Embed Size (px)

Citation preview

Item #6RESEARCH SEMINAR IN LAW, ECONOMICS, AND ORGANIZATIONProfessors Bebchuk, Hart, and Kaplow

Monday, November 14, 2005Pound 108, 12:30 p.m.

CORPORATE GOVERNANCE IN CONTEXT

By Bengt Holmstrom

0

Corporate Governance in Context

Bengt Holmstrom, MIT

Harvard Law School

November, 2005

Corporate Governance in Context

Bengt Holmstrom, MIT

Harvard Law School

November, 2005

1

Warren Buffett:

“In judging whether corporate America is serious about reforming itself, CEO pay remains the acid test. To date, the results aren’t encouraging”

Annual Letter to Shareholders 2004, Berkshire Hathaway

2

The Power Hypothesis

• CG system fundamentally flawed

• CEOs too powerful, boards too weak (Bebchuk-Fried, 2004)

• Correct power imbalance by giving shareholders intervention rights (Bebchuk, 2005)

• CG system fundamentally flawed

• CEOs too powerful, boards too weak (Bebchuk-Fried, 2004)

• Correct power imbalance by giving shareholders intervention rights (Bebchuk, 2005)

3

Power Hypothesis – two challenges

• Timing test:– why did system perform so well for so long?

– why did executive pay get out of hand in 1990s?

• Governance test:– do boards of closely held firms (family firms, buy-out firms) act very differently?

• Timing test:– why did system perform so well for so long?

– why did executive pay get out of hand in 1990s?

• Governance test:– do boards of closely held firms (family firms, buy-out firms) act very differently?

4

Corporate governance system –the two main tasks

• Decide who decides (selection problem)

• Make sure those in charge act responsibly (incentive problem)

• Decide who decides (selection problem)

• Make sure those in charge act responsibly (incentive problem)

5

Outline

• Historical context – rise of shareholder value

• Executive compensation –levels, structure and process

• Governance context – role of boards

• Reforms – selective job redesign

• Historical context – rise of shareholder value

• Executive compensation –levels, structure and process

• Governance context – role of boards

• Reforms – selective job redesign

6

Rise of Shareholder Value

7

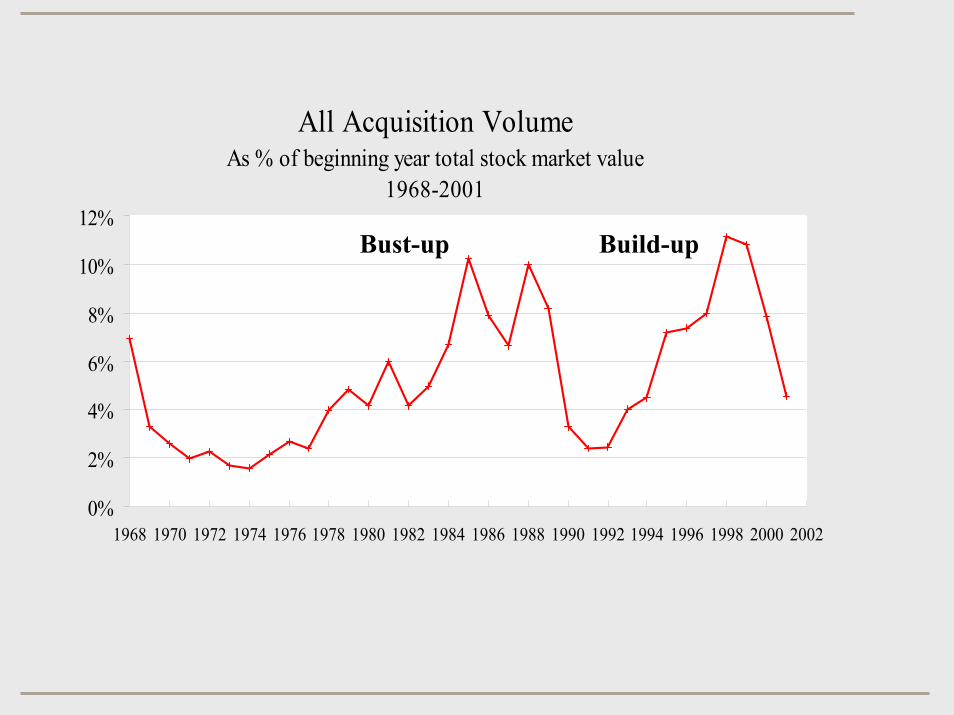

All Acquisition Volume As % of beginning year total stock market value

1968-2001

0%

2%

4%

6%

8%

10%

12%

1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

Bust-up Build-up

8

Two big restructuring waves

80s bust-up wave:– Hostile deals (takeovers)– Going private (over 100 Billion/yr)– All cash, high leverage (institutional money)– Targets: firms with excess cash

90s build-up wave:– Friendly deals – Publicly traded– Share swaps, stock options– Targets: consolidating industries

80s bust-up wave:– Hostile deals (takeovers)– Going private (over 100 Billion/yr)– All cash, high leverage (institutional money)– Targets: firms with excess cash

90s build-up wave:– Friendly deals – Publicly traded– Share swaps, stock options– Targets: consolidating industries

9

Why did this happen?

• Greed (Blair)• Return to healthy capitalism (Jensen)

….but WHY NOW?

• Need to understand past as well as present

• Greed (Blair)• Return to healthy capitalism (Jensen)

….but WHY NOW?

• Need to understand past as well as present

10

An alternative interpretation

• Deregulation, technological change created need for reallocation of capital

• Shareholders (market) got involved in reassigning decision rights (capital)

• Scandals a side-effect of system creating strong incentives for corporate restructuring

• On net a positive outcome – stock markets, profits soared, acquisitions paid off (?)

• Deregulation, technological change created need for reallocation of capital

• Shareholders (market) got involved in reassigning decision rights (capital)

• Scandals a side-effect of system creating strong incentives for corporate restructuring

• On net a positive outcome – stock markets, profits soared, acquisitions paid off (?)

11

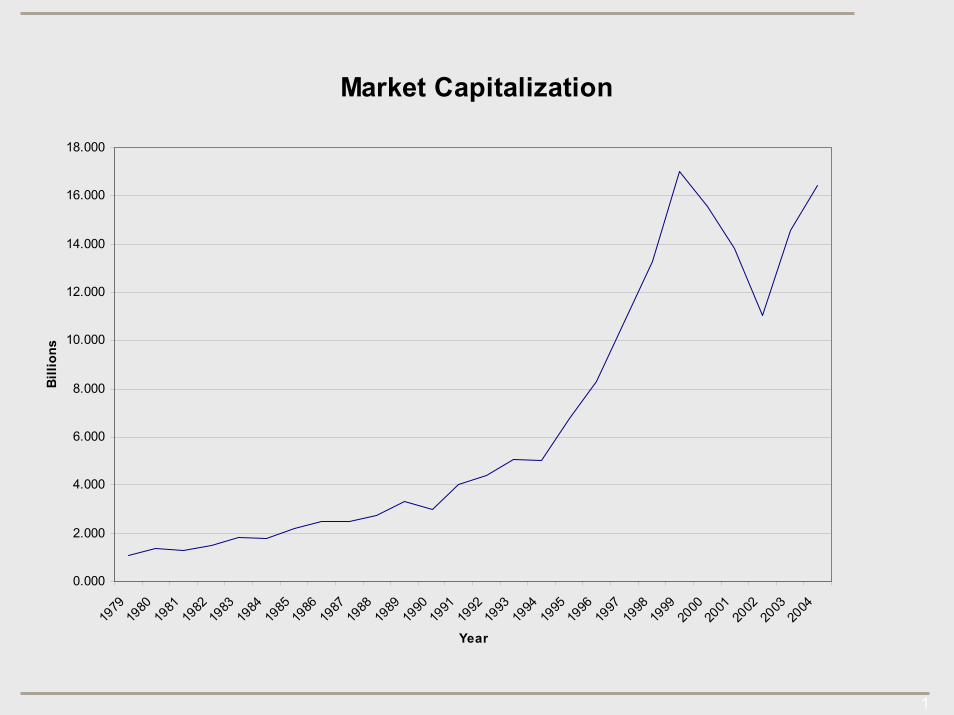

Market Capitalization

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

Billi

ons

12

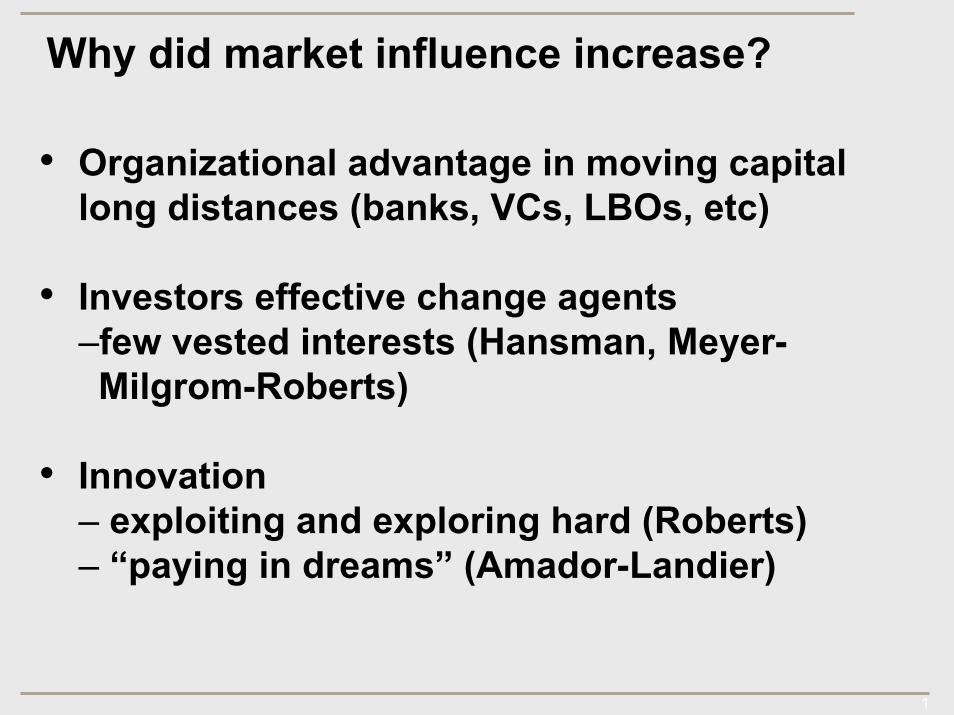

Why did market influence increase?

• Organizational advantage in moving capital long distances (banks, VCs, LBOs, etc)

• Investors effective change agents–few vested interests (Hansman, Meyer-Milgrom-Roberts)

• Innovation– exploiting and exploring hard (Roberts)– “paying in dreams” (Amador-Landier)

• Organizational advantage in moving capital long distances (banks, VCs, LBOs, etc)

• Investors effective change agents–few vested interests (Hansman, Meyer-Milgrom-Roberts)

• Innovation– exploiting and exploring hard (Roberts)– “paying in dreams” (Amador-Landier)

13

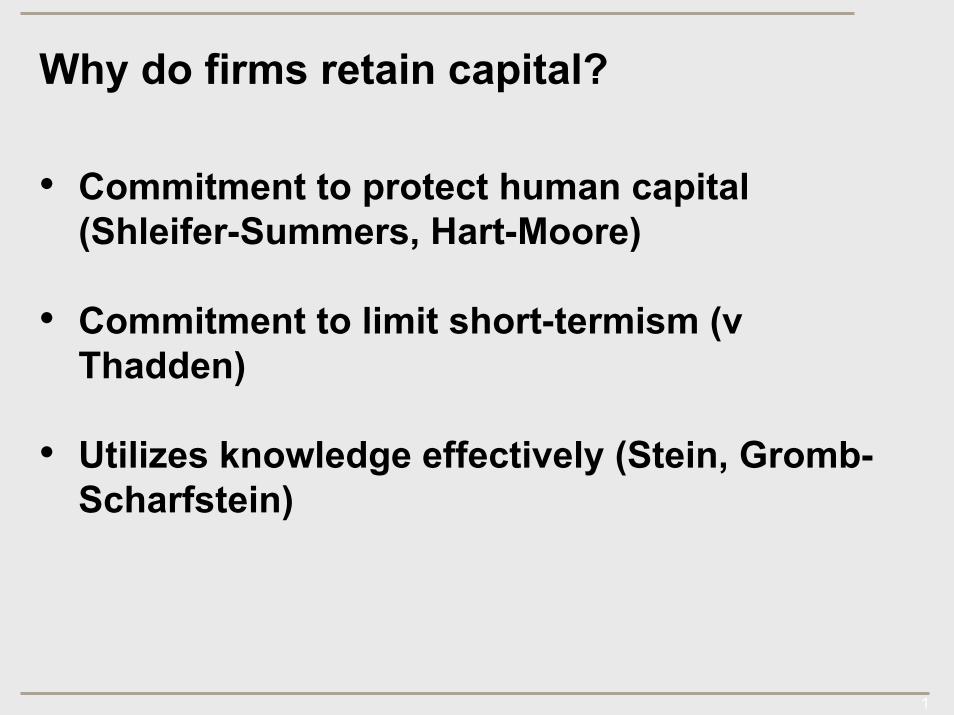

Why do firms retain capital?

• Commitment to protect human capital (Shleifer-Summers, Hart-Moore)

• Commitment to limit short-termism (v Thadden)

• Utilizes knowledge effectively (Stein, Gromb-Scharfstein)

• Commitment to protect human capital (Shleifer-Summers, Hart-Moore)

• Commitment to limit short-termism (v Thadden)

• Utilizes knowledge effectively (Stein, Gromb-Scharfstein)

14

Executive Compensation

15

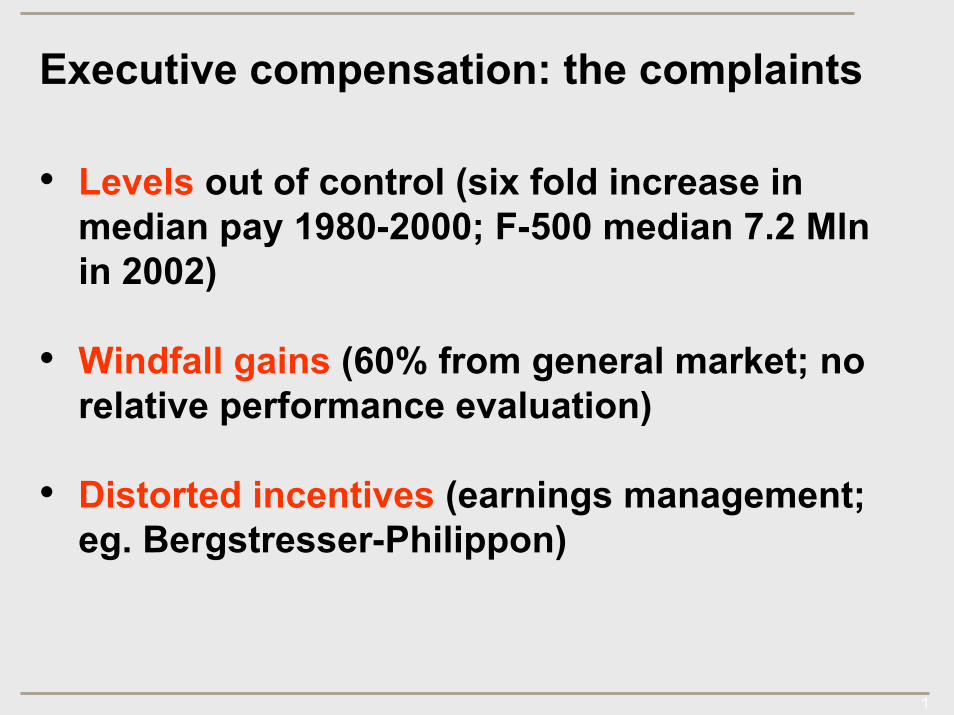

Executive compensation: the complaints

• Levels out of control (six fold increase in median pay 1980-2000; F-500 median 7.2 Mlnin 2002)

• Windfall gains (60% from general market; no relative performance evaluation)

• Distorted incentives (earnings management; eg. Bergstresser-Philippon)

• Levels out of control (six fold increase in median pay 1980-2000; F-500 median 7.2 Mlnin 2002)

• Windfall gains (60% from general market; no relative performance evaluation)

• Distorted incentives (earnings management; eg. Bergstresser-Philippon)

16

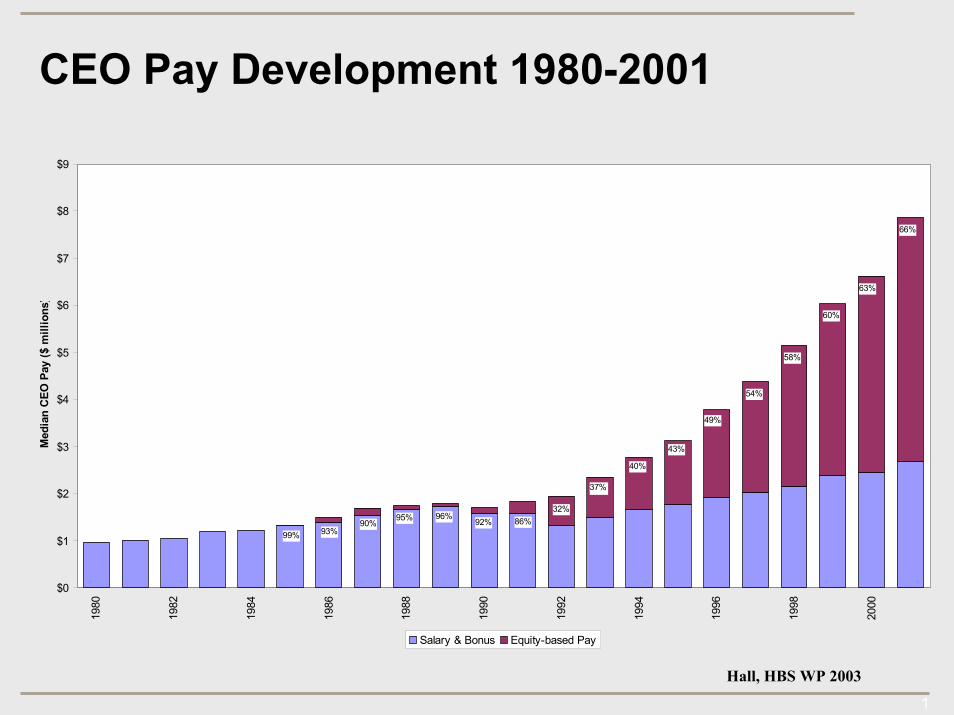

CEO Pay Development 1980-2001

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Med

ian

CEO

Pay

($ m

illio

ns)

Salary & Bonus Equity-based Pay

60%

58%

54%

49%

43%

40%

37%

32%86%92%

96%95%90%

93%99%

63%

66%

Hall, HBS WP 2003

17

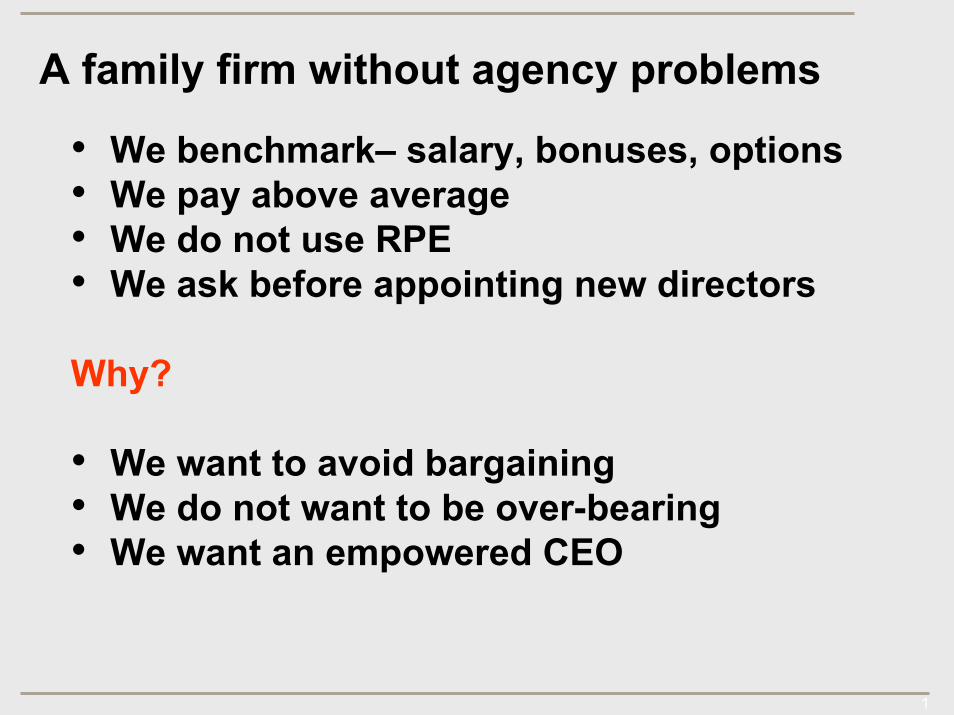

A family firm without agency problems

• We benchmark– salary, bonuses, options• We pay above average• We do not use RPE• We ask before appointing new directors

Why?

• We want to avoid bargaining• We do not want to be over-bearing• We want an empowered CEO

• We benchmark– salary, bonuses, options• We pay above average• We do not use RPE• We ask before appointing new directors

Why?

• We want to avoid bargaining• We do not want to be over-bearing• We want an empowered CEO

18

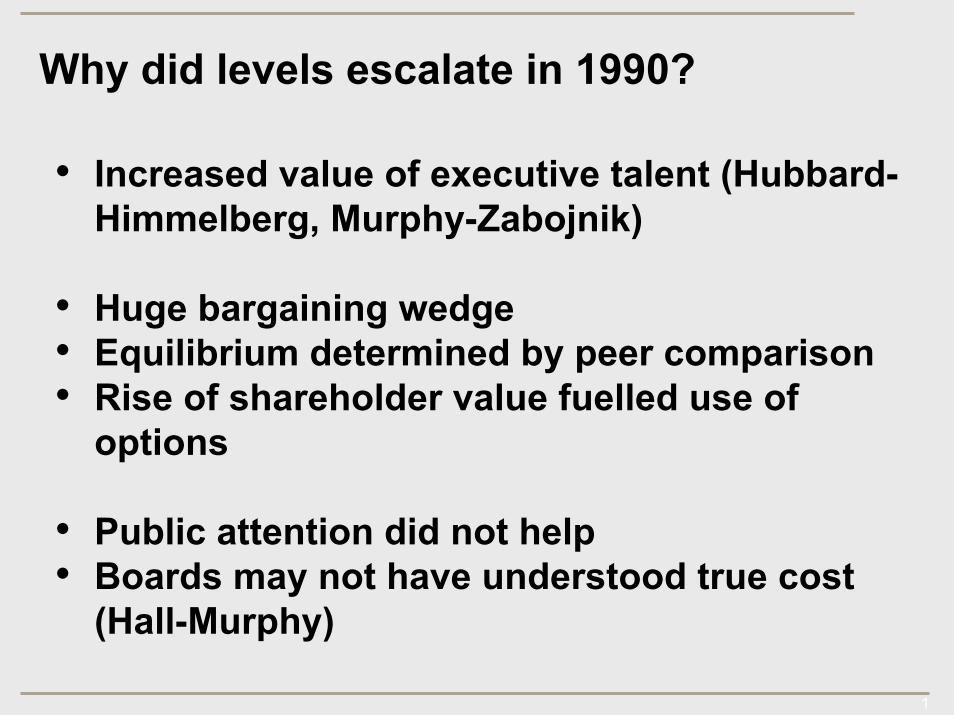

Why did levels escalate in 1990?

• Increased value of executive talent (Hubbard-Himmelberg, Murphy-Zabojnik)

• Huge bargaining wedge• Equilibrium determined by peer comparison• Rise of shareholder value fuelled use of

options

• Public attention did not help• Boards may not have understood true cost

(Hall-Murphy)

• Increased value of executive talent (Hubbard-Himmelberg, Murphy-Zabojnik)

• Huge bargaining wedge• Equilibrium determined by peer comparison• Rise of shareholder value fuelled use of

options

• Public attention did not help• Boards may not have understood true cost

(Hall-Murphy)

19

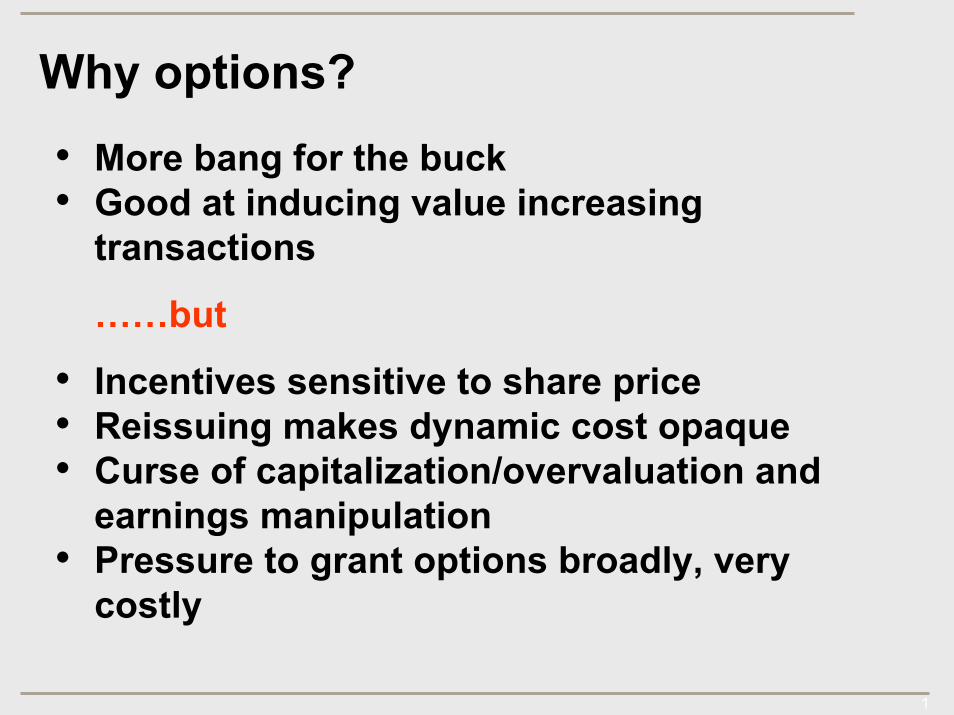

Why options?

• More bang for the buck• Good at inducing value increasing

transactions

……but

• Incentives sensitive to share price• Reissuing makes dynamic cost opaque• Curse of capitalization/overvaluation and

earnings manipulation• Pressure to grant options broadly, very

costly

• More bang for the buck• Good at inducing value increasing

transactions

……but

• Incentives sensitive to share price• Reissuing makes dynamic cost opaque• Curse of capitalization/overvaluation and

earnings manipulation• Pressure to grant options broadly, very

costly

20

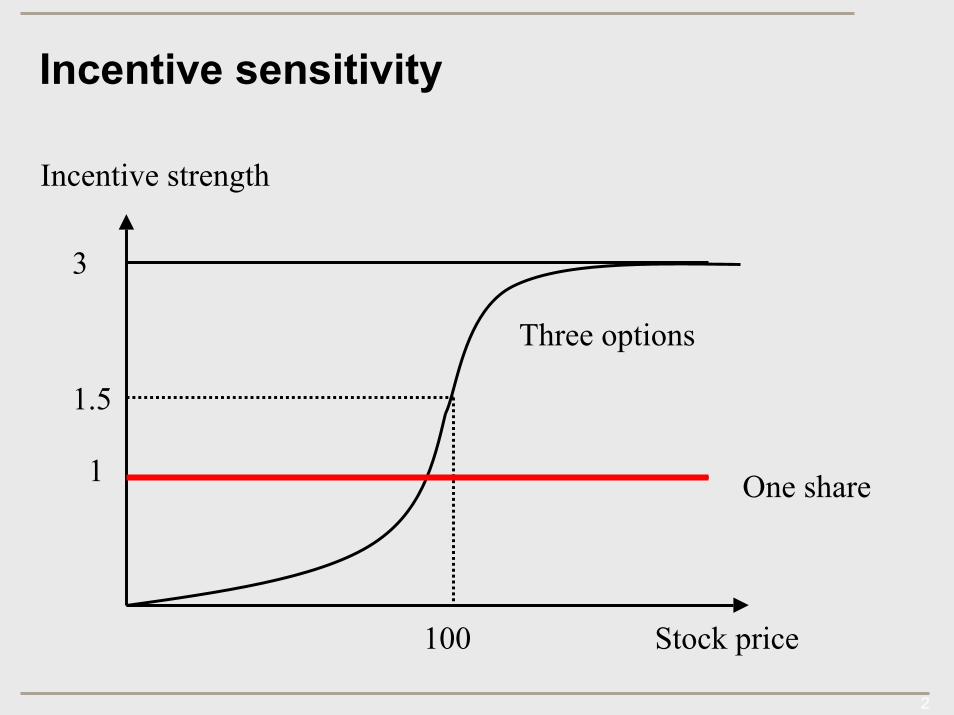

Incentive sensitivity

Incentive strength

3

Three options

1.5

1 One share

Stock price100

21

Some other issues

• What do you want to achieve?

• Partial transparency – leads to stealth compensation (Singh)

• Why so little relative performance evaluation? (LBOs, family firms)

• Implicit incentives – pros and cons of short-termism

• What do you want to achieve?

• Partial transparency – leads to stealth compensation (Singh)

• Why so little relative performance evaluation? (LBOs, family firms)

• Implicit incentives – pros and cons of short-termism

22

Improving compensation

• Structure:– Restricted stock (robust, transparent)– Longer horizons, fixed cash-out dates– Smaller, more frequent awards (partial indexation)

–Avoid performance plans

• Level: – More not less benchmarking

External credibility limits designs (ISS)

• Structure:– Restricted stock (robust, transparent)– Longer horizons, fixed cash-out dates– Smaller, more frequent awards (partial indexation)

–Avoid performance plans

• Level: – More not less benchmarking

External credibility limits designs (ISS)

23

The Role of Boards

24

Why do we have boards?

• Bebchuk (2005): treats executives and board as one body – “management”

• Where’s the role for boards?

• Three economic reasons:– Economizes on information acquisition– Protects confidentiality of information– Acts as intermediary (buffer) between

shareholders and management

• Bebchuk (2005): treats executives and board as one body – “management”

• Where’s the role for boards?

• Three economic reasons:– Economizes on information acquisition– Protects confidentiality of information– Acts as intermediary (buffer) between

shareholders and management

25

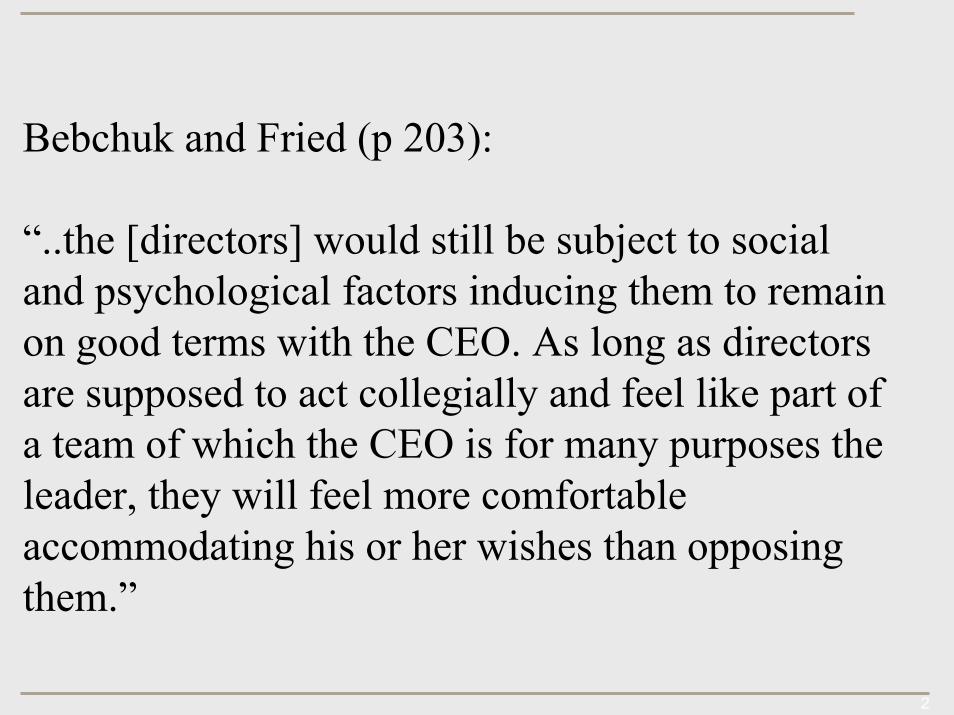

Bebchuk and Fried (p 203):

“..the [directors] would still be subject to social and psychological factors inducing them to remain on good terms with the CEO. As long as directors are supposed to act collegially and feel like part of a team of which the CEO is for many purposes the leader, they will feel more comfortable accommodating his or her wishes than opposing them.”

26

What do boards (try to) do?

• Evaluate (main task): Is the right team in charge? Does strategy make sense? Is capital efficiently used?

• Monitor (side task): Oversee conduct

• Auditors check fraud• Management designs strategy

• What is the objective of boards?

• Evaluate (main task): Is the right team in charge? Does strategy make sense? Is capital efficiently used?

• Monitor (side task): Oversee conduct

• Auditors check fraud• Management designs strategy

• What is the objective of boards?

27

Board challenges:

Challenge # 1: Challenge # 1:

Maintaining credibility with managementImpacts access to crucial, tacit information

Challenge # 2:

Maintaining credibility with shareholdersImpacts ability to use expert information

Maintaining credibility with managementImpacts access to crucial, tacit information

Challenge # 2:

Maintaining credibility with shareholdersImpacts ability to use expert information

28

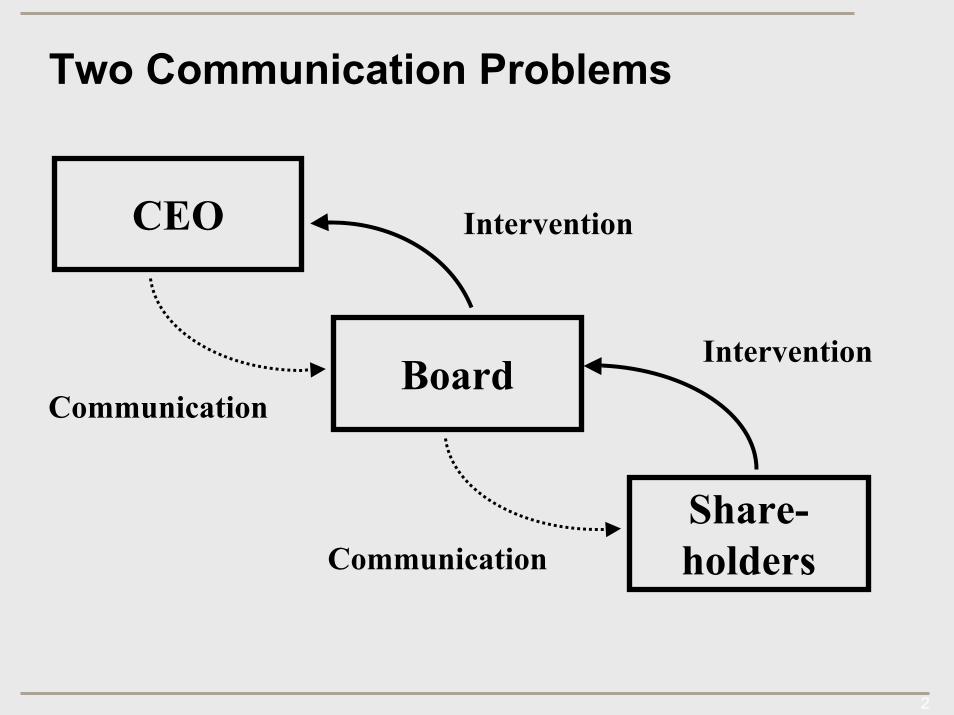

Two Communication Problems

CEO

Board

Intervention

Intervention

Communication

Share-holdersCommunication

29

Management-Board Game (Crawford-Sobel, Adams-Ferreira)

• Management wants a (reasonably) informed board:– needs board understanding in times of crises– values advice

….but

• Worried about excessive intervention. Over-bearing board kills information flow (family firms, Coca-Cola)

• Management wants a (reasonably) informed board:– needs board understanding in times of crises– values advice

….but

• Worried about excessive intervention. Over-bearing board kills information flow (family firms, Coca-Cola)

30

On entrenchment (Hermalin-Weisbach)

• Management that does well gains power• Leads to consolidation of power• This is an efficient commitment mechanism

Additional prediction:

• Dismissal has positive stock price effect it accords with public perception and negative if it goes against public perception

• Management that does well gains power• Leads to consolidation of power• This is an efficient commitment mechanism

Additional prediction:

• Dismissal has positive stock price effect it accords with public perception and negative if it goes against public perception

31

Board-Shareholder Game

• Reputation concerns can lead to limited use of information (Holmstrom, Ely-Valimaki)

• Shareholder pressure leads to short-termism(Stein), biased behavior (Aghion-Stein)

…therefore

• Entrenched board can be valuable (Fisman-Khurana and Rhodes-Kropf)

• Biased supervisor can be valuable (Dessein)

• Reputation concerns can lead to limited use of information (Holmstrom, Ely-Valimaki)

• Shareholder pressure leads to short-termism(Stein), biased behavior (Aghion-Stein)

…therefore

• Entrenched board can be valuable (Fisman-Khurana and Rhodes-Kropf)

• Biased supervisor can be valuable (Dessein)

32

One way to think about reforms – how do they affect information games?• Mandatory rules can facilitate board access to

information (eg non-executive sessions)

• Shareholder intervention rights can suppress board’s use of expert information

• Selective job re-design -- eg external evaluation of compensation plans (ISS versus GACP)

• Mandatory rules can facilitate board access to information (eg non-executive sessions)

• Shareholder intervention rights can suppress board’s use of expert information

• Selective job re-design -- eg external evaluation of compensation plans (ISS versus GACP)

33

Concluding observations

• Organizational experiments (Enron) may fail at times; that’s okay

• Public outrage part of overall corporate governance system

• Is advocacy a good social system for reforming corporate governance?

• Organizational experiments (Enron) may fail at times; that’s okay

• Public outrage part of overall corporate governance system

• Is advocacy a good social system for reforming corporate governance?

35

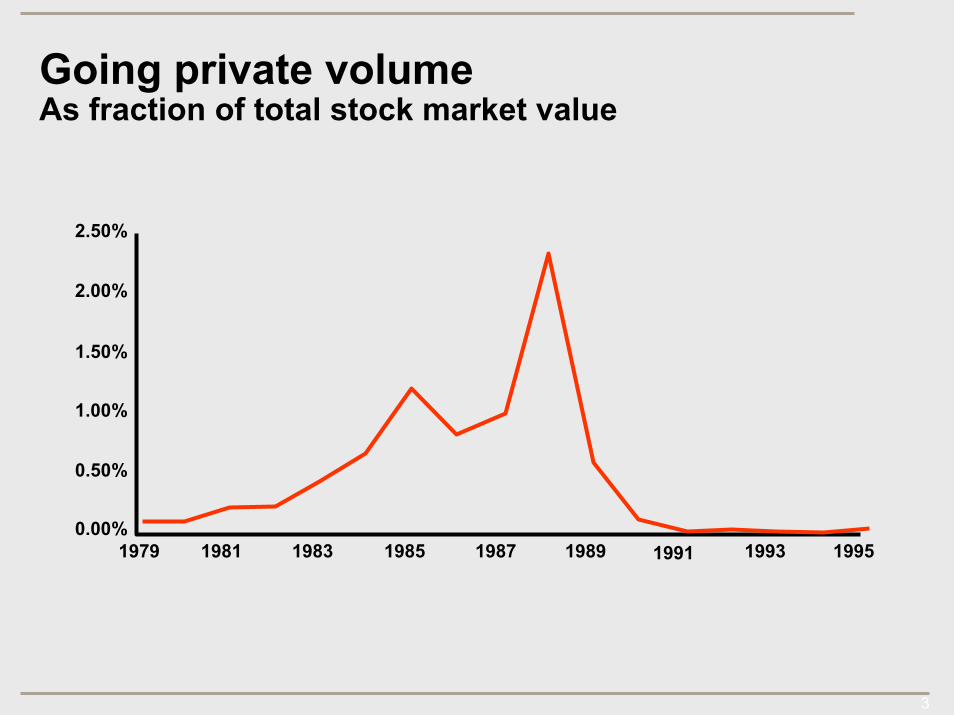

Going private volumeAs fraction of total stock market value

2.50%2.50%

2.00%2.00%

1.50%1.50%

1.00%1.00%

0.50%0.50%

197919790.00%0.00%

19811981 19831983 19851985 19871987 19891989 19911991 19931993 19951995

36

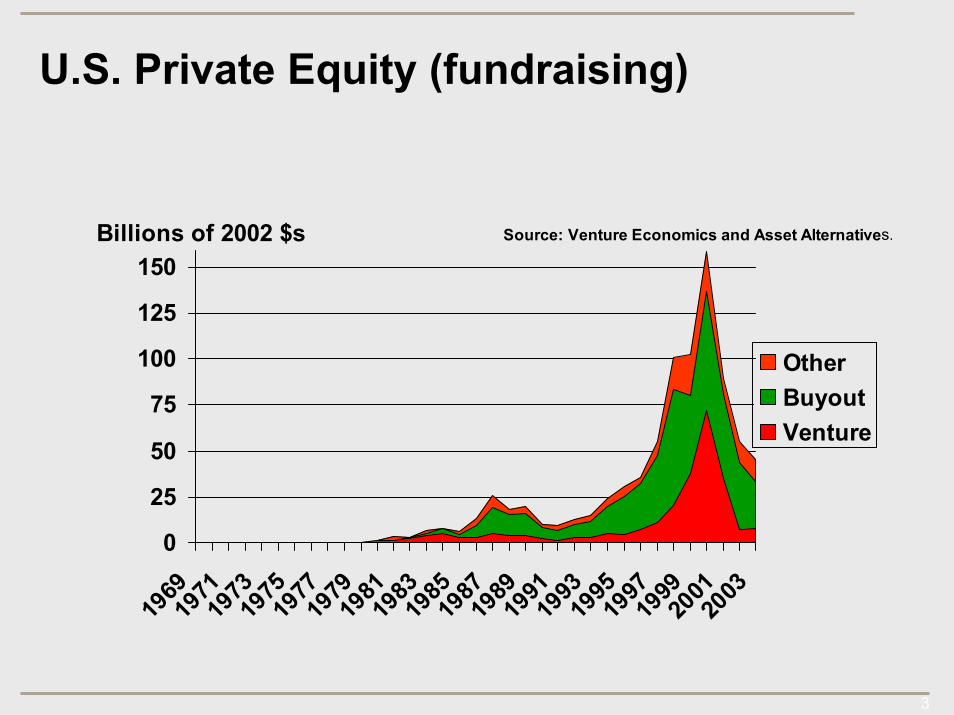

U.S. Private Equity (fundraising)

0

25

50

75

100

125

150

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

OtherBuyoutVenture

Billions of 2002 $s Source: Venture Economics and Asset Alternatives.

37

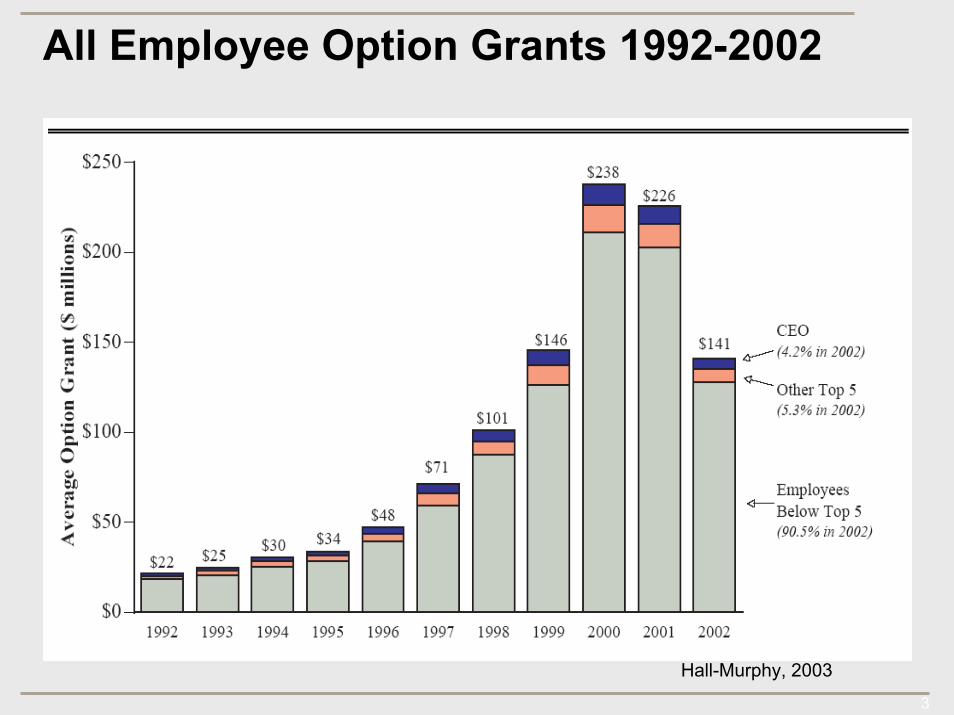

All Employee Option Grants 1992-2002

Hall-Murphy, 2003

38

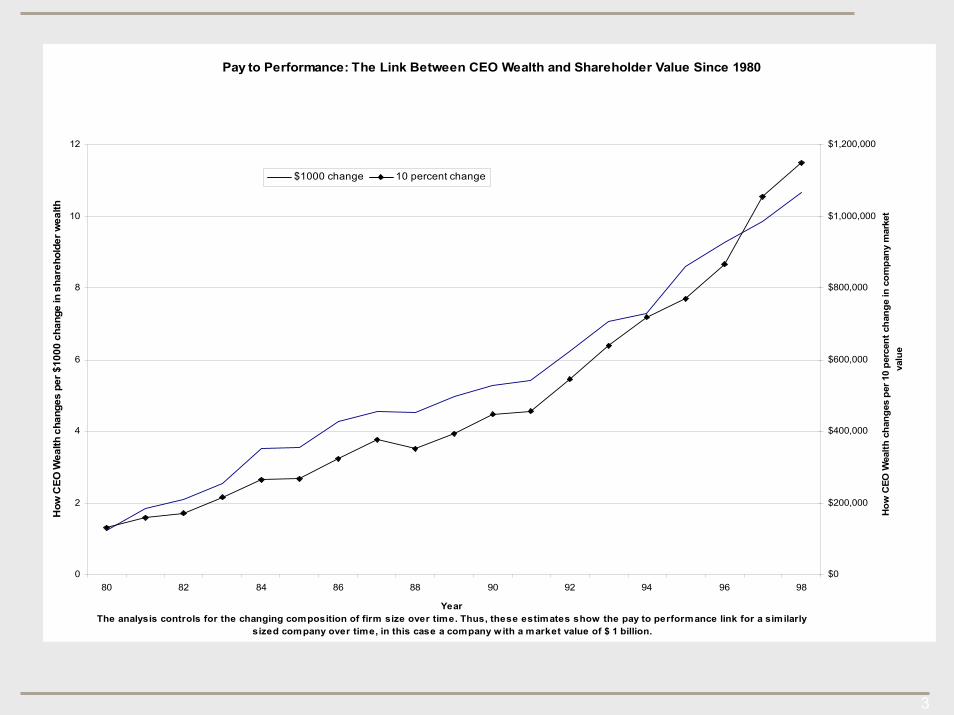

Pay to Performance: The Link Between CEO Wealth and Shareholder Value Since 1980

0

2

4

6

8

10

12

80 82 84 86 88 90 92 94 96 98

YearThe analysis controls for the changing composition of firm size over time. Thus, these estimates show the pay to performance link for a similarly

sized company over time, in this case a company w ith a market value of $ 1 billion.

How

CEO

Wea

lth c

hang

es p

er $

1000

cha

nge

in s

hare

hold

er w

ealth

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

How

CEO

Wea

lth c

hang

es p

er 1

0 pe

rcen

t cha

nge

in c

ompa

ny m

arke

t va

lue

$1000 change 10 percent change

39

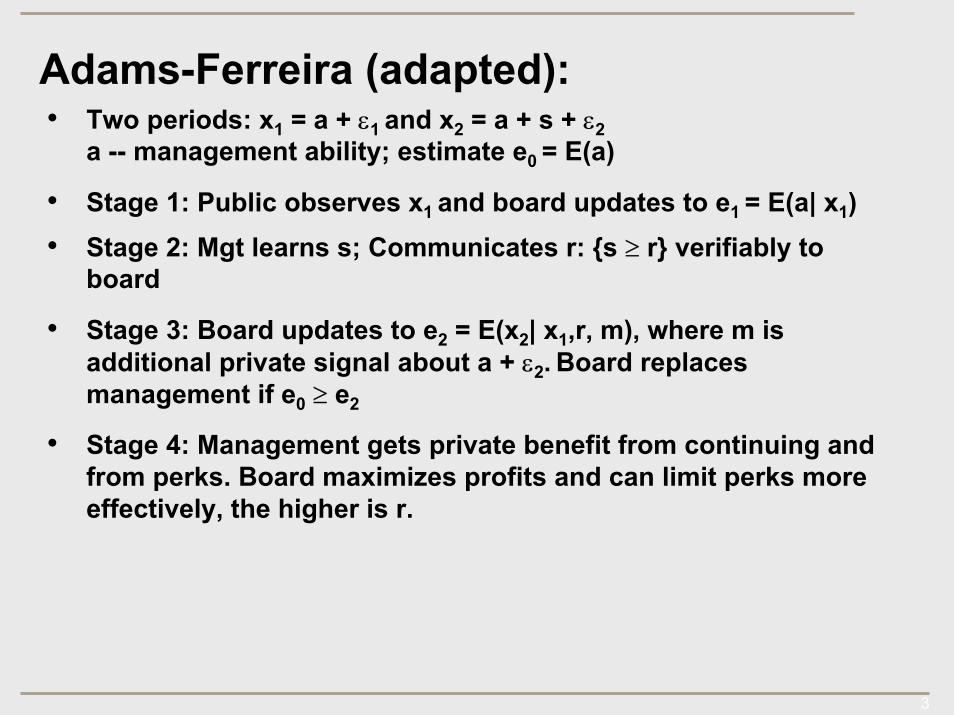

Adams-Ferreira (adapted):• Two periods: x1 = a + ε1 and x2 = a + s + ε2

a -- management ability; estimate e0 = E(a)

• Stage 1: Public observes x1 and board updates to e1 = E(a| x1)• Stage 2: Mgt learns s; Communicates r: {s ≥ r} verifiably to

board

• Stage 3: Board updates to e2 = E(x2| x1,r, m), where m is additional private signal about a + ε2. Board replaces management if e0 ≥ e2

• Stage 4: Management gets private benefit from continuing and from perks. Board maximizes profits and can limit perks more effectively, the higher is r.

• Two periods: x1 = a + ε1 and x2 = a + s + ε2 a -- management ability; estimate e0 = E(a)

• Stage 1: Public observes x1 and board updates to e1 = E(a| x1)• Stage 2: Mgt learns s; Communicates r: {s ≥ r} verifiably to

board

• Stage 3: Board updates to e2 = E(x2| x1,r, m), where m is additional private signal about a + ε2. Board replaces management if e0 ≥ e2

• Stage 4: Management gets private benefit from continuing and from perks. Board maximizes profits and can limit perks more effectively, the higher is r.

40

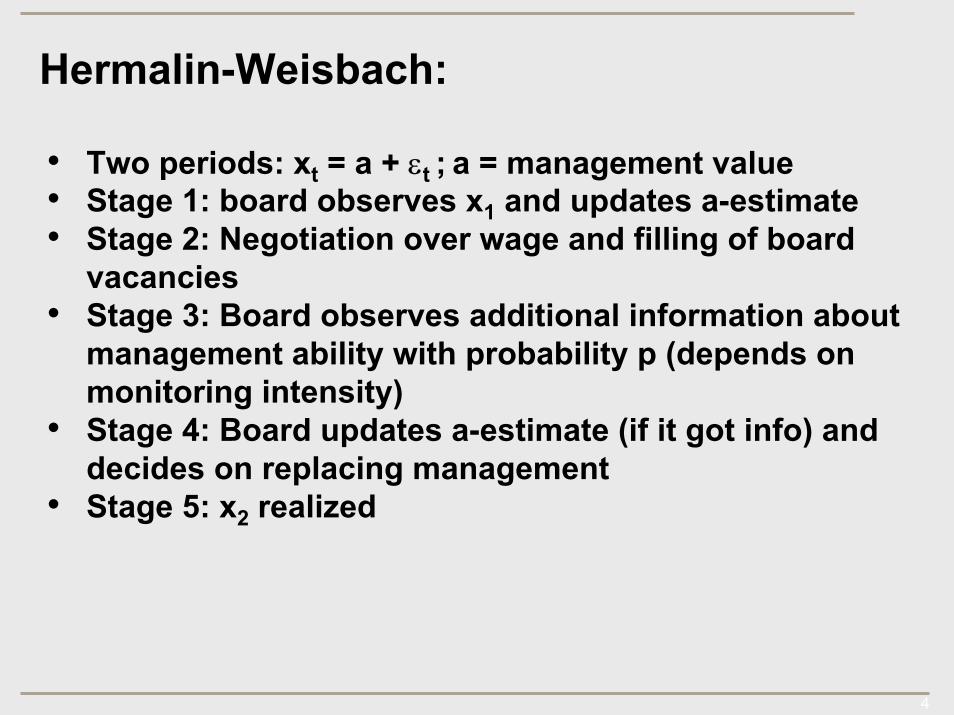

Hermalin-Weisbach:

• Two periods: xt = a + εt ; a = management value• Stage 1: board observes x1 and updates a-estimate• Stage 2: Negotiation over wage and filling of board

vacancies• Stage 3: Board observes additional information about

management ability with probability p (depends on monitoring intensity)

• Stage 4: Board updates a-estimate (if it got info) and decides on replacing management

• Stage 5: x2 realized

• Two periods: xt = a + εt ; a = management value• Stage 1: board observes x1 and updates a-estimate• Stage 2: Negotiation over wage and filling of board

vacancies• Stage 3: Board observes additional information about

management ability with probability p (depends on monitoring intensity)

• Stage 4: Board updates a-estimate (if it got info) and decides on replacing management

• Stage 5: x2 realized