Embed Size (px)

Citation preview

HELLENIC AMERICAN EDUCATIONAL FOUNDATION

Corporate Governance Review 2013 The Board of Directors of the companies in

FTSE/Athex Large Cap of Athens Stock Exchange

Vasileios Oikonomou

9/1/2014

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

1

Table of Contents Introduction

1. Hellenic Corporate Governance Code (HCGC)

2. FTSE/Athex Large Cap

3. Research Methodology

4. European Commission’s Action Plan 2012

5. Corporate Governance Code followed by firms

6. Implementation of the principles of corporate governance

1. Size of the Board of Directors

2. Composition of the Board of Directors

3. The presence of women on Board of Directors

4. Publication of the size and composition of the Board on the Corporate Governance

Statement.

5. Publication of brief curriculum vitae on the Corporate Governance Statement

6. Existence of a Remuneration Committee

7. Remuneration Disclosure

8. Evaluation of the Board

Conclusion

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

2

Introduction

The term “Corporate Governance” describes the way firms are managed and controlled.

In the past few decades, Europe has met with an extensive widespread of corporate governance issues.

Within a company, the principles of corporate governance are depicted on the corporate governance

code, a document based on the good will of each firm to adhere to the “comply or explain” principle.

After more than ten (10) years since the outbreak of corporate governance, the fundamental provisions

found in the corporate governance codes internationally have set the stage for the establishment of

international corporate governance standards in the European Union. This new approach to today’s

business world has been adopted by both the European Commission and International fora.

In Greece, the corporate governance framework has been developed by the Greek State through the

adoption of laws, such as law 3016/2002, that provide details on issues such as the composition of the

Board of Directors, Internal Audit, Remuneration and other areas which are considered critical to the

orderly functioning of the company. In addition, a number of legislative acts have contributed to the

smooth incorporation of European norms to the anomalies of Greek reality while providing a steady

basis for the future development of new standards of corporate governance.

1. Hellenic Corporate Governance Code

In Greece, the compliance to a Corporate Governance Code constitutes a prerequisite for companies to

enter the Athens Stock Exchange or any other formal market. Such a Code should have as a frame of

reference the relative regulatory framework and should be published on the official website of the

company. The company can either adopt its own code or follow the Hellenic Corporate Governance

Code (HCGC). This information should be disclosed in the company’s Corporate Governance annual

report. To the present day, the predominant Code of this kind has been the Hellenic Corporate

Governance Code (HCGC) of October 2013, which many firms have already adopted.

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

3

2. FTSE/Athex Large Cap

The FTSE/Athex Large Cap, index consists of the 25 largest and most liquid companies that trade in the

Athens Stock Exchange. The index was developed in September 1997 out of a partnership between the

Athens Stock Exchange and FTSE International1. The 25 companies that are currently included in the

Index and will be included in the sample of the research are:

1. METKA

2. HELLENIC PETROLEUM

3. MARFIN INVESTMENT GROUP

4. JUMBO

5. MYTILINEOS GROUP

6. PIREAUS PORT AUTHORITY S.A.

7. ALPHA BANK

8. NATIONAL BANK OF GREECE S.A.

9. PIRAEUS BANK

10. EUROBANK

11. GEK TERNA GROUP OF COMPANIES

12. TERNA ENERGY

13. OPAP

14. EYDAP

15. ATHEX GROUP

16. INTRALOT

17. MOTOROIL (HELLAS)

18. ELLAKTOR

19. OTE

20. TITAN

21. EUROBANK PROPERTIES

22. PUBLIC POWER CORPORATION S.A.

23. FF GROUP

24. VIOHALCO GROUP

25. COCA-COLA HBC

1 Source: http://www.bloomberg.com/quote/FTASE:IND

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

4

3. Research Methodology

The data that will be used in the sections bellow were collected as part of a contribution to Grant

Thornton’s (Greek annex) data collection for the Corporate Governance Survey that is expected to be

published in the forthcoming months. The different sections of the current Review were inspired from

those stated in the HCGC which can be found in Athex’s website2. Finally, data were extracted from the

Statement of Corporate Governance, found in each company’s Annual Financial Report for 2013, and

corporal websites. For two of the companies (Viohalco Group and Coca Cola HBC) which are no longer

primarily traded in the Athens Stock Exchange, information was retrieved from their Corporate

Governance Code and relative publications found on their corporal websites.

The present Corporate Governance Review 2013 will focus primarily on the role and responsibilities of

the Board of Directors and will explore the extend to which companies members of the FTSE/Athex

Large Cap of the Athens Stock Exchange follow the HCGC practices and guidelines. Such practices that

will be examined have to do with the size and composition of the Board of Directors, the presence of

women on Board of Directors, the publication of the size and composition of the Board on the Corporate

Governance Statement, the publication of a brief curriculum vitae the existence of a Remuneration

Committee, Remuneration disclosure, and measures of evaluating the Board.

4. European Commission’s Action Plan 2012

Trying to build on the success of the 2003 Action Plan on Corporate Governance, the European

Commission (EC) launched another Action Plan in 2012 with the goal of improving the problems of

excess risk-taking and sort-termism that concern the market in the recent years. As described in the

memo published by the EC, the primary focus of the Action Plan is on EU liability companies, listed on a

European Stock Exchange. For this reason the Plan contains suggestions for the improvement of the

existing legal framework regarding Corporate Governance and identifies three (3) main lines of action:

Enhancing transparency, Engaging shareholders and Supporting companies.

Regarding the issue of enhancing transparency, the EC has decided that “companies need to provide

better information about their corporate governance and society at large”. However, the idea of

transparency admittedly works both ways as it is deemed essential for the companies to know who their

shareholders are and what interests they pursue if they are to codetermine their future strategies.

As for the issue of engaging shareholders, the Commission suggests that shareholders should have more

freedoms to oversee remuneration policy and related party transactions. In more detail, according to

the Green Papers published by the Commission in 2010 and 2011 there is “a perceived lack of

shareholder interest in holding management accountable for their decisions and actions, compounded

by the fact that many shareholders appear to hold their shares for only a short period of time”. This

phenomenon of sort-termism on behalf of the stakeholders and their apathy towards the assessment of

2 Source: http://www.helex.gr/web/guest/esed-hellenic-cgc

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

5

the management seems to be strongly connected to the 2008 global financial crisis for which society

largely failed in holding accountable those who abused their power.

The last line of action that is highlighted in the Action Plan has to do with supporting companies’ growth

and competitiveness. This emphasizes the need for simplifications in the procedures of cross-border

operations of European enterprises, particularly in the case of medium-sized companies.

In addressing the above problems, the Commission targets at making the regulatory framework more

user-friendly through the use of legislation and non-complicated laws. With the global Financial Crisis of

2008 being a vivid illustration of the lack of adequate corporate governance practices, it is true that

concerted action is required on a national and an international level to improve the diversity and

efficiency of the Board of Directors and align the interests of senior management with those of the

shareholders.3

3 Sources: http://www.ecgi.org/tcgd/2012/documents/121212_company-law-corporate-governance-action-

plan_en.pdf , http://europa.eu/rapid/press-release_MEMO-12-972_el.htm

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

6

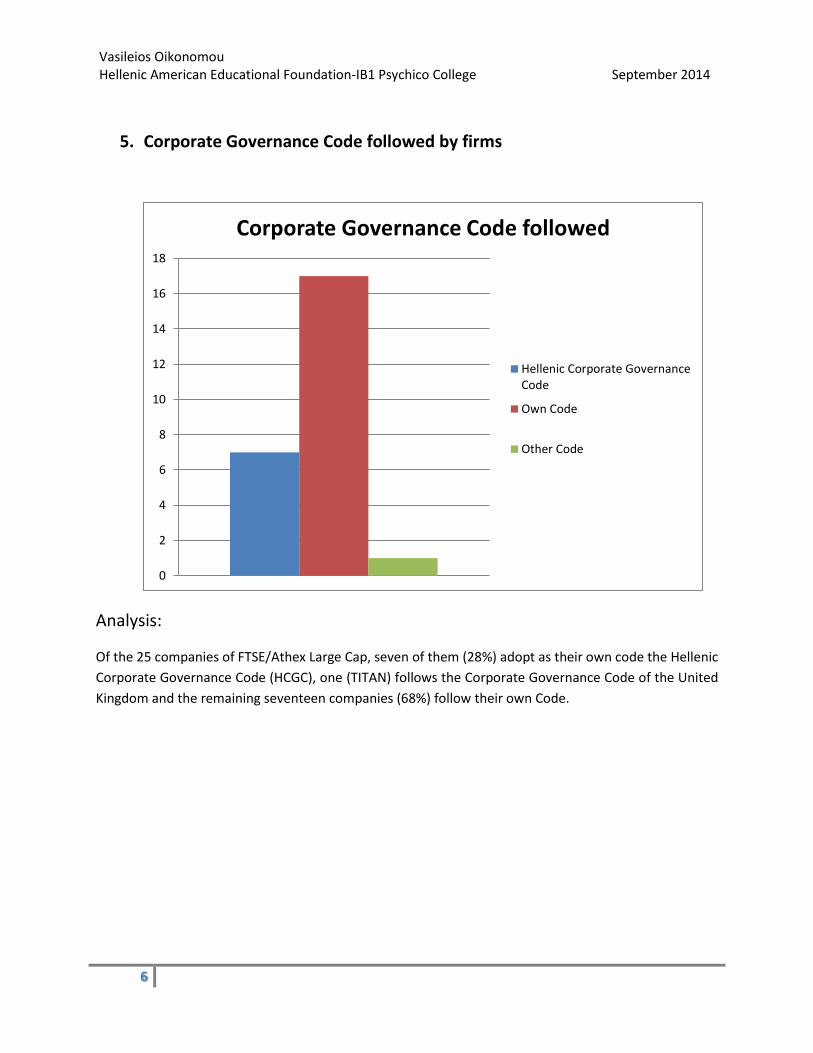

5. Corporate Governance Code followed by firms

Analysis:

Of the 25 companies of FTSE/Athex Large Cap, seven of them (28%) adopt as their own code the Hellenic

Corporate Governance Code (HCGC), one (TITAN) follows the Corporate Governance Code of the United

Kingdom and the remaining seventeen companies (68%) follow their own Code.

0

2

4

6

8

10

12

14

16

18

Corporate Governance Code followed

Hellenic Corporate GovernanceCode

Own Code

Other Code

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

7

6. Implementation of the principles of corporate governance

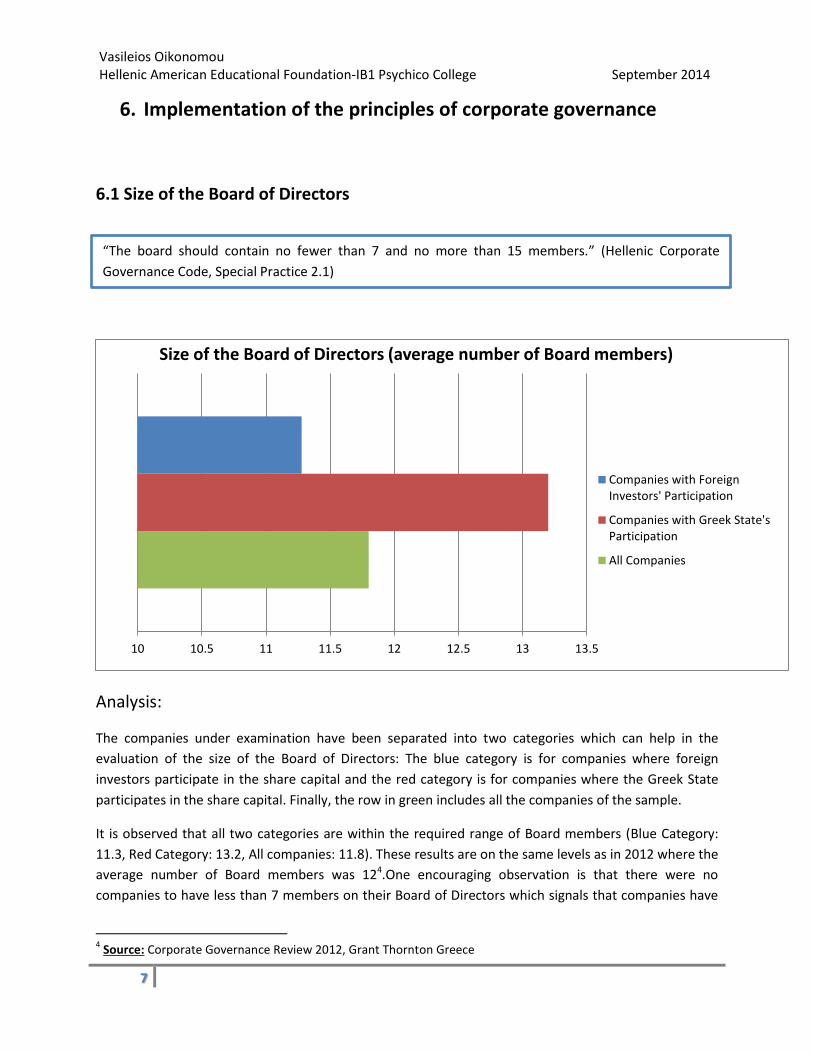

6.1 Size of the Board of Directors

Analysis:

The companies under examination have been separated into two categories which can help in the

evaluation of the size of the Board of Directors: The blue category is for companies where foreign

investors participate in the share capital and the red category is for companies where the Greek State

participates in the share capital. Finally, the row in green includes all the companies of the sample.

It is observed that all two categories are within the required range of Board members (Blue Category:

11.3, Red Category: 13.2, All companies: 11.8). These results are on the same levels as in 2012 where the

average number of Board members was 124.One encouraging observation is that there were no

companies to have less than 7 members on their Board of Directors which signals that companies have

4 Source: Corporate Governance Review 2012, Grant Thornton Greece

10 10.5 11 11.5 12 12.5 13 13.5

Size of the Board of Directors (average number of Board members)

Companies with ForeignInvestors' Participation

Companies with Greek State'sParticipation

All Companies

“The board should contain no fewer than 7 and no more than 15 members.” (Hellenic Corporate

Governance Code, Special Practice 2.1)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

8

grasped the importance of a larger Board which can be more effective and diverse than a smaller one.

However, the same cannot be said about the upper limit for the size of the Board. Two (2) out of

twenty-five (25) companies presented Boards larger than fifteen (15) members. One common

characteristic of these companies was that the Greek State was the main shareholder in both cases, with

the ability to choose almost half the members of the Board.

In conclusion, the statistics seem to confirm an upward trend in the average size of the Board of

Directors in the past years. For 2013, the number might have decreased by 0.2 units, however it is still

notably larger compared to the 2011 statistics (11 members on Board of Directors).

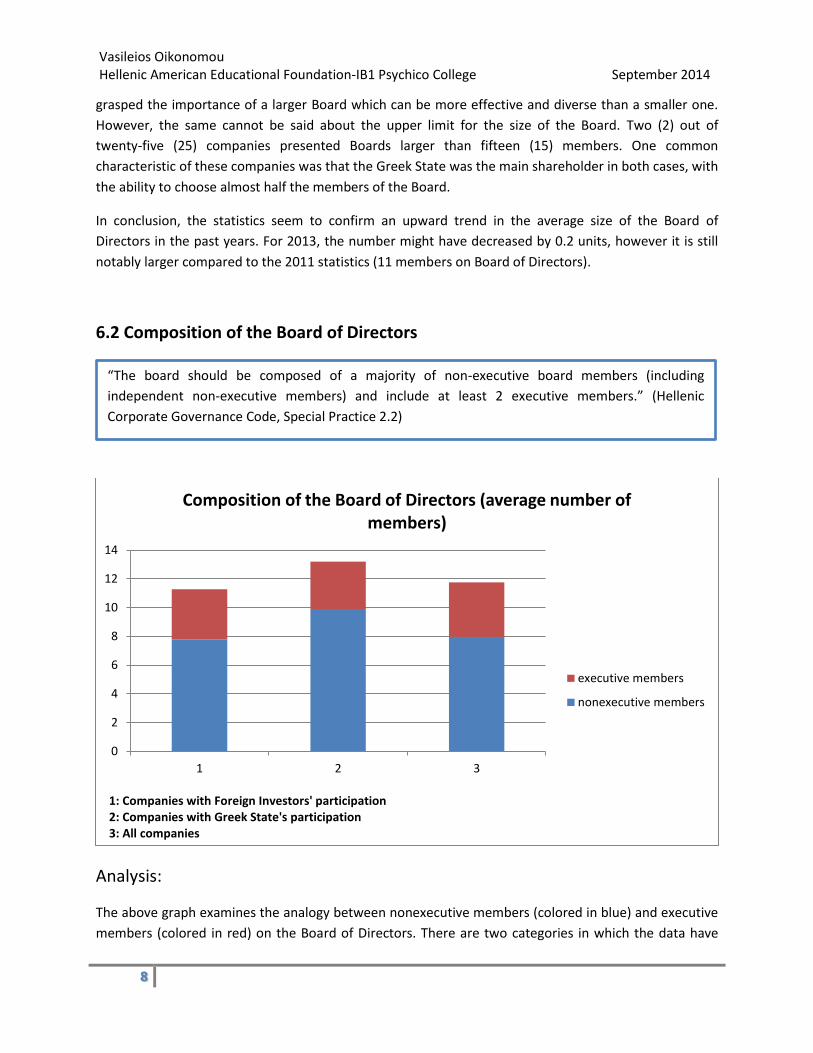

6.2 Composition of the Board of Directors

Analysis:

The above graph examines the analogy between nonexecutive members (colored in blue) and executive

members (colored in red) on the Board of Directors. There are two categories in which the data have

0

2

4

6

8

10

12

14

1 2 3

1: Companies with Foreign Investors' participation 2: Companies with Greek State's participation 3: All companies

Composition of the Board of Directors (average number of members)

executive members

nonexecutive members

“The board should be composed of a majority of non-executive board members (including

independent non-executive members) and include at least 2 executive members.” (Hellenic

Corporate Governance Code, Special Practice 2.2)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

9

been arranged. The first one includes companies with Foreign Investor’s participation, meaning foreign

investment funds or firms, but not individuals. The second one includes companies with Greek State’s

participation, or any other institution controlled by the Greek State. Finally, the column includes all

companies found in the FTSE/Athex Large Cap Index.

Clearly, nonexecutive members constitute the majority of the members in both categories. This is a

positive sign which reveals that almost all companies have complied with the relative special practice of

the Hellenic Greek Corporate Governance Code. Another interesting piece of evidence that arose from

data collection has to do with the fact that the number of independent nonexecutive members is almost

half the number of all nonexecutive members. Moreover, according to the Corporate Governance

Review 2012 and Corporate Governance Review 2011 conducted by Grant Thornton Greece, the overall

number of nonexecutive members has remained stable since 2011.

6.3 Presence of women on Board of Directors

Findex

Analysis:

As it can be seen from special practice 2.8 of the HCGC, there is no specific pretext that gives a definite

number of women on Board of Directors. However, companies are called upon to present and explain

0 0.2 0.4 0.6 0.8 1 1.2 1.4

Women on Board of Directors (average number of women per Board)

Companies with Foreign Investors'Participation

Companies with the Greek State'sparticipation

All companies

“The diversity policy including, gender balance, for board members, as adopted by the board, shall be published on the company’s website. The corporate governance statement shall make specific reference to the diversity policy applied by the company in relation to the composition of its board and the percentage of each gender represented on board and senior executive team.” (Hellenic Corporate Governance Code, Special Practice 2.8)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

10

their diversity strategy, which implies putting them on the spot for the sadly small number of women on

their Board of directors. The same separation as in the previous two sections exists.

The average number of women on Board of Directors is 1 which is a very low and dissatisfying number

given that this number is kept relatively stable in the past years while at the same time the number of

Board members is on the rise. What is more, many out of the 25 women on the Board of Directors seem

to be somehow related to the President of the Board. There are cases in which the only woman on the

Board of Director is the wife of the President of the Board who also happens to be the major

shareholder of the company. In addition, none of the companies is close to achieving the target of the

European Commission for gender equality, namely for women to comprise close to 40% of the

nonexecutive Board members. Lastly, there are nine (9) companies in the FTSE/Athex Large Cap which

have no women on their Boards. With that in mind, and also looking at the blue relative to the red

category, there are reasons to believe that the already low percentage of women on the Board (8.5%)

could be even lower if the Greek government chooses to proceed with the policy of privatization, as the

Greek State is responsible for allocating most of the women on the Boards it influences.

All in all, women on the Board of Directors are very few in number. Companies should be encouraged to

increase their numbers of women. The above numbers for the Greek market are considerably lower

than those in other European Markets. Therefore, the Greek State, in association with the European

Commission should attempt to incentivize shareholders and companies towards nominating and

including more women as members of the Board of Directors.

6.4 Publication of the size and composition of the Board on the Corporate

Governance statement

Analysis:

All the companies included in the sample publish in their Corporate Government Statements the

composition of the Board of Directors, the names of the Board’s members and the names of the

Committees of the Board. Lastly, all companies determine the number of nonexecutive members on the

Board.

“A corporate governance statement included in the annual report should provide information on

the board’s composition and include the names of the chairman, the vice-chairman, the chief

executive, as well as the heads and members of all board committees and the company Secretary.

In addition, the Statement shall name the non-executive members the board considers to be

independent.” (Hellenic Corporate Governance Code, Special Practice 2.6)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

11

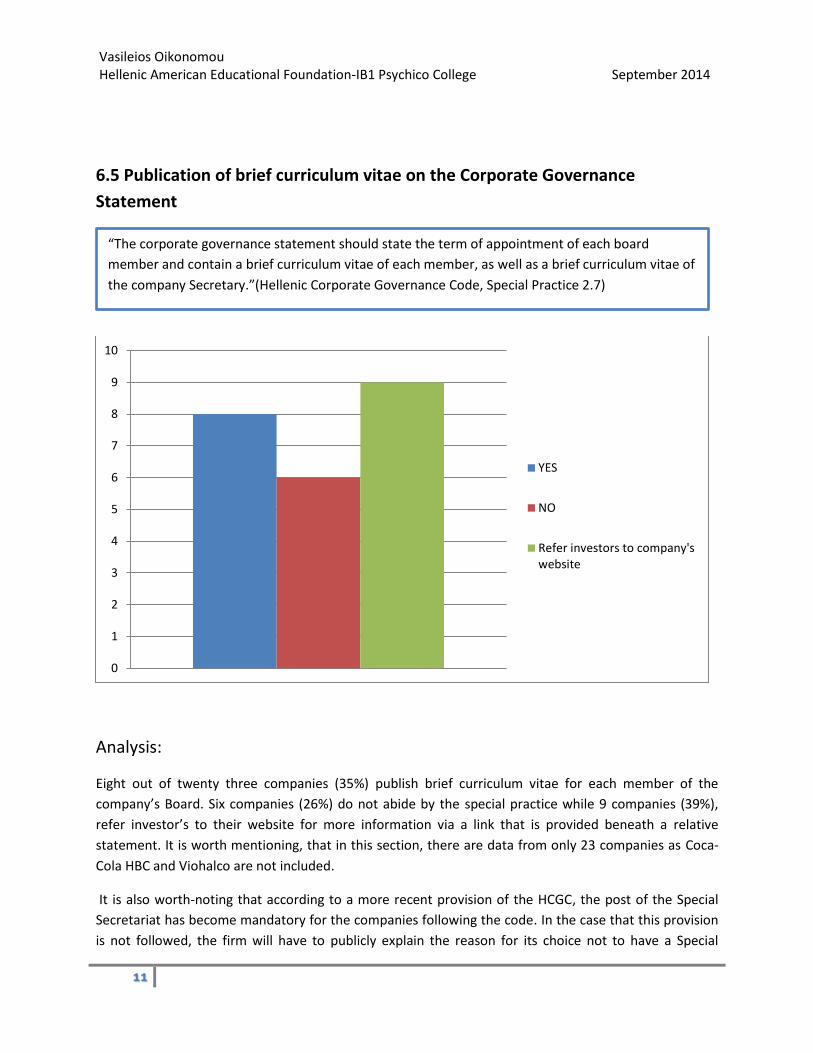

6.5 Publication of brief curriculum vitae on the Corporate Governance

Statement

Analysis:

Eight out of twenty three companies (35%) publish brief curriculum vitae for each member of the

company’s Board. Six companies (26%) do not abide by the special practice while 9 companies (39%),

refer investor’s to their website for more information via a link that is provided beneath a relative

statement. It is worth mentioning, that in this section, there are data from only 23 companies as Coca-

Cola HBC and Viohalco are not included.

It is also worth-noting that according to a more recent provision of the HCGC, the post of the Special

Secretariat has become mandatory for the companies following the code. In the case that this provision

is not followed, the firm will have to publicly explain the reason for its choice not to have a Special

0

1

2

3

4

5

6

7

8

9

10

YES

NO

Refer investors to company'swebsite

“The corporate governance statement should state the term of appointment of each board

member and contain a brief curriculum vitae of each member, as well as a brief curriculum vitae of

the company Secretary.”(Hellenic Corporate Governance Code, Special Practice 2.7)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

12

Secretariat. According to the research made, of the 25 companies of the sample, 8 of them have

established a Special Secretariat whilst only 4 of them publish his/her curriculum vitae.

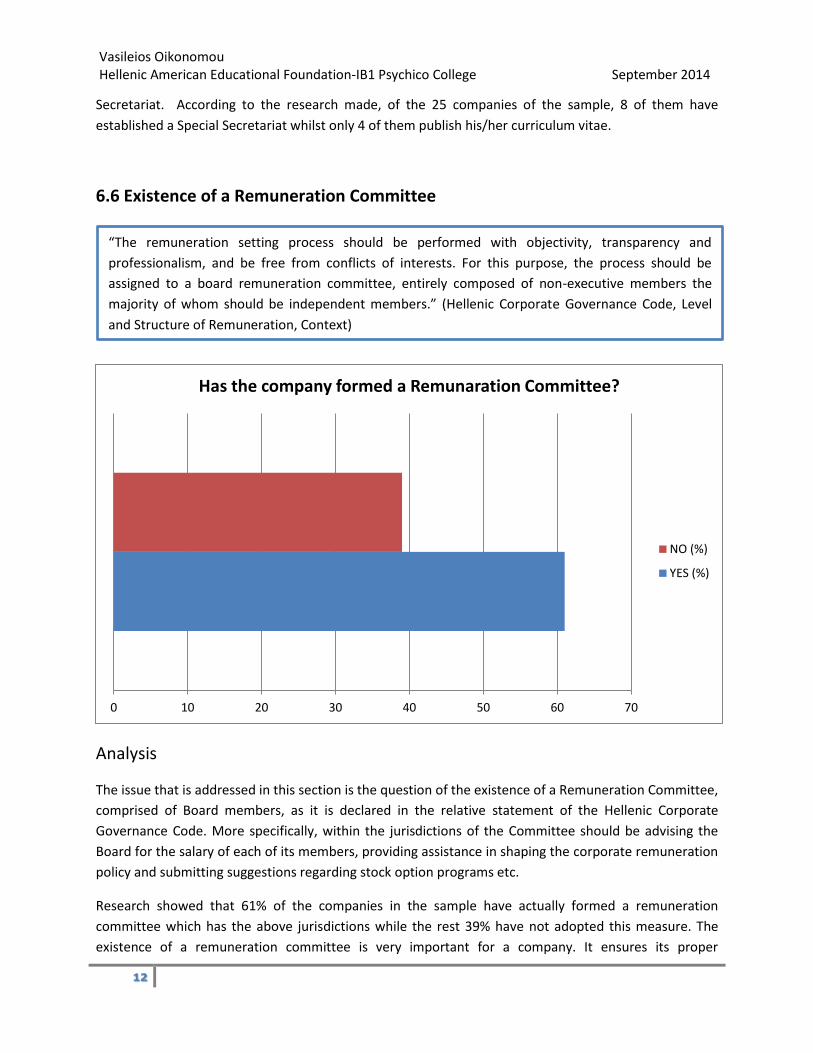

6.6 Existence of a Remuneration Committee

Analysis

The issue that is addressed in this section is the question of the existence of a Remuneration Committee,

comprised of Board members, as it is declared in the relative statement of the Hellenic Corporate

Governance Code. More specifically, within the jurisdictions of the Committee should be advising the

Board for the salary of each of its members, providing assistance in shaping the corporate remuneration

policy and submitting suggestions regarding stock option programs etc.

Research showed that 61% of the companies in the sample have actually formed a remuneration

committee which has the above jurisdictions while the rest 39% have not adopted this measure. The

existence of a remuneration committee is very important for a company. It ensures its proper

0 10 20 30 40 50 60 70

Has the company formed a Remunaration Committee?

NO (%)

YES (%)

“The remuneration setting process should be performed with objectivity, transparency and

professionalism, and be free from conflicts of interests. For this purpose, the process should be

assigned to a board remuneration committee, entirely composed of non-executive members the

majority of whom should be independent members.” (Hellenic Corporate Governance Code, Level

and Structure of Remuneration, Context)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

13

functioning and the alignment of the interests of senior management with those of the shareholders.

Unfortunately, although the majority of companies have complied with the provisions of the HCGC,

there is still a sizeable minority, which does not do so.

6.7 Remuneration Disclosure

Analysis:

According to the above practice taken by the Hellenic Corporate Governance Code, listed companies

should publish the remuneration of each of their Board Members. This should include, the wage,

bonuses and compensations that each member receives for his participation on Board Committees or

any other services that he provides to the company.

Research conducted on the above issue showed that no company publishes the remuneration of its

members according to the requirements provided by the Hellenic Corporate Governance Code. In the

past few years, this practice of the HCGC has been much debated as some critics of the above provision

suggest that disclosing such information regarding the remuneration of the Board members constitutes

a violation of their privacy and leaves them exposed to public malpractice.

“The remuneration report of board members should be part of the corporate governance statement.

The remuneration report for the financial year should contain:

the policy and principles of the company on executive remuneration;

the method of assessing performance and calculating variable compensation for board

members, including the qualitative and quantitative performance criteria used;

the main elements of the individual board member service contracts, including duration of

the contract;

the total remuneration paid to each board member during the year for their services in the

company and its affiliates, broken down into salary, bonuses, eventual severance payments,

as well as a description of the type and amount of any other awards or benefits granted;

the number of shares and stock options granted to individual board members during the

financial year, including vesting, exercise and expiry dates, options price, as well as the

number of such rights exercised.” (Hellenic Corporate Governance Code, Special Practice

1.11)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

14

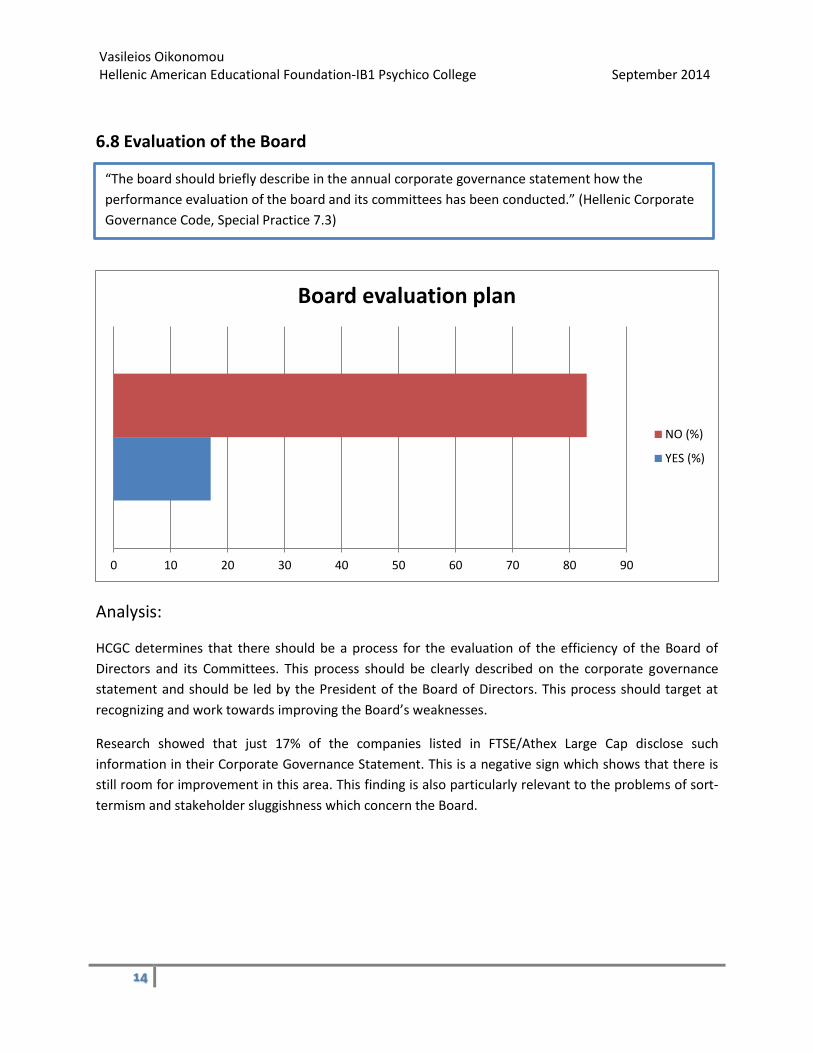

6.8 Evaluation of the Board

Analysis:

HCGC determines that there should be a process for the evaluation of the efficiency of the Board of

Directors and its Committees. This process should be clearly described on the corporate governance

statement and should be led by the President of the Board of Directors. This process should target at

recognizing and work towards improving the Board’s weaknesses.

Research showed that just 17% of the companies listed in FTSE/Athex Large Cap disclose such

information in their Corporate Governance Statement. This is a negative sign which shows that there is

still room for improvement in this area. This finding is also particularly relevant to the problems of sort-

termism and stakeholder sluggishness which concern the Board.

0 10 20 30 40 50 60 70 80 90

Board evaluation plan

NO (%)

YES (%)

“The board should briefly describe in the annual corporate governance statement how the

performance evaluation of the board and its committees has been conducted.” (Hellenic Corporate

Governance Code, Special Practice 7.3)

Vasileios Oikonomou Hellenic American Educational Foundation-IB1 Psychico College September 2014

15

Conclusion

The current Corporate Governance Review 2013 has brought to light evidence that highlight both

improvements to the current state of Corporate Governance in Greece but also weaknesses that persist

from previous years. As an overall observation, companies seem to abide by the spirit of the HCGC

regarding issues that concern the proper functioning of the Board, although there are major steps that

should be taken to ensure gender diversity and stronger women’s presence in places of senior

management. Additionally, it seems that most companies have not yet adopted the advised measures to

engage their shareholders in issues of Corporate Governance and especially those relative to the

remuneration of the Board. Nevertheless, Corporate Governance seems to be more important than ever

and should take priority as it is a potent tool in preserving transparency and accountability in today’s

business world.

Bibliography

1. http://www.bloomberg.com/quote/FTASE:IND

2. http://www.helex.gr/web/guest/esed-hellenic-cgc

3. http://www.ecgi.org/tcgd/2012/documents/121212_company-law-corporate-governance-

action-plan_en.pdf

4. http://europa.eu/rapid/press-release_MEMO-12-972_el.htm

5. Corporate Governance Review 2012, Grant Thornton Greece