Embed Size (px)

Citation preview

Corporate Restructuring, Merger, Demerger

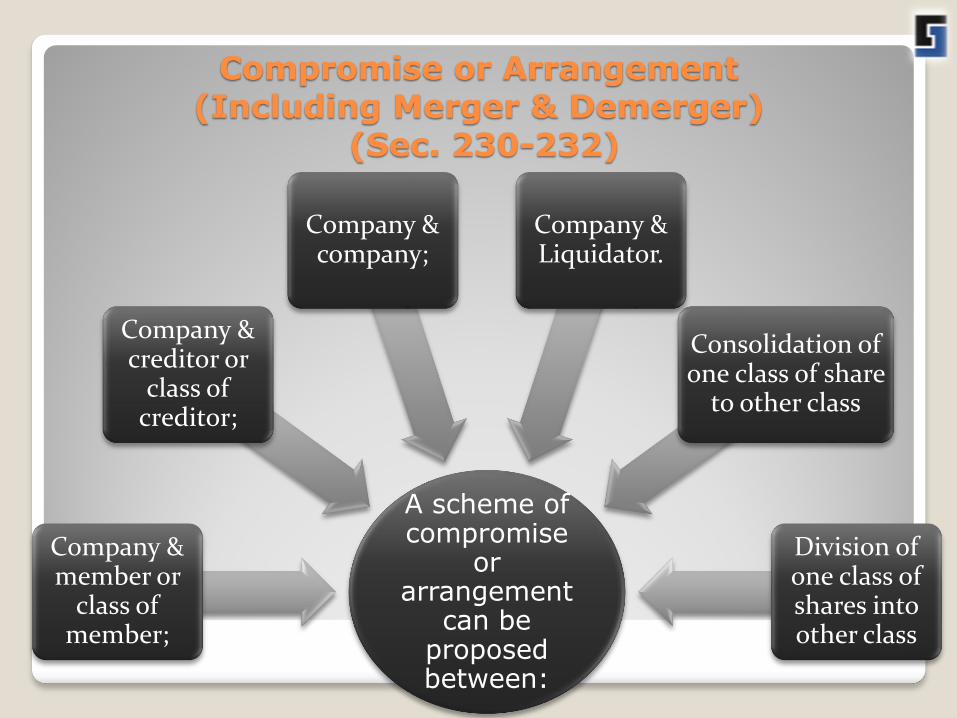

Compromise or Arrangement (Including Merger & Demerger)

(Sec. 230-232)

A scheme of compromise

or arrangement

can be proposed between:

Company & member or

class of member;

Company & creditor or

class of creditor;

Company & company;

Company & Liquidator.

Consolidation of one class of share

to other class

Division of one class of shares into other class

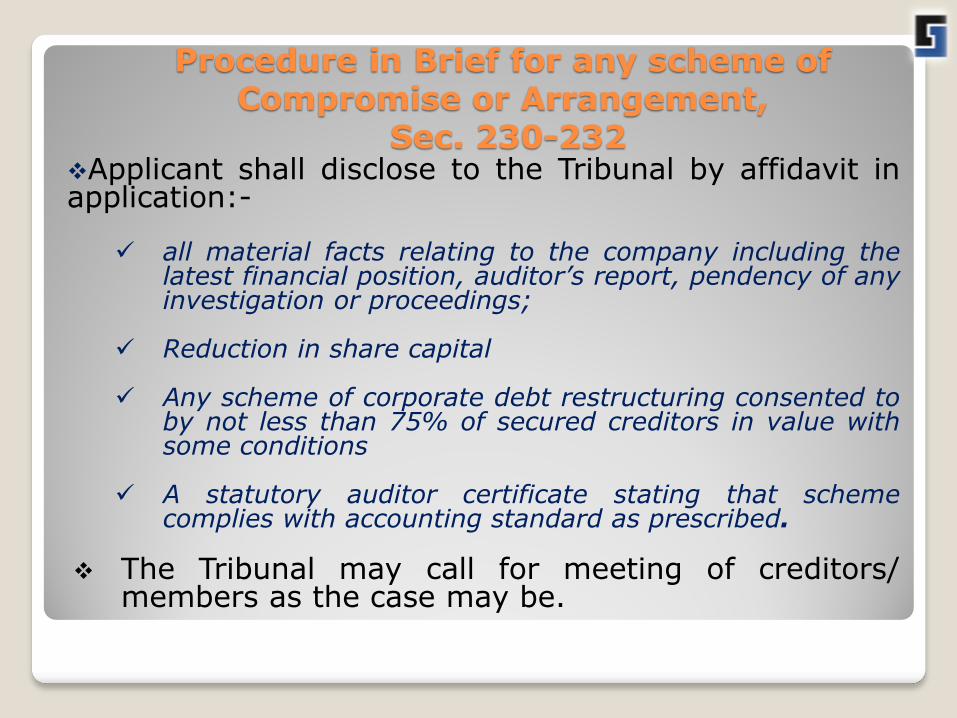

Procedure in Brief for any scheme of Compromise or Arrangement,

Sec. 230-232 Applicant shall disclose to the Tribunal by affidavit in application:-

all material facts relating to the company including the latest financial position, auditor’s report, pendency of any investigation or proceedings;

Reduction in share capital

Any scheme of corporate debt restructuring consented to

by not less than 75% of secured creditors in value with some conditions

A statutory auditor certificate stating that scheme complies with accounting standard as prescribed.

The Tribunal may call for meeting of creditors/

members as the case may be.

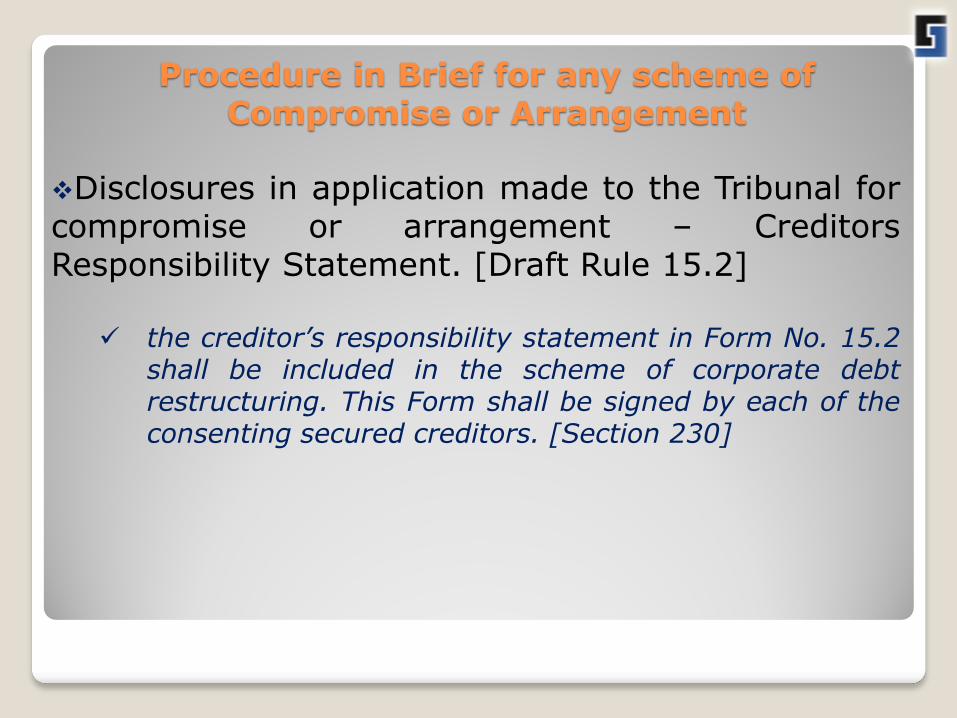

Procedure in Brief for any scheme of Compromise or Arrangement

Disclosures in application made to the Tribunal for compromise or arrangement – Creditors Responsibility Statement. [Draft Rule 15.2]

the creditor’s responsibility statement in Form No. 15.2 shall be included in the scheme of corporate debt restructuring. This Form shall be signed by each of the consenting secured creditors. [Section 230]

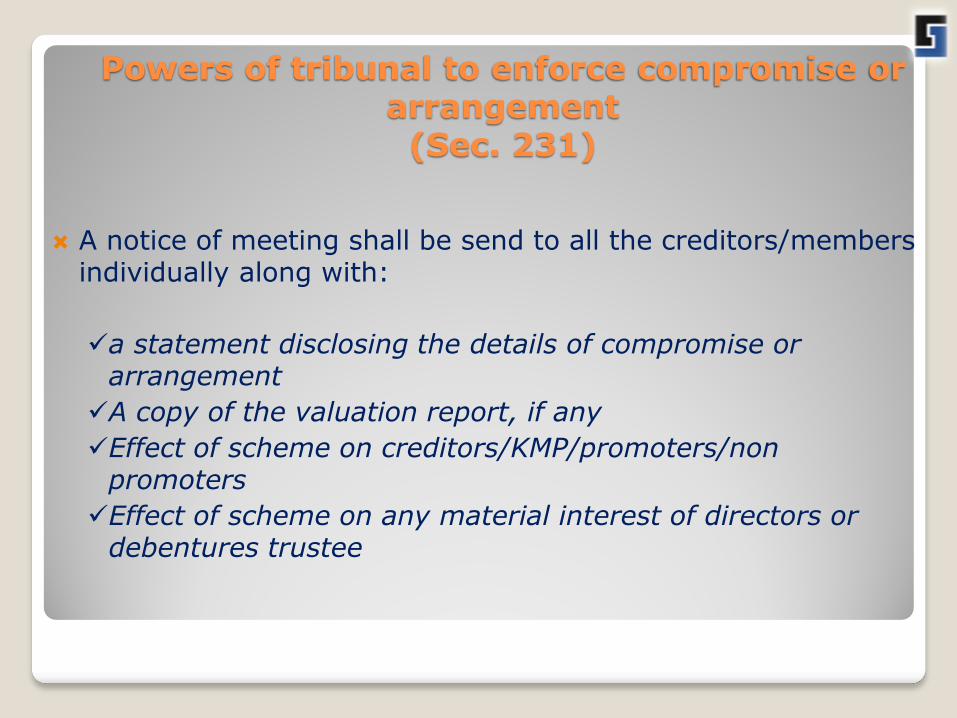

Powers of tribunal to enforce compromise or arrangement

(Sec. 231)

A notice of meeting shall be send to all the creditors/members individually along with:

a statement disclosing the details of compromise or arrangement

A copy of the valuation report, if any

Effect of scheme on creditors/KMP/promoters/non promoters

Effect of scheme on any material interest of directors or debentures trustee

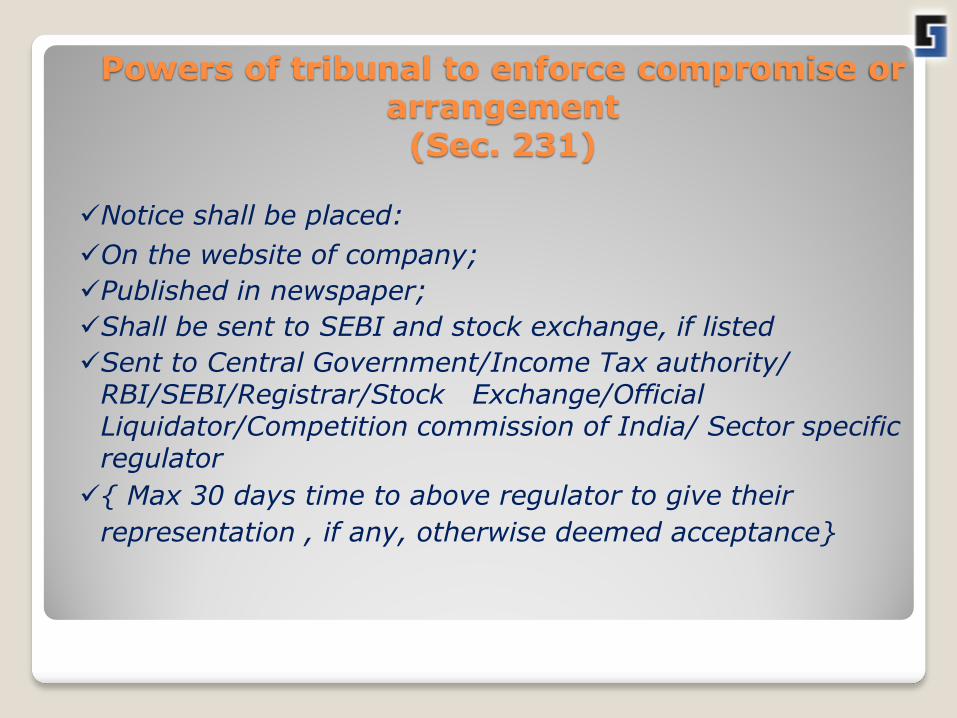

Powers of tribunal to enforce compromise or arrangement

(Sec. 231)

Notice shall be placed:

On the website of company;

Published in newspaper;

Shall be sent to SEBI and stock exchange, if listed

Sent to Central Government/Income Tax authority/ RBI/SEBI/Registrar/Stock Exchange/Official Liquidator/Competition commission of India/ Sector specific regulator

{ Max 30 days time to above regulator to give their

representation , if any, otherwise deemed acceptance}

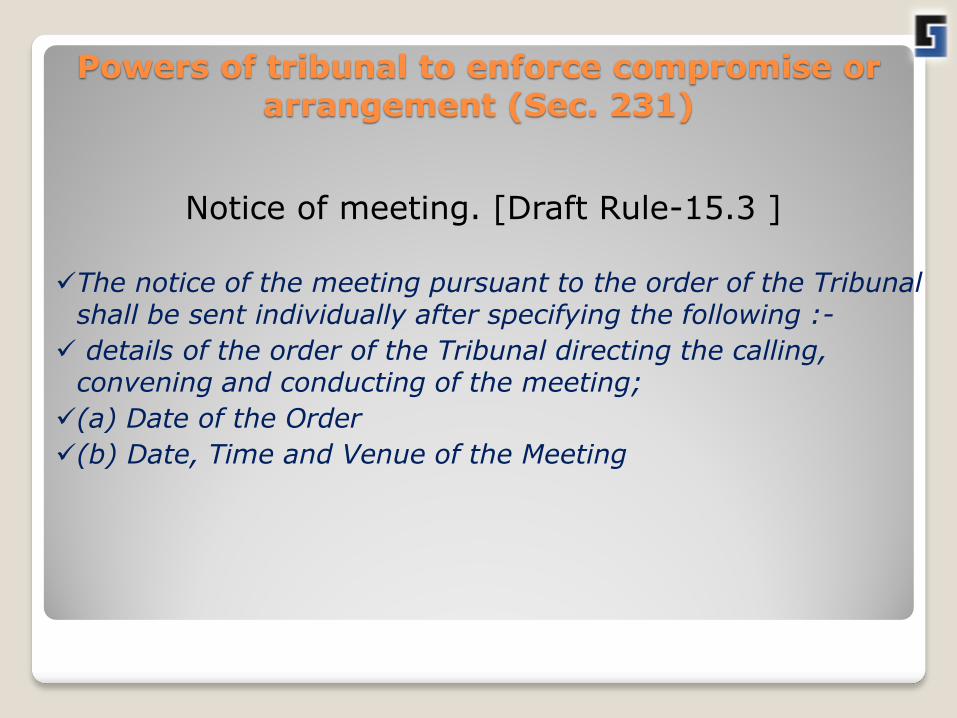

Powers of tribunal to enforce compromise or

arrangement (Sec. 231)

Notice of meeting. [Draft Rule-15.3 ]

The notice of the meeting pursuant to the order of the Tribunal shall be sent individually after specifying the following :-

details of the order of the Tribunal directing the calling, convening and conducting of the meeting;

(a) Date of the Order

(b) Date, Time and Venue of the Meeting

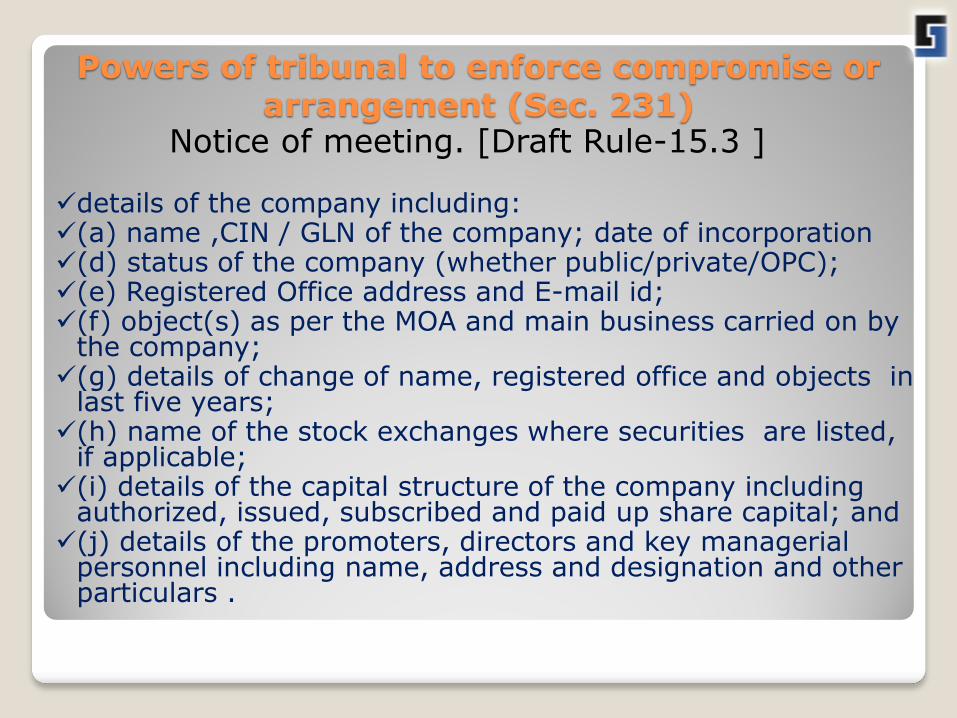

Powers of tribunal to enforce compromise or

arrangement (Sec. 231)

Notice of meeting. [Draft Rule-15.3 ]

details of the company including: (a) name ,CIN / GLN of the company; date of incorporation (d) status of the company (whether public/private/OPC); (e) Registered Office address and E-mail id; (f) object(s) as per the MOA and main business carried on by

the company; (g) details of change of name, registered office and objects in

last five years; (h) name of the stock exchanges where securities are listed,

if applicable; (i) details of the capital structure of the company including

authorized, issued, subscribed and paid up share capital; and (j) details of the promoters, directors and key managerial

personnel including name, address and designation and other particulars .

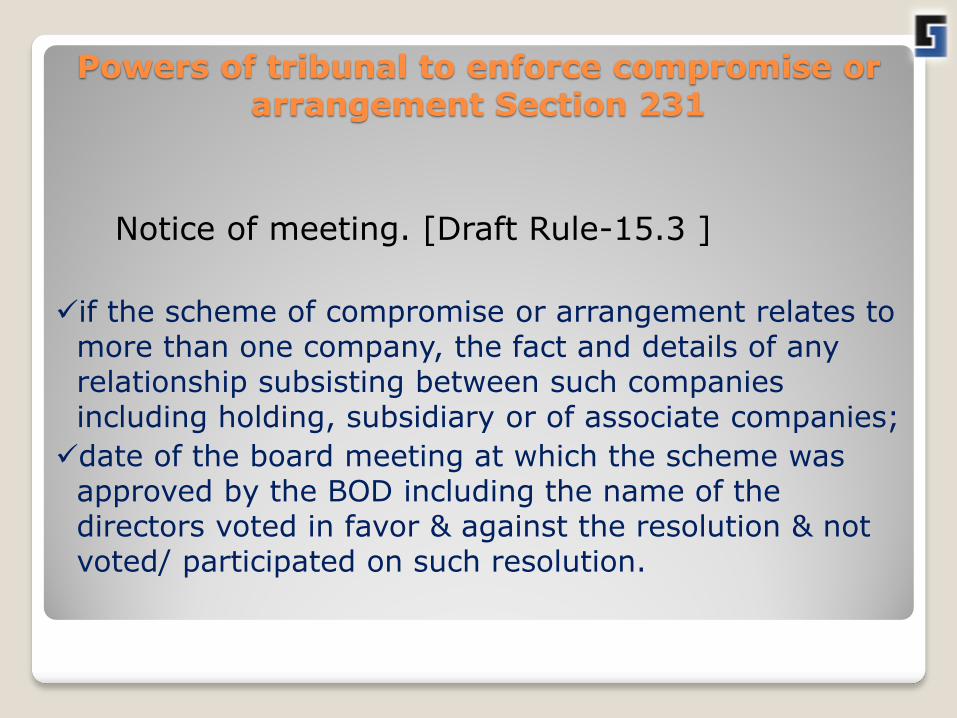

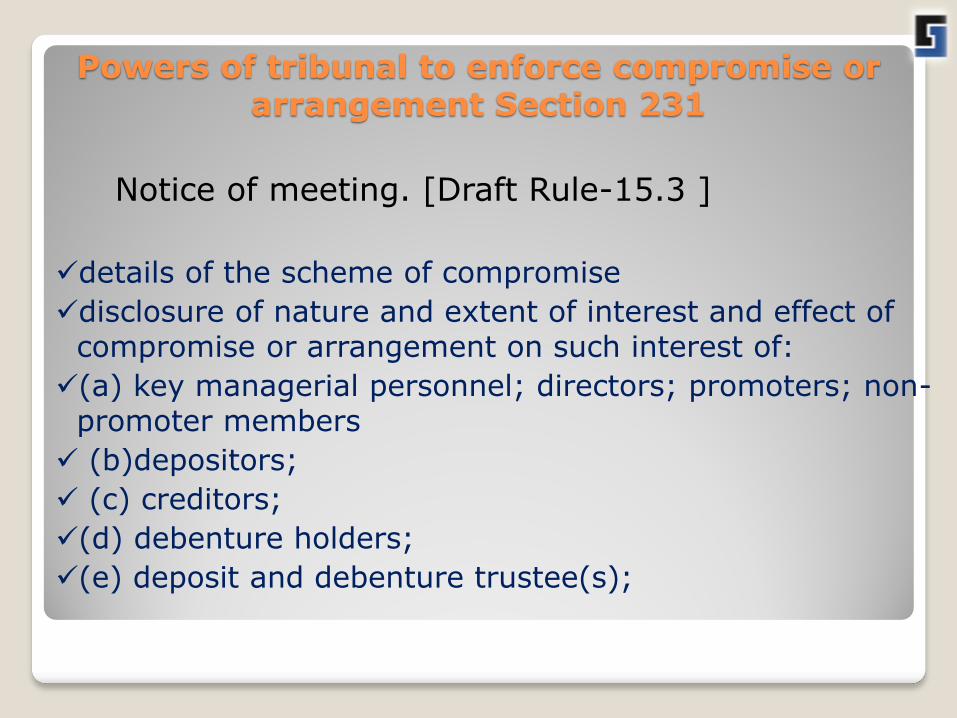

Powers of tribunal to enforce compromise or arrangement Section 231

Notice of meeting. [Draft Rule-15.3 ]

if the scheme of compromise or arrangement relates to more than one company, the fact and details of any relationship subsisting between such companies including holding, subsidiary or of associate companies;

date of the board meeting at which the scheme was approved by the BOD including the name of the directors voted in favor & against the resolution & not voted/ participated on such resolution.

Powers of tribunal to enforce compromise or arrangement Section 231

Notice of meeting. [Draft Rule-15.3 ]

details of the scheme of compromise

disclosure of nature and extent of interest and effect of compromise or arrangement on such interest of:

(a) key managerial personnel; directors; promoters; non-promoter members

(b)depositors;

(c) creditors;

(d) debenture holders;

(e) deposit and debenture trustee(s);

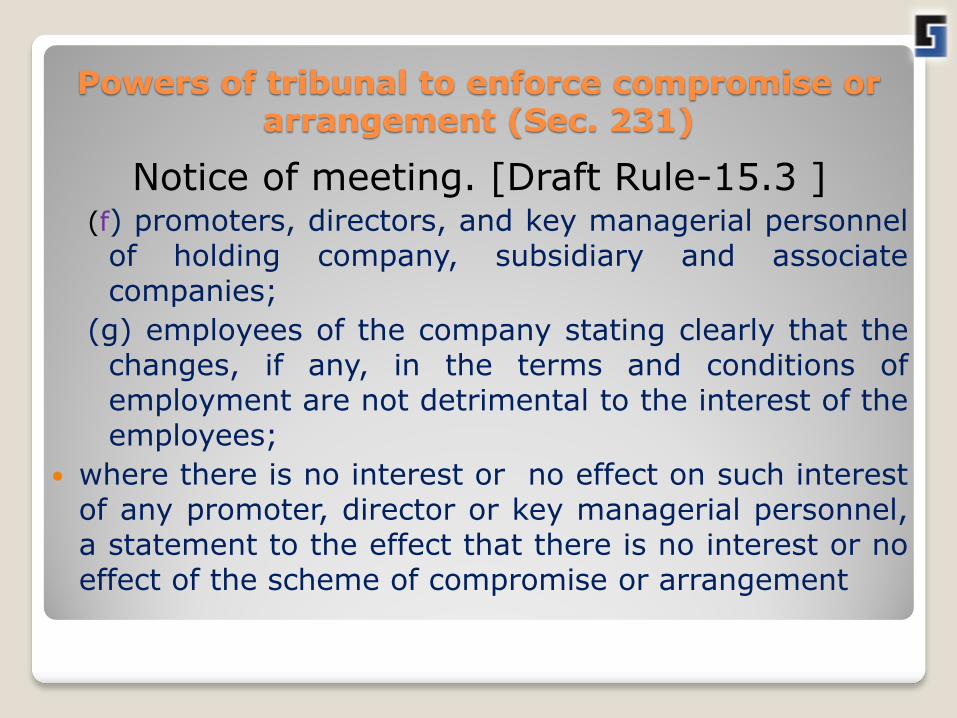

Powers of tribunal to enforce compromise or arrangement (Sec. 231)

Notice of meeting. [Draft Rule-15.3 ]

(f) promoters, directors, and key managerial personnel of holding company, subsidiary and associate companies;

(g) employees of the company stating clearly that the changes, if any, in the terms and conditions of employment are not detrimental to the interest of the employees;

where there is no interest or no effect on such interest of any promoter, director or key managerial personnel, a statement to the effect that there is no interest or no effect of the scheme of compromise or arrangement

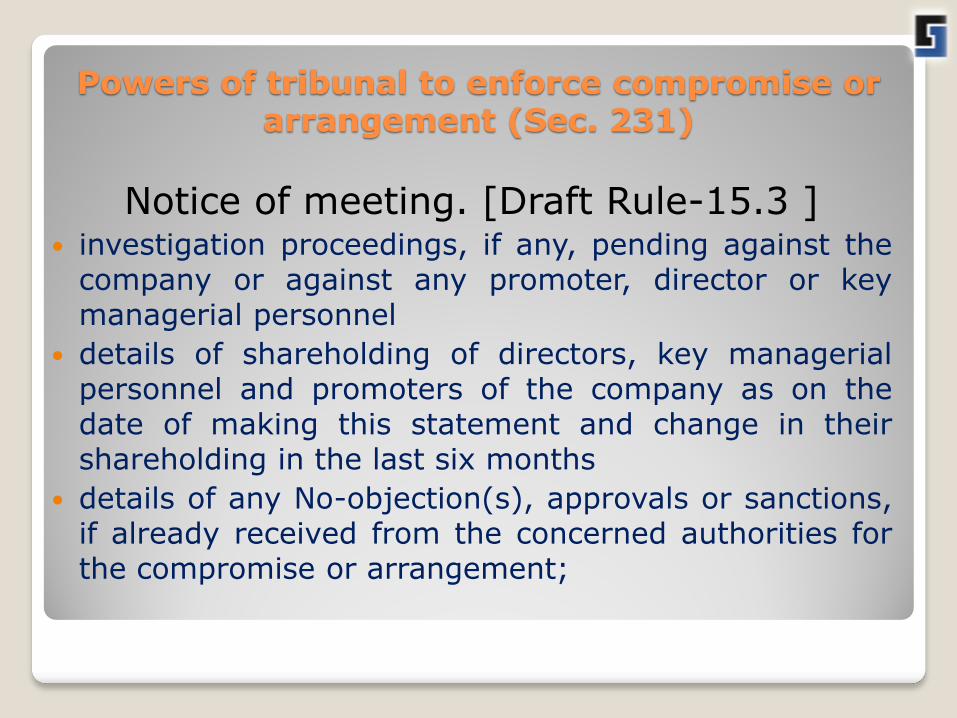

Powers of tribunal to enforce compromise or arrangement (Sec. 231)

Notice of meeting. [Draft Rule-15.3 ] investigation proceedings, if any, pending against the

company or against any promoter, director or key managerial personnel

details of shareholding of directors, key managerial personnel and promoters of the company as on the date of making this statement and change in their shareholding in the last six months

details of any No-objection(s), approvals or sanctions, if already received from the concerned authorities for the compromise or arrangement;

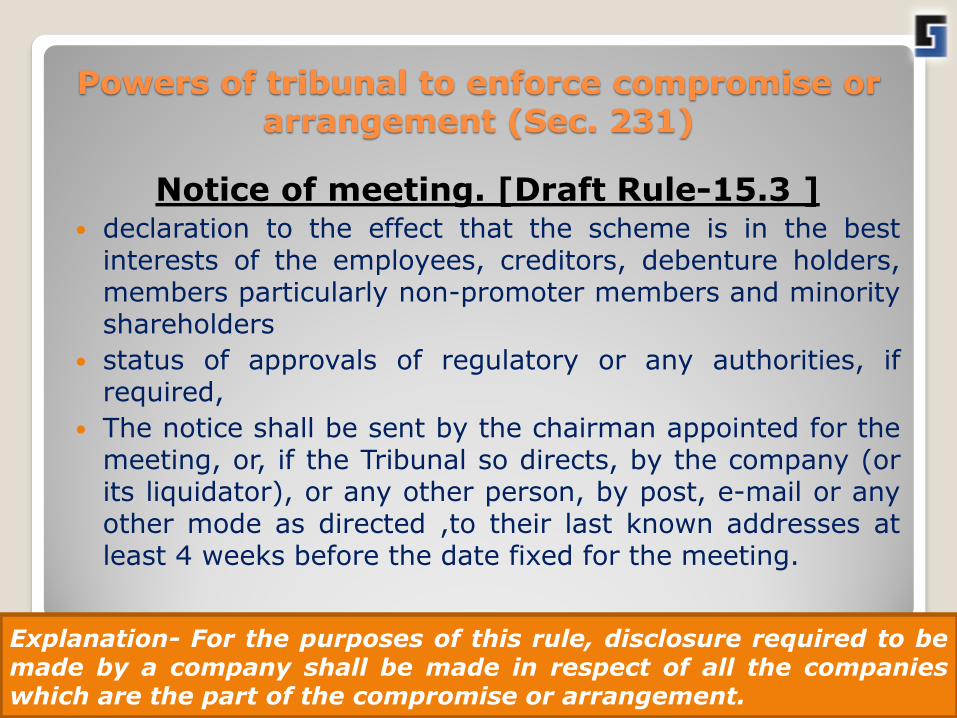

Powers of tribunal to enforce compromise or

arrangement (Sec. 231)

Notice of meeting. [Draft Rule-15.3 ] declaration to the effect that the scheme is in the best

interests of the employees, creditors, debenture holders, members particularly non-promoter members and minority shareholders

status of approvals of regulatory or any authorities, if required,

The notice shall be sent by the chairman appointed for the meeting, or, if the Tribunal so directs, by the company (or its liquidator), or any other person, by post, e-mail or any other mode as directed ,to their last known addresses at least 4 weeks before the date fixed for the meeting.

Explanation- For the purposes of this rule, disclosure required to be made by a company shall be made in respect of all the companies which are the part of the compromise or arrangement.

Powers of tribunal to enforce compromise or arrangement (Sec. 231)

Advertisement of the notice of meeting [Draft Rule 15.5]

The notice of the meeting shall be advertised in such

newspapers and in such manner as the Tribunal may direct, not less than 14 clear days before the date fixed for the meeting. The advertisement shall be in Form No. 15.5.

Notice to dissenting shareholders

Notice to dissenting shareholders for acquiring the shares. [Draft Rule 15.27 ] section 235 (1) , the transferee company shall send a notice in Form No. 15.16 to the dissenting shareholder(s) of the transferor company, at the last intimated address of such shareholder, for acquiring the shares of such dissenting shareholders.

Procedure……………contd.

Mode of Voting for meeting of Member or creditors: In person; By Proxy; By Postal Ballot.

Minimum voting required for passing the resolution: Majority of persons with 3/4th in value of creditors

Majority of persons with 3/4th in value of members

Objection to scheme Members holding Minimum 10% shareholding in company

Creditor holding minimum 5% of outstanding debt as per latest audited Financial statement.

Power of Tribunal

[Rule 15.20 & 15.21]

In case of compromise or arrangement involving merger, the Companies is required to file a Statement of Compliance of order of the Tribunal with Registrar every year. The tribunal may also either suo moto or on the application of any interested person, may direct the company to file a report of working of the scheme and also on receipt of the report pass such order as it may think necessary.

[Rule 15.22]

The Tribunal has been empowered to pass order staying of commencement of any suit or proceeding against the Company.

.

Power of Tribunal

[Rule 15.33]

Save as otherwise provided in these rules, National Company Law Tribunal Rules, 2013, shall apply to the circumstances in which these rules do not specifically provide or elaborate in relation to any matter.

Enforcement of Scheme Sec. 231/392

The tribunal have powers:-

To supervise the implementation of the

Scheme of compromise or arrangement.

To make modification in the scheme for proper

implementation

To make order of winding up (deemed as order under

Section 273),if the scheme cannot be implemented after

modification also

Merger or Demerger of companies Section 232/394

Additional requirement in case of scheme of Merger or Demerger: The report of expert on valuation, if any;

Supplementary accounting treatment if annual accounts of merging company are older then 6 months;

Manner of allotment of shares to non resident after approval of Tribunal;

Merger or Demerger of companies Section 232/394

No Treasury stock to be maintained A certificate by CA/CS/CWA be filed with Registrar in

such form as prescribed till the time scheme of Merger or demerger is given effect.

Merger or Demerger of companies Section 232/394

Compromise or arrangement includes `demerger’ [Draft Rule 15.31 ]’

demerger’ means transfer, of its one or more undertakings by a ‘demerged company’ to any ‘resulting company’ in such a manner as provided in section 2(19AA) of the Income Tax Act, 1961, subject to fulfilling the conditions stipulated in section 2(19AA) of IT Act and shares have been allotted by the ‘resulting company’ to the share holders of the .demerged company’ against the transfer of assets and liabilities.

Merger or Demerger of companies Section 232/394

Compromise or arrangement includes `demerger’ [Draft Rule 15.31 ]’

For the purpose of the compromise in the nature of ‘demerger’ till the Accounting Standards is prescribed for the purpose of ‘demerger’, the Accounting Treatment shall be in accordance with the conditions stipulated in section 2(19AA) of the Income Tax Act, 1961 &

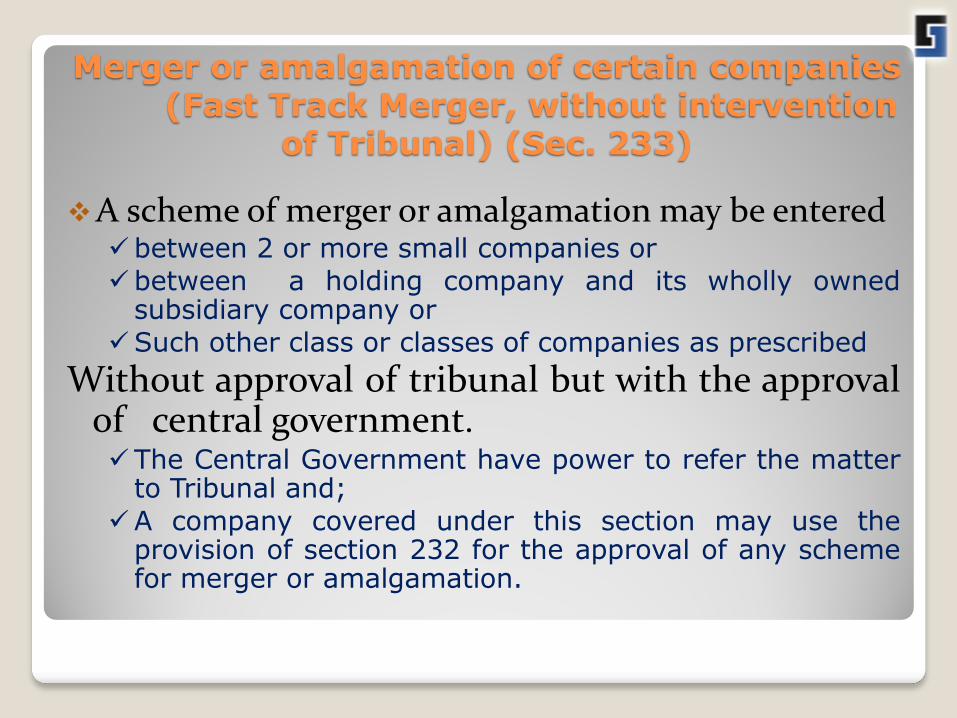

Merger or amalgamation of certain companies (Fast Track Merger, without intervention

of Tribunal) (Sec. 233)

A scheme of merger or amalgamation may be entered between 2 or more small companies or

between a holding company and its wholly owned subsidiary company or

Such other class or classes of companies as prescribed

Without approval of tribunal but with the approval of central government. The Central Government have power to refer the matter

to Tribunal and;

A company covered under this section may use the provision of section 232 for the approval of any scheme for merger or amalgamation.

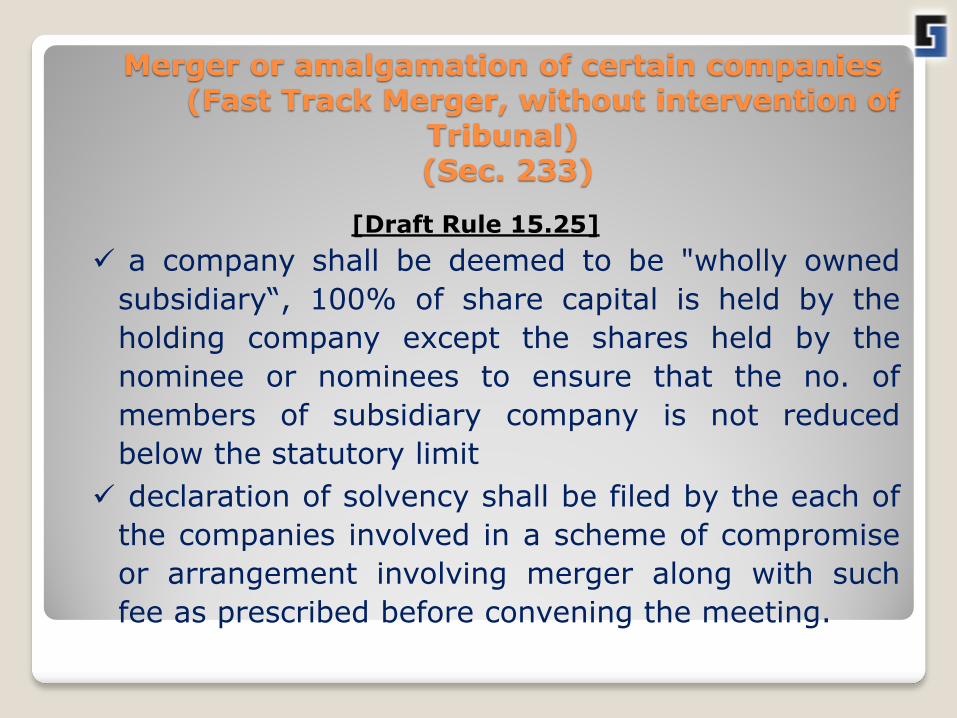

Merger or amalgamation of certain companies (Fast Track Merger, without intervention of

Tribunal) (Sec. 233)

[Draft Rule 15.25]

a company shall be deemed to be "wholly owned

subsidiary“, 100% of share capital is held by the

holding company except the shares held by the

nominee or nominees to ensure that the no. of

members of subsidiary company is not reduced

below the statutory limit

declaration of solvency shall be filed by the each of

the companies involved in a scheme of compromise

or arrangement involving merger along with such

fee as prescribed before convening the meeting.

Merger or amalgamation of certain companies (Fast Track Merger, without intervention of

Tribunal) (Sec. 233)

[Draft Rule 15.25]

The notice of the meeting to the members and

creditors shall be accompanied by :-

(a) a statement, section 230 (3);

(b) the declaration of solvency made section 233 (1)(c);

(c) a copy of the scheme.

transferee company shall, within 7 days after the conclusion of the meeting(s, file in Form No. 15.13 a copy of the scheme along with report with the CG, ROC & Official Liquidator, where the registered office of the company is situated.

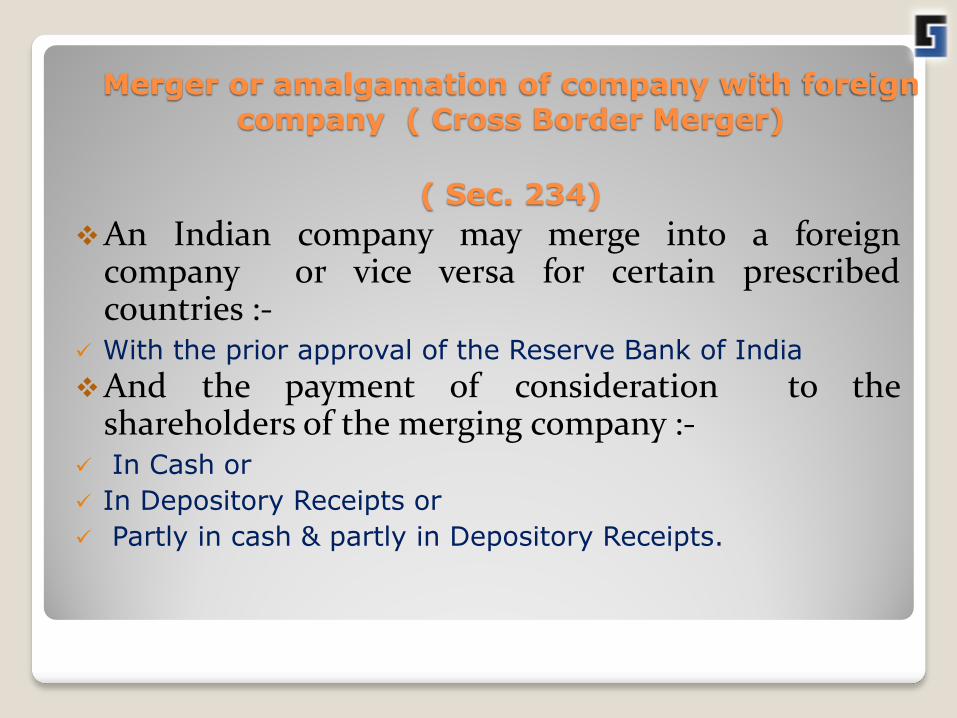

Merger or amalgamation of company with foreign company ( Cross Border Merger)

( Sec. 234)

An Indian company may merge into a foreign company or vice versa for certain prescribed countries :-

With the prior approval of the Reserve Bank of India

And the payment of consideration to the shareholders of the merging company :-

In Cash or

In Depository Receipts or

Partly in cash & partly in Depository Receipts.

Purchase of minority shareholding (Sec. 236)

• Of 90% or more of the issued share capital of

any company

An acquirer, or person acting in concert becoming registered

holder

• Of 90% or more of the issued share capital of any company

Any person or group of person by virtue of amalgamation, share Exchange, Conversion of securities or for any other reason becoming holder

Shall notify the company of their intension to buy the remaining equity shares

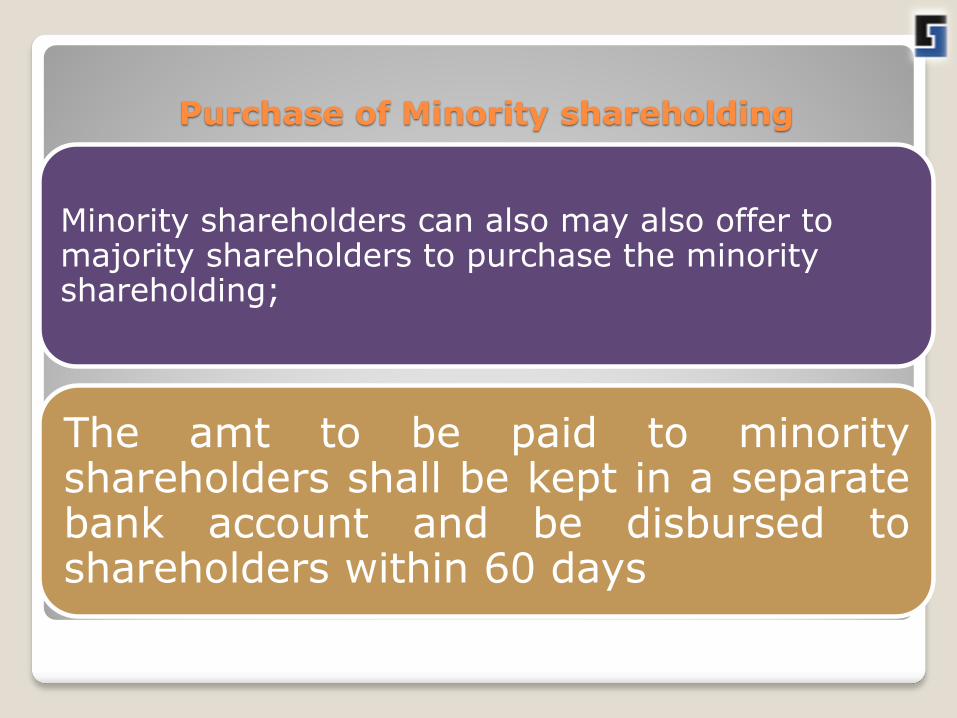

Purchase of Minority shareholding

Minority shareholders can also may also offer to majority shareholders to purchase the minority shareholding;

The amt to be paid to minority shareholders shall be kept in a separate bank account and be disbursed to shareholders within 60 days

Purchase of Minority shareholding

Determination of price for purchase of minority

shareholding. [Draft Rule 15.28]

Section 236 (2) , the registered valuer shall determine the price (offer price) to be paid by the acquirer, person or group of persons for purchase of equity shares of the minority shareholders as per the following rules:

In the case of a listed company

the registered valuer shall also provide a proper valuation report of valuation addressed to the Board of directors giving justification for such valuation

Purchase of Minority shareholding

Determination of price for purchase of minority

shareholding. [Draft Rule 15.28]

the registered valuer shall also provide a proper valuation report/basis of valuation addressed to the Board of directors of the company giving justification for such valuation.

In the case of an unlisted company and a private company, the offer price shall be determined after taking into account the following factors:- (a) the highest price paid by the acquirer, person or group of persons for acquisition during last 12 months; (b) the fair price of shares to be determined by the registered valuer after taking into account valuation parameters including return on net worth, book value, EPS, price earning

Preservation of books and papers of amalgamated companies

(Sec. 239)

The books and papers of amalgamated company or whose shares have been acquired by, another company under this Chapter:

shall not be disposed of without prior permission of Central Government.

Any person may be appointed by the Government to examine books of accounts & Papers

Liability of officers in respect of offences committed prior to merger, amalgamation etc

(Sec. 240)

The liabilities of officer in default of transferor company prior to its merger, amalgamation or acquisition shall continue after such merger, amalgamation or acquisition

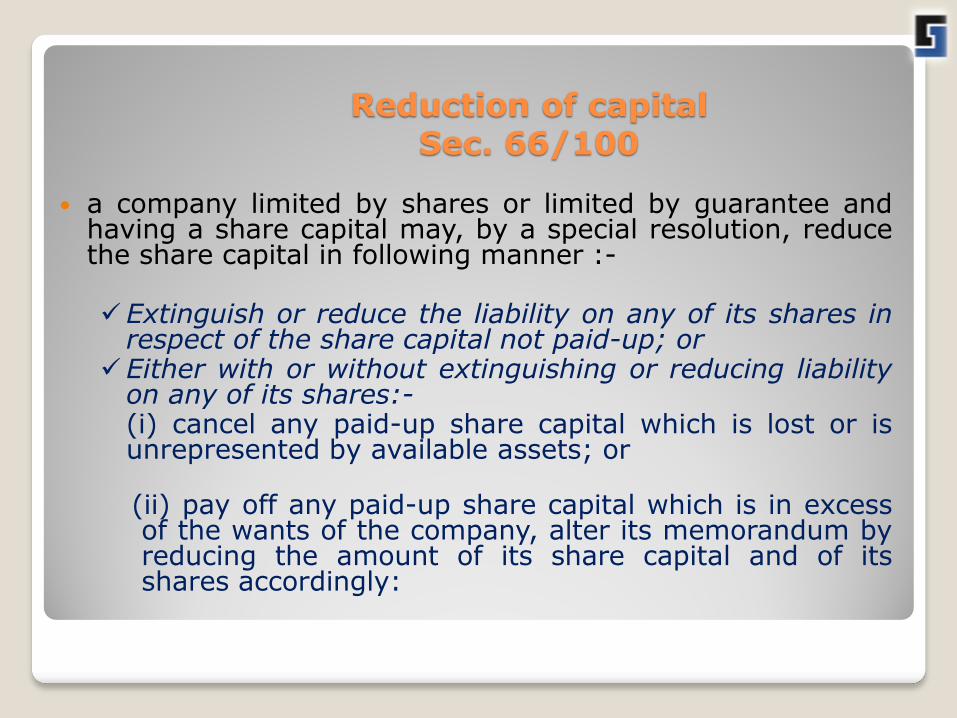

Reduction of capital Sec. 66/100

a company limited by shares or limited by guarantee and having a share capital may, by a special resolution, reduce the share capital in following manner :- Extinguish or reduce the liability on any of its shares in

respect of the share capital not paid-up; or Either with or without extinguishing or reducing liability

on any of its shares:- (i) cancel any paid-up share capital which is lost or is

unrepresented by available assets; or

(ii) pay off any paid-up share capital which is in excess of the wants of the company, alter its memorandum by reducing the amount of its share capital and of its shares accordingly:

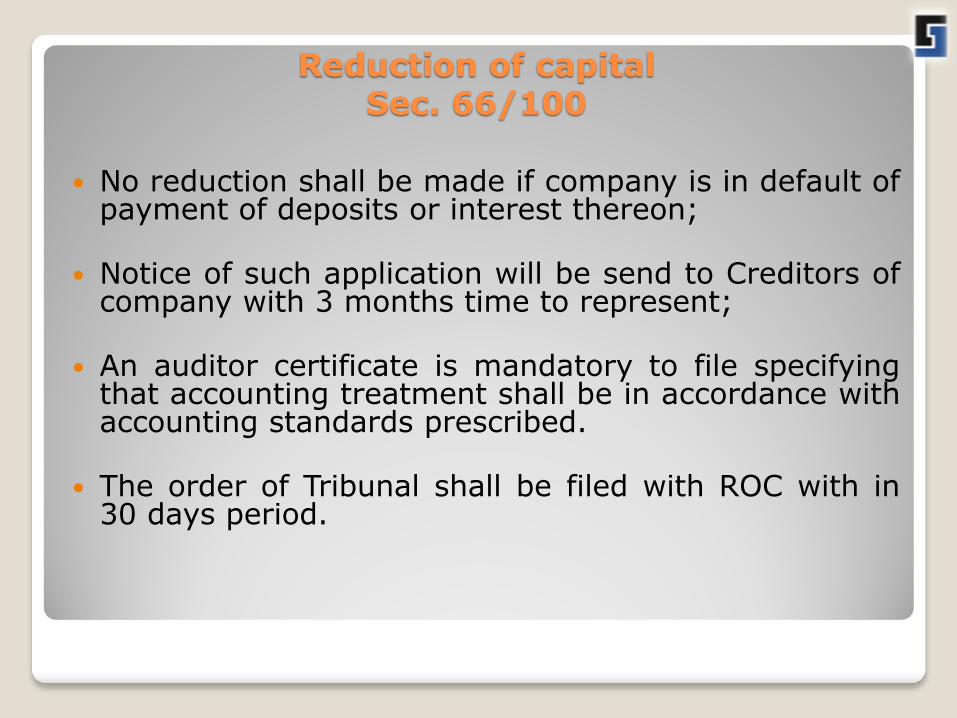

Reduction of capital Sec. 66/100

No reduction shall be made if company is in default of

payment of deposits or interest thereon;

Notice of such application will be send to Creditors of company with 3 months time to represent;

An auditor certificate is mandatory to file specifying that accounting treatment shall be in accordance with accounting standards prescribed.

The order of Tribunal shall be filed with ROC with in 30 days period.

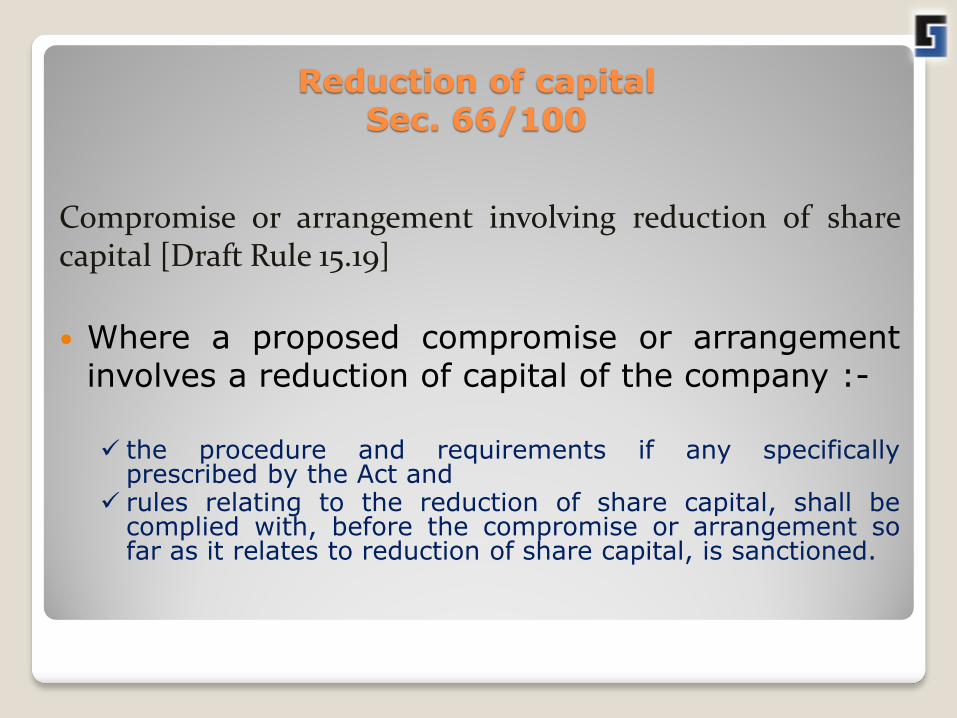

Reduction of capital Sec. 66/100

Compromise or arrangement involving reduction of share capital [Draft Rule 15.19]

Where a proposed compromise or arrangement involves a reduction of capital of the company :-

the procedure and requirements if any specifically

prescribed by the Act and rules relating to the reduction of share capital, shall be

complied with, before the compromise or arrangement so far as it relates to reduction of share capital, is sanctioned.

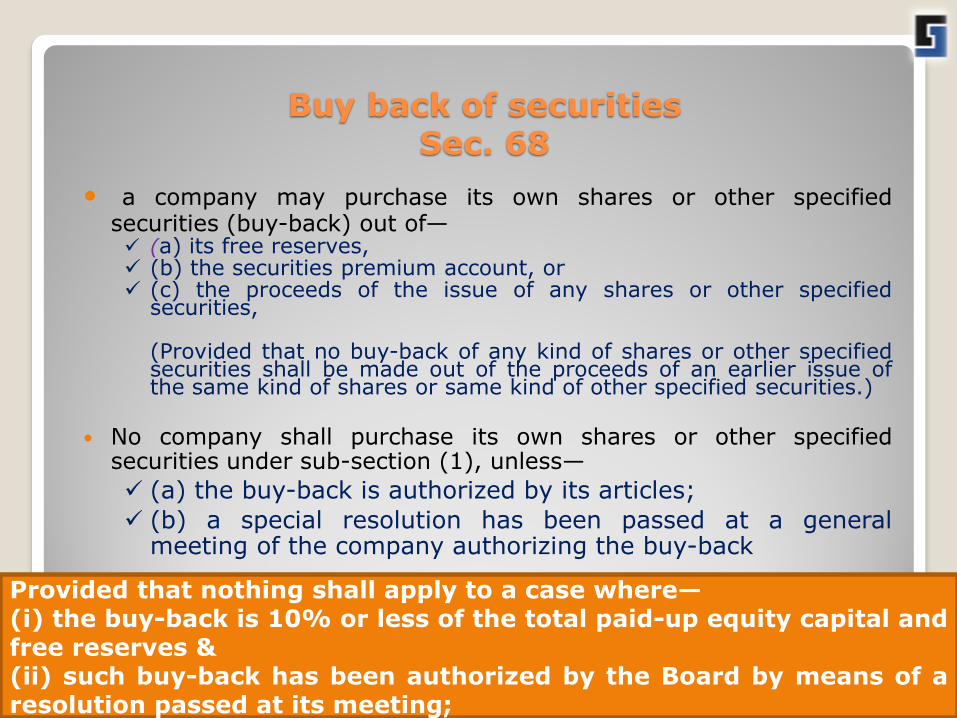

Buy back of securities Sec. 68

a company may purchase its own shares or other specified securities (buy-back) out of— (a) its free reserves, (b) the securities premium account, or (c) the proceeds of the issue of any shares or other specified

securities, (Provided that no buy-back of any kind of shares or other specified

securities shall be made out of the proceeds of an earlier issue of the same kind of shares or same kind of other specified securities.)

No company shall purchase its own shares or other specified securities under sub-section (1), unless—

(a) the buy-back is authorized by its articles;

(b) a special resolution has been passed at a general meeting of the company authorizing the buy-back

Provided that nothing shall apply to a case where— (i) the buy-back is 10% or less of the total paid-up equity capital and free reserves & (ii) such buy-back has been authorized by the Board by means of a resolution passed at its meeting;

Buy back of securities Sec. 68

the buy-back is 25% or less of the aggregate of paid-up capital and free reserves

Provided that in respect of the buy-back of equity shares in any financial year, the reference to twenty-five per cent. shall be construed with respect to its total paid-up equity capital in that financial year]

the ratio of the aggregate of secured and unsecured debts owed by the company after buy-back is not more than twice the paid-up capital and its free reserves:

Buy back of securities Sec. 68

[Provided that the Central Government may, by order, notify a higher ratio of the debt to capital and free reserves for a class or classes of companies]

all the shares or other specified securities for buy-back are fully paid-up

the buy-back of securities listed on any recognized stock exchange is in accordance with the regulations made by the Securities and Exchange Board in this behalf; and

the buy-back in respect of other specified securities is in accordance with such rules as may be prescribed:

[Provided that no offer of buy-back shall be made within a period of one year reckoned from the date of the closure of the preceding offer of buy-back, if any]

Buy back of securities Sec. 68

The notice of the meeting at which the special resolution is proposed to be passed shall be accompanied by an explanatory statement stating—

(a) a full and complete disclosure of all material facts;

(b) the necessity for the buy-back;

(c) the class of shares or securities intended to be purchased under the buy-back;

(d) the amount to be invested under the buy-back; and

(e) the time-limit for completion of buy-back.

Buy back of securities Sec. 68

Every buy-back shall be completed within a period of one year from the date of passing of the special resolution, or as the case may be, the resolution passed by the Board

The buy-back under sub-section (1) may be—

(a)from the existing shareholders or security holders on a proportionate basis;

(b) from the open market;

(c)by purchasing the securities issued to employees of the company pursuant to a scheme of stock option or sweat equity.

Buy back of securities Sec. 68

Where a company proposes to buy-back its own specified securities in pursuance of a special resolution shall before making such buy-back, file with ROC & SEBI, a declaration of solvency .

signed by at least 2 directors of the company, one of whom shall be the MD, if any,&

verified by an affidavit that the Board of Directors has made a full inquiry into the affairs of the company that it is capable of meeting its liabilities & will not be rendered insolvent within a period of 1 year from the date of declaration

[Provided that no declaration of solvency shall be filed with the SEBI whose shares are not listed on any recognized stock exchange.]

Where a company buys back its own shares or other specified securities, it shall

extinguish and physically destroy the shares or securities so bought back within seven days of the last date of completion of buy-back.

Buy back of securities Sec. 68

Where a company completes a buy-back of securities, it shall not make a further issue of the same kind of securities including allotment of new shares or other specified securities within a period of 6 months except by way of a bonus issue or in the discharge of subsisting obligations such as conversion of

warrants, stock option schemes, sweat equity or conversion of preference shares or debentures into equity shares

Where a company buys back its shares or other specified securities shall maintain a register of the shares or securities so bought, the consideration paid for the shares or securities bought back, the date of cancellation of shares or securities, the date of extinguishing and physically destroying the shares or

securities. A company shall, after the completion of the buy-back file with the ROC &

SEBI a return containing such particulars relating to the buy-back within 30 days of completion, [Provided that no return shall be filed with the Securities and Exchange Board by a company whose shares are not listed on any recognized stock exchange]

Buy back of securities Sec. 68

Buy-back of shares or other securities [ Rule 17 of Companies (Shares and Debentures), Rules

2014]

the following rules shall be complied with by private companies and unlisted public companies for buy-back of their securities :-

For passing a special resolution the explanatory statement to be annexed to the notice of the general meeting shall contain the following disclosures.

The company shall, before the buy-back of shares, file with the ROC a letter of offer in Form No. 4.8, along with the fee .

[Provided that such letter of offer shall be dated and signed on behalf of the Board of directors of the company by not less than two directors of the company, one of whom shall be the managing director, where there is one.]

Buy back of securities Sec. 68 (Cont..)

Buy-back of shares or other securities [ Rule 17 of Companies (Shares and Debentures), Rules

2014]

Listed company shall file, along with the letter of offer, a declaration of solvency in Form No. SH- 9 along with the fee with the ROC & the SEBI, and signed by at least two directors of the company, one of whom shall be the MD if any, and verified by an affidavit as specified in the said Form.

The letter of offer shall be dispatched to the shareholders or security holders immediately after filing the same with the ROC.

Buy back of securities Sec. 68

Buy-back of shares or other securities [ Rule 17 of Companies (Shares and Debentures), Rules 2014]

The offer for buy-back shall remain open for a period of not less than 15 days and not exceeding 30 days from the date of dispatch of the letter of offer.

If no. of securities offered is more than the total no. of securities to be bought back, the acceptance per shareholder shall be on proportionate basis out of the total shares offered.

The company shall complete the verifications of the offers received within 15 days from the date of closure of the offer and the securities lodged shall be deemed to be accepted unless a communication of rejection is made within 21 days from the closure of the offer.

Buy back of securities Sec. 68

Buy-back of shares or other securities [ Rule 17 of Companies (Shares and Debentures), Rules 2014]

The company shall immediately after closure of the offer, open a separate bank account and deposit such sum, as would make up the entire sum due and payable as consideration for the shares tendered for buy-back .

The company shall within 7 days of the time specified :-

(a) make payment of consideration in cash to those security holders whose securities have been accepted, or

(b) return the share certificates to the security holders whose securities have not been accepted at all or the balance of securities in case of part acceptance .

Buy back of securities Sec. 68

Buy-back of shares or other securities [Draft Rule 4.15]

The company, after the completion of the buy-back, shall file with the Registrar, and in case of a listed company with the ROC and the SEBI, a return in the Form No. 4.11 along with the fee

There shall be annexed to the return filed with the Registrar in Form No. 4.14, a certificate in Form No. 4.15 signed by two directors of the company including the MD if any, certifying that the buy-back of securities has been made in compliance with the provisions of the ACT

Reduction of capital Sec. 66/100

No reduction shall be made if company is in default of payment of deposits or interest thereon;

Notice of such application will be send to Creditors of company with 3 months time to represent;

An auditor certificate is mandatory to file specifying that accounting treatment shall be in accordance with accounting standards prescribed.

The order of Tribunal shall be filed with ROC with in 30 days

period.

Reduction of capital Sec. 66/100

Compromise or arrangement involving reduction of share capital [Draft Rule 15.19]

Where a proposed compromise or arrangement involves a reduction of capital of the company :- the procedure and requirements if any specifically

prescribed by the Act and

rules relating to the reduction of share capital, shall be complied with, before the compromise or arrangement so far as it relates to reduction of share capital, is sanctioned.

Buy back of securities Sec. 68

Buy-back of shares or other securities [Rule. 7]

the following rules shall be complied with by private companies and unlisted public companies for buy-back of their securities :-

For passing a special resolution the explanatory statement to be annexed to the notice of the general meeting shall contain the following disclosures.

The company shall, before the buy-back of shares, file with the ROC a letter of offer in Form SH. 8, along with the fee .

[Provided that such letter of offer shall be dated and signed on behalf of the Board of directors of the company by not less than two directors of the company, one of whom shall be the managing director, where there is one.]

Thanks

Arun Gupta

managing counsel

factum legal , advocates & solicitors

Tel : (O) 011-41066313 (M) 9810275571

www.factumlegal.com;

“It is good to have an end to journey toward; but it is the journey that matters, in the end.”