Embed Size (px)

Citation preview

University of SunderlandMaster of Business Administration (MBA)

Global CorporateStrategy

Published byThe University of Sunderland

The publisher endeavours to ensure that all its materials are freefrom bias or discrimination on grounds of religious or politicalbelief, gender, race or physical ability. These course materials areproduced from paper derived from sustainable forests where thereplacement rate exceeds consumption.

The copying, storage in any retrieval system, transmission,reproduction in any form or resale of the course materials or anypart thereof without the prior written permission of the Universityof Sunderland is an infringement of copyright and will result inlegal proceedings.

© University of Sunderland 2004

Every effort has been made to trace all copyright owners ofmaterial used in this module but if any have been inadvertentlyoverlooked, the University of Sunderland Press will be please tomake the necessary arrangement at the first opportunity.

These materials have been produced by the University ofSunderland Business School in conjunction with ResourceDevelopment International.

Global Corporate Strategy

Contents

How to use this workbook

Introduction

Unit 1Strategy Defined and Key Concepts

Introduction 1Definition of Strategy 2Levels of Strategy 5Strategic Concepts 7Strategic Thinking 9Strategic Models 12Summary 34

Unit 2Strategic Capability

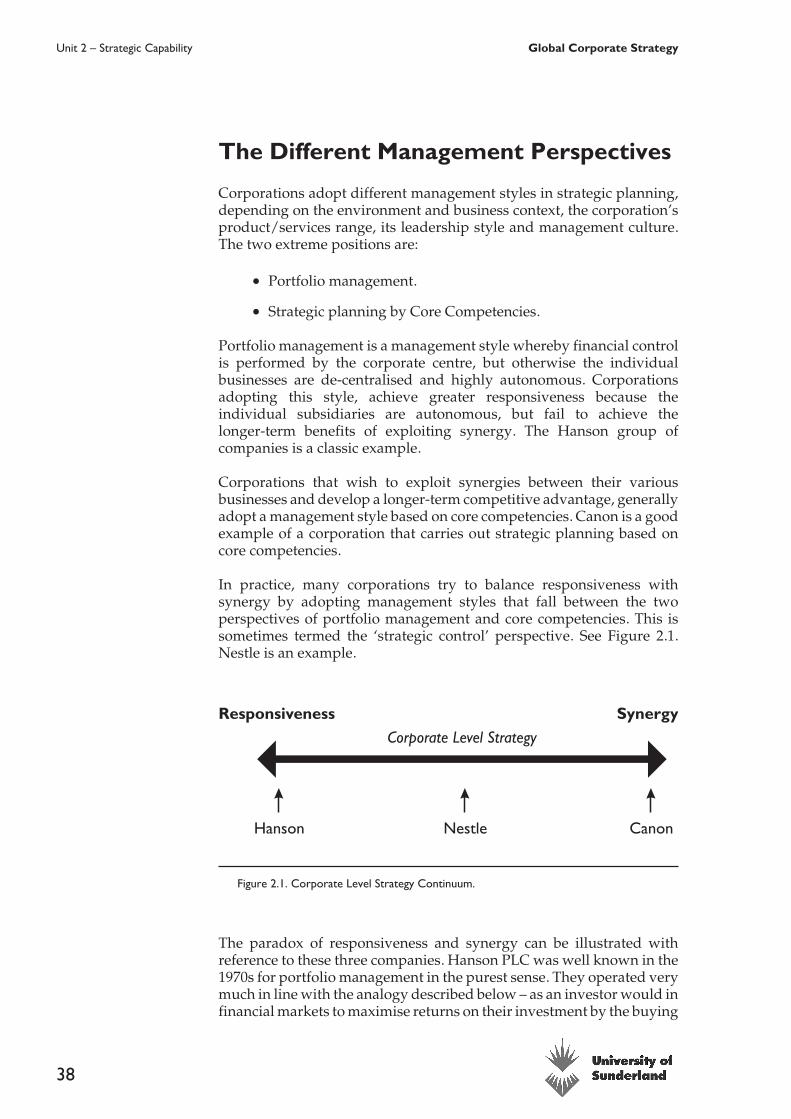

Introduction 37The Different Management Perspectives 38Portfolio Management 39The Core competencies perspective 48Divestment 51Summary 57

Unit 3Globalisation

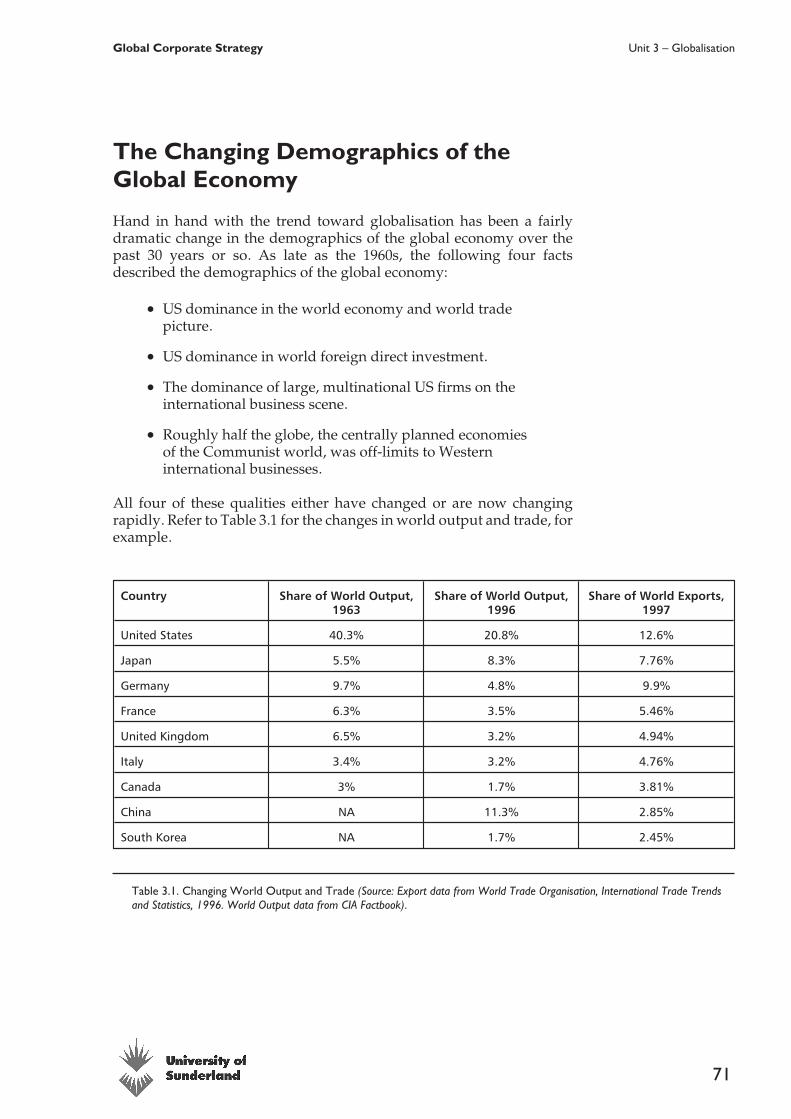

Introduction 61What is Globalisation 61The Globalisation of Markets 66The Globalisation of Production 68Drivers of Globalisation 70The Changing Demographics of the Global Economy 73The Globalisation Debate: Prosperity or Impoverishment? 76Managing in the Global Marketplace 78Summary 88

Unit 4‘Altering the Boundary’ – Alliances and Mergers

Introduction 91Paradox of Competition and Co-operation 92Global Strategic Alliances 92Mergers and Acquisitions 104Summary 131

Unit 5Value Management

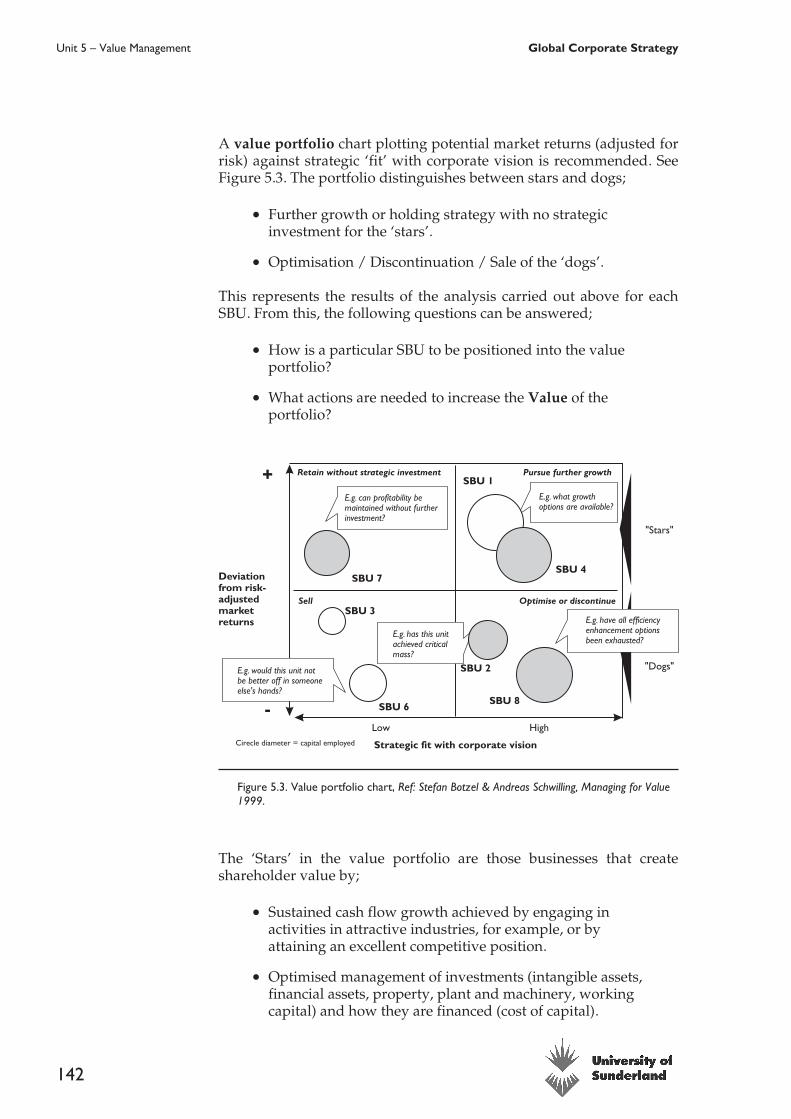

Introduction 133Paradox of Profitability and Responsibility 134The Concept of Value 134Value Management 137What is a Value-Driven Approach 141Summary 151

Unit 6Corporate Governance and Ethics

Introduction 155Corporate Governance 156Business Ethics 173Summary 188

Unit 7Managing Complexity

Introduction 191Paradox of Control and Chaos 192Systems Thinking 193Soft Systems Methodology (SSM) 200Strategic Control? 204Summary 207

Unit 8Knowledge Management

Introduction 209Theoretical Concepts on Knowledge 210Knowledge 212Knowledge Transfer 215Practical steps to promote Knowledge Management 218Summary 237

Unit 9Innovation

Introduction 239Innovation strategies 240Innovation and established companies 241Conclusion 248Summary 255

Unit 10Strategic IT and e-Business

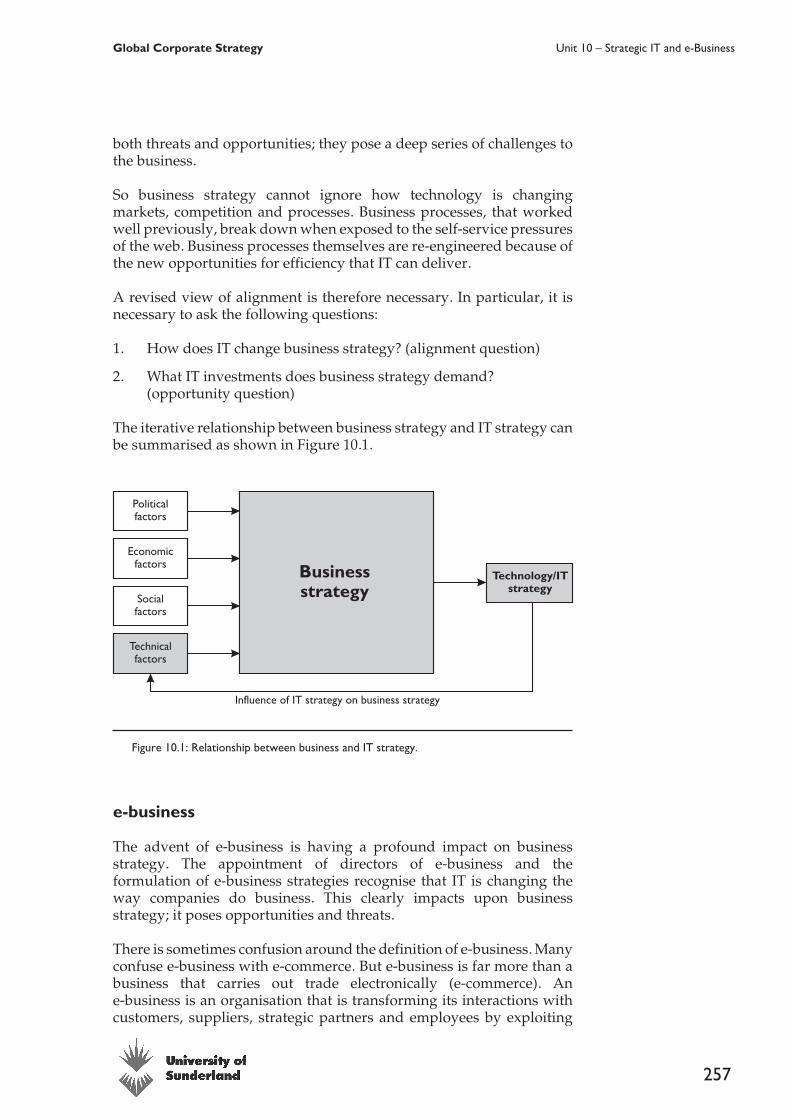

Introduction 259The Link between Business and IT Strategy 260IT Strategy Methodology 264Summary 275References 276

5

Global Corporate Strategy Global Corporate Strategy – Contents

How to use this workbook

This workbook has been designed to provide you with the coursematerial necessary to complete Global Corporate Strategy by distancelearning. At various stages throughout the module you will encountericons as outlined below which indicate what you are required to do tohelp you learn.

This Activity icon refers to an activity where you are required to undertake aspecific task. These could include reading, questioning, writing, research,analysing, evaluating, etc.

This Activity Feedback icon is used to provide you with the informationrequired to confirm and reinforce the learning outcomes of the activity.

This icon shows where the Virtual Campus could be useful as a medium fordiscussion on the relevant topic.

This Key Point icon is included to stress the importance of a particular pieceof information.

It is important that you utilise these icons as together they will provideyou with the underpinning knowledge required to understand conceptsand theories and apply them to the business and managementenvironment. Try to use your own background knowledge whencompleting the activities and draw the best ideas and solutions you canfrom your work experience. If possible, discuss your ideas with otherstudents or your colleagues; this will make learning much morestimulating. Remember, if in doubt, or you need answers to anyquestions about this workbook or how to study, ask your tutor.

i

Global Corporate Strategy

Preface

Corporate Strategy is a very wide and all encompassing subject area.One only has to look at the relative content of individual key texts in thisarea (e.g. De Wit & Meyer, Lynch, Johnson & Scholes, etc.) to appreciatethe volume of material that has been written over the years.

However, relatively speaking, it is the newest area of managementresearch. Initial work in strategy took place in the early sixties. In theirbook Strategy Safari, Mintzberg, Alhstrand and Lampel (1998) breakdown strategy theory development into ten schools of thought and thisprovides a thoughtful starting point for the study of this module. It alsoindicates a wide range of divergent views on the subject. The ten schoolsare;

1 The Design school – strategy seeks to match internal capabilitiesto external possibilities

2 The Planning school – strategy is a formal, planned process

3 The Positioning school – only a few key strategies are desirable inany given industry (generic strategy) and these are formulated byanalytical processes

4 The Entrepreneurial school – strategy is a ‘visionary’ processwhere an organisation is responsive to the dictating individual

5 The Cognitive school – strategy is a mental process dependantupon what the strategy process means in the mind of thestrategist (human cognition)

6 The Learning school – strategies emerge as people /organisations come to learn about a situation as well as theirorganisation’s capability of dealing with it

7 The Power school – the use of power and politics to negotiatestrategies favourable to particular interests

8 The Cultural school – strategy as a collective process of socialinteraction, based on the beliefs and understandings shared bythe members of an organisation

9 The Environmental school – the business environment becomesthe central actor in the strategy making process – the organisationmust respond to these forces

iii

10 The Configuration school – strategy making is a process ofleaping from one state to another with relative stability inbetween

All of these schools have key writers. However, it would be erroneous toregard these schools as being ‘separated’ or that it is right to look at thesein isolation. Indeed, it is the opposite. Each perspective is inter-mingledwith one another and interacts over time. Mintzberg, Alhstrand andLampel use the analogy of an elephant to emphasise the holistic natureof strategy - one cannot get a clear picture of ‘the elephant’ by looking ateach separate part of its body. Hence, as a student of strategy, you mustkeep in mind ALL TEN schools.

The ten schools can be split into two ‘types’. Schools 1-3 can be seen as‘prescriptive’, that is to say they are based on the belief that CorporateStrategy is a planned, analytical hard data process. On the other hand,Schools 4-10 can be seen as ‘descriptive’. In these areas, writers believethat strategy is a complex, uncertain, subjective and ‘soft’ data process.There is a range of theory and academic writing to support all of theseperspectives.

Another range of key perspectives is related to your core textbooksupplied with these materials. Whereas major texts such as Johnson &Scholes, and Lynch take a ‘linear’ view of strategy by presentingconcepts ‘one after the other’, de Wit & Meyer (2004) analyse a series of‘paradoxes’. They define the opposite ends of a continuum, leaving thestudent with the tools to analyse case studies and decide for themselvesthe key strategic perspective for organisations. This approach isparticularly important for this module.

Students will be expected to produce an academic and fully referencedargument seeking to define the key strategic perspectives oforganisations. The argument, and supporting evidence, produced is key– stating an appropriate school of thought or positioning anorganisation in relation to a strategic paradox is not the key issue. Theability to analyse (rather than describe) strategy and coming to areasoned judgement is the overriding objective in assessment.

The paradoxes addressed by de Wit & Meyer (2004) are;

� The Paradox of Logic and Creativity (Strategic Thinking –Rational vs. Generative).

� The Paradox of Deliberateness and Emergentness(Strategy Formulation – Planned vs. Incremental).

� The Paradox of Revolution and Evolution (StrategicChange – Continuous vs. Discontinuous).

� The Paradox of Markets and Resources (Business LevelStrategy – Outside-In vs. Inside-Out).

iv

Preface Global Corporate Strategy

� The Paradox of Responsiveness and Synergy (CorporateLevel Strategy – Portfolio vs. Core Competence).

� The Paradox of Competition and Co-operation (NetworkLevel Strategy – Discrete vs. Embedded Organisations).

� The Paradox of Compliance and Choice (IndustryContext – Industry Evolution vs. Industry Creation).

� The Paradox of Control and Chaos (OrganisationalContext – Leadership vs. Dynamics).

� The Paradox of Globalisation and Localisation(International Context – Global Convergence vs.International Diversity).

� The Paradox of Profitability and Responsibility(Organisational Purpose – Shareholder Value vs.Stakeholder Values).

Naturally, many of theses dichotomies can be examined in isolation butare, similarly to the schools of thought above, likely to be interrelatedand so discussing and building an academic argument in respect of onewill inevitably lead to another.

It would be possible to provide you with a module that deals withseparate areas of an organisation individually. Indeed, this type ofmodule has been delivered many times in the past. In other words, it ispossible to look at marketing, HRM, operations, finance, etc, as separateentities and reflect the ‘strategic’ aspects of these areas. However, thiswould not give due credence to the fact that strategy is essentially a‘holistic’ subject. That is to say, ‘corporate strategy’ affects theorganisation as a whole. Each element of an organisation cannot beconsidered in isolation. Therefore, corporate strategy must be examinedin an ‘all embracing’ manner.

One must be careful to use the word ‘organisation’. If the word‘business’ were to be used this would tend to ignore some veryproductive study areas in public and ‘not for profit’ organisations.Much can be learned from such organisations and, although‘businesses’ are typically used to demonstrate key points, organisationswhose prime objective is not related to profitability cannot be ignored.

Many contemporary issues in ‘strategy’ are reflected in this module.Once again, it is erroneous to regard each of the ten ‘themes’ as existingin isolation or in ‘silos’. There are links between themes that, in somecase, will be pointed out in the text, but in others it will be left to yourown imagination and analytical ability. Individual techniques such asthose employed in marketing and finance, for example, are onlytouched on where necessary. This would detract from the ‘ethos’ of thismodule.

v

Global Corporate Strategy Preface

Due to the nature of the subject area it is impossible to cover all aspects –simply think about how long it would take to read one of the key textsfrom cover to cover! The topics omitted are still important – the studytime allocated to this module is not enough to cover everything.Therefore, it is in your interests to read more widely than the specifiedreading dictates.

The module will enable you to recognise and describe many differentfeatures of organisations. However, the module will encourage you toanalyse these issues and be able to understand why organisations dowhat they do and look critically at their strategic decisions. You shouldbe able to recognise and understand the importance of the variousaspects of strategic decision making and implementation processes.

You should remember that it is a Masters level module and you willonly reap the full benefits if you put in the effort. This means preparingwell and fully utilizing other arrangements to enhance your learning,e.g. tutor support and contributing to remote discussion and chat viaavailable virtual learning environments.

vi

Preface Global Corporate Strategy

Unit 1

Strategy Defined and KeyConcepts

LEARNING OUTCOMES

Following the completion of this unit you should be able to:

� Explain what corporate strategy is.

� Evaluate the importance of strategy to a manager in an organisation.

� Compare the characteristics of strategic decision making.

� Assess the skills required to be a strategist.

� Assess the holistic nature of strategy.

Introduction

The term corporate strategy can bring to mind various aspects ofcorporate management. Vision, competition, competitive advantage,new markets, managing for shareholder value, moulding corporateculture, operational processes for execution, strategic plans all come tomind. But what exactly is strategy?

In this unit we shall define strategy, particularly as it applies to amanager. We shall also look at the various levels of strategy, and the keyrole of strategic thinking within an organisation. We shall examine therole of strategic ‘models’ and how they can assist organisations inbreaking down the complexity of strategic thinking. In particular, weshall examine the Johnson & Scholes model.

Depending on the maturity of the market that a company operateswithin, the maturity of the company, and the corporate managementculture, organisations adopt different approaches to strategy. Theapproach can be classified as deliberate, emergent or incremental, andwe shall examine the differences between them.

1

Finally, we shall look at two case studies to understand how the keyconcepts of strategy apply practically within organisations.

Definition of Strategy

There is no universal definition of strategy. Strategy applies to manydisparate fields such as gaming strategy, economic strategy, investmentstrategy, military strategy, marketing strategy and indeed corporateglobal strategy. Taking a conventional approach, strategy can bethought of as a long term plan of action or execution designed to achievea particular goal, such as achieving competitive advantage for anorganisation. It reflects the values, expectations and goals of those whoare in power within the organisation.

These logical / prescriptive ideas about strategy emanate from the‘prescriptive’ approach as advocated by early strategic writers (seePreface and the text Strategy Safari (Mintzberg et al, 1998)). Many earlywriters continue to be widely quoted, e.g. Michael Porter. Many recentwriters have challenged this view of strategy. The study of corporatestrategy has moved on into ‘softer’ areas and these issues need to bekept in mind.

Early thinking (1960s) could be said to be ‘modernist’ in view, i.e. aunitary perspective – there was a single way to perform the task ofstrategy. There was an idea that data (both internal and external) couldbe fed into an analysis machine and the answer (the strategy) could bechurned out. The ‘postmodern’ view refuted this, saying that a strategistview should be ‘pluralist’, i.e. take many diverse things into account andthis is evidenced by a number of writers. For example, the view of‘planning’ as opposed to ‘emergence’ – both viewpoints are supportedby a wealth of academic writing (see later discussion in this unit).

However, as a starting point, we will consider some ‘prescriptive’definitions and concepts to try to begin to appreciate the complexity ofthis subject.

Lessons from military strategy

Generalising strategy can be misleading, as the context is important.However, the military definition of strategy can be very helpful in thecontext of business, as the approach to winning in the businessenvironment is very similar to winning a war. Success in businessrequires a sharp focus, and does indeed involve winning battles andgaining competitive advantage over the ‘enemy’, in this case thecompetitor.

Military strategy is the ‘holistic’ deployment of resources in such a waythat the outcome of a war is influenced. As with military strategy, it is

2

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

vital that corporate strategy is ‘holistic’ to be successful. To achieve thecorporate strategy, the whole organisation must be focused on the samecorporate goals and must team, execute and win in the marketplace. Aswith a war, a razor sharp focus is required to win in the marketplace.

Strategic vs. tactical

An important distinction to make at this point is between the strategicand tactical. The terms feature in the military as well as in business, andit is important to understand the difference.

As we have just observed, strategy must be holistic – it must involve thewhole organisation and its objective is to achieve the goal (or win the‘war’) defined by the company. Tactical measures are actions ormanoeuvres carried out to win individual battles, which mayeventually, after a number of battles, win the ‘war’.

In the context of business, a tactical measure may, for example, involveruthless, but short-term, price-cutting, in order to grab market-shareand remove a competitor. A strategic move, on the other hand, may bean acquisition in order to move into a new market area. Tacticalmeasures are usually short-term, whereas strategy is long-term. A seriesof tactical measures can help achieve the long-term strategy.

VIRTUAL CAMPUS

Discuss with your colleagues how a tactical action in your work contextfurthered the company’s strategy. In particular, how it influenced:

� Competitive position.

� Market share.

� Customer satisfaction.

� Short-term vs. Long term profits and margins.

� New opportunities.

Business strategy

Some definitions of business strategy that are helpful are as follows:

3

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

‘Corporate strategy is the pattern of minor objectives,purposes or goals and essential policies or plans forachieving those goals, stated in such a way as to definewhat business the company is in or is to be in and the kindof company it is or is to be’

Andrews K (1971). Page 8, Lynch.

‘Strategy is the direction and scope of an organisation overthe long term: which achieves advantage for theorganisation through its configuration of its resourceswithin a changing environment, to meet the needs ofmarkets and fulfil stakeholders' expectations.’

Page 10, Johnson and Scholes

KEY POINT

Characteristics of business strategy are as follows:

� Sets direction and scope over the long term to achieve goals.

� Designed to achieve competitive advantage.

� Directs business in a changing and evolving environment.

� Holistic and pervasive of the whole organisation; covering therange and depth of its activities.

� Achieved by teaming, executing and winning in themarketplace.

� Fulfills stakeholder expectations; survival as a minimum andcreation of added value as a maximum.

ACTIVITY

Read p. 1-19 of Chapter 1 and section 2.1 of the key text, De Wit, B & Meyer, R

4

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

Levels of Strategy

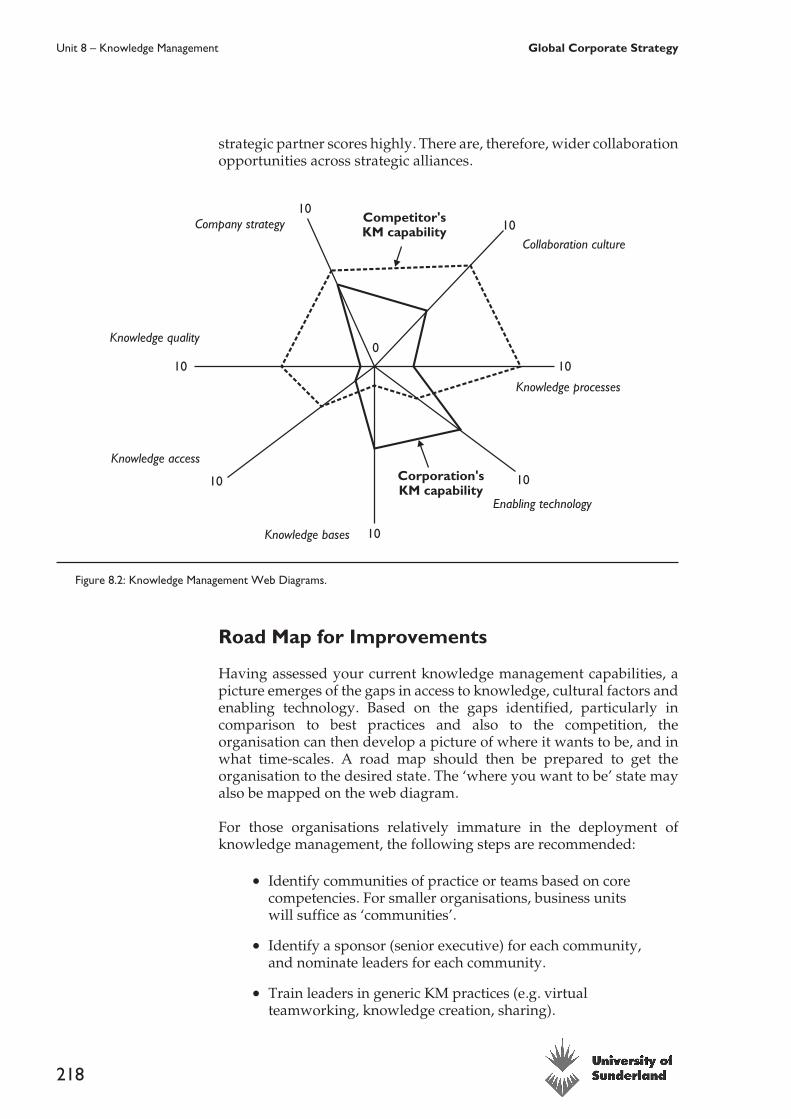

Strategy can be distinguished by the levels at which it occurs. Refer toFigure 1.1.

Corporate Strategy:

� Defines the strategy for the corporation (or organisation)as a whole, and is cascaded to business units below.

� Must be holistic and define the overall purpose and scopeof the organisation.

� Must be visionary in some measure.

� Must ensure that the different parts of the organisationadd value to the overall strategy.

� Must meet the expectations of major stakeholders.

Business Unit strategy:

� Must be derived and be aligned with the corporatestrategy.

� Must be focused on how to compete in the particularmarkets or business areas for which the business unit hasresponsibility.

� Can be visionary and creative within the context of itsbusiness remit.

Operational Strategy:

� Must define and deliver the operational processesrequired to achieve the corporate and business unitstrategy.

5

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

BusinessUnit Strategy

BusinessUnit Strategy

BusinessUnit Strategy

Corporate StrategyO

perational Strategy

Figure 1.1: Levels of corporate strategy.

� Must address the resource and resource developmentplans to support corporate and business unit strategy.

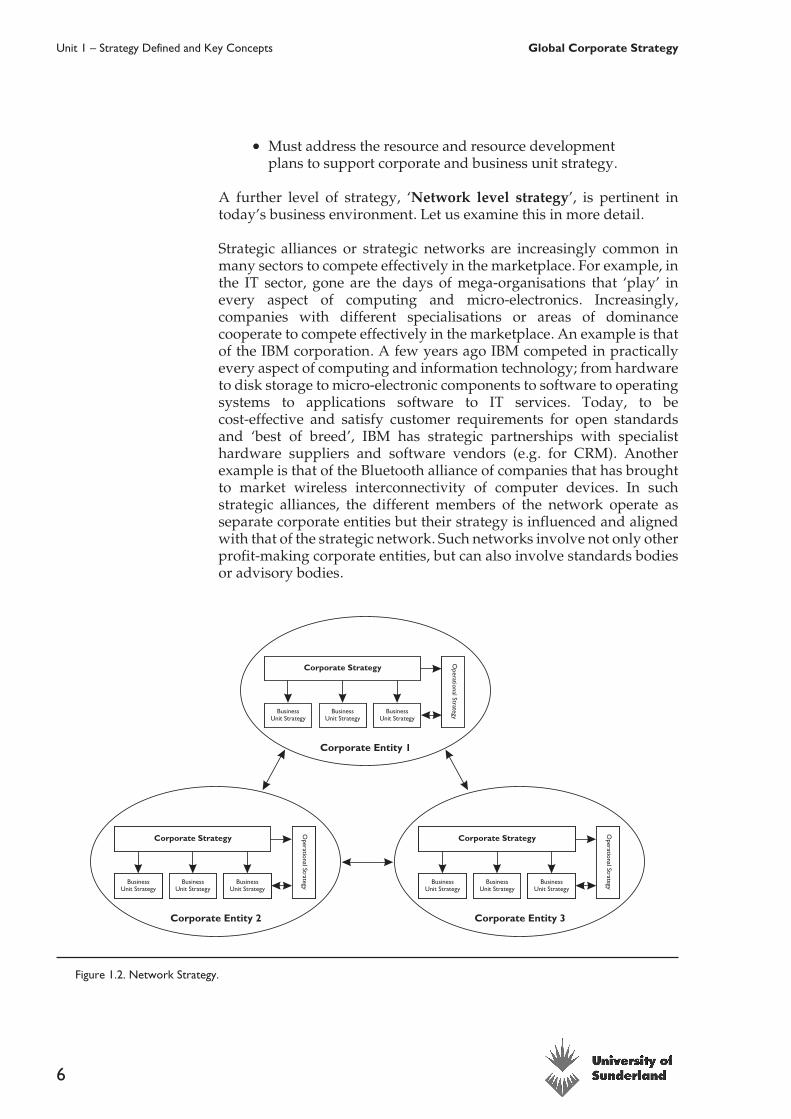

A further level of strategy, ‘Network level strategy’, is pertinent intoday’s business environment. Let us examine this in more detail.

Strategic alliances or strategic networks are increasingly common inmany sectors to compete effectively in the marketplace. For example, inthe IT sector, gone are the days of mega-organisations that ‘play’ inevery aspect of computing and micro-electronics. Increasingly,companies with different specialisations or areas of dominancecooperate to compete effectively in the marketplace. An example is thatof the IBM corporation. A few years ago IBM competed in practicallyevery aspect of computing and information technology; from hardwareto disk storage to micro-electronic components to software to operatingsystems to applications software to IT services. Today, to becost-effective and satisfy customer requirements for open standardsand ‘best of breed’, IBM has strategic partnerships with specialisthardware suppliers and software vendors (e.g. for CRM). Anotherexample is that of the Bluetooth alliance of companies that has broughtto market wireless interconnectivity of computer devices. In suchstrategic alliances, the different members of the network operate asseparate corporate entities but their strategy is influenced and alignedwith that of the strategic network. Such networks involve not only otherprofit-making corporate entities, but can also involve standards bodiesor advisory bodies.

6

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

BusinessUnit Strategy

BusinessUnit Strategy

BusinessUnit Strategy

Corporate Strategy

Operational Strategy

Corporate Entity 1

BusinessUnit Strategy

BusinessUnit Strategy

BusinessUnit Strategy

Corporate Strategy

Operational Strategy

Corporate Entity 3

BusinessUnit Strategy

BusinessUnit Strategy

BusinessUnit Strategy

Corporate Strategy

Operational Strategy

Corporate Entity 2

Figure 1.2. Network Strategy.

ACTIVITY

Think of an example, perhaps from your own work context, of how corporatestrategy translated to business unit strategy and operational strategy.

Did networks or strategic alliances play a role in moulding corporate strategy?

Strategy and the manager

Developing and deploying strategy successfully depends on managersunderstanding the key and high impact aspects of strategy. Managersshould:

� Ensure that strategies are part of the overall corporatestrategy.

� Ensure that strategies are consistent, coherent, effectiveand appropriate.

� Ensure that strategies are sustainable and supported byoperational processes.

� Understand an organisation’s business environment.

� Understand the attributes of the organisation and whatmakes it unique/distinctive.

� Be aware of the organisation’s resources, capabilities,competencies and customers.

� Understand how the organisation’s advantages can beexploited.

� Understand and exploit the existence of any strategicnetworks/alliances.

Strategic Concepts

A number of factors influence the type of strategy an organisationadopts. These factors include the maturity of an organisation, maturityof the market sector it operates in, its corporate management culture,and market leadership goals.

There are broadly two types of strategic concepts:

7

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

� Strategic ‘Fit’: Strategic Fit is the matching of anorganisation’s strategy to the environment it operates in.It is really identifying opportunities that exist in thecurrent environment and tailoring strategy to capitaliseon it. Competitive advantage is achieved by correctpositioning within the existing marketplace.

� Strategic ‘Stretch’: Strategic Stretch, on the other hand, iswhen an organisation pro-actively stretches its resourcesand competencies to create new opportunities andcapitalise on them. It means identifying resources anddeveloping competencies to pre-empt and create newopportunities in the marketplace. Competitive advantageis achieved by not only meeting existing market needs butalso future market needs. It is a resource-led approachwith investment from the heart of the corporate centre.

ACTIVITY

Can you think of an example of strategic fit?

Now can you think of a company that has or is adopting strategic stretch?

ACTIVITY FEEDBACK

You probably thought of many examples of strategic fit, but perhaps had moredifficulty with examples of strategic stretch.

One example of strategic stretch is the Waitrose/Ocado partnership in theUK, which provides on-line grocery shopping and home delivery service.Currently, in the UK, the market for on-line shopping is small. With theexception of Tesco, which makes a small profit on on-line deliveries, mostcompanies providing this service make huge losses, and many are withdrawingfrom this service altogether. Waitrose/Ocado are also making losses currently.However, they are strategically stretching themselves, and investingconsiderable amounts to expand services. They forecast a huge marketopportunity in a few years to come. Waitrose operates in wealthy,middle-class areas, where the average weekly spend, on groceries, is in excessof £150 a week. If on-line shopping takes off (as they predict it will, inapproximately 2-3 years time), Waitrose/Ocado would have carvedthemselves a very lucrative market, indeed.

8

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

Strategic Thinking

Where previously (in the 1970s and 1980s) the focus was on managerialskills in strategic planning, now the emphasis is on strategic thinking.Strategic thinking has creativity at its heart, and encourages the entireorganisation to be involved. It minimises the risks associated withmanagement power over strategy.

A simplistic definition of strategic thinking is finding the answers to thefollowing:

� Where are we now?

� Where do we want to go?

� How do we get there?

For an organisation to be successful, strategic thinking must dominateits entire corporate culture. Strategic thinking must be ingrained, be atthe forefront and influence every manager’s daily actions. It cannot be a‘one off’ or ‘once a year’ activity.

The following extract from Porter (1977) is helpful in highlighting theimportance of strategic thinking.

‘There are no substitutes for strategic thinking. Improvingquality is meaningless without knowing what kind ofquality is relevant in competitive terms. Nurturingcorporate culture is useless unless the culture is alignedwith a company’s approach to competing. Entrepreneurshipunguided by a strategic perspective is much more likely tofail than succeed.

Strategic thinking cannot occur only once a year, accordingto a rigid routine. It should inform a company’s dailyactions. Moreover the information necessary for goodstrategic thinking is equally vital to running a business –designing marketing material, setting prices and deliveryschedules.

There is a dangerous tendency today to practise single-issuemanagement. The truth, of course, is that there is no easyanswer. Quality, manufacturing, corporate culture ,entrepreneurship and strategic thinking are all important.Concern for one does not imply all these aspects ofmanagement. One cannot ignore strategic thinking infavour of maintaining a supportive culture, just as onecannot ignore quality no matter how elegant is the strategicplan.’

Porter (1977)

9

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

De Wit & Meyer discuss the paradox of Logic and Creativity. They seestrategy as a ‘wicked’ problem, i.e. ambiguity, complexity anduncertainty prevail in making strategic decisions. The implication is thatcreative (or generative) thinking is crucial to enable managers (and theirorganisations) to move beyond the obvious, from the comfortable to theuncomfortable to be successful. This is often termed ‘lateral’ thinking or‘thinking out of the box’.

Nevertheless, a role for ‘logic’ is still in place. A manager still needs to beable to think rationally and be analytical in certain circumstances.However, they are ‘bounded’ by their own rational thought and so arelimited in what they can achieve.

ACTIVITY

Learn more about Strategic Thinking by reading the introductory section toChapter 2 (p 51-67) in your key textbook, De Wit, B & Meyer, R

Information Processing, Thinking and Strategy

Strategic thinking involves the processing of information by managersto define strategy. Two different modes of information processing havebeen described (Walsh, 1995):

� Bottom-up processing.

� Top-down processing.

Bottom-up processing

The characteristics of bottom-up processing, in the context of strategicthinking, are:

� Driven by the process of gathering detailed informationfrom all levels.

� Decision making is then carried out after elaborateanalysis of the strategic problem, or issue underconsideration, and a review of all possible solutions.

Top-down processing

The characteristics of top-down processing, in the context of strategicthinking, are:

10

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

� Driven by the recall and application of theory/models toreal-life situations encountered.

� Strategies are derived from the experience of the successof previous strategies.

� Elaborate theories are rarely applied. Simple, abstractrule-of-thumb approaches take precedence.

In practice, the majority of strategic decisions are made using top-downprocessing, and rely on the skills and experience of top levelmanagement.

Neither approach lends itself well to less routine and novel strategicdecisions (such as entering a new market or bringing to market a novelproduct/service). Such decisions require vision, creativity as well asbusiness realism.

Another important factor in strategic decision thinking is the role ofuncertainly. Uncertainties can take the form of missing information, butother times arises simply from the unknowable. Such uncertainties canpose risks as well as new business opportunities. What makes a marketleader is how that organisation predicts future opportunities from anuncertain environment. Through leadership companies are able toinfluence and guide the market with their own ideas and thereby createnew opportunities.

Strategic Thinking: skills

Strategic thinking has many dimensions, and demands a variety ofskills, as follows:

� A strategist needs to understand issues at the functional,technical and unit levels, as strategy must be holistic andintegrated across all levels.

� A strategist needs to identify the significance of currentissues and from that knowledge project strategy into thefuture.

� A good strategist needs to balance the use ofdata/information, analysis of issues with that ofexperience, knowledge and understanding to predict thefuture

� A strategist needs to be creative. Creativity in strategyrenders competitive advantage.

The following factors strengthen strategic thinking:

� Relevance and realism in thinking.

11

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

� Rigour.

� A varied approach to information processing.

� A balance between theory and practice to cross-checkvalidity.

� A critical and challenging approach.

ACTIVITY

It is good practice for strategic decisions to be evaluated against set criteria.From your own work experience, can you identify the criteria (in the form ofbullet points) against which strategy can be judged.

ACTIVITY FEEDBACK

You would have come up with a number of ideas. Some of which may bespecific to the industry/sector in which you operate. A good list of evaluationcriteria is outlined in the key textbook, De Wit, B & Meyer, R, ‘Criteria forEvaluation’, pages 74-75.

Strategic Models

Strategic thinking is a complex area. As such there is a role for strategic‘models’ that can enable analysis. However, they should be used withcaution, noting that theoretical models can over-simplify the practicaland complex issues faced by organisations in the real world.

Firstly, it is helpful to recognise that strategic thinking has threedimensions to it as shown in Figure 1.3.

12

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

The process, content and context of strategies define the scope ofstrategic thinking, and must be considered together as they are closelyinter-related. Let us look at each of these in turn:

� Process: The actions or processes that support how thestrategy is analysed, determined, implemented/executed,changed and controlled. These processes link together orinteract as the strategy unfolds in what may be achanging environment.

� Content: The result of the strategy process is content. Itaddresses the main actions of the proposed strategy.

� Context: Concerns the business circumstances orenvironment in which the strategy operates or will bedeveloped. This can be the ‘inner’ context, referring to theorganisational setting or corporate culture of theorganisation. Or it can be the ‘outer’ context, such asexternal economic, political, business, environmentalfactors.

ACTIVITY

Can you think of some examples of how inner context can influence strategy.

Similarly, think of an example of how outer context influences anorganisation’s strategy.

13

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

Context

StrategyProcess

Content

Figure 1.3. The dimensions of strategic thinking.

ACTIVITY FEEDBACK

You may have thought of one or two examples of how inner context influencesstrategy. Here is another example.

Shell and Exxon are giant oil corporations. However, they are organised verydifferently. Shell has a structure that favours and devolves power to national orregional management. Whereas, Exxon has a strong corporate focus with anemphasis on functional and product lines of structure.

In the Shell structure, strategic thinking is carried out at the regional level (e.g.by operating companies such as PDO in Oman, Brunei). The corporateheadquarters at The Hague does influence strategy at regional levels, butdoesn’t dictate business unit-level strategy.

In the Exxon example, the corporate body defines strategy. Strategy is thencascaded to the functional units. Processes and standards (e.g. IT standards andsoftware applications) are defined by the corporate body.

ACTIVITY

Can you now think of an example of how outer context influences anorganisation’s strategy?

ACTIVITY FEEDBACK

Increasingly environmental and ethical factors strongly influence strategy. Suchfactors are outside the control of the organisation, but nevertheless theorganisation must adhere to it.

Many Western companies utilise cheap factory labour from third-worldcountries, such as India, Taiwan, etc. More recently, skilled jobs, such as callcentre operations, have also moved to countries such as India, as it is morecost-effective. Raised environmental and ethical awareness has forcedWestern companies to pay fair wages and provide satisfactory workingconditions in these countries. Company stakeholders often demand ethicaland sound environmental practices. This is an example of outer context,where the company must comply with external influences.

14

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

ACTIVITY

Reinforce your understanding of the dimensions of strategy by re-readingp.5-11 of the key text, De Wit, B & Meyer, R.

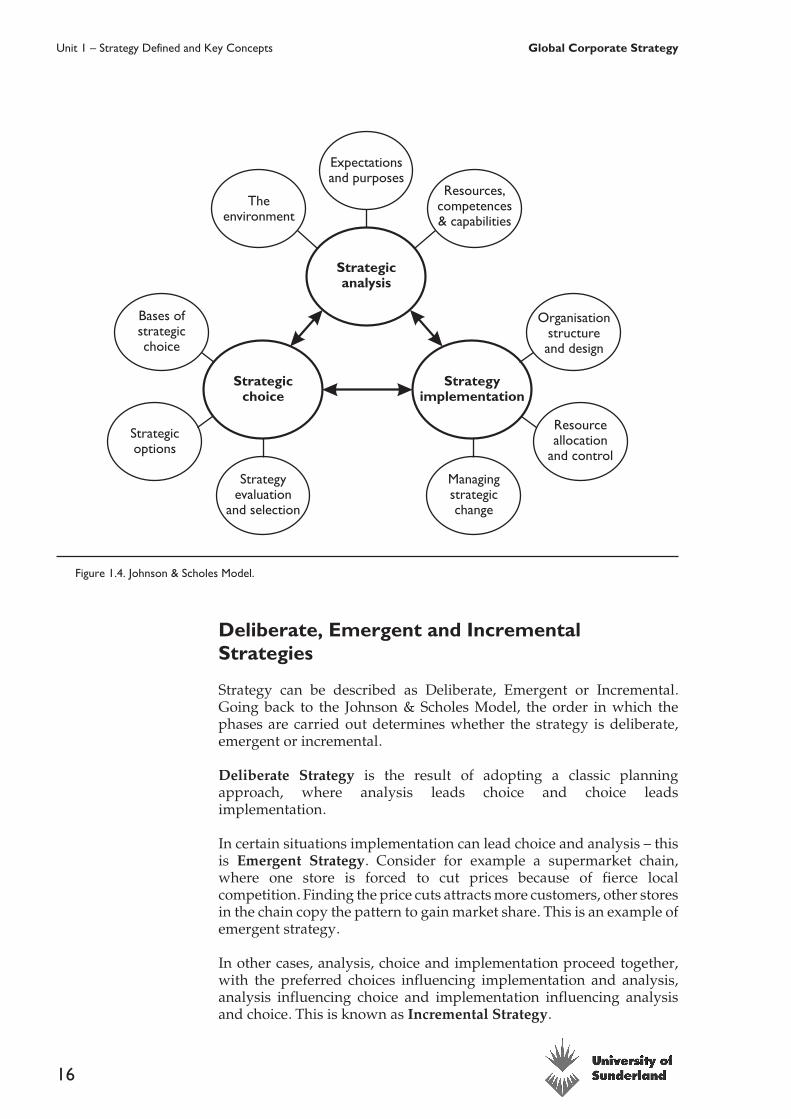

Johnson & Scholes Model

Johnson and Scholes developed and elaborated an approach to strategyfirst put forward by Argenti in 1980. Argenti identified the distinctphases in strategic management, which can be grouped as follows:

STRATEGIC ANALYSIS

� Target Setting.

� Gap Analysis.

� Strategic Appraisal.

�STRATEGIC CHOICE

� Strategic formulation.

�STRATEGIC IMPLEMENTATION

As the arrows indicate above, Argenti suggested that strategic analysisshould precede choice, and choice precede implementation. In reality,the phases often overlap. The overlapping nature of the phases waselaborated by Johnson and Scholes. Figure 1.4 shows types of issues thatshould be considered within the strategy development phases.

15

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

Deliberate, Emergent and IncrementalStrategies

Strategy can be described as Deliberate, Emergent or Incremental.Going back to the Johnson & Scholes Model, the order in which thephases are carried out determines whether the strategy is deliberate,emergent or incremental.

Deliberate Strategy is the result of adopting a classic planningapproach, where analysis leads choice and choice leadsimplementation.

In certain situations implementation can lead choice and analysis – thisis Emergent Strategy. Consider for example a supermarket chain,where one store is forced to cut prices because of fierce localcompetition. Finding the price cuts attracts more customers, other storesin the chain copy the pattern to gain market share. This is an example ofemergent strategy.

In other cases, analysis, choice and implementation proceed together,with the preferred choices influencing implementation and analysis,analysis influencing choice and implementation influencing analysisand choice. This is known as Incremental Strategy.

16

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

Strategicanalysis

Strategyimplementation

Strategicchoice

Bases ofstrategicchoice

Strategicoptions

Strategyevaluation

and selection

Organisationstructureand design

Resourceallocation

and control

Managingstrategicchange

Expectationsand purposes

Theenvironment

Resources,competences& capabilities

Figure 1.4. Johnson & Scholes Model.

REVIEW ACTIVITY

Learn more about the above by reading the section ‘The paradox ofDeliberateness and Emergentness’ in your key text, De Wit, B & Meyer, R,p.111-116.

Also learn about the strategic planning perspective vs. strategic incrementalismby reading p.117 – 123 of your key textbook, De Wit, B & Meyer, R.

Now apply what you have learned in this unit to your own work context.

1. Are you aware of your organisation’s corporate strategy? Are youaware of your business unit strategy?

2. How is strategy formulated in your workplace?

3. Would you describe it as deliberate, emergent or incremental?

4. From what you have learned, can the strategy process be improved? Ifso how?

5. What do you see as the major obstacles in your organisation tostrategy development and strategy execution?

6. How can these obstacles be removed?

Share your thoughts on the questions above with colleagues, either on theVirtual Campus or at your workplace. Solicit their input and ideas also,especially on items 4 and 6 above.

CASE STUDY 1 – IKEA

Read the following extract about IKEA;

(Source: Johnson & Scholes; Chapter 1 pages 6,7 & 229 and Sunday Times, 22February 1998.)

In 1953, just four years after Ingvar Kamprad had produced his first mail ordercatalogue featuring locally produced furniture, he opened his first store inAlmhult, Sweden. Since then, he and his successors have created a globalnetwork of stores in 28 countries. Initially, stores were opened only inScandinavia, but as greater levels of success were experienced, stores werebuilt in countries further afield where the rewards, but also the risks of failure,were much higher. In all these countries the retailing concept of Ingvar

17

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

Kamprad remained the same: ‘to offer a wide range of furnishing items of gooddesign and function at prices so low that the majority of people can afford tobuy them’.

In the 1980s, Anders Moberg became the chief executive. However, theinfluence of Ingvar Kamprad could still be found. IKEA had always been frugal inits approach. In its early years it had relocated to Denmark to escape Swedishtaxation. Echoes of the same philosophy and style could be seen in AndersMoberg. He would arrive at the office in the company Nissan Primera, dressedin informal clothes, and clock in just as other employees did. When abroad hetravelled on economy class air tickets and stayed in modest hotels. Heexpected his executives to do likewise. Such prudence was extended to thecompany whose shares were held in trust by a Dutch charitable foundation andnot traded. Furthermore, IKEA’s expansion plans envisaged only internalfunding with 15% of turnover being reinvested.

The 1980s saw rapid growth. IKEA benefited from changing customerattitudes, from status and designer labels to functionality, encouraged by aneconomic recession. It also developed a number of unique elements whichcame to make up IKEA’s winning business formula: simple, high qualityScandinavian design, global sourcing of components, knock-down furniture kitsthat customers transported and assembled themselves, huge suburban storeswith plenty of parking and amenities such as cafés, restaurants, wheelchairs andeven supervised child-care facilities. A key feature of IKEA’s concept wasuniversal customer appeal crossing national boundaries, with both theproducts and shopping experience designed to support this appeal. Customerscame from different lifestyles: from new homeowners to business executivesneeding more office capacity. They all expected well styled, high quality homefurnishings, reasonably priced and readily available. IKEA met this expectationby encouraging customers to create value for themselves by taking on certaintasks traditionally done by the manufacturer and retailer, for example theassembly and delivery of products to their homes.

IKEA made sure that every aspect of its business system was designed to makeit easy for customers to adapt to their new role. For example, information toassist customers make their purchase decisions was provided in a 200-pageglossy catalogue; during their visit to the store customers were supplied withtape measures, pens and notepaper to reduce the number of sales staffrequired; furniture was displayed in 100 model rooms; and sales staff wereexpected to involve themselves with customers only when asked.

To deliver low-cost yet high-quality products consistently, IKEA also had 30buying offices around the world whose prime purpose was to identify potentialsuppliers. Designers at headquarters then reviewed these to decide whichwould provide what for each of the products, their overall aim being to designfor low cost and ease of manufacture. The most economical suppliers werealways chosen over traditional suppliers, so a shirt manufacturer might beemployed to produce seat covers. Although the process through whichacceptance to become an IKEA supplier was not easy, it was highly coveted,for, once part of the IKEA system, suppliers gained access to global markets,and received technical assistance, leased equipment, and advice on how tobring production up to world quality standards. By the mid 1990s, IKEA was

18

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

offering a range of 12,000 items, from 1,800 suppliers in 45 countries at prices20-40% lower than for comparable goods. However, by 1998 the means ofachieving low cost was receiving some critical attention. It was reported thatIKEA was sourcing its goods from suppliers in eastern Europe which paid itsworkers poverty level wages.

IKEA was the subject of a hard-hitting article in the Sunday Times in February1998. The article concerned the working and living conditions in Romanianfurniture factories. Although IKEA did not own any of the 25 factories whichproduced furniture for its stores, it had provided collateral for at least onefactory to be bought from the state in 1992. In fact, there were allegations fromthe Federation of Wood Workers that the directors of the factory usedmoney from IKEA and disregarded the law under which Romanian employeesare entitled to be given the option of buying their own factory as a cooperative.

The article observed that the appalling conditions in Romania flew in the face ofthe politically correct image of IKEA fostered by Ingvar Kamprad who regularlywrote memos to staff which started with ‘Dear IKEA family’.

The managing director of this factory admitted that he kept a competitive edgeby paying employees an average of about 20p per hour (about one-fortieth ofthe pay levels in Sweden). IKEA’s response to these issues was that it had nomanagement responsibility for any Romanian factory. It accepted, however,that conditions were poor and that it had provided the collateral necessary forthe purchase of one factory. It also restated its financial support for theRomanian furniture industry through credits which allowed new buildings withbetter working conditions. It believed that trade was better than aid and that itintended to continue to assist with financial and technical support and byexpanding orders.

Having to cope with widely dispersed sources of components and high-volumeorders made it imperative for IKEA to have an efficient system for ordering itssupplies, integrating them into products and delivering them to the stores. Thiswas achieved through a world network of fourteen warehouses. Theseprovided storage but also acted as logistical control points, consolidationcentres and transit hubs, and aided the integration of supply and demand,reducing the need to store production runs for long periods, holding downunit costs by minimising the costs of inventory and helping stores to anticipateneeds and eliminate shortages.

By the end of the 1990s, IKEA was turning its attention to new opportunitiesfor growth. It had opened stores in eastern Europe and the one-time Sovietrepublics, believing these represented great future potential. In 1997, itannounced its plan to open twelve new stores a year internationally in citiessuch as Frankfurt, Shanghai, Chicago and Roclab in Poland and to doublemanufacturing capacity by building up to twenty factories in eastern Europe by2002. There were also plans to develop new areas of business. In partnershipwith a building contractor, IKEA was market testing, in Sweden, ‘flat packed’housing which could be assembled by two men and a crane in a week at pricesabout 30% less than the going rate. It was also developing new sources ofsupply, entering into an agreement with a timber company to develop newwood material for furniture. However, the company was also facing problems.

19

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

IKEA was experiencing growing competition on an international front. It haddecided to implement a programme of cost savings, rationalising its supplychain and product range in order to cut purchasing costs by an overall averageof 10%. The company had stated the intention of cutting what had become2,400 suppliers by one-quarter and focusing on increased volumes with asmaller range of products and fewer suppliers.

In 1996, Ingvar Kamprad announced that IKEA would be split into three,comprising the retailing operations, an organisation holding the franchise andtrademarks, and a third arm involved mainly in finance and banking. The firsttwo would form the core of the group, controlled at arm’s length by trust-likeorganisations; the latter’s shares would be jointly owned by Kamprad’s threesons. The structure was devised in an effort to ensure that the privately heldorganisation should not be broken up or sold off in a succession battle afterIngvar Kamprad retired. He also wanted to ensure that it would not be putunder the sorts of external pressures for continual growth often faced bypublicly quoted companies. Internally, IKEA’s strategy was managed atdifferent levels. A committee of senior executives at headquarters in Denmarkwas responsible for overseeing investment in new markets and stores;responsibility for product development and purchasing lay with IKEA ofSweden; and country managers tailored the presentation and marketing ofproducts to home territories.

Questions:

1. Summarise IKEA’s corporate strategy.

2. Note down the characteristics of IKEA’s strategy which could beexplained by the notions of:

� Strategic management as ‘environmental fit’

� Strategic management as the ‘stretching’ of itscapabilities.

3. Comment on IKEA’s ethical stance

(You may wish to revisit this question after you have completed Unit 6. Unit 6covers corporate ethics in more detail)

20

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

CASE STUDY FEEDBACK

Feedback on Question 1:

These are some of the considerations on strategy and strategic decisions in thecontext of the IKEA case study.

� Strategic decisions affect the long-term direction of an organisation.IKEA set out along a path which was difficult to reverse. In the1950s and 1960s the company was, essentially, a Scandinavianfurnishing retailer. By the late 1990s the whole thrust of its strategyhad shifted to a global scale and IKEA was facing the challenge ofhow to develop into the twenty-first century. In so doing it had toconsider other key issues.

� Strategic decisions are normally about trying to achieve someadvantage for the organisation, for example over competition. IKEAhad been successful not because it was the same as all otherfurniture retailers, but because it was different and offeredparticular benefits which distinguished it from other retailers.Similarly, strategic advantage could be thought of as providing higherquality value-for-money services than other providers in the publicsector, thus attracting support and funding from government.Strategic decisions are sometimes conceived of, therefore, as thesearch for effective positioning in relation to competitors so as toachieve advantage in a market or in relation to suppliers.

� Strategic decisions are likely to be concerned with the scope of anorganisation’s activities. Does (and should) the organisationconcentrate on one area of activity, or should it have many? Forexample, for years IKEA had defined the boundaries of its businessin terms of the type of product (‘furnishing items of good design andfunction’) and mode of service (large retail outlets and mail order).While not owning its manufacturing, it did have an in-house designcapability, which specified and controlled what manufacturerssupplied to the company. There were signs by the late 1990s,however, that IKEA was extending its product scope fromfurnishings into other product areas, as with its experiments withhousing. Over the years it had also substantially widened itsgeographical scope to become one of the few truly multinationalretailers in the world.

� Strategy can be seen as the matching of the activities of an organisationto the environment in which it operates. This is sometimes known as‘the search for strategic fit.’ While the market for furnishings wasmature, with little prospect of overall growth, the management ofIKEA had seen that the retail provision of furnishing in mostcountries did not meet the expectations of customers. Customersfrequently had to wait for delivery of items, which were highly

21

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

priced. The market provided another opportunity. Customertastes were relatively common in different countries except inspecialised segments of the market: buyers wanted everydayfurniture which was well designed and looked good, but whichwas reasonably priced.

IKEA also knew that it faced significant differences in its markets. Bythe 1990s the number of countries in which IKEA was representedwas a great deal larger than in the company’s early days. This meantthat IKEA had to understand buying habits and preferences from amuch wider base, from markets close to its Swedish home, to theUSA, and even to the Far East and eastern Europe.

IKEA could no longer assume that its knowledge of earlier marketswould necessarily apply: for example, it had found that shopping habitsin the USA differed substantially from those in Europe, and this hadrequired a change in the way it serviced the market. Therefore, whilethe principles of IKEA’s business idea were adhered to around theworld to produce a consistent product quality and shoppingexperience, store management had been given a greater degree offreedom to adapt to local market needs.

IKEA’s management had, however, decided that there were somemarkets, attractive though they were, where it did not make sense totry to control IKEA’s operations directly. Here the companyrecognised that local knowledge in fine-tuning the business to localneeds was vital; or the problems of long-distance control were toogreat to manage the operation effectively on this basis. It had,therefore, established local joint ventures through franchisearrangements.

There were wider environmental issues, which affected IKEA’sfortunes; for example, IKEA was less susceptible to economicdownturn than many of its competitors. This may have been becauseits prices were often lower; but it was also because, when a customertook a purchasing decision at IKEA, he or she walked away with thegoods. In other stores, since delivery was often delayed, purchasedecisions were also often delayed. Economic conditions in thedifferent countries in which IKEA operated did, however, affect itssuccess: for example, the growth in car ownership, particularly in lesshighly developed countries, determined the percentage of thepopulation which could shop at an IKEA store.

� Strategies may require major resource changes for anorganisation. For example, the decision that IKEA took todevelop its operations internationally had significantimplications in terms of its need to obtain properties fordevelopment and access to funds by which to do this,sometimes for projects which might be seen as high risk – forexample, entering new markets in times of recession. The sizeof the operation in terms of numbers of people working in it,property and physical stock held had to rise significantly. The

22

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

need to control a multinational enterprise, as opposed to a nationaloperation, also began to require skills and control systems of adifferent sort. It was a problem which many retailers found difficultycoping with. A major reason has been that retailers underestimatethe extent to which their resource commitments rise and how theneed to control them takes on quite different proportions.Strategies, then, need to be considered not only in terms of theextent to which the existing resource capability of the organisationis suited to opportunities, but also in terms of the extent to whichresources can be obtained and controlled to develop a strategy forthe future.

� Strategic decisions are likely to affect operational decisions. Forexample, the internationalisation of IKEA required a whole series ofdecisions at operational level. Management and control structuresto deal with the geographical spread of the firm had to change. Theway in which suppliers were controlled and the methods ofdeveloping and distributing stock required revision to deal with theextended distribution logistics. Marketing and advertising policiesneeded to be reviewed by country to ensure their suitability todifferent customer behaviours and tastes. Personnel policies andpractices had to be reviewed. Store operations needed to changetoo. For example, in the USA, IKEA saw the need to add to thecore product range from local suppliers, install serviced loading baysand erect bollards to stop the shopping trolleys being taken to allparts of the car parks, which are very large in the USA.

This link between overall strategy and operational aspects of theorganisation is important for two other reasons. First, if theoperational aspects of the organisation are not in line with thestrategy, then, no matter how well considered the strategy is, it willnot succeed. Second, it is at the operational level that real strategicadvantage can be achieved. IKEA has been successful not only becauseof a good strategic concept, but also because the detail of how theconcept is put into effect – the strategic architecture – in terms of itslogistics of buying and servicing, shop layout and merchandising tosupplier and customer relations, all developed over many years, isdifficult to imitate.

The strategy of an organisation is affected not only by environmentalforces and resource availability, but also by the values and expectationsof those who have power in and around the organisation. In somerespects, strategy can be thought of as a reflection of the attitudes andbeliefs of those who have most influence on the organisation.Whether a company is expansionist or more concerned withconsolidation, and where the boundaries are drawn for a company’sactivities, may say much about the values and attitudes of those whoinfluence strategy – the stakeholders of the organisation. In IKEA theinsistence on internal financing influenced long-term development andthe direction of the company: the influences of the founder and chiefexecutive remained pronounced. The emphasis on frugality andsimplicity clearly influenced the way the company operated. Indeed,

23

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

critics pointed to what they saw as a disregard for the well-being andwelfare of the low-paid workers of suppliers in the name of keepingdown costs.

The conclusion from the above case study is that strategic decisions oftenexhibit the following characteristics:

1. Complex: especially for multinational organisations such as IKEAwith a wide range of products/services.

2. Involve uncertainty: They often involve taking decisions about thefuture, which is impossible for managers to be sure about.

3. Require an integrated approach: Managers have to work acrosscross-functional and operational boundaries, and come to agreementswith other managers who may have different interests and priorities.They also have to manage external relationships such as with suppliers,distributors and customers.

4. Involve change: Strategic decisions often involve change. Not only isit problematic to decide upon and plan change, it is even moreproblematic to implement change if the organisation’s culture is not inline with the desired future strategy. In the case of IKEA there werethe following strong influences: (i) family owned company with noshareholder/financial market influence on strategy (ii) Swedishinfluence, reflecting Swedish values.

Feedback on Question 2:

Decisions on whether a company takes an environment led approach (fit) or aresource based approach (stretch) is often complex. IKEA is such an examplewhere arguments can be formed to justify both.

Taking a strategic fit approach means, as in the case of IKEA, trying to identifythe opportunities which exist in the environment and tailoring the futurestrategy to capitalise on these, for example by locating in particularlyfavourable markets or seeking to appeal to attractive market segments.

However, strategy can also be seen as building on or ‘stretching’ an organisation’sresources and competencies to create opportunities or to capitalise on them.

The product range IKEA had designed and developed was not only low costbut unique, not only because of its kit form but also in its style and image. IKEAbenefited from years of design experience dedicated to its operation andmarkets. The logistics of the operation, from sourcing of products to controlof stock and the immediate supply of the product to take away, had beenlearned over many years and provided not only a quite distinct way ofoperating, but a service greatly appreciated by customers. In short, both theresources and experience built up over the years had been consciouslydeveloped to service the evident opportunity in the market place.

24

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

IKEA then ‘stretched’ its capabilities, using its experience in the furnituremarket, to create a different market opportunity. It set out to reinvent value,and experimented with housing in the late 1990s. It started to think aboutvalue in a new way; one in which consumers are also suppliers, suppliers arealso customers, and IKEA itself is not so much a retailer but as a central hub forservices, goods, design, management, support and even entertainment.

In practice, organisations such as IKEA, develop strategies on the basis ofenvironmental ‘fit’ and ‘stretch’. IKEA’s experiment with housing was theresult of identifying a new market opportunity, but it was also an attempt tocapitalise on its skills in developing kit-form products at low-cost.

Feedback on Question 3:

The issues to consider are:

� Is it good business practice to achieve high profits by lowering costs,irrespective of the ethical issues in the Romanian factories?

� Is the local population in Romania, grateful for having IKEA’scontract? Or was IKEA exploiting low labour cost locations?

� IKEA’s view of this is that it is a ‘sub-contract’ arrangement, and it isnot up to them how the workers are treated. Is this a realisticattitude?

� How should IKEA deal with public pressure and use its influence toimprove working conditions and workers rights?

Revisit this question after you have covered Unit 6.

CASE STUDY 2 – POWERGEN

The next case study is case study 5, PowerGen: Strategy and CorporatePlanning’ in your key textbook, De Wit, B & Meyer, R (p. 709-720).

Below is the case synopsis:

CASE SYNOPSIS

PowerGen was vested as a British electricity generation company in1990 as the result of the privatisation of the UK energy systems. Theprevious state owned “Central Electricity Generating Board” was splitinto three companies, of which PowerGen was the smallest. All threecompanies were asked to compete in the market, and the market was

25

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

opened for further new entrants as well. Along with the privatisationand liberalisation, the government introduced completely newmechanisms of matching supply and demand, such as an electricity poolor the creation of a separate transmission company, and theinstallation of new regulatory institutions. All market players neededto learn how to operate an energy market, where before there wasonly a central planning agency.

As the name of CEGB implied, the institution from which PowerGenemerged, had strong planning instincts for fulfilling its task to supplyelectricity to British households and industry. Therefore, it was notsurprising when PowerGen started preparations for being anindependent company in 1988, that a very detailed strategic planningsystem was installed with the help of McKinsey consultants. However,already in 1992, only two years after the operational start of thecompany, a substantial reorganisation was conducted, which triggereda complete change of the strategic planning system as well. When thisnew planning system failed to function satisfactorily in 1993, it wassubstantially revised for the 1994 planning cycle.

In 1996 the company underwent again a major reorganisation,adjusting the company to a number of internal and external strategicdevelopments. That also caused the strategic planning system to besubstantially revised. In particular it was now broadened to include ahighly sophisticated scenario development module to be conducted onthe business unit level.

The corporate composition did not stabilise thereafter either. In 1998PowerGen completed a major purchase of a regional energydistribution company, merger discussions with US partners continuedon and off, government interference changed the pricing arrangementsof the industry and dictated strategic directions, etc. It seemed that theplanning system was always several steps behind the actual conditionsof the company. On the other hand, without the planning support,how could the company have assessed its choices in the rapidlychanging environment of European energy markets in the 1990s?

Now read the full case study (pages 709-720 of key textbook, De Wit, B &Meyer, R) with the following learning objectives in mind:

� Understand the need for formal planning systems.

� Understand possible designs of formal planning systems.

� Identify the common pitfalls of formal planning systems.

� Conceive alternatives for formal planning systems.

26

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

Questions:

1. Identify four different development stages of the strategy planningsystem that PowerGen was using between 1990 and 1996. Cataloguethe key changes from one stage to the next. What were the reasonsfor these particular changes? Which reasons are attributable toforeseeable circumstances, and which reasons are attributable tounforeseeable circumstances?

2. What were some of the major strategy decisions that were taken atPowerGen? Speculate to what extent the results of the strategicplanning system were used for making these various corporatestrategy decisions.

3. Collect the hints in the case, which suggest that there is also a parallelstrategy formation process in place that operates in a moreincremental, emergent fashion.

CASE STUDY FEEDBACK

Feedback on Question 1:

PowerGen’s strategy planning system developed in four different stages duringthe first six years of its privatisation.

Phase I:

Occurred in 1990 with strongly centralised formation and planning. Performedin a functional structure by the commercial division, and focused on pooloperation.

Context: where and by whom?

� In a renewed, functional structure of the organisation.

� Led and managed by a large, centralised planning team at thecommercial division, monopolising the strategy planning anddecision making within the corporation.

� Separated financial role within the Finance division for reviews andprojection of plans.

Process: how and when?

� Deliberate formation.

27

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

� 5-stage planning process: business unit – aggregation –divisional plans – aggregation – corporate plan .

� Use of scenarios concerning market share, pool prices andcompetitor analysis for the core business.

� 12-month process.

Content:

� Focus of strategy: the operation of the pool.

� Diversification and early internationalisation.

� Planning focused on resource implications of strategicdecisions.

Phase II

Occurred in 1992. To some extent decentralised formation and planning,under responsibility of rather autonomous division directors, supported bydivisionalised financial staff and a downsized corporate planning team.

Context: where and by whom?

� From a functional structure towards three divisions with profitand cost centres.

� Decentralisation of (strategic) decision making and planning tothe divisions, headed by empowered MDs.

� Replacement of the large, central planning team by businesslevel planning staff within the divisions.

� Introduction of a small central strategic planning function,responsible for both corporate strategy development andcorporate planning.

� Reallocation of financial planning support towards within thefinance department.

Process. how and when?

� Business units developed own business plans, reviewed bydivisional boards, and incorporated in corporate plans; theprocess itself did not change too much – merely theresponsibilities of making up the plans had shifted profoundly.

� Shortened planning cycle to nine months.

28

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

Content:

� Shift in business unit responsibility and culture: from expenditurelimits towards operating results, from meeting centrally set targetsto exploring their potential, with increased options and widenedcommercial focus.

� Less detailed level of planning.

Reasons:

� Devolution and introduction of an internal market.

� Diversification (first attempts of internationalisation) and earlyverticalisation of the businesses required increased responsivenessat business unit level.

Phase III

Occurred in 1994, with a focus on regaining fit between strategy developmentsand financial priorities.

Context: where and by whom?

� Responsibility for the plan and for managing the corporate planningprocess was passed to the director of finance, effectively increasingthe influence of financial considerations in the planning process.

� Scenario development was partly delegated to business units, whichbecame responsible for developing a number of scenarios showinghow the market might develop, and the plans that followed ‘were tobe robust to those possibilities’.

Reasons

� Foreseen profit margins lower than forecasted, because ofregulatory intervention (introduction of capped wholesale prices)and competition (increased market share of Nuclear Electric).

� Unforeseen extended planning cycle, because of massiverecalculations of forecasts.

� Unforeseen rift between strategic decisions and financial priorities.Emanated from a strategy and planning process with fewindependent checks and balances from a financial point of view.

� Unforeseen failure of the centre to communicate (foreseen)scenario information fully.

29

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

� Desire to eliminate divisional bureaucracy in managing theplanning process, because of conflicts between different layersof the corporation.

Phase IV

Occurred in 1996 with further delegation of the strategic decision-making andplanning process to business units, between which common strategic managementactivities were increasingly co-ordinated and increasingly emergent.

Context: where and by whom?

� From divisional structure towards clusters of business units.

� Shift and separation of strategy responsibilities: BU planningprocess to BU finance manager; BU strategy development toother BU staff member.

� Strategy triangle between CEO (for corporate strategy,supported by Finance Director (for corporate financialimplications) and corporate strategist & planner), group MD(responsible for business unit strategy, assisted by financemanager, who managed the planning process).

Process. how and when?

� Strategic actions increasingly in reaction to environmental(industry dynamics and regulatory) changes, in a continuousabsorption of the external perspective and its impact onstrategic options.

� Decentralisation of scenario development: from corporatescenarios as a guideline, towards scenario development atbusiness unit level.

� Horizontal co-ordination (not centralisation) betweenmulti-units, with integratedstrategic management andorganisational development (skills transfer, human resourceplanning, etc.).

� From pre-set details towards a more gradually evolvingprocess, with ongoing examination of BU strategy, withincreased scope for absorption of emergent issues intodevelopment and planning cycle.

� Decrease in formality of process (including debating, lobbyingfor and formation of coalitions for strategic options andactions between corporate and business levels).

� Sequenced process: first BU strategy, than BU planning.

30

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

� Differentiation among guidelines for the different businesses.

� Five-year horizon.

Content

� The highly increased impact of regulatory forces on PowerGenincreasingly required a pattern of political bargaining with theenvironment. Instead of planning the future in detail, a pattern ofaction and reaction with environmental forces became a highlyinfluential factor in PowerGen’s strategic behaviour.

Organisational systems

� Encouragement of planning system initiatives by BUs within acorporate context (such as the multi unit scenario development).

� Reviews by team of BUs and corporate level.

� Introduction of bonus system, related to strategy process.

Reasons

� Increase in environmental complexity and uncertainty, because ofdiversification, competition and new regulation.

� An unforeseen need for co-ordination between the differentstrategising activities of BU.

� Foreseen need for independent management of several ‘new’businesses.

� Need for separation and autonomy of marketing and sales, inanticipation of liberalisation of core markets.

� Need for even further autonomy of business units, in order tocreate increased focus for business units’ specific circumstances.

Feedback on Question 2:

1. Development of generation power. PowerGen began to develop itsgeneration capacity to better fit commercial and environmentalrequirements, through improving the flexibility of the coal units anddeveloping gas-fired stations. The move to flexible production camealong with the anticipated need for flexibility in the supply of energy.Before the liberalisation, the previous planning mechanism could easilyforesee total demand on a yearly basis, dividing the total and allocatingparts to the various generation units. But in the fresh market, thedemand for energy could easily alter significantly, mainly due to the

31

Global Corporate Strategy Unit 1 – Strategy Defined and Key Concepts

new market mechanism: the wholesale pool. To be responsive to thisnew market logic, production needed to be flexible.

Note, however, that the very step of introducing flexible production,actually opposed the whole idea of the formalised, long and detailedplanning process that was adapted by PowerGen in 1990. Because ofthe electricity pool, it became much harder to forecast exactproduction demand.

2. Leveraging of core competencies. PowerGen’s moved to leverage hercore competencies in other energy-related areas, both vertically andhorizontally (internationalisation). Examples include:

� Upstream: acquisition of assets in the North Sea andLiverpool Bay.

� Downstream: formation of a joint venture with Conoco,Kinetica; plans included the supply of gas to powerstations, including PowerGen’s, and large businesses;establishment of Combined Heat & Power (CHP);acquisition of East Midlands Electricity plc. (EME), ‘98.

� International: (early stage) power station and miningacquisitions in eastern Germany and Hungary, withconstruction projects in Portugal and Indonesia. Later onin the 1990s, further foreign direct investments in plantsand projects overseas.

� Commissioning of two new CHP plants.

As stated in the case, PowerGen strategy anticipated that it wouldsuffer an inevitable reduction in market share, together with pressuresfor price reduction. Consequently, the company recognised thatgrowth in the medium and longer term would require theestablishment of new income streams in other energy-related areaswhere its core competencies could create value. The case reveals dataon slow growth perspectives for PowerGen’s core industry in the UKon the one hand, and high growth forecasts in domestic energy relatedareas and increasing international demand for power on the otherhand. Probably, within the planning cycle, external industryassessments had come up with these insights, forming the basis forenvironmental scenarios. This ultimately resulted in the formulation ofstrategic options at PowerGen and the strategic choice of a path togrowth in a still standing UK market.

3. Intended sell of PowerGen North Sea (1997/1998). In the case of theacquisition of EME, it is to be assumed, that the ‘one-stop-shop’(supplying all household’s energy needs) strategy had been pushed forby strategists as the solution for ensuring long-term profitability atPowerGen. Also, the case explicates that integration of generation and

32

Unit 1 – Strategy Defined and Key Concepts Global Corporate Strategy

distribution provided necessary expertise for similar futureinternational acquisitions.

4. Merging explorations with US utility groups. Clearly, from a content pointof view, the strategy and planning process focused on leveraging corecompetencies for expansion of its business. In fact, in the later ‘90sPowerGen’s challenge was to get individual business units to be moreresponsive in leveraging core competencies of PowerGen tooperations in both domestic and overseas markets. One could arguethat the planning process of PowerGen from 1996 successfullymanaged this challenge, by engaging delegated business units in thestrategic management process.

Note, that the allocation of the strategy and planning process to thecommercial division in 1990, might indeed have affected the strategicchoices made by PowerGen. Identification of strategic issues by thisdivision might be completely different when the strategic managementfunction was allocated to the finance department (as in 1992), forexample.