Embed Size (px)

Citation preview

0

July, 2017

Corporate

Presentation

1 1

Disclaimer

This presentation may contain financial or business projections regarding recent acquisitions, their

financial or business impact, management expectations and objectives regarding such acquisitions and

current management expectations on the operating and financial performance of The Company, based

on assumptions that, as of today, are considered valid. Financial and business projections are

estimates and do not constitute any declaration of historical facts. Words such as “anticipates”,

“could”, “may”, “can”, “plans”, “believes”, “estimates”, “expects”, “projects”, “pretends”, “probable”,

“will”, “should”, and any other similar expression or word with a similar meaning pretend to identify

such expressions as projections. It is uncertain if the anticipated events will happen and in case they

happen, the impact they may have in Alicorp’s or The Consolidated Company’s operating and financial

results. Alicorp does not assume any obligation to update any financial or business projections

included in this presentation to reflect events or circumstances that may happen.

2

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

2

Our Strategy for creating value 2

3

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

3

Our Strategy for creating value 2

4

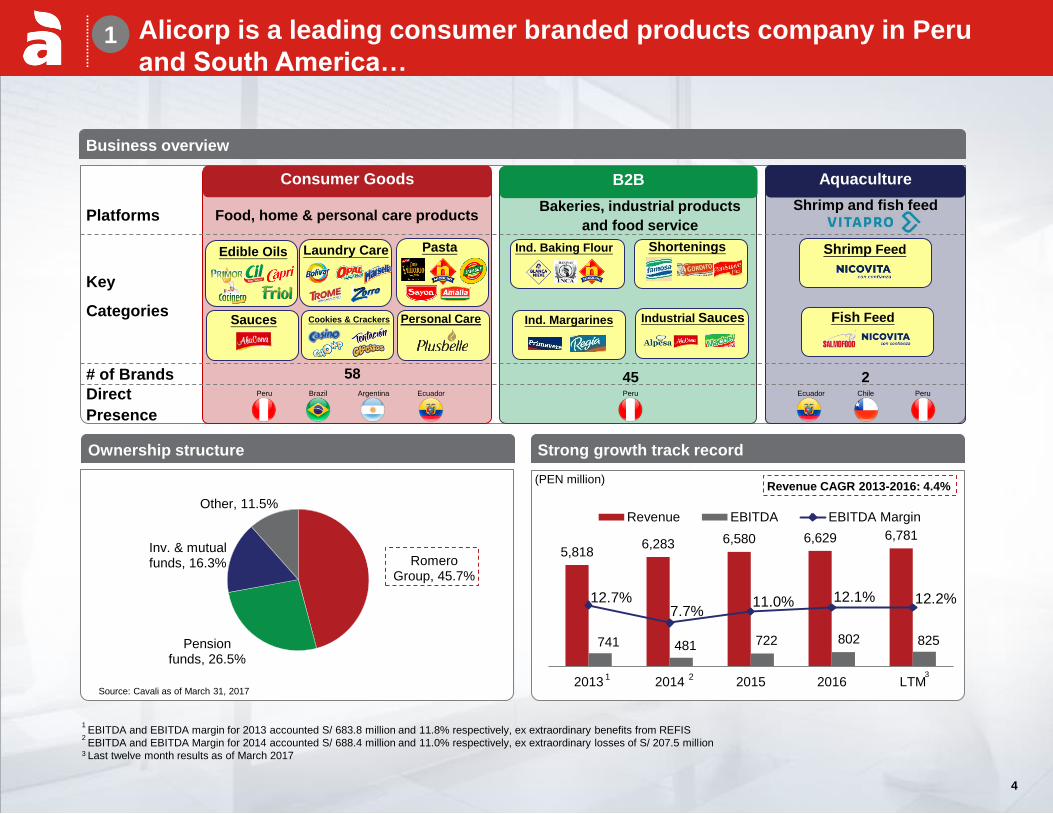

Romero Group, 45.7%

Pension funds, 26.5%

Inv. & mutual funds, 16.3%

Other, 11.5%

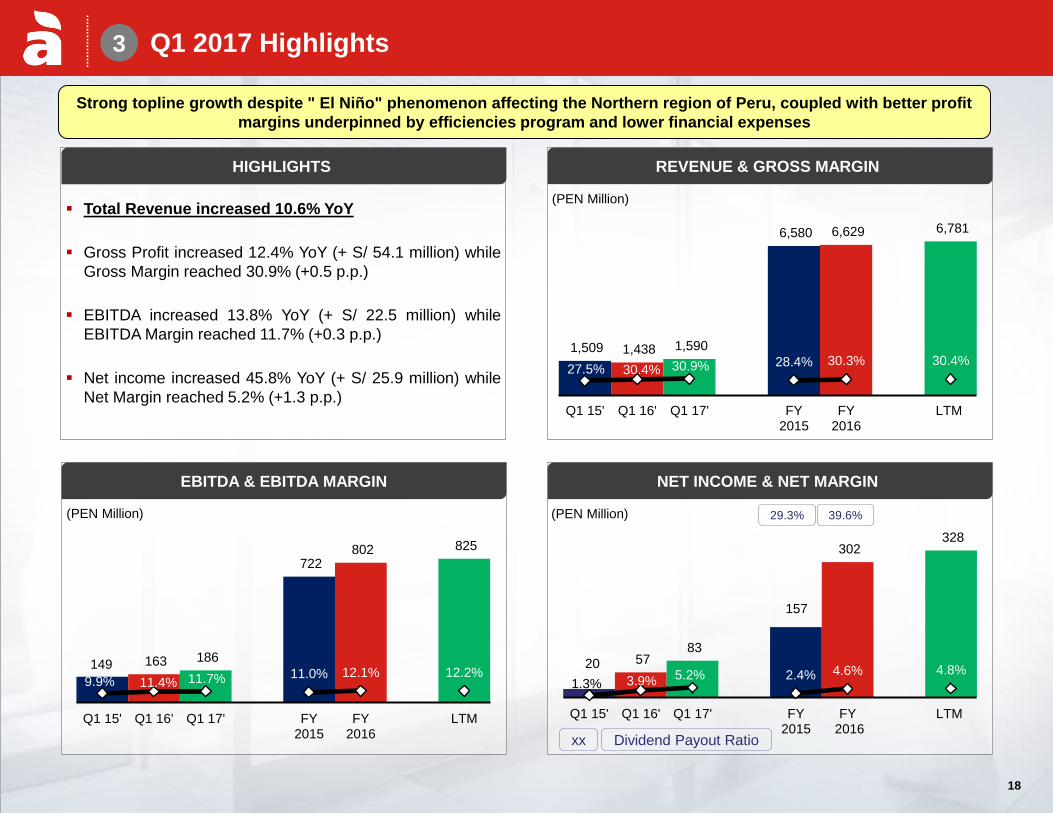

5,818 6,283 6,580 6,629 6,781

741 481 722 802 825

12.7% 7.7%

11.0% 12.1% 12.2%

2013 2014 2015 2016 LTM

Revenue EBITDA EBITDA Margin

Ownership structure

Business overview

Strong growth track record

(PEN million)

1 EBITDA and EBITDA margin for 2013 accounted S/ 683.8 million and 11.8% respectively, ex extraordinary benefits from REFIS

2 EBITDA and EBITDA Margin for 2014 accounted S/ 688.4 million and 11.0% respectively, ex extraordinary losses of S/ 207.5 million

3 Last twelve month results as of March 2017

Source: Cavali as of March 31, 2017

Key

Categories

Edible Oils Laundry Care

Sauces Cookies & Crackers

Platforms Food, home & personal care products

# of Brands

Direct

Presence

Consumer Goods

Bakeries, industrial products

and food service

Shrimp and fish feed

45 2

Ind. Baking Flour Shortenings

Ind. Margarines Industrial Sauces

Shrimp Feed

Fish Feed

B2B Aquaculture

Pasta

Peru Argentina Ecuador Brazil Ecuador Peru Chile Peru

Personal Care

Revenue CAGR 2013-2016: 4.4%

58

2 1 3

Alicorp is a leading consumer branded products company in Peru

and South America…

4

1

5

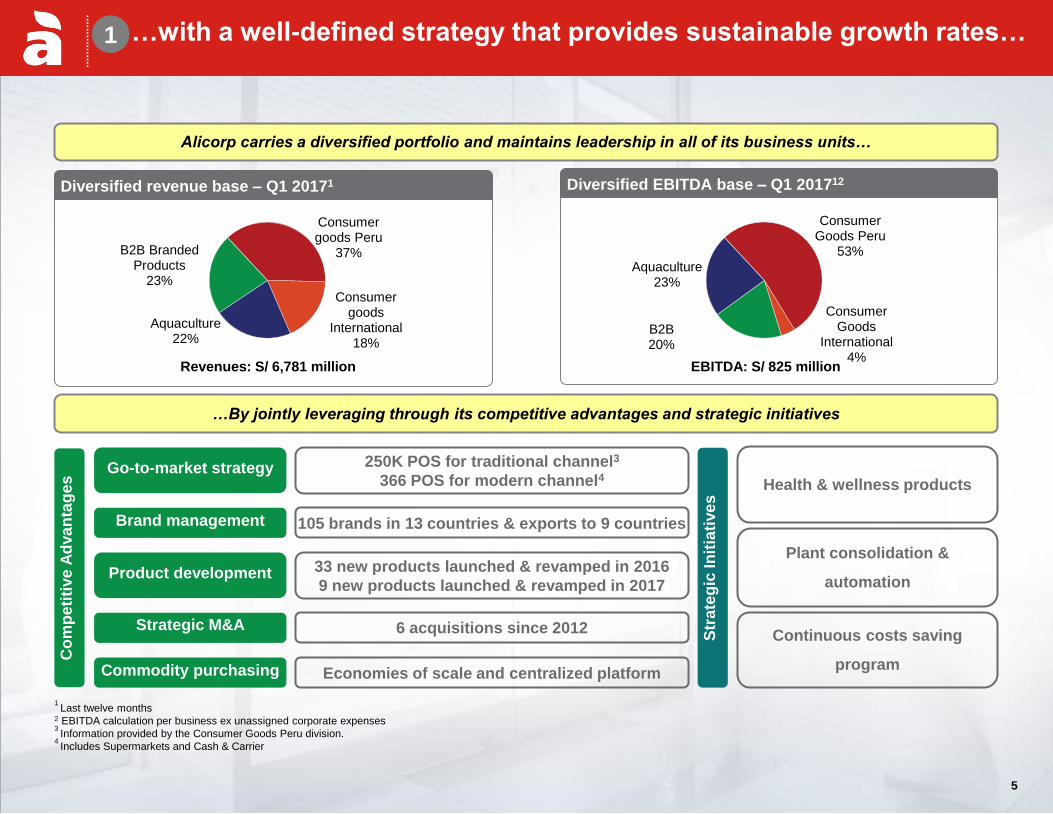

Consumer Goods Peru

53%

Consumer Goods

International 4%

B2B 20%

Aquaculture 23%

Consumer goods Peru

37%

Consumer goods

International 18%

Aquaculture 22%

B2B Branded Products

23%

Commodity purchasing

Go-to-market strategy

Brand management

Strategic M&A

Product development

105 brands in 13 countries & exports to 9 countries

33 new products launched & revamped in 2016

9 new products launched & revamped in 2017

Economies of scale and centralized platform

…By jointly leveraging through its competitive advantages and strategic initiatives

250K POS for traditional channel3

366 POS for modern channel4

6 acquisitions since 2012

Health & wellness products

Plant consolidation &

automation

Continuous costs saving

program

Co

mp

eti

tive

Ad

va

nta

ges

Str

ate

gic

In

itia

tive

s

Diversified revenue base – Q1 20171

Revenues: S/ 6,781 million EBITDA: S/ 825 million

Diversified EBITDA base – Q1 201712

Alicorp carries a diversified portfolio and maintains leadership in all of its business units…

1 Last twelve months

2 EBITDA calculation per business ex unassigned corporate expenses 3 Information provided by the Consumer Goods Peru division.

4 Includes Supermarkets and Cash & Carrier

…with a well-defined strategy that provides sustainable growth rates…

5

1

6

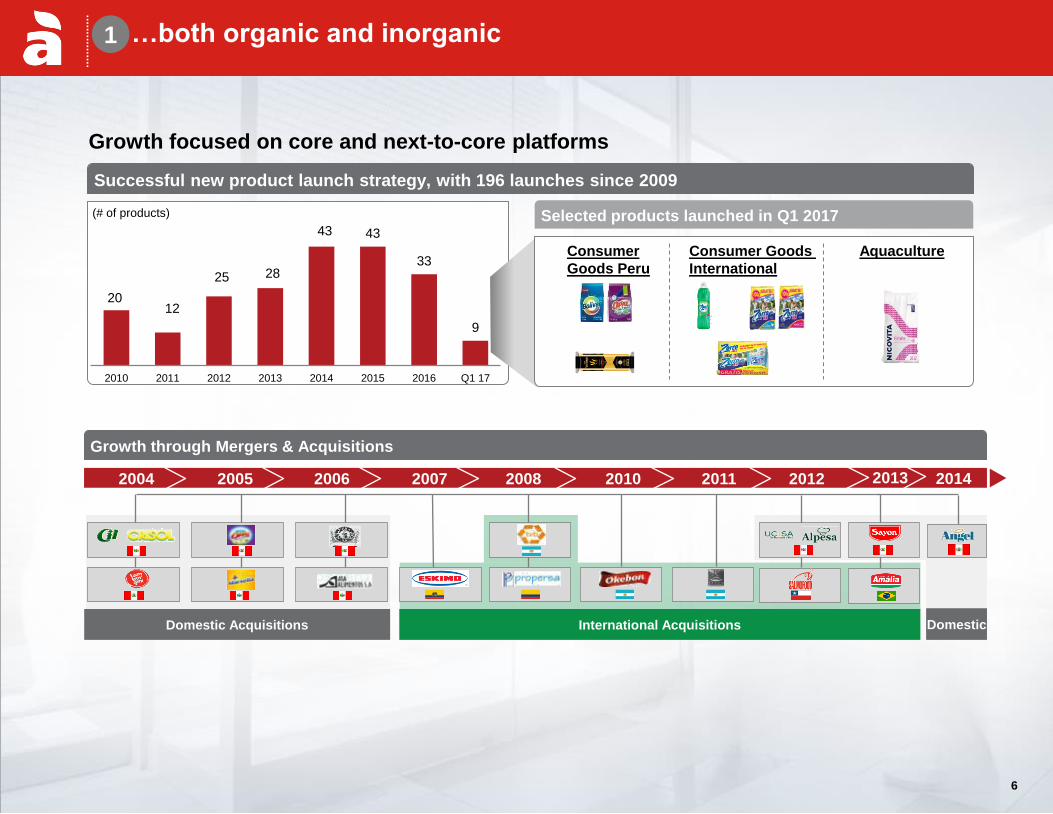

20 12

25 28

43 43

33

9

2010 2011 2012 2013 2014 2015 2016 Q1 17

Selected products launched in Q1 2017

Successful new product launch strategy, with 196 launches since 2009

Growth through Mergers & Acquisitions

International Acquisitions Domestic Acquisitions

2012 2004 2005 2006 2007 2008 2010 2011

Growth focused on core and next-to-core platforms

Consumer

Goods Peru

Consumer Goods

International

(# of products)

2013 2014

Domestic

…both organic and inorganic

Aquaculture

6

1

7

Alicorp is the leading consumer goods company, competing with global and local players, such as

Procter & Gamble, Unilever, Mondelez, Nestle, Carozzi, among others

1 Alicorp has +50% of the market share. 2 Based on consolidate Revenue of the last twelve months as of March 2017. 3 LTM as of March 2017. Calculation per business ex unassigned corporate expenses

Ranked #1 in over 10 product categories1

33.9% 53.1% Source: Kantar World Panel

In Consumer Goods Peru (CGP), we are market leaders in almost every

category in which we participate

Category Brands Position % of sales2 % of EBITDA3 Competitors

Laundry Detergents #1 8.0% 18.9%

Edible Oils #1 7.9% 9.7%

Pasta #1 5.6% 7.4%

Cookies & Crackers #1 3.7% -0.8%

Mayonnaise #1 2.8% 6.5%

Laundry Soap #1 2.0% 4.5%

Cereals #1 1.4% 1.9%

Margarines #1 1.2% 2.4%

Household Flour #1 1.0% 2.3%

Juice Powders #1 0.3% 0.3%

7

1

8

1Includes Detergents and Laundry Soap

Pre

miu

m

Ma

ins

trea

m

Va

lue

Market and customer segmentation allows a more efficient pricing process and pass-through of

commodities price increases

Product classification

Edible Oils Pasta Laundry Care1 Cookies & Crackers Flour

…thanks to a strategy that focuses on effective market and customer

segmentation…

8

1

9

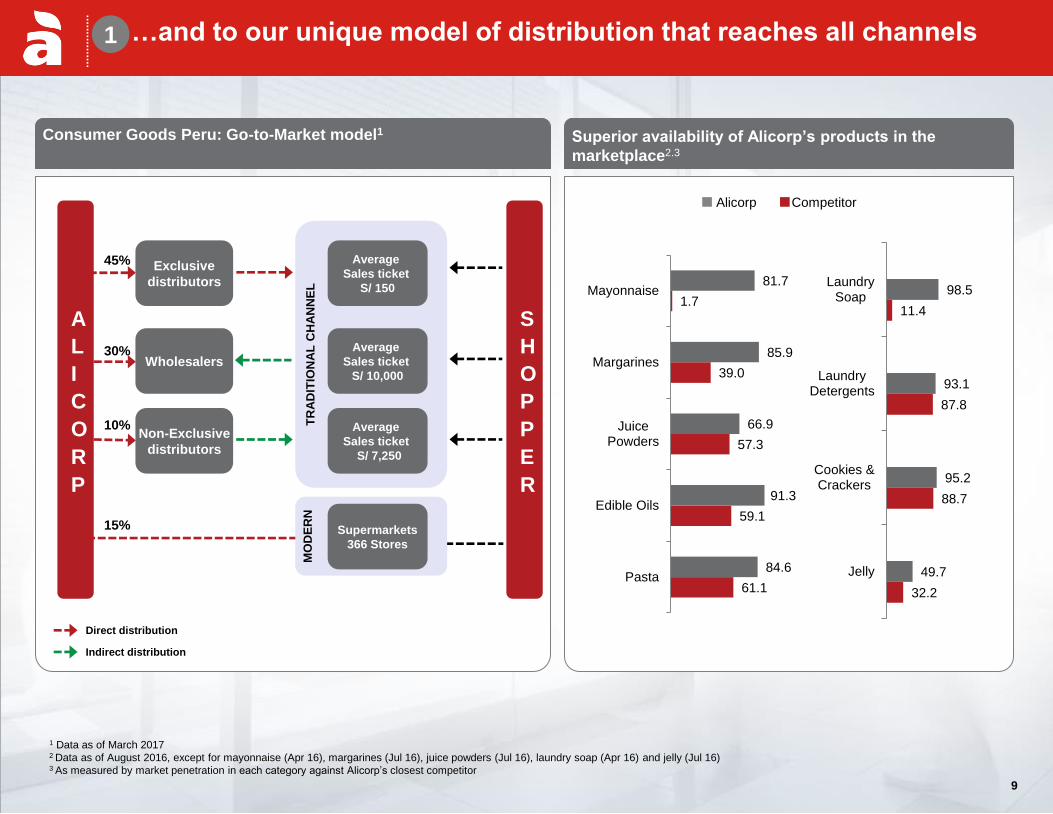

Consumer Goods Peru: Go-to-Market model1

Alicorp Competitor

1 Data as of March 2017

2 Data as of August 2016, except for mayonnaise (Apr 16), margarines (Jul 16), juice powders (Jul 16), laundry soap (Apr 16) and jelly (Jul 16) 3 As measured by market penetration in each category against Alicorp’s closest competitor

TR

AD

ITIO

NA

L C

HA

NN

EL

A

L

I

C

O

R

P

Average

Sales ticket

S/ 7,250

Average

Sales ticket

S/ 10,000

Non-Exclusive

distributors

Wholesalers

Direct distribution

Indirect distribution

S

H

O

P

P

E

R

30%

10%

15%

Superior availability of Alicorp’s products in the

marketplace2.3

MO

DE

RN

Supermarkets

366 Stores

61.1

59.1

57.3

39.0

1.7

84.6

91.3

66.9

85.9

81.7

Pasta

Edible Oils

JuicePowders

Margarines

Mayonnaise

32.2

88.7

87.8

11.4

49.7

95.2

93.1

98.5

Jelly

Cookies &Crackers

LaundryDetergents

LaundrySoap

Average

Sales ticket

S/ 150

Exclusive

distributors

45%

…and to our unique model of distribution that reaches all channels 1

9

10

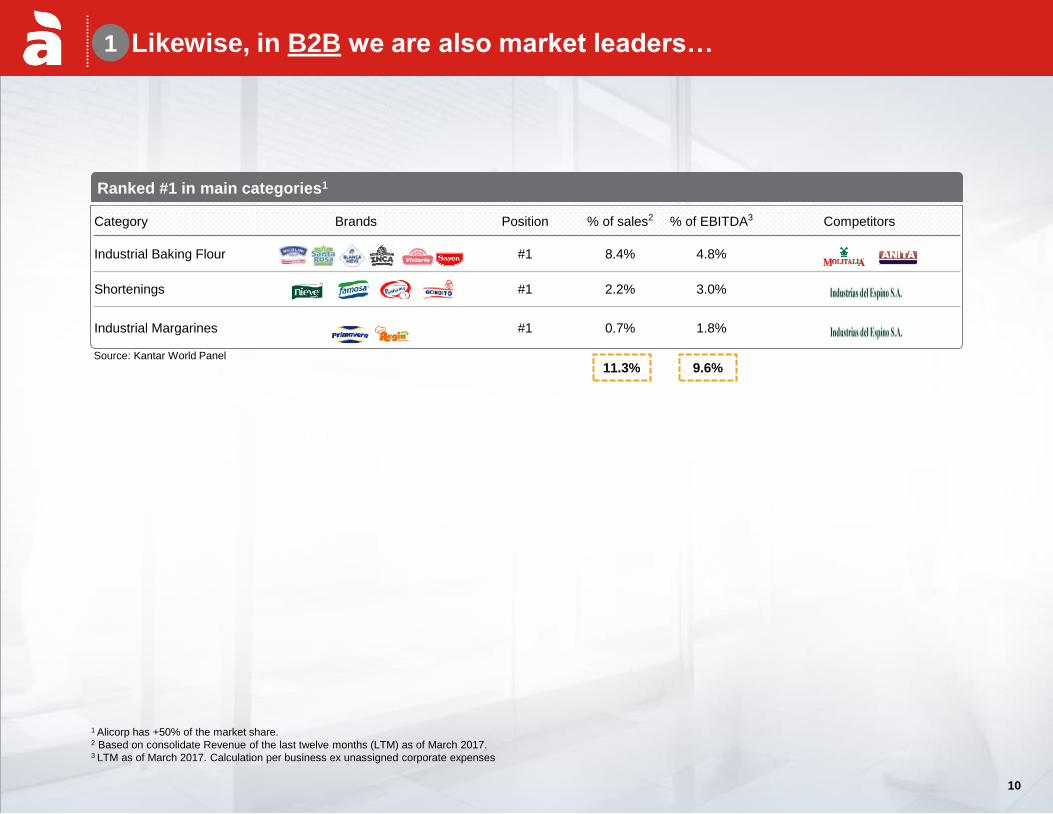

Category Brands Position % of sales2 % of EBITDA3 Competitors

Industrial Baking Flour #1 8.4% 4.8%

Shortenings #1 2.2% 3.0%

Industrial Margarines #1 0.7% 1.8%

Likewise, in B2B we are also market leaders…

Ranked #1 in main categories1

11.3% 9.6% Source: Kantar World Panel

1 Alicorp has +50% of the market share. 2 Based on consolidate Revenue of the last twelve months (LTM) as of March 2017. 3 LTM as of March 2017. Calculation per business ex unassigned corporate expenses

1

10

11

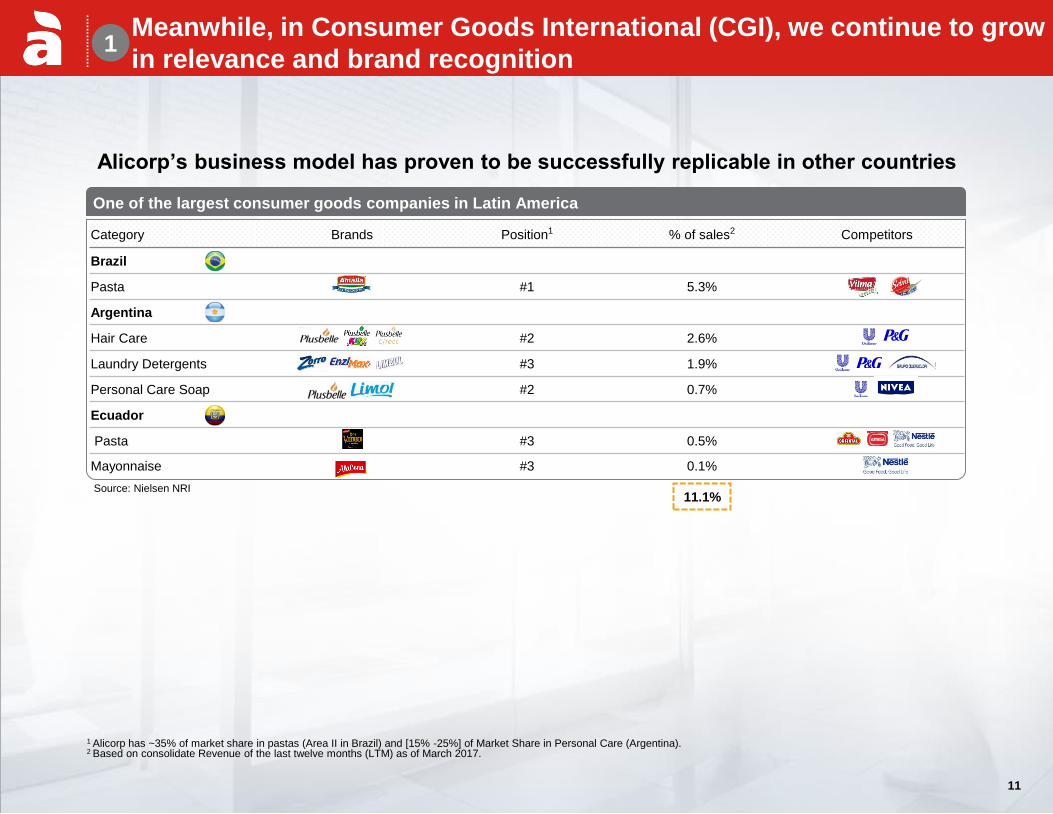

Category Brands Position1 % of sales2 Competitors

Brazil

Pasta #1 5.3%

Argentina

Hair Care #2 2.6%

Laundry Detergents #3 1.9%

Personal Care Soap #2 0.7%

Ecuador

Pasta #3 0.5%

Mayonnaise #3 0.1%

One of the largest consumer goods companies in Latin America

Alicorp’s business model has proven to be successfully replicable in other countries

11.1% Source: Nielsen NRI

Meanwhile, in Consumer Goods International (CGI), we continue to grow

in relevance and brand recognition

1 Alicorp has ~35% of market share in pastas (Area II in Brazil) and [15% -25%] of Market Share in Personal Care (Argentina). 2 Based on consolidate Revenue of the last twelve months (LTM) as of March 2017.

11

1

12

Category Brands Position % of sales2 Competitors

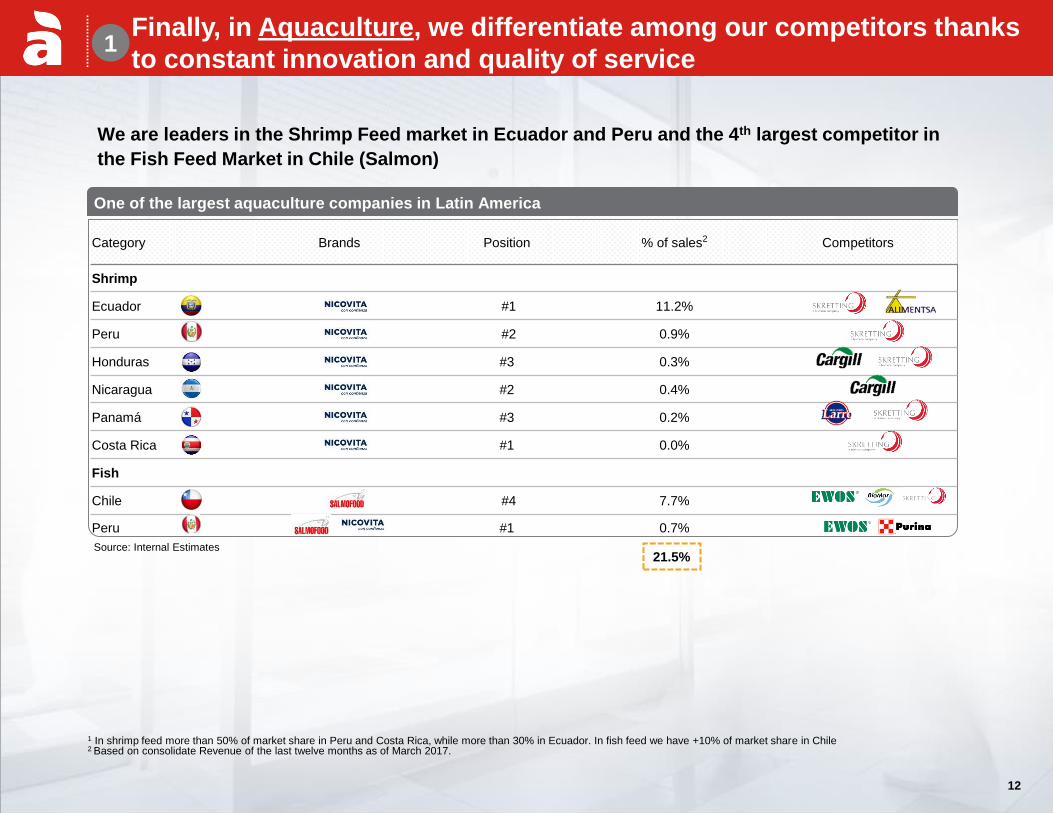

Shrimp

Ecuador #1 11.2%

Peru #2 0.9%

Honduras #3 0.3%

Nicaragua #2 0.4%

Panamá #3 0.2%

Costa Rica #1 0.0%

Fish

Chile #4 7.7%

Peru #1 0.7%

One of the largest aquaculture companies in Latin America

21.5%

1 In shrimp feed more than 50% of market share in Peru and Costa Rica, while more than 30% in Ecuador. In fish feed we have +10% of market share in Chile 2 Based on consolidate Revenue of the last twelve months as of March 2017.

Source: Internal Estimates

We are leaders in the Shrimp Feed market in Ecuador and Peru and the 4th largest competitor in

the Fish Feed Market in Chile (Salmon)

Finally, in Aquaculture, we differentiate among our competitors thanks

to constant innovation and quality of service

12

1

13

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

13

Our Strategy for creating value 2

14

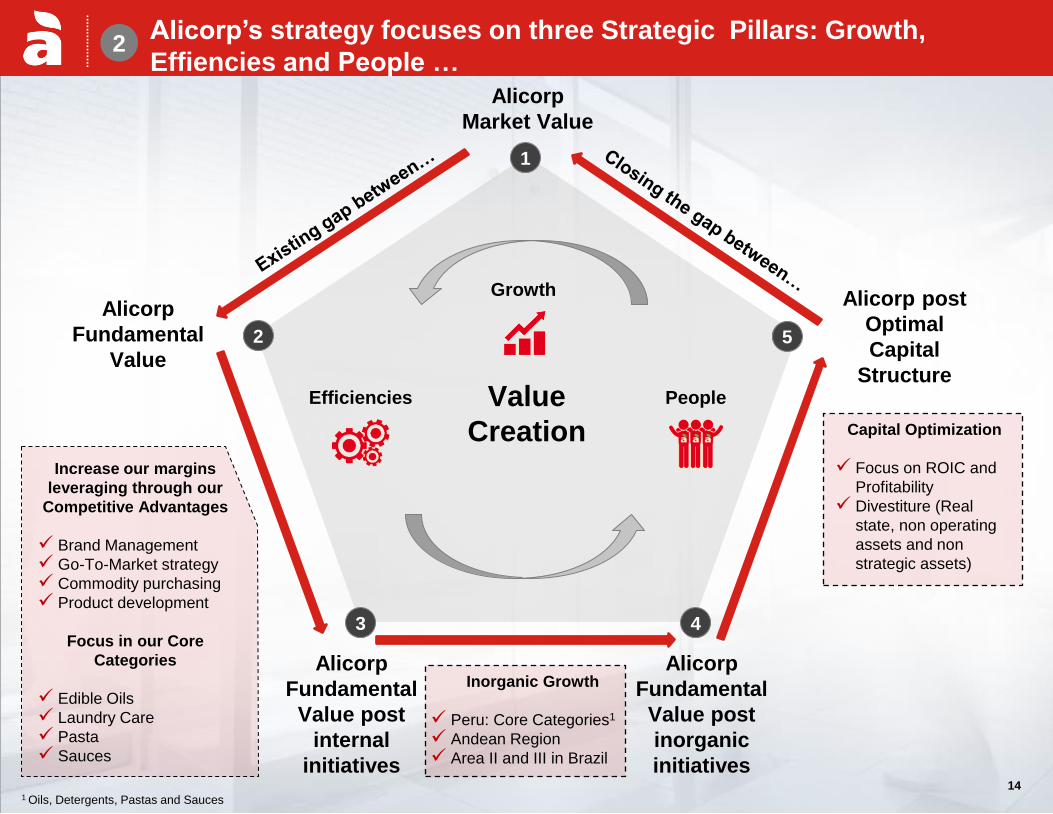

Alicorp’s strategy focuses on three Strategic Pillars: Growth,

Effiencies and People … 2

14

Value

Creation

1

2

3 4

5

Growth

Efficiencies People

Alicorp

Market Value

Alicorp

Fundamental

Value

Alicorp post

Optimal

Capital

Structure

Increase our margins

leveraging through our

Competitive Advantages

Brand Management

Go-To-Market strategy

Commodity purchasing

Product development

Focus in our Core

Categories

Edible Oils

Laundry Care

Pasta

Sauces

Alicorp

Fundamental

Value post

internal

initiatives

Alicorp

Fundamental

Value post

inorganic

initiatives

Inorganic Growth

Peru: Core Categories1

Andean Region

Area II and III in Brazil

Capital Optimization

Focus on ROIC and

Profitability

Divestiture (Real

state, non operating

assets and non

strategic assets)

1 Oils, Detergents, Pastas and Sauces

15

People

“One Alicorp” mindset

• Transfer knowledge and best

practices across the

organization

• Leverage corporate capabilites

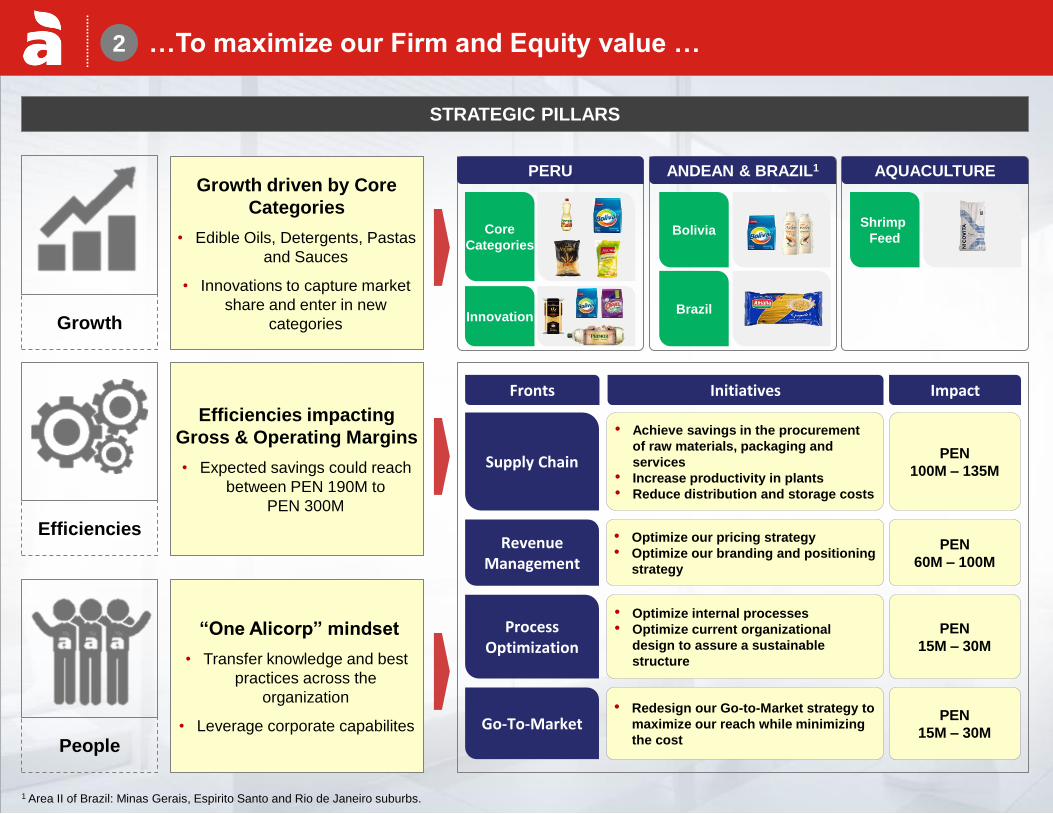

STRATEGIC PILLARS

Growth

2

Growth driven by Core

Categories

• Edible Oils, Detergents, Pastas

and Sauces

• Innovations to capture market

share and enter in new

categories

Efficiencies

Efficiencies impacting

Gross & Operating Margins

• Expected savings could reach

between PEN 190M to

PEN 300M

PERU ANDEAN & BRAZIL1 AQUACULTURE

Shrimp

Feed Core

Categories

Innovation

Bolivia

Brazil

1 Area II of Brazil: Minas Gerais, Espirito Santo and Rio de Janeiro suburbs.

…To maximize our Firm and Equity value …

Initiatives Impact Fronts

Supply Chain

• Achieve savings in the procurement

of raw materials, packaging and

services

• Increase productivity in plants

• Reduce distribution and storage costs

PEN

100M – 135M

Process Optimization

• Optimize internal processes

• Optimize current organizational

design to assure a sustainable

structure

PEN

15M – 30M

Go-To-Market • Redesign our Go-to-Market strategy to

maximize our reach while minimizing

the cost

PEN

15M – 30M

Revenue Management

• Optimize our pricing strategy

• Optimize our branding and positioning

strategy

PEN

60M – 100M

16

NO

PA

T / IN

VE

ST

ED

CA

PIT

AL

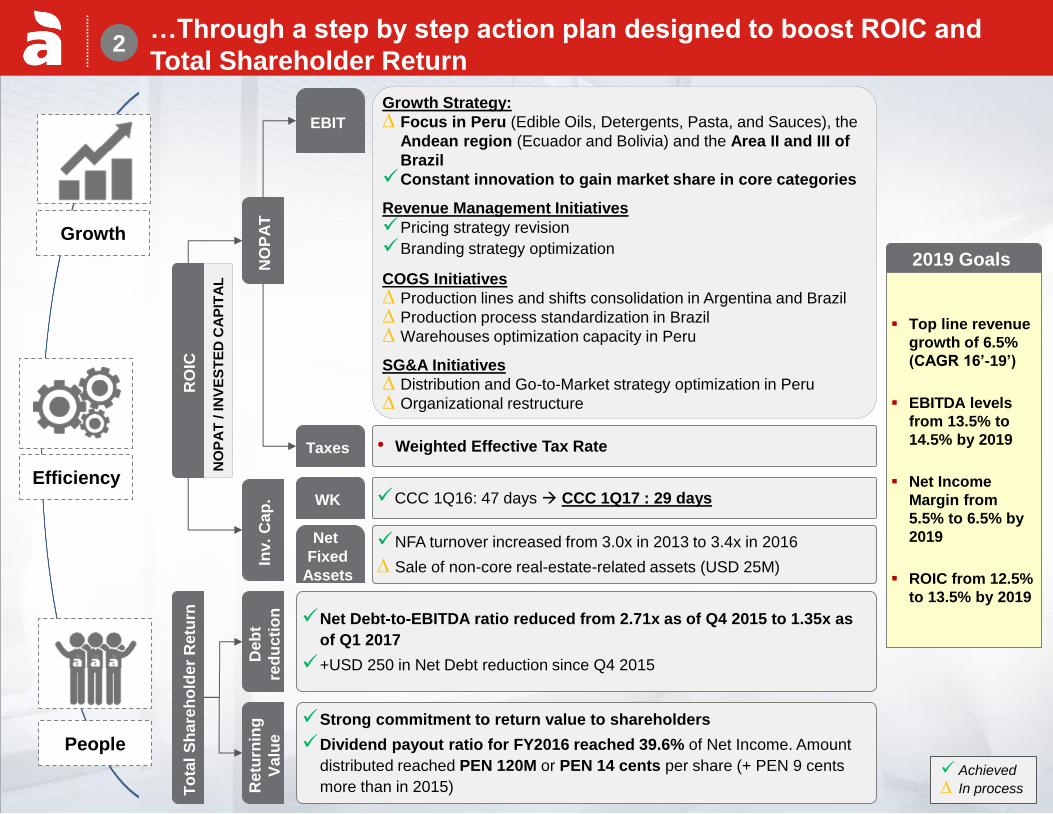

2 …Through a step by step action plan designed to boost ROIC and

Total Shareholder Return

NO

PA

T

Inv.

Cap

.

EBIT

Taxes

WK

Net

Fixed

Assets

Growth Strategy:

∆ Focus in Peru (Edible Oils, Detergents, Pasta, and Sauces), the

Andean region (Ecuador and Bolivia) and the Area II and III of

Brazil

Constant innovation to gain market share in core categories

Revenue Management Initiatives

Pricing strategy revision

Branding strategy optimization

COGS Initiatives

∆ Production lines and shifts consolidation in Argentina and Brazil

∆ Production process standardization in Brazil

∆ Warehouses optimization capacity in Peru

SG&A Initiatives

∆ Distribution and Go-to-Market strategy optimization in Peru

∆ Organizational restructure

CCC 1Q16: 47 days CCC 1Q17 : 29 days

• Weighted Effective Tax Rate

2019 Goals

Top line revenue

growth of 6.5%

(CAGR 16’-19’)

EBITDA levels

from 13.5% to

14.5% by 2019

Net Income

Margin from

5.5% to 6.5% by

2019

ROIC from 12.5%

to 13.5% by 2019

RO

IC

Efficiency

People

Growth

Achieved

∆ In process To

tal

Sh

are

ho

lde

r R

etu

rn

De

bt

red

ucti

on

Re

turn

ing

Va

lue

Net Debt-to-EBITDA ratio reduced from 2.71x as of Q4 2015 to 1.35x as

of Q1 2017

+USD 250 in Net Debt reduction since Q4 2015

Strong commitment to return value to shareholders

Dividend payout ratio for FY2016 reached 39.6% of Net Income. Amount

distributed reached PEN 120M or PEN 14 cents per share (+ PEN 9 cents

more than in 2015)

NFA turnover increased from 3.0x in 2013 to 3.4x in 2016

∆ Sale of non-core real-estate-related assets (USD 25M)

17

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

17

Our Strategy for creating value 2

18

3 Q1 2017 Highlights

20 57 83

157

302 328

1.3% 3.9% 5.2% 2.4% 4.6% 4.8%

Q1 15' Q1 16' Q1 17' FY2015

FY 2016

LTM

149 163 186

722 802 825

9.9% 11.4% 11.7% 11.0% 12.1% 12.2%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

1,509 1,438 1,590

6,580 6,629 6,781

27.5% 30.4% 30.9% 28.4% 30.3% 30.4%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

Total Revenue increased 10.6% YoY

Gross Profit increased 12.4% YoY (+ S/ 54.1 million) while

Gross Margin reached 30.9% (+0.5 p.p.)

EBITDA increased 13.8% YoY (+ S/ 22.5 million) while

EBITDA Margin reached 11.7% (+0.3 p.p.)

Net income increased 45.8% YoY (+ S/ 25.9 million) while

Net Margin reached 5.2% (+1.3 p.p.)

HIGHLIGHTS

(PEN Million)

REVENUE & GROSS MARGIN

EBITDA & EBITDA MARGIN NET INCOME & NET MARGIN

(PEN Million) (PEN Million)

Strong topline growth despite " El Niño" phenomenon affecting the Northern region of Peru, coupled with better profit

margins underpinned by efficiencies program and lower financial expenses

39.6% 29.3%

xx Dividend Payout Ratio

18

19

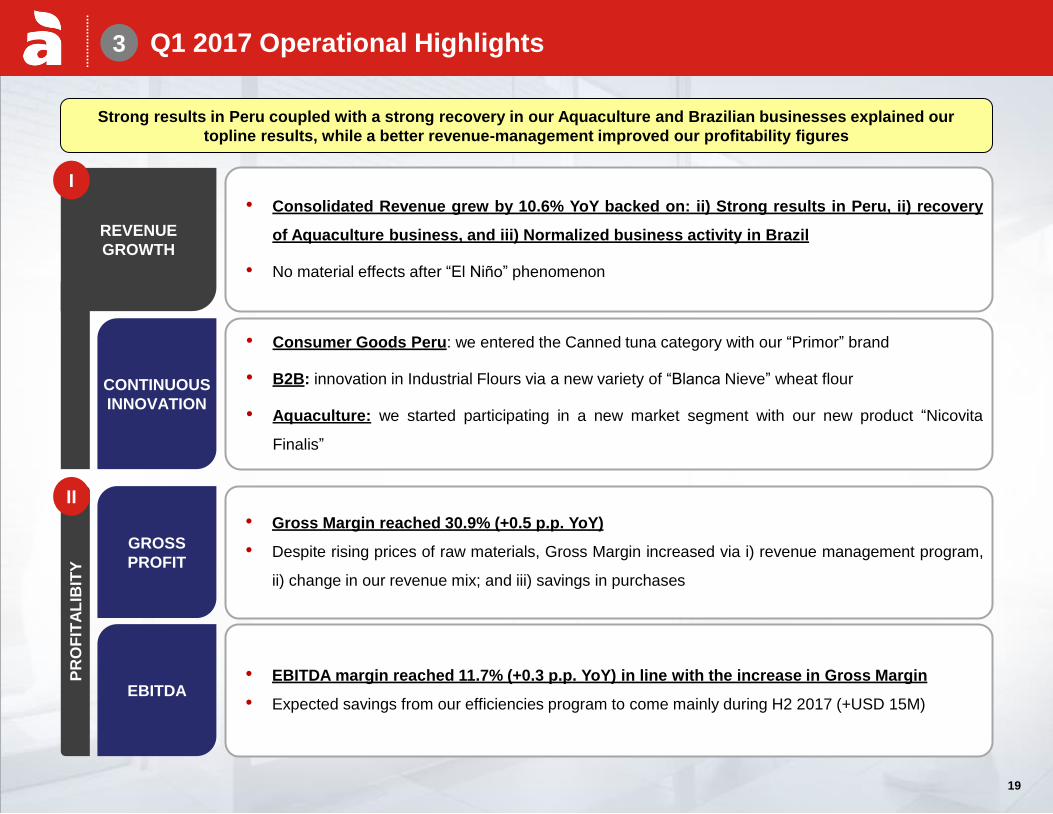

Q1 2017 Operational Highlights 3

Strong results in Peru coupled with a strong recovery in our Aquaculture and Brazilian businesses explained our

topline results, while a better revenue-management improved our profitability figures

REVENUE

GROWTH

PR

OF

ITA

LIB

ITY

• Consolidated Revenue grew by 10.6% YoY backed on: ii) Strong results in Peru, ii) recovery

of Aquaculture business, and iii) Normalized business activity in Brazil

• No material effects after “El Niño” phenomenon

• Gross Margin reached 30.9% (+0.5 p.p. YoY)

• Despite rising prices of raw materials, Gross Margin increased via i) revenue management program,

ii) change in our revenue mix; and iii) savings in purchases

GROSS

PROFIT

EBITDA • EBITDA margin reached 11.7% (+0.3 p.p. YoY) in line with the increase in Gross Margin

• Expected savings from our efficiencies program to come mainly during H2 2017 (+USD 15M)

I

II

CONTINUOUS

INNOVATION

• Consumer Goods Peru: we entered the Canned tuna category with our “Primor” brand

• B2B: innovation in Industrial Flours via a new variety of “Blanca Nieve” wheat flour

• Aquaculture: we started participating in a new market segment with our new product “Nicovita

Finalis”

19

20

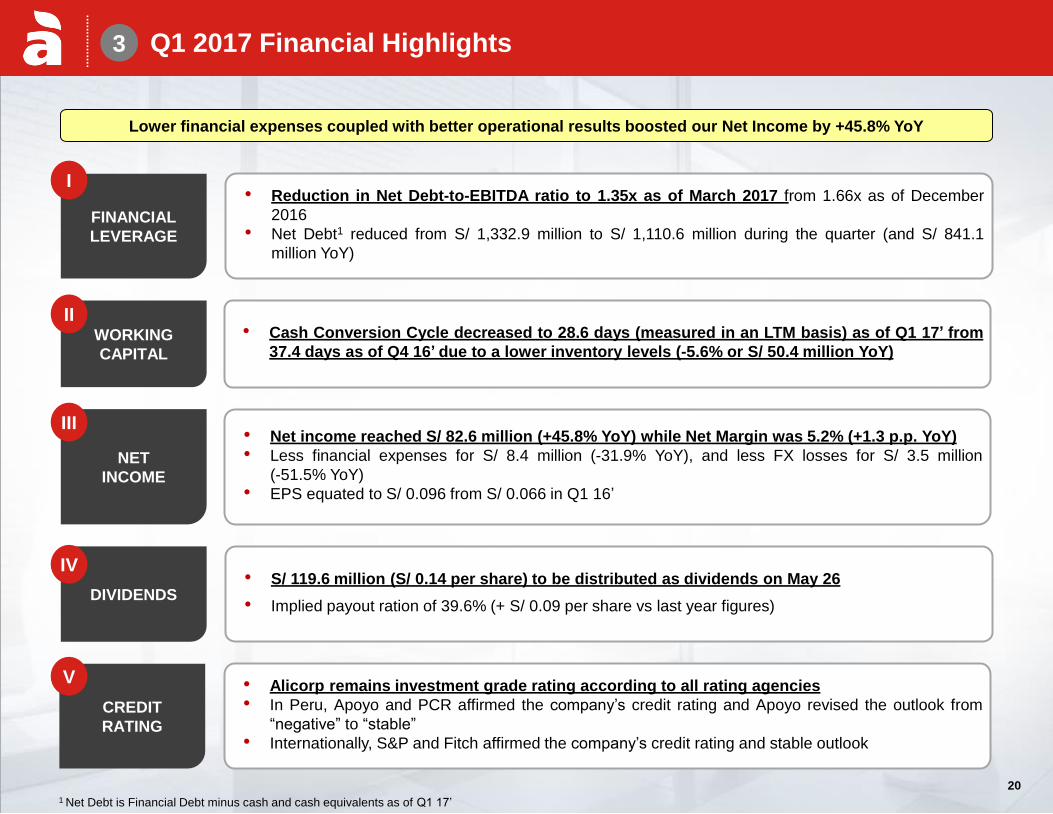

Q1 2017 Financial Highlights 3

Lower financial expenses coupled with better operational results boosted our Net Income by +45.8% YoY

FINANCIAL

LEVERAGE

WORKING

CAPITAL

DIVIDENDS

• Reduction in Net Debt-to-EBITDA ratio to 1.35x as of March 2017 from 1.66x as of December

2016

• Net Debt1 reduced from S/ 1,332.9 million to S/ 1,110.6 million during the quarter (and S/ 841.1

million YoY)

• Cash Conversion Cycle decreased to 28.6 days (measured in an LTM basis) as of Q1 17’ from

37.4 days as of Q4 16’ due to a lower inventory levels (-5.6% or S/ 50.4 million YoY)

• S/ 119.6 million (S/ 0.14 per share) to be distributed as dividends on May 26

• Implied payout ration of 39.6% (+ S/ 0.09 per share vs last year figures)

I

II

IV

1 Net Debt is Financial Debt minus cash and cash equivalents as of Q1 17’

NET

INCOME

III • Net income reached S/ 82.6 million (+45.8% YoY) while Net Margin was 5.2% (+1.3 p.p. YoY)

• Less financial expenses for S/ 8.4 million (-31.9% YoY), and less FX losses for S/ 3.5 million

(-51.5% YoY)

• EPS equated to S/ 0.096 from S/ 0.066 in Q1 16’

20

CREDIT

RATING

• Alicorp remains investment grade rating according to all rating agencies

• In Peru, Apoyo and PCR affirmed the company’s credit rating and Apoyo revised the outlook from

“negative” to “stable”

• Internationally, S&P and Fitch affirmed the company’s credit rating and stable outlook

V

21

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

21

Our Strategy for creating value 2

22

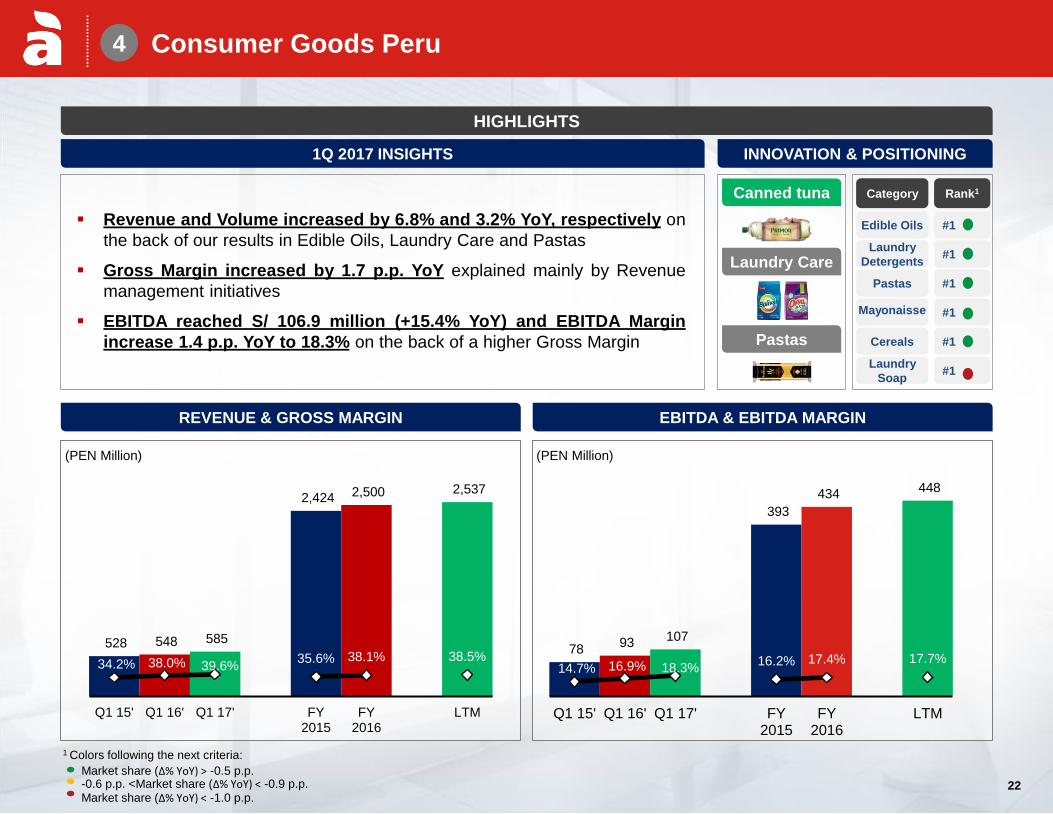

Consumer Goods Peru

22

Revenue and Volume increased by 6.8% and 3.2% YoY, respectively on

the back of our results in Edible Oils, Laundry Care and Pastas

Gross Margin increased by 1.7 p.p. YoY explained mainly by Revenue

management initiatives

EBITDA reached S/ 106.9 million (+15.4% YoY) and EBITDA Margin

increase 1.4 p.p. YoY to 18.3% on the back of a higher Gross Margin

(PEN Million) (PEN Million)

78 93 107

393

434 448

14.7% 16.9% 18.3% 16.2% 17.4% 17.7%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

HIGHLIGHTS

REVENUE & GROSS MARGIN

4

EBITDA & EBITDA MARGIN

INNOVATION & POSITIONING 1Q 2017 INSIGHTS

Canned tuna

Laundry Care

Pastas

528 548 585

2,424 2,500 2,537

34.2% 38.0% 39.6% 35.6% 38.1% 38.5%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

Category Rank1

Edible Oils #1

Laundry

Detergents #1

Pastas #1

Mayonaisse #1

Cereals #1

Laundry

Soap #1

Market share (Δ% YoY) > -0.5 p.p. -0.6 p.p. <Market share (Δ% YoY) < -0.9 p.p. Market share (Δ% YoY) < -1.0 p.p.

1 Colors following the next criteria:

23

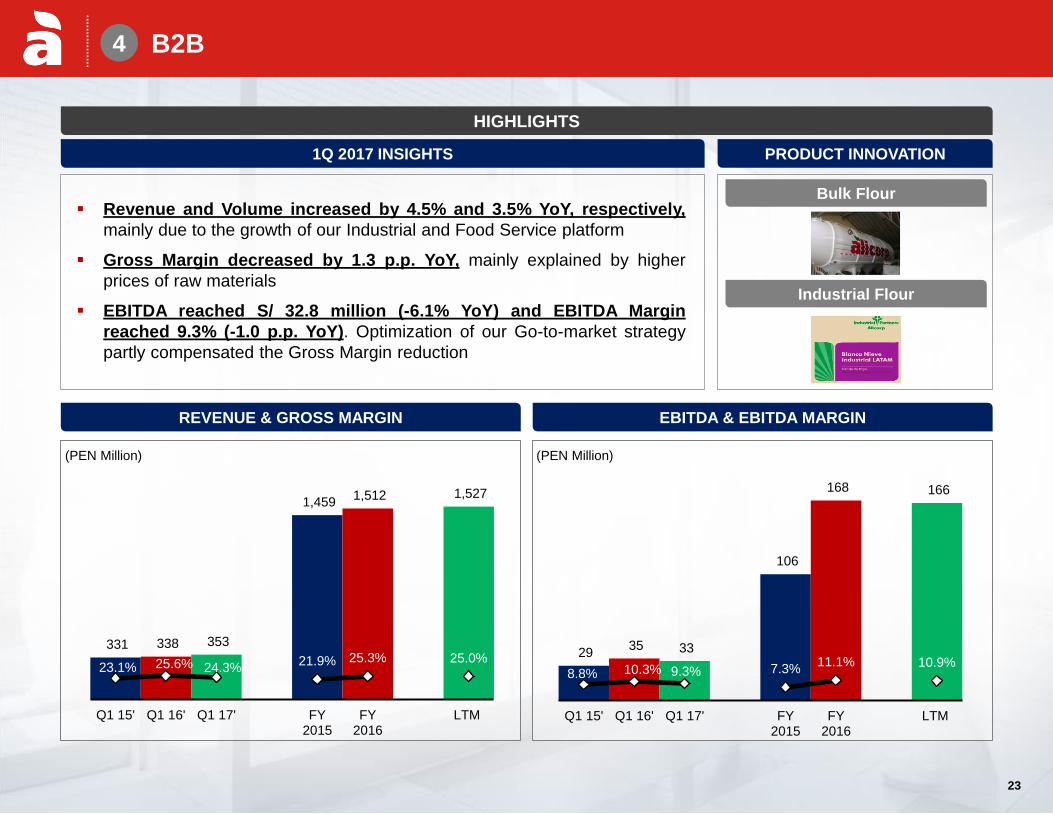

B2B

Revenue and Volume increased by 4.5% and 3.5% YoY, respectively,

mainly due to the growth of our Industrial and Food Service platform

Gross Margin decreased by 1.3 p.p. YoY, mainly explained by higher

prices of raw materials

EBITDA reached S/ 32.8 million (-6.1% YoY) and EBITDA Margin

reached 9.3% (-1.0 p.p. YoY). Optimization of our Go-to-market strategy

partly compensated the Gross Margin reduction

(PEN Million) (PEN Million)

HIGHLIGHTS

4

EBITDA & EBITDA MARGIN

PRODUCT INNOVATION 1Q 2017 INSIGHTS

331 338 353

1,459 1,512 1,527

23.1% 25.6% 24.3% 21.9% 25.3% 25.0%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

Bulk Flour

Industrial Flour

REVENUE & GROSS MARGIN

29 35 33

106

168 166

8.8% 10.3% 9.3% 7.3% 11.1% 10.9%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

23

24

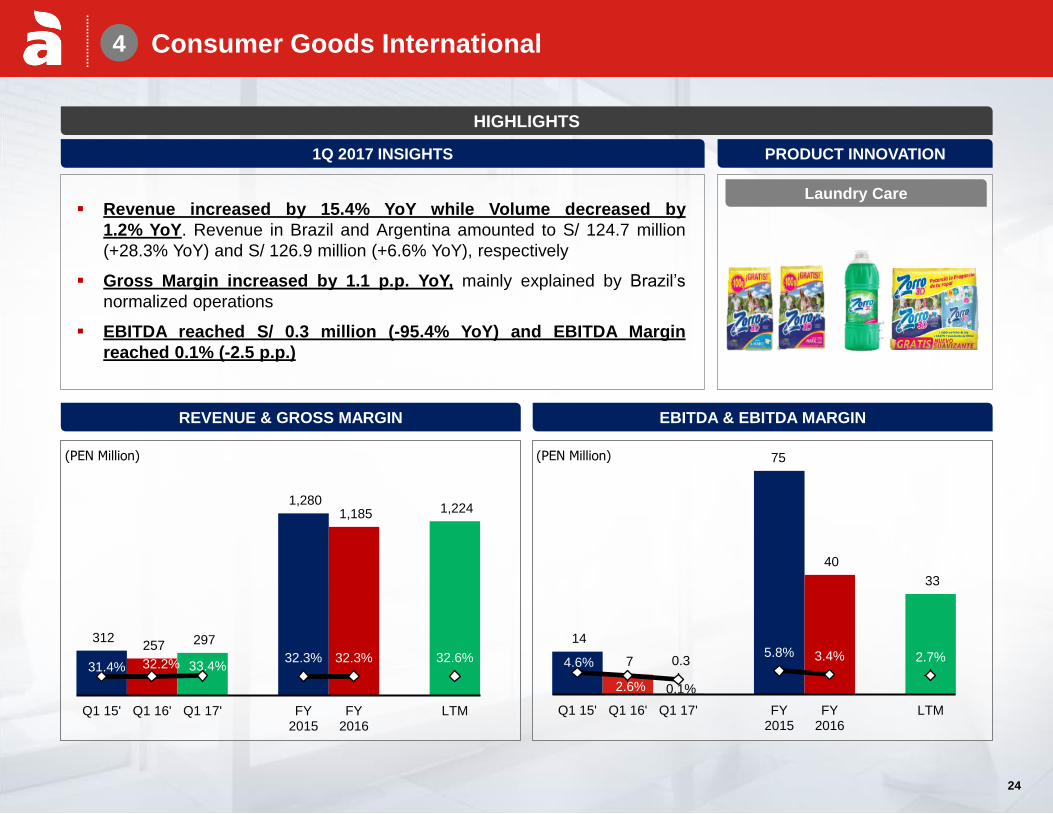

Consumer Goods International

Revenue increased by 15.4% YoY while Volume decreased by

1.2% YoY. Revenue in Brazil and Argentina amounted to S/ 124.7 million

(+28.3% YoY) and S/ 126.9 million (+6.6% YoY), respectively

Gross Margin increased by 1.1 p.p. YoY, mainly explained by Brazil’s

normalized operations

EBITDA reached S/ 0.3 million (-95.4% YoY) and EBITDA Margin

reached 0.1% (-2.5 p.p.)

(PEN Million) (PEN Million)

HIGHLIGHTS

4

EBITDA & EBITDA MARGIN

PRODUCT INNOVATION 1Q 2017 INSIGHTS

312 257 297

1,280 1,185 1,224

31.4% 32.2% 33.4% 32.3% 32.3% 32.6%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

14

7 0.3

75

40

33

4.6%

2.6% 0.1%

5.8% 3.4% 2.7%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

Laundry Care

REVENUE & GROSS MARGIN

24

25

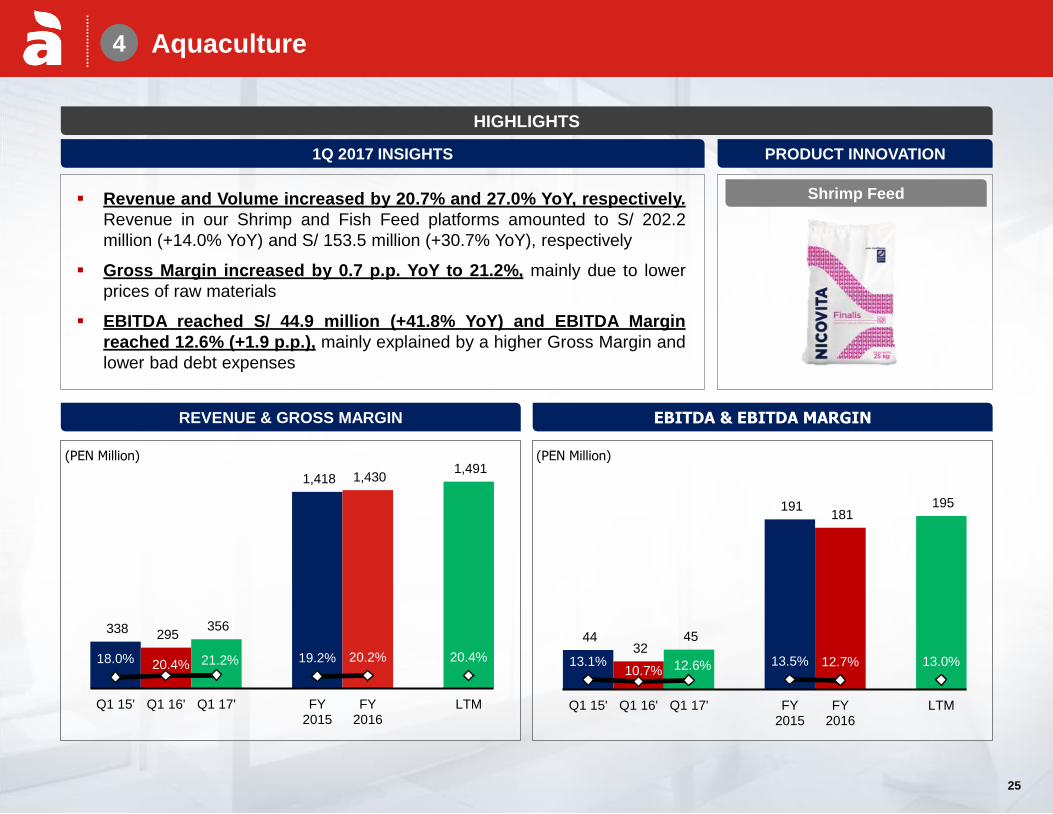

Aquaculture

Revenue and Volume increased by 20.7% and 27.0% YoY, respectively.

Revenue in our Shrimp and Fish Feed platforms amounted to S/ 202.2

million (+14.0% YoY) and S/ 153.5 million (+30.7% YoY), respectively

Gross Margin increased by 0.7 p.p. YoY to 21.2%, mainly due to lower

prices of raw materials

EBITDA reached S/ 44.9 million (+41.8% YoY) and EBITDA Margin

reached 12.6% (+1.9 p.p.), mainly explained by a higher Gross Margin and

lower bad debt expenses

(PEN Million) (PEN Million)

HIGHLIGHTS

4

EBITDA & EBITDA MARGIN

PRODUCT INNOVATION 1Q 2017 INSIGHTS

338 295 356

1,418 1,430 1,491

18.0% 20.4% 21.2% 19.2% 20.2% 20.4%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

44 32

45

191 181

195

13.1% 10.7% 12.6% 13.5% 12.7% 13.0%

Q1 15' Q1 16' Q1 17' FY2015

FY2016

LTM

Shrimp Feed

REVENUE & GROSS MARGIN

25

26

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

26

Our Strategy for creating value 2

27

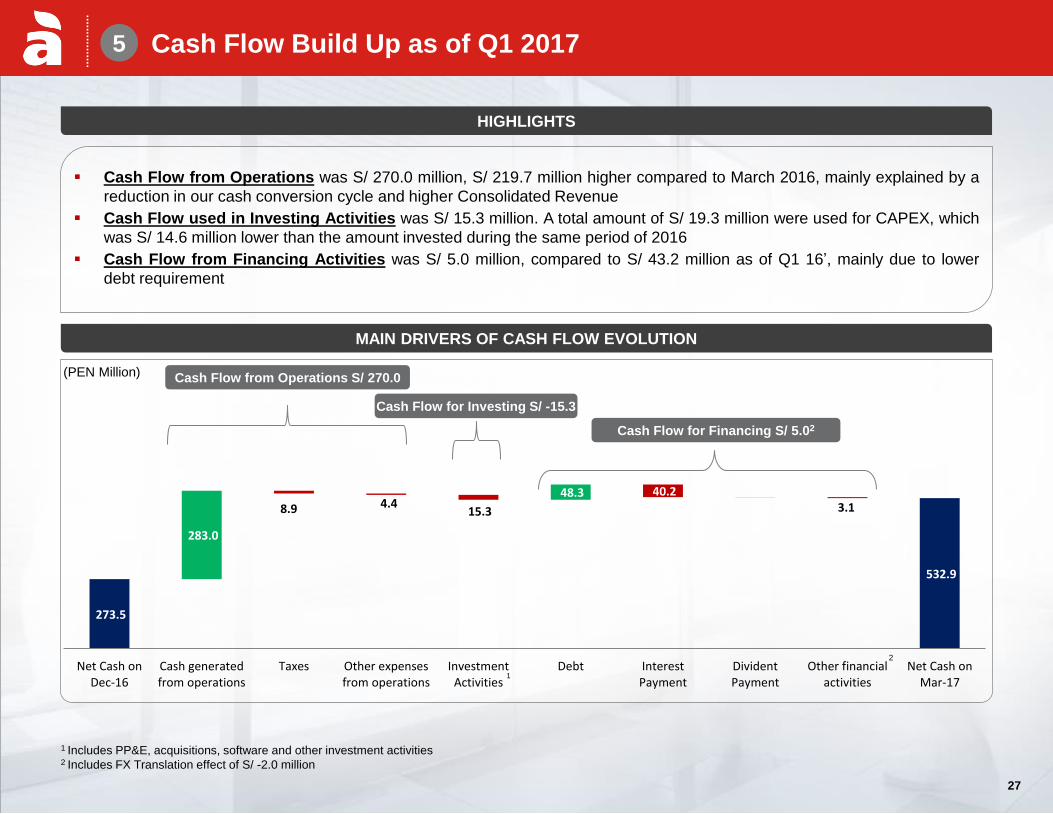

273.5

532.9

283.0

48.3 8.9 4.4

15.3

40.2 3.1

Net Cash onDec-16

Cash generatedfrom operations

Taxes Other expensesfrom operations

InvestmentActivities

Debt InterestPayment

DividentPayment

Other financialactivities

Net Cash onMar-17

1

Cash Flow Build Up as of Q1 2017

Cash Flow from Operations was S/ 270.0 million, S/ 219.7 million higher compared to March 2016, mainly explained by a

reduction in our cash conversion cycle and higher Consolidated Revenue

Cash Flow used in Investing Activities was S/ 15.3 million. A total amount of S/ 19.3 million were used for CAPEX, which

was S/ 14.6 million lower than the amount invested during the same period of 2016

Cash Flow from Financing Activities was S/ 5.0 million, compared to S/ 43.2 million as of Q1 16’, mainly due to lower

debt requirement

1 Includes PP&E, acquisitions, software and other investment activities

2 Includes FX Translation effect of S/ -2.0 million

(PEN Million) Cash Flow from Operations S/ 270.0

Cash Flow for Financing S/ 5.02

Cash Flow for Investing S/ -15.3

2

MAIN DRIVERS OF CASH FLOW EVOLUTION

HIGHLIGHTS

1

5

27

28

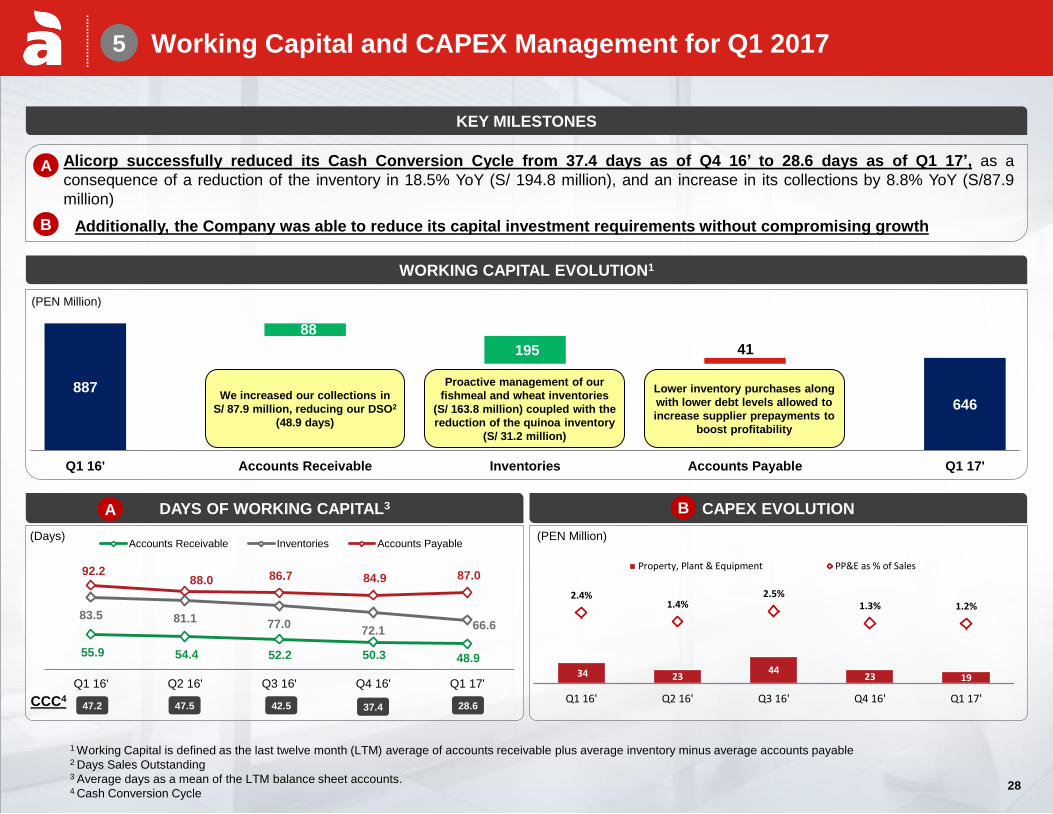

55.9 54.4 52.2 50.3 48.9

83.5 81.1 77.0 72.1 66.6

92.2 88.0 86.7 84.9 87.0

Q1 16' Q2 16' Q3 16' Q4 16' Q1 17'

Accounts Receivable Inventories Accounts Payable

Working Capital and CAPEX Management for Q1 2017

KEY MILESTONES

• Alicorp successfully reduced its Cash Conversion Cycle from 37.4 days as of Q4 16’ to 28.6 days as of Q1 17’, as a

consequence of a reduction of the inventory in 18.5% YoY (S/ 194.8 million), and an increase in its collections by 8.8% YoY (S/87.9

million)

• DAdditionally, the Company was able to reduce its capital investment requirements without compromising growth

A

B

A

(PEN Million)

CAPEX EVOLUTION A B

1 Working Capital is defined as the last twelve month (LTM) average of accounts receivable plus average inventory minus average accounts payable

2 Days Sales Outstanding

3 Average days as a mean of the LTM balance sheet accounts. 4 Cash Conversion Cycle

(Days)

CCC4 47.5 47.2 42.5 28.6

(PEN Million)

WORKING CAPITAL EVOLUTION1

DAYS OF WORKING CAPITAL3 A

88

195 41

887

646

Q1 16' Accounts Receivable Inventories Accounts Payable Q1 17'

Mill

ares

34 23 44

23 19

2.4% 1.4%

2.5% 1.3% 1.2%

Q1 16' Q2 16' Q3 16' Q4 16' Q1 17'

Mill

ares

Property, Plant & Equipment PP&E as % of Sales

37.4

We increased our collections in

S/ 87.9 million, reducing our DSO2

(48.9 days)

Proactive management of our

fishmeal and wheat inventories

(S/ 163.8 million) coupled with the

reduction of the quinoa inventory

(S/ 31.2 million)

Lower inventory purchases along

with lower debt levels allowed to

increase supplier prepayments to

boost profitability

5

28

29

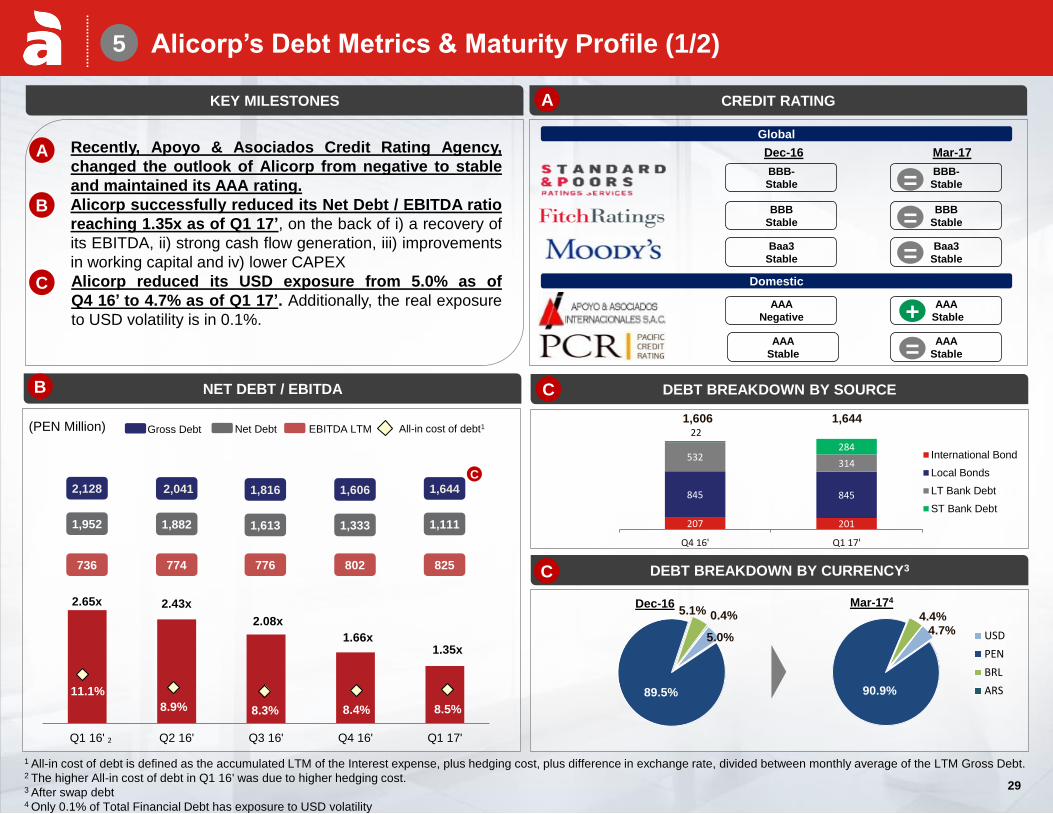

5.0%

89.5%

5.1% 0.4%

4.7%

90.9%

4.4%

USD

PEN

BRL

ARS

2.65x 2.43x

2.08x

1.66x 1.35x

Q1 16' Q2 16' Q3 16' Q4 16' Q1 17'

11.1%

8.9% 8.3% 8.4% 8.5%

207 201

845 845

532 314

22

284

Q4 16' Q1 17'

International Bond

Local Bonds

LT Bank Debt

ST Bank Debt

Alicorp’s Debt Metrics & Maturity Profile (1/2)

• Recently, Apoyo & Asociados Credit Rating Agency,

changed the outlook of Alicorp from negative to stable

and maintained its AAA rating.

• Alicorp successfully reduced its Net Debt / EBITDA ratio

reaching 1.35x as of Q1 17’, on the back of i) a recovery of

its EBITDA, ii) strong cash flow generation, iii) improvements

in working capital and iv) lower CAPEX

Alicorp reduced its USD exposure from 5.0% as of

Q4 16’ to 4.7% as of Q1 17’. Additionally, the real exposure

to USD volatility is in 0.1%.

A

B

A

Global

Domestic

BBB-

Stable

BBB

Stable

Baa3

Stable

AAA

Negative

AAA

Stable

KEY MILESTONES CREDIT RATING

DEBT BREAKDOWN BY SOURCE

5

C

C

NET DEBT / EBITDA

1,952

736

(PEN Million) Net Debt EBITDA LTM

1,882

774

1,613

776

1,333

802

1,111

825

B

Dec-16 Mar-17

DEBT BREAKDOWN BY CURRENCY3

Dec-16 Mar-174

1,606 1,644

A

C

BBB-

Stable

BBB

Stable

Baa3

Stable

AAA

Stable

AAA

Stable

All-in cost of debt1

+

=

2,128 2,041 1,816 1,606 1,644

=

=

=

Gross Debt

C

1 All-in cost of debt is defined as the accumulated LTM of the Interest expense, plus hedging cost, plus difference in exchange rate, divided between monthly average of the LTM Gross Debt.

2 The higher All-in cost of debt in Q1 16' was due to higher hedging cost.

3 After swap debt 4 Only 0.1% of Total Financial Debt has exposure to USD volatility

2

29

30

284

64

116

216

97

8

361

50 100 100 100 100

50

2017 2018 2019 2020 2023 2025 2026 2027 2028 2029 2030

Short-Term Bank Debt Long-Term Bank Debt Local Bonds International Bonds

Alicorp’s Debt Metrics & Maturity Profile (2/2)

DURATION AS OF MARCH 2017 WAS 3.90 YEARS VS. 4.25 YEARS AS OF DECEMBER 2016

Mar 2017: Total Debt: PEN 1.644 billion

Dec 2016: Total Debt: PEN 1.606 billion

242

5

104

116

116

463

70

70

207

201

15.0% 24.4% 6.1% 0.5% 22.9.% 3.0% 6.2% 6.2% 6.2% 3.2% 6.2%

160

104

116

70 160

208

392

98

8

367

50

100 100 100 100

50

2017 2018 2019 2020 2023 2025 2026 2027 2028 2029 2030

70

201

160

28.2% 13.1% 5.9% 0.5% 21.9% 3.0% 6.1% 6.1% 6.1% 3.0% 6.1%

Debt Breakdown by Currency1

5.0%

89.5%

5.1% 0.4% 4.7%

90.9%

4.4%

USD

PEN

BRL

ARS

1 After Swap Debt

Due to a strong cash flow generation in Q1 17‘ and a lower level of leverage, Alicorp reduced its duration to achieve lower

interest expenses

30

31

Index

5

6 Guidance 2017

Q1 2017 Highlights

1

3

Financial Metrics

4 Q1 2017 Business & Operating Review

About Alicorp

31

Our Strategy for creating value 2

32

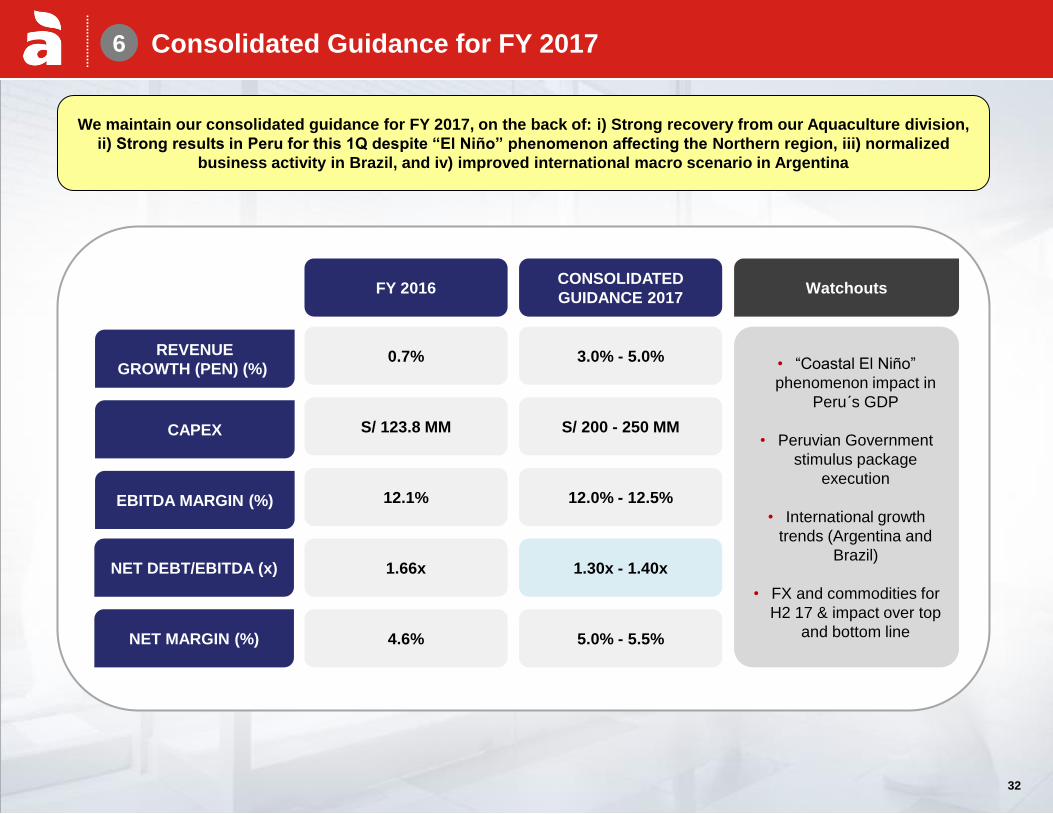

Consolidated Guidance for FY 2017

FY 2016

0.7%

12.1%

S/ 123.8 MM

1.66x NET DEBT/EBITDA (x)

CONSOLIDATED

GUIDANCE 2017

3.0% - 5.0%

12.0% - 12.5%

S/ 200 - 250 MM

1.30x - 1.40x

4.6% NET MARGIN (%) 5.0% - 5.5%

REVENUE

GROWTH (PEN) (%)

EBITDA MARGIN (%)

CAPEX

6

We maintain our consolidated guidance for FY 2017, on the back of: i) Strong recovery from our Aquaculture division,

ii) Strong results in Peru for this 1Q despite “El Niño” phenomenon affecting the Northern region, iii) normalized

business activity in Brazil, and iv) improved international macro scenario in Argentina

• “Coastal El Niño”

phenomenon impact in

Peru´s GDP

• Peruvian Government

stimulus package

execution

• International growth

trends (Argentina and

Brazil)

• FX and commodities for

H2 17 & impact over top

and bottom line

Watchouts

32

33

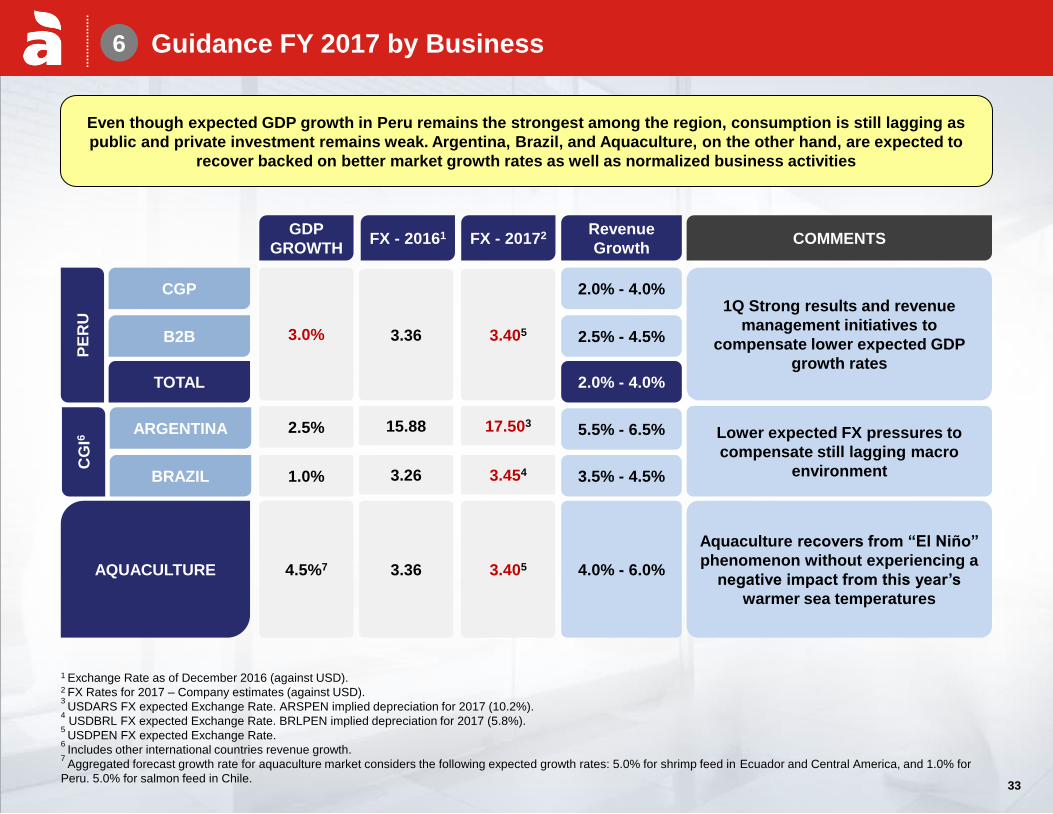

Guidance FY 2017 by Business

1 Exchange Rate as of December 2016 (against USD). 2 FX Rates for 2017 – Company estimates (against USD). 3 USDARS FX expected Exchange Rate. ARSPEN implied depreciation for 2017 (10.2%). 4 USDBRL FX expected Exchange Rate. BRLPEN implied depreciation for 2017 (5.8%).

5 USDPEN FX expected Exchange Rate. 6 Includes other international countries revenue growth. 7 Aggregated forecast growth rate for aquaculture market considers the following expected growth rates: 5.0% for shrimp feed in Ecuador and Central America, and 1.0% for

Peru. 5.0% for salmon feed in Chile.

6

FX - 20172

3.405

17.503

3.405

3.454

CGP

2.5% - 4.5%

PE

RU

2.0% - 4.0%

B2B

3.5% - 4.5%

5.5% - 6.5% ARGENTINA

CG

I6

BRAZIL

AQUACULTURE

3.0%

2.5%

1.0%

Revenue

Growth

GDP

GROWTH FX - 20161

3.36

15.88

4.5%7 3.36 4.0% - 6.0%

3.26

TOTAL 2.0% - 4.0%

Even though expected GDP growth in Peru remains the strongest among the region, consumption is still lagging as

public and private investment remains weak. Argentina, Brazil, and Aquaculture, on the other hand, are expected to

recover backed on better market growth rates as well as normalized business activities

COMMENTS

1Q Strong results and revenue

management initiatives to

compensate lower expected GDP

growth rates

Lower expected FX pressures to

compensate still lagging macro

environment

Aquaculture recovers from “El Niño”

phenomenon without experiencing a

negative impact from this year’s

warmer sea temperatures

33