and non-family executives

12

Why List?

Providing a main source of funding

Creating opportunities for the company to finance new investments

Expected future appreciation in the company’s share price and the value of the company

Helping the company to expand domestically and internationally

Sustainability of family owned business

13

Benefits associated with Growth Generated Through Retained Earnings

Maintain full control

Keep core values

Quick decision-making and ability to experiment

Keep balance between profit and commitment to quality and innovation

No restrictions on how to use capital

14

Disadvantages associated with growth generated through retained earnings

Limited access to finance

Slower growth

Absence of external discipline (strategic decision-making and oversight)

15

Benefits associated with growth generated through private equity

Strengthens capital structure Fewer restrictions on how funds are used than public

listing No scheduled (fixed) repayment (dividends can be deferred

and cash can be utilised to address business needs)

Enhances credibility with stakeholders

Introduces private equity culture Strategic input into the direction of the business by

investor Access to a broader network of contacts Increased financial management controls and reporting

16

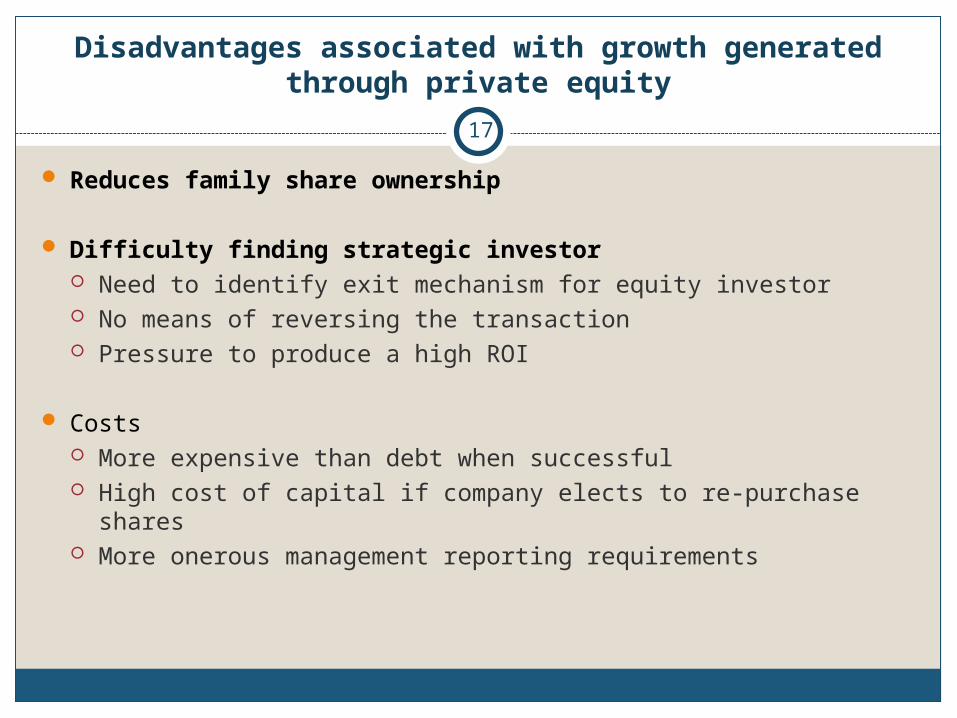

Disadvantages associated with growth generated through private equity

Reduces family share ownership

Difficulty finding strategic investor Need to identify exit mechanism for equity investor No means of reversing the transaction Pressure to produce a high ROI

Costs More expensive than debt when successful High cost of capital if company elects to re-purchase shares More onerous management reporting requirements

17

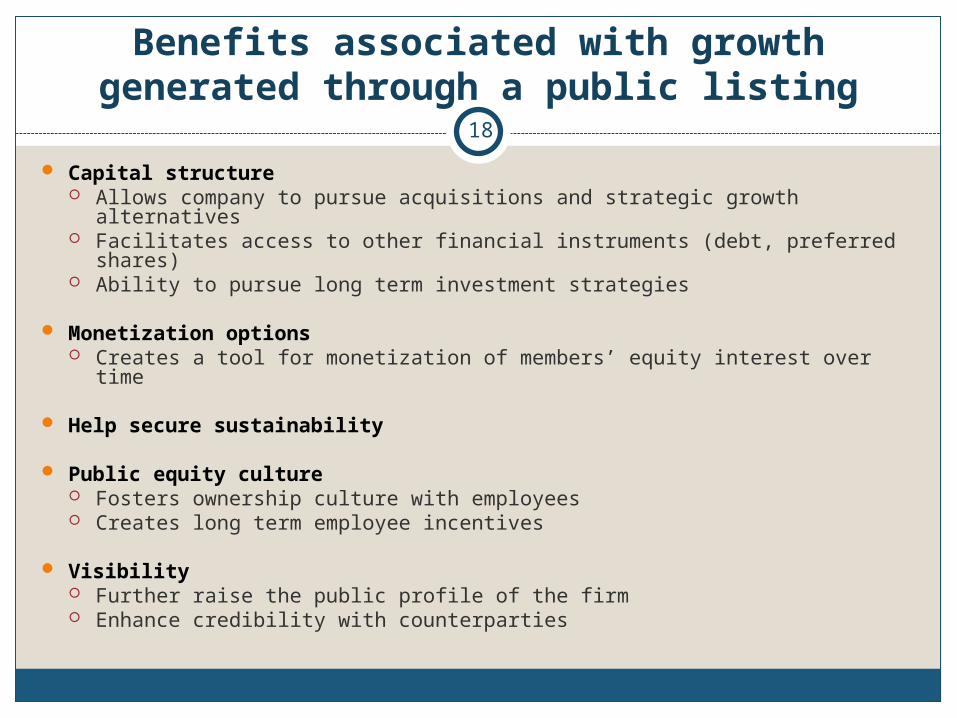

Benefits associated with growth generated through a public listing

Capital structure Allows company to pursue acquisitions and strategic growth alternatives Facilitates access to other financial instruments (debt, preferred shares) Ability to pursue long term investment strategies

Monetization options Creates a tool for monetization of members’ equity interest over time

Help secure sustainability

Public equity culture Fosters ownership culture with employees Creates long term employee incentives

Visibility Further raise the public profile of the firm Enhance credibility with counterparties

18

Disadvantages associated with growth generated through a public listing

Reduces family share ownership

Legal & regulatory compliance Initial and ongoing compliance with disclosure regimes can be a

burden

Increased public scrutiny Financial and organizational details disclosed to the public Public reaction may contribute to stock price volatility

Public shareholder base Public shareholder base requires time, attention and information Risk of adversarial shareholder base Potentially less say over operation of the business and strategic

goals

19

A Roadmap for Smooth Progression

Create a three to five-member transitional Advisory Board

Appoint a Corporate Secretary

Develop the company’s organic documents (by-laws and charter)

2

Strive for full compliance with Listing rules and regulations

Non Listed Listed

Strengthen Disclosure & Control Environment

Protect Rights of Shareholder & Stakeholders

Formalize. Create Advisory

Board

Transition to Board of Directors

1 3 4

Formalize the Advisory Board to be a real Board of Directors

Appoint a professional CEO

Define roles and set responsibilities

Form an audit committee, with non-executive members

Form an independent Audit Committee

Form Governance, Nominations and/or Remuneration Comm.

Develop, adopt, and publicly disclose a written corporate governance policy

Establish risk mgmt. internal control & audit

Keep an eye on these rules and regulations from day 1

20

Specific Challenges for FOEs

Need to distinguish family and company relationships Dissensions between family members who are actively working and those who are

not Financial relationships

Informality of governance policies “Common” understandings not universally held or understood by outsider (or

insiders!)

Weakness of control environment Founder is still is on top of everything …

Managing growth: More complex with succeeding generation Owner / manager equation shifts Growing number of non-family managers require formal system Incentivising non-family managers

Succession Who from the next generation is up for the challenge … do they have the same

drive?

21

Challenges: Overlapping Roles andResponsibilities

Familymember

Manager

Owner Director

22

Conclusions

For the family-owned business, good governance makes all the difference.

Family firms with effective governance practices are more likely to do strategic planning and to do succession planning.

On average, they grow faster and live longer.

23

We must not be managers. We must be experts in corporate

governance.*

*Source: A fourth-generation family leader

24

A Self-Assessment and Client Orientation Tool25

1. 1. AcceptableAcceptable

2. Extra 2. Extra StepsSteps

3. Major 3. Major ContributionContribution

ss4. 4.

LeadershipLeadership

Commitment to Commitment to Good Corporate Good Corporate GovernanceGovernance

Structure and Structure and Functioning of the Functioning of the Board of DirectorsBoard of Directors

Control Control Environment and Environment and ProcessesProcesses

Transparency and Transparency and DisclosureDisclosure

Treatment of Treatment of Minority Minority ShareholdersShareholders

LEVELS

AT

TR

IBU

TE

S

PROGRESSION

Attribute 1: Commitment to Good Corporate Governance

26

LEVEL 1LEVEL 1Understanding the Understanding the

need to need to professionalize professionalize the Companythe Company

LEVEL 2LEVEL 2First concrete steps First concrete steps

toward best toward best practicespractices

LEVEL 3LEVEL 3Implementation of Implementation of

best practicesbest practices

LEVEL 4LEVEL 4LeadershipLeadership

The basic The basic formalities of formalities of corporate corporate governance are in governance are in place including a place including a (i) Board of (i) Board of Directors, (ii) Directors, (ii) Annual Annual Shareholders Shareholders meeting and (ii) meeting and (ii) Shareholders Shareholders identified and identified and recorded. recorded.

Board member or Board member or high-level high-level executive executive explicitly charged explicitly charged with responsibility with responsibility for improving for improving corporate corporate governance governance practices. practices.

Written policies Written policies established established addressing key addressing key elements in family elements in family firm governance, firm governance, including (i) including (i) succession succession planning; (ii) planning; (ii) human resources human resources and family-and family-member member employment; and employment; and (iii) non-family-(iii) non-family-member share member share ownership. ownership.

Management/Management/Board approves Board approves annual calendar of annual calendar of corporate events. corporate events.

Corporate Corporate Governance policy Governance policy covers (i) role of covers (i) role of Board vis-à-vis Board vis-à-vis management; and management; and (ii) long-term (ii) long-term planning for planning for corporate corporate governance of governance of company company commensurate commensurate with business with business plan. plan.

Applicable Applicable corporate corporate governance, governance, accounting, accounting, auditing and auditing and internal controls, internal controls, and shareholder and shareholder information information practices are practices are equivalent to equivalent to those in place at those in place at best practice best practice public companies public companies (i.e., little would (i.e., little would needed to make needed to make an IPO). an IPO).

Company fully Company fully complies with all complies with all applicable applicable provisions of provisions of voluntary code of voluntary code of best practices of best practices of the country the country

A. C

OM

MIT

ME

NT

TO

CO

RP

OR

AT

E G

OV

ER

NA

NC

E

Attribute 2: Structure and Functioning of the Board

27

LEVEL 1LEVEL 1Understanding Understanding

the need to the need to professionalize professionalize the Companythe Company

LEVEL 2LEVEL 2First concrete steps First concrete steps

toward best practicestoward best practices

LEVEL 3LEVEL 3Implementation of Implementation of

best practicesbest practices

LEVEL 4LEVEL 4LeadershipLeadership

Board of Board of Directors Directors constituted constituted and meets and meets periodicallyperiodically

Board meetings held Board meetings held according to a regular according to a regular schedule, agenda schedule, agenda prepared in advance, prepared in advance, minutes prepared and minutes prepared and approved. approved.

Non-family members Non-family members (probably company (probably company executives or ex-executives or ex-executives) appointed executives) appointed to the Board and core to the Board and core competency (skill competency (skill mix) review of Board mix) review of Board conducted, or conducted, or advisory Board of advisory Board of independent independent professionals professionals established and established and consulted on a consulted on a regular basis. regular basis.

Board composition Board composition (competencies/skil(competencies/skill mix) adequate to l mix) adequate to oversight duties. oversight duties.

Annual evaluation Annual evaluation conducted. conducted.

Audit Committee Audit Committee of non-Executive of non-Executive Directors Directors established. established.

Directors Directors independent of independent of management and management and owners appointed owners appointed to the Board to the Board (perhaps (perhaps “graduated” from “graduated” from the advisory the advisory Board). Board).

Audit committee Audit committee composed entirely composed entirely of independent of independent directors. directors.

Nominating Nominating Committee Committee established. established.

B. S

TR

UC

TU

RE

AN

D F

UN

CT

ION

ING

OF

TH

E B

OA

RD

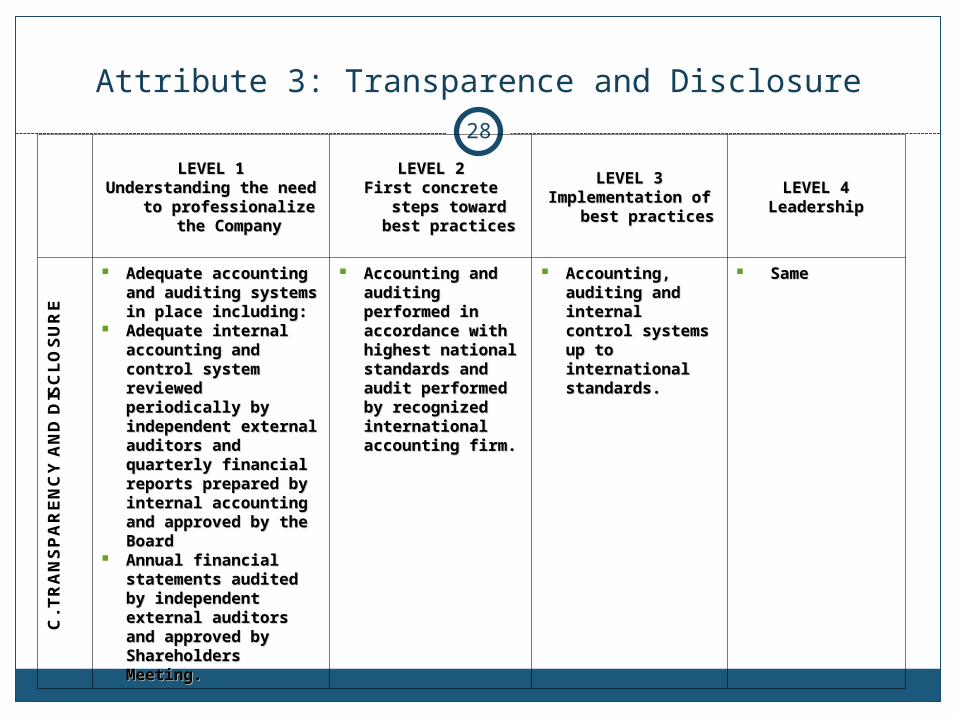

Attribute 3: Transparence and Disclosure

28LEVEL 1LEVEL 1

Understanding the Understanding the need to need to

professionalize the professionalize the CompanyCompany

LEVEL 2LEVEL 2First concrete steps First concrete steps

toward best toward best practicespractices

LEVEL 3LEVEL 3Implementation of Implementation of

best practicesbest practices

LEVEL 4LEVEL 4LeadershipLeadership

Adequate accounting Adequate accounting and auditing systems and auditing systems in place including: in place including:

Adequate internal Adequate internal accounting and accounting and control system control system reviewed periodically reviewed periodically by independent by independent external auditors external auditors and quarterly and quarterly financial reports financial reports prepared by internal prepared by internal accounting and accounting and approved by the approved by the Board Board

Annual financial Annual financial statements audited statements audited by independent by independent external auditors external auditors and approved by and approved by Shareholders Shareholders Meeting. Meeting.

Accounting and Accounting and auditing auditing performed in performed in accordance with accordance with highest national highest national standards and standards and audit performed audit performed by recognized by recognized international international accounting firm. accounting firm.

Accounting, Accounting, auditing and auditing and internal control internal control systems up to systems up to international international standards. standards.

SameSame

C. T

RA

NS

PA

RE

NC

Y A

ND

DIS

CL

OS

UR

E

Attribute 4: Control Environment & Processes

29

LEVEL 1LEVEL 1Understanding the Understanding the

need to need to professionalize the professionalize the

CompanyCompany

LEVEL 2LEVEL 2First First

concrete concrete steps steps

toward best toward best practicespractices

LEVEL 3LEVEL 3ImplementaImplementation of best tion of best practicespractices

LEVEL 4LEVEL 4LeadershipLeadership

Adequate Adequate internal control internal control systems are in systems are in place and are place and are periodically periodically reviewed by reviewed by independent independent external external auditors. auditors.

Internal Internal audit and audit and internal internal control control systems systems are in are in accordancaccordance with e with highest highest national national standardsstandards..

Internal Internal audit and audit and internal internal control control systems systems are are consistenconsistent with t with highest highest internatiointernational nal standardsstandards..

SameSame

C.

CO

NT

RO

L E

NV

IRO

NM

EN

T

AN

D

PR

OC

ES

SE

SS

Attribute 5: Shareholder Rights

30

LEVEL 1LEVEL 1Understanding the Understanding the

need to need to professionalize the professionalize the

CompanyCompany

LEVEL 2LEVEL 2First concrete steps First concrete steps

toward best toward best practicespractices

LEVEL 3LEVEL 3Implementation of Implementation of

best practicesbest practices

LEVEL 4LEVEL 4LeadershipLeadership

All shareholders All shareholders kept informed of kept informed of company policy, company policy, strategy and strategy and results of results of operations. operations.

Annual Annual shareholders shareholders meetings held. meetings held.

Shareholders Shareholders provided with all provided with all material material information and information and detailed agenda detailed agenda in advance of in advance of shareholders shareholders meetings. meetings.

Family council Family council established (if established (if number of family number of family members large members large or substantial or substantial portion are not portion are not working in the working in the business). business).

Company in Company in position to position to quickly quickly implement all implement all aspects of best aspects of best practice code practice code with respect to with respect to shareholders shareholders were company to were company to go public. go public.

D. S

HA

RE

HO

LD

ER R

igh

ts