Embed Size (px)

Citation preview

BISA School Meeting, Autumn 2012

Prof. Stefania Servalli

1

BUSINESS ETHICS AND CORPORATE GOVERNANCE

Corporate Governance weaknesses and failures

BISA School Meeting, Autumn 2012

AimThis lecture considers ways in whichcorporate governance weaknesses havecontributed to corporate failure.

Enron as case study.Watch this film “The smartest guys inthe room"http://watchdocumentaries.com/enron-the-smartest-guys-in-the-room/

BISA School Meeting, Autumn 2012

CG and Corporate FailureThe Collapse of Enron

Enron:• Energy company based in Houston• Created by Kenneth Lay in 1985

• CEO was Jeffrey Skilling

BISA School Meeting, Autumn 2012

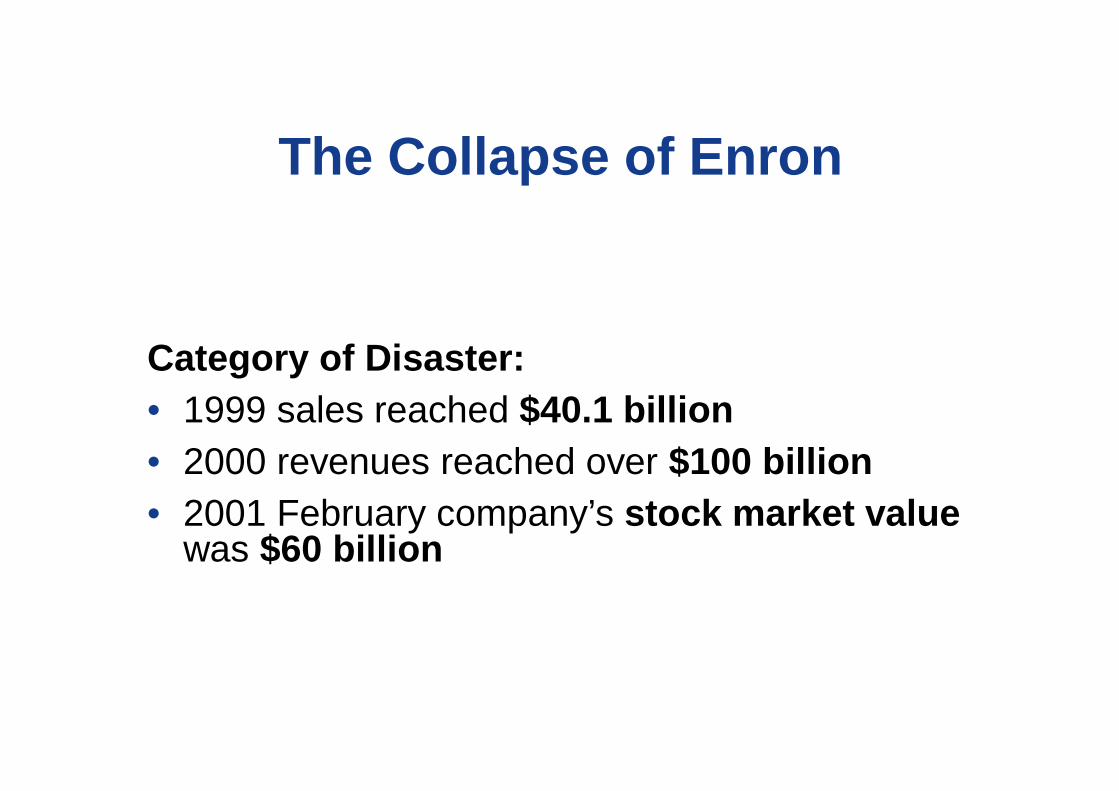

The Collapse of Enron

Category of Disaster:• 1999 sales reached $40.1 billion• 2000 revenues reached over $100 billion• 2001 February company’s stock market value

was $60 billion

BISA School Meeting, Autumn 2012

The Collapse of EnronEnron:• In 16 years: from a small company to the world’s largest energy trading company

In 2001 they changed the words over the main door in Houston from

The world’s leading energy companyto

The world’s leading company

BISA School Meeting, Autumn 2012

The Collapse of EnronEnron:• Handling risk management derivatives• Weather derivatives were invented by Enron (1997)

“Weather derivatives had aninauspicious start: the firsttrade was done by Enron in1997. The instruments wereinitially used by American energycompanies to hedge against theeffect that unseasonaltemperatures could have on gassales.”

4th February 2012

BISA School Meeting, Autumn 2012

The Collapse of EnronEnron:• Online platform was adopted for trading

(Enrononline) with a great success (1999)

From an energy company

to a financial and energy trading company

BISA School Meeting, Autumn 2012

BISA School Meeting, Autumn 2012

BISA School Meeting, Autumn 2012

BISA School Meeting, Autumn 2012

• August 2001• Jeffrey Skilling (CEO) left the company

• October 2001• Enron’s shares fell by 19%

• November 2001• S&P downgraded Enron’s debt to junk bond

status

BISA School Meeting, Autumn 2012

• Nevertheless … (1st November 2001)

BISA School Meeting, Autumn 2012

• Nevertheless … (1st November 2001)

BISA School Meeting, Autumn 2012

But …

• December 2001• Enron filed for bankruptcy

• January 2002• Kenneth Lay resigned

BISA School Meeting, Autumn 2012

• January 2002

• Arthur Andersen fired partner in charge of Enron’s audit, David Duncan, for ordering disposal of documents

• March 2002

• Berardino resigned as chief executive of Andersen

• October 2002

• Andrew Fastow, former finance director of Enron, charged with: money laundering, wire and mail fraud, conspiracy to inflate profits to enrich himself

BISA School Meeting, Autumn 2012

Enron’s devious accounting

• Recorded profits from a joint venture with Blockbuster Video that never materialize

• One ‘special purpose’ vehicle, Chewco, created by Enron to offload liabilities for off-balance-sheet financing purposes

Accounting fraud!

BISA School Meeting, Autumn 2012

Reasons of disaster?

• Exaggerated focus on EPS (its main aim as declared in 2000 financial report)

Considering CG Theory, what’s the risk?

Short-termism and temptation to cheat!

BISA School Meeting, Autumn 2012

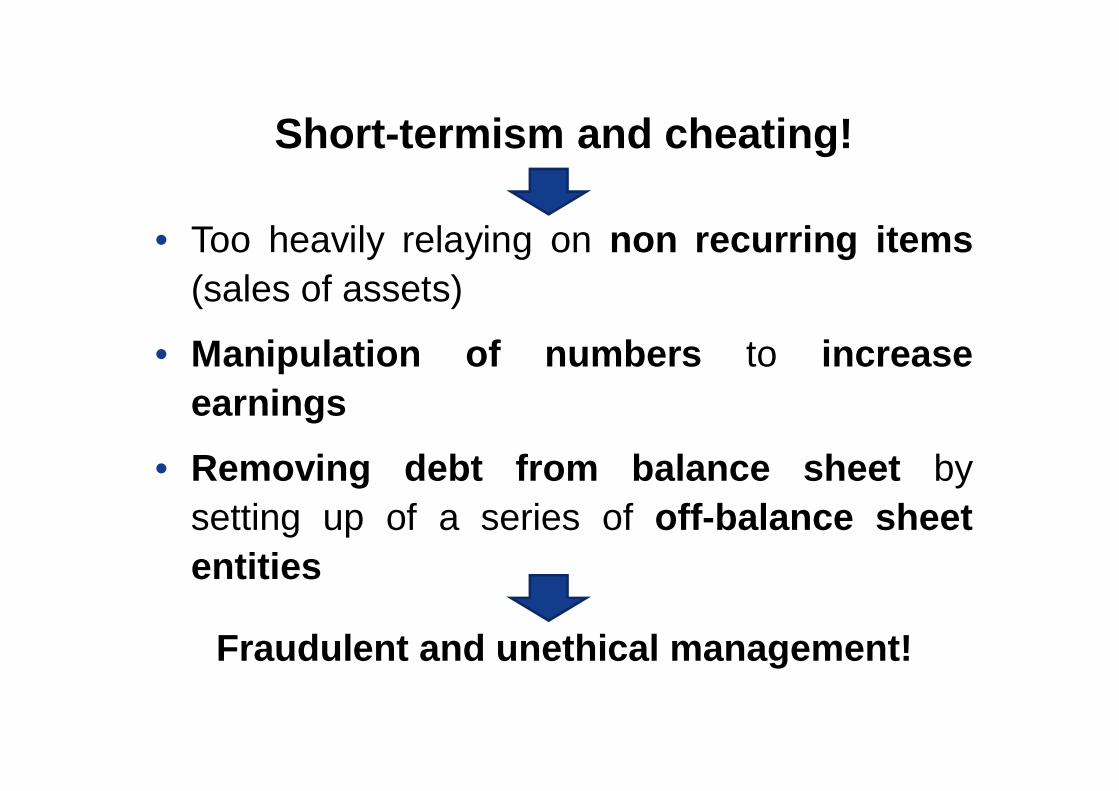

Short-termism and cheating!

• Too heavily relaying on non recurring items(sales of assets)

• Manipulation of numbers to increaseearnings

• Removing debt from balance sheet bysetting up of a series of off-balance sheetentities

Fraudulent and unethical management!

BISA School Meeting, Autumn 2012

Fraudulent and unethical management!

• In addition …Top executive sold over 1 billion $of Enron shares to other investors

… Insider trading!Information asymmetry

Agency problems

BISA School Meeting, Autumn 2012

And what about internal and external auditors?

Internal auditor:• IA was a weak function.

Why? • Chairman of IA Committee Wendy Gramm was the wife

of Senator Philip Gramm who received huge politicaldonations from Enron;

• Lord Wakeham of the IA Committee had a consultancycontract

Conflict of interests, not independent!

BISA School Meeting, Autumn 2012

External auditor:

• Strong conflict of interest:25$million audit + 27$million for consultancy

• Familiarity with top executives

• Overlooked effects on the financialreporting of some operations

• Shredded the documents of the audit

BISA School Meeting, Autumn 2012

The Enron Trial• January 2006 Trials of top ex-directors began• Federal investigators were convinced top

directors:• responsible for use of creative accounting to

conceal debt and massage reported profits

• 25th May 2006 Lay and Skilling wereconvicted on fraud charges– Lay found guilty on all six charges of fraud and

conspiracy– Skilling found guilty on 19 charges of fraud,

conspiracy, insider trading and making falsestatements

BISA School Meeting, Autumn 2012

The Enron Trial

BISA School Meeting, Autumn 2012

The Enron Trial

Kenneth Lay:Died before the final sentence

Jeffrey Skilling: conviction of 14 years

BISA School Meeting, Autumn 2012

Effects on Accounting Profession

Carnegie, G.D. & Napier C.J. (2010),Traditional accountants and businessprofessionals: Portraying the accountingprofession after Enron, Accounting,Organizations and Society, Volume 35,Issue 3, pp. 360-376.

BISA School Meeting, Autumn 2012

Effects on Accounting ProfessionAbstract

Society’s perception of the legitimacy of the accounting profession and itsmembers is grounded in the verbal and visual images of accountants thatare projected not only by accountants themselves but also by the media.The paper uses the critical literature on stereotypes to examine how bookswritten for a general readership on Enron and other recent corporatefailures portray accountants and accounting, and the implications theirauthors draw for corporate governance and the survival of the financialsystem. The paper explores how commentators have analyzed the changingactivities of accountants (including the rise of consulting) and havecontrasted the personalities of “founding fathers” of the US accountingprofession with their early 21st-century successors. The paper concludesthat changing stereotypes of accountants are evidence of “negativesignals of movement” for accounting as a profession.

BISA School Meeting, Autumn 2012

Themes identified by Carnegie & Napier

• The character of accountants

• Honesty, integrity and trust

• The shredding of integrity

BISA School Meeting, Autumn 2012

The character of accountants

• Old stereotypes:– Bean-counter, boring technocrat with green

eyeshades– Honesty, integrity, competence

• New images:– Youth and aggressiveness, backslapping

BISA School Meeting, Autumn 2012

• Specific contrast:– Carl Bass (Andersen technical

partner) “by-the-book, resolutely cheerless”

– David Duncan (Andersen engagement partner) “party boy”, “sharply handsome”

The character of accountants

BISA School Meeting, Autumn 2012

Honesty, integrity and trust• Integrity as key characteristic of accountants in the

past• Accountants (Auditors) of 1990s not persons of

integrity?– “In the end, it was all about the bucks. . . . The four

cornerstones of success at Andersen – peoplemanagement, quality, thought leadership and financialperformance – were referred to colloquially as ‘threepebbles and a boulder’. The boulder was financialperformance. The rest, it seemed, was a joke.” [Toffler]

PeeblePeople mgmt

QualityThought Leadership

BoulderFinancial Performance

BISA School Meeting, Autumn 2012

The shredding of integrity

• Shredding of integrity as a powerful image:– “The Enron story shifted from a reasonably contained accounting scandal to a full-blown,

all-American morality play . . . reduced to a few simple elements that anyone couldunderstand, i.e., greedy executives live large while duping loyal employees and unwittingshareholders.” [Swartz, 2003]

[Swartz, M. (2003). Power failure: The rise and fall of Enron. London: Aurum Press]

• Auditors: Serving the public interest vs pleasing the client

• ‘‘Enron prompted Congress to wonder if accountant werecorrupt. WorldCom prompted Congress to wonder ifaccountants were incompetent” Brewster (2003, p.283)

[Brewster, N. (2003). Unaccountable: How the accounting profession forfeited a public trust. Hoboken: John Wiley]

BISA School Meeting, Autumn 2012

CG problems in Enron

• Excutive and non-excutive:– Unfettered power in the hand of the chief

executive– Non-executive directors ineffective– Poor moral character of directors, willing

to fraud– Lack of understanding of risk and

derivatives used

BISA School Meeting, Autumn 2012

• Management:Enron Trader:

“All the money you guys stole from the poor grandmothers?”

***

Enron Trader:

“You just steal money from California to the tune of a million bucks or two a day”

Enron Trader:

“Can we rephrase that?”

Audacity, Ambition, Arrogance

CG problems in Enron

BISA School Meeting, Autumn 2012

CG problems in Enron

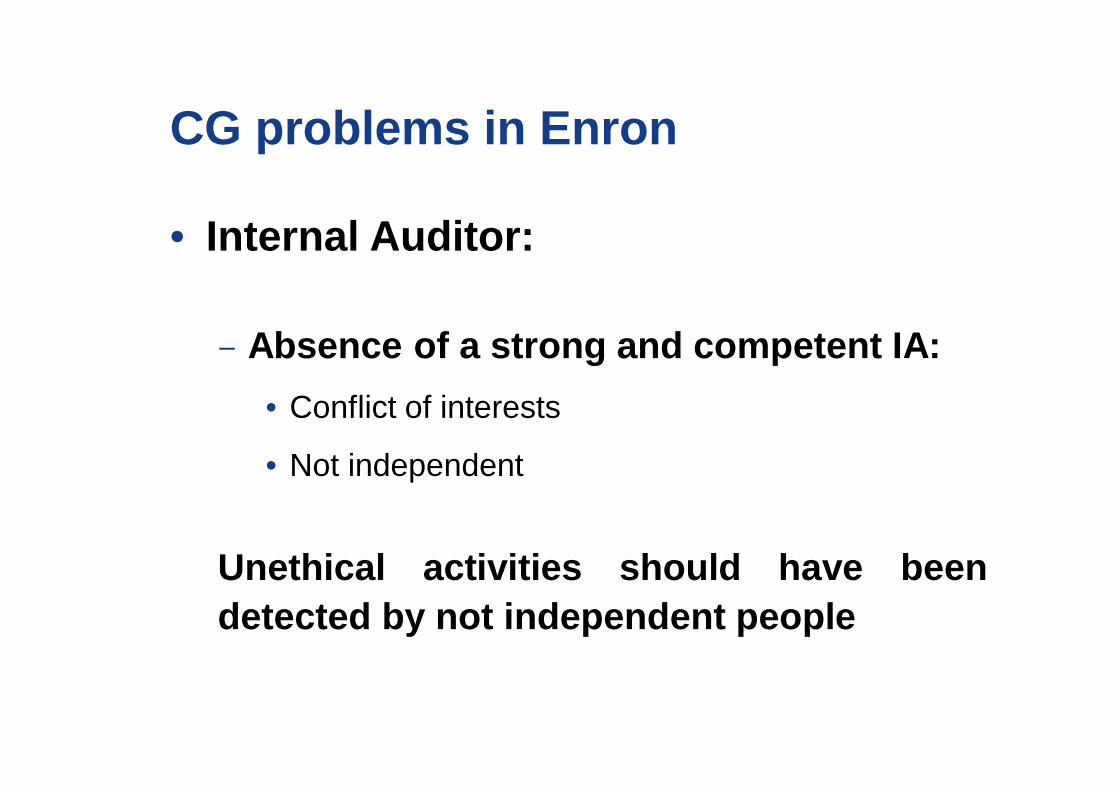

• Internal Auditor:

– Absence of a strong and competent IA:• Conflict of interests

• Not independent

Unethical activities should have beendetected by not independent people

BISA School Meeting, Autumn 2012

CG problems in Enron

• External Auditor:

– Conflict of interests: audit + consultancyservices

– Familiarity

– Destruction of documents

Opinion on financial reports should haveexpressed by people with conflict ofinterests

BISA School Meeting, Autumn 2012

After Enron• 2002 Sarbanes-Oxley Act

Regulated approach to CG problems

Other countries principle approach (UK)

But, remember …

• No matter how many mechanisms are in place to ensure that companies are run in an accountable manner, people at the top can act unethically

CG checks and balances can detect unethical behaviour not cure them

BISA School Meeting, Autumn 2012

Concluding

https://www.youtube.com/watch?v=vtpDFTm-fOA

What is it?

The segment at the end of the Enron commercials

Did they ask why?

BISA School Meeting, Autumn 2012

Learning outcomesexplain the contribution of CG weaknesses to

corporate failure

discuss different CG aspect involved in Enron collapse

References• Solomon (2013),Corporate Governance and Accountability, Chapter 2.

• Carnegie, G.D. & Napier C.J. (2010), Traditional accountants and business professionals: Portraying the accounting profession after Enron, Accounting, Organizations and Society, Volume 35, Issue 3, pp. 360-376.

![Insull Enron SSRN - The Wall Street Journal2005] FROM INSULL TO ENRON 35 FROM INSULL TO ENRON: CORPORATE (RE)REGULATION AFTER THE RISE AND FALL OF TWO ENERGY ICONS …](https://img.pdfslide.net/doc/110x75/60acd17a67674c75da294203/insull-enron-ssrn-the-wall-street-journal-2005-from-insull-to-enron-35-from-insull.jpg)

![[Enron] New hire welcome binder (policies, org chart, tips, etc.)mattmg83.github.io/cynicalcapitalist/documents/[Enron... · 2019-09-27 · Enron Operator (71)853·6161 Enron Voice](https://img.pdfslide.net/doc/110x75/5f1e01293cf2d927c4643421/enron-new-hire-welcome-binder-policies-org-chart-tips-etc-enron-2019-09-27.jpg)